Lecture # 7 -- Taxes and Subsidies

|

|

|

- Dorothy Osborne

- 5 years ago

- Views:

Transcription

1 I. Emission Fees Lecture # 7 -- Taxes and Subsidies Recall that the problem with externalities is that they are not reflected in prices. o The government can rectify the problem by setting a price for pollution. o The goal is to set the fee so that the polluter incorporates the social cost. If MAC is known, simply set the fee equal to MAC at the optimal level of pollution. o The firm will find it beneficial to abate up to this point, since abating is cheaper than paying the fee. o After this point, paying the tax is cheaper than abatement, so no further abatement occurs. o Note that since MAC = MD at the optimal level, the firm is taking into account the value of the damage it is doing. o If MAC is unknown, the fee should be based on the expected value (the best guess of MAC). The main advantage of emissions fees is that, when there is more than one polluter, they achieve a given level of pollution control at the lowest possible cost. o Thus, economists say that emissions fees are an efficient environmental policy. o An efficient solution is found when the marginal abatement costs are equal across all firms. At this point, there is no way to shift abatement responsibilities among the firms and achieve a lower total cost. However, the cost to each individual firm is greater, since the firms pay both abatement costs and the fees. Thus, emissions fees are politically unpopular.

2 Firm 1 Firm 2 Emissions Abatement MC TC Emissions Abatement MC TC Goal: Reduce pollution by 10 units Command and Control: Each firm reduces by 5 units Abatement Costs Firm Firm Total Costs: Emissions Fee: $5 per ton Abatement Costs Tax bill Total Payments Firm Firm Total Cost LESSON: Tax equates MAC across firms. Therefore, it achieves the pollution control target at minimum cost.

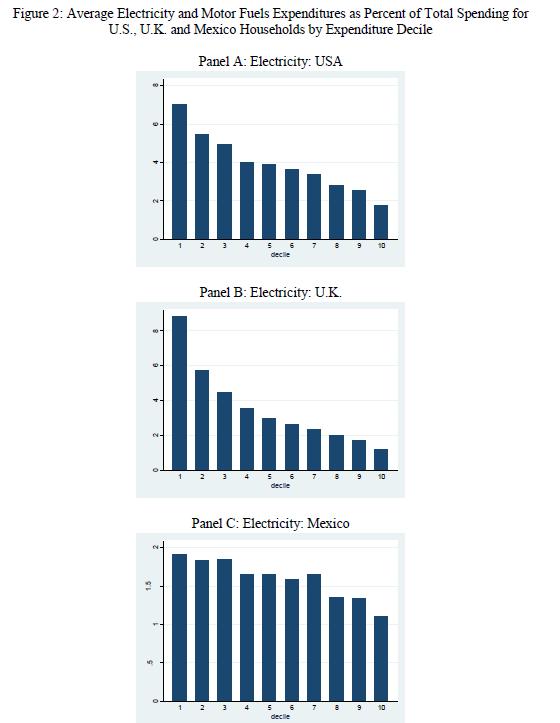

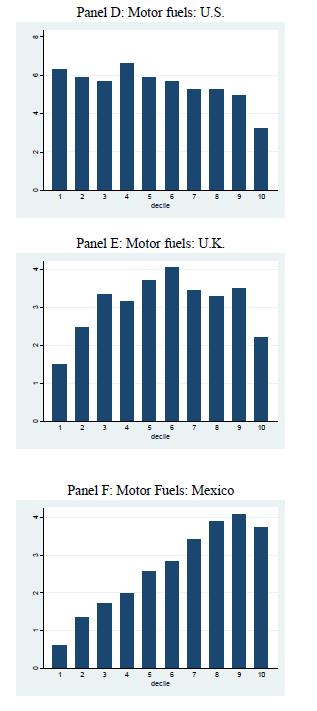

3 Another potential advantage of fees over CAC is that fees encourage innovation. o Once you ve met a CAC regulation, you have little incentive to do better. o However, if you lower your MAC, you can abate more, and pay less in fees. See, for example, figure 12-7 in Field. Disadvantages of taxes and emission fees o Uncertainty Compared to command and control, emission fees provide more certainty on costs, but less certainty on the final level of emissions. o Geographically-varying damage Market-based policies guarantee an overall goal, but they don't guarantee which firms will reduce and which firms won't. If firms near an urban center choose to pay the fee rather than reduce emissions, damages may remain high. Varying the fee based on potential damages can help address this. o Monitoring costs To charge a fee per unit of pollution, all pollution must be monitored and measured. o Less popular politically Firms have a higher tax bill All new taxes unpopular in the U.S. o Incompatibility with firm decision-making Firms may not respond to small taxes because the department paying them is different from the department managing o Distributional issues Concerns about equity might make some environmental taxes politically unpopular. For example, lower income families spend more of their income on gasoline, making a gas tax a regressive. While all policies raise the possibility of costs being passed on to consumers, there are more costs to be passed on here, as firms pay both for abatement and the fee for the remaining units of pollution. Pizer and Sexton (NBER Working Paper #23318, 2017), look at consumption patterns by total household expenditure decile (vertical equity) For electricity, shares of consumption are higher for lower expenditure households For gasoline, taxes are less regressive In Mexico, higher expenditure families spend more on gasoline

4

, there is more variation for lower income")

5 Looking at horizontal equity (variation within expenditure deciles), there is more variation for lower income households

6 The reading on implementing a carbon tax provides an example of how the use of revenue matters Figure 2 shows that a carbon tax itself (graph on left) is regressive Lowest income quantile spends a larger percentage of its income How the revenue is used (discussed more later in class) can change this Refundable credits help poor families more Lower personal or corporate taxes help higher income families (graphs on right -- % of income going to taxes falls for lowest quantiles with a credit, for example)

7 II. Implementation Issues Questions for designing an environmental excise tax: 1. What is to be taxed? That is, what is the tax base? May be direct (e.g. CFCs, emissions), or indirect (e.g. gasoline) Could also use a multi-part tax: tax sale of an indirect commodity and subsidize clean technology to encourage people to change behavior E.g. tax fuel and subsidize fuel efficient cars to encourage people to buy more efficient cars, since cannot tax emissions from vehicles directly Administrative costs are part of this decision Want to tax users directly However, it may be difficult to know the users There may be many users. For CFCs, it was easier to tax production than tax each user. Consider example of taxing CO2 emissions from the reading: Emissions come from vehicles, electricity production, airplanes, industry, agriculture, etc. Emissions not easily monitored, so likely would tax fuel A carbon tax on fuel captures emissions from combustion, but ignores processes like cement manufacturing or land use. Doesn t reward processes such as carbon capture and storage. Also need to consider other greenhouse gases, such as methane. 2. What tax rate to impose? This is where most of the economic analysis comes in. In principle, the tax should reflect marginal damages But knowing MD is difficult Other options (from carbon tax paper): Calibrate tax path to hit specified emissions targets (e.g. 2 o warming) Choose a level that is politically feasible that can be adjusted later. Although we also might not know about MAC, taxes may help us learn about the MAC of firms. They will choose to pay the tax when tax < MAC. Thus, while we might not be able to determine where MD=MAC, we can get a cost-effective allocation of abatement for a given target without needing to know MAC

8 3. Are their ancillary policy goals? Taxes are not enacted in a policy vacuum. Multiple goals often conflict. For example, exports are exempt from the ozone depletion tax, so that US exports are not at a disadvantage compared to products from countries without the tax. This conflicts with environmental goals. Environmentally, CFC is a global pollutant, so where the CFC is shouldn t matter. Common conflict: revenue vs. abatement Taxes are a source of revenue. If an environmental tax is successful, it lowers emissions, thus lowering the tax base. Therefore, if revenues are important, we might adjust the rate. What should be done with the revenue? Some economists have argued that these taxes not only help the environment, but that they also improve economic efficiency. The double-dividend hypothesis the idea that the revenues from environmental taxes could be used to lower other taxes, thus providing an additional gain for the economy. Most taxes cause distortions in the economy. However, environmental taxes correct a distortion. Since the revenues from environmental taxes can be used to lower other taxes, the economy benefits.

9 There are two versions: Weak double dividend: there is a welfare gain from using the revenue raised to lower other taxes Not controversial Strong double dividend: environmental taxes reduce the overall distortionary effects of taxation Implies a no regrets policy we re better off even if the environmental benefits are zero This is more controversial. Most economists have not found evidence of such benefits. The problem is that environmental taxes have two effects: Revenue effect the taxes raise additional revenue that can be used to cut other distortionary taxes. This increases welfare. Interdependency effect the increased taxes distort other markets (primarily the labor market). This reduces welfare. For example, Marron et al. note that a carbon tax would reduce profits and thus taxes from firms. The problem is that the tax base of environmental taxes is small. Thus, they raise little revenue relative to larger taxes such as income taxes. As a result, the benefits of reducing other tax rates are small.

10 III. Examples Environmental tax examples o British Columbia enacted a carbon tax in 2008 Covers GHG from fossil fuels Exemptions for greenhouse growers established in 2012 over concerns they were uncompetitive with California and Mexico Covers 70-75% of BC GHG emissions Tax rate started at $10 Canadian, reached $30 Canadian in 2012 Effect on emissions Studies suggest roughly 5-15% reduction in emissions Effect on growth Compared to other provinces, no negative effect on BC growth rates Use of revenues Revenue-neutral BC Ministry of Finance must file an annual report showing how revenues are used. The report is reviewed by the BC legislature. At first, most revenue lowered corporate and personal income taxes More recently, revenue goes to targeted tax cuts in particular sectors (including motion pictures!) Thus, it is becoming more political o Overall, most environmental taxes focus on air pollution, particularly energy consumption About 2/3 of revenues from environmental taxes come from fuel taxes But, in many countries, are more like a user fee than a Pigouvian tax. The federal gas tax is essentially a user fee, since revenues go into the Highway Trust Fund Reducing pollution is not a goal of the federal gas tax. Parry (2014) shows that taxes in many countries below the level needed to cover social costs Exceptions include Brazil, Germany, Israel, UK o Vehicle taxes in some countries consider environmental impact Vehicle taxes in Norway depend on a vehicle s CO2 emissions per km, weight, and engine power o U.S. tax on ozone-depleting chemicals Passed in 1989 to eliminate chlorofluorocarbons (CFCs) following the Montreal Protocol Production of CFCs is taxed per pound. The tax rate increases over time

11 Examples of subsidies in U.S. o Brownfield development grants (also include changes in liability law) o Tax credits for alternative fuels Hybrid vehicles Residential solar o Income tax credits for easements in Colorado Income tax credits are available for 50% of the fair-market value of the easement, up to $375,000. For those with less taxable income, such as ranchers, there are two options: If there is a budget surplus, the credit is refundable. If there is no surplus, the credits can be sold to buyers who have more taxable income. The credits sell for cents per dollar of credit. There is little regulation of the valuation of easements Some transactions have been found to be fraudulent Colorado doesn't audit the credits. This is left to the Internal Revenue Service. Impact Total acres protected: 2000: 350, : almost 1 million Cost to government in lost revenue: 2001: $2.3 million 2005: $85.1 million Proponents argue that, despite lost tax revenue, the preserved open space raises the value of neighboring land. o Note that all these subsidies have a cost: there is lost tax revenue.

Introduction. Introduction. Pollution: A Negative Externality. Introduction. In this chapter, look for the answers to these questions: Externalities

Externalities P R I N C I P L E S O F MICROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 7 update 8 Thomson South-Western, all rights reserved In this chapter, look

Externalities P R I N C I P L E S O F MICROECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 7 update 8 Thomson South-Western, all rights reserved In this chapter, look

GHG EMISSIONS TAX RATIONALE AND DESIGN ELEMENTS GRZEGORZ PESZKO, LEAD ECONOMIST, WORLD BANK

GHG EMISSIONS TAX RATIONALE AND DESIGN ELEMENTS GRZEGORZ PESZKO, LEAD ECONOMIST, WORLD BANK Carbon taxes often higher then ETS prices Source: World Bank, State and Trends of carbon Pricing 2015 2 Tax on

GHG EMISSIONS TAX RATIONALE AND DESIGN ELEMENTS GRZEGORZ PESZKO, LEAD ECONOMIST, WORLD BANK Carbon taxes often higher then ETS prices Source: World Bank, State and Trends of carbon Pricing 2015 2 Tax on

Environmental taxes: economic principles and the UK experience

Environmental taxes: economic principles and the UK experience Andrew Leicester 25 th September 2012 Energy and Environmental Taxation Workshop, Deusto University Organised by Economics for Energy and

Environmental taxes: economic principles and the UK experience Andrew Leicester 25 th September 2012 Energy and Environmental Taxation Workshop, Deusto University Organised by Economics for Energy and

IS BRITISH COLUMBIA S CARBON TAX GOOD FOR HOUSEHOLD INCOME? WORKING PAPER

IS BRITISH COLUMBIA S CARBON TAX GOOD FOR HOUSEHOLD INCOME? WORKING PAPER July 2013 Authors Noel Melton Jotham Peters Navius Research Inc. Vancouver/Toronto Is British Columbia's Carbon Tax Good for Household

IS BRITISH COLUMBIA S CARBON TAX GOOD FOR HOUSEHOLD INCOME? WORKING PAPER July 2013 Authors Noel Melton Jotham Peters Navius Research Inc. Vancouver/Toronto Is British Columbia's Carbon Tax Good for Household

MARKET FAILURE 1: EXTERNALITIES. BUS111 MICROECONOMICS Lecture 8

MARKET FAILURE 1: EXTERNALITIES BUS111 MICROECONOMICS Lecture 8 Examples Externalities When I drive to work I cause congestion for all the other road-users When my neighbours paint their house, I enjoy

MARKET FAILURE 1: EXTERNALITIES BUS111 MICROECONOMICS Lecture 8 Examples Externalities When I drive to work I cause congestion for all the other road-users When my neighbours paint their house, I enjoy

Economic Impact Analysis: Washington s Initiative 732

1 Page September 12, 2016 Economic Impact Analysis: Washington s Initiative 732 Executive Summary Introduction Washington s Initiative 732 (I-732) will be on the ballot this November for Washington voters.

1 Page September 12, 2016 Economic Impact Analysis: Washington s Initiative 732 Executive Summary Introduction Washington s Initiative 732 (I-732) will be on the ballot this November for Washington voters.

The Case for Carbon Pricing. Naomi Oreskes 21 September 2017

The Case for Carbon Pricing Naomi Oreskes 21 September 2017 The basic argument: Pay for pollution; Pollution is a cost, but the free market does not recognize that cost; It is external to the marketplace.

The Case for Carbon Pricing Naomi Oreskes 21 September 2017 The basic argument: Pay for pollution; Pollution is a cost, but the free market does not recognize that cost; It is external to the marketplace.

New Study Shows that Returning Carbon Revenues Directly to Households would be Net Financially Positive for the Vast Majority of Households

Carbon Dividends Would Benefit Canadian Families New Study Shows that Returning Carbon Revenues Directly to Households would be Net Financially Positive for the Vast Majority of Households September 24,

Carbon Dividends Would Benefit Canadian Families New Study Shows that Returning Carbon Revenues Directly to Households would be Net Financially Positive for the Vast Majority of Households September 24,

Average Global Temperature,

5 C H A P T E R 5 E X T E R N A L I T I E S : P R O B L E M S A N D S O L U T I O N S Average Global Temperature, 1880 2011 Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright 2012

5 C H A P T E R 5 E X T E R N A L I T I E S : P R O B L E M S A N D S O L U T I O N S Average Global Temperature, 1880 2011 Public Finance and Public Policy Jonathan Gruber Fourth Edition Copyright 2012

H.R American Clean Energy and Security Act of 2009

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE June 5, 2009 H.R. 2454 American Clean Energy and Security Act of 2009 As ordered reported by the House Committee on Energy and Commerce on May 21, 2009 SUMMARY

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE June 5, 2009 H.R. 2454 American Clean Energy and Security Act of 2009 As ordered reported by the House Committee on Energy and Commerce on May 21, 2009 SUMMARY

Microeconomics. The Design of the Tax System. Introduction. In this chapter, look for the answers to these questions: N.

C H A P T E R 12 The Design of the Tax System P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

C H A P T E R 12 The Design of the Tax System P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of Cengage Learning, all rights

Economics 4315/7315: Public Economics

Saku Aura Department of Economics - University of Missouri 1 / 36 Externalities: An effect of an agent s action to another agent s outcome agent={firm, consumer} outcome={profit,utility} 2 / 36 Pecuniary

Saku Aura Department of Economics - University of Missouri 1 / 36 Externalities: An effect of an agent s action to another agent s outcome agent={firm, consumer} outcome={profit,utility} 2 / 36 Pecuniary

Does a carbon policy really burden low-income families?

Climate Change Policy Inititative April 20, 2017 Does a carbon policy really burden low-income families? Don Fullerton, Gutsgell Professor, Department of Finance, University of Illinois at Urbana-Champaign

Climate Change Policy Inititative April 20, 2017 Does a carbon policy really burden low-income families? Don Fullerton, Gutsgell Professor, Department of Finance, University of Illinois at Urbana-Champaign

2. Constitutional principles or rules with influence on the legislative procedure regarding non-fiscal purposed tax rules

Taxation for non-fiscal purposes By Anne Gro Enger 1 1. Introduction Taxation is most of all connected to the idea of providing revenue, but is actually composed by two main purposes: taxation for fiscal

Taxation for non-fiscal purposes By Anne Gro Enger 1 1. Introduction Taxation is most of all connected to the idea of providing revenue, but is actually composed by two main purposes: taxation for fiscal

NBER WORKING PAPER SERIES TWO GENERALIZATIONS OF A DEPOSIT-REFUND SYSTEM. Don Fullerton Ann Wolverton

NBER WORKING PAPER SERIES TWO GENERALIZATIONS OF A DEPOSIT-REFUND SYSTEM Don Fullerton Ann Wolverton Working Paper 7505 http://www.nber.org/papers/w7505 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES TWO GENERALIZATIONS OF A DEPOSIT-REFUND SYSTEM Don Fullerton Ann Wolverton Working Paper 7505 http://www.nber.org/papers/w7505 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

Microeconomics. Externalities. Introduction. N. Gregory Mankiw. In this chapter, look for the answers to these questions:

C H A P T E R 10 Externalities P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of CengageLearning, all rights reserved 2010

C H A P T E R 10 Externalities P R I N C I P L E S O F Microeconomics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 2010 South-Western, a part of CengageLearning, all rights reserved 2010

Carbon taxation an instrument for developing countries to raise revenues and support national climate policies

Distr.: General 30 March 2017 Original: English Committee of Experts on International Cooperation in Tax Matters Fourteenth Session New York, 03-06April 2017 Agenda item 3 (b) (vi) Environmental Tax Issues

Distr.: General 30 March 2017 Original: English Committee of Experts on International Cooperation in Tax Matters Fourteenth Session New York, 03-06April 2017 Agenda item 3 (b) (vi) Environmental Tax Issues

CARBON FORESTRY OVERVIEW

CARBON FORESTRY OVERVIEW Alaska SAF Carbon Conference April 13, 2018 Julius Pasay Forest and Grassland Asset Manager Presentation Outline About The Climate Trust Carbon Markets Forest Carbon Investments

CARBON FORESTRY OVERVIEW Alaska SAF Carbon Conference April 13, 2018 Julius Pasay Forest and Grassland Asset Manager Presentation Outline About The Climate Trust Carbon Markets Forest Carbon Investments

14.41 Final Exam Jonathan Gruber. True/False/Uncertain (95% of credit based on explanation; 5 minutes each)

") 14.41 Final Exam Jonathan Gruber True/False/Uncertain (95% of credit based on explanation; 5 minutes each) 1) The definition of property rights will eliminate the problem of externalities. Uncertain. Also

14.41 Final Exam Jonathan Gruber True/False/Uncertain (95% of credit based on explanation; 5 minutes each) 1) The definition of property rights will eliminate the problem of externalities. Uncertain. Also

An Analysis of Impacts on Households at Different Income Levels from Carbon Pollution Pricing in Maryland

An Analysis of Impacts on Households at Different Income Levels from Carbon Pollution Pricing in Maryland Marc Breslow, Ph.D., Policy & Research Director, Climate XChange Chynna Pickens, Climate XChange

An Analysis of Impacts on Households at Different Income Levels from Carbon Pollution Pricing in Maryland Marc Breslow, Ph.D., Policy & Research Director, Climate XChange Chynna Pickens, Climate XChange

Economics Sixth Edition

N. Gregory Mankiw Principles of Economics Sixth Edition 10 Externalities Premium PowerPoint Slides by Ron Cronovich In this chapter, look for the answers to these questions: What is an externality? Why

N. Gregory Mankiw Principles of Economics Sixth Edition 10 Externalities Premium PowerPoint Slides by Ron Cronovich In this chapter, look for the answers to these questions: What is an externality? Why

The Benefits of a Carbon Tax Swedish experiences and a focus on developing countries

1 The Benefits of a Carbon Tax Swedish experiences and a focus on developing countries Susanne Åkerfeldt Senior Advisor Ministry of Finance, Sweden susanne.akerfeldt@gov.se +46 8 405 1382; +46 70 681 25

1 The Benefits of a Carbon Tax Swedish experiences and a focus on developing countries Susanne Åkerfeldt Senior Advisor Ministry of Finance, Sweden susanne.akerfeldt@gov.se +46 8 405 1382; +46 70 681 25

SENATE COMMITTEE ON APPROPRIATIONS Senator Ricardo Lara, Chair Regular Session

SENATE COMMITTEE ON APPROPRIATIONS Senator Ricardo Lara, Chair 2017-2018 Regular Session AB 398 (Eduardo Garcia) - California Global Warming Solutions Act of 2006: market-based compliance mechanisms: fire

SENATE COMMITTEE ON APPROPRIATIONS Senator Ricardo Lara, Chair 2017-2018 Regular Session AB 398 (Eduardo Garcia) - California Global Warming Solutions Act of 2006: market-based compliance mechanisms: fire

Economics 230a, Fall 2014 Lecture Note 7: Externalities, the Marginal Cost of Public Funds, and Imperfect Competition

Economics 230a, Fall 2014 Lecture Note 7: Externalities, the Marginal Cost of Public Funds, and Imperfect Competition We have seen that some approaches to dealing with externalities (for example, taxes

Economics 230a, Fall 2014 Lecture Note 7: Externalities, the Marginal Cost of Public Funds, and Imperfect Competition We have seen that some approaches to dealing with externalities (for example, taxes

ASSEMBLY BILL No. 1341

california legislature 2017 18 regular session ASSEMBLY BILL No. 1341 Introduced by Assembly Member Calderon February 17, 2017 An act to add Section 44258.6 to the Health and Safety Code, and to amend

california legislature 2017 18 regular session ASSEMBLY BILL No. 1341 Introduced by Assembly Member Calderon February 17, 2017 An act to add Section 44258.6 to the Health and Safety Code, and to amend

Deep Dive into Policy Instruments Emissions Trading Schemes. Pablo Benitez, PhD World Bank Hanoi, Vietnam March 14, 2014

Deep Dive into Policy Instruments Emissions Trading Schemes Pablo Benitez, PhD World Bank Hanoi, Vietnam March 14, 2014 bout this Lesson In this lesson, you will review: n overview of emissions trading

Deep Dive into Policy Instruments Emissions Trading Schemes Pablo Benitez, PhD World Bank Hanoi, Vietnam March 14, 2014 bout this Lesson In this lesson, you will review: n overview of emissions trading

By Eduardo Porter. ENERGY &

ENERGY & ENVIRONME&MJtNt\ttU.ork@timeJJ '~.. " ~")&( ECONOMIC SCENE '"'""''-'~'-Co '"-'""' ""0"'""'-'W-

ENERGY & ENVIRONME&MJtNt\ttU.ork@timeJJ '~.. " ~")&( ECONOMIC SCENE '"'""''-'~'-Co '"-'""' ""0"'""'-'W-

Carbon Tax a Good Idea for Developing Countries?

1 Carbon Tax a Good Idea for Developing Countries? Susanne Åkerfeldt Senior Advisor Ministry of Finance, Sweden susanne.akerfeldt@gov.se +46 8 405 1382 Presentation at the 13 th Session of The United Nations

1 Carbon Tax a Good Idea for Developing Countries? Susanne Åkerfeldt Senior Advisor Ministry of Finance, Sweden susanne.akerfeldt@gov.se +46 8 405 1382 Presentation at the 13 th Session of The United Nations

Green Taxation: a contribution to sustainability

Green Taxation: a contribution to sustainability The European Semester and Green Tax Reforms (environmental taxation and the removal of environmental Harmful subsidies) - a Contribution to the wider fiscal

Green Taxation: a contribution to sustainability The European Semester and Green Tax Reforms (environmental taxation and the removal of environmental Harmful subsidies) - a Contribution to the wider fiscal

The Clean Technology Fund. U.S. Treasury Department. June 2008

The Clean Technology Fund U.S. Treasury Department June 2008 Clean Technology Fund Overview Why What Who How much How When 1 Why? By 2030, 80% of GHG emission growth is expected to come from non-oecd countries,

The Clean Technology Fund U.S. Treasury Department June 2008 Clean Technology Fund Overview Why What Who How much How When 1 Why? By 2030, 80% of GHG emission growth is expected to come from non-oecd countries,

A broad-based charge on fossil fuels, or carbon tax, payable by fuel producers and distributors; and

2018 Issue No. 2 18 January 2018 Tax Alert Canada Canada releases federal carbon tax pricing proposals EY Tax Alerts cover significant tax news, developments and changes in legislation that affect Canadian

2018 Issue No. 2 18 January 2018 Tax Alert Canada Canada releases federal carbon tax pricing proposals EY Tax Alerts cover significant tax news, developments and changes in legislation that affect Canadian

General Certificate of Education Advanced Level Examination June 2012

General Certificate of Education Advanced Level Examination June 2012 Economics ECON3 Unit 3 Business Economics and the Distribution of Income Tuesday 12 June 2012 1.30 pm to 3.30 pm For this paper you

General Certificate of Education Advanced Level Examination June 2012 Economics ECON3 Unit 3 Business Economics and the Distribution of Income Tuesday 12 June 2012 1.30 pm to 3.30 pm For this paper you

8. Market-Based Instruments Emission Fees and Tradeable Emission Permits

8. Market-Based Instruments Emission Fees and Tradeable Emission Permits 8.1 Introduction Recall that cost-effective implementation of a given aggregate emission target requires that marginal abatement

8. Market-Based Instruments Emission Fees and Tradeable Emission Permits 8.1 Introduction Recall that cost-effective implementation of a given aggregate emission target requires that marginal abatement

Earmarking Environmental Taxes. The U.S. Experience

Earmarking Environmental Taxes The U.S. Experience Daniel Hemel March 4, 2016 The Promise of Pigouvian Taxes Tax = marginal social cost of emissions can efficient level of pollution The Problem with Pigouvian

Earmarking Environmental Taxes The U.S. Experience Daniel Hemel March 4, 2016 The Promise of Pigouvian Taxes Tax = marginal social cost of emissions can efficient level of pollution The Problem with Pigouvian

Economics. Introduction. Introduction. Examples of Negative Externalities. Recap of Welfare Economics. Premium PowerPoint Slides by Ron Cronovich

C H A T E R In this chapter, look for the answers to these questions: E Externalities RINCILE OF Economics I N. Gregory Mankiw remium oweroint lides by Ron Cronovich 9 outh-western, a part of Cengage Learning,

C H A T E R In this chapter, look for the answers to these questions: E Externalities RINCILE OF Economics I N. Gregory Mankiw remium oweroint lides by Ron Cronovich 9 outh-western, a part of Cengage Learning,

SOPAAN April-Sept. :2014. Green Tax in India

Green Tax in India Ms. Manisha Gaur Assistant Professor Post Graduate Govt. College Sector-46, Chandigarh Abstract Tax imposed on the public has two reasons, one is to generate revenue for the Govt. and

Green Tax in India Ms. Manisha Gaur Assistant Professor Post Graduate Govt. College Sector-46, Chandigarh Abstract Tax imposed on the public has two reasons, one is to generate revenue for the Govt. and

Introduction to Green Tax & Budget Reform (GTBR)

") Introduction to Green Tax & Budget Reform (GTBR) Green Growth: A Path to Good Governance By Ian Barnes Environment and Development Division United Nations Economic and Social Commission for Asia and the

Introduction to Green Tax & Budget Reform (GTBR) Green Growth: A Path to Good Governance By Ian Barnes Environment and Development Division United Nations Economic and Social Commission for Asia and the

The Double Dividend: Fact or Fallacy?

Andrea Garnero Master PPD - Paris School of Economics March 31 th 2010 1 2 First approaches More recent approaches 3 Some calibrations for France Other countries 4 1 2 First approaches More recent approaches

Andrea Garnero Master PPD - Paris School of Economics March 31 th 2010 1 2 First approaches More recent approaches 3 Some calibrations for France Other countries 4 1 2 First approaches More recent approaches

OVERVIEW PRELIMINARY DRAFT REGULATION FOR A CALIFORNIA CAP-AND-TRADE PROGRAM - FOR PUBLIC REVIEW AND COMMENT - November 24, 2009

OVERVIEW PRELIMINARY DRAFT REGULATION FOR A CALIFORNIA CAP-AND-TRADE PROGRAM - - November 24, 2009 CALIFORNIA CAP ON GREENHOUSE GAS EMISSIONS AND MARKET-BASED COMPLIANCE MECHANISMS IN ACCORDANCE WITH CALIFORNIA

OVERVIEW PRELIMINARY DRAFT REGULATION FOR A CALIFORNIA CAP-AND-TRADE PROGRAM - - November 24, 2009 CALIFORNIA CAP ON GREENHOUSE GAS EMISSIONS AND MARKET-BASED COMPLIANCE MECHANISMS IN ACCORDANCE WITH CALIFORNIA

Chapter 14: Taxes and Government Spending Section 1

Chapter 14: Taxes and Government Spending Section 1 Objectives 1. Identify the sources of the government s authority to tax. 2. Describe types of tax bases and tax structures. 3. List the characteristics

Chapter 14: Taxes and Government Spending Section 1 Objectives 1. Identify the sources of the government s authority to tax. 2. Describe types of tax bases and tax structures. 3. List the characteristics

Economics. Interdependence and the Gains from Trade. Interdependence. In this chapter, look for the answers to these questions: N.

C H A P T E R 3 Interdependence and the Gains from Trade P R I N C I P L E S O F Economics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 29 South-Western, a part of Cengage Learning, all

C H A P T E R 3 Interdependence and the Gains from Trade P R I N C I P L E S O F Economics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich 29 South-Western, a part of Cengage Learning, all

GHG EMISSIONS TRADING SYSTEMS RATIONALE AND DESIGN ELEMENTS GRZEGORZ PESZKO, LEAD ECONOMIST, WORLD BANK

GHG EMISSIONS TRADING SYSTEMS RATIONALE AND DESIGN ELEMENTS GRZEGORZ PESZKO, LEAD ECONOMIST, WORLD BANK Emission trading systems: definition and rationale Regulation where the government establishes a

GHG EMISSIONS TRADING SYSTEMS RATIONALE AND DESIGN ELEMENTS GRZEGORZ PESZKO, LEAD ECONOMIST, WORLD BANK Emission trading systems: definition and rationale Regulation where the government establishes a

The Benefits of a Carbon Tax Swedish experiences and a focus on developing countries

The Benefits of a Carbon Tax Swedish experiences and a focus on developing countries 1 Why is a Carbon Tax Important Now? Tax Base Protection for Developing Countries Huge challenges Increased revenues

The Benefits of a Carbon Tax Swedish experiences and a focus on developing countries 1 Why is a Carbon Tax Important Now? Tax Base Protection for Developing Countries Huge challenges Increased revenues

Discounting the Benefits of Climate Change Policies Using Uncertain Rates

Discounting the Benefits of Climate Change Policies Using Uncertain Rates Richard Newell and William Pizer Evaluating environmental policies, such as the mitigation of greenhouse gases, frequently requires

Discounting the Benefits of Climate Change Policies Using Uncertain Rates Richard Newell and William Pizer Evaluating environmental policies, such as the mitigation of greenhouse gases, frequently requires

ECON 1001 B. Come to the PASS workshop with your mock exam complete. During the workshop you can work with other students to review your work.

It is most beneficial to you to write this mock midterm UNDER EXAM CONDITIONS. This means: Complete the midterm in _1.5 hour(s). Work on your own. Keep your notes and textbook closed. Attempt every question.

It is most beneficial to you to write this mock midterm UNDER EXAM CONDITIONS. This means: Complete the midterm in _1.5 hour(s). Work on your own. Keep your notes and textbook closed. Attempt every question.

FAQ - Environmental Pollution Tax Law in Viet Nam -

What are the taxed objects and planned tax rates? Viet Nam seeks to implement tax on the following commodities: Refined fuels (gasoline, diesel, mazut, paraffin, kerosene) Coal Hdrochlorofluorocarbon (HCFC)

What are the taxed objects and planned tax rates? Viet Nam seeks to implement tax on the following commodities: Refined fuels (gasoline, diesel, mazut, paraffin, kerosene) Coal Hdrochlorofluorocarbon (HCFC)

The Private Provision of International Impure Public Goods: the Case of Climate Policy

The Private Provision of International Impure Public Goods: the Case of Climate Policy Martin Altemeyer-Bartscher Dirk T.G. Rübbelke Anil Markandya September 2010 Preliminary Version Please do not cite

The Private Provision of International Impure Public Goods: the Case of Climate Policy Martin Altemeyer-Bartscher Dirk T.G. Rübbelke Anil Markandya September 2010 Preliminary Version Please do not cite

Cost Containment through Offsets in the Cap-and-Trade Program under California s Global Warming Solutions Act 1 July 2011

Cost Containment through Offsets in the Cap-and-Trade Program under California s Global Warming Solutions Act 1 July 2011 This document outlines the results of the economic modeling performed by the Environmental

Cost Containment through Offsets in the Cap-and-Trade Program under California s Global Warming Solutions Act 1 July 2011 This document outlines the results of the economic modeling performed by the Environmental

Environmental taxation and the double dividend

International Society for Ecological Economics Internet Encyclopaedia of Ecological Economics Environmental taxation and the double dividend William K. Jaeger February 2003 I. Introduction Environmental

International Society for Ecological Economics Internet Encyclopaedia of Ecological Economics Environmental taxation and the double dividend William K. Jaeger February 2003 I. Introduction Environmental

Coversheet: Tax and the environment Paper I: Frameworks

Coversheet: Tax and the environment Paper I: Frameworks Background Paper for Session 8 of the Tax Working Group April 2018 Purpose of discussion This paper: introduces potential frameworks for using taxes

Coversheet: Tax and the environment Paper I: Frameworks Background Paper for Session 8 of the Tax Working Group April 2018 Purpose of discussion This paper: introduces potential frameworks for using taxes

After Fukushima: A New Role for Energy Taxes in Switzerland

After Fukushima: A New Role for Energy Taxes in Switzerland Dr. Pierre-Alain Bruchez Economic Analysis and Policy Advice, Swiss Federal Finance Administration Economic Policy Seminar University of Lausanne,

After Fukushima: A New Role for Energy Taxes in Switzerland Dr. Pierre-Alain Bruchez Economic Analysis and Policy Advice, Swiss Federal Finance Administration Economic Policy Seminar University of Lausanne,

Environmental Economic Theory No. 11 (8 January 2019)

") Professional Career Program Environmental Economic Theory No. 11 (8 January 2019) Chapter 12. Incentive-based strategies: Transferable Discharge Permits Instructor: Eiji HOSODA Textbook: Barry.C. Field

Professional Career Program Environmental Economic Theory No. 11 (8 January 2019) Chapter 12. Incentive-based strategies: Transferable Discharge Permits Instructor: Eiji HOSODA Textbook: Barry.C. Field

Road pricing, company cars and the mobility budget. Bruno De Borger University of Antwerp and KULeuven

Road pricing, company cars and the mobility budget Bruno De Borger University of Antwerp and KULeuven 1. Introduction: a policy package to improve mobility Transport and mobility have huge benefits to

Road pricing, company cars and the mobility budget Bruno De Borger University of Antwerp and KULeuven 1. Introduction: a policy package to improve mobility Transport and mobility have huge benefits to

WG5/6 Sub-Working. EU Emissions Trading Scheme - Auctioning Proceeds

WG5/6 Sub-Working EU Emissions Trading Scheme - Auctioning Proceeds Introduction of Paper Under the current EU Emissions Trading Directive, Member States are required to submit a National Allocation Plan

WG5/6 Sub-Working EU Emissions Trading Scheme - Auctioning Proceeds Introduction of Paper Under the current EU Emissions Trading Directive, Member States are required to submit a National Allocation Plan

Fossil-fuel subsidy reform in Mexico. Green Growth & Sustainable Development Forum

Fossil-fuel subsidy reform in Mexico Green Growth & Sustainable Development Forum November 2014 1 14 Retail Prices in Mexico do not accurately follow international prices (USA). Mexico and USA regular

Fossil-fuel subsidy reform in Mexico Green Growth & Sustainable Development Forum November 2014 1 14 Retail Prices in Mexico do not accurately follow international prices (USA). Mexico and USA regular

Externalities: Problems and Solutions

5.1 Externality Theory Externalities: Problems and Solutions 5.2 Private-Sector Solutions to Negative Externalities 5.3 Public-Sector Remedies for Externalities 5.4 Distinctions between Price and Quantity

5.1 Externality Theory Externalities: Problems and Solutions 5.2 Private-Sector Solutions to Negative Externalities 5.3 Public-Sector Remedies for Externalities 5.4 Distinctions between Price and Quantity

Carbon Dividends Would Benefit New Brunswick Families. October 17th Study: Carbon Dividends would benefit Canadian families

Carbon Dividends Would Benefit New Brunswick Families New Study Shows that Returning Carbon Revenues Directly to New Brunswick Households would be Net Financially Positive for the Vast Majority of Households

Carbon Dividends Would Benefit New Brunswick Families New Study Shows that Returning Carbon Revenues Directly to New Brunswick Households would be Net Financially Positive for the Vast Majority of Households

Economics. Interdependence. Interdependence. Production Possibilities in the U.S.

9/17/21 C H A P T E R 3 Interdependence and the Gains from Trade P R I N C I P L E S O F Economics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich Modified by Joseph Tao-yi Wang 21 South-Western,

9/17/21 C H A P T E R 3 Interdependence and the Gains from Trade P R I N C I P L E S O F Economics N. Gregory Mankiw Premium PowerPoint Slides by Ron Cronovich Modified by Joseph Tao-yi Wang 21 South-Western,

The Recent Development of Diverse Energy Taxation Bills in Taiwan: A Comparative Study

The Recent Development of Diverse Energy Taxation Bills in Taiwan: A Comparative Study Anton Ming-Zhi Gao 1 antongao@mx.nthu.edu.tw Assistant Professor, Institute of Law for Science and Technology (ILST),

The Recent Development of Diverse Energy Taxation Bills in Taiwan: A Comparative Study Anton Ming-Zhi Gao 1 antongao@mx.nthu.edu.tw Assistant Professor, Institute of Law for Science and Technology (ILST),

Review: Final Challenge Environmental Economics: ECO 345 Fall 2009

Review: Final Challenge Environmental Economics: ECO 345 Fall 2009 The following questions review only the class notes since the last homework. The formulas provided below will also be provided on the

Review: Final Challenge Environmental Economics: ECO 345 Fall 2009 The following questions review only the class notes since the last homework. The formulas provided below will also be provided on the

Externalities and Public Goods (Chp.-5 and Chp.-6) Part-2

Part-2") Externalities and Public Goods (Chp.-5 and Chp.-6) Part-2 Previous Lecture Negative Externalities Production Consumer Positive Externalities Production Consumer Solutions Private Negotiations (Coasian)

Externalities and Public Goods (Chp.-5 and Chp.-6) Part-2 Previous Lecture Negative Externalities Production Consumer Positive Externalities Production Consumer Solutions Private Negotiations (Coasian)

Northwest Economic Research Center College of Urban and Public Affairs. Carbon Tax Analysis for Oregon August 2014

Northwest Economic Research Center College of Urban and Public Affairs Carbon Tax Analysis for Oregon August 2014 Objectives 1. Carbon tax level & tax base 2. Evaluate economic impacts on various sectors

Northwest Economic Research Center College of Urban and Public Affairs Carbon Tax Analysis for Oregon August 2014 Objectives 1. Carbon tax level & tax base 2. Evaluate economic impacts on various sectors

Macroeconomic Theory and Policy

ECO 209Y Macroeconomic Theory and Policy Lecture 2: National Income Accounting Gustavo Indart Slide1 Gross Domestic Product Gross Domestic Product (GDP) is the value of all final goods and services produced

ECO 209Y Macroeconomic Theory and Policy Lecture 2: National Income Accounting Gustavo Indart Slide1 Gross Domestic Product Gross Domestic Product (GDP) is the value of all final goods and services produced

Fact sheet: Financing climate change action Investment and financial flows for a strengthened response to climate change

Fact sheet: Financing climate change action Investment and financial flows for a strengthened response to climate change In 2007, a review entitled Report on the analysis of existing and potential investment

Fact sheet: Financing climate change action Investment and financial flows for a strengthened response to climate change In 2007, a review entitled Report on the analysis of existing and potential investment

Lecture 6. Economic Fluctuations and Unemployment

Lecture 6 Economic Fluctuations and Unemployment Growth and Fluctuations Growth and Fluctuations Growth and Fluctuations Growth and Fluctuations In 2002, economists calculated that the average British

Lecture 6 Economic Fluctuations and Unemployment Growth and Fluctuations Growth and Fluctuations Growth and Fluctuations Growth and Fluctuations In 2002, economists calculated that the average British

APPENDIX B: WHOLESALE AND RETAIL PRICE FORECAST

Seventh Northwest Conservation and Electric Power Plan APPENDIX B: WHOLESALE AND RETAIL PRICE FORECAST Contents Introduction... 3 Key Findings... 3 Background... 5 Methodology... 7 Inputs and Assumptions...

Seventh Northwest Conservation and Electric Power Plan APPENDIX B: WHOLESALE AND RETAIL PRICE FORECAST Contents Introduction... 3 Key Findings... 3 Background... 5 Methodology... 7 Inputs and Assumptions...

Response to UNFCCC Secretariat request for proposals on: Information on strategies and approaches for mobilizing scaled-up climate finance (COP)

") SustainUS September 2, 2013 Response to UNFCCC Secretariat request for proposals on: Information on strategies and approaches for mobilizing scaled-up climate finance (COP) Global Funding for adaptation

SustainUS September 2, 2013 Response to UNFCCC Secretariat request for proposals on: Information on strategies and approaches for mobilizing scaled-up climate finance (COP) Global Funding for adaptation

University of Victoria. Economics 325 Public Economics SOLUTIONS

University of Victoria Economics 325 Public Economics SOLUTIONS Martin Farnham Problem Set #5 Note: Answer each question as clearly and concisely as possible. Use of diagrams, where appropriate, is strongly

University of Victoria Economics 325 Public Economics SOLUTIONS Martin Farnham Problem Set #5 Note: Answer each question as clearly and concisely as possible. Use of diagrams, where appropriate, is strongly

SENATE DOCKET, NO FILED ON: 1/18/2019. SENATE... No. The Commonwealth of Massachusetts PRESENTED BY: Michael J. Barrett

SENATE DOCKET, NO. 1817 FILED ON: 1/18/2019 SENATE.............. No. The Commonwealth of Massachusetts PRESENTED BY: Michael J. Barrett To the Honorable Senate and House of Representatives of the Commonwealth

SENATE DOCKET, NO. 1817 FILED ON: 1/18/2019 SENATE.............. No. The Commonwealth of Massachusetts PRESENTED BY: Michael J. Barrett To the Honorable Senate and House of Representatives of the Commonwealth

Energy Policy and Tax Reform. Donald B. Marron * Director, Urban-Brookings Tax Policy Center

Energy Policy and Tax Reform Donald B. Marron * Director, Urban-Brookings Tax Policy Center www.taxpolicycenter.org Testimony before the Subcommittee on Select Revenue Measures and the Subcommittee on

Energy Policy and Tax Reform Donald B. Marron * Director, Urban-Brookings Tax Policy Center www.taxpolicycenter.org Testimony before the Subcommittee on Select Revenue Measures and the Subcommittee on

Benefits and Costs. Reilly, Kathleen

University of Michigan Deep Blue deepblue.lib.umich.edu 2016 Benefits and Costs Reilly, Kathleen Reilly, Kathleen (2016). "Benefits and Costs," Agora Journal of Urban Planning and Design, 88-95. http://hdl.handle.net/2027.42/120313

University of Michigan Deep Blue deepblue.lib.umich.edu 2016 Benefits and Costs Reilly, Kathleen Reilly, Kathleen (2016). "Benefits and Costs," Agora Journal of Urban Planning and Design, 88-95. http://hdl.handle.net/2027.42/120313

The Heterogeneous Effects of Gasoline Taxes: Why Where We Live Matters

The Heterogeneous Effects of Gasoline Taxes: Why Where We Live Matters Heather Stephens (West Virginia University) Elisheba Spiller (Environmental Defense Fund) Yong Chen (Oregon State University) 33RD

The Heterogeneous Effects of Gasoline Taxes: Why Where We Live Matters Heather Stephens (West Virginia University) Elisheba Spiller (Environmental Defense Fund) Yong Chen (Oregon State University) 33RD

Pricing Carbon in Oregon:

I S S U E B R I E F Pricing Carbon in Oregon: Carbon Offset Aggregation Jeremy Hunt Brian Kittler June 2018 Leadership in Conservation Thought, Policy and Action HIGHLIGHTS This brief offers a review of

I S S U E B R I E F Pricing Carbon in Oregon: Carbon Offset Aggregation Jeremy Hunt Brian Kittler June 2018 Leadership in Conservation Thought, Policy and Action HIGHLIGHTS This brief offers a review of

Sin-type taxes around the world

Sin-type taxes around the world Colleen Freeburg Global Director Indirect Taxes General Motors Company Tel: +1 313 667 0967 Email: colleen.freeburg@gm.com Jeff Smith Manager, Indirect Tax Pembina Pipeline

Sin-type taxes around the world Colleen Freeburg Global Director Indirect Taxes General Motors Company Tel: +1 313 667 0967 Email: colleen.freeburg@gm.com Jeff Smith Manager, Indirect Tax Pembina Pipeline

CRS Report for Congress Received through the CRS Web

Order Code RS20343 Updated January 10, 2002 CRS Report for Congress Received through the CRS Web Federal Excise Taxes on Tobacco Products: Rates and Revenues Louis Alan Talley Specialist in Taxation Government

Order Code RS20343 Updated January 10, 2002 CRS Report for Congress Received through the CRS Web Federal Excise Taxes on Tobacco Products: Rates and Revenues Louis Alan Talley Specialist in Taxation Government

ECON 460 Suggested Answers for Questions 7, 8, 10 and 11 Answer:

ECON 4 Suggested Answers for Questions 7, 8, 10 and 11 Suppose the government wishes to regulate mercury emissions of factories in a specific industry by either setting an emissions standard or imposing

ECON 4 Suggested Answers for Questions 7, 8, 10 and 11 Suppose the government wishes to regulate mercury emissions of factories in a specific industry by either setting an emissions standard or imposing

ENV/EPOC/WPNEP/T(2009)2/FINAL. Working Party on National Environmental Policies Working Group on Transport

2/FINAL. Working Party on National Environmental Policies Working Group on Transport") Unclassified ENV/EPOC/WPNEP/T(29)2/FINAL ENV/EPOC/WPNEP/T(29)2/FINAL Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 3-Sep-29

Unclassified ENV/EPOC/WPNEP/T(29)2/FINAL ENV/EPOC/WPNEP/T(29)2/FINAL Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 3-Sep-29

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION Stated in Canadian dollars

Questor Technology Inc. INDEPENDENT AUDITORS REPORT To the Shareholders of Questor Technology Inc.: We have audited the accompanying consolidated financial statements of Questor Technology Inc., which

Questor Technology Inc. INDEPENDENT AUDITORS REPORT To the Shareholders of Questor Technology Inc.: We have audited the accompanying consolidated financial statements of Questor Technology Inc., which

Oil Industry Tax and Deficit Issues

Robert Pirog Specialist in Energy Economics July 21, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 wwwcrsgov R40715 c11173008 Summary

Robert Pirog Specialist in Energy Economics July 21, 2009 Congressional Research Service CRS Report for Congress Prepared for Members and Committees of Congress 7-5700 wwwcrsgov R40715 c11173008 Summary

April 2016 Dale Beugin Richard Lipsey Christopher Ragan France St-Hilaire Vincent Thivierge

PROVINCIAL CARBON PRICING AND HOUSEHOLD FAIRNESS April 2016 Dale Beugin Richard Lipsey Christopher Ragan France St-Hilaire Vincent Thivierge ACKNOWLEDGMENTS We thank Jennifer Jones, Shawna Brown, and the

PROVINCIAL CARBON PRICING AND HOUSEHOLD FAIRNESS April 2016 Dale Beugin Richard Lipsey Christopher Ragan France St-Hilaire Vincent Thivierge ACKNOWLEDGMENTS We thank Jennifer Jones, Shawna Brown, and the

Expanding the Tax Base in Kenya: A Case for Innovation

Expanding the Tax Base in Kenya: A Case for Innovation Presentation by: Robert Waruiru Associate Director, KPMG Advisory Services Limited CCPA-K September 2017 TABLE OF CONTENTS Introduction Trends in

Expanding the Tax Base in Kenya: A Case for Innovation Presentation by: Robert Waruiru Associate Director, KPMG Advisory Services Limited CCPA-K September 2017 TABLE OF CONTENTS Introduction Trends in

CHAPTER 17. BE IT ENACTED by the Senate and General Assembly of the State of New Jersey:

CHAPTER 17 AN ACT concerning clean energy, amending and supplementing P.L.1999, c.23, amending P.L.2010, c.57, and supplementing P.L.2005, c.354 (C.34:1A-85 et seq.). BE IT ENACTED by the Senate and General

CHAPTER 17 AN ACT concerning clean energy, amending and supplementing P.L.1999, c.23, amending P.L.2010, c.57, and supplementing P.L.2005, c.354 (C.34:1A-85 et seq.). BE IT ENACTED by the Senate and General

Elements of a Trade and Climate Code

5 Elements of a Trade and Climate Code A Code of Good WTO Practice on Greenhouse Gas Emissions Controls should delineate a large green space for measures that are designed to limit greenhouse gas emissions

5 Elements of a Trade and Climate Code A Code of Good WTO Practice on Greenhouse Gas Emissions Controls should delineate a large green space for measures that are designed to limit greenhouse gas emissions

Using a Carbon Tax to Meet U.S. International Climate Pledges

Using a Carbon Tax to Meet U.S. International Climate Pledges Introduction and Motivation U.S. pledge in the Paris agreement Reduce greenhouse gas emissions by 26-28 percent, relative to 2005, by 2025

Using a Carbon Tax to Meet U.S. International Climate Pledges Introduction and Motivation U.S. pledge in the Paris agreement Reduce greenhouse gas emissions by 26-28 percent, relative to 2005, by 2025

Summary of California s Proposed Cap-and-Trade Regulations

Summary of California s Proposed Cap-and-Trade Regulations On October 28, 2010, the California Air Resources Board (ARB) released its proposed regulations for greenhouse gas cap-and-trade program. The

Summary of California s Proposed Cap-and-Trade Regulations On October 28, 2010, the California Air Resources Board (ARB) released its proposed regulations for greenhouse gas cap-and-trade program. The

Beyond a curmudgeonly few, there is little debate now on the efficiency case for levying user charges. Harry Clarke

Beyond a curmudgeonly few, there is little debate now on the efficiency case for levying user charges. Harry Clarke 1 Congestion charging: a curmudgeon s view Mark Harrison Roads, cars and taxes Crawford

Beyond a curmudgeonly few, there is little debate now on the efficiency case for levying user charges. Harry Clarke 1 Congestion charging: a curmudgeon s view Mark Harrison Roads, cars and taxes Crawford

Re: Clallam County PUD s opposition to carbon tax legislation (PUD letter attached)

") September 23, 2014 Board of Commissioners Clallam County PUD 2431 E. Highway 101 P.O. Box 1090 Port Angeles, WA 98362 Re: Clallam County PUD s opposition to carbon tax legislation (PUD letter attached)

September 23, 2014 Board of Commissioners Clallam County PUD 2431 E. Highway 101 P.O. Box 1090 Port Angeles, WA 98362 Re: Clallam County PUD s opposition to carbon tax legislation (PUD letter attached)

Lecture 12: Taxes. Session ID: DDEE. EC101 DD & EE / Manove Taxes & International Trade p 1. EC101 DD & EE / Manove Clicker Question p 2

Lecture 12: Taxes Session ID: DDEE Taxes & International Trade p 1 Clicker Question p 2 Summary of DWL from Price Controls When the distribution of income is very unequal, WTP is not a good measure of

Lecture 12: Taxes Session ID: DDEE Taxes & International Trade p 1 Clicker Question p 2 Summary of DWL from Price Controls When the distribution of income is very unequal, WTP is not a good measure of

Choose the single best answer for each question. Do all of your scratch work in the margins or on the back of the last page.

Econ 101, Section 21, S10, Schroeter Exam #3, Special code = 1 Choose the single best answer for each question. Do all of your scratch work in the margins or on the back of the last page. 1. For a country

Econ 101, Section 21, S10, Schroeter Exam #3, Special code = 1 Choose the single best answer for each question. Do all of your scratch work in the margins or on the back of the last page. 1. For a country

A U.S. Carbon Tax and the Earned Income Tax Credit: An Analysis of Potential Linkages

A U.S. Carbon Tax and the Earned Income Tax Credit: An Analysis of Potential Linkages Aparna Mathur and Adele C. Morris June 30, 2017 This paper examines, individually and jointly, an excise tax on carbon

A U.S. Carbon Tax and the Earned Income Tax Credit: An Analysis of Potential Linkages Aparna Mathur and Adele C. Morris June 30, 2017 This paper examines, individually and jointly, an excise tax on carbon

The Environment, Health, and Safety. Chapter 13. McGraw-Hill/Irwin. Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

The Environment, Health, and Safety Chapter 13 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Use economic analysis to show how U.S. health

The Environment, Health, and Safety Chapter 13 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Use economic analysis to show how U.S. health

The Environment, Health, and Safety. Chapter 13. Learning Objectives

The Environment, Health, and Safety Chapter 13 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Use economic analysis to show how U.S. health

The Environment, Health, and Safety Chapter 13 McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives 1. Use economic analysis to show how U.S. health

Interdependence. Interdependence and the Gains from Trade. In this chapter, look for the answers to these questions:

3 Interdependence and the Gains from Trade P R I N C I P L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 28 update 28 South-Western, a part of Cengage Learning,

3 Interdependence and the Gains from Trade P R I N C I P L E S O F ECONOMICS FOURTH EDITION N. GREGORY MANKIW Premium PowerPoint Slides by Ron Cronovich 28 update 28 South-Western, a part of Cengage Learning,

RGGI Program Review: REMI Modeling Results

RGGI Program Review: REMI Modeling Results Inputs and Draft Results from MRPS Case Run December 2017 Modeling Inputs 2 Overall Modeling Methodology Two broad set of inputs used to model the economic impacts

RGGI Program Review: REMI Modeling Results Inputs and Draft Results from MRPS Case Run December 2017 Modeling Inputs 2 Overall Modeling Methodology Two broad set of inputs used to model the economic impacts

Green Finance for Green Growth

2010/FMM/006 Agenda Item: Plenary 2 Green Finance for Green Growth Purpose: Information Submitted by: Korea 17 th Finance Ministers Meeting Kyoto, Japan 5-6 November 2010 EXECUTIVE SUMMARY Required Action/Decision

2010/FMM/006 Agenda Item: Plenary 2 Green Finance for Green Growth Purpose: Information Submitted by: Korea 17 th Finance Ministers Meeting Kyoto, Japan 5-6 November 2010 EXECUTIVE SUMMARY Required Action/Decision

Excise Tax 102. Energy & Environmental Taxes. Frank Boland Chief, CC:PSI:7

Excise Tax 102 Energy & Environmental Taxes January 21, 2011 Frank Boland Chief, CC:PSI:7 BA, TCU; JD, SMU IRS since 1977 Branch chief of excise tax branch in IRS Counsel since 2003 Principal author or

Excise Tax 102 Energy & Environmental Taxes January 21, 2011 Frank Boland Chief, CC:PSI:7 BA, TCU; JD, SMU IRS since 1977 Branch chief of excise tax branch in IRS Counsel since 2003 Principal author or

Independent Auditors Report

Independent Auditors Report To the Shareholders of Questor Technology Inc. We have audited the accompanying consolidated financial statements of Questor Technology Inc., which comprise the consolidated

Independent Auditors Report To the Shareholders of Questor Technology Inc. We have audited the accompanying consolidated financial statements of Questor Technology Inc., which comprise the consolidated

A N ENERGY ECONOMY I NTERAC TION MODEL FOR EGYPT

A N ENERGY ECONOMY I NTERAC TION MODEL FOR EGYPT RESULTS OF ALTERNATIVE PRICE REFORM SCENARIOS B Y MOTAZ KHORSHID Vice President of the British University in Egypt (BUE) Ex-Vice President of Cairo University

A N ENERGY ECONOMY I NTERAC TION MODEL FOR EGYPT RESULTS OF ALTERNATIVE PRICE REFORM SCENARIOS B Y MOTAZ KHORSHID Vice President of the British University in Egypt (BUE) Ex-Vice President of Cairo University

United Nations Environment Programme

UNITED NATIONS United Nations Environment Programme Distr. GENERAL UNEP/OzL.Pro/ExCom/64/44 15 June 2011 EP ORIGINAL: ENGLISH EXECUTIVE COMMITTEE OF THE MULTILATERAL FUND FOR THE IMPLEMENTATION OF THE

UNITED NATIONS United Nations Environment Programme Distr. GENERAL UNEP/OzL.Pro/ExCom/64/44 15 June 2011 EP ORIGINAL: ENGLISH EXECUTIVE COMMITTEE OF THE MULTILATERAL FUND FOR THE IMPLEMENTATION OF THE

NET FISCAL INCIDENCE AT THE REGIONAL LEVEL : A COMPUTABLE GENERAL EQUILIBRIUM MODEL WITH VOTING. Saloua Sehili

NET FISCAL INCIDENCE AT THE REGIONAL LEVEL : A COMPUTABLE GENERAL EQUILIBRIUM MODEL WITH VOTING Saloua Sehili FRP Report No. 20 September 1998 ACKNOWLEDGEMENTS This report is based on the author s dissertation:

NET FISCAL INCIDENCE AT THE REGIONAL LEVEL : A COMPUTABLE GENERAL EQUILIBRIUM MODEL WITH VOTING Saloua Sehili FRP Report No. 20 September 1998 ACKNOWLEDGEMENTS This report is based on the author s dissertation: