Tax Reform and Fairness for Families Presentation to the President s Advisory Panel on Tax Reform New Orleans, LA March 23, 2005

|

|

|

- Emerald Harrington

- 5 years ago

- Views:

Transcription

1 Tax Reform and Fairness for Families Presentation to the President s Advisory Panel on Tax Reform New Orleans, LA March 23, 2005 Eugene Steuerle Co-Director, Urban-Brookings Tax Policy Center & Former Economic Coordinator, Treasury Project for Tax Reform 1

2 Outline Tax system affects almost every area of family s life Many tax subsidies are complex, unfair, inefficient, non-transparent, and corrupting IRS does NOT monitor subsidies effectiveness Much spending is hidden in taxation Much taxation is hidden in spending Tax reform cannot avoid addressing these policies True tax reform identifies who is going to pay 2

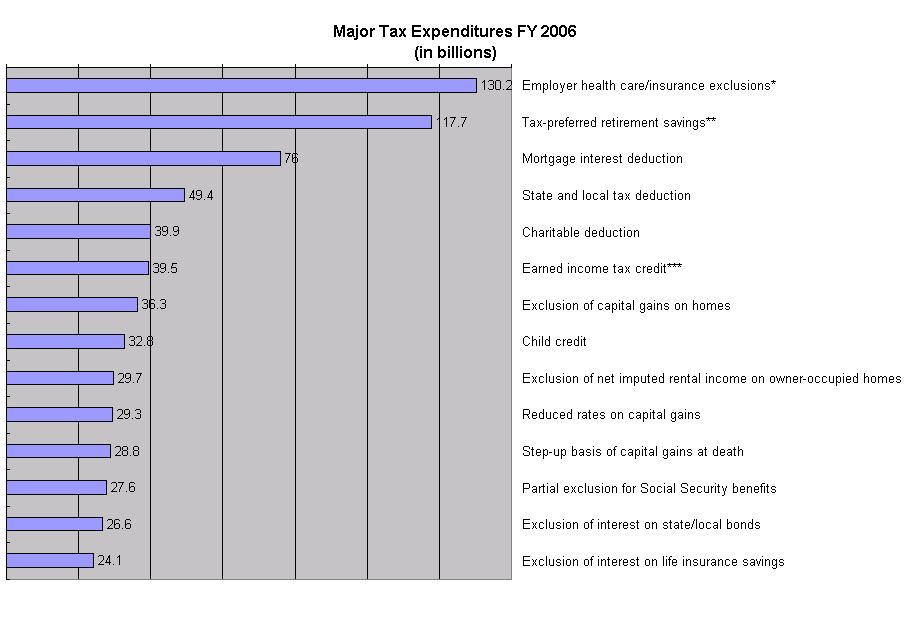

3 Pervasiveness of Tax Subsidies Child-related subsidies (EITC larger than welfare) Housing tax subsidies(larger than HUD budget) Charitable incentives Subsidies for states/localities Health tax subsidies (for workers, larger than any direct spending program) Retirement/saving incentives (revenue loss greater than total personal saving) Higher education incentives Business subsidies (that differentiate among families by source of income, not ability to pay) 3

4 4

5 Many Subsidies Poorly Designed As Tax or Spending Programs Complex Provide unequal justice to taxpayers with equal ability to pay (horizontal inequity) Regressive (vertical inequity) Poorly targeted to need n-transparent Corrupting 5

6 Child Provisions & Phase Outs Earned Income Tax Credit Refundable Child Credit Dependent Exemption EITC phase out Child credit phase out Dependent exemption phase out Dependent exemption as AMT tax shelter Head of household status Some opportunities: one unified credit; integrate phase outs or fold into rate schedule 6

7 Tax Benefits for a Typical Head of Household with Two Children in Tax Year 2003 $6,000 Value of Tax & Transfer Benefits $5,000 $4,000 $3,000 $2,000 $1,000 Earned Income Tax Credit Dependent Exemption Child Tax Credit $0 $0k $10k $20k $30k $40k $50k $60k $70k $80k $90k $100k Family Wage Income 7

8 Housing Subsidies: Mainly Through Tax Code For poor, rental but no ownership subsidies (e.g., low income housing tax credit) For moderate income, no rental or tax subsidies, only higher prices For middle class, some tax breaks For higher-income, the largest subsidies Interest deduction rules confusing & prone to error (e.g., secondary versus primary mortgages) Some opportunities: simplify & level out the subsidies 8

9 9

10 Charitable Incentives Subsidies could be better designed to promote giving Cash and in-kind contributions sources of cheating & invite corruption Little IRS enforcement for charitable organizations For some contributions, government subsidy goes mainly to intermediaries, not to charity Some opportunities: fold together bills for improving incentives & removing abuses (Senator Grassley statement & my Senate Finance testimony) 10

11 State & Local State & local tax deduction Capped already because of AMT Proposed for elimination in 1984 Treasury study Public purpose tax-exempt bonds Private purpose tax-exempt bonds Often promote arbitrage, not net new investment Favor lobbyists with political connections Newer credit based bonds (e.g. for local school construction) Empowerment/enterprise zones Favor those on right side of the street Some opportunties: AMT forces decision on S&L tax deductibility; limit or better target private bonds/zone subsidies to real needs 11

12 Health Tax Subsidies Largest for the richest and those with highest cost plans Current subsidies of about $150 billion will rise by another $100 billion annually within a few years That increase of $100 billion will likely INCREASE number of uninsured By adding to cost pressures Some opportunities: Spend additional subsidies more wisely & distribute to reduce # of uninsured 12

13 Retirement Plan Subsidies Dozens of plan options Substantial complexity Much of return lost to intermediaries Tax subsidies for retirement now in excess of total personal saving! Existing subsidies not for saving, but deposits Some opportunities: Simplify, level out subsidies 13

14 Retirement Plan Options Under Current Law The Private Pension SystemIn a Qualifi ed Plans 403 Tax Sheltered Annuities 408, 408A s n-qualified Deferred Compensation Defined Benefit Plans Defined Contribution Plans 403a Annuities 403b Arrangements Individual s 457(b) Plans Standard Cash Balance Money Purchase Stock Bonus Profit Sharing Thrif t Empl oyee Contributions Only Empl oyer Contributions s s s ESOPs 401k 401k 401k 401k Standard 401k SIMPLE 401k 401k 401k Standard 401k Standard 401k 401k 401(K) Standard Contributions Contributions SEP s Empl oyer s SIMPLE s s Execut ive Compensation Arrangements 457f Government Tax Exempt Employers Other Empl oyers 14

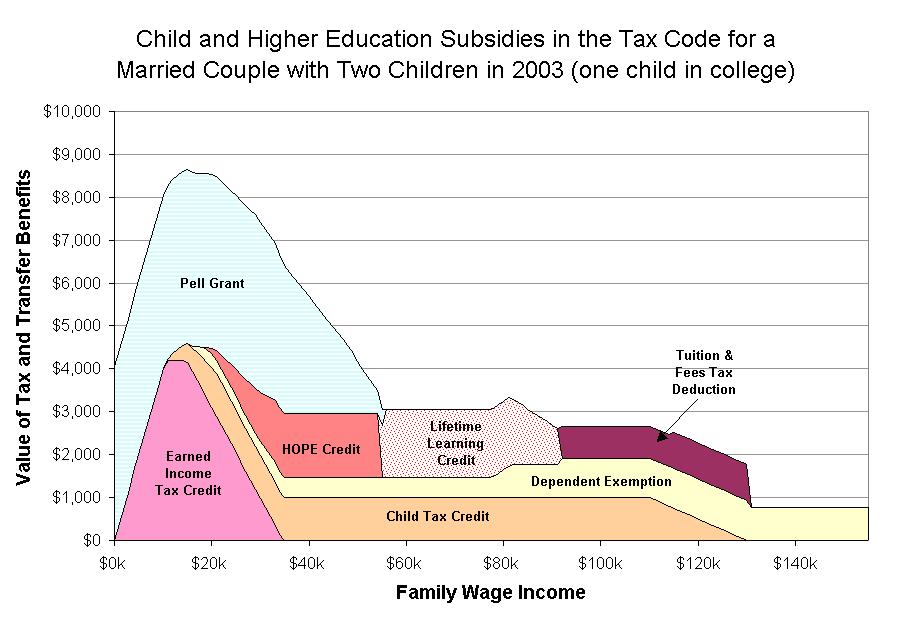

15 Higher Education Subsidies Many and contradictory Distributed somewhat randomly Complex and not well integrated with direct aid Often high marginal tax rates Some opportunities: Unify into one tax program; fold into Pell grants 15

16 16

17 Some Business Tax Incentives Special subsidies by type of business (e.g., small business, energy) Affect families very differently t based on ability to pay Often favor rich owner of subsidized business over poor owner of unsubsidized business Some opportunities: Target benefits better; if consumption tax treatment sought, treat interest deductions consistently 17

18 Trade-offs still required EXAMPLES Simplicity may dictate rough justice Simple subsidies may be very inefficient Progressivity often leads to high tax rates & marriage penalties on moderate income taxpayers 18

19 Weak Enforcement & Monitoring Great difficulty administering ncompliance highest when no reports (1099s) Very few taxpayers audited Almost no monitoring for effectiveness for almost all subsidies Treasury & IRS proclaim inability: Don t have data ( data constraints may limit assessment of effectiveness U.S. Treasury) Can t currently fulfill Government Performance & Results Act of 1983 (GPRA) requirement to develop strategic plans for programs 19

20 Why Spending is Hidden in Taxation Tax subsidies in budget show up as: Reduced taxation increase in spending In reality Same economic effects as spending Cause higher tax rates Perhaps 1/4 to 1/3 of all government spending is in tax system Social spending now larger fraction of pie 20

21 21

22 Many Taxes Hidden Derives mainly from: (1) Phase outs in tax programs (2) Phase outs in spending programs Net result for moderate income families: Very high marginal tax rates Huge marriage penalties Implications: Concern over high tax rates must take into account other government programs Removal of income tax still leaves many families subject to income accounting 22

23 23

24 Is There a Magic Bullet? Current system really like three: Poor child credits, EITC expenditures Middle class incentives, deductions galore Rich - zero taxes on many accruals - double taxes on some income Solving for one group doesn t solve for others Endless search for magic bullet Flat tax, consumption tax Still must decide charitable, housing & other policy 24

25 Conclusion Tax reform is possible We ve done it before Budget necessity and public outrage over complexity of AMT could force issue But it s very hard work Tax reform is a test case for systemic reform requirements of a new fiscal era Recognizing who pays Requiring proof of performance to continue programs 25

Taxation-Overview (Chapter 18)

") (Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

(Chapter 18) So far, we have talked about different government expenditure items: Education Social Security Health insurance Welfare programs How does local and federal governments finance such programs?

Our Tax System Revealed. Lee R. Nackman, Ph.D. October 24, 2018

Our Tax System Revealed Lee R. Nackman, Ph.D. October 24, 2018!1 Topics Tax System Desiderata Follow the Money! Social Security Payroll Taxes Sales Taxes Federal Individual Income Taxes The Big Picture:

Our Tax System Revealed Lee R. Nackman, Ph.D. October 24, 2018!1 Topics Tax System Desiderata Follow the Money! Social Security Payroll Taxes Sales Taxes Federal Individual Income Taxes The Big Picture:

Income Taxes and Tax Rates for Sample Families, 2006 Greg Leiserson. December 2006

Income Taxes and Tax Rates for Sample Families, 2006 Greg Leiserson December 2006 This article examines how much income tax families pay in different situations, as well as the effective marginal tax rates

Income Taxes and Tax Rates for Sample Families, 2006 Greg Leiserson December 2006 This article examines how much income tax families pay in different situations, as well as the effective marginal tax rates

CTJ. Citizens for Tax Justice

CTJ Citizens for Tax Justice September 19, 2011 Contact: Steve Wamhoff (202) 299-1066 x33 Revenue Provisions in President s Jobs Bill The American Jobs Act proposed by President Barack Obama includes provisions

CTJ Citizens for Tax Justice September 19, 2011 Contact: Steve Wamhoff (202) 299-1066 x33 Revenue Provisions in President s Jobs Bill The American Jobs Act proposed by President Barack Obama includes provisions

The Distribution of Federal Taxes, Jeffrey Rohaly

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

xiii Executive Summary

Executive Summary President George W. Bush created the President s Advisory Panel on Federal Tax Reform in January 2005. The President instructed the Panel to recommend options that would make the tax

Executive Summary President George W. Bush created the President s Advisory Panel on Federal Tax Reform in January 2005. The President instructed the Panel to recommend options that would make the tax

DEPARTMENT OF THE TREASURY OFFICE OF PUBLIC AFFAIRS

DEPARTMENT OF THE TREASURY OFFICE OF PUBLIC AFFAIRS Embargoed Until 12:30 EST Contact: Brookly McLaughlin November 18, 2004 202-622-1996 Samuel W. Bodman, Deputy Secretary of the Treasury Remarks before

DEPARTMENT OF THE TREASURY OFFICE OF PUBLIC AFFAIRS Embargoed Until 12:30 EST Contact: Brookly McLaughlin November 18, 2004 202-622-1996 Samuel W. Bodman, Deputy Secretary of the Treasury Remarks before

Testimony to the President s Tax Reform Panel

Testimony to the President s Tax Reform Panel John D. Podesta President Center for American Progress May 11, 2005 Overview The Center for American Progress Tax Reform Plan Fair and Responsible Reform The

Testimony to the President s Tax Reform Panel John D. Podesta President Center for American Progress May 11, 2005 Overview The Center for American Progress Tax Reform Plan Fair and Responsible Reform The

Observations on Tax Reform Testimony before the President s Advisory Panel on Federal Tax Reform. Jon Talisman Capitol Tax Partners May 17, 2005

Observations on Tax Reform Testimony before the President s Advisory Panel on Federal Tax Reform Jon Talisman Capitol Tax Partners May 17, 2005 Groundhog Day Similar calls for reform have been made over

Observations on Tax Reform Testimony before the President s Advisory Panel on Federal Tax Reform Jon Talisman Capitol Tax Partners May 17, 2005 Groundhog Day Similar calls for reform have been made over

The Effects of the Candidates Tax Plans on Households at Different Income Levels: Examples

CTJ October 29, 2008 Citizens for Tax Justice Contact: Bob McIntyre (202) 299-1066 x22 The Effects of the Candidates Tax Plans on Households at Different Income Levels: Examples Presidential candidates

CTJ October 29, 2008 Citizens for Tax Justice Contact: Bob McIntyre (202) 299-1066 x22 The Effects of the Candidates Tax Plans on Households at Different Income Levels: Examples Presidential candidates

Submission on April 29, to the. President's Advisory Panel on Federal Tax Reform. E. Martin Davidoff, CPA, Esq. Individually

Submission on to the President's Advisory Panel on Federal Tax Reform by E. Martin Davidoff, CPA, Esq. Individually Contact Information E. Martin Davidoff, CPA, Esq. E. Martin Davidoff & Associates Certified

Submission on to the President's Advisory Panel on Federal Tax Reform by E. Martin Davidoff, CPA, Esq. Individually Contact Information E. Martin Davidoff, CPA, Esq. E. Martin Davidoff & Associates Certified

Time Investment Gains and Losses

To Our Clients and Friends: The federal income tax rates for 2015 are the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. However, the rate bracket beginning and ending points are increased

To Our Clients and Friends: The federal income tax rates for 2015 are the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. However, the rate bracket beginning and ending points are increased

WEALTH CARE KIT SM. Income Tax Planning. A website built by the National Endowment for Financial Education dedicated to your financial well-being.

WEALTH CARE KIT SM Income Tax Planning A website built by the dedicated to your financial well-being. As the joke goes, figuring out your taxes is pretty easy just add up how much money you made last year

WEALTH CARE KIT SM Income Tax Planning A website built by the dedicated to your financial well-being. As the joke goes, figuring out your taxes is pretty easy just add up how much money you made last year

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

REFORMING CHARITABLE TAX INCENTIVES: ASSESSING EVIDENCE AND POLICY OPTIONS Joseph Rosenberg and Eugene Steuerle November 15, 2018 The federal tax treatment of charitable giving and the nonprofit sector

The tax reform of 2017 explained

I nnealta C A P I T A L SPECIALISTS IN ACTIVE MANAGEMENT OF ETF PORTFOLIOS The tax reform of 2017 explained Key takeaways: Recently introduced tax reform covers three main areas: taxes on individuals,

I nnealta C A P I T A L SPECIALISTS IN ACTIVE MANAGEMENT OF ETF PORTFOLIOS The tax reform of 2017 explained Key takeaways: Recently introduced tax reform covers three main areas: taxes on individuals,

PERSONAL INCOME TAXES

PERSONAL INCOME TAXES CHAPTER 35 WHERE PERSONAL INCOME TAXES FIT In 2008 the federal government collected $2,524 billion in taxes. $1,146 billion of that was collected from the personal income tax. The

PERSONAL INCOME TAXES CHAPTER 35 WHERE PERSONAL INCOME TAXES FIT In 2008 the federal government collected $2,524 billion in taxes. $1,146 billion of that was collected from the personal income tax. The

on-line Reports Low-Income Tax Policy: Increases in Tax Credits for Tax Year 2003 are Good News for Working Families

on-line Reports November 2003 Introduction Low-Income Tax Policy: Increases in Tax Credits for Tax Year 2003 are Good News for Working Families When many low- and moderate-income taxpayers file their 2003

on-line Reports November 2003 Introduction Low-Income Tax Policy: Increases in Tax Credits for Tax Year 2003 are Good News for Working Families When many low- and moderate-income taxpayers file their 2003

Federal Income Tax Treatment of the Family

Jane G. Gravelle Senior Specialist in Economic Policy November 23, 2016 Congressional Research Service 7-5700 www.crs.gov RL33755 Summary Individual income tax provisions have shifted over time, first

Jane G. Gravelle Senior Specialist in Economic Policy November 23, 2016 Congressional Research Service 7-5700 www.crs.gov RL33755 Summary Individual income tax provisions have shifted over time, first

Income inequality an insufficient consumption in China. Li Gan Southwestern University of Finance and Economics Texas A&M University

Income inequality an insufficient consumption in China Li Gan Southwestern University of Finance and Economics Texas A&M University 目 1 An Introduction of CHFS Contents 2 3 Inequality and Consumption A

Income inequality an insufficient consumption in China Li Gan Southwestern University of Finance and Economics Texas A&M University 目 1 An Introduction of CHFS Contents 2 3 Inequality and Consumption A

Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive?

Citizens for Tax Justice December 11, 2009 Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive? Summary Senate Democrats have proposed a new,

Citizens for Tax Justice December 11, 2009 Would the Senate Democrats proposed excise tax on highcost employer-paid health insurance benefits be progressive? Summary Senate Democrats have proposed a new,

The Growth and Investment Tax Plan

Chapter Seven The Growth and Investment Tax Plan Courtesy of Marina Sagona The Panel evaluated a number of tax reform proposals that would shift our current income tax system toward a consumption tax.

Chapter Seven The Growth and Investment Tax Plan Courtesy of Marina Sagona The Panel evaluated a number of tax reform proposals that would shift our current income tax system toward a consumption tax.

Tax Reform, Tax Arbitrage, and the Taxation of Carried Interest. Testimony of C. Eugene Steuerle

Tax Reform, Tax Arbitrage, and the Taxation of Carried Interest Testimony of C. Eugene Steuerle Senior Fellow, The Urban Institute Before the Committee on Ways and Means U.S. House of Representatives Congress

Tax Reform, Tax Arbitrage, and the Taxation of Carried Interest Testimony of C. Eugene Steuerle Senior Fellow, The Urban Institute Before the Committee on Ways and Means U.S. House of Representatives Congress

Economic Implications Cont

Mortgage Down Payment & Tax Subsidies Promoting home ownership Economic Implications (& Benefits) of Home Ownership Homes are crucial to low-income families for financial asset building. Over 66 percent

Mortgage Down Payment & Tax Subsidies Promoting home ownership Economic Implications (& Benefits) of Home Ownership Homes are crucial to low-income families for financial asset building. Over 66 percent

POLICY REPORT The Iowa Policy Project

POLICY REPORT The Iowa Policy Project Child & Family Policy Center April 2003 The Merits of a Cigarette Tax, With Alternative Tax Offsets By Charles Bruner and Peter S. Fisher Driven partly by state budget

POLICY REPORT The Iowa Policy Project Child & Family Policy Center April 2003 The Merits of a Cigarette Tax, With Alternative Tax Offsets By Charles Bruner and Peter S. Fisher Driven partly by state budget

H.R. 1 TAX CUT AND JOBS ACT. By: Michelle McCarthy, Esq. and Tyler Murray, Esq.

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

POLICY BRIEF. Tax legislation enacted in 2001 increased the value of the Child Tax

The Brookings Institution POLICY BRIEF July 2003 Welfare Reform & Beyond #26 Related Brookings Resources One Percent for the Kids Isabel V. Sawhill, ed. Brookings Institution Press (2003) Welfare Reform

The Brookings Institution POLICY BRIEF July 2003 Welfare Reform & Beyond #26 Related Brookings Resources One Percent for the Kids Isabel V. Sawhill, ed. Brookings Institution Press (2003) Welfare Reform

PRELIMINARY ANALYSIS OF THE FAMILY FAIRNESS AND OPPORTUNITY TAX REFORM ACT

PRELIMINARY ANALYSIS OF THE FAMILY FAIRNESS AND OPPORTUNITY TAX REFORM ACT Len Burman, Elaine Maag, Georgia Ivsin, and Jeff Rohaly 1 Urban-Brookings Tax Policy Center March 4, 2014 On October 30, 2013,

PRELIMINARY ANALYSIS OF THE FAMILY FAIRNESS AND OPPORTUNITY TAX REFORM ACT Len Burman, Elaine Maag, Georgia Ivsin, and Jeff Rohaly 1 Urban-Brookings Tax Policy Center March 4, 2014 On October 30, 2013,

Personal Income Tax Weakness & Possible Remedies: Outdated and Inequitable Tax Provisions

California s Tax System Report #7b Personal Income Tax Weakness & Possible Remedies: Outdated and Inequitable Tax Provisions Professor Annette Nellen San José State University and Irvine Fellow, New America

California s Tax System Report #7b Personal Income Tax Weakness & Possible Remedies: Outdated and Inequitable Tax Provisions Professor Annette Nellen San José State University and Irvine Fellow, New America

Inequality and Redistribution

Inequality and Redistribution Chapter 19 CHAPTER IN PERSPECTIVE In chapter 19 we conclude our study of income determination by looking at the extent and sources of economic inequality and examining how

Inequality and Redistribution Chapter 19 CHAPTER IN PERSPECTIVE In chapter 19 we conclude our study of income determination by looking at the extent and sources of economic inequality and examining how

Welfare and Child Care Reauthorization 2003: Options and Opportunities. June 1, 2003

Brookings Institution Center on Urban and Metropolitan Policy Welfare and Child Care Reauthorization 2003: Options and Opportunities June 1, 2003 Presentation Outline Changes made to welfare policy in

Brookings Institution Center on Urban and Metropolitan Policy Welfare and Child Care Reauthorization 2003: Options and Opportunities June 1, 2003 Presentation Outline Changes made to welfare policy in

Wealth Inequality in the United States (panelist)

") University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman January 3, 2007 Wealth Inequality in the United States (panelist) JONATHAN B FORMAN, University of Oklahoma Available

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman January 3, 2007 Wealth Inequality in the United States (panelist) JONATHAN B FORMAN, University of Oklahoma Available

2018 Year-End Tax Planning for Individuals

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

Tax Cut by Income Group, Fully Phased-In

Testimony of Michael P. Ettlinger, Tax Policy Director, The Institute on Taxation and Economic Policy, before the Rhode Island Senate Select Committee. October 7, 1999 Analysis of Proposed Tax Cut Good

Testimony of Michael P. Ettlinger, Tax Policy Director, The Institute on Taxation and Economic Policy, before the Rhode Island Senate Select Committee. October 7, 1999 Analysis of Proposed Tax Cut Good

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

HISTORY CONT. HISTORY HOW IT WORKS CONT. HOW IT WORKS HOW IT WORKS CONT. HOW IT WORK CONT. How To Report See Handout

HISTORY Prior to the Tax Reform Act of 1986 all interest payments on personal debt was tax deductible The Tax Reform Act of 86 amended the Internal revenue code to disallow deductions for all personal

HISTORY Prior to the Tax Reform Act of 1986 all interest payments on personal debt was tax deductible The Tax Reform Act of 86 amended the Internal revenue code to disallow deductions for all personal

14.41 Final Exam Jonathan Gruber. True/False/Uncertain (95% of credit based on explanation; 5 minutes each)

") 14.41 Final Exam Jonathan Gruber True/False/Uncertain (95% of credit based on explanation; 5 minutes each) 1) The definition of property rights will eliminate the problem of externalities. Uncertain. Also

14.41 Final Exam Jonathan Gruber True/False/Uncertain (95% of credit based on explanation; 5 minutes each) 1) The definition of property rights will eliminate the problem of externalities. Uncertain. Also

Investing in Children

Issue Brief #1 Investing in Children Losing Ground? Federal Investments in Children Will Shrink Over the Next Decade if Present Policies Continue Between 2006 and 2017, the share of the budget pie that

Issue Brief #1 Investing in Children Losing Ground? Federal Investments in Children Will Shrink Over the Next Decade if Present Policies Continue Between 2006 and 2017, the share of the budget pie that

2017 Mid-Year Tax Planning

To Our Clients and Friends: 2017 Mid-Year Tax Planning As we write this letter, the federal income tax rates for this year are still the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. The

To Our Clients and Friends: 2017 Mid-Year Tax Planning As we write this letter, the federal income tax rates for this year are still the same as last year: 10%, 15%, 25%, 28%, 33%, 35%, and 39.6%. The

100 West Fifth Street, Suite 1100 Tulsa, Oklahoma Federal Tax Alert. January 4, 2018

100 West Fifth Street, Suite 1100 Tulsa, Oklahoma 74103-4217 918-595-4800 Federal Tax Alert January 4, 2018 Federal Tax Reform; H. R. 1-Tax Cuts and Jobs Act The following is a summary of some of the significant

100 West Fifth Street, Suite 1100 Tulsa, Oklahoma 74103-4217 918-595-4800 Federal Tax Alert January 4, 2018 Federal Tax Reform; H. R. 1-Tax Cuts and Jobs Act The following is a summary of some of the significant

TAX POLICY CENTER BRIEFING BOOK. Background. Q. What are tax expenditures and how are they structured?

What are tax expenditures and how are they structured? TAX EXPENDITURES 1/5 Q. What are tax expenditures and how are they structured? A. Tax expenditures are special provisions of the tax code such as

What are tax expenditures and how are they structured? TAX EXPENDITURES 1/5 Q. What are tax expenditures and how are they structured? A. Tax expenditures are special provisions of the tax code such as

U.S. House of Representatives COMMITTEE ON WAYS AND MEANS

U.S. House of Representatives COMMITTEE ON WAYS AND MEANS The TAX CUTS & JOBS ACT CHARGE & RESPONSE Americans have been waiting for years for Washington to fix this broken tax code because they know it

U.S. House of Representatives COMMITTEE ON WAYS AND MEANS The TAX CUTS & JOBS ACT CHARGE & RESPONSE Americans have been waiting for years for Washington to fix this broken tax code because they know it

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

INCOME TAX CONSIDERATIONS FOR 2014 INCOME TAX RETURNS Following are income tax items that could affect your return for 2014. Please review and make sure you have alerted your tax consultant for all of

Before we get to specific suggestions, here are two important considerations to keep in mind.

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

A Whole New Ballgame: How Tax Reform Will Affect Dentists Tax Reform Guide.

2018 Tax Reform Guide A Whole New Ballgame: How Tax Reform Will Affect Dentists Copyright 2018 Adam Shay CPA, PLLC. All rights reserved. A Whole New Ballgame: How Tax Reform Will Affect Dentists For most

2018 Tax Reform Guide A Whole New Ballgame: How Tax Reform Will Affect Dentists Copyright 2018 Adam Shay CPA, PLLC. All rights reserved. A Whole New Ballgame: How Tax Reform Will Affect Dentists For most

2004 Tax-smart strategies guide. Keep more of what you earn

2004 Tax-smart strategies guide Keep more of what you earn 2004 Tax-smart strategies guide Keep more of what you earn As a taxpayer, you currently have some of the largest tax cuts in history working

2004 Tax-smart strategies guide Keep more of what you earn 2004 Tax-smart strategies guide Keep more of what you earn As a taxpayer, you currently have some of the largest tax cuts in history working

Year-End Tax Moves for Income Tax Rates for 2015

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

FALL 2018 PERSPECTIVES THE NEW TAX LAW: TOP QUESTIONS FROM OUR CLIENTS

FALL 2018 PERSPECTIVES THE NEW TAX LAW: TOP QUESTIONS FROM OUR CLIENTS ABBOT DOWNING PERSPECTIVES Fall 2018 In this issue: The New Tax Law: Top Questions From Our Clients 3 Only the Beginning 7 Contributors:

FALL 2018 PERSPECTIVES THE NEW TAX LAW: TOP QUESTIONS FROM OUR CLIENTS ABBOT DOWNING PERSPECTIVES Fall 2018 In this issue: The New Tax Law: Top Questions From Our Clients 3 Only the Beginning 7 Contributors:

REVENUE MOBILIZATION IN SUB-SAHARAN AFRICA. Nairobi, Kenya

REVENUE MOBILIZATION IN SUB-SAHARAN AFRICA Victoria Perry Nairobi, Kenya March 21-22, 22 2011 Overview Context Objectives, trends and strategies Issues and lessons Institutions and transparency Conclusions

REVENUE MOBILIZATION IN SUB-SAHARAN AFRICA Victoria Perry Nairobi, Kenya March 21-22, 22 2011 Overview Context Objectives, trends and strategies Issues and lessons Institutions and transparency Conclusions

FISCAL DEMOCRACY OR Why Sound Fiscal Policy, Budget Consolidation, and Inclusive Growth Require Fewer, Not More Attempts to Control the Future

FISCAL DEMOCRACY OR Why Sound Fiscal Policy, Budget Consolidation, and Inclusive Growth Require Fewer, Not More Attempts to Control the Future OECD-WB Conference on Challenges and policies for promoting

FISCAL DEMOCRACY OR Why Sound Fiscal Policy, Budget Consolidation, and Inclusive Growth Require Fewer, Not More Attempts to Control the Future OECD-WB Conference on Challenges and policies for promoting

Comment to the President s Advisory Panel on Tax Reform Submitted by The Enterprise Foundation/Enterprise Social Investment Corporation June 10, 2005

Comment to the President s Advisory Panel on Tax Reform Submitted by The Enterprise Foundation/Enterprise Social Investment Corporation June 10, 2005 Introduction and Overview The Enterprise Foundation

Comment to the President s Advisory Panel on Tax Reform Submitted by The Enterprise Foundation/Enterprise Social Investment Corporation June 10, 2005 Introduction and Overview The Enterprise Foundation

Federal Tax Reform and State and Local Governments

Federal Tax Reform and State and Local Governments Materials to Accompany Remarks Robert Ebel and Kim Rueben The Urban-Brookings New Mexico Tax Policy Conference April 19 and 20, 2005 Source: Kim Rueben,

Federal Tax Reform and State and Local Governments Materials to Accompany Remarks Robert Ebel and Kim Rueben The Urban-Brookings New Mexico Tax Policy Conference April 19 and 20, 2005 Source: Kim Rueben,

Tax Issues and Consequences in Financial Planning. Course #5505E/QAS5505E Course Material

Tax Issues and Consequences in Financial Planning Course #5505E/QAS5505E Course Material Introduction Tax Issues and Consequences in Financial Planning (Course #5505E/QAS5505E) Table of Contents Page PART

Tax Issues and Consequences in Financial Planning Course #5505E/QAS5505E Course Material Introduction Tax Issues and Consequences in Financial Planning (Course #5505E/QAS5505E) Table of Contents Page PART

Highlights of the Senate Tax Cuts and Jobs Act

WEALTH SOLUTIONS GROUP Highlights of the Senate Tax Cuts and Jobs Act The Senate passed a bill with the same name as the House, but with plenty of other differences The Senate version of a tax reform proposal

WEALTH SOLUTIONS GROUP Highlights of the Senate Tax Cuts and Jobs Act The Senate passed a bill with the same name as the House, but with plenty of other differences The Senate version of a tax reform proposal

What Federal Tax Reform Means for State and Local Tax and Fiscal Policies

What Federal Tax Reform Means for State and Local Tax and Fiscal Policies Kim Rueben * Senior Fellow, Urban Brookings Tax Policy Center www.taxpolicycenter.org Testimony before the Senate Committee on

What Federal Tax Reform Means for State and Local Tax and Fiscal Policies Kim Rueben * Senior Fellow, Urban Brookings Tax Policy Center www.taxpolicycenter.org Testimony before the Senate Committee on

July 31, First Street NE, Suite 510 Washington, DC Tel: Fax:

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org July 31, 2012 PROPOSED TAX REFORM REQUIREMENTS WOULD INVITE HIGHER DEFICITS AND A SHIFT

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org July 31, 2012 PROPOSED TAX REFORM REQUIREMENTS WOULD INVITE HIGHER DEFICITS AND A SHIFT

Chapter 02 Policy Standards for a Good Tax

Chapter 02 Policy Standards for a Good Tax True / False Questions 1. A tax meets the standard of sufficiency if it is easy for people to pay the tax. 2. The federal government is not required to pay interest

Chapter 02 Policy Standards for a Good Tax True / False Questions 1. A tax meets the standard of sufficiency if it is easy for people to pay the tax. 2. The federal government is not required to pay interest

On Tax-Transfer Integration: Let Us Return to the Ability-To-Pay Principle

On Tax-Transfer Integration: Let Us Return to the Ability-To-Pay Principle Thomas A. Wilson* The attempt to replace the type of welfare or means-tested support for the poor with a much simpler system through

On Tax-Transfer Integration: Let Us Return to the Ability-To-Pay Principle Thomas A. Wilson* The attempt to replace the type of welfare or means-tested support for the poor with a much simpler system through

TESTIMONY OF BRUCE MARKS. Chief Executive Officer. Neighborhood Assistance Corporation of America (NACA)

") TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

TESTIMONY OF BRUCE MARKS Chief Executive Officer Neighborhood Assistance Corporation of America (NACA) My name is Bruce Marks. I am Chief Executive Officer of the Neighborhood Assistance Corporation of

Year-end tax planning for 2017 Things to consider

Year-end tax planning for 2017 Things to consider Case Sabatini Contact information: 470 Streets Run Road Pittsburgh, PA 15236 412.881.4411 1 CaseSabatini.com Reminder about due dates March 15 (Extend

Year-end tax planning for 2017 Things to consider Case Sabatini Contact information: 470 Streets Run Road Pittsburgh, PA 15236 412.881.4411 1 CaseSabatini.com Reminder about due dates March 15 (Extend

PERSONAL INCOME TAXES IN THAILAND THE UNITED STATES. 1. The Tax Base: Basic Rules for Calculating Taxable Income and Why Much of Income Is Untaxed

19/11/2015 C h a p t e r 14 PERSONAL INCOME TAXES IN THAILAND THE UNITED STATES Public Finance, 10 th Edition David N. Hyman Adapted by Chairat Aemkulwat for Public Economics 2952331 Outline: Chapter 14

19/11/2015 C h a p t e r 14 PERSONAL INCOME TAXES IN THAILAND THE UNITED STATES Public Finance, 10 th Edition David N. Hyman Adapted by Chairat Aemkulwat for Public Economics 2952331 Outline: Chapter 14

Tax Alliance for Economic Mobility: Asset Building Tax Policy Reform Proposals Original April 2014, with updates April 2015

Tax Alliance for Economic Mobility: Asset Building Tax Policy Reform Proposals Original April 2014, with updates April 2015 PROPOSAL BACKGROUND RESOURCES Child Savings Universal savings accounts at birth

Tax Alliance for Economic Mobility: Asset Building Tax Policy Reform Proposals Original April 2014, with updates April 2015 PROPOSAL BACKGROUND RESOURCES Child Savings Universal savings accounts at birth

Governor s tax cut plan sets stage for service cuts Reforms for fairness and simplicity could be achieved without losing revenue

Governor s tax cut plan sets stage for service cuts Reforms for fairness and simplicity could be achieved without losing revenue By Peter S. Fisher Summary Iowa s General Assembly opened with promises

Governor s tax cut plan sets stage for service cuts Reforms for fairness and simplicity could be achieved without losing revenue By Peter S. Fisher Summary Iowa s General Assembly opened with promises

Dallas CPA Society CPE Conference

Dallas CPA Society CPE Conference What We re Going to Cover Section 7216 Brief History Only criminal penalty applicable to preparers Prohibits misuse of taxpayer information Regs 1/1/09 required advance

Dallas CPA Society CPE Conference What We re Going to Cover Section 7216 Brief History Only criminal penalty applicable to preparers Prohibits misuse of taxpayer information Regs 1/1/09 required advance

THE NATIONAL COMMISSION ON FISCAL RESPONSIBILITY AND REFORM. The Moment of Truth

THE NATIONAL COMMISSION ON FISCAL RESPONSIBILITY AND REFORM The Moment of Truth DECEMBER 2010 II. Tax Reform America's tax code is broken and must be reformed. In the quarter century since the last comprehensive

THE NATIONAL COMMISSION ON FISCAL RESPONSIBILITY AND REFORM The Moment of Truth DECEMBER 2010 II. Tax Reform America's tax code is broken and must be reformed. In the quarter century since the last comprehensive

Trump s Tax Scam: What can we expect from the Tax Cuts and Jobs Act and how can we resist it? by Peter Bohmer February 23, 2018

Trump s Tax Scam: What can we expect from the Tax Cuts and Jobs Act and how can we resist it? by Peter Bohmer February 23, 2018 The December 2017 tax deform legislation, The Tax Cuts and Jobs Act (TCJA)

Trump s Tax Scam: What can we expect from the Tax Cuts and Jobs Act and how can we resist it? by Peter Bohmer February 23, 2018 The December 2017 tax deform legislation, The Tax Cuts and Jobs Act (TCJA)

Tax Planning Guide

ATA CPA GROUP, LLC 2014-2015 Tax Planning Guide 2014-2015 Brought to you by ATA CPA GROUP, LLC Individual Taxes Do you contribute to a retirement savings plan at work? With an employer-sponsored retirement

ATA CPA GROUP, LLC 2014-2015 Tax Planning Guide 2014-2015 Brought to you by ATA CPA GROUP, LLC Individual Taxes Do you contribute to a retirement savings plan at work? With an employer-sponsored retirement

DeLeon & Stang, CPAs and Advisors

Dear Clients and Friends: This year-end tax planning letter is intended only to serve as a general guideline. Of course, your personal circumstances may require in-depth examination. We would be glad to

Dear Clients and Friends: This year-end tax planning letter is intended only to serve as a general guideline. Of course, your personal circumstances may require in-depth examination. We would be glad to

A Whole New Ballgame: How Tax Reform Will Affect Individuals and Businesses Tax Reform Guide.

2018 Tax Reform Guide A Whole New Ballgame: How Tax Reform Will Affect Individuals and Businesses Copyright 2018 Adam Shay CPA, PLLC. All rights reserved. A Whole New Ballgame: How Tax Reform Will Affect

2018 Tax Reform Guide A Whole New Ballgame: How Tax Reform Will Affect Individuals and Businesses Copyright 2018 Adam Shay CPA, PLLC. All rights reserved. A Whole New Ballgame: How Tax Reform Will Affect

Barn Report. A Dairy Keeper Resource

Barn Report. A Dairy Keeper Resource January 20, 2012 Report 12.017 A Laundry List of 2011 Tax Law Changes This page was last updated January 10, 2011. Please check back regularly as the tax laws will

Barn Report. A Dairy Keeper Resource January 20, 2012 Report 12.017 A Laundry List of 2011 Tax Law Changes This page was last updated January 10, 2011. Please check back regularly as the tax laws will

Tax-cutting time is ticking away. Review options for accelerating income. Dear Clients and Friends,

Dear Clients and Friends, Taxes are going to be a major issue for the rest of 2012 and for much of 2013. On January 1, 2013, the country faces what Federal Reserve Chairman Ben Bernanke has called a fiscal

Dear Clients and Friends, Taxes are going to be a major issue for the rest of 2012 and for much of 2013. On January 1, 2013, the country faces what Federal Reserve Chairman Ben Bernanke has called a fiscal

Chapter 12. The Design of the Tax System. Introduction. Introduction. In this chapter, look for the answers to these questions:

Chapter 12. The Design of the Tax System Introduction One of the Ten Principles from Chapter 1: A government can sometimes improve market outcomes. providing public goods regulating use of common resources

Chapter 12. The Design of the Tax System Introduction One of the Ten Principles from Chapter 1: A government can sometimes improve market outcomes. providing public goods regulating use of common resources

INTRODUCTION TAXES: EQUITY VS. EFFICIENCY WEALTH PERSONAL INCOME THE LORENZ CURVE THE SIZE DISTRIBUTION OF INCOME

INTRODUCTION Taxes affect production as well as distribution. This creates a potential tradeoff between the goal of equity and the goal of efficiency. The chapter focuses on the following questions: How

INTRODUCTION Taxes affect production as well as distribution. This creates a potential tradeoff between the goal of equity and the goal of efficiency. The chapter focuses on the following questions: How

Deficit Day to Bankruptcy Day

Deficit Day to Bankruptcy Day April 2014 copies of this presentation can be found at Jan 1 Dec 31 Deficit Day! How much government spending do people fund with their tax dollars? Top 1% 56 days 2% to 5%

Deficit Day to Bankruptcy Day April 2014 copies of this presentation can be found at Jan 1 Dec 31 Deficit Day! How much government spending do people fund with their tax dollars? Top 1% 56 days 2% to 5%

Here is a quick summary of most-important tax changes starting with those that affect individuals. Payroll Tax Holiday Is Over

January 11, 2013 To Our Clients and Friends: The American Taxpayer Relief Act of 2012 (better known as the fiscal cliff legislation) became law on 1/2/13. Due to the expiration of the so-called payroll

January 11, 2013 To Our Clients and Friends: The American Taxpayer Relief Act of 2012 (better known as the fiscal cliff legislation) became law on 1/2/13. Due to the expiration of the so-called payroll

Separate here and give Form W-4 to your employer. Keep the top part for your records. Employee s Withholding Allowance Certificate

Form W-4 (2017) Purpose. Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. Consider completing a new Form W-4 each year and when your personal or financial

Form W-4 (2017) Purpose. Complete Form W-4 so that your employer can withhold the correct federal income tax from your pay. Consider completing a new Form W-4 each year and when your personal or financial

Year-End Tax Planning Letter

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2013 Year-End Tax Planning Letter 54 North Country Road Miller Place, NY 11764 (877) 474-3747 or (631) 474-9400 www.ceschinipllc.com Introduction Tax planning is inherently complex, with the most powerful

2013 NEW DEVELOPMENTS LETTER

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

Tax Policy for Low-Income Families: The Earned Income Tax Credit

Tax Policy for Low-Income Families: The Earned Income Tax Credit Hilary Hoynes, University of California, Davis Tax Policy in the Obama Era January 30, 2009 1 Overview and Issues In the last 15 years,

Tax Policy for Low-Income Families: The Earned Income Tax Credit Hilary Hoynes, University of California, Davis Tax Policy in the Obama Era January 30, 2009 1 Overview and Issues In the last 15 years,

ECON 1100 Global Economics (Fall 2013) The Distribution Function of Government portions for Exam 4

The Distribution Function of Government portions for Exam 4") ECON 1100 Global Economics (Fall 2013) The Distribution Function of Government portions for Exam 4 Relevant Readings from the Required Textbooks: Economics Chapter 12, Income Distribution and Poverty Problems

ECON 1100 Global Economics (Fall 2013) The Distribution Function of Government portions for Exam 4 Relevant Readings from the Required Textbooks: Economics Chapter 12, Income Distribution and Poverty Problems

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 16, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Top Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 16, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Top Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the

Tax Briefing Tax Cuts and Jobs Act December 4, 2017 Highlights Changes to Individual Tax Rates Special Tax Rules for Pass-Throughs Enhanced Child Tax Credit Larger Standard Deduction Corporate Tax Rate

Tax Briefing Tax Cuts and Jobs Act December 4, 2017 Highlights Changes to Individual Tax Rates Special Tax Rules for Pass-Throughs Enhanced Child Tax Credit Larger Standard Deduction Corporate Tax Rate

2017 YEAR-END. tax planning INDIVIDUALS. guide for

2017 YEAR-END tax planning INDIVIDUALS guide for year in review 2017 is unlike any previous tax year. Major congressional tax reform proposals that generally would go into effect in 2018 if signed into

2017 YEAR-END tax planning INDIVIDUALS guide for year in review 2017 is unlike any previous tax year. Major congressional tax reform proposals that generally would go into effect in 2018 if signed into

Year-end Tax Moves for 2015

Year-end Tax Moves for 2015 PRESENTED BY: One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal,

Year-end Tax Moves for 2015 PRESENTED BY: One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal,

Year-end Tax Moves for 2017

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

ISSUE BRIEF. The House and Senate each passed slightly different. Improving the Tax Cuts and Jobs Act: A Path for the Conference Committee

ISSUE BRIEF No. 4794 Improving the Tax Cuts and Jobs Act: A Path for the Conference Committee Adam N. Michel The House and Senate each passed slightly different versions of the Tax Cuts and Jobs Act. The

ISSUE BRIEF No. 4794 Improving the Tax Cuts and Jobs Act: A Path for the Conference Committee Adam N. Michel The House and Senate each passed slightly different versions of the Tax Cuts and Jobs Act. The

Summary An issue in the development of the new health care reform plan is the effect on small business. One concern is the effect of a pay or play man

Jane G. Gravelle Senior Specialist in Economic Policy October 2, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov R40775 Summary

Jane G. Gravelle Senior Specialist in Economic Policy October 2, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 www.crs.gov R40775 Summary

Solutions Network Tax Services

Solutions Network Tax Services Fax 877 469 4558 Phone 877 604 6636 ext 3 Information Needed to Prepare U.S. Tax Return Please send copies of W2s, and evidence of foreign income (if any) and any 1099s received.

Solutions Network Tax Services Fax 877 469 4558 Phone 877 604 6636 ext 3 Information Needed to Prepare U.S. Tax Return Please send copies of W2s, and evidence of foreign income (if any) and any 1099s received.

Chapter 1 Introduction to Federal Taxation and Understanding the Federal Tax Law

1 Introduction to Federal Taxation and Understanding the Federal Tax Law SUMMARY OF CHAPTER This chapter presents information on the magnitude of federal taxes collected and on taxpayer obligations. Also,

1 Introduction to Federal Taxation and Understanding the Federal Tax Law SUMMARY OF CHAPTER This chapter presents information on the magnitude of federal taxes collected and on taxpayer obligations. Also,

TAX QUESTIONS

This Questionnaire is one of the FIVE Minimum Tax Packet Items Page 1 of 7 Taxpayer Names This short questionnaire covers most of the tax reporting areas that I need to know about to prepare accurate tax

This Questionnaire is one of the FIVE Minimum Tax Packet Items Page 1 of 7 Taxpayer Names This short questionnaire covers most of the tax reporting areas that I need to know about to prepare accurate tax

Dear Client: Basic Numbers You Need to Know

Dear Client: As 2013 draws to a close, there is still time to reduce your 2013 tax bill and plan ahead for 2014. This letter highlights several potential tax-saving opportunities for you to consider. I

Dear Client: As 2013 draws to a close, there is still time to reduce your 2013 tax bill and plan ahead for 2014. This letter highlights several potential tax-saving opportunities for you to consider. I

HEALTH INSURANCE DEDUCTION OF LITTLE HELP TO THE UNINSURED. by Joel Friedman and Iris J. Lav

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org Revised October 18, 2000 HEALTH INSURANCE DEDUCTION OF LITTLE HELP TO THE UNINSURED

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org Revised October 18, 2000 HEALTH INSURANCE DEDUCTION OF LITTLE HELP TO THE UNINSURED

Learning from Opportunity Zones: How to improve place-based policies

Report Learning from Opportunity Zones: How to improve place-based policies Hilary Gelfond and Adam LooneyFriday, October 19, 2018 C ongress created Opportunity Zones to funnel investment to economically

Report Learning from Opportunity Zones: How to improve place-based policies Hilary Gelfond and Adam LooneyFriday, October 19, 2018 C ongress created Opportunity Zones to funnel investment to economically

Before we get to specific suggestions, here are two important considerations to keep in mind.

November 1, 2017 To Our Clients and Friends: As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. This has been an interesting year in

November 1, 2017 To Our Clients and Friends: As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. This has been an interesting year in

Redistribution and Tax Expenditures: The Earned Income Tax Credit

Redistribution and Tax Expenditures: The Earned Income Tax Credit Nada Eissa, Georgetown University Hilary Hoynes, University of California, Davis Tax Expenditures Project Conference March 2008 1 Overview

Redistribution and Tax Expenditures: The Earned Income Tax Credit Nada Eissa, Georgetown University Hilary Hoynes, University of California, Davis Tax Expenditures Project Conference March 2008 1 Overview

Charitable Giving After the Tax Cuts and Jobs Act

Charitable Giving After the Tax Cuts and Jobs Act Giving and the Tax Cuts and Jobs Act In the fall of 2017, members of Congress and the President declared that they would complete tax reform by the end

Charitable Giving After the Tax Cuts and Jobs Act Giving and the Tax Cuts and Jobs Act In the fall of 2017, members of Congress and the President declared that they would complete tax reform by the end

PERSONAL INCOME TAXES

PERSONAL INCOME TAXES CHAPTER OBJECTIVES After you have taxed your patience and gotten to the end of this chapter you will understand the rudiments of how taxes work. You should understand the concepts

PERSONAL INCOME TAXES CHAPTER OBJECTIVES After you have taxed your patience and gotten to the end of this chapter you will understand the rudiments of how taxes work. You should understand the concepts

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

THE BEST RETIREMENT INVESTMENT OPTIONS

THE BEST RETIREMENT INVESTMENT OPTIONS by Lew Nason, RFC, LUTCF, CFLA If you could design your ultimate retirement savings vehicle, what benefits or features would you like it to have? Let your imagination

THE BEST RETIREMENT INVESTMENT OPTIONS by Lew Nason, RFC, LUTCF, CFLA If you could design your ultimate retirement savings vehicle, what benefits or features would you like it to have? Let your imagination

A POST-HURRICANE POLICY RESPONSE TO POVERTY IN AMERICA Ray Boshara, Reid Cramer, Leslie Parrish, and Anne Stuhldreher

October 2005 A POST-HURRICANE POLICY RESPONSE TO POVERTY IN AMERICA Ray Boshara, Reid Cramer, Leslie Parrish, and Anne Stuhldreher The recent hurricanes wrought havoc on families and communities across

October 2005 A POST-HURRICANE POLICY RESPONSE TO POVERTY IN AMERICA Ray Boshara, Reid Cramer, Leslie Parrish, and Anne Stuhldreher The recent hurricanes wrought havoc on families and communities across

THE MIDDLE-CLASS SQUEEZE: DC s Tax System Falls Most Heavily on Moderate-Income Families

THE MIDDLE-CLASS SQUEEZE: DC s Tax System Falls Most Heavily on Moderate-Income Families December 1, 2009 Families in the District with incomes of $20,000 to $60,000 pay one-tenth of their incomes in DC

THE MIDDLE-CLASS SQUEEZE: DC s Tax System Falls Most Heavily on Moderate-Income Families December 1, 2009 Families in the District with incomes of $20,000 to $60,000 pay one-tenth of their incomes in DC