Lewis Rice Presents: Advanced Estate Planning Techniques for 2016 and Beyond. September 27, 2016

|

|

|

- Asher Eaton

- 5 years ago

- Views:

Transcription

1 Lewis Rice Presents: Advanced Estate Planning Techniques for 2016 and Beyond September 27, 2016

2 The New Section 2704(b) Proposed Regulations: Insights & Planning Implications Jaime R. Mendez, Michael D. Mulligan, Brian J. Figueroa and Rachel M. Hirshberg September 27, 2016

3 History of the 2704 Regulations

4 The 2704(b) Proposed Regulations

5 The Proposed Regulations IRC 2704(b) Section : Transfers subject to applicable restrictions NEW Section : Transfers subject to disregarded restrictions Section : Definition of controlled entity expanded Section : Lapse of certain rights Section : Effective Date

6 2704(b) Transfers Subject to Applicable Restrictions (1) Any applicable restriction shall be disregarded in determining the value of a transferred interest. (2) An applicable restriction is any restriction: (A) which effectively limits the ability of the corporation or partnership to liquidate, and (B) which the transferor or any member of the transferor s family, either alone or collectively, has the right remove, in whole or in part, after such transfer..... (4) The Secretary may by regulations provide that other restrictions shall be disregarded in determining the value of the transfer of any interest in a corporation or partnership to a member of the transferor s family if such restriction has the effect of reducing the value of the transferred interest for purposes of this subtitle but does not ultimately reduce the value of such interest to the transferee.

7 Proposed Reg Disregarded Restrictions When a partnership interest is transferred to a family member, certain restrictions will be disregarded in valuing the interest, for transfer tax purposes. A disregarded restriction is a restriction that: limits the ability of an interest holder to compel liquidation or redemption of that interest on no more than six months notice for cash or property equal to at least minimum value. Prop. Reg (b)(1)(i)-(iii).

8 Disregarded Restrictions Minimum Value Minimum Value is an interest s pro rata share of the net fair market value of the entity s assets. Minimum Value = (fair market value of entity s assets entity s debts*) x share represented by interest. Prop. Reg (b)(1)(ii). *Only reduced by entity s debts to the extent that the debts would be deductible under IRC 2053 if they had been claims against a decedent s estate.

9 Disregarded Restrictions Cash or Property Interest holder must receive cash or property in exchange for his interest Interest may not be redeemed for an intra-family promissory note (i.e, a note issued by an entity, its owners, or a related person), unless: Entity is engaged in an active trade or business; At least 60% of the entity s value consists of non-passive trade/business assets; Liquidation proceeds (i.e., payments on the note) are not attributable to 6166(b)(9)(B) passive assets; The note is adequately secured; The note requires periodic payments on a non-deferred basis; The note is issued at market interest rates (not AFRs); and, The note has a fair market value on the date of liquidation equal to the liquidation proceeds.

10 Disregarded Restrictions Family Control A restriction is only a disregarded restriction if, after the transfer, the restriction will lapse or can be removed by the transferor or any member of the transferor s family. An interest held by a nonfamily member that gives the nonfamily member the power to prevent the removal of the restriction is also disregarded, unless the interest: Has been held by that nonfamily member for at least 3 years; Represents at least a 10% interest in the entity; Represents at least a 20% interest in the entity, when aggregated with other nonfamily members; and, Can be redeemed by the nonfamily holder on no more than 6 months notice, for cash or other property.

11 Exceptions Restrictions that Will Not be Disregarded Commercially reasonable restrictions imposed by unrelated investors. Restrictions that are mandatory and unavoidable under federal or state law. This includes a limitation on the ability to liquidate the entity (in whole or in part) that is more restrictive than the limitations that would apply under the state law generally applicable to the entity in the absence of the restriction. Safe Harbor: No restriction will be disregarded if every holder of an interest in the entity has the power to redeem his/her interest on no more than 6 months notice, for cash or other property. Not a deemed put.

12 Effect of Disregarded Restriction If a restriction is disregarded under Section (b)(1), the fair market value of the transferred interest is determined under generally applicable valuation principles, including any appropriate discounts or premiums, as if the disregarded restriction did not exist.

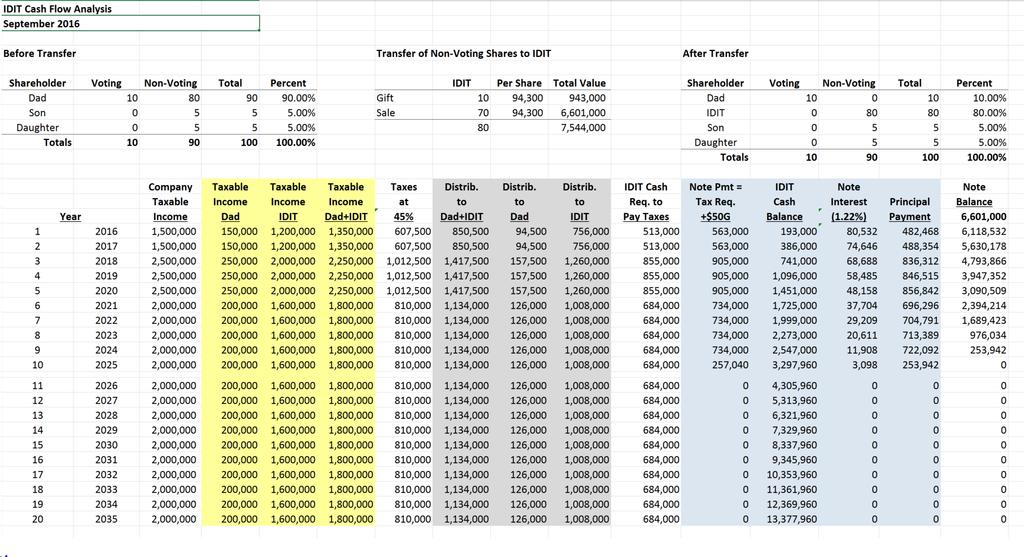

13 Controlled Entity Expanded Definition Current regulations apply to corporations and partnerships. Proposed regulations stat that 2704 applies to corporations, partnerships, LLCs and any other entity or arrangement that is a business entity within the meaning of [Treas. Reg.] (a).

14 Lapse of Certain Rights Expanded Meaning of Voting Right Assignee Interests Proposed regulations clarify that the transfer of a partnership interest to an assignee that neither has nor may exercise the voting or liquidation rights of a partner is a lapse of the voting and liquidation rights associated with the transferred interest. Expanded Meaning of Voting Right Proposed regulations provide that In the case of a limited liability company, the right of a member to participate in company management is a voting right.

15 Lapse of Certain Rights New Three-Year Rule Lapse of voting or liquidation right in family-owned entity is transfer by individual who held right if entity is controlled by transferor and members of transferor s family immediately before and after lapse. Family control includes all descendants of parents of transferor or transferor s spouse. But does not apply if rights with respect to transferred interest are not restricted or eliminated. Reg (c)(1). Proposed regulations would deny exception for transfers occurring within three years before transferor s death [described in preamble as bright-line test ]. The lapse is treated as a lapse occurring on the transferor s date of death, includible in the gross estate pursuant to section 2704(a).

16 Effective Dates Provisions of proposed regulations applicable to voting and liquidation rights are proposed to apply to rights and restrictions created after October 8, 1990, but only to transfers occurring after date regulations are published as final. New rules for Disregarding Certain Restrictions on Redemption or Liquidation (Prop. Reg ) will not take effect until 30 days after date regulations are published as final. See 5 U.S.C. 553(d) (provision of Administrative Procedure Act rule applicable to legislative regulations). Public comments due November 2. Public hearing to be held on December 1. Regulations could be finalized any time thereafter.

17

18 Practical Considerations in Sale of Business Entity to IDIT Kimberly B. McDermott and Marian V. Bo Mehan September 27, 2016

19 Structure of Sale Transaction

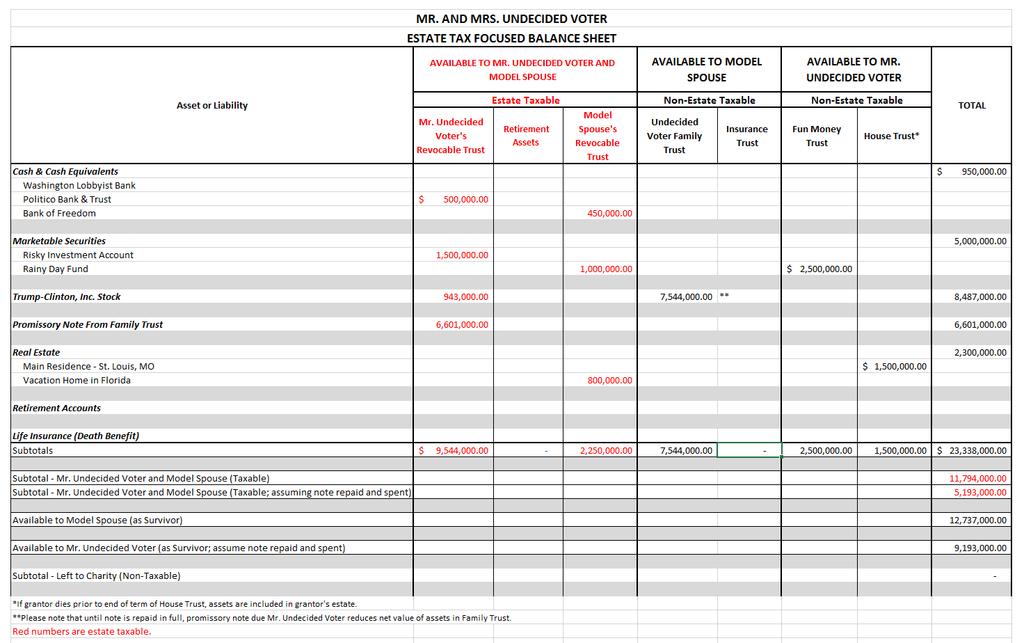

20 MR. AND MRS. UNDECIDED VOTER Gift from Mr. Undecided Voter 10% Non-Voting Stock Fair Market Value: $943,000 TRUMP-CLINTON, INC. (assuming $945,000 distributions annually, of which $47,250 is distributed to two children who own 5% and balance as follows) 80% of distribution ($756,000) Sold by Mr. Undecided Voter 70% Non-Voting Stock Fair Market Value: $6,601,000 9 year promissory note The Undecided Voter Family Trust Mr. Undecided Voter, sole Trustee 80% Non-Voting Stock in Trump-Clinton, Inc. Fair Market Value: $7,544,000 Note Due to Mr. Undecided Voter: $6,601,000 Annual Interest at 1.22% - $80, % of distribution ($94,500) Because the trust is a grantor trust to Mr. Undecided Voter, there will be no income or capital gains tax consequence to the payment of interest, whether in cash or in kind. Mr. Undecided Voter may also forgive any unpaid interest, as well as principal, if he wishes, up to the annual exclusion amount available to Mr. Undecided Voter (and, if she is agreeable, Mrs. Model Spouse), with no gift tax consequences. Up to $756,000 note payment Mr. Undecided Voter 1. Mr. Undecided Voter owned 90% of the Company prior to the transaction 10% (all) of the voting stock and 80% of the non-voting stock. Each of his two children owns 5% of the non-voting stock prior to and after the transaction. 2. An appraisal was obtained, which resulted in the value of 1% of non-voting stock equaling $94,300.

21 Intentionally Defective Irrevocable Trust Grantor trust during Mr. Undecided Voter s lifetime Permissible S corporation shareholder during Mr. Undecided Voter s lifetime After Mr. Undecided Voter s death, IDIT drafted to qualify as ESBT or QSST During Mr. Undecided Voter s life, he pays income taxes on assets of IDIT, increasing assets passing to IDIT beneficiaries Assets sold or gifted to IDIT without recognizing taxable gain Assets sold or gifted to IDIT no longer included in Mr. Undecided Voter s estate Mr. Undecided Voter cannot be a beneficiary but spouse can be beneficiary Mr. Undecided Voter may act as Trustee (unless voting stock is owned by IDIT or Mr. Undecided Voter transfers stock possessing at least 20% of total combined voting power of all classes of stock to IDIT)

22 Ways Grantor is Protected Financially Number 1: Repayment of the Promissory Note The promissory note given by the IDIT can be structured to provide regular payments of interest or interest and principal If cash flow is insufficient to repay the note, renegotiate the terms of the note. Document the renegotiation with an amended and restated promissory note using the then current Applicable Federal Rate

23 Ways Grantor is Protected Financially Number 2: Swap Assets Mr. Undecided Voter can swap liquid assets owned by the IDIT for illiquid assets owned by the Mr. Undecided Voter if of equivalent value Use power to swap assets to move low basis assets from the IDIT to Mr. Undecided Voter s estate in exchange for higher basis assets Written memorialization of swap and gift tax return

24 Ways Grantor is Protected Financially Number 3: Spouse as Beneficiary of IDIT Model Spouse could be named as a beneficiary of the IDIT at the outset If Mr. Undecided Voter is uncomfortable naming Model Spouse as an IDIT beneficiary at the outset, a third party (not Mr. Undecided Voter, Model Spouse or any descendant) can be given the ability to add Model Spouse as a beneficiary in the future Once promissory note is repaid, if Model Spouse is a beneficiary and living, Trustees of IDIT can make distributions to Model Spouse from the IDIT for health, support and maintenance (best to use other estate taxable assets first)

25 Ways Grantor is Protected Financially Number 4: Borrow If Model Spouse is not beneficiary of IDIT and/or promissory note given in connection with the sale has been fully repaid, Mr. Undecided Voter can borrow funds from the IDIT Document with promissory note using at least Applicable Federal Rate for interest, which is typically lower than market rate Required annual interest payments may evidence a loan that more closely resembles a third party loan

26 Ways Grantor is Protected Financially Number 5: Grantor Trust Status Turn off grantor trust status IDIT must pay income taxes on assets owned by IDIT Model Spouse can no longer be beneficiary of IDIT Mr. Undecided Voter can no longer have power to borrow from IDIT Neither Mr. Undecided Voter nor Model Spouse can serve as Trustee once grantor trust status is switched off

27

28

29

30 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Matthew J. Madsen and Joel L. Weeks September 27, 2016

31 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate

32 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Key Financial Data Fair Market Value Less Commission 20,000,000 Debt on Contributed Property 9,300,000 Total Accumulated Depreciation 4,700,000 Total Adjusted Basis in Contributed Property 2,800,000 Estimated Tax Rate on Gain Subject to Depreciation Recapture 33.1% Estimated Tax Rate on Gain in Excess of Depreciation Recapture 28.4% Estimated Ordinary Tax Rate 43.2%

33 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate A Few Key Tax Issues for Donor FMV deduction based on value of real estate Qualified Appraisal Rules What about discounts for real estate owned by an LLC or other entity? Put option as a consideration Mismatch with estate/gift values under proposed 2704 regs. Deduction reduces income at top brackets and works it way down Deduction excess over AGI limits carried over up to 5 years and unused carryover expires with the donor

34 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate A Few Key Tax Issues for Donor Relief of Indebtedness = Bargain Sale Apportionment of basis to sale and charitable portions Adjusted basis allocated to sale in example is $1,302,000 Taxation of sale portion will trigger recapture of depreciation at a special 25% rate and depreciation in excess of straight-line depreciation will reduce the charitable contribution deduction Depreciation recapture allocated to sale in example is $2,185,500 How Late is Too Late Assignment of Income Doctrine Sale of Property by Charity within 3 Years (special reporting on IRS Form 8282)

35 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate A Few Key Tax Issues for the Charity Debt Raises Issue of Unrelated Business Taxable Income Interesting UBIT exception for certain debts IRC Sec. 514(c)(2)(B) UBIT and impact on support test for publicly supported charities UBIT and impact on 501(c)(3) status of any charitable organization Excess Business Holdings Issues for Real Estate Owned in an Entity if Charity is a Donor Advised Fund, Private Foundation or Certain Supporting Organizations There several are other due diligence and process issues for the charity which we are not covering in this presentation. Also, for purposes of simplicity, we have ignored the Pease tax and made some general assumptions about applicable federal and state tax rates.

36 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes Option 1: Pre-Sale Charitable Gift of Real Estate (or LLC that owns Real Estate) Option 2: Post-Sale Charitable Gift of Cash Proceeds from Sale Option 3: Charitable Gift of Appreciated Marketable Securities

37 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes Option 1: Pre-Sale Charitable Gift of Real Estate (or LLC that owns Real Estate) Charitable Contribution Deduction = $6.420M Tax Benefit of Charitable Contribution = $2.774M Tax on Bargain Sale Element (the debt) = $1.424M $434k depreciation recapture $990k capital gains

38 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes Option 1: Pre-Sale Charitable Gift of Real Estate (or LLC that owns Real Estate) Cost to Mr. Real Estate is approximately $2.007M Benefit to Charity is approximately $6.420M If no UBIT, approximately $6.420M If UBIT, approximately $4.487M Leverage of gift approximately

39 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes Option 2: Post-Sale Charitable Gift of Cash Proceeds from Sale Sale nets Mr. Real Estate approximately $3.357M after income taxes Tax benefit of charitable gift is approximately $1.450M Cost to Mr. Real Estate is the difference of $1.907M Benefit to Charity is $3.357M Leverage is approximately 1.76

40 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes Option 3: Charitable Gift of Appreciated Marketable Securities Assume same basis in stock as the appreciated real estate on a percentage basis A sale of $4.441M of stock would net Mr. Real Estate the same $3.357M he would net from sale of the real estate Tax benefit of charitable gift is approximately $1.919M Cost of gift is approximately $1.438M Benefit to charity is $4.441M Leverage of gift is approximately 3.09

41 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes A Deeper Look at the Outcomes Option 1 (pre-sale gift) leverage rises from 3.20 to 5.33 Option 2 (post-sale gift) leverage rises from 1.76 to 2.93 Option 3 (marketable securities gift) leverage rises from 3.09 to 5.15

42 Mr. Real Estate Charitable Gift of Debt Financed Depreciated Commercial Real Estate Comparison of Alternatives and How to Think About Outcomes A Deeper Look at the Outcomes Typical family making a charitable gift at this level has a large taxable estate The donor is unlikely to consume the wealth during his lifetime Therefore, the donated wealth would be part of the donor s estate and the next generation would receive $0.60 on the dollar This increases the leverage because it decreases the cost of the gift in the hands of the next generation

43

44 Not So Set In Stone: Modifying Irrevocable Trusts in Missouri and Illinois Robert J. Will and Timothy D. Yeaglin September 27, 2016

45 Main Avenues of Modification Nonjudicial Settlement Agreements Nonjudicial Modifications Decanting Trust Protectors Judicial Modifications and Terminations

46 Headline of Page Subhead of Page Content for page Content for page Sub content

47 Nonjudicial Settlement Agreements Interested parties in Missouri and Illinois may enter into a binding agreement with respect to several matters involving a trust. The Grantor/Settlor need not be living for the agreement to be effective. Such matters include: (i) the interpretation or construction of trust terms; (ii) directions to the trustees to refrain from an act or to grant the trustee powers; (iii) the resignation or appointment of trustees; and (iv) the determination of trustee compensation.

48 Nonjudicial Settlement Agreements These agreements cannot be used to terminate a trust or modify dispositive provisions, with or without the concurrence of the Settlor/Grantor. Interested parties must sign the agreement. They include the trustees and beneficiaries. Virtual Representation can help reduce number of signatures. The consent of one person may bind another person in certain circumstances.

49 Nonjudicial Settlement Agreements Parents->Minor or unborn children (if no conflict of interest) Holders of broad/special or general powers of appointment->takers in default and potential appointees Trustees-> beneficiaries (if no conflict of interest) Persons with substantially similar interests -> minors, unborn, incapacitated and those unable to be located (if no conflict of interest) and in terms of a settlement agreement only, Qualified Beneficiaries can bind any non-qualified beneficiary.

50 Nonjudicial Modification Agreements Irrevocable Trusts may be modified in Missouri with the consent of the Settlor/Grantor and the beneficiaries, even if the modification is inconsistent with the purpose of the trust. Thus, dispositive provisions can be modified in this fashion if all of the beneficiaries agree (or are virtually represented). The Settlor cannot bind any beneficiary. Qualified Beneficiaries who have substantially similar interests with more remote beneficiaries cannot bind known (but remote) beneficiaries with respect to this Agreement.

51 Nonjudicial Modification Agreements Considerations: Are Consents by Beneficiaries considered gifts in certain circumstances? For instance, if a beneficiary consents to changing an outright distribution to a distribution to the beneficiary, subject to a lifetime trust, has a gift been made? Are there GST consequences? Is there a 2036 problem with the Settlor/Grantor assisting in the modification of an irrevocable trust he/she created? Florida does not allow a nonjudicial modification while a Settlor/Grantor is alive due to this concern.

52 Decanting - Not Just for Wine and Spirits Any More This newer modification technique is increasing in popularity. It is accomplished by a Trustee transferring assets from the old, less ideal trust to a new trust with better terms. To properly decant in Missouri: The original trust must allow the trustee to have at least the discretion to distribute income or principal to beneficiaries, even if that discretion is limited by an applicable standard (health, support, maintenance, etc.)

53 Decanting - Not Just for Wine and Spirits Any More The new trust must only provide for beneficiaries named in the original trust; no new beneficiaries allowed. The new trust may provide for fewer original beneficiaries than the original trust. Typically, we advise that a third party trustee perform the decanting. Income interests in certain trusts (Grantor Retained Annuity Trusts; Charitable Remainder Trusts; Marital Trusts) cannot be reduced. The Permissible Beneficiaries of the new trust must be notified 60 days prior to the decanting (unless this is waived). Spendthrift clauses do not prevent decanting in Missouri.

54 Decanting - Not Just for Wine and Spirits Any More Decanting is likely preferable to a Nonjudicial Modification. Beneficiary consents are not required, thus removing the concern about gifts being made through consents. The Settlor is not involved in the decanting process (again, we recommend a third-party Trustee). The final product is a newly funded irrevocable trust rather than a modified irrevocable trust in terms of optics.

55 Decanting - Not Just for Wine and Spirits Any More Illinois decanting is more restrictive. If the document limits the trustee s absolute discretion with an applicable standard (health, support, etc.), then (i) the beneficiaries of the new trust must match the beneficiaries of the old trust and (ii) the distribution language (income/principal) and the powers of appointment must all be the same as the old trust. These rules are relaxed in Illinois to allow for decanting into special needs trusts with respect to a disabled beneficiary s interest. Florida s law is even more restrictive. Trustees cannot decant in Florida if an applicable standard is provided.

56 Trust Protectors Missouri law provides for the role of a Trust Protector, who is someone other than the Settlor/Grantor, Trustee or beneficiary. A Trust Protector may have powers that are expressly described in the document, including those powers to: (i) modify or amend the trust instrument; (ii) terminate the trust; and/or (iii) increase, decrease, modify, or restrict the interests of the beneficiary or beneficiaries of the trust.

57 Trust Protectors Advantages of Trust Protectors Modifications by Trust Protectors are easier than nonjudicial modifications or judicial modifications because beneficiaries and other parties do not need to agree and no court is involved. It is arguable that Trust Protector modifications are easier than decanting because assets are not transferred between trusts (new accounts are not required, etc.). As with all modification options: flexibility Disadvantages of Trust Protectors Finding someone to actually act in the role. Fiduciary duties to Settlor and beneficiaries? Limited case law; potentially volatile area argument if evidence that Settlor asks Trust Protector to make changes to irrevocable trust.

58 Judicial Modifications and Terminations - Bob Will Most common when the Settlor is no longer living (otherwise, the nonjudicial route is available) or when not all beneficiaries agree. If all adult beneficiaries consent, a court may (if an non-consenting beneficiary s interest is protected): reduce or eliminate the interests of some beneficiaries and increase those of others; change the times or amounts of payments and distributions to beneficiaries; provide for termination of the trust at a time earlier or later than that specified by its term.

59 Judicial Modifications and Terminations - Bob Will If not all adult beneficiaries agree, a court may still modify the trust if the court is: satisfied that the interests of a beneficiary who does not consent will be adequately protected; and, in the case of a termination, the party seeking termination establishes that continuance of the trust is not necessary to achieve any material purpose of the trust; or in the case of a modification, the party seeking modification establishes that the modification is not inconsistent with a material purpose of the trust, and the modification is not specifically prohibited by the terms of the trust.

60 Judicial Modifications and Terminations Bob Will Work performed for corporate fiduciaries Charitable v. non-charitable modifications Venue Issues in St. Louis (County vs. City) Discussion regarding various scenarios and anecdotal experiences concerning judicial modifications and terminations

Session 1: Estate Planning Hot Topics: 2016

Session 1: Estate Planning Hot Topics: 2016 Christopher T. Rogers In this presentation we will review several current estate planning/estate tax topics, including (i) an introduction to the Beneficiary

Session 1: Estate Planning Hot Topics: 2016 Christopher T. Rogers In this presentation we will review several current estate planning/estate tax topics, including (i) an introduction to the Beneficiary

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS The Estate Planning Council of Greater Miami October 20, 2016 Louis Nostro, Esquire Nostro Jones, P.A. Miami, Florida lnostro@nostrojones.com

THE DESIGN, FUNDING, ADMINISTRATION & REPAIR OF GRATS, QPRTS & SALES TO IDGTS The Estate Planning Council of Greater Miami October 20, 2016 Louis Nostro, Esquire Nostro Jones, P.A. Miami, Florida lnostro@nostrojones.com

THE ESTATE PLANNER S SIX PACK

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Tenth Floor Columbia Center 101 West Big Beaver Road Troy, Michigan 48084-5280 (248) 457-7000 Fax (248) 457-7219 SPECIAL REPORT www.disinherit-irs.com For persons with taxable estates, there is an assortment

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Selected Subchapter J Subjects: From the Plumbing to the Planning, Preventing Pitfalls with Potential Payoffs January 24, 2018 Alan S. Halperin Paul, Weiss, Rifkind, Wharton & Garrison LLP Amy E. Heller

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning Where Were We vs. Where Are We Now 2017 2018 (Pre-Act) 2018 (Post-Act) Transfer Tax Rate 40% 40% 40% Estate/Gift Tax Exemption $5.49 million

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning Where Were We vs. Where Are We Now 2017 2018 (Pre-Act) 2018 (Post-Act) Transfer Tax Rate 40% 40% 40% Estate/Gift Tax Exemption $5.49 million

ANALYSIS: Analysis of the New Proposed Regulations Under Code 2704

ANALYSIS: Analysis of the New Proposed Regulations Under Code 2704 Analysis of the New Proposed Regulations Under Code 2704 by Jeramie J. Fortenberry, JD, LLM Executive Editor, WealthCounsel LLC On August

ANALYSIS: Analysis of the New Proposed Regulations Under Code 2704 Analysis of the New Proposed Regulations Under Code 2704 by Jeramie J. Fortenberry, JD, LLM Executive Editor, WealthCounsel LLC On August

678 TRUSTS: PLANNING STRATEGIES AND PITFALLS By Marvin E. Blum

678 TRUSTS: PLANNING STRATEGIES AND PITFALLS By Marvin E. Blum Typically, when a client is considering options to help reduce estate taxes, the client must consider techniques that require the client to

678 TRUSTS: PLANNING STRATEGIES AND PITFALLS By Marvin E. Blum Typically, when a client is considering options to help reduce estate taxes, the client must consider techniques that require the client to

Recent Developments in the Estate and Gift Tax Area. Annual Business Plan and the Proposed Regulations under Section 2642

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

Estate Planning. Uncertain Times. IRS Circular 230 Disclosure

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

Estate Planning IRS Circular 230 Disclosure To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments)

BOSTON BAR ASSOCIATION

BOSTON BAR ASSOCIATION ESTATE PLANNING FOR OWNERS OF CLOSELY HELD BUSINESSES Jeffrey W. Roberts, Esq. and Johanna Wise Sullivan, Esq. Nutter, McClennen & Fish, LLP Goals o What is the client hoping to

BOSTON BAR ASSOCIATION ESTATE PLANNING FOR OWNERS OF CLOSELY HELD BUSINESSES Jeffrey W. Roberts, Esq. and Johanna Wise Sullivan, Esq. Nutter, McClennen & Fish, LLP Goals o What is the client hoping to

The BDIT (Beneficiary Defective Inheritor's Trust)

") Estate Planning Hot Topics: 2016 (Beneficiary Defective Inheritor's Trust) Is a version of the Intentionally Defective Grantor Trust Grantor (Parent): (a) creates trust fbo next generation and (b) Grantor/Parent

Estate Planning Hot Topics: 2016 (Beneficiary Defective Inheritor's Trust) Is a version of the Intentionally Defective Grantor Trust Grantor (Parent): (a) creates trust fbo next generation and (b) Grantor/Parent

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Using Advanced Irrevocable Trusts for Income and Estate Tax Savings: Making 2012 Count The next nine months are an exceptional window of opportunity for your clients to make family wealth transfers. The

Spring 2011 Issue # 2. Introduction. Grantor Trusts & Intentionally Defective Irrevocable Trusts (IDITs) Issues & Uses in Estate Planning

Issues & Uses in Estate Planning") Spring 2011 Issue # 2 Grantor Trusts & Intentionally Defective Irrevocable Trusts (IDITs) Issues & Uses in Estate Planning I. INTRODUCTION II. USING GRANTOR TRUSTS III. REQUIREMENTS FOR GRANTOR TRUST STATUS

Spring 2011 Issue # 2 Grantor Trusts & Intentionally Defective Irrevocable Trusts (IDITs) Issues & Uses in Estate Planning I. INTRODUCTION II. USING GRANTOR TRUSTS III. REQUIREMENTS FOR GRANTOR TRUST STATUS

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER Patricia M. Annino, Attorney Prince Lobel Tye LLP Birmingham Estate Planning Council May 20, 2016 WHY IS IT IMPORTANT? Closely held business owners

CHARITABLE GIFTING AND THE CLOSELY HELD BUSINESS OWNER Patricia M. Annino, Attorney Prince Lobel Tye LLP Birmingham Estate Planning Council May 20, 2016 WHY IS IT IMPORTANT? Closely held business owners

1. The Regulatory Approach

Section 2601. Tax Imposed 26 CFR 26.2601 1: Effective dates. T.D. 8912 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 26 Generation-Skipping Transfer Issues AGENCY: Internal Revenue Service

Section 2601. Tax Imposed 26 CFR 26.2601 1: Effective dates. T.D. 8912 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 26 Generation-Skipping Transfer Issues AGENCY: Internal Revenue Service

Rev. Proc , IRB 224, 07/24/2008, IRC Sec(s). 642

. 642") Rev. Proc. 2008-45, 2008-30 IRB 224, 07/24/2008, IRC Sec(s). 642 Charitable lead unitrusts sample forms. Headnote: IRS provides sample forms for inter vivos nongrantor and grantor charitable lead unitrusts.

Rev. Proc. 2008-45, 2008-30 IRB 224, 07/24/2008, IRC Sec(s). 642 Charitable lead unitrusts sample forms. Headnote: IRS provides sample forms for inter vivos nongrantor and grantor charitable lead unitrusts.

2018 Advanced Estate Planning Survey Course. CHAPTER I Current Events/New Tax Law Issues Rick E. Graves Wilmington

2018 Advanced Estate Planning Survey Course TABLE OF CONTENTS CHAPTER I Current Events/New Tax Law Issues Rick E. Graves Wilmington A. Introduction... I-1 B. Transfer Tax Planning... I-2 1. Still 4,000...

2018 Advanced Estate Planning Survey Course TABLE OF CONTENTS CHAPTER I Current Events/New Tax Law Issues Rick E. Graves Wilmington A. Introduction... I-1 B. Transfer Tax Planning... I-2 1. Still 4,000...

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity 04.23.2012 04.23.2012 NEWS BY: FARHAD AGHDAMI 2012 may present the single greatest opportunity for wealth transfer planning in recent memory.

Wealth Transfer Planning in 2012: Perfect Storm of Opportunity 04.23.2012 04.23.2012 NEWS BY: FARHAD AGHDAMI 2012 may present the single greatest opportunity for wealth transfer planning in recent memory.

Effective Strategies for Wealth Transfer

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Effective Strategies for Wealth Transfer The Prudential Insurance Company of America, Newark, NJ. 0265295-00002-00 Ed. 02/2016 Exp. 08/04/2017 UNDERSTANDING WEALTH TRANSFER What strategy to use and when?

Grantor Trusts. Maine Tax Forum

Grantor Trusts Maine Tax Forum Jeremiah W. Doyle IV Senior Vice President BNY Mellon Private Wealth Management Boston, MA jere.doyle@bnymellon.com (617) 722-7420 November, 2017 1 Grantor Trusts AGENDA

Grantor Trusts Maine Tax Forum Jeremiah W. Doyle IV Senior Vice President BNY Mellon Private Wealth Management Boston, MA jere.doyle@bnymellon.com (617) 722-7420 November, 2017 1 Grantor Trusts AGENDA

THE AMERICAN COLLEGE OF TRUST AND ESTATE COUNSEL (ACTEC) COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 2704 [REG ] SUMMARY

![THE AMERICAN COLLEGE OF TRUST AND ESTATE COUNSEL (ACTEC) COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 2704 [REG ] SUMMARY](/thumbs/91/107522212.jpg "THE AMERICAN COLLEGE OF TRUST AND ESTATE COUNSEL (ACTEC) COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 2704 [REG ] SUMMARY") THE AMERICAN COLLEGE OF TRUST AND ESTATE COUNSEL (ACTEC) COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 2704 [REG-163113-02] SUMMARY These comments of The American College of Trust and Estate Counsel (ACTEC)

THE AMERICAN COLLEGE OF TRUST AND ESTATE COUNSEL (ACTEC) COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 2704 [REG-163113-02] SUMMARY These comments of The American College of Trust and Estate Counsel (ACTEC)

Taming the Planning B.E.A.S.T.

Taming the Planning B.E.A.S.T. Tulsa Estate Planning Forum October 9 th, 2017 James M. Duggan, M.B.A., J.D. DUGGAN BERTSCH, LLC 303 West Madison, Suite 1000 Chicago, Illinois 60606-3321 e-mail: jduggan@dugganbertsch.com

Taming the Planning B.E.A.S.T. Tulsa Estate Planning Forum October 9 th, 2017 James M. Duggan, M.B.A., J.D. DUGGAN BERTSCH, LLC 303 West Madison, Suite 1000 Chicago, Illinois 60606-3321 e-mail: jduggan@dugganbertsch.com

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs

& Rolling GRATs") Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

Advanced Sales White Paper: Grantor Retained Annuity Trusts ( GRATs ) & Rolling GRATs February, 2014 Contact us: AdvancedSales@voya.com This material is designed to provide general information for use

Estate Planning under the New Tax Law

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

Tax, Benefits, and Private Client JANUARY 2018 NO. 1 Estate Planning under the New Tax Law This client alert is part of a special series on the Tax Cuts and Jobs Act and related changes to the tax code,

MAKE YOUR CHARITABLE ESTATE PLAN GREAT AGAIN Charitable Planning with Retirement Accounts: Strategies, Traps & Solutions

MAKE YOUR CHARITABLE ESTATE PLAN GREAT AGAIN Charitable Planning with Retirement Accounts: Strategies, Traps & Solutions Christopher R. Hoyt Professor of Law University of Missouri (Kansas City) School

MAKE YOUR CHARITABLE ESTATE PLAN GREAT AGAIN Charitable Planning with Retirement Accounts: Strategies, Traps & Solutions Christopher R. Hoyt Professor of Law University of Missouri (Kansas City) School

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset.

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

Comprehensive Charitable Planning

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

CLIENT GUIDE Advanced Markets Comprehensive Charitable Planning John Hancock Life Insurance Company (U.S.A.) (John Hancock) John Hancock Life Insurance Company of New York (John Hancock) LIFE-5175 1/17

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES Presented by: Michael M. Gordon Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, Delaware 19806 302-652-2900 mgordon@gfmlaw.com

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES Presented by: Michael M. Gordon Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, Delaware 19806 302-652-2900 mgordon@gfmlaw.com

Advanced marketing concepts. Brought to you by the Advanced Consulting Group of Nationwide

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Advanced marketing concepts Brought to you by the Advanced Consulting Group of Nationwide Breaking down and simplifying financial planning techniques When your clients have complex estate, retirement or

Gregory W. Sampson Looper Reed & McGraw, P.C

Gregory W. Sampson Looper Reed & McGraw, P.C 469-320-6097 GSampson@LRMLaw.com www.lrmlaw.com 2010 Looper Reed & McGraw, P.C. The information contained herein is subject to change without notice Basic Estate

Gregory W. Sampson Looper Reed & McGraw, P.C 469-320-6097 GSampson@LRMLaw.com www.lrmlaw.com 2010 Looper Reed & McGraw, P.C. The information contained herein is subject to change without notice Basic Estate

Charitable Planning CLIENT GUIDE

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Charitable Planning CLIENT GUIDE CHARITABLE PLANNING Giving to charity can provide many benefits and opportunities, both to the charity and to you. The charity, benefits from a donation that can help further

Business Interests: Planning Considerations

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Business Interests: Planning Considerations Business owners have unusual opportunities when it comes to making gifts to The First Church of Christ, Scientist. They have the flexibility of giving from their

Insurance-Related Best Practices Guide for Buy-Sell Agreements

Insurance-Related Best Practices Guide for Buy-Sell Agreements The buy-sell agreement review and feedback process at the Principal Financial Group has allowed us to observe many different drafting approaches

Insurance-Related Best Practices Guide for Buy-Sell Agreements The buy-sell agreement review and feedback process at the Principal Financial Group has allowed us to observe many different drafting approaches

Insurance-related best practices guide for buy-sell agreements

Buy-sell agreements Insurance-related best practices guide for buy-sell agreements All businesses are different. And business owners need their buy-sell agreements to work for their business. We ve reviewed

Buy-sell agreements Insurance-related best practices guide for buy-sell agreements All businesses are different. And business owners need their buy-sell agreements to work for their business. We ve reviewed

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

WEALTH TRANSFER STRATEGIES FOR FAMILIES DECEMBER 13, 2018 To Receive CPE Credit Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete group

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2019 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

PREPARING GIFT TAX RETURNS

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

An Overview of Trust Modification and Decanting

An Overview of Trust Modification and Decanting Probate and Pumpernickel September 26, 2014 J. Aaron Nelson, Jr. Merline and Meacham, P.A. 812 East North Street (29603) P.O. Box 10796 Greenville, SC 29601

An Overview of Trust Modification and Decanting Probate and Pumpernickel September 26, 2014 J. Aaron Nelson, Jr. Merline and Meacham, P.A. 812 East North Street (29603) P.O. Box 10796 Greenville, SC 29601

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.

and Rolling GRATs. Producer Guide. For agent use only. Not for public distribution.") Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Grantor Retained Annuity Trusts ( GRATs ) and Rolling GRATs Producer Guide Introduction to GRATs and Rolling GRATs The Grantor Retained Annuity Trust ( GRAT ) is a flexible planning tool which can be used

Section 643. Definitions Applicable to Subparts A, B, C, and D

Section 643. Definitions Applicable to Subparts A, B, C, and D 26 CFR 1.643(a) 3: Capital gains and losses. T.D. 9102 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 1, 20, 25, and 26

Section 643. Definitions Applicable to Subparts A, B, C, and D 26 CFR 1.643(a) 3: Capital gains and losses. T.D. 9102 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 1, 20, 25, and 26

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014)

") THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

THE MAGIC OF CHARITABLE GIVING Win-Win Strategies That Benefit Both the Charity and the Donor (ILLUSTRATIONS BASED ON RATES AND TAXES FOR APRIL 2014) Presented to: CENTENNIAL ESTATE PLANNING COUNCIL November

11/9/2012. Estate and Charitable Planning Before the End of IRS Circular 230. Historical Estate Tax Rates and Exemptions

Estate and Charitable Planning Before the End of 2012 SOL S. REIFER, J.D., LL.M. KYLE C. POST, J.D., LL.M. WRIGHT GINSBERG BRUSILOW P.C. 14755 PRESTON ROAD, SUITE 600 DALLAS, TEXAS 75254 972-788-1600 sreifer@wgblawfirm.com

Estate and Charitable Planning Before the End of 2012 SOL S. REIFER, J.D., LL.M. KYLE C. POST, J.D., LL.M. WRIGHT GINSBERG BRUSILOW P.C. 14755 PRESTON ROAD, SUITE 600 DALLAS, TEXAS 75254 972-788-1600 sreifer@wgblawfirm.com

Memorandum FILE. Naim D. Bulbulia, Esq. Estate Planning Primer

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Memorandum TO FROM FILE Naim D. Bulbulia, Esq. DATE May 5, 2005 RE Estate Planning Primer The following memorandum has been prepared in order to provide you with an overview of estate and gift tax law

Wealth Transfer and Charitable Planning Strategies. Handbook

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Wealth Transfer and Charitable Planning Strategies Handbook Wealth Transfer and Charitable Planning Strategies Handbook This handbook contains 12 core wealth transfer and charitable planning strategies.

Planning and Drafting charitable Lead trusts

includes irs-approved sample trust forms Planning and Drafting charitable Lead trusts TABLE OF CONTENTS What is a Qualified charitable Lead trust?......................... 3 Forms of lead trusts...........................................

includes irs-approved sample trust forms Planning and Drafting charitable Lead trusts TABLE OF CONTENTS What is a Qualified charitable Lead trust?......................... 3 Forms of lead trusts...........................................

Charitable Giving Techniques

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

Charitable Giving Techniques Helping achieve your charitable and estate-planning goals Trust Tip A trust can be thought of as having two parts an income interest and a remainder interest. The income interest

DECANTING ISSUES MEMO UNIFORM DECANTING DISTRIBUTIONS DRAFTING COMMITTEE

DECANTING ISSUES MEMO UNIFORM DECANTING DISTRIBUTIONS DRAFTING COMMITTEE I. Defining Decanting and the Middle Way A. Decanting as an Exercise of a Fiduciary Power. Decanting is an exercise of a fiduciary

DECANTING ISSUES MEMO UNIFORM DECANTING DISTRIBUTIONS DRAFTING COMMITTEE I. Defining Decanting and the Middle Way A. Decanting as an Exercise of a Fiduciary Power. Decanting is an exercise of a fiduciary

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS HOW ESTATE & ASSET PROTECTION CAN SAVE MILLIONS You should consider creating an Intentionally Defective Irrevocable Trust ( IDIT ) and gifting assets to

SQUEEZE, FREEZE, & BURN: ESTATE PLANNING WITH 678 TRUSTS Written materials prepared by Marvin E. Blum, J.D./C.P.A.

777 Main Street, Suite 700 Fort Worth, Texas 76102 Phone: (817) 334-0066 303 Colorado St., Suite 2250 Austin, Texas 78701 Phone: (512) 579-4060 www.theblumfirm.com 300 Crescent Court, Suite 1350 Dallas,

777 Main Street, Suite 700 Fort Worth, Texas 76102 Phone: (817) 334-0066 303 Colorado St., Suite 2250 Austin, Texas 78701 Phone: (512) 579-4060 www.theblumfirm.com 300 Crescent Court, Suite 1350 Dallas,

The Advisor s Guide to Donating Illiquid Assets

The Advisor s Guide to Donating Illiquid Assets by Barbara Benware Vice President, Investment Oversight and Risk and Denise Schuh Director, Charitable Strategies Group About the authors: Barbara Benware

The Advisor s Guide to Donating Illiquid Assets by Barbara Benware Vice President, Investment Oversight and Risk and Denise Schuh Director, Charitable Strategies Group About the authors: Barbara Benware

Section 367 limits use of the reorganization

8 POINTS TO REMEMBER Editor s Note: POINTS TO REMEMBER are individual submissions to the Newsletter from Section of Taxation members with insights to share. Although these items are subject to selection

8 POINTS TO REMEMBER Editor s Note: POINTS TO REMEMBER are individual submissions to the Newsletter from Section of Taxation members with insights to share. Although these items are subject to selection

How To Use an Intentionally Defective Irrevocable Trust To Freeze an Estate

How To Use an Intentionally Defective Irrevocable Trust To Freeze an Estate Michael D. Mulligan All section references are to the Internal Revenue Code ( IRC ) unless otherwise indicated. ETIP, to estate

How To Use an Intentionally Defective Irrevocable Trust To Freeze an Estate Michael D. Mulligan All section references are to the Internal Revenue Code ( IRC ) unless otherwise indicated. ETIP, to estate

numer cal anal ysi shown, esul nei her guar ant ees nor ect ons, and act ual esul may gni cant Any assumpt ons est es, on, her val ues hypot het cal

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Table of Contents Disclaimer Notice... 1 Disclosure Notice... 2 Charitable Gift Annuity (CGA)... 3 Charitable Giving Techniques... 4 Charitable Lead Annuity Trust (CLAT)... 5 Charitable Lead Unitrust (CLUT)...

Donations of Complex Assets to the LDS Church. Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT (801)

") Donations of Complex Assets to the LDS Church Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT 84111 (801) 323-5946 bandrewsen@kmclaw.com Overview of Presentation What is a complex asset? Almost

Donations of Complex Assets to the LDS Church Brent Andrewsen, Esq. 50 E. South Temple Salt Lake City, UT 84111 (801) 323-5946 bandrewsen@kmclaw.com Overview of Presentation What is a complex asset? Almost

Chapter 59 FREEZING TECHNIQUES CORPORATIONS AND PARTNERSHIPS

Chapter 59 FREEZING TECHNIQUES CORPORATIONS AND PARTNERSHIPS WHAT IS IT? In the most fundamental sense, an estate freeze is any planning device where the owner of property attempts to freeze the present

Chapter 59 FREEZING TECHNIQUES CORPORATIONS AND PARTNERSHIPS WHAT IS IT? In the most fundamental sense, an estate freeze is any planning device where the owner of property attempts to freeze the present

Leveraging wealth transfer using a sale to a defective grantor trust

Sale to a Grantor Trust Strategy Leveraging wealth transfer using a sale to a defective grantor trust Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF

Sale to a Grantor Trust Strategy Leveraging wealth transfer using a sale to a defective grantor trust Not a bank or credit union deposit, obligation or guarantee May lose value Not FDIC or NCUA/NCUSIF

2018 Federal Tax Pocket Guide

2018 Federal Tax Pocket Guide For Advisers and Planners n Federal Individual Income Tax n Income Tax on Estates and Trusts n Federal Corporation Tax n Federal Income Tax on Capital Gains n Federal Alternative

2018 Federal Tax Pocket Guide For Advisers and Planners n Federal Individual Income Tax n Income Tax on Estates and Trusts n Federal Corporation Tax n Federal Income Tax on Capital Gains n Federal Alternative

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ Fax

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

ANITA J. SIEGEL, ESQ. Siegel & Bergman, LLC 365 South Street Morristown, NJ 07960 973-285-5007 Fax 973-285-5008 ajs@sblawllc.com CHARITABLE PLANNING A PRIMER April 4, 2011 Planning for charitable gifts

2017 Tax Cuts and Jobs Act

2017 Tax Cuts and Jobs Act The most significant changes in tax law since the 1986 tax reform were enacted in December 2017. The following charts detail the provisions most relevant to high income and high-net-worth

2017 Tax Cuts and Jobs Act The most significant changes in tax law since the 1986 tax reform were enacted in December 2017. The following charts detail the provisions most relevant to high income and high-net-worth

New York Enacts Important New Law Governing a Trustee s Power to Pay Trust Assets to a New Trust

PAMELA EHRENKRANZ (PEhrenkranz@wlrk.com) is chair of the Trusts and Estates Practice Group at Wachtell, Lipton, Rosen & Katz in New York. Her practice is focused on developing estate plans for individual

PAMELA EHRENKRANZ (PEhrenkranz@wlrk.com) is chair of the Trusts and Estates Practice Group at Wachtell, Lipton, Rosen & Katz in New York. Her practice is focused on developing estate plans for individual

FLORIDA IRREVOCABLE TRUST AMENDMENT MECHANISMS. By Charles (Chuck) Rubin & Jenna Rubin

Rubin & Jenna Rubin") FLORIDA IRREVOCABLE TRUST AMENDMENT MECHANISMS By Charles (Chuck) Rubin & Jenna Rubin Gutter Chaves Josepher Rubin Forman Fleisher Miller P.A. www.floridatax.com Last Updated: May 2018 OTHER LINKS FROM

FLORIDA IRREVOCABLE TRUST AMENDMENT MECHANISMS By Charles (Chuck) Rubin & Jenna Rubin Gutter Chaves Josepher Rubin Forman Fleisher Miller P.A. www.floridatax.com Last Updated: May 2018 OTHER LINKS FROM

Comprehensive Charitable Planning

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

Advanced Markets Client Guide Comprehensive Charitable Planning Charitable gifts that preserve personal wealth. Comprehensive Charitable Planning Giving to charity can provide many benefits and opportunities,

INCOME TAX DEDUCTIONS FOR CHARITABLE BEQUESTS OF IRD

INCOME TAX DEDUCTIONS FOR CHARITABLE BEQUESTS OF IRD Will an estate or trust get a charitable income tax deduction when income in respect of a decedent is donated to a charity? TABLE OF CONTENTS Christopher

INCOME TAX DEDUCTIONS FOR CHARITABLE BEQUESTS OF IRD Will an estate or trust get a charitable income tax deduction when income in respect of a decedent is donated to a charity? TABLE OF CONTENTS Christopher

The Use of Pass-Through Entities in Asset Protection and Wealth Transfer Planning

The Use of Pass-Through Entities in Asset Protection and Wealth Transfer Planning DANIEL W DALY III 2323 S. Shepherd, 14 th Floor Houston, TX 77019 713-979- 4701 daly@ohdlegal.com www.ohdlegal.com Judge

The Use of Pass-Through Entities in Asset Protection and Wealth Transfer Planning DANIEL W DALY III 2323 S. Shepherd, 14 th Floor Houston, TX 77019 713-979- 4701 daly@ohdlegal.com www.ohdlegal.com Judge

S Corporation Planning

S Corporation Planning Details Written by Martin M. Shenkman, CPA, MBA, PFS, AEP, JD The income tax is the new estate tax. With a federal estate tax exemption at over $5 million and increasing by an inflation

S Corporation Planning Details Written by Martin M. Shenkman, CPA, MBA, PFS, AEP, JD The income tax is the new estate tax. With a federal estate tax exemption at over $5 million and increasing by an inflation

Title 12 - Decedents' Estates and Fiduciary Relations. Part VI Allocation of Principal and Income

Part VI Allocation of Principal and Income Chapter 61 DELAWARE UNIFORM PRINCIPAL AND INCOME ACT Subchapter I Definitions and General Principles 61-101 Short title. Subchapters I through VI of this chapter

Part VI Allocation of Principal and Income Chapter 61 DELAWARE UNIFORM PRINCIPAL AND INCOME ACT Subchapter I Definitions and General Principles 61-101 Short title. Subchapters I through VI of this chapter

Intentionally Defective (?) Grantor Trusts

Grantor Trusts") Intentionally Defective (?) Grantor Trusts Owen@GivnerKaye.com 1 What We Will Cover [Part 1]: 1. How Did The Grantor Trust Rules Originate? P. 3 2. Common Examples of Grantor Trusts. P. 4 3. What Do We

Intentionally Defective (?) Grantor Trusts Owen@GivnerKaye.com 1 What We Will Cover [Part 1]: 1. How Did The Grantor Trust Rules Originate? P. 3 2. Common Examples of Grantor Trusts. P. 4 3. What Do We

Estate Planning for IRAs & Qualified Plans

Estate Planning for IRAs & Qualified Plans Presented by Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP All Rights Reserved 1 Outline Foundation Concepts 401(a)(9) Regulations Estate Planning

Estate Planning for IRAs & Qualified Plans Presented by Robert S. Keebler, CPA/PFS, MST, AEP Keebler & Associates, LLP All Rights Reserved 1 Outline Foundation Concepts 401(a)(9) Regulations Estate Planning

Delaware Tax Institute Income Tax Planning With Trusts After Tax Reform

Delaware Tax Institute Income Tax Planning With Trusts After Tax Reform December 7, 2018 By: Daniel F. Hayward, Esq. Effects of Tax Reform Tax reform resulted in a dramatic increase in the size of the

Delaware Tax Institute Income Tax Planning With Trusts After Tax Reform December 7, 2018 By: Daniel F. Hayward, Esq. Effects of Tax Reform Tax reform resulted in a dramatic increase in the size of the

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Sale to an Intentionally Defective Irrevocable Trust

Sale to an Intentionally Defective Irrevocable Trust Concept An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

Sale to an Intentionally Defective Irrevocable Trust Concept An Intentionally Defective Irrevocable Trust (IDIT) is an irrevocable trust established by a grantor generally for the benefit of the grantor

New York State Bar Association Tax Aspects of Real Property Transactions. Estate Planning for Investment Real Estate: Don t Forget the Income Tax Side

New York State Bar Association Tax Aspects of Real Property Transactions Estate Planning for Investment Real Estate: Don t Forget the Income Tax Side By Stephen M. Breitstone, Esq. Meltzer, Lippe, Goldstein

New York State Bar Association Tax Aspects of Real Property Transactions Estate Planning for Investment Real Estate: Don t Forget the Income Tax Side By Stephen M. Breitstone, Esq. Meltzer, Lippe, Goldstein

Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012

Month Year Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012 BY RENEE M. GABBARD, LISA M. LAFOURCADE & MEGAN S. ACOSTA It appears that the current favorable estate, gift

Month Year Temporary Estate, Gift and GST Tax Laws Provide Unprecedented Opportunities in 2012 BY RENEE M. GABBARD, LISA M. LAFOURCADE & MEGAN S. ACOSTA It appears that the current favorable estate, gift

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Unified transfer tax system $10,000,000 exclusion/exemption for gift, estate and GST tax for years 2018 2025 Indexed for inflation: $11.18

MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS JULY 9, 2018 Unified transfer tax system $10,000,000 exclusion/exemption for gift, estate and GST tax for years 2018 2025 Indexed for inflation: $11.18

The Estate Planner s Passthrough or Passback Entity of Choice the Grantor Trust (Part Two)

") The Estate Planner s Passthrough or Passback Entity of Choice the Grantor Trust (Part Two) 1. A Tree is not a Tree When You call it a Bush This column discussed in the edition of the JPTE the importance

The Estate Planner s Passthrough or Passback Entity of Choice the Grantor Trust (Part Two) 1. A Tree is not a Tree When You call it a Bush This column discussed in the edition of the JPTE the importance

SUMMARIES OF STATE DECANTING STATUTES

SUMMARIES OF STATE DECANTING STATUTES As of August 22, 2014 compiled by Susan T. Bart Schiff Hardin LLP, Chicago, Illinois If you have an update or revision to a state summary, please contact Susan T.

SUMMARIES OF STATE DECANTING STATUTES As of August 22, 2014 compiled by Susan T. Bart Schiff Hardin LLP, Chicago, Illinois If you have an update or revision to a state summary, please contact Susan T.

Buy-Sell Agreements. Buy-Sell Agreements. Advantages of Buy-Sell Agreements. Thomas P. Langdon

Buy-Sell Agreements Buy-Sell Agreements Obligates one party to sell and another to buy a business interest Often triggered upon Death of business owner Disability of business owner Advantages of Buy-Sell

Buy-Sell Agreements Buy-Sell Agreements Obligates one party to sell and another to buy a business interest Often triggered upon Death of business owner Disability of business owner Advantages of Buy-Sell

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts. Philip M. Lindquist, Dallas, TX

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts Philip M. Lindquist, Dallas, TX Copyright 2014 by K&L Gates LLP. All rights reserved. Introduction

Basic Trust & Estate Income Tax Planning, Including a Discussion of Intentionally Defective Grantor Trusts Philip M. Lindquist, Dallas, TX Copyright 2014 by K&L Gates LLP. All rights reserved. Introduction

Cushing, Morris, Armbruster & Montgomery, LLP. Some Tax-Efficient Ways of Making Gifts

Cushing, Morris, Armbruster & Montgomery, LLP Some Tax-Efficient Ways of Making Gifts For wealth transfer tax planning, it is blessed to give. It is more blessed still to give while living (rather than

Cushing, Morris, Armbruster & Montgomery, LLP Some Tax-Efficient Ways of Making Gifts For wealth transfer tax planning, it is blessed to give. It is more blessed still to give while living (rather than

STATE OF NEW JERSEY. SENATE, No SENATE JUDICIARY COMMITTEE STATEMENT TO. with committee amendments DATED: DECEMBER 17, 2015

SENATE JUDICIARY COMMITTEE STATEMENT TO SENATE, No. 2035 with committee amendments STATE OF NEW JERSEY DATED: DECEMBER 17, 2015 The Senate Judiciary Committee reports favorably and with committee amendments

SENATE JUDICIARY COMMITTEE STATEMENT TO SENATE, No. 2035 with committee amendments STATE OF NEW JERSEY DATED: DECEMBER 17, 2015 The Senate Judiciary Committee reports favorably and with committee amendments

Estate Planning. Insight on. Adapting to the times Estate planning focus shifts to income taxes. International estate planning 101

Insight on Estate Planning June/July 2014 Adapting to the times Estate planning focus shifts to income taxes International estate planning 101 When is the optimal time to begin receiving Social Security?

Insight on Estate Planning June/July 2014 Adapting to the times Estate planning focus shifts to income taxes International estate planning 101 When is the optimal time to begin receiving Social Security?

4/26/2018 (c) William P. Streng 1

William P. Streng 1") CHAPTER 16 Charitable Gift Transfers Circumstances where charitable gifts are of significant interest to clients: 1) Clients have no direct descendants. 2) Clients have substantial assets and genuine charitable

CHAPTER 16 Charitable Gift Transfers Circumstances where charitable gifts are of significant interest to clients: 1) Clients have no direct descendants. 2) Clients have substantial assets and genuine charitable

Charitable Giving for Entrepreneurs after TCJA

Charitable Giving for Entrepreneurs after TCJA Brian T. Whitlock, CPA, JD, LLM THE GLOBAL FOODBANKING NETWORK Agenda Overview of charitable giving pre-tcja Review TCJA Changes Impacting Charitable Giving

Charitable Giving for Entrepreneurs after TCJA Brian T. Whitlock, CPA, JD, LLM THE GLOBAL FOODBANKING NETWORK Agenda Overview of charitable giving pre-tcja Review TCJA Changes Impacting Charitable Giving

Post-Mortem Planning Steve R. Akers

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Post-Mortem Planning Steve R. Akers Bessemer Trust Dallas, Texas akers@bessemer.com Copyright 2012 by Bessemer Trust Company, N.A. All rights reserved I. PLANNING ISSUES FOR 2010 DECEDENTS A. Default Rule

Magical Mystery Tour: Naming a Special Needs Trust as Beneficiary of a Retirement Plan

Magical Mystery Tour: Naming a Special Needs Trust as Beneficiary of a Retirement Plan Presenter: Dennis M. Sandoval Stetson 2017 Special Needs Trust National Conference St. Petersburg, Florida 2010-2017

Magical Mystery Tour: Naming a Special Needs Trust as Beneficiary of a Retirement Plan Presenter: Dennis M. Sandoval Stetson 2017 Special Needs Trust National Conference St. Petersburg, Florida 2010-2017

NEW YORK State Decanting Summary 1

NEW YORK State Decanting Summary 1 STATUTORY HISTORY Statutory citation N.Y. EST. POWERS & TRUSTS 10-6.6 Effective Date 7/24/92 Amendment Date(s) 8/17/11; 11/13/13 ABILITY TO DECANT 1. Discretionary distribution

NEW YORK State Decanting Summary 1 STATUTORY HISTORY Statutory citation N.Y. EST. POWERS & TRUSTS 10-6.6 Effective Date 7/24/92 Amendment Date(s) 8/17/11; 11/13/13 ABILITY TO DECANT 1. Discretionary distribution

The CPA s Guide to Financial & Estate Planning Planning with Life Insurance. Presented by: Steven G. Siegel, J.D., LL.M.

The CPA s Guide to Financial & Estate Planning Planning with Life Insurance Presented by: Steven G. Siegel, J.D., LL.M. (Taxation) Earn CPE #AICPApfp 2 Helpful Hints #AICPApfp 3 About the PFP Section &

The CPA s Guide to Financial & Estate Planning Planning with Life Insurance Presented by: Steven G. Siegel, J.D., LL.M. (Taxation) Earn CPE #AICPApfp 2 Helpful Hints #AICPApfp 3 About the PFP Section &

Estate Planning in 2019

CLIENT MEMORANDUM Estate Planning in 2019 January 14, 2019 The Tax Cuts and Jobs Act (the Act ), which took effect January 1, 2018, made sweeping changes to the federal tax landscape. Of particular relevance

CLIENT MEMORANDUM Estate Planning in 2019 January 14, 2019 The Tax Cuts and Jobs Act (the Act ), which took effect January 1, 2018, made sweeping changes to the federal tax landscape. Of particular relevance

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP November 9, 2016 1 FIDUCIARY INCOME TAX BOOT CAMP INCOME TAXATION OF TRUSTS AND ESTATES Presenters: Gregory V. Gadarian Steven W.

Southern Arizona Estate Planning Council FIDUCIARY INCOME TAX BOOT CAMP November 9, 2016 1 FIDUCIARY INCOME TAX BOOT CAMP INCOME TAXATION OF TRUSTS AND ESTATES Presenters: Gregory V. Gadarian Steven W.

Charitable Giving Techniques

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Charitable Giving Techniques Giving to charity used to be as simple as writing a check or dropping off old clothes at a charitable organization. But this type of giving, although appropriate for some,

Strategies for Reducing Wealth and Transfer Taxes. By, Pattie S. Christensen, Esq

Strategies for Reducing Wealth and Transfer Taxes By, Pattie S. Christensen, Esq A. Lifetime Gifts The current gift tax program permits a person to transfer up to $13,000 worth of gifts of a present interest

Strategies for Reducing Wealth and Transfer Taxes By, Pattie S. Christensen, Esq A. Lifetime Gifts The current gift tax program permits a person to transfer up to $13,000 worth of gifts of a present interest

Reciprocal Trust Doctrine

Reciprocal Trust Doctrine Overview With the increased lifetime gifting opportunities, clients are often faced with seemingly conflicting objectives of reducing the taxable estate and retaining access to

Reciprocal Trust Doctrine Overview With the increased lifetime gifting opportunities, clients are often faced with seemingly conflicting objectives of reducing the taxable estate and retaining access to

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

Investment and Estate Planning Opportunities for High Net Worth Individuals in 2013 Presented By: CPA, MST, AEP Keebler & Associates, May 2, 2013 Phone: (920) 593-1701 E-mail: robert.keebler@keeblerandassociates.com

PROPOSED AMENDMENTS TO THE REVISED GEORGIA TRUST CODE OF 2010

PROPOSED AMENDMENTS TO THE REVISED GEORGIA TRUST CODE OF 2010 State Bar of Georgia, Fiduciary Law Section Trust Code Revision Committee December 13, 2016 In 2015, the Executive Committee appointed a new

PROPOSED AMENDMENTS TO THE REVISED GEORGIA TRUST CODE OF 2010 State Bar of Georgia, Fiduciary Law Section Trust Code Revision Committee December 13, 2016 In 2015, the Executive Committee appointed a new

Restricting Valuation Discounts. Practical Implications of the Proposed Regulations to IRC 2704

Restricting Valuation Discounts Practical Implications of the Proposed Regulations to IRC 2704 IRC 2704 Special Valuation Rules Special Rules for valuing intra-family transfers of interest in corporations

Restricting Valuation Discounts Practical Implications of the Proposed Regulations to IRC 2704 IRC 2704 Special Valuation Rules Special Rules for valuing intra-family transfers of interest in corporations

President Obama s Fiscal Year 2012 Revenue Proposals

President Obama s Fiscal Year 2012 Revenue Proposals Proposals Relating to Individuals and Estate and Gift Taxation SUMMARY On February 14, 2011, the Obama Administration (the Administration ) released

President Obama s Fiscal Year 2012 Revenue Proposals Proposals Relating to Individuals and Estate and Gift Taxation SUMMARY On February 14, 2011, the Obama Administration (the Administration ) released

The Impact of U.S. Tax Reform on International Private Clients and Their Foreign Trusts

The Impact of U.S. Tax Reform on International Private Clients and Their Trusts Hal J. Webb: Partner Head of International Private Client Services STEP Cayman April 19, 2018 1 Gift and Estate Tax Exemption

The Impact of U.S. Tax Reform on International Private Clients and Their Trusts Hal J. Webb: Partner Head of International Private Client Services STEP Cayman April 19, 2018 1 Gift and Estate Tax Exemption