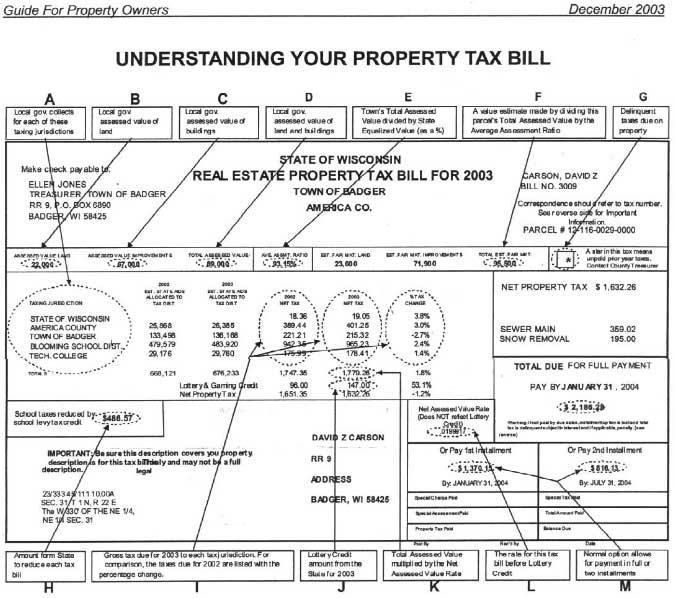

Understanding Your Tax Bill. A Basic Understanding of Tax Assessment and Taxation

|

|

|

- Bonnie Bond

- 5 years ago

- Views:

Transcription

1 Understanding Your Tax Bill A Basic Understanding of Tax Assessment and Taxation

2

3 Taxation Cycle Assessment Process-Assessor places values on properties Equalization Process by DOR-equalized value total that determines tax rates & apportionment is calculated Budget Process-levies are set Apportionment Process-levy amounts are apportioned to taxpayers

4 ASSESSMENT Taxes based on Assessment Effective Date of Assessment is January 1 of each year Assessor values properties based on market and State of Wisconsin percentages

5 Assessment Process Local Assessors place value on property specified under s73.03(2a) stats From View From best information that can be practically obtained Value of Land and Buildings should equal the Market value

6 Assessment Criteria Quality of construction Average: older home, simple ranch Less than average: Wausau, Modular Square footage-main floor + or for basement, garage, porches, decks, sunrooms Executive Homes central vacuum, wired for sound, highest grade materials, extra heavy frame, fireplace Cost of construction-state manual basic cost times grade factor given by assessor Depreciation Waterfront property is generally considered more desirable and this is reflected in assessment PLACING VALUE ON PROPERTY IS A BALANCING ACT

7 OPEN BOOK All property records are Open Records If possible, meet with assessor to discuss values prior to Open Book Assessor is allowed to make changes at the Open Book Session If not satisfied, property owners can protest values by requesting a hearing at the Board of Review

8 BOARD OF REVIEW Assessor s Value is presumed correct To have correction made, owner must prove property is overvalued in comparison with similar properties use arm s length sales/recent sales of comparable properties size of lot, size and age of buildings, depreciation and income potential

9 APPEALS If a taxpayer is not satisfied with decision of Board of Review Circuit Court Appeals Department of Revenue Appeals Consult AND of the State Statutes

10 DEPARTMENT OF REVENUE Department of Revenue analyzes reports to determine value Statement of Assessment Assessor s final report Equalized value is driven by sales Transfer returns from current year used to establish equalized value DOR establishes: total equalized value of properties total equalized value of each class of property

11 STRATEGIES USED TO DETERMINE EQUALIZED VALUE Sales Analysis Use Value Analysis Property Appraisals Local Reports s WI State Corrections

12 SALES ANALYSIS 2 methods: assessment-to sales ratio studies compare selling prices with local assessment sufficient number of sales = reflect the overall accuracy unit value projections used to value swamp and waste, forest land or other property transfer returns are used to form database of all sales in the state

13 ASSESSMENT TO SALES ANALYSIS After analysis of properties, assessment ratio is 93.13%

14 USE VALUE ANALYSIS values are estimated from the income that could be generated by the land/capitalization rate values produced by the income approach adjusted based on land rental information from UW-EX agents

15 PROPERTY APPRAISALS Sample appraisals are used as a further test of quality of sales-based value projections Property appraisals are used when there is a lack of sales activity These are used in an analysis similar to the assessment/sales method

16 LOCAL REPORTS CLERK S STATEMENT OF ASSESSMENTS Summarizes the final values on the local assessment roll for real and personal property This report compared with the assessor s report for any changes ASSESSORS FINAL REPORT This report contains the same info as SOA, but analyzes the reasons for the change

17 SEC WI STATS CORRECTIONS Significant effort is spent reviewing prior year equalized value determinations because many assessors file previous reports late Equalized values must be certified to jurisdiction by August 15 of each year

18 FINALIZING EQUALIZED VALUE DOR determines market value of each class of real and personal property in the state Municipalities or counties can appeal its equalized value by Oct 15 Equalized value of school districts within its borders derives school district s equalized value

19 Taxing using assessed value Town A=$20,000, assessed value (28.6%) of total assessed value Town B=$50,000, assessed value (71.4%) of total assessed value Town A would pay 28.6% of levy Town B would pay 71.4% of levy

20 Taxing using equalized value Town A has $50,000, of equalized value (50%) of total equalized value Town B has $50,000, of equalized value (50%) of total equalized value Each town would pay ½ of the levied taxes

21 USE OF EQUALIZED VALUES Property tax levies of jurisdictions are apportioned to each municipality based on equalized value This must be done to apportion taxes fairly to all property owners

22 EQUALIZATION Assessed value is important for maintaining equity among taxpayers within municipality Assessed values used to distribute tax burden among individual taxpayers Equalized values used to distribute state levy among counties county levy among municipalities

23 BUDGET PROCESS Budget hearings with departments County Level Meet with Governing Committee Meet with Finance Committee Approve or cut budgets Approval of County Board (Town Board)

24 COUNTY CLERK Clerk is provided with total equalized value of the county (see next sheet) Because of imposed 1992 levy limits levy rate cannot exceed 1992 rate Clerk apportions taxes to local municipalities using equalized value

25 Report used to apportion County Levy

26 APPORTIONMENT PROCESS Process of dividing tax levies for each jurisdiction among all municipalities which contain territory in the jurisdiction Done by percentages Total equalized value of town, village or city goes up your % of taxes goes up 1992 Levy Limits tax rate cannot exceed the tax rate of 1992.

27

28 COUNTY TREASURER Local clerks prepare a mill rate worksheet Includes total levy for each taxing district Includes estimated state aids figure County Treasurer s office calculates individual mill rate Individual mill rates added minus state aids = net mill rate used to calculate taxes

29 **for villages & cities that have TID districts, use column E from Tax Worksheet PC-202 MILL RATE: GREEN LAKE COUNTY BERLIN SCHOOL TAX YEAR 2007 MILL RATE INPUT SHEET MUNICIPALITY NO: 206 CITY OF BERLIN MILL RATE WORKSHEET Aggregate Ratio Used to Calculate ESTIMATED FAIR MARKET VALUE: Mill Rate Calculations TAXING JURISDICTIONS CERTIFIED LEVY AMOUNT** ASSESSED VALUE MILL RATE # STATE 38, ,795, COUNTY 1,183, ,795, LOCAL 1,601, ,795, SCHOOL DT #0434 BERLIN 1,949, ,795, SCHOOL DT # SCHOOL DT # SCHOOL DT # MPTC # , ,795, SPECIAL DT # SPECIAL DT # SPECIAL DT # TOTAL GENERAL TAXES TO COLLECT 5,076, ESTIMATED MAJOR STATE AIDS TAXING JURISDICTIONS YR: 2006 STATE AIDS YR: 2007 STATE AIDS COUNTY 87,635 88,262 LOCAL 2,136,115 2,134,323 SCHOOL DT #0434 BERLIN 4,287,785 4,338,033 SCHOOL DT # SCHOOL DT # SCHOOL DT # MPTC # ,587 50,526 TOTAL 6,565,122 6,611,144 SCHOOL LEVY TAX CREDIT ASSESSED VALUE MILL RATE AMOUNT CERTIFIED 347, ,795, EQUALIZED VALUE SCHOOL TAX RATE (lottery credit only) MAX CREDIT VALUE LOTTERY CREDIT SCHOOL DT #0434 BERLIN , SCHOOL DT # SCHOOL DT # SCHOOL DT # Clerk Date Phone Number

30 SUMMARY ASSESSOR VALUES PROPERTY TAXPAYERS CAN ACCEPT OR APPEAL DOR ANALYZES DATA AND CERTIFIES TOTAL EQUALIZED VALUE COUNTY CLERK USES THESE VALUES TO APPORTION TAXES USING TAX RATE COUNTY TREASURER CALCULATES TAXES USING MILL RATE TAX BILL PREPARED AND MAILED COLLECTION AND QUESTION PROCESS

31 Taxes Assessments, budgets, apportionments all fit together to produce tax bills State Cty School MPTI Local SD Assets Budget Appor

32 Tax Bill Info Tax Bill Shows all values of property Shows all amounts of tax Description of WHERE your dollars are spent

33

34 Vocabulary Assessment Value placed on property by assessor Budget Set at each level of government Approved by elected representatives Apportionment Process of dividing tax levies for each taxing jurisdiction among all municipalities, based on value of district

35 Where to Get More Information Local Assessor County and Town Board Meetings School District Meetings Department of Revenue website County website

36

How to use the calendar: Scroll through the document to see all months or use the bookmarks on the left to access each month

2014 Calendar How to use the calendar: Scroll through the document to see all months or use the bookmarks on the left to access each month Abbreviations: DNR Wisconsin Department of Natural Resources DOA

2014 Calendar How to use the calendar: Scroll through the document to see all months or use the bookmarks on the left to access each month Abbreviations: DNR Wisconsin Department of Natural Resources DOA

DOR Update. MTAW Fall Conference September 26, 2014 Wisconsin Department of Revenue

DOR Update MTAW Fall Conference September 26, 2014 Wisconsin Department of Revenue Valeah Foy 1 Agenda Division of State & Local Finance Technical l& Assessment tservices Manufacturing Equalization Local

DOR Update MTAW Fall Conference September 26, 2014 Wisconsin Department of Revenue Valeah Foy 1 Agenda Division of State & Local Finance Technical l& Assessment tservices Manufacturing Equalization Local

2009 Guide for Property Owners

2009 Guide for Property Owners Wisconsin Department of Revenue Division of State & Local Finance Bureau of Assessment Practices P.O. Box 8971 Madison, WI 53708-8971 E-mail: bapdor@revenue.wi.gov Prop 060

2009 Guide for Property Owners Wisconsin Department of Revenue Division of State & Local Finance Bureau of Assessment Practices P.O. Box 8971 Madison, WI 53708-8971 E-mail: bapdor@revenue.wi.gov Prop 060

DOR Update. Presenter. Municipal Treasurers. Valeah Foy Director, Local Government Services 10/4/2017. September 2017

DOR Update Municipal Treasurers September 1 Presenter Valeah Foy Director, Local Government Services 2 1 Topics of Discussion SLF division updates Electronic filing Law changes State debt collection Resources

DOR Update Municipal Treasurers September 1 Presenter Valeah Foy Director, Local Government Services 2 1 Topics of Discussion SLF division updates Electronic filing Law changes State debt collection Resources

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK April 2018

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

2017 Statistical Revaluation Forum. August 29, Judie Belanger, Director of Finance & Administration. Rosann Lentz, City Assessor

2017 Statistical Revaluation Forum August 29, 2017 Judie Belanger, Director of Finance & Administration Rosann Lentz, City Assessor Mike Tarello and Kevin Leen Vision Government Solutions In the State

2017 Statistical Revaluation Forum August 29, 2017 Judie Belanger, Director of Finance & Administration Rosann Lentz, City Assessor Mike Tarello and Kevin Leen Vision Government Solutions In the State

DOR Update. Clerk, Treasurers & Finance Officers Institute Stevens Point June 21, Wisconsin Department of Revenue

DOR Update Clerk, Treasurers & Finance Officers Institute Stevens Point June 21, 1 Presenters Valeah Foy, Director Local Government Services Deb Werner Kelln, Revenue Auditor Local Government Services

DOR Update Clerk, Treasurers & Finance Officers Institute Stevens Point June 21, 1 Presenters Valeah Foy, Director Local Government Services Deb Werner Kelln, Revenue Auditor Local Government Services

DOR Update 6/21/2017. Presenters. Topics of Discussion. Clerk, Treasurers & Finance Officers Institute Stevens Point June 21, 2017

6/21/ DOR Update Clerk, Treasurers & Finance Officers Institute Stevens Point June 21, 1 Presenters Valeah Foy, Director Local Government Services Deb Werner Kelln, Revenue Auditor Local Government Services

6/21/ DOR Update Clerk, Treasurers & Finance Officers Institute Stevens Point June 21, 1 Presenters Valeah Foy, Director Local Government Services Deb Werner Kelln, Revenue Auditor Local Government Services

Appendix A: Overview of Illinois property tax system

Appendix A: Overview of Illinois property tax system Across Illinois, more than 6,000 units of government billed taxpayers a total of $29.8 billion in 2017, $19.2 billion of which was billed to residential

Appendix A: Overview of Illinois property tax system Across Illinois, more than 6,000 units of government billed taxpayers a total of $29.8 billion in 2017, $19.2 billion of which was billed to residential

BACKRGROUND INFORMATION:

The City of Sparta is seeking proposals for the following work: Statutory assessment services for three year period (2015, 2016, and 2017) beginning January 1, 2015.This will be regular annual maintenance

The City of Sparta is seeking proposals for the following work: Statutory assessment services for three year period (2015, 2016, and 2017) beginning January 1, 2015.This will be regular annual maintenance

PROPERTY TAX 101 PRESENTED BY: TORRANCE COUNTY ASSESSOR - BETTY CABBER HIDALGO COUNTY TREASURER - TYLER MASSEY

PROPERTY TAX 101 PRESENTED BY: TORRANCE COUNTY ASSESSOR - BETTY CABBER HIDALGO COUNTY TREASURER - TYLER MASSEY What does all of this mean!? ASSESSMENTS RESIDENTAL NON RESIDENTIAL PERSONAL PROPERTY PROTEST

PROPERTY TAX 101 PRESENTED BY: TORRANCE COUNTY ASSESSOR - BETTY CABBER HIDALGO COUNTY TREASURER - TYLER MASSEY What does all of this mean!? ASSESSMENTS RESIDENTAL NON RESIDENTIAL PERSONAL PROPERTY PROTEST

Session of HOUSE BILL No By Committee on Taxation 1-30

Session of 0 HOUSE BILL No. By Committee on Taxation -0 0 0 0 AN ACT concerning property taxation; relating to distribution of taxes paid under protest; amending K.S.A. 0 Supp. -00 and repealing the existing

Session of 0 HOUSE BILL No. By Committee on Taxation -0 0 0 0 AN ACT concerning property taxation; relating to distribution of taxes paid under protest; amending K.S.A. 0 Supp. -00 and repealing the existing

Reassessment New Castle County. R. Douglas Sensabaugh Manager Office of Property Assessment

Reassessment New Castle County R. Douglas Sensabaugh Manager Assessment Base Assessments in Delaware are over thirty years old The last reassessment in each County was New Castle County: 1983 Sussex County:

Reassessment New Castle County R. Douglas Sensabaugh Manager Assessment Base Assessments in Delaware are over thirty years old The last reassessment in each County was New Castle County: 1983 Sussex County:

New Hampshire Municipal Tax Rates: How Are They Calculated? And How Do They Change? March 27, 2017

New Hampshire Municipal Tax Rates: How Are They Calculated? And How Do They Change? March 27, 2017 Stephan W. Hamilton, Director Municipal & Property Division NH Department of Revenue Administration John

New Hampshire Municipal Tax Rates: How Are They Calculated? And How Do They Change? March 27, 2017 Stephan W. Hamilton, Director Municipal & Property Division NH Department of Revenue Administration John

Plainfield Community Consolidated School District #202 LOCAL PROPERTY TAX TOPICS, INFORMATION, AND THE 2016 TAX

Plainfield Community Consolidated School District #202 LOCAL PROPERTY TAX TOPICS, INFORMATION, AND THE 2016 TAX LEVY 1 Table of Contents I. Overview of the Tax Levy and Extension Process II. Calculating

Plainfield Community Consolidated School District #202 LOCAL PROPERTY TAX TOPICS, INFORMATION, AND THE 2016 TAX LEVY 1 Table of Contents I. Overview of the Tax Levy and Extension Process II. Calculating

Assessor s Office. Our Township Blackberry Our Community. Any Relief in Sight for Property Taxes? Uwe Rotter CIAO. Did You Know?

Assessor s Office Uwe Rotter CIAO Any Relief in Sight for Property Taxes? Many residents of our township have contacted my office questioning the value of their assessment in a steadily declining market

Assessor s Office Uwe Rotter CIAO Any Relief in Sight for Property Taxes? Many residents of our township have contacted my office questioning the value of their assessment in a steadily declining market

STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK April 2018

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

SUBJECT: Property Tax and Equalization Calendar for 2019 STATE TAX COMMISSION 2019 PROPERTY TAX, COLLECTIONS AND EQUALIZATION CALENDAR

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER Bulletin No. 17 of 2018 October 22, 2018 Property Tax and Equalization Calendar for

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER Bulletin No. 17 of 2018 October 22, 2018 Property Tax and Equalization Calendar for

PORTAGE COUNTY FUND STRUCTURE

PORTAGE COUNTY FUND STRUCTURE Governmental Funds Proprietary Funds General Fund Debt Service Capital Projects Special Revenue Funds (Major) Special Revenue Funds (Non Major) Enterprise Funds Internal Service

PORTAGE COUNTY FUND STRUCTURE Governmental Funds Proprietary Funds General Fund Debt Service Capital Projects Special Revenue Funds (Major) Special Revenue Funds (Non Major) Enterprise Funds Internal Service

McCreary Veselka Bragg & Allen P.C. Attorneys at Law. A Guide for Setting Tax Rates

McCreary Veselka Bragg & Allen P.C. Attorneys at Law A Guide for Setting Tax Rates TRUTH-IN-TAXATION 2018 for Our Clients We are pleased to present this easy-to-use guidebook to help you with this year

McCreary Veselka Bragg & Allen P.C. Attorneys at Law A Guide for Setting Tax Rates TRUTH-IN-TAXATION 2018 for Our Clients We are pleased to present this easy-to-use guidebook to help you with this year

Abatements and Refunds

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

H 5209 S T A T E O F R H O D E I S L A N D

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

LC000 0 -- H 0 S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 0 A N A C T RELATING TO TAXATION - LEVY AND ASSESSMENT OF LOCAL TAXES Introduced By: Representative Michael

An introductory guide to creating local budgets

An introductory guide to creating local budgets 150-504-406 (09-07) 150-504-406 (Rev. 10-01) TOC Table of Contents Introduction...1-4 Phase 1: Preparing the proposed budget...5-26 Phase 2: Approving the

An introductory guide to creating local budgets 150-504-406 (09-07) 150-504-406 (Rev. 10-01) TOC Table of Contents Introduction...1-4 Phase 1: Preparing the proposed budget...5-26 Phase 2: Approving the

Property Tax Rate Adoption: Deadlines, Notices & Hearings

Property Tax Rate Adoption: Deadlines, Notices & Hearings John Kennedy (512) 472-8838 jkennedy@ttara.org www.ttara.org Presented to the TXOGA Property Tax Representatives Annual Conference March 7, 2018

Property Tax Rate Adoption: Deadlines, Notices & Hearings John Kennedy (512) 472-8838 jkennedy@ttara.org www.ttara.org Presented to the TXOGA Property Tax Representatives Annual Conference March 7, 2018

The Revaluation Experience

Appendix 2 The Revaluation Experience 2007-2013 Presented to the Special Commission to Study Property Revaluation October 8 th, 2013 2006 to 2013 Assessments & Tax Bills Sample Properties 2006 2007 2010

Appendix 2 The Revaluation Experience 2007-2013 Presented to the Special Commission to Study Property Revaluation October 8 th, 2013 2006 to 2013 Assessments & Tax Bills Sample Properties 2006 2007 2010

Budget Summary and Budget Hearing

: By Claire Silverman, League Legal Counsel All municipalities must prepare an annual budget. Although time periods vary depending on a municipality s process, the budget process typically commences in

: By Claire Silverman, League Legal Counsel All municipalities must prepare an annual budget. Although time periods vary depending on a municipality s process, the budget process typically commences in

Budget and Property Tax Rate Adoption

Budget and Property Tax Rate Adoption February 2015 Training Leela R. Fireside, Assistant City Attorney, Austin Texas. (contact info: leela.fireside@austintexas.gov or (512) 974-2163) Main Statutes There

Budget and Property Tax Rate Adoption February 2015 Training Leela R. Fireside, Assistant City Attorney, Austin Texas. (contact info: leela.fireside@austintexas.gov or (512) 974-2163) Main Statutes There

2017 Salt Lake County Board of Equalization Administrative Rules

2017 Salt Lake County Board of Equalization Administrative Rules Adopted 18 July 2017 TABLE OF CONTENTS I. GENERAL PROVISIONS... 1 II. AUTHORITY OF THE BOARD OF EQUALIZATION... 1 III. APPLICATIONS FOR

2017 Salt Lake County Board of Equalization Administrative Rules Adopted 18 July 2017 TABLE OF CONTENTS I. GENERAL PROVISIONS... 1 II. AUTHORITY OF THE BOARD OF EQUALIZATION... 1 III. APPLICATIONS FOR

Staff Presentation to the House Finance Committee June 6, 2017

Staff Presentation to the House Finance Committee June 6, 2017 Objective End ability for municipalities to tax motor vehicles over a fixed period of time and reimburse them for the lost tax revenue 2 History

Staff Presentation to the House Finance Committee June 6, 2017 Objective End ability for municipalities to tax motor vehicles over a fixed period of time and reimburse them for the lost tax revenue 2 History

Appealing Your Tax Assessment

Appealing Your Tax Assessment On January 1, 2016 Jackson County implemented the latest real property revaluation assessment as required by North Carolina General Statutes (NCGS) 105-286. The assessment

Appealing Your Tax Assessment On January 1, 2016 Jackson County implemented the latest real property revaluation assessment as required by North Carolina General Statutes (NCGS) 105-286. The assessment

Overview Of Municipal Budgeting From Preparation to Execution

The information provided here is for informational and educational purposes and current as of the date of publication. The information is not a substitute for legal advice. Consult your attorney for advice

The information provided here is for informational and educational purposes and current as of the date of publication. The information is not a substitute for legal advice. Consult your attorney for advice

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-216. Town of Lyons. Real Property Tax Exemptions Administration

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-216 Town of Lyons Real Property Tax Exemptions Administration FEBRUARY 2019 Contents Report Highlights.............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-216 Town of Lyons Real Property Tax Exemptions Administration FEBRUARY 2019 Contents Report Highlights.............................

CHAPTER 3 FINANCE AND TAXATION 3.03 DISPOSAL OF COUNTY-OWNED SURPLUS PERSONAL PROPERTY

CHAPTER 3 FINANCE AND TAXATION 3.01 PROCUREMENT POLICY (3) Compliance (4) Budget Funds (5) Non-Budgeted Funds 3.02 AGREEMENTS (1) Agreements 3.03 DISPOSAL OF COUNTY-OWNED SURPLUS PERSONAL PROPERTY 3.04

CHAPTER 3 FINANCE AND TAXATION 3.01 PROCUREMENT POLICY (3) Compliance (4) Budget Funds (5) Non-Budgeted Funds 3.02 AGREEMENTS (1) Agreements 3.03 DISPOSAL OF COUNTY-OWNED SURPLUS PERSONAL PROPERTY 3.04

Property Taxes and How They Affect Cities. What is Property Tax? 6/4/2018. Really, All I Care About is... How Much Money Can My City Get?

Property Taxes and How They Affect Cities Presented by Wendy Semmler Property Tax Program Manager SD Dept. of Revenue What is Property Tax? Ad valorem tax on all property that has been deemed taxable by

Property Taxes and How They Affect Cities Presented by Wendy Semmler Property Tax Program Manager SD Dept. of Revenue What is Property Tax? Ad valorem tax on all property that has been deemed taxable by

TAX OBJECTION COMPLAINT PACKET

TAX OBJECTION COMPLAINT PACKET TAX OBJECTION COMPLAINT REQUIREMENTS THAT NEED TO BE MET BEFORE A TAX OBJECTION CAN BE FILED. 1. If a person desires to file a he/she shall pay all of the taxes due within

TAX OBJECTION COMPLAINT PACKET TAX OBJECTION COMPLAINT REQUIREMENTS THAT NEED TO BE MET BEFORE A TAX OBJECTION CAN BE FILED. 1. If a person desires to file a he/she shall pay all of the taxes due within

STATE TAX COMMISSION 2018 PROPERTY TAX, COLLECTIONS AND EQUALIZATION CALENDAR

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Equalization Directors and Assessors The State Tax Commission Bulletin No.

5102 (Rev. 04-15) RICK SNYDER GOVERNOR STATE OF MICHIGAN DEPARTMENT OF TREASURY LANSING NICK A. KHOURI STATE TREASURER TO: FROM: Equalization Directors and Assessors The State Tax Commission Bulletin No.

TOWN OF WASCOTT DOUGLAS COUNTY, WISCONSIN FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Year Ended TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT... 1 BASIC FINANCIAL STATEMENTS Statement of Activities and Net Position Modified Cash Basis...

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION Year Ended TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT... 1 BASIC FINANCIAL STATEMENTS Statement of Activities and Net Position Modified Cash Basis...

COMMONWEALTH OF MASSACHUSETTS APPELLATE TAX BOARD. THOMAS E. KNATT v. BOARD OF ASSESSORS OF THE TOWN OF CONCORD

COMMONWEALTH OF MASSACHUSETTS APPELLATE TAX BOARD THOMAS E. KNATT v. BOARD OF ASSESSORS OF THE TOWN OF CONCORD Docket No. F298604 Promulgated: December 30, 2009 This is an appeal filed under the formal

COMMONWEALTH OF MASSACHUSETTS APPELLATE TAX BOARD THOMAS E. KNATT v. BOARD OF ASSESSORS OF THE TOWN OF CONCORD Docket No. F298604 Promulgated: December 30, 2009 This is an appeal filed under the formal

Department of Revenue Analysis of H.F (Lenczewski) / S.F (Bakk) Fund Impact

/ S.F (Bakk) Fund Impact") 0B U Department Technical Bill February 22, 2010 DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2971 (Lenczewski) / S.F. 2696 (Bakk) Fund Impact UF.Y. 2010U UF.Y. 2011U UF.Y. 2012U

0B U Department Technical Bill February 22, 2010 DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2971 (Lenczewski) / S.F. 2696 (Bakk) Fund Impact UF.Y. 2010U UF.Y. 2011U UF.Y. 2012U

Property Tax Hands-on Workshop

Property Tax Hands-on Workshop July 17, 2018 1 Why? 1 Dexter Community Schools 2016-17 Foundation Allowance $7,799 x 3,582.17 students* = $27,937,344** * Blended student counts 10% Feb 2016 and 90% Oct

Property Tax Hands-on Workshop July 17, 2018 1 Why? 1 Dexter Community Schools 2016-17 Foundation Allowance $7,799 x 3,582.17 students* = $27,937,344** * Blended student counts 10% Feb 2016 and 90% Oct

INFORMAL AND FORMAL APPEAL ADMINISTRATIVE POLICY AND PROCEDURES

Board of Assessment Appeals of Tioga County INFORMAL AND FORMAL APPEAL ADMINISTRATIVE POLICY AND PROCEDURES PART I - REASSESSMENT YEAR Periodically, the county will undergo a county-wide equalization reassessment.

Board of Assessment Appeals of Tioga County INFORMAL AND FORMAL APPEAL ADMINISTRATIVE POLICY AND PROCEDURES PART I - REASSESSMENT YEAR Periodically, the county will undergo a county-wide equalization reassessment.

(Effective for taxable years beginning before January 1, 2017) Franchise or privilege tax on domestic and foreign corporations.

Franchise or privilege tax on domestic and foreign corporations.") 105-122. (Effective for taxable years beginning before January 1, 2017) Franchise or privilege tax on domestic and foreign corporations. (a) An annual franchise or privilege tax is imposed on a corporation

105-122. (Effective for taxable years beginning before January 1, 2017) Franchise or privilege tax on domestic and foreign corporations. (a) An annual franchise or privilege tax is imposed on a corporation

General Sales and Use Tax Transfer of Tax on Motor Vehicle Leases Based on 6.5% Rate Instead of 6.875% $3,800 $4,000 $4,200 $4,200 $4,200

February 17, 2015 State Taxes Only Department of Revenue Analysis of S.F. 826 (Skoe) / H.F. 848 (Davids) Governor s Tax Policy Bill DOR Administrative Costs/Savings Fund Impact F.Y. 2015 F.Y. 2016 F.Y.

February 17, 2015 State Taxes Only Department of Revenue Analysis of S.F. 826 (Skoe) / H.F. 848 (Davids) Governor s Tax Policy Bill DOR Administrative Costs/Savings Fund Impact F.Y. 2015 F.Y. 2016 F.Y.

UNDERSTANDING YOUR PROPERTY TAXES. Presentation to Meadville City Council February 20, 2019

UNDERSTANDING YOUR PROPERTY TAXES Presentation to Meadville City Council February 20, 2019 This is your home 2 Your view of your home 3 A buyer s view 4 A lender s view 5 An appraiser s view 6 A tax assessor

UNDERSTANDING YOUR PROPERTY TAXES Presentation to Meadville City Council February 20, 2019 This is your home 2 Your view of your home 3 A buyer s view 4 A lender s view 5 An appraiser s view 6 A tax assessor

Report of Assessed Values And Tax Process for Tax Year 2018 (April 1, March 31, 2019)

") City of Dover New Hampshire Report of Assessed Values And Tax Process for Tax Year 2018 (April 1, 2018 - March 31, 2019) Budget Period Fiscal Year 2019 (July 1, 2018 - June 30, 2019) Prepared By City of

City of Dover New Hampshire Report of Assessed Values And Tax Process for Tax Year 2018 (April 1, 2018 - March 31, 2019) Budget Period Fiscal Year 2019 (July 1, 2018 - June 30, 2019) Prepared By City of

August 2017 Legal Calendar

1 Assessor On or before this date, the assessor must forward approved homestead exemption applications and a copy of the certification of disability status to the Tax Commissioner. 77-3517(1) 1 Assessor

1 Assessor On or before this date, the assessor must forward approved homestead exemption applications and a copy of the certification of disability status to the Tax Commissioner. 77-3517(1) 1 Assessor

FACTS ABOUT MANUFACTURED

FACTS ABOUT MANUFACTURED HOME PROPERTY TAXES LESLIE MORGAN Shasta County Assessor-Recorder Shasta County does not discriminate on the basis of disability. Our ADA Coordinator may be reached at 530-225-5515;

FACTS ABOUT MANUFACTURED HOME PROPERTY TAXES LESLIE MORGAN Shasta County Assessor-Recorder Shasta County does not discriminate on the basis of disability. Our ADA Coordinator may be reached at 530-225-5515;

It s Budget Time! Contents

Introduction In this publication, we have summarized the major changes in state law that effect city/ town budgets. We suggest review of this special report by all persons directly involved in the budget

Introduction In this publication, we have summarized the major changes in state law that effect city/ town budgets. We suggest review of this special report by all persons directly involved in the budget

Title 36: TAXATION. Chapter 101: GENERAL PROVISIONS. Table of Contents Part 2. PROPERTY TAXES...

Title 36: TAXATION Chapter 101: GENERAL PROVISIONS Table of Contents Part 2. PROPERTY TAXES... Subchapter 1. POWERS AND DUTIES OF STATE TAX ASSESSOR... 3 Section 201. SUPERVISION AND ADMINISTRATION...

Title 36: TAXATION Chapter 101: GENERAL PROVISIONS Table of Contents Part 2. PROPERTY TAXES... Subchapter 1. POWERS AND DUTIES OF STATE TAX ASSESSOR... 3 Section 201. SUPERVISION AND ADMINISTRATION...

Truth-in-Taxation Instructions for Payable 2019

Truth-in-Taxation Instructions for Payable 2019 Key Points Public meetings must take place at 6:00 p.m. or later Certification of Compliance must be submitted on or before Dec. 28, 2018 Questions? Please

Truth-in-Taxation Instructions for Payable 2019 Key Points Public meetings must take place at 6:00 p.m. or later Certification of Compliance must be submitted on or before Dec. 28, 2018 Questions? Please

County Budget Form Instruction Manual

Auditor of Public Accounts County Budget Form Instruction Manual This Manual is provided to assist Nebraska counties in preparing/ completing their Budget Forms in compliance with State Statutes. The information

Auditor of Public Accounts County Budget Form Instruction Manual This Manual is provided to assist Nebraska counties in preparing/ completing their Budget Forms in compliance with State Statutes. The information

ARIZONA TAX: CURRENT ISSUES, 2006 AND 2007 LEGISLATION AND CASE LAW

ARIZONA TAX: CURRENT ISSUES, 2006 AND 2007 LEGISLATION AND CASE LAW 2006 LEGISLATION By: Pat Derdenger, Partner Steptoe & Johnson LLP 201 East Washington Street, 16 th Floor Phoenix, Arizona 85004-2382

ARIZONA TAX: CURRENT ISSUES, 2006 AND 2007 LEGISLATION AND CASE LAW 2006 LEGISLATION By: Pat Derdenger, Partner Steptoe & Johnson LLP 201 East Washington Street, 16 th Floor Phoenix, Arizona 85004-2382

RESOLUTION NUMBER 3305

RESOLUTION NUMBER 3305 RESOLUTION OF INTENTION OF THE CITY COUNCIL OF THE CITY OF PERRIS TO ESTABLISH COMMUNITY FACILITIES DISTRICT NO. 2004-5 (AMBER OAKS II) OF THE CITY OF PERRIS AND TO AUTHORIZE THE

RESOLUTION NUMBER 3305 RESOLUTION OF INTENTION OF THE CITY COUNCIL OF THE CITY OF PERRIS TO ESTABLISH COMMUNITY FACILITIES DISTRICT NO. 2004-5 (AMBER OAKS II) OF THE CITY OF PERRIS AND TO AUTHORIZE THE

School District of Milton Board of Education

School District of Milton Board of Education Financing a Facility Referendum Lisa Voisin, Managing Director 414-765-3801 lvoisin@rwbaird.com Robert W. Baird & Co. Incorporated ( Baird ) is not recommending

School District of Milton Board of Education Financing a Facility Referendum Lisa Voisin, Managing Director 414-765-3801 lvoisin@rwbaird.com Robert W. Baird & Co. Incorporated ( Baird ) is not recommending

Property Taxes: Revenue Impact and Taxable Value Updates. MSBO Annual Conference April 19, 2018

Property Taxes: Revenue Impact and Taxable Value Updates MSBO Annual Conference April 19, 2018 1 State Aid Formula State Revenue = Foundation Allowance X Pupil Membership Local Revenue 2 State Aid Formula

Property Taxes: Revenue Impact and Taxable Value Updates MSBO Annual Conference April 19, 2018 1 State Aid Formula State Revenue = Foundation Allowance X Pupil Membership Local Revenue 2 State Aid Formula

Wisconsin Budget Toolkit

Wisconsin Budget Toolkit INTRODUCTION Updated January 2016 Countless times a day, you are affected by state budget decisions. When you turn on the water, send your child to school, turn on a light, or

Wisconsin Budget Toolkit INTRODUCTION Updated January 2016 Countless times a day, you are affected by state budget decisions. When you turn on the water, send your child to school, turn on a light, or

It s Budget Time! Contents

Introduction In this publication, we have summarized the major changes in state law that affects city/ town budgets. We suggest review of this special report by all persons directly involved in the budget

Introduction In this publication, we have summarized the major changes in state law that affects city/ town budgets. We suggest review of this special report by all persons directly involved in the budget

2017 Effective Tax Rate Worksheet DUMAS CITY

Page 1 of 14 2017 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2016 total taxable value. Enter the amount of 2016 taxable value on the 2016 tax roll

Page 1 of 14 2017 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2016 total taxable value. Enter the amount of 2016 taxable value on the 2016 tax roll

To establish a policy that guides City assessment review activities to help ensure stability and accuracy of the assessment base.

EFFECTIVE: June 1, 2007 REPLACES: new PAGE: 1 of 13 POLICY STATEMENT: To establish a policy that guides City assessment review activities to help ensure stability and accuracy of the assessment base. PURPOSE:

EFFECTIVE: June 1, 2007 REPLACES: new PAGE: 1 of 13 POLICY STATEMENT: To establish a policy that guides City assessment review activities to help ensure stability and accuracy of the assessment base. PURPOSE:

Tax Computation Manual

Tax Computation Manual 2010 Published by Property Tax Division 150-800-438 (Rev. 10-10) Table of Contents Introduction...ii Key Dates...iii Property Tax Computation Flowchart...iv Chapter 1 Certification

Tax Computation Manual 2010 Published by Property Tax Division 150-800-438 (Rev. 10-10) Table of Contents Introduction...ii Key Dates...iii Property Tax Computation Flowchart...iv Chapter 1 Certification

06.07 ALTERNATE METHODS OF TAXATION

06.07 ALTERNATE METHODS OF TAXATION Overview There are methods of property taxation that differ from the normal calculations described elsewhere in this manual. This section provides an overview of three

06.07 ALTERNATE METHODS OF TAXATION Overview There are methods of property taxation that differ from the normal calculations described elsewhere in this manual. This section provides an overview of three

Revenue Gain or (Loss) F.Y F.Y F.Y F.Y (000 s) General Fund $0 $0 $0 $0

F.Y F.Y F.Y F.Y (000 s) General Fund $0 $0 $0 $0") Department Technical Bill February 27, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No Department of Revenue Analysis of H.F. 2300 (Abrams) Revenue Gain

Department Technical Bill February 27, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No Department of Revenue Analysis of H.F. 2300 (Abrams) Revenue Gain

FUNDAMENTALS OF MUNICIPAL REVENUE PROPERTY TAX BASICS. August 22, 2017 WHAT IS TAXED? WHO DOES THE WORK? WHAT IS THE TIMING?

FUNDAMENTALS OF MUNICIPAL REVENUE PROPERTY TAX BASICS August 22, 2017 WHAT IS TAXED? WHO DOES THE WORK? WHAT IS THE TIMING? 2 PROPERTY TAX BASICS THE PROCESS WHAT, WHO, AND WHEN 3 Proposition 13 California

FUNDAMENTALS OF MUNICIPAL REVENUE PROPERTY TAX BASICS August 22, 2017 WHAT IS TAXED? WHO DOES THE WORK? WHAT IS THE TIMING? 2 PROPERTY TAX BASICS THE PROCESS WHAT, WHO, AND WHEN 3 Proposition 13 California

Town of Cross Plains, Wisconsin Accounting Procedures

Town of Cross Plains, Wisconsin Accounting Procedures Introduction The Board is responsible for establishing policies and procedures that govern the financial practices to be followed by the Town Clerk,

Town of Cross Plains, Wisconsin Accounting Procedures Introduction The Board is responsible for establishing policies and procedures that govern the financial practices to be followed by the Town Clerk,

HUTCHINSON CITY COUNCIL POLICY - 10

HUTCHINSON CITY COUNCIL POLICY - 10 SUBJECT: TAX EXEMPTIONS FOR ECONOMIC DEVELOPMENT DATE: First Approved: October 1, 1991 Amended: January 19, 1993 Amended: March 16, 1993 Amended: January 18, 1994 Amended:

HUTCHINSON CITY COUNCIL POLICY - 10 SUBJECT: TAX EXEMPTIONS FOR ECONOMIC DEVELOPMENT DATE: First Approved: October 1, 1991 Amended: January 19, 1993 Amended: March 16, 1993 Amended: January 18, 1994 Amended:

Property Tax System Overview. Prepared for the Property Tax Working Group

Property Tax System Overview Prepared for the Property Tax Working Group Property Tax Research 9/27/2010 Introduction Property tax in Minnesota is an ad valorem tax. This means that property is taxed

Property Tax System Overview Prepared for the Property Tax Working Group Property Tax Research 9/27/2010 Introduction Property tax in Minnesota is an ad valorem tax. This means that property is taxed

Cost Benefit Analysis Worksheets Key (Pages 1,2 and 3 of Worksheet)

") City Worksheet Cost Benefit Analysis Worksheets Key (Pages 1,2 and 3 of Worksheet) The firm s expansion might not be located in any city, and therefore would not be eligible for a city s tax abatement.

City Worksheet Cost Benefit Analysis Worksheets Key (Pages 1,2 and 3 of Worksheet) The firm s expansion might not be located in any city, and therefore would not be eligible for a city s tax abatement.

S T A T E O F M I C H I G A N BOARD OF COMMISSIONERS OF THE COUNTY OF ALLEGAN. WHEREAS, the Board of Commissioners of the County of

S T A T E O F M I C H I G A N BOARD OF COMMISSIONERS OF THE COUNTY OF ALLEGAN 2017 MILLAGE LEVY SET COUNTY MILLAGE RATES WHEREAS, the Board of Commissioners of the County of Allegan has held a public hearing

S T A T E O F M I C H I G A N BOARD OF COMMISSIONERS OF THE COUNTY OF ALLEGAN 2017 MILLAGE LEVY SET COUNTY MILLAGE RATES WHEREAS, the Board of Commissioners of the County of Allegan has held a public hearing

Department of Revenue Analysis of H.F (Abrams)/ S.F (Moua) As Proposed to be Amended. General Fund $0 $0 $0 $0

/ S.F (Moua) As Proposed to be Amended. General Fund $0 $0 $0 $0") Department Policy Bill March 15, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2552 (Abrams)/ S.F. 2716 (Moua) As Proposed

Department Policy Bill March 15, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2552 (Abrams)/ S.F. 2716 (Moua) As Proposed

Understanding the Budget Process

Office of the New York State Comptroller Division of Local Government and School Accountability LOCAL GOVERNMENT MANAGEMENT GUIDE Understanding the Budget Process Thomas P. DiNapoli State Comptroller Table

Office of the New York State Comptroller Division of Local Government and School Accountability LOCAL GOVERNMENT MANAGEMENT GUIDE Understanding the Budget Process Thomas P. DiNapoli State Comptroller Table

ORDINANCE NO WHEREAS, on September 14, 2004, the Board of Supervisors (the Board of

ORDINANCE NO. 834 AN ORDINANCE OF THE BOARD OF SUPERVISORS OF RIVERSIDE COUNTY, CALIFORNIA AUTHORIZING THE LEVY OF SPECIAL TAXES IN COMMUNITY FACILITIES DISTRICT NO. 04-2 (LAKE HILLS CREST) OF THE COUNTY

ORDINANCE NO. 834 AN ORDINANCE OF THE BOARD OF SUPERVISORS OF RIVERSIDE COUNTY, CALIFORNIA AUTHORIZING THE LEVY OF SPECIAL TAXES IN COMMUNITY FACILITIES DISTRICT NO. 04-2 (LAKE HILLS CREST) OF THE COUNTY

BUDGET PREPARATION CALENDAR FY Date Activity Participants

2006 2007 October 1- Update CIE/Tax Requirements and calculate December 1 adjusted budget Department/Divisions January 10 Budget Advisory Committee Meeting Public January 12 SWA Disposal Fee budget estimates

2006 2007 October 1- Update CIE/Tax Requirements and calculate December 1 adjusted budget Department/Divisions January 10 Budget Advisory Committee Meeting Public January 12 SWA Disposal Fee budget estimates

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-210. Town of Milo. Real Property Tax Exemptions Administration

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-210 Town of Milo Real Property Tax Exemptions Administration JANUARY 2019 Contents Report Highlights............................

DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY REPORT OF EXAMINATION 2018M-210 Town of Milo Real Property Tax Exemptions Administration JANUARY 2019 Contents Report Highlights............................

A GUIDE TO PROPERTY TAXES

2018 A GUIDE TO PROPERTY TAXES CITY OF YELLOWKNIFE 1. What property taxes are used for The City of Yellowknife will raise 76% of all 2017 operating revenue through property taxation. As well, Yellowknife

2018 A GUIDE TO PROPERTY TAXES CITY OF YELLOWKNIFE 1. What property taxes are used for The City of Yellowknife will raise 76% of all 2017 operating revenue through property taxation. As well, Yellowknife

Richland School District

Richland School District April 5, 2016 Referendum Ballot and Cost Impact Presentation Presented by: Carol Wirth, President 1020 N. Broadway, Suite G-9 Milwaukee, WI 53202 Phone 414/434-9644 Question 1

Richland School District April 5, 2016 Referendum Ballot and Cost Impact Presentation Presented by: Carol Wirth, President 1020 N. Broadway, Suite G-9 Milwaukee, WI 53202 Phone 414/434-9644 Question 1

The Board of Supervisors of the County of Riverside ordains as follows:

ORDINANCE NO. 936 AN ORDINANCE OF THE COUNTY OF RIVERSIDE AUTHORIZING THE LEVY OF A SPECIAL TAX WITHIN COMMUNITY FACILITIES DISTRICT NO. 17-2M (BELLA VISTA II) OF THE COUNTY OF RIVERSIDE The Board of Supervisors

ORDINANCE NO. 936 AN ORDINANCE OF THE COUNTY OF RIVERSIDE AUTHORIZING THE LEVY OF A SPECIAL TAX WITHIN COMMUNITY FACILITIES DISTRICT NO. 17-2M (BELLA VISTA II) OF THE COUNTY OF RIVERSIDE The Board of Supervisors

SENATE AMENDMENTS TO A-ENGROSSED HOUSE BILL 4028

th OREGON LEGISLATIVE ASSEMBLY-- Regular Session SENATE AMENDMENTS TO A-ENGROSSED HOUSE BILL 0 By COMMITTEE ON FINANCE AND REVENUE March 1 1 1 1 1 On page 1 of the printed A-engrossed bill, line, after

th OREGON LEGISLATIVE ASSEMBLY-- Regular Session SENATE AMENDMENTS TO A-ENGROSSED HOUSE BILL 0 By COMMITTEE ON FINANCE AND REVENUE March 1 1 1 1 1 On page 1 of the printed A-engrossed bill, line, after

COMMONWEALTH OF MASSACHUSETTS APPELLATE TAX BOARD. DIANE MARIE PAGANO v. BOARD OF ASSESSORS OF THE TOWN OF SWAMPSCOTT

COMMONWEALTH OF MASSACHUSETTS APPELLATE TAX BOARD DIANE MARIE PAGANO v. BOARD OF ASSESSORS OF THE TOWN OF SWAMPSCOTT Docket No. F309859 Promulgated: February 7, 2012 This is an appeal originally filed

COMMONWEALTH OF MASSACHUSETTS APPELLATE TAX BOARD DIANE MARIE PAGANO v. BOARD OF ASSESSORS OF THE TOWN OF SWAMPSCOTT Docket No. F309859 Promulgated: February 7, 2012 This is an appeal originally filed

TOWN OF LINN ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2009

TOWN OF LINN ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2009 TOWN OF LINN TABLE OF CONTENTS For the Year Ended December 31, 2009 Page Independent Auditor s Report 1-2 Basic Financial Statements:

TOWN OF LINN ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2009 TOWN OF LINN TABLE OF CONTENTS For the Year Ended December 31, 2009 Page Independent Auditor s Report 1-2 Basic Financial Statements:

2007 Effective Tax Rate Worksheet Neverland County - General

Page 1 of 12 2007 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2006 total taxable value. Enter the amount of 2006 taxable value on the 2006 tax roll

Page 1 of 12 2007 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2006 total taxable value. Enter the amount of 2006 taxable value on the 2006 tax roll

Cory Plager, Financial Services Director NorthEast Washington ESD

Cory Plager, Financial Services Director NorthEast Washington ESD 101 cplager@esd101.net 509.789.3564 Dave Loomer, Levy Specialist Spokane County dloomer@spokanecounty.org 509.477.5914 Jon Gores, Managing

Cory Plager, Financial Services Director NorthEast Washington ESD 101 cplager@esd101.net 509.789.3564 Dave Loomer, Levy Specialist Spokane County dloomer@spokanecounty.org 509.477.5914 Jon Gores, Managing

CHAPTER 3 FINANCE AND TAXATION 3.03 DISPOSAL OF COUNTY-OWNED SURPLUS PERSONAL PROPERTY

CHAPTER 3 FINANCE AND TAXATION 3.01 PURCHASING POLICY (1) Public Works Bidding (2) Agreements 3.02 PURCHASING AGENT (1) Supplies, Equipment and Purchases of Services (2) Capital Outlay Items 3.03 DISPOSAL

CHAPTER 3 FINANCE AND TAXATION 3.01 PURCHASING POLICY (1) Public Works Bidding (2) Agreements 3.02 PURCHASING AGENT (1) Supplies, Equipment and Purchases of Services (2) Capital Outlay Items 3.03 DISPOSAL

BUDGET CONTENTS - FUNDS

BUDGET CONTENTS - FUNDS Open page - USD Information - DO FIRST C033-Cost of Living C01-Certificate C034-Vocational Education C02-Levy Limits for Tax Funds C035-Gifts/Grants C04-Worksheet 1 C042-Special

BUDGET CONTENTS - FUNDS Open page - USD Information - DO FIRST C033-Cost of Living C01-Certificate C034-Vocational Education C02-Levy Limits for Tax Funds C035-Gifts/Grants C04-Worksheet 1 C042-Special

Alliance Management Group. Tax Year 2012 Update

Alliance Management Group Tax Year 2012 Update Part I: Overview How is Your Real Property Valued? The Assessor is mandated by Arizona State Statute to value property at its Full Cash (Market) Value. Full

Alliance Management Group Tax Year 2012 Update Part I: Overview How is Your Real Property Valued? The Assessor is mandated by Arizona State Statute to value property at its Full Cash (Market) Value. Full

BUDGET CONTENTS - FUNDS

BUDGET CONTENTS - FUNDS Open page - USD Information - DO FIRST C033-Cost of Living C01-Certificate C034-Vocational Education C02-Levy Limits for Tax Funds C035-Gifts/Grants C04-Worksheet 1 C042-Special

BUDGET CONTENTS - FUNDS Open page - USD Information - DO FIRST C033-Cost of Living C01-Certificate C034-Vocational Education C02-Levy Limits for Tax Funds C035-Gifts/Grants C04-Worksheet 1 C042-Special

INFORMATION FOR THE MIDDLEBOROUGH TAXPAYER

INFORMATION FOR THE MIDDLEBOROUGH TAXPAYER The Board of Assessors Anthony Freitas, Chairman Paula Burdick Frederick Eayrs and Barbara Erickson, M.A.A. Assessor/Appraiser Town of Middleborough Assessors

INFORMATION FOR THE MIDDLEBOROUGH TAXPAYER The Board of Assessors Anthony Freitas, Chairman Paula Burdick Frederick Eayrs and Barbara Erickson, M.A.A. Assessor/Appraiser Town of Middleborough Assessors

BUDGET CONTENTS - FUNDS

BUDGET CONTENTS - FUNDS Open page - USD Information - DO FIRST C033-Cost of Living C01-Certificate C034-Vocational Education C02-Levy Limits for Tax Funds C035-Gifts/Grants C04-Worksheet 1 C042-Special

BUDGET CONTENTS - FUNDS Open page - USD Information - DO FIRST C033-Cost of Living C01-Certificate C034-Vocational Education C02-Levy Limits for Tax Funds C035-Gifts/Grants C04-Worksheet 1 C042-Special

A SHORT AND SIMPLE GLIMPSE AT THE PROPERTY TAX IN NEW JERSEY

A SHORT AND SIMPLE GLIMPSE AT THE PROPERTY TAX IN NEW JERSEY Look at this bill. How come my property taxes are so high? In order to answer that question, you need to consider all the factors that go into

A SHORT AND SIMPLE GLIMPSE AT THE PROPERTY TAX IN NEW JERSEY Look at this bill. How come my property taxes are so high? In order to answer that question, you need to consider all the factors that go into

WISCONSIN INDIANHEAD TECHNICAL COLLEGE

WISCONSIN INDIANHEAD TECHNICAL COLLEGE Annual Audited Financial Statements for fiscal year ended June 30, 2012 Wisconsin Indianhead Technical College District Shell Lake, WI Financial Statements With

WISCONSIN INDIANHEAD TECHNICAL COLLEGE Annual Audited Financial Statements for fiscal year ended June 30, 2012 Wisconsin Indianhead Technical College District Shell Lake, WI Financial Statements With

Georgia Department of Revenue. February 19, 2018 Local Government Services

February 19, 2018 Local Government Services 1 2018 DIGEST SUBMISSION Due on or before September 4 (Tuesday) 2 The Tax Digest is a listing of assessments and exemptions Real and Personal Property Timber

February 19, 2018 Local Government Services 1 2018 DIGEST SUBMISSION Due on or before September 4 (Tuesday) 2 The Tax Digest is a listing of assessments and exemptions Real and Personal Property Timber

TOWN OF LINN ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2008

TOWN OF LINN ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2008 TOWN OF LINN TABLE OF CONTENTS For the Year Ended December 31, 2008 Page Independent Auditor s Report 1-2 Basic Financial Statements:

TOWN OF LINN ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED DECEMBER 31, 2008 TOWN OF LINN TABLE OF CONTENTS For the Year Ended December 31, 2008 Page Independent Auditor s Report 1-2 Basic Financial Statements:

Cook County Property Tax Appeals. Patricia Smolin Business Reference Librarian Mount Prospect Public Library June, 2013

Cook County Property Tax Appeals Patricia Smolin Business Reference Librarian Mount Prospect Public Library June, 2013 Sources Cook County Assessor http://www.cookcountyassessor.com/ Cook County Treasurer

Cook County Property Tax Appeals Patricia Smolin Business Reference Librarian Mount Prospect Public Library June, 2013 Sources Cook County Assessor http://www.cookcountyassessor.com/ Cook County Treasurer

Debt Service Management

Debt Service Management WASBO Fall Conference October 4, 2013 11:15 AM 12:15 PM Presenters Lisa M. Voisin, Director 414-765-3801 lvoisin@rwbaird.com Michel D. Clark, Director 414-765-7326 mdclark@rwbaird.com

Debt Service Management WASBO Fall Conference October 4, 2013 11:15 AM 12:15 PM Presenters Lisa M. Voisin, Director 414-765-3801 lvoisin@rwbaird.com Michel D. Clark, Director 414-765-7326 mdclark@rwbaird.com

Property Taxes. Property Taxes. Property Taxes: From Levy Certification to Individual Tax Statement

: From Levy Certification to Individual Tax Statement Shelby McQuay Ehlers Andrea Uhl Ehlers May 11, 2017 1 Overview District officials are sometimes expected to explain property taxes in detail: At school

: From Levy Certification to Individual Tax Statement Shelby McQuay Ehlers Andrea Uhl Ehlers May 11, 2017 1 Overview District officials are sometimes expected to explain property taxes in detail: At school

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE This Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the City of St. Augustine. The manual is an in depth

FY 2018 Revenue Manual CITY OF ST. AUGUSTINE This Revenue Manual was developed to provide a comprehensive reference source for all revenue collected by the City of St. Augustine. The manual is an in depth

PROPERTY ASSESSMENT AND TAXATION

AUTHORITY The City and Borough of Juneau s authorization to levy a property tax is provided under Alaska State Statute Section 29.45. Under this section, the State requires the Assessor to assess property

AUTHORITY The City and Borough of Juneau s authorization to levy a property tax is provided under Alaska State Statute Section 29.45. Under this section, the State requires the Assessor to assess property

CAROLE KEETON STRAYHORN,

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

B Y-LAW NO Being a by-law to establish municipal and education tax rates for the year 2015.

THE CORPORATION OF THE CITY OF ELLIOT LAKE B Y-LAW NO. 15-12 Being a by-law to establish municipal and education tax rates for the year 2015. The Council of The Corporation of the City of Elliot Lake ENACTS

THE CORPORATION OF THE CITY OF ELLIOT LAKE B Y-LAW NO. 15-12 Being a by-law to establish municipal and education tax rates for the year 2015. The Council of The Corporation of the City of Elliot Lake ENACTS

Regional School District Budget Process and Financial Procedures

Regional School District Budget Process and Financial Procedures Presentation to Association of Town Finance Committees October 23, 2010 Christine M. Lynch, DESE 1 Regional School District Stats Membership

Regional School District Budget Process and Financial Procedures Presentation to Association of Town Finance Committees October 23, 2010 Christine M. Lynch, DESE 1 Regional School District Stats Membership

Duties of Department of Revenue. NC General Statutes - Chapter 105 Article 15 1

Article 15. Duties of Department and Property Tax Commission as to Assessments. 105-288. Property Tax Commission. (a) Creation and Membership. The Property Tax Commission is created. It consists of five

Article 15. Duties of Department and Property Tax Commission as to Assessments. 105-288. Property Tax Commission. (a) Creation and Membership. The Property Tax Commission is created. It consists of five