Overview. How many Town Accountant's come across payroll issues?

|

|

|

- Kristopher Curtis

- 5 years ago

- Views:

Transcription

1 Eric Kinsherf, CPA

2 Introduction There are a variety of payroll related issues that are encountered by the Town Accountant The Town Accountant's role in the payroll is shared with the Treasurer Town Accountant should be aware of all the issues associated with payroll There are plenty of resources for both the Town Accountant and Treasurer

3 Agenda Overview Payroll Warrants Federal and State filing requirements Payroll Calculations Reconciling Withholding Accounts FLSA IRS Employee/Contractor Classification Other Payroll Issues Summarize

4 Overview How many Town Accountant's come across payroll issues? Goal: to address issues and come away with a deeper understanding of the Payroll process

5 Payroll Warrants

6 Payroll Methods In-House using Municipal Software Treasurer files required reports Treasurer reconciles & produces W2s Treasurer prints checks or direct deposits Treasurer makes withholding payments Warrant & Journal entries produced from System Treasurer s payroll position is critical Treasurer responsible for Maintenance of Software and Data Security Outsourced Payroll Outsourced vendor files required reports Vendor produces W2s Vendor prints checks or direct deposits Vendor makes withholding payments Typically, warrant produced in system after importing journal entry from the vendor Some of the Risk are mitigated Outsourced vendor responsible for Maintenance of Software and Data Security

7 Payroll Warrant Sample Process Sample process 1. Timesheet submitted by departments with a cover page summarizing accounts to be charged 2. Accountant checks pay rates to ensure conformance to contracts (Should happen) 3. Accountant totals all cover pages to get a total amount to be charged (Should happen) 4. Treasurer or Departments input timesheets into payroll system 5. Treasurer produces a summary report for the Accountant 6. Accountant reconciles the Total and Produces/Signs Payroll Warrant (Gross Payroll) 7. Warrant is countersigned by appropriate person(s) (Mayor, BOS, Town Manager) 8. Treasurer initiates distribution of checks and direct deposits

8 Payroll Segregation of Duties Reduces Risk of Fraud Where possible, the following payroll responsibilities should be segregated: Setting up New Employees and Terminating Employees Authorizing Wage Rates Entering or Changing Pay Rates in the Payroll System Entering time into the Payroll System Processing & Printing checks or making direct deposits Distribution of physical check Reconciliation of the payroll bank account

9 Federal and State Forms and Filing Requirements

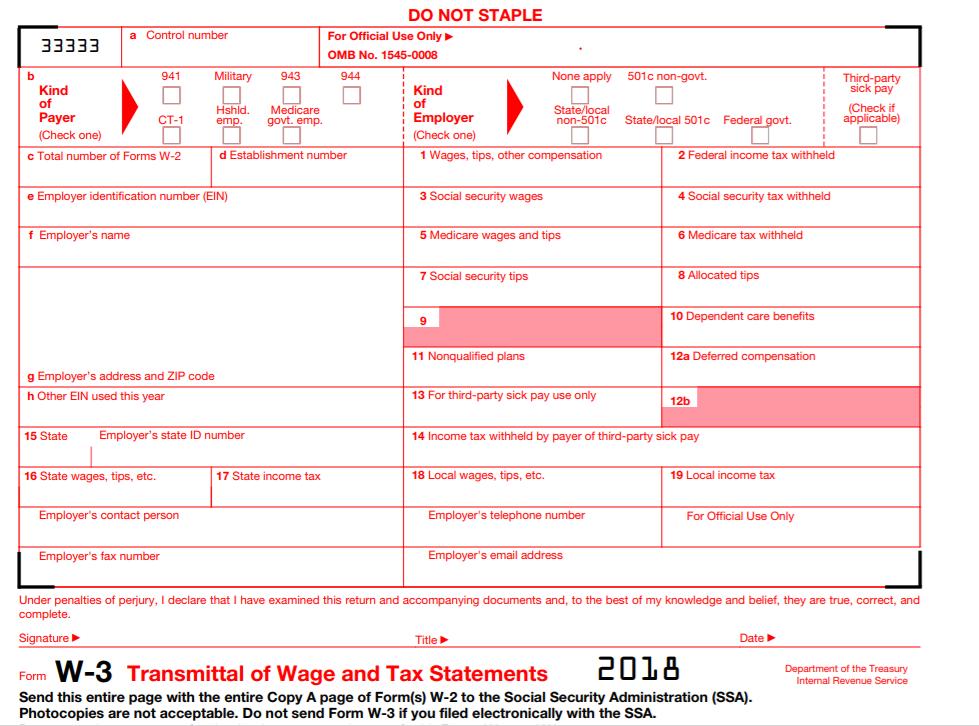

10 Federal & State Forms and Filing Requirements Forms Description Deadline W2s Employee Wage and Tax Statement W3 Transmittal of Income & Tax Statements W2 form that an employer must send to an employee and the IRS, SSA, and DOR Reports an employee's annual wages and the amount of taxes withheld Shows TOTAL earnings, Social Security wages, Medicare wages and withholding for all employees Annual can mail or digital form to employees Due: On or before January 31 Annual along with W2s - mail or e-file to IRS AND SSA Due: On or before January 31 M3 Reconciliation of Massachusetts Income Taxes Withheld for Employers Any employer filing 50 or more W-2s for a particular calendar year must submit the W-2 file to DOR in a "machine-readable form." A "machinereadable form" includes files uploaded through MassTaxConnect and electronic data transfers. Annual along with W2s - mail or e-file to Mass DOR unless greater than 50 W2s. Due: On or before January 31

11 W3 Form

12 M3 Form

13 SSA Verification Service The Social Security Number Verification Service (SSNVS) allows employers to match their record of employee names and Social Security numbers (SSNs) with Social Security records before preparing and submitting Forms W-2. Making sure names and SSNs on the W-2 match. Note: It is illegal to use the service to verify SSNs of potential new hires or contractors or in the preparation of tax returns.

14 SSA Accuwage Online Free application from Social Security Administration that enables you to check W-2 and W-2c (Corrected Wage and Tax Statement) Wage reports for correctness before uploading them to Business Services Online (BSO).

15 Federal & State Forms and Filing Requirements Forms Description Deadline 941 Employers Quarterly Federal Tax Return Report of wages paid to employees and withholdings made by employers. It also includes information on the employer's share of Medicare and Social Security taxes during the period reported Quarterly can mail or e-file. Due: April 30, July 31, October 31, and January Annual Federal Tax Return M941 Massachusetts State Tax Return or MassTaxConnect. Annual liability for social security, Medicare, and withheld federal income taxes is $1,000 or less Every employer who expects to withhold from $1,201 and $25,000 in income taxes per year must file Form M-941 on a monthly basis; from $101 and $1,200 in income taxes per year on a quarterly basis; or $100 or less on an annual basis. If greater than $25,000 than must file using MassTaxConnect. Annual and Due January 31 Monthly basis, return and payment are due on or before the 15th day of the month following the monthly withholding period, except for March, June, September and December; then due the last day of the month following the withholding period. Quarterly Same as 941 above Annual Same as 944 above

16 Federal & State Forms and Filing Requirements Forms Description Deadline Federal Unemployment Tax Act (FUTA) Return PAYMENTS BY THE EMPLOYER ONLY NO EMPLOYEE DEDUCTIONS An organization that is exempt from income tax under section 501(c)(3) of the Internal Revenue Code is also exempt from FUTA. Calculate the tax due on each employee's wages until they exceed the $7,000 threshold. The 2018 rate is 6 percent. Decrease this federal rate by up to 5.4 percent of the rate you pay to your state, sometimes referred to as SUTA tax. Although Form 940 covers a calendar year, you may have to deposit your FUTA tax before you file your return. If your FUTA tax is more than $500 for the calendar year, you must deposit at least one quarterly payment. You must determine when to deposit your tax based on the amount of your quarterly tax liability. Massachusetts Unemployment Tax WR-1 Employers Quarterly Report of Wages Paid. 2 methods Reimbursable (No payments till Employee Files Claim) or Contributory (Wages until exceed $15,000 threshold) Reimbursable State Bills Monthly for all Costs incurred. Contributory Quarterly. Assigned a rate not to exceed 4.61% Due 15 th after Quarter Month

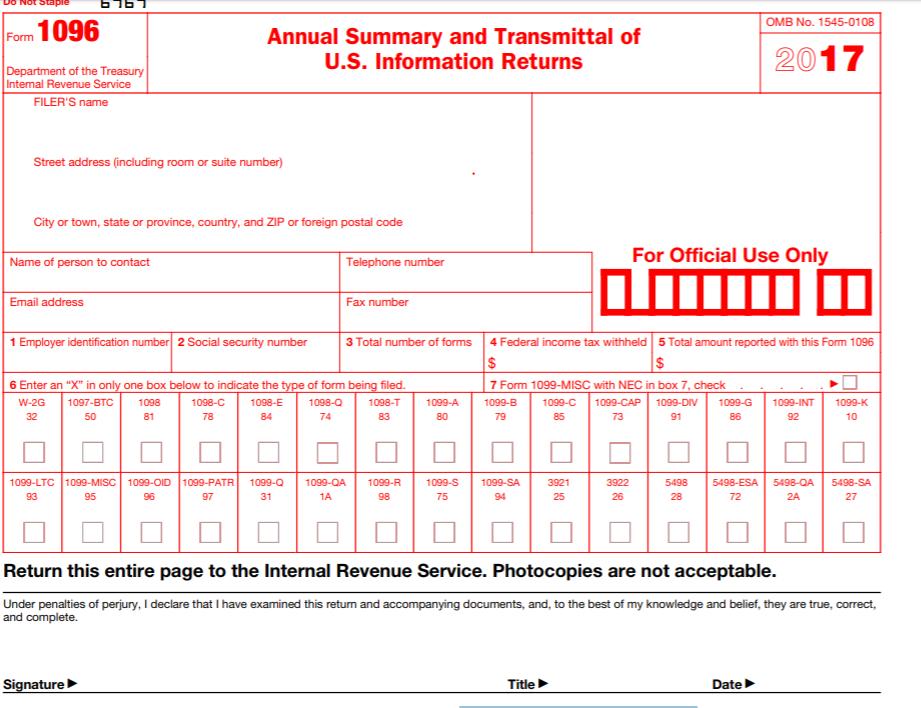

17 Federal & State Forms and Filing Requirements Forms Description Deadline 1095-C Employer-Provided Health Insurance Offer and Coverage 1096 Annual Summary and Transmittal of U.S. Information Returns 1099-MISC (Miscellaneous Income) Form sent to each Employee to show if enrolled in Employer-Provided Health Insurance. Form used when filing certain forms. See the Box to the right. General rule - Must issue to each person to whom you have paid at least $600 in rents, services (including parts and materials), prizes and awards, or other income payments. Generally, you must file 1095-C by February 28 if filing on paper (or March 31 if filing electronically) of the year following the calendar year to which the return relates. For calendar year 2017, 1095-C are required to be filed by February 28, 2018, or April 2, 2018, if filing electronically. File Form 1096 as follows. With Forms 1097, 1098, 1099, 3921, 3922, or W-2G, file by February 28, Caution: File Form MISC by January 31, 2018, if you are reporting nonemployee compensation in box 7. Also, check box 7 above. With Forms 5498, file by May 31, Due to Recipient by January 31

18 1096 Form

19 Payroll Calculations

20 Payroll Calculation Common Questions Salaried Employee with biweekly pay 26, 26.1 or 26.2? School Superintendent get paid 1/26 th of their salary on July 1 check? 27 payrolls in a fiscal or calendar year? Answer: Refer to the Union or Other Contract. Annual Pay: Annual Salary Working days in Year = Per Diem Rate. Receive the Exact Annual Salary within the fiscal year Hourly and weekly: Typically need to budget for an extra day. Not simply weekly pay times 52 weeks.

21 Payroll Calculations Common Questions When does the pay period end? Answer: Be aware that different groups can have different days the payroll week ends. This is common for Fire, Police School, DPW, and Clerical.

22 Reconciling Withholding Accounts

23 Reconciling Withholding Accounts Understanding the Accounting Entries: A. Payroll Warrant Processed Gross Payroll $50,000 Various Withholding Accounts $15,000 Cash (Net Payroll) $35,000 (SEE BELOW) Employee have Various Deductions withheld Cash $15,000 Federal W/H $4,000 Medicare $ 700 State Income W/H $2500 Child Support $500 Medical Insurance $2700 Dental Insurance $1000 Retirement $3000 Union Dues $ 600 Etc. B. When the payments are submitted to the Government or Company Debit the deduction account (employee portion) and Credit Cash

24 Reconciling Withholding Accounts Identify How and When the Payments are Made (Example) Deductions How When Federal Income Tax Electronically Treasurer submits payment right after warrant approved Medicare Electronically Same as above State Electronically Same as above Child Support Electronically Same as above Medical Insurance Check Insurance Company sends an invoice for the following month. Ex) In November sends the Invoice for December Premium. Dental Insurance Check Same as Medical Insurance Retirement Check Treasurer submits payment right after warrant approved Union Dues Check Treasurer reconciles monthly amount deducted by employee and completes voucher to be processed for payment.

25 Tips for reconciling Withholding Accounts Timely!! Ideally at least monthly. For Federal and State Withholdings, If submitting weekly payments then should have a zero balance or only the last payroll withholding amount. Identify differences and determine if timing or an error. For Insurance and Other withholdings accounts, where the company is paid monthly, ensure the portion of payment charge to the general ledger deduction account matches the employee amount withheld for that period. Identify differences and determine if timing or an error.

26 FLSA Wage and Hour

27 FLSA Overtime Final Rule December 1, 2016 the final rule updates the salary threshold under which most white-collar workers are entitled to Overtime. The threshold is $913 a week or $47,476 for a full year worked. Goal is Overtime Protection that leads to better work-life balance and can benefit employers by increasing productivity and decreasing turnover. FLSA notes that the new rule - minimal impact State and Local Governments.

28 FLSA Overtime Hours worked over 40 in a workweek at a rate not less than time and one-half their regular rates of pay. Different workweeks may be established for different employees or groups of employees. Averaging of hours over two or more weeks is not permitted. Does not require overtime pay for work on Saturdays, Sundays, holidays, or regular days of rest, unless overtime is worked on such days. Does not require Double Time.

29 What is included in OT Pay? Shift Differential Non-discretionary bonuses like Attendance Pay Longevity Pay Any money received by an employee "for work" is part of the employee's regular rate of pay. Example: Educational "stipends" such as money paid to employees who have attained a specified degree, and "tuition assistance" programs in which the employer pays all or part of the costs of courses successfully completed by employees. Educational Stipend is "compensation for work," includable in the regular rate. Tuition Reimbursement is not includable.

30 When is OT paid? The rule is that FLSA wages must be paid "when due," which normally means at the next regularly scheduled pay day. Late pay" is generally the same as "no pay" under the FLSA. This can be important because an employer that fails to pay wages when due may be liable for liquidated damages (double damages).

31 Fire & Law Enforcement Work Periods Public-sector (government) Fire or Police departments may establish special "7(k) work periods" for sworn firefighters or Law Enforcement, which can increase the FLSA overtime "thresholds" beyond the normal 40 hour week. Work period may be 7 to 28 consecutive days. OT is required when hours worked in the work period exceed maximum hours outlined in the formula in the regulations (Police 43 hours/7 days and Fire is 53 hours/per 7 days) OT is determined and paid out at the end of a work period. Example: Work period = 14 days Regulation (Police) = After working 86 hours must receive OT. Regulation (Fire) = After working 106 hours must receive OT.

32 IRS Employee vs Contractor Classification

33 Employee vs Independent Contractor In any employee-independent contractor determination, all information that provides evidence of the degree of control and the degree of independence must be considered. Facts that provide evidence of the degree of control and independence fall into 3 categories: 1. Behavioral control 2. Financial control 3. Type of relationship of parties If unsure, recommend contacting an attorney or the IRS determine by filing form SS-8. Source: 2018 IRS Publication 15-A

34 Employee or Independent Contractor? Jack contracted with a Town to complete a roof. Following: 1. Jack is doing business as Plum Roofing 2. Signed Contract with flat rate for service 3. Jack is a Licensed Roofer, carries Workmen s Comp & Liability Insurance 4. Jack hires his own roofers who are treated as employees 5. Jack is responsible for any problems with the roofing work

35 Employee or Independent Contractor? Jill accepts a position as a Substitute Teacher at a School 1. Jill is provided instructions on when, where, and how to do the work. 2. Jill is to use the School Equipment and Supplies. 3. Jill is to attend the School training program prior to working at the School. 4. Jill is guaranteed a regular hourly wage amount and provided some employee type benefits such as insurance, vacation and sick pay. 5. Jill receives an annual performance review from the School.

36 Other Payroll Issues

37 Other Payroll Issues Senior Tax Work-Off Abatement IGR Handout Impute Value of Take home vehicle (Slide) IRS Accountable/Non Accountable Plans IOD, W/C, Disability, 3 rd Party Sick Pay (Not Taxable) 403B(Tax Sheltered Annuities)/457B (Deferred Comp) MA state law allowing for retention of fees Election workers FICA/OBRA Exemption ($1,800 annual wages) Public vs. Redacted (Slide)

38 Fringe Benefit: Personal Use of Municipal Provided Vehicle IRS Options: 1. Lease Value Rule = Annual Lease Value (IRS Table) * % Personal Use 2. Cents-Per-Mile Rule = IRS Mileage Rate * Personal Mileage 3. Commuting Value Rule = One way Commute ($1.50) * Number of One Ways **IRS Publication 15-B for Details Payroll System Processing a Year End (Fringe Benefit) Adjustment: No increase to Net Pay Taxed as regular wages Reported on Form W-2 Box 14

39 Public vs Redacted Employee records must be produced as public records in response to a request seeking information regularly kept in a staff directory, payroll database or similar, such as employee names, job classification, salary information, etc. List of Exemptions from disclosure under MGL, Chapter 4, Section 7(26)(c) if not sure what Exemption to use seek legal counsel. Exemption (c) The Privacy Exemption is the most frequently invoked exemption. The language of the exemption limits its application to: personnel and medical files or information; also any other materials or data relating to a specifically named individual, the disclosure of which may constitute an unwarranted invasion of personal privacy.

40 Request for Information Fee Municipalities with a population of over 20,000 may not assess a fee for the first two hours of time spent searching for, compiling, segregating, redacting and reproducing a requested record. Municipalities with a population of 20,000 and under may assess a fee, including the first two hours, for time spent searching for, compiling, segregating, redacting and reproducing a requested record. Population data shall be determined by the decennial US. Census and it shall be the burden of the RAO to provide population data information when responding to a request. A municipal records access officer may not assess a fee of more than $25 per hour for the cost to comply with a request for public records unless approved by the Supervisor through a petition process.

41 Summarize There are a variety of payroll related issues that are encountered by the Town Accountant The Town Accountant's role in the payroll is shared with the Treasurer Town Accountant should be aware of all the issues associated with payroll There are plenty of resources for both the Town Accountant and Treasurer

PAYROLL SOURCE TABLE OF CONTENTS

PAYROLL SOURCE TABLE OF CONTENTS SECTION 1: THE EMPLOYER-EMPLOYEE RELATIONSHIP 1.1 Importance of the Determination... 1-2 1.2 Employee vs. Independent Contractor... 1-2 1.2-1 Common Law Test... 1-3 1.2-2

PAYROLL SOURCE TABLE OF CONTENTS SECTION 1: THE EMPLOYER-EMPLOYEE RELATIONSHIP 1.1 Importance of the Determination... 1-2 1.2 Employee vs. Independent Contractor... 1-2 1.2-1 Common Law Test... 1-3 1.2-2

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005 Agenda 1. Federal Payroll Filings a. Payroll Related Forms b. Proper Completion of Federal Forms c. Federal Payroll

Archdiocese of Baltimore- Federal, State, & Other Filing Requirements January 13, 2005 Agenda 1. Federal Payroll Filings a. Payroll Related Forms b. Proper Completion of Federal Forms c. Federal Payroll

The Small Business Employment Tax Guide

The Small Business Employment Tax Guide Roanoke Regional Small Business Development Center 210 S. Jefferson Street, Roanoke, Virginia 24011 www.roanokesmallbusiness.org Roanoke Small Business Development

The Small Business Employment Tax Guide Roanoke Regional Small Business Development Center 210 S. Jefferson Street, Roanoke, Virginia 24011 www.roanokesmallbusiness.org Roanoke Small Business Development

Worker Classification: Employee or Independent Contractor?

Worker Classification: Employee or Independent Contractor? Doug Blade July 24, 2013 A Note Before We Begin This presentation is designed to provide information not specific determination for any situation.

Worker Classification: Employee or Independent Contractor? Doug Blade July 24, 2013 A Note Before We Begin This presentation is designed to provide information not specific determination for any situation.

2017 Take Home Quiz #1

Employee/Independent Contractor 1. To satisfy the Reasonable Basis test and treat a worker as an independent contractor, a company can rely on all of the following methods EXCEPT: A. a private letter ruling

Employee/Independent Contractor 1. To satisfy the Reasonable Basis test and treat a worker as an independent contractor, a company can rely on all of the following methods EXCEPT: A. a private letter ruling

Payroll Management Edition. Steven M. Bragg

Payroll Management 2018 Edition Steven M. Bragg Chapter 1 Payroll Management... 1 Learning Objectives... 1 Introduction... 1 Payroll Cycle Duration... 1 Streamlined Timekeeping... 3 Electronic Payments...

Payroll Management 2018 Edition Steven M. Bragg Chapter 1 Payroll Management... 1 Learning Objectives... 1 Introduction... 1 Payroll Cycle Duration... 1 Streamlined Timekeeping... 3 Electronic Payments...

2017 Year-End Tax Memo

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

2017 Year-End Tax Memo An Annual Publication of Large & Gilbert, Inc. January 2018 Large & Gilbert, Inc., is a full service CPA firm specializing in Accounting, Tax, Consulting, Business Advisory, Wealth

Chapter 8: Payroll Accounting: Employee Earnings and Deductions Lecture Notes

Chapter 8: Payroll Accounting: Employee Earnings and Deductions Lecture Notes I. Employees and Independent Contractors A. Distinction 1. Employees a) Works under the control and direction of an employer.

Chapter 8: Payroll Accounting: Employee Earnings and Deductions Lecture Notes I. Employees and Independent Contractors A. Distinction 1. Employees a) Works under the control and direction of an employer.

Section 6 Withholding Taxes (Student Guide) Table of Contents Introduction

Table of Contents Introduction") Section 6 Withholding Taxes (Student Guide) Table of Contents Introduction... - 2 - Topics from Content Outline... - 2 - The Principle of Actual or Constructive Payment... - 2 - Social Security Numbers...

Section 6 Withholding Taxes (Student Guide) Table of Contents Introduction... - 2 - Topics from Content Outline... - 2 - The Principle of Actual or Constructive Payment... - 2 - Social Security Numbers...

Chapter 1: Payroll Fundamentals Challenges Concepts

Table of Chapter 1: Payroll Fundamentals.... 1-1 1.1 Challenges... 1-1 1.2 Concepts.... 1-2 1.2.1 Employees vs. Independent Contractors...1-3 1.2.2 Common Law and Reasonable Basis Tests...1-4 1.2.3 Temporary

Table of Chapter 1: Payroll Fundamentals.... 1-1 1.1 Challenges... 1-1 1.2 Concepts.... 1-2 1.2.1 Employees vs. Independent Contractors...1-3 1.2.2 Common Law and Reasonable Basis Tests...1-4 1.2.3 Temporary

This is a list of items you should gather for the Income Tax Preparation

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

Welcome to our Annual Payroll Update Webinar

2018 Payroll Year End Update Presented by: Tammy Mearig & Beth Landis December 18, 2018 Welcome Welcome to our Annual Payroll Update Webinar 1 Agenda Payroll Information Brochure Review What s New and

2018 Payroll Year End Update Presented by: Tammy Mearig & Beth Landis December 18, 2018 Welcome Welcome to our Annual Payroll Update Webinar 1 Agenda Payroll Information Brochure Review What s New and

YEAR-END UPDATE FOR PAYROLL AND RELATED TAXES WITH ADDITIONAL INFORMATION FOR INDIVIDUALS

YEAR-END UPDATE FOR PAYROLL AND RELATED TAXES WITH ADDITIONAL INFORMATION FOR INDIVIDUALS JANUARY 2011 This memo provides information that is useful in the annual preparation of employment related forms

YEAR-END UPDATE FOR PAYROLL AND RELATED TAXES WITH ADDITIONAL INFORMATION FOR INDIVIDUALS JANUARY 2011 This memo provides information that is useful in the annual preparation of employment related forms

2016 Year End Guide. Dear Valued Payroll Dynamics Client,

2016 Year End Guide Dear Valued Payroll Dynamics Client, The end of 2016 is approaching! Payroll Dynamics knows that our clients rely on us to guide them through the complexities of year-end payroll and

2016 Year End Guide Dear Valued Payroll Dynamics Client, The end of 2016 is approaching! Payroll Dynamics knows that our clients rely on us to guide them through the complexities of year-end payroll and

Kula Aupuni Niihau A Kahelelani Aloha (KANAKA) Public Charter School (PCS)

Public Charter School (PCS)") Kula Aupuni Niihau A Kahelelani Aloha (KANAKA) Public Charter School (PCS) KANAKA Financial Operations Manual Prepared by: Carbonaro CPAs & Management Group 1885 Main Street, Suite 408, Wailuku, HI 96793

Kula Aupuni Niihau A Kahelelani Aloha (KANAKA) Public Charter School (PCS) KANAKA Financial Operations Manual Prepared by: Carbonaro CPAs & Management Group 1885 Main Street, Suite 408, Wailuku, HI 96793

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM Verification of reported member city payrolls is vital to the financial integrity of the association. As set forth under

MISSOURI INTERGOVERNMENTAL RISK MANAGEMENT ASSOCIATION PAYROLL VERIFICATION PROGRAM Verification of reported member city payrolls is vital to the financial integrity of the association. As set forth under

Chapter 5 Eligible Earnings

IN THIS CHAPTER: PERA-Eligible Salary Compensation that is not Salary Closer Look at Some Types of Pay Workers Compensation Payments Pay while on Personal, Parental or Military Leave Members on Paid Medical

IN THIS CHAPTER: PERA-Eligible Salary Compensation that is not Salary Closer Look at Some Types of Pay Workers Compensation Payments Pay while on Personal, Parental or Military Leave Members on Paid Medical

TECH FLEX. In the announcement increasing the mileage rates, IRS Commissioner Doug Shulman stated the following:

JULY 2008 TECH FLEX ISSUE VII The topics covered in this issue are: Benefits: IRS Increases Mileage Reimbursement Rates Further HSA Guidance Released by IRS CMS Releases Updated Medicare Part D Notices

JULY 2008 TECH FLEX ISSUE VII The topics covered in this issue are: Benefits: IRS Increases Mileage Reimbursement Rates Further HSA Guidance Released by IRS CMS Releases Updated Medicare Part D Notices

2018 Payroll Update Reference Guide

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

2018 Payroll Update Reference Guide Jones & Roth is providing this Payroll Update as a reference guide for you. It is not meant to be all-inclusive. If there is a payroll item that you have questions about,

PAYROLL & RELATED TAX ISSUES. Bruce A. Beyler, CPA

PAYROLL & RELATED TAX ISSUES Bruce A. Beyler, CPA Index of Topics u u u Worker Classification Compensation Fringe Benefits u Some New Items for 2016 u u u u Wage & Tax Statement (Form W-2) and Box 12 Codes

PAYROLL & RELATED TAX ISSUES Bruce A. Beyler, CPA Index of Topics u u u Worker Classification Compensation Fringe Benefits u Some New Items for 2016 u u u u Wage & Tax Statement (Form W-2) and Box 12 Codes

Terms. Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go!

Payroll Unit Terms Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go! Payroll Pay Periods Weekly 52 checks a year Biweekly 26 checks a year, every other

Payroll Unit Terms Write down as many payroll terms or payroll taxes that you can think of in 2 minutes. Ready, Set, Go! Payroll Pay Periods Weekly 52 checks a year Biweekly 26 checks a year, every other

Development of year-end work plan Create the year-end team (e.g., Payroll, HR, IT, and Accounting) and focus on the following tasks:

and focus on the following tasks:") Presentation topics > Development of year-end work plan > Management and completion of year-end tasks > Form W-4 compliance > Social Security number (SSN) verification > Form W-2 reporting > IRS Publication

Presentation topics > Development of year-end work plan > Management and completion of year-end tasks > Form W-4 compliance > Social Security number (SSN) verification > Form W-2 reporting > IRS Publication

BASIC EMPLOYER PAYROLL ISSUES

BASIC EMPLOYER PAYROLL ISSUES It's important to have a basic understanding of your tax obligations as an employer since Federal and State laws have numerous requirements that must be met from both a legal

BASIC EMPLOYER PAYROLL ISSUES It's important to have a basic understanding of your tax obligations as an employer since Federal and State laws have numerous requirements that must be met from both a legal

Appendices - Introduction

Appendices - Introduction For more than one reason, we have posted a printable "pdf" copy of the appendices listed below, on our website @: http://www.full-chargebookkeeping.com/ > Resources & Links page.

Appendices - Introduction For more than one reason, we have posted a printable "pdf" copy of the appendices listed below, on our website @: http://www.full-chargebookkeeping.com/ > Resources & Links page.

BOLES METZGER BROSIUS & WALBORN PC CERTIFIED PUBLIC ACCOUNTANTS AND CONSULTANTS

BOLES METZGER BROSIUS & WALBORN PC CERTIFIED PUBLIC ACCOUNTANTS AND CONSULTANTS 3601 N. FRONT STREET HARRISBURG, PA 17110 PHONE: (717) 238-0446 FAX: (717) 238-3960 www.bmbwcpa.com WILLIAM B. BOLES, CPA/ABV,

BOLES METZGER BROSIUS & WALBORN PC CERTIFIED PUBLIC ACCOUNTANTS AND CONSULTANTS 3601 N. FRONT STREET HARRISBURG, PA 17110 PHONE: (717) 238-0446 FAX: (717) 238-3960 www.bmbwcpa.com WILLIAM B. BOLES, CPA/ABV,

MEMO #3. Tax and Reporting Procedures for Congregations. Pensions and Benefits USA. Caution! Determine employee classifications accurately.

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

MEMO #3 Tax and Reporting Procedures for Congregations Pensions and Benefits USA The tax and reporting requirements with which churches must comply often seem to complicate the task of the local church

PAYROLL ACCOUNTING (04)

") 6 Pages Contestant Number Payroll Accounting Regional 2012 Time Rank PAYROLL ACCOUNTING (04) Regional 2012 Multiple Choice (15 @ 2 points each) 30 pts Short Answer (6 @ 6 points each) 36 pts Problem 1:

6 Pages Contestant Number Payroll Accounting Regional 2012 Time Rank PAYROLL ACCOUNTING (04) Regional 2012 Multiple Choice (15 @ 2 points each) 30 pts Short Answer (6 @ 6 points each) 36 pts Problem 1:

Small Business Tax and Form Calendar

BONUS CHAPTER 2 Small Business Tax and Form Calendar Here we ve assembled all the key tax dates you need to know and the federal forms that must be submitted on those dates. The dates listed are the actual

BONUS CHAPTER 2 Small Business Tax and Form Calendar Here we ve assembled all the key tax dates you need to know and the federal forms that must be submitted on those dates. The dates listed are the actual

EMPLOYEE VS CONTRACTOR

INTERNAL REVENUE SERVICE EMPLOYEE VS CONTRACTOR Presented By: Deishun Garmon-Robinson Badge Number: FSLG Specialist Tax Exempt and Government Entities Internal Revenue Service 1110 Montlimar Drive, Suite

INTERNAL REVENUE SERVICE EMPLOYEE VS CONTRACTOR Presented By: Deishun Garmon-Robinson Badge Number: FSLG Specialist Tax Exempt and Government Entities Internal Revenue Service 1110 Montlimar Drive, Suite

Paychex 2017 Employer Year-end Guide

Paychex 2017 Employer Year-end Guide Overview Paychex is committed to helping you prepare and plan for year-end. Please use this guide to help make sure you have a successful 2017 year-end. The guide contains

Paychex 2017 Employer Year-end Guide Overview Paychex is committed to helping you prepare and plan for year-end. Please use this guide to help make sure you have a successful 2017 year-end. The guide contains

Sage Abra HRMS I Planning Guide. The Payroll Manager s Guide to Year-End

I Planning Guide The Payroll Manager s Guide to Year-End Table of Contents Introduction... 1 What s Involved in Payroll Processing and Year-End Compliance... 1 Checklist for Year-End 2011... 2-3 Looking

I Planning Guide The Payroll Manager s Guide to Year-End Table of Contents Introduction... 1 What s Involved in Payroll Processing and Year-End Compliance... 1 Checklist for Year-End 2011... 2-3 Looking

Treasurer s Glossary of Terms A

Treasurer s Glossary of Terms A Access - A database package that comes with Microsoft Office accrual basis accounting - A method of accounting where income is recognized when earned, even if not yet received,

Treasurer s Glossary of Terms A Access - A database package that comes with Microsoft Office accrual basis accounting - A method of accounting where income is recognized when earned, even if not yet received,

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

ACCOUNTING POLICIES AND PROCEDURES MANUAL

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

Board Policy No

Board Policy No. 2015-16-6 Fiscal Policies and Procedures Handbook Created by: TABLE OF CONTENTS Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Contracts... 2 Accounts Payable... 4 Bank Check

Board Policy No. 2015-16-6 Fiscal Policies and Procedures Handbook Created by: TABLE OF CONTENTS Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Contracts... 2 Accounts Payable... 4 Bank Check

Payroll Reference Manual

Payroll Reference Manual 2018-2019 2018-2019 Payroll Reference Manual Table of Contents Section I - Year End Preparation Year End Checklist 6 Year End Balancing/Reconciliations 8 Annual Reconciliation

Payroll Reference Manual 2018-2019 2018-2019 Payroll Reference Manual Table of Contents Section I - Year End Preparation Year End Checklist 6 Year End Balancing/Reconciliations 8 Annual Reconciliation

2008 Tax Rates and Information Bulletin

Albin, Randall & Bennett, CPAs 2008 Tax Rates and Information Bulletin 06/08 2008 TAX UPDATE BULLETIN TABLE OF CONTENTS Topic Page Number Payroll Withholding Rates and Limits...1 Backup Withholding...2

Albin, Randall & Bennett, CPAs 2008 Tax Rates and Information Bulletin 06/08 2008 TAX UPDATE BULLETIN TABLE OF CONTENTS Topic Page Number Payroll Withholding Rates and Limits...1 Backup Withholding...2

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2018 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2018 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

EMPLOYMENT TAX OVERVIEW

IRS Employment Tax Overview Patsy Kerns, Federal State and Local Government PASBO 62 ND ANNUAL CONFERENCE AND EXHIBITS, PITTSBURGH March 2017 1 EMPLOYMENT TAX OVERVIEW FRINGE BENEFITS ACCOUNTABLE PLANS

IRS Employment Tax Overview Patsy Kerns, Federal State and Local Government PASBO 62 ND ANNUAL CONFERENCE AND EXHIBITS, PITTSBURGH March 2017 1 EMPLOYMENT TAX OVERVIEW FRINGE BENEFITS ACCOUNTABLE PLANS

Labor Rate Guidelines

ReRe Labor Rate Guidelines Polices - Procedures - Guidelines Prepared for MASSPORT Date of Issue 10/2017 Revision: 2 (9/18) 1 Introduction These labor rate guidelines ( Guidelines ) and supporting templates

ReRe Labor Rate Guidelines Polices - Procedures - Guidelines Prepared for MASSPORT Date of Issue 10/2017 Revision: 2 (9/18) 1 Introduction These labor rate guidelines ( Guidelines ) and supporting templates

Payroll Tax Guide For Minnesota Businesses

Payroll Tax Guide For Minnesota Businesses 2017-2018 PAYROLL TAX GUIDE FOR MINNESOTA BUSINESSES Olsen Thielen & Co., Ltd. Certified Public Accountants & Consultants 2675 Long Lake Road 300 Prairie Center

Payroll Tax Guide For Minnesota Businesses 2017-2018 PAYROLL TAX GUIDE FOR MINNESOTA BUSINESSES Olsen Thielen & Co., Ltd. Certified Public Accountants & Consultants 2675 Long Lake Road 300 Prairie Center

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

The Pension Boards United Church of Christ, Inc. 2019 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Click

Federal Reporting. The Pension Boards United Church of Christ, Inc.

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

The Pension Boards United Church of Christ, Inc. 2015 Federal Reporting Requirements for Churches Prepared by Church Law & Tax Report Published by The Pension Boards United Church of Christ, Inc. Federal

SECTION 8: Employer Identification Numbers (EIN) Employer Identification Number (EIN) Cont

Employer Identification Number (EIN) Cont") SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) to ensure that all payments are credited to

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) to ensure that all payments are credited to

Construction Accounting

Construction Accounting Steven M. Bragg Chapter 1 Overview of the Construction Industry... 1 Learning Objectives... 1 Introduction... 1 Nature of the Construction Contractor... 2 Bonding Requirements...

Construction Accounting Steven M. Bragg Chapter 1 Overview of the Construction Industry... 1 Learning Objectives... 1 Introduction... 1 Nature of the Construction Contractor... 2 Bonding Requirements...

Federal Reporting Requirements for Churches*

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

Federal Reporting Requirements for Churches* Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2016 Christianity Today International. Federal Reporting Requirements by

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report Copyright 2014 Christianity Today International. Federal Reporting Requirements

Preparing for an Internal Revenue Service Review for a Housing Authority

Preparing for an Internal Revenue Service Review for a Housing Authority Prepared by Urlaub & Co., PLLC, Certified Public Accountants (580) 332-4802 Presented by Ronald Urlaub, CPA 1 Objectives To understand

Preparing for an Internal Revenue Service Review for a Housing Authority Prepared by Urlaub & Co., PLLC, Certified Public Accountants (580) 332-4802 Presented by Ronald Urlaub, CPA 1 Objectives To understand

A Peer-to-Peer Exchange on AAAs Performing Financial Management Services: Managing the "The Boring Part" of Consumer Direction

A Peer-to-Peer Exchange on AAAs Performing Financial Management Services: Managing the "The Boring Part" of Consumer Direction National Resource Center for Participant-Directed Services 2/4/10 Mollie (Grotpeter)

A Peer-to-Peer Exchange on AAAs Performing Financial Management Services: Managing the "The Boring Part" of Consumer Direction National Resource Center for Participant-Directed Services 2/4/10 Mollie (Grotpeter)

Premium Audit Guide. What is a premium audit? Types of audits. Payroll as a premium basis. Information requested at time of audit

Premium Audit Guide What is a premium audit? The purpose of a premium audit is to verify information necessary to calculate an insured s final premium for a specific policy term. When a policy is initially

Premium Audit Guide What is a premium audit? The purpose of a premium audit is to verify information necessary to calculate an insured s final premium for a specific policy term. When a policy is initially

2013 Year End Customer Guide

November 2013 Wells Fargo Business Payroll Services 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide The 2013 year-end

November 2013 Wells Fargo Business Payroll Services 2013 Year End Customer Guide 2013 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Welcome to the 2013 year-end customer guide The 2013 year-end

Enclosed you will find the following information to help you prepare for year-end 2018:

Product Guide Dear Valued Deluxe Payroll Client, This guide has been designed to assist our clients through the year-end process and to meet critical deadlines. Our goal is to ensure an accurate and timely

Product Guide Dear Valued Deluxe Payroll Client, This guide has been designed to assist our clients through the year-end process and to meet critical deadlines. Our goal is to ensure an accurate and timely

Employer Obligation to Maintain and Report Records

New Jersey Department of Labor and Workforce Development Chapter 194, Laws of New Jersey, 2009, Relating to Employer Obligation to Maintain and Report Records Regarding Wages, Benefits, Taxes and Other

New Jersey Department of Labor and Workforce Development Chapter 194, Laws of New Jersey, 2009, Relating to Employer Obligation to Maintain and Report Records Regarding Wages, Benefits, Taxes and Other

Dear Valued Payce Client,

8 0 2 1 Dear Valued Payce Client, This guide has been designed to assist our clients through the year-end process and to meet critical deadlines. Our goal is to ensure an accurate and timely delivery of

8 0 2 1 Dear Valued Payce Client, This guide has been designed to assist our clients through the year-end process and to meet critical deadlines. Our goal is to ensure an accurate and timely delivery of

We hope the following summarized payroll, sales tax and form 1099 information will be helpful to you in the coming New Year.

Dear Client: We hope the following summarized payroll, sales tax and form 1099 information will be helpful to you in the coming New Year. Rates and Limits For 2017 FEDERAL PAYROLL TAXES FICA- The Social

Dear Client: We hope the following summarized payroll, sales tax and form 1099 information will be helpful to you in the coming New Year. Rates and Limits For 2017 FEDERAL PAYROLL TAXES FICA- The Social

Payroll Concepts. Lessons. Module 1:

Module 1: Payroll Concepts Introduction to Payroll in the United States... 1-2 Documents Employers Request... 1-2 Social Security Numbers... 1-2 Methods of Paying Employees... 1-3 Withholding Taxes...

Module 1: Payroll Concepts Introduction to Payroll in the United States... 1-2 Documents Employers Request... 1-2 Social Security Numbers... 1-2 Methods of Paying Employees... 1-3 Withholding Taxes...

Pay_910 Gift Cards, Gifts, Prizes and Awards Prepared By: Associate Controller Disbursements Approved By: John Kirsits Effective Date: 4/12/2016

Pay_910 Gift Cards, Gifts, Prizes and Awards Prepared By: Associate Controller Disbursements Approved By: John Kirsits Effective Date: 4/12/2016 Purpose The policy provides University departments with

Pay_910 Gift Cards, Gifts, Prizes and Awards Prepared By: Associate Controller Disbursements Approved By: John Kirsits Effective Date: 4/12/2016 Purpose The policy provides University departments with

NOACSC Tax Hot Topics. September 21, 2018 Christopher E. Axene, CPA

NOACSC Tax Hot Topics September 21, 2018 Christopher E. Axene, CPA Fringe Benefits - The Good (?) First rule of thumb cash (or its equivalent) paid to employees is always taxable unless it is a reimbursement

NOACSC Tax Hot Topics September 21, 2018 Christopher E. Axene, CPA Fringe Benefits - The Good (?) First rule of thumb cash (or its equivalent) paid to employees is always taxable unless it is a reimbursement

2017 Year-end OptRight Customer Guide

October 2017 Business Payroll Services 2017 Year-end OptRight Customer Guide 2017 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Making it easier to prepare for your year-end payroll needs This

October 2017 Business Payroll Services 2017 Year-end OptRight Customer Guide 2017 Wells Fargo Bank N.A. All rights reserved. Member FDIC. Making it easier to prepare for your year-end payroll needs This

An Employer s Guide To Payroll

An Employer s Guide To Payroll Solutions That Save You Time www.timeplus.com Table of Contents NEW BUSINESS CHECKLIST...2 EMPLOYER IDENTIFICATION NUMBER...3 TELE-TIN...4 FAIR LABOR STANDARDS ACT...4 Wage

An Employer s Guide To Payroll Solutions That Save You Time www.timeplus.com Table of Contents NEW BUSINESS CHECKLIST...2 EMPLOYER IDENTIFICATION NUMBER...3 TELE-TIN...4 FAIR LABOR STANDARDS ACT...4 Wage

1 Exam Prep Florida Contractor s Reference Manual Practice Test 3

1 Exam Prep Florida Contractor s Reference Manual Practice Test 3 1. Before improving any real property, the owner should file a with the county clerk's office. A. Notice of commencement. B. Waiver of

1 Exam Prep Florida Contractor s Reference Manual Practice Test 3 1. Before improving any real property, the owner should file a with the county clerk's office. A. Notice of commencement. B. Waiver of

JANUARY 2014 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS

JANUARY 2014 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS This letter sets forth employee payroll tax withholding rates, employer payroll tax rates in effect for 2014 and some pertinent

JANUARY 2014 UPDATE ON PAYROLL, EMPLOYMENT TAXES AND INFORMATION RETURNS This letter sets forth employee payroll tax withholding rates, employer payroll tax rates in effect for 2014 and some pertinent

Employer's Tax Guide to Fringe Benefits

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2013 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2013 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Chapter 11 Payroll Taxes, Deposits, and Reports

Chapter 11 - Payroll Taxes, Deposits, and Reports Chapter 11 Payroll Taxes, Deposits, and Reports TEACHING OBJECTIVES 11-1) Explain how and when payroll taxes are paid to the government. 11-2) Compute

Chapter 11 - Payroll Taxes, Deposits, and Reports Chapter 11 Payroll Taxes, Deposits, and Reports TEACHING OBJECTIVES 11-1) Explain how and when payroll taxes are paid to the government. 11-2) Compute

Employer Training: Reporting 101. Slide 1

Employer Training: Reporting 101 Slide 1 Reporting 101 - Always contact your PERA representative with questions. - Best practices for reporting PERA. Reporting Overview PERA is a 100% reporting Agency.

Employer Training: Reporting 101 Slide 1 Reporting 101 - Always contact your PERA representative with questions. - Best practices for reporting PERA. Reporting Overview PERA is a 100% reporting Agency.

Employer's Tax Guide to Fringe Benefits

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2014 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

Department of the Treasury Internal Revenue Service Publication 15-B Cat. No. 29744N Employer's Tax Guide to Fringe Benefits For use in 2014 Contents What's New... 1 Reminders... 2 Introduction... 2 1.

PAYROLL ACCOUNTING (04)

") 6 Pages Contestant Number Payroll Accounting Regional 2012 Time Rank PAYROLL ACCOUNTING (04) Regional 2012 Multiple Choice (15 @ 2 points each) 30 pts Short Answer (6 @ 6 points each) 36 pts Problem 1:

6 Pages Contestant Number Payroll Accounting Regional 2012 Time Rank PAYROLL ACCOUNTING (04) Regional 2012 Multiple Choice (15 @ 2 points each) 30 pts Short Answer (6 @ 6 points each) 36 pts Problem 1:

1099s, 1095s and Year End Payroll

1099s, 1095s and Year End Payroll DENNIS MUYSKENS HOGAN - HANSEN P.C. Agenda 1099s What are they? Who receives them? Types of 1099s Procedures Filing 1099s 1095s What are they? Types of 1095s Procedures

1099s, 1095s and Year End Payroll DENNIS MUYSKENS HOGAN - HANSEN P.C. Agenda 1099s What are they? Who receives them? Types of 1099s Procedures Filing 1099s 1095s What are they? Types of 1095s Procedures

Introduction to Payroll in the United States Documents Employers Request Social Security Numbers

Module 1: Payroll Concepts Introduction to Payroll in the United States... 1-2 Documents Employers Request... 1-2 Social Security Numbers... 1-2 Methods of Paying Employees... 1-3 Withholding Taxes...

Module 1: Payroll Concepts Introduction to Payroll in the United States... 1-2 Documents Employers Request... 1-2 Social Security Numbers... 1-2 Methods of Paying Employees... 1-3 Withholding Taxes...

Oregon-Idaho Annual Conference

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

Oregon-Idaho Annual Conference The United Methodist Church 1505 SW 18 th Avenue Portland OR 97201 503.226.7931 1.800.593.7539 www.umoi.org W-2 Instructions and other General Tax Information Remember that

36 th Annual Employment Issues Update. Jennifer Bickford, Paraprofessional Manager HBK CPAs and Consultants

36 th Annual Employment Issues Update Jennifer Bickford, Paraprofessional Manager HBK CPAs and Consultants jbickford@hbkcpa.com 814-336-1512 Federal Payroll Taxes - 2017 Form 941 Rates and Wage Bases Federal

36 th Annual Employment Issues Update Jennifer Bickford, Paraprofessional Manager HBK CPAs and Consultants jbickford@hbkcpa.com 814-336-1512 Federal Payroll Taxes - 2017 Form 941 Rates and Wage Bases Federal

Preparing and Maintaining a Vendor F/EA FMS Provider Policies and Procedures Manual

Tasks to Be Performed by a Vendor Fiscal/Employer Agent (F/EA) FMS Provider Operating Under Section 3504 of the IRS Code and Rev. Proc. 70-6, Proposed Notice 2003-70, as Applicable and REG-137036-08 1

Tasks to Be Performed by a Vendor Fiscal/Employer Agent (F/EA) FMS Provider Operating Under Section 3504 of the IRS Code and Rev. Proc. 70-6, Proposed Notice 2003-70, as Applicable and REG-137036-08 1

9 - Federal Tax Reporting/ Social Security

Illinois Municipal Retirement Fund Federal Tax Reporting & Social Security / SECTION 9 9 - Federal Tax Reporting/ Social Security APPENDIX - FEDERAL TAX REPORTING/SOCIAL SECURITY... 291 9.00 INTRODUCTION...

Illinois Municipal Retirement Fund Federal Tax Reporting & Social Security / SECTION 9 9 - Federal Tax Reporting/ Social Security APPENDIX - FEDERAL TAX REPORTING/SOCIAL SECURITY... 291 9.00 INTRODUCTION...

SAMPLE FEDERAL REPORTING REQUIREMENTS. for Churches. Richard R. Hammar, J.D., LL.M., CPA Senior Editor, Church Law & Tax Report

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Attachment 1. Computation of expenses, allocable to tax-free ministerial income, that are nondeductible. % of Nondeductible Expenses Parsonage allowance: Taxable Tax-Free Total M inisterial retirement

Oregon Domestic Combined Payroll. Tax Report. Oregon Department of Revenue

Oregon Domestic Combined Payroll 2013 Tax Report Oregon Department of Revenue Oregon Employment Department Oregon Department of Consumer & Business Services Forms and Instructions For Oregon Domestic Employers

Oregon Domestic Combined Payroll 2013 Tax Report Oregon Department of Revenue Oregon Employment Department Oregon Department of Consumer & Business Services Forms and Instructions For Oregon Domestic Employers

Payroll Reference Manual

2010 2011 Payroll Reference Manual Baden, Gage & Schroeder, LLC 6920 Pointe Inverness Way, Suite 300 Fort Wayne, IN 46804 260.422.2551 www.badencpa.com 2010-2011 Payroll Reference Manual Table of Contents

2010 2011 Payroll Reference Manual Baden, Gage & Schroeder, LLC 6920 Pointe Inverness Way, Suite 300 Fort Wayne, IN 46804 260.422.2551 www.badencpa.com 2010-2011 Payroll Reference Manual Table of Contents

1099 vs. W2 1/30/ vs. W 2. Classifying Independent Contractors and Employees

1099 vs. W2 Classifying Independent Contractors and Employees February 23, 2019 1099 vs. W 2 In this webinar we will discuss the classification criteria used to identify an individual/worker as an independent

1099 vs. W2 Classifying Independent Contractors and Employees February 23, 2019 1099 vs. W 2 In this webinar we will discuss the classification criteria used to identify an individual/worker as an independent

Chapter 13 Payroll Accounting, Taxes, and Reports

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

Chapter 13 Payroll Accounting, Taxes, and Reports -- The payroll register and employee earnings records provide all the payroll information needed to prepare a payroll and payroll tax reports. Journal

SECTION 8: Depositing and Reporting Withheld Taxes

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) The EIN is a nine-digit number, expressed as

SECTION 8: Depositing and Reporting Withheld Taxes 1 Employer Identification Numbers (EIN) All employers are assigned an Employer Identification Number (EIN) The EIN is a nine-digit number, expressed as

2012 Year-End Guide & Reply Form

2012 Year-End Guide & Reply Form To ensure the accuracy and timeliness of your W-2s and year-end processing, Please complete and return the attached reply form by Friday, November 30, 2012. Would you like

2012 Year-End Guide & Reply Form To ensure the accuracy and timeliness of your W-2s and year-end processing, Please complete and return the attached reply form by Friday, November 30, 2012. Would you like

City of Petaluma - Benefit Costs - FY For Full Time Employees - Appointed and Elected Officials Updated:

For Units 1, 2 and 3: Health Benefits Monthly Annual Health Benefits - PEMHCA Contribution 2016 $ 125 CalPERS - PEMHCA Contribution - Total City Contribution (includes PEMHCA contribution) Employee $ 700.95

For Units 1, 2 and 3: Health Benefits Monthly Annual Health Benefits - PEMHCA Contribution 2016 $ 125 CalPERS - PEMHCA Contribution - Total City Contribution (includes PEMHCA contribution) Employee $ 700.95

End-of-Year Payroll Processing

DECEMBER 2014 CHECKLIST OF TO-DO ITEMS Register for EFTPS (for new employers not yet registered). Order Forms W-2, W-3, 1099 and 1096. Order payroll tax update programs for computerized payroll systems.

DECEMBER 2014 CHECKLIST OF TO-DO ITEMS Register for EFTPS (for new employers not yet registered). Order Forms W-2, W-3, 1099 and 1096. Order payroll tax update programs for computerized payroll systems.

Orthodox Church in America Tax Help for Parish Treasurers

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Orthodox Church in America Tax Help for Parish Treasurers INTRODUCTION Taxes in the United States are complex and consequences for noncompliance can be significant. Furthermore, there are nuances in the

Conformity with GAAP is essential for consistency and comparability in financial reporting.

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) & FINANCIAL ACCOUNTING STANDARD BOARD (FASB) The term generally accepted accounting principles refer to the standards, rules, and procedures that serve as

GENERALLY ACCEPTED ACCOUNTING PRINCIPLES (GAAP) & FINANCIAL ACCOUNTING STANDARD BOARD (FASB) The term generally accepted accounting principles refer to the standards, rules, and procedures that serve as

Payroll Benefits and Year End Reminders for 2018 and Changes for Presented by: Debbie Denny Tax Manager

Payroll Benefits and Year End Reminders for 2018 and Changes for 2019 Presented by: Debbie Denny Tax Manager Topics W-2 Information Fringe Benefits Exempt vs. Nonexempt Employees FSA s Employee vs. Independent

Payroll Benefits and Year End Reminders for 2018 and Changes for 2019 Presented by: Debbie Denny Tax Manager Topics W-2 Information Fringe Benefits Exempt vs. Nonexempt Employees FSA s Employee vs. Independent

Local Church Treasurer/Finance Training

Local Church Treasurer/Finance Training 2018 Welcome!! Christine Dodson, Treasurer JoAnna Ezuka, Benefits Coordinator Sandy Lee, Benefits Specialist Chrisy Powell, Property Management & Insurance Katherine

Local Church Treasurer/Finance Training 2018 Welcome!! Christine Dodson, Treasurer JoAnna Ezuka, Benefits Coordinator Sandy Lee, Benefits Specialist Chrisy Powell, Property Management & Insurance Katherine

BELMONT COUNTY BOARD OF COMMISSIONERS PERSONNEL POLICY MANUAL SECTION 5 CLASSIFICATION AND COMPENSATION

SECTION 5 CLASSIFICATION AND COMPENSATION 5.1 Compensation Plan 5.2 Overtime 5.3 Pay Period 5.4 Compensatory Time 5.5 Payroll Deductions 5.6 Retirement Plan and Deferred Compensation 5.7 Workers= Compensation

SECTION 5 CLASSIFICATION AND COMPENSATION 5.1 Compensation Plan 5.2 Overtime 5.3 Pay Period 5.4 Compensatory Time 5.5 Payroll Deductions 5.6 Retirement Plan and Deferred Compensation 5.7 Workers= Compensation

P&B. Memo #3. The tax and reporting requirements with which churches must comply. Tax and Reporting Procedures for Congregations

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

P&B Memo #3 Pensions and Benefits USA, Church of the Nazarene Tax and Reporting Procedures for Congregations The tax and reporting requirements with which churches must comply often seem to complicate

International Dark-Sky Association Cost Allocation Plan

International Dark-Sky Association Cost Allocation Plan Adopted 15 September 2014 1 Purpose The purpose of the cost allocation plan is to summarize, in writing, the methods and procedures that this International

International Dark-Sky Association Cost Allocation Plan Adopted 15 September 2014 1 Purpose The purpose of the cost allocation plan is to summarize, in writing, the methods and procedures that this International

January 20, Congress Extends Payroll Tax Holiday through February 29, 2012

January 20, 2012 Re: 2012 Accountants Memorandum Update Congress Extends Payroll Tax Holiday through February 29, 2012 Late in 2011 Congress voted to extend for two months the reduced payroll tax rate

January 20, 2012 Re: 2012 Accountants Memorandum Update Congress Extends Payroll Tax Holiday through February 29, 2012 Late in 2011 Congress voted to extend for two months the reduced payroll tax rate

Federal Reporting Requirements for Churches

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

Federal Reporting Requirements for Churches Prepared by Richard R. Hammar, J.D., LL.M., CPA Senior Editor, CHURCH LAW & TAX REPORT Copyright 2013 Christianity Today International. Federal Reporting Requirements

AccuBuild Calendar Year End Notes

AccuBuild 2016 2 Table of Contents 1. 3 1.1... 3 1.2 Create a Bonus Check... 4 1.3 Create a Fringe Benefit Check... 5 1.4 Health Insurance Reporting on W-2s for 2015... 7 1.5 Order Tax Forms... 9 1.5.1

AccuBuild 2016 2 Table of Contents 1. 3 1.1... 3 1.2 Create a Bonus Check... 4 1.3 Create a Fringe Benefit Check... 5 1.4 Health Insurance Reporting on W-2s for 2015... 7 1.5 Order Tax Forms... 9 1.5.1

Personnel Resolution Covering Unrepresented Officers and Employees. January 1, 2018

Personnel Resolution Covering Unrepresented Officers and Employees January 1, 2018 i Table of Contents ARTICLE 1 GENERAL ADMINISTRATIVE PROVISIONS... 1 1.1 APPOINTING AUTHORITY... 1 1.2 APPLICABILITY...

Personnel Resolution Covering Unrepresented Officers and Employees January 1, 2018 i Table of Contents ARTICLE 1 GENERAL ADMINISTRATIVE PROVISIONS... 1 1.1 APPOINTING AUTHORITY... 1 1.2 APPLICABILITY...

2006 Payroll Calendar Year End Procedures

2006 Payroll Calendar Year End Procedures page Summary of Procedures Before you Begin the Close... 2 Year End Menu.. 3 Circular E... 3 W2 Process Menu Options. 4 Miscellaneous Codes Add-On Maintenance........

2006 Payroll Calendar Year End Procedures page Summary of Procedures Before you Begin the Close... 2 Year End Menu.. 3 Circular E... 3 W2 Process Menu Options. 4 Miscellaneous Codes Add-On Maintenance........

Tax Update for State and Local Governments

Tax Update for State and Local Governments Fringe Benefit and Tax Reporting Overview Presented by: Ashley M. Summers, CPA Tax Manager Sales & Use Tax Reminder Retail Sales and Use tax exemptions can now

Tax Update for State and Local Governments Fringe Benefit and Tax Reporting Overview Presented by: Ashley M. Summers, CPA Tax Manager Sales & Use Tax Reminder Retail Sales and Use tax exemptions can now

ST. LUCIE COUNTY SCHOOL BOARD SALARY SCHEDULES, SECTION 1 GENERAL PROVISIONS

I. Salary Schedules ST. LUCIE COUNTY SCHOOL BOARD SALARY SCHEDULES, SECTION 1 GENERAL PROVISIONS The salary schedules adopted by the School Board of Saint Lucie County are effective July 1, 2017 and continue

I. Salary Schedules ST. LUCIE COUNTY SCHOOL BOARD SALARY SCHEDULES, SECTION 1 GENERAL PROVISIONS The salary schedules adopted by the School Board of Saint Lucie County are effective July 1, 2017 and continue

FINANCIAL POLICIES & PROCEDURES

TOWN OF CONWAY FINANCIAL POLICIES & PROCEDURES Adopted February 19, 2013 Adoption Date Treasurer Accountant Selectboard Revision Date Treasurer Accountant Selectboard/Admin 2 TABLE OF CONTENTS RECEIPTS...5

TOWN OF CONWAY FINANCIAL POLICIES & PROCEDURES Adopted February 19, 2013 Adoption Date Treasurer Accountant Selectboard Revision Date Treasurer Accountant Selectboard/Admin 2 TABLE OF CONTENTS RECEIPTS...5

2015 Year End Payroll Processing

2015 Year End Payroll Processing The end of another calendar year is upon us, we would like to take this opportunity to THANK YOU for your continued business. The fourth quarter of the year is a busy time

2015 Year End Payroll Processing The end of another calendar year is upon us, we would like to take this opportunity to THANK YOU for your continued business. The fourth quarter of the year is a busy time

YEAR END GUIDE. TABLE OF CONTENTS Page 2. Page 3. Page 4 Page 5. DATES and Holidays. BEFORE YOUR LAST PAYROLL

YOUR GUIDE TO YEAR END 2013/2014 TABLE OF CONTENTS Page 2 BEFORE YOUR LAST PAYROLL W2 Edit List, Tax Letters Top 5 Items to Review Page 3 BEFORE YOUR FIRST PAYROLL Top 5 Items to Review Page 4 Page 5 2014

YOUR GUIDE TO YEAR END 2013/2014 TABLE OF CONTENTS Page 2 BEFORE YOUR LAST PAYROLL W2 Edit List, Tax Letters Top 5 Items to Review Page 3 BEFORE YOUR FIRST PAYROLL Top 5 Items to Review Page 4 Page 5 2014

BY BROTHERHOOD MUTUAL A STRESS-FREE PROCEDURAL GUIDE. End-of-Year Payroll, Simplified 1

BY BROTHERHOOD MUTUAL BY BROTHERHOOD MUTUAL End-of-Year Payroll, Simplified A STRESS-FREE PROCEDURAL GUIDE End-of-Year Payroll, Simplified 1 Welcome to End-of-Year Payroll, Simplified The key to successfully

BY BROTHERHOOD MUTUAL BY BROTHERHOOD MUTUAL End-of-Year Payroll, Simplified A STRESS-FREE PROCEDURAL GUIDE End-of-Year Payroll, Simplified 1 Welcome to End-of-Year Payroll, Simplified The key to successfully