Annexation Issues: Emergency Services Districts. TML Annexation Conference May 12-13, 2016

|

|

|

- Briana Gwendoline Holt

- 5 years ago

- Views:

Transcription

1 Annexation Issues: Emergency Services Districts TML Annexation Conference May 12-13, 2016

2 What is an ESD? ESDs are local political subdivisions established under the Constitution of the State of Texas that may provide fire, rescue, EMS and other emergency services Governed by 5 commissioners appointed by County Commissioners Court - except in Harris, Smith and Orange Counties and multicounty ESDs, where they are elected

3 Why are ESDs created? Insufficient funding for Volunteer Fire Departments through donations or County support Inability to spread funding for City Fire Departments outside City limits ESDs Ensure adequate funding of local fire, EMS, rescue and other emergency services ESDs spread funding for emergency services among everyone that might receive those services

4 ESD Statistics Over 300 ESDs in Texas Primarily funded by property taxes not to exceed Constitutional Cap of $0.10 per $100 One-Third with Tax Rates >$0.09/$100 Approx. 70 ESDs collect Sales Tax Up to 2% local cap, 1/8% increments

5 Most Current Map of ESDs in Texas Source: Texas State Association of Fire and Emergency Districts 2015

6 Laws Governing ESDs Article III, Section 48-e of the Texas Constitution Chapter 775 of the Texas Health & Safety Code Texas Open Meetings and Public Information Acts Election Code Property Tax Code Public Funds Investment Act Professional Services Procurement Act Chapter 2269 of the Government Code relating to construction of facilities And More!

7 Types of ESD Operations If you have seen one ESD, you have seen one ESD Volunteer Departments Volunteers have other jobs in local community Combined Departments Paid staff to cover shifts when volunteers are out of community at work Employee Departments Insufficient volunteer manpower to meet call volume demands of service area

8 Basic Creation Process Requires Petition by Qualified Voters to County Consent of a City Required at Creation if the proposed area includes ETJ or City Limits Acceptance by County Commissioners Court Public Hearing on Creation Determination by County Commissioners Court County Election on Creation

9 Dealing with an ESD in the ANNEXATION PROCESS

10 City Annexation into ESD Cities may annex into and EITHER: Choose to remove the annexed territory from an ESD; or Leave the annexed territory in the ESD. Certain procedures apply to annexation process ESD entitled to compensation under certain circumstances

11

12 Removal of Territory by Municipality City Must: Complete all other municipal procedures necessary to annex territory in an ESD, AND If City intends to provide emergency services to the territory by the use of municipal personnel or by some method other than by use of the ESD, send written notice to the Secretary of ESD board by CMRRR.

13 Removal of Territory by Municipality The territory remains part of the ESD and does not become part of the City until the secretary of the ESD board receives the notice. On receipt of the notice, the ESD board must immediately change its records to show that the territory has been disannexed from the ESD and is prohibited from providing further services to the residents of that territory.

14 Removal of Territory by Municipality Holders of any outstanding and unpaid bonds, warrants, or other obligations of the ESD, including loans and lease-purchase agreements, are not impacted by annexation, BUT The municipality must compensate the ESD for share of those obligations immediately after ESD disannexation of the territory. ESD must apply compensation to the payment of the annexed territory's pro rata share of the ESD s obligations.

15 Compensation for Removal The amount of compensation is determined by District s Debt x ( AV of Annexed Area AV of District) District's Debt determined at time of annexation AV determined based on the most recent certified county property tax rolls at the time of annexation. Total indebtedness includes loans and leasepurchase agreements, but does not include: a loan or lease-purchase agreement the district enters into after the district receives notice of the municipality's intent to annex district territory; or any indebtedness attributed to any real or personal property that the district requires a municipality to purchase.

16 Purchase of Property On the ESD s request, a municipality is required to purchase from the ESD - at fair market value - any real or personal property used to provide emergency services in the disannexed territory.

17 The Result

18

19 City Annexation within ESD If City inside an ESD wants to annex territory within the ESD Same Procedures and Requirements Apply City may remove annexed territory from ESD

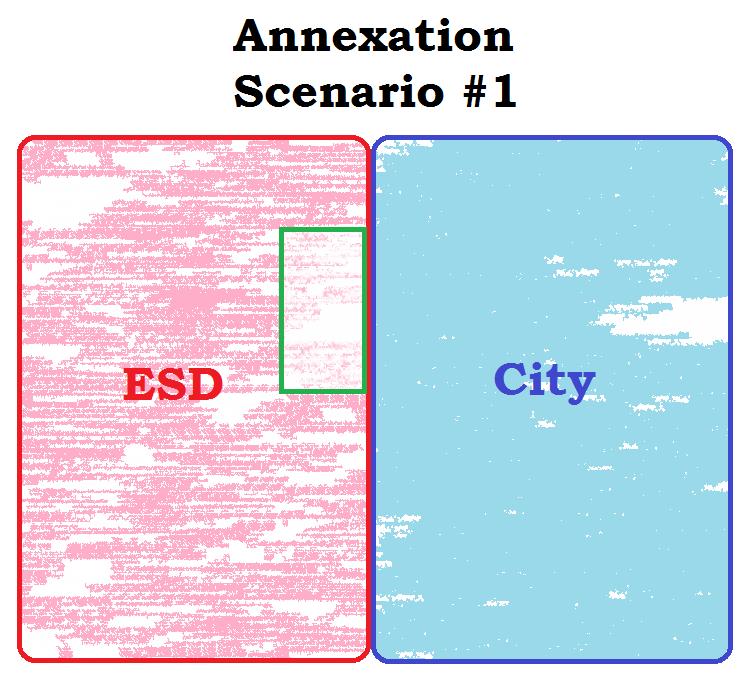

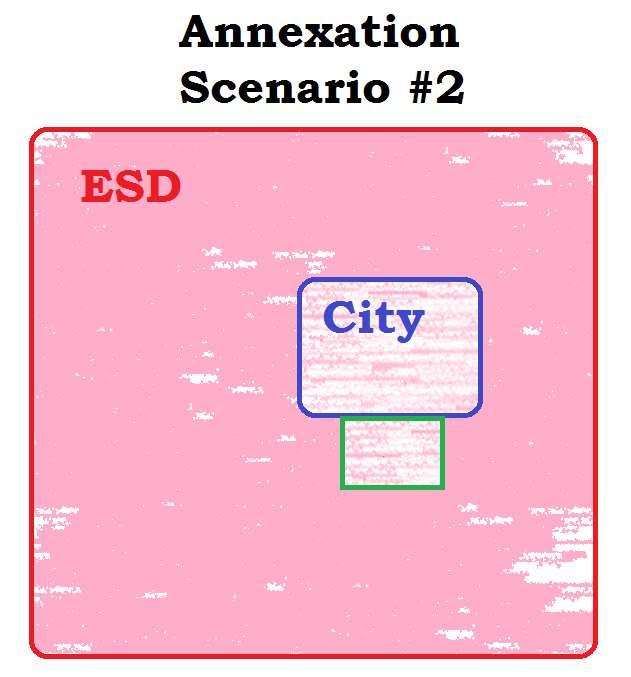

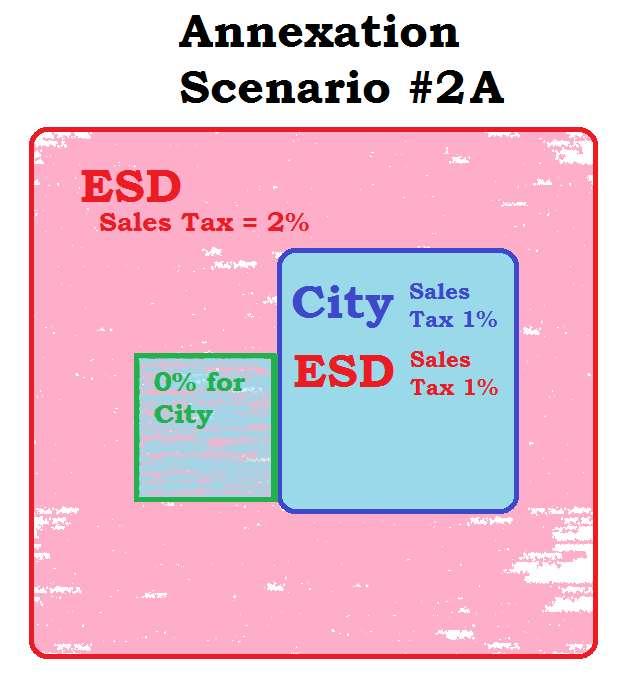

20 City Annexation within ESD City may not want to remove area from ESD if does not provide those emergency services City property tax rates apply within annexed area and must be consistent with rest of City City sales tax expands with City, with some exceptions

21

22 Annexation Challenges ESD needs revenue to operate, especially given $0.10 ad valorem tax cap City wants to promote economic development through tax abatements and other agreements City wants additional tax revenue to keep City s ad valorem tax low

23 Sales Tax Challenges What if City within ESD wants to annex for sales tax revenue? What if remaining 2% local sales tax is already committed to ESD? ESD is authorized to have non-uniform sales tax ( carve out )

24

25 Sales Tax Challenges Annexation results in reduction of ESD (or other political subdivision) sales tax to amount required for total local sales tax to equal 2%, BUT

26 Sales Tax Challenges Comptroller must withhold from the municipality's monthly sales and use tax allocation an amount equal to the amount that would have been collected by the entity had the municipality not imposed or increased its sales and use tax or annexed the area in the entity less amounts that the entity collects following the municipality's levy of or increase in its sales and use tax or annexation of the area in the entity.

27 Sales Tax Challenges Comptroller is required to withhold and pay the amount withheld to the ESD under policies or procedures that the Comptroller considers reasonable. This results in City not receiving full additional sales tax from annexed area that remains in the ESD

28

29 Sales Tax Challenges This process does not apply if and during any period in which an ESD has outstanding indebtedness or obligations that are payable wholly or partly from the sales and use tax revenue of the entity.

30 Solutions But, the law provides options for resolving challenges through: Sales Tax Sharing Agreement Economic Development Agreements Other Interlocal Cooperation Agreements

31 Solutions Sales Tax Sharing Agreement Authorized by ESD Statute Allows City and ESD to agree to allocation of sales tax revenue in the annexed area Comptroller must pay out sales tax pursuant to agreement

32 Solutions Economic Development Agreements Under City s general authority for these types of agreements 380 Tax Agreements 312 Tax Abatement Agreements 311 Tax Increment Financing Others

33 Solutions Interlocal Cooperation Agreements Shared programs Service related Communications Fire Code/Fire Marshal Administration More

34 Things to Remember Communication is Key Early and often Keep Perspective City focus on City residents and taxpayers ESD focus on ESD residents and taxpayers These are not necessarily the same group Vision Think outside the box to achieve win-win

35 Questions? John Carlton

CAROLE KEETON STRAYHORN,

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

Truth-In-Taxation A Guide for Setting School District Tax Rates July 2006 CAROLE KEETON STRAYHORN, Texas Comptroller TEXAS PROPERTY TAX Truth-In-Taxation A Guide for Setting School District Tax Rates

LEGAL COMPLIANCE MANUAL PUBLIC INDEBTEDNESS

PUBLIC INDEBTEDNESS LEGAL COMPLIANCE MANUAL PUBLIC INDEBTEDNESS Introduction The power of a government unit to incur indebtedness is governed by statutory and home rule charter provisions. Statutory provisions

PUBLIC INDEBTEDNESS LEGAL COMPLIANCE MANUAL PUBLIC INDEBTEDNESS Introduction The power of a government unit to incur indebtedness is governed by statutory and home rule charter provisions. Statutory provisions

DATE ISSUED: 3/17/ of 16 UPDATE 104 CCG(LEGAL)-P

-P") Table of Contents Section I: Maintenance Taxes... 2 Tax Rate Cap... 2 Appraisal Roll... 2 Disaster Area... 3 Meeting on Budget and Proposed Tax Rate... 3 Tax Rate... 4 Effective Tax Rate... 5 Maintenance

Table of Contents Section I: Maintenance Taxes... 2 Tax Rate Cap... 2 Appraisal Roll... 2 Disaster Area... 3 Meeting on Budget and Proposed Tax Rate... 3 Tax Rate... 4 Effective Tax Rate... 5 Maintenance

Basic Legal Requirements for the Budget, Tax Rate, and Audit. Bill Longley TML Legislative Counsel

Basic Legal Requirements for the Budget, Tax Rate, and Audit Bill Longley TML Legislative Counsel Key Budget Questions What statute governs budget adoption? Local Government Code Chapter 102 Is an annual

Basic Legal Requirements for the Budget, Tax Rate, and Audit Bill Longley TML Legislative Counsel Key Budget Questions What statute governs budget adoption? Local Government Code Chapter 102 Is an annual

Page 1 of 9 LOCAL GOVERNMENT CODE TITLE 12. PLANNING AND DEVELOPMENT SUBTITLE A. MUNICIPAL PLANNING AND DEVELOPMENT CHAPTER 377. MUNICIPAL DEVELOPMENT DISTRICTS SUBCHAPTER A. GENERAL PROVISIONS Sec. 377.001.

Page 1 of 9 LOCAL GOVERNMENT CODE TITLE 12. PLANNING AND DEVELOPMENT SUBTITLE A. MUNICIPAL PLANNING AND DEVELOPMENT CHAPTER 377. MUNICIPAL DEVELOPMENT DISTRICTS SUBCHAPTER A. GENERAL PROVISIONS Sec. 377.001.

TAX INCREMENT REINVESTMENT ZONE NUMBER ONE CITY OF OAK RIDGE NORTH, TEXAS

TAX INCREMENT REINVESTMENT ZONE NUMBER ONE CITY OF OAK RIDGE NORTH, TEXAS 2015 ANNUAL REPORT Tax Year Ending December 31, 2015 TABLE OF CONTENTS City of Oak Ridge North, Texas 2015 City Council... 1 2015

TAX INCREMENT REINVESTMENT ZONE NUMBER ONE CITY OF OAK RIDGE NORTH, TEXAS 2015 ANNUAL REPORT Tax Year Ending December 31, 2015 TABLE OF CONTENTS City of Oak Ridge North, Texas 2015 City Council... 1 2015

TAX INCREMENT REINVESTMENT ZONE NUMBER ONE CITY OF OAK RIDGE NORTH, TEXAS

TAX INCREMENT REINVESTMENT ZONE NUMBER ONE CITY OF OAK RIDGE NORTH, TEXAS 2016 ANNUAL REPORT Tax Year Ending December 31, 2016 TABLE OF CONTENTS City of Oak Ridge North, Texas 2016 City Council... 1 2016

TAX INCREMENT REINVESTMENT ZONE NUMBER ONE CITY OF OAK RIDGE NORTH, TEXAS 2016 ANNUAL REPORT Tax Year Ending December 31, 2016 TABLE OF CONTENTS City of Oak Ridge North, Texas 2016 City Council... 1 2016

Significant State Statutes. For the Budget Season

Significant State Statutes For the 2016-2017 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2016 Legislative

Significant State Statutes For the 2016-2017 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2016 Legislative

Audit of the Orange County Tax Collector s Office Delinquent Tangible Personal Property Tax Collection Function

Audit of the Orange County Tax Collector s Office Delinquent Tangible Personal Property Tax Collection Function Report by the Office of County Comptroller Martha O. Haynie, CPA County Comptroller County

Audit of the Orange County Tax Collector s Office Delinquent Tangible Personal Property Tax Collection Function Report by the Office of County Comptroller Martha O. Haynie, CPA County Comptroller County

SPECIAL ASSESSMENT DISTRICTS HANDBOOK

SPECIAL ASSESSMENT DISTRICTS HANDBOOK ADOPTED BY THE HIGHLANDS COUNTY BOARD OF COUNTY COMMISSIONERS November 18, 2003 Special Assessment Districts Handbook of Highlands County Table of Contents SECTION

SPECIAL ASSESSMENT DISTRICTS HANDBOOK ADOPTED BY THE HIGHLANDS COUNTY BOARD OF COUNTY COMMISSIONERS November 18, 2003 Special Assessment Districts Handbook of Highlands County Table of Contents SECTION

HARRIS COUNTY EMERGENCY SERVICES DISTRICT NO.

Report on Financial Statements (With Supplemental Material) For the Year Ended December 31, 2017 BREEDLOVE & CO., P.C. CERTIFIED PUBLIC ACCOUNTANTS TABLE OF CONTENTS Independent Auditors Report... 1-2

Report on Financial Statements (With Supplemental Material) For the Year Ended December 31, 2017 BREEDLOVE & CO., P.C. CERTIFIED PUBLIC ACCOUNTANTS TABLE OF CONTENTS Independent Auditors Report... 1-2

Property Tax Rate Adoption: Deadlines, Notices & Hearings

Property Tax Rate Adoption: Deadlines, Notices & Hearings John Kennedy (512) 472-8838 jkennedy@ttara.org www.ttara.org Presented to the TXOGA Property Tax Representatives Annual Conference March 7, 2018

Property Tax Rate Adoption: Deadlines, Notices & Hearings John Kennedy (512) 472-8838 jkennedy@ttara.org www.ttara.org Presented to the TXOGA Property Tax Representatives Annual Conference March 7, 2018

Municipal Finance Basics. Leela Fireside, Assistant City Attorney City of Austin, Law Department 2018

Municipal Finance Basics Leela Fireside, Assistant City Attorney City of Austin, Law Department 2018 1 Overview General Legal Framework Getting Money Spending Money Good Resources to learn more. 2 Getting

Municipal Finance Basics Leela Fireside, Assistant City Attorney City of Austin, Law Department 2018 1 Overview General Legal Framework Getting Money Spending Money Good Resources to learn more. 2 Getting

Northwood Municipal Utility District No. 1

Harris County, Texas Accountants' Report and Financial Statements Contents Independent Accountants' Report on Financial Statements and Supplementary Information... 1 Management's Discussion and Analysis...

Harris County, Texas Accountants' Report and Financial Statements Contents Independent Accountants' Report on Financial Statements and Supplementary Information... 1 Management's Discussion and Analysis...

DATE ISSUED: 1/17/ of 9 UPDATE 112 CCG(LEGAL)-P

-P") Table of Contents Tax Rate Adoption... 2 Maintenance Taxes... 2 Assessor and Collector... 2 Certified Estimate of Values... 2 Appraisal Roll... 2 Truth-in-Taxation Requirements... 3 Tax Rate Adoption Requirements...

Table of Contents Tax Rate Adoption... 2 Maintenance Taxes... 2 Assessor and Collector... 2 Certified Estimate of Values... 2 Appraisal Roll... 2 Truth-in-Taxation Requirements... 3 Tax Rate Adoption Requirements...

GLOSSARY. Adopted Budget - The financial plan of revenues and expenditures for a fiscal year as adopted by the Board of County Commissioners.

GLOSSARY Accrual A revenue or expense which gets recognized in the accounting period it is earned or incurred, even if it is received or paid in a subsequent period. Accrual Accounting - A system that

GLOSSARY Accrual A revenue or expense which gets recognized in the accounting period it is earned or incurred, even if it is received or paid in a subsequent period. Accrual Accounting - A system that

A G E N D A LEWISVILLE MUNICIPAL ANNEX COMMUNITY MEETING ROOM 1197 WEST MAIN STREET AT CIVIC CIRCLE LEWISVILLE, TEXAS

A G E N D A JOINT MEETING OF LEWISVILLE CITY COUNCIL, CRIME CONTROL AND PREVENTION DISTRICT BOARD AND FIRE CONTROL, PREVENTION AND EMERGENCY MEDICAL SERVICES DISTRICT BOARD* SATURDAY, AUGUST 13, 2016 LEWISVILLE

A G E N D A JOINT MEETING OF LEWISVILLE CITY COUNCIL, CRIME CONTROL AND PREVENTION DISTRICT BOARD AND FIRE CONTROL, PREVENTION AND EMERGENCY MEDICAL SERVICES DISTRICT BOARD* SATURDAY, AUGUST 13, 2016 LEWISVILLE

HARRIS COUNTY MUNICIPAL UTILITY DISTRICT NO. 238 HARRIS COUNTY, TEXAS ANNUAL AUDIT REPORT AUGUST 31, 2018

HARRIS COUNTY MUNICIPAL UTILITY DISTRICT NO. 238 HARRIS COUNTY, TEXAS ANNUAL AUDIT REPORT AUGUST 31, 2018 C O N T E N T S INDEPENDENT AUDITOR S REPORT 1-2 MANAGEMENT S DISCUSSION AND ANALYSIS 3-8 BASIC

HARRIS COUNTY MUNICIPAL UTILITY DISTRICT NO. 238 HARRIS COUNTY, TEXAS ANNUAL AUDIT REPORT AUGUST 31, 2018 C O N T E N T S INDEPENDENT AUDITOR S REPORT 1-2 MANAGEMENT S DISCUSSION AND ANALYSIS 3-8 BASIC

HARRIS COUNTY EMERGENCY SERVICES DISTRICT NO.

Report on Financial Statements (With Supplemental Material) For the Year Ended December 31, 2016 BREEDLOVE & CO., P.C. CERTIFIED PUBLIC ACCOUNTANTS TABLE OF CONTENTS Independent Auditors Report... 1-2

Report on Financial Statements (With Supplemental Material) For the Year Ended December 31, 2016 BREEDLOVE & CO., P.C. CERTIFIED PUBLIC ACCOUNTANTS TABLE OF CONTENTS Independent Auditors Report... 1-2

THE TEXAS CONSTITUTION ARTICLE 9. COUNTIES. Sec.A1.AACREATION AND MODIFICATION OF COUNTIES. The

THE TEXAS CONSTITUTION ARTICLE 9. COUNTIES Sec.A1.AACREATION AND MODIFICATION OF COUNTIES. The Legislature shall have power to create counties for the convenience of the people subject to the following

THE TEXAS CONSTITUTION ARTICLE 9. COUNTIES Sec.A1.AACREATION AND MODIFICATION OF COUNTIES. The Legislature shall have power to create counties for the convenience of the people subject to the following

Significant State Statutes. For the Budget Season

Significant State Statutes For the 2017-2018 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2017 Legislative

Significant State Statutes For the 2017-2018 Budget Season Every effort has been made to have the State Statutes contained within to be verbatim and to reflect all changes made during the 2017 Legislative

Tax Computation Manual

Tax Computation Manual 2010 Published by Property Tax Division 150-800-438 (Rev. 10-10) Table of Contents Introduction...ii Key Dates...iii Property Tax Computation Flowchart...iv Chapter 1 Certification

Tax Computation Manual 2010 Published by Property Tax Division 150-800-438 (Rev. 10-10) Table of Contents Introduction...ii Key Dates...iii Property Tax Computation Flowchart...iv Chapter 1 Certification

16 th Annual Riley Fletcher Basic Municipal Law Seminar Austin, Texas Thursday, February 5, 2015

16 th Annual Riley Fletcher Basic Municipal Law Seminar Austin, Texas Thursday, February 5, 2015 Kuruvilla (K.O.) Oommen Deputy City Attorney City of Irving, Texas Handbook for Mayors and Councilmembers

16 th Annual Riley Fletcher Basic Municipal Law Seminar Austin, Texas Thursday, February 5, 2015 Kuruvilla (K.O.) Oommen Deputy City Attorney City of Irving, Texas Handbook for Mayors and Councilmembers

IC Chapter 14. Redevelopment of Areas Needing Redevelopment Generally; Redevelopment Commissions

IC 36-7-14 Chapter 14. Redevelopment of Areas Needing Redevelopment Generally; Redevelopment Commissions IC 36-7-14-1 Application of chapter; jurisdiction in excluded cities that elect to be governed by

IC 36-7-14 Chapter 14. Redevelopment of Areas Needing Redevelopment Generally; Redevelopment Commissions IC 36-7-14-1 Application of chapter; jurisdiction in excluded cities that elect to be governed by

2017 Tax Rate Calculation Worksheet Date: 08/10/ :17 AM Taxing Units Other Than School Districts or Water Districts

2017 Tax Rate Calculation Worksheet Date: 08/10/2017 11:17 AM Taxing Units Other Than School Districts or Water Districts City of Dalworthington Gardens Taxing Unit Name Phone (area code and number) Taxing

2017 Tax Rate Calculation Worksheet Date: 08/10/2017 11:17 AM Taxing Units Other Than School Districts or Water Districts City of Dalworthington Gardens Taxing Unit Name Phone (area code and number) Taxing

IC Chapter 41. Cumulative Fund Tax Levy Procedures

IC 6-1.1-41 Chapter 41. Cumulative Fund Tax Levy Procedures IC 6-1.1-41-1 Application of chapter Sec. 1. This chapter applies to establishing and imposing a tax levy for cumulative funds under the following:

IC 6-1.1-41 Chapter 41. Cumulative Fund Tax Levy Procedures IC 6-1.1-41-1 Application of chapter Sec. 1. This chapter applies to establishing and imposing a tax levy for cumulative funds under the following:

HARRIS COUNTY, TEXAS

HARRIS COUNTY, TEXAS COMMISSIONERS COURT: c/o Community Services Dept. ED EMMETT. 8410 Lantern Point Drive COUNTY JUDGE Houston, Texas 77054 EL FRANCO LEE (713) 578-2000 COMMISSIONER, PRECINCT 1 SYLVIA

HARRIS COUNTY, TEXAS COMMISSIONERS COURT: c/o Community Services Dept. ED EMMETT. 8410 Lantern Point Drive COUNTY JUDGE Houston, Texas 77054 EL FRANCO LEE (713) 578-2000 COMMISSIONER, PRECINCT 1 SYLVIA

CERTIFICATION OF TAXABLE VALUE

CRTIFICATION OF TAXABL VALU Year : 218 County : VOLUSIA Principal Authority : Taxing Authority : HOLLY HILL HOLLY HILL OPRATING Reset Form Print Form DR-42 Rule 12D-16.2 Florida Administrative Code ffective

CRTIFICATION OF TAXABL VALU Year : 218 County : VOLUSIA Principal Authority : Taxing Authority : HOLLY HILL HOLLY HILL OPRATING Reset Form Print Form DR-42 Rule 12D-16.2 Florida Administrative Code ffective

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 SESSION LAW HOUSE BILL 129

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 SESSION LAW 2011-84 HOUSE BILL 129 AN ACT TO PROTECT JOBS AND INVESTMENT BY REGULATING LOCAL GOVERNMENT COMPETITION WITH PRIVATE BUSINESS. Whereas, certain

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 SESSION LAW 2011-84 HOUSE BILL 129 AN ACT TO PROTECT JOBS AND INVESTMENT BY REGULATING LOCAL GOVERNMENT COMPETITION WITH PRIVATE BUSINESS. Whereas, certain

Special Taxing Districts in North Carolina. Kara A. Millonzi Associate Professor of Public Law and Government UNC Chapel Hill School of Government

Special Taxing Districts in North Carolina Kara A. Millonzi Associate Professor of Public Law and Government UNC Chapel Hill School of Government Can you legally commit a portion of property tax proceeds

Special Taxing Districts in North Carolina Kara A. Millonzi Associate Professor of Public Law and Government UNC Chapel Hill School of Government Can you legally commit a portion of property tax proceeds

King County Fire Protection District No. 44 (Mountain View Fire and Rescue)

") Financial Statements Audit Report King County Fire Protection District No. 44 (Mountain View Fire and Rescue) For the period January 1, 2017 through December 31, 2017 Published January 24, 2019 Report

Financial Statements Audit Report King County Fire Protection District No. 44 (Mountain View Fire and Rescue) For the period January 1, 2017 through December 31, 2017 Published January 24, 2019 Report

TAX LIMITATION AND OPT OUT INFORMATION FOR ALL TAXING DISTRICTS. (Except School Districts) For Taxes Payable in Calendar Year 2012

For Taxes Payable in Calendar Year 2012") TAX LIMITATION AND OPT OUT INFORMATION FOR ALL TAXING DISTRICTS (Except School Districts) For Taxes Payable in Calendar Year 2012 INFORMATION PROVIDED BY: DEPARTMENT OF REVENUE PROPERTY & SPECIAL TAX DIVISION

TAX LIMITATION AND OPT OUT INFORMATION FOR ALL TAXING DISTRICTS (Except School Districts) For Taxes Payable in Calendar Year 2012 INFORMATION PROVIDED BY: DEPARTMENT OF REVENUE PROPERTY & SPECIAL TAX DIVISION

IC Chapter 38. Food and Beverage Taxes in Wayne County

IC 6-9-38 Chapter 38. Food and Beverage Taxes in Wayne County IC 6-9-38-1 Application of chapter Sec. 1. This chapter applies to a county having a population of more than sixty-eight thousand nine hundred

IC 6-9-38 Chapter 38. Food and Beverage Taxes in Wayne County IC 6-9-38-1 Application of chapter Sec. 1. This chapter applies to a county having a population of more than sixty-eight thousand nine hundred

PERSONAL PROPERTY TAX RELIEF ACT SPECIAL REVIEW SEPTEMBER 2004

PERSONAL PROPERTY TAX RELIEF ACT SPECIAL REVIEW SEPTEMBER 2004 EXECUTIVE SUMMARY We have completed our study of the Personal Property Tax Relief Act (the Act) as amended by Chapter 1 of the Act of Assembly

PERSONAL PROPERTY TAX RELIEF ACT SPECIAL REVIEW SEPTEMBER 2004 EXECUTIVE SUMMARY We have completed our study of the Personal Property Tax Relief Act (the Act) as amended by Chapter 1 of the Act of Assembly

McCreary Veselka Bragg & Allen P.C. Attorneys at Law. A Guide for Setting Tax Rates

McCreary Veselka Bragg & Allen P.C. Attorneys at Law A Guide for Setting Tax Rates TRUTH-IN-TAXATION 2018 for Our Clients We are pleased to present this easy-to-use guidebook to help you with this year

McCreary Veselka Bragg & Allen P.C. Attorneys at Law A Guide for Setting Tax Rates TRUTH-IN-TAXATION 2018 for Our Clients We are pleased to present this easy-to-use guidebook to help you with this year

IC Chapter 14. Miscellaneous Provisions

IC 5-1-14 Chapter 14. Miscellaneous Provisions IC 5-1-14-1 Bonds, notes, or warrants not subject to maximum interest rate limitations Sec. 1. (a) Any bonds, notes, or warrants, whether payable from property

IC 5-1-14 Chapter 14. Miscellaneous Provisions IC 5-1-14-1 Bonds, notes, or warrants not subject to maximum interest rate limitations Sec. 1. (a) Any bonds, notes, or warrants, whether payable from property

King County Fire Protection District No. 44 (Mountain View Fire and Rescue)

") Financial Statements Audit Report King County Fire Protection District No. 44 (Mountain View Fire and Rescue) For the period January 1, 2016 through December 31, 2016 Published January 4, 2018 Report No.

Financial Statements Audit Report King County Fire Protection District No. 44 (Mountain View Fire and Rescue) For the period January 1, 2016 through December 31, 2016 Published January 4, 2018 Report No.

RESOLUTION NO A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF CASTLE PINES, COLORADO, CERTIFYING THE MILL LEVY

RESOLUTION NO. 12-69 A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF CASTLE PINES, COLORADO, CERTIFYING THE MILL LEVY WHEREAS, the City Manager serving as the City Budget Officer prepared and presented

RESOLUTION NO. 12-69 A RESOLUTION OF THE CITY COUNCIL OF THE CITY OF CASTLE PINES, COLORADO, CERTIFYING THE MILL LEVY WHEREAS, the City Manager serving as the City Budget Officer prepared and presented

Maryland Wage Payment and Collection Law ("MWPCL")

") Maryland Wage Payment and Collection Law ("MWPCL") Md. Code, Lab. & Empl. Art., 3-501 et seq. 3-501. Definitions... 1 3-502. Payment of wage... 1 3-503. Deductions... 2 3-504. Notice of wages and paydays...

Maryland Wage Payment and Collection Law ("MWPCL") Md. Code, Lab. & Empl. Art., 3-501 et seq. 3-501. Definitions... 1 3-502. Payment of wage... 1 3-503. Deductions... 2 3-504. Notice of wages and paydays...

The Mysterious Property Tax Limitations

The Mysterious Property Tax Limitations Presented by Diann Locke Levies & Appeals Specialist Department of Revenue Property Tax Limitations Regular levies are subject to various limitations: 1. Budget

The Mysterious Property Tax Limitations Presented by Diann Locke Levies & Appeals Specialist Department of Revenue Property Tax Limitations Regular levies are subject to various limitations: 1. Budget

County of El Paso Guidelines and Criteria For Tax Abatement Assistance

County of El Paso Guidelines and Criteria For Tax Abatement Assistance I. AUTHORIZATION The County of El Paso is authorized to provide tax abatement benefits in accordance with the State of Texas Property

County of El Paso Guidelines and Criteria For Tax Abatement Assistance I. AUTHORIZATION The County of El Paso is authorized to provide tax abatement benefits in accordance with the State of Texas Property

Municipal Utility District ( MUD )

") Municipal Utility District ( MUD ) vs. Public Improvement District ( PID ) vs. Tax Increment Reinvestment Zone ( TIRZ ) The following identifies certain pertinent matters relating to, and comparing, Municipal

Municipal Utility District ( MUD ) vs. Public Improvement District ( PID ) vs. Tax Increment Reinvestment Zone ( TIRZ ) The following identifies certain pertinent matters relating to, and comparing, Municipal

Senate Bill No. 1 Committee of the Whole

Senate Bill No. 1 Committee of the Whole CHAPTER... AN ACT relating to commerce; providing for the issuance of transferable tax credits and the partial abatement of certain taxes to a project that satisfies

Senate Bill No. 1 Committee of the Whole CHAPTER... AN ACT relating to commerce; providing for the issuance of transferable tax credits and the partial abatement of certain taxes to a project that satisfies

AGENDA BACKGROUND. Date: August 7, AGENDA ITEM: Discuss and review the Budget for the Fiscal Year PRESENTER:

1 2 AGENDA BACKGROUND AGENDA ITEM: Discuss and review the Budget for the Fiscal Year 2017-2018. Date: August 7, 2017 PRESENTER: Matt Fielder, City Manager BACKGROUND: The purpose of this item is to discuss

1 2 AGENDA BACKGROUND AGENDA ITEM: Discuss and review the Budget for the Fiscal Year 2017-2018. Date: August 7, 2017 PRESENTER: Matt Fielder, City Manager BACKGROUND: The purpose of this item is to discuss

Emergency Services Volunteer Length of Service Award Program Act P.L. 1997, c. 388, as amended by P.L. 2001, c. 272

C.40A:14-183 Short Title. C.40A:14-184 Definitions relative to retirement benefits for certain municipal emergency services volunteers. C.40A:14-185 Establishment, termination of length of service award

C.40A:14-183 Short Title. C.40A:14-184 Definitions relative to retirement benefits for certain municipal emergency services volunteers. C.40A:14-185 Establishment, termination of length of service award

Published on e-li (https://ctas-eli.ctas.tennessee.edu) February 10, 2018 Capital Funding Sources and Debt Financing

February 10, 2018 Capital Funding Sources and Debt Financing") Published on e-li (https://ctas-eli.ctas.tennessee.edu) February 10, 2018 Capital Funding Sources and Debt Financing Dear Reader: The following document was created from the CTAS electronic library known

Published on e-li (https://ctas-eli.ctas.tennessee.edu) February 10, 2018 Capital Funding Sources and Debt Financing Dear Reader: The following document was created from the CTAS electronic library known

Plan of Reorganization

Initial Plan of Reorganization Whiteland Fire Protection Prepared by the Legislative Bodies of the Town of Whiteland and The Whiteland Fire Protection District Dated: A. Introduction The Town of Whiteland

Initial Plan of Reorganization Whiteland Fire Protection Prepared by the Legislative Bodies of the Town of Whiteland and The Whiteland Fire Protection District Dated: A. Introduction The Town of Whiteland

Municipal Revenue Sources & the Hancock Amendment Presented June 16, 2011 by Joe Lauber Missouri Municipal League Elected Officials Training Seminar

Municipal Revenue Sources & the Hancock Amendment Presented June 16, 2011 by Joe Lauber Missouri Municipal League Elected Officials Training Seminar Serving those who serve the public Overview of Topics

Municipal Revenue Sources & the Hancock Amendment Presented June 16, 2011 by Joe Lauber Missouri Municipal League Elected Officials Training Seminar Serving those who serve the public Overview of Topics

Town of Babylon Industrial Agency Uniform Tax Exemption Policy & Guidelines

Town of Babylon Industrial Agency Uniform Tax Exemption Policy & Guidelines It is recognized that under the provisions of Article 18-A of the General Municipal Law the (the Act ) Town of Babylon Industrial

Town of Babylon Industrial Agency Uniform Tax Exemption Policy & Guidelines It is recognized that under the provisions of Article 18-A of the General Municipal Law the (the Act ) Town of Babylon Industrial

GUIDELINES AND CRITERIA FOR GRANTING TAX ABATEMENT IN A REINVESTMENT ZONE CREATED IN BRAZORIA COUNTY

GUIDELINES AND CRITERIA FOR GRANTING TAX ABATEMENT IN A REINVESTMENT ZONE CREATED IN BRAZORIA COUNTY WHEREAS, the creation, retention and diversification of job opportunities that bring new wealth are

GUIDELINES AND CRITERIA FOR GRANTING TAX ABATEMENT IN A REINVESTMENT ZONE CREATED IN BRAZORIA COUNTY WHEREAS, the creation, retention and diversification of job opportunities that bring new wealth are

RE: TAX LEVY INFORMATION

Board Member: October 14, 2010 RE: TAX LEVY INFORMATION Cook County Multiplier/Level of Assessments Over the past year, a fundamental change in the property tax assessment process for Cook County was enacted

Board Member: October 14, 2010 RE: TAX LEVY INFORMATION Cook County Multiplier/Level of Assessments Over the past year, a fundamental change in the property tax assessment process for Cook County was enacted

CERTIFICATION OF TAXABLE VALUE

CRTIFICATION OF TAXABL VALU Year : 2017 County : HNDRY Principal Authority : Taxing Authority : Reset Form Print Form DR-420 Rule 12D-16.002 Florida Administrative Code ffective 11/12 SCTION I : COMPLTD

CRTIFICATION OF TAXABL VALU Year : 2017 County : HNDRY Principal Authority : Taxing Authority : Reset Form Print Form DR-420 Rule 12D-16.002 Florida Administrative Code ffective 11/12 SCTION I : COMPLTD

Financing for Jax-Florida

Financing for Jax-Florida A) What are the financing alternatives to bring Jax-Florida to Collier County? The productivity committee has identified 7 funding alternatives: a franchise fee, three property

Financing for Jax-Florida A) What are the financing alternatives to bring Jax-Florida to Collier County? The productivity committee has identified 7 funding alternatives: a franchise fee, three property

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2011 HOUSE DRH70039-LM-18B* (02/01) Short Title: Level Playing Field/Local Gov't Competition.

Short Title: Level Playing Field/Local Gov't Competition.") H GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 HOUSE DRH00-LM-B* (0/0) D Short Title: Level Playing Field/Local Gov't Competition. (Public) Sponsors: Referred to: Representative Avila. 0 0 0 A BILL TO

H GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 0 HOUSE DRH00-LM-B* (0/0) D Short Title: Level Playing Field/Local Gov't Competition. (Public) Sponsors: Referred to: Representative Avila. 0 0 0 A BILL TO

A History of. Property Taxes in

A History of Property Taxes in Austin and Travis County Presented by: 4210 SPICEWOOD SPRINGS ROAD, SUITE 211 AUSTIN, TEXAS 78759 512.302.5800 Ad Valorem Property Taxes Executive Summary The consistent

A History of Property Taxes in Austin and Travis County Presented by: 4210 SPICEWOOD SPRINGS ROAD, SUITE 211 AUSTIN, TEXAS 78759 512.302.5800 Ad Valorem Property Taxes Executive Summary The consistent

King County Fire Protection District No. 44 (Mountain View Fire and Rescue)

") Financial Statements Audit Report King County Fire Protection District No. 44 (Mountain View Fire and Rescue) For the period January 1, 2015 through December 31, 2015 Published February 2, 2017 Report

Financial Statements Audit Report King County Fire Protection District No. 44 (Mountain View Fire and Rescue) For the period January 1, 2015 through December 31, 2015 Published February 2, 2017 Report

AN ACT. Be it enacted by the General Assembly of the State of Ohio:

(131st General Assembly) (Amended Substitute House Bill Number 233) AN ACT To amend sections 133.04, 133.06, 149.311, 709.024, 709.19, 3317.021, 4582.56, 5501.311, 5709.12, 5709.121, 5709.82, 5709.83,

(131st General Assembly) (Amended Substitute House Bill Number 233) AN ACT To amend sections 133.04, 133.06, 149.311, 709.024, 709.19, 3317.021, 4582.56, 5501.311, 5709.12, 5709.121, 5709.82, 5709.83,

2017 Effective Tax Rate Worksheet DUMAS CITY

Page 1 of 14 2017 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2016 total taxable value. Enter the amount of 2016 taxable value on the 2016 tax roll

Page 1 of 14 2017 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2016 total taxable value. Enter the amount of 2016 taxable value on the 2016 tax roll

UNIFORM TAX EXEMPTION POLICY

UCIDA Ulster County Industrial Development Agency UNIFORM TAX EXEMPTION POLICY SECTION 1. PURPOSE AND AUTHORITY. Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law

UCIDA Ulster County Industrial Development Agency UNIFORM TAX EXEMPTION POLICY SECTION 1. PURPOSE AND AUTHORITY. Pursuant to Section 874(4)(a) of Title One of Article 18-A of the General Municipal Law

There is no legal debt limit for counties in Virginia, since the issuance of all county general obligation debt is subject to referendum.

DEBT MANAGEMENT DEBT MANAGEMENT AND POLICIES Pursuant to the Constitution of Virginia and the Public Finance Act, the County is authorized to issue general obligation bonds secured by a pledge of its full

DEBT MANAGEMENT DEBT MANAGEMENT AND POLICIES Pursuant to the Constitution of Virginia and the Public Finance Act, the County is authorized to issue general obligation bonds secured by a pledge of its full

Department of Revenue Analysis of H.F. 751 (Abrams) / S.F. 748 (Belanger) As Proposed to Be Amended

/ S.F. 748 (Belanger) As Proposed to Be Amended") Governor s Tax Bill Original and Supplemental Proposals April 4, 2003 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 751 (Abrams)

Governor s Tax Bill Original and Supplemental Proposals April 4, 2003 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 751 (Abrams)

through : Repealed by Session Laws 1995 (Regular Session, 1996), c. 747, s. 6.

, c. 747, s. 6.") Article 84. Local Firefighters' Relief Funds. 58-84-1: Repealed by Session Laws 2006-196, s. 6, effective January 1, 2008, and applicable to proceeds credited to the Department of Insurance on or after

Article 84. Local Firefighters' Relief Funds. 58-84-1: Repealed by Session Laws 2006-196, s. 6, effective January 1, 2008, and applicable to proceeds credited to the Department of Insurance on or after

HOUSE BILL 1224: Local Options Sales Tax for Education/Tax and Econ. Dev. Fund Modifications

2013-2014 General Assembly HOUSE BILL 1224: Local Options Sales Tax for Education/Tax and Econ. Dev. Fund Modifications Committee: Senate Finance Date: July 14, 2014 Introduced by: Rep. Presnell Prepared

2013-2014 General Assembly HOUSE BILL 1224: Local Options Sales Tax for Education/Tax and Econ. Dev. Fund Modifications Committee: Senate Finance Date: July 14, 2014 Introduced by: Rep. Presnell Prepared

Art Development Corporation Act of Short title. Definitions

Art. 5190.6. Development Corporation Act of 1979 Short title Sec. 1. This Act may be cited as the "Development Corporation Act of 1979." Definitions Sec. 2. Wherever used in this Act unless a different

Art. 5190.6. Development Corporation Act of 1979 Short title Sec. 1. This Act may be cited as the "Development Corporation Act of 1979." Definitions Sec. 2. Wherever used in this Act unless a different

SUBCHAPTER VIII. LOCAL GOVERNMENT SALES AND USE TAX.

SUBCHAPTER VIII. LOCAL GOVERNMENT SALES AND USE TAX. Article 39. First One-Cent (1 ) Local Government Sales and Use Tax. 105-463. Short title. This Article shall be known as the First One-Cent (1 ) Local

SUBCHAPTER VIII. LOCAL GOVERNMENT SALES AND USE TAX. Article 39. First One-Cent (1 ) Local Government Sales and Use Tax. 105-463. Short title. This Article shall be known as the First One-Cent (1 ) Local

CHAPTER Senate Bill No. 2142

CHAPTER 2011-67 Senate Bill No. 2142 An act relating to water management districts; amending s. 373.503, F.S.; removing obsolete provisions; requiring the Legislature to annually review the preliminary

CHAPTER 2011-67 Senate Bill No. 2142 An act relating to water management districts; amending s. 373.503, F.S.; removing obsolete provisions; requiring the Legislature to annually review the preliminary

Proposed Omega Bay TIRZ. City of La Marque Public Hearing January 14, 2019

Proposed Omega Bay TIRZ City of La Marque Public Hearing January 14, 2019 Outline TIRZ Definition and How They Work TIRZ Creation Process Composition & Role of the Board of Directors Omega Bay TIRZ Concept

Proposed Omega Bay TIRZ City of La Marque Public Hearing January 14, 2019 Outline TIRZ Definition and How They Work TIRZ Creation Process Composition & Role of the Board of Directors Omega Bay TIRZ Concept

VILLAGE OF LAKEVIEW LOGAN COUNTY, OHIO

AUDIT REPORT FOR THE YEARS ENDED DECEMBER 31, 2009 & 2008 Charles E. Harris and Associates, Inc. Certified Public Accountants and Government Consultants Village Council Village of Lakeview 125 N. Main

AUDIT REPORT FOR THE YEARS ENDED DECEMBER 31, 2009 & 2008 Charles E. Harris and Associates, Inc. Certified Public Accountants and Government Consultants Village Council Village of Lakeview 125 N. Main

2018 Tax Rate Calculation Worksheet

2018 Tax Rate Calculation Worksheet Taxing Units Other Than School Districts or Water Districts GENERAL INFORMATION: Tax Code Section 26.04(c) requires an officer or employee designated by the governing

2018 Tax Rate Calculation Worksheet Taxing Units Other Than School Districts or Water Districts GENERAL INFORMATION: Tax Code Section 26.04(c) requires an officer or employee designated by the governing

Heritage Harbour North Community Development District

Heritage Harbour North Community Development District FINANCIAL STATEMENTS September 30, 2015 Table of Contents September 30, 2015 Independent Auditors Report 1 Financial Statements: Management s Discussion

Heritage Harbour North Community Development District FINANCIAL STATEMENTS September 30, 2015 Table of Contents September 30, 2015 Independent Auditors Report 1 Financial Statements: Management s Discussion

MONTGOMERY COUNTY EMERGENCY SERVICES DISTRICT NO. 8

MONTGOMERY COUNTY EMERGENCY SERVICES DISTRICT NO. 8 MONTGOMERY COUNTY, TEXAS ANNUAL FINANCIAL REPORT McCALL GIBSON SWEDLUND BARFOOT PLLC Certified Public Accountants MONTGOMERY COUNTY EMERGENCY SERVICES

MONTGOMERY COUNTY EMERGENCY SERVICES DISTRICT NO. 8 MONTGOMERY COUNTY, TEXAS ANNUAL FINANCIAL REPORT McCALL GIBSON SWEDLUND BARFOOT PLLC Certified Public Accountants MONTGOMERY COUNTY EMERGENCY SERVICES

Tarrant County s Outstanding Debt

The following financial information was obtained from Commissioners Court archive records and Series Official Statements. The original issue premium associated with sale of the s is included in the. Refunding

The following financial information was obtained from Commissioners Court archive records and Series Official Statements. The original issue premium associated with sale of the s is included in the. Refunding

Fiscal Year 2018 COMMUNITY REDEVELOPMENT AGENCY (CRA) PROFILE

PROFILE") Fiscal Year 2018 COMMUNITY REDEVELOPMENT AGENCY (CRA) PROFILE NAME OF ENTITY Lauderdale Lakes Community Redevelopment Agency PURPOSE OF ENTITY The Lauderdale Lakes Community Redevelopment Agency (CRA)

Fiscal Year 2018 COMMUNITY REDEVELOPMENT AGENCY (CRA) PROFILE NAME OF ENTITY Lauderdale Lakes Community Redevelopment Agency PURPOSE OF ENTITY The Lauderdale Lakes Community Redevelopment Agency (CRA)

FINANCIAL MANAGEMENT PERFORMANCE CRITERIA

The City Council originally adopted the Financial Management Performance Criteria (FMPC) on March 15, 1978 to provide standards and guidelines for the City s financial managerial decision making and to

The City Council originally adopted the Financial Management Performance Criteria (FMPC) on March 15, 1978 to provide standards and guidelines for the City s financial managerial decision making and to

Abatements and Refunds

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

Abatements and Refunds Janeen Ogden Colorado Division of Property Taxation CCTA Conference Colorado Springs, Colorado June 29, 2010 1 Abatements & Refunds Definitions Need for Abatements History of Abatement

Mecklenburg County Fire Protection Service Districts Report

Mecklenburg County Fire Protection Service Districts Report February 21, 2012 1 Part 1: Overview Background and Justification The County proposes a new funding vehicle for delivery of fire protection services

Mecklenburg County Fire Protection Service Districts Report February 21, 2012 1 Part 1: Overview Background and Justification The County proposes a new funding vehicle for delivery of fire protection services

CITY OF MIDLOTHIAN SCHEDULE OF TAX ABATEMENT EVENTS

STEP 1 STEP 2 STEP 3 STEP 4 STEP 5 STEP 6 STEP 7 STEP 8 STEP 9 STEP 10 Request Tax Abatement information and application form. Application for abatement received by MED/City. Discussions with applicant

STEP 1 STEP 2 STEP 3 STEP 4 STEP 5 STEP 6 STEP 7 STEP 8 STEP 9 STEP 10 Request Tax Abatement information and application form. Application for abatement received by MED/City. Discussions with applicant

ADOPTED REGULATION OF THE COMMITTEE ON LOCAL GOVERNMENT FINANCE. LCB File No. R022-08

ADOPTED REGULATION OF THE COMMITTEE ON LOCAL GOVERNMENT FINANCE LCB File No. R022-08 Effective on April 17, 2008, for the purposes of budgeting and making any calculations required for planning and budgeting

ADOPTED REGULATION OF THE COMMITTEE ON LOCAL GOVERNMENT FINANCE LCB File No. R022-08 Effective on April 17, 2008, for the purposes of budgeting and making any calculations required for planning and budgeting

St. Francis Area Schools

2018 Payable 2019 Truth In Taxation Public Meeting 7:00 pm December 10, 2018 at the District Office Community Room Truth in Taxation Law Minnesota s Truth in Taxation Law requires that cities, counties

2018 Payable 2019 Truth In Taxation Public Meeting 7:00 pm December 10, 2018 at the District Office Community Room Truth in Taxation Law Minnesota s Truth in Taxation Law requires that cities, counties

ARTICLE 13 SCIENTIFIC AND CULTURAL FACILITIES DISTRICT

Document 1 of 20 CULTURAL FACILITIES DISTRICT ARTICLE 13 SCIENTIFIC AND CULTURAL FACILITIES DISTRICT Editor's note: For a discussion of the difference between service authorities authorized by section

Document 1 of 20 CULTURAL FACILITIES DISTRICT ARTICLE 13 SCIENTIFIC AND CULTURAL FACILITIES DISTRICT Editor's note: For a discussion of the difference between service authorities authorized by section

Title 35-A: PUBLIC UTILITIES

Title 35-A: PUBLIC UTILITIES Chapter 29: MAINE PUBLIC UTILITY FINANCING BANK ACT Table of Contents Part 2. PUBLIC UTILITIES... Section 2901. TITLE... 3 Section 2902. FINDINGS AND DECLARATION OF PURPOSE...

Title 35-A: PUBLIC UTILITIES Chapter 29: MAINE PUBLIC UTILITY FINANCING BANK ACT Table of Contents Part 2. PUBLIC UTILITIES... Section 2901. TITLE... 3 Section 2902. FINDINGS AND DECLARATION OF PURPOSE...

AGENDA BACKGROUND. Date: August 6, AGENDA ITEM: Discuss and review the Budget for the Fiscal Year PRESENTER:

1 2 AGENDA BACKGROUND AGENDA ITEM: Discuss and review the Budget for the Fiscal Year 2018-2019. Date: August 6, 2018 PRESENTER: Matt Fielder, City Manager BACKGROUND: The purpose of this item is to discuss

1 2 AGENDA BACKGROUND AGENDA ITEM: Discuss and review the Budget for the Fiscal Year 2018-2019. Date: August 6, 2018 PRESENTER: Matt Fielder, City Manager BACKGROUND: The purpose of this item is to discuss

TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES

PTO TM #16-01 TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules within the Property Tax Oversight Program. RULE

PTO TM #16-01 TRANSMITTAL MEMORANDUM PROPERTY TAX OVERSIGHT RULES PURPOSE: This transmittal memorandum contains changes to the Department of Revenue Rules within the Property Tax Oversight Program. RULE

Board of Supervisors WAYNE COUNTY

Board of Supervisors WAYNE COUNTY RESOLUTION NO. 529-11: ADOPT A LOCAL LAW AMENDING WAYNE COUNTY S SELF INSURANCE PLAN FOR WORKER S COMPENSATION Mrs. Collier presented the following: WHEREAS, a proposed

Board of Supervisors WAYNE COUNTY RESOLUTION NO. 529-11: ADOPT A LOCAL LAW AMENDING WAYNE COUNTY S SELF INSURANCE PLAN FOR WORKER S COMPENSATION Mrs. Collier presented the following: WHEREAS, a proposed

75th OREGON LEGISLATIVE ASSEMBLY Regular Session. Enrolled. Senate Bill 916 CHAPTER... AN ACT

75th OREGON LEGISLATIVE ASSEMBLY--2009 Regular Session Sponsored by Senator MORSE Enrolled Senate Bill 916 CHAPTER... AN ACT Relating to local government budgets; creating new provisions; and amending

75th OREGON LEGISLATIVE ASSEMBLY--2009 Regular Session Sponsored by Senator MORSE Enrolled Senate Bill 916 CHAPTER... AN ACT Relating to local government budgets; creating new provisions; and amending

ST. TAMMANY PARISH FIRE PROTECTION DISTRICT NO. 3

05JUL20 ;.:;!!: 06 ST. TAMMANY PARISH FIRE PROTECTION DISTRICT NO. 3 December 31,2004 Audit of Financial Statements Under provisions of state law, this report is a public document. Acopy of the report

05JUL20 ;.:;!!: 06 ST. TAMMANY PARISH FIRE PROTECTION DISTRICT NO. 3 December 31,2004 Audit of Financial Statements Under provisions of state law, this report is a public document. Acopy of the report

State Tax Return. Another Blow To State And Local Funding Options -- Georgia Supreme Court Diminishes The Value Of "Tax Allocation District" Funding

April 2008 State Tax Return Volume 15 Number 2 Another Blow To State And Local Funding Options -- Georgia Supreme Court Diminishes The Value Of "Tax Allocation District" Funding E. Kendrick Smith Mace

April 2008 State Tax Return Volume 15 Number 2 Another Blow To State And Local Funding Options -- Georgia Supreme Court Diminishes The Value Of "Tax Allocation District" Funding E. Kendrick Smith Mace

Florida Legislative Committee on Intergovernmental Relations

Jeff Atwater President Florida Legislative Committee on Intergovernmental Relations Issue Brief Utilization of Local Option Sales Taxes by Florida Counties in Fiscal Year 2009-10 November 2009 Larry Cretul

Jeff Atwater President Florida Legislative Committee on Intergovernmental Relations Issue Brief Utilization of Local Option Sales Taxes by Florida Counties in Fiscal Year 2009-10 November 2009 Larry Cretul

TAX RATE ADOPTION & NOTICES

Oldham County Judge Don R. Allred TAX RATE ADOPTION & NOTICES!! 26.01 Submission of Rolls to Taxing Unit!! (a) By July 25 the chief appraiser shall prepare and certify to the assessor the appraisal roll.!!

Oldham County Judge Don R. Allred TAX RATE ADOPTION & NOTICES!! 26.01 Submission of Rolls to Taxing Unit!! (a) By July 25 the chief appraiser shall prepare and certify to the assessor the appraisal roll.!!

Vistancia Community Facilities District Peoria, Arizona. Financial Report

Vistancia Community Facilities District Peoria, Arizona Financial Report For Fiscal Year Ended June 30, 2004 District Board: John Keegan, Chairman Bob Barrett Pat Dennis Ken Forgia Vicki Hunt Carlo Leone

Vistancia Community Facilities District Peoria, Arizona Financial Report For Fiscal Year Ended June 30, 2004 District Board: John Keegan, Chairman Bob Barrett Pat Dennis Ken Forgia Vicki Hunt Carlo Leone

Economic Development Program Administration

Economic Development Program Administration 1 Erin Clark, RTA, EDFP o City of Arlington Public Finance Administrator for 8 years o 18 years total with City of Arlington o Bachelor of Business Administration/Management

Economic Development Program Administration 1 Erin Clark, RTA, EDFP o City of Arlington Public Finance Administrator for 8 years o 18 years total with City of Arlington o Bachelor of Business Administration/Management

NOW THEREFORE, BE IT RESOLVED BY THE BOARD OF MANAGERS OF THE EL PASO COUNTY HOSPITAL DISTRICT: /

RESOLUTION OF THE BOARD OF MANAGERS OF EL PASO COUNTY HOSPITAL DISTRICT APPROVING AND AUTHORIZING A TAX ANTICIPATION LOAN AGREEMENT; AUTHORIZING CERTAIN DISTRICT OFFICIALS TO EFFECT SUCH LOAN AND EXECUTE

RESOLUTION OF THE BOARD OF MANAGERS OF EL PASO COUNTY HOSPITAL DISTRICT APPROVING AND AUTHORIZING A TAX ANTICIPATION LOAN AGREEMENT; AUTHORIZING CERTAIN DISTRICT OFFICIALS TO EFFECT SUCH LOAN AND EXECUTE

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW HOUSE BILL 148

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-527 HOUSE BILL 148 AN ACT TO ESTABLISH A CONGESTION RELIEF AND INTERMODAL TRANSPORTATION 21 ST CENTURY FUND; TO PROVIDE FOR ALLOCATION OF

GENERAL ASSEMBLY OF NORTH CAROLINA SESSION 2009 SESSION LAW 2009-527 HOUSE BILL 148 AN ACT TO ESTABLISH A CONGESTION RELIEF AND INTERMODAL TRANSPORTATION 21 ST CENTURY FUND; TO PROVIDE FOR ALLOCATION OF

T E X A S. Tax-Related State and Local Economic Development Programs

OFFICE OF THE COMPTROLLER T E X A S Tax-Related State and Local Programs FEBRUARY 2006 C AROLE KEETON STRAYHORN, TEXAS COMPTROLLER Tax-Related State and Local Programs I. es Value Limitation & Tax Credits

OFFICE OF THE COMPTROLLER T E X A S Tax-Related State and Local Programs FEBRUARY 2006 C AROLE KEETON STRAYHORN, TEXAS COMPTROLLER Tax-Related State and Local Programs I. es Value Limitation & Tax Credits

Tax Abatement Agreements

Revised Prepared by: Jeff Moore Brown & Hofmeister, L.L.P. 740 East Campbell Road, Suite 800 75081 (214) 747-6100 In General: 1. What is a tax abatement agreement? The authority to enter into tax abatement

Revised Prepared by: Jeff Moore Brown & Hofmeister, L.L.P. 740 East Campbell Road, Suite 800 75081 (214) 747-6100 In General: 1. What is a tax abatement agreement? The authority to enter into tax abatement

Tax Election Ballot Measures

Tax Election Ballot Measures Table of Contents Chapter 1 - General Information... 1 Chapter 2 - Elections and Budgets... 2 Chapter 3 - Types of Property Taxes... 3 Chapter 4 - Ballot Titles... 4 Index...

Tax Election Ballot Measures Table of Contents Chapter 1 - General Information... 1 Chapter 2 - Elections and Budgets... 2 Chapter 3 - Types of Property Taxes... 3 Chapter 4 - Ballot Titles... 4 Index...

UNOFFICIAL COPY OF HOUSE BILL 1312 A BILL ENTITLED

UNOFFICIAL COPY OF HOUSE BILL 1312 R2 6lr2645 CF 6lr2597 By: Delegate Bronrott Introduced and read first time: February 10, 2006 Assigned to: Environmental Matters 1 AN ACT concerning A BILL ENTITLED 2

UNOFFICIAL COPY OF HOUSE BILL 1312 R2 6lr2645 CF 6lr2597 By: Delegate Bronrott Introduced and read first time: February 10, 2006 Assigned to: Environmental Matters 1 AN ACT concerning A BILL ENTITLED 2

2018 Effective Tax Rate Worksheet

2018 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2017 total taxable value. Enter the amount of 2017 taxable value on the 2017 tax roll today. Include

2018 Effective Tax Rate Worksheet See pages 13 to 16 for an explanation of the effective tax rate. 1. 2017 total taxable value. Enter the amount of 2017 taxable value on the 2017 tax roll today. Include

A. The proper issuance of permits and inspection activities by Surry County relating to fire prevention; and

A 2005 FIRE PREVENTION AND PROTECTION ORDINANCE FOR SURRY COUNTY, NORTH CAROLINA, AND AN ORDINANCE TO ADOPT SECTION 105, ENTITLED PERMITS, OF THE NORTH CAROLINA FIRE PREVENTION CODE, AS PART OF THE 2005

A 2005 FIRE PREVENTION AND PROTECTION ORDINANCE FOR SURRY COUNTY, NORTH CAROLINA, AND AN ORDINANCE TO ADOPT SECTION 105, ENTITLED PERMITS, OF THE NORTH CAROLINA FIRE PREVENTION CODE, AS PART OF THE 2005

MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: AREA: Billing and Collections

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.08.01 AREA: Billing and Collections TITLE/SUBJECT: Accounts Receivable I. POLICY STATEMENT

TEXAS SOUTHERN UNIVERSITY MANUAL OF ADMINISTRATIVE POLICIES AND PROCEDURES SECTION: Fiscal Affairs NUMBER: 03.08.01 AREA: Billing and Collections TITLE/SUBJECT: Accounts Receivable I. POLICY STATEMENT