SOLID INVESTMENT AND FINANCIAL STRATEGIES. For 2017 and Beyond

|

|

|

- Ursula Lynch

- 5 years ago

- Views:

Transcription

1 SOLID INVESTMENT AND FINANCIAL STRATEGIES For 2017 and Beyond 1

2 ENTITY CHOICE CONSIDERATIONS Distribution of Entity Choices Of all the choices you make when starting a business, one of the most important is the type of legal organization you select for your company. This decision can affect how much you pay in taxes, the amount of paperwork your business is required to do, the personal liability you face and your ability to borrow money. Business formation is controlled by the law of the state where your business is organized. This fact sheet provides a quick look at the differences between the most common forms of business entities. The most common forms of businesses are: Sole Proprietorships Partnerships Corporations Limited Liability Companies (LLC) While state law controls the formation of your business, federal tax law controls how your business is taxed. Federal tax law recognizes an additional business form, the Subchapter S Corporation. 2

3 All businesses must file an annual return. The form you use depends on how your business is organized. Sole proprietorships and corporations file an income tax return. Partnerships and S Corporations file an information return. For an LLC with at least two members, except for some businesses that are automatically classified as a corporation, it can choose to be classified for tax purposes as either a corporation or a partnership. A business with a single member can choose to be classified as either a corporation or disregarded as an entity separate from its owner, that is, a disregarded entity. As a disregarded entity the LLC will not file a separate return instead all the income or loss is reported by the single member/owner on its annual return. The answer to the question What structure makes the most sense? depends on the individual circumstances of each business owner. The type of business entity you choose will depend on: Liability Taxation Recordkeeping Sole Proprietorship A sole proprietorship is the most common form of business organization. It s easy to form and offers complete control to the owner. It is any unincorporated business owned entirely by one individual. In general, the owner is also personally liable for all financial obligations and debts of the business. (State law may also govern this area depending on the state.) Sole proprietors can operate any kind of business. It must be a business, not an investment or hobby. It can be full-time or part-time work. This includes operating a: Shop or retail trade business Large company with employees Home based business One person consulting firm Every sole proprietor is required to keep sufficient records to comply with federal tax requirements regarding business records. Generally, sole proprietors file Schedule C or C-EZ, Profit or Loss from Business, with their Form Sole proprietor farmers file Schedule F, Profit or Loss from Farming. Your net business income or loss is combined with your other income and deductions and taxed at individual rates on your personal tax return. 3

4 Sole proprietors must also pay self-employment tax on the net income reported on Schedule C or Schedule F. You may also be able to deduct one-half of SE tax on your Use Schedule SE, Self-Employment Tax, to compute this tax. Sole proprietors do not have taxes withheld from their business income so you will generally need to make quarterly estimated tax payments if you expect to make a profit. These estimated payments include both income tax and selfemployment taxes for Social Security and Medicare. Subchapter S Corporation The Subchapter S corporation is a variation of the standard corporation. The S corporation allows income or losses to be passed through to individual tax returns, similar to a partnership. The rules for Subchapter S corporations are found in Subchapter S of Chapter 1 of the Internal Revenue Code. An S corporation has the same corporate structure as a standard corporation. It is a legal entity, chartered under state law, and is separate from its shareholders and officers. There is generally limited liability for corporate shareholders. The difference is that the corporation files an election on Form 2553, Election by a Small Business Corporation, to be treated differently for federal tax purposes. Generally, an S corporation is exempt from federal income tax other than tax on certain capital gains and passive income. It is treated in the same way as a partnership, in that generally taxes are not paid at the corporate level. An S corporation files Form 1120S, U.S. Corporation Income Tax Return for an S Corporation. The income flows through to be reported on the shareholders individual returns. Schedule K-1, Shareholder s Share of Income, Credits and Deductions, is completed with Form 1120S for each shareholder. The Schedule K-1 tells shareholders their allocable share of corporate income and deductions. Shareholders must pay tax on their share of corporate income, regardless of whether it is actually distributed. Why is the S-corporation the Entity of Choice by so many tax professionals? 4

5 Here is an example of how an S-corporation could save you in SE taxes if you were a one person S-corporation. Example: The taxable income generated by your S-corporation business is estimated to be $100,000 for 2016 or 2017 before you pay yourself. You take a $50,000 salary. Only that amount is hit with the 15.3 percent federal Social Security and Medicare tax, which amounts to $7,650. You can withdraw the remaining corporate cash flow in the form of distributions to yourself that will not be subject to SE taxes (this will be added to your personal income on which you will pay tax at your current tax bracket). If you operate the same business as an LLC or sole proprietorship (assuming one owner) where each member is subject to SE taxes, you owe SE tax on your entire $100,000 profit, for a total of $14,130 ($100, = $92, %). Operating as an S-corporation could save you thousands ($14,130 $7,650 = $6,480). Remember: You must be able to show that a $50,000 salary is reasonable. If the IRS thinks it s too low, it may try to reclassify all or part of your purported cash distributions as disguised wages. Future tax bills look to possibly remove this tax break. Limited Liability Company A Limited Liability Company (LLC) is a relatively new business structure allowed by state statute. LLCs are popular because, similar to a corporation, owners generally have limited personal liability for the debts and actions of the LLC. Other features of LLCs are more like a partnership, providing management flexibility and the benefit of passthrough taxation. Owners of an LLC are called members. Since most states do not restrict ownership, members may include individuals, corporations, other LLCs and foreign entities. Most states also permit single member LLCs, those having only one owner. 5

6 A few types of businesses generally cannot be LLCs, such as banks and insurance companies. Check your state s requirements and the federal tax regulations for further information. There are special rules for foreign LLCs. For additional information on the kinds of tax returns to file, how to handle employment taxes and possible pitfalls, refer to Publication 3402, Tax Issues for Limited Liability Companies. Which structure best suits your business? One form is not necessarily better than any other. Each business owner must assess his or her own needs. It may be important to seek advice from business experts and professionals when considering the advantages and disadvantages of a business entity. 6

7 Retirement Plan Considerations INCREASE IN RETIREMENT PLAN CONTRIBUTION LIMITS The limits on contributions to retirement plans are increased as shown on the following table. Retirement Plan Contribution Limits Year IRA Simple 401(k) Def Cont SEP % of Profit /25 Catch-up Contributions for individuals 50 years or older for certain Plans: IRA or ROTH IRA $1,000 SIMPLE PLANS $3, (k) $6,000 Note: The SEP IRA does not allow catch-up contributions 7

8 The 401(k) series A good way to increase retirement plan contributions on lower levels of profit. (or S Corporation Salaries) Must be started by end of first year, you can t wait until the following year to set up like a SEP IRA Only problem is that if a self employed person is not maximizing contributions to their current retirement plan, they won t do it to the 401(k) either The 401(k) series Solo (k) or Safe Harbor 401(k) Profit $50,000 $80,000 $220,000 Cont: $18,000 $18,000 $18, % 12,500 20,000 36,000 =401(k) $30,500 $38,000 $54,000 If 50+ $36,500 $44,000 $60,500 vs SEP $10-12K $16-20K $54,000 8

9 Roth 401(k) NOT SUBJECT TO INCOME LIMITS OF ROTH IRA Not Tax Deductible, but distributions are generally tax free 401K Loans available Maximum deferral per employee will be $18,000OR $24,000/year for age 50+ Maximum contribution from employer is 25% of employees compensation. Combined contribution between employer and employee not to exceed $54,000/year (2017) 9

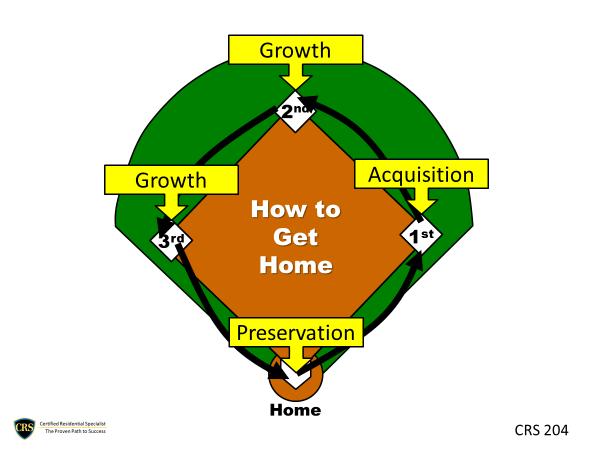

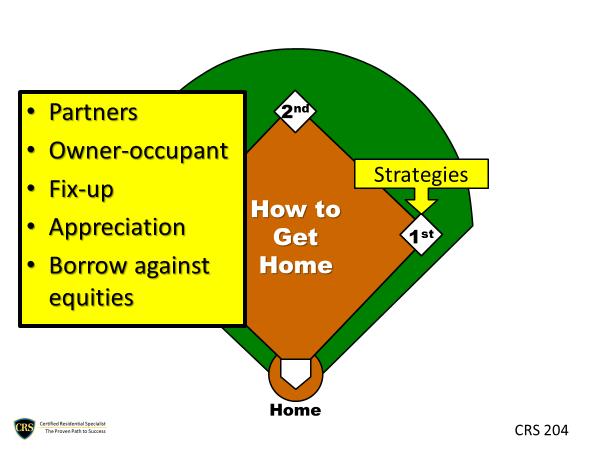

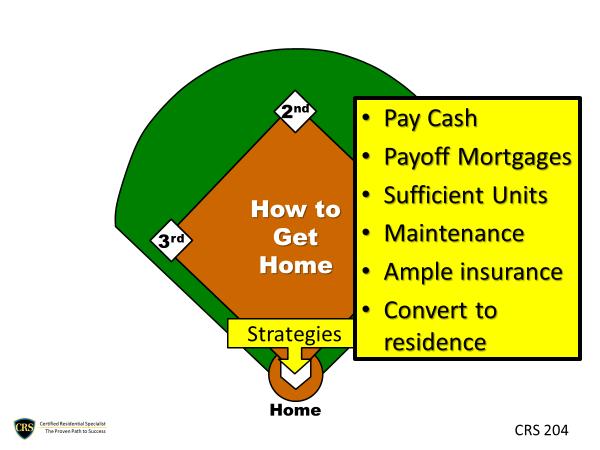

10 Investment Considerations Consider Purchasing Investment Real Estate in this market The IDEAL Formula I D E A L Income from Cash Flows Depreciation Deductions Equity Buildup Appreciation Leverage 10

11 Investing in Real Estate for the Benefit of the Client and the Realtor Return on Investment and Cash Flow 11

12 12

13 13

14 14

15 15

16 Tax Advantages-The Real Estate Professional Rule SPECIAL RULE FOR RENTAL REAL ESTATE Under this special rule if you actively participate in your rental real estate you may offset or deduct up to $25,000 (12,500 if married and filing separately) of passive losses against non-passive income. To qualify, However, you must meet all of the following tests: 1. you own at least 10% interest in the rental activity 2. you cannot hold your interest as a limited partner 3. the rental activity cannot be subject to a net lease 4. you or your spouse must actively participate in the rental activity Making management decisions is the key to qualifying as being active. It is not necessary for you to manage the property yourself if you retain the management decision responsibilities. You need to be active in the decision making process. A deduction of up to $25,000 in net real estate rental passive losses from nonpassive income by a taxpayer is limited also to taxpayers with an adjusted Gross Income (AGI) of no more than $100,000. If the taxpayer's AGI exceeds $150,000, no part of the $25,000 allowance is available. For AGI between $100,000 and $150,000, the $25,000 allowance will be reduced by 50% of that amount over $100,000 up to $150,

17 EXAMPLE: A taxpayer has adjusted gross income (AGI) of $137,500. The maximum deduction available in this tax year will be $6,250. ($137,500 - $100,000) = 37,500 X 50% = $18,750 $25,000 - $18,750 = $6,250 SUSPENSION RULES Amounts that are disallowed as deductions under the passive loss limitation are carried forward, or "suspended," and can be used to offset net passive income in future years from any source. If not used up before the property generating the passive loss is sold, the suspended losses are deductible in the year of sale from any type of income. REAL ESTATE PROFESSIONAL RULE Probably one of the most significant positive changes of the 1993 Omnibus Reconciliation Act affecting real estate professionals is the modification to the passive loss rules. Commencing in 1994 real estate professionals may offset losses from real estate against non-passive income. A person is considered a real estate professional if more than half of the personal services he/she performs are in real property trades or businesses in which he/she materially participates. Real property businesses are development, construction, acquisition, rental, management, brokerage, etc. Of particular benefit may be this rule as it applies to spouses filing a joint return. One spouse may qualify and have losses which may be offset against the other spouses income. To treat losses from rental real estate as non-passive you met three conditions: 1. You must materially participate in the real estate activity creating the loss. That means regular, continuous and substantial participation. 17

18 2. More than half of your business - connected personal efforts must be concentrated in a real estate business or businesses. 3. You must materially participate in your real estate business, or businesses. Warning!!!!!!!!!!!! For my buy-hold-rent investors, beware of fairly recent IRS wins in courts against individuals who own rental properties and who have deducted tax losses from the operation of their rentals. Since 1994, accountants and their clients have been operating under a mistaken impression of the Real Estate Professional Rules of the 1993 tax law change. Under that tax change, it appeared that Realtors who met the rules could take unlimited write-offs from their properties. However, in the past several years, the courts have been finding that indeed, we cannot write-off all of our deductions unless we meet very, very, very, specific requirements. The crux of the problem is identified in the IRS s own instructions to its agents who will be auditing rental property deductions and losses of Realtors. IRS MSSP Guidelines Beginning with the 1994 year, a taxpayer who meets ALL of the following can deduct current rental real estate losses in full regardless of how high his/her AGI might be: 1. More than half of the taxpayer's personal services in all businesses must be in real property businesses. A real property business is real property development, construction, acquisition, conversion, rental, management, leasing, or brokerage. 2. The taxpayer must spend more than 750 hours a year in real property trades or businesses. NOTE: For time to be counted in either of the above two tests, the taxpayer must materially participate in the activity. 3. The taxpayer must materially participate in each rental real estate activity unless he or she has filed an election to group all rental real estate activities as one (for purposes of materially participating). My observation: Fulltime Realtors should have no problem meeting rules number #1 and #2, however, rule #3 looks to be very troubling. What Realtors have to be able to show is that they are materially participating in the management of each property, unless they make a special election to aggregate their rental properties, wherein they only need to show that they are materially participating in the management of ALL their rental properties. The IRS uses a time line of 500 hours per year as one of it s tests of material participation, and 100 hours per year as another test. In either case, however, the election to aggregate is of PRIME importance on your 2017 return (2016, if not yet filed), so that the investor only has to be able to prove the 500 or 100 hour test on ALL of their rental properties, instead of having to meet those tests on EACH of their rental properties. Please, please talk to your accountant 18

19 about this election, because most of us in the business have simply misunderstood this point. I have included a draft of the proper election language for your use. Election Wording Election to Treat All Real Estate Interests as One Activity (IRC Section 469(c)(7)(A)) and Regulation (g)(3) Tax Year 2014 Helen J. Smith 4572 South Providence Street Urbana, IL SSN: Pursuant to IRC Section 469(c)(7)(a), Helen J. Smith, SSN elects to treat all rental real estate interests as one activity to qualify as a materially participating real estate professional this tax year. Estate and Succession Planning Current Federal Estate tax Exemption is $5,540,000 and the current Annual Gift Tax Exemption is $14,000. Let me explain what this means. 19

20 What are your Plans???????? 1. Build Net Worth? 2. Grow Mail Box Income? 3. Leave Net Worth to Heirs? 4. Leave Income Stream to Heirs? 5. Do Your Heirs want the Properties???????? 6. Do your heirs want to work as hard as you do?????? Suffice it to say that leaving real estate to your heirs, or others for that matter, at your death can be a spectacular way to keep the tax man at bay, depending on: 1. Your total net worth 2. How you have used trusts 3. Use of CRATS 4. And other strategies beyond the scope of this brief seminar Acquisition Strategies 20

21 21

22 22

23 23

24 The Internal Revenue Code Section 1031 Exchange-A property improvement issue DEFERRING TAX ON RENTAL REAL ESTATE BY EXCHANGING A. What is an Exchange 1. Disposing (selling) of one property and the acquisition (buying) of another property 2. Usually involves three (or more) parties 24

25 Logistics of an exchange. Chart 1. The regular exchange Chad is the Seller (Exchanger) Direct Deeding: Contract date is February 1, 2017 Closing March 5 Sales Proceeds Ann Ann is the Buyer of Chad s Qualified Intermediary 45-day Identification Period deadline is April 19, day deadline is Sept 1, Purchase Proceeds Direct Deeding Jane Identification date is 4/1/17, Contract date is 4/1/17 Closing date is June Jane is the Seller of replacement property to 25

26 Logistics of an Exchange The fact that a contract has been negotiated for the purchase of the replacement property prior to the sale of the relinquished property will not preclude a tax-deferred exchange result. A seller who has entered into a contract to sell the relinquished property may still enter into an exchange of the property, if an exchange agreement is entered into prior to closing. On the other side of the exchange, the seller of the relinquished property may enter into a contract to purchase the replacement property prior to closing on the sale of the relinquished property. The Language of Exchanging 1. Like-kind property 2. Unlike-kind property a. Cash b. Boot c. Net loan relief 3. Gain a. Realized b. Recognize c. Unrecognized Delayed Exchanges 1. Purpose is to allow a person to dispose of their property without knowing exactly what the new property will be 2. You have days from the day of sale to the replacement property 3. You have days from a day out sale to the replacement property 4. You must place sale proceeds in a qualified and properly set up escrow account 26

27 A COMBINATION OF BOTH RETIREMENT PLANS AND INVESTING IN REAL ESTATE CONSIDER THE REAL ESTATE IRA A. Introduction This opportunity is legal although few professionals really understand the details. This opportunity is very complex, although after you have done it once, the process does not seem that difficult. This opportunity is like a ladder, at the first rung, everyone can quickly grasp the details, but as you climb the ladder, the higher rungs become much more difficult to both understand and to implement. I have used the phrase, Many are called but few are chosen to emphasize that while many, many, many real estate agents get very excited about the possibilities of this investment, if 10% of them actually follow up and make the investment I would be surprised. B. Terminology 1. The ability to purchase real estate in a retirement plan includes ALL retirement plans. This means that the following retirement plans can own real estate properties. a. IRA b. ROTH IRA c. SEP (Simplified Employee Pension) d. 401(k) e. Profit sharing plan f. Money purchase plan g. Defined benefit plan Custodian or Trustee-A custodian or trustee is required for all individual account arrangements. These two terms are synonymous. A custodian or trustee must be a bank, federally insured credit union, savings and loan institution, or other entity approved by the IRS to act as trustee or custodian. An individual cannot qualify as trustee or 27

28 C. Advantages custodian. The trustee or custodian is the entity which is responsible for receiving and holding contributions and plan assets; maintaining accurate records of contributions, earnings, distributions, and other relevant records; making distributions to beneficiaries, and providing annual statements to account holders. The most commonly used name for these custodians or trustees is SPECIAL ASSET TRUSTEE, and the 5 better known SAT s are: a. Equity Trust, Elyria, OH b. Entrust, Oakland, CA c. Fiserve, Denver, CO d. Pensco e. Sterling Trust, Waco, TX Among the most obvious advantages of investing retirement plan assets in real estate properties are: 1. Income tax (Federal and State) deferral. Keeping the money that would otherwise be paid in taxes in the investment 2. Investing in what you know as opposed to conventional investment vehicles such as stocks, bonds, and mutual funds that you may not understand as well 3. Investing in what you can control 4. If a ROTH IRA is used to own the real estate properties, the opportunity for tax-free profits, as opposed to tax deferred profits is available D. Disadvantages Not all is a bed of roses with this investment alternative. The following list provides reasons why you should not consider the Real Estate IRA. 1. The federal income tax rates, both marginal and capital gains rates, have never been lower. So paying your taxes now, (owning the property outside of your retirement plan) may be a wise decision. 2. Any tax write-offs attributable to the rental property owned by the retirement plan are not deductible 3. Complexity, complexity, complexity!!!!! 4. Finding professional advisors that know what they are doing 5. Avoid Prohibited Transactions!!!! These are: a. Personally borrowing money from your retirement plan b. Selling property to your retirement plan c. Receiving unreasonable compensation for managing the property 28

29 d. Using the retirement plan as a security for a loan e. Purchasing property for personal use with your retirement plan funds 29

Trusteed Cross Purchase Buy-Sell Agreement

Steilacoom Investments Steilacoom Investments D. O. Magnus Brandfors President 208 Wilkes Street Steilacoom, WA 98388 253-582-5225 magnus@steilacoominvestments.com www.steilacoominvestments.com Trusteed

Steilacoom Investments Steilacoom Investments D. O. Magnus Brandfors President 208 Wilkes Street Steilacoom, WA 98388 253-582-5225 magnus@steilacoominvestments.com www.steilacoominvestments.com Trusteed

UNDERSTANDING REQUIRED MINIMUM DISTRIBUTIONS

MAKING ADVISED CHOICES RETIREMENT UNDERSTANDING REQUIRED MINIMUM DISTRIBUTIONS PRUDENTIAL CAN HELP Prudential has developed this guide to help you avoid common and costly mistakes, provide valuable retirement

MAKING ADVISED CHOICES RETIREMENT UNDERSTANDING REQUIRED MINIMUM DISTRIBUTIONS PRUDENTIAL CAN HELP Prudential has developed this guide to help you avoid common and costly mistakes, provide valuable retirement

Cross Purchase (Crisscross) Buy-Sell Agreement

Buy-Sell Agreement") One Resource Group 13548 Zubrick Road Roanoke, IN 46783 888-467-6755 Life_Sales@ORGCorp.com Cross Purchase (Crisscross) Buy-Sell Agreement Page 1 of 9, see disclaimer on final page Cross Purchase (Crisscross)

One Resource Group 13548 Zubrick Road Roanoke, IN 46783 888-467-6755 Life_Sales@ORGCorp.com Cross Purchase (Crisscross) Buy-Sell Agreement Page 1 of 9, see disclaimer on final page Cross Purchase (Crisscross)

Learn about distribution options for your employer retirement plan assets. Investor education

Learn about distribution options for your employer retirement plan assets Investor education It s your retirement: Choose wisely As you plan your retirement, you ll need to decide what to do with the

Learn about distribution options for your employer retirement plan assets Investor education It s your retirement: Choose wisely As you plan your retirement, you ll need to decide what to do with the

Establishing a SEP for 2014

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

Published Since 1984 ALSO IN THIS ISSUE Understanding Box 2 (Rollover Contributions) on the 2014 Form 5498, Page 2 Administering An HSA After the HSA Owner Dies, Page 4 Email Guidance - No Authority Exists

RETIREMENT STRATEGIES. Understanding Required Minimum Distributions

RETIREMENT STRATEGIES Understanding Required Minimum Distributions We can help We have developed this guide to help you avoid common and costly mistakes, provide valuable retirement planning information,

RETIREMENT STRATEGIES Understanding Required Minimum Distributions We can help We have developed this guide to help you avoid common and costly mistakes, provide valuable retirement planning information,

Check Book IRA IRA TM. Check Book. Check Book IRA, LLC THE SOLO 401(K) Redmond OR Cave Creek AZ San Antonio TX.

Redmond OR Cave Creek AZ San Antonio TX.") THE SOLO 401(K), LLC Redmond OR Cave Creek AZ San Antonio TX BBB Rating: A+ 1 You know how important it is for a self employed business owner to maintain financial security for yourself and your family.

THE SOLO 401(K), LLC Redmond OR Cave Creek AZ San Antonio TX BBB Rating: A+ 1 You know how important it is for a self employed business owner to maintain financial security for yourself and your family.

AN OPPORTUNITY TO FUND RETIREMENT WITH A ROTH IRA

AN OPPORTUNITY TO FUND RETIREMENT WITH A ROTH IRA Consider Doing Business with Pacific Life VLC0707-0318W AN OPPORTUNITY FOR RETIREMENT SAVINGS If you have funds in an Individual Retirement Account (IRA),

AN OPPORTUNITY TO FUND RETIREMENT WITH A ROTH IRA Consider Doing Business with Pacific Life VLC0707-0318W AN OPPORTUNITY FOR RETIREMENT SAVINGS If you have funds in an Individual Retirement Account (IRA),

take your ira in a new direction yours

take your ira in a new direction yours Self-Directed IRAs: A New World of Investment Opportunities Have you thought about a self-directed IRA as your retirement strategy? Do you know what this is? Many

take your ira in a new direction yours Self-Directed IRAs: A New World of Investment Opportunities Have you thought about a self-directed IRA as your retirement strategy? Do you know what this is? Many

OPERATING A BUSINESS TAX CONSIDERATIONS

OPERATING A BUSINESS TAX CONSIDERATIONS 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 OPERATING A BUSINESS: Tax Considerations Tax accounting

OPERATING A BUSINESS TAX CONSIDERATIONS 2 STARTING A BUSINES RETIREMENT STRATEGIE OPERATING A BUSINES MARRIAG INVESTING TAX SMAR ESTATE PLANNIN 3 OPERATING A BUSINESS: Tax Considerations Tax accounting

SEP UPDATING USE PROTOTYPE OR IRS FORM 5305-SEP?

Published Since 1984 ALSO IN THIS ISSUE What to Do An IRA Customers Wants Help Correcting an Excess Contribution?, Page 2 How Many 5498s Must an Institution Prepare for an Accountholder?, Page 3 IRS Guidance

Published Since 1984 ALSO IN THIS ISSUE What to Do An IRA Customers Wants Help Correcting an Excess Contribution?, Page 2 How Many 5498s Must an Institution Prepare for an Accountholder?, Page 3 IRS Guidance

2018 TAX AND FINANCIAL PLANNING TABLES

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

2018 TAX AND FINANCIAL PLANNING TABLES An overview of important changes, rates, rules and deadlines to assist your 2018 tax planning What you will see in this brochure Important Deadlines 2018 Income Tax

One-Way Buy-Sell Agreement

One Resource Group 13548 Zubrick Road Roanoke, IN 46783 888-467-6755 Life_Sales@ORGCorp.com One-Way Buy-Sell Agreement Page 1 of 8, see disclaimer on final page One-Way Buy-Sell Agreement What is it? Legal

One Resource Group 13548 Zubrick Road Roanoke, IN 46783 888-467-6755 Life_Sales@ORGCorp.com One-Way Buy-Sell Agreement Page 1 of 8, see disclaimer on final page One-Way Buy-Sell Agreement What is it? Legal

Tax-cutting time is ticking away. Review options for accelerating income. Dear Clients and Friends,

Dear Clients and Friends, Taxes are going to be a major issue for the rest of 2012 and for much of 2013. On January 1, 2013, the country faces what Federal Reserve Chairman Ben Bernanke has called a fiscal

Dear Clients and Friends, Taxes are going to be a major issue for the rest of 2012 and for much of 2013. On January 1, 2013, the country faces what Federal Reserve Chairman Ben Bernanke has called a fiscal

1031 Exchange Overview - A Layman s View March 2016

1031 Exchange Overview - A Layman s View March 2016 NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it may omit

1031 Exchange Overview - A Layman s View March 2016 NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it may omit

TRANSAMERICA PREMIER FUNDS. Disclosure Statement and Custodial Agreement for IRAs. Table of Contents

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

2018 Year-End Tax Planning for Individuals

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

2018 Year-End Tax Planning for Individuals There is still time to reduce your 2018 tax bill and plan ahead for 2019 if you act soon. This letter highlights several potential tax-saving opportunities for

Qualified Plans Tax Law Changes KANSAS CITY LIFE INSURANCE COMPANY

Qualified Plans Tax Law Changes KANSAS CITY LIFE INSURANCE COMPANY One of the best ways to save for retirement is with a qualified retirement savings plan. Some plans are employer-sponsored. With others,

Qualified Plans Tax Law Changes KANSAS CITY LIFE INSURANCE COMPANY One of the best ways to save for retirement is with a qualified retirement savings plan. Some plans are employer-sponsored. With others,

PERSONAL FINANCE. individual retirement accounts (IRAs)

") PERSONAL FINANCE individual retirement accounts (IRAs) 1 our purpose To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

PERSONAL FINANCE individual retirement accounts (IRAs) 1 our purpose To lead and inspire actions that improve financial readiness for the military and local community. table of contents The Basics Of IRAs...

President Obama Proposes Radical IRA/Pension Law Changes

Published Since 1984 ALSO IN THIS ISSUE Caution Tax Software Giving People the Wrong Idea About Making a Non-deductible IRA Contribution and Then Converting it, Page 2 Understanding the Impact of Emancipation

Published Since 1984 ALSO IN THIS ISSUE Caution Tax Software Giving People the Wrong Idea About Making a Non-deductible IRA Contribution and Then Converting it, Page 2 Understanding the Impact of Emancipation

Social Security Planning

Stephanie E. Doyle Investment Management Stephanie Doyle Investment Advisor 14111 Bloomingdale Manor Cypress, TX 77429 713-447-5319 investmentmgmt@entouch.net investmentmgt.net Social Security Planning

Stephanie E. Doyle Investment Management Stephanie Doyle Investment Advisor 14111 Bloomingdale Manor Cypress, TX 77429 713-447-5319 investmentmgmt@entouch.net investmentmgt.net Social Security Planning

Law Office Of Keith R. Miles, LLC July 28, 2015

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Traditional IRAs Page 1

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Traditional IRAs Page 1

Rollovers from Employer-Sponsored Retirement Plans

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

Farm Business Arrangement Alternatives

Farm Business Arrangement Alternatives Introduction If the new and established operators decide to farm together after the testing stage, they are ready to move from the beginning farm business arrangement

Farm Business Arrangement Alternatives Introduction If the new and established operators decide to farm together after the testing stage, they are ready to move from the beginning farm business arrangement

2017 INCOME AND PAYROLL TAX RATES

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

2017-2018 Tax Tables A quick reference for income, estate and gift tax information QUICK LINKS: 2017 Income and Payroll Tax Rates 2018 Income and Payroll Tax Rates Corporate Tax Rates Alternative Minimum

It s All About the Business

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

It s All About the Business Planning Strategies Integrated with Life Insurance to Help a Business Owner Accomplish Goals for Retirement, Business Perpetuation, Successful Business Transition, and Estate

Preserving and Transferring IRA Assets

Preserving and Transferring IRA Assets september 2017 The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth potential,

Preserving and Transferring IRA Assets september 2017 The focus on retirement accounts is shifting. Yes, it s still important to make regular contributions to take advantage of tax-deferred growth potential,

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

DISTRIBUTION PLANNING

DISTRIBUTION PLANNING In 5 Easy Steps 2.5 Million Baby Boomers Will Turn Age 70 in 2016 Get the Definitive Guide to RMD Planning at: www.irahelp.com/rmd-guide Calculating the Pro-Rata Rule in 5 Easy Steps

DISTRIBUTION PLANNING In 5 Easy Steps 2.5 Million Baby Boomers Will Turn Age 70 in 2016 Get the Definitive Guide to RMD Planning at: www.irahelp.com/rmd-guide Calculating the Pro-Rata Rule in 5 Easy Steps

2018 IRA Contribution Limit Guide. Information to help you choose the retirement or other savings account that s best for you

2018 IRA Contribution Limit Guide Information to help you choose the retirement or other savings account that s best for you 2018 IRA Contribution Limit Guide Self-directed account annual contribution

2018 IRA Contribution Limit Guide Information to help you choose the retirement or other savings account that s best for you 2018 IRA Contribution Limit Guide Self-directed account annual contribution

29. Retirement 4: Understanding Individual and Small-Business Plans

29. Retirement 4: Understanding Individual and Small-Business Plans Introduction Whether you work for a large or a small company or are self-employed, you need to plan for retirement. This chapter will

29. Retirement 4: Understanding Individual and Small-Business Plans Introduction Whether you work for a large or a small company or are self-employed, you need to plan for retirement. This chapter will

Farm Business Arrangement Alternatives. Introduction. Sole Proprietorships. Partnerships. Farm Business Arrangements Page 1

Farm Business Arrangement Alternatives Philip E. Harris Department of Agricultural and Applied Economics and Center for Dairy Profitability University of Wisconsin-Madison/Extension (Revised 14 January

Farm Business Arrangement Alternatives Philip E. Harris Department of Agricultural and Applied Economics and Center for Dairy Profitability University of Wisconsin-Madison/Extension (Revised 14 January

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

YOUR GUIDE TO IDENTIFYING YOUR TAX RETURN OPPORTUNITIES 2 At Transamerica, we re committed to providing you with the tools and information you need to make the right financial decisions. IRS Form 1040

Call: or Visit us at: LaughlinUSA.com

Welcome We wanted to give our thanks in advance to the readers of this whitepaper who are moved to comment, share, blog or generally discuss the contents herein. We encourage you to reach out and share

Welcome We wanted to give our thanks in advance to the readers of this whitepaper who are moved to comment, share, blog or generally discuss the contents herein. We encourage you to reach out and share

IRS Issues 2013 COLAs. New IRA Contribution Limits for 2013 $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE New IRA Contribution Limits for 2013 $5,500 and $6,500 IRA Contribution Deductibility Charts for 2012 and 2013, Page 2 Roth IRA Contribution Charts for 2012 and

Published Since 1984 ALSO IN THIS ISSUE New IRA Contribution Limits for 2013 $5,500 and $6,500 IRA Contribution Deductibility Charts for 2012 and 2013, Page 2 Roth IRA Contribution Charts for 2012 and

1031 Exchange Overview

1031 Exchange Overview NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it omits rules and considerations that could

1031 Exchange Overview NOTE: This paper is a basic overview of IRC section 1031 tax deferred exchanges. It is not intended to be a guide to such an exchange, as it omits rules and considerations that could

IRAs. Your Retirement Advisor

Your Retirement Advisor 508-798-5115 lynnt@yourretirementadvisor.com www.yourretirementadvisor.com IRAs March, 2017 Page 1 of 8, see disclaimer on final page Both traditional and Roth IRAs feature tax-sheltered

Your Retirement Advisor 508-798-5115 lynnt@yourretirementadvisor.com www.yourretirementadvisor.com IRAs March, 2017 Page 1 of 8, see disclaimer on final page Both traditional and Roth IRAs feature tax-sheltered

WHICH IRA IS RIGHT FOR YOU?

WHICH IRA IS RIGHT FOR YOU? WHICH IRA IS RIGHT FOR YOU? 1 Saving for retirement in a self-directed Individual Retirement Account (IRA) comes with many advantages: access to a broad variety of investment

WHICH IRA IS RIGHT FOR YOU? WHICH IRA IS RIGHT FOR YOU? 1 Saving for retirement in a self-directed Individual Retirement Account (IRA) comes with many advantages: access to a broad variety of investment

Expanding Retirement Savings Opportunities with Roth Accounts

Defined Contribution Plans Expanding Retirement Savings Opportunities with Roth Accounts A growing number of plan sponsors are finding that adding Roth features to their retirement plan helps provide the

Defined Contribution Plans Expanding Retirement Savings Opportunities with Roth Accounts A growing number of plan sponsors are finding that adding Roth features to their retirement plan helps provide the

INDIVIDUAL 401(k) PLAN

PLAN") INDIVIDUAL 401(k) PLAN Guidebook CONTENTS WELCOME. When you commit to saving for retirement, you want to invest with a company that shares your dedication to hard work and results. At T. Rowe Price, we

INDIVIDUAL 401(k) PLAN Guidebook CONTENTS WELCOME. When you commit to saving for retirement, you want to invest with a company that shares your dedication to hard work and results. At T. Rowe Price, we

Self-Directed Investing Overview. A guide to Equity Trust accounts

Self-Directed Investing Overview A guide to Equity Trust accounts Contents You Have Options for Investing in Your Future 4 Should You Consider an IRA? 5 Nearly Endless Investment Options 7 Individual

Self-Directed Investing Overview A guide to Equity Trust accounts Contents You Have Options for Investing in Your Future 4 Should You Consider an IRA? 5 Nearly Endless Investment Options 7 Individual

Franklin Templeton IRA

Investor s Guide Franklin Templeton IRA Traditional IRA Roth IRA Whether you are just starting to save or entering retirement, an IRA can be an important part of a sound financial strategy to meet your

Investor s Guide Franklin Templeton IRA Traditional IRA Roth IRA Whether you are just starting to save or entering retirement, an IRA can be an important part of a sound financial strategy to meet your

RETIREMENT STRATEGIES. Your IRA Planning for Tomorrow Today

RETIREMENT STRATEGIES Your IRA Planning for Tomorrow Today Achieving a comfortable future requires more from you more planning and more resources than in the past. Investment Products: ARE NOT INSURED

RETIREMENT STRATEGIES Your IRA Planning for Tomorrow Today Achieving a comfortable future requires more from you more planning and more resources than in the past. Investment Products: ARE NOT INSURED

RMD Impact When a Surviving Spouse Elects to Treat the Deceased Spouse s IRA as Their Own

Published Since 1984 ALSO IN THIS ISSUE HSA Contribution Limits for Domestic Partners and Other Unmarried Individuals Versus Married Individuals, Page 3 Handling Excess IRA Contributions for 2008 and 2009,

Published Since 1984 ALSO IN THIS ISSUE HSA Contribution Limits for Domestic Partners and Other Unmarried Individuals Versus Married Individuals, Page 3 Handling Excess IRA Contributions for 2008 and 2009,

THE EVOLUTION OF THE ROTH 401(K)

") THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

THE EVOLUTION OF THE ROTH 401(K) I. WHAT IS A ROTH 401(K)? A. Legislative History. 1. The Economic Growth and Tax Relief Reconciliation Act of 2001 ( EGTRRA ) authorized the establishment of Roth 401(k)

Year-End Tax Moves for Income Tax Rates for 2015

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Year-End Tax Moves for 2015 One of our major goals is to help our clients identify opportunities that coordinate tax reduction with their investment portfolios. In order to achieve this goal, we stay current

Circumstances in Which an IRA May Owe Taxes 1

Circumstances in Which an IRA May Owe Taxes 1 By: H. Quincy Long, Phone: 281-492-3434 Attorney and President of Fax: 281-646-9701 Entrust Retirement Services, Inc. Toll-Free: 800-320-5950 17171 Park Row,

Circumstances in Which an IRA May Owe Taxes 1 By: H. Quincy Long, Phone: 281-492-3434 Attorney and President of Fax: 281-646-9701 Entrust Retirement Services, Inc. Toll-Free: 800-320-5950 17171 Park Row,

No Direct Rollovers From One to Another IRA

Published Since 1984 ALSO IN THIS ISSUE More Than a Check is Needed for an IRA Transfer, Page 2 BE CAREFUL The RMD Must be Completed Before Any Roth IRA Conversion, Page 3 IRA Contribution Due Dates, Page

Published Since 1984 ALSO IN THIS ISSUE More Than a Check is Needed for an IRA Transfer, Page 2 BE CAREFUL The RMD Must be Completed Before Any Roth IRA Conversion, Page 3 IRA Contribution Due Dates, Page

Self-Directed Real Estate 101. How Does Real Estate Investing in an IRA Really Work?

Self-Directed Real Estate 101 How Does Real Estate Investing in an IRA Really Work? Table of Contents Part I: Establishing an Account with a Self-Directed IRA Custodian Part II: Funding a New Self-Directed

Self-Directed Real Estate 101 How Does Real Estate Investing in an IRA Really Work? Table of Contents Part I: Establishing an Account with a Self-Directed IRA Custodian Part II: Funding a New Self-Directed

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2017, September 20, 2017. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2017, September 20, 2017. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Are IRA Amendments Required For ?

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Published Since 1984 ALSO IN THIS ISSUE Administering Beneficiary/Inherited IRAs, Page 2 IRS Extends Transition Relief For an IRA Custodian s Payments to a State s Unclaimed Property Fund, Page 2 Understanding

Cleveland Clinic Akron General Retirement Program

Cleveland Clinic Akron General Retirement Program A good thing is getting better. New Fee Structure for All Cleveland Clinic/Akron General Plans New Option to Save Above the IRS Limits in your Matched

Cleveland Clinic Akron General Retirement Program A good thing is getting better. New Fee Structure for All Cleveland Clinic/Akron General Plans New Option to Save Above the IRS Limits in your Matched

IRA Contribution Limits for 2018 Unchanged at $5,500 and $6,500; 401(k) Limits Do Change

Limits Do Change") Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Limits for 2018 Page 1 IRA Contribution Deductibility Charts 2017 and 2018, Page 2 Roth IRA Contribution Charts for 2017 and 2018, Page 3 SEP and

Converting or Rolling Over Traditional IRAs to Roth IRAs

Cole FInancial Consulting Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Converting or Rolling Over Traditional IRAs

Cole FInancial Consulting Jennifer J. Cole, CFA, MBA P.O. Box 1109 Sandia Park, NM 505-286-7915 JCole@ColeFinancialConsulting.com ColeFinancialConsulting.com Converting or Rolling Over Traditional IRAs

Anyone may so arrange his affairs that his taxes shall be so low as possible;

Anyone may so arrange his affairs that his taxes shall be so low as possible; he is not bound to choose the pattern which will best pay the treasury; there is not even a patriotic duty to increase one

Anyone may so arrange his affairs that his taxes shall be so low as possible; he is not bound to choose the pattern which will best pay the treasury; there is not even a patriotic duty to increase one

Before we get to specific suggestions, here are two important considerations to keep in mind.

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

To Our Clients and Friends As we get closer to the end of yet another year, it s time to tie up the loose ends and implement tax saving strategies. With the fate of many of the long favored tax breaks

Rollover IRAs. Consider the advantages of consolidating your retirement savings PROOF 3

Rollover IRAs Consider the advantages of consolidating your retirement savings O O R P 3 F Consider the Advantages of Consolidating Your Retirement Savings If you have changed jobs, left the workforce

Rollover IRAs Consider the advantages of consolidating your retirement savings O O R P 3 F Consider the Advantages of Consolidating Your Retirement Savings If you have changed jobs, left the workforce

Law Offices of Bradley J. Frigon 6500 S. Quebec St. Suite 330 Englewood, CO

2018 National Conference on Special Needs Planning and Special Needs Trusts Tax Reform and Year End Tax Planning for Self Settled and Third Party Trusts Bradley J. Frigon October 18, 2018 Law Offices of

2018 National Conference on Special Needs Planning and Special Needs Trusts Tax Reform and Year End Tax Planning for Self Settled and Third Party Trusts Bradley J. Frigon October 18, 2018 Law Offices of

Financial Advisor. Understanding IRAs. January 15, 2019 Page 1 of 5, see disclaimer on final page

Financial Advisor Understanding IRAs Page 1 of 5, see disclaimer on final page Understanding IRAs An individual retirement arrangement (IRA) is a personal savings plan that offers specific tax benefits.

Financial Advisor Understanding IRAs Page 1 of 5, see disclaimer on final page Understanding IRAs An individual retirement arrangement (IRA) is a personal savings plan that offers specific tax benefits.

Death Benefit Distribution Claim Form Spousal Beneficiary

Death Benefit Distribution Claim Form Spousal Beneficiary READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF THE PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF QUALIFIED JOINT AND 50% CONTINGENT

Death Benefit Distribution Claim Form Spousal Beneficiary READ THE ATTACHED IRS SPECIAL TAX NOTICE: IF THE PLAN ALLOWS FOR AN ANNUITY OPTION, READ THE WRITTEN EXPLANATION OF QUALIFIED JOINT AND 50% CONTINGENT

Caution: Special rules apply to certain distributions to reservists and national guardsmen called to active duty after September 11, 2001.

LPL Financial Sims & Karr Financial Solutions Roger C. Sims Jason R Karr, Alex M. Means 304 North Main Street Greer, SC 29650 864-879-0337 simsandkarr@lpl.com www.simskarr.com Roth IRAs Page 1 of 13, see

LPL Financial Sims & Karr Financial Solutions Roger C. Sims Jason R Karr, Alex M. Means 304 North Main Street Greer, SC 29650 864-879-0337 simsandkarr@lpl.com www.simskarr.com Roth IRAs Page 1 of 13, see

Taking Distributions from. Tax-Deferred Retirement. Savings Plans

Taking Distributions from Tax-Deferred Retirement Savings Plans Putting money into an employer s retirement plan is just the first step toward financial security in retirement. How you withdraw the money

Taking Distributions from Tax-Deferred Retirement Savings Plans Putting money into an employer s retirement plan is just the first step toward financial security in retirement. How you withdraw the money

Solo 401k Contributions

Solo 401k Contributions In this guide, you'll learn how to calculate your Solo 401k contributions and how to document those contributions for your CPA and/or tax preparer. DISCLAIMER: Please note that

Solo 401k Contributions In this guide, you'll learn how to calculate your Solo 401k contributions and how to document those contributions for your CPA and/or tax preparer. DISCLAIMER: Please note that

Tax and Personal Finance. Brandon Horton

Disclaimer: The information in this document is not legal advice. This document is for educational purposes only and provides a general overview of various tax- and finance-related topics. It is not a

Disclaimer: The information in this document is not legal advice. This document is for educational purposes only and provides a general overview of various tax- and finance-related topics. It is not a

Copyright 2008 Maurice Glazer

Tax Considerations for the Global Entrepreneur / Investor The Glazer Group Maurice M. Glazer Worked in the industry since 1960 Tax and Accounting Specialist Speaker at numerous corporate and organization

Tax Considerations for the Global Entrepreneur / Investor The Glazer Group Maurice M. Glazer Worked in the industry since 1960 Tax and Accounting Specialist Speaker at numerous corporate and organization

SOLO(CB) RETIREMENT PLAN SPECIALISTS

RETIREMENT PLAN SPECIALISTS") SOLO(CB) RETIREMENT PLAN SPECIALISTS A Cash Balance Plan for the Self-Employed WHAT IS A SOLO(CB)? A Solo(cb) plan (a one-participant cash balance plan) is a cash balance defined benefit plan created specifically

SOLO(CB) RETIREMENT PLAN SPECIALISTS A Cash Balance Plan for the Self-Employed WHAT IS A SOLO(CB)? A Solo(cb) plan (a one-participant cash balance plan) is a cash balance defined benefit plan created specifically

DISCLOSURE STATEMENTS AND CUSTODIAL ACCOUNT AGREEMENT

Traditional and Roth Individual Retirement Account Informational Booklet DISCLOSURE STATEMENTS AND CUSTODIAL ACCOUNT AGREEMENT 15810M REV 01-18 TABLE OF CONTENTS THE LIVEWELL MUTUAL FUND TRADITIONAL INDIVIDUAL

Traditional and Roth Individual Retirement Account Informational Booklet DISCLOSURE STATEMENTS AND CUSTODIAL ACCOUNT AGREEMENT 15810M REV 01-18 TABLE OF CONTENTS THE LIVEWELL MUTUAL FUND TRADITIONAL INDIVIDUAL

UNDERWRITING THE SELF-EMPLOYED BORROWER

UNDERWRITING THE SELF-EMPLOYED BORROWER 2014 www.archmicu.com 2015 Arch Mortgage Insurance Company 114-11-14-CU Table of Contents Introduction Automated Underwriting & the Self-Employed Borrower...1 Basic

UNDERWRITING THE SELF-EMPLOYED BORROWER 2014 www.archmicu.com 2015 Arch Mortgage Insurance Company 114-11-14-CU Table of Contents Introduction Automated Underwriting & the Self-Employed Borrower...1 Basic

Tax Basics for Small Business

Tax Basics for Small Business 19 th Edition Attorney Frederick W. Daily Introduction... 1 Chapter 1 Tax Basics... 3 Learning Objectives... 3 Introduction... 3 How Tax Law Is Made and Administered: The

Tax Basics for Small Business 19 th Edition Attorney Frederick W. Daily Introduction... 1 Chapter 1 Tax Basics... 3 Learning Objectives... 3 Introduction... 3 How Tax Law Is Made and Administered: The

AMERUS LIFE INSURANCE COMPANY

AMERUS LIFE INSURANCE COMPANY IRA DISCLOSURE STATEMENT INTRODUCTION This Individual Retirement Annuity ("IRA") is an annuity contract issued by AmerUs Life Insurance Company ("AMERUS") to fund an individual's

AMERUS LIFE INSURANCE COMPANY IRA DISCLOSURE STATEMENT INTRODUCTION This Individual Retirement Annuity ("IRA") is an annuity contract issued by AmerUs Life Insurance Company ("AMERUS") to fund an individual's

impact March/April 2010 Don t lose out on rental real estate losses When can you write off bad business debts?

tax March/April 2010 impact Don t lose out on rental real estate losses When can you write off bad business debts? Home is where the tax savings are How joint home purchases can reduce estate taxes Tax

tax March/April 2010 impact Don t lose out on rental real estate losses When can you write off bad business debts? Home is where the tax savings are How joint home purchases can reduce estate taxes Tax

RETIREMENT STRATEGIES

RETIREMENT STRATEGIES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel And Entertainment

RETIREMENT STRATEGIES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel And Entertainment

IRS Issues 2014 IRA/Pension Limits. IRA Contribution Limits for 2014 Unchanged at $5,500 and $6,500 ALSO IN THIS ISSUE

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

Published Since 1984 ALSO IN THIS ISSUE IRA Contribution Deductibility Charts 2013 and 2014, Page 2 Roth IRA Contribution Charts for 2013 and 2014, Page 3 SEP and SIMPLE Limits, Page 3 Saver s Credit Limits

2013 Retirement Plan Summary

Understanding the differences among retirement plan alternatives 2013 Retirement Plan Summary If you re establishing a new retirement plan, selecting the appropriate design is the first step in providing

Understanding the differences among retirement plan alternatives 2013 Retirement Plan Summary If you re establishing a new retirement plan, selecting the appropriate design is the first step in providing

The Answers to 46 Frequently Asked Questions about Retirement

The Answers to 46 Frequently Asked Questions about Retirement 1. Where will my retirement income come from? According to the Social Security Administration, many retirees receive income from four main

The Answers to 46 Frequently Asked Questions about Retirement 1. Where will my retirement income come from? According to the Social Security Administration, many retirees receive income from four main

Helpful Information for Filing 2018 Income Taxes and Proactive Tax Planning for 2019

Helpful Information for Filing 2018 Income Taxes and Proactive Tax Planning for 2019 Tax planning should always be a key focus when reviewing your personal financial situation. One of our goals as financial

Helpful Information for Filing 2018 Income Taxes and Proactive Tax Planning for 2019 Tax planning should always be a key focus when reviewing your personal financial situation. One of our goals as financial

GUIDE TO SMALL BUSINESS RETIREMENT PLANS

GUIDE TO SMALL BUSINESS RETIREMENT PLANS By offering your employees a quality retirement plan, it helps show you care about their financial future. Once you decide to offer a retirement plan to your employees,

GUIDE TO SMALL BUSINESS RETIREMENT PLANS By offering your employees a quality retirement plan, it helps show you care about their financial future. Once you decide to offer a retirement plan to your employees,

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

Self-Directed Real Estate 101. How Does Real Estate Investing in an IRA Really Work?

Self-Directed Real Estate 101 How Does Real Estate Investing in an IRA Really Work? Table of Contents Part I: Establishing an Account with a Self-Directed IRA Custodian 3 Part II: Funding a New Self-Directed

Self-Directed Real Estate 101 How Does Real Estate Investing in an IRA Really Work? Table of Contents Part I: Establishing an Account with a Self-Directed IRA Custodian 3 Part II: Funding a New Self-Directed

Chapter Seven LEARNING OBJECTIVES OVERVIEW. 7.1 Taxation of Personal Life Insurance Premiums. Cash Values

Chapter Seven Federal Tax Considerations and Retirement Plans LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

Chapter Seven Federal Tax Considerations and Retirement Plans LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

Voya Select Advantage IRA

Voya Select Advantage IRA Mutal Fund Custodial Account Maxwell An Investor s Best Friend Securities and advisory services offered through SagePoint Financial, Inc., member FINRA/SIPC. Insurance offered

Voya Select Advantage IRA Mutal Fund Custodial Account Maxwell An Investor s Best Friend Securities and advisory services offered through SagePoint Financial, Inc., member FINRA/SIPC. Insurance offered

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS LECTURE NOTES

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS 10.1 FORMS OF DOING BUSINESS LECTURE NOTES 1. Legal Forms. Business entities can be organized into the following principal legal forms. Sole proprietorship.

CHAPTER 10 COMPARATIVE FORMS OF DOING BUSINESS 10.1 FORMS OF DOING BUSINESS LECTURE NOTES 1. Legal Forms. Business entities can be organized into the following principal legal forms. Sole proprietorship.

2017 Tax Update. Class Notes Tax Update Class Notes.indb 1 12/30/2016 8:56:12 AM

2017 Tax Update Class Notes 2017 Tax Update Class Notes.indb 1 12/30/2016 8:56:12 AM At press time, this edition contains the most complete and accurate information currently available. Owing to the nature

2017 Tax Update Class Notes 2017 Tax Update Class Notes.indb 1 12/30/2016 8:56:12 AM At press time, this edition contains the most complete and accurate information currently available. Owing to the nature

are pretax deferrals or roth contributions better for your employees?

The Rules of Roth are pretax deferrals or roth contributions better for your employees? INSIDE: A BRIEF HISTORY OF ROTH CREATING AN ACTION PLAN ROTH CHECKLIST Each of your workers has a unique story, and

The Rules of Roth are pretax deferrals or roth contributions better for your employees? INSIDE: A BRIEF HISTORY OF ROTH CREATING AN ACTION PLAN ROTH CHECKLIST Each of your workers has a unique story, and

A GUIDE TO PREPARING FOR RETIREMENT

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

A GUIDE TO PREPARING FOR RETIREMENT MaineSaves A Guide to Preparing for Retirement MaineSaves, the State of Maine s voluntary retirement savings plan, is designed to help you move forward on your journey

Single. Retirement Plan A Guide for Owner-Only Businesses. Retirement

Retirement Single KSM Retirement Plan A Guide for Owner-Only Businesses Not FDIC Insured May Lose Value Not Bank Guaranteed OppenheimerFunds is not undertaking to provide impartial investment advice or

Retirement Single KSM Retirement Plan A Guide for Owner-Only Businesses Not FDIC Insured May Lose Value Not Bank Guaranteed OppenheimerFunds is not undertaking to provide impartial investment advice or

11 Biggest Rollover Blunders (and How to Avoid Them)

") 11 Biggest Rollover Blunders (and How to Avoid Them) Rolling over your funds for retirement presents a number of opportunities for error. Having a set of guidelines and preventive touch points is necessary

11 Biggest Rollover Blunders (and How to Avoid Them) Rolling over your funds for retirement presents a number of opportunities for error. Having a set of guidelines and preventive touch points is necessary

BONDI & Co. LLC CERTIFIED PUBLIC ACCOUNTANTS MANAGEMENT CONSULTANTS

tax May/June 2011 IMPACT Work-related education When can you deduct your expenses? The icing on the cake A QPRT allows you to save estate taxes on your home while still living in it How to maximize deductions

tax May/June 2011 IMPACT Work-related education When can you deduct your expenses? The icing on the cake A QPRT allows you to save estate taxes on your home while still living in it How to maximize deductions

Choosing a Retirement Plan for Your Business

February 2017 Choosing a Retirement Plan for Your Business introduction Table of Contents Building Your Retirement Starting and maintaining a retirement plan for your business can be easier than you think

February 2017 Choosing a Retirement Plan for Your Business introduction Table of Contents Building Your Retirement Starting and maintaining a retirement plan for your business can be easier than you think

chart RETIREMENT PLANS 8 RETIREMENT PLAN BENEFITS AVAILABLE RETIREMENT PLANS Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

Broker. Federal Income Tax Laws Affecting Real Estate. Chapter 14. Copyright Gold Coast Schools 1

Broker Chapter 14 Federal Income Tax Laws Affecting Real Estate Copyright Gold Coast Schools 1 Learning Objectives List the 2 principal tax deductions available to homeowners List the 2 types of home loans

Broker Chapter 14 Federal Income Tax Laws Affecting Real Estate Copyright Gold Coast Schools 1 Learning Objectives List the 2 principal tax deductions available to homeowners List the 2 types of home loans

Year-End Tax Planning Letter

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

Client Letter: Year-End Tax Planning for 2018 (Individuals)

") Client Letter: Year-End Tax Planning for 2018 (Individuals) Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2018 tax bill. Unlike

Client Letter: Year-End Tax Planning for 2018 (Individuals) Just as the daylight hours are getting shorter, so is the time for fine tuning any last-minute strategies to lower your 2018 tax bill. Unlike

SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan

Profit Sharing Plan") SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

SUMMARY PLAN DESCRIPTION Standard Textile 401(k) Profit Sharing Plan This information is not intended to be a substitute for specific individualized tax, legal, or investment planning advice. Where specific

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

EXPLORING QUALIFIED RETIREMENT PLANS. What you need to know to decide which plan is right for your business.

EXPLORING QUALIFIED RETIREMENT PLANS What you need to know to decide which plan is right for your business. 2 EXPLORING QUALIFIED RETIREMENT PLANS For many businesses, offering a qualified retirement plan

EXPLORING QUALIFIED RETIREMENT PLANS What you need to know to decide which plan is right for your business. 2 EXPLORING QUALIFIED RETIREMENT PLANS For many businesses, offering a qualified retirement plan

State Street Bank and Trust Company Universal IRA Information Kit

STATE STREET BANK AND TRUST COMPANY TRADITIONAL AND ROTH IRA INFORMATION KIT IMPORTANT NOTICE This kit describes the Traditional and Roth IRA rules as modified by the Economic Growth and Tax Relief Reconciliation

STATE STREET BANK AND TRUST COMPANY TRADITIONAL AND ROTH IRA INFORMATION KIT IMPORTANT NOTICE This kit describes the Traditional and Roth IRA rules as modified by the Economic Growth and Tax Relief Reconciliation