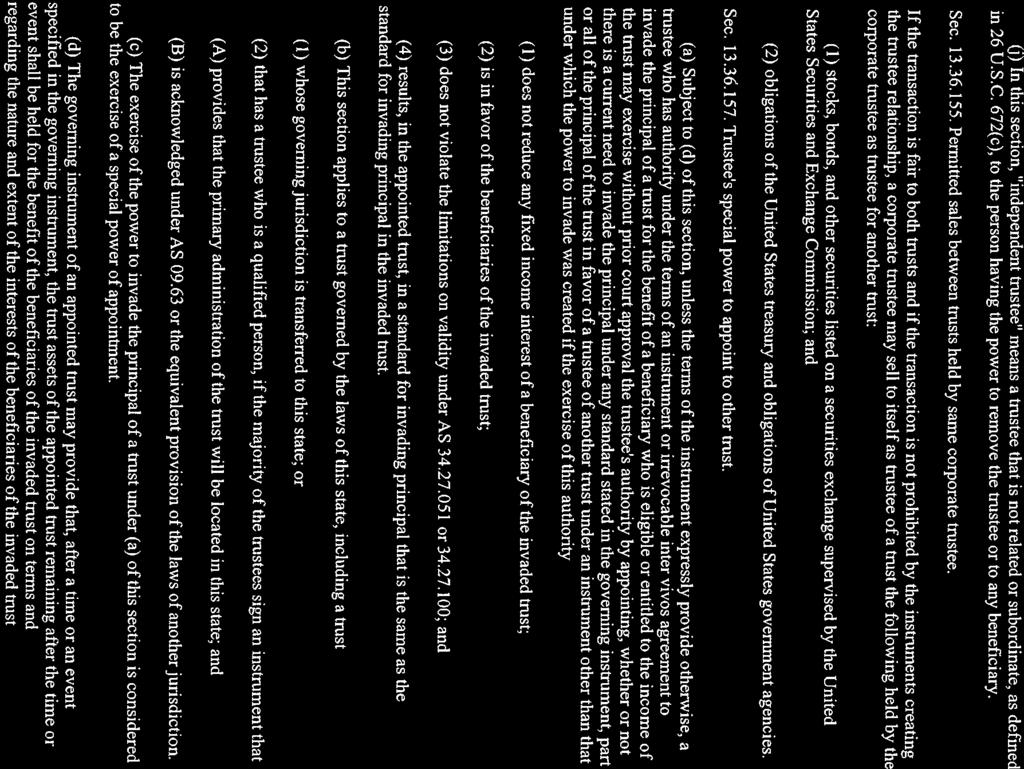

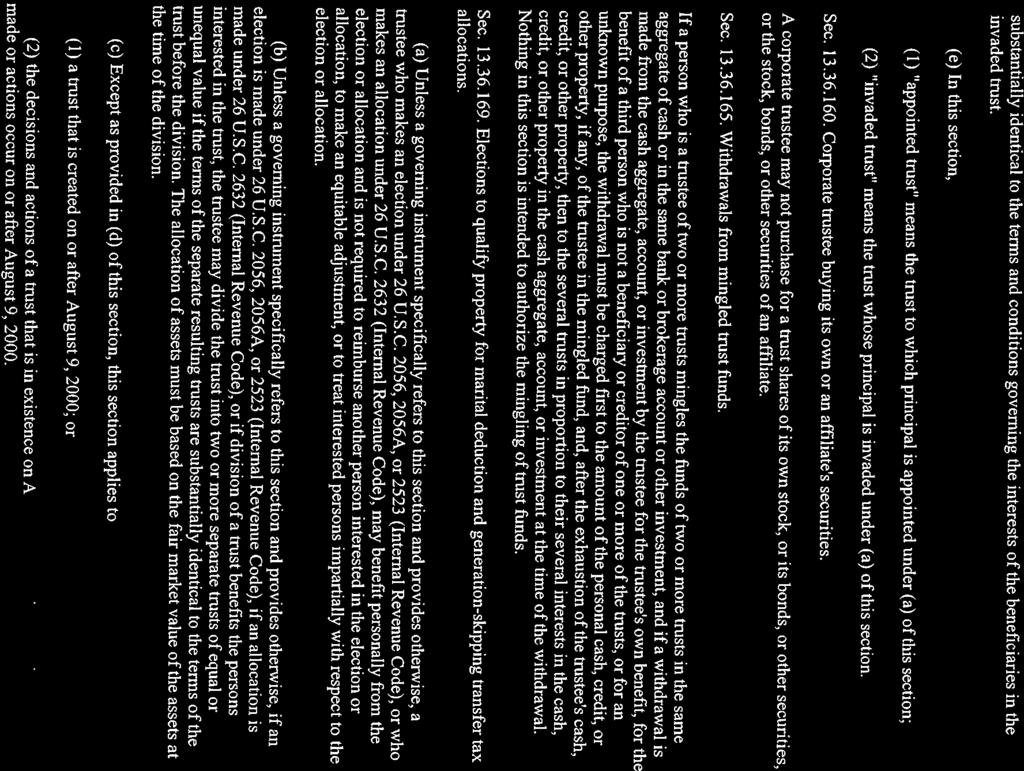

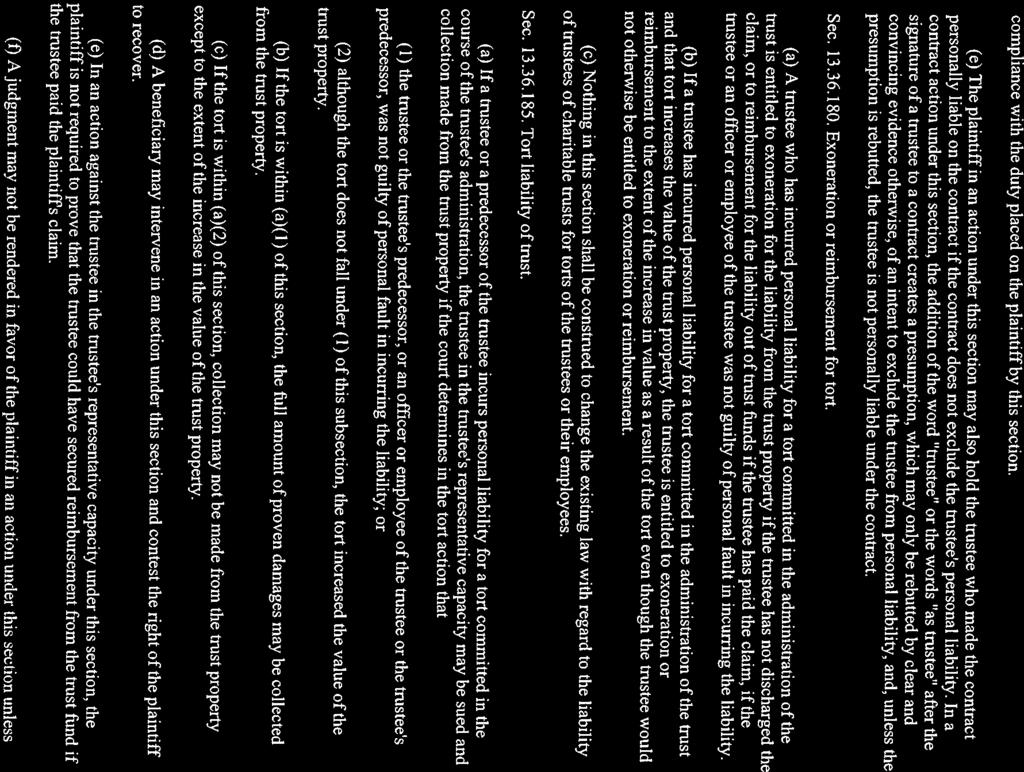

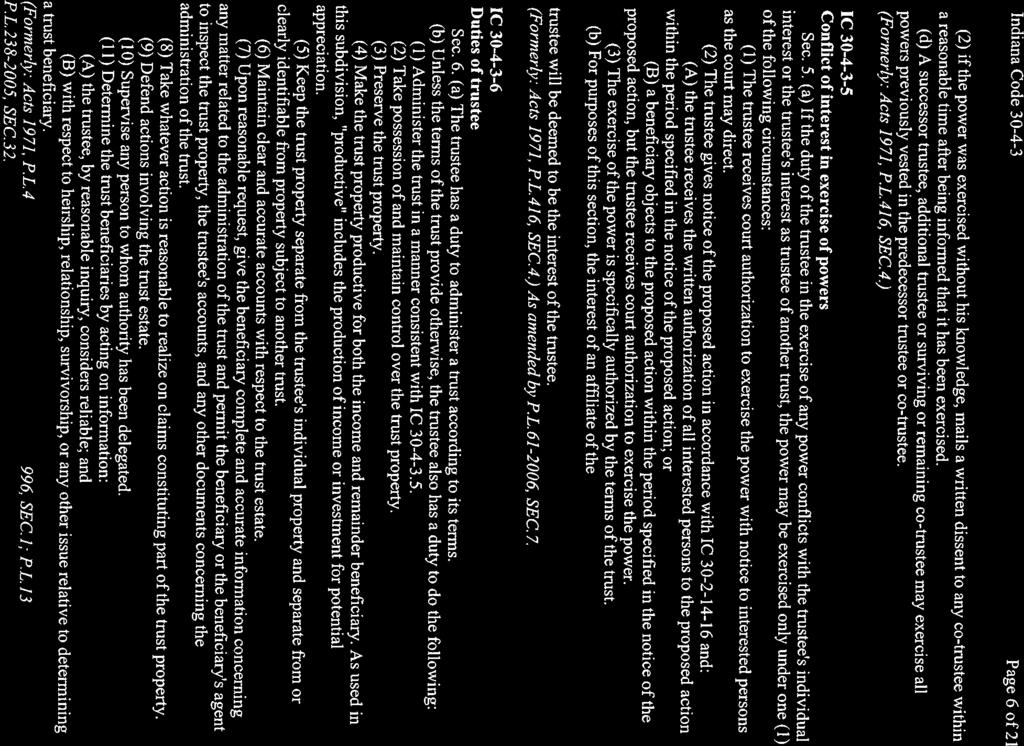

Trust Decanting: Flexibility and Danger Crafting Trust Terms to Achieve Tax Benefits, Revise Fiduciary Powers, and Mitigate Beneficiary Liability

|

|

|

- Louisa Edwards

- 5 years ago

- Views:

Transcription

1 Presenting a live 100 minute webinar with interactive Q&A Trust Decanting: Flexibility and Danger Crafting Trust Terms to Achieve Tax Benefits, Revise Fiduciary Powers, and Mitigate Beneficiary Liability THURSDAY, OCTOBER 6, pm Eastern 12pm Central 11am Mountain 10am Pacific Td Today s faculty features: James P. Spica, Member, Dickinson Wright, Detroit Meryl G. Finkelstein, Sr. Counsel, Fulbright & Jaworski, New York Thomas R. Pulsifer, Partner, Morris Nichol Arsht & Tunnell, Wilmington, Del. Todd A. Flubacher, Partner, Morris Nichols Arsht & Tunnell, Wilmington, Del. The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions ed to registrants for additional information. If you have any questions, please contact Customer Service at ext. 10.

2 Appendix Ancillary Outline: Decanting Tax Advantaged Trusts in Michigan Post Perpetuities Reform RAP Applicability for Property Subject to Michigan Law (1) Is the interest in question ( instant interest ) a nonvested interest 1 or a power of appointment? No Yes The RAP is irrelevant to the instant interest s validity (2) Is the instant interest an interest in, or power over, real property? No Yes (3) Is the instant interest an interest in, or power over, (personal) property held in a trust that was revocable on, or created after, May 28, 2008? No Yes Michigan s USRAP applies to the instant interest (90- year wait-andsee) 2 Michigan s USRAP applies to the instant interest (90- year wait-andsee) (4) Does the trust include assets that were held in a trust that was irrevocable on September 25, 1985, which assets, in the meantime, (a) have continuously been held in trust and (b) have not been subject to a general power of appointment? 3 No Yes Michigan s USRAP applies to the instant interest (90- year wait-andsee) 1 I.e., a contingent interest created by transfer. 2 The adoption of the uniform statutory rule against perpetuities displaced the common law RAP in Michigan with respect to interests created on or after the USRAP s 1988 effective date. See MICH. COMP. LAWS ANN The common law perpetuities testing period is still relevant under the USRAP, for an interest that must vest (if at all) within that period is, for that reason, valid under the USRAP. Id But an interest that may vest beyond the common law period cannot be invalid under the USRAP before the relevant wait-and-see period elapses, a result that flatly contradicts the common law RAP. See id. Thus, one should not confuse the continued relevance of the common law testing period with continued application of the common law RAP itself: the USRAP makes use of the former while displacing the latter. 3 At this point, in order to keep the flowchart binary (i.e., Yes or No, but not both), we have to adopt a sort of separate-share rule: if a trust comprises both (a) assets described in question (4) and (b) other assets, the respective shares are treated as separate trusts for purposes of the flowchart. With respect to the share that comprises assets described in question (4), the answer to question (4) is, Yes ; with respect to the share that comprises other assets, the answer to question (4) is, No. Stafford Publications CLE Webinar App. 1

3 (5) Was the instant interest created 4 by the exercise of a power of appointment? No Yes The RAP is irrelevant to the instant interest s validity 5 (6) Was the power whose exercise created the instant interest itself created by the exercise of a power of appointment? No Yes The RAP is irrelevant to the instant interest s validity (7) Was the power whose exercise created the instant interest ( second power ) a presently exercisable general power of appointment? No Yes (8) Was the power ( first power ) whose exercise created the second power a general power of appointment? No Yes The RAP is irrelevant to the instant interest s validity The RAP is irrelevant to the instant interest s validity 4 For purposes of this flowchart, a preexisting power of appointment p1 is created by another power p2 to the extent an exercise of p2 newly subjects assets to p1. Thus, for example, if a power holder H exercises her power to appoint asset A by adding A to a preexisting trust T over which a beneficiary B has a power of appointment, then (for purposes of this flowchart) B s power over A is created by the exercise of H s power. 5 Note that this is not to say that such interests cannot be affected by saving clauses provisions in trust or other governing instruments designed to ensure that the RAP is not violated. Saving clauses do not apply the RAP to the interests they govern; rather, they prevent the RAP from invalidating those interests by forcing the interests either to vest or terminate within the relevant perpetuities testing period. If a saving clause specifies what is taken (by the drafter) to be the relevant testing period, it may force vesting regardless whether any RAP is actually applicable. A trust provision, for instance, that simply terminates all nonvested interests twenty-one years after the death of the survivor of certain people living at the time of the trust s creation is liable to have that effect regardless whether any form of RAP is applicable. Saving clauses vest or terminate interests; they do not invalidate them. So, to say that the RAP is irrelevant to a given interest's validity says nothing about whether the interest is liable to be convulsed by the effect of a saving clause. Stafford Publications CLE Webinar App. 2

4 (9) Was either the first power or the second power a fiduciary power? 6 No Yes Michigan s USRAP applies to the instant interest (360- year wait-andsee) The RAP is irrelevant to the instant interest s validity 6 I.e., a power of appointment held by a trustee in a fiduciary capacity. See MICH. COMP. LAWS ANN (b). DETROIT v1 Stafford Publications CLE Webinar App. 3

5 STRAFFORD PUBLICATIONS WEBINAR Trust Decanting: Flexibility and Danger Thursday, October 6, 1:00-2:30 PM (EDT) THE USES AND BENEFITS OF DECANTING AND DECANTING S CONCEPTUAL BASIS IN THE COMMON LAW Ancillary Outline: Decanting Tax Advantaged Trusts in Michigan James P. Spica Dickinson Wright PLLC Detroit I. Introduction A. The General Problem The general problem with which we are concerned is fear and ambition for the longevity of "GST tax advantages," namely the status of assets that are "GST tax exempt," because "grandfathered" under the Treasury's GST tax effective date regulations, or "GST-exclusion sheltered," having a "zero inclusion ratio," because of an allocation of the GST exemption described in Internal Revenue Code section For our purposes, it will not be oversimplifying to say that a grandfathered trust is one that was irrevocable on September 25, B. Significant Date Lines, Federal and State Thus the first analytically significant date line we encounter is September 25, The second date line of significance is the effective date of rule against perpetuities ( RAP ) reform (or freedom). In Michigan, the timeline on which the vintage of a GST tax advantaged trust subject to Michigan law is marked looks like this: ---9/25/ /28/08 (RAP) In Delaware, the timeline (for a GST tax advantaged trust subject to Delaware law) is: ---9/25/ (RAP) See Treas. Reg (b)(1)(i). A more accurate description would have to refer also to the regulations transition rules for wills and revocable trusts executed before October 22, 1986 and for certain cases involving mental incompetency. See id (b)(2)-(3). 2 See Personal Property Trust Perpetuities Act, 2008 Mich. Pub. Acts 148 (codified at MICH. COMP. LAWS ANN ). 3 Delaware repealed its RAP for personal property held in trust in See H.B. 245, 138th Gen. Assem., Reg. Sess. (Del. 1995), 70 Del. Laws 164.

6 C. Latitude and Constraint Matrix Whether fear or ambition predominates in one's motivation depends on (1) what the GST tax advantaged trust one is worried about provides and (2) where that trust's irrevocability falls on the relevant timeline. The logical possibilities for spotting a trust on the Michigan timeline are set out below with alternative assumptions about one aspect of what the GST tax advantaged trust we are worried about provides, viz., special powers of appointment. Irrevocability Power Holder On or before 9/25/85 After 9/25/85 but on or before 5/28/08 After 5/28/08 Beneficiary Case 1 Case 3 Case 5 Trustee Case 2 Case 4 Case 6 D. The Restatement (Third) s Tentative Muddle A trustee's discretionary power of distribution is a special power of appointment within the meaning of Michigan's Powers of Appointment Act of This tracks the treatment of a trustee s power to make discretionary distributions in the Restatement (Second) of Property: Donative Transfers ( Restatement (Second) ). 5 For reasons that will not bear scrutiny, the authors of Tentative Draft No. 5 of the Restatement (Third) of Property: Wills and Other Donative Transfers ( Restatement (Third) ) have elected not to call a trustee s power to make discretionary distributions a power of appointment, 6 though the Restatement (Third) s substantive analysis of such fiduciary powers does not differ from that of the Restatement (Second). 7 In this, the authors of Tentative Draft No. 5 are ignoring what is (literally!) textbook knowledge on the classification of special powers of appointment. To be absolutely accurate, we should point out that a power of appointment may be created in a trustee, a beneficiary of a trust, a person with a legal interest not held in trust, or in a person who has no other interest in the property.... A trustee who has discretion to pay income or principal to a named beneficiary, or discretion to 4 See MICH. COMP. LAWS ANN (c);.112 (i). 5 See RESTATEMENT (SECOND) OF PROP.: DONATIVE TRANSFERS 11.1 (1986). 6 See RESTATEMENT (THIRD) OF PROP.: WILLS & OTHER DONATIVE TRANSFERS 17.1 cmt. g (Tentative Draft No. 5, 2006). 7 See id. Stafford Publications CLE Webinar 1-2

7 spray income among a group of beneficiaries, has a special power of appointment. 8 E. The Breadth and Narrowness of Our View Decanting is often described as involving the exercise only of fiduciary, special powers of appointment. 9 So, by treating decanting (as we shall) as involving also nonfiduciary powers, we are taking a broader view of the subject. But, by focusing on powers of appointment, we are narrowing our view of the general problem described above, for decanting involves what is, decidedly, a proper subset of the occasions for fear or ambition for the longevity of GST tax advantages. There are things one can do well that will increase such longevity, and things one can do badly that will vitiate it, that do not involve powers of appointment at all. For example, in a situation in which the trustee has no discretion to make any distribution and no beneficiary has any power to appoint trust assets, on the one hand (1) a settlement agreement could extend the life of a grandfathered trust for longer than the exercise of any power of appointment (if there were any) could do 10 ; and, on the other hand, (2) a trust modified on consents could (a) forfeit grandfathered status by shifting a beneficial interest to a younger generation 11 or (b) waste an allocated GST exemption by causing the trust's assets to be includable in the transfer tax base of a current beneficiary. But we shall keep the focus on special powers of appointment as the peculiar province of trust decanting we shall confine ourselves, that is, to occasions for fear or ambition for the longevity of GST tax advantages that have particularly to do with special powers of appointment. II. Case 1 A. The GST Tax Effective Date Regulations Very Own RAP The Treasury s GST tax effective date regulations subject the tax advantage of grandfathered status to a RAP of their own ( Regulatory RAP ), and the Regulatory RAP is expressly liable to be fouled by the exercise of a special power of appointment. 12 The regulations generally exempt from GST tax any generation skipping transfer under a trust that was irrevocable on September 25, 1985 to the extent assets are not added to the trust after that date. 13 There are elaborate rules about what constitutes an addition to the assets of a grandfathered trust for this purpose, including a rule that if a nonfiduciary, nongeneral power of appointment is exercised in such a way that the vesting, absolute ownership or power of alienation of an interest in assets of the grandfathered trust may be postponed or suspended beyond the Regulatory RAP period, the assets subject to the exercise may lose exempt status, thence forward being fully subject to GST tax JESSE DUKEMINIER ET AL., WILLS, TRUSTS, AND ESTATES 591 (7th ed. 2005). 9 See, e.g., William R. Culp, Jr. & Briani Bennett Mellen, Trust Decanting: An Overview and Introduction to Creative Planning Opportunities, 45 REAL PROP. TR. & EST. L.J. 1, 1 (Spring 2010). 10 See Treas. Reg (b)(4)(i)(B). 11 See id (b)(4)(i)(D). 12 See id (b)(1)(v)(B); (b)(4)(i)(A). 13 See id (b)(1)(i). 14 See id (b)(1)(v)(B). The precise effect of loss of grandfathered status is not spelled out in the effective date regulations, and the Service has taken inconsistent positions in private letter rulings. See generally Culp & Mellen, supra note 9, at 22. Stafford Publications CLE Webinar 1-3

8 The regulations contemplate that the exempt status of assets subject to a trust that was irrevocable on September 25, 1985 may survive the assets being appointed to a new trust, provided the appointment may not postpone or suspend the vesting, absolute ownership or power of alienation of an interest in the assets beyond the Regulatory RAP period. 15 The Regulatory RAP period is twenty-one years from the death of any life in being at the time the grandfathered trust became irrevocable (plus gestation), 16 though in a nod to the uniform statutory rule against perpetuities ( USRAP ), the regulations grant that: [T]he exercise of a power of appointment that validly postpones or suspends the vesting, absolute ownership or power of alienation of an interest in property for a term of years that will not exceed 90 years (measured from the date of creation of the trust) will not be considered an exercise that postpones or suspends vesting, absolute ownership or power of alienation beyond the [regulatory] perpetuities period. 17 B. Fear: Longer-of-the-Two Provisions It is important to notice that the ninety-year period specified in the Treasury regulations as the Regulatory RAP alternative to the common law perpetuities testing period is not a waitand-see period. Whereas the USRAP sets out two tests for validity, one to be satisfied (if at all) at the time a nonvested interest or a power of appointment is created, and one to be satisfied (if necessary) anytime within ninety years thereafter, 18 the Treasury regulations set out two alternative tests both to be satisfied at the time of exercise: an exercise of a nongeneral power is unoffending under the regulations if either (i) it cannot cause postponement or suspension of vesting, absolute ownership or the power of alienation beyond twenty-one years from the death of some life in being at the time the grandfathered trust became irrevocable (plus gestation) or (ii) it cannot cause postponement or suspension of vesting, absolute ownership or the power of alienation beyond ninety years from the date of the trust s creation. It follows that the exercise of a nongeneral power of appointment that may postpone or suspend vesting, absolute ownership or the power of alienation for the longer of (i) the common law testing period or (ii) ninety years satisfies neither of the regulatory tests, for as of the time of exercise, it is possible both (A) that vesting, absolute ownership or the power of alienation will be postponed or suspended for longer than twenty-one years from the death of some life in being at the time the grandfathered trust became irrevocable (in case all of the measuring lives terminate prematurely) and (B) that postponement or suspension will be longer than ninety years (in case one of the measuring lives demonstrates pronounced longevity) See Treas. Reg (b)(1)(v)(D)(ex. 4) (especially the last sentence). 16 See id (b)(1)(v)(B)(2) (emphasis in quotation added); (b)(4)(i)(a)(2). 17 Id (b)(1)(v)(B)(2). See also id (b)(4)(i)(A)(2). See generally Jesse Dukeminier, The Uniform Statutory Rule Against Perpetuities and the GST Tax: New Perils for Practitioners and New Opportunities, 185 REAL PROP. TR. & EST. L.J. 185, (1995). 18 See MICH. COMP. LAWS ANN (1). 19 See Treas. Reg (b)(1)(v)(D)(ex. 6). See also Dukeminier, supra note 17, at Stafford Publications CLE Webinar 1-4

9 That is the reason for section 1(e) of the USRAP as amended in 1990 by the National Conference of Commissioners on Uniform State Laws. 20 Michigan, which failed to enact section 1(e) when it originally adopted the USRAP, adopted a version of the provision, tailored for what the Personal Property Trust Perpetuities Act of 2008 ( 2008 Act ) defines as special appointee trusts, 21 when it adopted the 2008 Act. 22 Michigan s version of section 1(e) appears in Michigan USRAP section 2(5): (5) If, in measuring a period from the creation of a trust or other property arrangement that was irrevocable on September 25, 1985, language in an instrument governing the effect of an exercise of a power of appointment over property exempt from federal generation skipping transfer tax (a) seeks to disallow the vesting or termination of any interest or trust beyond, (b) seeks to postpone the vesting or termination of any interest or trust until, or (c) seeks to operate in effect in any similar fashion upon, the later of (i) the expiration of a period of time ending with, or not exceeding 21 years after, the death of the survivor of specified lives in being at the creation of the trust or other property arrangement or (ii) the expiration of a period of time that exceeds or might exceed 21 years after the death of the survivor of lives in being at the creation of the trust or other property arrangement, that language is inoperative to the extent it produces a period of time that exceeds 21 years after the death of the survivor of the specified lives. 23 Now, Michigan has not had a rule against suspension of absolute ownership or the power of alienation with respect to land since 1949 and has never had a rule against suspension of absolute ownership or the power of alienation with respect to personal property. 24 But the addition of section 2(5) to Michigan s USRAP provided a substantial statutory safeguard against 20 Dukeminier, supra note 17, at See MICH. COMP. LAWS ANN as amended by 2011 Mich. Pub. Acts Compare Unif. Statutory Rule Against Perpetuities 1(e) (amended 1990), 8B U.L.A. 237 (2001) with MICH. COMP. LAWS ANN (5) as amended by 2008 Mich. Pub. Acts 149 (effective May 28, 2008). See James P. Spica, Rule Against Perpetuities Repeal in Michigan, MICH. PROB. & EST. PLAN. J., Summer 2008, at See MICH. COMP. LAWS ANN (5). 24 The common law RAP was partly superseded in Michigan, from 1847 to 1949, by statutory provisions limiting suspension of the power of alienation. See Lantis v. Cook, 69 N.W.2d 849 (Mich. 1955). Those provisions applied only to real property. Rodney v. Stotz, 273 N.W. 404 (Mich. 1937). Later amendments repealed the provisions and restored the applicability of the common law RAP to real property, thereby making uniform the rule as to perpetuities applicable to real and personal property. Public Act. No. 38, 1948 Mich. Pub. Acts 38 (effective September 23, 1949) (codified as MICH. COMP. LAWS ANN ). And there was no rule against suspension of the power of alienation at common law. See John C. Gray, The Rule Against Perpetuities (4th ed. 1942). Of course, the rule against suspension of the power of alienation has to be distinguished from prohibitions against direct restraints on alienation that may be ineffective per se, without regard to their duration. See, e.g., Stephen E. Greer, The Delaware Tax Trap and the Abolition of the Rule Against Perpetuities, 28 EST. PLAN. 68, 70 (2001). Stafford Publications CLE Webinar 1-5

10 inadvertent loss of GST tax exempt status with respect to powers of appointment over the assets of grandfathered trusts. Given that the maximum period for which exercise of a nongeneral power can postpone vesting is measured from the time the power was created, 25 section 2(5) is competent to rescue situations involving exercises of nongeneral powers subject to many common types of perpetuities saving clauses. C. Fear: Wait-and-See Periods and Perpetuity It is important to note, however, that section 2(5) does not make Michigan s USRAP foolproof with respect to grandfathered generation skipping trusts, for the scope of USRAP section 1(e) itself is far from clear. 26 We do not know, for instance, how section 2(5) would be applied if an instrument containing no saving clause at all should exercise a nongeneral power over a grandfathered trust so as clearly to violate the common law RAP with respect to one vesting contingency ( C1 ), but satisfy the common law rule with respect to an alternative contingency ( C2 ). In that case, the interest is valid under the common law rule if it vests on C2, by virtue the so-called alternative contingencies doctrine, and the interest is valid if it vests on C1 within ninety years, by virtue of the USRAP s ninety-year wait-and-see period. Thus, the USRAP is liable to provide a statutory longer-of-the-two provision in this case. 27 The 2008 Act does not apply to personal property the transfer tax status of which is still affected by the property s having been held in a trust that was grandfathered under the effective date regulations. 28 (The RAP-applicability flowchart in the Appendix schematically locates special appointee trusts among other circumstances in which Michigan s USRAP applies to property subject to Michigan law after the 2008 Act s effective date.) So, the exercise of a special power of appointment over such property in favor of a trust that became irrevocable after, May 28, 2008 will not complicate the analysis under the Treasury regulations. But practitioners deploying alternative vesting contingencies would do well either (1) to force interests created by the exercise to vest before the ninetieth anniversary of the grandfathered trust s creation or (2) to satisfy the common law RAP. D. Ambition: Extraneous Measuring Lives The effective date regulations preclude a tax-advantaged perpetuity, but the Regulatory RAP alternative of the common law testing period offers some scope for longevity planning: extending beyond any life in being at the date of the creation of the trust plus a period of 21 years We should imagine a pool of measuring lives comprising people who bid fair to achieve longevity, all of whom were born on (or, perhaps, up to three years before) the date on which the grandfathered trust became irrevocable See MICH. COMP. LAWS ANN See Dukeminier, supra note 17, at See id. 28 See MICH. COMP. LAWS ANN as amended by 2011 Mich. Pub. Acts Treas. Reg (b)(1)(v)(B)(2) (emphasis added). Stafford Publications CLE Webinar 1-6

11 III. Case 2 A. Fiduciary Special Powers Subject to the Regulatory RAP The effective date regulations (1) subject fiduciary, special powers of appointment to the Regulatory RAP, (2) raise exactly the same fears for longevity discussed above and (3) offer exactly the same scope for ambition (longevity planning) provided the terms of the grandfathered trust or state law at the time the grandfathered trust became irrevocable authorized the distribution to a new trust (or retention of the principal in the continuing trust) without the consent or approval of any beneficiary or court. 30 B. Regulation Section (b)(4)(i)(D) There is no scope for ambition (longevity planning) at all in the regulations alternative safe harbor for the exercise of a fiduciary, special power of appointment (which must be an exercise that does not shift a beneficial interest in the trust to a younger generation of beneficiaries), for that alternative requires that the exercise not extend the time for vesting of any beneficial interest in the trust beyond the period provided for in the original trust. 31 C. Common Law Decanting The Restatement (Second) and Tentative Draft No. 5 of the Restatement (Third) both support the proposition that a trustee s power to make discretionary distributions entails the power to make distributions in trust for permissible distributees unless the trust instrument that created the discretionary power manifests a contrary intent. 32 There is (as far as the author knows) no decided case binding as precedent on Michigan judges that stands for that proposition. 33 But the absence of local precedent has not prevented states considering decanting legislation from asserting that their decanting statutes are at least partly declaratory of common law applicable prior to enactment. 34 Indeed, a legislative decanting regime for Michigan, which has been proposed by Greenleaf Trust and is currently before committees of the Trust Counsel Committee of the Michigan Bankers Association and the Council of the Probate and Estate Planning Section of the State Bar, purports to be partly declarative. In any case, unless the instrument governing the grandfathered trust expressly authorizes the trustee to decant (that is, to make distributions to permissible distributees in trust), and 30 See id (b)(4)(i)(A). 31 Id (b)(4)(i)(D). 32 See RESTATEMENT (SECOND) OF PROP.: DONATIVE TRANSFERS 19.3 cmt. a illus. 2 (1986); RESTATEMENT (THIRD) OF PROP.: WILLS & OTHER DONATIVE TRANSFERS 17.1 (Tentative Draft No. 5, 2006). 33 In Paine v. Kaufman (In re Estate of Resiman), 702 N.W.2d 658 (Mich. Ct. App. 2005), the Michigan Court of Appeals adduced the foundational provisions of the Restatement (Second), but the case before the court involved a nonfiduciary power and the instrument creating the power expressly authorized appointment in trust. 34 See WILLIAM J. MCGRAW III, OHIO STATE BAR ASSOCIATION, REPORT OF THE ESTATE PLANNING, TRUST AND PROBATE LAW SECTION (n.d.), Resources/pubs/councilfiles/EstPlanComReport.pdf (explaining a proposal to enact new section of the Ohio Trust Code authorizing decanting). Stafford Publications CLE Webinar 1-7

12 provided the instrument does not rule out the trustee s decanting, 35 the scope for longevity planning in Case 2 depends on the plausibility of the claim that, as indicated in the Restatements, the common law authorizes the trustee to make distributions in trust for the benefit of permissible distributees. IV. Case 3 A. The Irrelevance of the Effective Date Regulations With Case 3, we turn our attention to GST-exclusion sheltered assets (assets having an inclusion ratio of zero because of an allocation of the GST exemption described in Code section 2631). There is absolutely nothing in the Treasury s effective date regulations that has anything to do with the GST exemption. 36 B. The Stultification of Negative Implication It is true that the Service regularly rules that there is no threat to GST-exclusion-sheltered status in circumstances in which there would be no threat to GST-tax-exempt status. 37 It is also true that only an imbecile would reason as follows: (1) If John has leapt three feet vertically, he has leapt one foot vertically; (2) John has not leapt three feet vertically; Therefore, (3) John has not leapt one foot vertically. As this example (of the logical fallacy of denying the antecedent ) suggests, to say that there is no threat to GST-exclusion-sheltered status in circumstances in which there would be no threat to GST-tax-exempt status (even if it is true), says absolutely nothing about the case in which there would be a threat to GST-tax-exempt status (if GST-tax-exempt status were relevant). The Services penchant for adverting to the effective date regulations apropos of situations to which they do not apply lends no credence whatsoever to the idea that the Regulatory RAP applies to exercises of special powers of appointment over assets to which GST exemption has been allocated. C. The Abortive Section (a)(4) The Treasury did once propose to apply the Regulatory RAP in just that way, that is to exercises of special powers of appointment over assets to which GST exemption has been 35 For the proposition that the instrument creating a power of appointment can limit the manner of the power s exercise in any particular, see MICH. COMP. LAWS ANN (c) (defining power of appointment as a power... which enables the donee of the power to designate, within any limits that may be prescribed, the transferees of the property [subject to the power] );.115(2) (requiring that an exercise comply with the requirements, if any, of the creating instrument as to the manner, time and conditions of the exercise ). See also Hannan v. Slush, 5 F.2d 718, 722 (E.D. Mich. 1925) (requiring that the power be exercised in the mode prescribed by donor). 36 See Treas. Reg (b)(4). See also, e.g., Culp & Mellen, supra note 9, at See, e.g., I.R.S. Priv. Ltr. Rul (May 29, 2007); I.R.S. Priv. Ltr. Rul (May 8, 2009). Stafford Publications CLE Webinar 1-8

13 allocated. Prior to the adoption of the final GST tax regulations, the proposed regulations under section 2652 provided: The exercise of a power of appointment that is not a general power of appointment (as defined in section 2041(b)) is treated as a transfer subject to Federal estate or gift tax by the holder of the power if the power is exercised in a manner that may postpone or suspend the vesting, absolute ownership, or power of alienation of an interest in property for a period, measured from the date of creation of the trust, extending beyond any specified life in being at the date of creation of the trust plus a period of 21 years plus, if necessary, a reasonable period of gestation (perpetuities period). For purposes of this paragraph (a)(4), the exercise of a power of appointment that validly postpones or suspends the vesting, absolute ownership or power of alienation of an interest in property for a term of years that will not exceed 90 years (measured from the date of creation of the trust) is not an exercise that may extend beyond the perpetuities period. 38 But a subsequent amendment to the proposed regulation deleted this provision 39 leaving no trace of the Treasury s faint-hearted attempt to extend the Regulatory RAP beyond the effective date provisions. D. Ambition: Access to Perpetuity (and Herein of the Difference Between Decanting and Mergers) The upshot is that there is no GST tax prohibition against extending, by the exercise of a special power of appointment, the period during which GST-exemption-sheltered assets will be held in trust. 40 With respect to personal property, in Michigan, that means access to perpetuity (or, at least, the 360-year wait-and-see period provided in the 2008 Act s anti-delaware-taxtrap provision), for (except with regard to special appointee trusts ) the 2008 Act applies to nonvested interests in personal property held in any trust revocable on, or created after, MAY 28, So, if assets of a pre-may 28, 2008 trust to which GST exemption was allocated are appointed by means of a special power to a post-may 28, 2008 trust, the assets GST-exemptionsheltered status may last either forever, or if the power thus exercised was created by another power under the circumstances described in the 2008 Act s anti-delaware-tax-trap provision, then for 360 years from the date the earlier power was created. 42 The ability to appoint into the new perpetuities regime by the creation of a new trust raises what may be one important difference, for purposes of Cases 3 and 4, between decanting 38 Prop. Treas. Reg (a)(4), 61 Fed. Reg (June 12, 1996) (subsequently amended by T.D. 8720, C.B. 187). Cf Treas. Reg (b)(1)(v)(B); (b)(4)(i)(A). 39 T.D. 8720, C.B See Culp & Mellen, supra note 9, at 23; CAROL A. HARRINGTON ET AL., GENERATION- SKIPPING TRANSFER TAX: ANALYSIS WITH FORMS 2.02[1] (2d ed. 2001). 41 See MICH. COMP. LAWS ANN As to the exception for special appointee trusts, see supra note 28 and accompanying text. 42 See MICH. COMP. LAWS ANN Stafford Publications CLE Webinar 1-9

14 the assets of an old trust into a new one, on the one hand, and the merger of an old trust with a new one, on the other: the Michigan Trust Code s merger provision may require the segregation of perpetuities parcels, depending how the phrase the rule against perpetuities speaks from different dates with reference to the trusts is interpreted. 43 E. Fear: Absence of Authority to Appoint in Trust If the instrument creating the power over the GST-exemption-sheltered assets expressly provides that the holder may appoint in trust for a permissible appointee, the holder s power to decant is clear. 44 The Restatements (Second) and (Third) stand for the proposition that unless the instrument creating a special power of appointment manifests a contrary intent, the holder of such a power may exercise the power by creating a trust for the benefit of one or more permissible appointees. 45 But if the instrument creating the power rules out appointments in trust, the power cannot provide access to perpetuity. 46 F. Fear: The Delaware Tax Trap The 2008 Act s anti-delaware-tax-trap provision prevents appointment by means of a special power to a post-may 28, 2008 trust subject to Michigan law from springing the Delaware tax trap. 47 It is still possible under the 2008 Act to spring the Delaware tax trap by creating a presently exercisable general power of appointment, 48 but the risk of someone s doing that inadvertently in this setting is practically nil, for the objective of preserving the life of GSTexemption-sheltered status precludes the creation of a general power of any kind. V. Case 4 Like the provisions on nonfiduciary, special powers of appointment, the effective date regulations provisions on fiduciary, special powers only apply to grandfathered trusts. 49 So, unless the trust instrument expresses an intent to the contrary, 50 a trustee with a special power of appointment may entertain exactly the same ambition for the longevity of GST-exclusionsheltered status as a beneficiary holding such a power may entertain. Furthermore, unless the trustee is also a beneficiary of the trust in question, the Delaware tax trap will be irrelevant See MICH. COMP. LAWS ANN (2) (emphasis added). 44 See Paine v. Kaufman (In re Estate of Resiman), 702 N.W.2d 658 (Mich. Ct. App. 2005). 45 See RESTATEMENT (SECOND) OF PROP.: DONATIVE TRANSFERS 19.3 (n.b., cmt. a, illus. 2) (1986); RESTATEMENT (THIRD) OF PROP.: WILLS & OTHER DONATIVE TRANSFERS (n.b., cmt. d) (Tentative Draft No. 5, 2006). 46 See supra note See generally, James P. Spica, A Trap for the Wary: Delaware s Anti-Delaware-Tax-Trap Statute Is Too Clever by Half (of Infinity), 43 REAL PROP. TR. & EST. L. J. 673, (2009). 48 See id. at n See Treas. Reg (b)(4). 50 See supra note 35; notes and accompanying text. 51 See Spica, supra note 47, at 675. Stafford Publications CLE Webinar 1-10

15 VI. Cases 5 and 6 Without regard to any transfer from one trust to another, GST-exclusion-sheltered status may last forever in Cases 5 and 6, at least for trusts to which GST exemption is allocated before the effective date (if ever there is one) of the proposal in the President s Fiscal Year 2012 Budget that property should be GST-exclusion sheltered only for ninety years from the date the GST exclusion is allocated. 52 As proposed, this ninety-year limitation would apply only to allocations made after the date of enactment. 53 VII. Conclusion The fear in Cases 1 and 2 is fear of an alien power, namely the Regulatory RAP. Because of that alien power, the height of ambition, in those cases, is a pool of measuring lives. In Cases 3 and 4, despite the Service s posturing in private letter rulings, there is nothing to fear from the Regulatory RAP, very little to fear from the Delaware tax trap, and much to hope from the access to perpetuity provided by the 2008 Act. For the nonce, Cases 5 and 6 are like Cases 3 and 4, without the necessity of any movement (without the necessity, that is, of appointing assets from one trust to another) in order to achieve the perpetuity of GST-exemption-sheltered status. The future, however, holds the possibility of enactment of the proposal in the President s Fiscal Year 2012 Budget prospectively to impose a unitary GST-exemption-shelter shelf life on all allocations of the GST exemption. 54 DETROIT v1 52 DEPT. OF THE TREASURY, GENERAL EXPLANATIONS OF THE ADMINISTRATION S FISCAL YEAR 2012 REVENUE PROPOSALS (2011). 53 See id. at See supra notes and accompanying text. Stafford Publications CLE Webinar 1-11

16 Strafford Publications Webinar October 6, 2011 THE DELAWARE DECANTING STATUTE Thomas R. Pulsifer Morris Nichols Arsht & Tunnell LLP 1201 North Market Street P. O. Box 1347 Wilmington, DE Telephone: (302) Facsimile: (302)

17 Table of Contents Page I. Introduction...1 A. The Concept... 1 B. Terminology... 2 II. The Statute...2 A. Overview of How the Statute Works... 2 B. Statutory Details... 3 III. Mechanics...4 A. How Is Decanting Done... 4 B. When Is Decanting Permitted... 5 C. Protecting the Trustee... 5 D. Ascertainable Standard... 6 E. Governing Law Considerations... 6 IV. Possible Uses of Decanting Statute...7 A. Alter Administrative Provisions... 7 B. Clarify Ambiguous Provisions... 8 C. Extend the Life of Trust... 8 D. Create Subtrusts... 9 E. Avoid State Income Tax... 9 F. Grant Powers of Appointment V. Generation-Skipping Transfer Tax Considerations...10 A. Treasury Reg (b)(4)(i)(D)... 10

18 The Delaware Decanting Statute I. Introduction A. The Concept At least ten states (Alaska, Arizona, Delaware, Florida, Nevada, New Hampshire, New York, North Carolina, South Dakota and Tennessee) have enacted so-called decanting statutes. The statutes vary in their details but the fundamental concept behind each is essentially the same in that all of the statutes permit trustees authorized to make outright distributions from a trust to instead make such distributions in further trust. The concept is simple but the implications and opportunities are immense and complex. This outline focuses entirely on Delaware s decanting statute. Delaware s decanting statute (12 Del. C. 3528) permits trustees empowered to distribute trust principal outright to, or among, trust beneficiaries, whether the power is discretionary or exercisable pursuant to an enforceable distribution standard, to instead distribute trust assets to a different trust for the benefit of one or more of the beneficiaries to whom the trustee could have made an outright distribution. The practical opportunity (and customary use) afforded by this statute is to permit the trustee to make a distribution from a trust governed by an outdated trust instrument to a new trust governed by a modern trust instrument held upon beneficial terms substantially identical to the beneficial terms of the old trust. Thus, without in any way altering the trust s beneficial terms, a trust trapped in an old document can be decanted to a new vessel incorporating modern investment provisions, updated administrative provisions and other useful provisions without the necessity of a court-supervised reformation. However, this customary use of the decanting statute is no more than the tip of the iceberg, as the possible uses of the decanting statute are as varied and

19 numerous as the ideas that spring from the minds of thoughtful and creative trustees and their advisors. B. Terminology For convenience and ease of understanding, the term first governing instrument is used throughout this outline to refer to an existing trust instrument, including a trust agreement, Will, court order or any other document that creates a trust (referred to herein as the first trust ) from which assets may be distributed in further trust pursuant to the decanting statute. The term second governing instrument is intended to refer to whatever document created the trust (referred to herein as the second trust ) to which assets from the first trust may be distributed pursuant to the decanting statute. The second governing instrument might be a newly minted declaration of trust made by the trustee; could be a preexisting trust instrument that created a trust already in existence prior to the decanting transaction or could be the same document, that exercises the trustee s decanting power. II. The Statute A. Overview of How the Statute Works In brief, the statute simply enables the trustee to make principal distributions in further trust when and to the extent that the trustee is empowered by the first governing instrument to make principal distributions outright. The statute does not address the possibility of decanting income so income may not be decanted as such. Of course, if the trustee is empowered to accumulate income and add it to principal, then, as a practical matter, income also may be decanted. Furthermore, if the first governing instrument requires income to be distributed, a trustee empowered to distribute principal outright could, subject to a special rule - 2 -

20 for marital deduction trusts, decant to a second trust in which the income beneficiaries of the first trust are no longer eligible to receive income. B. Statutory Details The detailed rules of the statute work essentially like the rules of a board game. The trustee is empowered by the statute to craft the second governing instrument in whatever manner seems best to the trustee (abiding by the fiduciary duties, standard of care and distributing standards imposed upon the trustee by the first governing instrument) so long as the trustee does not violate any of the rules imposed by the statute as limitations upon the trustee s decanting power. One such rule is that the second trust must have only beneficiaries who were eligible to receive principal distributions from the first trust. So the trustee may not add new beneficiaries. However, the trustee may grant one or more general or limited powers of appointment to one or more beneficiaries of the first trust who were eligible to receive distributions from the first trust. As a result, the trustee and first trust beneficiaries collectively may fairly be said to possess the ability (without adverse transfer tax consequences) to cause the benefits of first trust property to be enjoyed by persons who were not beneficiaries of the first trust. Another of the statutory rules is that the trustee may provide in the second governing instrument that, at a time or upon an event specified in the second governing instrument, the assets of the second trust shall thereafter be held for the benefit of the beneficiaries of the first trust upon terms and conditions concerning the nature and extent of each such beneficiary s interest that are substantially identical to the first governing instrument s terms and conditions concerning such beneficial interests. This means, among other things, that all of the provisions of the first governing instrument regarding beneficiaries other than those currently eligible to receive distributions (such as those who may be eligible to receive distributions in the future and - 3 -

21 remaindermen) may be preserved in the second governing instrument. However, the trustee may not add new current or non-current beneficiaries nor accelerate or otherwise alter the interests of the various non-current beneficiaries identified in the first governing instrument. So, for example, if the trustee is empowered by the first governing instrument to sprinkle distributions among the descendants of the settlor and the first governing instrument provides that the remaining trust assets pass to charity upon the death of the settlor s last living descendant, the trustee could create a second trust for the benefit of some (but less than all) of the settlor s descendants but could not provide for a distribution from the second trust to charity sooner than was permitted by the first governing trust (meaning no charity could take anything from the second trust so long as any descendant of the settlor remained living). The remaining rules are rules that prevent the trustee from (a) decanting from a revocable trust; (b) delaying the time that interests in a so-called minor s trust vest and become distributable; (c) decanting if the first governing instrument expressly forbids decanting; (d) reducing an income interest in a trust for which a marital deduction has been taken for federal estate or gift tax purposes; and (e) decanting property subject to a current withdrawal right held by a trust beneficiary who is the only beneficiary eligible for current distributions. III. Mechanics A. How Is Decanting Done The Delaware statute provides that the decanting transaction whereby trust assets are distributed from one trust to another trust must be accomplished by an instrument in writing, signed and acknowledged by the trustee and filed with the records of the trust. In this instance, the statute seems plainly to refer to the records of the first trust but it seems evident the trustee (or the two trustees if the second trust s trustee is a different trustee) for both trusts ought to keep - 4 -

22 a copy of this written instrument among the trust records. The statute mentions acknowledgment, which means that the written instrument must be notarized. Beyond these few formalities, the trustee is left to the trustee s own devices to determine how best to arrange the mechanics of decanting transactions. B. When Is Decanting Permitted Unless the first governing instrument expressly prohibits decanting, a trustee may, under Delaware law, decant whenever the trustee has authority to make outright principal distributions whether or not the trustee s distribution power is limited by an ascertainable standard but only to the extent that trust principal is currently distributable. So, for example, if the trustee may distribute up to 5% of principal annually for the education of beneficiaries, the trustee may only decant to that extent and for that purpose. C. Protecting the Trustee As a practical matter, decanting is far more likely to be employed and in a far more creative and potentially beneficial manner in cases where the trustee is adequately protected from potential liability for having engaged in the decanting transaction. Therefore, decanting works best when the trustee is fully protected from liability for having undertaken the decanting transaction. Under Delaware law, adult trust beneficiaries may release a trustee from liability for engaging in a decanting transaction. 12 Del. C Furthermore, the releases of the trust s adult beneficiaries and presumptive remaindermen generally will bind the trust s minor and unborn beneficiaries and contingent remaindermen. 12 Del. C Not surprisingly, trustees tend to be far more receptive to decanting opportunities when all of the current adult and presumptive remaindermen beneficiaries are prepared to consent to the transaction in a fashion that binds the other trust beneficiaries

23 D. Ascertainable Standard Some state s decanting statutes appear to permit decanting only when the trustee is permitted to distribute trust principal in the trustee s sole discretion and not pursuant to an ascertainable standard. The Delaware decanting statute, however, permits decanting in every case where the trustee is empowered to distribute principal without regard to whether the trustee s distribution power is constrained by an ascertainable standard. Of course, if an ascertainable standard is imposed upon the trustee, the trustee must abide by that standard when decanting just as would be the case if the trustee were making an outright distribution from the trust. E. Governing Law Considerations The Delaware decanting statute provides that the use of the statute to decant shall be considered the exercise of a power of appointment (other than a power to appoint to the powerholder, the powerholder s creditors, the powerholder s estate, or the creditors of the powerholder s estate) and shall be subject to the provisions of Chapter 5 of Title 25 of the Delaware Code concerning the time at which the permissible period of the rule against perpetuities begins and the law which determines the permissible period of the rule against perpetuities. Chapter 5 of Title 25, together with the Delaware Chancery Court s opinion in Wilmington Trust Company v. Wilmington Trust Company (26 Del. Ch. 397, 1942), makes clear that the validity of the exercise of a limited power of appointment (and, by virtue of the cross reference in the decanting statute, the validity of a decanting transaction) is governed by Delaware law whenever the trust has its situs in Delaware at the time that the power is exercised. This result is confirmed by the express provisions of 12 Del. C. 3528(f) which was added to the statute by a 2011 amendment. Accordingly, the trustee of a trust initially created outside - 6 -

24 Delaware and governed initially by the law of some other jurisdiction, could, as a matter of Delaware law, decant pursuant to the Delaware decanting statute if the trust s situs were moved to Delaware. Thus, a trustee should be able to use the decanting statute whenever the trust is administered in Delaware even if some other jurisdiction s laws govern the trust s validity, construction and administration. It should be noted, however, that in most cases Delaware law would govern matters of administration for so long as the trust s situs is Delaware. See 12 Del. C Furthermore, Delaware s release statute (12 Del. C. 3588) and virtual representation statute (12 Del. C. 3547) might not be available unless Delaware law governs administration meaning that the utility of the decanting statute might be severely compromised given the understandable reluctance of trustees to decant without some assurance that the beneficiaries will not sue the trustee if the decanting turns out to produce some adverse consequence from the point of view of one or more of the beneficiaries. IV. Possible Uses of Decanting Statute A. Alter Administrative Provisions Probably the most obvious and common use of decanting statutes in Delaware and elsewhere is to improve the trust s administrative provisions without altering beneficial interests in any manner. The statute can be used in Delaware, for example, to (i) add a direction or consent investment or distribution adviser to invest or participate in the investment of some or all of the trust assets or direct or participate in distribution decisions; (ii) modernize antiquated provisions; (iii) incorporate modern or more flexible investment authority; (iv) enumerate express powers useful or perhaps essential to the trustee; (v) add other advisers; (vi) add trust protectors or similar fiduciaries having special roles or powers such as the ability to oversee or remove trustees or other fiduciaries; (vii) revise provisions that otherwise might cause potential - 7 -

25 tax problems; and (viii) revise standards of care or liability as appropriate to increase trust flexibility. B. Clarify Ambiguous Provisions Ambiguous provisions and other inartful provisions may be addressed by decanting to a second trust governed by a second governing instrument identical to the first governing instrument except to the extent necessary to resolve the ambiguity or other problematic provisions appearing in the first governing instrument. However, in such cases, if the resolution of an ambiguity even arguably alters beneficial interests, or could in any circumstance have the effect of altering beneficial interests, a prudent trustee will not generally engage in the decanting transaction unless the trustee is protected by appropriate releases binding all of the current and potential trust beneficiaries and the trustee, in consultation with competent advisers, is satisfied that the resolution does not raise material tax considerations as there are many situations in which altering ambiguous provisions could create adverse income, gift or generation-skipping transfer tax consequences. C. Extend the Life of Trust As was mentioned in III.E above, the Delaware decanting statute provides that the use of the statute to decant shall be considered the exercise of a limited power of appointment and shall be subject to the provisions of Chapter 5 of Title 25 of the Delaware Code covering the time at which the permissible period of the rule against perpetuities begins. For the reasons explained in III.E, Delaware law will govern this issue if the trust is located in Delaware at the time of the decanting and under a unique provision of Delaware law it is possible to commence a new perpetuities period by virtue of the exercise of a limited power of appointment. Consequently, and without regard to the law governing the validity of the first trust or whether - 8 -

26 the first trust is of limited duration, a trustee may validly decant from a first trust of limited duration to a second trust of longer duration than the first including to a second trust of perpetual duration. For creditor protection purposes, state income tax avoidance and for many other reasons, the possibility of decanting to allow assets to remain in trust for longer than permitted by the first governing instrument may be extremely advantageous. However, in any case where the first trust is exempt from generation-skipping transfer tax by reason of the effective date rules or the allocation of generation-skipping transfer tax exemption to the first trust, the second trust will be subject to the generation-skipping transfer tax, for the reasons explained in V.A. below, unless (i) all of the beneficial interests in the second trust vest at the same time as the beneficial interests would have vested under the terms of the first governing instrument and (ii) the trust assets are includible in the gross estate of the beneficiaries in whom the beneficial interests vest if any of those beneficiaries die before those assets are distributed to them. D. Create Subtrusts Trustees frequently encounter material divergences in the needs and investment philosophies of a trust s beneficiaries. One solution that often ameliorates the tension sometimes caused by differing beneficiary needs and investment philosophies is to divide the assets of a single trust into separate trusts or separately invested trust shares for the appropriate beneficiaries or beneficiary groups. Decanting to separate trusts or to a second trust with appropriate subtrust or share language can often accomplish the desired result. E. Avoid State Income Tax Although the topic is beyond the scope of an outline discussing Delaware law, it appears that, pursuant to the income taxation laws of some states, trusts created by residents of the state are subject to state income taxes while identical trusts created by nonresidents of the - 9 -

27 state are not subject to state income taxation. If so, it may be that a trust created by a decanting (in most cases the second trust to which trust assets are decanted is, at least as a matter of trust law, created by the trustee of the first trust) would not be subject to income taxation by a state that taxes the first trust s income because the first trust was created by a resident of the state while the second trust was not. F. Grant Powers of Appointment Although Delaware law does not permit a trustee to create new trust beneficiaries by means of a decanting (and a contrary rule, such as appears to exist in some states, may create grave public policy concerns not to mention angst among settlors), the statute does permit the trustee to grant a general or limited power of appointment over trust property to a beneficiary to whom the trustee otherwise could have appointed the property made subject to the power. This provision seems not to raise public policy concerns as it seems appropriate to permit the trustee to allow a beneficiary to decide who takes the trust property in cases where the trustee could alternatively have distributed the property to the beneficiary who could then have given the property to whomever the beneficiary wished. The difference between the two alternatives is, of course, that while both achieve the same economic result, the outright distribution and gift often will produce adverse gift tax consequences while decanting to a second trust and granting a limited power of appointment can, with proper planning, be done in many cases so as to avoid the federal gift tax. V. Generation-Skipping Transfer Tax Considerations A. Treasury Reg (b)(4)(i)(D) Example (2) appearing in Treasury Regulation (b)(4)(i)(E) expressly addresses the fact pattern that appears to be applicable in every case where assets held in a first

28 trust that is exempt from the generation-skipping transfer tax by reason of the effective date rules (that is, the first trust is a grandfathered trust) are decanted to a second trust. The Example posits a scenario in which assets are decanted from a grandfathered trust to another trust pursuant to a state decanting statute that was not in existence at the time the grandfathered trust became irrevocable. As no decanting statutes existed prior to the advent of the current generationskipping transfer tax regime, it appears that all decantings from grandfathered trusts made pursuant to a state decanting statute are covered by Example (2). The Example concludes that the decanting constitutes a modification governed by Treasury Regulation (b)(4)(i)(D). This conclusion seems plainly correct because that regulation covers all modifications not described in paragraphs (b)(4)(i)(a), (B) or (C). Paragraph (A) in tantalizing, but apparently misleading, fashion provides that a decanting is treated as the exercise of a power (meaning the duration of the trust can be extended in certain cases) but only if the state law permitting the decanting existed before the trust became irrevocable (as is never the case given the recent vintage of the decanting statutes). As paragraphs (B) and (C) of (b)(4)(i) offer nothing of interest to decanting transactions, all statutory decantings with respect to grandfathered trusts are stuck with the straightjacket of paragraph (D). It is worth noting, however, that a trust, exempt from generation-skipping transfer tax by reason of the allocation of generation-skipping transfer tax exemption, which was created in a state that permits decanting and was created after the enactment of that state s decanting statute apparently is covered by paragraph (A) as the Internal Revenue Service as repeatedly ruled, in the private letter ruling context, that the regulatory principles concerning grandfathered trusts should apply with equal force to trusts exempt from the generation-skipping transfer tax by reason of the allocation of generation-skipping transfer tax exemption. In any case, the aforementioned straightjacket of

29 paragraph (D), apparently applicable to all grandfathered trusts, provides, in substance, that the decanting will not cause the second trust to be subject to the generation-skipping transfer tax provided that (i) the decanting could not (under any circumstance) shift a beneficial interest in the trust to a beneficiary who occupies a lower generation (as defined in Code section 2651) than the person or persons who held the beneficial interest prior to the decanting and (ii) the decanting does not extend the time for vesting of any beneficial interest in the trust beyond the period provided for in the first trust. As a result, great care must be taken in decanting assets from a grandfathered trust. However, it plainly is permissible to extend the duration of the trust so long as there is no delay in the vesting of interests

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

Strafford Publications Webinar. October 6, 2011 THE DELAWARE DECANTING STATUTE

Strafford Publications Webinar October 6, 2011 THE DELAWARE DECANTING STATUTE Thomas R. Pulsifer Morris Nichols Arsht & Tunnell LLP 1201 North Market Street P. O. Box 1347 Wilmington, DE 19899-1347 Telephone:

Strafford Publications Webinar October 6, 2011 THE DELAWARE DECANTING STATUTE Thomas R. Pulsifer Morris Nichols Arsht & Tunnell LLP 1201 North Market Street P. O. Box 1347 Wilmington, DE 19899-1347 Telephone:

Trust Decanting: Flexibility and Danger Achieving Tax Benefits, Revising Fiduciary Powers, and Mitigating Trustee Liability

Presenting a live 90-minute webinar with interactive Q&A Trust Decanting: Flexibility and Danger Achieving Tax Benefits, Revising Fiduciary Powers, and Mitigating Trustee Liability TUESDAY, OCTOBER 2,

Presenting a live 90-minute webinar with interactive Q&A Trust Decanting: Flexibility and Danger Achieving Tax Benefits, Revising Fiduciary Powers, and Mitigating Trustee Liability TUESDAY, OCTOBER 2,

www.morrisnichols.com 1 Strafford Publications Webinar November 12, 2013 Trust Decanting: FLEXIBILITY AND DANGER Todd A. Flubacher Morris, Nichols, Arsht & Tunnell LP 1201 North Market Street P. O. Box

www.morrisnichols.com 1 Strafford Publications Webinar November 12, 2013 Trust Decanting: FLEXIBILITY AND DANGER Todd A. Flubacher Morris, Nichols, Arsht & Tunnell LP 1201 North Market Street P. O. Box

Alert. Delaware Trust Act 2018 Legislative Update. Section 3547 Representation by a person with a substantially identical interest.

Trusts, Estates & Tax Alert September 18, 2018 Delaware Trust Act 2018 Legislative Update Recently enacted legislation ( Trust Act 2018 ) provides settlors, beneficiaries, fiduciaries and nonfiduciary

Trusts, Estates & Tax Alert September 18, 2018 Delaware Trust Act 2018 Legislative Update Recently enacted legislation ( Trust Act 2018 ) provides settlors, beneficiaries, fiduciaries and nonfiduciary

1. The Regulatory Approach

Section 2601. Tax Imposed 26 CFR 26.2601 1: Effective dates. T.D. 8912 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 26 Generation-Skipping Transfer Issues AGENCY: Internal Revenue Service

Section 2601. Tax Imposed 26 CFR 26.2601 1: Effective dates. T.D. 8912 DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Part 26 Generation-Skipping Transfer Issues AGENCY: Internal Revenue Service

Trust Decanting: Flexibility and Danger Achieving Tax Benefits, Revising Fiduciary Powers, and Mitigating Trustee Liability

Presenting a live 90-minute webinar with interactive Q&A Trust Decanting: Flexibility and Danger Achieving Tax Benefits, Revising Fiduciary Powers, and Mitigating Trustee Liability TUESDAY, MAY 12, 2015

Presenting a live 90-minute webinar with interactive Q&A Trust Decanting: Flexibility and Danger Achieving Tax Benefits, Revising Fiduciary Powers, and Mitigating Trustee Liability TUESDAY, MAY 12, 2015

SUMMARIES OF STATE DECANTING STATUTES

SUMMARIES OF STATE DECANTING STATUTES As of August 22, 2014 compiled by Susan T. Bart Schiff Hardin LLP, Chicago, Illinois If you have an update or revision to a state summary, please contact Susan T.

SUMMARIES OF STATE DECANTING STATUTES As of August 22, 2014 compiled by Susan T. Bart Schiff Hardin LLP, Chicago, Illinois If you have an update or revision to a state summary, please contact Susan T.

ABA Section of Real Property, Trust & Estate Law 23 rd Annual Spring Symposia New York, NY

ABA Section of Real Property, Trust & Estate Law 23 rd Annual Spring Symposia New York, NY Powers of Appointment: Exercising Powers over Perpetual Trusts & Other Tips for Drafting May 3, 2012 8:30 9:30

ABA Section of Real Property, Trust & Estate Law 23 rd Annual Spring Symposia New York, NY Powers of Appointment: Exercising Powers over Perpetual Trusts & Other Tips for Drafting May 3, 2012 8:30 9:30

An Overview of Trust Modification and Decanting

An Overview of Trust Modification and Decanting Probate and Pumpernickel September 26, 2014 J. Aaron Nelson, Jr. Merline and Meacham, P.A. 812 East North Street (29603) P.O. Box 10796 Greenville, SC 29601

An Overview of Trust Modification and Decanting Probate and Pumpernickel September 26, 2014 J. Aaron Nelson, Jr. Merline and Meacham, P.A. 812 East North Street (29603) P.O. Box 10796 Greenville, SC 29601

Trust Decanting Tax Consequences Navigating Income, Estate, Gift, and GST Tax Implications and Potential Safe Harbor Rules

Presenting a live 90-minute webinar with interactive Q&A Trust Decanting Tax Consequences Navigating Income, Estate, Gift, and GST Tax Implications and Potential Safe Harbor Rules TUESDAY, FEBRUARY 19,

Presenting a live 90-minute webinar with interactive Q&A Trust Decanting Tax Consequences Navigating Income, Estate, Gift, and GST Tax Implications and Potential Safe Harbor Rules TUESDAY, FEBRUARY 19,

Section 3301 of Title 12 defines certain terms used in

PAGE 1 OF 6 Trust Act 2011 Changes to the Delaware Code On July 13, 2011, Delaware Governor Jack Markell signed Trust Act 2011 into law, effective August 1, 2011. Trust Act 2011 provides advancements in

PAGE 1 OF 6 Trust Act 2011 Changes to the Delaware Code On July 13, 2011, Delaware Governor Jack Markell signed Trust Act 2011 into law, effective August 1, 2011. Trust Act 2011 provides advancements in

DECANTING ISSUES MEMO UNIFORM DECANTING DISTRIBUTIONS DRAFTING COMMITTEE

DECANTING ISSUES MEMO UNIFORM DECANTING DISTRIBUTIONS DRAFTING COMMITTEE I. Defining Decanting and the Middle Way A. Decanting as an Exercise of a Fiduciary Power. Decanting is an exercise of a fiduciary

DECANTING ISSUES MEMO UNIFORM DECANTING DISTRIBUTIONS DRAFTING COMMITTEE I. Defining Decanting and the Middle Way A. Decanting as an Exercise of a Fiduciary Power. Decanting is an exercise of a fiduciary

NORTH CAROLINA State Decanting Summary 1

NORTH CAROLINA State Decanting Summary 1 STATUTORY HISTORY Statutory citation N.C. GEN. STAT. 36C-8-816.1 Effective Date 10/1/09 Amendment Date(s) 7/20/10; 6/12/13; 10/1/15 ABILITY TO DECANT 1. Discretionary

NORTH CAROLINA State Decanting Summary 1 STATUTORY HISTORY Statutory citation N.C. GEN. STAT. 36C-8-816.1 Effective Date 10/1/09 Amendment Date(s) 7/20/10; 6/12/13; 10/1/15 ABILITY TO DECANT 1. Discretionary

NORTH CAROLINA 1 State Decanting Summary 2

NORTH CAROLINA 1 State Decanting Summary 2 STATUTORY HISTORY Statutory citation N.C. GEN. STAT. 36C-8-816.1 Effective Date 10/1/09 Amendment Date(s) 7/20/10; 6/12/13 ABILITY TO DECANT 1. Discretionary

NORTH CAROLINA 1 State Decanting Summary 2 STATUTORY HISTORY Statutory citation N.C. GEN. STAT. 36C-8-816.1 Effective Date 10/1/09 Amendment Date(s) 7/20/10; 6/12/13 ABILITY TO DECANT 1. Discretionary

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES Presented by: Michael M. Gordon Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, Delaware 19806 302-652-2900 mgordon@gfmlaw.com

THE USE OF ASSET PROTECTION TRUSTS FOR TAX PLANNING PURPOSES Presented by: Michael M. Gordon Gordon, Fournaris & Mammarella, P.A. 1925 Lovering Avenue Wilmington, Delaware 19806 302-652-2900 mgordon@gfmlaw.com

The Internal Revenue Service ruled in Rev. Rul

PAGE 1 OF 5 Trust Act 2010 Changes to Title 12 of the Delaware Code On July 2, 2010, Delaware Governor Jack Markell signed Trust Act 2010 into law, effective August 1, 2010. The Governor also signed into

PAGE 1 OF 5 Trust Act 2010 Changes to Title 12 of the Delaware Code On July 2, 2010, Delaware Governor Jack Markell signed Trust Act 2010 into law, effective August 1, 2010. The Governor also signed into

MASSACHUSETTS UNIFORM TRUST DECANTING ACT

Report of the Standing Committee on Massachusetts Legislation Relating to Wills, Trusts, Estates and Fiduciary Administration on the proposed MASSACHUSETTS UNIFORM TRUST DECANTING ACT Introduction The

Report of the Standing Committee on Massachusetts Legislation Relating to Wills, Trusts, Estates and Fiduciary Administration on the proposed MASSACHUSETTS UNIFORM TRUST DECANTING ACT Introduction The

New York Enacts Important New Law Governing a Trustee s Power to Pay Trust Assets to a New Trust

PAMELA EHRENKRANZ (PEhrenkranz@wlrk.com) is chair of the Trusts and Estates Practice Group at Wachtell, Lipton, Rosen & Katz in New York. Her practice is focused on developing estate plans for individual

PAMELA EHRENKRANZ (PEhrenkranz@wlrk.com) is chair of the Trusts and Estates Practice Group at Wachtell, Lipton, Rosen & Katz in New York. Her practice is focused on developing estate plans for individual

DECANTING AND PRIVATE SETTLEMENT AGREEMENTS CINCINNATI ESTATE PLANNING COUNCIL MAY 10, 2012

DECANTING AND PRIVATE SETTLEMENT AGREEMENTS CINCINNATI ESTATE PLANNING COUNCIL MAY 10, 2012 J. MICHAEL COONEY, ESQ. Dinsmore & Shohl LLP 255 E. Fifth Street, Suite 1900 Cincinnati, OH 45202 I. DECANTING:

DECANTING AND PRIVATE SETTLEMENT AGREEMENTS CINCINNATI ESTATE PLANNING COUNCIL MAY 10, 2012 J. MICHAEL COONEY, ESQ. Dinsmore & Shohl LLP 255 E. Fifth Street, Suite 1900 Cincinnati, OH 45202 I. DECANTING:

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS Delaware Trust Conference October 24, 2017 Leigh-Alexandra Basha McDermott, Will & Emery 500 Capitol Street, N.W. Washington, DC 20001 lbasha@mwe.com

MANAGING TRIVIAL PURSUITS: DOMESTICATION OF FOREIGN TRUSTS Delaware Trust Conference October 24, 2017 Leigh-Alexandra Basha McDermott, Will & Emery 500 Capitol Street, N.W. Washington, DC 20001 lbasha@mwe.com

studies Decanting is not just for sommeliers Gerry W. Beyer* Melissa J. Willms**

estate planning Introduction The term decanting sounds mysterious, but in reality, decanting is simply a form of trust modification initiated by a trustee. The trustee accomplishes the modification by

estate planning Introduction The term decanting sounds mysterious, but in reality, decanting is simply a form of trust modification initiated by a trustee. The trustee accomplishes the modification by

Morris, Nichols, Arsht & Tunnell LLP. Eliminate a Trust's State Income Tax. June An update from our Trusts & Estates Group

June 2006 Morris, Nichols, Arsht & Tunnell LLP An update from our Trusts & Estates Group Eliminate a Trust's State Income Tax A Delaware non-grantor/incomplete gift trust can help you do it. That is, if

June 2006 Morris, Nichols, Arsht & Tunnell LLP An update from our Trusts & Estates Group Eliminate a Trust's State Income Tax A Delaware non-grantor/incomplete gift trust can help you do it. That is, if

Powers of Appointment Primer. Part 2: Taxation of Powers of Appointment BY GRIFFIN BRIDGERS, SUSAN L. BOOTHBY, AND LISA C. WILLCOX

FEATURE TRUST TITLE AND ESTATE LAW Powers of Appointment Primer Part 2: Taxation of Powers of Appointment BY GRIFFIN BRIDGERS, SUSAN L. BOOTHBY, AND LISA C. WILLCOX This is the second in a two-part series

FEATURE TRUST TITLE AND ESTATE LAW Powers of Appointment Primer Part 2: Taxation of Powers of Appointment BY GRIFFIN BRIDGERS, SUSAN L. BOOTHBY, AND LISA C. WILLCOX This is the second in a two-part series

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

KENTUCKY 1 State Decanting Summary 2

KENTUCKY 1 State Decanting Summary 2 STATUTORY HISTORY Statutory citation KY. REV. STAT. ANN. 386.175 (effective 7/12/12) Effective Date 7/12/12 Amendment Date(s) ABILITY TO DECANT 1. Discretionary distribution

KENTUCKY 1 State Decanting Summary 2 STATUTORY HISTORY Statutory citation KY. REV. STAT. ANN. 386.175 (effective 7/12/12) Effective Date 7/12/12 Amendment Date(s) ABILITY TO DECANT 1. Discretionary distribution

PROPOSED AMENDMENTS TO THE REVISED GEORGIA TRUST CODE OF 2010

PROPOSED AMENDMENTS TO THE REVISED GEORGIA TRUST CODE OF 2010 State Bar of Georgia, Fiduciary Law Section Trust Code Revision Committee December 13, 2016 In 2015, the Executive Committee appointed a new

PROPOSED AMENDMENTS TO THE REVISED GEORGIA TRUST CODE OF 2010 State Bar of Georgia, Fiduciary Law Section Trust Code Revision Committee December 13, 2016 In 2015, the Executive Committee appointed a new

WISCONSIN State Decanting Summary 1

WISCONSIN State Decanting Summary 1 STATUTORY HISTORY Statutory citation 701.0418 Effective Date 7/1/14 Amendment Date(s) ABILITY TO DECANT 1. Discretionary distribution authority required to decant? 2.

WISCONSIN State Decanting Summary 1 STATUTORY HISTORY Statutory citation 701.0418 Effective Date 7/1/14 Amendment Date(s) ABILITY TO DECANT 1. Discretionary distribution authority required to decant? 2.

Meet the New Principal and Income Act And Say Goodbye to RUPIA

Meet the New Principal and Income Act And Say Goodbye to RUPIA PRINCIPAL AND INCOME LEGISLATION is important to every lawyer who drafts wills and trusts. It provides a basic operating system for trusts

Meet the New Principal and Income Act And Say Goodbye to RUPIA PRINCIPAL AND INCOME LEGISLATION is important to every lawyer who drafts wills and trusts. It provides a basic operating system for trusts

Fixing an Irrevocable Trust: Decanting and Creative Solutions

Fixing an Irrevocable Trust: Decanting and Creative Solutions California Society of CPAs May 13, 2015 11:30 am - 2:00 pm Olympic Collection Abby L.T. Feinman Laura K. Zeigler Partner Principal, Fiduciary

Fixing an Irrevocable Trust: Decanting and Creative Solutions California Society of CPAs May 13, 2015 11:30 am - 2:00 pm Olympic Collection Abby L.T. Feinman Laura K. Zeigler Partner Principal, Fiduciary

DIVISION VI POWERS OF APPOINTMENT

DIVISION VI POWERS OF APPOINTMENT Scope of Division VI. Division VI addresses powers of appointment. Historical development. In the history of English law, powers of appointment were primarily the outgrowth

DIVISION VI POWERS OF APPOINTMENT Scope of Division VI. Division VI addresses powers of appointment. Historical development. In the history of English law, powers of appointment were primarily the outgrowth

Report of the Estate Planning, Trust and Probate Law Section

Report of the Estate Planning, Trust and Probate Law Section 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 To the Council of Delegates: The Estate Planning,

Report of the Estate Planning, Trust and Probate Law Section 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 To the Council of Delegates: The Estate Planning,

Steve Leimberg's Estate Planning Newsletter - Archive Message #2295

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #2295 Date: 30-Mar-15 From: Steve Leimberg's Estate Planning Newsletter Subject: James M. Kane: Income Tax Planning Using the Delaware

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #2295 Date: 30-Mar-15 From: Steve Leimberg's Estate Planning Newsletter Subject: James M. Kane: Income Tax Planning Using the Delaware

Trust Dispositions of IRAs and Qualified Plans: Structuring See-Through Trusts and Stretch Provisions

Presenting a live 90-minute webinar with interactive Q&A PLEASE PRINT THESE MATERIALS. THE SPEAKER WILL BE REFERENCING THIS DOCUMENT DURING THE PROGRAM Trust Dispositions of IRAs and Qualified Plans: Structuring

Presenting a live 90-minute webinar with interactive Q&A PLEASE PRINT THESE MATERIALS. THE SPEAKER WILL BE REFERENCING THIS DOCUMENT DURING THE PROGRAM Trust Dispositions of IRAs and Qualified Plans: Structuring

DECANTING COMES OF AGE

DECANTING COMES OF AGE Presented to the ABA Tax Section Estate and Gift Taxes Committee May 6, 2011 Washington, D.C. Farhad Aghdami Williams Mullen Center 200 South 10 th Street - Suite 1600 Richmond,

DECANTING COMES OF AGE Presented to the ABA Tax Section Estate and Gift Taxes Committee May 6, 2011 Washington, D.C. Farhad Aghdami Williams Mullen Center 200 South 10 th Street - Suite 1600 Richmond,

TRUST POWERHOLDERS AND THEIR CREDITORS Asset Protection Committee ACTEC Annual Meeting San Antonio TX Les Raatz March 7, 2018.

TRUST POWERHOLDERS AND THEIR CREDITORS Asset Protection Committee ACTEC Annual Meeting San Antonio TX Les Raatz March 7, 2018 v3-13-18 TABLE OF CONTENTS Page A. AUTHORITIVE SOURCES:... 1 B. POWERS OF APPOINTMENT:...

TRUST POWERHOLDERS AND THEIR CREDITORS Asset Protection Committee ACTEC Annual Meeting San Antonio TX Les Raatz March 7, 2018 v3-13-18 TABLE OF CONTENTS Page A. AUTHORITIVE SOURCES:... 1 B. POWERS OF APPOINTMENT:...

MICHIGAN State Decanting Summary M.C.L.A a 1

MICHIGAN State Decanting Summary M.C.L.A. 700.7820a 1 STATUTORY HISTORY Statutory citation M.C.L.A. 700.7820a Effective Date 12/28/12 Amendment Date(s) ABILITY TO DECANT 1. Discretionary distribution authority

MICHIGAN State Decanting Summary M.C.L.A. 700.7820a 1 STATUTORY HISTORY Statutory citation M.C.L.A. 700.7820a Effective Date 12/28/12 Amendment Date(s) ABILITY TO DECANT 1. Discretionary distribution authority

GOOD N PLENTY: WEALTH TRANSFER AND INCOME TAX PLANNING OPPORTUNITIES UNDER THE 2017 TAX ACT

GOOD N PLENTY: WEALTH TRANSFER AND INCOME TAX PLANNING OPPORTUNITIES UNDER THE 2017 TAX ACT 2018 Delaware Trust Conference Todd A. Flubacher Morris, Nichols, Arsht & Tunnell LLP 1201 North Market Street

GOOD N PLENTY: WEALTH TRANSFER AND INCOME TAX PLANNING OPPORTUNITIES UNDER THE 2017 TAX ACT 2018 Delaware Trust Conference Todd A. Flubacher Morris, Nichols, Arsht & Tunnell LLP 1201 North Market Street

STATE BAR OF CALIFORNIA TAXATION SECTION ESTATE AND GIFT TAX COMMITTEE 1. PROPOSAL TO CLARIFY TREASURY REGULATION SECTION 1.