Reporting the Like-Kind Exchange of Real Estate Using IRS Form 8824

|

|

|

- Wesley Bailey

- 5 years ago

- Views:

Transcription

1 Compliments of Realty Exchange Corporation Your Nationwide Qualified Intermediary for the Tax Deferred Exchange of Real Estate 4500 Martinwood Drive, Haymarket, VA Local: (703) Fax: Reporting the Like-Kind Exchange of Real Estate Using IRS Form 8824 January 2005 Edition This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is presented with the understanding that the publisher is not engaged in rendering legal or accounting service. If legal or other assistance is required, the services of a competent professional should be sought. From a Declaration of Principals jointly adopted by a Committee of the American Bar Association and a Committee of Publishers and Associations. 1994, 2005 Ed Horan, CES, Haymarket, VA. ed@1031.us

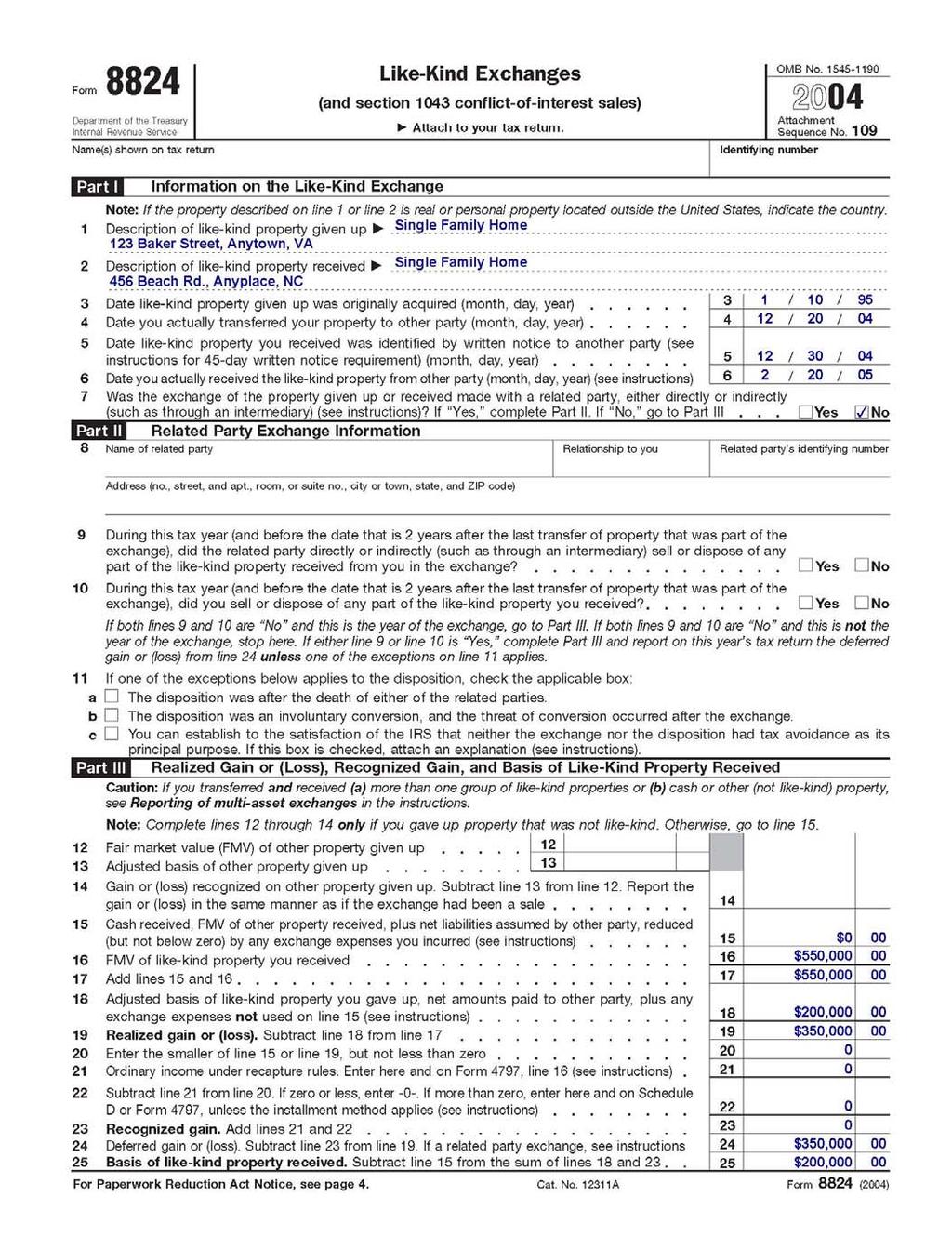

2 1. WHEN DO WE REPORT THE ECHANGE TO THE IRS? The exchange is reported to the IRS for the tax year in which the first relinquished property is transferred. Regardless of the fact that the replacement property(ies) are transferred in the following tax year. Example: Exchangor settles on relinquished property on Dec. 15, and then settles on replacement property May 1, Exchangor would file Form 8824 with 2004 return, after filing an on time request for an extension. 2. HOW DO WE REPORT THE ECHANGE? The Exchange is reported on IRS Form 8824, Like-Kind Exchanges. The Form 8824 is divided into three parts: Part I. Information on the Like-Kind Exchange. Part II. Related Party Exchange Information, and Part III. Realized Gain or (Loss), Recognized Gain, and Basis of Like-Kind Property Received If the exchangor has recognized gain, in addition to Form 8824, the exchangor may need to report the gain on IRS Form 4797, Sales of Business Property, Schedule D (Form 1040), Capital Gains and Losses, and/or Form 6252, Installment Sale Income. See paragraph 6 below. 3. COMPLETING PART I INFORMATION ON THE LIKE-KIND ECHANGE. For lines 1 and 2 in Part I the exchangor should show for real property the address, and type of property. For personal property a short description should be entered. All property involved in each exchange is included on the single Form Include an attachment if additional space is required. Line 5 is normally the date the qualified intermediary was provided the identification of the replacement property. In the event the replacement property is settled prior to the 45th day, then separate identification is not required, and the transfer date for the replacement property may be shown on Line 5. If you made more then one like-kind exchange in the same year - (a) you may report each exchange on a separate Form 8824, or (b) you may file only one summary Form 8824 and attach your own statement showing all the information requested on Form 8824 for each exchange. Include your name and tax ID number at the top of each page of the statement. On the summary Form 8824, enter only your name and tax ID number, then the word Summary on Line 1, the total recognized gain from all exchanges on Line 23, and the total basis of all like-kind property received on Line COMPLETING PART II RELATED PARTY ECHANGE INFORMATION. Part II is only completed when either the relinquished property was transferred to a related party and/or the replacement property was purchased from a related party, directly or indirectly. A related party includes the exchangor s spouse, child, grandchild, parent, grand parent, brother or sister, or a related corporation, S corporation, partnership, or trust in which the exchangor has over a 1

3 50% interest. See IRC Section 1031(f). If the exchange is made with a related party then you must also file Form 8824 for the 2 years following the year of exchange. See specific IRS Instructions for Line COMPLETING PART III REALIZED AND RECOGNIZED GAIN, and BASIS OF NEW PROPERTY. Part III is the most important and most difficult part of the form to complete. Part III provides for the reporting of: a. Ordinary gain (or loss) on other property (i.e. non-like property) given up (see lines 12, 13, and 14) b. Ordinary income under the recapture rules (see lines 21 and 22, and Instructions). Do not confuse with recapture of Section 1250 depreciation. There is no recapture if depreciable real property is exchanged for other depreciable real property. If depreciable real property is exchanged for non-depreciable real property (ex: rental house for land) then the total depreciation taken in excess of straight line could be recaptured. If the value of depreciable property received in the exchange (ex: improvements to the land) exceeds the amount of additional or excess depreciation, then no depreciation will be recaptured. Few properties exist today that have excess depreciation. c. Multi-Asset Exchanges. Note that Multi-Asset exchanges are covered in detail in Section (j)-1 of the regulations. An exchange is only reported as a multi-asset exchange if the exchangor transferred AND received more than one group of like-kind properties, or cash or other non-like property. Few real estate exchanges are multi-asset exchanges. d. Realized Gain, Recognized Gain and Basis of Like-Kind Property Received. This is the primary purpose of Part III and Form To complete Part III starting on Line 15 requires the use of the Worksheet enclosed. EAMPLE: To show the use of the Worksheet we will use the following example of an exchange transaction. In this example the exchangor will buy up in value and reinvest all the cash proceeds received. This situation best demonstrates the vast majority of completed exchanges. 1. Basis. The cost basis in the property being relinquished (with improvements) is $150,000, and $45,000 has been taken in depreciation over a ten year period. 2. Relinquished Property. The relinquished property contract price is $500,000 and the current debt to be paid off at settlement is $90,000. The exchangor had $40,000 in exchange expenses and the $370,000 in proceeds (exchange escrow funds) were placed in a qualified escrow account by the Qualified Intermediary. 3. Replacement Property. The replacement property was purchased for $550,000 and a new loan was obtained for $180,000. The cash down payment was $370,000 and exchange expenses were $5,000. 2

4 The Worksheet is broken down into four steps as follows: STEP 1 IT IS IMPORTANT TO READ EACH NOTE!! Gain Realized from Property Relinquished. The first step is to determine the amount of total capital gain that is being realized. 1. FMV of Relinquished Property (Note 1) $500,000 Note 1: FMV is normally contract price 2. Less: Adjusted Basis 2a. Cost (with improvements) $150,000 2b. Less: Depreciation - 45, , Less: Total Exchange Expenses (Note 2) Note 2: Exchange expenses include allowable selling expenses for the relinquished property and the acquisition cost of replacement properties. 3a. Relinquished Property $40,000 3b. Replacement Property +5,000-45, Equals Realized Gain $350,000 Line 4 is posted to Line 19 on Form 8824 STEP 2 Determining Recognized Gain. This is the most important step in the process as it establishes how much of the Capital Gain realized will in fact be recognized and become taxable income. Line 15 at the end of Step 2 reflects the taxable Boot and is transferred to Line 15 on Form 8824 the boot line 5. Relief of Debt on relinquished property $ 90, Less: Debt acquired on replacement property 180, Equals Net relief of Liabilities [Not less then 0] -0- These 3 lines determine if there is any mortgage boot. If debt acquired is less then debt relief mortgage boot results. Answer may not be less then zero because excess mortgage cannot offset cash boot. 3

5 WORKSHEET TO COMPLETE Part III of IRS LIKE-KIND ECHANGE FORM 8824 (Bold line numbers on the right refer to Form 8824) Line 0n STEP 1. Gain Realized from Property Relinquished Form FMV of Relinquished Property (Note 1) $ 500, less: Adjusted Basis 2a. Cost (with improvements) $ 150,000 2b. less: Depreciation Allowed 45, , less: Total Exchange Expenses (Note 2) 3a. Relinquished Property $ 40,000 3b. Replacement Property + 5,000 45, Equals Realized Gain $ 350,000 (Line 19) STEP 2. Recognized Gain 5. Relief of debt on relinquished property $ 90, less: Debt acquired on replacement property 180, Equals Net relief of liabilities (Not less then 0) $ 0 8. plus: Cash (Down Payment) received (Note 3 ) + 410, less: Cash paid (Down payment) (Note 4) 370, less: Total Exchange Expenses - (from Line 3) 45, less: FMV of other property relinquished Equals total Boot received (Not less then 0) $ plus: FMV of other property, cash & Notes received Equals total NET boot received (Lines ) $ Recognized Gain (Taxable income) (the smaller of Line 4 or 14 above) $ 0 (Line 15) STEP 3. Realized Gain Deferred 16. Realized Gain (Line 4) $ 350, less: Recognized Gain (taxable income - Line 15 above) Equals Realized Gain Deferred $ 350,000 (Line 24) STEP 4. Basis of New Property 19. FMV of Replacement Property (Note 1) $ 550,000 (Line 16) 20. less: Realized Gain Deferred (Line 18 above) 350, Equals Total Basis is New Property(ies) $ 200,000 (Lines 25 & 18) NOTES: (1) FMV is normally contract price. (2) Exchange expenses are allowable selling expenses for the relinquished property and the acquisition cost of replacement properties. For the replacement property do not include loan costs or prepaids as exchange expenses. (3) FMV of relinquished property (Line 1) less debt relief (Line 5) less FMV of other property received, including value of owner held Notes (Line 13) should equal cash received. (4) Cash down payment is normally the difference between contract price and loan amount, less any seller non-closing cost credits/allowances. 4

6 8. Plus: Cash down payment received (Note 3) +410,000 Note 3: FMV of relinquished property (line 1) less debt relief (line 5) less FMV of other property received, including value of owner held Notes (Line 13) should equal cash received. 9. Less: Cash paid (down payment) (Note 4) 370,000 Note 4: Cash down payment is normally the difference between replacement property contract price and loan amount, less any seller non-closing cost credits/allowances 10. Less: Total Exchange Expenses (from Line 3 above) 45, Less: FMV of other property relinquished -0- Other property is non-like property, such as personal property 12. Equals total boot received (Not less then 0) $ Plus: FMV of other property, cash & Notes received If a Note is received and made payable to the exchangor it will be treated in accordance with installment sale rules. 14. Equals total NET boot received (Lines ) $ Recognized Gain (Taxable Income) [the smaller of Line 4 or 14 above] $ -0- Line 15 is posted to Line 15 on IRS Form 8824 STEP 3 Realized Gain Deferred. This step determines how much of the realized gain will be deferred. 16. Realized Gain (from Line 4 above) $350, Less: Recognized Gain (Taxable Income) (Line 15) 0 _ 18. Equals Realized Gain deferred $ 350,000 Line 18 is posted to Line 24 on IRS Form

7 6

8 STEP 4 Basis of New Property. This step determines what the basis will be in the new properties. From this basis is subtracted the proportionate value of the land. The balance is the value of the improvements for depreciation purposes. See paragraph 7 below for the revised rules on depreciation of the replacement property. 19. FMV of Replacement Property $550,000 Line 19 is posted to Line 16 on IRS Form Less: Realized Gain Deferred (from Line 18 above) 350, Equals Total Basis in New Property(ies) $ 200,000 Line 21 is posted to both Lines 18 and 25 on IRS Form 8824 Completion of IRS Form With the lines posted from the Worksheet the remaining open lines in Part III can then be calculated. (see also IRS Instructions for Form 8824). Visit IRS web site and search for Form Select current Form 8824 Fill-in Form. You can type your information in and print out a final copy. 6. ADDITIONAL FORMS MAY BE REQUIRED. Once Form 8824 is completed then any additional forms required may be completed. If Line 22, Form 8824 is zero congratulations no additional forms are required. a. Form 4797, Sales of Business Property. Use Form 4797 to report the exchange of property used in your trade or business or held for production of rents. In the unlikely event you have gain on Line 21 on Form 8824 to be recaptured as ordinary income it will be shown on Line 16, Form From Line 22 on Form 8824, transfer the remaining realized gain (that portion not being reported as an installment sale) to Line 5 on Form For individual taxpayers this gain will be combined with other gains or losses and posted to Line 11, Schedule D, Form b. Schedule D, Form 1040, Capital Gains & Losses. For investment property not reported on Form 4797 transfer Line 22, Form 8824 (except installment sale amount) directly to Line 11, Schedule D, Form If Line 16, Schedule D shows a gain and you took Section 1250 depreciation then on Line 19, Schedule D enter the amount from Line 18 of the Worksheet on Page D-8 of Instructions for Schedule D. Section 1250 property is basically all rental real estate on which depreciation is taken. Important: Start the Page D-8 Worksheet by entering on Line 12 the smaller of (a) the Section 1250 depreciation taken on the relinquished property (see Step 1, line 2.b. of Worksheet enclosed) or (b) the recognized gain from Line 22, Form

9 c. Form 6252, Installment Sale Income. That portion of the amount on Line 22, Form 8824 to be treated as an installment sale is reported on Form If there is any installment sale income then it is carried forward from Line 26, Form 6252 and reported on Line 11, Schedule D or line 4, Form (see IRS Publication 537, Installment Sales) d. Schedule E and Form 8582, Passive Activity Loss Limitations. If you have suspended passive losses from the rental property you are exchanging then you may use those losses to offset any taxable boot you may be receiving. Use Worksheet 5 to Form 8582 to determine the amount of allowed loss (column c) for the specific property being exchanged. This allowed loss then is posted to Line 23, Schedule E. Any suspended passive losses on the exchanged property not used are carried forward to the replacement property (see IRS Publication 925, Passive Activity and At-Risk Rules, and the Instructions for Form 8582). 7. DEPRECIATION OF REPLACEMENT PROPERTY. In January 2000 IRS Notice described the way a new replacement property was to be depreciated. Then in early 2004 the IRS published in T.D detailed temporary and proposed regulations amending Section 168. Under the new regulations the general rule remains that the taxpayer must depreciate the remaining relinquished property adjusted basis (called the exchanged basis) over the remaining recovery period using the same depreciation method as if it were a continuation of the relinquished property depreciation schedule. However, if the replacement property is not residential, then the remaining exchanged basis and the new excess basis would be depreciated using the 39 year schedule. Any increase in the basis (called the excess basis) will be treated as newly acquired property and will be depreciated over 27.5 or 39 years using a new straight line depreciation schedule. No depreciation will be claimed for the period between the transfer of the relinquished property and the receipt of the replacement property. The new regulation does permit the taxpayer to elect out of the rules and to treat the entire replacement property as a new asset. To make this election see IRS instructions for IRS Form 4562, Depreciation and Amortization. Example: An exchangor has been taking depreciation for 10 years on a residential rental purchased for $150,000. He has taken $4,500 in depreciation annually leaving an exchanged basis of $105,000. If he purchases a residential replacement property with a total new basis of $200,000 (per line 25 of Form 8824) his depreciation schedules for the replacement property would be as follows: Continuation of Old Schedule for Remaining 17.5 years: $4,500 per year for 17.5 years New Schedule for Amount of Excess Basis for 27.5 years: If the value of the new property depreciable improvements were 82.5% then the $95,000 increase in basis ($200, ,000) would be depreciated as follows: $95, % = $78,375 divided by 27.5 years. The result would be $2,850 in annual depreciation to be taken for 27.5 years. Note: The above applies to real estate replacement property depreciation. The temporary regulations also cover Involuntary Conversions under IRC 1033, and other like-kind exchanges. For complete text see IRB , April 5, 2004, T.D. 9115, at 8

10 LIKE KIND ECHANGE ALLOCATION of SETTLEMENT COSTS RELINQUISHED PROPERTY Non-Exchange Expenses HUD 1 Exchange 1040 Schedule E Debt Line # Item (note 1) Expense (note 3) Adjustment/Expense Relief 700 Commission 800 Loan Fees 1100 Title Charges 1200 Recording Fees 1300 Additional Charges Termite Courier Fees Exchange Fees Pre-paid by Seller HOA/Condo Fee Taxes Pay-off of Mortgage Principal Pay-off Interest Lender Charges Items Unpaid by Exchangor 519 Taxes HOA/Condo Fees Escrow for Repairs REPLACEMENT PROPERTY Non-Exchange Expenses HUD 1 Exchange 1040 Schedule E Loan Line # Item Expense (note 3) Adjustment/Expense Costs 700 Commission 800- Loan Fees Loan Points (note 2) 803 Appraisal Fee 900 Prepaids Interest Insurance 100 HOA/Condo Fee 1000 Lender Reserves (Taxes + Insurance) (note 4) 1100 Title Charges Title Insurance 1200 Recording Fees 1300 Additional Charges Exchange Fees Termite Courier Fees Survey Notes: (1) Include items paid outside of closing (POC), (2) Points paid for loan are amortized over the life of the loan, (3) Exchange expense relates to the costs to dispose of relinquished property and costs to acquire replacement property, (4) Deductible when paid by lender. 9

11 WORKSHEET TO COMPLETE Part III of IRS LIKE-KIND ECHANGE FORM 8824 (Bold line numbers on the right refer to Form 8824) Line 0n STEP 1. Gain Realized from Property Relinquished Form FMV of Relinquished Property (Note 1) $ 2. less: Adjusted Basis 2a. Cost (with improvements) $ 2b. less: Depreciation Allowed 3. less: Total Exchange Expenses (Note 2) 3a. Relinquished Property $ 3b. Replacement Property + 4. Equals Realized Gain $ (Line 19) STEP 2. Recognized Gain 5. Relief of debt on relinquished property $ 6. less: Debt acquired on replacement property 7. Equals Net relief of liabilities (Not less then 0) $ 8. plus: Cash (Down Payment) received (Note 3) + 9. less: Cash paid (Down payment) (Note 4) 10. less: Total Exchange Expenses - (from Line 3) 11. less: FMV of other property relinquished 12. Equals total Boot received (Not less then 0) $ 13. plus: FMV of other property, cash & Notes received Equals total NET boot received (Lines ) $ 15. Recognized Gain (Taxable income) (the smaller of Line 4 or 14 above) $ (Line 15) STEP 3. Realized Gain Deferred 16. Realized Gain (Line 4) $ 17. less: Recognized Gain (taxable income - Line 15 above) 18. Equals Realized Gain Deferred $ (Line 24) STEP 4. Basis of New Property 19. FMV of Replacement Property (Note 1) $ (Line 16) 20. less: Realized Gain Deferred (Line 18 above) 21. Equals Total Basis is New Property(ies) $ (Lines 25 & 18) NOTES: (1) FMV is normally contract price. (2) Exchange expenses are allowable selling expenses for the relinquished property and the acquisition cost of replacement properties. For the replacement property do not include loan costs or prepaids as exchange expenses. (3) FMV of relinquished property (Line 1) less debt relief (Line 5) less FMV of other property received, including value of owner held Notes (Line 13) should equal cash received. (4) Cash down payment is normally the difference between contract price and loan amount, less any seller non-closing cost credits/allowances. 2005, Ed Horan, CES, Haymarket, VA ed@1031.us 10

Realty Exchange Corporation

Realty Exchange Corporation The attached information will help explain the steps to create a successful taxdeferred exchange to: Save Thousands of Dollars in Taxes! Realty Exchange Corporation is one of

Realty Exchange Corporation The attached information will help explain the steps to create a successful taxdeferred exchange to: Save Thousands of Dollars in Taxes! Realty Exchange Corporation is one of

Using the TaxPak Buy-Down Example

Using the TaxPak Buy-Down Example Buying Up When the New Property has a purchase price that is higher than the sale price of your Old Now let s crunch some numbers! To illustrate Part III of Form 8824,

Using the TaxPak Buy-Down Example Buying Up When the New Property has a purchase price that is higher than the sale price of your Old Now let s crunch some numbers! To illustrate Part III of Form 8824,

1031 Exchange Reporting Guide

2014 1031 Exchange Reporting Guide Helping to Simplify the Reporting of your 1031 Exchange 1.800.828.1031.1031 www.1031 1031CORP CORP.com Introduction In our on-going commitment to provide our valued clients

2014 1031 Exchange Reporting Guide Helping to Simplify the Reporting of your 1031 Exchange 1.800.828.1031.1031 www.1031 1031CORP CORP.com Introduction In our on-going commitment to provide our valued clients

ABOUT CASCADE EXCHANGE SERVICES, INC. (CES):

:") ABOUT CASCADE EXCHANGE SERVICES, INC. (CES): CES, a qualified tax deferred exchange intermediary performing accommodation services since 1990, offers nationwide exchange capabilities to our clients. We

ABOUT CASCADE EXCHANGE SERVICES, INC. (CES): CES, a qualified tax deferred exchange intermediary performing accommodation services since 1990, offers nationwide exchange capabilities to our clients. We

The Voice of the 1031 Industry

Building for the Future Why should a QI know how to fill out an 8824 tax form? Many of us are bombarded with questions that are technically outside our job description. Because this is our subject, many

Building for the Future Why should a QI know how to fill out an 8824 tax form? Many of us are bombarded with questions that are technically outside our job description. Because this is our subject, many

9/6/2018. Building for the Future. Why should a QI know how to fill out an 8824 tax form? The Voice of the 1031 Industry.

Building for the Future Why should a QI know how to fill out an 8824 tax form? Many of us are bombarded with questions that are technically outside our job description. Because this is our subject, many

Building for the Future Why should a QI know how to fill out an 8824 tax form? Many of us are bombarded with questions that are technically outside our job description. Because this is our subject, many

GuideBook Reporting Your 1031 Exchange

TaxPak GuideBook 2018 for Tax-year 2017 Reporting Your 1031 Exchange Exclusively for clients of This GuideBook was written by the 1031 Exchange Experts llc to help clients sort through the complexities

TaxPak GuideBook 2018 for Tax-year 2017 Reporting Your 1031 Exchange Exclusively for clients of This GuideBook was written by the 1031 Exchange Experts llc to help clients sort through the complexities

U.S. INTERNAL REVENUE CODE SECTION 1031 TAX DEFERRED LIKE KIND EXCHANGES. This outline has been modified to reflect the recent changes in the tax law.

U.S. INTERNAL REVENUE CODE SECTION 1031 TAX DEFERRED LIKE KIND EXCHANGES This outline has been modified to reflect the recent changes in the tax law. I. SECTION 1031 LIKE KIND EXCHANGE A. What is a 1031

U.S. INTERNAL REVENUE CODE SECTION 1031 TAX DEFERRED LIKE KIND EXCHANGES This outline has been modified to reflect the recent changes in the tax law. I. SECTION 1031 LIKE KIND EXCHANGE A. What is a 1031

2018 Schedule LK, Like-Kind Exchanges

2018 Schedule LK, Like-Kind Exchanges Used in combination with Schedules M1NC, M2NC, M2SBNC, M4NC, KFNC, KSNC, KPCNC, and KPINC. *187031* Name Social Security Number/Minnesota Tax ID Number/FEIN Before

2018 Schedule LK, Like-Kind Exchanges Used in combination with Schedules M1NC, M2NC, M2SBNC, M4NC, KFNC, KSNC, KPCNC, and KPINC. *187031* Name Social Security Number/Minnesota Tax ID Number/FEIN Before

Section 1031 Tax Deferred Exchanges. A Guide to the Best Strategy for Real Estate Investment

Section 1031 Tax Deferred Exchanges A Guide to the Best Strategy for Real Estate Investment Jon Fisher 303-850-4197 Vice President Land Title Exchange Corporation Cell: 303-981-8866 Fax: 303-393-4849

Section 1031 Tax Deferred Exchanges A Guide to the Best Strategy for Real Estate Investment Jon Fisher 303-850-4197 Vice President Land Title Exchange Corporation Cell: 303-981-8866 Fax: 303-393-4849

Installment Sales. Contents. For use in preparing 2012 Returns. Publication 537 Cat. No V. Future Developments. Reminder.

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

Department of the Treasury Internal Revenue Service Publication 537 Cat. No. 15067V Installment Sales For use in preparing 2012 Returns Contents Future Developments... 1 Reminder... 1 Introduction... 1

Broker. Federal Income Tax Laws Affecting Real Estate. Chapter 14. Copyright Gold Coast Schools 1

Broker Chapter 14 Federal Income Tax Laws Affecting Real Estate Copyright Gold Coast Schools 1 Learning Objectives List the 2 principal tax deductions available to homeowners List the 2 types of home loans

Broker Chapter 14 Federal Income Tax Laws Affecting Real Estate Copyright Gold Coast Schools 1 Learning Objectives List the 2 principal tax deductions available to homeowners List the 2 types of home loans

97 Partner's Instructions for Schedule K-1 (Form 1065)

") 97 Department Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Credits, Deductions, etc. (For Partner's Use Only) Section references are to the Internal Revenue Code unless

97 Department Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Credits, Deductions, etc. (For Partner's Use Only) Section references are to the Internal Revenue Code unless

Like-Kind Exchange Mechanics 2018

Like-Kind Exchange Mechanics 2018 Mark A. Vogel Tax Education Services Denver, Colorado mvogel.tax@gmail.com mvogel@du.edu (Handouts - 158 pages.) 1. Questions for the Instructor: Administrative Matters

Like-Kind Exchange Mechanics 2018 Mark A. Vogel Tax Education Services Denver, Colorado mvogel.tax@gmail.com mvogel@du.edu (Handouts - 158 pages.) 1. Questions for the Instructor: Administrative Matters

Important Tax Notice to U.S. Investors

Important Tax Notice to U.S. Investors This statement is provided for Investors who are United States persons for purposes of the U.S. Internal Revenue Code of 1986, as amended ( IRC ) and the regulations

Important Tax Notice to U.S. Investors This statement is provided for Investors who are United States persons for purposes of the U.S. Internal Revenue Code of 1986, as amended ( IRC ) and the regulations

CARL PIKUS VP Main Austin/San Antonio Dallas

CARL PIKUS VP CARL.PIKUS@ipx1031.com 512-956-0908 Main 512-956-0908 Austin/San Antonio 972-371-5371 Dallas 2 Exchange Structures with A Qualified Intermediary Simultaneous *With Qualified Intermediary

CARL PIKUS VP CARL.PIKUS@ipx1031.com 512-956-0908 Main 512-956-0908 Austin/San Antonio 972-371-5371 Dallas 2 Exchange Structures with A Qualified Intermediary Simultaneous *With Qualified Intermediary

Appendix B Pali Rao, istockphoto

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

Capital Gains and Losses

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

FIDUCIARY TAX ORGANIZER (FORM 1041)

") Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

1031 Exchange: Advanced Strategies

1031 Exchange: Advanced Strategies Presented by: Leonard Spoto Principal Asset Exchange Company Matt Ferencei Business Dev. Manager Asset Exchange Company What is an Accommodator? Holds all sale proceeds

1031 Exchange: Advanced Strategies Presented by: Leonard Spoto Principal Asset Exchange Company Matt Ferencei Business Dev. Manager Asset Exchange Company What is an Accommodator? Holds all sale proceeds

TAX MEMORANDUM. CPAs, Clients & Associates. David L. Silverman, Esq. Shirlee Aminoff, Esq. DATE: April 2, Attorney-Client Privilege

LAW OFFICES DAVID L. SILVERMAN, J.D., LL.M. 2001 MARCUS AVENUE LAKE SUCCESS, NEW YORK 11042 (516) 466-5900 SILVERMAN, DAVID L. TELECOPIER (516) 437-7292 NYTAXATTY@AOL.COM AMINOFF, SHIRLEE AMINOFFS@GMAIL.COM

LAW OFFICES DAVID L. SILVERMAN, J.D., LL.M. 2001 MARCUS AVENUE LAKE SUCCESS, NEW YORK 11042 (516) 466-5900 SILVERMAN, DAVID L. TELECOPIER (516) 437-7292 NYTAXATTY@AOL.COM AMINOFF, SHIRLEE AMINOFFS@GMAIL.COM

2014 TAX INSTRUCTIONS

APACHE OFFSHORE INVESTMENT PARTNERSHIP 2014 TAX INSTRUCTIONS ONE POST OAK CENTRAL 2000 POST OAK BOULEVARD SUITE 100 HOUSTON, TX 77056-4400 (713) 296-6000 EXPLANATION OF TERMS These explanations are brief

APACHE OFFSHORE INVESTMENT PARTNERSHIP 2014 TAX INSTRUCTIONS ONE POST OAK CENTRAL 2000 POST OAK BOULEVARD SUITE 100 HOUSTON, TX 77056-4400 (713) 296-6000 EXPLANATION OF TERMS These explanations are brief

Rental Real Estate Deductions

Rental Real Estate Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Tax Deduction Basics for Landlords... 1 Learning Objectives... 1 Introduction... 1 How Landlords Are Taxed... 1 Income Taxes

Rental Real Estate Deductions 15 th Edition Stephen Fishman, J.D. Chapter 1 Tax Deduction Basics for Landlords... 1 Learning Objectives... 1 Introduction... 1 How Landlords Are Taxed... 1 Income Taxes

ESTATE OR TRUST TAX ORGANIZER FORM New Estate or Trust Administrators Information Needed

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

SALLY W EMANUEL If a joint return, spouse's first name M.I. Last name Suffix Spouse's social security number

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 2011, or

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 2011, or

Closing Disclosure Form

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

Closing Disclosure Form The Closing Disclosure form is designed to detail all financial particulars of a transaction and it must be delivered to the borrower at least three days before closing. It might

ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) Enter amount from Worksheet 1, line 3...

Enter amount from Worksheet 1, line 3...") 1350 Print your name STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE I-335 (Rev. 3/22/16) ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 3410 (Attach I-335

1350 Print your name STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE I-335 (Rev. 3/22/16) ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 3410 (Attach I-335

A Potpourri of Section 1031 Issues. Louis S. Weller Deloitte Tax LLP San Francisco, California Telephone:

A Potpourri of Section 1031 Issues by Louis S. Weller Deloitte Tax LLP San Francisco, California Telephone: 415.783.4459 Email: lweller@deloitte.com Any tax advice included in this written communication

A Potpourri of Section 1031 Issues by Louis S. Weller Deloitte Tax LLP San Francisco, California Telephone: 415.783.4459 Email: lweller@deloitte.com Any tax advice included in this written communication

1031 Tax Deferred Real Estate Transactions & Reverse 1031 Transactions

1031 Tax Deferred Real Estate Transactions & Reverse 1031 Transactions Continuing Real Estate Education Seminar Pierre E. Debbas, Esq. Romer Debbas, LLP 183 Madison Avenue Suite 904 New York, NY 10016

1031 Tax Deferred Real Estate Transactions & Reverse 1031 Transactions Continuing Real Estate Education Seminar Pierre E. Debbas, Esq. Romer Debbas, LLP 183 Madison Avenue Suite 904 New York, NY 10016

2011 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc.

Partner s Share of Income, Deductions, Credits, etc.") 2011 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only) Department of the Treasury Internal Revenue Service Section references

2011 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only) Department of the Treasury Internal Revenue Service Section references

Chapter 20. Federal Income Taxation. IRS Tax Classifications. IRS Tax Classifications. Taxation of Individuals & Corporations

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

Federal Income Taxation Chapter 20 Income Taxation and Value Whether you like it or not, you have a silent partner who shares in your enterprise If RE investors are successful, federal (& usually state)

FIDUCIARY TAX ORGANIZER FORM 1041

FIDUCIARY TAX ORGANIZER FORM 1041 Enclosed is an organizer that I provide to my tax clients in order to assist them in gathering the information necessary to prepare their fiduciary income tax returns.

FIDUCIARY TAX ORGANIZER FORM 1041 Enclosed is an organizer that I provide to my tax clients in order to assist them in gathering the information necessary to prepare their fiduciary income tax returns.

USING IRC SECTION 1031 TO CREATE AND PRESERVE WEALTH

USING IRC SECTION 1031 TO CREATE AND PRESERVE WEALTH A SECTION 1031 EXCHANGE IS THE MEANS BY WHICH ONE CAN DEFER CAPITAL GAINS TAXES ON THE SALE OF PROPERTY HELD FOR INVESTMENT OR PRODUCTIVE USE- BY EXCHANGING

USING IRC SECTION 1031 TO CREATE AND PRESERVE WEALTH A SECTION 1031 EXCHANGE IS THE MEANS BY WHICH ONE CAN DEFER CAPITAL GAINS TAXES ON THE SALE OF PROPERTY HELD FOR INVESTMENT OR PRODUCTIVE USE- BY EXCHANGING

Exempt Organization Business Income Tax Return

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( c ) ( 3 ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business

Form 990-T Department of the Treasury Internal Revenue Service Check box if A address changed B Exempt under section 501( c ) ( 3 ) 408(e) 408A 220(e) 530(a) Print or Type Exempt Organization Business

ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 1a. Enter amount from Worksheet 1, line a. $.

1a. Enter amount from Worksheet 1, line a. $.") 1350 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE I-335 (Rev. 8/2/10) ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 3410 (Attach I-335 and all supporting

1350 STATE OF SOUTH CAROLINA DEPARTMENT OF REVENUE I-335 (Rev. 8/2/10) ACTIVE TRADE OR BUSINESS INCOME REDUCED RATE COMPUTATION (Complete one I-335 for each return) 3410 (Attach I-335 and all supporting

2013 Instructions for Schedule E (Form 1040)

") Department of the Treasury Internal Revenue Service 2013 Instructions for Schedule E (Form 1040) Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate,

Department of the Treasury Internal Revenue Service 2013 Instructions for Schedule E (Form 1040) Supplemental Income and Loss Use Schedule E (Form 1040) to report income or loss from rental real estate,

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2016 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2016 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

Form 4797 Chapter 3 pp Agricultural Tax Issues

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

Form 4797 Chapter 3 pp. 85-118 2018 Agricultural Tax Issues Form 4797 Page 85 Reporting of gains and losses on the disposition of business property. The collection point for gains and losses reported elsewhere.

City, town or post office, state, and ZIP code. If you have a foreign address, see page 14.

Form 1040 Label (See instructions on page 14.) Use the IRS label. Otherwise, please print or type. L E L H E R E Department of the Treasury Internal Revenue Service U.S. Individual Income Tax Return 2009

Form 1040 Label (See instructions on page 14.) Use the IRS label. Otherwise, please print or type. L E L H E R E Department of the Treasury Internal Revenue Service U.S. Individual Income Tax Return 2009

Selling Your Home. Contents. Important Change for Important Reminders. Publication 523 Cat. No W. For use in preparing 1998 Returns

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 1998 Returns Contents Introduction... 2 Chapter 1. Main Home... 2 Chapter 2. Rules

Department of the Treasury Internal Revenue Service Publication 523 Cat. No. 15044W Selling Your Home For use in preparing 1998 Returns Contents Introduction... 2 Chapter 1. Main Home... 2 Chapter 2. Rules

1031 Exchange Overview

1031 Exchange Overview NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it omits rules and considerations that could

1031 Exchange Overview NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it omits rules and considerations that could

San Juan Basin Royalty Trust

San Juan Basin Royalty Trust 300 West Seventh Street, Suite B Fort Worth, Texas 76102 Telephone: 866/809-4553 Website: www.sjbrt.com January 31, 2012 IMPORTANT TAX INFORMATION To Unit holders: We enclose

San Juan Basin Royalty Trust 300 West Seventh Street, Suite B Fort Worth, Texas 76102 Telephone: 866/809-4553 Website: www.sjbrt.com January 31, 2012 IMPORTANT TAX INFORMATION To Unit holders: We enclose

Instructions for Form 6251

2017 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

2017 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. General

San Juan Basin Royalty Trust

San Juan Basin Royalty Trust 300 West Seventh Street, Suite B Fort Worth, Texas 76102 Telephone: (866) 809-4553 Website: www.sjbrt.com January 31, 2013 IMPORTANT TAX INFORMATION To Unit holders: We enclose

San Juan Basin Royalty Trust 300 West Seventh Street, Suite B Fort Worth, Texas 76102 Telephone: (866) 809-4553 Website: www.sjbrt.com January 31, 2013 IMPORTANT TAX INFORMATION To Unit holders: We enclose

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

New RESPA Rule FAQs (New items are in bold) General 1) Q: When does the new RESPA Rule take effect? A: The November 2008 RESPA Rule was effective January 16, 2009. Implementation of the provisions are

1031 Exchange Overview - A Layman s View March 2016

1031 Exchange Overview - A Layman s View March 2016 NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it may omit

1031 Exchange Overview - A Layman s View March 2016 NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it may omit

VILLAGE OF NEW LONDON, OHIO INCOME TAX RETURN AND DECLARATION

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

VILLAGE OF NEW LONDON Return Service Requested TO: INCOME TAX DEPARTMENT 115 EAST MAIN STREET NEW LONDON, OHIO 44851 PRE-SORTED FIRST CLASS MAIL U.S. POSTAGE PAID NEW LONDON, OHIO Permit No. 5 VILLAGE

Send us your next 1031 Exchange, Fast Nationwide Service, Low Rates. Click Here!

The Real Estate Exchange Company Qualified Intermediaries for Section 1031 Exchanges since 1990 Tax Alert Newsletter July 15, 2002 - VOL. 1, NO. 19 Realty Exchangers Tax Alert is a FREE biweekly newsletter

The Real Estate Exchange Company Qualified Intermediaries for Section 1031 Exchanges since 1990 Tax Alert Newsletter July 15, 2002 - VOL. 1, NO. 19 Realty Exchangers Tax Alert is a FREE biweekly newsletter

Home Mortgage Interest Deduction

Department of the Treasury Internal Revenue Service Publication 936 Cat.. 10426G Home Mortgage Interest Deduction For use in preparing 2012 Returns Contents Reminders... 1 Introduction... 1 Part I. Home

Department of the Treasury Internal Revenue Service Publication 936 Cat.. 10426G Home Mortgage Interest Deduction For use in preparing 2012 Returns Contents Reminders... 1 Introduction... 1 Part I. Home

IF 1031 IS TAX DEFERRED ONLY, WHEN DO I PAY THE TAXES? Only when you finally sell the property you exchanged into, without doing another exchange.

WHAT IS THE PRIMARY BENEFIT OF A DEFERRED EXCHANGE? The primary benefit for owners disposing of business or investment held property is the opportunity to "YOU PAY NO CAPITAL GAINS TAX". WHERE DID 1031

WHAT IS THE PRIMARY BENEFIT OF A DEFERRED EXCHANGE? The primary benefit for owners disposing of business or investment held property is the opportunity to "YOU PAY NO CAPITAL GAINS TAX". WHERE DID 1031

Reporting Installment Sales and Repossessions

Reporting Installment Sales and Repossessions GAIL ABBOTT, EA FOR BLUE RIDGE CHAPTER OF VIRGINIA SOCIETY OF ENROLLED AGENTS OCTOBER 19, 2016 What is an Installment Sale? Sale of Property where you receive

Reporting Installment Sales and Repossessions GAIL ABBOTT, EA FOR BLUE RIDGE CHAPTER OF VIRGINIA SOCIETY OF ENROLLED AGENTS OCTOBER 19, 2016 What is an Installment Sale? Sale of Property where you receive

U.S. Income Tax Return for an S Corporation

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Go to www.irs.gov/form1120s for

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Go to www.irs.gov/form1120s for

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2018 Publication 4012, VITA/TCE Resource Guide

2018 Publication 4012, VITA/TCE Resource Guide Publication 4012 B-4 In the second text box, in the left margin of the page, change Line 21 to: B-7A Schedule 1 Make a pen/ink change in Publication 4012.

2018 Publication 4012, VITA/TCE Resource Guide Publication 4012 B-4 In the second text box, in the left margin of the page, change Line 21 to: B-7A Schedule 1 Make a pen/ink change in Publication 4012.

IRC 1031 Tax Deferred Exchange Exchanges. Whitney Brennan Vice President Southeast Region, IPX

IRC 1031 Tax Deferred Exchange 1031 Exchanges Whitney Brennan Vice President Southeast Region, IPX1031 1 Course Objectives Today s program is designed to help you better understand: Objective 1 Objective

IRC 1031 Tax Deferred Exchange 1031 Exchanges Whitney Brennan Vice President Southeast Region, IPX1031 1 Course Objectives Today s program is designed to help you better understand: Objective 1 Objective

Partner's Instructions for Schedule K-1 (Form 1065)

") 2017 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

2017 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE

New York State Department of Taxation and Finance Office of Counsel STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. M150511A The Department of Taxation and Finance

New York State Department of Taxation and Finance Office of Counsel STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. M150511A The Department of Taxation and Finance

Instructions for Completing the Uniform Residential Loan Application

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

Instructions for Completing the Uniform Residential Loan Application Uniform Residential Loan Application The Uniform Residential Loan Application (URLA) contains the following sections: Section 1. Borrower

FEB

2007 22FEB2008084453 Permian Basin Royalty Trust 901 Main Street, Suite 1700 Post Office Box 830650 Dallas, Texas 75283-0650 Telephone Toll-Free 1-877-228-5085 February 18, 2008 IMPORTANT TAX INFORMATION

2007 22FEB2008084453 Permian Basin Royalty Trust 901 Main Street, Suite 1700 Post Office Box 830650 Dallas, Texas 75283-0650 Telephone Toll-Free 1-877-228-5085 February 18, 2008 IMPORTANT TAX INFORMATION

Final RESPA Rule Requirements

Final RESPA Rule Requirements 1 Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November

Final RESPA Rule Requirements 1 Final RESPA Rule Requirements The Department of Housing and Urban Development (HUD) released its final rule on the Real Estate Settlement Procedures Act (RESPA) on November

PUBLIC INSPECTION COPY

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

Form 990-T Department of the Treasury Internal Revenue Service A Check box if address changed Exempt Organization Business Income Tax Return (and proxy tax under section 6033(e)) For calendar year 2011

The Tax Cuts and Jobs Act of 2017 and Internal Revenue Code Section

The Tax Cuts and Jobs Act of 2017 and Internal Revenue Code Section 1031 1 David M. Sengstock, JD Mick Law P.C. LLO November 23, 2018 How does one manage an Internal Revenue Code Section 199A qualified

The Tax Cuts and Jobs Act of 2017 and Internal Revenue Code Section 1031 1 David M. Sengstock, JD Mick Law P.C. LLO November 23, 2018 How does one manage an Internal Revenue Code Section 199A qualified

U.S. Income Tax Return for an S Corporation

Form Department of the Treasury Internal Revenue Service () Paid Preparer Use Only Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

Form Department of the Treasury Internal Revenue Service () Paid Preparer Use Only Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information.

Internal Revenue Bulletin: March 22, 2010

Internal Revenue Bulletin: 2010-12 March 22, 2010 Safe Harbor Method of Reporting Gain or Loss Under 1031 Like-Kind Exchange with Qualified Intermediary (QI) Bankruptcy or Receivership (see Section 5 below

Internal Revenue Bulletin: 2010-12 March 22, 2010 Safe Harbor Method of Reporting Gain or Loss Under 1031 Like-Kind Exchange with Qualified Intermediary (QI) Bankruptcy or Receivership (see Section 5 below

Indianapolis IN Change in trust's name applicable ; Total... G 24h

Deductions 15a Other deductions not subject to the 2% floor (attach schedule).................................. 15a b Allowable miscellaneous itemized deductions subject to the 2% floor.........................................

Deductions 15a Other deductions not subject to the 2% floor (attach schedule).................................. 15a b Allowable miscellaneous itemized deductions subject to the 2% floor.........................................

Chapter Money Education 13-1

Chapter 13 Nontaxable transaction Realized gain/loss not currently recognized Recognition is postponed to a future date Basis, potential depreciation recapture, and holding period carry over Tax-free transaction

Chapter 13 Nontaxable transaction Realized gain/loss not currently recognized Recognition is postponed to a future date Basis, potential depreciation recapture, and holding period carry over Tax-free transaction

Advance Draft. as of Member s Share of Income, Deductions, Credits, etc.

TAXABLE YEAR 2011 Member s Share of Income, Deductions, Credits, etc. CALIFORNIA SCHEDULE K-1 (568) For calendar year 2011 or fiscal year beginning month day year, and ending month day year. Member s identifying

TAXABLE YEAR 2011 Member s Share of Income, Deductions, Credits, etc. CALIFORNIA SCHEDULE K-1 (568) For calendar year 2011 or fiscal year beginning month day year, and ending month day year. Member s identifying

Bob Smith Betty Smith Home address (number and street). If you have a P.O.box, see instructions. J Important!

. If you have a P.O.box, see instructions. J Important!") Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

San Juan Basin Royalty Trust

San Juan Basin Royalty Trust 2525 Ridgmar Boulevard, Suite 100 Fort Worth, Texas 76116 Telephone 866/809-4553 Website: www.sjbrt.com January 31, 2007 IMPORTANT TAX INFORMATION TO UNIT HOLDERS: We enclose

San Juan Basin Royalty Trust 2525 Ridgmar Boulevard, Suite 100 Fort Worth, Texas 76116 Telephone 866/809-4553 Website: www.sjbrt.com January 31, 2007 IMPORTANT TAX INFORMATION TO UNIT HOLDERS: We enclose

Section 168. Accelerated Cost Recovery System

Section 168. Accelerated Cost Recovery System 26 CFR 1.168(a) 1T: Modified accelerated cost recovery system (temporary). T.D. 9115 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 Depreciation

Section 168. Accelerated Cost Recovery System 26 CFR 1.168(a) 1T: Modified accelerated cost recovery system (temporary). T.D. 9115 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 1 Depreciation

3. Use the Fee drop-down list to select another fee to add to that same section. The pop-up window changes when the new fee is selected.

How to add, edit and delete fees To create a Closing Disclosure, information is entered in Order Entry, Closing Data Entry, and the Closing Disclosure Details screen. If only a Buyer s or Seller s Settlement

How to add, edit and delete fees To create a Closing Disclosure, information is entered in Order Entry, Closing Data Entry, and the Closing Disclosure Details screen. If only a Buyer s or Seller s Settlement

. Your completed tax organizer needs to be received no later than

Organizer Estate and trust This organizer is designed to assist you in gathering the information required for preparation of fiduciary tax returns. Please complete it in full and provide details and documentation

Organizer Estate and trust This organizer is designed to assist you in gathering the information required for preparation of fiduciary tax returns. Please complete it in full and provide details and documentation

University Associates Limited Partnership HUD Project No.:

Financial Statements (With Supplementary Information) and Independent Auditor s Report December 31, 2012 Index Page Mortgagor s Certification 4 Managing Agent s Certification 5 Independent Auditor s Report

Financial Statements (With Supplementary Information) and Independent Auditor s Report December 31, 2012 Index Page Mortgagor s Certification 4 Managing Agent s Certification 5 Independent Auditor s Report

Revenue Procedure

CLICK HERE to return to the home page Revenue Procedure 2005-14 February 14, 2005 SECTION 1. PURPOSE This revenue procedure provides guidance on the application of and 1031 of the Internal Revenue Code

CLICK HERE to return to the home page Revenue Procedure 2005-14 February 14, 2005 SECTION 1. PURPOSE This revenue procedure provides guidance on the application of and 1031 of the Internal Revenue Code

WEST VIRGINIA STATE TAX DEPARTMENT SCHEDULE MITC-1 CREDIT FOR MANUFACTURING INVESTMENT

WV/MITC-1 Rev. 02/10 WEST VIRGINIA STATE TAX DEPARTMENT SCHEDULE MITC-1 CREDIT FOR MANUFACTURING INVESTMENT BUSINESS NAME IDENTIFICATION NUMBER TAX PERIOD MM DD YYYY TO MM DD YYYY COMPUTATION OF ELIGIBLE

WV/MITC-1 Rev. 02/10 WEST VIRGINIA STATE TAX DEPARTMENT SCHEDULE MITC-1 CREDIT FOR MANUFACTURING INVESTMENT BUSINESS NAME IDENTIFICATION NUMBER TAX PERIOD MM DD YYYY TO MM DD YYYY COMPUTATION OF ELIGIBLE

Street address (suite/room no.) City (if the corporation has a foreign address, see instructions.) State ZIP code

City (if the corporation has a foreign address, see instructions.) State ZIP code") TAXABLE YEAR 2018 California S Corporation Franchise or Income Tax Return FORM 100S For calendar year 2018 or fiscal year beginning and ending. (m m / d d / y y y y) (m m / d d / y y y y) RP Corporation

TAXABLE YEAR 2018 California S Corporation Franchise or Income Tax Return FORM 100S For calendar year 2018 or fiscal year beginning and ending. (m m / d d / y y y y) (m m / d d / y y y y) RP Corporation

2010 Instructions for Form 6251 Alternative Minimum Tax Individuals

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2010 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2010 Instructions for Form 6251 Alternative Minimum Tax Individuals Department of the Treasury Internal

Teresa Person, CES Course No Provider No. 0001

Teresa Person, CES tperson@1031exchangecorp.com Historical Perspective Original Tax Law Defers or Eliminates Tax on Capital Gains Gain or loss is not recognized when property held for use in trade or

Teresa Person, CES tperson@1031exchangecorp.com Historical Perspective Original Tax Law Defers or Eliminates Tax on Capital Gains Gain or loss is not recognized when property held for use in trade or

Partner's Instructions for Schedule K-1 (Form 1065)

") 2018 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

2018 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

2016 Tax Information Guide

2016 Tax Information Guide To Our Clients: Please retain this booklet with your 2016 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information

2016 Tax Information Guide To Our Clients: Please retain this booklet with your 2016 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information

PPC 1120 Deskbook Practice Aids. Industry-leading tools for tax professionals

PPC 1120 Deskbook Practice Aids Industry-leading tools for tax professionals PPC 1120 DESKBOOK PPC 1120 DESKBOOK PRACTICE AIDS 2 1120 Worksheets WORKSHEET W101: Accumulated Earnings Tax Computation WORKSHEET

PPC 1120 Deskbook Practice Aids Industry-leading tools for tax professionals PPC 1120 DESKBOOK PPC 1120 DESKBOOK PRACTICE AIDS 2 1120 Worksheets WORKSHEET W101: Accumulated Earnings Tax Computation WORKSHEET

Chapter 10B. Tax Aspects of Real Estate and Real Estate Sales *

0001 [ST: 10B-1] [ED: 10B-7] [REL: 162] (Beg Group) Composed: Wed Feb 28 15:17:37 EST 2018 Chapter 10B Tax Aspects of Real Estate and Real Estate Sales * SCOPE This chapter covers the fundamentals of the

0001 [ST: 10B-1] [ED: 10B-7] [REL: 162] (Beg Group) Composed: Wed Feb 28 15:17:37 EST 2018 Chapter 10B Tax Aspects of Real Estate and Real Estate Sales * SCOPE This chapter covers the fundamentals of the

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

SUMMARY OF KEY PROVISIONS OF HOUSE BILL VS. SENATE BILL FOR REAL ESTATE FINANCE INDUSTRY. Corporations/Businesses

SUMMARY OF KEY PROVISIONS OF HOUSE BILL VS. SENATE BILL FOR REAL ESTATE FINANCE INDUSTRY Provision Current Law House Bill Senate Bill Notes Corporate Tax Rates Tax Rates for Pass-through Entities Four

SUMMARY OF KEY PROVISIONS OF HOUSE BILL VS. SENATE BILL FOR REAL ESTATE FINANCE INDUSTRY Provision Current Law House Bill Senate Bill Notes Corporate Tax Rates Tax Rates for Pass-through Entities Four

San Juan Basin Royalty Trust

San Juan Basin Royalty Trust 300 West Seventh Street, Suite B Fort Worth, Texas 76102 Telephone toll-free: 1-866-809-4553 Website: www.sjbrt.com January 31, 2019 IMPORTANT TAX INFORMATION To Unit holders:

San Juan Basin Royalty Trust 300 West Seventh Street, Suite B Fort Worth, Texas 76102 Telephone toll-free: 1-866-809-4553 Website: www.sjbrt.com January 31, 2019 IMPORTANT TAX INFORMATION To Unit holders:

Instructions for Schedule I (Form 1041) Alternative Minimum Tax Estates and Trusts

Alternative Minimum Tax Estates and Trusts") 2009 Instructions for Schedule I (Form 1041) Alternative Minimum Tax Estates and Trusts Department of the Treasury Internal Revenue Service Section references are to the Internal deduction (NOLD), a capital

2009 Instructions for Schedule I (Form 1041) Alternative Minimum Tax Estates and Trusts Department of the Treasury Internal Revenue Service Section references are to the Internal deduction (NOLD), a capital

Form 3 Partnership Return of Income 2017 PARTNERSHIP NAME

PRINT IN BLACK INK FOR PRIVACY ACT NOTICE, SEE INSTRUCTIONS. Calendar year filers enter 01-01-2017 and 12-31-2017 below. Fiscal year filers enter appropriate dates. Tax year beginning Tax year ending Form

PRINT IN BLACK INK FOR PRIVACY ACT NOTICE, SEE INSTRUCTIONS. Calendar year filers enter 01-01-2017 and 12-31-2017 below. Fiscal year filers enter appropriate dates. Tax year beginning Tax year ending Form

Bankruptcy Questions Answered!

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Bankruptcy Questions Answered! by ROBERT E. McKENZIE, EA, ATTORNEY 2017 ARNSTEIN & LEHR SUITE 1200 120 SOUTH RIVERSIDE PLAZA CHICAGO, ILLINOIS 60606 (312) 876-7100 REMCKENZIE@ARNSTEIN.COM http://www.mckenzielaw.com

Liquidating Family Partnerships: Avoiding Income and Gift Tax. By Carol A. Cantrell Cantrell & Cantrell, PLLC

1 Liquidating Family Partnerships: Avoiding Income and Gift Tax By Carol A. Cantrell Cantrell & Cantrell, PLLC 713-333-0555 ccantrell@cctaxlaw.com Why Liquidate a Partner s Interest? The partnership no

1 Liquidating Family Partnerships: Avoiding Income and Gift Tax By Carol A. Cantrell Cantrell & Cantrell, PLLC 713-333-0555 ccantrell@cctaxlaw.com Why Liquidate a Partner s Interest? The partnership no

US Tax Information for Diplomatic Families at the Australian Embassy

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

US Tax Information for Diplomatic Families at the Australian Rick Ward LLC January 25, 2018 Disclosure This presentation has been prepared by LLC. The information in this presentation is current as of

White Paper Vacation Home Tax Considerations

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

White Paper www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC, MSRB Page 2 Table of Contents... 3 What

Page 1 IRC Section Jobs & Growth Tax Act. Exchange... Don't Sell. Page 4 Why Starker Services? It's Not a Secret Anymore

Table Of Contents Page 1 IRC Section 1031 Page 2 Page 3 2003 Jobs & Growth Tax Act Exchange... Don't Sell Page 4 Why Starker Services? Page 5 Page 6 Page 7 Page 8 Page 9 It's Not a Secret Anymore "Like-Kind"

Table Of Contents Page 1 IRC Section 1031 Page 2 Page 3 2003 Jobs & Growth Tax Act Exchange... Don't Sell Page 4 Why Starker Services? Page 5 Page 6 Page 7 Page 8 Page 9 It's Not a Secret Anymore "Like-Kind"

PUYALLUP SCHOOL DISTRICT. Domestic Partner Health Coverage

PUYALLUP SCHOOL DISTRICT Domestic Partner Health Coverage Instructions: To cover your domestic partner and/or your partner s children under your District dental, vision or health plan please review this

PUYALLUP SCHOOL DISTRICT Domestic Partner Health Coverage Instructions: To cover your domestic partner and/or your partner s children under your District dental, vision or health plan please review this

Access to the worksheet is available via View buttons located at the bottom of the application and closing stage questions.

GFE/HUD Data Entry Worksheet Form 21720 Entries to complete the Good Faith Estimate and HUD Settlement Statements are made from the GFE/HUD Worksheet, form number 21720. Access to the worksheet is available

GFE/HUD Data Entry Worksheet Form 21720 Entries to complete the Good Faith Estimate and HUD Settlement Statements are made from the GFE/HUD Worksheet, form number 21720. Access to the worksheet is available

Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev.

First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev.") Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev. December 2010) Department of the Treasury Internal Revenue Service Section

Instructions for Form 5405 (Rev. March 2011) First-Time Homebuyer Credit and Repayment of the Credit For use with Form 5405 (Rev. December 2010) Department of the Treasury Internal Revenue Service Section

Housing Finance Authority (HFA) of Pinellas County (the Issuer ) NOTICES TO BUYERS/AUTHORIZATION

of Pinellas County (the Issuer ) NOTICES TO BUYERS/AUTHORIZATION") Servicer Loan # Housing Finance Authority (HFA) of Pinellas County (the Issuer ) NOTICES TO BUYERS/AUTHORIZATION NOTICE OF POTENTIAL RECAPTURE This mortgage loan is funded from the proceeds of a tax-exempt

Servicer Loan # Housing Finance Authority (HFA) of Pinellas County (the Issuer ) NOTICES TO BUYERS/AUTHORIZATION NOTICE OF POTENTIAL RECAPTURE This mortgage loan is funded from the proceeds of a tax-exempt

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Shopping for your home loan Settlement cost booklet CFPB (Consumer Financial Protection Bureau) January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development.

Shareholder s Share of Income, Deductions, Credits, etc.

Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service 2010 For calendar year 2010, or tax year beginning, 2010 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc.

Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service 2010 For calendar year 2010, or tax year beginning, 2010 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc.