Extenders/tax reform/legislative outlook

|

|

|

- Stella Lester

- 5 years ago

- Views:

Transcription

1

2 Agenda > Extenders/tax reform/legislative outlook > Repair and maintenance opportunities > Year-end tax planning strategies > Affordable Care Act update > State and local tax update 2

3 Extenders/tax reform/legislative outlook

4 Lame duck Congress: What will happen with extender provisions? > Research and New Markets tax credits > 15 SL for qualified leasehold improvements > 50 percent bonus depreciation > Increased section 179 ($500,000) > Reduced BIG recognition period for S corporations > Numerous other provisions 4

5 House proposals > House wants some business incentives made permanent > Look at others on a case-by-case basis > House passed on Dec. 3, 2014, a one-year extension basically retroactive to Jan. 1, 2014, and will further address next year 5

6 Senate proposals > Senate wants two-year, across-the-board extension of the expiring provisions > Work on tax reform during the two-year period > Appears the Senate will accept the House bill 6

7 White House position > No permanent extension of business provisions without permanent extension of middle-class provisions > Have not detailed middle-class provisions > Likely to include: Child care tax credit Earned income and higher education credit May seek to revive low income housing credit 7

8 What to expect? > R&D credit made permanent > Either increased section 179 expensing or 50 percent bonus depreciation made permanent > One- or two-year extension on most extenders > Child tax credit and earned income credit made permanent in exchange for above > Any similarity between the above and actual legislation is purely coincidental 8

9 Prospects for tax reform? > Rate increases off the table > Close loopholes > Carried interests > Professional service firms to accrual method ($10 million of gross receipts) > LIFO repeal > Repeal of IRC 199 > Restrict or eliminate IRC 1031, like-kind exchanges 9

10 Repair and maintenance opportunities

11 Repair and maintenance (R&M) opportunities > De minimis safe harbor > Routine maintenance safe harbor for buildings > Method changes cap to repair and repair to cap > Election to capitalize repair costs > Dispositions > Late partial disposition election 11

12 De minimis safe harbor > Taxpayers may rely on this safe harbor to expense tangible property under a certain dollar threshold > A written accounting procedure must be in place at the beginning of the taxable year: For taxpayers with an applicable financial statement, the dollar amount is not to exceed $5,000 per item For taxpayers without an applicable financial statement, the dollar amount is not to exceed $500 per item > The safe harbor is elected annually by including a statement on a timely filed original federal return (including extensions) > The election may not be revoked and may not be made by filing an application for change in accounting method 12

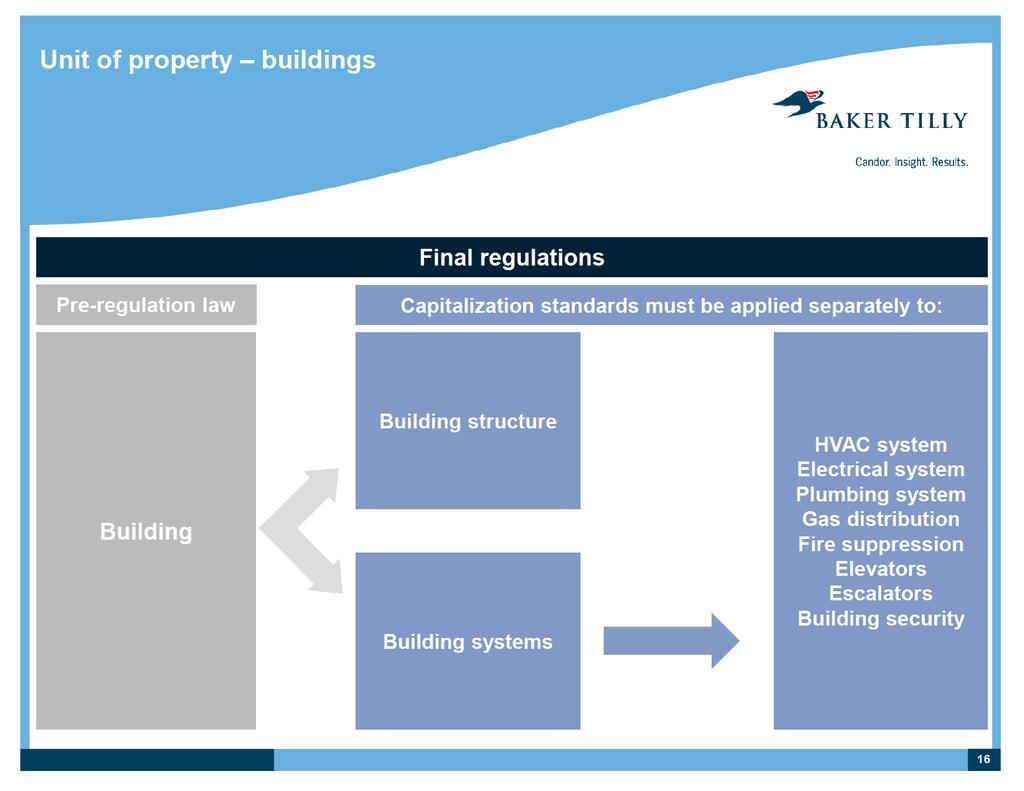

13 Routine maintenance safe harbor for buildings > Recurring activities that a taxpayer expects to perform as a result of the taxpayer s use of the building to keep the building structure or system in its ordinarily efficient operating condition > The taxpayer must reasonably expect to perform the activities more than once during a 10-year period beginning at the time the building structure or building system is placed in service > Amounts incurred for activities that do not meet the safe harbor are subject to analysis under the general rules for improvements > Cannot start to use prospectively must analyze overall repairs vs. capitalization method first! 13

14 Method changes cap to repair > This automatic method change covers potentially deductible R&M costs that are currently capitalized and being depreciated > Key questions Did you file a cap to repair 3115 in a prior year? o If yes, is the method consistent with the final regs? What is the magnitude of the capitalized R&M costs? Do you want/need deductions in 2014? 14

15 Method changes repair to cap > This automatic method change covers expenditures that must be capitalized under the final regs, but were deducted in prior years > Key questions What kind of items have been deducted as R&M expenses over the past 3 to 5 years? Did you treat an entire building as the unit of property for purposes of the cap vs. repair analysis? 15

16

17

18 Election to capitalize repair costs > Taxpayers may elect to treat amounts paid during the taxable year for R&M as amounts paid to improve tangible property, if the costs are incurred in the taxpayer s trade or business and if the costs are treated as capital expenditures on the taxpayer s books > The election applies to all amounts paid for R&M on tangible property in that taxable year > This annual, irrevocable election is made by attaching a statement to a timely filed original federal tax return (including extensions) for the taxable year in which the taxpayer pays these amounts 18

19 Dispositions > Taxpayers may take a loss on the disposition of a structural component of a building, or a portion of a structural component of a building, recognized in the tax year of the disposition > Also, taxpayers may forgo a loss on the disposition of a structural component of a building or a portion of a structural component of a building > The partial disposition election is made by claiming the gain or loss on a timely filed original tax return for the year in which the portion of an asset is disposed 19

20 Late partial disposition election > The late partial disposition election will be treated as an automatic change in method of accounting for a limited period of time > The change must be made for any taxable year beginning on or after Jan. 2, 2012, and beginning before Jan. 1, 2015 > In other words, 2014 is the last opportunity to go back and immediately deduct the remaining cost of ghost assets 20

21 Year-end tax planning strategies

22 Effective use of tax brackets and rates > Timing of income and deductions: Accelerate deductions into years where your tax bracket may be higher, and Defer income into years where your tax bracket is lower Consider deferring deductions affected by the alternative minimum tax (AMT) if you are currently subject to AMT, but may not be next year > Consider selling capital gain property on an installment basis: If taxable income is below $400,000 (single) or $450,000 (married filing jointly), then capital gains rates will be 15 percent If taxable income is above that, capital gains rates go up to 20 percent 22

23 Effective use of losses > Net operating losses (NOLs) can either be carried back to offset income from prior years or forward to offset future income If taxable income in prior years was low, or income was taxed at more favorable rates, it may be beneficial to elect to use the NOLs in future years instead If you expect an NOL in the current year that you would like to carry back, try to file your return as soon as possible; corporations can try filing for a quick refund > Capital losses are most beneficial when they can be used to offset capital gains Stocks with large unrealized losses can be sold and used to offset stock with large capital gains 23

24 Effective use of losses (cont.) > A few useful items to consider when you expect losses from a pass-through entity: Losses can only be used to the extent of basis An S corporation owner can increase basis with a properly documented shareholder loan > Passive activity losses are limited to passive income If you expect passive losses, see if you can increase your involvement in the activity enough to be considered materially participating Material participation may allow you to deduct losses 24

25 Charitable donations of property > If you have appreciated property, consider donating it to a charitable organization rather than selling it You will generally receive the deduction based on the fair market value of the property But since the property was donated, you won t have to pay taxes on the appreciated value 25

26 Accelerating business deductions > If you expect higher taxable income, consider trying to accelerate any business deductions Some expiring tax provisions may be extended, like bonus depreciation, so you could consider accelerating fixed asset purchases 26

27 Affordable Care Act update

28 Reimbursement arrangements > Employer reimbursement of premiums Employee purchased individual health coverage Updated guidance from the Department of Labor, Department of Health and Human Services, Department of the Treasury No longer permitted on pre-tax or post-tax basis 28

29 Reimbursement arrangements Example #1 > Facts S corporation with one shareholder Health insurance policy in company name; covers only the shareholder There are other employees in the entity > Questions Is the employer subject to the penalty? Will a group policy cure the issue? How are reimbursed premiums handled for tax purposes? 29

30 Reimbursement arrangements Example #2 > Facts University has union workers; new contract negotiations underway Health premiums paid by university and subtracted from wages on pre-tax basis Union wants to insure workers on union plan but deduct payment made to union to cover health insurance on pre-tax basis > Question Is payment of union dues a pre-tax payment? 30

31

32 Reporting ACA compliance > New required forms: Form 1095-B, Health Coverage Form 1095-C, Employer Provided Health Insurance Offer and Coverage Form 1094-B, Transmittal of Health Coverage Information Returns Form 1094-C, Transmittal of Employer-Provided Health Insurance and Coverage Information Returns Form 8941, Credit for Small Employer Health Insurance Premiums 32

33

34 Reporting ACA compliance > Form 1094-B, Transmittal of Health Coverage Information Returns Report total Forms 1095-B filed > Form 1094-C, Transmittal of Employer-Provided Health Insurance Offer and Coverage Information Return Report total Forms 1095-C filed Filed by applicable large employers (ALEs) Contains four parts: 1. ALE member information 2. Certifications of eligibility 3. Monthly information 4. Aggregated ALE group members 34

35 Employer reporting requirements > Deadlines: Returns due Feb. 28 (March 31 if filed electronically) o First return due Monday, March 1, 2016 Employee statements due Jan. 31 o First statements due Monday, Feb. 1, 2016 Electronic furnishing rules similar to W-2 35

36 Reporting ACA compliance > Potential issues Electronic reporting to employees Data collection o o Union-covered employees Social Security numbers 36

37 IRS enforcement > Full coverage box line 61 of Form 1040 > Form 8965, Health Coverage Exemptions > The H notices CP 15H, Shared Responsibility Payment Civil Penalties Notice CP 21H/22H, Shared Responsibility Payment Adjustment Notice 37

38 State and local tax update

39 Key topics > State and local tax arena in 2014 > Income and franchise taxes > Pass-through entities > Sales and use taxes > Other state and local tax developments 39

40 The state and local tax arena in 2014 > FY 2015 state fiscal conditions have improved with the economic rebound but caution flags are popping up > Total general fund revenue is expected to rise by $23.6 billion to $749.2 billion, a 3.25 percent increase > Adjusted for inflation, total state revenue is still projected to be below the 2008 level > Fifteen states are considering or have enacted tax cuts estimated at $2.5 billion, e.g., New York > State budget reserves are falling and are expected to be more than $18 billion below the FY 2013 level, a decline of nearly 25 percent 40

41 The state and local tax arena in 2014 > The quest for new tax revenues continues in some states with proposed increases in states like Illinois > The battle between businesses and state and local tax officials over nexus is still intense > US-foreign tax minimization (base erosion and profit sharing (BEPS)) by multinational companies has caught attention of state revenue agencies > Federal legislation to allow states to collect sales tax on Internet sales (Marketplace Fairness Act (MFA)) stalled again > Pass-through entities: increasingly popular but facing complex state tax requirements > State revenue agencies pouring more money into anti-fraud and enforcement efforts 41

42 Income and franchise taxes > States continue to pursue aggressive nexus and apportionment policies > Recent study indicates that 39 states have adopted an economic presence test for income/franchise tax purposes, i.e., physical presence is unnecessary to impose tax > Bright-line or factor presence tests California, Colorado, Connecticut, and others > Mandatory combined reporting is spreading New York, Rhode Island 42

43 Income and franchise taxes > Anti-BEPS at state level? Multistate Tax Commission hearings on transfer pricing New Jersey proposal targets companies that have executed an inversion Companies fight improper use of transfer pricing (Chainbridge appeals) > Apportionment: Multistate Tax Compact (MTC) three-factor refund claims and litigation Taxpayer win in Michigan (IBM decision) but the state attempts to claw back the benefits with retroactive MTC repeal > Software providers and cloud computing sales factor issues (Illinois Department of Revenue rules SaaS is a service, not prewritten software) 43

44 Income and franchise taxes > Services and intangibles: Continued movement to market sourcing for sales factor from cost of performance Market sourcing looks to where customers receive the benefit of the service vs. where work is done Nineteen states have adopted market sourcing MTC endorsement of market sourcing with three-factor, double-weighted sales apportionment Market sourcing guidelines are vague and difficult to apply in practice; audit experience is limited o o Massachusetts issued new rules for market sourcing Customer headquarters, billing address, vendor work site? 44

45 Pass-through entities > Pass-through entities: S corporations, limited liability companies, limited liability partnerships, and limited partnerships > Nexus: ownership creates nexus in most states > Pass-through entity-level taxes: Illinois, New Hampshire, Tennessee, Texas, Washington DC, and other states > Allocation and apportionment: factor flow-through? > Composite returns: elective or mandatory? Illinois eliminated composite return in 2014 > Withholding requirements in more than 30 states Stiff penalties for noncompliance even when nonresident owners file state individual income tax returns 45

46 Sales and use taxes > States continue to focus on Internet, catalog, and other remote sellers. Estimated potential sales tax revenue: $25 billion to $35 billion? State attack turned away again as MFA remains in House Judiciary Committee as Congress ends session > Click-through nexus: Sixteen states have adopted in some form; New Jersey is the latest Illinois reenacted statute to tax remote sellers after losing a state supreme court decision > Out-of-state seller notification requirements: Colorado case before the US Supreme Court (DMA v. Brohl) 46

47 Sales and use taxes > Issues and concerns over current proposals to tax remote sellers: Hodgepodge of nexus rules is not addressed or limited, e.g., affiliate, click-through, agency Continued lack of uniformity among states and localities in taxability of goods and services Compliance costs imposed on businesses will be high, even with safe harbor for small sellers Software is not a panacea Tax increase for consumers? What about uniformity for other taxes, e.g., income and franchise taxes? 47

48 Sales and use taxes > Cloud computing Continuing uncertainty as to the sales and use tax status of cloud computing Michigan courts hold that cloud computing for electronic information access is a nontaxable service, not prewritten software Taxable canned software in some states, e.g., New York Taxable telecommunications service in others, e.g., South Carolina Are all forms of cloud services treated the same, e.g., SaaS, IaaS, and PaaS? 48

49 Other state tax developments > Taxation and regulation of e-cigarettes > Qui tam (whistleblower) tax actions > State tax agencies beefing up efforts to combat identity theft, false refund claims, and other underreporting Investing in big data and technology to mine deeper into data from IRS, e.g., 1099s, other states, and own electronic data sources > Unclaimed property growing awareness on part of state that it is potentially a major revenue source Noncompliance can lead to material exposure Unlimited look-back period with interest and penalties Use of bounty hunters by state to audit and identify nonfilers Aggressive reporting rules, e.g., Delaware 49

50 SALT planning for 2014 year-end > Nexus review and planning > Examine international activities for potential state tax issues > ASC 740/FAS 109 and ASC 450 issues and opportunities, e.g., voluntary disclosure agreements, due diligence > Analyze apportionment and combined reporting positions (MTC refund claims?) > Sales tax: planning for MFA, click-through, or affiliate nexus > Consumer use tax compliance: procedures review > PTE withholding changes or waivers > Personal income tax and planning for change of residence 50

51 Disclosure The content in this presentation is a resource for Baker Tilly Virchow Krause, LLP clients and prospective clients. The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity. In specific circumstances, the services of a professional should be sought. Tax information, if any, contained in this communication was not intended or written to be used by any person for the purpose of avoiding penalties, nor should such information be construed as an opinion upon which any person may rely. The intended recipients of this communication and any attachments are not subject to any limitation on the disclosure of the tax treatment or tax structure of any transaction or matter that is the subject of this communication and any attachments.

2017 Year-End State and Local Tax Update Jason Sneeringer, CPA Tax Manager

2017 Year-End State and Local Tax Update Jason Sneeringer, CPA Tax Manager Agenda Current state and local tax (SALT) atmosphere Nexus Sales & use tax Unclaimed property Property tax Income & Franchise

2017 Year-End State and Local Tax Update Jason Sneeringer, CPA Tax Manager Agenda Current state and local tax (SALT) atmosphere Nexus Sales & use tax Unclaimed property Property tax Income & Franchise

Estimated Impact of the TCJA. November 19, 2018

Estimated Impact of the TCJA November 19, 2018 Importance of Tax Conformity Tax Conformity Why We Conform to the Internal Revenue Code ( IRC ) Virginia tax returns start with federal determination of income

Estimated Impact of the TCJA November 19, 2018 Importance of Tax Conformity Tax Conformity Why We Conform to the Internal Revenue Code ( IRC ) Virginia tax returns start with federal determination of income

Compliance and reporting: recent developments and issues. 1 May 2013

Compliance and reporting: recent developments and issues 1 May 2013 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate

Compliance and reporting: recent developments and issues 1 May 2013 Disclaimer Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate

Publication 9, Construction and Building Contractors, California State Board of Equalization, December 2015

January 2016 California Construction and Building Contractors Tax Guidance Issued The California State Board of Equalization has updated its publication on the sales and use tax treatment and responsibilities

January 2016 California Construction and Building Contractors Tax Guidance Issued The California State Board of Equalization has updated its publication on the sales and use tax treatment and responsibilities

What is State Tax Nexus and How Does the Supreme Court s Wayfair Decision Change Things?

What is State Tax Nexus and How Does the Supreme Court s Wayfair Decision Change Things? The material appearing in this presentation is for informational purposes only and should not be construed as advice

What is State Tax Nexus and How Does the Supreme Court s Wayfair Decision Change Things? The material appearing in this presentation is for informational purposes only and should not be construed as advice

STATE APPORTIONMENT UPDATE

STATE APPORTIONMENT UPDATE Sourcing of Services and Market-based Souring Laura Holmes Senior Director BDO USA February 16, 2016 TEI Houston Chapter Tax School Laura Holmes, CPA State and Local Tax Senior

STATE APPORTIONMENT UPDATE Sourcing of Services and Market-based Souring Laura Holmes Senior Director BDO USA February 16, 2016 TEI Houston Chapter Tax School Laura Holmes, CPA State and Local Tax Senior

Agenda. Income/franchise tax. Nexus Sourcing of Revenue for Services Uniformity and Simplicity Intercompany Transactions Update. Salt Lunch and Learn

Income/franchise tax Salt Lunch and Learn Agenda Nexus Sourcing of Revenue for Services Uniformity and Simplicity Intercompany Transactions Update Texas Louisiana 2 1 Multistate -Nexus Nexus Taxpayer s

Income/franchise tax Salt Lunch and Learn Agenda Nexus Sourcing of Revenue for Services Uniformity and Simplicity Intercompany Transactions Update Texas Louisiana 2 1 Multistate -Nexus Nexus Taxpayer s

California and Multistate

Chapter 7 California and Multistate 1 Topics California Income and Franchise Taxes Sales and Use Taxes Property Taxes Miscellaneous Multistate 2 Contacting FTB FTB Pub 1240 https://www.ftb.ca.gov/forms/misc/1240.pdf

Chapter 7 California and Multistate 1 Topics California Income and Franchise Taxes Sales and Use Taxes Property Taxes Miscellaneous Multistate 2 Contacting FTB FTB Pub 1240 https://www.ftb.ca.gov/forms/misc/1240.pdf

Wayfair The Impact on Manufacturers November 7, 2018

Wayfair The Impact on Manufacturers November 7, 2018 1 Welcome Georgia Association of Manufacturers! 2 Presenters Peter Giroux, SALT Partner Dixon Hughes Goodman LLP Atlanta peter.giroux@dhg.com 404.575.8924

Wayfair The Impact on Manufacturers November 7, 2018 1 Welcome Georgia Association of Manufacturers! 2 Presenters Peter Giroux, SALT Partner Dixon Hughes Goodman LLP Atlanta peter.giroux@dhg.com 404.575.8924

Multistate Income Tax

Multistate Income Tax Marion Kopin, CPA Kopin & Company, CPA, PC mkopin@kopincpa.com Multistate Income Taxation Overview Forty-seven states and the District of Columbia impose some type of income or franchise

Multistate Income Tax Marion Kopin, CPA Kopin & Company, CPA, PC mkopin@kopincpa.com Multistate Income Taxation Overview Forty-seven states and the District of Columbia impose some type of income or franchise

Trump Tax Plan: Impact and Strategy

Trump Tax Plan: Impact and Strategy The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication of this information is not intended

Trump Tax Plan: Impact and Strategy The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication of this information is not intended

SOUTH DAKOTA V. WAYFAIR

A CLOSER LOOK: STATE TAX & PRACTICAL IMPLICATIONS OF THE US SUPREME COURT S DECISION IN SOUTH DAKOTA V. WAYFAIR Part II: Practical Implications for Retailers June 28, 2018 Presenters: Adam Beckerink (Chicago)

A CLOSER LOOK: STATE TAX & PRACTICAL IMPLICATIONS OF THE US SUPREME COURT S DECISION IN SOUTH DAKOTA V. WAYFAIR Part II: Practical Implications for Retailers June 28, 2018 Presenters: Adam Beckerink (Chicago)

Caveat venditor: The implications of Wayfair for US inbounds

Caveat venditor: The implications of Wayfair for US inbounds Tuesday, November 13, 2018 10:00-11:00 am ET We will be starting soon Please disable pop-up blocking software before viewing this webcast CPE

Caveat venditor: The implications of Wayfair for US inbounds Tuesday, November 13, 2018 10:00-11:00 am ET We will be starting soon Please disable pop-up blocking software before viewing this webcast CPE

Colorado Out of State Retailers Must Begin Collecting Sales Tax Soon

September 2018 Colorado Out of State Retailers Must Begin Collecting Sales Tax Soon Out of state retailers must collect sales tax if they meet Colorado s economic nexus requirements. Collection requirements

September 2018 Colorado Out of State Retailers Must Begin Collecting Sales Tax Soon Out of state retailers must collect sales tax if they meet Colorado s economic nexus requirements. Collection requirements

Latest Developments in State and Local Tax Due Diligence for Private Equity

Latest Developments in State and Local Tax Due Diligence for Private Equity Andrew Finkle, CPA, JD, LL.M. Daniel Kidney, CPA, JD Rance Morton, CPA Investment advisory services are offered through CliftonLarsonAllen

Latest Developments in State and Local Tax Due Diligence for Private Equity Andrew Finkle, CPA, JD, LL.M. Daniel Kidney, CPA, JD Rance Morton, CPA Investment advisory services are offered through CliftonLarsonAllen

How Does Federal Law Treat GILTI?

August 2018 Connecticut Connecticut Issues GILTI Guidance Connecticut issued guidance on the treatment of global intangible low taxed income (GILTI). The guidance applies to corporate business taxpayers

August 2018 Connecticut Connecticut Issues GILTI Guidance Connecticut issued guidance on the treatment of global intangible low taxed income (GILTI). The guidance applies to corporate business taxpayers

The 2018 National Multistate Tax Symposium Take the lead Tax reform and fortifying state positions. February 7-9, 2018

The 2018 National Multistate Tax Symposium Take the lead Tax reform and fortifying state positions February 7-9, 2018 State tax twists and turns: What s happened that surprised us Valerie Dickerson, Deloitte

The 2018 National Multistate Tax Symposium Take the lead Tax reform and fortifying state positions February 7-9, 2018 State tax twists and turns: What s happened that surprised us Valerie Dickerson, Deloitte

NEW YORK STATE BAR ASSOCIATION TAX SECTION. Annual Meeting. State and Local Tax Implications of Federal Tax Reform.

NEW YORK STATE BAR ASSOCIATION TAX SECTION Annual Meeting State and Local Tax Implications of Federal Tax Reform January 23, 2018 Chair: Irwin M. Slomka, Morrison & Foerster LLP, New York City Joshua E.

NEW YORK STATE BAR ASSOCIATION TAX SECTION Annual Meeting State and Local Tax Implications of Federal Tax Reform January 23, 2018 Chair: Irwin M. Slomka, Morrison & Foerster LLP, New York City Joshua E.

Federal Tax Reform Idaho Impact

Federal Tax Reform Idaho Impact The potential effect of federal tax reform for Idaho On December 22, 2017, the President signed into law the Tax Cuts and Jobs Act. This legislation includes provisions

Federal Tax Reform Idaho Impact The potential effect of federal tax reform for Idaho On December 22, 2017, the President signed into law the Tax Cuts and Jobs Act. This legislation includes provisions

DUE DILIGENCE GUIDE (SAMPLE) COMPANY XYZ, INC. FOR THE YEARS ENDED DECEMBER 31, -

COMPANY XYZ, INC. FOR THE YEARS ENDED DECEMBER 31, -") DUE DILIGENCE GUIDE (SAMPLE) COMPANY XYZ, INC. FOR THE YEARS ENDED DECEMBER 31, - I. BUSINESS OVERVIEW II. III. A. Obtain business background (possible sources) 1. SEC Filings a) 10K Filings b) 10Q Filings

DUE DILIGENCE GUIDE (SAMPLE) COMPANY XYZ, INC. FOR THE YEARS ENDED DECEMBER 31, - I. BUSINESS OVERVIEW II. III. A. Obtain business background (possible sources) 1. SEC Filings a) 10K Filings b) 10Q Filings

Top Questions About the New Tax Law

Top Questions About the New Tax Law The American workforce is stressed out and finances play a major role. Many workers say they re living paycheckto-paycheck, and the routine is stressing them out so

Top Questions About the New Tax Law The American workforce is stressed out and finances play a major role. Many workers say they re living paycheckto-paycheck, and the routine is stressing them out so

Staff Presentation to the House Finance Committee June 1, 2017

Staff Presentation to the House Finance Committee June 1, 2017 1 Article 9 Remote Sellers Governor s original article with subsequent amendments heard 3/22 Re-write submitted 5/25 Tonight s presentation

Staff Presentation to the House Finance Committee June 1, 2017 1 Article 9 Remote Sellers Governor s original article with subsequent amendments heard 3/22 Re-write submitted 5/25 Tonight s presentation

SALES TAX AND WAYFAIR -

SALES TAX AND WAYFAIR - WHAT DOES IT MEAN FOR YOUR BUSINESS? by Karen Poist, CPA On June 21, 2018, the Supreme Court issued its decision on the South Dakota v. Wayfair, Inc. case (Wayfair). This is the

SALES TAX AND WAYFAIR - WHAT DOES IT MEAN FOR YOUR BUSINESS? by Karen Poist, CPA On June 21, 2018, the Supreme Court issued its decision on the South Dakota v. Wayfair, Inc. case (Wayfair). This is the

Tax Guide For Minnesota Businesses

Tax Guide For Minnesota Businesses 2017-2018 TAX GUIDE FOR MINNESOTA BUSINESSES Olsen Thielen & Co., Ltd. Certified Public Accountants & Consultants 2675 Long Lake Road 300 Prairie Center Drive #300 Roseville,

Tax Guide For Minnesota Businesses 2017-2018 TAX GUIDE FOR MINNESOTA BUSINESSES Olsen Thielen & Co., Ltd. Certified Public Accountants & Consultants 2675 Long Lake Road 300 Prairie Center Drive #300 Roseville,

State responses to tax reform

State responses to tax reform Federal tax reform- an overview H.R. 1 signed into law December 22, 2017 Included elements of the House and Senate versions of the bills - Not many surprises in conference

State responses to tax reform Federal tax reform- an overview H.R. 1 signed into law December 22, 2017 Included elements of the House and Senate versions of the bills - Not many surprises in conference

2013 NEW DEVELOPMENTS LETTER

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

Event title or other. listed gets listed here.

Event title or other Wayfair and Beyond listed gets listed here. Lindsay Galvin lindsay.j.galvin@pwc.com Good morning! Lindsay Galvin, State and Local Tax Director Phone: 412 315 9740 Email: lindsay.j.galvin@pwc.com

Event title or other Wayfair and Beyond listed gets listed here. Lindsay Galvin lindsay.j.galvin@pwc.com Good morning! Lindsay Galvin, State and Local Tax Director Phone: 412 315 9740 Email: lindsay.j.galvin@pwc.com

STATE & LOCAL TAX NEXUS: WHEN HAVE YOU CROSSED THE LINE?

STATE & LOCAL TAX NEXUS: WHEN HAVE YOU CROSSED THE LINE? Mary Reiser, CPA SALT Services Senior Managing Consultant mreiser@bkd.com Jana Gradeva, CMI SALT Services Senior Managing Consultant jgradeva@bkd.com

STATE & LOCAL TAX NEXUS: WHEN HAVE YOU CROSSED THE LINE? Mary Reiser, CPA SALT Services Senior Managing Consultant mreiser@bkd.com Jana Gradeva, CMI SALT Services Senior Managing Consultant jgradeva@bkd.com

Kathryn M. Jaques Summer Tax Institute June 2017

Kathryn M. Jaques Summer Tax Institute June 2017 } General partnership } Limited partnership } Limited liability partnership (LLP) } Limited liability company (LLC) Multiple member LLC Single member LLC

Kathryn M. Jaques Summer Tax Institute June 2017 } General partnership } Limited partnership } Limited liability partnership (LLP) } Limited liability company (LLC) Multiple member LLC Single member LLC

HLB State Tax Update Mike Herold, JD Regional Director - State and Local Tax Services

HLB State Tax Update Mike Herold, JD Regional Director - State and Local Tax Services mherold@eidebailly.com 612.253.6671 Overview State Nexus Expansion Efforts Major Audit Issues Apportionment Best Practices

HLB State Tax Update Mike Herold, JD Regional Director - State and Local Tax Services mherold@eidebailly.com 612.253.6671 Overview State Nexus Expansion Efforts Major Audit Issues Apportionment Best Practices

Federal Remote Seller Collection Authority FAQ Workgroup

Goals of Workgroup Federal Remote Seller Collection Authority FAQ Workgroup A. Develop questions and answers for Streamlined and non-streamlined states, remote and non-remote sellers, consumers, legislators,

Goals of Workgroup Federal Remote Seller Collection Authority FAQ Workgroup A. Develop questions and answers for Streamlined and non-streamlined states, remote and non-remote sellers, consumers, legislators,

The Honorable Max Baucus, Chairman The Honorable Dave Camp, Chairman

The Honorable Max Baucus, Chairman, Chairman Senate Committee on Finance House Committee on Ways & Means 219 Dirksen Senate Office Building 1102 Longworth House Office Building Washington, DC 20510 Washington,

The Honorable Max Baucus, Chairman, Chairman Senate Committee on Finance House Committee on Ways & Means 219 Dirksen Senate Office Building 1102 Longworth House Office Building Washington, DC 20510 Washington,

Year-end business tax planning

Year-end business tax planning Dec 6, 2018 The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity In specific circumstances,

Year-end business tax planning Dec 6, 2018 The information provided here is of a general nature and is not intended to address the specific circumstances of any individual or entity In specific circumstances,

TWIST-Q Summary of Developments First Quarter 2018

TWIST-Q Summary of Developments First Quarter 2018 This checklist includes developments for Quarter 1 of 2018 that have occurred prior to the date of publication. Please note that certain Quarter 1 items

TWIST-Q Summary of Developments First Quarter 2018 This checklist includes developments for Quarter 1 of 2018 that have occurred prior to the date of publication. Please note that certain Quarter 1 items

Accounting for Income Taxes Quarterly Hot Topics

In this issue: Accounting Developments Federal International Multistate Controversy Did You Know? Additional resources: Financial Accounting & Reporting - Income Taxes Dbriefs Webcasts Heads Up Newsletter

In this issue: Accounting Developments Federal International Multistate Controversy Did You Know? Additional resources: Financial Accounting & Reporting - Income Taxes Dbriefs Webcasts Heads Up Newsletter

1/29/2011. Mark G. Bodner Bureau Chief Complex Civil Enforcement Bureau Medicaid Control Unit Office of the Attorney General

Mark G. Bodner Bureau Chief Complex Civil Enforcement Bureau Medicaid Control Unit Office of the Attorney General The enactment of the Medicare and Medicaid Anti-Fraud and Abuse Amendments of 1977 authorized

Mark G. Bodner Bureau Chief Complex Civil Enforcement Bureau Medicaid Control Unit Office of the Attorney General The enactment of the Medicare and Medicaid Anti-Fraud and Abuse Amendments of 1977 authorized

TaxNewsFlash. KPMG report: Compilation of state responses to Wayfair

TaxNewsFlash United States No. 2018-277 July 23, 2018 KPMG report: Compilation of state responses to Wayfair The tax authorities or officials of various U.S. states have issued statements and guidance

TaxNewsFlash United States No. 2018-277 July 23, 2018 KPMG report: Compilation of state responses to Wayfair The tax authorities or officials of various U.S. states have issued statements and guidance

State and Local Taxation Update: Information Sharing and Transparency

Jeffrey A. Friedman, Partner Michele Borens, Partner May 14, 2014 TEI Denver Chapter State and Local Taxation Update: Information Sharing and Transparency Agenda Transparency in State Taxation What Type

Jeffrey A. Friedman, Partner Michele Borens, Partner May 14, 2014 TEI Denver Chapter State and Local Taxation Update: Information Sharing and Transparency Agenda Transparency in State Taxation What Type

Investment Advisor Roundtable 2015 Year-End Tax Update November 4, 2015

Investment Advisor Roundtable 2015 Year-End Tax Update November 4, 2015 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf & Company, P.C. Wolf & Company, P.C. Founded in

Investment Advisor Roundtable 2015 Year-End Tax Update November 4, 2015 MEMBER OF PKF NORTH AMERICA, AN ASSOCIATION OF LEGALLY INDEPENDENT FIRMS 2013 Wolf & Company, P.C. Wolf & Company, P.C. Founded in

2017 YEAR-END CHECKLIST. YEO & YEO CPAs & BUSINESS CONSULTANTS YEO & YEO. yeoandyeo.com

2017 YEAR-END YEO & YEO TAX CPAs & BUSINESS PLANNING CONSULTANTS CHECKLIST YEO & YEO CPAs & BUSINESS CONSULTANTS yeoandyeo.com As the end of the year approaches, it is a good time to think of planning

2017 YEAR-END YEO & YEO TAX CPAs & BUSINESS PLANNING CONSULTANTS CHECKLIST YEO & YEO CPAs & BUSINESS CONSULTANTS yeoandyeo.com As the end of the year approaches, it is a good time to think of planning

Year-End Tax Planning Letter

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

H.R. 1 TAX CUT AND JOBS ACT. By: Michelle McCarthy, Esq. and Tyler Murray, Esq.

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

Southeastern Association of Tax Administrators Conference 68 th Annual Meeting

Southeastern Association of Tax Administrators Conference 68 th Annual Meeting Marketplace Sales Tax Collection / Use Tax Reporting States Move to Capture More Untaxed Remote Sales July 16, 2018 Presented

Southeastern Association of Tax Administrators Conference 68 th Annual Meeting Marketplace Sales Tax Collection / Use Tax Reporting States Move to Capture More Untaxed Remote Sales July 16, 2018 Presented

2016 year-end tax considerations for businesses Legislative changes and other tax concerns that may impact planning

2016 year-end tax considerations for businesses Legislative changes and other tax concerns that may impact planning This guide reflects the tax considerations and legislative changes that we believe create

2016 year-end tax considerations for businesses Legislative changes and other tax concerns that may impact planning This guide reflects the tax considerations and legislative changes that we believe create

How Federal Tax Reform is Changing the State Tax Landscape

How Federal Tax Reform is Changing the State Tax Landscape Matthew Melinson, Partner Grant Thornton LLP - Philadelphia Drew VandenBrul, Managing Director Grant Thornton LLP - Philadelphia Kevin Milligan,

How Federal Tax Reform is Changing the State Tax Landscape Matthew Melinson, Partner Grant Thornton LLP - Philadelphia Drew VandenBrul, Managing Director Grant Thornton LLP - Philadelphia Kevin Milligan,

These slides are at Chapter 6. C Corporations. California and Multistate Developments. California

These slides are at http://mntaxclass.com. C Corporations Chapter 6 California and Multistate Developments California 2 2 What about TCJA conformity? 3 Considerations CA conforms to IRC as of 1/1/15 with

These slides are at http://mntaxclass.com. C Corporations Chapter 6 California and Multistate Developments California 2 2 What about TCJA conformity? 3 Considerations CA conforms to IRC as of 1/1/15 with

A report from Springfield

A report from Springfield Keith Staats Executive Director Illinois Chamber of Commerce Tax Institute The Impact of the State Budget on the Illinois Tax Climate Chicago Tax Club April 2, 2018 1 The Condition

A report from Springfield Keith Staats Executive Director Illinois Chamber of Commerce Tax Institute The Impact of the State Budget on the Illinois Tax Climate Chicago Tax Club April 2, 2018 1 The Condition

Personal Income Tax Orientation. House Committee on Revenue Legislative Revenue Office 1/23/2019

Personal Income Tax Orientation Legislative Revenue Office 1/23/2019 2 Orientation Overview Who files PIT Income and Tax Computation OR Pass-Through Entity Reduced Rates What s New Other States Note on

Personal Income Tax Orientation Legislative Revenue Office 1/23/2019 2 Orientation Overview Who files PIT Income and Tax Computation OR Pass-Through Entity Reduced Rates What s New Other States Note on

The Aftermath of Wayfair: What s Next?

The Aftermath of Wayfair: What s Next? Giles Sutton and Tommy Varnell August 1, 2018 Webinar 1 Agenda Nexus Background Examining the Wayfair Holding Anticipating the Impact of Wayfair on Private Equity

The Aftermath of Wayfair: What s Next? Giles Sutton and Tommy Varnell August 1, 2018 Webinar 1 Agenda Nexus Background Examining the Wayfair Holding Anticipating the Impact of Wayfair on Private Equity

District of Columbia. Summary of the Effects of Major Provisions of the Tax Cuts and Jobs Act on District Residents and Businesses

Summary of the Effects of Major Provisions of the Tax Cuts and Jobs Act on District Residents and Businesses February 27, 2018 1 Tax Changes Under the TCJA The Tax Cuts and Jobs Act (TCJA) is the most

Summary of the Effects of Major Provisions of the Tax Cuts and Jobs Act on District Residents and Businesses February 27, 2018 1 Tax Changes Under the TCJA The Tax Cuts and Jobs Act (TCJA) is the most

OPERATING A BUSINESS TAX CONSIDERATIONS

OPERATING A BUSINESS TAX CONSIDERATIONS 2 3 OPERATING A BUSINESS: Tax Considerations Tax accounting and recordkeeping play a major role in operating your business and how much you must give to Uncle Sam.

OPERATING A BUSINESS TAX CONSIDERATIONS 2 3 OPERATING A BUSINESS: Tax Considerations Tax accounting and recordkeeping play a major role in operating your business and how much you must give to Uncle Sam.

Corporate Income Tax Issues and Trends

Corporate Income Tax Issues and Trends Barb Dickerson Deloitte Tax LLP ATRA Outlook Conference November 17, 2006 Audit.Tax.Consulting.Financial Advisory. Determination of Tax Base Federal Taxable Income

Corporate Income Tax Issues and Trends Barb Dickerson Deloitte Tax LLP ATRA Outlook Conference November 17, 2006 Audit.Tax.Consulting.Financial Advisory. Determination of Tax Base Federal Taxable Income

Individual year-end planning and tax law updates

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

Individual yearend planning and tax law updates October 29, 2013 Baker Tilly refers to Baker Tilly Virchow Krause, LLP, an independently owned and managed member of Baker Tilly International. 1 Presenters

US tax thought leadership December 18, 2017

US tax thought leadership December 18, 2017 This thought leadership compares the conference committee report released on December 15, 2017 with the existing tax provisions and its impact on US corporate

US tax thought leadership December 18, 2017 This thought leadership compares the conference committee report released on December 15, 2017 with the existing tax provisions and its impact on US corporate

Year-End Tax Planning and Looking Forward

2015 Year-End Tax Planning Year-End Tax Planning and Looking Forward November 9, 2015 Dear Clients and Friends: As year-end approaches, developing tax planning strategies for individuals and businesses

2015 Year-End Tax Planning Year-End Tax Planning and Looking Forward November 9, 2015 Dear Clients and Friends: As year-end approaches, developing tax planning strategies for individuals and businesses

California and Multistate

California and Multistate Chapter 6 1 Conformity Conformity in General FTB Information Letter 2014-01 See text in outline. https://www.ftb.ca.gov/forms/updates/conformity.shtml 2 Conformity references

California and Multistate Chapter 6 1 Conformity Conformity in General FTB Information Letter 2014-01 See text in outline. https://www.ftb.ca.gov/forms/updates/conformity.shtml 2 Conformity references

11/7/2017. Bio. Our agenda. Year-End Tax Planning for Private or Small Businesses & Individuals Webinar Heather Alley, CPA & Nathan Clark, CPA

Year-End Tax Planning for Private or Small Businesses & Individuals Webinar Heather Alley, CPA & Nathan Clark, CPA Bio Heather Alley Partner, DHG Tax 828.236.5848 heather.alley@dhgllp.com Nathan Clark

Year-End Tax Planning for Private or Small Businesses & Individuals Webinar Heather Alley, CPA & Nathan Clark, CPA Bio Heather Alley Partner, DHG Tax 828.236.5848 heather.alley@dhgllp.com Nathan Clark

2018 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS

2018 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this is the time of year we normally suggest possible year-end tax strategies for our clients. However, from a

2018 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this is the time of year we normally suggest possible year-end tax strategies for our clients. However, from a

2017 Annual Meeting FEDERATION OF TAX ADMINISTRATORS June 13, 2017 THE WESTIN SEATTLE. Federal Partnership Audit Legislation State Impacts

Federal Partnership Audit Legislation State Impacts Panelists Moderator: Helen Hecht, Esq. General Counsel Multistate Tax Commission Suzanne Leighton, CPA MST Deputy Secretary for Compliance and Collections

Federal Partnership Audit Legislation State Impacts Panelists Moderator: Helen Hecht, Esq. General Counsel Multistate Tax Commission Suzanne Leighton, CPA MST Deputy Secretary for Compliance and Collections

US Taxation- A Primer

WIRC of the ICAI- Seminar Series on Global Updates- I US Taxation- A Primer Presented by : 7 th May, 2011 CA. Shishir Lagu Session Overview Introduction Corporate Tax Overview Federal Income Tax State

WIRC of the ICAI- Seminar Series on Global Updates- I US Taxation- A Primer Presented by : 7 th May, 2011 CA. Shishir Lagu Session Overview Introduction Corporate Tax Overview Federal Income Tax State

Is your bank prepared for the new tax law? March 14, :00 PM ET

Please disable pop-up blocking software before viewing this webcast Is your bank prepared for the new tax law? March 14, 2018 2:00 PM ET 1 CPE reminders To receive CPE, you must be active for the entire

Please disable pop-up blocking software before viewing this webcast Is your bank prepared for the new tax law? March 14, 2018 2:00 PM ET 1 CPE reminders To receive CPE, you must be active for the entire

Welcome to Tax Update Your hosts: For Businesses & Estates Gary McBride and Annette Nellen Federal and California Tax Update for Businesses & Estates Dec 2015/Jan2016 http://mntaxclass.com Slides Supplements

Welcome to Tax Update Your hosts: For Businesses & Estates Gary McBride and Annette Nellen Federal and California Tax Update for Businesses & Estates Dec 2015/Jan2016 http://mntaxclass.com Slides Supplements

Private Letter Ruling No. PLR , Colorado Department of Revenue, October 3, 2017, released December 2017

January 2018 Colorado Presence of Employee In-State Created Nexus The Colorado Department of Revenue has issued a private letter ruling stating that the presence of a taxpayer s employee in Colorado established

January 2018 Colorado Presence of Employee In-State Created Nexus The Colorado Department of Revenue has issued a private letter ruling stating that the presence of a taxpayer s employee in Colorado established

From the Hill to the Street: An insider s perspective. Not FDIC Insured Not Bank Guaranteed May Lose Value

From the Hill to the Street: An insider s perspective Not FDIC Insured Not Bank Guaranteed May Lose Value Eaton Vance Investment Managers From the Hill to the Street An Insiders Perspective Sponsored by:

From the Hill to the Street: An insider s perspective Not FDIC Insured Not Bank Guaranteed May Lose Value Eaton Vance Investment Managers From the Hill to the Street An Insiders Perspective Sponsored by:

Q40 Table of Contents

Q40 Table of Contents Tab 1: 2014 Tax Table 2014 Tax Computation Worksheet State Individual Income Tax Quick Reference Chart (2014) General Alabama Alaska Arizona Arkansas California Colorado Connecticut

Q40 Table of Contents Tab 1: 2014 Tax Table 2014 Tax Computation Worksheet State Individual Income Tax Quick Reference Chart (2014) General Alabama Alaska Arizona Arkansas California Colorado Connecticut

Staff Presentation to the House Finance Committee February 7, 2019

Staff Presentation to the House Finance Committee February 7, 2019 1 Remote Sellers H 5150 Article 2 H 5151 Article 5, Sec. 11 (same as Art. 2) H 5278 Stand alone duplicate Mobile Sports betting H 5150

Staff Presentation to the House Finance Committee February 7, 2019 1 Remote Sellers H 5150 Article 2 H 5151 Article 5, Sec. 11 (same as Art. 2) H 5278 Stand alone duplicate Mobile Sports betting H 5150

OPERATING A BUSINESS TAX CONSIDERATIONS

OPERATING A BUSINESS TAX CONSIDERATIONS 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 OPERATING A BUSINESS: Tax Considerations Tax accounting

OPERATING A BUSINESS TAX CONSIDERATIONS 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 OPERATING A BUSINESS: Tax Considerations Tax accounting

The aftermath of Wayfair: Developments and action steps for businesses

The aftermath of Wayfair: Developments and action steps for businesses Wednesday, September 5, 2018 1-2:30 pm ET We will be starting soon Please disable pop-up blocking software before viewing this webcast

The aftermath of Wayfair: Developments and action steps for businesses Wednesday, September 5, 2018 1-2:30 pm ET We will be starting soon Please disable pop-up blocking software before viewing this webcast

Individual Taxation and Planning

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Tax Recommendations and Actions in Other States. Joel Michael House Research Department June 9, 2011

Tax Recommendations and Actions in Other States Joel Michael House Research Department June 9, 2011 Governors FY 2012 Recommendations 12 governors recommend net revenue (tax and fee) increases 12 governors

Tax Recommendations and Actions in Other States Joel Michael House Research Department June 9, 2011 Governors FY 2012 Recommendations 12 governors recommend net revenue (tax and fee) increases 12 governors

Pennsylvania Corporate Income Tax Return Instructions 2012 >>>CLICK HERE<<<

Pennsylvania Corporate Income Tax Return Instructions 2012 2015/Estimated Forms 2014 2013 2012 2011 2010 Personal Income Tax Guide PA- 20S/PA-65 CP -- 2014 PA Schedule CP - Corporate Partner Withholding

Pennsylvania Corporate Income Tax Return Instructions 2012 2015/Estimated Forms 2014 2013 2012 2011 2010 Personal Income Tax Guide PA- 20S/PA-65 CP -- 2014 PA Schedule CP - Corporate Partner Withholding

WSRP, LLC Salt Lake City UT, Lehi UT & Las Vegas NV

Background on WSRP The firm began in 1985 with 6 people. Now the firm has over 100 + professionals and one of the largest CPA firms in Utah. Offices in SLC, Lehi, Las Vegas, and Ogden shortly. We primarily

Background on WSRP The firm began in 1985 with 6 people. Now the firm has over 100 + professionals and one of the largest CPA firms in Utah. Offices in SLC, Lehi, Las Vegas, and Ogden shortly. We primarily

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

LOCALLY ADMINISTERED SALES AND USE TAXES A REPORT PREPARED FOR THE INSTITUTE FOR PROFESSIONALS IN TAXATION

LOCALLY ADMINISTERED SALES AND USE TAXES A REPORT PREPARED FOR THE INSTITUTE FOR PROFESSIONALS IN TAXATION PART III: OPTIONS FOR REDUCING COSTS RELATED TO LOCALLY ADMINISTERED SALES AND USE TAXES Prepared

LOCALLY ADMINISTERED SALES AND USE TAXES A REPORT PREPARED FOR THE INSTITUTE FOR PROFESSIONALS IN TAXATION PART III: OPTIONS FOR REDUCING COSTS RELATED TO LOCALLY ADMINISTERED SALES AND USE TAXES Prepared

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

Opportunity Zones Tax incentives for investing in low-income communities

Opportunity Zones Tax incentives for investing in low-income communities Overview > Established by Tax Cut and Jobs Act of 2017 > 8,700 zones in the US (11% of the country) > Only capital gains can be

Opportunity Zones Tax incentives for investing in low-income communities Overview > Established by Tax Cut and Jobs Act of 2017 > 8,700 zones in the US (11% of the country) > Only capital gains can be

business owner issues and depreciation deductions

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

Maximizing small-biz incentives in the Recovery Act

Maximizing small-biz incentives in the Recovery Act The $787 billion American Recovery and Reinvestment Act of 2009 (P.L. 111-5, Feb. 17, 2009) provides almost $300 billion in tax relief. As a stimulus

Maximizing small-biz incentives in the Recovery Act The $787 billion American Recovery and Reinvestment Act of 2009 (P.L. 111-5, Feb. 17, 2009) provides almost $300 billion in tax relief. As a stimulus

State & Local Tax Alert

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Ohio Enacts Budget Including Expanded Sales Tax Nexus, Municipal Income Tax Changes, and Amnesty Program The Ohio

State & Local Tax Alert Breaking state and local tax developments from Grant Thornton LLP Ohio Enacts Budget Including Expanded Sales Tax Nexus, Municipal Income Tax Changes, and Amnesty Program The Ohio

What Nexus Standard Would the Bill Require to Impose an Income Tax?

All States Income Tax Nexus Legislation Introduced in Congress November 2018 A bill introduced in the U.S. House of Representatives would: establish a federal physical presence nexus standard for state

All States Income Tax Nexus Legislation Introduced in Congress November 2018 A bill introduced in the U.S. House of Representatives would: establish a federal physical presence nexus standard for state

2016 Year-End Tax Planning Letter

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

9NOV2016 2016 Year-End Tax Planning Letter Dear Vista Wealth Clients and Friends, As 2016 draws to a close, you should give consideration to year-end tax planning strategies. This letter highlights some

TaxNewsFlash. KPMG report: Follow-up state actions, Wayfair decision (DC, IL, MD, MA, NE, NJ, NM, SC, SD)

") TaxNewsFlash United States No. 2018-406 October 1, 2018 KPMG report: Follow-up state actions, Wayfair decision (DC, IL, MD, MA, NE, NJ, NM, SC, SD) State governments have continued to issue guidance or

TaxNewsFlash United States No. 2018-406 October 1, 2018 KPMG report: Follow-up state actions, Wayfair decision (DC, IL, MD, MA, NE, NJ, NM, SC, SD) State governments have continued to issue guidance or

Let s Talk Taxes. Jim Forbes, CPA. February 12, 2013

Let s Talk Taxes Jim Forbes, CPA February 12, 2013 The income tax had made more liars out of the American people than golf. Will Rogers AGENDA The hardest thing in the world to understand is the income

Let s Talk Taxes Jim Forbes, CPA February 12, 2013 The income tax had made more liars out of the American people than golf. Will Rogers AGENDA The hardest thing in the world to understand is the income

IRC 965, BEAT, GILTI and FDII Through the Lens of a SALT Professional + Recent Developments

IRC 965, BEAT, GILTI and FDII Through the Lens of a SALT Professional + Recent Developments June 21, 2018 Korwin Roskos (Moderator) Senior Tax Manager-State & Local Tax, Amazon Vice Chair of TEI s SALT

IRC 965, BEAT, GILTI and FDII Through the Lens of a SALT Professional + Recent Developments June 21, 2018 Korwin Roskos (Moderator) Senior Tax Manager-State & Local Tax, Amazon Vice Chair of TEI s SALT

Midyear Tax Planning Letter

Midyear Tax Planning Letter 2015 Introduction Tax planning for 2015 is a venture in uncertainty. Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately,

Midyear Tax Planning Letter 2015 Introduction Tax planning for 2015 is a venture in uncertainty. Last December, Congress passed legislation extending a number of expired tax provisions. Unfortunately,

By Brian McCuller, JD, CPA, and Andrew Hill, JD

Impact of the PATH ACT and Other Business Legislation By Brian McCuller, JD, CPA, and Andrew Hill, JD The dust has settled on 2015 s state and federal tax legislation. There is much welcome news for Tennessee

Impact of the PATH ACT and Other Business Legislation By Brian McCuller, JD, CPA, and Andrew Hill, JD The dust has settled on 2015 s state and federal tax legislation. There is much welcome news for Tennessee

Michigan Business Tax Frequently Asked Questions

NOTICE: The MBT was amended by 145 PA 2007 on December 1, 2007. Act 145 imposes an annual surcharge to taxpayers' MBT liability, as well as makes other changes. Some of the FAQs below have revised answers

NOTICE: The MBT was amended by 145 PA 2007 on December 1, 2007. Act 145 imposes an annual surcharge to taxpayers' MBT liability, as well as makes other changes. Some of the FAQs below have revised answers

Your Comprehensive Guide to 2013 Year-End Tax Planning

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

Your Comprehensive Guide to 2013 Year-End Tax Planning Early in 2013, the 2012 Taxpayer Relief Act was enacted and the Bush-era tax cuts, which were scheduled to sunset at the end of 2012, were permanently

2017 State Tax Legislative Outlook

Maria Todorova, Partner, Sutherland Madison Barnett, Counsel, Sutherland Robert Garvey, Principal, PwC TEI San Diego State and Local Tax Seminar September 29, 2016 2017 State Tax Legislative Outlook All

Maria Todorova, Partner, Sutherland Madison Barnett, Counsel, Sutherland Robert Garvey, Principal, PwC TEI San Diego State and Local Tax Seminar September 29, 2016 2017 State Tax Legislative Outlook All

SALT Alert! : Significant Corporation Business Tax Changes Enacted in New Jersey

SALT Alert! 2018-11: Significant Corporation Business Tax Changes Enacted in New Jersey On July 1, 2018, New Jersey Governor Phil Murphy signed and conditionally vetoed a number of bills that implement

SALT Alert! 2018-11: Significant Corporation Business Tax Changes Enacted in New Jersey On July 1, 2018, New Jersey Governor Phil Murphy signed and conditionally vetoed a number of bills that implement

Federal Tax Reform: 2017 Timeline

Federal Tax Reform: 2017 Timeline June 24, 2016 - House Republicans released their vision for tax reform (the Blueprint). April 26, 2017 - Sept. 27, 2017 - President Trump released his overall vision for

Federal Tax Reform: 2017 Timeline June 24, 2016 - House Republicans released their vision for tax reform (the Blueprint). April 26, 2017 - Sept. 27, 2017 - President Trump released his overall vision for

American Payroll Association

American Payroll Association Government Relations Washington, DC June 2, 2015 Statement for the Record Submitted to the House Judiciary Subcommittee on Regulatory Reform, Commercial and Antitrust Law In

American Payroll Association Government Relations Washington, DC June 2, 2015 Statement for the Record Submitted to the House Judiciary Subcommittee on Regulatory Reform, Commercial and Antitrust Law In

Income/Franchise: Idaho State Tax Commission Discusses How Recently Enacted Federal Tax Reforms May Affect State Income Taxation

State Tax Matters The power of knowing. In this issue: Income/Franchise: Idaho State Tax Commission Discusses How Recently Enacted Federal Tax Reforms May Affect State Income Taxation... 1 Income/Franchise:

State Tax Matters The power of knowing. In this issue: Income/Franchise: Idaho State Tax Commission Discusses How Recently Enacted Federal Tax Reforms May Affect State Income Taxation... 1 Income/Franchise:

Tax Cuts & Jobs Act: Considerations for Funds

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

Tax Cuts & Jobs Act: Considerations for Funds December 22, 2017 On December 22, 2017, the President signed into law the 2017 U.S. tax reform bill formerly known as the Tax Cuts & Jobs Act (the TCJA ).

2017 Year-End Tax Planning

& C O M PA N Y, L L C, C PA s 2017 Year-End Tax Planning 1101 Wootton Parkway, Suite 400 Rockville, MD 20852 Phone: (301) 260-0809 Fax: (202) 204-6322 950 North Washington, St Suite 238 Alexandria, VA

& C O M PA N Y, L L C, C PA s 2017 Year-End Tax Planning 1101 Wootton Parkway, Suite 400 Rockville, MD 20852 Phone: (301) 260-0809 Fax: (202) 204-6322 950 North Washington, St Suite 238 Alexandria, VA

KPMG Share Forum. The Wayfair decision: navigating a world without Quill. Los Angeles, CA

KPMG Share Forum The Wayfair decision: navigating a world without Quill Los Angeles, CA [August 23, 2018 Notices The following information is not intended to be written advice concerning one or more Federal

KPMG Share Forum The Wayfair decision: navigating a world without Quill Los Angeles, CA [August 23, 2018 Notices The following information is not intended to be written advice concerning one or more Federal

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

HOW TO DEAL WITH INCOME AND ESTATE TAX TIMEBOMBS Nicholas J. Houle CPA/PFS CFP 2010 Ag Summit Principal December, 2010 LarsonAllen Financial LLC Chicago, IL Minneapolis, MN 612-376-4760 nhoule@larsonallen.com

Understanding Oregon s Throwback Rule for Apportioning Corporate Income

Understanding Oregon s Throwback Rule for Apportioning Corporate Income Senate Interim Committee on Finance and Revenue January 12, 2018 2 Apportioning Corporate Income Apportionment is a method of dividing

Understanding Oregon s Throwback Rule for Apportioning Corporate Income Senate Interim Committee on Finance and Revenue January 12, 2018 2 Apportioning Corporate Income Apportionment is a method of dividing

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Fifteenth Edition (January 2014)

") LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Texas Franchise Tax Deskbook Managers Staff File Fifteenth Edition (January 2014) Highlights of this Edition The following are some important

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS Route To: Partners PPC's Texas Franchise Tax Deskbook Managers Staff File Fifteenth Edition (January 2014) Highlights of this Edition The following are some important

Aviation Tax Law Webinar March 4, 2014

Aviation Tax Law Webinar March 4, 2014 New Developments in State Sales and Use Taxes on Aircraft Purchases Key Sales and Use Tax Planning Tools 1 Presented by: Christopher B. Younger 1054 31st Street NW,

Aviation Tax Law Webinar March 4, 2014 New Developments in State Sales and Use Taxes on Aircraft Purchases Key Sales and Use Tax Planning Tools 1 Presented by: Christopher B. Younger 1054 31st Street NW,