All your Tax Updates online

|

|

|

- Ashley Cook

- 5 years ago

- Views:

Transcription

1 All your Tax Updates online

2 Workbook Live Chat Internal Tax Session CPD Hours Product demos

3 Agenda 1 MYOB Tax Changes Software changes and updates in the 2018 tax release 2Budget Commentary Tax highlights and summary from the 2018 Federal Budget 3 PLS Review Overview of the how, why and when of PLS to date plus what s next 4 ATO Pre-fill A walk through the new ATO Pre-fill features and workflow for I Returns 5Support Matters What s changed with your support options and a look at some common tax calls 6 Dates All the important dates for your reference

4 1MYOB Tax Changes Software changes and updates in the 2018 tax release

5 MYOB Tax Changes Tax Changes affecting Multiple Entity Types Tax Changes for Individual Entities Tax Changes for Partnership Entities Tax Changes for Trust Entities Tax Changes for Company Entities Tax Changes for Superannuation and Self Managed Super Funds Superannuation Changes From 1 July 2017

6 Tax Changes affecting Multiple Entity Types

7 Tax changes affecting multiple entity types Temporary Budget Repair Levy Concludes Foreign Residents Capital Gains Tax Main Residence Exemption and Principle Asset Test Increased Capital Gains Tax Discount for Investors in Affordable Housing Changes to Foreign Resident Capital Gains Withholding Accelerated Depreciation for Small Business Entities further Extended Limiting Plant and Equipment Depreciation Deductions for Residential Assets Vacancy Fee for Foreign Acquisition of Residential Property Capital Gains Tax Changes to the Principle Asset Test International Dealings Schedule Tax Incentives for Early Stage Innovation Companies Tax Incentives for Early Stage Venture Capital Limited Partnerships Junior Minerals Exploration Incentive Country by Country Reporting - Phase 2 Diverted Profits Tax Removal of Residential Rental Property Travel Expenses for Individuals

8 Treasury Laws Amendment (Temporary Budget Repair Levy) Act received Royal Assent 25 June 2014 The application of the Temporary Budget Repair Levy (TBRL) ceased to apply after 30 Jun 2017 The assessment year will therefore no longer include the additional 2% TBRL for incomes exceeding $180,000 Temporary Budget Repair Levy Concludes MYOB Tax has been updated to remove the TBRL component from the associated tax calculations These changes include removal of the: TBRL information for Individuals in the Medicare schedule TBRL information for Trusts where the Trustee was liable under S99A TBRL notes for Companies in the Company Tax Rates TBRL notes for Superannuation Funds and SMSFs in the Superannuation Fund Tax Rates Forms affected - I T C F MS

9 Treasury Laws Amendment (Reducing Pressure on Housing Affordability Measures No 2) Bill Second Reading 19 March 2018 Denies Capital Gains Tax (CGT) Main Residence Exemption for foreign tax residents Measure applies from 9 May 2017 (7:30pm AEST) Foreign Residents Capital Gains Tax Main Residence Exemption and Principle Asset Test Existing properties grandfathered until 30 June 2019 Foreign residents disposing of property after 9 May 2017 must determine CGT liability and comply with CGT withholding rules Foreign resident beneficiaries of Resident Deceased Estates will be entitled to an apportionment of CGT Transitional arrangements apply to previously lodged Foreign Resident returns providing the tax payer reviews their CGT obligations in a reasonable time frame Forms affected - I T

10 Treasury Laws Amendment (Reducing Pressure on Housing Affordability Measures No 2) Bill Second Reading 19 March 2018 Provides an additional 10% Capital Gains Tax (CGT) discount to resident individuals investing in qualifying affordable housing Increases CGT discount rate up to 60% from 50% Increased Capital Gains Tax Discount for Investors in Affordable Housing Also applies to affordable housing investments by a Managed Investment Trust (MIT) with discount distributed to resident individuals Qualifying affordable housing must be: Provided at below market rent Made available to eligible tenants on low to moderate household incomes Managed through a registered community housing provider For a minimum investment period of three years If this bill is passed MYOB Tax will be amended to include a new Affordable housing days field in the Capital Gains Item worksheet Forms affected - I T (g)

11 Treasury Laws Amendment (Foreign Resident Capital Gains Withholding Payments) Act received Royal Assent 22 June 2017 Implements measures announced in the 2017 Federal Budget to extend Foreign Resident Capital Gains Withholding (FRCGW) obligations on asset disposals Reduces the threshold for real property interests down to $750,000 (from $2m) Increases the withholding rate up to 12.5% (increase from 10%) Changes to Foreign Resident Capital Gains Withholding Applies to contracts entered into on or after 1 July 2017 Changes to existing withholding obligations regime on asset disposals mainly affecting land, buildings, residential and commercial property sales Withholding can be avoided for Australian Resident Vendors as follows: Real Property - ATO Clearance Certificate (by settlement date) Other Asset Types - Vendor Declaration Likewise Foreign Resident Vendors may apply for a rate variation or make an Australian real property asset declaration No changes to MYOB Tax for information only

12 Treasury Laws Amendment (Accelerated Depreciation for Small Business Entities) Act received Royal Assent 22 June 2017 Extension of the Small Business Entity (SBE) instant asset write-off regime up to 30 June 2018 for assets less than $20,000 Accelerated Depreciation for Small Business Entities further Extended SBE Eligibility Criteria - covers over 98% of Australian Businesses Annual turnover less than $10m Turnover is aggregated Note these SBE measures: Mandates that all SBE assets be handled under the Simplified Depreciation Rules Provides for instant write-off of Small Business Pool balances less than $20,000 Limits assets subject to accelerated depreciation are less than $20,000 Additional details in the Budget Commentary No changes to MYOB Tax - Depreciation Worksheet calculations remain unchanged No changes to MYOB Tax for information only

13 Treasury Laws Amendment (Housing Tax Integrity) Act received Royal Assent 30 November 2017 Depreciation deductions on previously used plant and equipment for residential rental properties are now no longer claimable Limiting Plant and Equipment Depreciation Deductions for Residential Assets Applies to assets acquired at or after 9 May 2017 (7:30pm AEST) Effectively stops depreciation double dipping resulting from property purchase asset revaluation activities Depreciation treatment for purchases of additional new plant and equipment assets remains unchanged The measures specifically targets Rental Property ownership by Individual tax payers or Personal Structures. For example, SMSF or Trust Excludes Individuals (and Personal Structures) genuinely carrying on a rental property business Transfers of new and renovated property are excluded if no depreciation has been previously claimed. For example, developer sales Forms affected - I P T MS (ren) (d)

(d)")

14 Limiting Plant and Equipment Depreciation Deductions for Residential Assets Reminder text box added to Rental Property Schedule Information text and new Y/N field (to nominate deduction status) added to Depreciation Worksheet New non-deductible depreciation summary line Forms affected - I P T MS (ren) (d)

15 Treasury Laws Amendment (Housing Tax Integrity) Act received Royal Assent 30 November 2017 Individual Travel Expenses for any residential rental property purposes are no longer claimable Removal of Residential Rental Property Travel Expenses for Individuals Travel expenses can still be claimed: If carrying a business of property investment For commercial investment properties By excluded entities (for example, company, super fund, public unit trust) ATO commentary: Owning several properties is not generally considered a rental property business The receipt of rental payments does not constitute a rental property business Travel expenses are still excluded from the capital gains calculation cost base There are no changes to MYOB Tax because rental travel deductions are claimable in some situations No changes to MYOB Tax for information only

16 Foreign Acquisitions and Takeovers Fees Imposition Amendment (Vacancy Fees) Act received Royal Assent 30 November 2017 Vacancy Fee for Foreign Acquisitions of Residential Property Applies to foreign owners of unoccupied residential property or residential property not genuinely available for rent Genuine availability is determined by rental market access for at least 183 days in a vacancy year on at least 30 day terms Each vacancy year starts with the owners occupancy day anniversary (for example, settlement) Vacancy fees are $5,500 up to $1m with specific calculated values above that Applies to Foreign Investment Review Board (FIRB) applications after 9 May 2017 (7:30pm AEST) Ownership is widely defined to cover Companies, Partnerships and Trusts with substantial foreign interests. For example, > 20% foreign ownership Foreign owners are required to report annually to the Commissioner of Taxation Mandatory reporting based on individual residential property Must be submitted within 30 days of the end of the vacancy year The ATO will advise any applicable (Ghost Tax) vacancy fees No changes to MYOB Tax for information only

17 Treasury Laws Amendment (Reducing Pressure on Housing Affordability Measures No 2) Bill Second Reading 19 March 2018 Provides for the application of the Principal Assets Test on an associate inclusive basis from 9 May 2017 (7:30pm AEST) Capital Gains Tax Changes to the Principal Asset Test Ensures that Foreign Tax Residents cannot avoid Capital Gains Tax (CGT) by separation of indirect interests in Australian real property Each individual related business interest will be separately assessed as to whether the assets are principally Taxable Australian Real Property (TARP) The separate associated interests will then be aggregated to satisfy the 10% total participation interest test for CGT ATO Administrative Treatment Returns may continue to be lodged until the proposal is passed into law Tax payers need to review their tax position once passed and lodge amendments as appropriate in a reasonable time frame No tax shortfall penalties will be applied and any interest accrued will be remitted No changes to MYOB Tax for information only

18 Tax Laws Amendment (Combating Multinational Tax Avoidance) Act received Royal Assent 11 December 2015 Diverted Profits Tax Act received Royal Assent 4 April 2017 Hybrid Mismatch Legislation - currently at Exposure Draft 7 March 2018 The Government has addressed concern regarding multinationals shifting profits out of Australia using associated foreign entities International Dealings Schedule This business strategy is being addressed with Diverted Profits Tax (DPT) and Base Erosion Profit Sharing (BEPS) legislation Broad suite of international measures to combat tax avoidance in line with OECD initiatives The International Dealings Schedule (IDS) provides focus on these tax avoidance activities by multinationals The IDS changes are designed to provide global substance and transparency for future compliance risk modelling and analysis The MYOB Tax IDS schedule has several new and altered labels for 2018 Forms affected - P T C (ids)

19 Changes to the International Dealings Schedule (IDS)

20 Tax Laws Amendment (Tax Incentives for Innovation) Act received Royal Assent 5 May 2016 Treasury Laws Amendment (2017 Measures No 1) Act received Royal Assent 4 April 2017 Provides concessional tax treatment for newly issued shares in qualifying Early Stage Innovation Companies (ESIC) with high growth potential by Angel Investors Tax Incentives for Early Stage Innovation Companies Eligible high-wealth investors qualify as a sophisticated investor otherwise they are a retail (non-sophisticated) investor Forms affected - I T C F MS

21 Investments in Early Stage Innovation Companies (ESIC) may be eligible for a non-refundable tax offset of 20% and modified Capital Gains Tax (CGT) Separate non-refundable tax offset limits and CGT concessions apply to sophisticated and retail investors MYOB Tax 2017 included changes to enable initial claim of the offset Tax Incentives for Early Stage Innovation Companies MYOB Tax 2018 will also: Include carried forward tax offsets and pre-populate where appropriate Apply modified CGT treatment in relation to qualifying shares Pre-fill the tax offset from the ESIC report NOTE ESICs must provide the Commissioner information about their investors within 31 days after the end of the financial year Forms affected - I T C F MS

22 Tax Laws Amendment (Tax Incentives for Innovation) Act received Royal Assent 5 May 2016 Treasury Laws Amendment (2017 Measures No 1) Act received Royal Assent 4 April 2017 Tax Incentives for Early Stage Venture Capital Limited Partnerships Investments by a limited partner in an Early Stage Venture Capital Limited Partnership (ESVCLP) may be eligible for a non-refundable tax offset of 10% and modified Capital Gains Tax (CGT) Measures also increase the ESVCLP fund size from $100m up to $200m and allows a wider range of investment activities Forms affected - I T C F MS

23 Tax Incentives for Early Stage Innovation Companies (ESIC) and Venture Capital Limited Partnerships (ESVCLP)

24 Labels for capturing ESIC and ESVCLP tax offsets Individual Company Fund & SMSF Trusts Partnership Item T8 Label K Item T8 Label M Item T9 Label L Item T9 Label O Item 22 Label L Item 22 Label P Item 23 Label M Item 23 Label R Calculation statement: Item 52 Label H Item 52 Label I Item 55 Label T Item 55 Label K Item 55 Label J Item 55 Label M Label D1 Label D2 Label D3 Label D4 ESVCLP ESVCLP ESIC ESIC ESVCLP ESVCLP ESIC ESIC ESVCLP ESVCLP (Reassigned from 2017 ESIC use) ESIC ESIC Label D Non-refundable non-carry forward tax offsets (D1 + D2 + D3 + D4) Label T Beneficiary Distribution statement worksheet Label J Beneficiary Distribution statement worksheet Item 51 Partners Distribution statement worksheet ESVCLP (Reassigned from 2017 Total Offset use) ESIC ESVCLP (Reassigned from 2017 Total Offset use) ESVCLP ESIC ESIC ESVCLP (Reassigned from 2017 Total Offset use) ESIC New quick access links to ESIC & ESVCLP worksheets Two new fields to manage distribution to Partners

25 Treasury Laws Amendment (Junior Minerals Exploration Incentive) Bill received Royal Assent 4 April 2017 The Junior Minerals Exploration Incentive (JMEI) provides a tax incentive for investment in small mineral exploration companies JMEI replaces the Exploration Development Incentive that ceased on 30 June 2017 The Government has set an annual exploration credit cap over the next four years totaling $100m and allocation is on a first-come first-served basis Junior Minerals Exploration Incentive Eligible exploration companies can issue a tax credit portion to investors from their own tax losses associated with greenfield mineral exploration Tax credits can only be issued against new shares in that income year These issued credits reduce the companies carried-forward losses Companies are liable for excess exploration credit tax and shortfall interest Australian Resident shareholders will be entitled to a refundable tax offset Note: Companies will receive franking credits and distribute these to shareholders NOTE Exploration companies have to seek JMEI approval by electronic application to the ATO and there are associated reporting requirements Forms affected - I P T C F MS

26 Tax Laws Amendment (Combating Multinational Tax Avoidance) Act received Royal Assent 11 December 2015 Country-by-Country (CbC) Reporting is part of the broad suite of measures to combat international tax avoidance by more comprehensive exchanges of information between countries These measures also provide revised standards for transfer pricing documentation Country by Country Reporting Phase 2 CbC reporting implements Action 13 of the OECD/G20 Base Erosion and Profit Shifting (BEPS) Action Plan Applies to Significant Global Entities (SGE) and consolidated groups with annual incomes of A$1 Billion or more Essentially requires higher levels of disclosure encompassing CbC report, master file and local file being lodged within 12 months of the end of their income year Australian entities falling under the CbC reporting regime generally require local file lodging requirement as part of a consolidated group NOTE MYOB Tax provides for relevant data capture in the International Dealings Schedule (IDS) but does not currently cover the preparation or lodgment of the CbC Report and associated files Forms affected - I P T C F MS

27 Treasury Laws Amendment (Combating Multinational Tax Avoidance) Act received Royal Assent on 4 April 2017 Measures designed to provide the ATO with extended powers dealing with tax payers transferring profits to related parties offshore using contrived arrangements to avoid Australian Tax Part of the package design to tackle multinational tax avoidance Also addresses the issue of providing timely information for resolution of tax disputes Diverted Profits Tax Diverted Profits Tax (DPT) imposes a penalty rate of 40% The DPT assessment process imposes liability at assessment, requires upfront payment and requires the tax payer to substantiate non-liability Essentially - you are guilty until you prove otherwise!!! DPT only applies to Significant Global Entities (SGE) for income years starting 1 July 2017 or when the tax benefit occurs after this date Australian Income must be > $25m Sufficient Foreign Tax Test and Sufficient Economic Substance Test exemptions apply No changes to MYOB Tax for information only

28 Tax Changes for Individual Entities

29 Tax Changes for Individual Entities Medicare Levy Low-Income Threshold Increase Temporary Budget Repair Levy Fringe Benefit Tax Changes - FBT Rate Sunset Fringe Benefit Tax Changes and Income Tests for Tax Offsets Allocation of PAYG Credits and Payments Received against Overseas Repayment Levies Cost of Managing Tax Affairs - New Reporting Requirements Tax Deductions for Personal Superannuation Contributions Tax Offset for Spouse Contributions - Increase in Income Threshold Transfer Balance Cap Transfer Balance Cap - Defined Benefit Income Stream Taxable Government Grants and Specified Payments Reporting

30 In line with inflation the Medicare Levy Low-Income Thresholds have been increased for the income year The threshold values for are as follows: Increased to: Up from: Singles $21,980 $21,655 Medicare Levy Low-Income Threshold Increase Couples (Family) $37,089 $36,541 Dependent Child $3,406 $3,356 Single Seniors and Pensioners (SAPTO) $34,758 $34,244 Marries Seniors and Pensioners $48,385 $47,670 MYOB Tax has been updated to reflect the new threshold calculation values Forms affected - I (mlv)

31 Tax Laws Amendment (Temporary Budget Repair Levy) Act received Royal Assent on 25 June 2014 Fringe Benefits Tax Amendment (Temporary Budget Repair Levy) Act received Royal Assent on 25 June 2014 Temporary Budget Repair Levy Fringe Benefit Tax Related Changes Fringe Benefit Tax Rate Sunset The application of the Temporary Budget Repair Levy (TBRL) ceased to apply after 30 June 2017 and the assessment year will therefore no longer include the additional 2% TBRL for incomes exceeding $180,000 Under the TBRL regime there was also an additional 2% applied to Fringe Benefits Tax starting on 1 April 2015 up until 31 March 2017 MYOB Tax has been updated to reverse the FBT increase and restore the rate to 47% for all calculations Forms affected - I

32 Budget Savings (Omnibus) Act 2016 : Schedule 15 Fringe Benefits - received Royal Assent on 16 September 2016 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent on 29 November 2016 From 1 July 2017 removes the Reportable Fringe Benefits Amounts (RFBA) adjustment (49%) from the calculation of Adjusted Taxable Income (ATI) Fringe Benefit Tax Changes and Income Tests for Tax Offsets ATI is used in the calculation of many entitlements including: Net Medical Expenses Tax Offset (NMETO) Dependent (Invalid and Invalid Carer) Tax Offset (DICTO) Low-Income Superannuation Tax Offset (LISTO) Dependent Child for Medicare Levy purposes Also removes RFBA adjustment from the calculation of Rebate Income used to determine eligibility for Seniors and Pensioners Tax Offsets There is no change to RFBA treatment for benefits received from employers who are exempt from Fringe Benefits Tax (FBT) under Section 57A of the FBT Assessment Act For example, hospitals Forms affected - I

33 Education Legislation Amendment (Overseas Debt Recovery) Act 2015 and the Student Loans (Overseas Debtors Repayment Levy) Act received Royal Assent on 26 November 2015 These Acts provided for the recovery of Higher Education Loan Program (HELP) and Trade Support Loans (TSL) repayments from debtors residing overseas Allocation of PAYG Credits and Payments Received against Overseas Repayment Levies Essentially these Acts imposed the same repayment obligations on Australians living overseas as applied to those living locally Overseas debtors are required to register contact details with the ATO Section 8AAZLD of the Tax Administration Act 1953 stipulates that Pay As You Go Withholding (PAYGW) credits are applied against income contingent loans amounts before being applied against other non-running Balance Account (RBA) amounts (which includes income tax) Accordingly the ATO will apply payments from overseas debtors against any HELP or TSL loan repayment commitments before payment of any other tax obligations No changes to MYOB Tax for information only

V - Category 3 income Forms")

34 Cost of Managing Tax Affairs Individuals claim the Cost of Managing Tax Affairs at label D10 Label D10 records a range of claimable amounts To provide a more accurate breakdown the ATO have split label D10 into three sub-components N - Interest charged by the ATO L - Litigation costs M - Other expenses incurred in managing your tax affairs Other Income As a corresponding change the ATO have also revised the Other income item 24 by splitting the Category 1 income label Y - Category 1 income X - Category 2 income (ATO interest) V - Category 3 income Forms affected - I

35 Treasury Laws Amendment (Fair and Sustainable Superannuation) Bill received Royal Assent 29 November 2016 Tax Deductions for Personal Superannuation Contributions Removes the 10% salary and wages income rule for an Income Tax Deduction for Personal Superannuation Contributions to eligible funds Effective from 1 July 2017 and applies to most Australians under 75 Tax payers aged 65 to 74 will need to meet the Work Test Contributions are included in the individual s Concessional Contributions Cap (CC) Note: the Concessional Cap has been reduced to $25,000 from 1 July 2017 Contributions are subject to 15% contributions tax Individuals are still required to lodge a Notice of Intention (NOI) to claim the deduction with their fund before lodging their tax return Can only claim a deduction for the amount on the NOI Contributions by members to certain schemes and funds are not eligible For example, a Constitutionally Protected Fund (CPF) MYOB Tax has been updated to remove the 10% Salary and Wages Income Rule confirmation field on the Personal superannuation contributions worksheet Forms affected - I (psc)

36 Treasury Laws Amendment (Fair and Sustainable Superannuation) Bill received Royal Assent 29 November 2016 Tax Offset for Spouse Contributions Increase in Income Threshold Increases the Income Threshold for Spousal Contributions up to $37,000 Effective from 1 July 2017 (Increase from previous $10,800 threshold) Applies to super contributions for any married or de facto spouse Provides for an 18% tax offset of up to $540 (Maximum $3,000 Contribution) Tax payers aged 65 to 74 will need to meet the Work Test Contributions are included in the individual s Concessional Contributions Cap (CC) Note: the Concessional Cap has been reduced to $25,000 from 1 July 2017 Contributions are subject to 15% contributions tax The offset is not claimable when the spouse receiving the contribution: Exceeded their Non-concessional Contributions Cap (NCC) for the relevant financial year Has a Total Superannuation Balance (TSB) that is equal to or exceeds the General Transfer Balance Cap ($1.6m for ) before the start of the financial year The MYOB Tax internal calculation base has been changed for Item T3 Super Contributions on behalf of your spouse and additional information has been added to the Spouse Superannuation Contributions (ssc) schedule regarding eligibility criteria Forms affected - I (ssc)

37 Tax Offset for Spouse Contributions Increase in Income Threshold New conditions regarding eligibility criteria for Item T3 Superannuation contributions on behalf of your spouse Forms affected - I (ssc)

38 Treasury Laws Amendment (Fair and Sustainable Superannuation) Bill received Royal Assent 29 November 2016 Places a cap on the amounts that can be transferred from concessionally taxed accumulation accounts to a tax-free retirement account Transfer Balance Cap Effectivity limits the ability of high wealth retirees to pursue earnings tax exemptions Measure is effective from 1 July 2017 The cap is $1.6m for the financial year The cap will be indexed in $100,000 increments in line with the Consumer Price Index Increment indexation at current CPI would be around 5 years Individuals exceeding the Transfer Balance Cap will generally need to commute the excess amount back to accumulation The ATO will advise and crystallise the excess transfer amount The ATO Default Commutation Notice advises the voluntary commutation date (60 days) and the superannuation funds they will send Commutation Authorities to in the case of non-compliance Excess Transfer Balance Tax will apply on the transfer balance earnings for the period when the cap was exceeded Excess transfer balance earnings are calculated on a notional basis and will compound daily Forms affected - I (pen)

39 If the taxpayer receives a Defined Benefit Income Stream they have to determine the overall value of their Defined Benefit Income Stream This calculation is the lifetime special value of the defined benefit stream The taxpayer needs to calculate whether the Defined Benefit Income Stream fits within the $1.6m Transfer Balance Cap (TBC) and if not subsequent tax treatments will apply from 1 July 2017 Transfer Balance Cap Defined Benefit Income Stream A Defined Benefit Income Stream Cap of $100,000 will apply for This cap will also be subject to the same indexation regime as the general TBC When the Defined Benefit Income Stream exceeds the $100,000 Cap Taxpayers with mixed income streams can commute account based income amounts back into accumulation or withdraw lump sum payments The excess value of the income stream(s) will be treated as taxable income but is subject to further concessional arrangements REF ATO Guidance note for Super - 5 (JS ) ATO Web Site - Transfer Balance Cap (QC 50880) Forms affected - I (pen)

40 Transfer Balance Cap Defined Benefit Income Stream The following tax arrangements apply when the Defined Benefit Income Stream exceeds the $100,000 Cap 50% of the tax-free component plus the tax element above the cap is taxed at marginal rates The tax offset for untaxed defined benefit income is limited to the taxpayer cap The untaxed portion will be applied before the taxed source Tax payers turning 60 will have apportioned caps for that year MYOB Tax has two changes: A new Label M Assessable amount from capped defined benefit income stream at item 7 Australian annuities and superannuation income streams Additional instructions in the Tax offset worksheet at Item T2 Australian superannuation income stream NOTE ATO Guidance note for Super - 5 (JS ) ATO Web Site - Transfer Balance Cap (QC 50880) Forms affected - I (pen)

41 Tax Administration Act Schedule 1 Subdivision 396-B The Tax Administration Act covers the reporting of government grants and payments While this is not new, additional third-party reporting legislation now requires that government entities report on some grants and payments Taxable Government Grants and Specified Payments Reporting This reporting includes grants paid to third party entities with an ABN and payments for the supply of services Transactions for the first reporting period 1 July 2017 to 30 June 2018 must be lodged by 28 August 2018 This data will be available on the ATO Pre-fill Report NOTE The Import from Tax Office Pre-filled Report option in MYOB Tax 2018 has been updated to import these transactions at Item 24 Other Income Label V Category 3 Income Code D Taxable Scholarship/Bursaries etc. Forms affected - I (oly)

42 Tax Changes for Partnership Entities

43 Tax Changes for Partnership Entities No partnership changes for tax 2018

44 Tax Changes for Trust Entities

45 Tax Changes for Trust Entities No trust changes for tax 2018

46 Tax Changes for Company Entities

47 Tax Changes for Company Entities Tax Rate Reduction for Companies who qualify as Base Rate Entities Extension of Tax Rate Reduction for Companies Tax Rate Reductions for Companies - Franking Credits

48 Treasury Laws Amendment (Enterprise Tax Plan) Act received Royal Assent 19 May 2017 Provides for a reduction in the corporate tax rate to 27.5% (down from 30%) for entities with an aggregated turnover of less than: $25m for the income year $50m for the income year Tax Rate Reduction for Companies who qualify as Base Rate Entities Companies self-assess their eligibility for the lower corporate tax rate Company entities eligible for this lower corporate tax rate will be known as a Base Rate Entity (BRE) There is the possible impact of substituted accounting periods The corporate tax rate will be further reduced for BREs as follows: Income year - 27% Income year - 26% Income year - 25% MYOB Tax contains changes to forms, rates, calculations and tests Forms affected - C

49 Treasury Laws Amendment (Enterprise Tax Plan Base Rate Entities) Bill Senate first reading 12 February 2018 This bill has not yet been passed and current expectation is that it will be passed into law sometime in June 2018 Tax Rate Reduction for Companies who qualify as Base Rate Entities The bill will modify the requirements to qualify as a base rate entity Replaces the existing business test with a passive income test Passive income includes items such as interest, royalties, rent, nonportfolio dividends, net capital gains, non-share dividends and income arising from Partnerships or Trusts that is predominately passive Companies with greater than an 80% passive income will not be eligible for the lower corporate tax rates In general the following entities will still be considered to be BREs: Non-profit companies Pooled Development Funds Retirement savings account providers Public trading trusts Forms affected - C

50 Treasury Laws Amendment (Enterprise Tax Plan 2) Bill Senate first reading 12 February 2018 Provides for the extension of corporate tax rate reductions to all corporate entities This bill has not yet been passed and current expectation is that there will be vigorous opposition raised in the Senate Extension of Tax Rate Reduction for Companies If the bill is passed in its current form this would result in the following corporate tax rates being applicable: Income Year Tax Rate Complying Condition % $100m aggregate turnover % under $250m aggregate turnover % under $500m aggregate turnover % under $1,000m aggregate turnover % % % - Forms affected - C

51 The maximum Franking Credit that can be allocated to a Corporate Frankable Distribution will be based on that entity s applicable Corporate Tax Rate for Imputation Purposes (CTRFIP) Simply the company must frank their distributions for the current year on the assumption that their current year income will be the same as the previous year Tax Rate Reduction for Companies Franking Credits So for the income year the Corporate Tax Rate for Imputation Purposes will be: 27.5% - if the company met the Base Rate Entity requirements for the prior income year, or the company is a Base Rate Entity in its first year of business This may mean that the company has a current corporate tax rate of 30% but a Franking Credit Rate for Imputation Purposes of 27.5% 30% - for all other companies NOTE Practical Compliance Guide PGC 2017/D7 covers the situation whereby distributions have been issued based on an incorrect franking rate - shareholders have to be advised who may then need to file amended returns Forms affected - C

52 Tax Rate reduction for Companies that qualify as Base Rate Entities (BRE)

53 Tax Changes for Superannuation & Self Managed Super Funds

54 Tax Changes for Superannuation & Self Managed Super Funds Strengthening the Integrity of Income Streams Removing the Existing Anti-detriment Provisions Total Superannuation Balance Transfer Balance Cap - Capital Gains Tax Relief

55 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 Treasury Laws Amendment (2017 Measures No 2) Act 2017 Superannuation Reform Package Amending Provisions - received Royal Assent 22 June 2017 Transitions to Retirement Income Streams (TRIS) allow people to who have reached their preservation age to access their superannuation benefits without having to retire or leave their jobs Strengthening the Integrity of Income Streams TRIS was intended to allow older workers to transition to retirement Reduced working hours being supplemented by the superannuation income stream The TRIS payments are generally subject to Exempt Current Pension Income (ECPI) However, TRIS has often been used by the taxpayer to simply continue working and avoid tax The government will remove the TRIS tax advantages and retain the original transitional retirement benefits Forms affected - F MS (xf)

56 As at 1 July 2017 these changes include: Removal of the tax-exempt status of asset income for TRIS accounts not in retirement phase - such income will be taxed at 15%. Removal of tax-free treatment for lump sum superannuation income stream payments. Lump sum payments will not count towards an individual s annual minimum pension payments. All commutations of superannuation income streams will be treated as lump sums. Strengthening the Integrity of Income Streams Superannuation Funds and SMSFs need to ensure that TRIS payments being accessed by the tax payer meet the general TRIS legislative intent Need to clearly identify the change between fund accumulation and retirement phases. Treat costs as deductible where the TRIS is not eligible for transitional purposes. Identify and report to the ATO all TRIS accounts in accumulation phase. MYOB Tax contains several changes as follows: Fund Return (F) - Section B Label Y (instructional changes) SMSF Return (MS) - Section A : Q10 (instructional changes) SMSF Return (MS) - Section B Label Y (instructional changes) SMSF Return (MS) - Sections F & G Member and supplementary member information New field to record the number of TRIS accounts in accumulation phase Forms affected - F MS (xf)

57 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 This measure commenced on 1 July 2017 and the change removes the existing anti-detriment provision to ensure a consistent treatment of lump sum death benefits across all superannuation Anti-detriment provisions provided options for a fund to claim a tax deduction for additional payments to eligible dependents on the death of a member Removing the Existing Anti-detriment Provisions These additional payments could refund the 15% contributions tax paid by the deceased member over their lifetime The Act provides for a two-year transitional period up to 30 July 2019 MYOB Tax contains instructional changes as follows: Fund Return (F) - Section C SMSF Return (MS) - Section G Forms affected - F MS

58 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 The Total Superannuation Balance (TSB) is the fund balance as at 30 June reported each financial year There are multiple superannuation changes dependent on the individual s TSB Total Superannuation Balance From 1 July 2017 the TSB will be used to determine eligibility for: the unused concessional contributions cap carry-forward the non-concessional contributions cap and the two or three-year bring forward period the government co-contribution The tax offset for spouse contributions SMSF (or small APRA funds) to determine use of the segregated assets method to calculate exempt current pension income Forms affected - MS (xf)

Label S3 - Retirement phase account")

59 Total Superannuation Balance There are no changes to MYOB Tax for Fund Returns (F) but the SMSF Return (MS) has additional labels to calculate the TSB correctly SMSF - Section F and G: Member Supplementary member information Label S1 - Accumulation phase account balance Label S2 - Retirement phase account balance (Non-capped defined benefit income) Label S3 - Retirement phase account balance (Capped defined benefit income) Label X1 - Accumulation phase value Lebel X2 - Retirement phase value Analysis labels S1 + S2 + S3 must equal Label S - Closing Account Balance Labels X1 & X2 are optionally completed if the mandatory fields aren t equal to the accumulation and retirement phase values Forms affected - MS (xf)

60 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 The introduction of the Transfer Balance Cap (TBC) effective from 1 July 2017 ($1.6m for ) affects Individual Returns (I) for In complying with Transfer Balance Cap provisions superannuation funds would have been liable to a capital gains event and Capital Gains Tax (CGT) relief was available for one (1) year in some circumstances Transfer Balance Cap Capital Gains Tax Relief Funds utilising the CGT relief were required to notify the Commissioner by lodging a CGT Schedule prior to lodging their tax return Where a fund has so notified the Commissioner, they now need to report that for the deferred notional gain has been realised MYOB Tax has been changed as follows: BW Schedule Item 8 Remove label F Capital gains deferred due to CGT relief Remove label G Capital gain amount deferred CGT Schedule Item 1 Add label S Amount of capital gain previously deferred under transitional CGT relief for superannuation funds Forms affected - F MS (bw) (cgt)

61 Superannuation Changes from 1 July 2017

62 Superannuation Changes from 1 July 2017 Concessional Contributions Cap Non-concessional Contributions Cap Five Year Carry Forward of Concessional Contributions Cap First Home Super Saver Scheme Division 293 Threshold Reduction Streamlining Superannuation Release Authorities Innovative Retirement Income Stream Products

63 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 The annual concessional contributions cap on pre-tax superannuation contributions will be reduced down to $25,000 (from $30,000 or $35,000) for the year The differential age based cap treatment has been removed All Defined Benefit Contributions for members of a Defined Benefit Fund (DBF) will be included in the cap from the year onwards Concessional Contributions Cap Reduction MYOB Tax calculations have been updated to reflect these Concessional Contribution Cap changes Fund managers should note the changed reporting requirements for: Member Contribution Statements (MCS) Transfer Balance Report (TBAR) Member Account Attribution Service (MAAS) New Streamlined Release Authorities cover the release process of amounts from superannuation funds for concessional contributions

64 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 The annual con-concessional contributions cap will be reduced down to $100,000 (from $180,000) for the year Non-concessional contributions for Individuals with a Total Superannuation Balance (TSB) of more that the General Transfer Balance Cap ($1.6m for ) will be in excess Non-Concessional Contributions Cap Reduction Individuals under age 65 can generally bring forward 2 years of nonconcessional contributions ($300,000 over 3 years) The TSB on the day prior to the period will determine the bring forward amount TSB above $1.5m - no bring forward TSB above $1.4m - bring forward limited to $200,000 over 2 years There are no changes to MYOB Tax The new Streamlined Release Authorities also cover the release process of amounts from superannuation funds for non-concessional contributions

65 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 From 1 July 2018 individuals with a Total Superannuation Balance less than $500,000 can make catch-up concessional contributions They can access their unused Concessional Contribution Cap for a period of Five (5) Years Five Year Carry Forward of Concessional Contributions Cap Any unused concessional contribution cap will expire after 5 years The financial year will be the first period in which an Individuals concessional contribution cap can be extended by accessing previously unused concessional contributions There are no changes to MYOB Tax

66 Treasury Laws Amendment (Reducing Pressure on Housing Affordability Measures No 1) Act received Royal Assent 13 December 2017 First Home Super Saver Tax Act received Royal Assent 13 December 2017 The First Home Super Saver Scheme (FHSS) enables taxpayers to save for a first home deposit within their superannuation fund FHSS enables taxpayers to save using the concessional tax superannuation regime Scheme eligibility is taxpayer based - therefore relationship status has no impact First Home Super Saver Scheme From 1 July 2017 a taxpayer can make voluntary contributions into their superannuation fund under the following conditions: Concessional contributions (including salary sacrifice) - taxed at 15% Non-concessional contributions all contributions are subject to existing superannuation contribution caps Contributions can be made to multiple funds Contributions to defined benefit funds or constitutionally protected funds are not eligible for FHSS Note: FHSS is a scheme to access funds and not an account

67 From 1 July 2018 the voluntary contributions together with the associated earnings can be released to assist with the purchase of a first home First Home Super Saver Scheme First Home Super Saver Scheme (FHSS) releases are based on application and are subject to the following: the maximum FHSS release amount outlined in the FHSS determination there is a limit of $15,000 against contributions for any one year (together with earnings) the maximum FHSS withdrawal is $30,000 (together with earnings) First In - First Out processing and non-concessional contributions take precedence a single FHSS release application restriction FHSS releases are subject to ATO withholding and will be taxed at the taxpayers marginal rate (including Medicare) less a 30% tax offset a catch for some taxpayers may be the allocation of FHSS funds against other Commonwealth debt before release an ATO service processing time of up to 12 working days will apply the fund may also apply additional fees or changes a FHSS release does not affect the calculation of concessional or nonconcessional contributions for cap determination purposes for the relevant year unused FHSS release amounts must be repaid and are subject to a 20% FHSS tax There are no changes to MYOB Tax

68 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 From 1 July 2017 the Division 293 income threshold for the year has been reduced to $250,0000 (down from $300,000) High-Income Earners pay tax on their concessional superannuation contributions at 30% above this threshold Division 293 Threshold Reduction The MYOB Tax calculations have been changed to reflect the new threshold value

69 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 The ATO have introduced additional streamlining of Superannuation Release Authorities with electronic forms processing on the portal Essentially these changes move processing to a single combined approach and have a variable implementation impact Streamlining Superannuation Release Authorities Financial year onwards Excess concessional contributions determinations and amended determinations Excess non-concessional contributions determinations and amended determinations Excess non-concessional contributions tax and amended assessments Financial year onwards Division 293 due and payable tax assessments and amended assessments Division 293 deferred debt assessments and amended assessments Financial year onwards First Home Super Saver Scheme There are no changes to MYOB Tax

70 Treasury Laws Amendment (Fair and Sustainable Superannuation) Act received Royal Assent 29 November 2016 Innovative Retirement Income Stream Products Measures designed to stimulate the development of retirement products Covers lifetime product initiatives such as deferred products and group self-annuities Designed to provide retirees with greater choice and flexibility From 1 July 2017 the government has removed the tax barriers and streamlined the process for product providers to deal with government agencies Such products were previously required to make annual payments to the earnings on assets to be tax exempt Treat the reporting of such lifetime products to be the same as other superannuation products Total Superannuation Balance (TSB) Transfer Balance Cap (TBC) Contribution Caps There are no changes to MYOB Tax

71 2Budget Commentary Tax highlights and summary from the 2018 Federal Budget

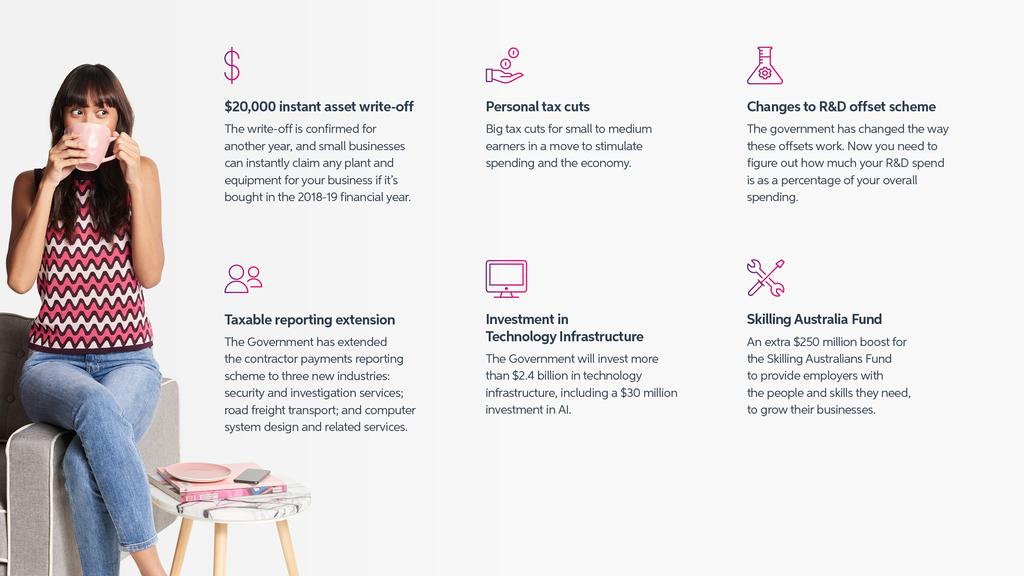

72

73 Commentary Federal Budget 2018 Individuals Business Superannuation Black Economy Measures Post Budget Mutterings and Related Matters

74 Individuals Seven-year Personal Income Tax (PIT) Plan to be implemented in three steps Step 1: Low and Middle-Income Tax Offset to be introduced A Low and Middle-Income Tax Offset (LMITO) will provide a lump sum non-refundable tax offset Assessed by the ATO and processed at tax assessment Will apply to income years from to for taxable incomes up to $125,333 Taxable Income LMITO < $37,000 $200 $37,000 - $47,999 $200 plus 3c per $ above $37,000 $48,000 - $90,000 $530 $90,001 - $125,333 $530 less 1.5c per $ above $90,000 The LMITO will be in addition to the existing Low-Income Tax Offset (LITO)

75 Step 2: Bracket creep relief for middle-income tax payers From 1 July 2018 the 32.5% tax bracket threshold will increase to $90,000 (up from $87,000) From 1 July 2022 the Low-Income Tax Offset (LITO) will increase to $645 (up from $445) LITO will be changed for incomes up to $66,667 Taxable Income LITO < $37,000 $645 $37,001 - $41,000 $645 less 6.5c per $ above $37,000 $41,001 - $66,667 $385 less 1.5c per $ above $41,000 the 19% tax bracket threshold will increase to $41,000 (up from $37,000) the 32.5% tax bracket threshold will be further increased to $120,000 (up from $90,000)

76 Step 3: 37% personal income tax bracket removal From 1 July 2024 the 37% tax bracket will be removed the 32.5% tax bracket threshold will increase to $200,000 (up from $120,000) Essentially this leaves four (4) tax brackets as illustrated in the following table: Tax Rate Threshold Threshold Nil < $18,200 < $18,200 19% $18,201 - $37,000 $18,201 - $41, % $ $87,000 $41,001 - $200,000 37% $87,001 - $180,000 45% > $180,000 > $200,000

77 Medicare Changes Medicare low-income thresholds will be increased from 1 July 2017 Increased to: Up from: Singles $21,980 $21,655 Couples $37,089 $36,541 Dependent Child $3,406 $3,356 Single Seniors and Pensioners (SAPTO) $34,758 $34,244 Married Seniors and Pensioners $48,385 $47,670 The proposed increase in the Medicare levy from 2% to 2.5% of taxable income that was to apply from 1 July 2019 will now not proceed this will also affect other consequential linked tax rate changes such as Fringe Benefits Tax (FBT)

78 Income Tax Exemption for certain Veteran Payments From 1 May 2018 Supplementary amounts paid to veterans and full payments made to a spouse (or partner) of a deceased veteran will be exempt from income tax This includes such payments as pension supplements, rent assistance and remote area allowances Licence schemes of an Individual s Fame or Image This measure is intended to target the licencing of an Individual s fame or image to other related entities such as a Company or Trust - often referred to as the fame tax Income from that arrangement goes to the licence holder and can create opportunities to take advantage of differential tax treatments and avoided tax outcomes From 1 July 2018 all remuneration including non-cash benefits resulting from the commercial exploitation of fame or image will be included as assessable income of that Individual

79 Business Research and Development Tax Incentive Changes The Research and Development (R&D) Tax Incentive calculation will change for income years beginning on or after 1 July 2018 The threshold for claiming accelerated R&D Incentives will increase to $150m (up from $100m) Some R&D changes have a differential application dependent on the company's aggregated annual turnover Companies with an annual aggregated turnover of less than $20m (Smaller R&D claimant) Companies with an annual aggregated turnover of greater than $20m

80 Companies with Annual Aggregated Annual Turnover of less than $20m Current R&D Incentive A 43.5% refundable tax offset is available with a minimum eligible R&D expenditure of $20,000 per annum Proposed R&D Incentive A refundable tax offset of 13.5% above the company's corporate tax rate (CTR) The proposed tax offset rate would remain the same at 43.5% for most entities The newly defined Base Rate Entities (BRE) have a lower CTR and therefore have a tax offset of 41% The maximum refundable tax offset will be capped at $4m per financial year R&D tax offsets above the $4m cap can be carried-forward to future years as non-refundable tax offsets

81 Companies with Annual Aggregated Annual Turnover of more than $20m Current R&D Incentive A 38.5% non-refundable tax offset is available with a minimum eligible R&D expenditure of $20,000 per annum Proposed R&D Incentive Introduction of an entity R&D Intensity Percentage based on the amount of company expenditure spent on R&D Four levels of non-refundable tax offset based on the R&D intensity percentage and the entities corporate tax rate R&D Intensity% BRE offset% Std offset% 0-2% 31.5% 34% 2-5% 34% 36.5% 5-10% 36.5% 39% > 10% 40% 42.5%

82 $20,000 Asset Immediate Write-off Extended The Small Business Entity (SBE) instant write-off regime for assets less than $20,000 will be further extended for another 12 months SBEs will get an immediate deduction for all assets costing less than $20,000 and installed ready for use on or before 30 June 2019 SBE Eligibility Criteria - covers over 98% of Australian Business Annual turnover less than $10m Mandates that all SBE assets be handled under the Simplified Depreciation Rules Includes the instant write-off of Small Business Pool balances less than $20,000 The lock out laws which prevent SBEs from re-entering the pooling rules for five (5) years when they opt out will continue to be suspended until 30 June 2019

83 Division 7A Unpaid Present Entitlements Rule Strengthened Division 7A of the Income Tax Assessment Act 1936 will be amended to clarify the circumstances regarding application to Unpaid Present Entitlements (UPE) This integrity rule covers the UPE resulting in situations when a related private company hasn t yet been paid a trust distribution as a beneficiary but has provided a benefit to its shareholder This measure will ensure the value of the UPE is either: repaid to the private company over time as a complying loan or subject to tax as a dividend Division 7A amendments are part of the reforms announced in the 10-Year Enterprises Tax Plan in the budget The amendments will be deferred to take effect from 1 July 2019 so that all Division 7A amendments progress as a consolidated package

84 Deductions for Vacant Land to be Denied From 1 July 2019 tax deductions will not be claimable for expenses associated with holding vacant land and any such costs cannot be carried forward to later income years These measures will apply to land held for both residential or commercial purposes Denied deductions such as borrowing expenses and council rates may still be used as part of the asset cost base for Capital Gains Tax (CGT) purposes on sale The measure does not apply to land where an occupiable rental property exists or the land is used for business purposes such as primary production This integrity measure will address the issue of deductions being improperly claimed for expenses such as interest costs where the land is not genuinely held for the purpose of earning accessible income

85 Small Business Capital Gains Concession for assignment of Partnership Rights From 8 May 2018 (7:30pm AEST) the Small Business Capital Gains Tax (CGT) Concession will no longer be available to partners that assign their rights to the future income of a partnership The SBE CGT concessions assist owners of small business by providing relief from CGT on the disposal of assets related to the partnership business This integrity measure will clarify use of the Everett Assignment and the associated sale of the partnership assets for SBE CGT concession purposes Everett Assignment High Court decision regarding the assignment of partnership income to the wife Some taxpayers were inappropriately accessing these concessions by assigning their rights to future partnership income to an entity without giving that entity any role in the partnership

86 Non-compliant Payments to Employees and Contractors From 1 July 2019 business will no longer be able to claim deductions for payments to employees when the employer has not meet met their Pay as You Go (PAYG) obligations These PAYG obligations include reporting or remitting PAYG to the ATO These measures also cover the business deduction on payments to contractors subject to withholding A business paying a contractor who did not provide an ABN must make a withholding at the top marginal tax rate When this is not down correctly the entire payment is non-deductible

87 Significant Global Entity Definition The definition of Significant Global Entity (SGE) will be amended to include members of large multinational groups headed by Private Companies, Trusts, Partnerships and Investment entities The current definition encompasses only groups headed by Public Companies and Private Companies required to provide consolidated financial statements This measure applies to income years commencing on or after 1 July 2018 This change will extend the application of the SGE information collection regime and ensure that the Commissioner will be able to monitor Australia s multinational tax integrity rules Multi-national Anti-avoidance Law (MAAL) Diverted Profits Tax (DPT)

88 Tightening of Thin Capitalisation Rules This change will ensure that the value of assets for Thin Capitalisation purposes will be aligned with the value included in the financial statements Essentially this means that asset valuations used to justify debt deductions are robust This measure applies to income years commencing on or after 1 July 2019 with transitional arrangements available for asset valuations made before 8 May 2018 (7:30pm AEST) Foreign controlled consolidated groups who also control a foreign entity will be treated as both outward and inward investment vehicles for Thin Capitalisation purposes This ensures inbound investors cannot access tests that are only intended for outward investors

89 Tax Exempt Entity Loans Tax exempt entities that become taxable after 8 May 2018 will not be able to claim tax deductions arising from the repayment of the principle on a concessional loan Such deductions result from the complex interaction between the rules for Taxation of Financial Arrangements (TOFA) and the rules dealing with Deemed Market Values for Tax Exempt Entities Concessional loans entered into by a tax exempt entity that has become taxable will be valued as if they were originally made on commercial terms This integrity measure is designed to protect the future revenue base

90 Removal of Capital Gains Tax Discount for Managed Investment Trusts and Attribution Managed Investment Trusts Managed Investment Trusts (MIT) and Attribution Management Investment Trusts (AMIT) will not be able to apply the 50% Capital Gains Tax (CGT) discount at the trust level This prevents CGT discounts flowing through to beneficiaries who would not be entitled to the CGT discount in their own right The change ensures that an investors income from MITs and AMITs is taxed correctly as if they had invested directly This measure applies to payments made from 1 July 2019

91 Extension of Anti-avoidance Rules for Circular Trust Distributions The anti-avoidance rule that applies to a Closely Held Trust engaging in circular trust distributions will be extended to cover Family trusts Circular Trust Distributions occur where trusts are beneficiaries of each other in a round robin arrangement The ATO can impose tax on such distributions at a rate equal to the top Individual Tax Rate plus the Medicare Levy This measure will apply from 1 July 2019

92 Testamentary Trusts and Injected Assets The Concessional Tax Rates available to minors receiving income from a Testamentary Trust will be limited to income derived from assets that are transferred from the deceased estate or the proceeds of the sale of those assets Income received by minors from a Testamentary Trust is taxed at normal adult tax rates rather than the higher rates applying to minors An injection of assets unrelated to the deceased estate into the Testamentary Trust could enable an inappropriate benefit from the lower tax rate This measure clarifies the tax rates for minors and applies from 1 July 2019

93 Superannuation Self Managed Superannuation Fund Membership Self Managed Superannuation Funds (SMSF) will be allowed to have up to six (6) members Applies from 1 July 2019 Self Managed Superannuation Fund Audit Cycle Self Managed Superannuation Funds (SMSF) with a history of good record keeping and compliance will have changed annual audit requirements SMSF trustees that have three (3) consecutive years of clear audit reports and timely lodgments will qualify This change applies from 1 July 2019

94 Preventing Inadvertent Concessional Cap Breaches Individuals whose income exceeds $263,157 per annum and who work for multiple employers will be able to nominate that wages from an employer are not subject to the Superannuation Guarantee (SG) This change is intended to ensure that Individuals can avoid unintentionally breaching the $25,000 annual concessional contributions cap due to multiple compulsory SG contributions This measure applies from 1 July 2018

95 Personal Contributions Deductions Integrity Individual Income Tax returns will include a tick box for Individuals with personal superannuation contributions to confirm that they have complied with the requirements to submit a Notice of Intent (NOI) The NOI is required when the taxpayer intends to take a tax deduction for the contributions When no NOI is received by the superannuation fund no tax is paid by the fund but the Individual taxpayer has also taken the deduction against taxable income This measure applies from 1 July 2018

96 Recent Retiree - Personal Superannuation Work Test An exemption from the Work Test for voluntary superannuation contributions will be introduced Currently the work test restricts the ability to make voluntary superannuation contributions for individuals aged and working more than 40 hours in any 30 day period The work test exemption allows retirees flexibility to address their financial affairs in the transition to retirement The change applies to people aged with superannuation balances below $300,000 in the first year the retiree does not meet the work test This measure applies from 1 July 2019

97 Black Economy Measures Illegal Phoenixing and Black Economy Reforms The government will reform the corporations and tax laws to provide regulators with the ability to deter and disrupt illegal phoenix activity Illegal phoenixing involves the deliberate misuse of the corporate form The package includes reforms to: introduce new offences targeting those who conduct or facilitate illegal phoenixing prevent directors improperly backdating resignations to avoid liability or prosecution limiting the ability of directors to resign when this would leave the company with no directors restrict the ability of related creditors to vote on the appointment, removal or replacement of an external administrator extend the director penalty regime to GST, Luxury Car Tax and Wine Equalisation Tax expand the ATO s power to retain refunds where there are outstanding tax obligations

98 Taxable Payments Reporting System Expansion The Taxable Payments Reporting System (TPAR) will be expanded to include the following industries: Security Providers Investigation Services Road Freight Transport Computer Design and related services These changes are in response to the Black Economy Taskforce findings which identified these industries as being at higher risk of non-compliance with tax obligations The ATO will be providing a new online TPAR processing option to streamline manual reporting This measure applies from 1 July 2019 with the first subsequent TPAR due on 28 Aug 2020

99 Large Government Contract Tenders Business seeking to tender for large Australian Government contracts will be required to provide a statement of compliance regarding the status of their tax obligations The proposal will apply to contract tendering over $4m (including GST) This measure applies from 1 July 2019

100 Post Budget Musing, Mutterings and Related Matters Several Members of the House have indicated that they will vigorously oppose various budget matters and this could have a significant impact of the packaged nature of some measures Kelly O Dwyer, the Minister for Revenue and Financial Services, has announced the intention to provide a one-off 12 month amnesty starting 24 May 2018 for historical under-payment of Super Guarantee (SGC) - this is thought to be a pre-cursor to a stricter penalty regime following the introduction of Single Touch Payroll (STP) Significant market commentary surrounding the proposed introduction of a $10,000 economy wide cash payment limit has been widely noted An extension to the pension loans scheme was announced to provide pensioners over the age of 65 with a reverse mortgage of $11,799pa (for an Individual) using the equity in their own home Provides an income stream with a 5.25% interest rate Administered by the Department of Human Services

101 Several changes will be introduced to cap and control various Superannuation Fund fees Charge the ATO with managing the consolidation of Low Balance Superfunds 3% annual cap on passive fees for fund balance below $6,000 Removal on exit fees for all superfund accounts Change the application of integrated Insurance options The removal of Luxury Car Tax on the reimportation of vehicles sent overseas for refurbishment From 1 July 2019 the treatment of GST on online hotel bookings will be treated the same for both domestic and off-shore agencies The Civil Aviation Authority will be granted $3m to manage safety standards for both commercial and recreational drone usage Also of interest was the announcement to provide the International Cricket Council (ICC) a five (5) year tax exemption for the Twenty20 World Cup being held in 2020

102 3PLS Review Overview of the how, why and when of PLS to date plus what s next

103 PLS Review The Practitioner Lodgment Service (PLS) started to replace the ATO's venerable Electronic Lodging System in early 2017 PLS uses high security communication technology to send Standard Business Reporting (SBR) messages over the internet to the ATO's SBR End-point Messages are transported using the Hypertext Transport Protocol Secure (HTTPS) protocol and encrypted using Transport Layer Security (TLS) Essentially this is a more interactive technology environment as compared to ELS and will enable the ATO to further extend and enhance their interactive services This is a mandated change and all standard return lodging for 2018 will now be managed entirely through PLS Furthermore the ATO expect to retire the existing ELS service for all forms from 2017 onwards in December 2018

104 Lodgment Manager Home Page

105 PLS is simple to configure and works in Terminal Server environments May require Windows Firewall reconfiguration Provides a simultaneous lodging solution PLS Service availability and uptime has been variable ATO PLS Lodgment Manager Review Generally the migration to PLS has been very straight-forward PLS provides the benefits of real-time lodging and subsequent portal updates ATO Deeper Validation means that returns are being more rigorously checked Ongoing service development will further extend and enhance the service capabilities

106 Track the status of returns through the PLS workflow Lodgment Manager Completed Ready to Lodge Transmitting Transmitted Lodged Rejected Clean Validation Prepared for Lodgment Being transmitted by the MYOB PLS Service Received by MYOB Lodged Return (Hidden by default) Rejected Return

107 PLS Lodgment Flow TRANSMITTED

108 PLS New features for 2018 PLS Lodgment Batch Management Provides a similar "batching" capability to ELS PLS Pre-fill ATO PLS Pre-fill option for I Returns

109 PLS Lodgment Batch Management Assigns a unique Batch ID during the lodging process New Lodgment Batch Viewer Home Page Date-driven real-time batch information status display Option to print Combined Validation Report

110 Currently under development ATO Client Reports - expected release 2018 Q3 ATO Lodging Statistic Reports - expected release 2018 Q3 ATO EFT Reconciliation Report - expected release 2018 Q3 PLS Planned new features PLS Desktop Activity Statements - expected release 2018 Q4 Future extension Integration of Online PLS Form lodging status to Desktop Electronic Notices of Assessment

111 4ATO Pre-fill A walk through the new ATO Pre-fill features and workflow for I Returns

112 ATO PLS Pre-fill for I Returns The I Return PLS pre-fill productivity feature was introduced in MYOB Tax Pre-fill is built around the ATO SBR online services technology Replaces the previous Tax Agent Portal based approach and provides both extended and enhanced functionality Note: Only I Return pre-fill data is available from the ATO for pre-filling Uses an interactive pre-fill request and download option Can process either for an individual client or for a selected client list Clients must have a Tax File Number (TFN) assigned Downloaded pre-fill reports are stored locally according to practice configuration Integrates with MYOB Document Manager (DM) if installed Simple point and click option to pre-fill downloaded data into tax returns Returns must be rolled over and "Ready to Pre-fill" ATO Pre-fill data cannot be edited but can be deleted at the individual schedule level The ATO requires pre-fill data to be explicitly accepted Each pre-fill item is considered to be a new line entry - not matched to existing data Pre-fill data does not roll-forward - it is designed to be completely refreshed

113 ATO PLS Pre-fill Report

114 ATO PLS Pre-fill Data Salary and wages Private Health Insurance Government payment Employee Share ATO interest Bank interest Dividends Averaging - PP Averaging - Div 405 Managed Fund Higher Education Pension - non super ETP Super income stream Super lump sum

115 Pre-fill Status Description Not Requested No pre-fill download has been requested ATO PLS Pre-fill Status Messages Downloading Download error Received Pre-fill download has been requested There was an error while requesting the pre-fill report Pre-fill Report has been received Pre-filled Tax return has been pre-filled Import error There was an error while importing the pre-fill data

116 ATO PLS Pre-fill for I Returns

117 5Support Matters What s changed with your support options and a look at some common tax calls

118 Practice Backup Strategy Installing updates Not keeping up to date with MYOB Releases Make sure you get the ebulletin Read the Release Notes Turn off Anti-virus during installation Support Matters General Basic system navigation Drop down menus Home page features - Field Chooser, Re-order, Re-size, Sorting, Grouping Practice Security - Tax Return Security Failed Migrations Migrations are a relatively straight forward project But they do require a degree of technical expertise There may also be wider implications such as PLS reconfiguration MYOB have remote and online services available to assist Interactive Voice Response (IVR) changes MYOB has a program of constant service improvement The IVR and associated queues will change with service requirements

119 How to restart the SBR Sender Service MYOB Tax SBR Server Sender - runs on the server Controlled through Windows Services Manager Recommended: Set up a Desktop Shortcut KB Support Matters The Top 3 Knowledge Base Articles PLS lodging - Troubleshooting returns stuck as Transmitting or Transmitted Knowledge Base article will assist with checking these returns In some cases correction will require MYOB Support assistance KB Machine Name not unique This occurs in situation where the system has detected a workstation conflict There can be various reasons for this situation Terminal Server environments generally require specific launch configuration KB 27473

120 The Information Experience Team have been working through a major project to review, reformat and consolidate the Online Help and Knowledge Base articles All articles are being reviewed Anything no longer relevant for current usage has been deleted Any duplication is being removed Information has been extensively checked for accuracy The articles have been reformatted for consistency Help and Knowledge Base Updates The project goal is the consolidation of the Help and Knowledge Base articles into a single self-service platform Providing simplified access Consistent searching experience Improved search results Enhanced presentation utilising collapsing menus Support for additional information linking and embedding Tax 2018 will include the new Help environment which will be extended to cover additional product modules over the coming months F1 Help Will continue to provide the consistent HELP experience

121 We have rebuilt the Knowledge Base

122 my.myob is still the access point

123 There is a new search landing page

124 Search the whole knowledge base or limit to a product Click the drop down arrow to select a product Enter your search here

125 Too many results - use the filters!!! Refine searches using the Filter by section to select a product

126 Great looking help KB Article ID and the product the article relates to remains the same Collapsing menu Feedback goes direct to the Information Experience Team

127 FAQs from the Support Team Distributing a Foreign Tax Credit (FTC) from a Trust return Distributing an overall trust loss between trusts (V335 error)

128 Distributing a Foreign Tax Credit from a Trust Return Issue When distributing a Foreign Tax Credit (FTC) via the <F4> distribution function, it does not populate the Foreign Income Tax Offset at Item 23 label Z Impact Overlapping of the FTC $1,000 rule for individuals Solution Modify the estimate generation by switching on the tax tables for the Trust and reverting the answers back when completed Additional details are available in the Knowledge Base article KB 33905

129 1. On the Front Cover answer Yes to the question Is any tax payable by the trustee? 2. Change Select applicable Tax Table to 9 Distributing a Foreign Tax Credit from a Trust Return 3. Navigate to and click in item 23 label Z then press F4 to process the distribution 4. At the Distribution tab, complete the distributions for all beneficiaries 5. Finish by reverting the changes made at Steps 1 & 2 back to the original values

130 Distributing an overall Trust loss between Trusts (V335 error) Issue Trust A has a capital gain together with a income loss and the overall position of Trust A is a gain This gain is now being distributed to Trust B who has a capital loss situation greater than the gain being distributed from Trust A The net result of the distribution will therefore be an overall loss situation for Trust B Impact Trust A has a capital gain together with a income loss and the overall position of Trust A is a gain Validating Trust B will produce a V335 error This is because MYOB Tax immediately offsets the capital gain against the capital loss and the validation check assumes that Trust B has only received a loss from Trust A Solution In Trust B remove the loss from item 8 and instead add the loss amount to the losses schedule

131 1. Go to the Income tab Item 8 and update label R to NIL Distributing an overall Trust loss between Trusts (V335 error) 2. On the Deductions tab at Item 25 enter NIL

5.")

132 3. Create a BP Losses schedule 4. Include the income losses incurred this year at Part A Distributing an overall Trust loss between Trusts (V335 error) 5. Complete the reconciliation at Part F

133 Place Holder Slide

134 Place Holder Slide

135 Place Holder Slide

136 Place Holder Slide

137 Place Holder Slide

138 Place Holder Slide

139 Place Holder Slide

140 6Dates All the important dates for your reference

141 Important Dates MYOB Tax v software release ATO ELS Gateways ATO PLS Lodgments ATO Refund Processing Tax 2018 will be released and available on my.myob for download Friday 22 June 2018 Will continue to accept 2018 Activity Statements only ELS Client Lists and EFT Reconciliation Report will remain available until Will accept 2018 tax forms from Monday 25 June 2018 Taxpayers should start receiving 2018 tax refunds from Tuesday 17 July September 2018

142 Extended support hours for the 2018 tax season Getting Assistance Extended Support Hours Monday to Friday 8:30am pm (AEST) 25 June 2018 to 10 August 2018 Saturdays 10.00am pm (AEST) 30 June July 2018

143 24/7 access to Online Help and Knowledge Base Online community forum for accountants Getting Assistance Online Services End of Financial Year Hub

144 MYOB Tax Tables

145

IT S MORE THAN A WORKBOOK. IT S READY TO GO WHEN YOU ARE.

IT S MORE THAN A WORKBOOK. IT S READY TO GO WHEN YOU ARE. Contents Contents... 2 Overview... 7 Tax changes affecting multiple returns... 10 Conclusion of the temporary budget repair levy (TBRL)... 10 Foreign

IT S MORE THAN A WORKBOOK. IT S READY TO GO WHEN YOU ARE. Contents Contents... 2 Overview... 7 Tax changes affecting multiple returns... 10 Conclusion of the temporary budget repair levy (TBRL)... 10 Foreign

Last night s Federal Budget contained a number of proposals that will impact the financial planning industry.

TapIn Flash For Adviser use only 2016/03 4 May 2016 2016-17 Federal Budget Adviser Briefing Last night s Federal Budget contained a number of proposals that will impact the financial planning industry.

TapIn Flash For Adviser use only 2016/03 4 May 2016 2016-17 Federal Budget Adviser Briefing Last night s Federal Budget contained a number of proposals that will impact the financial planning industry.

2016/17 Budget. 1. Effective Budget Night 7.30pm (AEST) 3 May New lifetime cap for non-concessional superannuation contributions

3 May New lifetime cap for non-concessional superannuation contributions") 2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

2018/19 Federal Budget

1. Personal income tax changes 1.1 Personal income tax plan 2018/19 Federal Budget The Government will introduce a seven-year, three-step, Personal Income Tax Plan, as follows: Step 1: Targeted tax relief

1. Personal income tax changes 1.1 Personal income tax plan 2018/19 Federal Budget The Government will introduce a seven-year, three-step, Personal Income Tax Plan, as follows: Step 1: Targeted tax relief

Superannuation changes

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners and small businesses. On Tuesday 3 May,

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners and small businesses. On Tuesday 3 May,

Guardian Investments - Budget 2016: What you need to know

Guardian Investments - Budget 2016: What you need to know This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support

Guardian Investments - Budget 2016: What you need to know This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support

Superannuation changes

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners small businesses. On Tuesday 3 May,

This year s Federal Budget includes the most significant changes to Australia s superannuation system since 2007, plus tax initiatives to support low income earners small businesses. On Tuesday 3 May,

2018/19 Federal Budget

2018/19 Federal Budget TECHNICAL UPDATE 08 MAY 2018 ADVISER USE ONLY Introduction On 8 May 2018, the Turnbull Government delivered the Federal Budget with a number of announcements impacting financial

2018/19 Federal Budget TECHNICAL UPDATE 08 MAY 2018 ADVISER USE ONLY Introduction On 8 May 2018, the Turnbull Government delivered the Federal Budget with a number of announcements impacting financial

2017 FEDERAL BUDGET SYNOPSIS

2017 FEDERAL BUDGET SYNOPSIS We provide below a brief summary of the changes that have been announced in Tuesday s federal budget together with a more detailed explanation of the various announcements