THE UNIVERSITY OF HONG KONG LIBRARIES. Hong Kong Collection. gift from Mr. Y.C. Wan

|

|

|

- Maximilian Bates

- 5 years ago

- Views:

Transcription

1

2 THE UNIVERSITY OF HONG KONG LIBRARIES Hong Kong Collection gift from Mr. Y.C. Wan

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27 >

28

29 Section 3 Re Part 4 value of places of residence provided; (see item (h) of Note 2 on pages 25-26) payments received from retirement schemes : - Unrecognized occupational retirement scheme: so much of any amount received representing the employer's contributions. - Recognized occupational retirement scheme ("ORSO scheme"): so much of any amount received by reason other than termination of service, death, incapacity or retirement representing the employer's contributions. In case of termination of service, so much of any excess of the amount received over the proportionate benefit as defined in Section 8(4)(b) of the Inland Revenue Ordinance representing the employer's contributions. - Mandatory Provident Fund scheme ("MPF scheme"): so much of any amount received by reason other than termination of service, death, incapacity or retirement representing the employer's voluntary contributions. In case of termination of service, so much of any excess of the amount received over the proportionate benefit as defined in Section 8(4)(b) of the Inland Revenue Ordinance representing the employer's voluntary contributions. Example An employee terminated his service after having worked for the employer for 7 years. A sum of $80,000 representing employer's contributions/voluntary contributions was received by him from the ORSO scheme/mpf scheme. Total employer's contributions/ voluntary contributions were $100,000. r> ^. A, r-^ ti>mr\r\f\f\ 7x 12months Proportionate benefit = $100,000 x months = $70,000 Employee's taxable benefit = sum received - proportionate benefit ^ = $80,000 - $70,000 ^ ^ " " " " = $10,000 - Any payment received pursuant to a judgment given under Section 57(3)(b) of the Occupational Retirement Schemes Ordinance that is attributable to the employer's contributions; such a payment is awarded by the court in respect of the shortfall between the employee's vested benefits and the amount received by him/her upon the winding up of the scheme. (Your employer should be able to confirm whether the scheme is an ORSO scheme.) 23

(i) (c) What is a share option gain?")

30 Section 3 Related Tax Rules Part 4 (b) Types of income to be excluded (need not be reported in the return) payment in lieu of notice; jury fees; severance payment received in accordance with the Employment Ordinance; Long Service Payment computed and received in accordance with the provisions in the Employment Ordinance. 4.1 (2)(i) (c) What is a share option gain? jgj] A share option gain refers to a gain realized by the exercise of, or by the assignment or release of, a right to acquire shares or stock in a corporation, such right being obtained by a director or employee of that or any other corporation by virtue of his office or employment. Full particulars should be supplied on a separate sheet showing : - the number of rights exercised, assigned or released; - the date on which these rights were exercised, assigned or released; - if exercised, the total open market value of the shares or stock at the time of exercise. If assigned or released, the amount or value of consideration received for the assignment or release of the rights; - the amount or value of the consideration given for the shares or stock, or for the grant of the rights, or for both. 4.1 (2)(ii) (d) What are lump sum payments? [M] Lump sum payments are: - sums paid upon retirement or termination of any office or employment or any contract of employment; or - deferred pay or arrears of pay resulting from a salary or wages award. They are chargeable to tax with the exceptions of those items listed in item (b) of Note 2 above under the heading "Types of income to be excluded". 4.1 (3) (e) Relating back of lump sum payment 26j You are entitled, upon application in writing, to have any lump sum payment referred to in item (d) above related back to the period in respect of which the payment was made. If this period exceeds three years, the payment shall be spread evenly over the three years ending on the date on which you were entitled to claim payment of the lump 24

31 Section 3 Related Tax Rules Part 4 sum or on tne last day of employment, whichever is the earlier. Depending on the circumstances, the relating back of lump sum payments may reduce your overall tax liability. 4.1 (3) (f) Claiming full or partial exemption of income IHJ A claim for full or partial exemption of income may be made on the following grounds: - no service was rendered in Hong Kong; services were rendered in Hong Kong during visits not exceeding a total of 60 days during the year; only income from services rendered in Hong Kong should be assessed; or part of the income has been subject to tax in another jurisdiction. f 4.2 (g) Place of residence provided If your employer or an associated corporation provided you with a place of residence, including places where all or part of the rent paid by you has been refunded, the value of such places of residence will have to be included in your assessable income. The term "associated corporation" means a corporation over which the employer has control or if the employer is a corporation, a corporation which has control over the employer, or a corporation which is under the control of the same person as is the employer. Control means the power of a person, either by the means of a holding of shares or by means of powers granted, to conduct the affairs of the corporation in accordance with his wishes. [H (h) Value of places of residence provided It is the rental value or the excess of rental value over the rent, if any, paid by you. The rental value is 10% of the total income from the employer after the appropriate deduction, or, if you elect, the rateable value. If the places of residence are in a hotel, hostel or boarding house, the rental value is 8% (for two rooms) or 4% (for one room) of the total income from the employer after appropriate deductions. Rent paid by you includes: - rent paid to landlord (if you are responsible for the payment of rates and management fees, which are accepted by your employer as part of the cost of providing the accommodation for the purpose of refund of rent, you may also include these as rent paid by you.) 25

Rateable value in general refers to the rateable value included in the valuation list prepared under the Rating Ordinance.")

32 Section 3 Related Tax Rules Part Deductions ~ ren * P a *d to employer or associated corporation in consideration of provision of place of residence (including the case of rent refund.) Rateable value in general refers to the rateable value included in the valuation list prepared under the Rating Ordinance. If a place of residence was not provided for the full year, please adjust the annual rateable value to reflect the value for the period of residence. If the rental value is less than the rent paid by you to the landlord and your employer or associated corporation, the value of place of residence will be regarded as $0. 4.3(1) (i) Outgoings and expenses ^ Deductions are limited to: - outgoings and expenses wholly, exclusively and necessarily incurred in the production of your assessable income. - depreciation allowances in respect of capital expenditure on machinery or plant, the use of which is essential to the production of your assessable income. For disabled employees, claims for depreciation allowance in respect of the costs of special aids and equipment such as wheelchairs and artificial limbs and their repair and maintenance expenses, may be admitted upon production of evidence to substantiate the amount incurred. Subscriptions paid to professional bodies are strictly speaking not allowable expenses. However, if the holding of the professional qualification is a prerequisite of employment, subscription to one of the relevant professional bodies is allowable by concession. 4.3 (2) (j) Expenses of self-education [gij (applicable to the year of assessment 1996/97 and onwards) Expenses paid by you on fees, including tuition and examination fees, in connection with a prescribed course of education to the extent that they have not been reimbursed or are not reimbursable by your employer or any other person are deductible. The maximum amount that can be deducted is $12,000 for the year of assessment 1996/97, $20,000 for the year of assessment 1997/98 and $30,000 for the year of assessment 1998/99 and onwards. A "prescribed course of education" is one undertaken at a specified institution (such as university, college, school, technical institution 26

33 Section 3 Related Tax Rules p ar t 4 and training centre) to gain or maintain qualifications for use in any employment. This could be a current employment or a planned new employment. Examples of qualifying courses undertaken are: - a management course taken by a business executive; - a commercial or computer course taken by a secretary or clerk; - a vocational training course taken by a technician; - a heavy goods vehicle driving course taken by a factory worker wishing to become a driver; - a continuing professional development seminar taken by an accountant or a lawyer. General interest classes, for example, a Tai Chi course, will not qualify as an employment-related course. 4.3 (3) (k) Approved charitable donations If The aggregate of approved charitable donations of not less than $100 paid by you or your spouse to charities which are exempt from tax under Section 88 of the Inland Revenue Ordinance or to the Government for charitable purposes shall be allowed as a deduction. Such deductions shall not exceed in any year of assessment 10% of your income after allowable expenses and depreciation allowances in that year. A list of these charities is published in The Government of the Hong Kong Special Administrative Region Gazette periodically. 4.3 (4) (I) Contributions to recognized retirement schemes f A recognized retirement scheme means: - a Mandatory Provident Fund scheme [MPF scheme] - a recognized occupational retirement scheme [ORSO scheme] The amount of mandatory contributions paid by you as an employee to a MPF scheme after the contribution provisions in the Mandatory Provident Fund Schemes Ordinance have come into operation (i.e. with effect from 1 Dec. 2000) is deductible under Salaries Tax. However, any voluntary contributions made by you are not deductible. The maximum amount that can be deducted is $12,000 for each year of assessment. If you have contributed to an ORSO scheme instead of a MPF scheme, the contributions paid by you to the ORSO scheme after 27

are also deductible under Salaries Tax.")

34 Section 3 Relate Part 4 the contribution provisions in the Mandatory Provident Fund Schemes Ordinance have come into operation (i.e. with effect from 1 Dec. 2000) are also deductible under Salaries Tax. However, the maximum amount deductible for each year of assessment should be the smallest of the following 3 amounts: - the actual amount of contributions you made to the ORSO scheme; - the amount of the mandatory contributions that you would have been required to pay if you had contributed as an employee in a MPF scheme; or - $12, (m) Election for joint assessment J34J A married couple may elect to receive a joint assessment if they would pay less tax under a single assessment basis on their combined incomes and allowances than under two separate assessments based on their respective individual incomes and allowances. Generally speaking, it is advantageous for a married couple to elect joint assessment when the total amount of allowances and concessionary deductions granted to one spouse is in excess of his/her net assessable income. You can visit the Department's web site ( and make use of the Salaries Tax Computation installed therein to easily ascertain whether joint assessment would be to your advantage. Alternatively, you can do the calculations yourself with reference to the allowances and tax rates table at Annex B. Profits Tax Part 5 Profits Tax is charged for each year of assessment on every person carrying on a trade, profession or business in Hong Kong in respect of his/ her assessable profits arising in or derived from Hong Kong. (a) Basis Period The basis period is: - the year ended 31 March of the year printed on the return; or where the annual accounts are made up to any day other than 31 March, the year ended on that day within the year printed on the return; or where the accounts are made up for each lunar year, the relevant lunar year that ended within the year printed on the return; or 28

35 Section 3 Related Tax Rules Part 5 * w here you commenced or ceased to carry on a business or changed its accounting date, the special period prescribed by Sections 18C, 18D or 18E of the Inland Revenue Ordinance. 5 (7) (b) Assessable Profits/Adjusted Losses [40J& 48] Certain adjustments are required to be made to the net profit/loss per accounts to arrive at the assessable profits/adjusted losses for tax purposes. (i) Adjustments to be added to the net profits or deducted from the losses for tax purposes Depreciation claimed in the accounts; Salaries paid to you and/or your spouse and charged in the accounts; Private share of utilities (e.g. proportion of rates, electricity, water) if the business premises are used for both business and residential purposes; Entertainment expenses not related to business; Capital items purchased; Messing/meals for yourself and/or your family; Penalties and fines; Non-business proportion of motor vehicle expenses; Rent paid or charged in the accounts for premises owned by you; Interest in respect of non-business or private expenditure. Where business and private expenditures are mixed, an appropriate proportion of the total interest charged must be adjusted; Expenses or outgoings to the extent to which they are not incurred in production of the assessable profits, e.g. personal or domestic expenses, gratuitous payments and donations. However, donations of not less than $100 in aggregate to charities which are exempt from tax under Section 88 of the Inland Revenue Ordinance, or to the Government for charitable purposes may be deducted, provided that the deduction does not exceed 10% of the assessable profits before set-off of losses. Contributions to recognized retirement scheme in the capacity of employer in excess of the maximum annual deduction of 15% of the total emoluments of the employees for the year. Voluntary contributions made for you or contributions made for your spouse to any Mandatory Provident Fund Scheme (MPF Scheme) which were charged in the accounts. Mandatory contributions to any MPF Scheme for you in excess 29

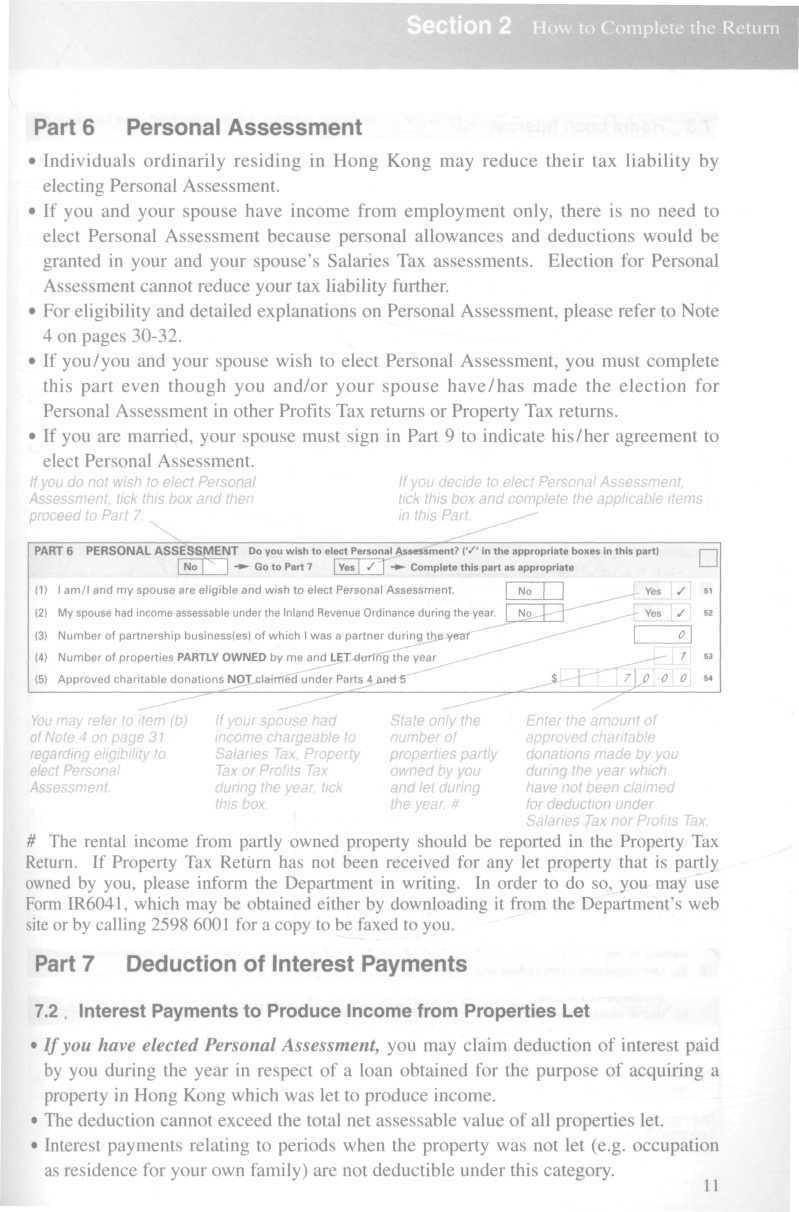

36 30 Section 3 Related X Part 5 of $12,000 for the year. The ceiling of $12,000 is to be reduced by the total of mandatory contributions, if any, to be allowed in Salaries Tax, Personal Assessment and Profits Tax (for any other business of which you are the proprietor or a partner) assessments in respect of yourself. (ii) Adjustments to be deducted from the net profits or added to the losses for tax purposes ; Depreciation allowances and deductions permitted under the Inland Revenue Ordinance; Profits of a capital nature or profits NOT arising in or derived from Hong Kong where these have been credited in the Profit and Loss Account; Dividends from a corporation. (c) Keeping Business Records The Inland Revenue Ordinance requires each person carrying on a trade, profession, or business in Hong Kong to keep sufficient records of his/her income and expenditure and assets and liabilities in relation to that trade, profession or business to enable his/her assessable profits to be readily ascertained. Business records must be retained for at least 7 years after the date of the transaction to which they relate. Failure to keep sufficient records may result in a fine of up to $100,000. (d) Change in business details Any change in the name, nature or business address of a business should be notified to the Business Registration Office within 1 month from the change in compliance with the Business Registration Ordinance. When submitting the tax return, if there have been such changes in business details which have not yet been reported to the Business Registration Office, you may report the details on a separate sheet and attach it to the tax return. It will be accepted as a notification under Section 8 of the Business Registration Ordinance. Note 4 Personal Assessment Part 6 (a) What Personal Assessment is and how it may work to reduce your tax liability The Inland Revenue Ordinance provides for the levying of three

37 SeCtiOn 3 Related Tax Rules Part 6 separate direct taxes for a year of assessment, namely Property Tax, Salaries Tax and Profits Tax. Individuals ordinarily residing in Hong Kong may be able to reduce their tax liability by electing Personal Assessment. ; Under Personal Assessment, income chargeable to Property Tax, Salaries Tax and Profits Tax is aggregated and from this total, the followings may be deducted: - business losses incurred in the year of assessment, - losses brought forward from previous years under Personal Assessment, - approved charitable donations, - interest payments on money borrowed for the purpose of producing property income, and - personal allowances and concessionary deductions. Tax at marginal rates (the same as those used for Salaries Tax) will then be imposed on the balance. Credit will be given for any tax already paid on the income included in the assessment. If the total of the tax already paid exceeds the tax chargeable under Personal Assessment, a refund will be made. 6 (1) (b) Who may elect Personal Assessment fjj An individual may elect Personal Assessment if: - he/she is 18 years of age or over, or under that age if both his/her parents are dead; and - the individual is or, if he/she is married, his/her spouse is a permanent or temporary resident in Hong Kong. For the purpose of Personal Assessment: - "permanent resident" means an individual who ordinarily resides in Hong Kong; - "temporary resident" means an individual who stays in Hong Kong for a period or a number of periods amounting to more than 180 days during the year of assessment in respect of which the election is made or for a period or periods amounting to more than 300 days in 2 consecutive years of assessment one of which is the year of assessment in respect of which the election is made. Where an eligible individual is married and not living apart from his or her spouse and both of them have income assessable under the Inland Revenue Ordinance, that individual may not elect Personal Assessment unless his or her spouse also elects Personal Assessment. 31

38 Section 3 Relate Part 6 (c) Time limit for electing for Personal Assessment If you wish to elect Personal Assessment, you may do so by completing the relevant parts of the tax return. In any case, election for Personal Assessment must be made in writing not later than 2 years after the end of the year of assessment in respect of which the election is made or 1 month after an assessment to tax on income or profits forming part of the individual's total income for such year of assessment becomes final and conclusive under Section 70 of the Inland Revenue Ordinance, whichever is the later. (d) Treatment of a Married Couple under Personal Assessment Unlike Salaries Tax, separate taxation for husband and wife is not applicable under Personal Assessment. A husband and wife are assessed jointly under Personal Assessment. The total income of an individual, as appropriately reduced, will be aggregated with that of his/her spouse to arrive at the joint total income of the couple for assessment purposes. Normally, the tax payable on the joint assessment is apportioned between the husband and the wife in proportion to their respective reduced total income, and each will be issued with a Notice of Assessment. However, where an additional assessment is issued, the whole of the tax payable under this assessment shall be charged on the spouse assessed in respect of that income. Note 5 Part Interest Payments to Produce Income from Properties Let Interest payments made by you during the year on any money borrowed for producing income chargeable to Property Tax shall'be allowed as a deduction under Personal Assessment, with the limitation that the deduction cannot exceed the total net assessable value of all properties let. Interest payments relating to periods of non-letting (e.g. occupation as residence for your own family) are not deductible under this category. 32

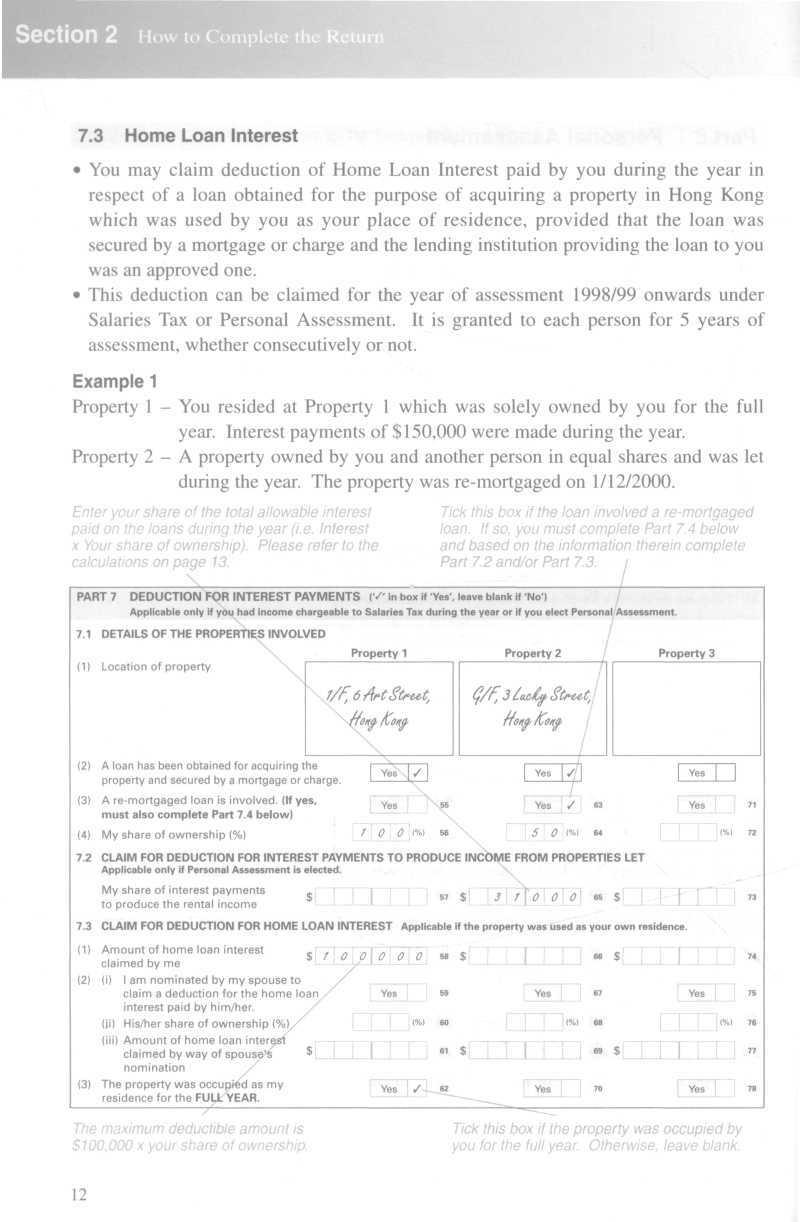

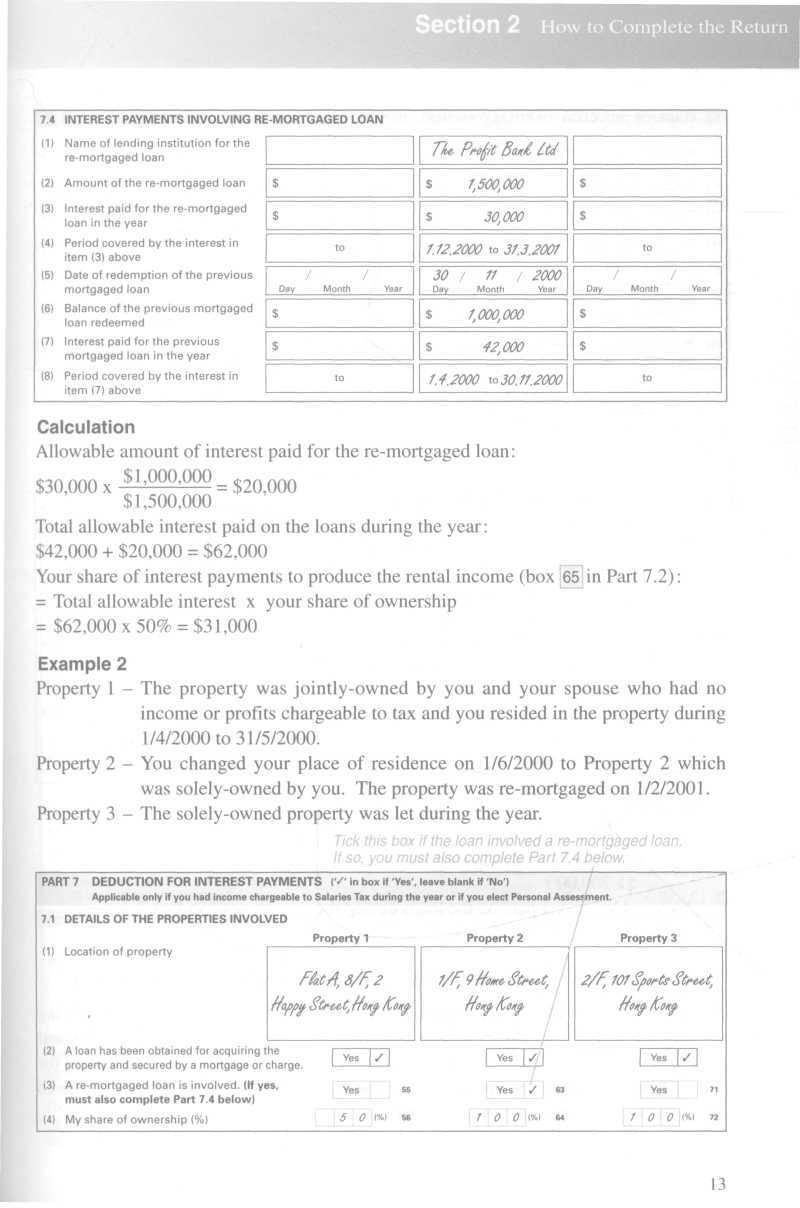

39 Section 3 Related Tax Rules Note 6 Part 7 I 7.3 Home Loan Interest With effect from the year of assessment 1998/99, home loan interest paid is deductible from a person's assessable income under Salaries Tax or from a person's total income under Personal Assessment. A person chargeable to tax at the standard rate is also entitled to the deduction. The deduction is granted to each person for 5 years of assessment, whether continuous or not. Where the deduction is granted to a person, his deductions position is shown in a notification from the Commissioner. (a) Qualifying Conditions All of the following conditions must be satisfied before the deduction can be claimed and granted: - You are the owner of the dwelling (as a sole owner, a joint tenant or tenant in common); The dwelling is a separate rateable unit under the Rating Ordinance, i.e. it is situated in Hong Kong; The dwelling is wholly or partly used by you as your place of residence in the year of assessment; Home loan interest is paid by you during the year of assessment on a loan which was obtained for the acquisition of the dwelling; The loan is secured by a mortgage or charge over the dwelling or over any other property in Hong Kong; and The lender is the Government, a financial institution, a registered credit union, a licensed money lender, the Hong Kong Housing Society, your employer, or any organization or association approved by the Commissioner of Inland Revenue. (b) Amount of Deduction (i) Sole Ownership -.- *"" If you are the sole owner of the dwelling, the amount deductible is the home loan interest actually paid by you in the year of assessment, subject to a maximum deduction of $100,000 for a year of assessment. (ii) Part Ownership If you are a joint tenant or tenant in common of the dwelling, the home loan interest is regarded as having been paid by the joint 33

40 Section 3 Related Part 7 tenants in equal shares, or by the tenants in common each in proportion to their share of ownership in the dwelling. The deductible amount is calculated accordingly. In each case, the maximum deduction of $100,000 is also similarly reduced. (iii) The amount of home loan interest paid would be reduced proportionately in calculating the allowable deduction, if: - the loan was not wholly for acquisition of property, or the property was not wholly used as a place of residence, or the property was not wholly used for the full year as a place of residence. (iv) Re-mortgaged Loan If the property was re-mortgaged to obtain additional funds for non-qualifying purposes, then no deduction is allowable for the interest paid on the additional loan amount. (c) Principal Place of Residence If you own more than one place of residence, you are only entitled to claim the deduction in respect of your principal place of residence. Likewise, where you and your spouse each owns a dwelling separately, only one of you is entitled to claim the deduction in respect of the dwelling which you regard as your principal place of residence. (d) Car Parking Space For any car parking space which is in the same development as the dwelling and used by you, the home loan interest on the car parking space is also deductible provided that home loan interest in respect of the dwelling is also claimed for the same year of assessment. (e) Revocation Where the deduction has been taken into account in ascertaining your tax liability under Salaries Tax or Personal Assessment, any revocation of claim should be made in writing within 6 months after the date of the Commissioner's notification. (f) Deduction for Married Persons Separate taxation As the income of a husband and wife is assessed separately under Salaries Tax, they should claim the deduction separately in the respective tax returns. 34

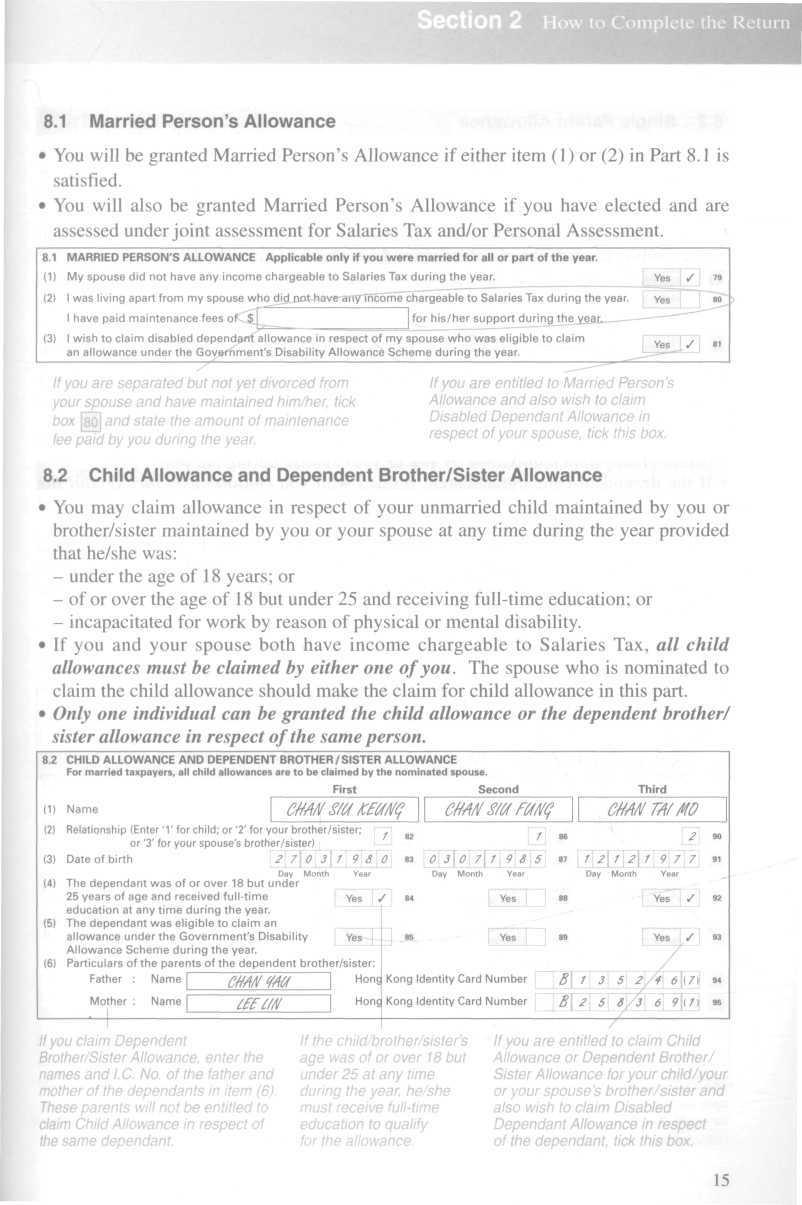

41 Section 3 Related Tax Rules Part 7 R Note 7 i Joint assessment Where both of the husband and wife have assessable income chargeable to Salaries Tax and one of them has income less than the total of allowable home loan interest and basic allowance, the couple may elect joint assessment so that the relevant home loan interest would be deductible from their aggregate assessable income. «Nomination of spouse to claim the deduction Where either a husband or a wife, being the owner of the dwelling, has no income, property or profits chargeable to tax during the year of assessment, he/she may nominate the other spouse to claim the deduction. The owner (and not the other spouse) would be regarded as having been allowed the deduction for a year of assessment. Personal Assessment Under Personal Assessment, the allowable home loan interest paid by a husband or a wife is first deducted from the total income of the relevant spouse. Any part of the deduction not fully utilised would be set off against the other spouse's total income but any excess would not be carried forward to be set off against the relevant spouse's total income for future years. Allowances and Elderly Residential Care Expenses i Part 8 Under Salaries Tax and Personal Assessment, you may claim various allowances if the conditions specified in the law are satisfied. 8.1 (a) Married Person's Allowance ra fjjjjjj (i) If you have income chargeable to Salaries Tax: - You are entitled to the Married Person's Allowance if you were, at any time during the year: - married and not living apart from your spouse and he/she did not have any income chargeable to Salaries Tax; or '' - married but living apart from your spouse who did not have any income chargeable to Salaries Tax and were maintaining or supporting him/her; or - you and your spouse have elected joint assessment, (ii) If you have elected Personal Assessment: - You are entitled to the Married Person's Allowance if you were, at any time during the year: - married and not living apart from your spouse; or - married but living apart from your spouse and were maintaining or supporting him/her. 35

Child Allowance and Dependent Brother/Sister Allowance (i) You may claim allowance in respect of your unmarried child maintained by you or brother/sister maintained by you or your spouse at any")

42 Section 3 R. in i T 8.2 (b) Child Allowance and Dependent Brother/Sister Allowance (i) You may claim allowance in respect of your unmarried child maintained by you or brother/sister maintained by you or your spouse at any time during the year provided that he/she was: - under the age of 18 years; or - of or over the age of 18 but under 25 and receiving full-time education; or - incapacitated for work by reason of physical or mental disability, (ii) "Child" refers to: - your or your spouse's or your former spouse's child; - a child adopted by you/your spouse/your former spouse; - your or your spouse's or your former spouse's step-child, (iii) "Brother or Sister" refers to: - your/your spouse's natural brother/sister; - your/your spouse's adopted brother/sister; - your/your spouse's step brother/sister. (iv) If both you and your spouse have income chargeable to Salaries Tax, all child allowances must be claimed by either one of you. There is no such requirement for the claiming of Dependent Brother/Sister Allowance. (v) You and your spouse may decide who will make the child allowance claim but once made, the nomination is not revocable without the consent of the Commissioner. Nevertheless, the nomination is valid for the year to which the return relates and you and your spouse may make a different nomination in other years. (vi) In general, the overall tax liabilities of a married couple may be minimized if a nomination is made in accordance with the following guidelines: - Situation (1) Only one spouse has income chargeable to Salaries Tax. (2) Both husband and wife have income chargeable to Salaries Tax. (3) Both husband and wife have income chargeable to Salaries Tax, and one of them is assessed at standard rate. Person to claim the Child Allowance The spouse who has income. The one who has higher income. The one whose income is NOT assessed at standard rate. 36

If you/your spouse and other individuals are entitled to claim Child Allowance or Dependent Brother or Sister Allowance in respect of the same person for the same year of assessment, you must")

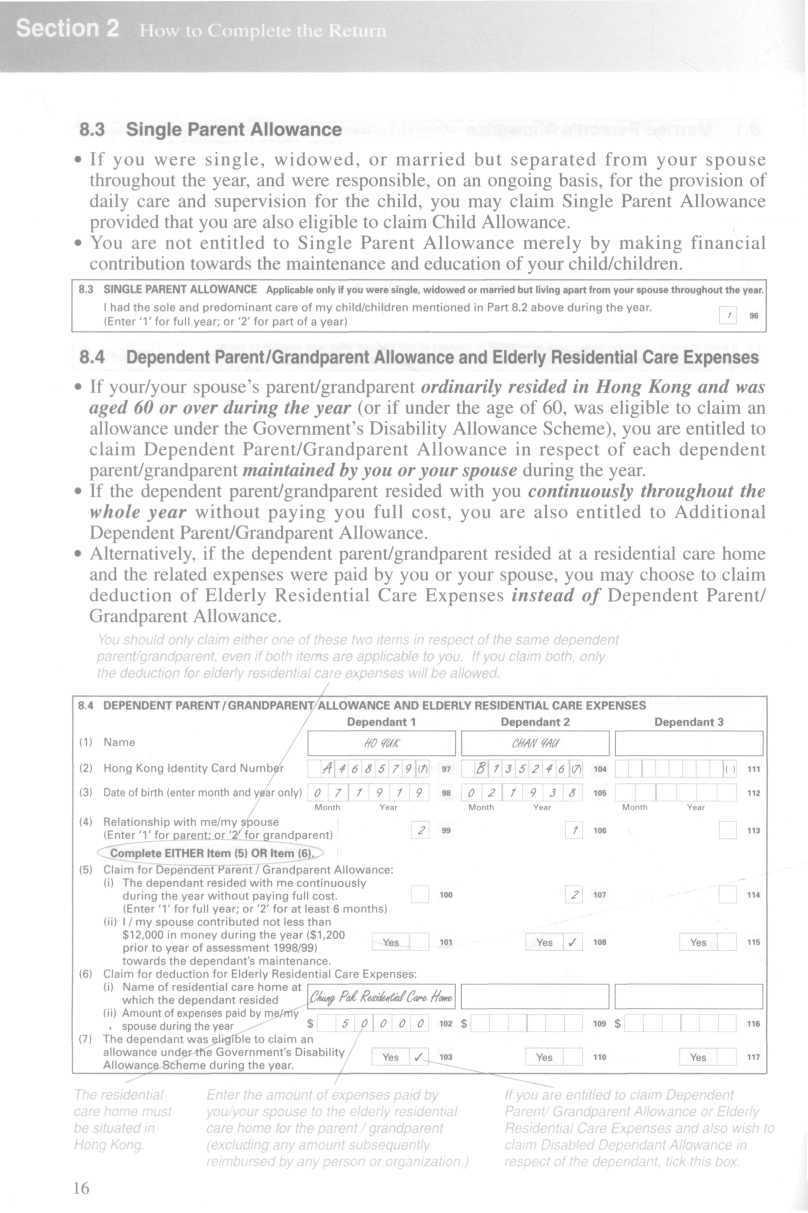

43 JOn 3 Related Tax Rules l ^P f I.,. (vii) If you/your spouse and other individuals are entitled to claim Child Allowance or Dependent Brother or Sister Allowance in respect of the same person for the same year of assessment, you must agree among yourselves which one is to have the allowance. If there is no agreement among yourselves, no allowance will be granted. (viii)disabled Dependant Allowance may be claimed in respect of a dependent child/brother/sister who is eligible to claim an allowance under the Government Disability Allowance Scheme administered by the Social Welfare Department. H 8.3 (c) Single Parent Allowance Hi (i) Single Parent Allowance may be granted where at any time during the year of assessment, you had the sole or predominant care of a child in respect of whom you were entitled to be granted Child Allowance. (ii) No Single Parent Allowance is allowable in respect of any second or subsequent child. (iii) Where more than one person has had the sole or predominant care of the same child at different periods within the year of assessment, the allowance is to be apportioned between the persons who provided the care based upon the respective periods when they provided the sole or predominant care. 8.4 (d) Dependent Parent/Grandparent Allowance and Elderly [97] to 1103 Residential Care Expenses (i) If your/your spouse's parent/grandparent ordinarily resided in Hong Kong and was aged 60 or over during the year (or if under the age of 60, was eligible to claim an allowance under the Government's Disability Allowance Scheme), you are entitled to a Dependent Parent Allowance or a Dependent Grandparent Allowance in respect of each dependent parent or grandparent maintained by you or your spouse, not being a spouse living apart from you, during the year. "Maintain" means that the parent or grandparent has either resided with you, otherwise than for full valuable consideration, for a continuous period of not less than 6 months or has received from you or your spouse not less than $12,000 ($1,200 prior to year of assessment 1998/99) in money towards his/her maintenance. If that parent or grandparent has resided with you otherwise than for full valuable consideration continuously throughout the year, you or your spouse is also entitled to an additional Dependent Parent Allowance or additional Dependent Grandparent Allowance. 37

44 Section 3 Related Tax Rules Part 8 (ii) You may claim a deduction for elderly residential care expenses paid (applicable to year of assessment 1998/99 and onwards) by you or your spouse to a residential care home in respect of your or your spouse's parent or grandparent under Salaries Tax and Personal Assessment. The deduction is allowed for the expenses actually paid to a residential care home in respect of the residential care received, subject to a maximum of $60,000 for a year of assessment for each parent or grandparent. The residential care home must be licensed or exempted from licensing under the Residential Care Homes (Elderly Persons) Ordinance, or is a nursing home registered under the Hospitals, Nursing Homes and Maternity Homes Registration Ordinance, (iii) "Parent" refers to: - Your or your spouse's natural father/mother; or a parent by whom you or your spouse were/was legally adopted; or a step-parent of you or your spouse; or a parent of your deceased spouse, (iv) "Grandparent" refers to: - a natural grandfather/grandmother of you or your spouse; or an adoptive grandparent of you or your spouse; or a step-grandparent of you or your spouse; or a grandparent of your deceased spouse. (v) Multiple Claims of deduction for Elderly Residential Care Expenses and Dependent Parent/Grandparent Allowances Only one individual can be granted the deduction for elderly residential care expenses or the dependent parent/grandparent allowances in respect of the same dependant. If you have claimed both the elderly residential care expenses and dependent parent/grandparent allowance for the same dependant for the same year of assessment, only the elderly residential care expenses will be granted. If you and other individuals are entitled to claim the deduction for elderly residential care expenses or dependent parent/ grandparent allowances in respect of the same dependant for the same year of assessment, you must reach agreement amongst yourselves as to who will make the claim. If no agreement is reached, no deduction or allowance will be granted. 38

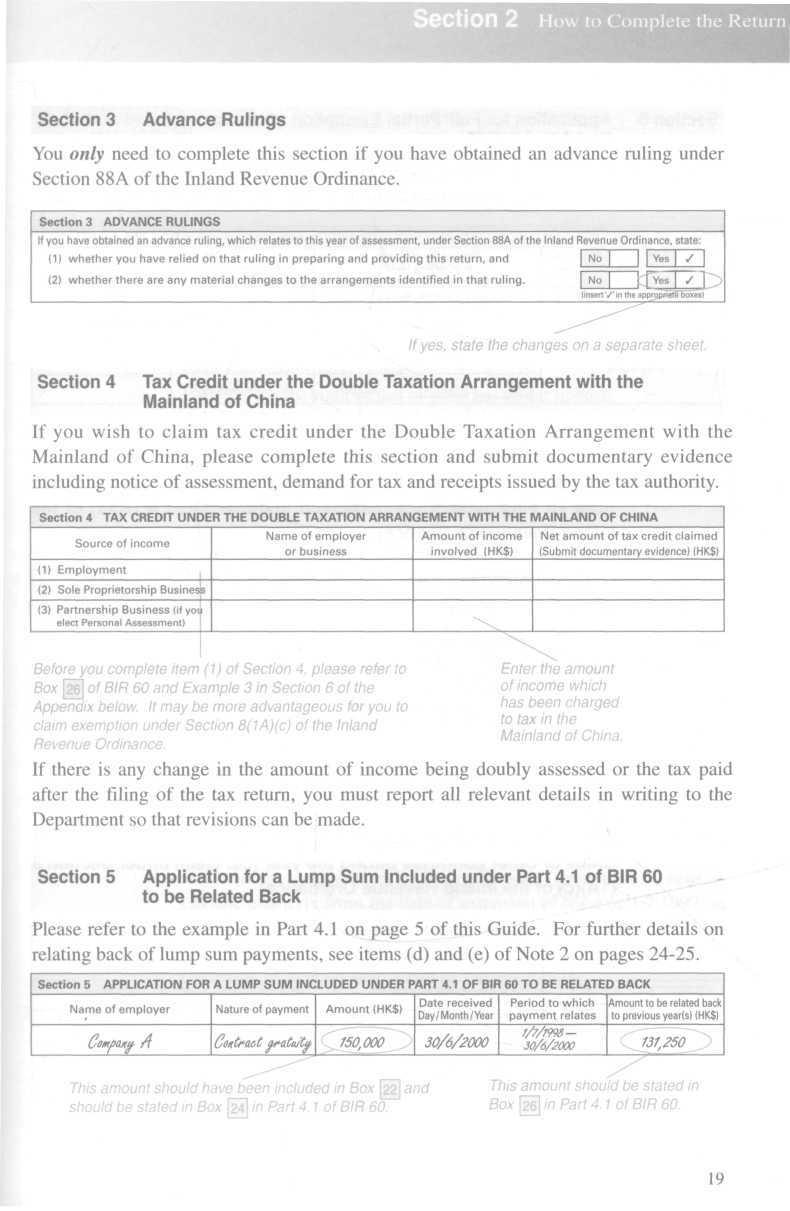

45 Section 3 R Tax Rules Part 8 (e) Disabled Dependant Allowances igj I (i) You are entitled to a Disabled Dependant Allowance in respect of 85 a disabled spouse, each disabled child, brother, sister, parent or [103] grandparent maintained by you or your spouse, not being a spouse living apart from you, during the year. (ii) To qualify for the allowance, the disabled dependant must be eligible to claim an allowance under the Government's Disability Allowance Scheme at any time during the year. The allowance is granted in addition to the following allowances or deduction in respect of the disabled person: - Married Person's Allowance Child Allowance Dependent Brother/Sister Allowance Dependent Parent/Grandparent Allowance Elderly Residential Care Expenses Note 8 Appendix to BIR 60 Section 3 Advance Rulings Under Section 88A of the Inland Revenue Ordinance, the Commissioner may, on an application made by a person in accordance with Part I of Schedule 10 of the Ordinance, make a ruling on the application of any provision of the Ordinance in relation to an arrangement. The applicant is required to pay fees in respect of such application. The minimum amount specified by the Ordinance is $10,000. If you have obtained a ruling and in preparing this return you are required to take into account the way in which a provision of the Ordinance applies to the arrangement identified in the ruling, you must disclose in the tax return: - whether you have relied on the ruling in preparing and providing the return; and - any material changes to the arrangement identified in the ruling. 39

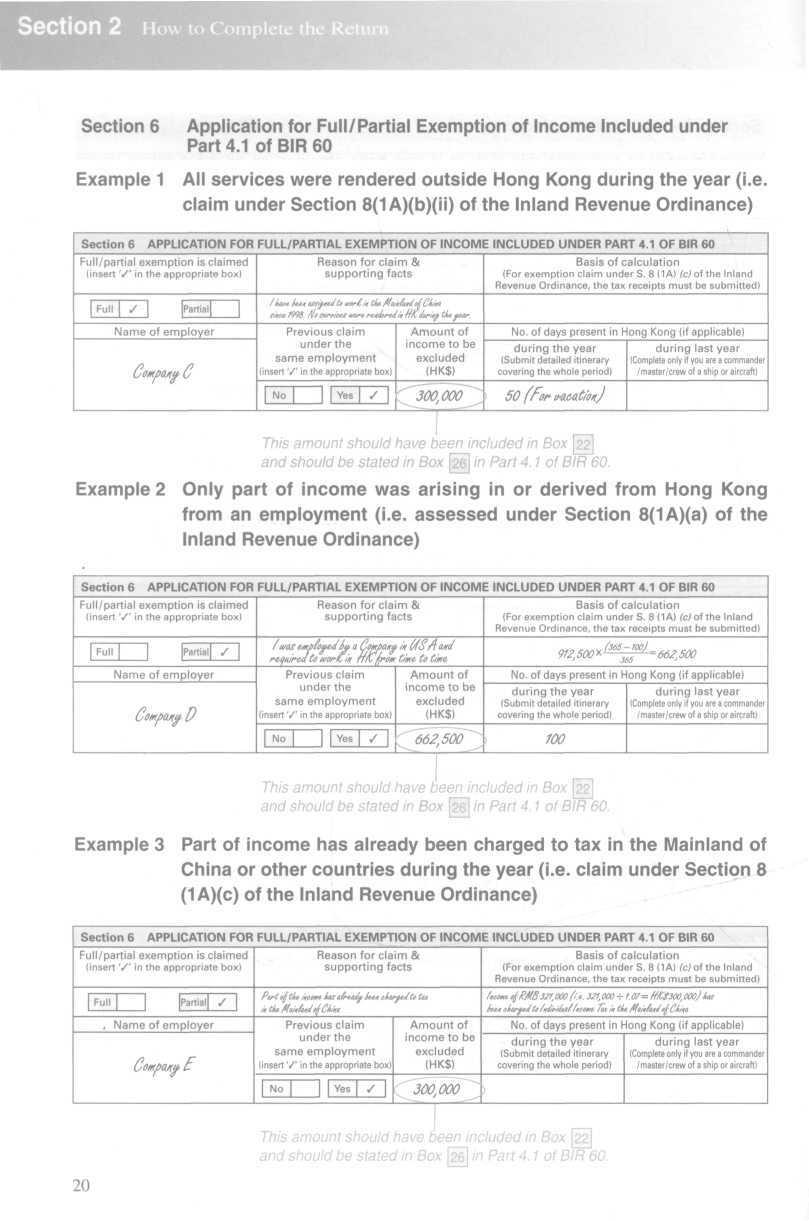

46 Section 3 Related Tax Rule Section 4 Tax Credit under the Double Taxation Arrangement with the Mainland of China On 10 April 1998, the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation On Income entered into force. The Arrangement has effect in respect of income derived from the Mainland on or after 1 July 1998 and to income derived from Hong Kong in any year of assessment commencing on or after 1 April Article 4 of the Arrangement provides that double taxation can be eliminated by the allowance of tax credit. Tax paid in the Mainland by a Hong Kong resident in respect of income subject to tax in Hong Kong can be allowed as a credit under the Arrangement against Hong Kong tax. The claim for tax credits may apply to Salaries Tax, Profits Tax or Tax under Personal Assessment. Section 5 Application for a Lump Sum Included under Part 4.1 of BIR 60 to be Related Back Please refer to item (e) of Note 2 on pages Section 6 Application for Full/Partial Exemption of Income Included under Part 4.1 of BIR 60 Please refer to item (f) of Note 2 on page

47 Tax Rate Table A/JJJ: Allowances and Tax Rate Table 1. Allowances Year of Assessment Basic Allowance 1995/96 $ 72, /97 $ 83, /98 $ 100, /99 onwards $ 108,000 Married Person's Allowance 144, , , ,000 Additional Allowance Single taxpayer Married taxpayer 7,000 14,000 7,000 14, Child Allowance For the l sl child For the 2 nd child For each of the 3 rd to 9 th child 22,000 22,000 11,000 24,500 24,500 12,500 27,000 27,000 14,000 30,000 30,000 15,000 Dependent Brother/Dependent Sister Allowance For each qualified brother/sister 24,500 27,000 30,000 Dependent Parent/Grandparent Allowance For each qualified 22,000 parent / grandparent Additional Dependent Parent/ Grandparent Allowance For each qualified 6,000 parent / grandparent Single Parent Allowance 40,000 Disabled Dependant Allowance For each qualified dependant 11,000 24,500 27,000 30,000 7,000 8,000 30,000 45,000 75, ,000 15,000 25,000 60,000 41

48 Annex B 2. Table Showing Tax on Net Chargeable Income Year of Assessment 1995/96 to 1996/ /98* 1998/99 onwards Net Chargeable Income Rate Tax Net Chargeable Income Rate Tax Net Chargeable Income Rate Tax On the first 20,000 2% ,000 2% ,000 2% 700 On the Next 30,000 50,000 9% 2,700 3,100 30,000 60,000 8% 2,400 3,000 35,000 7% 70,000 2,450 3,150 On the Next 30,000 80,000 17% 5,100 8,200 30,000 90,000 14% 4,200 7,200 35,000 12% 105,000 4,200 7,350 Remainder 20% 20% Net Chargeable Income = Total Income - Deductions - Allowances 17% 3. Standard Rate of Tax Tax charged shall not exceed the standard rate of tax applied to the net total income without Allowances, i.e. total assessable income less total deductions only. The standard rate for 1995/96 onwards is 15%*. The following table shows the amount of Net Total Income at which standard rate applies: 1995/ / /98* 1998/99 onwards Single Married Single Married Single Married Single Married 0 child 472, , , , ,000 1,016,000 1,443,000 2,361,000 1 child 560, , , , ,000 1,124,000 1,698,000 2,616,000 2 Children 648, , ,000 1,072, ,000 1,232,000 1,953,000 2,871,000 3 Children 692,000 1,008, ,000 1,122, ,000 1,288,000 2,080,500 2,998,500 Net Total Income = Total Income - Deductions v * 10% tax rebate applies to the tax charged for the year of assessment 1997/98. 42

49 # i^ How to Compute Your Own Tax Liability (a) The assessable value in Part 3, assessable income in Part 4, and/or assessable profits in Part 5 will form the basis on which the relevant amount of Property Tax, Salaries Tax and/or Profits Tax for the year (e.g. 2000/2001) and the amount of provisional tax for the next year (e.g. 2001/2002) are determined. Any provisional tax previously charged for the year (e.g. 2000/2001) will be set off against your final tax liability for the year (e.g. 2000/2001) and the provisional tax for the next year (e.g. 2001/2002). (b) If, however, you elect Personal Assessment for the year (see Note 4 on pages 30-32), all income accrued to you under Parts 3, 4 and 5 will be aggregated to compute your tax liability. A Personal Assessment Demand Note will be issued to you and if you are liable to Salaries Tax, a Salaries Tax Demand Note for final tax for the year and provisional tax for the next year will also be issued notwithstanding your election for Personal Assessment. (c) Examples (for the year of assessment 2000/2001) (i) Property Tax Total Assessable Value after deductions per Part 3 - ;. Less : Repairs and outgoings (statutory 20%) ^ Net Assessable Value Property Tax payable at the standard rate of 15% (ii) Salaries Tax Income per Part 4 (i.e. box 22 - box 26 + box 29 - box 30 - box 31 - box\&\- box[33]) Less : Deductions and allowances per Part 7 and Part 8 Net Chargeable Income Tax on first $35,000 at 2% Tax on the remaining $19,000 at 7% _ (iii) Profits Tax Assessable Profits per Part 5 Profits Tax payable at the standard rate of 15% $ 10,000 2,000 8,000 1, , ,000 54, ,330 2,030 10,000 1,500 <%&& 43

50 Annex C How to Co (iv) Personal Assessment (using the above examples) Net Assessable Value Income Assessable Profits Total income Less : Deductions and allowances Net Chargeable Income / Tax on first $35,000 at 2% Tax on next $35,000 at 7% Tax on remaining $2,000 at 12% Total tax payable under Personal Assessment 8, ,000 10, , ,000 72, , ,390 [If Personal Assessment is elected, the total tax payable is reduced from $4,730 ($1,200 + $2,030 + $1,500) to $3,390.] V ; Printed by the Printing Department (Printed on paper made from woodpulp derived from renewable forests) 44

51 XlEEDbEDb HKP G946 T2 R00 Guide to tax return - individuals (BIR60) [Hong Kong : Inland Revenue Dept., 2000] Date Due

52

A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT

INFORMATION PAMPHLET A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT 2003-2004 INLAND REVENUE DEPARTMENT THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION Inland Revenue

INFORMATION PAMPHLET A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT 2003-2004 INLAND REVENUE DEPARTMENT THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION Inland Revenue

UNIVERSITY OF HONG KONG LIBRARIES

UNIVERSITY OF HONG KONG LIBRARIES Inland Revenue Department Hong Kong A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT This pamphlet is issued for the general information of persons

UNIVERSITY OF HONG KONG LIBRARIES Inland Revenue Department Hong Kong A BRIEF GUIDE TO TAXES ADMINISTERED BY THE INLAND REVENUE DEPARTMENT This pamphlet is issued for the general information of persons

Accredited Accounting Technician Examination

Accredited Accounting Technician Examination Pilot Examination Paper Paper 5 Principles of Taxation Questions & Answers Booklet The Suggested Answers given in this booklet are purposely made to give more

Accredited Accounting Technician Examination Pilot Examination Paper Paper 5 Principles of Taxation Questions & Answers Booklet The Suggested Answers given in this booklet are purposely made to give more

Paper F6 (HKG) Taxation (Hong Kong) Monday 1 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Monday 1 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Monday 1 December 2008 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (Hong Kong) Monday 1 December 2008 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

THE TAXATION INSTITUTE OF HONG KONG CERTIFIED TAX ADVISER QUALIFYING EXAMINATION PAPER 1 HONG KONG TAX SUGGESTED ANSWERS.

THE TAXATION INSTITUTE OF HONG KONG CERTIFIED TAX ADVISER QUALIFYING EXAMINATION 2010 PAPER 1 HONG KONG TAX SUGGESTED ANSWERS Page 1 of 11 Question 1 Ignore provisional tax (a) ABC Limited Profits Tax

THE TAXATION INSTITUTE OF HONG KONG CERTIFIED TAX ADVISER QUALIFYING EXAMINATION 2010 PAPER 1 HONG KONG TAX SUGGESTED ANSWERS Page 1 of 11 Question 1 Ignore provisional tax (a) ABC Limited Profits Tax

Paper F6 (HKG) Taxation (Hong Kong) Thursday 9 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Thursday 9 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 9 June 2016 Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section A ALL

Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 9 June 2016 Time allowed Reading and planning: 15 minutes Writing: 3 hours This question paper is divided into two sections: Section A ALL

Accounting Technician Examinations. Pilot Examination Paper. Level II. Paper 5 Hong Kong Taxation. Questions Suggested Answers and Marking Scheme

香港專業會計員 會 THE HONG KONG ASSOCIATION OF ACCOUNTING TECHNICIANS (Incorporated with Limited Liability) Unit A, 7/F, Fortis Bank Tower, 77-79 Gloucester Road, Wanchai, Hong Kong. Accounting Technician Examinations

香港專業會計員 會 THE HONG KONG ASSOCIATION OF ACCOUNTING TECHNICIANS (Incorporated with Limited Liability) Unit A, 7/F, Fortis Bank Tower, 77-79 Gloucester Road, Wanchai, Hong Kong. Accounting Technician Examinations

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2010 Suggested Answers

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2010 Suggested Answers

Paper F6 (HKG) Taxation (Hong Kong) Thursday 7 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Thursday 7 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 7 June 2018 F6 HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are

Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 7 June 2018 F6 HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are

Paper F6 (HKG) Taxation (Hong Kong) Thursday 7 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Thursday 7 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Fundamentals Level Skills Module Taxation (Hong Kong) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 2011 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 2011 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 2017 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 2017 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 204 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 204 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

ATX HKG. Advanced Taxation Hong Kong (ATX HKG) Strategic Professional Options. Tuesday 4 December 2018

Strategic Professional Options. Tuesday 4 December 2018") Strategic Professional Options Advanced Taxation Hong Kong (ATX HKG) Tuesday 4 December 2018 ATX HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH

Strategic Professional Options Advanced Taxation Hong Kong (ATX HKG) Tuesday 4 December 2018 ATX HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH

Paper F6 (HKG) Taxation (Hong Kong) Monday 6 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Monday 6 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Monday 6 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Fundamentals Level Skills Module Taxation (Hong Kong) Monday 6 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION JUNE 2011 Time allowed 3 hours

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION JUNE 2011 Time allowed 3 hours

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2011 Suggested Answer

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2011 Suggested Answer

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 200 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 200 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 207 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 207 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 204 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 204 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 20 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 20 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION PILOT PAPER Time allowed 3 hours

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION PILOT PAPER Time allowed 3 hours

HKSAR Budget Summary

www.pkf-hk.com 2018-19 HKSAR Budget Summary 2018-19 HKSAR Budget Summary The Financial Secretary of the Hong Kong SAR Government, the Honourable Mr. Paul Chan Mo-po delivered the 2018-19 Budget Speech

www.pkf-hk.com 2018-19 HKSAR Budget Summary 2018-19 HKSAR Budget Summary The Financial Secretary of the Hong Kong SAR Government, the Honourable Mr. Paul Chan Mo-po delivered the 2018-19 Budget Speech

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION JUNE 2011 Suggested Answers The

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION JUNE 2011 Suggested Answers The

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 206 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 206 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 2012 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) December 2012 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Paper F6 (HKG) Taxation (Hong Kong) Monday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Hong Kong) Monday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Hong Kong) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

Fundamentals Level Skills Module Taxation (Hong Kong) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Rates

SYNOPSIS OF HONG KONG 2010/11 BUDGET

SYNOPSIS OF HONG KONG 2010/11 BUDGET [ Tax & Business Advisory Division ] A. HIGHLIGHT OF FINANCIAL INDICATORS IN HONG KONG Economic outlook is cautiously optimistic. Uncertainties and potential pitfalls

SYNOPSIS OF HONG KONG 2010/11 BUDGET [ Tax & Business Advisory Division ] A. HIGHLIGHT OF FINANCIAL INDICATORS IN HONG KONG Economic outlook is cautiously optimistic. Uncertainties and potential pitfalls

2014 No. XXX SOCIAL CARE, ENGLAND. The Care and Support (Charging and Assessment of Resources) Regulations 2014

Regulations 2014") S T A T U T O R Y I N S T R U M E N T S 2014 No. XXX SOCIAL CARE, ENGLAND The Care and Support (Charging and Assessment of Resources) Regulations 2014 Made - - - - 2014 Laid before Parliament 2014 Coming

S T A T U T O R Y I N S T R U M E N T S 2014 No. XXX SOCIAL CARE, ENGLAND The Care and Support (Charging and Assessment of Resources) Regulations 2014 Made - - - - 2014 Laid before Parliament 2014 Coming

Hong Kong. Investment basics. Currency Hong Kong Dollar (HKD) Foreign exchange control

Foreign exchange control") Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

2017/18 Hong Kong Budget Summary

Hong Kong Budget Summary www.moorestephens.com.hk Hong Kong Budget Summary Highlights Profits Tax A one-off tax reduction of 75% of profits tax for, subject to a ceiling of 20,000 Salaries Tax A one-off

Hong Kong Budget Summary www.moorestephens.com.hk Hong Kong Budget Summary Highlights Profits Tax A one-off tax reduction of 75% of profits tax for, subject to a ceiling of 20,000 Salaries Tax A one-off

Detailed competency map: Knowledge requirements. (AAT examination)

") Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

Detailed competency map: Knowledge requirements (AAT examination) Fields of competency The items listed are shown with an indicator of the minimum acceptable level of competency, based on a three-point

CHAPTER 11 (CORRECTED COPY 2)

") CHAPTER 11 (CORRECTED COPY 2) AN ACT concerning local government charitable fund and spillover fund management, and property tax credits and deductions, supplementing Title 54 of the Revised Statutes,

CHAPTER 11 (CORRECTED COPY 2) AN ACT concerning local government charitable fund and spillover fund management, and property tax credits and deductions, supplementing Title 54 of the Revised Statutes,

United Kingdom. I. Taxes on Corporate Income

OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2011 United Kingdom 1. Corporate income tax I. Taxes on Corporate Income Corporate profits

OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2011 United Kingdom 1. Corporate income tax I. Taxes on Corporate Income Corporate profits

Multiple Choice Questions 100 Marks All questions are compulsory

Sample Questions PTITUE TEST Hong Kong Taxation.. Time llowed 1 hour 45 minutes Multiple hoice Questions 100 Marks ll questions are compulsory o not open this question paper until instructed by the supervisor.

Sample Questions PTITUE TEST Hong Kong Taxation.. Time llowed 1 hour 45 minutes Multiple hoice Questions 100 Marks ll questions are compulsory o not open this question paper until instructed by the supervisor.

TX HKG. Taxation Hong Kong (TX HKG) Applied Skills. Tuesday 4 December The Association of Chartered Certified Accountants TX HKG ACCA

Applied Skills. Tuesday 4 December The Association of Chartered Certified Accountants TX HKG ACCA") Applied Skills Taxation Hong Kong (TX HKG) Tuesday 4 December 2018 TX HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Applied Skills Taxation Hong Kong (TX HKG) Tuesday 4 December 2018 TX HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions are compulsory

Sage in Tanzania 2017

Sage in Tanzania 2017 To withhold tax at the rate of 30% mentioned in paragraph 1 of the first schedule of Income Tax Act 2004 and remit them along with amount deducted from regular employees. Enquire

Sage in Tanzania 2017 To withhold tax at the rate of 30% mentioned in paragraph 1 of the first schedule of Income Tax Act 2004 and remit them along with amount deducted from regular employees. Enquire

Paper P6 (HKG) Advanced Taxation (Hong Kong) Friday 7 December Professional Level Options Module

Advanced Taxation (Hong Kong) Friday 7 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (Hong Kong) Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

Professional Level Options Module Advanced Taxation (Hong Kong) Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A

2018/19 Hong Kong Tax Facts and Figures

www.pwchk.com 2018/19 Hong Kong Tax Facts and Figures 2018/19 Hong Kong Tax Facts and Figures The information in this booklet is based on taxation laws and practices as of 28 February 2018 and incorporates

www.pwchk.com 2018/19 Hong Kong Tax Facts and Figures 2018/19 Hong Kong Tax Facts and Figures The information in this booklet is based on taxation laws and practices as of 28 February 2018 and incorporates

Guide to. Personal Income Tax Return Half Year 2017 (ภ.ง.ด.94) For taxpayers who received income under Section 40(5)-(8) of the Revenue Code

For taxpayers who received income under Section 40(5)-(8) of the Revenue Code") Guide to Personal Income Tax Return Half Year 2017 (ภ.ง.ด.94) For taxpayers who received income under Section 40(5)-(8) of the Revenue Code Bureau of Legal Affairs, Revenue Department, Bangkok Contents

Guide to Personal Income Tax Return Half Year 2017 (ภ.ง.ด.94) For taxpayers who received income under Section 40(5)-(8) of the Revenue Code Bureau of Legal Affairs, Revenue Department, Bangkok Contents

The chargeability of the profits in question depends on whether the share in B Ltd. is a trading stock or a long-term investment.

SECTION A CASE QUESTIONS Answer 1(a) The chargeability of the profits in question depends on whether the share in B Ltd. is a trading stock or a long-term investment. In Simmons v IRC [1980] 1 WLR 1196,

SECTION A CASE QUESTIONS Answer 1(a) The chargeability of the profits in question depends on whether the share in B Ltd. is a trading stock or a long-term investment. In Simmons v IRC [1980] 1 WLR 1196,

Activity to Develop and Demonstrate Competence. Distinguish between different classifications of taxes

Paper 5 Hong Kong Taxation Aim This paper aims at providing students with a general knowledge of the principles of taxation in Hong Kong and developing their ability to interpret and apply the taxing statutes

Paper 5 Hong Kong Taxation Aim This paper aims at providing students with a general knowledge of the principles of taxation in Hong Kong and developing their ability to interpret and apply the taxing statutes

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES. Suggested Answers

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Hong Kong Taxation Diet : December 2006 The suggested answers are published for the purpose of assisting

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES Suggested Answers Level : Professional Subject : Hong Kong Taxation Diet : December 2006 The suggested answers are published for the purpose of assisting

Part 44A TAX TREATMENT OF CIVIL PARTNERSHIPS. 1031D Election for assessment under section 1031C

Part 44A TAX TREATMENT OF CIVIL PARTNERSHIPS CHAPTER 1 Income Tax 1031A Interpretation (Chapter 1) 1031B Assessment as single persons 1031C Assessment of nominated civil partner in respect of income of

Part 44A TAX TREATMENT OF CIVIL PARTNERSHIPS CHAPTER 1 Income Tax 1031A Interpretation (Chapter 1) 1031B Assessment as single persons 1031C Assessment of nominated civil partner in respect of income of

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION JUNE 2012 Suggested Answer The

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION JUNE 2012 Suggested Answer The

Paper P6 (HKG) Advanced Taxation (Hong Kong) Thursday 7 December Professional Level Options Module

Advanced Taxation (Hong Kong) Thursday 7 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (Hong Kong) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Professional Level Options Module Advanced Taxation (Hong Kong) Thursday 7 December 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are

Kenya. Individual Taxation. Abbreviations. References. Latest Information: Author Catherine Mutava

Kenya Individual Taxation Author Catherine Mutava Latest Information: This chapter is based on information available up to 4 October 2017. Please find below the main changes made to this chapter up to

Kenya Individual Taxation Author Catherine Mutava Latest Information: This chapter is based on information available up to 4 October 2017. Please find below the main changes made to this chapter up to

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 203 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 203 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Disposals of business or farm on "retirement"

Disposals of business or farm on "retirement" Part 19-06-03 This document should be read in conjunction with section 598 of the Taxes Consolidation Act 1997 Document updated May 2018 Table of Contents

Disposals of business or farm on "retirement" Part 19-06-03 This document should be read in conjunction with section 598 of the Taxes Consolidation Act 1997 Document updated May 2018 Table of Contents

A Revenue Guide to Rental Income

A Revenue Guide to Rental Income Contents Introduction 2 What types of rental income are there? 2 What expenses can be claimed? 3 What is the position with regard to interest paid on borrowings? 4 What

A Revenue Guide to Rental Income Contents Introduction 2 What types of rental income are there? 2 What expenses can be claimed? 3 What is the position with regard to interest paid on borrowings? 4 What

Frequently Asked Questions and Answers

Frequently Asked Questions and Answers In general, this part is applicable to applicants using Full Version of Application. For applicants using Simplified Version of Application, they may make reference

Frequently Asked Questions and Answers In general, this part is applicable to applicants using Full Version of Application. For applicants using Simplified Version of Application, they may make reference

Paper P6 (HKG) Advanced Taxation (Hong Kong) Thursday 8 June Professional Level Options Module

Advanced Taxation (Hong Kong) Thursday 8 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (Hong Kong) Thursday 8 June 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are compulsory

Professional Level Options Module Advanced Taxation (Hong Kong) Thursday 8 June 2017 Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are compulsory

稅務編號 TIN: 李大富. Please read and follow the Guide Book in completing this return. 李大富余美人 G/F 28 HEE LOK STREET, HK

If you have not registered for etax previously, your Taxpayer Identification Number (TIN) will be printed here. If you wish to open your etax Account, please login at www.gov.hk/etax to apply for the etax

If you have not registered for etax previously, your Taxpayer Identification Number (TIN) will be printed here. If you wish to open your etax Account, please login at www.gov.hk/etax to apply for the etax

WHAT SHOULD I DO ABOUT TAX WHEN SOMEONE DIES (August 2009)

") WHAT SHOULD I DO ABOUT TAX WHEN SOMEONE DIES (August 2009) Contents 1. Introduction 2. Some General Terms and Procedures 3. If you are a Personal Representative 4. If you are a Beneficiary 5. If you are

WHAT SHOULD I DO ABOUT TAX WHEN SOMEONE DIES (August 2009) Contents 1. Introduction 2. Some General Terms and Procedures 3. If you are a Personal Representative 4. If you are a Beneficiary 5. If you are

Paper P6 (HKG) Advanced Taxation (Hong Kong) Thursday 7 June Professional Level Options Module

Advanced Taxation (Hong Kong) Thursday 7 June Professional Level Options Module") Professional Level Options Module Advanced Taxation Thursday 7 June 2018 P6 HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are compulsory

Professional Level Options Module Advanced Taxation Thursday 7 June 2018 P6 HKG ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH questions are compulsory

IN RESPECT OF FRINGE BENEFITS

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

GUIDE FOR EMPLOYERS IN RESPECT OF (2016 TAX YEAR) 1 PURPOSE 3 2 SCOPE 3 3 OBLIGATIONS OF THE EMPLOYER 3 4 BENEFITS GRANTED TO RELATIVES OF EMPLOYEES AND OTHERS 4 5 TAXABLE BENEFITS 4 5.1 ACQUISITION OF

(1) Carriage of goods and passengers shipped in Hong Kong within Hong Kong waters

Carriage of goods and passengers shipped in Hong Kong within Hong Kong waters") SECTION A CASE QUESTIONS Answer 1(a) The relevant sums are computed as follows: (1) Carriage of goods and passengers shipped in Hong Kong within Hong Kong waters HK$ 6,000,000 (2) Towage operations undertaken

SECTION A CASE QUESTIONS Answer 1(a) The relevant sums are computed as follows: (1) Carriage of goods and passengers shipped in Hong Kong within Hong Kong waters HK$ 6,000,000 (2) Towage operations undertaken

SNAPSHOTS OF HONG KONG BUDGET 2019/2020

SNAPSHOTS OF HONG KONG BUDGET 2019/2020 The Finance Secretary Mr. Paul Chan delivered his budget speech on 27 February 2019 against the backdrop of a significant fall in Hong Kong s fiscal surplus in 2018.

SNAPSHOTS OF HONG KONG BUDGET 2019/2020 The Finance Secretary Mr. Paul Chan delivered his budget speech on 27 February 2019 against the backdrop of a significant fall in Hong Kong s fiscal surplus in 2018.

Staff Regulations Appendix V

Appendix V Pension Scheme rules 1 Chapter I General provisions Article 1 - Scope 1. The Pension Scheme established by these Rules applies to the permanent staff, holding indefinite term or definite or

Appendix V Pension Scheme rules 1 Chapter I General provisions Article 1 - Scope 1. The Pension Scheme established by these Rules applies to the permanent staff, holding indefinite term or definite or

tes for Guidance Taxes Consolidation Act 1997 Finance Act 2017 Edition - Part 31

Part 31 Taxation of Settlors, etc in Respect of Settled or Transferred Income CHAPTER 1 Revocable dispositions for short periods and certain dispositions in favour of children 791 Income under revocable

Part 31 Taxation of Settlors, etc in Respect of Settled or Transferred Income CHAPTER 1 Revocable dispositions for short periods and certain dispositions in favour of children 791 Income under revocable

2018/19 HKSAR Budget Commentary. Sarah Chan / Alfred Chan March 1, 2018

2018/19 HKSAR Budget Commentary Sarah Chan / Alfred Chan March 1, 2018 Contents Statistics in 2018/19 Budget Relief Measures for Individuals Relief Measures for Businesses Overall Comments Tax Tips 2018.

2018/19 HKSAR Budget Commentary Sarah Chan / Alfred Chan March 1, 2018 Contents Statistics in 2018/19 Budget Relief Measures for Individuals Relief Measures for Businesses Overall Comments Tax Tips 2018.

This act shall be known and may be cited as the "Senior Citizens Rebate and Assistance Act."

4751-1. Short title This act shall be known and may be cited as the "Senior Citizens Rebate and Assistance Act." 4751-2. Declaration of policy In recognition of the severe economic plight of certain senior

4751-1. Short title This act shall be known and may be cited as the "Senior Citizens Rebate and Assistance Act." 4751-2. Declaration of policy In recognition of the severe economic plight of certain senior

International Tax Singapore Highlights 2018

International Tax Singapore Highlights 2018 Investment basics: Currency Singapore Dollar (SGD) Foreign exchange control There are no significant restrictions on foreign exchange transactions and capital

International Tax Singapore Highlights 2018 Investment basics: Currency Singapore Dollar (SGD) Foreign exchange control There are no significant restrictions on foreign exchange transactions and capital

5 Income of Other Persons Included in Assessee s Total Income

5 Income of Other Persons Included in Assessee s Total Income Learning Objectives After studying this chapter, you would be able to understand - why clubbing provisions have been incorporated in the Act

5 Income of Other Persons Included in Assessee s Total Income Learning Objectives After studying this chapter, you would be able to understand - why clubbing provisions have been incorporated in the Act

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2012 Suggested Answer

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES THE INSTITUTE OF CHARTERED SECRETARIES AND ADMINISTRATORS International Qualifying Scheme Examination HONG KONG TAXATION DECEMBER 2012 Suggested Answer

CAPITAL GAINS TAX ACT

CAPITAL GAINS TAX ACT ARRANGEMENT OF SECTIONS Section Section 1 Taxation of capital gains 2 Capital gains tax 3 Chargeable assets 4 Assets situated outside Nigeria 5 Exclusion of losses 6 Disposal of assets

CAPITAL GAINS TAX ACT ARRANGEMENT OF SECTIONS Section Section 1 Taxation of capital gains 2 Capital gains tax 3 Chargeable assets 4 Assets situated outside Nigeria 5 Exclusion of losses 6 Disposal of assets

OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2010

and Key Tax Features of Member countries 2010") OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2010 Sample excerpt United Kingdom 1. Corporate income tax I. Taxes on Corporate Income

OECD Model Tax Convention on Income and on Capital (Condensed version 2010) and Key Tax Features of Member countries 2010 Sample excerpt United Kingdom 1. Corporate income tax I. Taxes on Corporate Income

Care Home Guide: Funding

Care Home Guide: Funding CONTENTS Introduction 1 Care needs assessment 2 Care home funding assessment 4 Financial assessment Capital 7 Treatment of the value of your home as capital 10 Council deferred

Care Home Guide: Funding CONTENTS Introduction 1 Care needs assessment 2 Care home funding assessment 4 Financial assessment Capital 7 Treatment of the value of your home as capital 10 Council deferred

Chapter 11 Tax System

Chapter 11 Tax System www.pwc.com/mt/doingbusiness Doing Business in Malta Principal taxes The principal taxes under Maltese law are: Income tax, which includes tax on income and on capital gains of individuals,

Chapter 11 Tax System www.pwc.com/mt/doingbusiness Doing Business in Malta Principal taxes The principal taxes under Maltese law are: Income tax, which includes tax on income and on capital gains of individuals,

Ideally your contribution should be made as soon as possible in the year in order to shelter the investment income from tax.

Maximize RRSP Contributions. You should make your maximum RRSP contribution while you are working. You will get a tax deduction now at your current tax rate and you will be able to take the money out later

Maximize RRSP Contributions. You should make your maximum RRSP contribution while you are working. You will get a tax deduction now at your current tax rate and you will be able to take the money out later

BCL seconded four members to train GAL s production team and got reimbursed for the staff member s salary and 10% mark-up.

Question 1 1) A person carrying on trade, profession or business in Hong Kong with assessable profits arising in or derived from Hong Kong from such trade, profession or business will be chargeable to

Question 1 1) A person carrying on trade, profession or business in Hong Kong with assessable profits arising in or derived from Hong Kong from such trade, profession or business will be chargeable to

Income & Sales Tax Department. Income Tax Law. Law No. 57 of 1985 as amended by : Law No. ( 4 ) of 1992 Effective from Jan.

of 1992 Effective from Jan.") Income & Sales Tax Department Income Tax Law Law No. 57 of 1985 as amended by : Law No. ( 4 ) of 1992 Effective from Jan. 1 st 1991 Law No. ( 14 ) of 1995 Effective from Jan. 1 st 1996 Law No. (25) of

Income & Sales Tax Department Income Tax Law Law No. 57 of 1985 as amended by : Law No. ( 4 ) of 1992 Effective from Jan. 1 st 1991 Law No. ( 14 ) of 1995 Effective from Jan. 1 st 1996 Law No. (25) of

SECTION A CASE QUESTIONS. Answer 1(a)

") SECTION A CASE QUESTIONS Answer 1(a) Synergy may claim the bank interest income as exempt from profits tax under the Exemption from Profits Tax (Interest Income) Order 1998 ( the Order ) on the basis that

SECTION A CASE QUESTIONS Answer 1(a) Synergy may claim the bank interest income as exempt from profits tax under the Exemption from Profits Tax (Interest Income) Order 1998 ( the Order ) on the basis that

THE TAXATION INSTITUTE OF HONG KONG CERTIFIED TAX ADVISER QUALIFYING EXAMINATION PAPER 2 HONG KONG TAX SUGGESTED ANSWERS.

THE TAXATION INSTITUTE OF HONG KONG CERTIFIED TAX ADVISER QUALIFYING EXAMINATION 204 PAPER 2 HONG KONG TAX SUGGESTED ANSWERS Page of 4 Answer (a) Dominance Trading Limited Profits Tax Assessment Year of