International Trade: Mainstream and Heterodox Perspectives

|

|

|

- Samson Hines

- 5 years ago

- Views:

Transcription

1 International Trade: Mainstream and Heterodox Perspectives Anwar Shaikh New School for Social Research Department of Economics Homepage:

2 Trade and Gender 1. Standard trade theory Both nations gain from trade Trade is automatically balanced for both Full employment is maintained in both Patterns of trade are determined by comparative advantage

3 Trade and Gender If the developing country has a comparative advantage in unskilled labor activities, and if women are relatively concentrated in unskilled activities, then: Trade will expand relative employment of women, and raise their wage relative to that of skilled labor (Bhagwati 2004, Elson 2007).

4 Trade and Gender Historical Roots of Standard Trade Theory The key to the preceding predictions of standard trade theory lies in the theory of comparative costs Ricardo s derivation of comparative costs International trade regulated by international competition among profit-seeking firms Initial competitive disadvantages give way to final comparative advantages Neoclassical theory adds Full Employment HOS assumes common production conditions

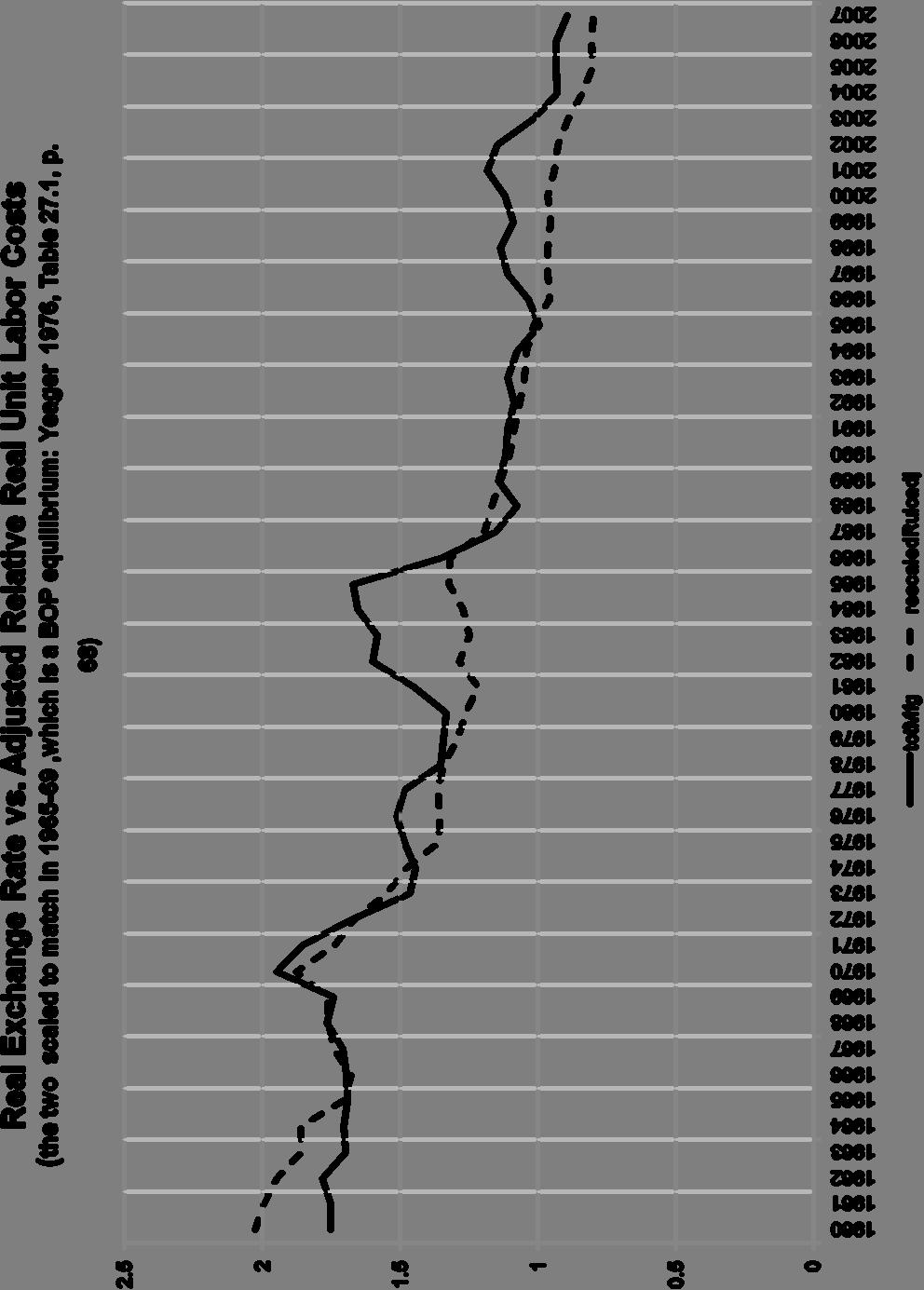

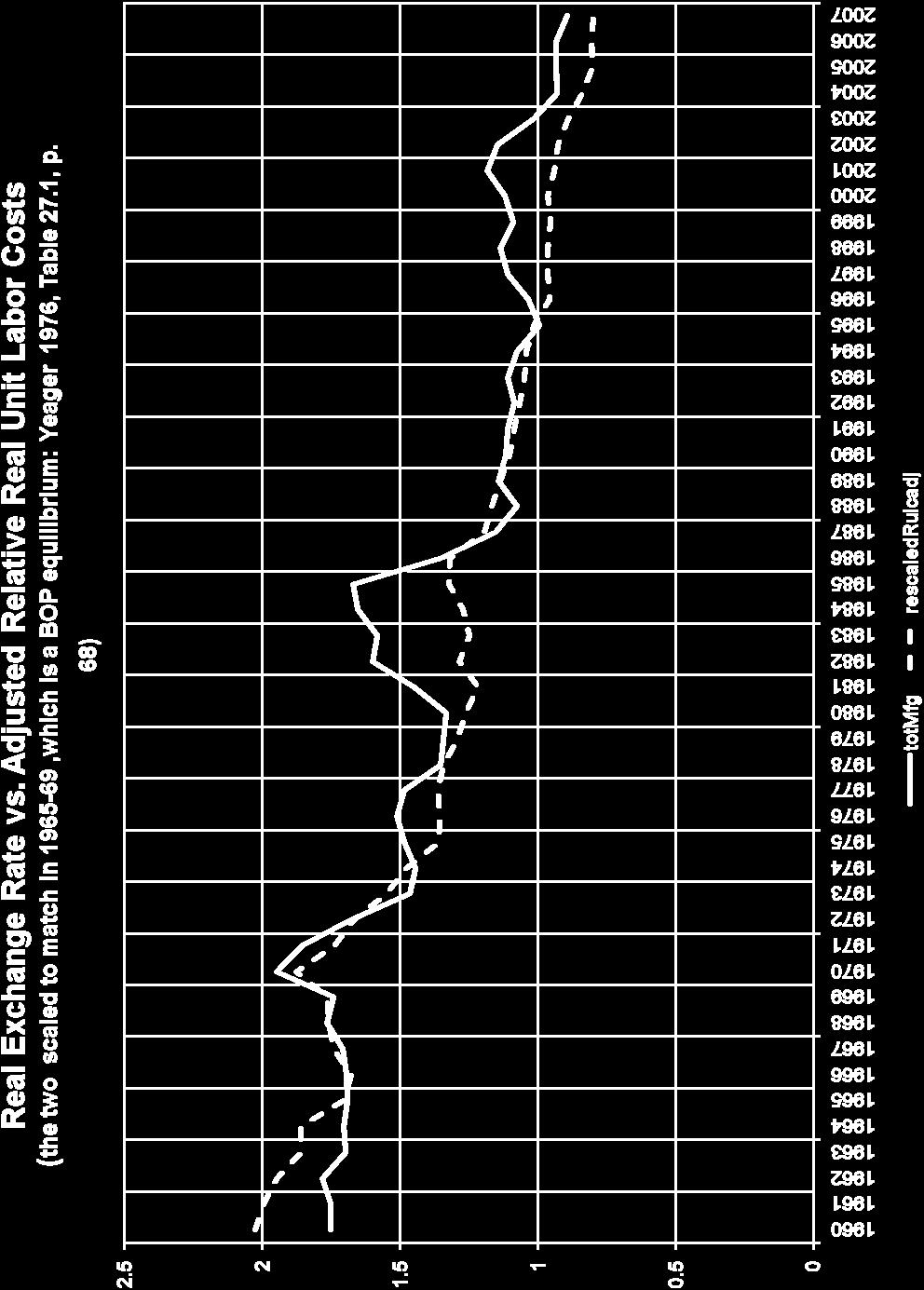

5 Balance of Trade as a Percentage of GDP 6.00 Fixed Exchange Rates Flexible Exchange Rates 4.00 Japan USA Source: OECD A. Shaikh

6 Balance of Trade as a Percentage of GDP 4.00 Fixed Exchange Rates Flexible Exchange Rates UK Canada Source: OECD A. Shaikh

7 Balance of Trade as a Percentage of GDP 6.00 Fixed Exchange Rates Flexible Exchange Rates W. Germany Unified Germany Australia Source: OECD A. Shaikh

8 English prices in Hypothetical Exchange Rates English prices in $ Regulating prices shown in bold US prices in $ English prices in $ US prices in $ p1uk p2uk e ($/ ) p1uk$ p1us p2uk$ p2us Regulating International Relative Price (p1*/p2*) Outcome $5 $20 $10 $ US dominates $6 $20 $12 $ US dominates $7 $20 $14 $ US dominates $8 $20 $16 $ US dominates $9 $20 $18 $ US dominates $10 $20 $20 $ US dominates $11 $20 $22 $ US dominates $12 $20 $24 $ US dominates $13 $20 $26 $ US dominates $14 $20 $28 $ US dominates $15 $20 $30 $ Comparative Cost Region $16 $20 $32 $ Comparative Cost Region $17 $20 $34 $ Comparative Cost Region $18 $20 $36 $ Comparative Cost Region $19 $20 $38 $ Comparative Cost Region $20 $20 $40 $ Comparative Cost Region $21 $20 $42 $ UK dominates $22 $20 $44 $ UK dominates $23 $20 $46 $ UK dominates $24 $20 $48 $ UK dominates $25 $20 $50 $ UK dominates

9 Note 1: Country A's prices in 's are converted via the exchange rate into international currency ($), while country B's are already in $'s Note 2: Hence in international currency ($), Country A's prices are pa1 = 10*e, pa2 = 20*e, while Country B's prices are pb1 = $20, pb2 = $30. Note 3: At the opening of trade at the initial exchange rate (e =.5), Country A has the lower international prices in both goods. i. According to Ricardo, the BOT surplus in Country A means that its exchange rate (e) appreciates ii. As the exchange rate (e) appreciates, the $-equivalent of Country A's prices rise. But since country B's prices are already in $, they do not change Note 4: The international regulating price in either sector (1 or 2) is the lower of the two country prices. Switchover points are at the highlighted exchange rates. Note 5: At the exchange rate e = 1.5 ( /$) [highlighted], (pa2)e = ( 20)(1.5 /$) = $30 = pb2 = 30$. This is the first crossover point Note 6: At the exchange rate e = 2 ( /$), (pa1)e = ( 10)(2 /$) $20 = = pb1 = 20$. This is second crossover point. Note 7: According to Ricardo, the exchange rate will rise if a country has a BOT surplus and fall if it has a BOT deficit: hence it can only stabilize when BOT = 0 i. But then the only feasible range of exchange rates is when each country has one regulating capital, so that each country can export one of the goods ii. The precise point within this feasible exchange rate range at which trade balances will then depend on export and import propensities in each country Note 8. When either country has both regulating capitals, its domestic price ratio determines the international price ratio: these are the regions of absolute cost advantage i. E.G. absolute cost advantage holds for Country A between for exchange rates below 1.5 /$, and holds for Country B for exchange rates above 2 /$ ii. However, the only feasible exchange rate range is when each country has one regulating capital iii. Hence in this range the international relative price is not determined by cost structures, but rather by the condition of balanced trade. iv. Such a range can only exist if the two countries have different initial price ratios, and within this range the trade balancing ratio will be between each country's initial price ratio v. Hence trade equilibrium, defined as BOT = 0, will always fall in the region of comparative costs

10

11

12 A Classical Theory of the Terms of Trade The key to the Ricardian story is the notion that the terms of trade will adjust automatically to make trade balanced As Ricardo notes, this implies that while national relative prices are determined by competitive costs, international relative prices (terms of trade) are not costdetermined Rather, international relative prices are determined by the requirements of balanced trade

13 A Classical Theory of the Terms of Trade We have seen that the empirical evidence does not support the comparative cost theory of trade One reaction has been to emphasize that it is oligopoly and monopoly power that regulates trade, not competition Hence a focus on imperfect competition But I want to argue that this is wrong: the problem lies in the how international competition is portrayed

14 A Classical Theory of the Terms of Trade The flaws in Ricardo s argument Quantity theory of money is wrong Feedback effect on costs is crucial

15

16 Table 2. Level of industrialization (manufacturing output per capita), (UK 1900=100) Total developed countries Total Third World Memo United Kingdom United States Source: (Bairoch 1977, volume 1, p. 404, as reproduced in Milanovic 2002, p. 12 )

17 Figure 1.20a: GDP Per Capita Richest 4 and Poorest 4 Countries 1990 International Geary-Khamis dollars (log Richest Poorest 4 Source: Maddison 2003 (World Hist Stat Maddison 2003.xls)

18 Figure 1.21: Ratio of the GDP Per Capita of the Richest 4 Countries to the Poorest Source: World Hist Stat Maddison 2003.xls

19 Figure 2: VMIR (Per Capita Vast Majority Income relative to GDP) by Country 2000 or closest Den Ger Nor Sw Can UK S. Kor India USA China Venez Mex Chile Netherlands Denmark Slovenia Slovak Republic Austria Finland Czech Republic Germany Sri Lanka Norway Luxembourg Sweden France Romania Bulgaria Greece Hungary Belarus Canada Taiwan Poland Italy United Kingdom Spain Belgium Lithuania Korea, Republic of Tajikistan Croatia Latvia Portugal Ghana Switzerland Kyrgyz Republic Estonia Tanzania Israel India Ethiopia Jordan Bangladesh Indonesia Moldova Viet Nam United States Mauritania Trinidad and Tobago Morocco China Russian Federation Jamaica Nepal Philippines Venezuela Thailand Cambodia Peru Turkey Uganda Madagascar Cameroon El Salvador Mexico Nicaragua Guinea Armenia Bolivia Panama Ecuador Chile Guatemala Countries VMIR

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Total Imports by Volume (Gallons per Country)

") 10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

Total Imports by Volume (Gallons per Country)

") 11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

Total Imports by Volume (Gallons per Country)

") 3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

Total Imports by Volume (Gallons per Country)

") 12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

Total Imports by Volume (Gallons per Country)

") 2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

Total Imports by Volume (Gallons per Country)

") 10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

Total Imports by Volume (Gallons per Country)

") 1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

Total Imports by Volume (Gallons per Country)

") 2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

Total Imports by Volume (Gallons per Country)

") 7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

Total Imports by Volume (Gallons per Country)

") 3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

Total Imports by Volume (Gallons per Country)

") 6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

Total Imports by Volume (Gallons per Country)

") 4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business

Household Debt and Business Cycles Worldwide Out-of-sample results based on IMF s new Global Debt Database Atif Mian Princeton University and NBER Amir Sufi University of Chicago Booth School of Business

Overview of FSC-certified forests January January Maps of extend of FSC-certified forest globally and country specific

Overview of FSCcertified forests January 2009 Maps of extend of FSCcertified forest globally and country specific Global certified forest area: 120.052.350 ha ( = 4,3%) + 11% Hectare FSCcertified forest

Overview of FSCcertified forests January 2009 Maps of extend of FSCcertified forest globally and country specific Global certified forest area: 120.052.350 ha ( = 4,3%) + 11% Hectare FSCcertified forest

Total Imports by Volume (Gallons per Country)

") 5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Index of Financial Inclusion. (A concept note)

") Index of Financial Inclusion (A concept note) Mandira Sarma Indian Council for Research on International Economic Relations Core 6A, 4th Floor, India Habitat Centre, Delhi 100003 Email: mandira@icrier.res.in

Index of Financial Inclusion (A concept note) Mandira Sarma Indian Council for Research on International Economic Relations Core 6A, 4th Floor, India Habitat Centre, Delhi 100003 Email: mandira@icrier.res.in

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Scale of Assessment of Members' Contributions for 2008

General Conference GC(51)/21 Date: 28 August 2007 General Distribution Original: English Fifty-first regular session Item 13 of the provisional agenda (GC(51)/1) Scale of Assessment of s' Contributions

General Conference GC(51)/21 Date: 28 August 2007 General Distribution Original: English Fifty-first regular session Item 13 of the provisional agenda (GC(51)/1) Scale of Assessment of s' Contributions

Dutch tax treaty overview Q3, 2012

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Summary 715 SUMMARY. Minimum Legal Fee Schedule. Loser Pays Statute. Prohibition Against Legal Advertising / Soliciting of Pro bono

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Withholding Tax Rate under DTAA

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Request to accept inclusive insurance P6L or EASY Pauschal

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

The Structure, Scope, and Independence of Banking Supervision Issues and International Evidence

The Structure, Scope, and Independence of Banking Supervision Issues and International Evidence Daniel Nolle Senior Financial Economist Office of the daniel.nolle@occ.treas.gov Presentation July 10, 2003

The Structure, Scope, and Independence of Banking Supervision Issues and International Evidence Daniel Nolle Senior Financial Economist Office of the daniel.nolle@occ.treas.gov Presentation July 10, 2003

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, July

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, July

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, January

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, January

Withholding tax rates 2016 as per Finance Act 2016

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, April

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, April

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, August

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, August

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, October

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, October

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, November

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, November

Long Association List of Jurisdictions Surveyed for Which a Response Has Been Received

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, October

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, October

Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%

![Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%](/thumbs/88/116150947.jpg "Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%") Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

SHARE IN OUR FUTURE AN ADVENTURE IN EMPLOYEE STOCK OWNERSHIP DEBBI MARCUS, UNILEVER

SHARE IN OUR FUTURE AN ADVENTURE IN EMPLOYEE STOCK OWNERSHIP DEBBI MARCUS, UNILEVER DEBBI.MARCUS@UNILEVER.COM RUTGERS SCHOOL OF MANAGEMENT AND LABOR RELATIONS NJ/NY CENTER FOR EMPLOYEE OWNERSHIP AGENDA

SHARE IN OUR FUTURE AN ADVENTURE IN EMPLOYEE STOCK OWNERSHIP DEBBI MARCUS, UNILEVER DEBBI.MARCUS@UNILEVER.COM RUTGERS SCHOOL OF MANAGEMENT AND LABOR RELATIONS NJ/NY CENTER FOR EMPLOYEE OWNERSHIP AGENDA

Other Tax Rates. Non-Resident Withholding Tax Rates for Treaty Countries 1

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

Clinical Trials Insurance

Allianz Global Corporate & Specialty Clinical Trials Insurance Global solutions for clinical trials liability Specialist cover for clinical research The challenges of international clinical research are

Allianz Global Corporate & Specialty Clinical Trials Insurance Global solutions for clinical trials liability Specialist cover for clinical research The challenges of international clinical research are

Non-resident withholding tax rates for treaty countries 1

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

n O v e m b e R Securities Industry And Financial Markets Global Addendum 2007 Volume I I No. New York n Washington n London n Hong Kong

ReseaRch RePORT n O v e m b e R 2 7 Securities Industry And Financial Markets Global Addendum 27 Volume I I No. 1 New York n Washington n London n Hong Kong SIFMA RESEARCH AND POLICY DEPARTMENT Michael

ReseaRch RePORT n O v e m b e R 2 7 Securities Industry And Financial Markets Global Addendum 27 Volume I I No. 1 New York n Washington n London n Hong Kong SIFMA RESEARCH AND POLICY DEPARTMENT Michael

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Appendix. Table S1: Construct Validity Tests for StateHist

Appendix Table S1: Construct Validity Tests for StateHist (5) (6) Roads Water Hospitals Doctors Mort5 LifeExp GDP/cap 60 4.24 6.72** 0.53* 0.67** 24.37** 6.97** (2.73) (1.59) (0.22) (0.09) (4.72) (0.85)

Appendix Table S1: Construct Validity Tests for StateHist (5) (6) Roads Water Hospitals Doctors Mort5 LifeExp GDP/cap 60 4.24 6.72** 0.53* 0.67** 24.37** 6.97** (2.73) (1.59) (0.22) (0.09) (4.72) (0.85)

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators Methodology The Starting a Foreign Investment indicators quantify several aspects of business establishment regimes important

ANNEX 2: Methodology and data of the Starting a Foreign Investment indicators Methodology The Starting a Foreign Investment indicators quantify several aspects of business establishment regimes important

Dutch tax treaty overview Q4, 2013

Dutch tax treaty overview Q4, 2013 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q4, 2013 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

(of 19 March 2013) Valid from 1 January A. Taxpayers

Valid from 1 January A. Taxpayers") Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

Does One Law Fit All? Cross-Country Evidence on Okun s Law

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES AT A GLANCE GEOGRAPHY 77 COUNTRIES COVERED 5 REGIONS Americas Asia Pacific Central & Eastern

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES AT A GLANCE GEOGRAPHY 77 COUNTRIES COVERED 5 REGIONS Americas Asia Pacific Central & Eastern

WORLD HEALTH ORGANISATION MONDIALE. NINTH WORLD HEALTH ASSEMBLY Jg? \ A9/P&B/19 ^! fr t 15 May 1956 Agenda item 6.5 îj. L,, л

WORLD HEALTH ORGANISATION MONDIALE ORGANIZATION DE LA SANTÉ NINTH WORLD HEALTH ASSEMBLY Jg? \ A9/P&B/19 ^! fr t 15 May 1956 Agenda item 6.5 îj. L,, л Q-u L. * ORIGINAL: ENÓLISH REVIEW AND APPROVAL OF THE

WORLD HEALTH ORGANISATION MONDIALE ORGANIZATION DE LA SANTÉ NINTH WORLD HEALTH ASSEMBLY Jg? \ A9/P&B/19 ^! fr t 15 May 1956 Agenda item 6.5 îj. L,, л Q-u L. * ORIGINAL: ENÓLISH REVIEW AND APPROVAL OF THE

YUM! Brands, Inc. Historical Financial Summary. Second Quarter, 2017

YUM! Brands, Inc. Historical Financial Summary Second Quarter, 2017 YUM! Brands, Inc. Consolidated Statements of Income (in millions, except per share amounts) 2017 2016 2015 YTD Q3 Q4 FY FY Revenues Company

YUM! Brands, Inc. Historical Financial Summary Second Quarter, 2017 YUM! Brands, Inc. Consolidated Statements of Income (in millions, except per share amounts) 2017 2016 2015 YTD Q3 Q4 FY FY Revenues Company

Asian Double Tax Treaties 2011

Corporate Establishment, Tax, Accounting & Payroll Throughout Asia Asian Double Tax Treaties 2011 A compilation of all Asian countries and regional double tax treaties and who they have signed them with.

Corporate Establishment, Tax, Accounting & Payroll Throughout Asia Asian Double Tax Treaties 2011 A compilation of all Asian countries and regional double tax treaties and who they have signed them with.

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS. Resolution No. 612

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 612 2010 Selective Increase in Authorized Capital Stock to Enhance Voice and Participation of Developing and Transition

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT BOARD OF GOVERNORS Resolution No. 612 2010 Selective Increase in Authorized Capital Stock to Enhance Voice and Participation of Developing and Transition

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Priorities for Productivity and Income (PPIs) Country Results

Country Results") Priorities for Productivity and Income (PPIs) Country Results Bolivia Alejandro Izquierdo Jimena Llopis Umberto Muratori Jose Juan Ruiz 2015 Priorities for Productivity and Income (PPIs) Country Results

Priorities for Productivity and Income (PPIs) Country Results Bolivia Alejandro Izquierdo Jimena Llopis Umberto Muratori Jose Juan Ruiz 2015 Priorities for Productivity and Income (PPIs) Country Results

TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA)

") TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA) In the period January - June 2018 the exports of goods from Bulgaria to the EU increased by 10.7% 2017 and amounted

TRADE IN GOODS OF BULGARIA WITH EU IN THE PERIOD JANUARY - JUNE 2018 (PRELIMINARY DATA) In the period January - June 2018 the exports of goods from Bulgaria to the EU increased by 10.7% 2017 and amounted

Pension Payments Made To Foreign Bank Accounts

West Midlands Pension Fund West Midlands Pension Fund Pension Payments Made To Foreign Bank Accounts A Guide to Worldlink Payment Services August 2012 What does WorldLink Payment Services offer? WorldLink

West Midlands Pension Fund West Midlands Pension Fund Pension Payments Made To Foreign Bank Accounts A Guide to Worldlink Payment Services August 2012 What does WorldLink Payment Services offer? WorldLink

WORLD HEALTH ORGANISATION MONDIALE O RGAN 1ZATION /О-' " DE LA SANTÉ

WORLD HEALTH ORGANISATION MONDIALE O RGAN 1ZATION /О-' " DE LA SANTÉ 1 / / TENTH WORLD HEALTH ASSEMBLY I Г 1 у ; aio/afl/8 г %-'r~,, 1 May 1957 Provisional agenda item 7*22 % / ; -у V... - " W - ' ORIGINAL:

WORLD HEALTH ORGANISATION MONDIALE O RGAN 1ZATION /О-' " DE LA SANTÉ 1 / / TENTH WORLD HEALTH ASSEMBLY I Г 1 у ; aio/afl/8 г %-'r~,, 1 May 1957 Provisional agenda item 7*22 % / ; -у V... - " W - ' ORIGINAL:

Valid from 1 January A. Taxpayers

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Annex Supporting international mobility: calculating salaries

Annex 5.2 - Supporting international mobility: calculating salaries Base salary refers to a fixed amount of money paid to an Employee in return for work performed and it is determined in accordance with

Annex 5.2 - Supporting international mobility: calculating salaries Base salary refers to a fixed amount of money paid to an Employee in return for work performed and it is determined in accordance with

APA & MAP COUNTRY GUIDE 2017 DENMARK

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

The Budget of the International Treaty. Financial Report The Core Administrative Budget

The Budget of the International Treaty Financial Report 2016 The Core Administrative Budget Including statements of amounts due and received for The Working Capital Reserve and The Third Party Beneficiary

The Budget of the International Treaty Financial Report 2016 The Core Administrative Budget Including statements of amounts due and received for The Working Capital Reserve and The Third Party Beneficiary

Section 872. Gross Income. Rev. Rul

Section 872. Gross Income (Also sections 883, 894.) 26 CFR 1.872 2: Exclusions from gross income of nonresident alien individuals. (Also 26 CFR 1.883 1.) This revenue ruling updates the list of countries

Section 872. Gross Income (Also sections 883, 894.) 26 CFR 1.872 2: Exclusions from gross income of nonresident alien individuals. (Also 26 CFR 1.883 1.) This revenue ruling updates the list of countries

CREDIT INSURANCE. To ensure peace, you must be prepared for war. CREDIT INSURANCE FUNDAMENTAL SOLUTION IN CREDIT RISK MANAGEMENT

FUNDAMENTAL SOLUTION IN CREDIT RISK MANAGEMENT I would like to extend my relations with that customer... I would like to enter a new market... We have high exposure for that customer... We have delayed

FUNDAMENTAL SOLUTION IN CREDIT RISK MANAGEMENT I would like to extend my relations with that customer... I would like to enter a new market... We have high exposure for that customer... We have delayed

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Withholding Tax Handbook BELGIUM. Version 1.2 Last Updated: June 20, New York Hong Kong London Madrid Milan Sydney

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

Index. tax evasion ethics in tax system change in Bureaucracy 3-11 Canada

Ability to pay principle 58 Administrative burden 51-79, 73-90, 430 Albania 112 Alternative Minimum Tax (AMT) 75 Anti-capitalistic mentality 318 Appeals in Armenia 317 Argentina 281-308 Armenia 113, 309-358

Ability to pay principle 58 Administrative burden 51-79, 73-90, 430 Albania 112 Alternative Minimum Tax (AMT) 75 Anti-capitalistic mentality 318 Appeals in Armenia 317 Argentina 281-308 Armenia 113, 309-358

IMPORTANT TAX INFORMATION

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

Robert Holzmann World Bank & University of Vienna

The Role of MDC Approach in Improving Pension Coverage Workshop on the Potential for Matching Defined Contribution (MDC) Schemes Washington, DC, June 6-7, 2011 Robert Holzmann World Bank & University of

The Role of MDC Approach in Improving Pension Coverage Workshop on the Potential for Matching Defined Contribution (MDC) Schemes Washington, DC, June 6-7, 2011 Robert Holzmann World Bank & University of

January 12 th,

www.financeisrael.mof.gov.il Table of Contents 1 Main Indicators 2 Real Economy 3 Foreign Trade and Balance of Payments 4 Labor Market 5 Fiscal Stance 6 Price Stability and Monetary Policy 7 Innovative

www.financeisrael.mof.gov.il Table of Contents 1 Main Indicators 2 Real Economy 3 Foreign Trade and Balance of Payments 4 Labor Market 5 Fiscal Stance 6 Price Stability and Monetary Policy 7 Innovative

World Consumer Income and Expenditure Patterns

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

International trade transparency: the issue in the World Trade Organization

Magalhães 11 International trade transparency: the issue in the World Trade Organization João Magalhães Introduction I was asked to participate in the discussion on international trade transparency with

Magalhães 11 International trade transparency: the issue in the World Trade Organization João Magalhães Introduction I was asked to participate in the discussion on international trade transparency with

Note on Revisions. Investing Across Borders 2010 Report

Note on Revisions Last revision: August 30, 2011 Investing Across Borders 2010 Report This note documents all data and revisions to the Investing Across Borders (IAB) 2010 report since its release on July

Note on Revisions Last revision: August 30, 2011 Investing Across Borders 2010 Report This note documents all data and revisions to the Investing Across Borders (IAB) 2010 report since its release on July

Institutions, Capital Flight and the Resource Curse. Ragnar Torvik Department of Economics Norwegian University of Science and Technology

Institutions, Capital Flight and the Resource Curse Ragnar Torvik Department of Economics Norwegian University of Science and Technology The resource curse Wave 1: Case studies, Gelb (1988) The resource

Institutions, Capital Flight and the Resource Curse Ragnar Torvik Department of Economics Norwegian University of Science and Technology The resource curse Wave 1: Case studies, Gelb (1988) The resource

FOREIGN ACTIVITY REPORT

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

Export promotion: evaluating the impact on aggregate exports and GDP

Export promotion: evaluating the impact on aggregate exports and GDP University of Geneva and International Trade Center ETPO meeting, Milan - October 14-16 2015 What do we know? Rose (2007): embassy presence

Export promotion: evaluating the impact on aggregate exports and GDP University of Geneva and International Trade Center ETPO meeting, Milan - October 14-16 2015 What do we know? Rose (2007): embassy presence

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

A Resolution on Enforcement Powers

A Resolution on Enforcement Powers Passed by the Presidents' Committee November 1997 CONSIDERING that the complex character of securities and futures transactions and the sophistication of fraudulent schemes

A Resolution on Enforcement Powers Passed by the Presidents' Committee November 1997 CONSIDERING that the complex character of securities and futures transactions and the sophistication of fraudulent schemes

JPMorgan Funds statistics report: Emerging Markets Debt Fund

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Emerging Markets Debt Fund Data as of November 30, 2016 Must be preceded or accompanied by a prospectus. jpmorganfunds.com

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE JPMorgan Funds statistics report: Emerging Markets Debt Fund Data as of November 30, 2016 Must be preceded or accompanied by a prospectus. jpmorganfunds.com

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland