$4,055,000 PERRIS PUBLIC FINANCING AUTHORITY TAX ALLOCATION REVENUE BONDS (1987 PROJECT LOAN), 2009 SERIES A

|

|

|

- Jemimah Henry

- 5 years ago

- Views:

Transcription

1 NEW ISSUE - BOOK-ENTRY ONLY RATING Standard & Poor s: A- (See CONCLUDING INFORMATION - RATING ON THE BONDS herein) In the opinion of Aleshire & Wynder, LLP, Bond Counsel, based on existing statutes, regulations, rulings and court decisions and assuming, among other matters, compliance with certain covenants, interest on the Bonds is excluded from gross income for federal income tax purposes and is exempt from current State of California personal income taxes. In the opinion of Bond Counsel, interest on the Bonds is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, although Bond Counsel observes that it is included in adjusted current earnings in calculating corporate alternative minimum taxable income. Bond Counsel expresses no opinion regarding other federal or State tax consequences relating to the ownership or disposition of, or the accrual or receipt of interest on, the Bonds. See LEGAL MATTERS TAX EXEMPTION herein. RIVERSIDE COUNTY STATE OF CALIFORNIA $4,055,000 PERRIS PUBLIC FINANCING AUTHORITY TAX ALLOCATION REVENUE BONDS (1987 PROJECT LOAN), 2009 SERIES A Dated: Date of Delivery Due: October 1 As Shown Below. The cover page contains certain information for quick reference only. It is not a summary of the issue. Potential investors must read the entire Official Statement to obtain information essential to making an informed investment decision. See BONDOWNERS RISKS herein for a discussion of special risk factors that should be considered in evaluating the investment quality of the Bonds. Interest on the Bonds is payable semiannually on April 1 and October 1 of each year, commencing on October 1, 2009, until maturity or earlier redemption (see THE BONDS - GENERAL PROVISIONS and THE BONDS - REDEMPTION herein). The information contained within this Official Statement was prepared under the direction of the Perris Public Financing Authority (the Authority ) by the following firm serving as Financing Consultant to the Authority. ROD GUNN ASSOCIATES, INC. MATURITY SCHEDULE $715,000 Serial Bonds Maturity Date Principal Interest Reoffering Maturity Date Principal Interest Reoffering _October 1_ Amount _Rate Rate October 1_ Amount _Rate Rate 2009 $65, % 3.250% 2015 $60, % 5.100% , % 3.350% , % 5.300% , % 4.250% , % 5.550% , % 4.400% , % 5.800% , % 4.600% , % 6.100% , % 4.850% $475, % Term Bonds due October 1, 2024, Price % $640, % Term Bonds due October 1, 2029, Price % $690, % Term Bonds due October 1, 2033, Price % $1,535, % Term Bonds due October 1, 2037, Price % The Bonds are payable solely from the revenues pledged under the Indenture (the Revenues ), consisting primarily of proceeds from the repayment of a loan (the 1987 Project Loan ) with respect to the Redevelopment Project-1987 (the 1987 Redevelopment Project ) to be made by the Authority to the Redevelopment Agency of the City of Perris (the Agency ) as described herein. The 1987 Project Loan is payable on a parity basis with certain obligations issued by the Agency in 2006 and is payable on a subordinate basis to certain additional obligations issued in 2001 by the Agency, all as described herein. The 1987 Project Loan is payable solely from Tax Revenues (as defined herein) attributable to the 1987 Redevelopment Project, as described herein (see SOURCES OF PAYMENT FOR THE BONDS, BONDOWNERS RISKS, THE 1987 REDEVELOPMENT PROJECT and TAX INCREMENT REVENUES herein). It is anticipated that the Bonds, in book-entry form, will be available for delivery through the facilities of The Depository Trust Company in New York, New York, on or about February 19, 2009 (see APPENDIX G - BOOK-ENTRY SYSTEM ). The date of the Official Statement is February 3, 2009.

2 PERRIS PUBLIC FINANCING AUTHORITY PERRIS, CALIFORNIA AUTHORITY BOARD AND CITY COUNCIL Daryl Busch, Chairperson and Mayor Al Landers, Vice Chairperson and Mayor Pro Tem Joanne H. Evans, Board Member and Council Member Raul (Mark) Yarbrough, Board Member and Council Member Rita Rogers, Board Member and Council Member AUTHORITY AND CITY STAFF Richard Belmudez, Executive Director and City Manager Ron Carr, Assistant Executive Director, Treasurer and Assistant City Manager Eric Dunn, Authority and Agency Counsel and City Attorney Judy L. Haughney, Secretary and City Clerk PROFESSIONAL SERVICES Bond Counsel Aleshire & Wynder, LLP Irvine, California Disclosure Counsel Fulbright & Jaworski L.L.P. Los Angeles, California City Attorney and Authority Counsel Aleshire & Wynder, LLP Irvine, California Financing Consultant Rod Gunn Associates, Inc. Huntington Beach, California Trustee Wells Fargo Bank, National Association Los Angeles, California Underwriter O Connor & Company Securities, Inc. Newport Beach, California Underwriter s Counsel McFarlin & Anderson LLP Lake Forest, California Dissemination Agent Willdan Financial Services Temecula, California FOR ADDITIONAL INFORMATION Ron Carr, City of Perris, California (951) O Connor & Company Securities, Inc. (949) i

3 GENERAL INFORMATION ABOUT THE OFFICIAL STATEMENT Use of Official Statement. This Official Statement is submitted in connection with the offer and sale of the Bonds referred to herein and may not be reproduced or used, in whole or in part, for any other purpose. This Official Statement is not to be construed as a contract with the purchasers of the Bonds. Estimates and Forecasts. When used in this Official Statement and in any continuing disclosure by the Agency, in any press release and in any oral statement made with the approval of an authorized officer of the Agency, the words or phrases will likely result, are expected to, will continue, is anticipated, estimate, forecast, expect, intend, and similar expressions identify forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, Section 21E of the United States Securities Exchange Act of 1934, as amended, and Section 27A of the United States Securities Act of 1933, as amended. Such statements are subject to risks and uncertainties that could cause actual results to differ materially from those contemplated in such forward-looking statements. Any forecast is subject to such uncertainties. Inevitably, some assumptions used to develop the forecasts will not be realized and unanticipated events and circumstances may occur. Therefore, there are likely to be differences between forecasts and actual results and those differences may be material. The information and expressions of opinion herein are subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, give rise to any implication that there has been no change in the affairs of the Agency or any other entity described or referenced herein since the date hereof. Neither the Authority nor the Agency plan to issue any updates or revisions to the forward-looking statements set forth in this Official Statement. Limited Offering. No dealer, broker, salesperson or other person has been authorized by the Authority or the Agency to give any information or to make any representations in connection with the offer or sale of the Bonds other than those contained herein and if given or made, such other information or representation must not be relied upon as having been authorized by the Authority, the Agency or the Underwriter. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the Bonds by a person in any jurisdiction in which it is unlawful for such person to make such an offer, solicitation or sale. Involvement of Underwriter. The Underwriter has submitted the following statement for inclusion in this Official Statement: The Underwriter has reviewed the information in this Official Statement in accordance with, and as a part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. The information and expressions of opinions herein are subject to change without notice and neither delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Authority, the Agency or any other entity described or referenced herein since the date hereof. All summaries of the documents referred to in this Official Statement are made subject to the provisions of such documents and do not purport to be complete statements of any or all of such provisions. THE BONDS HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON AN EXEMPTION FROM THE REGISTRATION REQUIREMENTS CONTAINED IN SUCH ACT. THE BONDS HAVE NOT BEEN REGISTERED OR QUALIFIED UNDER THE SECURITIES LAWS OF ANY STATE. ii

4 TABLE OF CONTENTS INTRODUCTORY STATEMENT...1 THE AUTHORITY...1 Authorization and Formation...1 Bond Authorization and Issuance...1 THE AGENCY...2 Authorization and Formation...2 The 1987 Redevelopment Project...2 The 1987 Project Loan Authorization...2 Tax Allocation Financing...3 Outstanding Indebtedness of the 1987 Redevelopment Project...3 SECURITY AND SOURCES OF REPAYMENT...3 The Indenture...3 The 1987 Project Loan Agreement...4 PURPOSE...4 The Bonds...4 The 1987 Project Loan...4 REDEMPTION OF THE BONDS...4 Mandatory Redemption from Optional Loan Prepayments...4 Mandatory Redemption upon Acceleration of the 1987 Project Loan...4 Mandatory Sinking Payment Redemption...5 THE BONDS GENERAL PROVISIONS...5 Denominations...5 Registration, Transfer and Exchange...5 Payment...5 Notice...5 LEGAL MATTERS...5 PROFESSIONAL SERVICES...6 FINANCIAL STATEMENTS...6 CONTINUING DISCLOSURE...6 AVAILABILITY OF LEGAL DOCUMENTS...7 SELECTED ESSENTIAL FACTS...8 ESTIMATED SOURCES AND USES OF FUNDS...10 THE BONDS...10 Sources of Funds...10 Uses of Funds...10 THE 1987 PROJECT LOAN...10 Sources of Funds...10 Uses of Funds...10 THE BONDS...11 GENERAL PROVISIONS...11 Repayment of the Bonds...11 Transfer or Exchange of Bonds...11 Bonds Mutilated, Lost, Destroyed or Stolen...11 REDEMPTION...12 Mandatory Sinking Payment Redemption...12 Mandatory Redemption from Optional Loan Prepayments...13 Mandatory Redemption upon Acceleration of the 1987 Project Loan...13 Notice of Redemption...13 Selection of Bonds for Redemption...13 Effect of Redemption...13 Partial Redemption...14 ADDITIONAL OBLIGATIONS...14 The Authority...14 The Agency...14 SCHEDULED DEBT SERVICE ON THE BONDS...16 SCHEDULED DEBT SERVICE ON THE 1987 PROJECT LOAN...18 SOURCES OF PAYMENT FOR THE BONDS...20 REPAYMENT OF THE BONDS...20 The Bonds...20 Reserve Fund...20 REPAYMENT OF THE 1987 PROJECT LOAN...20 Tax Allocation Financing...20 Pledge of Tax Revenues...21 Alternative Method of Tax Apportionment ( Teeter Plan )...22 BONDOWNERS RISKS...23 THE BONDS...23 General...23 No Liability of the Authority to the Owners...23 Loss of Tax Exemption...23 Secondary Market...23 No Effective Acceleration on Default...23 Enforceability of Remedies...24 THE 1987 PROJECT LOAN...24 Risk Factors Relating to the Reduction of Tax Revenues...24 Risk Factors Related to Real Estate Market Conditions...27 Risk Factors Related to Natural and Man-made Disasters...28 Risk Factors Relating to State Budget Legislation...28 Risk Factors Relating to the Bonds and the Redevelopment Law...29 Risk Factors Related to Bankruptcy of the Authority and the Agency...29 Risk Factors Related to Assumptions and Projections...30 PROPERTY TAXATION IN CALIFORNIA...31 CONSTITUTIONAL AMENDMENTS AFFECTING TAX INCREMENT REVENUES...31 IMPLEMENTING LEGISLATION...31 CONSTITUTIONAL CHALLENGES TO PROPERTY TAX SYSTEM...32 PROPERTY TAX COLLECTION PROCEDURES...32 SUPPLEMENTAL ASSESSMENTS...32 TAX COLLECTION FEES...33 UNITARY PROPERTY TAX...33 BUSINESS INVENTORY AND REPLACEMENT REVENUE...33 iii

5 PROPOSITION FUTURE INITIATIVES...34 THE AUTHORITY...35 GENERAL...35 AUTHORIZATION...35 The Bonds...35 The 1987 Project Loan...35 AUTHORITY FINANCIAL STATEMENTS...35 DEBT SERVICE COVERAGE ON THE AUTHORITY BONDS...35 THE AGENCY...37 GOVERNMENT ORGANIZATION...37 AGENCY POWERS...37 THE REDEVELOPMENT PLAN...38 General...38 Redevelopment Plan Limitations...38 AGENCY FINANCIAL ADMINISTRATION...40 Annual Budget...40 Agency Accounting Records and Financial Statements...40 Annual Financial Report...41 Filing of Statement of Indebtedness...41 THE 1987 REDEVELOPMENT PROJECT...43 GENERAL...43 ASSESSED VALUE BY LAND USE...43 TOP TEN TAXABLE PROPERTY OWNERS Redevelopment Project Map...46 TAX INCREMENT REVENUES...51 HISTORICAL TAXABLE VALUATIONS...51 ASSESSMENT APPEALS...51 PROPOSITION 8 ADJUSTMENTS...52 TRANSFERS OF OWNERSHIP...52 FORECLOSURES...52 DELINQUENCIES...52 PASS-THROUGH AGREEMENTS AND STATUTORY PAYMENTS...53 Pass-Though Agreements...53 Statutory Tax Sharing...55 Section Payments...57 HOUSING SET-ASIDE...57 PROJECTED TAX INCREMENT REVENUES ASSUMPTIONS...57 LEGAL MATTERS...59 ENFORCEABILITY OF REMEDIES...59 APPROVAL OF LEGAL PROCEEDINGS...59 TAX EXEMPTION...59 INFORMATION REPORTING AND BACKUP WITHHOLDING...60 ABSENCE OF LITIGATION...61 CONCLUDING INFORMATION...62 RATING ON THE BONDS...62 UNDERWRITING...62 EXPERTS...62 FINANCIAL STATEMENTS OF THE AGENCY...62 THE FINANCING CONSULTANT...62 FORWARD-LOOKING STATEMENTS...63 iv ADDITIONAL INFORMATION...63 REFERENCES...63 EXECUTION...63 APPENDIX A SUMMARY OF CERTAIN TERMS AND THE INDENTURE...A-1 APPENDIX B SUMMARY OF THE 1987 PROJECT LOAN AGREEMENT...B-1 APPENDIX C FISCAL CONSULTANT REPORT...C-1 APPENDIX D AGENCY FINANCIAL STATEMENTS...D-1 APPENDIX E FORM OF CONTINUING DISCLOSURE AGREEMENT...E-1 APPENDIX F FORM OF OPINION OF BOND COUNSEL... F-1 APPENDIX G BOOK-ENTRY SYSTEM... G-1

6 CITY OF PERRIS VICINITY MAP v

7 OFFICIAL STATEMENT $4,055,000 PERRIS PUBLIC FINANCING AUTHORITY TAX ALLOCATION REVENUE BONDS (1987 PROJECT LOAN), 2009 SERIES A This Official Statement which includes the cover page and appendices (the Official Statement ) is provided to furnish certain information concerning the sale by the Perris Public Financing Authority (the Authority ) of its Tax Allocation Revenue Bonds (1987 Project Loan), 2009 Series A (the Bonds ), in the aggregate principal amount of $4,055,000. INTRODUCTORY STATEMENT This Introductory Statement contains only a brief description of this issue and does not purport to be complete. The Introductory Statement is subject in all respects to more complete information in the entire Official Statement and the offering of the Bonds to potential investors is made only by means of the entire Official Statement and the documents summarized herein. Potential investors must read the entire Official Statement to obtain information essential to make an informed investment decision (see BONDOWNERS RISKS herein). THE AUTHORITY Authorization and Formation The Authority is a joint exercise of powers authority organized and existing under and by virtue of the Joint Exercise of Powers Act, constituting Articles 1 through 4 (commencing with Section 6500) of Chapter 5, Division 7, Title 1 of the Government Code of the State (the Joint Powers Act ). The City of Perris (the City ), pursuant to Resolution No. 1715, adopted on August 28, 1989, and the Redevelopment Agency of the City of Perris (the Agency ), pursuant to Resolution No. 120, adopted on August 28, 1989, formed the Authority by the execution of a joint exercise of powers agreement (see THE AUTHORITY herein). Bond Authorization and Issuance Pursuant to the Joint Powers Act, the Authority is authorized, among other things, to issue revenue bonds to provide funds to acquire local obligations issued by local agencies or to make loans to local agencies to finance or refinance public capital improvements, such revenue bonds to be repaid from the repayment of the local obligations so acquired by the Authority or repayment of the loan, such as the 1987 Project Loan (the 1987 Project Loan ) described herein (see INTRODUCTORY STATEMENT SECURITY AND SOURCES OF REPAYMENT below). The Bonds are being issued pursuant to the Indenture, as defined herein (see APPENDIX A SUMMARY OF CERTAIN TERMS AND THE INDENTURE ). The Bonds are being sold to the Underwriter pursuant to, and subject to the terms and conditions of, the Purchase Contract by and among the Underwriter, the Authority and the Agency (the Purchase Contract ). The Indenture and the Purchase Contract were approved by the Authority pursuant to Resolution No. 39 adopted on October 28, It is anticipated that the Bonds, in book-entry form, will be available for delivery through the facilities of The Depository Trust Company, on or about February 19, 2009 (see APPENDIX G - BOOK- ENTRY SYSTEM ). The Authority has issued other series of bonds. Each series is separately secured under the terms of an indenture for such other series of bonds. The Authority is not authorized to issue any additional bonds under the Indenture secured by repayment of the 1987 Project Loan except for refunding purposes. However, the Authority may in the future loan money to the Agency which loan may be payable on a parity with the 1987 Project Loan (see THE BONDS ADDITIONAL OBLIGATIONS herein). 1

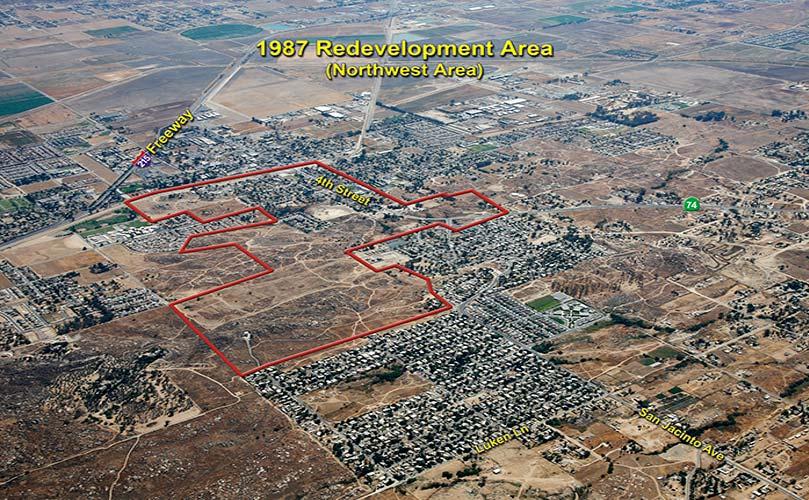

8 THE AGENCY Authorization and Formation The Agency is a public body, corporate and politic, existing under and by virtue of the Community Redevelopment Law of the State, constituting Part 1 of Division 24 (commencing with Section 33000) of the Health and Safety Code of the State (the Redevelopment Law ). The Agency was activated on March 9, The City Council of the City (the City Council ), at the same time, declared itself to be the members of the Agency and appointed the City Manager to be the Agency s Executive Director (see THE AGENCY herein). The Agency is comprised of 3 Redevelopment Projects: (i) the Central Perris and North Perris Redevelopment Project (the Central North Redevelopment Project ); (ii) the Redevelopment Project (the 1987 Redevelopment Project ) and (iii) the Redevelopment Project-1994 (the 1994 Redevelopment Project ). Collectively the Central North Redevelopment Project, the 1987 Redevelopment Project and the 1994 Redevelopment Project are referred to herein as the Redevelopment Projects. The 1987 Redevelopment Project The Perris City Council adopted the redevelopment plan (the Redevelopment Plan ) establishing the 1987 Redevelopment Project by Ordinance No. 687 on June 29, The redevelopment plan was subsequently amended by Ordinance No. 996 on December 12, On September 27, 2005, by the adoption of Ordinance No. 1171, the City Council amended the redevelopment plan pursuant to Senate Bill 1045 by extending by one year the duration of the redevelopment plan and the time frame to collect tax increment revenue. On February 14, 2006, the redevelopment plan was amended to reinstate eminent domain. On September 30, 2008, the City Council amended the redevelopment plan to eliminate the time limit on establishment of indebtedness by Ordinance No (which Ordinance will be effective 30 days thereafter) (see THE AGENCY THE REDEVELOPMENT PLAN Redevelopment Plan Limitations ). The 1987 Redevelopment Project has an area of approximately 2,030 acres, divided between four noncontiguous areas throughout the City (see THE 1987 REDEVELOPMENT PROJECT herein for a description of the 1987 Redevelopment Project). The 1987 Project Loan Authorization The Authority will be making the 1987 Project Loan to the Agency with respect to the 1987 Redevelopment Project (see Tax Allocation Financing below), in the amount of $4,055,000. The Agency authorized the 1987 Project Loan by resolution, adopted on October 28, The Agency has pledged a lien on Tax Revenues, as defined herein, to the repayment of the 1987 Project Loan. Tax Revenues consist of Tax Increment Revenues from the Agency s 1987 Redevelopment Project, excluding (i) amounts required to be deposited into the Agency s Low and Moderate Income Housing Fund, as defined herein, (ii) the SB 2557 County Administrative fees and collection charges and (iii) amounts required to be paid pursuant to certain Pass-Through Agreements and Statutory Tax Sharing (see SOURCES OF PAYMENT FOR THE BONDS, BONDOWNERS RISKS and TAX INCREMENT REVENUES herein). The pledge of Tax Revenues is on a subordinate basis with any payments required under the Agency s Loan Agreement, dated as of June 1, 2001, with respect to the 1987 Redevelopment Project (the 2001 Loan ) and relating to the Perris Public Financing Authority Tax Allocation Revenue Bonds, 2001 Series A. The pledge of Tax Revenues is on a parity basis with any payments required under the Agency s Loan Agreement, dated as of May 1, 2006, with respect to the 1987 Redevelopment Project (the 2006 Loan ) and relating to the Perris Public Financing Authority 2006 Tax Allocation Revenue Bonds (see Outstanding Indebtedness of the 1987 Redevelopment Project below) (see Tax Allocation Financing below and SOURCES OF PAYMENT FOR THE BONDS, BONDOWNERS RISKS and TAX INCREMENT REVENUES herein). 2

9 Tax Allocation Financing The Redevelopment Law provides a means for financing redevelopment projects based upon an allocation of taxes collected within a redevelopment project. The taxable valuation of a redevelopment project last equalized prior to adoption of the redevelopment plan, or base roll, is established and, except for any period during which the taxable valuation drops below the base year level, the taxing agencies within the redevelopment project thereafter receive the taxes produced by the levy of the then current tax rate upon the base roll. Taxes collected upon any increase in taxable valuation over the base roll (except such portion generated by rates levied to pay voter-approved bonded indebtedness on or after January 1, 1989, for the acquisition or improvement of real property) are allocated to a redevelopment agency (the Tax Increment Revenues ) and may be pledged by a redevelopment agency to the repayment of any indebtedness incurred in financing or refinancing a redevelopment project. Redevelopment agencies themselves have no authority to levy property taxes and must look specifically to the allocation of taxes produced as above indicated. Outstanding Indebtedness of the 1987 Redevelopment Project Pursuant to an Indenture of Trust, dated as of June 1, 2001, the Authority issued its Tax Allocation Revenue Bonds, 2001 Series A Bonds (the 2001 Bonds ) in the aggregate principal amount of $10,745,000 of which $9,270,000 currently remains outstanding. Proceeds of the 2001 Bonds were loaned to the Agency pursuant to a 1987 Project Loan Agreement and a Housing Loan Agreement both dated as of June 1, The loan pursuant to the 1987 Project Loan Agreement (the 2001 Loan ) was in the principal amount of $4,275,000 of which $3,795,000 currently remains outstanding. The 2001 Loan matures on October 1, The 1987 Project Loan is payable on a subordinate basis to the 2001 Loan. Pursuant to an Indenture of Trust, dated as of May 1, 2006, the Authority issued its 2006 Tax Allocation Revenue Bonds (the 2006 Bonds ) in the aggregate principal amount of $31,005,000, of which $30,570,000 currently remains outstanding. Proceeds of the 2006 Bonds were loaned to the Agency pursuant to separate loan agreements, all dated as of May 1, 2006, with each of the Redevelopment Projects and the Low and Moderate Income Housing Fund. The loan with respect to the 1987 Redevelopment Project (the 2006 Loan ) was in the principal amount of $5,220,000 of which $5,185,000 currently remains outstanding. The 2006 Loan matures October 1, The 1987 Project Loan is payable on a parity basis with the 2006 Loan. SECURITY AND SOURCES OF REPAYMENT The Indenture The Bonds are secured under an Indenture of Trust, dated as of February 1, 2009 (the Indenture ), by and between the Authority and Wells Fargo Bank, National Association, Los Angeles, California, as trustee (the Trustee ) (see APPENDIX A - SUMMARY OF THE INDENTURE ). The proceeds of the Bonds will be loaned by the Authority to the Agency pursuant to the 1987 Project Loan. The Bonds are payable from loan payments to be made to the Authority under the 1987 Project Loan, from amounts in the Reserve Fund created under the Indenture and from certain funds and accounts created under the Indenture, and from investment earnings thereon (the Revenues ) (see SOURCES OF PAYMENT FOR THE BONDS and BONDOWNERS RISKS herein). The Bonds are limited obligations of the Authority. The Bonds do not constitute a debt or liability of the City, the State of California (the State ) or of any political subdivision thereof, other than the Authority. The Authority shall be obligated to pay the principal of the Bonds, and the interest thereon, only from the funds described herein, and neither the faith and credit nor the taxing power of the City, the State or any of its political subdivisions is pledged to the payment of the principal of or the interest on the Bonds. The Authority has no taxing power. 3

10 The 1987 Project Loan Agreement The 1987 Project Loan is to be made and secured pursuant to the 1987 Project Loan Agreement (the 1987 Project Loan Agreement ) authorized by a Resolution of the Agency, adopted on October 28, A description of the 1987 Project Loan Agreement is set forth in APPENDIX B - SUMMARY OF THE 1987 PROJECT LOAN AGREEMENT. The 1987 Project Loan is made in accordance with the laws of the State, and particularly the Community Redevelopment Law of the State, constituting Part 1 of Division 24 (commencing with Section 33000) of the Health and Safety Code of the State. The Agency is authorized to issue additional obligations secured by Tax Revenues on a parity with the 1987 Project Loan (see THE BONDS - ADDITIONAL OBLIGATIONS - The Agency herein). The 1987 Project Loan is a limited obligation of the Agency. The 1987 Project Loan does not constitute a debt or liability of the State or of any political subdivision thereof, other than the Agency. The Agency shall be obligated to pay the principal of the 1987 Project Loan, and the interest thereon, only from the funds described herein, and neither the faith and credit nor the taxing power of the City, the State or any of its political subdivisions is pledged to the payment of the principal of or the interest on the 1987 Project Loan. The Agency has no ad valorem taxing power. PURPOSE The Bonds The Bonds are being issued to provide funds to make the 1987 Project Loan on the closing date and to pay the expenses of the Authority in connection with the issuance of the Bonds. In addition, Bond proceeds will be used to establish a reserve fund pursuant to the Indenture (see SOURCES OF PAYMENT FOR THE BONDS - REPAYMENT OF THE BONDS - Reserve Fund herein). The amount of the deposit into the Reserve Fund will be in the amount equal to $405,500 (see ESTIMATED SOURCES AND USES OF FUNDS herein). The 1987 Project Loan Proceeds of the 1987 Project Loan will be used by the Agency to finance redevelopment activities consisting of capital projects of the Agency and public improvements of benefit to the 1987 Redevelopment Project, and to pay the expenses of the Agency in connection with the 1987 Project Loan (see ESTIMATED SOURCES AND USES OF FUNDS herein). REDEMPTION OF THE BONDS Mandatory Redemption from Optional Loan Prepayments The Bonds are subject to mandatory redemption from optional prepayments under the 1987 Project Loan prior to maturity, in whole or in part, on a pro rata basis and by lot within a maturity, on October 1, 2018, and on any date thereafter at a redemption price equal to the principal amount thereof, plus accrued interest to the date of redemption, as described herein (see THE BONDS - REDEMPTION Mandatory Redemption From Optional Loan Prepayments herein). Mandatory Redemption upon Acceleration of the 1987 Project Loan The Bonds are also subject to mandatory redemption, without premium, prior to maturity, in whole or in part, on any date, from amounts credited toward the payment of principal of the 1987 Project Loan coming due and payable solely by reason of acceleration of the 1987 Project Loan (see THE BONDS - REDEMPTION - Mandatory Redemption upon Acceleration of the 1987 Project Loan herein). 4

11 Mandatory Sinking Payment Redemption The Bonds maturing October 1, 2024, October 1, 2029, October 1, 2033 and October 1, 2037, are subject to mandatory sinking payment redemption, without premium, prior to their maturity date, in part by lot on October 1 in each year commencing October 1, 2020, with respect to the Bonds maturing October 1, 2024, October 1, 2025 with to the Bonds maturing October 1, 2029, October 1, 2030 with respect to the Bonds maturing October 1, 2033, and October 1, 2034 with respect to the Bonds maturing October 1, 2037, from mandatory sinking payments under the Indenture (see THE BONDS - REDEMPTION Mandatory Sinking Payment Redemption herein). THE BONDS GENERAL PROVISIONS Denominations The Bonds will be issued in the minimum denomination of $5,000 each or any integral multiple thereof (see THE BONDS - GENERAL PROVISIONS herein). Registration, Transfer and Exchange The Bonds will be issued in fully-registered form without coupons. Any Bond may, in accordance with its terms, be transferred or exchanged, pursuant to the provisions of the Indenture (see THE BONDS - GENERAL PROVISIONS - Transfer or Exchange of Bonds herein). When delivered, the Bonds will be registered in the name of The Depository Trust Company, New York, New York ( DTC ), or its nominee. DTC will act as securities depository for the Bonds. Individual purchases of Bonds will be made in book-entry form only in the principal amount of $5,000 or any integral multiple thereof. Purchasers of beneficial interests in the Bonds will not receive certificates representing their ownership interests in Bonds purchased (see APPENDIX G - BOOK-ENTRY SYSTEM ). Payment Principal of the Bonds and any premium upon redemption will be payable in each of the years and in the amounts set forth on the cover page hereof upon surrender at the corporate trust office of the Trustee in Los Angeles, California. Interest on the Bonds will be paid by check of the Trustee mailed by first class mail on the Interest Payment Date (as defined in the Indenture) to the person entitled thereto (except as otherwise described herein for interest paid to an account in the continental United States of America by wire transfer as requested in writing no later than the applicable Record Date (as defined in the Indenture) by owners of $1,000,000 or more in aggregate principal amount of Bonds) (see THE BONDS - GENERAL PROVISIONS herein). Initially, interest on and principal and premium, if any, of the Bonds will be payable when due by wire of the Trustee to DTC which will, in turn, remit such interest, principal and premium, if any, to DTC Participants (as defined herein), which will, in turn, remit such interest, principal and premium, if any, to Beneficial Owners (as defined herein) of the Bonds (see APPENDIX G - BOOK-ENTRY SYSTEM ). Notice Notice of any redemption will be mailed by first class mail by the Trustee at least thirty (30) but no more than sixty (60) days prior to the date fixed for redemption to the registered owners of any Bonds designated for redemption and to the Securities Depositories and one or Information Services provided in the Indenture. Neither failure to receive such notice nor any defect in the notice so mailed will affect the sufficiency of the proceedings for redemption of such Bonds or the cessation of accrual of interest on the redemption date (see THE BONDS - REDEMPTION - Notice of Redemption herein). LEGAL MATTERS All legal proceedings in connection with the issuance of the Bonds are subject to the approving opinion of Aleshire & Wynder, LLP, Irvine, California, Bond Counsel. Such opinion, and certain tax consequences incident to the ownership of the Bonds, including certain exceptions to the tax treatment of interest, are described more fully under the heading LEGAL MATTERS herein. Certain legal matters will be passed on for the Authority and the Agency by Aleshire & Wynder, LLP, Irvine, California, as 5

12 City Attorney, Authority Counsel and Agency Counsel and by Fulbright & Jaworski L.L.P., Los Angeles, California, as Disclosure Counsel. Certain legal matters will be passed upon for the Underwriter by McFarlin & Anderson LLP, Lake Forest, California, as Underwriter s Counsel. PROFESSIONAL SERVICES Wells Fargo Bank, National Association, Los Angeles, California, will serve as Trustee under the Indenture. The Trustee will act on behalf of the Bondowners for the purpose of receiving all moneys required to be paid to the Trustee, to allocate, use and apply the same, to hold, receive and disburse the Revenues and other funds held under the Indenture, and otherwise to hold all the offices and perform all the functions and duties provided in the Indenture to be held and performed by the Trustee. Rod Gunn Associates, Inc., Huntington Beach, California, Financing Consultant (the Financing Consultant ), advised the Authority as to the financial structure and certain other financial matters relating to the Bonds. HdL Coren & Cone, Diamond Bar, California (the Fiscal Consultant ), prepared the Fiscal Consultant Report containing certain background information on the Agency and the 1987 Redevelopment Project, including the projection of Tax Revenues used in sizing and structuring the Bonds. See APPENDIX C - FISCAL CONSULTANT REPORT for more complete information regarding Tax Revenues. Fees payable to Bond Counsel, Disclosure Counsel, Underwriter s Counsel and the Financing Consultant are contingent upon the sale and delivery of the Bonds. FINANCIAL STATEMENTS The Agency s financial statements for the fiscal year ended June 30, 2008, are attached hereto as APPENDIX D and have been audited by Teaman, Ramirez & Smith, Certified Public Accountants, Riverside, California. The Agency has not requested, nor did the Agency obtain permission from, the auditor to include the audited financial statements as an appendix to this Official Statement. Accordingly, the auditor has not performed any post-audit work on the financial statements. CONTINUING DISCLOSURE The Agency has undertaken all responsibilities for any required continuing disclosure to Bondowners as described below. The Authority shall have no liability to the Bondowners or any other person with respect to such disclosures provided by the Agency. The Agency will covenant to provide annually certain financial information and operating data relating to the 1987 Redevelopment Project by not later than February 15 each year, commencing February 15, 2010, and to provide the audited Financial Statements of the Agency for the fiscal year ending June 30, 2009, and for each subsequent fiscal year when they are available (together, the Annual Report ), and to provide notices of the occurrence of certain other enumerated events. The Annual Report will be filed by the Trustee on behalf of the Agency with the Municipal Securities Rulemaking Board ( MSRB ) in an electronic format as prescribed by the MSRB. Until July 1, 2009, the notices of material events will be timely filed by the Authority with the MSRB, the National Recognized Municipal Securities Information Repository certified by the Securities and Exchange Commission Repositories and a State repository, if any. Effective July 1, 2009, such noticies of material events will be filed solely with the MSRB. The specific nature of the information to be contained in the Annual Report or the notices of material events and certain other terms of the continuing disclosure obligation are summarized in APPENDIX E - FORM OF CONTINUING DISCLOSURE AGREEMENT. The Agency has not previously failed to comply with any undertaking to provide any required continuing disclosure. 6

13 AVAILABILITY OF LEGAL DOCUMENTS The summaries and references contained herein with respect to the Indenture, the 1987 Project Loan Agreement, the Bonds, the 1987 Project Loan and other statutes or documents do not purport to be comprehensive or definitive and are qualified by reference to each such document or statute, and references to the Bonds are qualified in their entirety by reference to the form thereof included in the Indenture. Copies of the documents described herein are available for inspection during the period of initial offering of the Bonds at the offices of the Underwriter, O Connor & Company Securities, Inc., 620 Newport Center Drive, Suite 1100, Newport Beach, California, (949) Copies of these documents may be obtained after delivery of the Bonds from the Authority at the Office of the Assistant City Manager, 101 North D Street, Perris, California 92570, telephone (951)

14 SELECTED ESSENTIAL FACTS The following summary does not purport to be complete. Reference is hereby made to the complete Official Statement in this regard. THE BONDS Principal Amount of Bonds: $4,055,000 Additional Bonds: No Additional Bonds are authorized to be secured by the 1987 Project Loan except bonds issued to refund the Bonds (see THE BONDS ADDITIONAL OBLIGATIONS The Authority herein). First Optional Redemption Date: October 1, 2018, at 100% of principal amount (see THE BONDS - REDEMPTION Mandatory Redemption From Optional Loan Prepayments herein). Primary Source of Revenues for Repayment: The Bonds are repayable from Revenues, as defined herein, which primarily consist of the repayment of the 1987 Project Loan (see SOURCES OF PAYMENT FOR THE BONDS and BONDOWNERS RISKS herein). Priority: All the Bonds are equally secured by a first pledge of and lien on the Revenues as described herein (see SOURCES OF PAYMENT FOR THE BONDS REPAYMENT OF THE BONDS, BONDOWNERS RISKS herein and APPENDIX A - SUMMARY OF CERTAIN TERMS AND THE INDENTURE ). Debt Service Coverage from Repayment of 100% 1987 Project Loan (see THE AUTHORITY DEBT SERVICE COVERAGE ON THE AUTHORITY BONDS herein): THE 1987 PROJECT LOAN Principal Amount of the 1987 Project Loan: $4,055,000 Outstanding Principal Amount of the 2001 Loan: Outstanding Principal Amount of the 2006 Loan: Additional Indebtedness: $3,795,000 $5,185,000 Additional indebtedness on a parity with the 1987 Project Loan and the 2006 Loan is permitted subject to certain conditions. No senior obligations except the 2001 Loan and other Bonds to refund the 2001 Loan (see THE BONDS ADDITIONAL OBLIGATIONS The Agency herein). 8

15 Primary Source of Revenues for Repayment of the 1987 Project Loan and the 2006 Loan: Priority: Minimum Ratio of Estimated Tax Revenues in any Fiscal Year to Maximum Annual Debt Service on the 1987 Project Loan, 2001 Loan, and the 2006 Loan: Tax Revenues on a subordinate basis with the 2001 Loan and on a parity basis with the 2006 Loan (see TAX INCREMENT REVENUES herein). The Agency has pledged a lien on Tax Revenues, on a subordinate basis with the 2001 Loan and on a parity basis with the 2006 Loan (see SOURCES OF PAYMENT FOR THE BONDS and BONDOWNERS RISKS herein). 125% (see table entitled TAX REVENUES AND DEBT SERVICE herein). THE 1987 REDEVELOPMENT PROJECT Year Established: 1987 Last Date to Receive Tax Increment Revenues: June 28, 2038 Size (in Acres): 2,030 Acres Ten Largest Taxpayers (expressed as a percentage of total Secured and Unsecured Assessed Value): Land Use as a percentage of Fiscal Year assessed value: 30.99% (see THE 1987 REDEVELOPMENT PROJECT TOP TEN TAXABLE PROPERTY OWNERS herein). Residential 17.4%, Commercial 8.3%, Industrial 26.0%, Vacant Land 33.1%, Other 15.2% (see THE 1987 REDEVELOPMENT PROJECT ASSESSED VALUE BY LAND USE herein). 9

16 THE BONDS ESTIMATED SOURCES AND USES OF FUNDS Proceeds from the sale of the Bonds will be used to make the 1987 Project Loan to the Agency in the aggregate principal amounts indicated below. Under the provisions of the Indenture, the Trustee will receive the proceeds from the sale of the Bonds and will apply them as follows: Sources of Funds Bond Proceeds $4,055, Original Issue Discount (70,941.65) Underwriter s Discount (38,522.50) Net Bond Proceeds $3,945, Uses of Funds Loan Fund $3,396, Reserve Fund (1) 405, Costs of Issuance (2) 143, Total Uses $3,945, ( 1 ) An amount equal to the Reserve Requirement under the Indenture. (2) Expenses include fees of Bond Counsel, Disclosure Counsel, the Financing Consultant, Underwriter s Counsel, Trustee, Rating Agency, costs of printing the Official Statement, and other costs of issuance of the Bonds. THE 1987 PROJECT LOAN Under the provisions of the 1987 Project Loan Agreement, the Trustee will receive the proceeds of the 1987 Project Loan and will apply or credit them as follows: Sources of Funds Principal Amount of 1987 Project Loan $4,055, Loan Discount (658,739.15) Net Loan Proceeds $3,396, Uses of Funds Redevelopment Fund $3,351, Costs of Issuance (1) 45, Total Uses $3,396, (1) Costs of Issuance include fees of Bond Counsel, the Financing Consultant, Fiscal Consultant and Disclosure Counsel. 10

17 GENERAL PROVISIONS THE BONDS Repayment of the Bonds Interest is payable on the Bonds at the rates per annum set forth on the cover page hereof. Interest with respect to the Bonds will be computed on the basis of a year consisting of 360 days and twelve 30-day months. Each Bond will be dated as of the closing date, and interest with respect thereto will be payable from the Interest Payment Date next preceding the date of authentication thereof, unless (a) it is authenticated on or before an Interest Payment Date and after the close of business on the preceding Record Date, in which event it shall bear interest from such Interest Payment Date; (b) it is authenticated on or before September 15, 2009, in which event interest thereon will be payable from the closing date; or (c) interest on any Bond is in default as of the date of authentication, in which event interest thereon will be payable from the date to which interest has been paid in full, payable on each Interest Payment Date. Interest on the Bonds will be payable by check of the Trustee mailed by first class mail on the applicable Interest Payment Date to the person appearing on the registration books as the owner thereof, initially Cede & Co., or by wire transfer made on such Interest Payment Date to any owner of $1,000,000 or more in aggregate principal amount of outstanding Bonds, who shall have requested such transfer pursuant to written instructions provided prior to the applicable Record Date to the Trustee. The owners of the Bonds shown on the registration books on the Record Date for the Interest Payment Date will be deemed to be the owners of the Bonds on said Interest Payment Date for the purpose of the paying of interest. Principal of the Bonds and any premium upon early redemption is payable upon presentation and surrender thereof, at the corporate trust office of the Trustee in Los Angeles, California. Transfer or Exchange of Bonds Any Bond, in accordance with its terms, may be transferred or exchanged, pursuant to the provisions of the Indenture, upon surrender of such Bond for cancellation at the corporate trust office of the Trustee. Whenever any Bond or Bonds shall be surrendered for transfer or exchange, the Trustee shall authenticate and deliver a new Bond or Bonds for like aggregate principal amount or maturity amount of authorized denominations. The Trustee is not required to transfer or exchange any Bonds or portions thereof during the period established by the Trustee for selection of Bonds for redemption, or any Bonds selected for redemption. The cost of printing Bonds and any services rendered or expenses incurred by the Trustee in connection with any transfer shall be paid by the Authority. Bonds Mutilated, Lost, Destroyed or Stolen If any Bond becomes mutilated, the Authority, at the expense of the Bond Owner, will execute, and the Trustee will thereupon authenticate and deliver, a new Bond of like series and tenor in exchange and substitution for the Bond so mutilated, but only upon surrender to the Trustee of the Bond so mutilated. Every mutilated Bond so surrendered to the Trustee will be canceled by it. If any Bond is lost, destroyed or stolen, evidence of such loss, destruction or theft may be submitted to the Trustee and, if such evidence is satisfactory to the Trustee and indemnity for the Trustee and the Authority satisfactory to the Trustee shall be given, the Authority, at the expense of the Bondowner, will execute, and the Trustee will thereupon authenticate and deliver, a new Bond of like series and tenor in lieu of and in replacement for the Bond so lost, destroyed or stolen (or if any such Bond has matured or has been called for redemption, instead of issuing a replacement Bond, the Trustee may pay the same without surrender thereof upon receipt of indemnity satisfactory to the Trustee). The Trustee may require payment of a fee for preparing and authenticating each new Bond issued pursuant to the Indenture. Any Bond issued under the 11

18 provisions of the Indenture in lieu of any Bond alleged to be lost, destroyed or stolen will be entitled to the benefits of the Indenture with all other Bonds secured by the Indenture. REDEMPTION Mandatory Sinking Payment Redemption The Bonds maturing on October 1, 2024, October 1, 2029, October 1, 2033 and October 1, 2037, are subject to mandatory redemption, in part by lot, on October 1 in each year commencing October 1, 2020, in the case of the Bonds maturing on October 1, 2024, October 1, 2025, in the case of the Bonds maturing October 1, 2029, October 1, 2030, in the case of the Bonds maturing October 1, 2033, and October 1, 2034, in the case of the Bonds maturing on October 1, 2037, from mandatory sinking payments made by the Authority pursuant to the Indenture at a redemption price equal to the principal amount thereof to be redeemed, without premium, plus accrued interest thereon to the date of redemption as set forth in the following schedule; provided, however, that (i) in lieu of redemption thereof, the Bonds may be purchased by the Authority and tendered to the Trustee, and (ii) if some but not all of the Bonds have been redeemed pursuant to mandatory redemption from optional loan prepayments and mandatory redemption upon acceleration of the 1987 Project Loan provisions described herein, the total amount of all future sinking payments will be reduced by the aggregate principal amount of the Bonds so redeemed, to be allocated among such sinking payments on a pro rata basis (as nearly as practicable) in integral multiples of $5,000 as determined by the Authority. SCHEDULE OF MANDATORY SINKING PAYMENT REDEMPTIONS TERM BONDS MATURING OCTOBER 1, 2024 October 1 Year Principal Amount October 1 Year Principal Amount 2020 $80, $100, , ,000 (maturity) ,000 SCHEDULE OF MANDATORY SINKING PAYMENT REDEMPTIONS TERM BONDS MATURING OCTOBER 1, 2029 October 1 Year Principal Amount October 1 Year Principal Amount 2025 $110, $140, , ,000 (maturity) ,000 SCHEDULE OF MANDATORY SINKING PAYMENT REDEMPTIONS TERM BONDS MATURING OCTOBER 1, 2033 October 1 Year Principal Amount October 1 Year Principal Amount 2030 $155, $175, , ,000 (maturity) SCHEDULE OF MANDATORY SINKING PAYMENT REDEMPTIONS TERM BONDS MATURING OCTOBER 1, 2037 October 1 Year Principal Amount October 1 Year Principal Amount , , , ,000 (maturity) 12

19 Mandatory Redemption from Optional Loan Prepayments The Bonds are subject to mandatory redemption from optional prepayments under the 1987 Project Loan prior to maturity on any date on or after October 1, 2018, as a whole or in part, on a pro rata basis and by lot within a maturity, from loan prepayments by the Agency of all or any portion of the 1987 Project Loan at 100% of the principal amount of the Bonds to be redeemed together with accrued interest thereon to the date fixed for redemption. Mandatory Redemption upon Acceleration of the 1987 Project Loan The Bonds will also be subject to mandatory redemption in whole, or in part by maturity in a manner such that remaining payments on the 1987 Project Loan, calculated at the interest rates of the Bonds, will be sufficient to pay remaining debt service on the Bonds, as determined by the Authority, and by lot within a maturity, on any date, from amounts credited toward the payment of principal of the 1987 Project Loan coming due and payable solely by reason of an event of default and acceleration of the 1987 Project Loan pursuant to the 1987 Project Loan Agreement at a redemption price equal to the principal amount of the Bonds to be redeemed, without premium, together with accrued interest thereon to the redemption date (see APPENDIX B - SUMMARY OF THE 1987 PROJECT LOAN AGREEMENT - Events of Default and Acceleration of Maturities herein). The Bonds will be subject to mandatory redemption pursuant to the provisions of the Indenture solely from amounts credited towards the payment of principal of the 1987 Project Loan which has become due and payable by reason of such event of default and acceleration only. Notice of Redemption When redemption is authorized or required, written notice of redemption is required to be mailed by the Trustee to the respective owners of any Bonds designated for redemption at their addresses appearing on the bond registration books, to the Securities Depositories, and to the Information Services, all as provided in the Indenture, by first class mail, postage prepaid, no less than thirty (30), nor more than sixty (60), days prior to the date fixed for redemption. Neither failure to receive such notice nor any defect in the notice so mailed will affect the sufficiency of the proceedings for redemption of such Bonds or the cessation of accrual of interest on the redemption date. In addition to the foregoing notice, further notice will be given by the Trustee to any Bondowner whose Bond has been called for redemption but who has failed to tender his or her Bond for payment by the date which is sixty (60) days after the redemption date, but no defect in such further notice will in any manner defeat the effectiveness of a call for redemption. Selection of Bonds for Redemption Except as otherwise set forth in the Indenture, whenever provision is made in the Indenture for the redemption of less than all of the Bonds of any maturity, the Trustee shall select the Bonds to be redeemed from all Bonds of such maturity not previously called for redemption, by lot in any manner which the Authority in its sole discretion shall deem appropriate. For purposes of such selection, all Bonds shall be deemed to be comprised of separate $5,000 portions and such portions shall be treated as separate Bonds which may be separately redeemed. Effect of Redemption From and after the date fixed for redemption, if funds available for the payment of the principal of and interest (and premium, if any) on the Bonds so called for redemption shall have been duly provided, such Bonds so called shall cease to be entitled to any benefit under the Indenture other than the right to receive payment of the redemption price, and no interest shall accrue thereon from and after the redemption date specified in such notice. All Bonds redeemed pursuant to the Indenture shall be cancelled and destroyed. 13

20 Partial Redemption In the event only a portion of any Bond is called for redemption, then upon surrender of such Bond the Authority will execute and the Trustee will authenticate and deliver to the Bondowner thereof, at the expense of the Authority, a new Bond or Bonds of the same series and maturity date, of authorized denominations equal in an aggregate principal amount to the unredeemed portion of the Bond to be redeemed. ADDITIONAL OBLIGATIONS The Authority The Authority will not have any indebtedness secured by the Revenues other than the Bonds, except bonds issued to refund the Bonds. However, the Agency is authorized to issue additional obligations secured by the Tax Revenues on a parity with the 1987 Project Loan and the 2006 Loan, and the Authority may issue bonds to acquire the additional obligations of the Agency. When and if issued, each series of bonds of the Authority would be secured by a separate obligation of the Agency. The Agency The Agency has covenanted under the 1987 Project Loan Agreement that it will not issue any obligations senior to the obligations described herein other than to refund the 2001 Loan. In addition to the 1987 Project Loan and the 2006 Loan, the Agency may issue or incur Parity Debt (as defined in the 1987 Project Loan Agreement) secured by Tax Revenues in such principal amount as shall be determined by the Agency. The Agency may issue and deliver any Parity Debt subject to the following specific conditions which are conditions precedent to the issuance and delivery of such Parity Debt issued under the 1987 Project Loan Agreement: (a) No event of default shall have occurred and be continuing, and the Agency shall otherwise be in compliance with all covenants set forth in the 1987 Project Loan Agreement, the 2001 Loan Agreement and the 2006 Loan Agreement provided that the requirements of this Subsection (a) will not apply to any issue of Parity Debt all of the available proceeds of which will be applied to refund the 1987 Project Loan or any other Parity Debt in whole or in part. (b) The Tax Revenues for the then current fiscal year, as set forth in a written certificate of the Agency, as defined in the Indenture, based on assessed valuation of property in the 1987 Redevelopment Project as evidenced in the written records of the County of Riverside (the County ), shall be at least equal to one hundred twenty-five percent (125%) of the sum of maximum annual debt service on the 1987 Project Loan, the 2001 Loan, the 2006 Loan and all Parity Debt payable from Tax Revenues; provided that (i) the requirements of this Subsection (b) will not apply to any issue of Parity Debt all of the available proceeds of which will be applied to refund the 1987 Project Loan, the 2001 Loan, the 2006 Loan or other Parity Debt in whole or in part, and (ii) debt service on any Parity Debt the proceeds of which are deposited into an escrow fund meeting the requirements of Subsection (d) below will be disregarded for purposes of measuring maximum annual debt service. (c) The related parity debt instrument shall provide that: (1) Interest on such parity debt shall be payable on April 1 and October 1 in each year of the term of such parity debt except the first twelve-month period, during which interest may be payable on any April 1 or October 1; and (2) The principal of such parity debt shall not be payable on any date other than October 1 in any year. 14

21 (d) The proceeds of such Parity Debt may be deposited into an escrow fund to be held by a trustee, from which amounts may not be released to the Agency unless the Tax Revenues for the most recent fiscal year (as evidenced in the written records of the County of Riverside) at least equal one hundred twenty-five percent (125%) of maximum annual debt service with respect to the 1987 Project Loan, the 2001 Loan and the 2006 Loan and the portion of the Parity Debt to be released and any then outstanding Parity Debt. (e) For purposes of calculation of Tax Revenues under the 1987 Project Loan Agreement, Tax Revenues shall be calculated by using the most recent assessed values as evidenced in the written records of the County and a 1% tax rate (without regard to overrides). (f) The issuance of such Parity Debt shall not cause the Agency to exceed any applicable Redevelopment Plan limitations with respect to the 1987 Redevelopment Project. (g) The Agency shall file with the Trustee a Written Certificate of the Agency certifying that all of the foregoing conditions to the issuance of such Parity Debt have been satisfied (including any additional certifications as may be required by the 1987 Project Loan Agreement). 15

22 SCHEDULED DEBT SERVICE ON THE BONDS The following is the scheduled debt service on the Bonds. Interest Payment Date Principal Interest Annual Debt Service October 1, 2009 $65,000 $162, $227, April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, ,000 96, , April 1, , October 1, ,000 92, , April 1, , October 1, ,000 88, , April 1, , October 1, ,000 83, ,

23 Scheduled Debt Service on the Bonds (continued). Interest Payment Date Principal Interest Annual Debt Service April 1, 2030 $78, October 1, 2030 $155,000 78, $312, April 1, , October 1, ,000 73, , April 1, , October 1, ,000 67, , April 1, , October 1, ,000 61, , April 1, , October 1, ,000 54, , April 1, , October 1, ,000 47, , April 1, , October 1, ,000 39, , April 1, , October 1, ,000 31, ,

24 SCHEDULED DEBT SERVICE ON THE 1987 PROJECT LOAN The following is the scheduled debt service on the 1987 Project Loan. Interest Payment Date Principal Interest Annual Debt Service October 1, 2009 $65,000 $162, $227, April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, , , , April 1, , October 1, ,000 96, , April 1, , October 1, ,000 92, , April 1, , October 1, ,000 88, , April 1, , October 1, ,000 83, ,

25 Scheduled Debt Service on the 1987 Project Loan (continued). Interest Payment Date Principal Interest Annual Debt Service April 1, 2030 $78, October 1, 2030 $155,000 78, $312,285 April 1, , October 1, ,000 73, ,435 April 1, , October 1, ,000 67, ,535 April 1, , October 1, ,000 61, ,285 April 1, , October 1, ,000 54, ,985 April 1, , October 1, ,000 47, ,430 April 1, , October 1, ,000 39, ,810 April 1, , October 1, ,000 31, ,125 19

26 SOURCES OF PAYMENT FOR THE BONDS REPAYMENT OF THE BONDS The Bonds The Bonds are secured under an Indenture of Trust, dated as of February 1, 2009, by and between the Authority and Wells Fargo Bank, National Association, Los Angeles, California, as trustee (see APPENDIX A - SUMMARY OF CERTAIN TERMS AND THE INDENTURE ). The proceeds of the Bonds will be loaned to the Agency pursuant to the 1987 Project Loan Agreement. The Bonds are payable from loan payments to be made to the Authority under the 1987 Project Loan Agreement, from certain funds and accounts created under the Indenture, and from investment earnings thereon Project Loan payments to be made under the 1987 Project Loan Agreement are pledged to the payment of principal of and interest on the Bonds pursuant to the Indenture until the Bonds have been paid, or until sufficient moneys have been set aside irrevocably for that purpose. The Trustee will covenant to exercise such rights and remedies as may be necessary to enforce the 1987 Project Loan payments when due under the 1987 Project Loan Agreement and otherwise to attempt to protect the interests of the Bondowners in the event of default by the Authority. The Bonds are limited obligations of the Authority. The Bonds do not constitute a debt or liability of the State or of any political subdivision thereof, other than the Authority. The Authority shall be obligated to pay the principal of the Bonds and the interest thereon, only from the funds described herein and neither the faith and credit nor the taxing power of the City, the State or any of its political subdivisions is pledged to the payment of the principal of or the interest on the Bonds. The Authority has no taxing power. Reserve Fund In order to further secure the payment of principal of and interest on the Bonds, the Trustee is required to deposit in the Reserve Fund under the Indenture an amount sufficient to maintain the Reserve Requirement on deposit in the Reserve Fund. The Reserve Requirement means, in respect of any Bond Year as computed by the Authority, the least of (i) 10% of the original proceeds (within the meaning of section 148 of the Internal Revenue Code of 1986 (the Code )) of the Bonds, (ii) 125% of the average annual debt service as of the date of issuance, or (iii) the maximum annual debt service. In the event that the Agency fails to deposit with the Trustee the full amount required by the 1987 Project Loan Agreement to pay principal and interest due on the Bonds, the Trustee will withdraw from the Reserve Fund the difference between the amount required to be on deposit and the amount available on such date. Amounts in excess of the Reserve Requirement will be transferred to the Revenue Fund under the Indenture to be applied as a credit against the next succeeding loan payment under the 1987 Project Loan Agreement. REPAYMENT OF THE 1987 PROJECT LOAN Tax Allocation Financing In General. The Redevelopment Law provides a means for financing redevelopment projects based upon an allocation of taxes collected within a redevelopment project. The taxable valuation of a redevelopment project last equalized prior to adoption of the redevelopment plan, or base roll, is established and, except for any period during which the taxable valuation drops below the base year level, the taxing agencies within the redevelopment project thereafter receive the taxes produced by the levy of the then current tax rate upon the base roll. Taxes collected upon any increase in taxable valuation over the base roll (except such portion generated by rates levied to pay bonded indebtedness approved by the voters on or after January 1, 1989, for the acquisition or improvement of real property) 20

27 (herein, the Tax Increment Revenues ) are allocated to a redevelopment agency and may be pledged by a redevelopment agency to the repayment of any indebtedness incurred in financing or refinancing a redevelopment project. Redevelopment agencies themselves have no authority to levy property taxes and must look specifically to the allocation of taxes produced as above indicated. Allocation of Taxes. As provided in the Redevelopment Plan of the Agency with respect to the 1987 Redevelopment Project, and pursuant to Article 6 of Chapter 6 of the Redevelopment Law and Section 16 of Article XVI of the Constitution of the State of California, taxes levied upon taxable property in the 1987 Redevelopment Project each year by or for the benefit of the State of California and any city, county, city and county, district or other public corporation (herein collectively referred to as taxing agencies ) for fiscal years beginning after the effective date of the 1987 Redevelopment Project are divided as follows: (1) To Taxing Agencies: That portion of the taxes which would be produced by the rate upon which the tax is levied each year by or for each of said taxing agencies upon the total sum of the assessed value of the taxable property in the 1987 Redevelopment Project as shown upon the assessment roll used in connection with the taxation of such property by such taxing agency last equalized prior to the effective date of the ordinance approving the 1987 Redevelopment Project (or ordinances approving amendments to the Redevelopment Plan adding to the 1987 Redevelopment Project), shall be allocated to, and when collected shall be paid into, the funds of the respective taxing agencies as taxes by or for said taxing agencies on all other property are paid; and (2) To the Agency: Except for the taxes which are attributable to a tax rate levy by a taxing agency for the purpose of producing revenues to repay bonded indebtedness approved by the voters of the taxing agency on or after January 1, 1989, which shall be allocated to and when collected shall be paid to such taxing agency, that portion of said levied taxes each year in excess of the amounts provided in (1) above, shall be allocated to, and when collected, shall be paid into a special fund of the Agency to pay the principal of and interest on bonds, loans, moneys advanced to, or indebtedness (whether funded, refunded, assumed, or otherwise) incurred by the Agency to finance or refinance, in whole or in part, redevelopment activities within the 1987 Redevelopment Project. Unless and until the total assessed valuation of the taxable property in the 1987 Redevelopment Project exceeds the total assessed value of the taxable property in the 1987 Redevelopment Project as shown by the last equalized assessment roll referred to in paragraph (1) above, all of the taxes levied and collected upon the taxable property in the 1987 Redevelopment Project shall be paid into the funds of the respective taxing agencies. When said bonds, loans, advances, and indebtedness, if any, and interest thereon, have been paid, all moneys thereafter received from taxes upon the taxable property in the 1987 Redevelopment Project shall be paid into the funds of the respective taxing agencies as taxes on all other property are paid. The Agency is authorized to make pledges of the portion of taxes mentioned in paragraph (2) above to repay specific advances, loans and indebtedness as appropriate in carrying out the Redevelopment Plan for the 1987 Redevelopment Project. Pledge of Tax Revenues The Agency has pledged a lien on Tax Revenues, as defined herein, to the repayment of the 1987 Project Loan. The pledge of Tax Revenues is on a subordinate basis with any payments required under the Agency s Loan Agreement, dated as of June 1, 2001, with respect to the 1987 Redevelopment Project (the 2001 Loan ) and relating to the Perris Public Financing Authority Tax Allocation Revenue Bonds, 2001 Series A. The pledge of Tax Revenues is on a parity basis with any payments required under the Agency s Loan Agreement, dated as of May 1, 2006, with respect to the 1987 Redevelopment Project (the 2006 Loan ) and relating to the Perris Public Financing Authority 2006 Tax Allocation Revenue Bonds (see INTRODUCTORY STATEMENT THE AGENCY - The 1987 Project Loan Authorization and INTRODUCTORY STATEMENT THE AGENCY - Outstanding Indebtedness of the 1987 Redevelopment Project herein). 21

28 Tax Revenues consist of Tax Increment Revenues from the Agency s 1987 Redevelopment Project, excluding (i) amounts required to be deposited into the Agency s Low and Moderate Income Housing Fund, (ii) the SB 2557 County Administrative fees and collection charges and (iii) amounts required to be paid pursuant to certain Pass-Through Agreements, and Statutory Tax Sharing (as described herein). The 1987 Project Loan is a limited obligation of the Agency payable solely from Tax Revenues, and further, from certain funds and accounts created under the 1987 Project Loan Agreement and investment earnings thereon. The 1987 Project Loan does not constitute a debt or liability of the State or of any political subdivision thereof or a pledge of the faith and credit of the City, the State, or any such political subdivision, other than the Agency. Neither the City, the State nor the Agency shall be obligated to pay the principal of the 1987 Project Loan, or the interest thereon, except from the funds described herein, and neither the faith and credit nor the taxing power of the City, the State or any of its political subdivisions is pledged to the payment of the principal of or the interest on the 1987 Project Loan. The Agency has no ad valorem property taxing power. Alternative Method of Tax Apportionment ( Teeter Plan ) Sections 4701 through 4717 of the California Revenue and Taxation Code permit counties to use a method of apportioning taxes (commonly referred to as the Teeter Plan ) whereby all local agencies with historical delinquency rates less that 3%, including redevelopment agencies, receive from the County 100% of their respective shares of the amount secured ad valorem taxes levied, without regard to actual collections of taxes. Due to this allocation method, the Agency is held harmless from tax delinquencies and, as a consequence, the Agency receives no adjustments for redemption payments of delinquent collections. The unsecured taxes are allocated based on actual unsecured tax collections. The County makes a one-time adjustment for changes in the tax roll in the following year. The County of Riverside has adopted this method of distributing taxes and will continue to do so unless the County Board of Supervisors takes action to discontinue the practice. There is no assurance that the County will continue to allocate tax revenues in this manner. If this method of distributing taxes is discontinued, significant delinquencies in the payment of ad valorem taxes may have an adverse affect on the Agencies ability to make payments under the Housing Loan as such payments come due and payable and accordingly the Authority s ability to pay debt service on the Bonds. 22

29 BONDOWNERS RISKS BEFORE PURCHASING ANY OF THE BONDS, ALL PROSPECTIVE INVESTORS AND THEIR PROFESSIONAL ADVISORS SHOULD CAREFULLY CONSIDER, AMONG OTHER THINGS, THE FOLLOWING RISK FACTORS, WHICH ARE NOT MEANT TO BE AN EXHAUSTIVE LISTING OF ALL RISKS ASSOCIATED WITH THE PURCHASE OF THE BONDS. MOREOVER, THE ORDER OF PRESENTATION OF THE RISK FACTORS DOES NOT NECESSARILY REFLECT THE ORDER OF THEIR IMPORTANCE. The purchase of the Bonds involves investment risk. If a risk factor materializes to a sufficient degree, it could delay or prevent payment of principal of and/or interest on the Bonds. Such risk factors include, but are not limited to, the following matters. THE BONDS General The ability of the Authority to pay the principal of and interest on the Bonds depends upon the receipt by the Trustee of sufficient Revenues from repayment of the 1987 Project Loan, amounts on deposit in the Reserve Fund and interest earnings on amounts in the funds and accounts for the Bonds established by the Indenture. A number of risks that could adversely impact the security or payment of the Bonds are outlined below. No Liability of the Authority to the Owners Except as expressly provided in the Indenture, the Authority will not have any obligation or liability to the Owners of the Bonds with respect to the payment when due of the 1987 Project Loan, or with respect to the observance or performance by the Agency of other agreements, conditions, covenants and terms required to be observed or performed by it under the 1987 Project Loan, the 1987 Project Loan Agreement, the Indenture or any related documents or with respect to the performance by the Trustee of any duty required to be performed by it under the Indenture. Loss of Tax Exemption As discussed under the caption LEGAL MATTERS - TAX EXEMPTION herein, interest on the Bonds could become includable in gross income for purposes of federal income taxation retroactive to the date the Bonds were issued as a result of future acts or omissions of the Authority or the Agency in violation of its covenants contained in the Indenture, the Tax and Non-Arbitrage Certificate and other documents. Should such an event of taxability occur, the Bonds are not subject to special redemption or any increase in interest rate and will remain outstanding until maturity or until redeemed under one of the redemption provisions contained in the Indenture. Secondary Market There can be no guarantee that there will be a secondary market for the Bonds or, if a secondary market exists, that such Bonds can be sold for any particular price. Occasionally, because of general market conditions or because of adverse history or economic prospects connected with a particular issue, secondary marketing practices in connection with a particular issue are suspended or terminated. Additionally, prices of issues for which a market is being made will depend upon then prevailing circumstances. Such prices could be substantially different from the original purchase price. No Effective Acceleration on Default In the event of default under the Indenture, as a practical matter, Bondowners will be limited to obtaining the moneys in the Reserve Fund and enforcing the obligation of the Agency to repay the 1987 Project Loan on an annual basis to the extent of the Tax Revenues. No real or personal property in the

30 Redevelopment Project is pledged to secure the Bonds or the 1987 Project Loan and it is not anticipated that the Agency will have available moneys sufficient to redeem all of the Bonds or the 1987 Project Loan in the event of an acceleration resulting from an event of default. Enforceability of Remedies The remedies available to the Trustee and the registered owners of the Bonds upon an event of default under the Indenture or any other document described herein are in many respects dependent upon regulatory and judicial actions which are often subject to discretion and delay. Under existing law and judicial decisions, the remedies provided for under such documents may not be readily available or may be limited. The various legal opinions to be delivered concurrently with the delivery of the Bonds will be qualified to the extent that the enforceability of the legal documents with respect to the Bonds is subject to limitations imposed by bankruptcy, reorganization, insolvency or other similar laws affecting the rights of creditors generally and by equitable remedies and proceedings generally. THE 1987 PROJECT LOAN Risk Factors Relating to the Reduction of Tax Revenues General. Tax Increment Revenues allocated to the Agency (which constitute the principal source of repayment of the principal of and interest on the 1987 Project Loan, as discussed herein) are a portion of the taxes allocated to the Agency each year which are determined by the amount of incremental valuation of taxable property in the 1987 Redevelopment Project, the current rate or rates at which property in the 1987 Redevelopment Project is taxed and the percentage of taxes collected in the 1987 Redevelopment Project. The Agency has no taxing power, nor does the Agency have the power to affect the rate at which property is taxed. At least four types of events that are beyond the control of the Agency could occur and cause a reduction in Tax Increment Revenues arising from the 1987 Redevelopment Project, thereby impairing the ability of the Agency to make payments of principal of and interest and premium (if any) when due on the 1987 Project Loan and consequently, the Authority s ability to pay debt service on the Bonds. First, a reduction of taxable values of property or tax rates in the 1987 Redevelopment Project or a reduction of the rate of increase in taxable values of property in the 1987 Redevelopment Project caused by economic or other factors beyond the Agency s control (such as a relocation out of the 1987 Redevelopment Project by one or more major property owners, successful appeals by property owners for a reduction in a property s assessed value, a reduction of the general inflationary rate, a reduction in transfers of property, construction activity or other events that permit reassessment of property at lower values, or the destruction of property caused by natural or other disasters, including earthquakes) could occur, thereby causing a reduction in Tax Increment Revenues. Second, the California electorate or legislature could adopt limitations with the effect of reducing Tax Increment Revenues payable to the Agency. Such limitation already exists under Article XIIIA of the California Constitution, which was adopted pursuant to the initiative process. For a further description of Article XIIIA, see PROPERTY TAXATION IN CALIFORNIA -- CONSTITUTIONAL AMENDMENTS AFFECTING TAX INCREMENT REVENUES, herein. Third, a reduction in the tax rate applicable to property in the 1987 Redevelopment Project by reason of discontinuation of certain override tax levies in excess of the 1% basic levy will reduce Tax Increment Revenues otherwise available to pay debt service. Such override can be expected to decline over time until it reaches the 1% basic levy and may be discontinued at any time, which may cause a reduction in Tax Increment Revenues and consequently Tax Revenues. Fourth, delinquencies in the payment of property taxes by the owners of land in the 1987 Redevelopment Project could have an adverse effect on the Agency s ability to make timely payments of principal of and interest on the 1987 Project Loan and consequently, the Authority s ability to pay debt service on the 24