CONFLICTS OF INTEREST RELATED PARTIES RELATED PARTY TRANSACTIONS

|

|

|

- Amelia O’Neal’

- 5 years ago

- Views:

Transcription

1 CONFLICTS OF INTEREST RELATED PARTIES RELATED PARTY TRANSACTIONS

2 The problem Charity Trustees naturally bring with them to their position connections which can be of benefit to the charity Can lead to conflicts of interest or loyalty

3 Why is this an issue? Trustees have a legal duty to act only in the best interest of the charity Decisions not being made in the Charity s best interest Reputational damage Can be invalid or open to challenge Conflicts of interest are not a problem providing they are correctly and transparently addressed

4 Why is this an issue? Charity Commission see many cases of charities getting into difficulty because conflicts of interest were not addressed or were handled incorrectly Important to have in place robust systems

5 Who does this apply to? Trustees Senior management Someone able to engage charity in significant financial transactions

6 Three step process IDENTIFY PREVENT RECORD

7 IDENTIFY A conflict of interest is any situation in which a trustee s personal interests or loyalties could, or could be seen to, prevent the trustee from making a decision only in the best interests of the charity. There is a conflict of interest where there is a proposed transaction between the charity and a connected person of a trustee or senior person in the organisation. Similarly, there is a conflict of interest where there is a benefit or a potential benefit to a connected person

8 PREVENT Remove conflict of interest by not pursuing that action, undertaking it differently, not appointing trustee/trustee resignation Conflict of loyalty e.g. potential new trustee who is a trustee or is connected with another organisation operating in the same field / competing for funds etc.

9 PREVENT Follow law/governing document in respect of managing conflict In absence of governing document/legal provisions: require conflicted trustees to declare their interest at an early stage and, in most cases, withdraw from relevant meetings, discussions, decision making and votes consider updating their governing document to include provisions for dealing with conflicts of interest

10 PREVENT Exceptionally, need to seek the authority of the Commission where the conflict of interest is so acute or extensive that following these options will not allow the trustees to demonstrate that they have acted in the best interests of the charity

11 PREVENT Conflicts of interest often arise because a decision involves a potential trustee benefit. Trustee benefit must be properly authorised and the trustees must follow any conditions attached to the authority which say how the conflict of interest should be handled (legal requirements)

12 RECORD Trustees should formally record any conflicts of interest and how they were handled and must, if they prepare accruals accounts, disclose any trustee benefits in the charity s accounts

13 Examples of benefits to trustees Sell, loan or lease charity assets to a charity trustee acquire, borrow or lease assets from a trustee for the charity Pay a trustee for carrying out their trustee role Pay a trustee for carrying out a separate paid post within the charity, even if that trustee has recently resigned as a trustee Pay a trustee for carrying out a separate paid post as a director or employee of the charity s subsidiary trading company Pay a trustee, or a person or company closely connected to a trustee, for providing a service to the charity. This covers anything that would be regarded as a service and includes legal, accountancy or consultancy services through to painting or decorating the charity s premises, or any other maintenance work employ a trustee s spouse or other close relative at the charity (or at the charity s subsidiary trading company) Make a grant to a service user trustee, or a service user who is a close relative of a trustee Allow a service user trustee to influence service provision to their exclusive advantage

14 Good practice Include provisions in governing document to deal with conflicts of interest Conflicts of interest policy and register of interests Ensuring that meetings include an item to declare potential conflicts at the start and have it minuted Transparency public availability of register Pre-appointment issue for new trustees

15 RELATED PARTY TRANSACTION A related party transaction is a financial transaction between the related party and the charity. A related party transaction involves the transfer of assets or liabilities or the performance of services by, to or for a related party As auditors we have a duty to undertake work to identify such transactions

16 Donations from trustees Trustees may also give to the charity. Donations which are unrestricted do not have to be separately disclosed. However, if the trustee specified how the funds had to be used, then this may be exerting significant influence and so restricted donations by trustees do have to be disclosed.

17 Charity Commission Guidance /conflicts-of-interest-a-guide-for-charitytrustees-cc29/conflicts-of-interest-a-guide-forcharity-trustees

18 The Charity Commission's new regulatory approach - are you informed? Steve Law Head of Investigations Team Charity Commission for England and Wales Charity seminar HW Fisher & Company 11 November 2014

19 The Charity Commission The independent regulator of charities in England and Wales Five statutory objectives (s14 CA 2011) The compliance objective promoting compliance by charity trustees with their legal obligations Commission s functions (s15 (1)(3) CA 2011) Identifying and investigating apparent misconduct or mismanagement in the administration of charities taking remedial or protective action

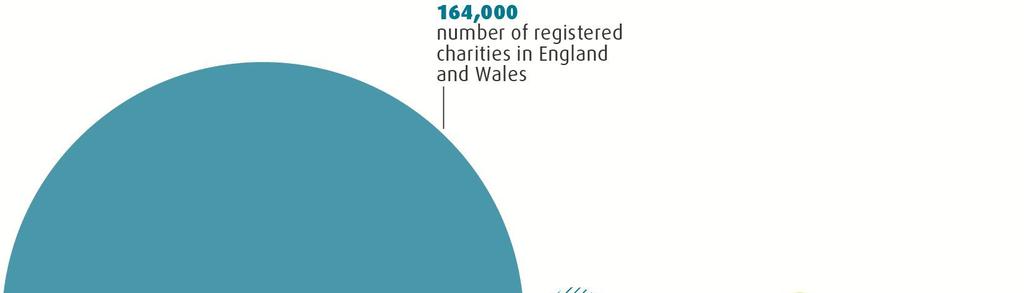

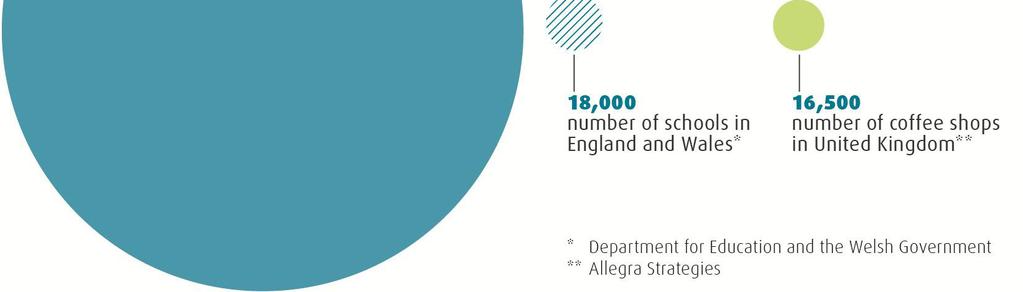

20 Facts about charity 164,000 registered charities 4,968 new registrations in million regular volunteers 1m charity trustees 940,000 charity workers > 64bn annual income of registered charities 106bn long term investments held by charities

21 Scale of charitable sector

22 Upholding public trust in charity Commission s work to uphold public trust our strategic approach how we are improving already plans for the months ahead Charities role in promoting public trust what the public expects of you what we expect of you

23 Context for charity regulation Changing public expectations of charity Demands for greater accountability Evidence of public giving charities less benefit of doubt Media focus on charities (e.g. pay, investments) Increased external scrutiny of Commission National Audit Office review of Commission s work Public Accounts Committee hearings Debates in Parliament Significant cuts to Commission funding CC budget m CC budget m = c. 50% real terms cut since 2007 New 8m funding To invest in technology and frontline operations

24 Our new strategic approach One of our most important statutory objectives is to increase public trust and confidence in charities. by concentrating on promoting compliance by charity trustees with their legal obligations, by enhancing the rigour with which we hold charities accountable, and by ensuring that we uphold the definition of charity under charity law (Statement of regulatory approach, Commission s Annual report and accounts 2013/2014)

25 Robust regulation in action 64 charities placed under inquiry (15 in ) 540 use of legal powers in investigative work (216 in ) Regulatory alerts e.g. recent alert on reporting serious incidents.

26 More proactive approach Operations / registrations New operations monitoring team 318 referrals, including 89 from registrations (between October 2013 & April 2014) Accounts monitoring Casework related and themed accounts reviews 1,664 sets of accounts reviewed Smarter, more focused guidance Clearer focus on expectations of trustees E.g. new Conflicts of Interest guidance

27 Greater transparency Greater openness about statutory inquiries announcing inquiries when its in the public interest marking open inquiries against charities online entry Reports of operational cases New online charity search tool more information about charities easier to access from mobile devices

28 What we need to do now Risk Better use of data Targeting work where it makes greatest impact Supporting increasingly proactive approach to case work Digitisation Digitising front-end services Streamlining low risk customer-facing services = recognising charities are our customers Structure Recruiting 5-strong senior management team Skills and talent management agenda

29 Over to you What can you do to promote public trust in charity?

30 Show integrity Have trustees: acted within their powers? acted in good faith and only in interests of charity? adequately informed themselves? taken into account all relevant factors, disregarded irrelevant factors? managed conflicts of interest? made decisions within range of decisions that reasonable trustee body would make?

31 Be accountable It is important that charities provide the public with information about how they spend their money

32 How accountable are charities? 86% charities filed annual returns on time 86% charities filed annual accounts on time 99% of sector income accounted for = over all compliance is high but: 58 charities have been subject to double defaulters class inquiry 47m of charitable funds now accounted for

33 Report serious incidents 1,280 serious incidents reported in > 580 reports so far this year = huge underreporting by charities Serious incidents include: fraud, theft, significant loss abuse of beneficiaries financial links to banned group Investigation by another regulator = actual or suspected

34 Final thought Charities play an essential and important role in society

35 Mismanagement in the Administration of a Charity Practical Examples of when an Interim Manager had been appointed and the actions that might be taken BRIAN JOHNSON

36 Mismanagement in the Administration of a Charity Busy people with good intentions and good causes Rapid growth and the need for time and skills resource Resource deficiency leading to shortcuts Leading to: governance failings; risk management short-comings; Late filing of statutory documents; and Value for money reduction. 36

37 Mismanagement in the Administration of a Charity Practical examples of governance failings charity acting outside of its constitution; proper meetings not being held; conflicts of interests; Trading subsidiaries acting reasonably; trustee remuneration; and Statutory documents not being filed on time. 37

38 Mismanagement in the Administration of a Charity Practical examples of risk management failings Entering into agreements without professional advice; Failing to keep a risk register; Controls, cash and fraud; Brand management; Trading and losses; Ensuring proper security is in place; Restricted funds; Insuring activities properly; and Ensuring the charity is meeting its objects. 38

39 Mismanagement in the Administration of a Charity Examples of when value for monetary considerations have been neglected: Not tendering properly; Not reviewing on-going contracts; Tax and corporate structures; Effective advertising and brand maintenance; All costs incurred are in pursuance of the charity s objects; and Capital expenditure and infrastructure programs are kept under control. 39

40 Mismanagement in the Administration of a Charity Professional advice; Auditors; Corporate structures and SPVs; Tax; Legal support; Employment; Health & Safety; Environment; Contractual and fundraising; and Charity Commission guidance 40

41 Mismanagement in the Administration of a Charity 41

Conflicts of interest: a guide for charity trustees

GUIDANCE Conflicts of interest: a guide for charity trustees MAY 2014 New format February 2017 Contents 1. About this guidance 2 2. Conflicts of interest: at a glance summary 5 3. Identifying conflicts

GUIDANCE Conflicts of interest: a guide for charity trustees MAY 2014 New format February 2017 Contents 1. About this guidance 2 2. Conflicts of interest: at a glance summary 5 3. Identifying conflicts

Inspiring Trusteeship. Key Issues in Charity Governance. Andrew Studd and Victoria Ehmann Charity and Social Business Team

Inspiring Trusteeship Key Issues in Charity Governance Andrew Studd and Victoria Ehmann Charity and Social Business Team Outline What is a charity? Legal structure the options for charities Impact of structure

Inspiring Trusteeship Key Issues in Charity Governance Andrew Studd and Victoria Ehmann Charity and Social Business Team Outline What is a charity? Legal structure the options for charities Impact of structure

This document is a record of the information provided in the Annual Return 2016.

Charity Commission Charity Commission Annual Return 2016 LINWOOD SCHOOL CHARITABLE TRUST Charity registration number: 279838 Submitted on 08/06/2017 Most of the information you give in this form will become

Charity Commission Charity Commission Annual Return 2016 LINWOOD SCHOOL CHARITABLE TRUST Charity registration number: 279838 Submitted on 08/06/2017 Most of the information you give in this form will become

This document is a record of the information provided in the Annual Return 2016.

Charity Commission Charity Commission Annual Return 2016 MAKING THE LEAP Charity registration number: 1058648 Submitted on 30/01/2017 Most of the information you give in this form will become publicly

Charity Commission Charity Commission Annual Return 2016 MAKING THE LEAP Charity registration number: 1058648 Submitted on 30/01/2017 Most of the information you give in this form will become publicly

Academy Trusts Guidance for Trustees

Academy Trusts Guidance for Trustees Jaime Parkes Email: jparkes@vwv.co.uk DDI: 0121 227 3703 Reference: jxp/1v199/1714 1 Introduction 1.1 This note provides some guidance on the duties and responsibilities

Academy Trusts Guidance for Trustees Jaime Parkes Email: jparkes@vwv.co.uk DDI: 0121 227 3703 Reference: jxp/1v199/1714 1 Introduction 1.1 This note provides some guidance on the duties and responsibilities

Charity Law and Governance

Charity Law and Governance scheme November 2016 ICSA 2016 Page 1 of 13 Section A 1 Three (1) 2 Any two of the following: (2) Charity Commission or Charity Commission for England and Wales (1) Office of

Charity Law and Governance scheme November 2016 ICSA 2016 Page 1 of 13 Section A 1 Three (1) 2 Any two of the following: (2) Charity Commission or Charity Commission for England and Wales (1) Office of

Personalised with your firms details. Charity News

Personalised with your firms details Charity News CHARITY NEWS Our Charity News includes useful guidance on keeping vulnerable beneficiaries, employees and volunteers safe. We also consider the impact

Personalised with your firms details Charity News CHARITY NEWS Our Charity News includes useful guidance on keeping vulnerable beneficiaries, employees and volunteers safe. We also consider the impact

Leicester Rape Crisis Limited. Directors' report and financial statements. for the year ended 31st March 2013

Directors' report and financial statements Company registration number 04381572 Charity registration number 1095540 Cheyettes Ltd Chartered Certified Accountants Leicester Financial statements Contents

Directors' report and financial statements Company registration number 04381572 Charity registration number 1095540 Cheyettes Ltd Chartered Certified Accountants Leicester Financial statements Contents

Memorandum of Understanding between the Scottish Charity Regulator and the Charity Commission for Northern Ireland

Memorandum of Understanding between the Scottish Charity Regulator and the Charity Commission for Northern Ireland Purpose of the Memorandum of Understanding The purpose of this memorandum of understanding

Memorandum of Understanding between the Scottish Charity Regulator and the Charity Commission for Northern Ireland Purpose of the Memorandum of Understanding The purpose of this memorandum of understanding

SC The Rangers Charity Foundation

SC033287 The Rangers Charity Foundation Report under section 33 of The Charities and Trustee Investment (Scotland) Act 2005 SC033287 The Rangers Charity Foundation _01 1. Executive summary OSCR has concluded

SC033287 The Rangers Charity Foundation Report under section 33 of The Charities and Trustee Investment (Scotland) Act 2005 SC033287 The Rangers Charity Foundation _01 1. Executive summary OSCR has concluded

Guide for Auditors and Independent Examiners

Guide for Auditors and Independent Examiners 1. The Royal British Legion Audit Requirements Branches of the Legion are not independent charities as they are all constituted under the same Royal Charter

Guide for Auditors and Independent Examiners 1. The Royal British Legion Audit Requirements Branches of the Legion are not independent charities as they are all constituted under the same Royal Charter

This document is a record of the information provided in the Annual Return 2017.

Charity Commission Charity Commission Annual Return 2017 MAKING THE LEAP Charity registration number: 1058648 Submitted on 10/01/2018 Most of the information you give in this form will become publicly

Charity Commission Charity Commission Annual Return 2017 MAKING THE LEAP Charity registration number: 1058648 Submitted on 10/01/2018 Most of the information you give in this form will become publicly

Cross-border charity regulation in Scotland Guidance on statutory requirements and reporting to the Office of the Scottish Charity Regulator

Cross-border charity regulation in Scotland Guidance on statutory requirements and reporting to the Office of the Scottish Charity Regulator www.oscr.org.uk Guidance on Regulation by the Office of the

Cross-border charity regulation in Scotland Guidance on statutory requirements and reporting to the Office of the Scottish Charity Regulator www.oscr.org.uk Guidance on Regulation by the Office of the

REGULATORY Code of practice

Reporting breaches of the law REGULATORY Code of practice 01 page 2 Regulatory Code of practice 01 REGULATORY Code of practice 01 Regulatory Code of practice 01 page 3 Contents Introduction page 4 At a

Reporting breaches of the law REGULATORY Code of practice 01 page 2 Regulatory Code of practice 01 REGULATORY Code of practice 01 Regulatory Code of practice 01 page 3 Contents Introduction page 4 At a

Guidance from the Charity Commission. The essential trustee: what you need to know. Appendix The charity framework in brief

Appendix 3 Guidance from the Charity Commission The essential trustee: what you need to know 1. The charity framework in brief This section sets out an overall description of the framework for charities,

Appendix 3 Guidance from the Charity Commission The essential trustee: what you need to know 1. The charity framework in brief This section sets out an overall description of the framework for charities,

Diocese of St Albans Trustee Training Workshop

Diocese of St Albans Trustee Training Workshop Amanda Francis September/October 2018 Welcome and Introduction Amanda Francis Partner at Buzzacott with responsibility for the audit of the Diocesan Board

Diocese of St Albans Trustee Training Workshop Amanda Francis September/October 2018 Welcome and Introduction Amanda Francis Partner at Buzzacott with responsibility for the audit of the Diocesan Board

(Including conflict of interests declaration - otherwise known as Register of Business Interests)

") Conflicts of Interest Policy (Including conflict of interests declaration - otherwise known as Register of Business Interests) Introduction All academies within the University of Chichester Academy Trust

Conflicts of Interest Policy (Including conflict of interests declaration - otherwise known as Register of Business Interests) Introduction All academies within the University of Chichester Academy Trust

Trust and confidence in the charities and not-for-profit sector. Trust and confidence in the charities and not-for-profit sector 1

Trust and confidence in the charities and not-for-profit sector Trust and confidence in the charities and not-for-profit sector 1 Contents Introduction 1 Charity governance 3 Executive pay and trustee

Trust and confidence in the charities and not-for-profit sector Trust and confidence in the charities and not-for-profit sector 1 Contents Introduction 1 Charity governance 3 Executive pay and trustee

This document is a record of the information provided in the Annual Return 2017.

Charity Commission Charity Commission Annual Return 2017 THE BODY DYSMORPHIC DISORDER FOUNDATION Charity registration number: 1153753 30 July 2018 Deadline Most of the information you give in this form

Charity Commission Charity Commission Annual Return 2017 THE BODY DYSMORPHIC DISORDER FOUNDATION Charity registration number: 1153753 30 July 2018 Deadline Most of the information you give in this form

Guideline Leaflet C01: Charity Legislation and Churches

Guideline Leaflet C01: Charity Legislation and Churches All Baptist churches are individual charities in their own right. This applies whether or not the church has registered as a charity with the Charity

Guideline Leaflet C01: Charity Legislation and Churches All Baptist churches are individual charities in their own right. This applies whether or not the church has registered as a charity with the Charity

Distress Centre Calgary. Financial Statements December 31, 2015

Financial Statements Independent Auditors Report To: The Members of Distress Centre Calgary We have audited the accompanying financial statements of Distress Centre Calgary, which comprise the statement

Financial Statements Independent Auditors Report To: The Members of Distress Centre Calgary We have audited the accompanying financial statements of Distress Centre Calgary, which comprise the statement

Charity reporting and

reporting and 6 Tilbury Place, Brighton, BN2 0GY 01273 606160 www.resourcecentre.org.uk accounts This guide summarises the requirement for charities to produce accounts, reports and returns each year.

reporting and 6 Tilbury Place, Brighton, BN2 0GY 01273 606160 www.resourcecentre.org.uk accounts This guide summarises the requirement for charities to produce accounts, reports and returns each year.

Technical factsheet Matters of material significance reportable to charity regulators

Technical factsheet Matters of material significance reportable to charity regulators Contents Page Introduction 2 Reportable matters 3 Reporting to the regulators 9 This factsheet has been produced in

Technical factsheet Matters of material significance reportable to charity regulators Contents Page Introduction 2 Reportable matters 3 Reporting to the regulators 9 This factsheet has been produced in

Exposure Draft: Practice Note 11: The audit of charities in the United Kingdom

Exposure Draft Financial Reporting Council May 2017 Exposure Draft: Practice Note 11: The audit of charities in the United Kingdom The Financial Reporting Council (FRC) is the UK s independent regulator

Exposure Draft Financial Reporting Council May 2017 Exposure Draft: Practice Note 11: The audit of charities in the United Kingdom The Financial Reporting Council (FRC) is the UK s independent regulator

Concerns Policy. Policy Title: Corporate Policy and Procedures. Policy No. CE POL Revision No. 001

Policy Title: Concerns Policy Division Compliance and Enforcement Policy No. CE POL 8.2.1 003 Revision No. 001 Author Tom Malone Date 18 April 2018 Approved By Charities Regulatory Authority Effective

Policy Title: Concerns Policy Division Compliance and Enforcement Policy No. CE POL 8.2.1 003 Revision No. 001 Author Tom Malone Date 18 April 2018 Approved By Charities Regulatory Authority Effective

The Scout Association Guidance on the 2005 Accounting and Audit Requirements for Group, Districts and Counties/Areas

The Scout Association Guidance on the 2005 Accounting and Audit Requirements for Group, Districts and Counties/Areas 1. Background In 2001 the Association updated its guidance for Counties, Areas, Districts

The Scout Association Guidance on the 2005 Accounting and Audit Requirements for Group, Districts and Counties/Areas 1. Background In 2001 the Association updated its guidance for Counties, Areas, Districts

Charities Seminar. 27 June Tom Malone FCCA Head of Compliance and Enforcement Charities Regulator

Charities Seminar 27 June 2018 Tom Malone FCCA Head of Compliance and Enforcement Charities Regulator Agenda Internal Financial Controls Managing Conflicts of Interest Proposed Accounting and Reporting

Charities Seminar 27 June 2018 Tom Malone FCCA Head of Compliance and Enforcement Charities Regulator Agenda Internal Financial Controls Managing Conflicts of Interest Proposed Accounting and Reporting

Duties of A Company Secretary. Tesse Akpeki 7 March 2017

Duties of A Company Secretary Tesse Akpeki 7 March 2017 What will we cover? Aspects of the role Statutory compliance including Companies House & Charity Commission compliance Providing support to the board

Duties of A Company Secretary Tesse Akpeki 7 March 2017 What will we cover? Aspects of the role Statutory compliance including Companies House & Charity Commission compliance Providing support to the board

Acceptance and Refusal of Donations Policy

Acceptance and Refusal of Donations Policy Reference: Date Approved: September 2016 Approving Body: Board of Trustees Implementation Date: Version: 4.0 Supersedes: 3.0 Stakeholder groups consulted: Target

Acceptance and Refusal of Donations Policy Reference: Date Approved: September 2016 Approving Body: Board of Trustees Implementation Date: Version: 4.0 Supersedes: 3.0 Stakeholder groups consulted: Target

Duties of a Company Secretary

Duties of a Company Secretary London 17 July 2018 Facilitator: Alan Clarkin 1 Objectives for the day By the end of the day participants will: understand the role of the company secretary know the legal

Duties of a Company Secretary London 17 July 2018 Facilitator: Alan Clarkin 1 Objectives for the day By the end of the day participants will: understand the role of the company secretary know the legal

Oxfordshire Deaf Children s Society. Constitution

Oxfordshire Deaf Children s Society Constitution 1 The name of the Society is: The Oxfordshire Deaf Children s Society Deafness is defined for the purposes of this constitution as: a degree of hearing

Oxfordshire Deaf Children s Society Constitution 1 The name of the Society is: The Oxfordshire Deaf Children s Society Deafness is defined for the purposes of this constitution as: a degree of hearing

Use of receipts and payments forms

Receipts and Payments Accounts Introductory Notes Purpose of pro forma receipts and payments accounts In England and Wales many smaller non-company charities may choose to prepare receipts and payments

Receipts and Payments Accounts Introductory Notes Purpose of pro forma receipts and payments accounts In England and Wales many smaller non-company charities may choose to prepare receipts and payments

For the year ended 31 August 2016 for Buckinghamshire University Technical College

Audit management letter For the year ended 31 August 2016 for Buckinghamshire University Technical College Contents 1. Introduction 1 2. Overview 2 3. Independence 5 4. Audit scope and objectives 7 5.

Audit management letter For the year ended 31 August 2016 for Buckinghamshire University Technical College Contents 1. Introduction 1 2. Overview 2 3. Independence 5 4. Audit scope and objectives 7 5.

Reporting Notifiable Events to OSCR

Reporting Notifiable Events to OSCR We aim to support public confidence in charities and their work. Part of our role is to try and prevent problems from happening, by providing guidance and advice to

Reporting Notifiable Events to OSCR We aim to support public confidence in charities and their work. Part of our role is to try and prevent problems from happening, by providing guidance and advice to

TABUNG AMAL AIDILFITRI TRUST FUND (Constituted under a Trust Deed in the Republic of Singapore) AUDITED FINANCIAL STATEMENTS- 31 MARCH 2017

AUDITED FINANCIAL STATEMENTS- 31 MARCH 2017") (Constituted under a Trust Deed in the Republic of Singapore) AUDITED FINANCIAL STATEMENTS- 31 MARCH 2017 M Barak & Co. Public Accountants and Chartered Accountants Singapore M Barak & Co. Auditors Responsibility

(Constituted under a Trust Deed in the Republic of Singapore) AUDITED FINANCIAL STATEMENTS- 31 MARCH 2017 M Barak & Co. Public Accountants and Chartered Accountants Singapore M Barak & Co. Auditors Responsibility

Accruals accounts. How to prepare accruals accounts and the trustees annual report

Accruals accounts How to prepare accruals accounts and the trustees annual report CCNI ARR04 consultation document 1 December 2015 The Charity Commission for Northern Ireland The Charity Commission for

Accruals accounts How to prepare accruals accounts and the trustees annual report CCNI ARR04 consultation document 1 December 2015 The Charity Commission for Northern Ireland The Charity Commission for

The Arts Society. (The Arts Society is the operating name of The National Association of Decorative and Fine Arts Societies)

") The Arts Society (The Arts Society is the operating name of The National Association of Decorative and Fine Arts Societies) Guidance for Societies considering registration as a Charity A: Background Guidance

The Arts Society (The Arts Society is the operating name of The National Association of Decorative and Fine Arts Societies) Guidance for Societies considering registration as a Charity A: Background Guidance

ABERCROMBY MELNYCHUK. Big Brothers of Greater Vancouver Financial Statements For the year ended July 31, 2017

Financial Statements For the year ended Financial Statements For the year ended Contents Independent Auditors' Report 2 Financial Statements Statement of Financial Position 4 Statement of Operations and

Financial Statements For the year ended Financial Statements For the year ended Contents Independent Auditors' Report 2 Financial Statements Statement of Financial Position 4 Statement of Operations and

Leaflet F04: Independent Examination of Church Accounts

Leaflet F04: Independent Examination of Church Accounts This explanatory document aims to provide guidance regarding independent Examination of Church Accounts. Page 1 Leaflet F04: Independent Examination

Leaflet F04: Independent Examination of Church Accounts This explanatory document aims to provide guidance regarding independent Examination of Church Accounts. Page 1 Leaflet F04: Independent Examination

ABERCROMBY MELNYCHUK. Big Brothers of Greater Vancouver Financial Statements For the year ended July 31, 2018

Financial Statements For the year ended Financial Statements For the year ended Contents Independent Auditors' Report 2 Financial Statements Statement of Financial Position 4 Statement of Operations and

Financial Statements For the year ended Financial Statements For the year ended Contents Independent Auditors' Report 2 Financial Statements Statement of Financial Position 4 Statement of Operations and

LAW COMMISSION RECOMMENDS MAKEOVER FOR NEW ZEALAND TRUST LAW

MEDIA RELEASE 11 September 2013 Hon Sir Grant Hammond KNZM President Law Commission LAW COMMISSION RECOMMENDS MAKEOVER FOR NEW ZEALAND TRUST LAW The Law Commission is recommending a new Act clarifying

MEDIA RELEASE 11 September 2013 Hon Sir Grant Hammond KNZM President Law Commission LAW COMMISSION RECOMMENDS MAKEOVER FOR NEW ZEALAND TRUST LAW The Law Commission is recommending a new Act clarifying

Small Charity Reporting

Small Charity Reporting Bulletin 2017 / 1 What is in this Bulletin? There are three key changes of relevance to auditors, independent examiners and preparers of charity accounts dealt with in this Bulletin:

Small Charity Reporting Bulletin 2017 / 1 What is in this Bulletin? There are three key changes of relevance to auditors, independent examiners and preparers of charity accounts dealt with in this Bulletin:

SHAKE IT UP AUSTRALIA CHARITABLE TRUST A.B.N FINANCIAL REPORT FOR THE YEAR ENDED 30 JUNE 2017

SHAKE IT UP AUSTRALIA CHARITABLE TRUST FINANCIAL REPORT INDEPENDENT AUDITOR'S REPORT TRUSTEES DECLARATION STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME STATEMENT OF FINANCIAL POSITION STATEMENT

SHAKE IT UP AUSTRALIA CHARITABLE TRUST FINANCIAL REPORT INDEPENDENT AUDITOR'S REPORT TRUSTEES DECLARATION STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME STATEMENT OF FINANCIAL POSITION STATEMENT

CLUB STRUCTURES 2015 A GUIDE TO CLUB STRUCTURES FOR SEMI- PROFESSIONAL AND AMATEUR SPORTS CLUBS BY CHARLES RUSSELL SPEECHLYS AND LAWINSPORT

CLUB STRUCTURES 2015 A GUIDE TO CLUB STRUCTURES FOR SEMI- PROFESSIONAL AND AMATEUR SPORTS CLUBS BY CHARLES RUSSELL SPEECHLYS AND LAWINSPORT LawInSport Limited 2015 INTRODUCTION In promoting the success

CLUB STRUCTURES 2015 A GUIDE TO CLUB STRUCTURES FOR SEMI- PROFESSIONAL AND AMATEUR SPORTS CLUBS BY CHARLES RUSSELL SPEECHLYS AND LAWINSPORT LawInSport Limited 2015 INTRODUCTION In promoting the success

SRI LANKA AUDITING STANDARD 720 OTHER INFORMATION IN DOCUMENTS CONTAINING AUDITED FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 720 OTHER INFORMATION IN DOCUMENTS CONTAINING (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-8 Access to Other Information 9 Consideration

SRI LANKA AUDITING STANDARD 720 OTHER INFORMATION IN DOCUMENTS CONTAINING (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-8 Access to Other Information 9 Consideration

Oversight over Public Charities: Fiduciary Duties of Trustees & Officers

Oversight over Public Charities: Fiduciary Duties of Trustees & Officers Massachusetts Trustees Conference March 1, 2018 Bernardo G. Cuadra Assistant Attorney General Non-Profit Organizations/Public Charities

Oversight over Public Charities: Fiduciary Duties of Trustees & Officers Massachusetts Trustees Conference March 1, 2018 Bernardo G. Cuadra Assistant Attorney General Non-Profit Organizations/Public Charities

Annex B: Payment and Expenses for Governors

Annex B: Payment and Expenses for Governors Introduction 1. This document has been produced by the Department for Business, Innovation and Skills (BIS) with advice from the Charity Commission to guide

Annex B: Payment and Expenses for Governors Introduction 1. This document has been produced by the Department for Business, Innovation and Skills (BIS) with advice from the Charity Commission to guide

Financial Regulations

Financial Regulations Page 1 of 15 CONTENTS 1. Overview 1.1 Introduction 1.2 Statutory Framework 1.3 Responsibilities 1.4 Separation of Duties 1.6 Review of the Financial Regulations 2. Financial Planning

Financial Regulations Page 1 of 15 CONTENTS 1. Overview 1.1 Introduction 1.2 Statutory Framework 1.3 Responsibilities 1.4 Separation of Duties 1.6 Review of the Financial Regulations 2. Financial Planning

Duties of A Company Secretary. Tesse Akpeki and Chinonso Denwigwe 2 November 2017

Duties of A Company Secretary Tesse Akpeki and Chinonso Denwigwe 2 November 2017 What will we cover? Company secretarial person specification Structural framework and regulatory landscape Statutory compliance

Duties of A Company Secretary Tesse Akpeki and Chinonso Denwigwe 2 November 2017 What will we cover? Company secretarial person specification Structural framework and regulatory landscape Statutory compliance

Charity trustee eligibility

Guidance note Charity trustee eligibility Contents Introduction Benefits of being a trustee Constitutional considerations Legal considerations Charity Commission waivers Acting while disqualified Due diligence

Guidance note Charity trustee eligibility Contents Introduction Benefits of being a trustee Constitutional considerations Legal considerations Charity Commission waivers Acting while disqualified Due diligence

LASA MEMORANDUM OF ASSOCIATION Page 1 Revised 2009

LASA MEMORANDUM OF ASSOCIATION Page 1 The Companies Acts 1985 & 2006 COMPANY LIMITED BY GUARANTEE Memorandum of Association of London Advice Services Alliance Company Limited Company number: 1794098 1.

LASA MEMORANDUM OF ASSOCIATION Page 1 The Companies Acts 1985 & 2006 COMPANY LIMITED BY GUARANTEE Memorandum of Association of London Advice Services Alliance Company Limited Company number: 1794098 1.

Charity Law and Governance

Charity Law and Governance scheme June 2018 ICSA 2018 Page 1 of 13 Section A 1 i. Community benefit society. (1) ii. Co-operative society. (1) Total (2) 2 B It is regulated only by the Charity Commission.

Charity Law and Governance scheme June 2018 ICSA 2018 Page 1 of 13 Section A 1 i. Community benefit society. (1) ii. Co-operative society. (1) Total (2) 2 B It is regulated only by the Charity Commission.

Group Financial Statements

Group Financial Statements Group Financial Statements 80 Statement of Directors Responsibilities 81 Independent Auditor s UK Report 87 Independent Auditor s US Report 88 Group Financial Statements 88 Group

Group Financial Statements Group Financial Statements 80 Statement of Directors Responsibilities 81 Independent Auditor s UK Report 87 Independent Auditor s US Report 88 Group Financial Statements 88 Group

Trustees Code of Conduct

Trustees Code of Conduct Surrey Wildlife Trust Policy Statement Introduction Every charity s trustees have legal duties and responsibilities. The most important of these are summarised in the Charity Commission

Trustees Code of Conduct Surrey Wildlife Trust Policy Statement Introduction Every charity s trustees have legal duties and responsibilities. The most important of these are summarised in the Charity Commission

This document is a record of the information provided in the Annual Return 2017.

Charity Commission Charity Commission Annual Return 2017 WORLD HERITAGE UK Charity registration number: 1163364 Submitted on 16/01/2018 Most of the information you give in this form will become publicly

Charity Commission Charity Commission Annual Return 2017 WORLD HERITAGE UK Charity registration number: 1163364 Submitted on 16/01/2018 Most of the information you give in this form will become publicly

Financial Regulations

Naphill Village Hall & Playing Fields Council Financial Regulations 1.0 Purpose The purpose of this document is to agree the management rules that will be applied to the financial affairs of the registered

Naphill Village Hall & Playing Fields Council Financial Regulations 1.0 Purpose The purpose of this document is to agree the management rules that will be applied to the financial affairs of the registered

S A F E G UARDING W O R K S H O P : C H I L D H O P E

S A F E G UARDING W O R K S H O P : C H I L D H O P E A I M S O F T H E C O U R S E Share the learning from UUK s safeguarding journey Prompt discussion about the challenges and opportunities other organisations

S A F E G UARDING W O R K S H O P : C H I L D H O P E A I M S O F T H E C O U R S E Share the learning from UUK s safeguarding journey Prompt discussion about the challenges and opportunities other organisations

Managing charity assets and resources

Managing charity assets and resources March 2011 Contents 1. Introduction 2 2. Financial management 4 3. Investing charitable funds 5 4. Identifying and managing risk 6 5. Sound internal financial controls

Managing charity assets and resources March 2011 Contents 1. Introduction 2 2. Financial management 4 3. Investing charitable funds 5 4. Identifying and managing risk 6 5. Sound internal financial controls

Charities and Benevolent Fundraising (Scotland) Regulations 2009 What this guide covers

Regulations 2009 What this guide covers") Charities and Benevolent Fundraising (Scotland) Regulations 2009 What this guide covers This is a technical guide explaining the rules set out in the 2009 Regulations Technical Guide: Charities and Benevolent

Charities and Benevolent Fundraising (Scotland) Regulations 2009 What this guide covers This is a technical guide explaining the rules set out in the 2009 Regulations Technical Guide: Charities and Benevolent

Councillors Guide. A guide to a councillor s role as charity trustee

Councillors Guide A guide to a councillor s role as charity trustee October 2012 1 The Charity Commission for Northern Ireland is the new regulator of charities in Northern Ireland, a non-departmental

Councillors Guide A guide to a councillor s role as charity trustee October 2012 1 The Charity Commission for Northern Ireland is the new regulator of charities in Northern Ireland, a non-departmental

COMPLIANCE & SUPPORT. Inquiry Report London Mill Hill Congregation of Jehovah s Witnesses. Registered Charity Number

COMPLIANCE & SUPPORT Inquiry Report London Mill Hill Congregation of Jehovah s Witnesses Registered Charity Number 1065638 A statement of the results of an inquiry into the London Mill Hill Congregation

COMPLIANCE & SUPPORT Inquiry Report London Mill Hill Congregation of Jehovah s Witnesses Registered Charity Number 1065638 A statement of the results of an inquiry into the London Mill Hill Congregation

Your Aviva Business Insurance Important Information

Your Aviva Business Insurance Important Information Material Circumstances IMPORTANT This policy is a legal contract Please remember that you must make a fair presentation of the risk to us. This means

Your Aviva Business Insurance Important Information Material Circumstances IMPORTANT This policy is a legal contract Please remember that you must make a fair presentation of the risk to us. This means

Reporting of relevant matters of interest to UK charity regulators. A guide for auditors and independent examiners

Reporting of relevant matters of interest to UK charity regulators A guide for auditors and independent examiners 1 The Charity Regulators The Charity Commission for Northern Ireland (CCNI) is the regulator

Reporting of relevant matters of interest to UK charity regulators A guide for auditors and independent examiners 1 The Charity Regulators The Charity Commission for Northern Ireland (CCNI) is the regulator

Consultation on Scottish Charity Law: NSS response

19/03/2019 Consultation on Scottish Charity Law: NSS response Introduction 1. The National Secular Society (NSS) works for the separation of religion and state, and for equal respect for everyone's human

19/03/2019 Consultation on Scottish Charity Law: NSS response Introduction 1. The National Secular Society (NSS) works for the separation of religion and state, and for equal respect for everyone's human

Giving confidently: The role of the Charity Commission in regulating charities. Charity Commission

Charity Commission Giving confidently: The role of the Charity Commission in regulating charities REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 234 Session 2001-2002: 25 October 2001 The National Audit

Charity Commission Giving confidently: The role of the Charity Commission in regulating charities REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 234 Session 2001-2002: 25 October 2001 The National Audit

in Documents Containing Audited Financial Statements

Issued June 2005 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 720 Other Information in Documents Containing Audited Financial

Issued June 2005 Effective for audits of financial statements for periods beginning on or after 15 December 2004 Hong Kong Standard on Auditing 720 Other Information in Documents Containing Audited Financial

April 2015 FC 158/12 E. Hundred and Fifty-eighth Session. Rome, May Anti-Fraud and Anti-Corruption Policy

April 2015 FC 158/12 E FINANCE COMMITTEE Hundred and Fifty-eighth Session Rome, 11-13 May 2015 Anti-Fraud and Anti-Corruption Policy Queries on the substantive content of this document may be addressed

April 2015 FC 158/12 E FINANCE COMMITTEE Hundred and Fifty-eighth Session Rome, 11-13 May 2015 Anti-Fraud and Anti-Corruption Policy Queries on the substantive content of this document may be addressed

Fraud, Bribery and Corruption Control Policy

Fraud, Bribery and Corruption Control Policy 1. Introduction DuluxGroup acknowledges the need for directors, executives, employees and contractors to observe the highest ethical standards of corporate

Fraud, Bribery and Corruption Control Policy 1. Introduction DuluxGroup acknowledges the need for directors, executives, employees and contractors to observe the highest ethical standards of corporate

Dealing with concerns about charities. Guidance on how the Charity Commission for Northern Ireland deals with concerns about charities

Dealing with concerns about charities Guidance on how the Charity Commission for Northern Ireland deals with concerns about charities CCNI EG044 1 December 2015 The Charity Commission for Northern Ireland

Dealing with concerns about charities Guidance on how the Charity Commission for Northern Ireland deals with concerns about charities CCNI EG044 1 December 2015 The Charity Commission for Northern Ireland

Firm Registration Form

Firm Registration Form This registration form should be completed by firms who are authorised and regulated by the Financial Conduct Authority. It is for advisers who wish to recommend our mortgage products,

Firm Registration Form This registration form should be completed by firms who are authorised and regulated by the Financial Conduct Authority. It is for advisers who wish to recommend our mortgage products,

Accounting and reporting by charities: statement of recommended practice (SORP) EXPOSURE DRAFT - JULY 2013

EXPOSURE DRAFT - JULY 2013") : statement of recommended practice (SORP) - JULY 2013 Accounting and reporting by charities: the statement of recommended practice (SORP) scope and application Introduction 1. The Statement of Recommended

: statement of recommended practice (SORP) - JULY 2013 Accounting and reporting by charities: the statement of recommended practice (SORP) scope and application Introduction 1. The Statement of Recommended

REPORT OF THE TRUSTEES AND FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 FOR CHRISTIAN PRISON RESOURCING

REGISTERED COMPANY NUMBER: 07131167 (England and Wales) REGISTERED CHARITY NUMBER: 1134592 REPORT OF THE TRUSTEES AND FINANCIAL STATEMENTS FOR CHRISTIAN PRISON RESOURCING Heather s Bookkeeping Services

REGISTERED COMPANY NUMBER: 07131167 (England and Wales) REGISTERED CHARITY NUMBER: 1134592 REPORT OF THE TRUSTEES AND FINANCIAL STATEMENTS FOR CHRISTIAN PRISON RESOURCING Heather s Bookkeeping Services

2 The Charity s registered office is to be situated in England and Wales. 3a) The Charity s object (3) was amended on 7th November 2016 to;

The Charity s object (3) was amended on 7th November 2016 to;") Memorandum of Association 1 THE COMPANIES ACTS 1985 TO 1989 PRIVATE COMPANY LIMITED BY GUARANTEE Memorandum of Association of Moving On (Durham) Ltd. 1 The company s name is Moving On (Durham) Ltd. (and

Memorandum of Association 1 THE COMPANIES ACTS 1985 TO 1989 PRIVATE COMPANY LIMITED BY GUARANTEE Memorandum of Association of Moving On (Durham) Ltd. 1 The company s name is Moving On (Durham) Ltd. (and

Charity. How transparent is your senior executive pay? Use your Trustees report to promote your charity. Gift Aid and subsidiaries

Charity How transparent is your senior executive pay? Use your Trustees report to promote your charity Gift Aid and subsidiaries Changes to the annual return for charities 2015 Filing accounts with the

Charity How transparent is your senior executive pay? Use your Trustees report to promote your charity Gift Aid and subsidiaries Changes to the annual return for charities 2015 Filing accounts with the

Section 3 Trustees Annual Report General Notes for preparing the Trustees Annual Report 6

Contents Page Section 1 Introduction 1 1.1 Introduction 1 1.2 Scope of this guidance 1 1.3 What are receipts and payments accounts? 1 1.4 How can these forms be used? 2 Section 2 Features of receipts and

Contents Page Section 1 Introduction 1 1.1 Introduction 1 1.2 Scope of this guidance 1 1.3 What are receipts and payments accounts? 1 1.4 How can these forms be used? 2 Section 2 Features of receipts and

ANTI-FRAUD, BRIBERY AND CORRUPTION POLICY AND STRATEGY THE VIEW TRUST

ANTI-FRAUD, BRIBERY AND CORRUPTION POLICY AND STRATEGY THE VIEW TRUST INTRODUCTION 1. Introduction 2. What are Fraud, Bribery and Corruption? 3. Purpose of this Document 4. Scope of this Document 5. Anti-Fraud,

ANTI-FRAUD, BRIBERY AND CORRUPTION POLICY AND STRATEGY THE VIEW TRUST INTRODUCTION 1. Introduction 2. What are Fraud, Bribery and Corruption? 3. Purpose of this Document 4. Scope of this Document 5. Anti-Fraud,

FRAUD PREVENTION POLICY

Page 1 of 13 FRAUD PREVENTION POLICY POLICY NO: 0094 Page 2 of 13 TABLE OF CONTENT Page 3 of 13 AMENDMENT AND APPROVAL RECORD TITLE: FRAUD PREVENTION POLICY Policy Number 0094 Effective Date From date

Page 1 of 13 FRAUD PREVENTION POLICY POLICY NO: 0094 Page 2 of 13 TABLE OF CONTENT Page 3 of 13 AMENDMENT AND APPROVAL RECORD TITLE: FRAUD PREVENTION POLICY Policy Number 0094 Effective Date From date

Financial Policies and Procedures Preventing Bribery, Corruption and Money Laundering (August 2018)

") Institute of Development Studies Financial Policies and Procedures Preventing Bribery, Corruption and Money Laundering (August 2018) Contents Page 1. Introduction 1 2. Principles 4 3. Bribery prevention

Institute of Development Studies Financial Policies and Procedures Preventing Bribery, Corruption and Money Laundering (August 2018) Contents Page 1. Introduction 1 2. Principles 4 3. Bribery prevention

BRIEFING FOR THE HOUSE OF COMMONS PUBLIC ADMINISTRATION SELECT COMMITTEE JULY Regulating charities: a landscape review

BRIEFING FOR THE HOUSE OF COMMONS PUBLIC ADMINISTRATION SELECT COMMITTEE JULY 2012 Regulating charities: a landscape review Our vision is to help the nation spend wisely. We apply the unique perspective

BRIEFING FOR THE HOUSE OF COMMONS PUBLIC ADMINISTRATION SELECT COMMITTEE JULY 2012 Regulating charities: a landscape review Our vision is to help the nation spend wisely. We apply the unique perspective

Financial disclosure reporting checklist

Financial disclosure reporting checklist Charities (FRS 102) Accounting and Reporting by Charities: Statement of Recommended Practice applicable to charities preparing their accounts in accordance with

Financial disclosure reporting checklist Charities (FRS 102) Accounting and Reporting by Charities: Statement of Recommended Practice applicable to charities preparing their accounts in accordance with

POLICY. Tiger Brands Anti-Bribery and Anti-Corruption Policy

and Anti- TABLE OF CONTENTS DOCUMENT CONTROL INFORMATION... 3 1 INTRODUCTION... 5 2 SCOPE... 5 3 OBJECTIVE... 5 4 POLICY DETAILS... 6 5 ROLES AND RESPONSIBILITIES... 10 6 COMPLIANCE... ERROR! BOOKMARK

and Anti- TABLE OF CONTENTS DOCUMENT CONTROL INFORMATION... 3 1 INTRODUCTION... 5 2 SCOPE... 5 3 OBJECTIVE... 5 4 POLICY DETAILS... 6 5 ROLES AND RESPONSIBILITIES... 10 6 COMPLIANCE... ERROR! BOOKMARK

Anti-bribery policy. Lynas Corporation Limited ACN

Lynas Corporation Limited ACN 009 066 648 Contents Lynas Corporation Limited... 1 1. Introduction... 1 2. Application... 1 3. Objectives... 2 4. Bribes... 2 5. Political Contributions and Charitable Contributions/

Lynas Corporation Limited ACN 009 066 648 Contents Lynas Corporation Limited... 1 1. Introduction... 1 2. Application... 1 3. Objectives... 2 4. Bribes... 2 5. Political Contributions and Charitable Contributions/

Practice Note 11 (Revised)

") Guidance Audit and Assurance Financial Reporting Council November 2017 Practice Note 11 (Revised) The audit of charities in the United Kingdom The Financial Reporting Council (FRC) is responsible for promoting

Guidance Audit and Assurance Financial Reporting Council November 2017 Practice Note 11 (Revised) The audit of charities in the United Kingdom The Financial Reporting Council (FRC) is responsible for promoting

THE COMPANIES ACT 2006 COMPANY LIMITED BY GUARANTEE AND NOT HAVING A SHARE CAPITAL. MEMORANDUM of ASSOCIATION of YOUTHBORDERS

THE COMPANIES ACT 2006 COMPANY LIMITED BY GUARANTEE AND NOT HAVING A SHARE CAPITAL MEMORANDUM of ASSOCIATION of YOUTHBORDERS THE COMPANIES ACT 2006 COMPANY LIMITED BY GUARANTEE AND NOT HAVING A SHARE CAPITAL

THE COMPANIES ACT 2006 COMPANY LIMITED BY GUARANTEE AND NOT HAVING A SHARE CAPITAL MEMORANDUM of ASSOCIATION of YOUTHBORDERS THE COMPANIES ACT 2006 COMPANY LIMITED BY GUARANTEE AND NOT HAVING A SHARE CAPITAL

CHARITY TERMS AND CONDITIONS

CHARITY TERMS AND CONDITIONS 1 YOUR TERMS AND CONDITIONS Here are the terms and conditions of your Virgin Money Charity Account. Together with your Key product information sheet with summary box, they

CHARITY TERMS AND CONDITIONS 1 YOUR TERMS AND CONDITIONS Here are the terms and conditions of your Virgin Money Charity Account. Together with your Key product information sheet with summary box, they

An overview of charity campaigning & the Electoral Commission guidance

An overview of charity campaigning & the Electoral Commission guidance 1. Introduction 1.1 This note explores charity law and electoral law in the context of a charity involved in campaigning, following

An overview of charity campaigning & the Electoral Commission guidance 1. Introduction 1.1 This note explores charity law and electoral law in the context of a charity involved in campaigning, following

OPTIONS FOR GIG ROWING CLUBS: LEGAL STRUCTURES

OPTIONS FOR GIG ROWING CLUBS: LEGAL STRUCTURES This note guide sets out some of the options for gig rowing clubs as to their possible legal structure. This guidance note does not constitute legal advice

OPTIONS FOR GIG ROWING CLUBS: LEGAL STRUCTURES This note guide sets out some of the options for gig rowing clubs as to their possible legal structure. This guidance note does not constitute legal advice

Breaching anti-bribery and anti-corruption law is a serious offence and represents a failure of our commitment to business integrity.

Anti-Bribery and Anti- Corruption Policy PURPOSE This document sets out Control Risks policy on bribery and corruption. Control Risks is committed to the highest ethical standards, and vigorously enforces

Anti-Bribery and Anti- Corruption Policy PURPOSE This document sets out Control Risks policy on bribery and corruption. Control Risks is committed to the highest ethical standards, and vigorously enforces

Receipts and payments accounts Period start date

For the from Enter charity name Receipts and payments accounts Period start date Period end date Day Month Year to Day Month Year Enter No. Section A Statement of receipts and payments A1 Receipts Donations

For the from Enter charity name Receipts and payments accounts Period start date Period end date Day Month Year to Day Month Year Enter No. Section A Statement of receipts and payments A1 Receipts Donations

Constitution of Evergreen Africa

Constitution of Evergreen Africa A Charitable Incorporated Organisation whose only voting members are its charity trustees. Date of constitution (last amended) 1 February 2015 1. Name. The name of the

Constitution of Evergreen Africa A Charitable Incorporated Organisation whose only voting members are its charity trustees. Date of constitution (last amended) 1 February 2015 1. Name. The name of the

Anti-Bribery Policy. The Company Compliance Officer is the Director of Organisational Effectiveness.

Anti-Bribery Policy Definitions For the purposes of this policy, the terms staff or member of staff/staff member shall mean officers of the Company, employees, service providers, contractors, consultants

Anti-Bribery Policy Definitions For the purposes of this policy, the terms staff or member of staff/staff member shall mean officers of the Company, employees, service providers, contractors, consultants

Who s In Charge: Control and Independence in Scottish Charities

Who s In Charge: Control and Independence in Scottish Charities Page : 02 Who s In Charge: Control and Independence in Scottish Charities 2011 Contents Page Executive Summary Introduction 4 Chapter 1.

Who s In Charge: Control and Independence in Scottish Charities Page : 02 Who s In Charge: Control and Independence in Scottish Charities 2011 Contents Page Executive Summary Introduction 4 Chapter 1.

The Royal Society reserves the right to vary the conditions of award at any time without prior notification.

Conditions of Award CA/12/14 These Conditions of Award set out the standard terms and conditions for all Royal Society Awards. The Conditions of Award should be read in conjunction with the Award Letter

Conditions of Award CA/12/14 These Conditions of Award set out the standard terms and conditions for all Royal Society Awards. The Conditions of Award should be read in conjunction with the Award Letter

Relate. Charities regulation in Ireland. What is a charity? May Contents

May 2018 Volume 45: Issue 5 ISSN 0790-4290 Contents Page No. Relate The journal of developments in social services, policy and legislation in Ireland 1. What is a charity? 4. Types of charitable organisations

May 2018 Volume 45: Issue 5 ISSN 0790-4290 Contents Page No. Relate The journal of developments in social services, policy and legislation in Ireland 1. What is a charity? 4. Types of charitable organisations

MOMENTUM COMMUNITY ECONOMIC DEVELOPMENT SOCIETY Financial Statements December 31, 2017

Financial Statements December 31, 2017 Index to Financial Statements INDEPENDENT AUDITOR'S REPORT 1-2 Page FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Operations 4 Statement of

Financial Statements December 31, 2017 Index to Financial Statements INDEPENDENT AUDITOR'S REPORT 1-2 Page FINANCIAL STATEMENTS Statement of Financial Position 3 Statement of Operations 4 Statement of

Charity Commission Annual Return 2018

DSC consultation response Charity Commission Annual Return 2018 November 2017 Daniel Ferrell-Schweppenstedde Policy and Public Affairs Manager Directory of Social Change 352 Holloway Road London N7 6PA

DSC consultation response Charity Commission Annual Return 2018 November 2017 Daniel Ferrell-Schweppenstedde Policy and Public Affairs Manager Directory of Social Change 352 Holloway Road London N7 6PA

Introduction Post-Audit Report Conclusion Appendix A Audit adjustments Appendix B Unadjusted misstatements...

Introduction... 1 Post-Audit Report... 1 Conclusion... 7 Appendix A Audit adjustments... 8 Appendix B Unadjusted misstatements... 9 Appendix C Audit findings and recommendations... 10 Appendix D Sector

Introduction... 1 Post-Audit Report... 1 Conclusion... 7 Appendix A Audit adjustments... 8 Appendix B Unadjusted misstatements... 9 Appendix C Audit findings and recommendations... 10 Appendix D Sector

LOTTERIES AND THE LAW

LOTTERIES AND THE LAW 2 Contents Page 1. Introduction 03 2. What is a lottery? 03 3. Society and Other Lotteries 03 4. Lotteries incidental to exempt entertainment 03 5. Private lotteries 04 6. Society

LOTTERIES AND THE LAW 2 Contents Page 1. Introduction 03 2. What is a lottery? 03 3. Society and Other Lotteries 03 4. Lotteries incidental to exempt entertainment 03 5. Private lotteries 04 6. Society

WOMEN IN NEED SOCIETY OF CALGARY

WOMEN IN NEED SOCIETY OF CALGARY Financial Statements December 31, 2013 Index to the Financial Statements For the Year Ended December 31, 2013 Page INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Statement

WOMEN IN NEED SOCIETY OF CALGARY Financial Statements December 31, 2013 Index to the Financial Statements For the Year Ended December 31, 2013 Page INDEPENDENT AUDITOR'S REPORT 1 FINANCIAL STATEMENTS Statement

For the period ended 31 December 2008

Directors report and financial statements For the period ended 31 December 2008 Registered number 447577 Charity number CHY17841 Directors Report and Financial Statements For the period ended 31 December

Directors report and financial statements For the period ended 31 December 2008 Registered number 447577 Charity number CHY17841 Directors Report and Financial Statements For the period ended 31 December