Valuation Control and PCA status: INDIA

|

|

|

- Noah James

- 5 years ago

- Views:

Transcription

1 Valuation Control and PCA status: INDIA

2 OUTLINE Organizational Structure Flow of Import Procedure Current status of Valuation Valuation control experience Valuation control : Problem & Challenges Current status of PCA PCA : Problem and Challenges

3 Central Board of Excise & Customs CBEC Offices - Administration - Tax Research Unit (TRU) - Customs - Central Excise - Service Tax - Co-ordination 2/12/2014 3

4 Central Board of Excise & Customs Field Offices Directorates and Chief Commissionerate Zones consisting of Commissionerates Directorate headed by Director General or Director Zone headed by Chief Commissioner Commissionerate headed by Commissioner 2/12/2014 4

5 CBEC Field Offices Contd. 12 Directorates General 4 Directorates & Central Revenues Control Lab. 23 Excise Zones 11 Customs Zones 93 Central Excise Commissionerates 36 Customs Commissionerates 7 Service Tax Commissionerates 2/12/2014 5

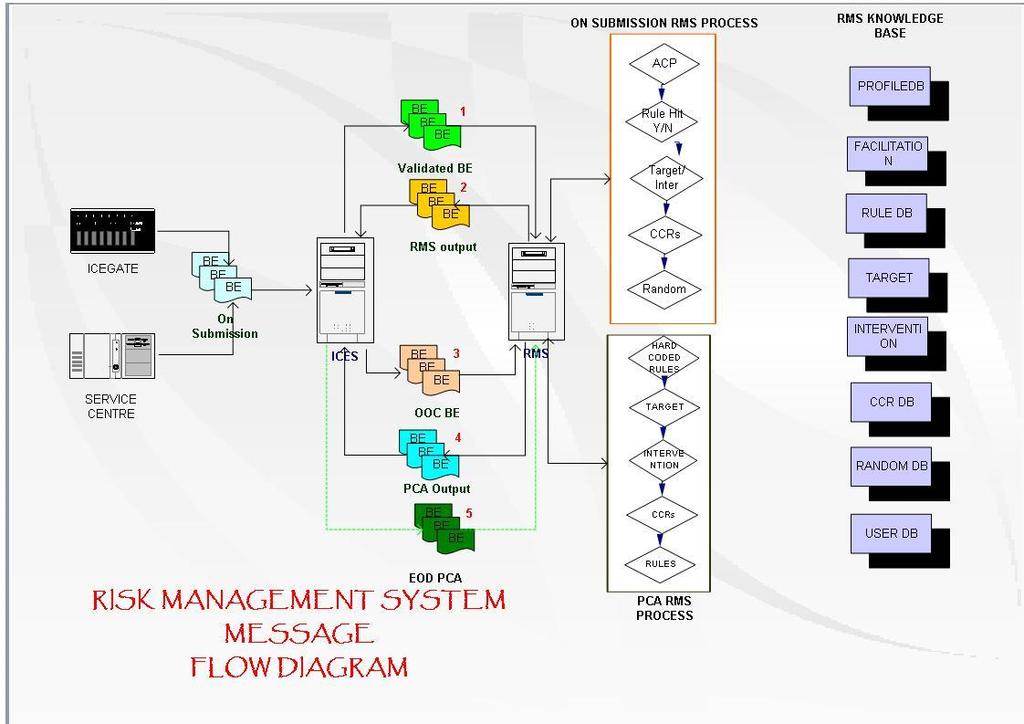

6 Vessel Arrival Customs Processes Air/ Shipping Ports Shipping Line License Management Customs DGFT Importer/ CHA Tax Payment Banks Importer/ CHA Cargo Manifest filing Line Air/ Sea Cargo & consol Agents Goods Assessment Importer/ CHA Other Govt. Agencies Cargo Examination Custodians Carrier Importer/ CHA Cargo Release Cargo Transshipment Source/ Dest Ports Carrier Agents Goods Declaration Importer Customs Broker (CHA) Port/ WH Charges Importer/ CHA Port Authorities Port Custodians Carriers/ CHA

7 Automated Customs Clearances with RMS E-Filing through ICEGATE No Assessment Risk Management System No Examination 7

8

9 Current status of Valuation India is a founding Member of the GATT (presently WTO) Was actively involved in the GATT negotiations (Tokyo Round, ), which developed the Agreement on Customs Valuation (ACV). India implemented the ACV in August 1988

10 SECTION 14. Valuation of goods. (1) For the purposes of the Customs Tariff Act, 1975, or any other law for the time being in force, the value of the imported goods. shall be the transaction value of such goods, that is to say, the price actually paid or payable for the goods when sold for export to India for delivery at the time and place of importation,.where the buyer and seller of the goods are not related and price is the sole consideration for the sale subject to such other conditions as may be specified in the rules made in this behalf :

11 Current status of Valuation Legal Provisions: The provisions of sub-section (1) of Section 14 apply for the valuation of both imported goods and export goods. However, a common valuation law at international level applies only to imported goods and its basic principles are laid down in Article VII of General Agreement on Tariffs and Trade (GATT), 1948, currently known as GATT 1994 (administered by the World Trade organization, WTO). The Indian valuation law under Section 14(1) of the Indian Customs Act is based on the principles of Article VII of the GATT.

12 Valuation Control Experience Customs Valuation (Determination of Value of Imported Goods) Rules, 2007 Transaction Value (Rule 3):primary basis for valuation However, it is subject to adjustment by certain Valuation Factors like Commissions and brokerage, except buying commissions; the cost of packing whether for labor or materials; Rejection of Transaction Value (Rule 12) if the truth or accuracy of the declaration is reasonably suspected or related party etc When the transaction value method is not applied, goods shall be valued by applying the subsequent methods in a strictly hierarchical order

13 Customs Valuation (Determination of Value of Imported Goods) Rules, 2007 at glance. Rule 1 Rule 2 Rule 3 Rule 4 Rule 5 Rule 6 Rule 7 Rule 8 Rule 9 Rule 10 Rule 11 Rule 12 Rule 13 Short title, commencement and application Definitions Determination of the method of valuation.- Transaction value of identical goods Transaction value of similar goods. Determination of value where value cannot be determined under rules 3, 4 and 5 Deductive value. Computed value. Residual method. Cost and services Declaration by the importer. Rejection of declared value. Interpretative notes. (schedule)

14 Valuation Control Experience Transaction value of identical goods(rule 4) Transaction value of similar goods(rule 5) If value can be determined on basis of declared value ie transaction value or of identical/similar goods (Rule 6) then Deductive value(rule 7) Computed value(rule 8) Residual method(rule 9) the value so determined shall not exceed the price at which such or like goods are ordinarily sold minimum customs values; or shouldn t be arbitrary or fictitious values

15 Valuation control : Problem and Challenges Under-invoicing Related Parties- Transfer Pricing Second Hand Goods Abnormal discount or abnormal reduction Special discounts limited to exclusive agents Misdeclaration of goods in parameters such as description, quality, quantity, country of origin, year of manufacture or production; Non declaration of parameters such as brand, grade, specifications that have relevance to value; The fraudulent or manipulated documents

16 Valuation control : Problem and Challenges However the biggest challenge for customs officers : to facilitate trade so that delays can be avoided and to see that interests of revenue and other legal prohibitions are not violated. To ensure this-thorough examination of the Bills of entry and physical examination Take time, and delay the clearance of imported /reduce dwell time to reconcile 2 conflicting interests i.e. faster clearance vis-à-vis customs checks-solution-post clearance audit.

17 Current Status of PCA Mentioned in Art VIII, GATT, Paragraph 1(c). Origin of the Self Assessment System & PCA : Kyoto Convention. Chapter 2: Kyoto C defines Customs Control as measure to ensure compliance with the Customs law. Chapter 6 of the Convention provides that Customs Control shall be limited to that necessary to ensure compliance with Customs law. Further, in application of Customs control : Use risk management- risk analysis to determine which persons/goods, including means of transportation, should be examined and the extent of examination. The Customs Authorities shall adopt a compliance measurement strategy like Audit Based Control to support risk management.

18 Current Status of PCA Post Clearance Compliance Verification(PCCV) - Introduced in 2005 the Risk Management System Operational Done at Custom Houses, mainly on basis of documents submitted /transaction value Short levies identified and Compliance requirements and Conformance to various declarations Biggest drawback : Documents/Systems & Procedures cant be verified

19 Current Status of PCA On-Site Post Clearance Audit (OSPCA) : Initiative based on Global best practices/increased compliance environment and trade facilitation OSPCA introduced w.e.f importers U/ Accredited Client Programme (ACP)- annual basis (FY) ACP 3 categories for coordination : being done By Central Excise Commissionerate In order to avoid duplication of exercise - OSPCA with Central Excise and Service Tax Audit

20 Current Status of PCA Going ahead PCA- by Custom Houses, shall continue side by side with OSPCA, the latter being done at the premises of the importers / exporters. To prevent duplication both PCA and OSPCA shall not be done for the same transaction. PCA dispensed with for ACP clients

21 Current Status of PCA By its very nature OSPCA is a broad based audit with focus on systems and procedures even though the short levies of duties, if any, shall continue to be determined on transaction basis. OSPCA allows verification of self-assessment on periodic basis by scrutiny of relevant business records at the importers / exporters premise reduced clearance time/ conformance to the declarations

22 Current Status of PCA Legal Authority Section 17(6) of the Customs Act, 1962, whichverification of correctness of assessment of duty on imported or export goods at the premise of importer or exporter. On Site Post Clearance Regulations 2011 has been notified(u/sec 157 of the CA,1962) which prescribes the manner of conducting audit at the premises of importer or exporter.

23 STATUS OF OSPCA IN INDIA PERIOD COVERAGE OUTCOME OCTOBER 2011 UPTO MARCH 2012 APRIL 2012 TO MARCH clients ( out of 260 ) 215 clients ( out of 308 ) 41 Objections ( Rs 10 crores ) 152 objections ( Rs 120 crores )

24 PCA : Problems and Challenges Training of Auditors / Availability In depth knowledge of accounting/business (mal)- practices Long drawn procedure with guidelines to adhere to - requires cooperation of assesse Standard practices are not adhered to by small businesses Large business - services of expert

25 PCA : Problems and Challenges Technological advancements Tariff evolution-in comparison to changing technology-rather slow Non compliance with audit objections (Penalty clause incorporated)

26 THANK YOU

Customs Valuation (Determination of Value of Imported Goods) Rules, 2007

Rules, 2007") Customs Valuation (Determination of Value of Imported Goods) Rules, 2007 Notification No. 94/2007 - Customs (N.T.) 1. Short title, commencement and application. (1)These rules may be called the Customs

Customs Valuation (Determination of Value of Imported Goods) Rules, 2007 Notification No. 94/2007 - Customs (N.T.) 1. Short title, commencement and application. (1)These rules may be called the Customs

[F.No.459/15/2007-Cus.V]

![[F.No.459/15/2007-Cus.V]](/thumbs/72/66374854.jpg "[F.No.459/15/2007-Cus.V]") [TO BE PUBLISHED IN PART-II, SECTION-3, SUB-SECTION (i) OF THE GAZETTE OF INDIA, EXTRAORDINARY] Government of India Ministry of Finance Department of Revenue No. 93/2007-CUSTOMS New Delhi, 13 th September,

[TO BE PUBLISHED IN PART-II, SECTION-3, SUB-SECTION (i) OF THE GAZETTE OF INDIA, EXTRAORDINARY] Government of India Ministry of Finance Department of Revenue No. 93/2007-CUSTOMS New Delhi, 13 th September,

Customs Valuation. Valuation of Imported/Export Goods where no Tariff Values fixed:

Customs Valuation The rates of customs duties leviable on imported goods (& export items in certain cases) are either specific or on ad valorem basis or at times specific cum ad valorem. When customs duties

Customs Valuation The rates of customs duties leviable on imported goods (& export items in certain cases) are either specific or on ad valorem basis or at times specific cum ad valorem. When customs duties

Customs Valuation Rules

Udayan Choksi, Advocate Customs Valuation Rules This Article discusses the rules in relation to customs valuation for imported goods and export goods, which were notified in 2007. The 2007 rules in relation

Udayan Choksi, Advocate Customs Valuation Rules This Article discusses the rules in relation to customs valuation for imported goods and export goods, which were notified in 2007. The 2007 rules in relation

Trade Facilitation. Chronology of events

1 Trade Facilitation Nisha Taneja Indian Council for Research on International Economic Relations Chronology of events 2 Singapore Ministerial Conference of WTO members (1996) : Four Singapore issues trade

1 Trade Facilitation Nisha Taneja Indian Council for Research on International Economic Relations Chronology of events 2 Singapore Ministerial Conference of WTO members (1996) : Four Singapore issues trade

Chapter 6. Customs Valuation

Chapter 6 Customs Valuation 1. Introduction: 1.1 The rates of Customs duties leviable on imported goods and export goods are either specific or on ad valorem basis or at times on specific cum ad valorem

Chapter 6 Customs Valuation 1. Introduction: 1.1 The rates of Customs duties leviable on imported goods and export goods are either specific or on ad valorem basis or at times on specific cum ad valorem

VALUATION. These Rules are framed by central Govt Under the provisions of Sec. 14 of Customs Act, 1962.

VALUATION Explain the provisions of determination of value under the Customs Valuation Rules in case the value declared by the importer does not represent the transaction or Valuation of the goods imported.

VALUATION Explain the provisions of determination of value under the Customs Valuation Rules in case the value declared by the importer does not represent the transaction or Valuation of the goods imported.

Customs Valuation (Determination of Price of Imported Goods) Rules, 1988

Rules, 1988") Customs Valuation (Determination of Price of Imported Goods) Rules, 988 Ntfn 5-Cus.(N.T.), dated 8.07.88 As amended by Ntfn No. 53/88-Cus(NT), dated 0.08.988; 7/89-Cus(NT), dated 9..989; 39/90-Cus(NT),

Customs Valuation (Determination of Price of Imported Goods) Rules, 988 Ntfn 5-Cus.(N.T.), dated 8.07.88 As amended by Ntfn No. 53/88-Cus(NT), dated 0.08.988; 7/89-Cus(NT), dated 9..989; 39/90-Cus(NT),

Service Tax on ocean freight the recent changes. (G. Natarajan, Advocate, Swamy Associates)

") Service Tax on ocean freight the recent changes (G. Natarajan, Advocate, Swamy Associates) The following services were kept in the negative list, when negative list based service tax levy was introduced

Service Tax on ocean freight the recent changes (G. Natarajan, Advocate, Swamy Associates) The following services were kept in the negative list, when negative list based service tax levy was introduced

A Handbook on the WTO Customs Valuation Agreement

A Handbook on the WTO Customs Valuation Agreement Sheri Rosenow and Brian J. O'Shea CAMBRIDGE UNIVERSITY PRESS CONTENTS List of Figures Foreword Preface Acknowledgements Acronyms and abbreviations page

A Handbook on the WTO Customs Valuation Agreement Sheri Rosenow and Brian J. O'Shea CAMBRIDGE UNIVERSITY PRESS CONTENTS List of Figures Foreword Preface Acknowledgements Acronyms and abbreviations page

Significant Initiativestaken by CBEC

ANNEXURE Significant Initiativestaken by CBEC I Customs Single Window - As part of Ease of Doing Business initiatives, CBEC has launched Single Window Interface for Facilitating Trade (SWIFT). SWIFT provides

ANNEXURE Significant Initiativestaken by CBEC I Customs Single Window - As part of Ease of Doing Business initiatives, CBEC has launched Single Window Interface for Facilitating Trade (SWIFT). SWIFT provides

PROPOSED AMENDMENTS TO THE CUSTOMS LAW May 2002 VALUE OF GOODS FOR CUSTOMS PURPOSES. Article 28 Application of customs value

PROPOSED AMENDMENTS TO THE CUSTOMS LAW May 2002 VALUE OF GOODS FOR CUSTOMS PURPOSES Article 28 Application of customs value The provisions of Article 28 to 39 of the Code shall determine the customs value

PROPOSED AMENDMENTS TO THE CUSTOMS LAW May 2002 VALUE OF GOODS FOR CUSTOMS PURPOSES Article 28 Application of customs value The provisions of Article 28 to 39 of the Code shall determine the customs value

CHAPTER 4 CUSTOMS PROCEDURES. Article 1: Definitions

CHAPTER 4 CUSTOMS PROCEDURES For the purposes of this Chapter: Article 1: Definitions customs law means such laws and regulations administered and enforced by the Customs Administration of a Party concerning

CHAPTER 4 CUSTOMS PROCEDURES For the purposes of this Chapter: Article 1: Definitions customs law means such laws and regulations administered and enforced by the Customs Administration of a Party concerning

Valuation under Customs

CA Final Paper 8 (Chapter5) Indirect Tax Laws Valuation under Customs Gajendra Maheshwari BCom(H), ACA, ICWA, LLM Legal Framework Customs Valuation: Background Specific provisions under Customs law for

CA Final Paper 8 (Chapter5) Indirect Tax Laws Valuation under Customs Gajendra Maheshwari BCom(H), ACA, ICWA, LLM Legal Framework Customs Valuation: Background Specific provisions under Customs law for

FORM NO. C.A.- 3 [See rule 6(1)] Form of Appeal to the Appellate Tribunal under sub-section (1) of section 129A of Customs Act, In the Customs,

![FORM NO. C.A.- 3 [See rule 6(1)] Form of Appeal to the Appellate Tribunal under sub-section (1) of section 129A of Customs Act, In the Customs,](/thumbs/93/112775252.jpg "FORM NO. C.A.- 3 [See rule 6(1)] Form of Appeal to the Appellate Tribunal under sub-section (1) of section 129A of Customs Act, In the Customs,") TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i) GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) NOTIFICATION New Delhi, the 10 th April, 2013

TO BE PUBLISHED IN THE GAZETTE OF INDIA EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i) GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) NOTIFICATION New Delhi, the 10 th April, 2013

CUSTOMS VALUATIONS FIJI EXPERIENCE

CUSTOMS VALUATIONS FIJI EXPERIENCE Biman Prasad Associate Professor and Head of School of Economics The University of the South Pacific & Parmod Achary General Manager, Development Services Fiji Islands

CUSTOMS VALUATIONS FIJI EXPERIENCE Biman Prasad Associate Professor and Head of School of Economics The University of the South Pacific & Parmod Achary General Manager, Development Services Fiji Islands

Subject: Project Imports Regulations, 1986 (PIR) Instructions regarding. *** Sir / Madam,

Instructions regarding. *** Sir / Madam,") Circular No.22/2011-Customs To F.No.528/38/2008-Cus.(TU) Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs 227-B, North Block. New Delhi-110001. 4 th May,

Circular No.22/2011-Customs To F.No.528/38/2008-Cus.(TU) Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs 227-B, North Block. New Delhi-110001. 4 th May,

MTP_Intermediate_Syllabus 2016_Dec2017_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

ANNEXURE A OFFICE OF THE COMMISSIONER OF CUSTOMS AND CENTRAL EXCISE NAGPUR II COMMISSIONERATE TELANGKHEDI ROAD, CIVIL LINES, NAGPUR

ANNEXURE A OFFICE OF THE COMMISSIONER OF CUSTOMS AND CENTRAL EXCISE NAGPUR II COMMISSIONERATE TELANGKHEDI ROAD, CIVIL LINES, NAGPUR-440001 LETTER of FACTORY STUFFING PERMISSION (LoFSP) This Letter of Factory

ANNEXURE A OFFICE OF THE COMMISSIONER OF CUSTOMS AND CENTRAL EXCISE NAGPUR II COMMISSIONERATE TELANGKHEDI ROAD, CIVIL LINES, NAGPUR-440001 LETTER of FACTORY STUFFING PERMISSION (LoFSP) This Letter of Factory

Valuation under the Customs Act, 1962

5 Valuation under the Customs Act, 1962 Question 1 Briefly explain the following with reference to the Customs (Determination of Value of Imported Goods) Rules, 2007: (i) Goods of the same class or kind

5 Valuation under the Customs Act, 1962 Question 1 Briefly explain the following with reference to the Customs (Determination of Value of Imported Goods) Rules, 2007: (i) Goods of the same class or kind

Excise duty on Gold jewellery.

Excise duty on Gold jewellery Dated 13 th July 2016 http://www.cbec.gov.in/resources//htdocs-cbec/deptt_offcr/do-ltr-jewellrytru1.pdf Relaxation given SSI exemption, the eligibility and exemption limit

Excise duty on Gold jewellery Dated 13 th July 2016 http://www.cbec.gov.in/resources//htdocs-cbec/deptt_offcr/do-ltr-jewellrytru1.pdf Relaxation given SSI exemption, the eligibility and exemption limit

INDIRECT TAX LAWS & PRACTICE. Paper-18. Syllabus Set-1. Answer of Postal test Paper. Set-1.

Paper-18 Syllabus-2016 Set-1 Answer of Postal test Paper Set-1 www.globalcma.in info@globalcma.in SECTION-A Q.1 B. i. 50% ii. CBEC iii. Receiver iv. Third Party Export v. 4% i. Form H ii. Gross Product

Paper-18 Syllabus-2016 Set-1 Answer of Postal test Paper Set-1 www.globalcma.in info@globalcma.in SECTION-A Q.1 B. i. 50% ii. CBEC iii. Receiver iv. Third Party Export v. 4% i. Form H ii. Gross Product

COURSE ON WTO LAW AND JURISPRUDENCE PART I: BASIC WTO LEGAL PRINCIPLES

COURSE ON WTO LAW AND JURISPRUDENCE PART I: BASIC WTO LEGAL PRINCIPLES Customs Valuation, Fees and Formalities Session 3 18 October 2018 AGENDA In this session, we will discuss: 1. Customs Valuation 2.

COURSE ON WTO LAW AND JURISPRUDENCE PART I: BASIC WTO LEGAL PRINCIPLES Customs Valuation, Fees and Formalities Session 3 18 October 2018 AGENDA In this session, we will discuss: 1. Customs Valuation 2.

FINAL November INDIRECT TAXATION Test Code 67 Branch (MULTIPLE) (Date : ) All questions are compulsory.

(Date : ) All questions are compulsory.") FINAL November 2017 INDIRECT TAXATION Test Code 67 Branch (MULTIPLE) (Date : 10.09.2017) (50 Marks) Note: All questions are compulsory. Answer 1(6 Marks) Status Holders are business leaders who have excelled

FINAL November 2017 INDIRECT TAXATION Test Code 67 Branch (MULTIPLE) (Date : 10.09.2017) (50 Marks) Note: All questions are compulsory. Answer 1(6 Marks) Status Holders are business leaders who have excelled

Chapter -2 Central Excise Law

1 Solution of Paper 10 Applied Indirect Taxes (CMA) December, 2012 Chapter -2 Central Excise Law Descriptive Question Answer (a): Particular CST Service tax Excise duty Customs duty 2012-Dec[2] (a) Taxable

1 Solution of Paper 10 Applied Indirect Taxes (CMA) December, 2012 Chapter -2 Central Excise Law Descriptive Question Answer (a): Particular CST Service tax Excise duty Customs duty 2012-Dec[2] (a) Taxable

CASE STUDY: INDIA VALUATION CONTROL PROGRAMME

CASE STUDY: INDIA VALUATION CONTROL PROGRAMME WORLD CUSTOMS ORGANIZATION JUNE 2012 TABLE OF CONTENTS 1. INTRODUCTION... 3 Background... 3 Brief overview of the programme... 3 Legal framework... 4 Organizational

CASE STUDY: INDIA VALUATION CONTROL PROGRAMME WORLD CUSTOMS ORGANIZATION JUNE 2012 TABLE OF CONTENTS 1. INTRODUCTION... 3 Background... 3 Brief overview of the programme... 3 Legal framework... 4 Organizational

CHAPTER 3 EXPORTS FROM INDIA SCHEMES

CHAPTER 3 EXPORTS FROM INDIA SCHEMES 3.00 Objective The objective of schemes under this chapter is to provide rewards to exporters to offset infrastructural inefficiencies and associated costs. 3.01 Exports

CHAPTER 3 EXPORTS FROM INDIA SCHEMES 3.00 Objective The objective of schemes under this chapter is to provide rewards to exporters to offset infrastructural inefficiencies and associated costs. 3.01 Exports

4 Valuation of Taxable Service

4 Valuation of Taxable Service 4.1 Valuation of taxable services for charging service tax [Section 67] Section 67 provides for the valuation of taxable services. The provisions of this section are discussed

4 Valuation of Taxable Service 4.1 Valuation of taxable services for charging service tax [Section 67] Section 67 provides for the valuation of taxable services. The provisions of this section are discussed

INDEPENDENT AUDITOR S REPORT

88 Standalone INDEPENDENT AUDITOR S REPORT to the Members of Hindustan Unilever Limited REPORT ON THE STANDALONE FINANCIAL STATEMENTS We have audited the accompanying standalone financial statements of

88 Standalone INDEPENDENT AUDITOR S REPORT to the Members of Hindustan Unilever Limited REPORT ON THE STANDALONE FINANCIAL STATEMENTS We have audited the accompanying standalone financial statements of

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 7

: 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of the Question Paper relate

: 1 : Roll No... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of the Question Paper relate

DUTY EXEMPTION SCHEMES

DUTY EXEMPTION SCHEMES - Contributed by CA Kewal Satra OBJECTIVE The basic objective of the schemes under this Chapter is to enable duty free import of inputs for export production, replenishment of inputs

DUTY EXEMPTION SCHEMES - Contributed by CA Kewal Satra OBJECTIVE The basic objective of the schemes under this Chapter is to enable duty free import of inputs for export production, replenishment of inputs

GENERAL PROCEDURES UNDER CENTRAL EXCISE

5 GENERAL PROCEDURES UNDER CENTRAL EXCISE SIGNIFICANT NOTIFICATIONS/CIRCULARS ISSUED BETWEEN 01.05.2014 AND 30.04.2015 1. Following amendments have been made in Central Excise Rules, 2002 [CER] vide Notification

5 GENERAL PROCEDURES UNDER CENTRAL EXCISE SIGNIFICANT NOTIFICATIONS/CIRCULARS ISSUED BETWEEN 01.05.2014 AND 30.04.2015 1. Following amendments have been made in Central Excise Rules, 2002 [CER] vide Notification

Customs Clearance & Tariffs

04 Customs Clearance & Tariffs 118 1. Customs Clearance Customs clearance refers to the import, export or return of goods pursuant to the procedures prescribed by the Customs Act. Customs clearance procedures

04 Customs Clearance & Tariffs 118 1. Customs Clearance Customs clearance refers to the import, export or return of goods pursuant to the procedures prescribed by the Customs Act. Customs clearance procedures

Seeking to expedite the movement, release, and clearance of goods in order to facilitate trade between the Parties; and

PROTOCOL TO THE 1989 TRADE AND INVESTMENT FRAMEWORK AGREEMENT BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE REPUBLIC OF THE PHILIPPINES CONCERNING CUSTOMS ADMINISTRATION

PROTOCOL TO THE 1989 TRADE AND INVESTMENT FRAMEWORK AGREEMENT BETWEEN THE GOVERNMENT OF THE UNITED STATES OF AMERICA AND THE GOVERNMENT OF THE REPUBLIC OF THE PHILIPPINES CONCERNING CUSTOMS ADMINISTRATION

1. Exemption to taxable services provided against scripissued under SEIS/ MEIS under FTP

Summary of Notifications, Circulars from 16 th March2015 to 15 th April 2015 SERVICE TAX 1. Exemption to taxable services provided against scripissued under SEIS/ MEIS under FTP 2015-2020 CBEC vide Notification

Summary of Notifications, Circulars from 16 th March2015 to 15 th April 2015 SERVICE TAX 1. Exemption to taxable services provided against scripissued under SEIS/ MEIS under FTP 2015-2020 CBEC vide Notification

EXAMINATION UNDER REGULATION 19 {3} OF CHALR, 2004 FOR ISSUE OF G CARD. Date of Examination : 28/12/2011 Total Marks : 100 Duration : 3 hours.

EXAMINATION UNDER REGULATION 19 {3} OF CHALR, 2004 FOR ISSUE OF G CARD Date of Examination : 28/12/2011 Total Marks : 100 Duration : 3 hours. ANSWER ANY TWENTY QUESTIONS. PART A 1) What is the charging

EXAMINATION UNDER REGULATION 19 {3} OF CHALR, 2004 FOR ISSUE OF G CARD Date of Examination : 28/12/2011 Total Marks : 100 Duration : 3 hours. ANSWER ANY TWENTY QUESTIONS. PART A 1) What is the charging

Respondent preferred an appeal there against before the Commissioner (Appeals), which by an order dated was allowed. Appellant preferred an

, which by an order dated was allowed. Appellant preferred an") IN THE SUPREME COURT OF INDIA Civil Appeal No. 5901 of 2006 Decided On: 03.03.2009 Commissioner of Central Excise, Noida Vs. Accurate Meters Ltd. Hon'ble Judges: S.B. Sinha, Asok Kumar Ganguly and R.M.

IN THE SUPREME COURT OF INDIA Civil Appeal No. 5901 of 2006 Decided On: 03.03.2009 Commissioner of Central Excise, Noida Vs. Accurate Meters Ltd. Hon'ble Judges: S.B. Sinha, Asok Kumar Ganguly and R.M.

BUDGET ANALYSIS

CUSTOMS ACT 1962 CUSTOMS ACT 1962 : 88 Section 2 is being amended to: (a) insert clause (3A) to define a beneficial owner as any person on whose behalf the goods are being imported or exported or who exercises

CUSTOMS ACT 1962 CUSTOMS ACT 1962 : 88 Section 2 is being amended to: (a) insert clause (3A) to define a beneficial owner as any person on whose behalf the goods are being imported or exported or who exercises

EU-Mexico Free Trade Agreement EU TEXTUAL PROPOSAL. Chapter on Trade in Goods. Article X.1. Scope. Article X.2

EU proposal April 2017 This document contains an EU proposal for a legal text on Goods in the Trade Part of a possible modernised EU-Mexico Association Agreement. It has been tabled for discussion with

EU proposal April 2017 This document contains an EU proposal for a legal text on Goods in the Trade Part of a possible modernised EU-Mexico Association Agreement. It has been tabled for discussion with

Veer Narmad South Gujarat University, Surat T.Y.B.Com. Semester 5

Semester 5 ( Customs & Central Excise Procedure & Practice : Part II) Paper No. V Course Code : CE 525 F(1) (1) Nature of customs Duty-objectives- Excise Duty and customs. (2) Laws relating to customs

Semester 5 ( Customs & Central Excise Procedure & Practice : Part II) Paper No. V Course Code : CE 525 F(1) (1) Nature of customs Duty-objectives- Excise Duty and customs. (2) Laws relating to customs

Article 26 Co-operation in the Field of Automotive Industry

Article 26 Co-operation in the Field of Automotive Industry The Countries shall co-operate, with the participation of their respective automotive industries, to further enhance competitiveness of the automotive

Article 26 Co-operation in the Field of Automotive Industry The Countries shall co-operate, with the participation of their respective automotive industries, to further enhance competitiveness of the automotive

(vii) CTD shall not be issued in favour of a dealer to whom invoice was issued for the same goods before the appointed date.

CTD shall not be issued in favour of a dealer to whom invoice was issued for the same goods before the appointed date.") Draft Rule for issue of Credit Transfer Document to be inserted in the CENVAT Credit Rules, 2004 for transfer of cenvat credit paid on specified goods available with a trader as on appointed date. A.(1)

Draft Rule for issue of Credit Transfer Document to be inserted in the CENVAT Credit Rules, 2004 for transfer of cenvat credit paid on specified goods available with a trader as on appointed date. A.(1)

CUSTOMS AND BORDER MANAGEMENT EXTERNAL STANDARD OPERATING PROCEDURE CUSTOMS VALUATION EXPORT VALUE

CUSTOMS AND BORDER MANAGEMENT EXTERNAL STANDARD OPERATING PROCEDURE CUSTOMS VALUATION EXPORT VALUE Revision: 0 Page 1 of 6 TABLE OF CONTENTS 1 SCOPE 3 2 PROCEDURE 4 2.1 Determine Export Value 4 2.1.1 Determine

CUSTOMS AND BORDER MANAGEMENT EXTERNAL STANDARD OPERATING PROCEDURE CUSTOMS VALUATION EXPORT VALUE Revision: 0 Page 1 of 6 TABLE OF CONTENTS 1 SCOPE 3 2 PROCEDURE 4 2.1 Determine Export Value 4 2.1.1 Determine

CHAPTER - 5 STATUTORY REQUIREMENTS OF FINANCIAL STATEMENTS & AUDIT OF DIVIDENDS

CHAPTER - 5 STATUTORY REQUIREMENTS OF FINANCIAL STATEMENTS & AUDIT OF DIVIDENDS MAINTENANCE OF BOOKS OF ACCOUNT Sec. 209(1) of Companies Act, 1956 requires every company to keep at its registered office

CHAPTER - 5 STATUTORY REQUIREMENTS OF FINANCIAL STATEMENTS & AUDIT OF DIVIDENDS MAINTENANCE OF BOOKS OF ACCOUNT Sec. 209(1) of Companies Act, 1956 requires every company to keep at its registered office

The Customs, Central Excise Duties and Service Tax Drawback (Amendment) Rules, 2006.

Rules, 2006.") The Customs, Central Excise Duties and Service Tax Drawback (Amendment) Rules, 2006. Notification No. 37/1995 - Customs (N.T.) dated 26/05/1995; amended by Notification No. 63/95-Customs (N.T.) dated 20-10-95;

The Customs, Central Excise Duties and Service Tax Drawback (Amendment) Rules, 2006. Notification No. 37/1995 - Customs (N.T.) dated 26/05/1995; amended by Notification No. 63/95-Customs (N.T.) dated 20-10-95;

TEXPROCIL. (A) Exports under Bond/ LUT or under Refund of IGST

Exports under Bond/ LUT or under Refund of IGST") Guidance Note on GST (A) Exports under Bond/ LUT or under Refund of IGST (I) Exports Zero rated supplies All exports as well as supplies to SEZs have been categorized as Zero rated supplies in the IGST

Guidance Note on GST (A) Exports under Bond/ LUT or under Refund of IGST (I) Exports Zero rated supplies All exports as well as supplies to SEZs have been categorized as Zero rated supplies in the IGST

Common Customs Law of the GCC States

The Cooperation Council for the Arab States of the Gulf Secretariat General Common Customs Law of the GCC States Rules of Implementation And Explanatory Notes Thereof This English text is to be used for

The Cooperation Council for the Arab States of the Gulf Secretariat General Common Customs Law of the GCC States Rules of Implementation And Explanatory Notes Thereof This English text is to be used for

Regulations of Exports, Imports And Customs in the Free Trade-Industrial Zones

Regulations of Exports, Imports And Customs in the Free Trade-Industrial Zones Decreed by the High Council of Free Trade-Industrial Zones September 1 l, 1994, No. k 70t/3845 January 16, 1997, No. K570T/

Regulations of Exports, Imports And Customs in the Free Trade-Industrial Zones Decreed by the High Council of Free Trade-Industrial Zones September 1 l, 1994, No. k 70t/3845 January 16, 1997, No. K570T/

ROUTINE PROCEDURES

A. REGISTRATION ROUTINE PROCEDURES AS SERVICE Procedure, conditions and safeguards for registration under service tax will be as prescribed by CBE&C by order rule 4(9) of Service Tax Rules, inserted w.e.f.

A. REGISTRATION ROUTINE PROCEDURES AS SERVICE Procedure, conditions and safeguards for registration under service tax will be as prescribed by CBE&C by order rule 4(9) of Service Tax Rules, inserted w.e.f.

APPENDIX 1 OPERATIONAL CERTIFICATION PROCEDURES FOR THE RULES OF ORIGIN

APPENDIX 1 OPERATIONAL CERTIFICATION PROCEDURES FOR THE RULES OF ORIGIN For the purposes of implementing Annex 3, the following operational procedures on the issuance of a Certificate of Origin, verification

APPENDIX 1 OPERATIONAL CERTIFICATION PROCEDURES FOR THE RULES OF ORIGIN For the purposes of implementing Annex 3, the following operational procedures on the issuance of a Certificate of Origin, verification

THE CUSTOMS ACT, 1962

I/11 THE CUSTOMS ACT, 1962 (Act No. 52 of 1962) 13th December, 1962 An Act to consolidate and amend the law relating to customs. Be it enacted by Parliament in the Thirteenth Year of the Republic of India

I/11 THE CUSTOMS ACT, 1962 (Act No. 52 of 1962) 13th December, 1962 An Act to consolidate and amend the law relating to customs. Be it enacted by Parliament in the Thirteenth Year of the Republic of India

[2012] 18 taxmann.com 256 (Article)

![[2012] 18 taxmann.com 256 (Article)](/thumbs/75/72354143.jpg "[2012] 18 taxmann.com 256 (Article)") [2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

[2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

Update on policy support available to the Apparel Sector - Its Impact on Exports

Apparel Export Promotion Council 30 January, 2018 Update on policy support available to the Apparel Sector - Its Impact on Exports Presented by: H K L Magu, Chairman The Apparel Industry Thanks Govt. for

Apparel Export Promotion Council 30 January, 2018 Update on policy support available to the Apparel Sector - Its Impact on Exports Presented by: H K L Magu, Chairman The Apparel Industry Thanks Govt. for

RENSEIGNEMENTS RELATIFS A LA MISE EN OEUVRE ET A L'ADMINISTRATION DE L'ACCORD. Addendum. Législation de la Turquie

ACCORD GENERAL SUR LES TARIFS DOUANIERS ET LE COMMERCE RESTRICTED VAL/l/Add.29 7 novembre 1994 Distribution spéciale (94-2328) Comité de l'évaluation en douane Original: anglais RENSEIGNEMENTS RELATIFS

ACCORD GENERAL SUR LES TARIFS DOUANIERS ET LE COMMERCE RESTRICTED VAL/l/Add.29 7 novembre 1994 Distribution spéciale (94-2328) Comité de l'évaluation en douane Original: anglais RENSEIGNEMENTS RELATIFS

1. Inclusion of cases filed with Settlement Commission in the "Call-Book"

Summary of Notifications, Circulars from 16 th December2014 to 15 th January 2015 EXCISE 1. Inclusion of cases filed with Settlement Commission in the "Call-Book" CBEC vide Circular No. 992/16/2014-CX.,

Summary of Notifications, Circulars from 16 th December2014 to 15 th January 2015 EXCISE 1. Inclusion of cases filed with Settlement Commission in the "Call-Book" CBEC vide Circular No. 992/16/2014-CX.,

FAQs Q1. Write a note on importance and demerits of custom duty. Ans. Importance of Customs duty Demerits of customs duty

FAQs Q1. Write a note on importance and demerits of custom duty. Ans. Importance of Customs duty a. Important source of revenue. b. Protection to domestic industry. c. Reduce deficit in the balance of

FAQs Q1. Write a note on importance and demerits of custom duty. Ans. Importance of Customs duty a. Important source of revenue. b. Protection to domestic industry. c. Reduce deficit in the balance of

Notification No. 88/ 2017-CUSTOMS (N.T.)

") [TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) Notification No. 88/ 2017-CUSTOMS (N.T.) New

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) Notification No. 88/ 2017-CUSTOMS (N.T.) New

FYJC. Subject : Organisation of Commerce & Management. Ch. 5. International Business SOLUTION

Date : Marks : 30 FYJC Subject : Ch. 5. International Business SOLUTION Duration: 1 Hr. 15 Min. Set No. : Q.1. Select the correct answer from the possible options given below and rewrite the statement:

Date : Marks : 30 FYJC Subject : Ch. 5. International Business SOLUTION Duration: 1 Hr. 15 Min. Set No. : Q.1. Select the correct answer from the possible options given below and rewrite the statement:

CUSTOMS PROCEDURES. Chapter 12 Import Export Management

Learning objectives: This chapter will help you to understand the full scope of the method and procedures of the Indian Customs Department applicable to the Import and Export consignments. 1.1 THE CUSTOMS

Learning objectives: This chapter will help you to understand the full scope of the method and procedures of the Indian Customs Department applicable to the Import and Export consignments. 1.1 THE CUSTOMS

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE CENTRAL BOARD OF EXCISE AND CUSTOMS SERVICE TAX WING NEW DELHI

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE CENTRAL BOARD OF EXCISE AND CUSTOMS SERVICE TAX WING NEW DELHI F.No.137/314/2012-Service Tax CIRCULAR NO. 185/4/2015-ST Dated: July 07, 2015

GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE CENTRAL BOARD OF EXCISE AND CUSTOMS SERVICE TAX WING NEW DELHI F.No.137/314/2012-Service Tax CIRCULAR NO. 185/4/2015-ST Dated: July 07, 2015

CERTIFICATE COURSE ON INDIRECT TAXES

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

Lao People s Democratic Republic Peace Independence Democracy Unity Prosperity

Lao People s Democratic Republic Peace Independence Democracy Unity Prosperity Ministry of Finance No. 2401/CD Customs Department Vientiane Capital, date: 29 September 2010 Instruction of the Director

Lao People s Democratic Republic Peace Independence Democracy Unity Prosperity Ministry of Finance No. 2401/CD Customs Department Vientiane Capital, date: 29 September 2010 Instruction of the Director

Applicability of GST on Import Clearances other than Port of Importation

Goods are imported in India and normally Bill of Entry for home consumption is filed. However, there will be a cases, where one needs to study the applicability of duty. Type of Sale Documents Applicable

Goods are imported in India and normally Bill of Entry for home consumption is filed. However, there will be a cases, where one needs to study the applicability of duty. Type of Sale Documents Applicable

Advanced Tax Laws and Practice 376

RollNo... Advanced Tax Laws and Practice 376 : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned

RollNo... Advanced Tax Laws and Practice 376 : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All references to sections mentioned

ARTICLE. On Finance Bill (Budget) Proposals 2013 Income Tax Act, 1961 By CA. SATISH AGARWAL

Proposals 2013 Income Tax Act, 1961 By CA. SATISH AGARWAL") ARTICLE On Finance Bill (Budget) Proposals 0 Income Tax Act, 96 By CA. SATISH AGARWAL Mobile : +99808957 Phone : +95769 Office : 9/4, East Patel Nagar, (Near Jaypee Sidharthe Hotel) New Delhi - 0008 :

ARTICLE On Finance Bill (Budget) Proposals 0 Income Tax Act, 96 By CA. SATISH AGARWAL Mobile : +99808957 Phone : +95769 Office : 9/4, East Patel Nagar, (Near Jaypee Sidharthe Hotel) New Delhi - 0008 :

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Summary of Notifications, Circulars from 16 th October, 2016 to 15 th November, 2016

Summary of Notifications, Circulars from 16 th October, 2016 to 15 th November, 2016 SERVICE TAX 1. Amendments regarding levy of Service Tax on "online information and database access or retrieval services"

Summary of Notifications, Circulars from 16 th October, 2016 to 15 th November, 2016 SERVICE TAX 1. Amendments regarding levy of Service Tax on "online information and database access or retrieval services"

CHAPTER 4 DUTY EXEMPTION / REMISSION SCHEMES

CHAPTER 4 DUTY EXEMPTION / REMISSION SCHEMES 4.00 Objective Schemes under this Chapter enable duty free import of inputs for export production, including replenishment of input or duty remission. 4.01

CHAPTER 4 DUTY EXEMPTION / REMISSION SCHEMES 4.00 Objective Schemes under this Chapter enable duty free import of inputs for export production, including replenishment of input or duty remission. 4.01

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012 A. SERVICE TAX 1. Pursuant to the negative list becoming effective from July 1, 2012, various consequential

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012 A. SERVICE TAX 1. Pursuant to the negative list becoming effective from July 1, 2012, various consequential

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE & SERVICE TAX, BHAVNAGAR

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE & SERVICE TAX, BHAVNAGAR Plot No. 67-76/B-1, Siddhi Sadan, Narayan Upadhya Road, Bhavnagar 364 001 Phone Number-0278-2523625 Fax No. 0278-2513086 Information

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE & SERVICE TAX, BHAVNAGAR Plot No. 67-76/B-1, Siddhi Sadan, Narayan Upadhya Road, Bhavnagar 364 001 Phone Number-0278-2523625 Fax No. 0278-2513086 Information

IMPORT & EXPORT (CUSTOMS)

") IMPORT & EXPORT (CUSTOMS) MCM711 Legal Framework of Construction 1 Prof. Rajiv Gupta, NICMAR Objectives: Introduction to laws pertaining to import and export. Description of the powers of the authorities

IMPORT & EXPORT (CUSTOMS) MCM711 Legal Framework of Construction 1 Prof. Rajiv Gupta, NICMAR Objectives: Introduction to laws pertaining to import and export. Description of the powers of the authorities

Office of the Development Commissioner Special Economic Zones Karnataka and Kerala Administrative Office, CSEZ, Kakkanad, Kochi, Kerala

To Office of the Development Commissioner Special Economic Zones Karnataka and Kerala Administrative Office, CSEZ, Kakkanad, Kochi, Kerala 682 037 All SEZ Developers All SEZ Units All Specified/Authorised

To Office of the Development Commissioner Special Economic Zones Karnataka and Kerala Administrative Office, CSEZ, Kakkanad, Kochi, Kerala 682 037 All SEZ Developers All SEZ Units All Specified/Authorised

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 7 PART A

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of Question Paper relate

: 1 : RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 7 NOTE : All references to sections mentioned in Part-A of Question Paper relate

Summary of Notifications, Circulars from 16 th June, 2016 to 15 th July, 2016

Summary of Notifications, Circulars from 16 th June, 2016 to 15 th July, 2016 SERVICE TAX 1. Services Provided prior to 31st May 2016 exempt from Krishi Kalyan Cess (KKC) The Central Government vide Notification

Summary of Notifications, Circulars from 16 th June, 2016 to 15 th July, 2016 SERVICE TAX 1. Services Provided prior to 31st May 2016 exempt from Krishi Kalyan Cess (KKC) The Central Government vide Notification

BACKGROUND OF INDIRECT TAX LAW INTRODUCTION TO CUSTOMS DUTY TYPE OF CUSTOM DUTIES

CONTENTS u Chapter-heads I-5 u Section-wise Index I-21 DIVISION ONE LIABILITY OF CUSTOMS DUTY 1 BACKGROUND OF INDIRECT TAX LAW 1.1 Features of Indirect Taxes 3 1.2 Constitution of India 4 1.3 Bill, Act,

CONTENTS u Chapter-heads I-5 u Section-wise Index I-21 DIVISION ONE LIABILITY OF CUSTOMS DUTY 1 BACKGROUND OF INDIRECT TAX LAW 1.1 Features of Indirect Taxes 3 1.2 Constitution of India 4 1.3 Bill, Act,

IGST REFUNDS - EXPORTS ROLE OF CUSTOMS

IGST REFUNDS - EXPORTS ROLE OF CUSTOMS BACKGROUND OF IGST REFUNDS ON EXPORTS Exports : Zero-Rated Supply: Eligible to Claim Refund As per Sec 2(23) of IGST Act: zero-rated supply shall have the meaning

IGST REFUNDS - EXPORTS ROLE OF CUSTOMS BACKGROUND OF IGST REFUNDS ON EXPORTS Exports : Zero-Rated Supply: Eligible to Claim Refund As per Sec 2(23) of IGST Act: zero-rated supply shall have the meaning

Bonded Processes. Inbond Transportation/Bonded Warehouse/Foreign Trade Zone. Gateway International Foreign Trade Zone

Bonded Processes Inbond Transportation/Bonded Warehouse/Foreign Trade Zone Gateway International Foreign Trade Zone What is Bonded Freight Freight that has not cleared on a consumption entry is considered

Bonded Processes Inbond Transportation/Bonded Warehouse/Foreign Trade Zone Gateway International Foreign Trade Zone What is Bonded Freight Freight that has not cleared on a consumption entry is considered

FOREIGN TRADE ZONES PETROLEUM TECHNICAL INFORMATION FOR PRE-ASSESSMENT SURVEY (TIPS)

") FOREIGN TRADE ZONES PETROLEUM TECHNICAL INFORMATION FOR PRE-ASSESSMENT SURVEY (TIPS) TABLE OF CONTENTS PART 1 BACKGROUND... 2 PART 2 PETROLEUM FTZ GUIDANCE... 2 2.1 EXAMPLES OF RED FLAGS...3 2.2 EXAMPLES

FOREIGN TRADE ZONES PETROLEUM TECHNICAL INFORMATION FOR PRE-ASSESSMENT SURVEY (TIPS) TABLE OF CONTENTS PART 1 BACKGROUND... 2 PART 2 PETROLEUM FTZ GUIDANCE... 2 2.1 EXAMPLES OF RED FLAGS...3 2.2 EXAMPLES

Important Service Tax Amendments through Union Budget 2016 (By CA. Vikas Khandelwal) 1. Krishi Kalyan Cess (Applicable w. e. f

1. Krishi Kalyan Cess (Applicable w. e. f") Important Service Tax Amendments through Union Budget 2016 (By CA. Vikas Khandelwal) 1. Krishi Kalyan Cess (Applicable w. e. f. 01.06.2016): Effective rate of service tax is being increased from 14.5%

Important Service Tax Amendments through Union Budget 2016 (By CA. Vikas Khandelwal) 1. Krishi Kalyan Cess (Applicable w. e. f. 01.06.2016): Effective rate of service tax is being increased from 14.5%

BACKGROUND OF INDIRECT TAX LAW

CONTENTS u Chapter-heads I-5 u Section-wise Index I-17 DIVISION ONE LIABILITY OF CUSTOMS DUTY 1 BACKGROUND OF INDIRECT TAX LAW 1.1 Features of Indirect Taxes 3 1.2 Constitution of India 4 1.3 Bill, Act,

CONTENTS u Chapter-heads I-5 u Section-wise Index I-17 DIVISION ONE LIABILITY OF CUSTOMS DUTY 1 BACKGROUND OF INDIRECT TAX LAW 1.1 Features of Indirect Taxes 3 1.2 Constitution of India 4 1.3 Bill, Act,

19 USC 1401a. NB: This unofficial compilation of the U.S. Code is current as of Jan. 4, 2012 (see

TITLE 19 - CUSTOMS DUTIES CHAPTER 4 - TARIFF ACT OF 1930 SUBTITLE III - ADMINISTRATIVE PROVISIONS Part I - Definitions and National Customs Automation Program subpart a - definitions 1401a. Value (a) Generally

TITLE 19 - CUSTOMS DUTIES CHAPTER 4 - TARIFF ACT OF 1930 SUBTITLE III - ADMINISTRATIVE PROVISIONS Part I - Definitions and National Customs Automation Program subpart a - definitions 1401a. Value (a) Generally

Customs and Excise (Border Processing Levy) Order 2015

Order 2015") 2015 Jerry Mateparae, Governor-General Order in Council At Wellington this 9th day of November 2015 Present: The Right Hon John Key presiding in Council Pursuant to section 288B of the Customs and Excise

2015 Jerry Mateparae, Governor-General Order in Council At Wellington this 9th day of November 2015 Present: The Right Hon John Key presiding in Council Pursuant to section 288B of the Customs and Excise

KDF3A INDIRECT TAXATION UNIT I -V

KDF3A INDIRECT TAXATION UNIT I -V Unit I : Syllabus Taxation Objectives of Taxation Canon of taxation Classification of Tax Difference between Direct & Indirect Tax. KDF3A-INDIRECT TAXATION 2 OVER VIEW

KDF3A INDIRECT TAXATION UNIT I -V Unit I : Syllabus Taxation Objectives of Taxation Canon of taxation Classification of Tax Difference between Direct & Indirect Tax. KDF3A-INDIRECT TAXATION 2 OVER VIEW

INFORMATION ON IMPLEMENTATION AND ADMINISTRATION OF THE AGREEMENT. Addendum. Legislation of the United States

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED SM1^1*981 Special Distribution Committee on Customs Valuation INFORMATION ON IMPLEMENTATION AND ADMINISTRATION OF THE AGREEMENT Addendum Legislation of

GENERAL AGREEMENT ON TARIFFS AND TRADE RESTRICTED SM1^1*981 Special Distribution Committee on Customs Valuation INFORMATION ON IMPLEMENTATION AND ADMINISTRATION OF THE AGREEMENT Addendum Legislation of

ANF-8. For claiming Duty Drawback on All Industry Rates/Fixation of Drawback Rates/Refund of Terminal Excise Duty.

ANF-8 For claiming Duty Drawback on All Industry Rates/Fixation of Drawback Rates/Refund of Terminal Excise Duty. (Please state Not Applicable wherever the information is not applicable to you ) 1. IEC

ANF-8 For claiming Duty Drawback on All Industry Rates/Fixation of Drawback Rates/Refund of Terminal Excise Duty. (Please state Not Applicable wherever the information is not applicable to you ) 1. IEC

SIPOY SATISH CA IPCC MAY-2013/ NOV-2013 F.Y F. A MARKS. VALUE ADDED TAX `100

SIPOY SATISH www.cacwacs.wordpress.com sipoysatish@gmail.com VALUE ADDED TAX 25 MARKS Including EXAMINATION QUESTIONS CA IPCC MAY-2013/ NOV-2013 F.Y. 2012-13 F. A. 2012 100 VALUE ADDED TAX INDEX 2 Q1 (V.

SIPOY SATISH www.cacwacs.wordpress.com sipoysatish@gmail.com VALUE ADDED TAX 25 MARKS Including EXAMINATION QUESTIONS CA IPCC MAY-2013/ NOV-2013 F.Y. 2012-13 F. A. 2012 100 VALUE ADDED TAX INDEX 2 Q1 (V.

TCS Provision at a Glance for FY

TCS Provision at a Glance for FY 2017-18 Who is Liable to Collect TCS As per Section 206C(1), Every Person being a seller of Goods of nature specified in table below shall, At the time of debiting to the

TCS Provision at a Glance for FY 2017-18 Who is Liable to Collect TCS As per Section 206C(1), Every Person being a seller of Goods of nature specified in table below shall, At the time of debiting to the

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE : AHMEDABAD-III 2 ND FLOOR, CUSTOM HOUSE, NEAR ALL INDIA RADIO, NAVRANGPURA, AHMEDABAD

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE : AHMEDABAD-III 2 ND FLOOR, CUSTOM HOUSE, NEAR ALL INDIA RADIO, NAVRANGPURA, AHMEDABAD-380009 Phone No. : 079 2754 3676 Fax No. 079 2754 3676 e-mail : ahmedab3@excise.nic.in

OFFICE OF THE COMMISSIONER OF CENTRAL EXCISE : AHMEDABAD-III 2 ND FLOOR, CUSTOM HOUSE, NEAR ALL INDIA RADIO, NAVRANGPURA, AHMEDABAD-380009 Phone No. : 079 2754 3676 Fax No. 079 2754 3676 e-mail : ahmedab3@excise.nic.in

Audit Protocol for the Private Copying Regulation Version 1 January 2018

Audit Protocol for the Private Copying Regulation Version 1 January 2018 Introduction This Audit Protocol elaborates on the obligations of the contracting parties by virtue of Article 10 of the Collection

Audit Protocol for the Private Copying Regulation Version 1 January 2018 Introduction This Audit Protocol elaborates on the obligations of the contracting parties by virtue of Article 10 of the Collection

Chapter 33 Black Sea Wheat Futures

Chapter 33 Black Sea Wheat Futures 33100. SCOPE OF CHAPTER This chapter is limited in application to Black Sea Wheat futures. The procedures for trading, clearing, inspection, delivery and settlement not

Chapter 33 Black Sea Wheat Futures 33100. SCOPE OF CHAPTER This chapter is limited in application to Black Sea Wheat futures. The procedures for trading, clearing, inspection, delivery and settlement not

1. Introduction 3. Customs and Excise Duties 2. Customs and Excise Clearance General Overview 4. Customs Duties Rebates

1. Introduction This notice is intended to provide an overview of Customs procedures applicable in the Republic of Botswana. The document focuses on the types of rebates that are offered to manufacturers

1. Introduction This notice is intended to provide an overview of Customs procedures applicable in the Republic of Botswana. The document focuses on the types of rebates that are offered to manufacturers

CUSTOMS CODE OF THE REPUBLIC OF KAZAKHSTAN

CUSTOMS CODE OF THE REPUBLIC OF KAZAKHSTAN Translated by TRADE FACILITATION AND INVESTMENT ACTIVITY ПРОЕКТ ПО РАЗВИТИЮ ТОРГОВЛИ И ИНВЕСТИЦИЯМ I. GENERAL PART...17 SECTION I. GENERAL PROVISIONS...17 CHAPTER

CUSTOMS CODE OF THE REPUBLIC OF KAZAKHSTAN Translated by TRADE FACILITATION AND INVESTMENT ACTIVITY ПРОЕКТ ПО РАЗВИТИЮ ТОРГОВЛИ И ИНВЕСТИЦИЯМ I. GENERAL PART...17 SECTION I. GENERAL PROVISIONS...17 CHAPTER

Rubber Declared Delivery Procedure

(As of October 9 th, 2018) Rubber Declared Delivery Procedure DISCLAIMER: This English translation is being provided for informational purposes only and represents a desire by the Exchange to promote better

(As of October 9 th, 2018) Rubber Declared Delivery Procedure DISCLAIMER: This English translation is being provided for informational purposes only and represents a desire by the Exchange to promote better

7 VAT Procedures. 1. Registration. Learning objectives

7 VAT Procedures Learning objectives After reading this chapter you will be able to understand: the provisions relating to registration under VAT laws. what is tax payer identification number (TIN). the

7 VAT Procedures Learning objectives After reading this chapter you will be able to understand: the provisions relating to registration under VAT laws. what is tax payer identification number (TIN). the

Copyright -The Institute of Chartered Accountants of India

PAPER 3 : ADVANCED AUDITING Answer all questions. Question 1 As an auditor how would you deal with the following? (a) There is a sales-tax demand of Rs. 3 crores against X Ltd. relating to prior years

PAPER 3 : ADVANCED AUDITING Answer all questions. Question 1 As an auditor how would you deal with the following? (a) There is a sales-tax demand of Rs. 3 crores against X Ltd. relating to prior years

OIO No. 08/JC/2011 Dated : BRIEF FACTS OF THE CASE:

BRIEF FACTS OF THE CASE: M/s Bhavin Impex Pvt. Ltd., Plot 129, GIDC, Phase - II, Dared, Dist: Jamnagar (100% EOU) (hereinafter referred to as the noticee ) are engaged in the manufacturing of brass sanitary

BRIEF FACTS OF THE CASE: M/s Bhavin Impex Pvt. Ltd., Plot 129, GIDC, Phase - II, Dared, Dist: Jamnagar (100% EOU) (hereinafter referred to as the noticee ) are engaged in the manufacturing of brass sanitary

Certified International Trade and Forex Professional VS-1262

Certified International Trade and Forex Professional VS-1262 Certified International Trade and Forex Professional Certification Code VS-1262 Import export business also known as international trading,

Certified International Trade and Forex Professional VS-1262 Certified International Trade and Forex Professional Certification Code VS-1262 Import export business also known as international trading,

Central Board of Excise & Customs

(Draft for circulation) Central Board of Excise & Customs Citizens Charter The CBEC is the apex body for the collection of duties of Excise, Customs and Services (Service Tax). This organization is working

(Draft for circulation) Central Board of Excise & Customs Citizens Charter The CBEC is the apex body for the collection of duties of Excise, Customs and Services (Service Tax). This organization is working

Goods & Services Tax

Goods & Services Tax Central Goods & Services Tax Act, 2017 Import & Export of Goods District Centre Janakpuri Study Circle Of NIRC of ICAI Friday, 25 th August, 2017 CA RohitVaswani, B.Com, FCA, ACMA,

Goods & Services Tax Central Goods & Services Tax Act, 2017 Import & Export of Goods District Centre Janakpuri Study Circle Of NIRC of ICAI Friday, 25 th August, 2017 CA RohitVaswani, B.Com, FCA, ACMA,

Practical Problems on Customs

Theory relevant to practical problems: Valuation under Customs: Practical Problems on Customs 1. Tariff Value as prescribed under section 14(2) of the Customs Act : In this case, the value of the goods

Theory relevant to practical problems: Valuation under Customs: Practical Problems on Customs 1. Tariff Value as prescribed under section 14(2) of the Customs Act : In this case, the value of the goods