FRT. No. of Pages : 6 Total Marks : 100

|

|

|

- Chloe Daniel

- 5 years ago

- Views:

Transcription

1 FRT No. of Pages : 6 Total Marks : 100 No. of Questions : 7 Time allowed: 3 hrs Question No.1 is compulsory and answer any five from the remaining six questions. Wherever necessary make suitable assumptions. Working notes should form part of your answer. 1 a) ABC Ltd. shows a net profit of ` 10,80,000 for 3rd quarter after incorporating the following: (i) Bad debt of ` 60,000 incurred during the year, 65% of the bad debts have been deferred to the next quarter (ii) Extraordinary loss of `56,000 incurred during the quarter has been fully recognized in this quarter (iii) Additional depreciation of `18,000 resulting from the change of method of depreciation. Do you agree with the treatment adopted by the company? If not, find out correct quarterly income as per AS-25. (5 Marks) b) Samrat Ltd. acquired a patent at a cost of `60 lacs for a period of 5 years and the product-life cycle is also 5 years. The company capitalized the cost and started amortizing the asset at `10 lacs per annum. After two years it was found that the product life-cycle may continue for another 4 years from then. The net cash flows from the product during these 4 years were expected to be `49,50,000; ` 54,00,000; ` 58,50,000 and `63,00,000. Find out the amortization cost of the patent for each of the year. (5 Marks) c) Explain the impact of the followings in line with AS-29 (i) A company follows a policy of refunding money to the dissatisfied customers if they claim within thirty days from the date of purchase and return the goods. It appears from the past experience that in a month only 0.30% of the customers claim refunds. The company sold goods amounting to ` 50 lacs during the last month of the financial year. Is there any contingency? (ii) An airline is required by law to overhaul its aircraft once every three years. The expenses to be incurred as classified as 'refurbishment costs'. Is there any provision to be recognized? (5 Marks) d) The notes to accounts of X Ltd. for the year include the following: Interest on bridge loan from banks and Financial Institutions and on Debentures specifically obtained for the Company s Fertiliser Project amounting to ` 1,80,80,000 has been capitalized during the year, which includes approximately ` 1,70,33,465 capitalized in respect of the utilization of loan and debenture money for the said purpose. Is the treatment correct? Briefly comment. (5 Marks) 2. The summarized Balance sheets of Aman Ltd. and its subsidiary Ayan Ltd. as at were as follows: Liabilities Share capital (Share of ` 10 each) Aman Ltd. Ayan Ltd. Assets Aman Ltd. Ayan Ltd. ` ` ` ` 50,00,000 10,00,000 Fixed assets 60,00,000 18,00,000 General reserves 50,00,000 20,00,000 Investment in Ayan Ltd. 6,00, (60,000 shares) Profit and Loss account 20,00,000 15,00,000 Sundry debtors 35,00,000 5,00,000 PRIME/ME39/FINAL 1

2 Secured loan 20,00,000 2,50,000 Inventories 30,00,000 25,00,000 Current liabilities 30,00,000 2,50,000 Cash and bank 39,00,000 2,00,000 1,70,00,000 50,00,000 1,70,00,000 50,00,000 Aman Ltd. holds 60% of the paid-up capital of Ayan Ltd. and the balance is held by a foreign company. A memorandum of understanding has been entered into with the foreign company by Aman Ltd. to the following effect: (i) The shares held by the foreign company will be sold to Aman Ltd. at a price per share to be calculated by capitalizing the yield at 15%. Yield, for this purpose, would mean 50% of the average of pre-tax profits for the last 3 years, which were ` 12 lakhs, ` 18 lakhs and `24 lakhs respectively. (Average tax rate was 40%). (ii) The actual cost of shares to the foreign company was ` 4,40,000 only. Gains accruing to the foreign company are taxable at 20%. The tax payable will be deducted from the sale proceeds and paid to government by Aman Ltd. 50% of the consideration (after payment of tax) will be remitted to the foreign company by Aman Ltd. and also any cash for fractional shares allotted. (iii) For the balance of consideration, Aman Ltd. would issue its shares at their intrinsic value. It was also decided that Aman Ltd. would absorb Ayan Ltd. Simultaneously by writing down the Fixed assets of Ayan Ltd. by 10%. The Balance Sheet figures included a sum of `1,00,000 due by Ayan Ltd. to Aman Ltd. and stock of Aman Ltd. included stock of `1,50,000 purchased from Ayan Ltd., who sold them at cost plus 20%. The entire arrangement was approved and put through by all concern effective from You are required to indicate how the above arrangements will be recorded in the books of Aman Ltd. and also prepare a Balance Sheet after absorption of Ayan Ltd. (16 Marks) 3. Following are the Balance Sheets of Veer Ltd. and Virat Ltd. as at Liabilities Veer Ltd. ` Viral Ltd. ` Assets Veet Ltd. ` Virat Ltd. ` Equity Share Capital 3,00,000 50,000 Land & Building 1,00,000 50,000 of ` 100 each fully paid Machinery 1,40,000 25,000 General Reserve 25,000 15, Shares in Virat 50,000 Ltd. Profit & Loss Account 40,000 20,000 Stock in Trade 35,000 20,000 Sundry Creditors 50,000 20,000 Debtors 75,000 10,000 Bills Payable 15,000 22,500 Bills Receivable 15,000 Cash at Bank 15,000 22,500 Total 8,60,000 2,55,000 Total 8,60,000 2,55,000 Prepare Consolidated Balance Sheet as at 31st March, 2012 and give proper working notes required for the Consolidated Balance Sheet, from the following additional Information (i) All the Bills Receivable of Veer Ltd. including those discounted were accepted by Virat Ltd. (ii) When Veer Ltd. had acquired 300 Shares in Virat Ltd., the latter had ` 10,000 in General Reserve and ` 2,500 Credit Balance in Profit and Loss Account. (iii) At the time of acquisition of further 50 Shares by Virat Ltd., the latter had ` 12,500 General Reserve and ` 14,000 Credit Balance in Profit and Loss Account, from which 20% dividend was paid by Virat Ltd. (iv) The dividends received by Veer Ltd. on these shares were credited to Profit & Loss Account. PRIME/ME39/FINAL 2

3 (v) Stock of Virat Ltd. includes goods valued at ` 10,000 purchased from Veer Ltd. which has made 25% profit on cost. (vi) For the financial year ending , Veer Ltd. had proposed a dividend of 10% and Virat Ltd. has proposed a dividend of 15%, but no effect has yet been given in the above Balance Sheets. (16 Marks) 4 (a) Mitra Ltd acquired 25% of shares in Friend Ltd as on for `9 Lakhs. The Balance Sheet of Friend Ltd as on is given below- Liabilities Amount ` Assets Amount ` Share Capital 15,00,000 Fixed Assets 15,00,000 Reserves and Surplus 15,00,000 Investments 6,00,000 Current Assets 9,00,000 Total 30,00,000 Total 30,00,000 Following additional information are available for the year ended i. Mitra Ltd received dividend from Friend Ltd for the year ended at 40% from the Reserves. ii. Friend Ltd made a profit After Tax of ` 21 Lakhs for the year ended iii. Friend Ltd declared a 50% for the year ended on Mitra Ltd is preparing consolidated Financial Statements in accordance with AS 21 for its various subsidiaries. Calculate Goodwill if any on acquisition of Friend Ltd. s shares. How Mitra Ltd will reflect the value of investment in Friend Ltd in the consolidated Financial Statements? How the dividend received from Friend Ltd will be shown in the consolidated Financial Statements? (8 Marks) (b) From the following information of Beta Ltd. calculate Earnings Per Share in accordance with AS-20: Year ` Year ` Net profit before tax 3,00,000 1,00,000 Current tax 40,000 30,000 Tax relating to earlier years 24,000 (13,000) Deferred tax 30,000 10,000 Profit after tax 2,06,000 73,000 Other information: (i) Profit includes compensation from Central Government towards loss on account of earthquake in 2010(non-taxable) ( ) 1,00,000; ( )-NIL (ii) Outstanding convertible 6% Preference shares 1,000 issued and paid on Face value `100, Conversion ratio 15 equity shares for every preference share. (iii) 15% convertible debentures of `1,000 each total face value ` 1,00,000 to be converted into 10 Equity shares per debenture issued and paid on (iv) Total no. of Equity shares outstanding as on , 20,000 including 10,000 bonus shares issued on , face value `100. (8 Marks) 5. The Balance Sheet of Jupiter Ltd. as on 31st March, 2012 is as under: (All figures are in lacs) Liabilities ` Assets ` Shares ` 10 each 3,000 Goodwill 744 Reserves (including provision for taxation of ` 300 lacs) 1,000 Premises and Land at cost 400 PRIME/ME39/FINAL 3

4 5% Debentures 2,000 Plant and Machinery 3,000 Secured Loans 200 Motor Vehicles (purchased on ) 40 Sundry Creditors 300 Raw materials at cost 920 Profit & Loss A/c Work-in-progress at cost 130 Balance from previous B/S `32 Finished Goods at cost 180 Profit for the year (After taxation) ` Book Debts 400 Investment (meant for replacement of Plant and Machinery) 1,600 Cash at Bank and Cash in hand 192 Discount on Debentures 10 Underwriting Commission The resale value of Premises and Land is ` 1,200 lacs and that of Plant and Machinery is ` 2,400 lacs. 20% is applicable to Motor Vehicles. Applicable depreciation on Premises and Land is 2%, and that on Plant and Machinery is 10%. Market value of the Investments is `1,500 lacs. 10% of book debts is bad. In a similar company the market value of equity shares of the same denomination is ` 25 per share and in such company dividend is consistently paid during last 5 20%. Contrary to this, Jupiter Ltd. is having a marked upward or downward trend in the case of dividend payment. Past 5 years profits of the company were as under: ` 67 lacs (-) ` 1,305 lacs (loss) ` 469 lacs ` 546 lacs ` 405 lacs The unusual negative profitability of the company during was due to the lock out in the major manufacturing unit of the company which happened in the beginning of the second quarter of the year and continued till the last quarter of Value the Goodwill of the Company on the basis of 4 years purchase of the Super Profit. (16 Marks) 6. (a) The following is the Profit and Loss Account of Morning Glory Ltd. for the year ended Profit and Loss Account for the year ended (` in lakhs) Notes ` ` Income: Sales 890 Other Income Expenditure: Production and operational expenses (a) 641 Administration expenses (Factory) (b) 33 Interest (c) 29 Depreciation (d) PRIME/ME39/FINAL 4

5 Notes : A. Production and Operational expenses Profit before taxes 225 Provision for taxes 30 Profit after tax 195 Balance as per last Balance Sheet Transferred to General Reserve 45 Dividend paid Surplus carried to Balance Sheet ` inlakhs Consumption of raw materials 293 Consumption of stores 59 Salaries, Wages, Gratuities etc. (Admn.) 82 Cess and Local taxes 98 Other manufacturing expenses B. Administration expenses include salaries, commission to Directors ` 9.00 lakhs.provision for doubtful debts ` 6.30 lakhs. C. `in lakhs Interest on loan from ICICI Bank for working capital 9 Interest on loan from ICICI Bank for fixed loan 10 Interest on loan from IFCI for fixed loan 8 Interest on Debentures 2 D. The charges for taxation include a transfer of ` 3.00 lakhs to the credit of Deferred Tax Account. E. Cess and Local taxes include Excise Duty, which is equal to 10% of cost of bought-in material. Prepare a Gross Value Added Statement of Morning Glory Ltd. and show also the reconciliation between Gross Value Added and Profit before taxation. (8 Marks) (b) On February 1, 2011, Purushottam Ltd. entered into a contract with Sun Ltd. to receive the fair value of 1,000 Purushottam Ltd. s own equity shares outstanding as on in exghange for payment of ` 1,04,000 in cash i.e. ` 104 per share. The contract will be settled in net cash on The fair value of this forward contract on the different dates were: (i) Fair value of forward on NIL (ii) Fair value of forward on ` 6,300 (iii) Fair value of forward on ` 2,000 Presuming that Purushottam Ltd. closes its books on 31st December each year, pass entries : (i) If net settled is in cash (ii) If net is settled by Sun Ltd. by delivering shares of Purushottam Ltd. (8 Marks) PRIME/ME39/FINAL 5

6 7. Answer any four from the following: (i) Tulip Ltd. is working on different projects which are likely to be completed within 3 years period. It recognizes revenue from these contracts on percentage of completion method for financial statements during 2010, 2011 and 2012 for `22,00,000, `32,00,000 and `42,00,000 respectively. However, for Income-tax purpose, it has adopted the completed contract method under which it has recognised revenue of `14,00,000, `36,00,000 and `46,00,000 for the years 2010, 2011 and 2012 respectively. Income-tax rate is 30%. Compute the amount of deferred tax asset/liability for the years 2010, 2011 and (ii) A company had imported raw materials worth US Dollars 6,00,000 on 5th January, 2012, when the exchange rate was ` 43 per US Dollar. The company had recorded the transaction in the books at the above mentioned rate. The payment for the import transaction was made on 5th April, 2012 when the exchange rate was ` 47 per US Dollar. However, on 31st March, 2012, the rate of exchange was `48 per US Dollar. The company passed an entry on 31st March, 2012 adjusting the cost of raw materials consumed for the difference between ` 47 and ` 43 per US Dollar. In the background of the relevant accounting standard, is the company s accounting treatment correct? Discuss. (iii) A Company belonging to the process industry carries out three consecutive processes. The output of the first process is taken as input of the second process, and the output of the second process is taken as input of the third process. The final product emerges out of the third process. It is also possible to outsource the intermediate products. It has been found that over a period time cost of production of the first process is 10% higher than the market price of the intermediate product available freely in the market. The company has decided to close down the first process as a measure of cost saving (vertical spin off) and outsource. Should this event be treated as discontinuing operation? (iv) A.Future Maintainable Profit before Interest-` 125 Lakhs; B. Normal Rate of Return on Long Term Funds is 20% and on Equity Funds is 25%; C. Long Term Funds of the Company is ` 320 Lakhs of which Equity Funds is ` 210 Lakhs; D. Interest on loan Fund is 18%. Find out leverage effect on the Goodwill if tax rate is =30%. (v) Write short note on Human resource Accounting. (4 x 4=16 Marks) PRIME/ME39/FINAL 6

7 PRIME ACADEMY 39 th SESSION MODEL EXAM - FINAL FINANCIAL REPORTING SUGGESTED ANSWERS 1 a) In the above case, the quarterly income has not been correctly stated. As per AS -25, "Interim Financial Reporting", the quarterly income should be adjusted and restated as follows: INR Net Profit as per P&L A/c 10,80,000 Adjustments for: Bad debt of `60,000 has been incurred during the current quarter. Out of (39,000) this, the company has deferred 65% i.e. `39,000 to the next quarter. This is not correct. So, `39,000, should therefore be deducted from `10,80,000, as it is wrongly overstated Treatment of Extra-ordinary loss of `56,000 is correct, hence no adjustment is required to be made against profits for this quarter Treatment of recognizing the additional depreciation of `18,000 is in line with the provisions of AS-25, hence, no adjustment is required Net Profit(adjusted) 10,51,000 b) As per AS-26, "Intangible Assets", the amortization method used should reflect the pattern in which the asset's economic benefits are consumed by the enterprise, if that pattern cannot be determined reliably, the straight line method should be used. In the instant case, the pattern of economic benefit in the form of net cash flows is determined reliably after two years. In the initial two years, the pattern of economic benefits could not have been reliably estimated therefore amortization was done at straight-line method, i.e. `10 lacs per annum. However, after two years pattern of economic benefits for the next five years in the form of net cash flows is reliably estimated as under and therefore amortization will also be done as per the pattern of cash inflows: c) Cash inflows (INR) Amount of amortization in the next 4 years (INR) 49,50,000 [40,00,000 x 49,50,000/2,25,00,000] = 8,80,000 54,00,000 [40,00,000 x 54,00,000/2,25,00,000] = 9,60,000 58,50,000 [40,00,000 x 58,50,000/2,25,00,000] = 10,40,000 63,00,000 [40,00,000 x 63,00,000/2,25,00,000] = 11,20,000 2,25,00,000 Balance of WDV = 40,00,000 (i) (ii) There is a probable present obligation as a result of past obligating event. The obligating event is the sale of product. Provision should be recognized as per AS-29. The best estimate for provision is ` 15,000 (50,00,000 x 0.30%). The airline company has to overhaul its aircraft/s once every three years. There is no present obligation. Hence, no provision is recognized. The costs of overhauling aircraft are not recognized as a provision because at the balance sheet date no obligation of overhauling aircraft exists independently of the company's future actions. Even a legal requirement to overhaul does not make the cost of overhaul/refurbishment cost a liability, because no obligation exists to overhaul the aircraft independently of the enterprise's future actions - the enterprise could avoid the future expenditure by its future actions, for example by selling the aircrafts. PRIME/ME39/FINAL 1

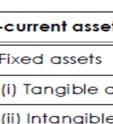

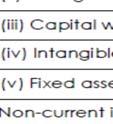

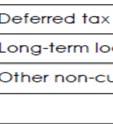

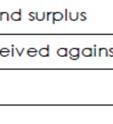

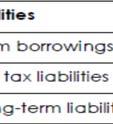

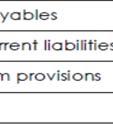

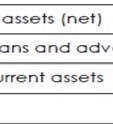

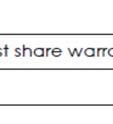

8 d) The treatment done by the company is not in accordance with AS 16 Borrowing Costs. As per para 10 of AS 16, to the extent that funds are borrowed specifically for the purpose of obtaining a qualifying asset, the amount of borrowing costs eligible for capitalisation on that asset should be determined as the actual borrowing costs incurred on that borrowing during the period. Hence, the capitalisation of borrowing costs should be restricted to the actual amount of interest expenditure i.e. ` 1,70,33,465. Thus, there is an excess capitalisation of ` 10,46,535. This has resulted in overstatement of profits by ` 10,46,535 and amount of fixed assets has also gone up by this amount. 2. Aman Ltd. Balance Sheet as at 1st April, 2012 [as per Revised Schedule VI] Particulars Note No Figures as at the Figures as at the end of current end of previous reporting period reporting period I EQUITY AND LIABILITIES ` ` (1) Shareholders funds : (a) Share Capital 1 53,34,660 (b) Reserves and Surplus 2 82,95,000 (c) Money received against share warrants (2) Share application money pending allotment (3) Non-current liabilities : (a) Long-term borrowings (b) Deferred tax liabilities (Net) (c) Other long term liabilities (d) Long term provisions (4) Current Liabilities : (a) Short-term borrowings 3 22,50,000 (b) Trade Payables (c) Other current liabilities 4 31,50,000 (d) Short-term provisions Total 1,96,98,980 II. ASSETS (1) Non-current assets : (a) Fixed assets (i) Tangible assets 5 76,20,000 (ii) Intangible assets (iii) Capital work-in progress (iv)intangible assets under development (b) Non-current Investment (c) Deferred tax assets (net) (d) Long-term loans and advances (e) Other non-current assets (2) Current assets : (a) Current investments PRIME/ME39/FINAL 2

9 (b) Inventories 6 54,75,000 (c) Trade receivables 7 39,00,000 (d) Cash and Cash equivalents 8 27,03,980 (e) Short-term loans and advances (f) Other Current assets Total 1,96,98,980 Annexure Note 1. Share Capital Particulars Amount (`) Share of INR 10 each shares 53,34,660 Share issued in lieu of purchase consideration shares (Share of INR 10 each) Total 53,34,660 Note 2. Reserves and Surplus Particulars Amount (`) General Reserve 50,00,000 Capital Reserve 13,20,000 Profit and Loss Account (` 20,00,000 Unrealised Profit on stock ` 25,000) 19,75,000 Total 82,95,000 Note 3. Short term Borrowings Particulars Amount (`) Secured Loans (` 20,00,000 + ` 2,50,000) 22,50,000 Total 22,50,000 Note 4. Other Current Liabilities Particulars Amount (`) Current Liabilities [(30,00, ,50,000) Mutual Debt 1,00,000] 31,50,000 Total 31,50,000 Note 5. Tangible Assets Particulars Amount (`) Fixed Assets 76,20,000 (` 78,00,000 Revaluation Loss ` 1,80,000) Total 76,20,000 Note 6. Inventories Particulars Amount (`) Inventories [(` 30,00, ,00,000) Unrealised Profit on stock ` 25,000] 54,75,000 Total 54,75,000 Note 7. Trade Receivables Particulars Amount (`) Sundry Debtors [(` 35,00,000 + ` 5,00,000) Mutual Debt. ` 1,00,000] 39,00,000 Total 39,00,000 PRIME/ME39/FINAL 3

10 Note 8. Cash and Cash Equivalents Particulars Amount (`) Cash at Bank 27,03,980 Total 27,03,980 Working Notes : i) Average of Pre-tax profit = = 18 Lakhs 3 Yield = 18 x 50 = 9 Lakhs 100 ii. Price per share of Ayan Ltd:- Capitalised value of yield of Ayan limited = 9 Lakhs X 100 = 60 lakhs 15 No. of shares = 1,00,000 Price per share = 60 lakhs / 1 lakh = 60 per share iii. Purchase consideration for 40% of share capital of Ayan Ltd. = X 60 X = 24,00,000 iv. Calculation of intrinsic value of shares of Aman Ltd. ` Total Assets excluding Investments in Ayan Ltd. 1,64,00,000 Value of Investment 60, ,00,000 2,00,00,000 Less: Outside Liabilities: Secured Loan 20,00,000 Current Liabilities 30,00,000 50,00,000 Net Assets 1,50,00,000 Intrinsic value per share = Net assets = = No of shares INR 30 per share v. Discharge of purchase consideration by Aman Ltd. Equity share Total Cash capital ` ` ` Payment of tax ) X 20 3,92,000 3,92,000 PRIME/ME39/FINAL 4

11 ( Issue of shares to foreign company 50% of ( ) = 10.04lakhs No. of shares issued by Aman Ltd 10,04,000 = 30 = 33, shares Value of shares capital = 33,466X30 Cash payment 50% of ( ) = lakhs 10, , ,04,000 10,04,000 Cash for fractional shares = X Total 10,03,980 13,96,020 24,00,000 vi. Calculation for Goodwill/Capital Reserve to Aman Ltd. ` Total of Assets as per Balance Sheet of Ayan Ltd. 50,00,000 Less: 10% Reduction in the value of Fixed Assets 1,80,000 (10 X 18,00,000) ,20,000 Less: Secured Loan 2,50,000 Current Liabilities 2,50,000 5,00,000 Net Assets 43,20,000 Less: Purchase consideration (outside shareholders) 24,00,000 19,20,000 Less: Investment in Ayan Ltd. as per Balance Sheet of Aman Ltd. 6,00,000 13,20,000 vii. Cash and Bank Balance of Aman Ltd. after acquisition of shares ` Opening Balance (Aman Ltd.) 39,00,000 Cash and Bank Balance of Ayan Ltd. 2,00,000 41,00,000 Less: Remittance to the foreign company 10,04,020 30,95,980 Less: T.D.S. paid to Government 3,92,000 3,92,000 27,03,980 PRIME/ME39/FINAL 5

12 3. viii. Unrealised profit included in stock of Aman Ltd = 1,50,000 x 20/100 ` 25, Basic Information Company Status Date of Acquisition Holding Status Holding Company = Veer Ltd. Lot 1 = 300 Shares = DOA - 1 Holding Company = 70% Subsidiary = Virat Ltd. Lot 2 = 50 Shares = DOA - 2 Minority Interest = 30% Date of Consolidation = Analysis of Reserves & Surplus of Virat Ltd. (a) General Reserve as per B/S = ` 15,000 As on DOA-1 For the period DOA-1 to DOA-2 (Lot 2 date) From DOA-2 to B/s Date (Lot 1 date) ` 12,500 - ` 10,000 = ` 2,500 (up to Consolidation) ` 10,000 For 300 Shares (Lot 1): Revenue ` 2,500) (bal. figure) Capital For 50 Shares (Lot 2): Capital Revenue Total Capital Profits = ` 10,000; Total Revenue Reserves = ` 5,000 Note: Addition to Reserves of `2,500 between DOA-1 and DOA-2 have been considered as Revenue Reserves in full, only for the purpose of determining the share of Minority Interest. After allocating for Minority Interest, the revenue portion of ` 250 (i.e. 10% Shares x ` 2,500) will be added to capital profits. (b) Profit & Loss Account Amount in INR P & L A/c Balance as per B/S 20,000 Less: Proposed Dividend = 50,000 x 15% 7,500 Adjusted Balance of Virat 12,500 As on DOA-1 (Lot 1 date) INR 2,500 Capital For the period DOA-1 to DOA-2 (Lot 2 date) INR 14,000-2,500 = INR 11,500 Less: Dividend out of this = INR 10,000 Net Balance = INR 1,500 For 300 Shares (Lot 1): Revenue For 50 Shares (Lot 2): Capital From DOA-2 to B/s Date (up to Consolidation) INR 8,500 (bal. figure) Revenue Total Capital Profits = INR 2,500; Total Revenue Reserves = INR 10,000 Note: Addition to P&L A/c `1,500 between DOA-1 and DOA-2 have been fully considered as Revenue only for the purpose of determining the share of Minority Interest. After allocating for minority Interest, the revenue portion of ` 150 (i.e. 10% Shares x ` 1,500) will be added to Capital Profits. PRIME/ME39/FINAL 6

13

14

15

16 4 (a

17

18 b) Calculation of capital employed Present value of assets: Premisess and land Plant and machinery Motor vehicles (book value less depreciation for ½ year) Raw materials Work-in-progress Finished goods Book debts (400 x 90% %) Investments in lacs 1,200 2, ,500 in lacs

19 Cash at bank and in hand 192 6,918 Less: Liabilities: Provision for taxation 300 5% Debentures 2,000 Secured loans 200 Sundry creditors 300 2,800 Total capital employed on , Profit available for shareholders for the year Profit for the year as per Balance Sheet 1,100 Less: Depreciation to be considered Premises and land 24* Plant & machinery 240* Motor vehicles Less: Bad debts 40 Profit for the year Average capital employed Total capital employed 4118 Less: ½ of profit for the current year [Refer point 2] 396 Average capital employed 3722 * Depreciation on premises and land and plant and machinery have been provided on the basis of assumption that the same has not been provided for earlier. 4. Average profit to determine Future Maintainable Profits (in lacs) Profit for the year Profit for the year Profit for the year Profit for the year Average Calculation of General Expectation: Jupiter Ltd. pays ` 2 as dividend (20%) for each share of ` 10. Market value of equity shares of the same denomination is ` 25 which fetches dividend of 20%. Therefore, share of ` 10 (Face value of shares of Jupiter Ltd.) is expected to fetch (20/25)x10 = 8% return. Since Domestic Ltd. is not having a stable record in payment of dividend, in its case the expectation may be assumed to be slightly higher, say 10%. 6. Calculation of super profit (in lacs) Future maintainable profit [See point 4] 553 Normal profit (10% of average capital employed as computed in point 3) Super Profit PRIME/ME39/FINAL 13

20 7. Valuation of Goodwill (in lacs) Goodwill at 4 years purchase of Super Profit Notes : (1) It is evident from the Balance Sheet that depreciation was not charged to Profit & Loss Account. (2) It is assumed that provision for taxation already made is sufficient. (3) While considering past profits for determining average profit, the years and have been left out, as during these years normal business was hampered. 6 a) Morning Glory Ltd. Gross Value Added Statement for the year ended 31st March, 2012 In Lakhs ` In Lakhs ` Sales 890 Less: Cost of bought in materials and services: Production and operational expenses ( ) 461 Administration expenses (33 9) 24 Interest on working capital loan 9 Excise duty (Refer working note) Value added by manufacturing and trading activities 341 Add: Other income 55 Total value added 396 Application of Value Added ` ` ` To Employees Salaries, wages, gratuities etc % To Directors % Salaries and commission To Government Cess and local taxes (98 55) 43 Income tax % To Providers of capital Interest on debentures 2 Interest on fixed loan 18 Dividends % To Provide for maintenance and expansion of the company 17 Depreciation 45 General reserve 3 Deferred tax % Retained profits (65 10) % PRIME/ME39/FINAL 14

21 Statement showing reconciliation of Gross Value Added with Profits before taxation In Lakhs ` In Lakhs ` Profits before taxes 225 Add: Depreciation 17 Directors remuneration 9 Salaries, wages & gratuities etc. 82 Cess and local taxes 43 Interest on debentures 2 Interest on fixed loan Total value added 396 Working Note: Calculation of Excise Duty Say cost of bought in materials and services is x Excise Duty is 10% of x = x/10 x = x/10 x = x/10 = 549 (approx.)* Excise Duty = = INR 55 * The above calculated excise duty is not exactly 10% of cost of bought in material amounting INR 549. The difference is due to approximation. b) Date Particulars Debit ` Credit ` At the time of inception 2003 July Stock option premium account Dr. 2,000 To Bank account 2,000 (Being premium paid to buy a stock option) Deposit for margin money account Dr To Bank account (Being margin money paid on stock option) At the time of settlement August (i) Option is settled by delivery of the asset Shares of PQR Ltd. account Dr To Deposit for margin money account To Bank account (Being option exercised and shares acquired, INR 12,000 margin money adjusted and the balance amount was paid) Profit and loss account Dr To Stock option premium account 2000 (Being the premium transferred to profit and loss account on exercise of option) PRIME/ME39/FINAL 15

22 (ii) Option is settled in cash Profit and loss account Dr. 2,000 To Stock option premium account 2000 (Being the premium transferred to P&L a/c Bank account (INR 100X10) Dr. 1,000 To Profit and loss account 1,000 (Being profit on exercise of option) 7. (i) Bank account Dr. 12,000 To Deposit for margin money account 12,000 (Being margin on equity stock option received back on exercise of option) Deferred tax asset/liability Tulip Ltd. Calculation of Deferred Tax Asset/Liability Year Accounting Income ` Taxable Income ` Timing (balance) ` Difference Deferred Tax Liability (balance) ` ,00,000 14,00,000 8,00,000 2,40,000 2,011 32,00,000 36,00,000 4,00,000 1,20,000 2,012 42,00,000 46,00, ,00,000 96,00,000 (ii) AS - 11 As per AS 11 (revised 2003), The Effects of Changes in Foreign Exchange Rates, monetary items denominated in a foreign currency should be reported using the closing rate at each balance sheet date. The effect of exchange difference should be taken into profit and loss account. Sundry creditors is a monetary item, hence should be valued at the closing rate i.e, ` 48 at 31st March, 2012 irrespective of the payment for the same subsequently at lower rate in the next financial year. The difference of ` 5 (48-43) per US dollar should be shown as an exchange loss in the profit and loss account for the year ended 31st March, 2012 and is not to be adjusted against the cost of rawmaterials. In the subsequent year, the company would record an exchange gain of Re.1 per US dollar, i.e., the difference between ` 48 and ` 47 per Us dollar. Hence, the accounting treatment adopted by the company is incorrect. (iii) Discontinuing Operations The change made by the company is focused on outsourcing of services, in respect of one single process in a sequence of process. The net effect of this change is closure of facility relating to process. This has been done by the company with a view to achieving productivity improvement and savings in costs. Such a change does not meet definition criteria in paragraph 3(a) of AS 24- namely, disposing of substantially in its entirety, such as by selling a component of the enterprise in a single transaction. The change is merely a cost-saving endeavor. Hence, this change over is not a discontinuing operation. PRIME/ME39/FINAL 16

23 (iv) Leverage A. Long Term Loan Funds= Total Long Term funds Less Equity Funds= INR ( ) lakhs= INR 110 Lakhs Interest at 18% thereon = ` 110 Lakhs X18% = ` lakhs B. Computation of future Maintainable Profit (` Lakhs) Particulars Shareholders Long Term funds approach Funds approach Profit Before Interest Less: Interest on Long term loan N.A Future Maintainable Profits before tax Less : Tax Expense at 30% Future Maintainable Profit After tax C. Computation of Goodwill under different approaches (INRLakhs) Particulars Shareholders Long Term funds approach Funds approach a. Future Maintainable Profit after tax b. Normal Rate of Return 25% 20% c. Normal Capital Employed =(a b) d. Actual Capital Employed (given) e. goodwill= (c-d) Hence, Leverage Effect on Goodwill = ` ( ) = ` Lakhs. (v) Human Resource Accounting (HRA) Human Resource Accounting (HRA) is an attempt to identify, quantify and report investments made in human resources of an organization. Leading public sector units like OIL, BHEL, andntpc etc. have started reporting human resources in their annual reports as additional information. Although human beings are considered as the prime mover for achieving productivity, and are placed above technology, equipment and money, the conventional accounting practice does not assign significance to the human resource. Human resources are not thus recognized as assets in the Balance Sheet While investments in human resources are not considered as assets and not amortised over the economic service life, the result is that the income and expenditure statement comprising current revenue and expenditure gives a incorrect picture of the real affairs of the organization. Accountants have been severely criticized by the Behavioural Scientists for their failure to value human resources, as this has come out as a handicap for effective management. Human resource accounting provides scope for planning and decision making in relation to proper manpower planning. Also, such accounting can bring out the effect of various new rules, procedures and incentives relating to work force,and in turn, can act as an eye opener for modifications of existing laws and statutes. PRIME/ME39/FINAL 17

24 2. 1. SMT No. of Pages: 4 Total Marks: 100 No. of Questions: 7 Time allowed: 3 hrs Question no: 1 is compulsory. Attempt any five out of the remaining six. Wherever appropriate, suitable assumptions should be made and indicated in the answer Working notes should form part of the answer (a) Given: a two- year, 8% annual coupon bond with a face value of ` 1,000 and with annual coupon payments that is fully taxable ; selling at par and an identical bond with same coupon rate and face value and anuual interest payments that is tax free What would be the yield and price on tax free bonds for an investor in 35% tax bracket to be indifferent between two bonds? (b) Dhanpat, an investor, is seeking the price to pay for a security, whose standard deviation is 5%. The correlation coefficient for the security with the market is 0.75 and the market standard deviation is 4%. The return from risk free securities is 6% and from the market portfolio is 11%. Dhanpat knows that only by calculating the required rate of return, he can determine the price to pay for the security. What is the required rate of return on the security? (c) While evaluating a capital project, a company is considering an option to buy a business from a third party at the cost of ` 50 crores. It is expected that in next one year, the value of such business will increase to ` 60 crores with probability 70% or decline to ` 45 crores with probability of 30%. The company may enter into an agreement with a party to sell the said business at `48 crores after one year if the company so desires. Assuming that this real option is like a European Call, with the strike price of the underlying real asset is `48 crores and the risk free interest rate is 9% p.a. Determine the value of this real option. (d) A company pays dividend of ` 2 per share with a growth rate of 7%. The risk free rate is 9% and the market rate of return is 13%. The company has a beta factor of However, due to a decision of the Finance manager, beta is likely to be increased to Find out the present as well as the likely value of the share after the decision. [ 4 x 5 = 20 Marks] (a) Trouble Free Solutions (TFS) is an authorized service center of a reputed domestic air conditioner manufacturing company. All complaints/ service related matters of Air conditioner are attended by this service center. The service center employs a large number of mechanics, each of whom is provided with a motor bike to attend the complaints. Each mechanic travels approximately 40,000 kms p.a. TFS decides to continue its present policy of always buying a new bike for its mechanics but wonders whether the present policy of replacing the bike every three year is optimal or not. It is of believe that as new models are entering into market on yearly basis, it wishes to consider whether a replacement of either one year or two years would be better option than present three year period. The fleet of bike is due for replacement shortly in near future. The purchase price of latest model bike is ` 55,000. Resale value of used bike at current prices in market is as follows: Period ` 1 Year old 35,000 2 Year old 21,000 3 Year old 9,000 Running and Maintenance expenses (excluding depreciation) are as follows: PRIME/ME39/FINAL 1

25 Year Road Taxes, Insurance etc. (`) Petrol Repair Maintenance etc. (`) 1 3,000 30, ,000 35, ,000 43,000 Using opportunity cost of capital as 10% you are required to determine optimal replacement period of bike. 3. (b) A Mutual Fund is holding the following assets in ` Crores : Investments in diversified equity shares Cash and Bank Balances The Beta of the portfolio is 1.1. The index future is selling at 4300 level. The Fund Manager apprehends that the index will fall at the most by 10%. How many index futures he should short for perfect hedging so that the portfolio beta is reduced to 1.00? One index future consists of 50 units. Substantiate your answer assuming the Fund Manager's apprehension will materialize. [2 x 8 = 16 Marks] (a) Consider the following operating information gathered from 3 companies that are identical except for their capital structures: P Ltd. ` Q Ltd. ` R Ltd. ` Total invested capital `100,000 `100, ,000 Debt/assets ratio Shares outstanding 6,100 8,300 10,000 Before-tax cost of debt 14% 12% 10% Cost of equity 26% 22% 20% Operating income(ebit) 25,000 25,000 25,000 Net Income 8,970 12,350 14,950 Tax rate 35% 35% 35% i. Compute the weighted average cost of capital, WACC, for each firm. ii. Compute the Economic Value Added, EVA, for each firm. iii. Based on the results of your computations in part b, which firm would be considered the best investment? Why? iv. Assume the industry P/E ratio generally is 15. Using the industry norm, estimate the price for each share. v. What factors would cause you to adjust the P/E ratio value used in part iv so that it is more appropriate? (b) Following information is available for two firms: Firm Objective Fixed rate Floating rate A Floating rate 10% L % B Fixed rate 11% L + 1% Explain how the two firms would enter into a swap transaction to reduce their interest costs, if A does not want to pay more than L %. [2 x 8 = 16 Marks] PRIME/ME39/FINAL 2

26 4. (a) Zumo & Co. is a watch manufacturing company and is all equity financed and has paid up capital `10,00,000 (`10 per shares). The other data related to the company is as follows: Year EPS (`) Net Dividend per share(rs) Zumo & Co. has hired one management consultant, Vidal Consultants to analyze the future earnings and other related item for the forthcoming years. As per Vidal Consultant s report : The earnings and dividend will grow at 25% for the next two years. Earnings are likely at rate of 10% from 3rd year and onwards. Further if there is reduction in earnings growth occurs dividend payout ratio will increase to 50% Calculate the estimated share price and P/E Ratio which analysts now expect for Zumo & Co., using the dividend valuation model. You may further assume that post tax cost of capital is 18%. (b) Lammer plc is a UK based company that regularly trades with companies in the USA. Several large transactions are due in five months time. These are shown below. The transactions are in 000 units of these currencies shown. Exports to: Imports from: Company USD 150UKP Company 2-890USD Company 3 110KP 750USD Exchange rate USD/ UKP Spot months forward rate Annual interest rates available to Lammer plc: Borrowing Investing UKP 5.5% 4.2% USD 4.0% 2.0% How the five month currency risk should be hedged? Consider Forward and money market operations and advice which is the best alternative. [2 x 8 = 16 Marks] 5. (a) Internet Services Ltd. is a listed company and the share prices have been volatile. An investor expects that the share price may fall from the present level of `1,900 and wants to make profit by a suitable option strategy. He is short of share at a price of ` 1,900and wants to protect himself against any loss. The following option rates are available : Strike price Call option Put option PRIME/ME39/FINAL 3

27 The investor decides to buy a call at a strike price of `1,800 and to write a put at a strike price of ` 2,000. Find out the profit or loss profile of the investor if the share price on the expiration date is `1,600, `1,700, `1,800, `1,900, `2,000 or `2,100 (b) Bharat Ltd. is a highly successful company and wishes to expand by acquiring other firms. Its expected high growth in earnings and dividends is reflected in its PE ratio of 17. The Board of Directors of Bharat Ltd. has been advised that if it were to take over firms with a lower PE ratio than its own, using a share for share exchange, then it could increase its reported earnings per share. China Ltd. has been suggested as a possible target for a take over, which has a PE ratio of 10 and 1,00,000 shares in issue with a share price of `15. Bharat Ltd. has 5,00,000 shares in issue with a share price of `12. You are required to calculate the change in earnings per share of Bharat Ltd., if it acquires the whole of China Ltd., by issuing shares at its market price of `12. Assume the price of Bharat Ltd. shares remains constant. Also compute the new PE ratio. [2 x 8 = 16 Marks] 6. (a) A mutual fund company introduces two schemes i.e. Dividend plan (Plan-D) and Bonus plan (Plan- B).The face value of the unit is `10. On Mr. K invested ` 2,00,000 each in Plan-D and Plan- B when the NAV was `38.20 and `35.60 respectively. Both the plans matured on Particulars of dividend and bonus declared over the period are as follows: Date Dividend Bonus Ratio Net Asset Value (`) Plan D Plan B : : : What is the effective yield per annum in respect of the above two plans? (b) L LTd is engaged in manufacturing and trading of handicrafts. It exported handicrafts worth AUS$ 2,50,000 to B Ltd of Australia under a letter of credit and submitted all its documents to its banker on July 20, However due to unavoidable circumstances bank could negotiate the bill on August 10 th 2014 and sent the money to L Ltd after collecting an exchange margin of 0.5%. The spot exchange rates in Mumbai and Singapore as on 20 th July and 10 th August are given below: July Aug Mumbai INR/ Euro Singapore SGD/ Euro SGD/AUS$ You are required to calculate the rupees received by the exporter on August 10 th and the loss or gain to the exporter due to delay in negotiation of bill under L/C. [2 x 8 = 16 Marks] 7. Answer any four (a) Beta of a security can be negative. Comment (b) Cross border leasing (c) Types/ forms of Factoring (d) External commercial borrowings (e) Book building [4 x 4 = 16 Marks] PRIME/ME39/FINAL 4

28 1 PRIME ACADEMY 39 th SESSION MODEL EXAM - FINAL STRATEGIC FINANCIAL MANAGEMENT SUGGESTED ANSWERS (a) For an investor to be indifferent, yield from both the bonds must be equal. Yield from taxable bond is 8(1-.35) = 5.2%. So, expected return from tax free bond is also 5.2%. Price today = PV of Interest and principal payments 5.2%. Interest = 8% of 1000 = 80 Year CF 5.2% DCF 1 Interest Interest Principal Price today = (b) Beta of the security = Std deviation of X x COR(X,Y)/ Std deviation Y = 5 x 0.75/ 4 = Required rate of return using CAPM = Rf + Beta(Rm-Rf) = (11-6) = % (c) ` crores Maximum expected value of business after 1 year = 60 present 9% 60/ NPV ( initial outlay 50) 5.05 Expected NPV as probability of this is only 70% 3.53 If the market value declines to 45crore, the company can sell for 48 crores Loss = PV of Crores = ` 5.96 Crores Thus maximum loss the company will incur is 5.96 which is the option premium or value of option (d) Ke= Rf + Beta(Rm- Rf) = (13-9) = 15% P0 = D1/ Ke-g = 2(1.07)/ = New beta after the decision is New Ke =16% and hence P0 =2.14/ = (a) Year Road Taxes (`) Petrol etc. (`) Total (`) PV (`) Cumulative PV (`) PV of Net Resale Outflow Price (`) (`) 1 3,000 30,000 33, ,997 29,997 31,815 (1,818) 2 3,000 35,000 38, ,388 61,385 17,346 44, ,000 43,000 46, ,546 95,931 6,759 89,172 Computation of EACs Year Purchase Net Price of Bike (`) (`) Outflow Total Outflow(`) 10% EAC (`) 1 55,000 (1,818) 53, , ,000 44,039 99, , ,000 89, , ,993 PRIME/ME39/FINAL 1

29 (b) 3 (a) Thus, from above table it is clear that EAC is least in case of 2 years, hence bike should be replaced every two years Number of index future to be sold by the Fund Manager is: 1.1 x 90,00,00,000/ (4,300x 50) = 4,605 Justification of the answer: Loss in the value of the portfolio if the index falls by 10% is = 10(1.10)% `90 Crore = `9.90 Crore. Gain from futures: Gain from one contract = 430 Total gain = 430 x 50 x 4605 = `9.90 crores i. WACCP = [14.0%(1-0.35)](0.80) %(0.20) = 12.48% WACCQ = [12.0%(1-0.35)](0.50) %(0.50) = 14.90% WACCR = [10.0%(1-0.35)](0.20) %(0.80) = 17.30% ii. EVA = EBIT(1 - T) - (WACC x Invested capital) EVAP = `25,000(1-0.35) - ( x `100,000) = ` 16,250 ` 12,480 = `3,770 EVAQ = `25,000(1-0.35) - ( x `100,000) = `16,250 - `14,900= `1,350 EVAR = `25,000(1-0.35) - ( x `100,000) = `16,250 - `17,300 = - `1,050 iii. EVAP > EVAQ > EVAR; Thus, P Ltd. would be considered the best investment. The result should have been obvious, given that the firms have the same EBIT, but WACCP < WACCQ < WACCR. iv. P Ltd. ` Q Ltd. ` R Ltd. ` EBIT 25,000 25,000 25,000 Interest (11,200) (6,000) (2,000) Taxable income 13,800 19,000 23,000 Tax (35%) 4,830 6,650 8,050 Net income 8,970 12,350 14,950 Shares 6,100 8,300 10,000 EPS Stock price v. Given the three firms have substantially different capital structures, we would expect that they also have different degrees of financial risk. Therefore, we might want to adjust the P/E ratios to account for the risk differences. (a) Following information is available for two firms: Firm Objective Fixed rate Floating rate A Floating rate 10% L % B Fixed rate 11% L + 1% Explain how the two firms would enter into a swap transaction to reduce their interest costs, if A does not want to pay more than L %. (b) Difference in interest rates: Fixed rate = Floating rate = L+1 -(L+0.75) 0.25 Net differential 0.75 PRIME/ME39/FINAL 2

30 Share of A 0.40 and B 0.35 Since fixed rate differential is greater, swap would work if A ltd would desire Floating rate. Steps for A 1. A borrows at fixed rate. Pays to bank at fixed rate (10.00 ) 2. Receive from B interest (step 1 + gain share of A) 3. Pay to B interest at floating rate (L ) Effective interest cost L Steps for B 1. Borrow from bank at floating rate (L+1%) 2. Pay to A fixed interest (10.40) 3. Receive from A Floating interest L Effective interest cost (a) Step 1: computation of dividends 1 to 3 and dividend for year 4 Year Growth EPS (`) DPS(`) % % % % (50% of EPS of 2012) Step 2: Compute price at the end of 2011 i.e beginning of 2012 P3 = D4/ (Ke- g) = 6.66/( ) = `83.25 Step 3: Price of share today = PV of dividends for years 1 to 3 and Price at year 3 Year DPS PVIF DCF Price today ` PE ratio = Price at the beginning of 2009/ EPS of 2008 = 59.09/6.2 =9.53 (b) The UK company has to hedge net outflow of $ 1150 thousands. (No hedging is done for home currency transaction). Forward: The UK firm shall be purchasing the $ i.e the bank shall be purchasing. The bid will be applicable. 5 months forward bid: 1 = $ Cost of purchasing 1150 thousands $ on 5 months forward basis = 11,50,000 / = 6,04,341. Interest on Investment of Dollars = 2 x 5/12 = 0.833% Let purchase $ 1150 thousands / i.e $ thousands Invest this Dollar amount (in 2 % p.a for 5 months Investment proceeds = 1150 thousand Dollars PRIME/ME39/FINAL 3

31 Use this investment proceeds to meet the liability of $ 1150 thousands (after 5 months from today) To purchase $ thousand, we require $ thousand / i.e thousands. Let s borrow m. Use this amount for purchasing $ thousands Repay the borrowed Home currency ( ) after five months, along with 5.50% p.a. Total amount of interest = x 5.50/100 x 5/12 = thousands Total amount payable = thousands thousands = thousands 5 (a) Call option bought: MP Action Pay off Premium Net pay off 1600 L L L E E E Put option written: Action Pay off Premium Net pay off Total 1600 E E E E L L (b) Particulars Bharat Ltd. China Ltd P E ratio No: of shares 50,00,000 10,00,000 MPS (`) EPS( MPS/PER) Earnings 35,30,000 15,00,000 Total earnings after merger is Lakhs = Lakhs No: of shares offered to China Ltd 10L x 5/12 I,e lacs EPS combined = 50.30L/( ) = Market value of combine entity = (12 x 50 L + 15 x10l)=750 L MPS = Market vale / New no: of shares =750/62.50=12 New PE ratio = MPS/EPS=12/ =14.92 Increase in EPS = = PRIME/ME39/FINAL 4

Revisionary Test Paper_Final_Syllabus 2008_Dec2013

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Question No.1(a) Paper 16 Advanced Financial Accounting & Reporting What is 'discontinuing operations' as per AS-24? Answer: As per Para 3 of the standard, a discontinuing operation is a component of an

Suggested Answer_Syl12_Dec13_Paper 18 FINAL EXAMINATION GROUP - IV

FINAL EXAMINATION GROUP - IV SYLLABUS - 2012 SUGGESTED ANSWERS TO QUESTION DECEMBER 2013 Paper 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP - IV SYLLABUS - 2012 SUGGESTED ANSWERS TO QUESTION DECEMBER 2013 Paper 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION (SYLLABUS 2008) GROUP IV SUGGESTED ANSWERS TO QUESTIONS. December Time Allowed : 3 Hours Full Marks : 100

GROUP IV SUGGESTED ANSWERS TO QUESTIONS. December Time Allowed : 3 Hours Full Marks : 100") 1 Suggested Answers to Question AFA FINAL EXAMINATION (SYLLABUS 2008) GROUP IV SUGGESTED ANSWERS TO QUESTIONS December 2012 Paper 16 : ADVANCED FINANCIAL ACCOUNTING AND REPORTING Time Allowed : 3 Hours

1 Suggested Answers to Question AFA FINAL EXAMINATION (SYLLABUS 2008) GROUP IV SUGGESTED ANSWERS TO QUESTIONS December 2012 Paper 16 : ADVANCED FINANCIAL ACCOUNTING AND REPORTING Time Allowed : 3 Hours

Paper 16 Advanced Financial Accounting and Reporting

Group IV Paper 16 Advanced Financial Accounting and Reporting 1. (a) Venus Ltd. has an asset, which is carried in the Balance Sheet on 31.3.2014 at 1,000 lakhs. As at that date the value in use is 800

Group IV Paper 16 Advanced Financial Accounting and Reporting 1. (a) Venus Ltd. has an asset, which is carried in the Balance Sheet on 31.3.2014 at 1,000 lakhs. As at that date the value in use is 800

Copyright -The Institute of Chartered Accountants of India. The forward contract is sold before its due date, hence considered as speculative.

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

PAPER 1: FINANCIAL REPORTING Answer all questions. Working notes should form part of the answer. Wherever necessary, suitable assumptions may be made by the candidates. Question 1 (a) Mr. A bought a forward

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

MOCK TEST PAPER - 2 FINAL: GROUP I PAPER 1: FINANCIAL REPORTING SUGGESTED ANSWERS/HINTS Test Series: October, 2017 1. (a) Statement Showing Impairment Loss ( in crores) Carrying amount of the machine as

Test Series: March, 2018

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

MOCK TEST PAPER INTERMEDIATE (NEW) : GROUP II PAPER 5 : ADVANCED ACCOUNTING Question No. 1 is compulsory. Answer any four questions from the remaining five questions. 1 Test Series: March, 2018 Wherever

Valuation. The Institute of Chartered Accountants of India

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

No. of Pages: 7 Total Marks: 100

LG No. of Pages: 7 Total Marks: 100 No of Questions: 7 Time Allowed: 3 Hrs Question No. 1 is compulsory Answer any five questions from the remaining six questions. Wherever necessary, suitable assumption(s)

LG No. of Pages: 7 Total Marks: 100 No of Questions: 7 Time Allowed: 3 Hrs Question No. 1 is compulsory Answer any five questions from the remaining six questions. Wherever necessary, suitable assumption(s)

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM. Test Code CIN 5010

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- ADVANCED ACCOUNTS Test Code CIN 5010 Date: 25.08.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION INTERMEDIATE N 2018 EXAM SUBJECT- ADVANCED ACCOUNTS Test Code CIN 5010 Date: 25.08.2018 Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

Revisionary Test Paper for June 2012 Examination

Question 1 Paper 16 Advanced Financial Accounting & Reporting How would you deal with the following in the annual accounts of a company for the year ended 31st March, 2012? (a) (b) Answer (a) The company

Question 1 Paper 16 Advanced Financial Accounting & Reporting How would you deal with the following in the annual accounts of a company for the year ended 31st March, 2012? (a) (b) Answer (a) The company

Valuation. The Institute of Chartered Accountants of India

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

9 Valuation BASIC CONCEPTS CONCEPT OF VALUATION Valuation means measurement of value in monetary term. Different measurement bases are: (a) Historical cost. Assets are recorded at the amount of cash or

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

SUGGESTED SOLUTION CA FINAL MAY 2017 EXAM FINANCIAL REPORTING Test Code - F M J 4 0 1 5 BRANCH - (MULTIPLE) (Date : ) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING Question 1 is compulsory (4 5 = 20 Marks) Answer any five questions from the remaining six questions (16 5 = 80 Marks).

Gurukripa s Guideline Answers to Nov 2014 Exam Questions CA Final FINANCIAL REPORTING Question 1 is compulsory (4 5 = 20 Marks) Answer any five questions from the remaining six questions (16 5 = 80 Marks).

File Downloaded From

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

PAPER 5 : ADVANCED ACCOUNTING

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting Question No. 1 is Compulsory. Answer any FIVE questions from the remaining SIX questions. Question 1(a)

SHREE GURU KRIPA S INSTITUTE OF MANAGEMENT Guideline Answers for November 2011 Financial Reporting Question No. 1 is Compulsory. Answer any FIVE questions from the remaining SIX questions. Question 1(a)

` 38,000 in the refurbishment of the premise. These are to be considered as

PAPER 1: FINANCIAL REPORTING Question No.1 is compulsory. Answer any five questions from the remaining six questions. Working notes should form part of the respective answers. Wherever necessary, candidates

PAPER 1: FINANCIAL REPORTING Question No.1 is compulsory. Answer any five questions from the remaining six questions. Working notes should form part of the respective answers. Wherever necessary, candidates

Answer to MTP_Final_Syllabus 2008_Jun2015_Set 1

Paper-16: Advanced Financial Accounting & Reporting Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Working Notes should form part of the answer.

Paper-16: Advanced Financial Accounting & Reporting Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Working Notes should form part of the answer.

Suggested Answer_Syl12_Dec2015_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper- 18 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2015 Paper- 18 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

SUGGESTED SOLUTION FINAL MAY 2019 EXAM. Test Code FNJ 7098

SUGGESTED SOLUTION FINAL MAY 2019 EXAM SUBJECT- FR Test Code FNJ 7098 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 Answer 1:

SUGGESTED SOLUTION FINAL MAY 2019 EXAM SUBJECT- FR Test Code FNJ 7098 BRANCH - () (Date :) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666 Answer 1:

Paper-12 : COMPANY ACCOUNTS & AUDIT

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Paper-12 : COMPANY ACCOUNTS & AUDIT Study Note 1: Conceptual Framework for Preparation and Presentation of Financial Statements Question No. 1 Discuss the use of the General Purpose Financial Statement

Gurukripa s Guideline Answers to May 2015 Exam Questions CA Final Financial Reporting

Gurukripa s Guideline Answers to May 2015 Exam Questions CA Final Financial Reporting Question No.1 is compulsory (4 5 = 20 Marks). Answer any five questions from the remaining six questions (16 5 = 80

Gurukripa s Guideline Answers to May 2015 Exam Questions CA Final Financial Reporting Question No.1 is compulsory (4 5 = 20 Marks). Answer any five questions from the remaining six questions (16 5 = 80

Suggested Answer_Syl12_June2016_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

Test Series: March, 2017

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary suitable

MOCK TEST PAPER INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: March, 2017 Wherever necessary suitable

Paper-18 : CORPORATE FINANCIAL REPORTING

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

Paper-18 : CORPORATE FINANCIAL REPORTING 1. (a) Write a note on IFRS. (b) Accounts of R Ltd. show a net profit of `7,20,000 for the third quarter of 2014 after incorporating the following: (i) Bad debts

PRIME ACADEMY 31st SESSION MODEL EXAM - FINAL FINANCIAL REPORTING QUESTION PAPER FRT. No. of Pages: 6 Total Marks: 100

PRIME ACADEMY 31st SESSION MODEL EXAM - FINAL FINANCIAL REPORTING QUESTION PAPER FRT No. of Pages: 6 Total Marks: 100 No of Questions: 6 Time Allowed: 3 Hrs All are compulsory 1. a) While preparing its

PRIME ACADEMY 31st SESSION MODEL EXAM - FINAL FINANCIAL REPORTING QUESTION PAPER FRT No. of Pages: 6 Total Marks: 100 No of Questions: 6 Time Allowed: 3 Hrs All are compulsory 1. a) While preparing its

MTP_Final_Syllabus 2008_Dec2014_Set 1

Paper-12: FINANCIAL MANAGEMENT & INTERNATIONAL FINANCE Time Allowed: 3 Hours Full Marks: 100 Answer Question No. 1 from Part A which is compulsory and any five questions from Part B. Working notes should

Paper-12: FINANCIAL MANAGEMENT & INTERNATIONAL FINANCE Time Allowed: 3 Hours Full Marks: 100 Answer Question No. 1 from Part A which is compulsory and any five questions from Part B. Working notes should

DEAR PRIME ACADEMY STUDENT, 1. FOR FINANCIAL INSTRUMENTS (PRACTICAL QUESTIONS), REFER TO ICAI BOOKLET ON THE SAME ONLY

, REFER TO ICAI BOOKLET ON THE SAME ONLY") DEAR PRIME ACADEMY STUDENT, 1. FOR FINANCIAL INSTRUMENTS (PRACTICAL QUESTIONS), REFER TO ICAI BOOKLET ON THE SAME ONLY 2. REFER LATEST RTP AND TO THAT EXTENT QUESTIONS THAT WERE COMMON IN THIS PRACTICE

DEAR PRIME ACADEMY STUDENT, 1. FOR FINANCIAL INSTRUMENTS (PRACTICAL QUESTIONS), REFER TO ICAI BOOKLET ON THE SAME ONLY 2. REFER LATEST RTP AND TO THAT EXTENT QUESTIONS THAT WERE COMMON IN THIS PRACTICE

PAPER 1 : ADVANCED ACCOUNTING Answer all questions. Working notes should form part of the answer.

Question 1 PAPER 1 : ADVANCED ACCOUNTING Answer all questions. Working notes should form part of the answer. The following information has been extracted from the Books of X Limited group (as at 31 st

Question 1 PAPER 1 : ADVANCED ACCOUNTING Answer all questions. Working notes should form part of the answer. The following information has been extracted from the Books of X Limited group (as at 31 st

Suggested Answer_Syl12_Dec2014_Paper_18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

The Institute of Chartered Accountants of India

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

PAPER 5 : ADVANCED ACCOUNTING Question No.1 is compulsory. Candidates are also required to answer any five questions from the remaining six questions. Working notes should form part of the respective answers.

THIS CHAPTER COMPRISES OF. Working knowledge of : AS 1, AS2, AS 3, AS 6, AS 7, AS 9, AS 10, AS 13, AS 14.

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter CHAPTER 1 Accounting Standards

Fixed Assets less depreciation. Reserves Cost of investment in B Ltd. Profit and loss balance

PAPER 1 : FINANCIAL REPORTING QUESTIONS Consolidated Financial Statements of Group Companies 1. From the following Balance Sheets of a group of companies and the other information provided, draw up the

PAPER 1 : FINANCIAL REPORTING QUESTIONS Consolidated Financial Statements of Group Companies 1. From the following Balance Sheets of a group of companies and the other information provided, draw up the

PTP_Final_Syllabus 2008_Jun 2015_Set 2

Paper-12: FINANCIAL MANAGEMENT & INTERNATIONAL FINANCE Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Answer Question No. 1 from Part A which is

Paper-12: FINANCIAL MANAGEMENT & INTERNATIONAL FINANCE Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Answer Question No. 1 from Part A which is

Suggested Answer_Syl12_Dec2017_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2017 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

Answer to MTP_Final _Syllabus 2016_Dec2017_Set 2 Paper 17- Corporate Financial Reporting

Paper 17- Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full

Paper 17- Corporate Financial Reporting Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full

Suggested Answer_Syl2012_Dec2014_Paper_20 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper- 20 : FINANCIAL ANALYSIS & BUSINESS VALUATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

P18_Practice Test Paper_Syl12_Dec13_Set 1

Corporate Financial Reporting Syllabus 2012 1. Answer any two from question No.1 [2 5] (a) Rose Ltd. entered into agreement with Tulip Ltd. for sale of goods of 8 lakhs at a profit of 20% on cost. The

Corporate Financial Reporting Syllabus 2012 1. Answer any two from question No.1 [2 5] (a) Rose Ltd. entered into agreement with Tulip Ltd. for sale of goods of 8 lakhs at a profit of 20% on cost. The

Financial Statements of Companies

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

2 Financial Statements of Companies BASIC CONCEPTS UNIT 1: PREPARATION OF FINANCIAL STATEMENTS While preparing the final accounts of a company the following should be kept in mind: Requirements of Schedule

Suggested Answer_Syl12_Dec2016_Paper 18 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

FINAL EXAMINATION GROUP IV (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2016 Paper- 18: CORPORATE FINANCIAL REPORTING Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

AMALGAMATION, ABSORPTION AND RECONSTRUCTION

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

CHAPTER-5 AMALGAMATION, ABSORPTION AND RECONSTRUCTION Q. 1. The following is the summarized Balance Sheet of A Ltd. as on 31.3.2012 Liabilities Assets 14,000 Equity shares of Sundry assets 18,00,000 100

UNIT 4 : AMALGAMATION AND RECONSTRUCTION

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

Company Accounts 3.1 UNIT 4 : AMALGAMATION AND RECONSTRUCTION (A) Write short notes on : Question 1 Amalgamation and Absorption of companies a comparison.(3 marks)(intermediate Nov. 1994) Answer In accounting

PAPER 1 : ADVANCED ACCOUNTING QUESTIONS

Company Accounts Internal Reconstruction of a Company PAPER 1 : ADVANCED ACCOUNTING QUESTIONS 1. Paradise Limited which had experienced trading difficulties, decided to reorganize its finances. On March

Company Accounts Internal Reconstruction of a Company PAPER 1 : ADVANCED ACCOUNTING QUESTIONS 1. Paradise Limited which had experienced trading difficulties, decided to reorganize its finances. On March

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

PAPER 3 : COST ACCOUNTING AND FINANCIAL MANAGEMENT PART I : COST ACCOUNTING QUESTIONS Material 1. The following information has been extracted from the records of a cotton merchant, for the month of March,

Revisionary Test Paper_Dec 2018

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

Final Group IV Paper 17 : CORPORATE FINANCIAL REPORTING (SYLLABUS 2016) 1. Multiple Choice Questions: Objectives (i) Mittal Ltd. has provided the following information: Depreciation as per accounting records

P18_Practice Test Paper_Syl12_Dec13_Set 3

Full Marks: 100 Paper 18 : Corporate Financial Reporting Time : 3 hours 1. Answer any two Questions from Question No.1 [2 5] (a) Write a note on IFRS. (b) As on 1st April, 2011 the Fair Value of Plan Assets

Full Marks: 100 Paper 18 : Corporate Financial Reporting Time : 3 hours 1. Answer any two Questions from Question No.1 [2 5] (a) Write a note on IFRS. (b) As on 1st April, 2011 the Fair Value of Plan Assets

PTP_Final_Syllabus 2008_Dec 2014_Set 2

Paper-18: BUSINESS VALUATION MANAGEMENT Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Answer Question No. 1 which is compulsory carrying 25 marks

Paper-18: BUSINESS VALUATION MANAGEMENT Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Answer Question No. 1 which is compulsory carrying 25 marks

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER. The Institute of Chartered Accountants of India

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

DISCLAIMER The Suggested Answers hosted in the website do not constitute the basis for evaluation of the students answers in the examination. The answers are prepared by the Faculty of the Board of Studies

Answer to MTP_Final _Syllabus 2016_Jun 2018_Set 1 Paper 17- Corporate Financial Reporting

Paper 17- Corporate Financial Reporting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full Marks : 100 Time

Paper 17- Corporate Financial Reporting DoS, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 17- Corporate Financial Reporting Full Marks : 100 Time

Suggested Answer_Syl2008_June 2015_Paper_16 FINAL EXAMINATION

FINAL EXAMINATION GROUP IV (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2015 Paper-16: ADVANCED FINANCIAL ACCOUNTING & REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

FINAL EXAMINATION GROUP IV (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS JUNE 2015 Paper-16: ADVANCED FINANCIAL ACCOUNTING & REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

PTP_Final_Syllabus 2008_Dec2014_Set 3

Paper-16: Advanced Financial Accounting & Reporting Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Working Notes should form part of the answer.

Paper-16: Advanced Financial Accounting & Reporting Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full marks. Working Notes should form part of the answer.

As at March 31, Note No. INR INR INR A 1

Balance Sheet as at March 31, 2017 As at March 31, 2017 As at March 31, 2016 (Amounts in lakhs) As at April 01, 2015 A 1 ASSETS Non-current assets (a) Property, Plant and Equipment 4 42,192.53 44,452.57

Balance Sheet as at March 31, 2017 As at March 31, 2017 As at March 31, 2016 (Amounts in lakhs) As at April 01, 2015 A 1 ASSETS Non-current assets (a) Property, Plant and Equipment 4 42,192.53 44,452.57

PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No.1 is compulsory. Attempt any five questions from the remaining six questions Working notes should form par t of the answer (a) Amal Ltd.

Question 1 PAPER 2 : STRATEGIC FINANCIAL MANAGEMENT Question No.1 is compulsory. Attempt any five questions from the remaining six questions Working notes should form par t of the answer (a) Amal Ltd.

FINAL EXAMINATION GROUP - IV (SYLLABUS 2016)

") FINAL EXAMINATION GROUP - IV (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper-17 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the right side indicate

FINAL EXAMINATION GROUP - IV (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS JUNE - 2017 Paper-17 : CORPORATE FINANCIAL REPORTING Time Allowed : 3 Hours Full Marks : 100 The figures in the right side indicate

cum interest. Journalise the transaction. (iv) Swaminathan owed to Subramanium the following sums :

Swaminathan owed to Subramanium the following sums :") Question 1 (i) (ii) PAPER 1 : ACCOUNTING Answer all questions Wherever appropriate, suitable assumption(s) should be made by the candidates. Working notes should form part of the answer A and B are partners

Question 1 (i) (ii) PAPER 1 : ACCOUNTING Answer all questions Wherever appropriate, suitable assumption(s) should be made by the candidates. Working notes should form part of the answer A and B are partners

Gurukripa s Guideline Answers for May 2016 Exam Questions CA Final Strategic Financial Management

Gurukripa s Guideline Answers for May 2016 Exam Questions CA Final Strategic Financial Management Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. Answer any 4 out of

Gurukripa s Guideline Answers for May 2016 Exam Questions CA Final Strategic Financial Management Question No.1 is Compulsory. Answer any 5 Questions from the remaining 6 Questions. Answer any 4 out of

6 Amalgamation. 1. Meaning of Amalgamation. Learning Objectives. After studying this chapter, you will be able to

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation After studying this chapter, you will be able to Learning Objectives Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept of transferee

6 Amalgamation of Companies

6 Amalgamation of Companies Learning Objectives After studying this chapter, you will be able to: Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept

6 Amalgamation of Companies Learning Objectives After studying this chapter, you will be able to: Understand the term Amalgamation and the methods of accounting for amalgamations. Appreciate the concept

FINAL EXAMINATION GROUP - IV (SYLLABUS 2012)