ACS Submission: Sanctions to Tackle Tobacco Duty Evasion and Other Excise Duty Evasion

|

|

|

- Arthur Ferguson

- 5 years ago

- Views:

Transcription

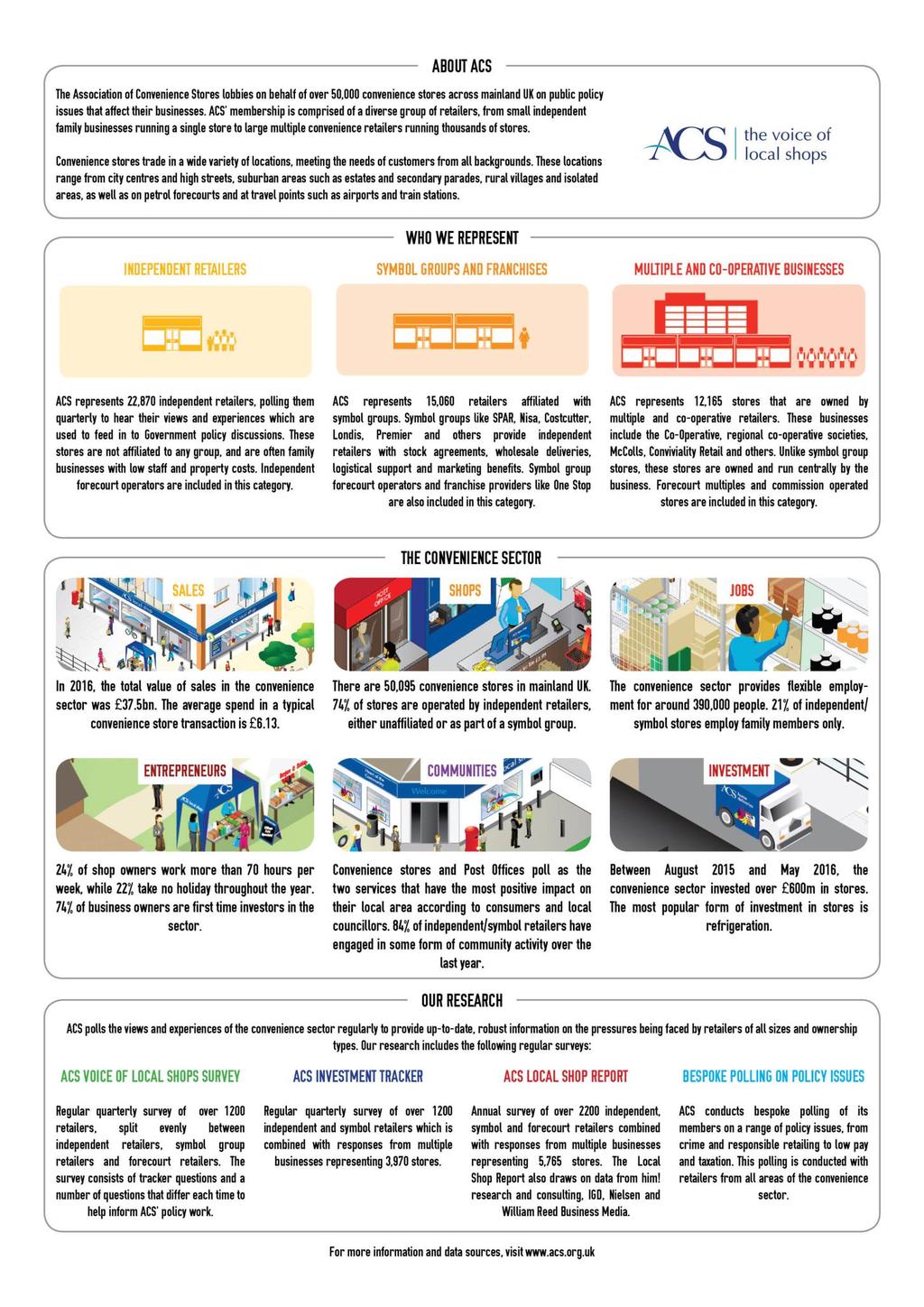

1 ACS Submission: Sanctions to Tackle Tobacco Duty Evasion and Other Excise Duty Evasion ACS (the Association of Convenience Stores) welcomes the opportunity to respond to HMRC s consultation on sanctions to tackle tobacco duty evasion. ACS represents 33,500 local shops across the UK, including the Co-Op, Spar UK, Nisa Retail and thousands of independent retailers. ACS works with the Scottish Grocers Federation, and this submission also represents their views on sanctions to tackle illicit tobacco. Tobacco is an important product category for convenience retailers, representing on average 15.4% of sales in the UK convenience market 1. Retailers work hard to ensure they retail these products responsibly through enforcing age restricted sales policies such as Challenge 25, to ensure that no one underage can buy tobacco products. In the last ten years, the retail industry has made significant progress in reducing underage sales, the most common way young people now access cigarettes is through proxy purchasing by being given them by other people (64%) 2, not from retail outlets. ACS welcomes HMRC s review of the current sanctions for retailers who sell illicit tobacco. The cost of the illicit tobacco trade to the Exchequer was 2.4 billion in and poses a significant threat to legitimate sales. ACS previously responded to HMRC s initial consultation on sanctions to tackle illicit tobacco, which can be found here. In our submission, we agreed that the criminal sanctions used by HMRC are an appropriate deterrent to prevent retailers selling non-duty paid goods. However, the sanctions must be communicated to retailers and effectively enforced 4. We also believe that more efficient use of existing sanctions and targeted enforcement activity will have a great impact on the illicit trade instead of the introduction of a tobacco register for tobacco products. HMRC have an extensive range of sanctions at their disposal to tackle the illicit tobacco trade but HMRC s enforcement activity is limited to the disruption of large scale tobacco smuggling at UK borders. In comparison, trading standards teams are responsible for tackling inland illicit tobacco activity, but have extremely limited powers and sanctions to deal with illicit tobacco and limited intelligence is shared with them by HMRC. Despite 91% of all trading standards teams in councils undertaking work in relation to illicit tobacco products, 5 the most common action was verbal or written warnings (56%). ACS does not believe that verbal or written warnings act as a significant deterrent to the sale of illicit tobacco, instead we want to see retailers that persistently trade in illicit tobacco products remove from the market by banning them from selling both tobacco and alcohol products. ACS recently conducted consumer polling, which suggests that a third of smokers see buying illicit tobacco as a victimless crime, 43% do not feel guilty about purchasing non-duty paid tobacco, and 75% do not fear enforcement action or sanctions for purchasing illicit 1 ACS Local Shop Report HSCIC: Smoking, drinking and drug use among young people in England in HMRC: Tobacco Tax Gaps ACS Submission: Sanctions to tackle illicit tobacco: a discussion document 5 CTSI: Tobacco Control Survey, England 2015/16

2 tobacco 6. Therefore, ACS calls on HMRC to take more action, both in terms of enforcement and communication to ensure that smokers are aware of the penalties and are deterred from purchasing illicit tobacco. As part of the review of illicit tobacco sanctions, we support HMRC s consideration of exploring sharing powers across partner agencies, removing trading licences and applying closure notices, and promoting more effective targeted use of appropriate sanctions to fit the offence at the lower end of the supply chain. As discussed in more detail later, we would like to see HMRC extend the use of Restricted Premise Orders, currently used for underage sales offences, to illicit tobacco offences creating a similar three strikes and you are out system. ACS urges HMRC to consider the following proposals as part of their review into current sanctions for illicit tobacco offences. 1. More effective sanctions should be made available to trading standards officers, including the revocation of alcohol licences for selling illicit tobacco. According to the most recent HMRC Tobacco Output (July 2016), only 62% 7 of individuals prosecuted for tobacco duty-fraud offences were convicted. It is often difficult and time consuming to prosecute an individual. ACS believes that it may be more effective and efficient if efforts moved towards revoking the alcohol licence of the premise involved. Removing a retailer s alcohol licence is more of an effective deterrent than any other sanction, as the loss of the ability to trade alcohol would undermine their ability to trade with full convenience offer expected by consumers. Removing alcohol licences for selling illicit tobacco and illicit alcohol is an underused sanction by all enforcement bodies. The reasons that enforcement bodies underuse this sanction are multi-faceted; it is not communicated that this sanction is available, the process to revoke a licence is viewed as complex and requires working across a number of local council departments. ACS strongly advocates greater use of the removal of alcohol licences from retailers for any engagement in the illicit market. We urge HMRC to work closely with the Home Office to make it easier to remove alcohol licenses from retailers persistently selling illicit tobacco. 2. Additional powers to trading standards officers to sanction retailers by using the Customs & Excise Management Act 1979 (CEMA) and better intelligence sharing. While we welcome that 91% of all councils 8 are focusing enforcement activity in relation to illicit tobacco products, we are concerned that 56% of actions 9 taken by trading standards teams to sanction retailers selling illicit tobacco are verbal of written warnings. An extension of powers to Trading Standards officers would enable them to deal with offenders quickly and more effectively than at present. There is also limited amount of intelligence shared between HMRC and local Trading Standards to enable effective and targeted enforcement activity. ACS believes that there needs to be a significant up-lift in inland enforcement activity by HMRC to reduce the illicit trade and additional powers should be given to trading standards officers in order to enforce more effectively. We recommend that trading standards be given 6 Jericho Chambers: Attitudes to Key Product Categories in Convenience Stores HMRC: Quarter 3 and 4 outputs: October 2015 to March CTSI: Tobacco Control Survey, England 2015/16 9 CTSI: Tobacco Control Survey, England 2015/16

3 the authority to sanction retailers participating in the sale of illicit tobacco using the Excise and Customs Management Act This Act specifically addresses the sale of non-duty paid tobacco as an offence. Sanctions can be placed on retailers who knowingly acquire non-duty paid excise goods with the intention of evading payment of duty and retailers who have taken preparatory steps for evasion of excise duty. This Act would mean trading standards officers could sanction retailers with an unlimited fine and/or 7-years imprisonment if convicted on indictment. 3. Extending Restricted Premise Orders and Restricted Sales Orders to include illicit tobacco as an offence. Trading standards officers already have powers available to them to make provision for Restricted Premises Orders (RPO) where there has been a total of three underage sales offences at a premises in a two-year period. This prohibits a retail premises from selling tobacco products for a period of up to 12 months. However, trading standards officers do not have the power to use RPOs to sanction retailers involved in the sale of non-duty paid tobacco products. We recommend that the scope of the use of Restricted Premises Orders (RPO) and Restricted Sales Orders (RSO) be extended to include illicit tobacco offences. The offence for breaching a RPO or RSO is far greater than the current powers available to trading standards officers. This would be a more effective way for dealing with low volume and low value illicit tobacco offences instead of fines or written or verbal warnings. This would also replicate the sanctions used under the Scottish Tobacco Registration system but without requiring HMRC to invest thousands in creating an English tobacco register. The Welsh Government is currently pursuing extending the scope of offences of RPO in the Public Health (Wales) Bill. In their consideration of the Bill, the National Assembly for Wales Health, Social Care and Sport Committee concluded that we share witnesses concerns regarding the supply of illegal (counterfeit and non-duty paid) tobacco, and believe that all opportunities for action to tackle this issue should be used 10. As such, the Committee recommended that work should be undertaken as a matter of priority to add offences relating to the sale of illegal tobacco to the list of offences which can contribute towards the making of a Restricted Premises Order for retail premises in Wales 11. We encourage HMRC to follow the Welsh Government s lead to extend the scope of RPOs to include illicit tobacco offences. ACS has responded to the relevant consultation questions below. For more information on this consultation please contact Julie Byers, ACS Public Affairs Manger by ing Julie.byers@acs.org.uk or call Increasing Financial Penalties for Repeat Offenders Question 1: Do you think that increasing financial penalties for subsequent tobacco wrongdoings will deter repeat offending? If not, why not and what more do you think we could do? 10 National Assembly for Wales Health, Social Care and Sport Committee: Public Health (Wales) Bill Committee Stage 1 Report 11 National Assembly for Wales Health, Social Care and Sport Committee: Public Health (Wales) Bill Committee Stage 1 Report

4 ACS supports HMRC s proposals to increase financial penalties to deter repeat offending, but this not a silver bullet for tackling the sale of illicit tobacco. ACS believes that the most effective deterrent would be to threaten to remove retailers from the market if they do persistently trade in illicit tobacco products. This means threatening to remove alcohol licence or the ability to trade in tobacco products for a limited period of time. If an alcohol licence or the ability to trade tobacco is lost the damage to a retailer s business will be far more significant than any fine as they will lose a significant proportion of their customers. 84% of convenience retailers have an alcohol licence and all convenience retailers sell tobacco; the loss of these product categories would undermine their businesses and therefore deter them from trading tobacco. As set out above (and currently being introduced by the National Assembly for Wales), we recommend that HMRC extend the use of RPOs and RSOs to include illicit tobacco offences which means retailers will lose their ability to trade tobacco for 12 months if they are found to be selling illicit tobacco. Question 2: Should such a multiplier apply to wrongdoings in other excise regimes? Yes, we believe that there should be increased financial penalties to deter repeat offenders for the sale of other non-duty paid goods. We broadly support fine multipliers for each excise regime but different regimes and products may require different approaches and should be assessed on a case by case basis. Question 3: What do you think about the proposal to increase the penalty by a proposed multiplier of 100% of PLR for each subsequent repeated tobacco wrongdoing? Is this enough or should it be more? We welcome the multiplier of 100% of PLR for each subsequent repeated illicit tobacco offence. While there is a significant financial deterrent in committing a second offence (jumps from 250 to 1,500), we believe more of a deterrent is needed for the third and fourth offences. Therefore, we recommend further increases in the financial penalty for third and fourth offences. Question 4: Do you think that maintaining reductions for cooperation and the quality of information disclosed for repeat tobacco wrongdoings is helpful in providing an incentive for individuals to cooperate with HMRC? Do you think there is a case for allowing no mitigation? Yes, we believe maintaining reductions for cooperation and quality of information can be helpful for incentivising individuals to cooperate with HMRC. A similar approach is taken in relation to sentencing guidelines for criminal sanctions in other areas. We recommend that HMRC should consider mitigating factors on a case by case basis. HMRC is best placed to judge the level of co-operation they receive from offenders and the value of the intelligence they share and assess whether a reduced sentence/ fine is proportionate. Question 5: What timescale should be considered from the first to second tobacco wrongdoing to trigger the ramping up of penalties? For example, does a 12 month period appear reasonable or a longer timescale to deter the repeat wrongdoers? To effectively deter repeat offenders, we believe there should be an extensive time period from the first to second wrongdoing to trigger increased penalties. Similar to a suspended

5 sentence, this would provide a greater deterrence to an offender that had committed a first offence from returning to selling illicit tobacco because of the considerably higher fine. A New Civil Penalty for Dealing in Illicit Product Question 6: Do you consider it would be appropriate to extend this provision to those selling other illicit products on which excise duties should have been paid? Question 7: Do you think that the new penalty would be an effective and proportionate sanction? If not, can you suggest an alternative approach? While we would welcome the creation of a new civil penalty instead of on the spot fines, we have concerns that this penalty will not act as sufficient deterrent to offenders trading in illicit tobacco. Whilst a formal process around a civil penalty is more severe than an on the spot fine, there is no real difference to the person perpetrating the crime in terms of cost or time. Trading standards currently have similar powers to sanction retailers. Trading standards officers can sanction retailers if they breach the Trade Marks Act 1994 (by selling counterfeit goods) or if they breach the Consumer Protection Act 1987 (by selling tobacco products which do not comply with UK labelling such as wrong fiscal markings). With these two powers, the maximum sentence that trading standards officers can impose on a retailer is a summary conviction of imprisonment, for a term not exceeding six months, or a fine not exceeding the statutory maximum, or both. Instead of introducing a new civil penalty, we recommend that trading standards be given the authority to sanction retailers participating in the sale of illicit tobacco using the Customs & Excise Management Act As stipulated above, this act specifically addresses the sale of non-duty paid tobacco as an offence, and means that trading standards officers could sanction retailers with an unlimited fine and/or 7-years imprisonment if convicted on indictment. We also recommend the extension of RPO and RSO to illicit tobacco offences to sanction retailers selling illicit tobacco. Question 8: Do you think that the new penalty should be on a sliding scale as determined by the potential lost revenue? If a new civil penalty were to be introduced, it should be on a sliding scale depending on the potential lose revenue and time spent selling. The sliding scale should replicate the proposals already outline in the consultation resulting in 100% increases. Question 9: Do you think that any new penalty should be subject to a maximum amount? We do not believe that a new financial penalty should be subject to a maximum amount. For fines to be a deterrent to retail premises selling these products they must be sufficiently severe. By not capping the fine amount and instead leaving it to the discretion of the enforcement officers or magistrates it will be a greater deterrent. Question 10: Who in the supply chain that is found to be dealing in illicit tobacco do you think that the new penalty should be issued to? How far could it extend?

6 It would be appropriate for the penalty to apply to all parties in the supply chain that can be connected with the offence, including retailers, wholesalers and consumers that are knowingly participating in the sale or purchase of illicit tobacco. Question 11: Do you believe that 30 days is sufficient time to pay the new penalty or do you think a different time limit is appropriate, if so what and why? Yes. Question 12: What are your views on the higher penalty amount for failing to pay within 30 days? Do you think HMRC/Trading Standards should issue a reminder letter to the responsible person before the 30 days are up? Yes Do you think 14 additional days is the right amount of time to pay the higher penalty? If not why? Yes At what level do you believe the second penalty should increase, by, for example, by 50% of the original amount, 100% or some other amount? 100% How do you think HMRC should deal with offenders who fail to pay a second penalty within the 14 days? Possible options HMRC are considering are: o Court Order issued demanding payment known as Order of Recovery o Application to the court for an attachment of earnings order (allows money to be deducted from wages to pay the fine or; o Application to the court to have deductions made from benefits to pay for the fine. Question 13: What design model do you believe would have the most impact on encouraging behaviour? Question 14: Should payment by instalments be in your opinion considered? If yes, why? Question 15: Are there any potential wider consequences of introducing the new penalty that we have not identified? As outlined throughout the consultation response, we believe the most effective sanction is to threaten to remove a retailers ability to trade by removing an alcohol licence or using a RPO or RSO. HMRC should consider adding these options to offenders that fail to pay the second penalty within a 14-day period. Reducing the threshold for the publication of details of people or companies that deliberately evade duty Naming and shaming of offenders can be an effective sanction and has been used in other enforcement regimes, for example National Minimum Wage, to good effect. However, the businesses that engage in trading illicit tobacco product in the convenience sector are very

7 small operators. Therefore, it is unlikely that the reputation risk of being named and shamed nationally, or even locally, will have a meaningful impact. We support HMRC s proposal to name and shame more businesses but it should not be the central focus of reviewing the tobacco sanctions regime. Question 16: Do you think the potential lost revenue threshold figure of 15,000 is sufficient to have a deterrent effect on those who persist in evading excise duty? We welcome the reduction in the potential lost revenue threshold from 25,000 to 15,000. This will result in more businesses being subject to further investigation and publicly named and shamed. Question 17: What are your views on publicising the details of companies or people who have evaded duty? Question 18: Do you consider the naming of individuals or companies to be an effective deterrent and likely to change behaviour? Yes, naming and shaming has worked effectively to deter offenders in other policy areas, including National Minimum Wage enforcement. However, we do not think the associated reputational damage that naming and shaming causes will have a detrimental impact on the smallest operators in the convenience sector that engage in illicit tobacco offences. Question 19: HMRC would publish the details on GOV.UK do you have any views on this? Specifically: Who else should HMRC inform- local press, local authority, local police, public health, tobacco manufacturers? Others? Do you think the message would have a greater deterrent if published by another source? If so, who and why? When publishing the details, should HMRC publish names in the community? If so, how and where? We agree with HMRC s suggested communications for naming and shaming retailers selling illicit tobacco. We believe that notifying local press, the local authority, local police, public health and tobacco manufacturers is appropriate to ensure that follow up action is taken to mitigate any future illicit tobacco offences being made by that retailer. When a tobacco manufacturer is notified that a retailer has be found to be selling illicit tobacco, if they provide a gantry to that store, they will remove it. Similarly, Camelot have previously taken action against retailers selling illicit tobacco by suspending their lottery contract with the retailer 12. If a retailer found to be selling illicit tobacco and is a member of a symbol group 13, we would also encourage HMRC to notify the head office of the symbol group who can then consider if they want to take further action for example removing supply from that business. A Statutory Duty of Care on landlords and landowners of properties or land Question 20: Would you be in favour of this approach? 12 Better Retailing: Gantries ripped out as JTI continues its campaign against the illicit trade 13 ACS Symbol Group Retailer members

8 We welcome the clarity that the introduction of the provision would have for trading standards officers considering the powers available them to tackle illicit tobacco. Currently, a number of trading standards teams have already taken it upon themselves to find alternative ways to sanction retailers selling illicit tobacco more effectively, including Medway Council who use legal pressure on landlords to close premises selling tobacco (more details can be found in Annex B). By stipulating a duty of care on a landlord, this would allow more trading standards teams to consider alternative, cost effective approaches to tackling illicit tobacco. However, before legislative proposals are considered, we suggest that best practice from trading standards teams such as Medway are shared amongst trading standards teams. While ACS does not represent the interests of landlords, we would like to highlight that 79% of independent retailers own their premises in the convenience sector 14. Question 21: Do you think the examples above are on the right lines to ensure that the duty of care is reasonable and proportionate? Question 22: What would be a reasonable expectation of the steps landlords/landowners should take and the timescale for doing this and for taking action if there are further transgressions? Question 23: What sanctions should HMRC apply to landlords or landowners who have not taken steps to prevent illicit tobacco or other illicit excise activity on the property or land? For example, should HMRC impose a financial penalty? Question 24: Are there any potential wider consequences of introducing a duty of care and a civil penalty that we have not identified? We suggest that if legislative proposals are considered to introduce a duty of care and civil penalties for landlords that HMRC should consult with associations that represent the interests of landlords. Question 25: Do you have any information that could inform the Impact Assessment? We do not have any information to inform the consultation s impact assessment. However, ACS has mechanisms in place to consult with the convenience sector and can offer HMRC the opportunity to pose a question in the ACS Voice of Local Shops survey (VOLS). VOLS is conducted every three months, which is a multiple-choice phone survey of 1,210 independent convenience store retailers. The survey provides the opportunity for ACS to ask policy related questions to obtain an insight into the perspectives of independent retailers. For more information on this submission, please contact Julie Byers, ACS Public Affairs Manager by ing Julie.Byers@acs.org.uk or calling ACS Local Shop Report 2016

9 ANNEX A

10 ANNEX B - Addressing the Proliferation of Shops Selling Illicit Tobacco Case Study - Medway Council 15 Medway experienced a proliferation of shops selling illicit tobacco. Medway Trading Standards officers decided to change up their enforcement activity by ending their enforcement cycle which was proving ineffective. Their enforcement cycle would include a visit, seizure of illicit goods, interview, report, prosecute, forfeit, then the cycle would repeat. It failed to recognise the fluid and ambiguous nature of those involved in the business; the minimal value in the stock that was being seized; their ability to immediately restock illicit goods; comparatively limited punishment prospects; and the huge profits being made. - Medway Trading Standards Once the retailers selling the non-duty paid tobacco products acquired small retail shops, they gained a new stream of customers and had the perception of legitimacy. Medway Trading Standards recognised that if the venue for their criminality could be removed then the scale and nature of their operation would be changed. It would no longer have the palatability of a retail transaction; it would have to be a nefarious deal. Instead of using the traditional enforcement cycle to sanction the retailer, they considered whether legal pressure could be applied to the letting agents and landlords that were permitting their premises to be used as venues for the commission of criminal offences. The provisions of The Proceed of Crime Act 2002 relating to Money Laundering were reviewed and it was considered that if a disclosure mechanism was created to place landlords and letting agents on notice that their tenants were using the property for the commission of offences and that the rent that was being paid to them was criminal property within sections 327 to 334 they would acquire a legal liability of money laundering. A project was devised to operate from July 2015 to December 2015 to make a concentrated effort to address illicit tobacco by collecting evidence to challenge the landlords and letting agents who were leasing the properties. A process was adopted where three tobacco seizures would be made from those shops chronically selling illegal tobacco to illustrate that a persistent criminal conduct was taking place. A disclosure bundle detailing our actions was then presented to the landlord and/or letting agent placing them on notice that the rent which was being collected was the proceeds of crime. It was explained that this payment of money represented criminal property within the Act and that the acceptance of any further payments exposed them to a potential criminal offence There was a level of reluctance by some landlords to terminate the tenancy, as the shops which these businesses use are often small and difficult to rent. However, the cumulative process of disclosure used in Medway created a situation where the continued occupancy by illicit tobacco sellers became untenable. 15 Trading Standards Today (April 2016): This is a No Smoking Venue.

Lucy Sutcliffe Fiscal Crime Liaison Officer Pretoria, South Africa

Lucy Sutcliffe Fiscal Crime Liaison Officer Pretoria, South Africa HM Revenue & Customs (HMRC) is the tax administration and customs authority for the United Kingdom. HMRC ensures that money is available

Lucy Sutcliffe Fiscal Crime Liaison Officer Pretoria, South Africa HM Revenue & Customs (HMRC) is the tax administration and customs authority for the United Kingdom. HMRC ensures that money is available

REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 226 SESSION JUNE HM Revenue & Customs. Progress in tackling tobacco smuggling

REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 226 SESSION 2013-14 6 JUNE 2013 HM Revenue & Customs Progress in tackling tobacco smuggling 4 Key facts Progress in tackling tobacco smuggling Key facts

REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 226 SESSION 2013-14 6 JUNE 2013 HM Revenue & Customs Progress in tackling tobacco smuggling 4 Key facts Progress in tackling tobacco smuggling Key facts

Tobacco Illicit Trade Protocol licensing of equipment and the supply chain HMRC. Chartered Trading Standards Institute response

Tobacco Illicit Trade Protocol licensing of equipment and the supply chain HMRC Chartered Trading Standards Institute response May 2016 www.tradingstandards.uk reg.no. RC000879 About The Chartered Trading

Tobacco Illicit Trade Protocol licensing of equipment and the supply chain HMRC Chartered Trading Standards Institute response May 2016 www.tradingstandards.uk reg.no. RC000879 About The Chartered Trading

Bar Council response to the consultation paper on Tackling offshore tax evasion: A new criminal offence

Bar Council response to the consultation paper on Tackling offshore tax evasion: A new criminal offence 1. This is the response of the General Council of the Bar of England and Wales (the Bar Council)

Bar Council response to the consultation paper on Tackling offshore tax evasion: A new criminal offence 1. This is the response of the General Council of the Bar of England and Wales (the Bar Council)

Our goal is to have sanctions that are consistent and fair, and that deter non-compliance and provide appropriate penalties.

Sanctions SANCTIONS AT A GLANCE Our goal is to have sanctions that are consistent and fair, and that deter non-compliance and provide appropriate penalties. We believe that the current range of Customs

Sanctions SANCTIONS AT A GLANCE Our goal is to have sanctions that are consistent and fair, and that deter non-compliance and provide appropriate penalties. We believe that the current range of Customs

Fighting Fraud Locally

Fighting Fraud Locally Fighting Tenancy Fraud the Threat to Housing Providers John Baker 26 November, London The scale of the problem - Annual Fraud Indicator 2013 Identified fraud loss for public sector

Fighting Fraud Locally Fighting Tenancy Fraud the Threat to Housing Providers John Baker 26 November, London The scale of the problem - Annual Fraud Indicator 2013 Identified fraud loss for public sector

NFA response to government consultation on social housing fraud

NFA response to government consultation on social housing fraud March 2012 Introduction The National Federation of ALMOs (NFA) represents 55 ALMOs which manage over 800,000 council homes across 54 local

NFA response to government consultation on social housing fraud March 2012 Introduction The National Federation of ALMOs (NFA) represents 55 ALMOs which manage over 800,000 council homes across 54 local

Member States capabilities in fighting tax crimes

United Kingdom Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax

United Kingdom Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax

Michael Connolly Head of Specialist Investigations Inland Detection Scotland, N.Ireland & NE England. Tackling Tobacco Smuggling Together

Michael Connolly Head of Specialist Investigations Inland Detection Scotland, N.Ireland & NE England Tackling Tobacco Smuggling Together HMRC Operational delivery HMRC Intelligence Strategy/Policy Investigation/Detection

Michael Connolly Head of Specialist Investigations Inland Detection Scotland, N.Ireland & NE England Tackling Tobacco Smuggling Together HMRC Operational delivery HMRC Intelligence Strategy/Policy Investigation/Detection

Summary: Analysis & Evidence Policy Option 1

1 Summary: Analysis & Evidence Policy Option 1 Description: Do Nothing FULL ECONOMIC ASSESSMENT Price Base Year 2015 COSTS ( m) PV Base Year 2017 Time Period Years 10 Total Transition (Constant Price)

1 Summary: Analysis & Evidence Policy Option 1 Description: Do Nothing FULL ECONOMIC ASSESSMENT Price Base Year 2015 COSTS ( m) PV Base Year 2017 Time Period Years 10 Total Transition (Constant Price)

STEP BRIEFING NOTE: Criminal Finances Act 2017 and 'Failure to prevent the facilitation of tax evasion

STEP BRIEFING NOTE: Criminal Finances Act 2017 and 'Failure to prevent the facilitation of tax evasion The Criminal Finances Act 2017 1 received Royal Assent on 27 April 2017. The Act contains the new

STEP BRIEFING NOTE: Criminal Finances Act 2017 and 'Failure to prevent the facilitation of tax evasion The Criminal Finances Act 2017 1 received Royal Assent on 27 April 2017. The Act contains the new

Landfill Tax: Whether to bring illegal waste sites within the scope of Landfill Tax

Landfill Tax: Whether to bring illegal waste sites within the scope of Landfill Tax UNITED RESOURCE OPERATORS CONSORTIUM LIMITED ( UROC ) Q1. Trade Body representing independent waste and resource operators.

Landfill Tax: Whether to bring illegal waste sites within the scope of Landfill Tax UNITED RESOURCE OPERATORS CONSORTIUM LIMITED ( UROC ) Q1. Trade Body representing independent waste and resource operators.

The Misuse and Smuggling of Hydrocarbon Oils

HM Customs and Excise: The Misuse and Smuggling of Hydrocarbon Oils REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 614 Session 2001-2002: 15 February 2002 LONDON: The Stationery Office 0.00 Ordered by

HM Customs and Excise: The Misuse and Smuggling of Hydrocarbon Oils REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 614 Session 2001-2002: 15 February 2002 LONDON: The Stationery Office 0.00 Ordered by

June Background

Response to Home Office and HM Treasury Consultation on legislative proposals for an Action Plan for anti-money laundering and counter-terrorist finance from the National Association of Estate Agents (NAEA)

Response to Home Office and HM Treasury Consultation on legislative proposals for an Action Plan for anti-money laundering and counter-terrorist finance from the National Association of Estate Agents (NAEA)

An Introduction to the Illicit Tobacco Trade. Adrian Welsh, Chief Legal and Compliance Officer

An Introduction to the Illicit Tobacco Trade Adrian Welsh, Chief Legal and Compliance Officer % Market Share Illicit Trade a global issue 600 BILLION Non Duty Paid 2 Measurement is not straightforward

An Introduction to the Illicit Tobacco Trade Adrian Welsh, Chief Legal and Compliance Officer % Market Share Illicit Trade a global issue 600 BILLION Non Duty Paid 2 Measurement is not straightforward

Cigarette smuggling and the financial damage for the EU

Cigarette smuggling and the financial damage for the EU State of play, possible solutions and emerging threats the perspective of the affected tobacco industry Stephen J S Payne September 17, 2012 Illicit

Cigarette smuggling and the financial damage for the EU State of play, possible solutions and emerging threats the perspective of the affected tobacco industry Stephen J S Payne September 17, 2012 Illicit

Behavioural challenge

Behavioural challenge 1 January 2018 Helen Adams considers the findings of research commissioned by HMRC into tax evasion and the sharing economy and what more could be done to improve compliance What

Behavioural challenge 1 January 2018 Helen Adams considers the findings of research commissioned by HMRC into tax evasion and the sharing economy and what more could be done to improve compliance What

SUBMISSION OF ACS TO THE TREASURY BUDGET 2012

SUBMISSION OF ACS TO THE TREASURY BUDGET 2012 ACS (the Association of Convenience Stores) represents 33,500 local shops (Annex1). These businesses are crucially important in bringing economic recovery

SUBMISSION OF ACS TO THE TREASURY BUDGET 2012 ACS (the Association of Convenience Stores) represents 33,500 local shops (Annex1). These businesses are crucially important in bringing economic recovery

Report. by the Comptroller and Auditor General. Criminal Justice System. Confiscation orders

Report by the Comptroller and Auditor General Criminal Justice System Confiscation orders HC 738 SESSION 2013-14 17 DECEMBER 2013 4 Key facts Confiscation orders Key facts 26p 133m 102m estimated amount

Report by the Comptroller and Auditor General Criminal Justice System Confiscation orders HC 738 SESSION 2013-14 17 DECEMBER 2013 4 Key facts Confiscation orders Key facts 26p 133m 102m estimated amount

Written evidence from HM Revenue & Customs. This covers the specific issues the Committee have asked HMRC to address in their evidence.

Written evidence from HM Revenue & Customs This covers the specific issues the Committee have asked HMRC to address in their evidence. 1. The amount and extent of fuel laundering and smuggling in Northern

Written evidence from HM Revenue & Customs This covers the specific issues the Committee have asked HMRC to address in their evidence. 1. The amount and extent of fuel laundering and smuggling in Northern

Impact Assessment (IA) Summary: Intervention and Options. Title:

Summary: Intervention and Options. Title:") Title: Fraud Penalties and Sanctions Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty s Revenue and Customs Pensions, Disability and Carer Service

Title: Fraud Penalties and Sanctions Lead department or agency: Department for Work and Pensions Other departments or agencies: Her Majesty s Revenue and Customs Pensions, Disability and Carer Service

1. ANZ supports the proposals to extend the AML/CFT Act to include those additional business sectors set out in Part 3 of the consultation paper.

22 September 2016 Ministry of Justice National Office Justice Centre 19 Aitken Street Wellington By email: aml@justice.govt.nz To whom it may concern ANZ submission on the consultation paper: Improving

22 September 2016 Ministry of Justice National Office Justice Centre 19 Aitken Street Wellington By email: aml@justice.govt.nz To whom it may concern ANZ submission on the consultation paper: Improving

The Prevention of Social Housing Fraud Act Paul Downie Deputy Director Affordable Housing Management & Standards

The Prevention of Social Housing Fraud Act 2013 Paul Downie Deputy Director Affordable Housing Management & Standards Social Housing Fraud abuse of social housing not only deprives of a settled home those

The Prevention of Social Housing Fraud Act 2013 Paul Downie Deputy Director Affordable Housing Management & Standards Social Housing Fraud abuse of social housing not only deprives of a settled home those

Measuring and Tackling Indirect Tax Losses An Update on the Government s Strategic Approach December 2004

Measuring and Tackling Indirect Tax Losses - 2004 An Update on the Government s Strategic Approach December 2004 1 Contents 1. Introduction 3 2. Measuring and Tackling VAT Losses 4 VAT Compliance Strategy

Measuring and Tackling Indirect Tax Losses - 2004 An Update on the Government s Strategic Approach December 2004 1 Contents 1. Introduction 3 2. Measuring and Tackling VAT Losses 4 VAT Compliance Strategy

Sanctions and Anti-Money Laundering Bill

Sanctions and Anti-Money Laundering Bill Committee Stage House of Lords Tuesday 21 November 2017 The Law Society of England and Wales is the independent professional body that works to support and represent

Sanctions and Anti-Money Laundering Bill Committee Stage House of Lords Tuesday 21 November 2017 The Law Society of England and Wales is the independent professional body that works to support and represent

APPENDIX 2 CORPORATE ANTI-FRAUD AND CORRUPTION STRATEGY

APPENDIX 2 CORPORATE ANTI-FRAUD AND CORRUPTION STRATEGY January 2017 CONTENTS Section Page 1 Introduction 3 2 Definition of Fraud 3 3 Standards 4 4 Corporate Framework and Culture 4 5 Roles and Responsibilities

APPENDIX 2 CORPORATE ANTI-FRAUD AND CORRUPTION STRATEGY January 2017 CONTENTS Section Page 1 Introduction 3 2 Definition of Fraud 3 3 Standards 4 4 Corporate Framework and Culture 4 5 Roles and Responsibilities

THE LINK BETWEEN ILLICIT TOBACCO TRADE AND ORGANISED CRIME Prof. Dr. Prof. h.c. Arndt Sinn, University of Osnabrück/ZEIS. - Introductory remarks -

Brussels, 23 March 2018 THE LINK BETWEEN ILLICIT TOBACCO TRADE AND ORGANISED CRIME Prof. Dr. Prof. h.c. Arndt Sinn, University of Osnabrück/ZEIS - Introductory remarks - Introduction: Organised crime as

Brussels, 23 March 2018 THE LINK BETWEEN ILLICIT TOBACCO TRADE AND ORGANISED CRIME Prof. Dr. Prof. h.c. Arndt Sinn, University of Osnabrück/ZEIS - Introductory remarks - Introduction: Organised crime as

An introduction to Civil Penalties for Employers. (Immigration, Asylum and Nationality Act 2006)

") An introduction to Civil Penalties for Employers (Immigration, Asylum and Nationality Act 2006) Alexander Barnfield Email alexanderbarnfield@no8chambers.co.uk Twitter @alexbarnfield @No8Chambers Clerks

An introduction to Civil Penalties for Employers (Immigration, Asylum and Nationality Act 2006) Alexander Barnfield Email alexanderbarnfield@no8chambers.co.uk Twitter @alexbarnfield @No8Chambers Clerks

Confiscation orders: progress review

Report by the Comptroller and Auditor General Criminal Justice System Confiscation orders: progress review HC 886 SESSION 2015-16 11 MARCH 2016 4 Key facts Confiscation orders: progress review Key facts

Report by the Comptroller and Auditor General Criminal Justice System Confiscation orders: progress review HC 886 SESSION 2015-16 11 MARCH 2016 4 Key facts Confiscation orders: progress review Key facts

Date of meeting: 4th December 2017 Senior Environmental Crime Officer The Unauthorised Deposit of Waste (Fixed Penalties) Regulations 2016

Regulations 2016") Report to: Cabinet Date of meeting: 4th December 2017 Report of: Title: Senior Environmental Crime Officer The Unauthorised Deposit of Waste (Fixed Penalties) Regulations 2016 1.0 Summary 1.1 1.2 1.3 On

Report to: Cabinet Date of meeting: 4th December 2017 Report of: Title: Senior Environmental Crime Officer The Unauthorised Deposit of Waste (Fixed Penalties) Regulations 2016 1.0 Summary 1.1 1.2 1.3 On

The Criminal Finances Act 2017: The Six Guiding Principles to Inform Prevention Procedures

The Criminal Finances Act 2017: The Six Guiding Principles to Inform Prevention Procedures The Criminal Finances Act introduces two new offences (the first relating to the UK and the other to a foreign

The Criminal Finances Act 2017: The Six Guiding Principles to Inform Prevention Procedures The Criminal Finances Act introduces two new offences (the first relating to the UK and the other to a foreign

AAT RESPONSE TO HMRC CONSULTATION DOCUMENT ON TACKLING OFFSHORE TAX EVASION: STRENGTHENING CIVIL DETERRENTS (RELEASED 19 AUGUST 2014)

") AAT RESPONSE TO HMRC CONSULTATION DOCUMENT ON TACKLING OFFSHORE TAX EVASION: STRENGTHENING CIVIL DETERRENTS (RELEASED 19 AUGUST 2014) 1 EXECUTIVE SUMMARY 1.1 The Association of Accounting Technicians (AAT)

AAT RESPONSE TO HMRC CONSULTATION DOCUMENT ON TACKLING OFFSHORE TAX EVASION: STRENGTHENING CIVIL DETERRENTS (RELEASED 19 AUGUST 2014) 1 EXECUTIVE SUMMARY 1.1 The Association of Accounting Technicians (AAT)

Working together to tackle illicit trade

Working together to tackle illicit trade Introduction Illicit trade in tobacco products is a significant and growing problem worldwide. Illicit trade in tobacco products creates uncontrolled and unaccountable

Working together to tackle illicit trade Introduction Illicit trade in tobacco products is a significant and growing problem worldwide. Illicit trade in tobacco products creates uncontrolled and unaccountable

Explanatory Memorandum to The Landfill Disposals Tax (Administration) (Wales) Regulations 2018

(Wales) Regulations 2018") Explanatory Memorandum to The Landfill Disposals Tax (Administration) (Wales) Regulations 2018 This Explanatory Memorandum has been prepared by Welsh Treasury, Tax Strategy, Policy and Engagement Division

Explanatory Memorandum to The Landfill Disposals Tax (Administration) (Wales) Regulations 2018 This Explanatory Memorandum has been prepared by Welsh Treasury, Tax Strategy, Policy and Engagement Division

Liquor Legislation Amendment (Statutory Review) Act Stakeholder Forum

Act Stakeholder Forum") Liquor Legislation Amendment (Statutory Review) Act 2014 Stakeholder Forum 1 December 2014 Welcome and overview Samantha Torres Director, Policy & Strategy 2013 Liquor Act review Statutory five-year statutory

Liquor Legislation Amendment (Statutory Review) Act 2014 Stakeholder Forum 1 December 2014 Welcome and overview Samantha Torres Director, Policy & Strategy 2013 Liquor Act review Statutory five-year statutory

NEW UK CRIMINAL OFFENCES OF FAILURE TO PREVENT FACILITATION OF TAX EVASION

NEW UK CRIMINAL OFFENCES OF FAILURE TO PREVENT FACILITATION OF TAX EVASION 05 December 2016 London Legal Briefings In our October 2016 briefing, we reported on the publication of the Criminal Finances

NEW UK CRIMINAL OFFENCES OF FAILURE TO PREVENT FACILITATION OF TAX EVASION 05 December 2016 London Legal Briefings In our October 2016 briefing, we reported on the publication of the Criminal Finances

Issues around plain packaging. UK Government consultation on standardised packaging for tobacco products

Issues around plain packaging. UK Government consultation on standardised packaging for tobacco products ECTA's view 1) Which option do you favour? Do nothing about tobacco packaging (maintain status quo).

Issues around plain packaging. UK Government consultation on standardised packaging for tobacco products ECTA's view 1) Which option do you favour? Do nothing about tobacco packaging (maintain status quo).

The Protocol to Eliminate Illicit Trade in Tobacco Products: an overview

The Protocol to Eliminate Illicit Trade in Tobacco Products: an overview Background The Protocol to Eliminate Illicit Trade in Tobacco Products is an international treaty with the objective of eliminating

The Protocol to Eliminate Illicit Trade in Tobacco Products: an overview Background The Protocol to Eliminate Illicit Trade in Tobacco Products is an international treaty with the objective of eliminating

SUMMARY OF RECOMMENDED POLICIES AND ACTION POINTS FROM THE REGIONAL ANTI-ILLICIT TRADE CONFERENCE HELD ON

SUMMARY OF RECOMMENDED POLICIES AND ACTION POINTS FROM THE REGIONAL ANTI-ILLICIT TRADE CONFERENCE HELD ON 15 th -16 TH SEPTEMBER 2016 AT INTERCONTINENTAL HOTEL NAIROBI, KENYA As part of the implementation

SUMMARY OF RECOMMENDED POLICIES AND ACTION POINTS FROM THE REGIONAL ANTI-ILLICIT TRADE CONFERENCE HELD ON 15 th -16 TH SEPTEMBER 2016 AT INTERCONTINENTAL HOTEL NAIROBI, KENYA As part of the implementation

FSMA market abuse regime: a review of the sunset clauses

FSMA market abuse regime: a review of the sunset clauses The ABI s Response to the HMT Treasury consultation paper Introduction The ABI welcomes the opportunity to respond to this consultation paper. ABI

FSMA market abuse regime: a review of the sunset clauses The ABI s Response to the HMT Treasury consultation paper Introduction The ABI welcomes the opportunity to respond to this consultation paper. ABI

Tax and the Rule of Law

Tax and the Rule of Law April 2015 2015 The Law Society. All rights reserved. Tax and the Rule of Law The Rule of Law The Law Society believes that, in recent years, there has been a tendency on the part

Tax and the Rule of Law April 2015 2015 The Law Society. All rights reserved. Tax and the Rule of Law The Rule of Law The Law Society believes that, in recent years, there has been a tendency on the part

Response to the HM Revenue & Customs consultation on whether to bring illegal waste sites within the scope of the Landfill Tax, March 2017

Response to the HM Revenue & Customs consultation on whether to bring illegal waste sites within the scope of the Landfill Tax, March 2017 1. The UK Environmental Law Association ( UKELA ) aims to make

Response to the HM Revenue & Customs consultation on whether to bring illegal waste sites within the scope of the Landfill Tax, March 2017 1. The UK Environmental Law Association ( UKELA ) aims to make

Produced by Corbin Communications Ltd.

Produced by Corbin Communications Ltd. Table of Contents Money Laundering 1 Terrorist Financing 1 The Threat 1 The Law 1 What are Revelent Business Activities? 2 Some Key provisions of the Proceeds of

Produced by Corbin Communications Ltd. Table of Contents Money Laundering 1 Terrorist Financing 1 The Threat 1 The Law 1 What are Revelent Business Activities? 2 Some Key provisions of the Proceeds of

Review of the Money Laundering Regulations 2007: The Government Response

Response to the HM Treasury consultation paper Review of the Money Laundering Regulations 2007: The Government Response September 2011 Fraud Advisory Panel Registered office: Chartered Accountants Hall,

Response to the HM Treasury consultation paper Review of the Money Laundering Regulations 2007: The Government Response September 2011 Fraud Advisory Panel Registered office: Chartered Accountants Hall,

BRITISH-IRISH PARLIAMENTARY ASSEMBLY. COMHLACHT IDIR-PHARLAIMINTEACH NA BREATAINE AGUS NA héireann REPORT. from. Committee A (Sovereign Matters)

") BRITISH-IRISH PARLIAMENTARY ASSEMBLY COMHLACHT IDIR-PHARLAIMINTEACH NA BREATAINE AGUS NA héireann REPORT from Committee A (Sovereign Matters) on Cross-border Police Cooperation and Illicit Trade 1 Background

BRITISH-IRISH PARLIAMENTARY ASSEMBLY COMHLACHT IDIR-PHARLAIMINTEACH NA BREATAINE AGUS NA héireann REPORT from Committee A (Sovereign Matters) on Cross-border Police Cooperation and Illicit Trade 1 Background

Criminal Finances Act 2017 Corporate responsibility post Mossack Fonseca

Criminal Finances Act 2017 Corporate responsibility post Mossack Fonseca Clare Connelly, Advocate Compass Chambers 1 Jun 2018 Government Policy Make it a crime if companies fail to put in place measures

Criminal Finances Act 2017 Corporate responsibility post Mossack Fonseca Clare Connelly, Advocate Compass Chambers 1 Jun 2018 Government Policy Make it a crime if companies fail to put in place measures

New Corporate Offences of Failing to Prevent the Facilitation of Tax Evasion:

New Corporate Offences of Failing to Prevent the Facilitation of Tax Evasion: Ten Frequently Asked Questions September 2017 Introduction The Criminal Finances Act 2017 (CFA) is now on the statute book

New Corporate Offences of Failing to Prevent the Facilitation of Tax Evasion: Ten Frequently Asked Questions September 2017 Introduction The Criminal Finances Act 2017 (CFA) is now on the statute book

MONEY LAUNDERING AND TERRORISM (PREVENTION) (AMENDMENT) ACT, 2013 ARRANGEMENT OF SECTIONS

(AMENDMENT) ACT, 2013 ARRANGEMENT OF SECTIONS") BELIZE: MONEY LAUNDERING AND TERRORISM (PREVENTION) (AMENDMENT) ACT, 2013 ARRANGEMENT OF SECTIONS 1. Short title. 2. of section 2. 3. of section 15. 4. of section 16. 5. of section 17. 6. of section 18.

BELIZE: MONEY LAUNDERING AND TERRORISM (PREVENTION) (AMENDMENT) ACT, 2013 ARRANGEMENT OF SECTIONS 1. Short title. 2. of section 2. 3. of section 15. 4. of section 16. 5. of section 17. 6. of section 18.

TISA Response to. Pension scams: consultation

TISA Response to Pension scams: consultation February 2017 About TISA TISA is a unique, consumer focused membership organisation. Our aim is to improve the financial wellbeing of UK consumers by aligning

TISA Response to Pension scams: consultation February 2017 About TISA TISA is a unique, consumer focused membership organisation. Our aim is to improve the financial wellbeing of UK consumers by aligning

Industry Perspective - Illicit Tobacco Trade and How to Tackle It. WCO Knowledge Academy Brussels 3 July 2014

Industry Perspective - Illicit Tobacco Trade and How to Tackle It WCO Knowledge Academy Brussels 3 July 2014 Industry Perspective illicit tobacco trade and how to tackle it Agenda 1. Extent, nature, impact

Industry Perspective - Illicit Tobacco Trade and How to Tackle It WCO Knowledge Academy Brussels 3 July 2014 Industry Perspective illicit tobacco trade and how to tackle it Agenda 1. Extent, nature, impact

1 Introduction. 2 Executive summary

HMRC Consultation Document Tackling offshore tax evasion: a new corporate criminal offence of failure to prevent the facilitation of evasion Response by the Chartered Institute of Taxation 1 Introduction

HMRC Consultation Document Tackling offshore tax evasion: a new corporate criminal offence of failure to prevent the facilitation of evasion Response by the Chartered Institute of Taxation 1 Introduction

CRIMINAL SENTENCING (EQUITY FINES) BILL

BILL") CRIMINAL SENTENCING (EQUITY FINES) BILL DR BILL WILSON MSP SUMMARY OF CONSULTATION RESPONSES Contents Introduction...1 General...2 Positive responses...2 Mixed responses...2 Unsupportive responses...3

CRIMINAL SENTENCING (EQUITY FINES) BILL DR BILL WILSON MSP SUMMARY OF CONSULTATION RESPONSES Contents Introduction...1 General...2 Positive responses...2 Mixed responses...2 Unsupportive responses...3

THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES TREASURY LAWS AMENDMENT (ILLICIT TOBACCO OFFENCES) BILL 2018

BILL 2018") 2016-2017-2018 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES TREASURY LAWS AMENDMENT (ILLICIT TOBACCO OFFENCES) BILL 2018 EXPLANATORY MEMORANDUM (Circulated by authority of the

2016-2017-2018 THE PARLIAMENT OF THE COMMONWEALTH OF AUSTRALIA HOUSE OF REPRESENTATIVES TREASURY LAWS AMENDMENT (ILLICIT TOBACCO OFFENCES) BILL 2018 EXPLANATORY MEMORANDUM (Circulated by authority of the

1 Introduction. 2 Executive summary

HMRC Consultation Document Tackling offshore tax evasion: Civil sanctions for enablers of offshore evasion Response by the Chartered Institute of Taxation 1 Introduction 1.1 This consultation is inviting

HMRC Consultation Document Tackling offshore tax evasion: Civil sanctions for enablers of offshore evasion Response by the Chartered Institute of Taxation 1 Introduction 1.1 This consultation is inviting

Losses to the Revenue from Frauds on Alcohol Duty

HM Customs and Excise Losses to the Revenue from Frauds on Alcohol Duty REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 178 Session 2001-2002: 19 July 2001 HM Customs and Excise Losses to the Revenue

HM Customs and Excise Losses to the Revenue from Frauds on Alcohol Duty REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 178 Session 2001-2002: 19 July 2001 HM Customs and Excise Losses to the Revenue

The Confiscation Investigation: Investigating the Financial Benefit Made from Crime

The Confiscation Investigation: Investigating the Financial Benefit Made from Crime Karen Bullock * Abstract The court-ordered confiscation order is the primary means of recovering a defendant s financial

The Confiscation Investigation: Investigating the Financial Benefit Made from Crime Karen Bullock * Abstract The court-ordered confiscation order is the primary means of recovering a defendant s financial

European Commission s Working Document on Implementing Measures under the Third Money Laundering Directive Response of the Law Society

European Commission s Working Document on Implementing Measures under the Third Money Laundering Directive Response of the Law Society 1 European Commission's Working Document on Implementing Measures

European Commission s Working Document on Implementing Measures under the Third Money Laundering Directive Response of the Law Society 1 European Commission's Working Document on Implementing Measures

Our ref COMM LIT/OPEN/-1/TIHA OH ZO'I5 Your ref

Simmons &Simmons Simmons &Simmons LLP CityPoint One Ropemaker Street London EC2Y 9SS United Kingdom T +44 20 7628 2020 F +44 20 7628 2070 DX Box No 12 Our ref COMM LIT/OPEN/-1/TIHA OH OCtOb@f ZO'I5 Your

Simmons &Simmons Simmons &Simmons LLP CityPoint One Ropemaker Street London EC2Y 9SS United Kingdom T +44 20 7628 2020 F +44 20 7628 2070 DX Box No 12 Our ref COMM LIT/OPEN/-1/TIHA OH OCtOb@f ZO'I5 Your

MONEY LAUNDERING - HIGH VALUE DEALERS

MONEY LAUNDERING - HIGH VALUE DEALERS Money Laundering - High Value Dealers The Money Laundering Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (the Regulations) apply to a

MONEY LAUNDERING - HIGH VALUE DEALERS Money Laundering - High Value Dealers The Money Laundering Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (the Regulations) apply to a

FRAUD ADVISORY PANEL REPRESENTATION 02/17

FRAUD ADVISORY PANEL REPRESENTATION 02/17 RESPONSE TO CORPORATE LIABILITY FOR ECONOMIC CRIME CALL FOR EVIDENCE PUBLISHED 13 JANUARY 2017 The Fraud Advisory Panel welcomes the opportunity to comment on

FRAUD ADVISORY PANEL REPRESENTATION 02/17 RESPONSE TO CORPORATE LIABILITY FOR ECONOMIC CRIME CALL FOR EVIDENCE PUBLISHED 13 JANUARY 2017 The Fraud Advisory Panel welcomes the opportunity to comment on

Member States capabilities in fighting tax crimes

Belgium Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax burden.

Belgium Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax burden.

Commercial legal policy

Commercial legal policy Policy summary Matrix Underwriting SME/ Commercial A Partner You Can Trust The purpose of this summary is to help you understand your insurance policy. It sets out the significant

Commercial legal policy Policy summary Matrix Underwriting SME/ Commercial A Partner You Can Trust The purpose of this summary is to help you understand your insurance policy. It sets out the significant

New UK Corporate Offences of Failure to Prevent the Facilitation of Tax Evasion

August 2017 New UK Corporate Offences of Failure to Prevent the Facilitation of Tax Evasion Overview Two new corporate criminal offences of failure to prevent the facilitation of tax evasion (the FTP offences

August 2017 New UK Corporate Offences of Failure to Prevent the Facilitation of Tax Evasion Overview Two new corporate criminal offences of failure to prevent the facilitation of tax evasion (the FTP offences

TENANCY FRAUD POLICY. Executive Summary. This document outlines our policy on how Orbit as a business approaches and manages Tenancy Fraud.

Document Title Version Tenancy Fraud Policy Final Release Date April 2018 Review Date March 2019 Extension Reason(s) Extension date approved Approver details Document Type Sponsor Author Customer and Communities

Document Title Version Tenancy Fraud Policy Final Release Date April 2018 Review Date March 2019 Extension Reason(s) Extension date approved Approver details Document Type Sponsor Author Customer and Communities

LOCAL GOVERNMENT AND REGENERATION COMMITTEE LOCAL GOVERNMENT FINANCE (UNOCCUPIED PROPERTIES ETC.) (SCOTLAND) BILL

(SCOTLAND) BILL") LOCAL GOVERNMENT AND REGENERATION COMMITTEE LOCAL GOVERNMENT FINANCE (UNOCCUPIED PROPERTIES ETC.) (SCOTLAND) BILL SUBMISSION FROM THE SCOTTISH PROPERTY FEDERATION 1. Thank you for inviting the Scottish

LOCAL GOVERNMENT AND REGENERATION COMMITTEE LOCAL GOVERNMENT FINANCE (UNOCCUPIED PROPERTIES ETC.) (SCOTLAND) BILL SUBMISSION FROM THE SCOTTISH PROPERTY FEDERATION 1. Thank you for inviting the Scottish

HUMAN CAPITAL FRAUD AND CORRUPTION PREVENTION

1. Policy Statement Grindrod Limited ( Grindrod ) is committed to its responsibility of protecting its revenue, expenditure, assets and reputation from any attempt by any person to gain financial or other

1. Policy Statement Grindrod Limited ( Grindrod ) is committed to its responsibility of protecting its revenue, expenditure, assets and reputation from any attempt by any person to gain financial or other

8 TH EUROPEAN HEALTHCARE FRAUD AND CORRUPTION NETWORK ANNUAL CONFERENCE 6 TH -7 TH OCTOBER KRAKOW

8 TH EUROPEAN HEALTHCARE FRAUD AND CORRUPTION NETWORK ANNUAL CONFERENCE 6 TH -7 TH OCTOBER KRAKOW Dave White Head of Fraud Investigation Service Department for Work and Pensions 1 Contents Introduction

8 TH EUROPEAN HEALTHCARE FRAUD AND CORRUPTION NETWORK ANNUAL CONFERENCE 6 TH -7 TH OCTOBER KRAKOW Dave White Head of Fraud Investigation Service Department for Work and Pensions 1 Contents Introduction

Name Summary Comments. Accounting Standards Review Board (ASRB)

") Name Summary Comments Accounting Standards Review Board (ASRB) Submission relates to Part 4 of the bill, which will transform the ASRB into the External Reporting Board (XRB), with a wider set of responsibilities.

Name Summary Comments Accounting Standards Review Board (ASRB) Submission relates to Part 4 of the bill, which will transform the ASRB into the External Reporting Board (XRB), with a wider set of responsibilities.

Corporate Criminal Offence: Failure to Prevent Facilitation of Tax Evasion

Tax Alert May 12, 2017 Corporate Criminal Offence: Failure to Prevent Facilitation of Tax Evasion The Criminal Finance Act 2017 received Royal Assent on April 27, 2017, making its way onto the statute

Tax Alert May 12, 2017 Corporate Criminal Offence: Failure to Prevent Facilitation of Tax Evasion The Criminal Finance Act 2017 received Royal Assent on April 27, 2017, making its way onto the statute

The UK s Corporate Offence of Failure to Prevent the Facilitation of Tax Evasion TTN Conference New York

The UK s Corporate Offence of Failure to Prevent the Facilitation of Tax Evasion TTN Conference New York 7 May 2018 2018 Milestone International Tax Partners LLP Overview of Slides 1. Transparency, Reporting

The UK s Corporate Offence of Failure to Prevent the Facilitation of Tax Evasion TTN Conference New York 7 May 2018 2018 Milestone International Tax Partners LLP Overview of Slides 1. Transparency, Reporting

Association of Accounting Technicians response to HMRC consultation document Tackling the hidden economy: Sanctions

Association of Accounting Technicians response to HMRC consultation document Tackling the hidden economy: Sanctions 1 Association of Accounting Technicians response to HMRC consultation document Tackling

Association of Accounting Technicians response to HMRC consultation document Tackling the hidden economy: Sanctions 1 Association of Accounting Technicians response to HMRC consultation document Tackling

Background. Questions. Principle

Response to Department for Business Innovations & Skills Beneficial Ownership Transparency discussion paper from National Association of Estate Agents (NAEA) April 2016 Background 1. National Association

Response to Department for Business Innovations & Skills Beneficial Ownership Transparency discussion paper from National Association of Estate Agents (NAEA) April 2016 Background 1. National Association

EXPLANATORY MEMORANDUM TO THE SERIOUS CRIME ACT 2007 (SPECIFIED ANTI-FRAUD ORGANISATIONS) ORDER No. 2353

ORDER No. 2353") EXPLANATORY MEMORANDUM TO THE SERIOUS CRIME ACT 2007 (SPECIFIED ANTI-FRAUD ORGANISATIONS) ORDER 2008 2008 No. 2353 1. This explanatory memorandum has been prepared by the Home Office and is laid before

EXPLANATORY MEMORANDUM TO THE SERIOUS CRIME ACT 2007 (SPECIFIED ANTI-FRAUD ORGANISATIONS) ORDER 2008 2008 No. 2353 1. This explanatory memorandum has been prepared by the Home Office and is laid before

We have seen and generally support the comments made by Law Society of England and Wales in its response (the Law Society Response).

.") City of London Law Society Company Law Committee response to the Department for Business Innovation and Skills Discussion Paper on Transparency & Trust: enhancing the transparency of UK company ownership

City of London Law Society Company Law Committee response to the Department for Business Innovation and Skills Discussion Paper on Transparency & Trust: enhancing the transparency of UK company ownership

Overview on anti-corruption rules and regulations in the UNITED KINGDOM

Overview on anti-corruption rules and regulations in the UNITED KINGDOM Author: Chris Whalley I. What is the anti-corruption legal framework in your country (including brief overview on active / passive

Overview on anti-corruption rules and regulations in the UNITED KINGDOM Author: Chris Whalley I. What is the anti-corruption legal framework in your country (including brief overview on active / passive

Upper Tribunal (Immigration and Asylum Chamber) DA/00257/2014 THE IMMIGRATION ACTS

DA/00257/2014 THE IMMIGRATION ACTS") Upper Tribunal (Immigration and Asylum Chamber) DA/00257/2014 THE IMMIGRATION ACTS Heard at: Field House Decision and Reasons Promulgated On 24 th November 2015 On 11 th December 2015 Before Upper Tribunal

Upper Tribunal (Immigration and Asylum Chamber) DA/00257/2014 THE IMMIGRATION ACTS Heard at: Field House Decision and Reasons Promulgated On 24 th November 2015 On 11 th December 2015 Before Upper Tribunal

Conduct and Competence Committee. Substantive Meeting. 08 December Nursing and Midwifery Council, George Street, Edinburgh, EH2 4LH

Conduct and Competence Committee Substantive Meeting 08 December 2016 Nursing and Midwifery Council, 114-116 George Street, Edinburgh, EH2 4LH Name of Registrant: NMC PIN: Part(s) of the register: Bernard

Conduct and Competence Committee Substantive Meeting 08 December 2016 Nursing and Midwifery Council, 114-116 George Street, Edinburgh, EH2 4LH Name of Registrant: NMC PIN: Part(s) of the register: Bernard

HMRC Consultation Document Tackling Offshore Tax Evasion: A Requirement to Correct Response by the Chartered Institute of Taxation

HMRC Consultation Document Tackling Offshore Tax Evasion: A Requirement to Correct Response by the Chartered Institute of Taxation 1 Introduction 1.1 This is the latest in a series of consultations by

HMRC Consultation Document Tackling Offshore Tax Evasion: A Requirement to Correct Response by the Chartered Institute of Taxation 1 Introduction 1.1 This is the latest in a series of consultations by

New Corporate Offence for failing to prevent Tax Evasion: Are you prepared?

New Corporate Offence for failing to prevent Tax Evasion: Are you prepared? The UK Government s desire to extend further its reach in policing financial crime in the UK and beyond shows no sign of abating

New Corporate Offence for failing to prevent Tax Evasion: Are you prepared? The UK Government s desire to extend further its reach in policing financial crime in the UK and beyond shows no sign of abating

The Central Bank of The Bahamas

The Central Bank of The Bahamas CONSULTATION PAPER on the Draft Banks and Trust Companies Regulation (Amendment) (No. 1) Bill, 2013 and the Draft Banks and Trust Companies (Administrative Monetary Penalties),

The Central Bank of The Bahamas CONSULTATION PAPER on the Draft Banks and Trust Companies Regulation (Amendment) (No. 1) Bill, 2013 and the Draft Banks and Trust Companies (Administrative Monetary Penalties),

Policies, Procedures, Guidelines and Protocols

Policies, Procedures, Guidelines and Protocols Document Details Title Anti-Crime Specialists and Human Resources Advisory Team Protocol Trust Ref No 1580-36302 Local Ref (optional) Main points the document

Policies, Procedures, Guidelines and Protocols Document Details Title Anti-Crime Specialists and Human Resources Advisory Team Protocol Trust Ref No 1580-36302 Local Ref (optional) Main points the document

HMRC Penalties: A Discussion Document The Law Society's response May 2015

HMRC Penalties: A Discussion Document The Law Society's response May 2015 2015 The Law Society. All rights reserved. Introduction 1. This response has been prepared by the Tax Committee of The Law Society

HMRC Penalties: A Discussion Document The Law Society's response May 2015 2015 The Law Society. All rights reserved. Introduction 1. This response has been prepared by the Tax Committee of The Law Society

The aim of all of these new developments is to try to bring more consistency and predictability to the way of working with the UK public sector.

20 August 2013 UK Public Procurement Law Digest: Policies, Policies, Policies By Alistair Maughan The UK and EU procurement law landscape in 2013 has been notable for the relative lack of interesting and

20 August 2013 UK Public Procurement Law Digest: Policies, Policies, Policies By Alistair Maughan The UK and EU procurement law landscape in 2013 has been notable for the relative lack of interesting and

NEW DUTIES OF FRENCH AN D HONG KONG COMPANIES IN LINE WITH OECD S UPSCALED STANDARD TO FIGHT AGAINST MONEY LAUNDERING WORLDWIDE 1 OUTLINE

NEW DUTIES OF FRENCH AN D HONG KONG COMPANIES IN LINE WITH OECD S UPSCALED STANDARD TO FIGHT AGAINST MONEY LAUNDERING WORLDWIDE 1 OUTLINE French Law. - Following the European Directive 2015/849 dated 20

NEW DUTIES OF FRENCH AN D HONG KONG COMPANIES IN LINE WITH OECD S UPSCALED STANDARD TO FIGHT AGAINST MONEY LAUNDERING WORLDWIDE 1 OUTLINE French Law. - Following the European Directive 2015/849 dated 20

http://e-asia.uoregon.edu HONG KONG TRADE SUMMARY The U.S. trade surplus with Hong Kong was $6.5 billion in 2004, an increase of $1.8 billion from $4.7 billion in 2003. U.S. goods exports in 2004 were

http://e-asia.uoregon.edu HONG KONG TRADE SUMMARY The U.S. trade surplus with Hong Kong was $6.5 billion in 2004, an increase of $1.8 billion from $4.7 billion in 2003. U.S. goods exports in 2004 were

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mr Alan Goddard Heard on: 30 August 2016 Location: The Adelphi, 1-11 John Adam Street,

DISCIPLINARY COMMITTEE OF THE ASSOCIATION OF CHARTERED CERTIFIED ACCOUNTANTS REASONS FOR DECISION In the matter of: Mr Alan Goddard Heard on: 30 August 2016 Location: The Adelphi, 1-11 John Adam Street,

AIMS WHITEPAPER: AMENDMENTS TO THE HEAVY VEHICLE NATIONAL LAW

1 Contents Introduction... 3 Background... 3 What has changed?... 4 Preparing for the Amendments... 5 Insurance implications... 6 2 Introduction With the introduction of the new Heavy Vehicle National

1 Contents Introduction... 3 Background... 3 What has changed?... 4 Preparing for the Amendments... 5 Insurance implications... 6 2 Introduction With the introduction of the new Heavy Vehicle National

STATE OPTIONS TO PREVENT AND REDUCE CIGARETTE SMUGGLING AND BLOCK OTHER ILLEGAL STATE TOBACCO TAX EVASION

STATE OPTIONS TO PREVENT AND REDUCE CIGARETTE SMUGGLING AND BLOCK OTHER ILLEGAL STATE TOBACCO TAX EVASION To try to block or reduce state tobacco tax increases, tobacco companies and their allies regularly

STATE OPTIONS TO PREVENT AND REDUCE CIGARETTE SMUGGLING AND BLOCK OTHER ILLEGAL STATE TOBACCO TAX EVASION To try to block or reduce state tobacco tax increases, tobacco companies and their allies regularly

Draft Registration of Overseas Entities Bill

17 September 2018 To: transparencyandtrust@beis.gov.uk Introduction 1. The British Property Federation (BPF) represents the commercial real estate sector. We promote the interests of those with a stake

17 September 2018 To: transparencyandtrust@beis.gov.uk Introduction 1. The British Property Federation (BPF) represents the commercial real estate sector. We promote the interests of those with a stake

gamevy Anti- Money Laundering Detecting and Preventing Financial Crime Training for Gamevy

gamevy Anti- Money Laundering Detecting and Preventing Financial Crime Training for Gamevy Introduction This document is Gamevy s training on anti- money laundering regulations within the context of our

gamevy Anti- Money Laundering Detecting and Preventing Financial Crime Training for Gamevy Introduction This document is Gamevy s training on anti- money laundering regulations within the context of our

ABCsolutions Inc. CREA - Introduction

CREA - Introduction The AMLTF course is designed to assist CREA members to comply in part with the training component under Canada s Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA)

CREA - Introduction The AMLTF course is designed to assist CREA members to comply in part with the training component under Canada s Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA)

Review of the Scrap Metal Dealers Act 2013

Review of the Scrap Metal Dealers Act 2013 Presented to Parliament by the Secretary of State for the Home Department by Command of Her Majesty December 2017 Cm 9552 Review of the Scrap Metal Dealers Act

Review of the Scrap Metal Dealers Act 2013 Presented to Parliament by the Secretary of State for the Home Department by Command of Her Majesty December 2017 Cm 9552 Review of the Scrap Metal Dealers Act

A Green Light to Rogue Landlords

Legal Aid, Sentencing and Punishment of Offenders Bill Briefing for Lords committee A Green Light to Rogue Landlords The legal aid cuts give a green light to rogue landlords by making it much harder for

Legal Aid, Sentencing and Punishment of Offenders Bill Briefing for Lords committee A Green Light to Rogue Landlords The legal aid cuts give a green light to rogue landlords by making it much harder for

Country Comparative Legal Guides. Ireland: Insurance & Reinsurance

Country Comparative Legal Guides Ireland: Insurance & Reinsurance Country Author: Matheson Sharon Daly, Partner sharon.daly@ma theson.com April McClements, Partner april.mcclement s@matheson.co m Darren

Country Comparative Legal Guides Ireland: Insurance & Reinsurance Country Author: Matheson Sharon Daly, Partner sharon.daly@ma theson.com April McClements, Partner april.mcclement s@matheson.co m Darren

Best practices. Chapter V

103 Chapter V Best practices This chapter describes best practices for tobacco tax policy, emphasizing the public health impact of tobacco taxes while also recognizing the importance of the revenues generated

103 Chapter V Best practices This chapter describes best practices for tobacco tax policy, emphasizing the public health impact of tobacco taxes while also recognizing the importance of the revenues generated

Recommendation of the Council for Further Combating Bribery of Foreign Public Officials in International Business Transactions

Working Group on Bribery in International Business Transactions Recommendation of the Council for Further Combating Bribery of Foreign Public Officials in International Business Transactions 26 NOVEMBER

Working Group on Bribery in International Business Transactions Recommendation of the Council for Further Combating Bribery of Foreign Public Officials in International Business Transactions 26 NOVEMBER

Fraud and Error Penalties and Sanctions. Equality impact assessment March 2011

Fraud and Error Penalties and Sanctions Equality impact assessment March 2011 Equality impact assessment for Fraud and Error Penalties and Sanctions Brief outline of the policy or service 1. The government

Fraud and Error Penalties and Sanctions Equality impact assessment March 2011 Equality impact assessment for Fraud and Error Penalties and Sanctions Brief outline of the policy or service 1. The government

HMRC fast facts. Record revenues for the UK. May 2014 Bulletin

May 2014 Bulletin HMRC fast facts Record revenues for the UK This Government inherited the largest deficit in peacetime history. We have made it our job to restore the nation s fiscal credibility by reducing

May 2014 Bulletin HMRC fast facts Record revenues for the UK This Government inherited the largest deficit in peacetime history. We have made it our job to restore the nation s fiscal credibility by reducing

Assessment of international and domestic risks of money laundering and terrorist financing affecting Scottish solicitors (May 2017)

") 1 Law Society of Scotland Assessment of international and domestic risks of money laundering and terrorist financing affecting Scottish solicitors (May 2017) 2 Index Introduction 3 Overall Conclusion 4

1 Law Society of Scotland Assessment of international and domestic risks of money laundering and terrorist financing affecting Scottish solicitors (May 2017) 2 Index Introduction 3 Overall Conclusion 4

Landfill Tax evasion by landfill operators and the new offences of facilitation 24 April 2017, 12:00 12:45

Landfill Tax evasion by landfill operators and the new offences of facilitation 24 April 2017, 12:00 12:45 Host Presenter Presenter Presenter Adam Read Resource Efficiency & Waste Management Practice Director

Landfill Tax evasion by landfill operators and the new offences of facilitation 24 April 2017, 12:00 12:45 Host Presenter Presenter Presenter Adam Read Resource Efficiency & Waste Management Practice Director