IFIC S OPERATION S ADVOCACY UPDATES JAMES C. CARMAN IFIC SENIOR POLICY ADVISOR, TAXATION

|

|

|

- Frederica McKenzie

- 5 years ago

- Views:

Transcription

1 IFIC S OPERATION S ADVOCACY UPDATES JAMES C. CARMAN IFIC SENIOR POLICY ADVISOR, TAXATION

2 IFIC ADVOCACY SUCCESSES The Advantage Rules Delayed implementation until January 1, 2019 Removal of Nil Reporting Requirement for CRS and FATCA reporting Reporting account holders US taxable status is sufficient - financial institutions (FIs) not required to also report whether the reportable account holder lives outside Canada for FATCA purposes Removal of requirement for mutual fund trusts to provide a list of their beneficiaries when filing their annual trust returns 2

3 IFIC ADVOCACY SUCCESSES Revenue Quebec will not be rejecting QESI files with valid registrations Revenue Quebec likely to accept updated registrations of TFSA rejects from prior years FIs allowed to use Customized Trading Summaries instead of RL18 s for 2017 Tax Year 2017 exemption from RL16 country by country requirement 3

4 CRA NAME/SIN MISMATCH REPORT Purpose of the Report CRA October Updates Requesting additions of full SIN and client account number at the financial institution 4

5 REASON FIELDS ON CRA SLIP & XML FILINGS Financial institutions are penalized for errors beyond their control Most commonly with Estate and Residency issues A reason code would allow FI to explain why the original slip needs to be canceled and replaced Advantages reduce number of calls CRA agents need to make and speeds up processing of corrections Penalty administration can be reduced or processed more efficiently 5

6 REASON FIELDS ON CRA SLIP & XML FILINGS (CONT.) Challenge is whether this information can prevent the initial assessment of the FI? Asking for special processing for Estates similar to TFSA s 6

7 ADDING REFERENCE NUMBER AND TAX YEAR ON PROGRAM ACCOUNT TRANSACTIONS Adding this information to the transaction description on account statements and on-line transactions would: Reduce the number of calls to the CRA tax processing unit or general inquiry line Speed up payment processing of penalties and assessments Support client inquiries that corrections have been posted Help FIs reconcile the account and ensure all files submitted have been posted 7

8 POTENTIAL AGENDA TOPICS FOR NEXT MEETING WITH CRA 104.(13.3) Invalid Designations by Mutual Fund Trusts Issuance of Tax Account Numbers in a timely fashion Reducing the copies of T-slips sent to investors Industry contact point for Estate filing questions 8

9 INFORMATION REPORTING CRS UPDATE

10 GLOBAL TAX TRANSPARENCY UBS tax evasion HSBC money laundering Switzerland / US DoJ Petrobas scandal Danish tax scam on dividends refund Panama Papers Bahamas Leaks The tax world has changed significantly Public scrutiny of personal and corporate tax affairs has radically increased Regulators are demanding global tax transparency (CRS* & FATCA**) to combat tax evasion Tax transparency is now a strategic, business wide issue for our clients Increased reporting, withholding and targeted enforcement Customers /investors * Common Reporting Standard ** Foreign Account Tax Compliance Act Government Reaction QI Regime (2001) FATCA signed into Law 871(m) regulations issued French mini FATCA UK CDOT regime BEPS EU Directive on DAC2 Russian FATCA First year FATCA reporting CRS came into effect for early adopters UK Criminal Penalties legislation to become law 10

11 CURRENT GLOBAL REPORTING LANDSCAPE FATCA (113) VS. CRS (102) US FATCA IGA Countries Anguilla Czech Rep. Iceland Mexico South Africa Barbados Denmark India Montserrat South Korea Belgium Estonia Ireland Netherlands Spain Bermuda Finland Isle of Man Norway Sweden Bulgaria France Italy Poland Turks & Caicos BVI Germany Jersey Portugal UK Cayman Is. Gibraltar Latvia Romania Colombia Greece Liechtenstein San Marino Croatia Greenland Lithuania Seychelles Curaçao Guernsey Luxembourg Slovak Rep. Cyprus Hungary Malta Slovenia Argentina Faroe Islands Niue CRS Early adopters (Jurisdictions undertaking first exchanges by 2017) Antigua Brazil Hong Kong Mauritius Switzerland Australia Canada Indonesia New Zealand Trinidad & Tob. Austria Chile Israel Saudi Arabia Turkey Azerbaijan China Japan Singapore UAE Bahamas Costa Rica Kuwait St. Kitts Bahrain Dominica Macao St. Lucia Macao Panama Grenada Malaysia St. Vincent Algeria Georgia Jamaica Paraguay Thailand Angola Guyana Kazakhstan Peru Tunisia Armenia Haiti Kosovo Philippines Turkmenistan Belarus Holy See Moldova Qatar Ukraine Cabo Verde Honduras Montenegro Samoa Uzbekistan Dom. Repub. Iraq Nicaragua Serbia Vietnam Taiwan Albania Brunei Marshall Isl. Pakistan Uruguay Andorra Cook Isl. Monaco Russia Vanuatu Aruba Ghana Nauru Samoa Belize Lebanon Nigeria (2019) St. Maarten CRS Second wave adopters (Jurisdictions undertaking first exchanges by 2018 or 2019) Jurisdictions that have not indicated a timeline or that have not yet committed to CRS

12 WHAT IS A TAX FUNCTION OPERATING MODEL? There has been substantial change to global customer tax laws and regulations in recent years These changes impact what financial firms tax functions must address A big challenge has been how they address it: their tax function operating model The tax function operating model is how a financial firm s organization, people, process, data, and technology operate and interact to comply and to deliver value to its business lines, leadership, and shareholders.

13 HOW FATCA AND CRS COMPARE 13

14 CANADIAN FI S IMPACTED BY FATCA AND CRS Financial Institution is Depository Institution Custodial Institution Investment entity => Funds Canadian Financial Institution is Resident in Canada Listed Financial Institution Reporting FI is not a non-reporting FI Government entity, Bank of Canada, etc. No concept of Deemed-Compliant FFI under CRS e.g. restricted funds => AMs that did not have reporting obligations under FATCA will under CRS 14

15 FATCA AND CRS PRODUCTS IN SCOPE FINANCIAL ACCOUNTS Depository accounts Includes credit cards and other revolving credit facilities (unless an excluded account); reloadable payment cards, GIC Custodial Accounts Equity and debt instruments in investment entities Cash value insurance contracts and annuity contracts Client name accounts Excluded accounts: RRSP, RRIF, PRPP, RPP, RDSP, RESP, DPSP, NISA, eligible funeral arrangements, TFSA CRS: Dormant accounts that do not exceed $1K USD Generally align between FATCA and CRS 15

16 IMPACT OF CRS ON FUNDS & DEALERS It is anticipated that the following entities will be considered FIs for the purposes of the CRS: Investment Funds Hedge Funds Private Equity Funds Similar Collective Vehicles Where an entity is considered an FI of the purposes of the CRS, it will be required to carry out the required documentation, due diligence and reporting procedures Do not assume that an entity is exempt from the requirements of the CRS just because it was exempt from FATCA/Part XVIII of the Income Tax Act (most notably, FI with local client base not exempt under CRS) Further, there is no exclusion for publicly traded interests in investment funds or preexisting accounts with a balance of less than $50,000 and therefore unit holdings previously considered out of scope for FATCA may be in scope for CRS 16

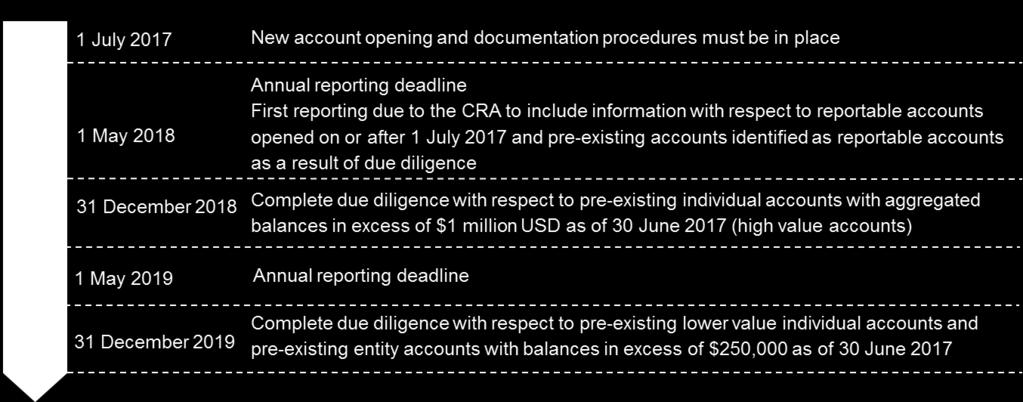

17 CRS MILESTONES 17

18 WHAT DO FINANCIAL INSTITUTIONS NEED IN THEIR TAX OPERATIONS? Required operations: Document and classify their customers Withhold and report on their customers accurately and on time Ensure control and oversight and certify compliance Remediate when necessary Resolve inquiries and controversy when necessary globally, for all required tax jurisdictions and rule-sets. How to support your team: Provide tax guidance for all relevant jurisdictions and rule-sets so operations understands what must be done Execute what must be done in a consistent and cost-sustainable way without upsetting customers Govern and control what is being done to ensure transparency, oversight and auditability Manage data in an efficient and structured way so outputs are accurate Adapt to change to adjust what is being done and ensure sustainable compliance 18

19 ACCOUNT OPENING: SELF CERTIFICATION No prescribed format for self-certificate under CRS may use CRA form, or develop an in-house form tailored to your customers Allows for account opening in person, on-line and via telephone; can be stand alone or embedded into account opening application Self-certifications (individuals) must include: Name Residence address Jurisdiction(s) of residence for tax purposes TIN Date of Birth Self certifications must be positively acknowledged by the client, via a signature or other means CRA has developed self-certification forms, both for individuals and entities, for FI s that have obligations under FATCA and CRS, or only CRS 19

20 ALLOCATION OF REPORTING RESPONSIBILITIES Nominee Name: Units held in nominee name (e.g. Investor A ) Fund confirms status of Dealer (GIIN) Dealer performs Due Diligence Dealer reports to CRA (Part XIX filing) Client Name: Units held directly in client name (e.g. Investor B ) Dealer performs Due Diligence Dealer provides CRS account holder status to Fund Fund reports to CRA (Part XIX filing) FUND DEALER A DEALER B INVESTOR A INVESTOR B 20

21 CRS REPORTING Reporting FI must provide its name, address and business number (BN) Funds with sub-fund classes of shares can report using the corporation s BN For each reportable account, the FI must provide account number and value/balance; additional information will depend on type of account 21

22 CRS REPORTING With regard to reportable persons, the FI must provide: Name Residence address Jurisdiction of tax residence Foreign TIN Canadian TIN Date of birth Controlling persons: note different requirements under CRS (Part XIX) and FATCA (Part XVIII), depending on the entity account type 22

23 NON-COMPLIANCE Non-compliance includes: Failure to file information returns On-going/repeated failure to supply accurate information or establish appropriate governance or due diligence Intentional provision of substantially incorrect information Deliberate or negligent omission of required information Active assistance to reportable persons in avoiding the reporting obligations under Part XIX 23

24 CUSTOMER TAX OPERATIONS NEED TRANSFORMATION SURVIVAL DEPENDS ON PIVOTING FROM BARE-BONES COMPLIANCE TO VALUE CREATION 1. Regulatory pressure toward international customer tax transparency continues relentlessly 2. Crippling financial penalty and criminal negligence loom as consequences for sticking with the status quo 3. Global compliance entails documenting and classifying customers, and withholding (if applicable) and/or reporting accurately and on time, for all tax jurisdictions, regulations and lines of business 4. Achieving this scope and scale of enterprise-wide compliance globally, while preventing spiraling costs and unhappy customers, in a way that is sustainable, controlled and adaptable to change this is a significant challenge

25 CUSTOMER TAX OPERATIONS NEED TRANSFORMATION SURVIVAL DEPENDS ON PIVOTING FROM BARE-BONES COMPLIANCE TO VALUE CREATION 5. To achieve this, financial institutions around the world must: Pivot from bare-minimum compliance with regulatory change to value creation through cost containment and risk reduction Consider alternative models for their end-to-end customer tax operations capability 6. Tax operations are not core to business objectives, and are increasingly pressured to do more with less 7. Tax operations traditional ways of providing capability to address growing needs are inadequate adding more headcount, enhancing desktop tools, deploying specific software, more rigorous training of staff will not suffice 8. Tax operations departments need to transform and consider new alternatives to provide their capability

26 CUSTOMER TAX OPERATIONS NEED TRANSFORMATION SURVIVAL DEPENDS ON PIVOTING FROM BARE-BONES COMPLIANCE TO VALUE CREATION Things to Consider: Integrated capability across customer tax operations functions Reliable and compliant outcomes from customer documentation through reporting Embedded controls and transparency to reduce risk Sustainable and scalable operating model Reduces current cost base, avoid future cost bloat Shed ownership of non-core processes and technology Integrated with global network of tax professionals Consistency of process and technology solutions Technology enablement and automation

27 THANK YOU! EY Contacts: Jillian Nicolson, Partner Operational Taxes Leader, Canada Financial Services & Insurance Brenda Didyk, Senior Manager Financial Services & Insurance

When will CbC reports need to be filled?

Who will be subject to CbCR? Country by Country Reporting (CbCR) applies to multinational companies (MNCs) with a combined revenue of euros 750 million or more When will CbC reports need to be filled?

Who will be subject to CbCR? Country by Country Reporting (CbCR) applies to multinational companies (MNCs) with a combined revenue of euros 750 million or more When will CbC reports need to be filled?

TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017

(CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017") Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

AUTOMATIC EXCHANGE OF INFORMATION (AEOI)

") AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

Tax Game Changers Yair Zorea, Tax Partner, PwC Israel Yitzhak Zahavy, Tax Supervisor, PwC Israel November 2015

www.pwc.com/il Tax Game Changers Yair Zorea, Tax Partner, Yitzhak Zahavy, Tax Supervisor, November 2015 Agenda FATCA Common Reporting Standard IRS Audit Trends A look under the hood 2 FATCA 3 Foreign Account

www.pwc.com/il Tax Game Changers Yair Zorea, Tax Partner, Yitzhak Zahavy, Tax Supervisor, November 2015 Agenda FATCA Common Reporting Standard IRS Audit Trends A look under the hood 2 FATCA 3 Foreign Account

UPDATE. COMMON REPORTING STANDARD IN THE CAYMAN ISLANDS. What is CRS? Participating Jurisdictions

www.kensington-trust.com UPDATE COMMON REPORTING STANDARD IN THE CAYMAN ISLANDS The Cayman Islands Tax Information Authority (International Tax Compliance) (Common Reporting Standard) Regulations, 2015

www.kensington-trust.com UPDATE COMMON REPORTING STANDARD IN THE CAYMAN ISLANDS The Cayman Islands Tax Information Authority (International Tax Compliance) (Common Reporting Standard) Regulations, 2015

TRANS WORLD COMPLIANCE, INC. CARIBBEAN ASSOCIATION OF BANKS, INC. & BARBADOS INTERNATIONAL BUSINESS ASSOC. Presents: FATCA compliance update

TRANS WORLD COMPLIANCE, INC. IN PARTNERSHIP WITH CARIBBEAN ASSOCIATION OF BANKS, INC. & BARBADOS INTERNATIONAL BUSINESS ASSOC. Presents: FATCA compliance update AGENDA Current FATCA status / update FATCA

TRANS WORLD COMPLIANCE, INC. IN PARTNERSHIP WITH CARIBBEAN ASSOCIATION OF BANKS, INC. & BARBADOS INTERNATIONAL BUSINESS ASSOC. Presents: FATCA compliance update AGENDA Current FATCA status / update FATCA

Argentina Tax amnesty: the day after

Argentina Tax amnesty: the day after Walter C. Keiniger December 2016 YES to amnesty: exchange of Information DTTs (Art. 26 OECD Model) Provisions or agreements signed by Argentina Bilateral Agreements

Argentina Tax amnesty: the day after Walter C. Keiniger December 2016 YES to amnesty: exchange of Information DTTs (Art. 26 OECD Model) Provisions or agreements signed by Argentina Bilateral Agreements

STANDARD FOR AUTOMATIC EXCHANGE OF FINANCIAL ACCOUNT INFORMATION. Philip Kerfs, OECD

STANDARD FOR AUTOMATIC EXCHANGE OF FINANCIAL ACCOUNT INFORMATION Philip Kerfs, OECD Overview Background, context and timeline The Standard: basic approach and key features Next steps: implementing the

STANDARD FOR AUTOMATIC EXCHANGE OF FINANCIAL ACCOUNT INFORMATION Philip Kerfs, OECD Overview Background, context and timeline The Standard: basic approach and key features Next steps: implementing the

FATCA. Its Implications for the Financial Services Industry in Belize (A Banking Perspective) February 19, 2015 Aldo J. Salazar

February 19, 2015 Aldo J. Salazar") FATCA Its Implications for the Financial Services Industry in Belize (A Banking Perspective) February 19, 2015 Aldo J. Salazar Introduction The Foreign Account Tax Compliance Act (FATCA) was signed into

FATCA Its Implications for the Financial Services Industry in Belize (A Banking Perspective) February 19, 2015 Aldo J. Salazar Introduction The Foreign Account Tax Compliance Act (FATCA) was signed into

Total Imports by Volume (Gallons per Country)

") 2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

Total Imports by Volume (Gallons per Country)

") 1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

Total Imports by Volume (Gallons per Country)

") 10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS. No. 32 of 2016

1 SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS No. 32 of 2016 Common Reporting Standard (Automatic Exchange of Financial Account Information) Regulations The Minister, in exercise of the powers

1 SAINT CHRISTOPHER AND NEVIS STATUTORY RULES AND ORDERS No. 32 of 2016 Common Reporting Standard (Automatic Exchange of Financial Account Information) Regulations The Minister, in exercise of the powers

Total Imports by Volume (Gallons per Country)

") 3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

Total Imports by Volume (Gallons per Country)

") 2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

Total Imports by Volume (Gallons per Country)

") 12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

Total Imports by Volume (Gallons per Country)

") 11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

Total Imports by Volume (Gallons per Country)

") 10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

Webinar: Common Reporting Standard. Game Plan for Compliance December 10, 2015

Webinar: Common Reporting Standard Game Plan for Compliance December 10, 2015 Presenters Moderator: Sara Pereda Director DMS Offshore Investment Services Roman Ipfling Director DMS International Tax Compliance

Webinar: Common Reporting Standard Game Plan for Compliance December 10, 2015 Presenters Moderator: Sara Pereda Director DMS Offshore Investment Services Roman Ipfling Director DMS International Tax Compliance

TAXATION (IMPLEMENTATION) (INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015

(INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015") Arrangement TAXATION (IMPLEMENTATION) (INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015 Arrangement Regulation 1 Interpretation... 3 2 Meaning of relevant date and relevant

Arrangement TAXATION (IMPLEMENTATION) (INTERNATIONAL TAX COMPLIANCE) (COMMON REPORTING STANDARD) (JERSEY) REGULATIONS 2015 Arrangement Regulation 1 Interpretation... 3 2 Meaning of relevant date and relevant

55/2005 and 78/2005 Convention on automatic exchange of information

INCOME TAX TREATIES AND AGREEMENTS ON THE TAXATION OF INCOME FROM SAV- INGS (IN FORCE, SIGNED, INITIALLED OR IN NEGOTIATING PROCESS, SITUATION ON 25th April 2018) Country Year of conclusion Number in the

INCOME TAX TREATIES AND AGREEMENTS ON THE TAXATION OF INCOME FROM SAV- INGS (IN FORCE, SIGNED, INITIALLED OR IN NEGOTIATING PROCESS, SITUATION ON 25th April 2018) Country Year of conclusion Number in the

Total Imports by Volume (Gallons per Country)

") 7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

THE COMMON REPORTING STANDARD ("CRS") UPDATE FOR OCORIAN CLIENTS

UPDATE FOR OCORIAN CLIENTS") JERSEY BRIEFING November 2015 THE COMMON REPORTING STANDARD ("CRS") UPDATE FOR OCORIAN CLIENTS At present 93 countries will implement CRS over a two year period commencing 1 January 2016. The CRS initiative

JERSEY BRIEFING November 2015 THE COMMON REPORTING STANDARD ("CRS") UPDATE FOR OCORIAN CLIENTS At present 93 countries will implement CRS over a two year period commencing 1 January 2016. The CRS initiative

GENERAL ANTI AVOIDANCE RULE RECENT CASE LAW IN ARGENTINA

GENERAL ANTI AVOIDANCE RULE RECENT CASE LAW IN ARGENTINA Leandro M. Passarella Passarella Abogados TTN Conferences Latin America 2014 Buenos Aires November 17, 2014 Background Past structures Case Law

GENERAL ANTI AVOIDANCE RULE RECENT CASE LAW IN ARGENTINA Leandro M. Passarella Passarella Abogados TTN Conferences Latin America 2014 Buenos Aires November 17, 2014 Background Past structures Case Law

Total Imports by Volume (Gallons per Country)

") 6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

Japan s DTA Strategy and its Implications to Developing Countries. April 9 th, 2015 Kentaro Ogata

Japan s DTA Strategy and its Implications to Developing Countries April 9 th, 2015 Kentaro Ogata Table of Contents Role of DTA DTA strategy: basics JP and DC perspectives New initiatives Growing focus

Japan s DTA Strategy and its Implications to Developing Countries April 9 th, 2015 Kentaro Ogata Table of Contents Role of DTA DTA strategy: basics JP and DC perspectives New initiatives Growing focus

Total Imports by Volume (Gallons per Country)

") 5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

SCHEDULE OF REVIEWS (DECEMBER 2017)

") 2016-2020 SCHEDULE OF REVIEWS (DECEMBER 2017) 2016-2021 SCHEDULE OF EOIR REVIEWS 1. At its meeting in Jakarta on 21-22 November 2013, the Global Forum agreed that a new round of peer reviews for the Exchange

2016-2020 SCHEDULE OF REVIEWS (DECEMBER 2017) 2016-2021 SCHEDULE OF EOIR REVIEWS 1. At its meeting in Jakarta on 21-22 November 2013, the Global Forum agreed that a new round of peer reviews for the Exchange

OECD Common Reporting Standard Getting into the Detail STEP / GAT

OECD Common Reporting Standard Getting into the Detail STEP / GAT Jo Huxtable Martin Popplewell 11 February 2016 Agenda Introduction CRS and the wider regulatory environment CRS latest developments and

OECD Common Reporting Standard Getting into the Detail STEP / GAT Jo Huxtable Martin Popplewell 11 February 2016 Agenda Introduction CRS and the wider regulatory environment CRS latest developments and

Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol

European Treaty Series - No. 127 Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol Strasbourg, 1.VI.2011 Annex B Competent authorities (*) States From A to F

European Treaty Series - No. 127 Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol Strasbourg, 1.VI.2011 Annex B Competent authorities (*) States From A to F

a closer look GLOBAL TAX WEEKLY ISSUE 249 AUGUST 17, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Total Imports by Volume (Gallons per Country)

") 4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

Intercontinental Trust Ltd COMMON REPORTING STANDARD

Intercontinental Trust Ltd COMMON REPORTING STANDARD 1 Conspectus The OECD, working in collaboration with G20 and in close co-operation with the EU, has developed a global standard for automatic exchange

Intercontinental Trust Ltd COMMON REPORTING STANDARD 1 Conspectus The OECD, working in collaboration with G20 and in close co-operation with the EU, has developed a global standard for automatic exchange

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

COSTAS TSIELEPIS & CO LTD

COSTAS TSIELEPIS & CO LTD TAX UPDATE Authored By: ALEXIS TSIELEPIS, Director, Head of Taxation VOLUME 5, ISSUE 2 knowledge Facts, information and skills acquired through experience or education; the theoretical

COSTAS TSIELEPIS & CO LTD TAX UPDATE Authored By: ALEXIS TSIELEPIS, Director, Head of Taxation VOLUME 5, ISSUE 2 knowledge Facts, information and skills acquired through experience or education; the theoretical

Common Reporting Standard

www.pwc.com Common Reporting Standard Singapore September 2016 1. Setting the scene 2 Asset management in the spotlight FATCA 3 CRS is the next wave of increasing global standards on Tax Information Reporting

www.pwc.com Common Reporting Standard Singapore September 2016 1. Setting the scene 2 Asset management in the spotlight FATCA 3 CRS is the next wave of increasing global standards on Tax Information Reporting

Tax Management International Journal

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 540, 09/12/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 540, 09/12/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

- Act Nr. XXXVII of 2013 on certain regulation connected with the international administrative cooperation on tax and other public burdens.

Dear Customer, The Hungarian Parliament introduced the Common Reporting Standards, CRS on the automatic financial data exchange with the effect of 01.01.2016. The aim of the regulation is to hinder the

Dear Customer, The Hungarian Parliament introduced the Common Reporting Standards, CRS on the automatic financial data exchange with the effect of 01.01.2016. The aim of the regulation is to hinder the

Total Imports by Volume (Gallons per Country)

") 3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

MEXICO - INTERNATIONAL TAX UPDATE -

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

A F R I C A WA T C H TRENDS AND MARKERS Signatories to the United Nations Convention against Transnational Organised Crime Afghanistan Albania Algeria Andorra Angola Antigua and Barbuda Argentina Armenia

RSM AND HFMWEEK CRS/FATCA SURVEY HOW DO FUNDS INTEND TO ADDRESS CRS AND FATCA COMPLIANCE CHALLENGES?

RSM AND HFMWEEK CRS/FATCA SURVEY HOW DO FUNDS INTEND TO ADDRESS CRS AND FATCA COMPLIANCE CHALLENGES? During the third quarter of 2016, RSM and Hedge Fund Management Week (HFMWeek) surveyed chief operating

RSM AND HFMWEEK CRS/FATCA SURVEY HOW DO FUNDS INTEND TO ADDRESS CRS AND FATCA COMPLIANCE CHALLENGES? During the third quarter of 2016, RSM and Hedge Fund Management Week (HFMWeek) surveyed chief operating

International Journal TM

International Journal TM Reproduced with permission from Tax Management International Journal, Vol. 47, No. 12, 12/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com

International Journal TM Reproduced with permission from Tax Management International Journal, Vol. 47, No. 12, 12/07/2018. Copyright 2018 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com

Tax certification for Entities FATCA and CRS

Schroder Investment Management Australia Limited Level 20, Angel Place 123 Pitt Street Sydney, NSW 2000 www.schroders.com.au AFSL 226473 ABN 22 000 443 274 Tax certification for Entities FATCA and CRS

Schroder Investment Management Australia Limited Level 20, Angel Place 123 Pitt Street Sydney, NSW 2000 www.schroders.com.au AFSL 226473 ABN 22 000 443 274 Tax certification for Entities FATCA and CRS

The Development of Tax Transparency in

The Development of Tax Transparency in OECD Countries Hoang Ha Nguyen Thi and Till Nikolka 1 Over the course of globalisation, governments have been confronted with the growing international dimension

The Development of Tax Transparency in OECD Countries Hoang Ha Nguyen Thi and Till Nikolka 1 Over the course of globalisation, governments have been confronted with the growing international dimension

FATCA: More than a Five Letter Word NACUBO Tax Forum 2014

FATCA: More than a Five Letter Word NACUBO Tax Forum 2014 Presented by: Nicole Bencik, Partner, Crowe Horwath LLP John Kelleher, Partner Crowe Horwath LLP Joel Levenson, Associate Director: Tax Compliance,

FATCA: More than a Five Letter Word NACUBO Tax Forum 2014 Presented by: Nicole Bencik, Partner, Crowe Horwath LLP John Kelleher, Partner Crowe Horwath LLP Joel Levenson, Associate Director: Tax Compliance,

FACT SHEET. Automatic exchange of information (AEOI)

") FACT SHEET Automatic exchange of information (AEOI) In a joint statement, a number of countries, including all major financial centres and Liechtenstein, have announced that they will introduce the new

FACT SHEET Automatic exchange of information (AEOI) In a joint statement, a number of countries, including all major financial centres and Liechtenstein, have announced that they will introduce the new

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

Current Status of U.S. Tax Treaties and International Tax Agreements

Tax Management International Journal TM Reproduced with permission from Tax Management International Journal, Vol. 47, No. 12, p. 788, 12/08/2017. Copyright 2017 by The Bureau of National Affairs, Inc.

Tax Management International Journal TM Reproduced with permission from Tax Management International Journal, Vol. 47, No. 12, p. 788, 12/08/2017. Copyright 2017 by The Bureau of National Affairs, Inc.

TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD

TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD 2 TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD A COMMON REPORTING STANDARD ACROSS THE WORLD The goalposts in international tax reporting are moving

TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD 2 TAX TRANSPARENCY THE NEW GLOBAL REPORTING STANDARD A COMMON REPORTING STANDARD ACROSS THE WORLD The goalposts in international tax reporting are moving

Withholding Tax Rates 2014*

Withholding Tax Rates 2014* (Rates are current as of 1 March 2014) Jurisdiction Dividends Interest Royalties Notes Afghanistan 20% 20% 20% International Tax Albania 10% 10% 10% Algeria 15% 10% 24% Andorra

Withholding Tax Rates 2014* (Rates are current as of 1 March 2014) Jurisdiction Dividends Interest Royalties Notes Afghanistan 20% 20% 20% International Tax Albania 10% 10% 10% Algeria 15% 10% 24% Andorra

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

Global Forum on Transparency and Exchange of Information for Tax Purposes. Statement of Outcomes

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development

Unclassified English/French Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 25-Sep-2009 English/French COUNCIL Council DECISION

Unclassified English/French Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 25-Sep-2009 English/French COUNCIL Council DECISION

Progress Towards Tax Transparency

COMMITTED TO YOU April 2015 Progress Towards Tax Transparency OECD Developments The Swiss Strategy Latest Steps Impact - What s Next Union Bancaire Privée, UBP SA Rue du Rhône 96-98 CP 1320 1211 Geneva

COMMITTED TO YOU April 2015 Progress Towards Tax Transparency OECD Developments The Swiss Strategy Latest Steps Impact - What s Next Union Bancaire Privée, UBP SA Rue du Rhône 96-98 CP 1320 1211 Geneva

CB CROSS BORDER YOUR GOAL. OUR MISSION.

CB CROSS BORDER YOUR GOAL. OUR MISSION. Your Chosen Counsel Because We care We are an international private wealth advisory We specialize in providing offshore solutions crossborderworldwide.com What we

CB CROSS BORDER YOUR GOAL. OUR MISSION. Your Chosen Counsel Because We care We are an international private wealth advisory We specialize in providing offshore solutions crossborderworldwide.com What we

Save up to 74% on U.S. postage.

BRITISH COLUMBIA RATE CARD 2019 Effective January 27 2019 Save up to 74% on U.S. postage. Postage from $2.66 USD Delivery within 4 business days Tracking included Chit Chats Insurance from $0.35 Canada

BRITISH COLUMBIA RATE CARD 2019 Effective January 27 2019 Save up to 74% on U.S. postage. Postage from $2.66 USD Delivery within 4 business days Tracking included Chit Chats Insurance from $0.35 Canada

A guide to FACTA and the new Common Reporting Standard. For advisers use only.

A guide to FACTA and the new Common Reporting Standard For advisers use only. Contents 01 Introduction 01 Background 02 How are we complying with FACTA in the UK? 02 How are we complying with FACTA in

A guide to FACTA and the new Common Reporting Standard For advisers use only. Contents 01 Introduction 01 Background 02 How are we complying with FACTA in the UK? 02 How are we complying with FACTA in

a closer look GLOBAL TAX WEEKLY ISSUE 204 OCTOBER 6, 2016

GLOBAL TAX WEEKLY a closer look ISSUE 204 OCTOBER 6, 2016 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 204 OCTOBER 6, 2016 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Cayman Islands - FATCA and CRS Top tips & pitfalls to avoid in 2018

Cayman Islands - FATCA and CRS Top tips & pitfalls to avoid in 018 In this article we share our tips for reporting success for a Cayman Investment Entity Financial Institution (FI) and common pitfalls

Cayman Islands - FATCA and CRS Top tips & pitfalls to avoid in 018 In this article we share our tips for reporting success for a Cayman Investment Entity Financial Institution (FI) and common pitfalls

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

FATCA: Developments & perspectives

FATCA: Developments & perspectives Automatic Exchange of Information 22 May 2014 FATCA evolves into CRS a multilateral automatic exchange of information 2010 The Foreign Account Tax Compliance Act (FATCA)

FATCA: Developments & perspectives Automatic Exchange of Information 22 May 2014 FATCA evolves into CRS a multilateral automatic exchange of information 2010 The Foreign Account Tax Compliance Act (FATCA)

Tax trends and issues for financial services. Michael Velten, Southeast Asia Financial Services Industry Tax Leader

Tax trends and issues for financial services Michael Velten, Southeast Asia Financial Services Industry Tax Leader Agenda Overview: Tax as a risk BEPS: A changing tax landscape CRS: Status in the region

Tax trends and issues for financial services Michael Velten, Southeast Asia Financial Services Industry Tax Leader Agenda Overview: Tax as a risk BEPS: A changing tax landscape CRS: Status in the region

Information Leaflet No. 5

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / May 2017 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch in the State.

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / May 2017 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch in the State.

Update on the Work of the Global Forum and Outline of Future Directions

Update on the Work of the Global Forum and Outline of Future Directions 4 th IMF-Japan High Level Tax Conference Tokyo, Japan Dónal Godfrey, Global Forum Secretariat Global Forum on Transparency and Exchange

Update on the Work of the Global Forum and Outline of Future Directions 4 th IMF-Japan High Level Tax Conference Tokyo, Japan Dónal Godfrey, Global Forum Secretariat Global Forum on Transparency and Exchange

Dutch tax treaty overview Q3, 2012

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Request to accept inclusive insurance P6L or EASY Pauschal

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

FATCA After the Final Regulations and IGA Proliferation

FATCA After the Final Regulations and IGA Proliferation Presented to the Princeton FATCA and CRS Forum on February 4, 2016 Steven D. Bortnick and Morgan L. Klinzing #37612904v.1 Steven D. Bortnick Partner,

FATCA After the Final Regulations and IGA Proliferation Presented to the Princeton FATCA and CRS Forum on February 4, 2016 Steven D. Bortnick and Morgan L. Klinzing #37612904v.1 Steven D. Bortnick Partner,

a closer look GLOBAL TAX WEEKLY ISSUE 255 SEPTEMBER 28, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 255 SEPTEMBER 28, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

GLOBAL TAX WEEKLY a closer look ISSUE 255 SEPTEMBER 28, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

Italy amends white list

26 August 2016 Global Tax Alert Italy amends white list EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: www.ey.com/taxalerts Executive

26 August 2016 Global Tax Alert Italy amends white list EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: www.ey.com/taxalerts Executive

Information Leaflet No. 5

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / FEBRUARY 2018 ii 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / FEBRUARY 2018 ii 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch

YUM! Brands, Inc. Historical Financial Summary. Second Quarter, 2017

YUM! Brands, Inc. Historical Financial Summary Second Quarter, 2017 YUM! Brands, Inc. Consolidated Statements of Income (in millions, except per share amounts) 2017 2016 2015 YTD Q3 Q4 FY FY Revenues Company

YUM! Brands, Inc. Historical Financial Summary Second Quarter, 2017 YUM! Brands, Inc. Consolidated Statements of Income (in millions, except per share amounts) 2017 2016 2015 YTD Q3 Q4 FY FY Revenues Company

Global Forum on Transparency and Exchange of Information for Tax Purposes

Global Forum on Transparency and Exchange of Information for Tax Purposes Automatic Exchange of Information Implementation Report 2017 AEOI Implementation Report 2017 1 2 Table of contents Executive summary...

Global Forum on Transparency and Exchange of Information for Tax Purposes Automatic Exchange of Information Implementation Report 2017 AEOI Implementation Report 2017 1 2 Table of contents Executive summary...

Luxembourg Country Profile

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

The Global Forum on Transparency and Exchange of Information for Tax Purposes

ANNEXES 1 The Global Forum on Transparency and Exchange of formation for Tax Purposes INFORMATION BRIEF November 2013 For more information please contact: Monica Bhatia, Head of the Global Forum Secretariat

ANNEXES 1 The Global Forum on Transparency and Exchange of formation for Tax Purposes INFORMATION BRIEF November 2013 For more information please contact: Monica Bhatia, Head of the Global Forum Secretariat

Save up to 74% on U.S. postage.

ONTARIO RATE CARD 2018 Save up to 74% on U.S. postage. Postage from $2.66 USD Delivery within 4 business days Tracking included Chit Chats Insurance from $0.35 Canada Post vs Chit Chats Bracelet 3 oz (85g)

ONTARIO RATE CARD 2018 Save up to 74% on U.S. postage. Postage from $2.66 USD Delivery within 4 business days Tracking included Chit Chats Insurance from $0.35 Canada Post vs Chit Chats Bracelet 3 oz (85g)

Withholding Tax Rates 2017*

Withholding Tax Rates 2017* International Tax Updated March 2017 Jurisdiction Dividends Interest Royalties Notes Albania 15% 15% 15% Algeria 15% 10% 24% Andorra 0% 0% 5% Angola 10% 15% 10% Anguilla 0%

Withholding Tax Rates 2017* International Tax Updated March 2017 Jurisdiction Dividends Interest Royalties Notes Albania 15% 15% 15% Algeria 15% 10% 24% Andorra 0% 0% 5% Angola 10% 15% 10% Anguilla 0%

FATCA Update May 2014

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

www.pwc.com The Basics Foreign Account Tax Compliance Act Purpose of Prevent and detect offshore tax evasion by US citizens Increased information reporting Enforced by withholding tax Effective begins

Deloitte TaxMax the 41st series The Arena of Tax Unveiled The unknown operational intricacies in business tax and tax controversies

Deloitte TaxMax the 41st series The Arena of Tax Unveiled The unknown operational intricacies in business tax and tax controversies Moderator: Chow Kuo Seng Speakers: Sivaram Nagappan, Malaysia Airlines

Deloitte TaxMax the 41st series The Arena of Tax Unveiled The unknown operational intricacies in business tax and tax controversies Moderator: Chow Kuo Seng Speakers: Sivaram Nagappan, Malaysia Airlines

CRS Form for Tax Residency Self Certification For Individuals, Joint Accounts (CRS I)

") For Individuals, Joint Accounts (CRS I) Please read these instructions carefully before completing the form Chapter XIIA of Income Tax Rules, 2002 and Regulations based on the OECD Common Reporting Standard

For Individuals, Joint Accounts (CRS I) Please read these instructions carefully before completing the form Chapter XIIA of Income Tax Rules, 2002 and Regulations based on the OECD Common Reporting Standard

Summary 715 SUMMARY. Minimum Legal Fee Schedule. Loser Pays Statute. Prohibition Against Legal Advertising / Soliciting of Pro bono

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Long Association List of Jurisdictions Surveyed for Which a Response Has Been Received

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

WGI Ranking for SA8000 System

Afghanistan not rated Highest Risk ALBANIA 47 High Risk ALGERIA 24 Highest Risk AMERICAN SAMOA 74 Lower Risk ANDORRA 91 Lower Risk ANGOLA 16 Highest Risk ANGUILLA 90 Lower Risk ANTIGUA AND BARBUDA 76 Lower

Afghanistan not rated Highest Risk ALBANIA 47 High Risk ALGERIA 24 Highest Risk AMERICAN SAMOA 74 Lower Risk ANDORRA 91 Lower Risk ANGOLA 16 Highest Risk ANGUILLA 90 Lower Risk ANTIGUA AND BARBUDA 76 Lower

The Structure, Scope, and Independence of Banking Supervision Issues and International Evidence

The Structure, Scope, and Independence of Banking Supervision Issues and International Evidence Daniel Nolle Senior Financial Economist Office of the daniel.nolle@occ.treas.gov Presentation July 10, 2003

The Structure, Scope, and Independence of Banking Supervision Issues and International Evidence Daniel Nolle Senior Financial Economist Office of the daniel.nolle@occ.treas.gov Presentation July 10, 2003

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Current Issues in International Tax Policy

Current Issues in International Tax Policy Shigeto HIKI Director, International Tax Policy Division, Tax Bureau, Ministry of Finance, Japan The Fourth IMF-Japan High-Level Tax Conference For Asian Countries

Current Issues in International Tax Policy Shigeto HIKI Director, International Tax Policy Division, Tax Bureau, Ministry of Finance, Japan The Fourth IMF-Japan High-Level Tax Conference For Asian Countries

FATCA FAQS FATCA AND THE MOVEMENT TO HARMONISE INTERNATIONAL TAX COMPLIANCE AND TRANSPARENCY

FATCA FAQS FATCA AND THE MOVEMENT TO HARMONISE INTERNATIONAL TAX COMPLIANCE AND TRANSPARENCY The last decade has seen an extraordinary number of tax information exchange agreements (TIEAs), which the Organisation

FATCA FAQS FATCA AND THE MOVEMENT TO HARMONISE INTERNATIONAL TAX COMPLIANCE AND TRANSPARENCY The last decade has seen an extraordinary number of tax information exchange agreements (TIEAs), which the Organisation

Real Estate & Private Equity workshop

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

(ISC)2 Career Impact Survey

2 Career Impact Survey") (ISC)2 Career Impact Survey 1. In what country are you located? Albania 0.0% 0 Andorra 0.0% 1 Angola 0.0% 0 Antigua and Barbuda 0.0% 0 Argentina 0.3% 9 Australia 2.0% 61 Austria 0.2% 6 Azerbaijan 0.0%

(ISC)2 Career Impact Survey 1. In what country are you located? Albania 0.0% 0 Andorra 0.0% 1 Angola 0.0% 0 Antigua and Barbuda 0.0% 0 Argentina 0.3% 9 Australia 2.0% 61 Austria 0.2% 6 Azerbaijan 0.0%

Pension Payments Made To Foreign Bank Accounts

West Midlands Pension Fund West Midlands Pension Fund Pension Payments Made To Foreign Bank Accounts A Guide to Worldlink Payment Services August 2012 What does WorldLink Payment Services offer? WorldLink

West Midlands Pension Fund West Midlands Pension Fund Pension Payments Made To Foreign Bank Accounts A Guide to Worldlink Payment Services August 2012 What does WorldLink Payment Services offer? WorldLink

Convention on Mutual Administrative Assistance in Tax Matters

Convention on Mutual Administrative Assistance in Tax Matters Strasbourg, 25.I.1988 Annex B Competent authorities (*) European Treaty Series - No. 127 States From A to F Albania Argentina Australia Austria

Convention on Mutual Administrative Assistance in Tax Matters Strasbourg, 25.I.1988 Annex B Competent authorities (*) European Treaty Series - No. 127 States From A to F Albania Argentina Australia Austria

a closer look GLOBAL TAX WEEKLY ISSUE 271 JANUARY 18, 2018

GLOBAL TAX WEEKLY a closer look ISSUE 271 JANUARY 18, 2018 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 271 JANUARY 18, 2018 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Spain France. England Netherlands. Wales Ukraine. Republic of Ireland Czech Republic. Romania Albania. Serbia Israel. FYR Macedonia Latvia

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey