STRUCTURE FOR

|

|

|

- Chloe Hodge

- 5 years ago

- Views:

Transcription

1 STRUCTURE FOR IMPACT

2 form follows function

3 how do you define success?

4 what is your Business model?

5 profit purpose tension zero sum game increasing purpose at the expense of profit often beneficiaries are a part of the supply chain

6 warby parker

7 optimal structures Benefit corporation flexible purpose corporation l3c b Corp certification

8 profit purpose alignment win - win scenario increasing purpose will increase profits Often beneficiaries are the customer

9 indigo

10 optimal legal structure corporation llc benefit corporation flexible purpose corporation l3c

11 decoupled All Purpose / No profit Beneficiaries are not linked to revenues third party must generate a revenue stream

12 charity : water

13 optimal legal structure nonprofit

14 Legal structures

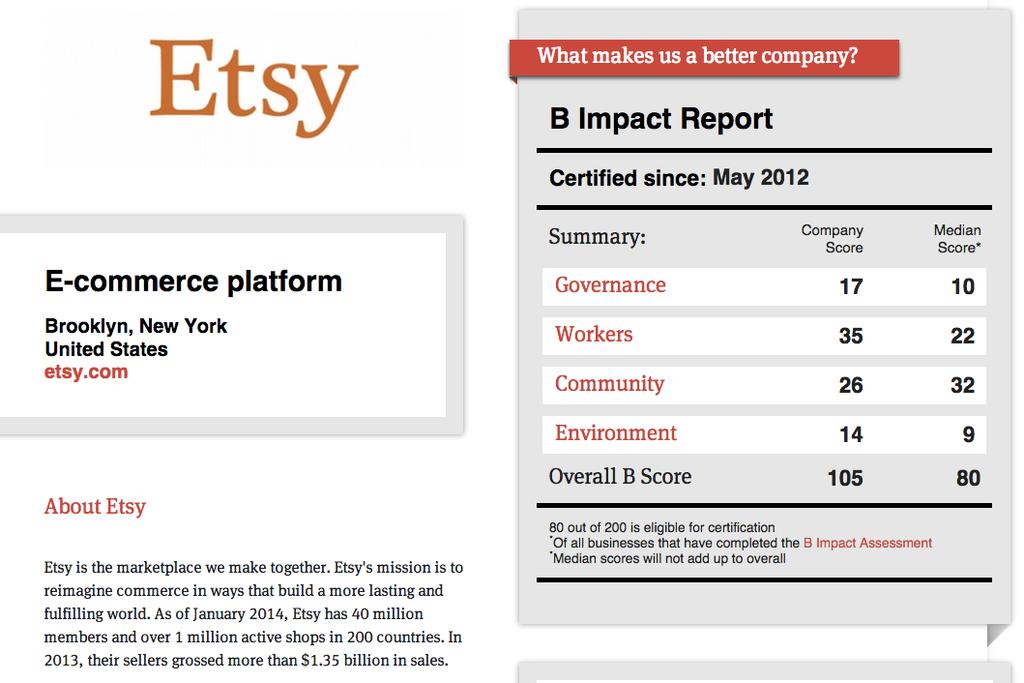

15 B corp certification

16 certification for sustainable business Voluntary certification Not legal structure can be applied to any legal structure differentiates good companies from companies with good marketing

17 formation 80/200 on B labs assessment include key language in organizing documents

18

19 management PERIODIC ASSESSMENT MUST PUBLISH RESULTS OF ASSESSMENT

20 taxation DEPENDING ON FORM 1ST TAX BREAKS IN THE CITY OF PHILADELPHIA

21 capital depends on legal structure

22 ETSY

23 benefit corporation

24 a new class of corporation mandate to operate for public benefit increase in transparency / accountability

25 general public benefit A MATERIAL POSITIVE IMPACT ON SOCIETY AND THE ENVIRONMENT, TAKEN AS A WHOLE, ASSESSED AGAINST A 3RD PARTY STANDARD, FROM THE BUSINESS AND OPERATIONS OF A BENEFIT CORPORATION.

26 third party standard DEVELOPED BY A PARTY NOT RELATED TO THE ENTITY IT S MEASURING TRANSPARENT IN ITS METHODOLOGY

27 specific public benefit PROVIDING INDIVIDUALS / COMMUNITIES WITH BENEFICIAL PRODUCTS OR SERVICES PROMOTING ECONOMIC OPPORTUNITIES FOR INDIVIDUALS OR COMMUNITIES BEYOND JOB CREATION Promoting health / Environmental preservation Promoting Arts / sciences

28 transparency ISSUE ANNUAL REPORT INCLUDING RECORD OF SUCCESSES AND FAILURES for general and specific public benefit 120 DAYS AFTER THE CLOSE OF THE FISCAL YEAR PUBLICLY AVAILABLE

29 formation FILE ARTICLES OF INCORPORATION STATing benefit corporation STATUS and specific public benefit IF EXISTING CORP, MUST HAVE 2/3 VOTE DRAFT BYLAWS HOLD ORGANIZATIONAL MEETING ISSUE STOCK including specific language

30 management MANAGED BY DIRECTORS OFFICERS RUN DAY TO DAY OPERATIONS DIRECTORS MUST TAKE BENEFIT INTO ACCOUNT ON ALL DECISION MAKING ANNUAL ASSESSMENT BY 3RD PARTY Most states require a benefit director

31 taxation SUBJECT TO CORPORATE TAX ON NET INCOME IF SHAREHOLDERS RECEIVE DIVIDENDS, THAT IS SUBJECT TO PERSONAL INCOME TAX no tax favored status... yet.

32 capital EQUITY DEBT PRI

33 METHOD

34 SOCIAL purpose corporation

35 a new class of corporation allows corporation to pursue a special purpose protects directors from shareholder suit

36 formation FILE ARTICLES OF INCORPORATION STATing FPC STATUS and special purpose IF EXISTING CORP, MUST HAVE 2/3 VOTE DRAFT BYLAWS HOLD ORGANIZATIONAL MEETING ISSUE STOCK

37 management MANAGED BY DIRECTORS OFFICERS RUN DAY TO DAY OPERATIONS DIRECTORS MAY CHOOSE TO INCLUDE BENEFIT IN DECISION MAKING NO 3RD PARTY VERIFICATION ANNUAL BENEFIT REPORT

38 taxation SUBJECT TO CORPORATE TAX ON NET INCOME IF SHAREHOLDERS RECEIVE DIVIDENDS, THAT IS SUBJECT TO PERSONAL INCOME TAX NO TAX FAVORED STATUS YET.

39 capital EQUITY DEBT PRI

40 L3C

41 a new class of LLC Elevates charitable purpose over profit allows a mix of philanthropic and private capital

42 program related investment TAX REFORM ACT OF 1969 REQUIRED STRICT CONSERVATIVE RULES ON FOUNDATION INVESTMENT PRI IS AN EXCEPTION FOR ORGANIZATIONS THAT HAVE A CHARITABLE PURPOSE USED INFREQUENTLY

43 formation FILE ARTICLES OF ORGANIZATION WITH THE STATE INCLUDE CHARITABLE PURPOSE IN ORGANIZING DOCS NEGOTIATE AND EXECUTE OPERATING AGREEMENT

44 management MOST FLEXIBLE LEAST AMOUNT OF FILINGS MEMBERS CAN OPERATE DAY TO DAY OR DELEGATE THAT TO MANAGERS

45 taxation MOST L3C S CHOOSE PASS THROUGH TAXATION TREATMENT NO TAX EXEMPT STATUS

46 capital DESIGNED SPECIFICALLY TO RECEIVE PRI EQUITY DEBT

47 moo milk

48

49 join the conversation BIT.LY/PPSUB

Chapter 500. (Senate Bill 595)

") MARTIN O'MALLEY, Governor Ch. 500 Chapter 500 (Senate Bill 595) AN ACT concerning Corporations and Associations Name Requirements for Benefit Corporations and Limited Liability Companies Election to Be

MARTIN O'MALLEY, Governor Ch. 500 Chapter 500 (Senate Bill 595) AN ACT concerning Corporations and Associations Name Requirements for Benefit Corporations and Limited Liability Companies Election to Be

HOUSE BILL (1lr2906) ENROLLED BILL Economic Matters/Judicial Proceedings. Read and Examined by Proofreaders:

ENROLLED BILL Economic Matters/Judicial Proceedings. Read and Examined by Proofreaders:") C Introduced by Delegate Feldman HOUSE BILL ENROLLED BILL Economic Matters/Judicial Proceedings (lr0) Read and Examined by Proofreaders: Proofreader. Proofreader. Sealed with the Great Seal and presented

C Introduced by Delegate Feldman HOUSE BILL ENROLLED BILL Economic Matters/Judicial Proceedings (lr0) Read and Examined by Proofreaders: Proofreader. Proofreader. Sealed with the Great Seal and presented

Connecticut Benefit Corporation How-To Guide

1 Benefit Corporation Connecticut Benefit Corporation How-To Guide Overview Unlike traditional corporations that make business decisions primarily to maximize shareholder value, benefit corporations aim

1 Benefit Corporation Connecticut Benefit Corporation How-To Guide Overview Unlike traditional corporations that make business decisions primarily to maximize shareholder value, benefit corporations aim

RUNNING A SOCIAL ENTERPRISE: LEGAL STRUCTURE AND TAX CONSIDERATIONS

RUNNING A SOCIAL ENTERPRISE: LEGAL STRUCTURE AND TAX CONSIDERATIONS Mission Edge: San Diego Accelerator + Impact Lab (SAIL) September 25, 2017 0 Questions for audience What are you hoping to learn? Is

RUNNING A SOCIAL ENTERPRISE: LEGAL STRUCTURE AND TAX CONSIDERATIONS Mission Edge: San Diego Accelerator + Impact Lab (SAIL) September 25, 2017 0 Questions for audience What are you hoping to learn? Is

No An act relating to the Vermont Benefit Corporations Act. (S.263) It is hereby enacted by the General Assembly of the State of Vermont:

It is hereby enacted by the General Assembly of the State of Vermont:") No. 113. An act relating to the Vermont Benefit Corporations Act. (S.263) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. 11A V.S.A. chapter 21 is added to read: CHAPTER 21.

No. 113. An act relating to the Vermont Benefit Corporations Act. (S.263) It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. 11A V.S.A. chapter 21 is added to read: CHAPTER 21.

Knowledge Share. Alternative. Navigating New choices for business formations

Knowledge Share Alternative ENTITIES Navigating New choices for business formations 2016 SEMINAR REFERENCE BOOK NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS Seminar Reference Book TABLE OF CONTENTS INTRODUCTION

Knowledge Share Alternative ENTITIES Navigating New choices for business formations 2016 SEMINAR REFERENCE BOOK NAVIGATING NEW CHOICES FOR BUSINESS FORMATIONS Seminar Reference Book TABLE OF CONTENTS INTRODUCTION

February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS

February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS UC Berkeley, February 20, 2018 Speakers Jennifer Barnette Cooley LLP Jesse Finfrock Morrison & Foerster LLP 1 How do non-profits and for-profits

February 20, 2018 LEGAL STRUCTURES FOR SOCIAL ENTREPRENEURS UC Berkeley, February 20, 2018 Speakers Jennifer Barnette Cooley LLP Jesse Finfrock Morrison & Foerster LLP 1 How do non-profits and for-profits

STEWARDSHIP PRINCIPLES MAY 2017

Stewardship Principles Stewardship for institutional investors means fulfilling their responsibilities as fiduciaries in meeting their obligations to their beneficiaries or clients. Stewardship is intended

Stewardship Principles Stewardship for institutional investors means fulfilling their responsibilities as fiduciaries in meeting their obligations to their beneficiaries or clients. Stewardship is intended

Family Wealth Advisors

Family Wealth Advisors Philanthropy Services Terms Glossary & Definitions 1. B Corporation B Corporations are certified by the nonprofit B Lab to meet standards of social and environmental performance,

Family Wealth Advisors Philanthropy Services Terms Glossary & Definitions 1. B Corporation B Corporations are certified by the nonprofit B Lab to meet standards of social and environmental performance,

Fiduciary Guidelines for Foundation & Endowment Trustees

1 Legal and Regulatory Oversight 3 Selecting and Monitoring Investment Managers 2 Developing a Spending Policy 2 Investment Policy Statements 3 Administration and Records online report consulting group

1 Legal and Regulatory Oversight 3 Selecting and Monitoring Investment Managers 2 Developing a Spending Policy 2 Investment Policy Statements 3 Administration and Records online report consulting group

Maryland Benefit Corporation How-To-Guide: Incorporating as a Benefit Corporation Step-by-Step October 2013 B Lab

Maryland Benefit Corporation How-To-Guide: Incorporating as a Benefit Corporation Step-by-Step October 2013 B Lab I. Introduction This paper serves as a guide for benefit corporation law. This guide will

Maryland Benefit Corporation How-To-Guide: Incorporating as a Benefit Corporation Step-by-Step October 2013 B Lab I. Introduction This paper serves as a guide for benefit corporation law. This guide will

The Evolution of Community Foundation Relationships with Agencies and Affiliates

The Evolution of Community Foundation Relationships with Agencies and Affiliates Suzanne Friday, Esq. Senior Legal Counsel Vice President of Legal Affairs Experience and Training - Past Counsel, Nature

The Evolution of Community Foundation Relationships with Agencies and Affiliates Suzanne Friday, Esq. Senior Legal Counsel Vice President of Legal Affairs Experience and Training - Past Counsel, Nature

Louisiana Benefit Corporation How-To-Guide: Incorporating as a Benefit Corporation Step-by-Step Guide

Louisiana Benefit Corporation How-To-Guide: Incorporating as a Benefit Corporation Step-by-Step Guide September 2013 B Lab and the New Orleans Business Alliance I. Introduction This paper serves as a guide

Louisiana Benefit Corporation How-To-Guide: Incorporating as a Benefit Corporation Step-by-Step Guide September 2013 B Lab and the New Orleans Business Alliance I. Introduction This paper serves as a guide

ASSEMBLY, No STATE OF NEW JERSEY. 214th LEGISLATURE INTRODUCED DECEMBER 6, 2010

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED DECEMBER, 0 Sponsored by: Assemblywoman CONNIE WAGNER District (Bergen) Assemblywoman LINDA STENDER District (Middlesex, Somerset and Union)

ASSEMBLY, No. STATE OF NEW JERSEY th LEGISLATURE INTRODUCED DECEMBER, 0 Sponsored by: Assemblywoman CONNIE WAGNER District (Bergen) Assemblywoman LINDA STENDER District (Middlesex, Somerset and Union)

Family Wealth Transfer

Family Wealth Transfer It can be difficult. Creating and growing significant wealth is hard. Likewise, the process of preserving and stewarding assets for you, your family, and your charitable priorities

Family Wealth Transfer It can be difficult. Creating and growing significant wealth is hard. Likewise, the process of preserving and stewarding assets for you, your family, and your charitable priorities

Last Updated: November SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire

Last Updated: November 2013 SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire Table of Contents 1. Nonprofit Corporations 2. For-Profit Corporations 3. Benefit Corporations 4. Limited

Last Updated: November 2013 SOUTH CAROLINA FORMS OF ORGANIZATION Wyche, P.A. Eric K. Graben, Esquire Table of Contents 1. Nonprofit Corporations 2. For-Profit Corporations 3. Benefit Corporations 4. Limited

Start Smart Law Presents: Social Enterprise - Profit with A Purpose

Start Smart Law Presents: Social Enterprise - Profit with A Purpose This is Not Legal Advice! Stephanie I do NOT practice law Purpose of Tonight s Session: To Make You a Better Consumer of Legal Services,

Start Smart Law Presents: Social Enterprise - Profit with A Purpose This is Not Legal Advice! Stephanie I do NOT practice law Purpose of Tonight s Session: To Make You a Better Consumer of Legal Services,

Family Wealth Advisors

Family Wealth Advisors Philanthropy Services Terms Glossary & Definitions 1. Purpose investments Coined by Bank of the West, this term includes impact investing, environmental and social governance (ESG),

Family Wealth Advisors Philanthropy Services Terms Glossary & Definitions 1. Purpose investments Coined by Bank of the West, this term includes impact investing, environmental and social governance (ESG),

SOCIAL PURPOSE CORPORATIONS AND BENEFIT CORPORATIONS NEW BUSINESS ENTITIES AUTHORIZED BY FLORIDA LAW

SOCIAL PURPOSE CORPORATIONS AND BENEFIT CORPORATIONS NEW BUSINESS ENTITIES AUTHORIZED BY FLORIDA LAW Jane D. Callahan, Esq. Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth, P.A. A. Introduction 1.

SOCIAL PURPOSE CORPORATIONS AND BENEFIT CORPORATIONS NEW BUSINESS ENTITIES AUTHORIZED BY FLORIDA LAW Jane D. Callahan, Esq. Dean, Mead, Egerton, Bloodworth, Capouano & Bozarth, P.A. A. Introduction 1.

Mission Align 360. Implementation Road Map

Mission Align 360 Implementation Road Map A process by which an organization, such as a foundation, examines all capital including human, financial and philanthropic for allocation toward its mission and

Mission Align 360 Implementation Road Map A process by which an organization, such as a foundation, examines all capital including human, financial and philanthropic for allocation toward its mission and

Ralph Berthon CPCOA Board Member

8 24 2017 To Incorporate or Remain An Association At the request of the Chinook Pass Cabin Owners Association (CPCOA) Board of Directors, I have put together these notes on associations and 501 (C) (7)

8 24 2017 To Incorporate or Remain An Association At the request of the Chinook Pass Cabin Owners Association (CPCOA) Board of Directors, I have put together these notes on associations and 501 (C) (7)

Principle 1: Institutional Investors should publicly disclose their policy on how they will discharge their stewardship responsibilities

Trilogy and Effective Investor Stewardship Principle 1: Institutional Investors should publicly disclose their policy on how they will discharge their stewardship responsibilities As an institutional investor,

Trilogy and Effective Investor Stewardship Principle 1: Institutional Investors should publicly disclose their policy on how they will discharge their stewardship responsibilities As an institutional investor,

8.1 Entrepreneurs 8.2 Sole Proprietorships and Partnerships 8.3 Corporations and Other Organizations

CHAPTER 8 Businesses 8.1 Entrepreneurs 8.2 Sole Proprietorships and Partnerships 8.3 Corporations and Other Organizations 1 CONTEMPORARY ECONOMICS: LESSON 8.1 Consider CHAPTER 8 Businesses Why do some

CHAPTER 8 Businesses 8.1 Entrepreneurs 8.2 Sole Proprietorships and Partnerships 8.3 Corporations and Other Organizations 1 CONTEMPORARY ECONOMICS: LESSON 8.1 Consider CHAPTER 8 Businesses Why do some

Medical Scheme Investment Conference 2012 Should ESG/CRISA considered when making investment decisions?

Medical Scheme Investment Conference 2012 Should ESG/CRISA considered when making investment decisions? Xolisa Dhlamini Independent Actuaries and Consultants August 2012 Contents Background to Responsible

Medical Scheme Investment Conference 2012 Should ESG/CRISA considered when making investment decisions? Xolisa Dhlamini Independent Actuaries and Consultants August 2012 Contents Background to Responsible

TENNESSEE S FOR PROFIT BENEFIT CORPORATION ACT: WILL MORE REGULATION ACHIEVE THE DESIRED RESULTS?

TENNESSEE S FOR PROFIT BENEFIT CORPORATION ACT: WILL MORE REGULATION ACHIEVE THE DESIRED RESULTS? Brian Krumm* Professor Murray provides an excellent overview of social enterprise law and his insights

TENNESSEE S FOR PROFIT BENEFIT CORPORATION ACT: WILL MORE REGULATION ACHIEVE THE DESIRED RESULTS? Brian Krumm* Professor Murray provides an excellent overview of social enterprise law and his insights

Nonprofits and Social Enterprise: Finding the Right Fit for Your Organization

Nonprofits and Social Enterprise: Finding the Right Fit for Your Organization Karen Leaffer 25th Annual Institute on Advising Nonprofit Organizations May 5, 2016 2016 Leaffer Law Group 1 Agenda 1. What

Nonprofits and Social Enterprise: Finding the Right Fit for Your Organization Karen Leaffer 25th Annual Institute on Advising Nonprofit Organizations May 5, 2016 2016 Leaffer Law Group 1 Agenda 1. What

Current as of April 2018 Comments related to any information in this Note should be addressed to Mai El-Sadany.

POLAND Current as of April 2018 Comments related to any information in this Note should be addressed to Mai El-Sadany. TABLE OF CONTENTS I. Summary A. Types of Organizations B. Tax Laws II. III. Applicable

POLAND Current as of April 2018 Comments related to any information in this Note should be addressed to Mai El-Sadany. TABLE OF CONTENTS I. Summary A. Types of Organizations B. Tax Laws II. III. Applicable

T A X A B L E F O U N D A T I O N S

T A X A B L E F O U N D A T I O N S Sarah D. McDaniel, Andrea Sanft, Beth Smith and Paul Stam 2016 While limited liability companies (LLC) have been used for years to house funds earmarked for philanthropy,

T A X A B L E F O U N D A T I O N S Sarah D. McDaniel, Andrea Sanft, Beth Smith and Paul Stam 2016 While limited liability companies (LLC) have been used for years to house funds earmarked for philanthropy,

IC-DISC TAX SAVINGS FOR EXPORTERS. An overlooked tax break that could be your big break. Reduce Current & Future Taxes

IC-DISC TAX SAVINGS FOR EXPORTERS An overlooked tax break that could be your big break Reduce Current & Future Taxes Interest Charge Domestic International Sales Corporation (IC-DISC) 1 What Is An IC-DISC?

IC-DISC TAX SAVINGS FOR EXPORTERS An overlooked tax break that could be your big break Reduce Current & Future Taxes Interest Charge Domestic International Sales Corporation (IC-DISC) 1 What Is An IC-DISC?

Announcing the Philanthropic Facilitation Act (H.R. 2832)

") Announcing the Philanthropic Facilitation Act (H.R. 2832) On July 25, 2013, Rep. Cory Gardner (R-CO) introduced the Philanthropic Facilitation Act (PFA) (H.R. 2832) which was written by Americans for Community

Announcing the Philanthropic Facilitation Act (H.R. 2832) On July 25, 2013, Rep. Cory Gardner (R-CO) introduced the Philanthropic Facilitation Act (PFA) (H.R. 2832) which was written by Americans for Community

Guidelines for Charitable Funds

Guidelines for Charitable Funds These guidelines describe how to open a charitable fund with the Catholic Community Foundation of Los Angeles (the Foundation ). We summarize the types of funds that are

Guidelines for Charitable Funds These guidelines describe how to open a charitable fund with the Catholic Community Foundation of Los Angeles (the Foundation ). We summarize the types of funds that are

Exemptions and Other Special Tax Treatment

Exemptions and Other Special Tax Treatment This technical document is part of a series of draft discussion papers created by Municipal Affairs staff and stakeholders to prepare for the Municipal Government

Exemptions and Other Special Tax Treatment This technical document is part of a series of draft discussion papers created by Municipal Affairs staff and stakeholders to prepare for the Municipal Government

PASS-THROUGH TAXPAYER OPPORTUNITY

PASS-THROUGH TAXPAYER OPPORTUNITY $10,000 Maximum Apogee Scholarship Fund 3330 Cumberland Blvd, Suite 400 Atlanta, GA 30339 P: (404) 419-7123 or 7127 F: (404) 419-7101 scholarships@apogeescholarships.org

PASS-THROUGH TAXPAYER OPPORTUNITY $10,000 Maximum Apogee Scholarship Fund 3330 Cumberland Blvd, Suite 400 Atlanta, GA 30339 P: (404) 419-7123 or 7127 F: (404) 419-7101 scholarships@apogeescholarships.org

Home Address City State Zip Code. Business Address City State Zip Code. Home Address City State Zip Code. Business Address City State Zip Code

THIS AGREEMENT is entered into this day of, 20, by the Greater Manhattan Community Foundation ( GMCF ), a Kansas not-for-profit charitable corporation, and. AUTHORIZED REPRESENTATIVE INFORMATION AUTHORIZED

THIS AGREEMENT is entered into this day of, 20, by the Greater Manhattan Community Foundation ( GMCF ), a Kansas not-for-profit charitable corporation, and. AUTHORIZED REPRESENTATIVE INFORMATION AUTHORIZED

BENEFIT CORPORATIONS. Chintan Panchal. Founder, RPCK Rastegar Panchal

BENEFIT CORPORATIONS Chintan Panchal Founder, RPCK Rastegar Panchal Benefit Corporations Purpose: create a general public benefit Director Duties: benefit corporations expand the purview of the board to

BENEFIT CORPORATIONS Chintan Panchal Founder, RPCK Rastegar Panchal Benefit Corporations Purpose: create a general public benefit Director Duties: benefit corporations expand the purview of the board to

June Private Foundation

June 2017 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

June 2017 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

Boulder Junction Community Foundation, Inc. Financial Statements

Boulder Junction Community Foundation, Inc. Financial Statements Years Ended December 31, 2017 and 2016 Financial Statements Years Ended December 31, 2017 and 2016 Table of Contents Independent Accountant's

Boulder Junction Community Foundation, Inc. Financial Statements Years Ended December 31, 2017 and 2016 Financial Statements Years Ended December 31, 2017 and 2016 Table of Contents Independent Accountant's

Introduction. The Assessment consists of: Evaluation questions that assess best practices. A rating system to rank your board s current practices.

ESG / Sustainability Governance Assessment: A Roadmap to Build a Sustainable Board By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com November 2017 Introduction This is a tool for

ESG / Sustainability Governance Assessment: A Roadmap to Build a Sustainable Board By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com November 2017 Introduction This is a tool for

Credit Suisse 23 rd Annual Energy Summit

Credit Suisse 23 rd Annual Energy Summit Bill Way, President and CEO Compete and Win NYSE: SWN Forward-Looking Statements This presentation includes forward-looking statements. Forward-looking statements

Credit Suisse 23 rd Annual Energy Summit Bill Way, President and CEO Compete and Win NYSE: SWN Forward-Looking Statements This presentation includes forward-looking statements. Forward-looking statements

Gift Acceptance Policy

INDIAN HILLS COMMUNITY COLLEGE FOUNDATION, INC. Gift Acceptance Policy The Indian Hills Community College Foundation, Inc., (the Foundation) exists to secure private gifts for the benefit of Indian Hills

INDIAN HILLS COMMUNITY COLLEGE FOUNDATION, INC. Gift Acceptance Policy The Indian Hills Community College Foundation, Inc., (the Foundation) exists to secure private gifts for the benefit of Indian Hills

MAY Private Foundation

MAY 2016 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

MAY 2016 Private Foundation A private foundation is a legal entity created, funded and operated for the primary purpose of making grants to charities. Because of its charitable mission, a private foundation

Responsible Investment Policy. July 2017

Responsible Investment Policy July 2017 Apax Partners Responsible Investment Policy July 2017 2 Mission Statement Apax s mission is to cultivate and help realize the potential of portfolio companies, their

Responsible Investment Policy July 2017 Apax Partners Responsible Investment Policy July 2017 2 Mission Statement Apax s mission is to cultivate and help realize the potential of portfolio companies, their

Home Address City State Zip Code. Business Address City State Zip Code. Home Address City State Zip Code. Business Address City State Zip Code

THIS AGREEMENT is entered into this day of, 20, by the Greater Manhattan Community Foundation ( GMCF ), a Kansas not-for-profit charitable corporation, and. DONOR ADVISOR INFORMATION Donor Advisor 1 (all

THIS AGREEMENT is entered into this day of, 20, by the Greater Manhattan Community Foundation ( GMCF ), a Kansas not-for-profit charitable corporation, and. DONOR ADVISOR INFORMATION Donor Advisor 1 (all

Legal Considerations for Social Enterprises

Legal Considerations for Social Enterprises Stephanie Ann Dangel Oded Green Eryn Correa Copyright 2016 by K&L Gates LLP. All rights reserved. OUTLINE What is a Social Enterprise? Choice of Entity For Profit

Legal Considerations for Social Enterprises Stephanie Ann Dangel Oded Green Eryn Correa Copyright 2016 by K&L Gates LLP. All rights reserved. OUTLINE What is a Social Enterprise? Choice of Entity For Profit

Benefit Corporation FAQ. Frequently Asked Questions for Investors.

FAQ Frequently Asked Questions for Investors www.benefitcorp.net Investor FAQ Q: How does a benefit corporation differ from a traditional corporation? A benefit corporation has a modified governance structure

FAQ Frequently Asked Questions for Investors www.benefitcorp.net Investor FAQ Q: How does a benefit corporation differ from a traditional corporation? A benefit corporation has a modified governance structure

Tax Exempt and Charitable Planning

Tax Exempt and Charitable Planning Bryan Cave lawyers routinely assist numerous nonprofit and tax-exempt organizations to achieve their missions. Our lawyers also routinely assist individuals interested

Tax Exempt and Charitable Planning Bryan Cave lawyers routinely assist numerous nonprofit and tax-exempt organizations to achieve their missions. Our lawyers also routinely assist individuals interested

Integrating Environmental, Social, and Governance Risks into Enterprise Risk Management. 7 May 2018

Integrating Environmental, Social, and Governance Risks into Enterprise Risk Management 7 May 2018 World Business Council for Sustainability Development MISSION: To accelerate the transition to a sustainable

Integrating Environmental, Social, and Governance Risks into Enterprise Risk Management 7 May 2018 World Business Council for Sustainability Development MISSION: To accelerate the transition to a sustainable

A Guide to Your Donor-Advised Fund

A Guide to Your Donor-Advised Fund Contents Introduction 1 About National Philanthropic Trust 1 About Hollencrest Securities 1 The Independent Charitable Gift Fund 1 Creating a Donor-Advised Fund 2 Contributions

A Guide to Your Donor-Advised Fund Contents Introduction 1 About National Philanthropic Trust 1 About Hollencrest Securities 1 The Independent Charitable Gift Fund 1 Creating a Donor-Advised Fund 2 Contributions

Submission. To the Senate Standing Committee on Social Affairs, Science and Technology. February Presented by Hilary Pearson, President

Submission To the Senate Standing Committee on Social Affairs, Science and Technology February 2018 Presented by Hilary Pearson, President Philanthropic Foundations Canada Fondations philanthropiques Canada

Submission To the Senate Standing Committee on Social Affairs, Science and Technology February 2018 Presented by Hilary Pearson, President Philanthropic Foundations Canada Fondations philanthropiques Canada

Statement on Climate Change

Statement on Climate Change BMO Financial Group (BMO) considers climate change one of the defining issues of our generation. Everyone, including BMO, bears responsibility for the effectiveness of the response.

Statement on Climate Change BMO Financial Group (BMO) considers climate change one of the defining issues of our generation. Everyone, including BMO, bears responsibility for the effectiveness of the response.

Gift Policy. Responsible Officer. Vice-Chancellor Approved by

Gift Policy Responsible Officer Vice-Chancellor Approved by Council Approved and commenced August, 2012 Review by August, 2015 Relevant Legislation, Ordinance, Rule and/or Governance Level Principle Scholarships

Gift Policy Responsible Officer Vice-Chancellor Approved by Council Approved and commenced August, 2012 Review by August, 2015 Relevant Legislation, Ordinance, Rule and/or Governance Level Principle Scholarships

PRI REPORTING FRAMEWORK 2018 Overview and Guidance

PRI REPORTING FRAMEWORK 2018 Overview and Guidance December 2017 reporting@unpri.org +44 (0) 20 3714 3187 THE SIX PRINCIPLES 1 2 3 4 5 6 We will incorporate ESG issues into investment analysis and decision-making

PRI REPORTING FRAMEWORK 2018 Overview and Guidance December 2017 reporting@unpri.org +44 (0) 20 3714 3187 THE SIX PRINCIPLES 1 2 3 4 5 6 We will incorporate ESG issues into investment analysis and decision-making

Key Provisions of 2017 Tax Reform

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

2016 Charitable Giving Review

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

2016 Charitable Giving Review SUMMARY TABLE OF CONTENTS With the end of the year approaching rapidly, Morgan Stanley Global Impact Funding Trust, Inc. ( Morgan Stanley GIFT ) would like to take this opportunity

A Guide to Your Donor-Advised Fund

A Guide to Your Donor-Advised Fund Introduction Thank you for your interest in establishing a donor-advised fund (DAF) with National Philanthropic Trust (NPT). NPT is a tax-exempt public charity under

A Guide to Your Donor-Advised Fund Introduction Thank you for your interest in establishing a donor-advised fund (DAF) with National Philanthropic Trust (NPT). NPT is a tax-exempt public charity under

CITY OF PARKSVILLE POLICY

CITY OF PARKSVILLE POLICY SUBJECT: Permissive Taxation POLICY NO: 6.15 Exemption Applications RESO. NO: 04-285 CROSS REF: EFFECTIVE DATE: September 8, 2004 APPROVED BY: Council REVISION DATE: July 15,

CITY OF PARKSVILLE POLICY SUBJECT: Permissive Taxation POLICY NO: 6.15 Exemption Applications RESO. NO: 04-285 CROSS REF: EFFECTIVE DATE: September 8, 2004 APPROVED BY: Council REVISION DATE: July 15,

INTRODUCING THE ILLINOIS L 3 C

INTRODUCING THE ILLINOIS L 3 C Marc J. Lane Hosted by: COMMUNITY ECONOMIC DEVELOPMENT LAW PROJECT Copyright 2009, by Marc J. Lane. All rights reserved. The 1-2 Punch Mission-related investing Program-related

INTRODUCING THE ILLINOIS L 3 C Marc J. Lane Hosted by: COMMUNITY ECONOMIC DEVELOPMENT LAW PROJECT Copyright 2009, by Marc J. Lane. All rights reserved. The 1-2 Punch Mission-related investing Program-related

Accounting, Counting & Recognition Beyond the Annual Fund

Accounting, Counting & Recognition Beyond the Annual Fund April 11, 2019 Marie Ruzek Senior Philanthropic Specialist, Wells Fargo Philanthropic Services Athena Mihas Vice President, Finance, Greater Twin

Accounting, Counting & Recognition Beyond the Annual Fund April 11, 2019 Marie Ruzek Senior Philanthropic Specialist, Wells Fargo Philanthropic Services Athena Mihas Vice President, Finance, Greater Twin

Methods of Giving to the University of Florida

I am pleased to have been able to make this gift to the university, but I am doubly pleased to know this was a good financial choice for me and my family that will reap benefits for many years to come.

I am pleased to have been able to make this gift to the university, but I am doubly pleased to know this was a good financial choice for me and my family that will reap benefits for many years to come.

The Annotated Will 2017: GRE and Charitable Donation Rules

The Annotated Will 2017: GRE and Charitable Donation Rules Darren G. Lund Benefits and Implications of GRE Status Graduated rate taxation for income retained in estate Ability to choose off-calendar year-end

The Annotated Will 2017: GRE and Charitable Donation Rules Darren G. Lund Benefits and Implications of GRE Status Graduated rate taxation for income retained in estate Ability to choose off-calendar year-end

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker Establishing a private foundation can be a fulfilling way to work with charities, but be prepared

Philanthropy as a Family Affair: Using a Private Foundation to Achieve Your Charitable Goals ~ Susan B. Hecker Establishing a private foundation can be a fulfilling way to work with charities, but be prepared

Significant increase in private sector financing of the SDGs benefitting poor and vulnerable people.

Background Launched in 2015, The Rockefeller Foundation s Zero Gap portfolio supports the R&D and piloting of new financing mechanisms to mobilize private sector capital towards the Nations (UN) Sustainable

Background Launched in 2015, The Rockefeller Foundation s Zero Gap portfolio supports the R&D and piloting of new financing mechanisms to mobilize private sector capital towards the Nations (UN) Sustainable

CALIFORNIA S LIMITED LIABILITY COMPANY ANNUAL FEE AND THE TAXATION OF MULTIPLE ENTITIES (Business Advisory No. 5)

") CALIFORNIA S LIMITED LIABILITY COMPANY ANNUAL FEE AND THE TAXATION OF MULTIPLE ENTITIES (Business Advisory No. 5) California has established permanent tax rates for limited liability companies (LLCs).

CALIFORNIA S LIMITED LIABILITY COMPANY ANNUAL FEE AND THE TAXATION OF MULTIPLE ENTITIES (Business Advisory No. 5) California has established permanent tax rates for limited liability companies (LLCs).

Charitable Remainder Annuity Trust Presentation Input Screen

Charitable Remainder Annuity Trust Presentation Input Screen Annuity Trust Questions Gift Asset Questions Case Name ----- NEW CASE ----- Gift Asset Type Cash Name for Reports Betty Anthropist Value of

Charitable Remainder Annuity Trust Presentation Input Screen Annuity Trust Questions Gift Asset Questions Case Name ----- NEW CASE ----- Gift Asset Type Cash Name for Reports Betty Anthropist Value of

PROF A.N. NEVHUTANDA CHAIRPERSON NATIONAL LOTTERIES BOARD 23 JUNE 2015

PROF A.N. NEVHUTANDA CHAIRPERSON NATIONAL LOTTERIES BOARD 23 JUNE 2015 1 EFFECTIVE REGULATION OF LOTTERIES WHAT NEEDS TO BE DONE OR IMPROVED Introduction of the National Lottery in South Africa At the

PROF A.N. NEVHUTANDA CHAIRPERSON NATIONAL LOTTERIES BOARD 23 JUNE 2015 1 EFFECTIVE REGULATION OF LOTTERIES WHAT NEEDS TO BE DONE OR IMPROVED Introduction of the National Lottery in South Africa At the

The First European Benefit Corporation: blurring the lines between social and business

The First European Benefit Corporation: blurring the lines between social and business Alissa Pelatan Roberto Randazzo A. Introduction In December 2015, the Italian parliament passed the Stability Act

The First European Benefit Corporation: blurring the lines between social and business Alissa Pelatan Roberto Randazzo A. Introduction In December 2015, the Italian parliament passed the Stability Act

Why Non-Profit Boards MUST Reduce Investment Costs and How They Can Do It

Why Non-Profit Boards MUST Reduce Investment Costs and How They Can Do It by Craig D. Price, CFP and Will Thompson, CFP, CFA Abstract: This white paper demonstrates the dramatic impact of investment fees

Why Non-Profit Boards MUST Reduce Investment Costs and How They Can Do It by Craig D. Price, CFP and Will Thompson, CFP, CFA Abstract: This white paper demonstrates the dramatic impact of investment fees

MPMA Sustainability Conference 2013

www.pwc.com MPMA Sustainability Conference 2013 Sustainability ratings: how transparency can drive performance 3 rd Sustainability is at the core of people, planet and profit dimensions The company s degree

www.pwc.com MPMA Sustainability Conference 2013 Sustainability ratings: how transparency can drive performance 3 rd Sustainability is at the core of people, planet and profit dimensions The company s degree

Walsh University Guide to Giving 3

Walsh University Guide to Giving Guide to Giving 3 Mission Statement M I S S ION S T A TE M ENT Walsh University is an independent, coeducational, Catholic, liberal arts and sciences institution. Founded

Walsh University Guide to Giving Guide to Giving 3 Mission Statement M I S S ION S T A TE M ENT Walsh University is an independent, coeducational, Catholic, liberal arts and sciences institution. Founded

Proposed Revision to the UK Stewardship Code Annex A - Revised UK Stewardship Code

Consultation Financial Reporting Council January 2019 Proposed Revision to the UK Stewardship Code Annex A - Revised UK Stewardship Code The FRC s mission is to promote transparency and integrity in business

Consultation Financial Reporting Council January 2019 Proposed Revision to the UK Stewardship Code Annex A - Revised UK Stewardship Code The FRC s mission is to promote transparency and integrity in business

Enter the Title of Your Presentation Here

THE OREGON COMMUNITY FOUNDATION Endowment Partners 101 Enter the Title of Your Presentation Here February 15, 2017 Agenda Community foundations The Endowment Partners Program Definition of endowment Investment

THE OREGON COMMUNITY FOUNDATION Endowment Partners 101 Enter the Title of Your Presentation Here February 15, 2017 Agenda Community foundations The Endowment Partners Program Definition of endowment Investment

IMPACT INVESTING MARKET MAP

IMPACT INVESTING MARKET MAP WHITE PAPER DOCUMENT FOR CONSULTATION An investor initiative in partnership with UNEP Finance Initiative and UN Global Compact WHITE PAPER - DOCUMENT FOR CONSULTATION FOREWORD

IMPACT INVESTING MARKET MAP WHITE PAPER DOCUMENT FOR CONSULTATION An investor initiative in partnership with UNEP Finance Initiative and UN Global Compact WHITE PAPER - DOCUMENT FOR CONSULTATION FOREWORD

GIFT ANNUITIES MADE EASY

GIFT ANNUITIES MADE EASY NO GREATER GIFT Provide for your future and the Earth s through a gift annuity I f you ve been looking for a way to deepen your support for Earthjustice, you might want to consider

GIFT ANNUITIES MADE EASY NO GREATER GIFT Provide for your future and the Earth s through a gift annuity I f you ve been looking for a way to deepen your support for Earthjustice, you might want to consider

Presentation to the Nonprofit Organizations Standing Committee of the State Bar of California Business Law Section September 14, 2017 ENDOWMENT LAW

Brigit Kavanagh Barbara Rhomberg 1025 Alameda De Las Pulgas, #123 Belmont, California 94002 (650) 394-6012 KRNONPROFITLAW. COM Presentation to the Nonprofit Organizations Standing Committee of the State

Brigit Kavanagh Barbara Rhomberg 1025 Alameda De Las Pulgas, #123 Belmont, California 94002 (650) 394-6012 KRNONPROFITLAW. COM Presentation to the Nonprofit Organizations Standing Committee of the State

Kelowna, British Columbia, Hones Its Financial Principles and Strategies

Kelowna, British Columbia, Hones Its Financial Principles and Strategies By Genelle Davidson Defining financial strength and stability enables a government to build its individual financial principles

Kelowna, British Columbia, Hones Its Financial Principles and Strategies By Genelle Davidson Defining financial strength and stability enables a government to build its individual financial principles

College and University Tax Update. EACUBO Conference May 30, 2014

College and University Tax Update EACUBO Conference May 30, 2014 Changes to the 2013 Form 990 Sixth year for the revised Form 990 No significant changes, mostly clarifications Ongoing interest in compensation

College and University Tax Update EACUBO Conference May 30, 2014 Changes to the 2013 Form 990 Sixth year for the revised Form 990 No significant changes, mostly clarifications Ongoing interest in compensation

Nonprofit Organizations

Attorneys in the Nonprofit Organizations Practice Area at Reid and Riege handle a wide variety of tax, corporate, fiduciary, endowment, financial, employment, insurance and regulatory issues for many types

Attorneys in the Nonprofit Organizations Practice Area at Reid and Riege handle a wide variety of tax, corporate, fiduciary, endowment, financial, employment, insurance and regulatory issues for many types

A Resource for Charitable Giving

A Resource for Charitable Giving Your clients care about giving. At the Community Foundation we help people contribute to their community during their lifetime, and through planned giving. Partnering with

A Resource for Charitable Giving Your clients care about giving. At the Community Foundation we help people contribute to their community during their lifetime, and through planned giving. Partnering with

Chapter 23: Non-profit institutions in the SNA... 2

Chapter 23: Non-profit institutions in the SNA... 2 A. Introduction... 2 1. Non profit institutions in the SNA... 2 2. A satellite account for NPIs... 3 B. The units included in the NPI satellite account...

Chapter 23: Non-profit institutions in the SNA... 2 A. Introduction... 2 1. Non profit institutions in the SNA... 2 2. A satellite account for NPIs... 3 B. The units included in the NPI satellite account...

Report of Independent Auditors and Financial Statements. Philanthropic Ventures Foundation

Report of Independent Auditors and Financial Statements Philanthropic Ventures Foundation December 31, 2017 and 2016 Table of Contents REPORT OF INDEPENDENT AUDITORS... 1 FINANCIAL STATEMENTS Statements

Report of Independent Auditors and Financial Statements Philanthropic Ventures Foundation December 31, 2017 and 2016 Table of Contents REPORT OF INDEPENDENT AUDITORS... 1 FINANCIAL STATEMENTS Statements

Tax Reform Legislation: Changes, Impacts, Planning Considerations

The following information and opinions are provided courtesy of Wells Fargo Bank N.A. Wealth Planning Update Tax Reform Legislation:, s, JANUARY 2018 Jay Messing, CFA, CFP Sr. Director of Planning Wells

The following information and opinions are provided courtesy of Wells Fargo Bank N.A. Wealth Planning Update Tax Reform Legislation:, s, JANUARY 2018 Jay Messing, CFA, CFP Sr. Director of Planning Wells

PERMISSIVE TAX EXEMPTION POLICY

PERMISSIVE TAX EXEMPTION POLICY BOWEN ISLAND MUNICIPALITY MISSION STATEMENT In carrying out its mandate, Bowen Island Municipality will work towards conducting operations in a way that: 1. Improves the

PERMISSIVE TAX EXEMPTION POLICY BOWEN ISLAND MUNICIPALITY MISSION STATEMENT In carrying out its mandate, Bowen Island Municipality will work towards conducting operations in a way that: 1. Improves the

Table of Contents I. Key points... 1 II. Key quotes... 3 III. Definitions... 4 IV. Best practices... 5

FRESHFIELDS BRUCKHAUS DERINGER, 2005. A legal framework for the integration of the environmental, social and governance issues into institutional investment. UKSIF summary, 2009. Table of Contents I. Key

FRESHFIELDS BRUCKHAUS DERINGER, 2005. A legal framework for the integration of the environmental, social and governance issues into institutional investment. UKSIF summary, 2009. Table of Contents I. Key

Report of Independent Auditors and Consolidated Financial Statements. Silicon Valley Community Foundation

Report of Independent Auditors and Consolidated Financial Statements Silicon Valley Community Foundation December 31, 2015 and 2014 CONTENTS PAGE REPORT OF INDEPENDENT AUDITORS...1 CONSOLIDATED FINANCIAL

Report of Independent Auditors and Consolidated Financial Statements Silicon Valley Community Foundation December 31, 2015 and 2014 CONTENTS PAGE REPORT OF INDEPENDENT AUDITORS...1 CONSOLIDATED FINANCIAL

1 Purpose and objectives of the policy

Date of this Policy: 27 March 2018 The information in this document forms part of the following Product Disclosure Statements: Cbus Industry Super Product Disclosure Cbus Sole Trader Product Disclosure

Date of this Policy: 27 March 2018 The information in this document forms part of the following Product Disclosure Statements: Cbus Industry Super Product Disclosure Cbus Sole Trader Product Disclosure

Wealth structuring and estate planning. Your vision and your legacy. Life s better when we re connected

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth structuring and estate planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Introduction. The Assessment consists of: A checklist of best, good and leading practices A rating system to rank your company s current practices.

ESG / CSR / Sustainability Governance and Management Assessment By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com September 2017 Introduction This ESG / CSR / Sustainability Governance

ESG / CSR / Sustainability Governance and Management Assessment By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com September 2017 Introduction This ESG / CSR / Sustainability Governance

Stewardship Principles for Institutional Investors Draft for Public Comment

Stewardship Principles for Institutional Investors Draft for Public Comment I. Preamble To enhance corporate governance of listed companies in Taiwan, facilitate sound development of companies and protect

Stewardship Principles for Institutional Investors Draft for Public Comment I. Preamble To enhance corporate governance of listed companies in Taiwan, facilitate sound development of companies and protect

2011 Charitable Giving Review

TAX-EXEMPT ORGANIZATIONS edwardswildman.com taxexempt.edwardswildman.com 2011 Charitable Giving Review With the end of the year approaching rapidly, we would like to take this opportunity to provide you

TAX-EXEMPT ORGANIZATIONS edwardswildman.com taxexempt.edwardswildman.com 2011 Charitable Giving Review With the end of the year approaching rapidly, we would like to take this opportunity to provide you

TRUST FUND BOARD POLICY

TRUST FUND BOARD POLICY Policy number: 3.3 Title: Relationships with External Groups Policy Approved By: Trust Fund Board Date: May 13, 2003 Resolution #: TFB 03/575 Revised Date: Sep. 28, 2015 Resolution

TRUST FUND BOARD POLICY Policy number: 3.3 Title: Relationships with External Groups Policy Approved By: Trust Fund Board Date: May 13, 2003 Resolution #: TFB 03/575 Revised Date: Sep. 28, 2015 Resolution

Adopted May 12, Statement of Investment Objectives And Principles

Statement of Investment Objectives And Principles Approved by City Council May 12, 2010 1 Statement of Investment Objectives and Principles SECTION 1: MANDATE 1.1 The Toronto Atmospheric Fund ( TAF ) is

Statement of Investment Objectives And Principles Approved by City Council May 12, 2010 1 Statement of Investment Objectives and Principles SECTION 1: MANDATE 1.1 The Toronto Atmospheric Fund ( TAF ) is

Home Address City State Zip Code. Business Address City State Zip Code. Home Address City State Zip Code. Business Address City State Zip Code

THIS AGREEMENT is entered into this day of, 20, by the Greater Manhattan Community Foundation ( GMCF ), a Kansas not-for-profit charitable corporation, and. DONOR ADVISOR INFORMATION Donor Advisor 1 (all

THIS AGREEMENT is entered into this day of, 20, by the Greater Manhattan Community Foundation ( GMCF ), a Kansas not-for-profit charitable corporation, and. DONOR ADVISOR INFORMATION Donor Advisor 1 (all

PLANNED GIVING GUIDE

PLANNED GIVING GUIDE You can Create your Own Legacy Making a difference is important to you. Charitable giving is an important part of your life and your core values. Like many people, you d like to know

PLANNED GIVING GUIDE You can Create your Own Legacy Making a difference is important to you. Charitable giving is an important part of your life and your core values. Like many people, you d like to know

IMPACT INVESTING AND DONOR-ADVISED FUNDS Extending Your Philanthropic Dollars

IMPACT INVESTING AND DONOR-ADVISED FUNDS Extending Your Philanthropic Dollars RBC GAM Fundamental Series Impact Investing and Donor-Advised Funds: Extending Your Philanthropic Dollars 1 Executive Summary

IMPACT INVESTING AND DONOR-ADVISED FUNDS Extending Your Philanthropic Dollars RBC GAM Fundamental Series Impact Investing and Donor-Advised Funds: Extending Your Philanthropic Dollars 1 Executive Summary

MEMBERSHIP DEFINITION AND DUES STRUCTURE PROPOSED CHANGES TO THE CONSTITUTION SOCIETY COUNCIL NOVMBER 12 & 13, 2017

CONSTITUTION 1 art 2.1 2.1 A Member is an employee of an granted bargaining rights or for which The Society is seeking such rights and who is eligible to be represented by The Society, subject to the qualifications

CONSTITUTION 1 art 2.1 2.1 A Member is an employee of an granted bargaining rights or for which The Society is seeking such rights and who is eligible to be represented by The Society, subject to the qualifications

THE NEW CONSERVATION TAX INCENTIVES. Stephen J. Small, Esq. (10/14/08)

") THE NEW CONSERVATION TAX INCENTIVES By Stephen J. Small, Esq. (10/14/08) On August 17, 2006, the President signed into law the Pension Protection Act of 2006. That law included the first major new income

THE NEW CONSERVATION TAX INCENTIVES By Stephen J. Small, Esq. (10/14/08) On August 17, 2006, the President signed into law the Pension Protection Act of 2006. That law included the first major new income

NCR FORMS STRATEGIC PARTNERSHIP WITH BLACKSTONE. November 12, 2015

NCR FORMS STRATEGIC PARTNERSHIP WITH BLACKSTONE November 12, 2015 FORWARD-LOOKING STATEMENTS Comments made during this conference call and in these materials contain forward-looking statements. Forward-looking

NCR FORMS STRATEGIC PARTNERSHIP WITH BLACKSTONE November 12, 2015 FORWARD-LOOKING STATEMENTS Comments made during this conference call and in these materials contain forward-looking statements. Forward-looking

eastsussex.gov.uk UK Stewardship Code Statement

eastsussex.gov.uk UK Stewardship Code Statement November 2018 Introduction The East Sussex Pension Fund (the Fund) recognises that Environmental, Social and Corporate Governance ( ESG ) issues can have

eastsussex.gov.uk UK Stewardship Code Statement November 2018 Introduction The East Sussex Pension Fund (the Fund) recognises that Environmental, Social and Corporate Governance ( ESG ) issues can have

Current as of July 2018 Comments related to any information in this Note should be addressed to Lily Liu.

ROMANIA Current as of July 2018 Comments related to any information in this Note should be addressed to Lily Liu. TABLE OF CONTENTS I. Summary II. III. IV. A. Types of Organizations B. Tax Laws Applicable

ROMANIA Current as of July 2018 Comments related to any information in this Note should be addressed to Lily Liu. TABLE OF CONTENTS I. Summary II. III. IV. A. Types of Organizations B. Tax Laws Applicable

INCOME Data Dictionary

INCOME 4-0000 MYOB 4-0000 Income For the purposes of this Chart of s, Income is also referred to as Revenue. Revenues are inflows or other enhancements of assets or decreases of liabilities that result

INCOME 4-0000 MYOB 4-0000 Income For the purposes of this Chart of s, Income is also referred to as Revenue. Revenues are inflows or other enhancements of assets or decreases of liabilities that result