Foreign Account Tax Compliance Act Steps to Compliance

|

|

|

- Magdalen Thornton

- 5 years ago

- Views:

Transcription

1 The Science of Finance Foreign Account Tax Compliance Act Steps to Compliance Grand Caymans \ January 2014

2 FATCA Steps to Compliance AGENDA: Legislative Update Steps to Compliance Part I Entity Analysis Part II Due Diligence Classification & Validation Document Collection Part III Registration Part IV Withholding & Reporting Questions \ 2

3 The Science of Finance FATCA Legislative Update

4 FATCA Steps to Compliance NO EXTENSION OF FATCA EFFECTIVE DATE: Treasury adamant that July FATCA effective date would not be changed. ELUSIVE FINAL FORMS W-8: IRS has said forms will not be out until "early 2014 perhaps as late as February HARMONIZATION REGULATIONS: Unfortunately, the IRS does not expect to issue these until "early" in Further, the IRS stressed that not all "harmonizations" will be to the rules contained in the FATCA regulations given the different policy goals of the three withholding regimes. (Chapter 3, Chapter 61 and Chapter 4). NEW SET OF CHAPTER 4 REGULATIONS: Treasury/IRS announced that they will issue a new set of FATCA regulations "early" in These will be regulatory changes resulting from comments on Final Regs, but did not specify what issues will be addressed \ 4

5 FATCA Steps to Compliance DIRECT REPORTING NFFES: Notice introduced of a new type of FATCA entity, "direct reporting non-financial foreign entities" ("DRNFFEs"). These are non-professionally managed passive entities that can opt to report their account holders directly to the IRS rather than to an FFI servicing their account. IGA SNAPSHOT: Treasury reported that there are 12 IGAs currently in place and another 17 expected by July 1, VOLUNTARY DISCLOSURES AND PENALTIES: The IRS noted that there has been an increase in voluntary disclosures of chapter 3 deficiencies because they were discovered in the course of FATCA implementation efforts. The IRS encouraged such voluntary disclosures but re-emphasized that it will not automatically waive penalties unless a good case can be made for a reasonable cause exception \ 5

6 FATCA Steps to Compliance REVENUE PROCEDURE : Revenue Procedure introduced the final FFI Agreement in December Changes include updates to cross-references and other changes to confirm FFI Agreement to the regulations. The most significant change is the addition of a 2 year transition period during which a reporting Model 2 FFI may elect to apply the FFI Agreement s due diligence procedures in lieu of those in Annex I of the FFI s IGA. The FFI Agreement was also made consistent with the Model II IGA by putting the above election in the hands of the Model II FFI, rather than the Model II country. \ 6

7 FATCA Steps to Compliance Jan 1, 2017 W/h for gross proceeds and passthru payments 2017 IGAs up for renegotiations June 30, 2016 All remaining preexisting accounts due diligence completion deadline Dec 31, 2015 Sponsored Entities no longer use SE GIIN. Must register themselves June 30, 2015 High value account due diligence remediation deadline Dec 31, 2014 Due Diligence deadline for Prima Facie FFIs July 2, 2014 Second list of PFFIs published [monthly thereafter] July 1, 2014 FATCA due diligence & W/h begins for New Accounts June 2, 2014 First List of PFFIs published April 25, 2014 FFI Register to be on June 2 List \ 7

8 The Science of Finance STEPS TO COMPLIANCE PART I - ENTITY ANALYSIS

9 FATCA Steps to Compliance Step 1 to any compliance process is scoping and analysis of the entities at hand. Step 2 - Perform a structure analysis of your Fund, corporation, partnership to determine whether entities (both affiliated or otherwise) are within or outside the scope of FATCA Step 3 Once determined, scope those considered Foreign Financial Institutions (FFI) vs. Non- Financial Foreign Entities (NFFEs). Step 4 Complete analysis on each of the entities determined to be within the scope of FATCA to ascertain the FATCA sub-status of each. Step 5 Determine whether: The entities would be part of an Expanded Affiliated Group (EAG). An EAG is partnership, or entity other than a corporation, is treated as a member of an EAG if another member holds greater than 50% of the beneficial interests in it OR The entities will be part of a Sponsoring Entity ( SE ) group. A SE is an entity that is not a QI, Withholding Foreign Partnership, or Withholding Foreign Trust that has agreed to sponsor a group of entities for FATCA due diligence & registration \ 9

10 FATCA Steps to Compliance For EAGS: Complete an EAG analysis which identifies the number of EAGs and the entities included EAG must select Lead FI responsible for initiation & management of registration for all EAG members. Lead FI gets a GIIN used by all members to register and provide to counterparties. Note that: FFI members of EAG must be PFFI or RDCFFI as a condition Excludes newly created investment funds started with seed capital from a member of the group Location of entities within an EAG is not a factor can be US or foreign. Only foreign entities required to register with the IRS \ 10

11 FATCA Steps to Compliance For Sponsoring Entities: A Sponsoring Entity [ SE ] must: Be authorized to manage FFI and enter into contracts on its behalf Register with the IRS as a SE Agree to perform, on behalf of the FFI, all due diligence, withholding, reporting, and other requirements the FFI was required to perform if it were a PFFI Identify FFI in all reporting completed on the FFI s behalf as required Not have its status as SE revoked by IRS A Sponsored Entity can use the SE s GIIN for 2014 and A Sponsored Entity must register at the conclusion of the transition period [12/31/15] and can no longer use the SE s GIIN \ 11

12 FATCA Steps to Compliance Step 6 Determine the domicile and the IGA Model jurisdiction in which the entity resides. Determination of (1) presence or absence of IGA Model Jurisdiction and (2) if IGA Model Jurisdiction present, which one [Model I or II] will dictate due diligence, documentation gathering, withholding and reporting obligations. IGA Model I vs. Model II and Non-IGA Jurisdiction obligations: IGA 1 IGA 2 No IGA Registration & GIIN RO FFI Agreement Reporting Yes No No Local Registration & GIINYes RO Yes FFI AgreementYes Reporting IRS Registration & GIIN RO FFI Agreement Reporting Yes Yes Yes IRS \ 12

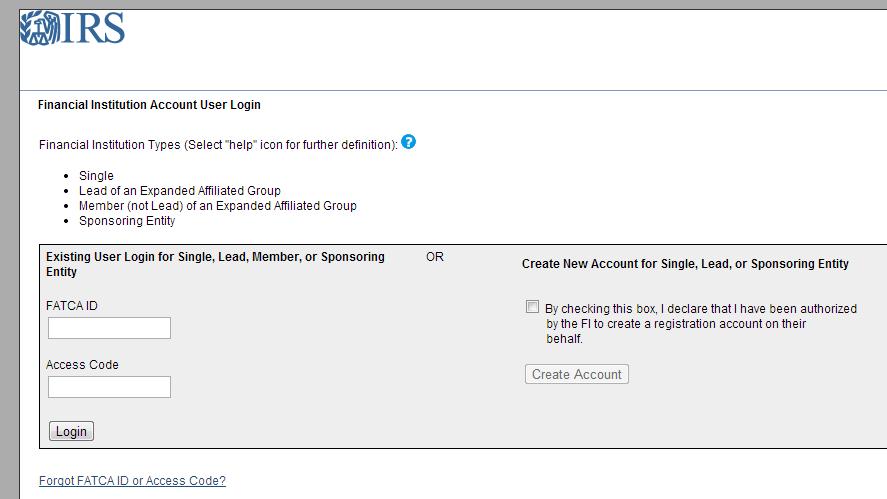

13 The Science of Finance STEPS TO COMPLIANCE PART II DUE DILIGENCE

14 FATCA Steps to Compliance Once all the entity analysis is complete, one can proceed to Due Diligence Document Collection: FATCA requires an immense amount of tax and KYC documentation collection effort. Collection of such documents per entity and proper organization of such documents is essential not only for the due diligence steps, but also for future audit prospects For FATCA due diligence purposes, the following types of documents are most relevant: Tax Documents: W-9, W-8(s) Client Ownership Structure: Org. chart, structure classification, organization contact list. Constitutional Documents: Article of Incorporation, Certificate of Formation, By-Laws, Certificate of LLP, Formation Document, Trust/ Deed Agreement, Corporate Resolutions, etc. Compliance Certifications: AML & Compliance Policy Certification, Foreign Bank Certificate, Anti- Money Laundering Letter, Bank License etc. \ 14

15 FATCA Steps to Compliance Classification and Validation are the next steps. Using the legal analyses and documents collected, an entity must decide on which of the entity FATCA classifications it falls under. Note that each of the classifications are specific to entity type and greater care at this juncture would minimize action on Change of Circumstance in the future. Once Classification has been determined, tax status must be validated using tax documents and constitutional documents. Entities may use services of third party vendor at this juncture to ensure that the tax documentation validation process has been vetted and signed off by the IRS. This also reduces future questions on validity of the tax validation process. The Sunset Rule: Generally, once a new tax form is released, the IRS provides for a 6 month sunset period. New form W-8BEN-E yet to be released should take advantage of that! \ 15

16 FATCA Steps to Compliance Pre-FATCA W8-BEN 1 page 1 form for entities & individuals BO identified and categorized in Part I Treaty benefit decided in Part II \ 16

17 FATCA Classifications FATCA Steps to Compliance \ 17

18 FATCA Steps to Compliance \ 18

19 The Science of Finance STEPS TO COMPLIANCE PART III REGISTRATION

20 FATCA Steps to Compliance The IRS Portal is the primary means for FFIs to interact with the IRS to complete and maintain their FATCA registrations, agreements and certifications. Portal is a paperless, secure & online. Portal has been open & accessible to FFIs from August FFIs are able to register as PFFIs, SEs, limited FFIs or registered deemed compliant FFIs (including Model I FFIs) Model I or Model II FFIs required to register so long as jurisdiction is identified on a list published by IRS of IGA countries, even if ratification of such IGA in the jurisdiction is not complete by July 1, 2014 Once FFI has registered, IRS will issue a Global Intermediary Identification Number ( GIIN ) to each Participating compliant FFI. GIIN will be assigned beginning no later than 2014 to be used as ID number for FFI s reporting obligations and identifying its status. Note: GIIN issue not immediate. IRS will electronically post first IRS list of PFFIs and registered deemed compliant FFIs on June 2, 2014, and will update the list on a monthly basis Last date by which a FFI can register to ensure inclusion on June 2014 FFI list is April 25, 2014 \ 20

21 FATCA Steps to Compliance Average Registration application input & submission time for each entity is expected to be about 1 hour. Does not include data to be collected on each entity before the registration process can begin. Some of the data required on each entity to be Registered are as follows: FI type (single, lead, member, or SE) FI s legal name, country of domicile/ country of residence for tax purposes. FI classification (i.e. participating FFI not covered by IGA, Reporting FI under Model UU, Limited FI etc.) FI s QI, Withholding Foreign Partnership, Withholding Foreign Trust status and EIN. Whether FI maintains branch in jurisdictions outside of its country of domicile, or the US in in the latter case, associated EINs. Business title for FATCA Responsible Officer, their contact information and legal name etc. Important to create a comprehensive checklist of information to be collected before registering on IRS Portal to reduce length of time it takes to register each entity. \ 21

22 FATCA Steps to Compliance \ 22

23 The Science of Finance STEPS TO COMPLIANCE PART IV WITHHOLDING & REPORTING

24 FATCA Steps to Compliance Withholding: No withholding for FFIs resident in IGA jurisdictions except in cases of unresolved significant non-compliance 30% Withholding for recalcitrant accounts including non-participating non-resident FFIs Withholding for New Accounts starts July 1, Withholding to be reported on form 1042-S beginning Reporting: IGA Model I to local jurisdiction. Formatting to be decided by local tax jurisdictions. IGA Model II and non- IGA jurisdiction Form 8966 or information following its directive Reporting will consist of information regarding: Substantial US owners of passive NFFEs and owner documented FFIs Certain information regarding US accounts PFFIs expected to report on payments to US Aggregate recalcitrant account information \ 24

25 Questions

26 Thank you.

27 Contact Information Sulolit Mukherjee Vice President, Global Tax Services Phone: Office Mobile \ 27

28 mines data pools intelligence surfaces information enables transparency builds platforms provides access scales volume extends networks & transforms business.

29 Disclaimer The information contained in this presentation is confidential. Any unauthorised use, disclosure, reproduction or dissemination, in full or in part, in any media or by any means, without the prior written permission of Markit Group Holdings Limited or any of its affiliates ("Markit") is strictly prohibited. Opinions, statements, estimates and projections in this presentation (including other media) are solely those of the individual author(s) at the time of writing and do not necessarily reflect the opinions of Markit. Neither Markit nor the author(s) has any obligation to update this presentation in the event that any content, opinion, statement, estimate or projection (collectively, "information") changes or subsequently becomes inaccurate. Markit makes no warranty, expressed or implied, as to the accuracy, completeness or timeliness of any information in this presentation, and shall not in any way be liable to any recipient for any inaccuracies or omissions. Without limiting the foregoing, Markit shall have no liability whatsoever to any recipient, whether in contract, in tort (including negligence), under warranty, under statute or otherwise, in respect of any loss or damage suffered by any recipient as a result of or in connection with any information provided, or any course of action determined, by it or any third party, whether or not based on any information provided. The inclusion of a link to an external website by Markit should not be understood to be an endorsement of that website or the site's owners (or their products/services). Markit is not responsible for either the content or output of external websites. Copyright 2013, Markit Group Limited. All rights reserved and all intellectual property rights are retained by Markit.

FATCA Service Bureau

2013 Processing FATCA Service Bureau A comprehensive FATCA compliance solution for the fund industry US tax law expertise Client documentation review Electronic tax form validation Secure document hosting

2013 Processing FATCA Service Bureau A comprehensive FATCA compliance solution for the fund industry US tax law expertise Client documentation review Electronic tax form validation Secure document hosting

Melissa Gow \ Director \ 9 May 2012

The Science of Finance Securities Lending Market Update CASLA Melissa Gow \ Director \ 9 May 2012 Scale of the Equity Securities Lending Market 12.0 Global Equities 10,000,000 Long-Short Ratio 11.0 10.0

The Science of Finance Securities Lending Market Update CASLA Melissa Gow \ Director \ 9 May 2012 Scale of the Equity Securities Lending Market 12.0 Global Equities 10,000,000 Long-Short Ratio 11.0 10.0

A closer look at the final regulations and the path forward

www.pwc.com FATCA A closer look at the final regulations and the path forward 19 February 2013 Circular 230: This document was not intended or written to be used, and it cannot be used, for the purpose

www.pwc.com FATCA A closer look at the final regulations and the path forward 19 February 2013 Circular 230: This document was not intended or written to be used, and it cannot be used, for the purpose

11th Annual Domestic Tax Conference. 28 April 2016 New York City

11th Annual Domestic Tax Conference 28 April 2016 New York City FATCA and other information reporting and withholding for nonfinancial services companies Disclaimer EY refers to the global organization,

11th Annual Domestic Tax Conference 28 April 2016 New York City FATCA and other information reporting and withholding for nonfinancial services companies Disclaimer EY refers to the global organization,

How Thai Financial Institutions are Preparing for FATCA s 31 Dec Deadline

How Thai Financial Institutions are Preparing for FATCA s 31 Dec Deadline AMCHAM: FATCA Overview 25 th June 2013 1 ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTENBYKPMGTOBEUSED,ANDCANNOTBEUSED,BYACLIENT

How Thai Financial Institutions are Preparing for FATCA s 31 Dec Deadline AMCHAM: FATCA Overview 25 th June 2013 1 ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTENBYKPMGTOBEUSED,ANDCANNOTBEUSED,BYACLIENT

Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations.

on multinational organizations.") Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations 1 May 2013 Disclaimer Ernst & Young refers to the global organization of member

Information reporting and withholding: the impact of Foreign Account Tax Compliance Act (FATCA) on multinational organizations 1 May 2013 Disclaimer Ernst & Young refers to the global organization of member

FOREIGN ACCOUNT TAX COMPLIANCE ACT: FINAL REGULATIONS AND CURRENT DEVELOPMENTS

FOREIGN ACCOUNT TAX COMPLIANCE ACT: FINAL REGULATIONS AND CURRENT DEVELOPMENTS J.P. Morgan Corporate & Investment Bank Presented by Client Tax Services April 2013 S T R I C T L Y P R I V A T E A N D C

FOREIGN ACCOUNT TAX COMPLIANCE ACT: FINAL REGULATIONS AND CURRENT DEVELOPMENTS J.P. Morgan Corporate & Investment Bank Presented by Client Tax Services April 2013 S T R I C T L Y P R I V A T E A N D C

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN FINANCIAL INSTITUTIONS

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN FINANCIAL INSTITUTIONS Barbados International Business Association Conference October 26, 2012 Bruce Zagaris Partner Berliner, Corcoran, & Rowe

FATCA:INVESTMENT REPORTING AND IMPLICATIONS FOR CARIBBEAN FINANCIAL INSTITUTIONS Barbados International Business Association Conference October 26, 2012 Bruce Zagaris Partner Berliner, Corcoran, & Rowe

FATCA-QIA INTERACTION

INTERNATIONAL CONFERENCE ON FATCA FATCA-QIA Laura Scapini Domenico Serranò Rome Palazzo Altieri 1 February 2013 Circular 230 Disclosure Any US tax advice contained herein was not intended or written to

INTERNATIONAL CONFERENCE ON FATCA FATCA-QIA Laura Scapini Domenico Serranò Rome Palazzo Altieri 1 February 2013 Circular 230 Disclosure Any US tax advice contained herein was not intended or written to

Foreign Account Tax Compliance Act: the Internal Revenue Service registration portal a walk through

Foreign Account Tax Compliance Act: the Internal Revenue Service registration portal a walk through Cayman Finance international tax seminar 23 January 2014 EY disclaimers Circular 230 disclaimer Any US

Foreign Account Tax Compliance Act: the Internal Revenue Service registration portal a walk through Cayman Finance international tax seminar 23 January 2014 EY disclaimers Circular 230 disclaimer Any US

Introduction to FATCA. Introduction to FATCA

Presented by: Joe Perera Strasburger & Price, LLP July 1, 2014 Agenda Legislative Purpose and Approach To Whom and To What Payments Does FATCA Apply? Rules Regarding Foreign Financial Institutions (FFIs)

Presented by: Joe Perera Strasburger & Price, LLP July 1, 2014 Agenda Legislative Purpose and Approach To Whom and To What Payments Does FATCA Apply? Rules Regarding Foreign Financial Institutions (FFIs)

Roundtable Discussion Foreign Account Tax Compliance Act (FATCA) Andrew Mitchel, Bob Rinninsland, Stan Ruchelman

Andrew Mitchel, Bob Rinninsland, Stan Ruchelman") Roundtable Discussion Foreign Account Tax Compliance Act (FATCA) Andrew Mitchel, Bob Rinninsland, Stan Ruchelman FATCA Introduction/Base Case Issues Effective March 18, 2010 enacted as part of the HIRE

Roundtable Discussion Foreign Account Tax Compliance Act (FATCA) Andrew Mitchel, Bob Rinninsland, Stan Ruchelman FATCA Introduction/Base Case Issues Effective March 18, 2010 enacted as part of the HIRE

Introduction to FATCA (Foreign Account Tax Compliance Act) Introduction to FATCA

Introduction to FATCA") (Foreign Account Tax Compliance Act) Jim Browne 214.651.4420 jim.browne@strasburger.com Joe Perera 210.250.6119 joe.perera@strasburger.com Agenda Background Rules for Withholding Agents Classification

(Foreign Account Tax Compliance Act) Jim Browne 214.651.4420 jim.browne@strasburger.com Joe Perera 210.250.6119 joe.perera@strasburger.com Agenda Background Rules for Withholding Agents Classification

Foreign Account Tax Compliance Act ( FATCA )

") Foreign Account Tax Compliance Act (FATCA) What Is It & Why Should I Care? Presented by: Cynthia J. Hoffman, CPA, J.D. Director of International Tax Advisory Services Schneider Downs & Co., Inc. April

Foreign Account Tax Compliance Act (FATCA) What Is It & Why Should I Care? Presented by: Cynthia J. Hoffman, CPA, J.D. Director of International Tax Advisory Services Schneider Downs & Co., Inc. April

The Final FATCA Regulations Are Out What Does It Mean for the Swiss Economy

The Final FATCA Regulations Are Out What Does It Mean for the Swiss Economy Erick C. Christensen Capgemini Financial Services Alan Winston Granwell DLA Piper This presentation is offered for information

The Final FATCA Regulations Are Out What Does It Mean for the Swiss Economy Erick C. Christensen Capgemini Financial Services Alan Winston Granwell DLA Piper This presentation is offered for information

IRS opens online FATCA registration system for financial institutions, issues related guidance

22 August 2013 IRS opens online FATCA registration system for financial institutions, issues related guidance Executive summary On 19 August 2013, the IRS announced the opening of the online registration

22 August 2013 IRS opens online FATCA registration system for financial institutions, issues related guidance Executive summary On 19 August 2013, the IRS announced the opening of the online registration

Securities Lending Market Update

The Science of Finance Securities Lending Market Update Sam Pierson \ Toronto \ 3 June 2015 Discussion topics Global sec lending snapshot and trends Canada sec lending snapshot and trends Canada equity

The Science of Finance Securities Lending Market Update Sam Pierson \ Toronto \ 3 June 2015 Discussion topics Global sec lending snapshot and trends Canada sec lending snapshot and trends Canada equity

FATCA the final countdown

www.pwc.co.uk TISA FATCA the final countdown 3 June 2013 Current state of play Year March 2010 What has been published? 2010 March 2010 Foreign Account Tax Compliance Act 2010 2010-2011 Aug 2010, April

www.pwc.co.uk TISA FATCA the final countdown 3 June 2013 Current state of play Year March 2010 What has been published? 2010 March 2010 Foreign Account Tax Compliance Act 2010 2010-2011 Aug 2010, April

FATCA: THE 2014 HORIZON

FATCA: THE 2014 HORIZON Breakout Session 5C FIBA 2014 AML Compliance Conference February 21, 2014 Gabriel Caballero, Esq. Gunster, Yoakley & Stewart, P.A. 2 South Biscayne Boulevard Suite #3400 Miami,

FATCA: THE 2014 HORIZON Breakout Session 5C FIBA 2014 AML Compliance Conference February 21, 2014 Gabriel Caballero, Esq. Gunster, Yoakley & Stewart, P.A. 2 South Biscayne Boulevard Suite #3400 Miami,

-Rohit Johri

FATCA Are you ready? -Rohit Johri Rohit.cfe@gmail.com 83221864 1 Disclaimer The views in this presentation belong to the speaker alone. This presentation is meant to be educational in nature and not a

FATCA Are you ready? -Rohit Johri Rohit.cfe@gmail.com 83221864 1 Disclaimer The views in this presentation belong to the speaker alone. This presentation is meant to be educational in nature and not a

FATCA Update and its Global Reach

FATCA Update and its Global Reach Sally Miller, Chief Executive Officer Institute of International Bankers FIRMA s 27 th National Risk Management Training Conference Las Vegas, Nevada May 2, 2013 1 Background

FATCA Update and its Global Reach Sally Miller, Chief Executive Officer Institute of International Bankers FIRMA s 27 th National Risk Management Training Conference Las Vegas, Nevada May 2, 2013 1 Background

KPMG TaxWatch Webcast: Final FATCA Regulations The Compliance Challenge Is On

KPMG TaxWatch Webcast: Final FATCA Regulations The Compliance Challenge Is On February 1, 2013 ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY

KPMG TaxWatch Webcast: Final FATCA Regulations The Compliance Challenge Is On February 1, 2013 ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY KPMG TO BE USED, AND CANNOT BE USED, BY

What Impact Will FATCA Have on Offshore Hedge Funds and How Should Such Funds Prepare for FATCA Compliance?

hedge LAW REPORT fund law and regulation FATCA What Impact Will FATCA Have on Offshore s and How Should Such Funds Prepare for FATCA Compliance? By Michele Gibbs Itri, Tannenbaum Helpern Syracuse & Hirschtritt,

hedge LAW REPORT fund law and regulation FATCA What Impact Will FATCA Have on Offshore s and How Should Such Funds Prepare for FATCA Compliance? By Michele Gibbs Itri, Tannenbaum Helpern Syracuse & Hirschtritt,

The Science of Finance GEMX. Randolf Tantzscher / Istanbul / June 2012

The Science of Finance GEMX Randolf Tantzscher / Istanbul / June 2012 GEMX Index Family Current countries GEMX Overall Asia EEMEA LatAm China India Indonesia Malaysia Philippines Sri Lanka Thailand Egypt

The Science of Finance GEMX Randolf Tantzscher / Istanbul / June 2012 GEMX Index Family Current countries GEMX Overall Asia EEMEA LatAm China India Indonesia Malaysia Philippines Sri Lanka Thailand Egypt

Key provisions of FATCA proposed regulations. Anastasia Urias Senior Manager

Key provisions of FATCA proposed regulations Anastasia Urias Senior Manager 1. Overview of keypoints 1 2 Significant highlights of FATCA FATCA was worked out by the United States of America in 2010. The

Key provisions of FATCA proposed regulations Anastasia Urias Senior Manager 1. Overview of keypoints 1 2 Significant highlights of FATCA FATCA was worked out by the United States of America in 2010. The

Abuse that Spawned FATCA

IFA USA Young IFA Network (YIN) International Tax Webinar April 27, 2012 FATCA Impact on International Business Transactions: Proposed Regulations and Other New Issues SPEAKERS Michael Hirschfeld Partner,

IFA USA Young IFA Network (YIN) International Tax Webinar April 27, 2012 FATCA Impact on International Business Transactions: Proposed Regulations and Other New Issues SPEAKERS Michael Hirschfeld Partner,

CRS/FATCA Entity Self-Certification

CRS/FATCA Entity Self-Certification Entities are required to notify Value Partners Investments ("VPI") in writing within 30 days of any change in circumstances (e.g., name or structure changes). In such

CRS/FATCA Entity Self-Certification Entities are required to notify Value Partners Investments ("VPI") in writing within 30 days of any change in circumstances (e.g., name or structure changes). In such

FATCA / AEOI Update. Current Status and Action Points for Cayman Entities. April 2016

FATCA / AEOI Update Current Status and Action Points for Cayman Entities April 2016 Current Status of FATCA and CRS in Cayman Current Position - FATCA Model 1 Intergovernmental Agreements ( IGA s) were

FATCA / AEOI Update Current Status and Action Points for Cayman Entities April 2016 Current Status of FATCA and CRS in Cayman Current Position - FATCA Model 1 Intergovernmental Agreements ( IGA s) were

Self Certification for Entity Clients U.S. Foreign Account Tax Compliance Act (FATCA) and the OECD Common Reporting Standard (CRS)

and the OECD Common Reporting Standard (CRS)") The require Deutsche Bank AG and its affiliates (collectively Deutsche Bank ) to collect and report certain tax related information about its clients. Please complete the sections below as directed and

The require Deutsche Bank AG and its affiliates (collectively Deutsche Bank ) to collect and report certain tax related information about its clients. Please complete the sections below as directed and

Guidance Notes on the requirements of the Intergovernmental Agreement between the United Arab Emirates and the United States

Guidance Notes on the requirements of the Intergovernmental Agreement between the United Arab Emirates and the United States Issue Date: 5 September 2016 Last Updated: 5 September 2016 Document Ref: UAE

Guidance Notes on the requirements of the Intergovernmental Agreement between the United Arab Emirates and the United States Issue Date: 5 September 2016 Last Updated: 5 September 2016 Document Ref: UAE

FATCA self-certification form

FATCA self-certification form We, the undersigned, representing, Registered Company name (in full) Trade name (if different from registered) hereby confirm to Clearstream Banking S.A. ( CBL ) our FATCA

FATCA self-certification form We, the undersigned, representing, Registered Company name (in full) Trade name (if different from registered) hereby confirm to Clearstream Banking S.A. ( CBL ) our FATCA

FATCA : Essentials and deadlines Overview of the main provisions and the key dates of the FATCA regulations

FATCA : Essentials and deadlines Overview of the main provisions and the key dates of the FATCA regulations July 2014 Tassos Yiasemides, Board Member Panayiotis Tziongouros, Supervisor Contents 1.0 FATCA

FATCA : Essentials and deadlines Overview of the main provisions and the key dates of the FATCA regulations July 2014 Tassos Yiasemides, Board Member Panayiotis Tziongouros, Supervisor Contents 1.0 FATCA

US FATCA and Its Impact on Retirement Funds. David W. Powell Principal Groom Law Group, Washington, DC

US FATCA and Its Impact on Retirement Funds David W. Powell Principal Groom Law Group, Washington, DC 1 Agenda US FATCA withholding and why non-us retirement funds should care Retirement plan exemptions

US FATCA and Its Impact on Retirement Funds David W. Powell Principal Groom Law Group, Washington, DC 1 Agenda US FATCA withholding and why non-us retirement funds should care Retirement plan exemptions

US Regulations

January 2015 Tax alert Cayman Islands FATCA tax alert Get the facts on FATCA! You can access current FATCA news and thought leadership. Type into your web browser: www.ey.com/fatca. On 4 July 2014, the

January 2015 Tax alert Cayman Islands FATCA tax alert Get the facts on FATCA! You can access current FATCA news and thought leadership. Type into your web browser: www.ey.com/fatca. On 4 July 2014, the

FATCA Workshop for Portfolio Managers

FATCA Workshop for Portfolio Managers Moderator: Michael Friedman, McMillan LLP Speakers Hugh Chasmar, Tax Partner, Deloitte Carlos Amoranto, Amoranto Consulting Carl Irvine, McMillan LLP David Sausen,

FATCA Workshop for Portfolio Managers Moderator: Michael Friedman, McMillan LLP Speakers Hugh Chasmar, Tax Partner, Deloitte Carlos Amoranto, Amoranto Consulting Carl Irvine, McMillan LLP David Sausen,

Foreign Account Tax Compliance Act Trust Update

Frank Hirth plc T +44 (0)20 7833 3500 1st Floor, 236 Gray s Inn Road F +44 (0)20 7833 2550 London WC1X 8HB E mail@frankhirth.com United Kingdom W www.frankhirth.com Foreign Account Tax Compliance Act Trust

Frank Hirth plc T +44 (0)20 7833 3500 1st Floor, 236 Gray s Inn Road F +44 (0)20 7833 2550 London WC1X 8HB E mail@frankhirth.com United Kingdom W www.frankhirth.com Foreign Account Tax Compliance Act Trust

Key Points in New W-8IMY Instructions

Key Points in New W-8IMY Instructions On June 19, the IRS finally released instructions to the new W-8IMY. Form W-8IMY, Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S.

Key Points in New W-8IMY Instructions On June 19, the IRS finally released instructions to the new W-8IMY. Form W-8IMY, Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S.

Ministry of Finance Bermuda

Ministry of Finance Bermuda FREQUENTLY ASKED QUESTIONS (FAQ) ON THE INTERNATIONAL TAX COMPLIANCE REQUIREMENTS OF THE INTERGOVERNMENTAL AGREEMENTS BETWEEN BERMUDA AND THE UNITED STATES OF AMERICA AND THE

Ministry of Finance Bermuda FREQUENTLY ASKED QUESTIONS (FAQ) ON THE INTERNATIONAL TAX COMPLIANCE REQUIREMENTS OF THE INTERGOVERNMENTAL AGREEMENTS BETWEEN BERMUDA AND THE UNITED STATES OF AMERICA AND THE

Markit Auctions. PENNVEST Nutrient Credit Trading Program Spot Auction Participation Phase Markit / New York / October 22, 2014

Markit Auctions PENNVEST Nutrient Credit Trading Program Spot Auction Participation Phase Markit / New York / October 22, 2014 Company overview -- Markit Markit is a leading, global financial information

Markit Auctions PENNVEST Nutrient Credit Trading Program Spot Auction Participation Phase Markit / New York / October 22, 2014 Company overview -- Markit Markit is a leading, global financial information

Determining U.S. Beneficial Ownership of Foreign Entities.

Date: 08/16/2013 TITLE Header F.A.T.C.A. Determining U.S. Beneficial Ownership of Foreign Entities. Presented by: Jose A. Romero, LL.M. Head of the Corporate Team / LATAM Curaçao Office Copyright Notice:

Date: 08/16/2013 TITLE Header F.A.T.C.A. Determining U.S. Beneficial Ownership of Foreign Entities. Presented by: Jose A. Romero, LL.M. Head of the Corporate Team / LATAM Curaçao Office Copyright Notice:

Sight FATCA. line of. Frequently asked questions. table of contents. November 2, 2012

line of Sight FATCA Frequently asked questions FOR INSTITUTIONAL INVESTORS table of contents November 2, 2012 PART I PROPOSED REGULATIONS and IRS Announcement OVERVIEW 1. What is the objective of the Foreign

line of Sight FATCA Frequently asked questions FOR INSTITUTIONAL INVESTORS table of contents November 2, 2012 PART I PROPOSED REGULATIONS and IRS Announcement OVERVIEW 1. What is the objective of the Foreign

FATCA: Why all Cayman Islands domiciled Investment Entities should act before the registration deadline of 31 December 2014

FATCA: Why all Cayman Islands domiciled Investment Entities should act before the registration deadline of 31 December 2014 Registration with the IRS The broad scope of the Foreign Account Tax Compliance

FATCA: Why all Cayman Islands domiciled Investment Entities should act before the registration deadline of 31 December 2014 Registration with the IRS The broad scope of the Foreign Account Tax Compliance

Who Must Provide Form W-8BEN-E

applicable, the withholding agent may rely on the Form W-8BEN-E to apply a reduced rate of, or exemption from, withholding. If you receive certain types of income, you must provide Form W-8BEN-E to: Claim

applicable, the withholding agent may rely on the Form W-8BEN-E to apply a reduced rate of, or exemption from, withholding. If you receive certain types of income, you must provide Form W-8BEN-E to: Claim

Markit iboxx Total Return Swaps

Markit iboxx Total Return Swaps Full First Coupon Trading Convention Copyright 2016 Markit Ltd Introduction 3 iboxx Standardised TRS 3 Introduction of the Full First Coupon 4 Floating Rate Determination

Markit iboxx Total Return Swaps Full First Coupon Trading Convention Copyright 2016 Markit Ltd Introduction 3 iboxx Standardised TRS 3 Introduction of the Full First Coupon 4 Floating Rate Determination

FATCA: Updates and Coordinating Regulations

FATCA: Updates and Coordinating Regulations Treasury Releases Last Substantial Regulations Package Necessary to Implement FATCA SUMMARY On February 20, 2014, the IRS and the Treasury Department issued

FATCA: Updates and Coordinating Regulations Treasury Releases Last Substantial Regulations Package Necessary to Implement FATCA SUMMARY On February 20, 2014, the IRS and the Treasury Department issued

WHITE PAPER. Impact of FATCA on Client Onboarding Achieve FATCA compliance with effective, result-oriented IT and operational changes

WHITE PAPER Impact of FATCA on Client Onboarding Achieve FATCA compliance with effective, result-oriented IT and operational changes In March 2010, the Foreign Account Tax Compliance Act (FATCA) was enacted

WHITE PAPER Impact of FATCA on Client Onboarding Achieve FATCA compliance with effective, result-oriented IT and operational changes In March 2010, the Foreign Account Tax Compliance Act (FATCA) was enacted

Are you ready for the upcoming margin rules? ISDA Amend webcast August 11th 2016

Are you ready for the upcoming margin rules? ISDA Amend webcast August 11th 2016 1 Speakers Katherine Tew Darras, General Counsel, ISDA Douglas J. Donahue, Partner, Mayer Brown LLP Samantha Riley, Assistant

Are you ready for the upcoming margin rules? ISDA Amend webcast August 11th 2016 1 Speakers Katherine Tew Darras, General Counsel, ISDA Douglas J. Donahue, Partner, Mayer Brown LLP Samantha Riley, Assistant

FATCA: An Update for STEP

FATCA: An Update for STEP N I C O L A V I R G I L L - R O L L E, P H D D I R E C T O R O F F I N A N C I A L S E R V I C E S M I N I S T R Y O F F I N A N C I A L S E R V I C E S 29 TH J A N U A R Y, 2

FATCA: An Update for STEP N I C O L A V I R G I L L - R O L L E, P H D D I R E C T O R O F F I N A N C I A L S E R V I C E S M I N I S T R Y O F F I N A N C I A L S E R V I C E S 29 TH J A N U A R Y, 2

Foreign Withholding Rules & FATCA

Foreign Withholding Rules & FATCA J. Brian Davis Douglas M. Andre Agenda Introduction and Scope Chapter 3 ( FDAP ) Withholding Chapter 4 ( FATCA ) Withholding Withholding Audits Problem Areas and Recent

Foreign Withholding Rules & FATCA J. Brian Davis Douglas M. Andre Agenda Introduction and Scope Chapter 3 ( FDAP ) Withholding Chapter 4 ( FATCA ) Withholding Withholding Audits Problem Areas and Recent

Fiduciary and Investment Risk Management Association 28 th National Risk Management Training Conference

Fiduciary and Investment Risk Management Association 28 th National Risk Management Training Conference Foreign Account Tax Compliance Act: Considerations for Trusts April 30, 2014 Michael Shepard Principal

Fiduciary and Investment Risk Management Association 28 th National Risk Management Training Conference Foreign Account Tax Compliance Act: Considerations for Trusts April 30, 2014 Michael Shepard Principal

Instructions for Form W-8BEN-E (Rev. July 2017)

") Instructions for Form W-8BEN-E (Rev. July 2017) Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) Department of the Treasury Internal Revenue Service

Instructions for Form W-8BEN-E (Rev. July 2017) Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities) Department of the Treasury Internal Revenue Service

FATCA for Trusts and Trustees

FATCA for Trusts and Trustees Ruby Banipal May 1, 2015 Presentation for TTN Conference (Miami) Agenda Executive Summary Background: Why was FATCA Created How FATCA Works Impact on Private Clients FATCA

FATCA for Trusts and Trustees Ruby Banipal May 1, 2015 Presentation for TTN Conference (Miami) Agenda Executive Summary Background: Why was FATCA Created How FATCA Works Impact on Private Clients FATCA

GOVERNMENT OF SEYCHELLES

GOVERNMENT OF SEYCHELLES GUIDANCE NOTES ON THE COMPLIANCE REQUIREMENTS OF THE INTERGOVERNMENTAL AGREEMENT BETWEEN THE SEYCHELLES AND THE UNITED STATES OF AMERICA VERSION 1.0 DATE OF ISSUE While every effort

GOVERNMENT OF SEYCHELLES GUIDANCE NOTES ON THE COMPLIANCE REQUIREMENTS OF THE INTERGOVERNMENTAL AGREEMENT BETWEEN THE SEYCHELLES AND THE UNITED STATES OF AMERICA VERSION 1.0 DATE OF ISSUE While every effort

Foreign Account Tax Compliance Act (FATCA)

") www.pwc.com Foreign Account Tax Compliance Act (FATCA) IRS Revenue Procedure 2014-13 FFI Agreement for Participating FFI and Reporting Model 2 FFI Released December 27, 2013 No claim to original U.S. Government

www.pwc.com Foreign Account Tax Compliance Act (FATCA) IRS Revenue Procedure 2014-13 FFI Agreement for Participating FFI and Reporting Model 2 FFI Released December 27, 2013 No claim to original U.S. Government

Withholding Certificates and Self-Certifications under FATCA

American Journal of Economics and Business Administration Review Articles Withholding Certificates and Self-Certifications under FATCA Stefan Kaestli Institute of Economics of the Polish Academy of Sciences,

American Journal of Economics and Business Administration Review Articles Withholding Certificates and Self-Certifications under FATCA Stefan Kaestli Institute of Economics of the Polish Academy of Sciences,

STEP Lausanne / Luncheon Meeting FATCA and the Trust Industry - Current Practical Issues. Erol Baruh

STEP Lausanne / Luncheon Meeting FATCA and the Trust Industry - Current Practical Issues Erol Baruh Table of Contents 1. Introduction 2. Classification of entities (FFI vs. NFFE) 3. Compliance method 4.

STEP Lausanne / Luncheon Meeting FATCA and the Trust Industry - Current Practical Issues Erol Baruh Table of Contents 1. Introduction 2. Classification of entities (FFI vs. NFFE) 3. Compliance method 4.

Foreign Account Tax Compliance Act (FATCA)

") www.pwc.com Foreign Account Tax Compliance Act (FATCA) FFI agreement for Participating FFI and Reporting Model 2 FFI Released October 29, 2013 No claim to original U.S. Government works This page intentionally

www.pwc.com Foreign Account Tax Compliance Act (FATCA) FFI agreement for Participating FFI and Reporting Model 2 FFI Released October 29, 2013 No claim to original U.S. Government works This page intentionally

FATCA: Impact on Cayman Islands Entities

FATCA: Impact on Cayman Islands Entities Preface This publication provides a brief overview of the impact on entities incorporated in the Cayman Islands of the foreign account tax compliance provisions

FATCA: Impact on Cayman Islands Entities Preface This publication provides a brief overview of the impact on entities incorporated in the Cayman Islands of the foreign account tax compliance provisions

Guidance Notes on the Implementation of FATCA in Ireland. Supplementary FAQ s

Guidance Notes on the Implementation of FATCA in Ireland Supplementary FAQ s These Frequently Asked Questions (FAQ s) are designed to supplement the Guidance Notes on the Implementation of FATCA in Ireland

Guidance Notes on the Implementation of FATCA in Ireland Supplementary FAQ s These Frequently Asked Questions (FAQ s) are designed to supplement the Guidance Notes on the Implementation of FATCA in Ireland

U.S. tax authorities issue guidance on foreign account tax compliance

U.S. tax authorities issue guidance on foreign account tax compliance The U.S. Treasury Department and the Internal Revenue Service (IRS) on 27 August 2010 issued initial and lengthy guidance under new

U.S. tax authorities issue guidance on foreign account tax compliance The U.S. Treasury Department and the Internal Revenue Service (IRS) on 27 August 2010 issued initial and lengthy guidance under new

Proposed Qualified Intermediary Agreement

www.pwc.de Proposed Qualified Intermediary Agreement Notice 2016-42 with a preamble by PwC The document referenced by this document is Notice 2016-42, released by the Internal Revenue Service on 1 July

www.pwc.de Proposed Qualified Intermediary Agreement Notice 2016-42 with a preamble by PwC The document referenced by this document is Notice 2016-42, released by the Internal Revenue Service on 1 July

The new W-8IMY: An Accounts Payable Perspective

The new W-8IMY: An Accounts Payable Perspective (and for those who just need an introduction to the form) On June 19, the IRS finally released instructions to the new W-8IMY. The form had been released

The new W-8IMY: An Accounts Payable Perspective (and for those who just need an introduction to the form) On June 19, the IRS finally released instructions to the new W-8IMY. The form had been released

Are you prepared for the next wave of margin rules? ISDA Amend webcast October 26th 2016

Are you prepared for the next wave of margin rules? ISDA Amend webcast October 26th 2016 1 Speakers Katherine Tew Darras, General Counsel, ISDA Douglas J. Donahue, Partner, Mayer Brown LLP Darren Thomas,

Are you prepared for the next wave of margin rules? ISDA Amend webcast October 26th 2016 1 Speakers Katherine Tew Darras, General Counsel, ISDA Douglas J. Donahue, Partner, Mayer Brown LLP Darren Thomas,

Explanations of Foreign Account Tax Compliance Acts (FATCA) and Common Reporting Standard (CRS) Terms used in the Application Form

and Common Reporting Standard (CRS) Terms used in the Application Form") Explanations of Foreign Account Tax Compliance Acts (FATCA) and Common Reporting Standard (CRS) Terms used in the Application Form Account Holder The term "Account Holder" (under CRS and FATCA) means the

Explanations of Foreign Account Tax Compliance Acts (FATCA) and Common Reporting Standard (CRS) Terms used in the Application Form Account Holder The term "Account Holder" (under CRS and FATCA) means the

Glossary. Canadian Financial Institution

Glossary Active Non-Financial Foreign Entity (ANFFE) Canadian Financial Institution Controlling Persons Deemed Compliant Foreign Financial Institution Excepted Foreign Financial Institution (EFFI) Exempted

Glossary Active Non-Financial Foreign Entity (ANFFE) Canadian Financial Institution Controlling Persons Deemed Compliant Foreign Financial Institution Excepted Foreign Financial Institution (EFFI) Exempted

FATCA Frequently Asked Questions (FAQs) Closing the distance

Closing the distance") FATCA Frequently Asked Questions (FAQs) Closing the distance Global Financial Services Industry 1. What is FATCA? FATCA stands for the Foreign Account Tax Compliance Act. It colloquially refers to provisions

FATCA Frequently Asked Questions (FAQs) Closing the distance Global Financial Services Industry 1. What is FATCA? FATCA stands for the Foreign Account Tax Compliance Act. It colloquially refers to provisions

W8-BEN-E Definitions and Validation Instructions

W8-BEN-E Definitions and Validation Instructions This document is for information purposes only and does not constitute advice. If any person reading this document requires further information they should

W8-BEN-E Definitions and Validation Instructions This document is for information purposes only and does not constitute advice. If any person reading this document requires further information they should

CLSA (UK) FATCA ANNEX

FATCA ANNEX") CLSA (UK) FATCA ANNEX 1. Definitions and Interpretation 1.1. In this FATCA Annex, including the Schedules hereto, capitalized terms have the meaning given to them in the "General Terms and Conditions of

CLSA (UK) FATCA ANNEX 1. Definitions and Interpretation 1.1. In this FATCA Annex, including the Schedules hereto, capitalized terms have the meaning given to them in the "General Terms and Conditions of

(Rev. June 2017) General Instructions. Purpose of Form. What s New

General Instructions. Purpose of Form. What s New") Department of the Treasury Instructions for Form W-8IMY Internal Revenue Service (Rev. June 2017) Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States

Department of the Treasury Instructions for Form W-8IMY Internal Revenue Service (Rev. June 2017) Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States

Instructions to the Entity Self Certification Form

Section A General Instructions to the Entity Self Certification Form 1. Foreign Account Tax Compliance Act (FATCA) FATCA is a component of the Hiring Incentives to Restore Employment Act (the HIRE Act),

Section A General Instructions to the Entity Self Certification Form 1. Foreign Account Tax Compliance Act (FATCA) FATCA is a component of the Hiring Incentives to Restore Employment Act (the HIRE Act),

FATCA: Final Regulations

Treasury Issues Long-Awaited Final Regulations on FATCA; U.S. Enters into Related Intergovernmental Agreement with Switzerland SUMMARY On January 17, 2013, the Treasury Department issued final regulations

Treasury Issues Long-Awaited Final Regulations on FATCA; U.S. Enters into Related Intergovernmental Agreement with Switzerland SUMMARY On January 17, 2013, the Treasury Department issued final regulations

FATCA: impact on data management. Jacob Gertel, Business Development April 2014

FATCA: impact on data management Jacob Gertel, Business Development April Agenda Introduction IRS Final Regulation and Amendments Highlights SIX Financial Information Data Offering Issuer Level Classification

FATCA: impact on data management Jacob Gertel, Business Development April Agenda Introduction IRS Final Regulation and Amendments Highlights SIX Financial Information Data Offering Issuer Level Classification

Client Alert. IRS Releases Final FATCA Regulations. Summary. Background

Number 1460 January 29, 2013 Client Alert Latham & Watkins Tax Department IRS Releases Final FATCA Regulations Summary The Regulations represent a significant step towards FATCA implementation, yet considerable

Number 1460 January 29, 2013 Client Alert Latham & Watkins Tax Department IRS Releases Final FATCA Regulations Summary The Regulations represent a significant step towards FATCA implementation, yet considerable

Bank Depository User Group Annual Meeting Foreign Account Tax Compliance Act (FATCA)

") www.pwc.com/us Bank Depository User Group Annual Meeting Foreign Account Tax Compliance Act (FATCA) October 23, 2012 Kenneth LaManna Agenda General overview and concepts Planning for compliance FATCA certification

www.pwc.com/us Bank Depository User Group Annual Meeting Foreign Account Tax Compliance Act (FATCA) October 23, 2012 Kenneth LaManna Agenda General overview and concepts Planning for compliance FATCA certification

Swiss Amercian Chamber of Commerce

US Clients and US Securities - No more? FATCA, Voluntary Disclosure, Estate Tax, Regulatory Requirements and more Swiss Amercian Chamber of Commerce 20 April 2011 FATCA in a Museum of Art? 20 April 2011

US Clients and US Securities - No more? FATCA, Voluntary Disclosure, Estate Tax, Regulatory Requirements and more Swiss Amercian Chamber of Commerce 20 April 2011 FATCA in a Museum of Art? 20 April 2011

taxnotes Agreement international by Denise Hintzke and Kelly Cruze Reprinted from Tax Notes Int l, August 29, 2016, p. 789

taxnotes The Impact of the Proposed U.S. QI Agreement by Denise Hintzke and Kelly Cruze Reprinted from Tax Notes Int l, August 29, 2016, p. 789 international Volume 83, Number 9 August 29, 2016 The Impact

taxnotes The Impact of the Proposed U.S. QI Agreement by Denise Hintzke and Kelly Cruze Reprinted from Tax Notes Int l, August 29, 2016, p. 789 international Volume 83, Number 9 August 29, 2016 The Impact

Part I Identification of Entity 1 Name of individual or organization that is acting as intermediary 2 Country of incorporation or organization

! " " # $ % $ & ' % ( ) # ( * " ) % $ & + %, $ ) - +. $! $ * # # * " ) % $ & + %, $ ) - +! $ * # / ( % + 0 " 1 # 2 $ * # / %! + $ +! % # % 3 + % $ $ # + $ 3 $ % $ & %, $ ) - # % $ & % # 4 % ) 0 4 1 % )

! " " # $ % $ & ' % ( ) # ( * " ) % $ & + %, $ ) - +. $! $ * # # * " ) % $ & + %, $ ) - +! $ * # / ( % + 0 " 1 # 2 $ * # / %! + $ +! % # % 3 + % $ $ # + $ 3 $ % $ & %, $ ) - # % $ & % # 4 % ) 0 4 1 % )

AML & KYC QUESTIONNAIRE FOR FINANCIAL INSTITUTIONS

AML & KYC QUESTIONNAIRE FOR FINANCIAL INSTITUTIONS SECTION 1 - GENERAL INFORMATION 1.1. Full name of institution 1.2. Legal form 1.3. Legal address 1.4. Phone and fax numbers 1.5. Official website 1.6.

AML & KYC QUESTIONNAIRE FOR FINANCIAL INSTITUTIONS SECTION 1 - GENERAL INFORMATION 1.1. Full name of institution 1.2. Legal form 1.3. Legal address 1.4. Phone and fax numbers 1.5. Official website 1.6.

Automatic Exchange of Information (AEI) Foreign Account Tax Compliance Act (FATCA)

Foreign Account Tax Compliance Act (FATCA)") Automatic Exchange of Information (AEI) Foreign Account Tax Compliance Act (FATCA) Addendum to UBS Self-Certification Forms with additional explanations of AEI / FATCA terms for Switzerland Please note:

Automatic Exchange of Information (AEI) Foreign Account Tax Compliance Act (FATCA) Addendum to UBS Self-Certification Forms with additional explanations of AEI / FATCA terms for Switzerland Please note:

U.S. Tax and Estate Law Impacting Canadian Clients. March 6, 2013

U.S. Tax and Estate Law Impacting Canadian Clients March 6, 2013 Agenda Changes to U.S. Tax Rates U.S. Tax Status FATCA Registration as a Participating FFI Americans Investing in Canadian Mutual Funds

U.S. Tax and Estate Law Impacting Canadian Clients March 6, 2013 Agenda Changes to U.S. Tax Rates U.S. Tax Status FATCA Registration as a Participating FFI Americans Investing in Canadian Mutual Funds

FATCA: Developments & Perspective

www.pwc.de FATCA: Developments & Perspective Luxembourg May 5, 2014 Agenda Section 1: Section 2: Section 3: Section 4: Section 5: Introduction Update to the Financial Account Tax Compliance Act Update

www.pwc.de FATCA: Developments & Perspective Luxembourg May 5, 2014 Agenda Section 1: Section 2: Section 3: Section 4: Section 5: Introduction Update to the Financial Account Tax Compliance Act Update

FATCA: IMPLEMENTATION IN THREE STEPS

FATCA: IMPLEMENTATION IN THREE STEPS Latin American financial institutions will be exposed to the risk of sanctions by the "Internal Revenue Service" or the "IRS", the largest and most powerful tax collection

FATCA: IMPLEMENTATION IN THREE STEPS Latin American financial institutions will be exposed to the risk of sanctions by the "Internal Revenue Service" or the "IRS", the largest and most powerful tax collection

Foreign Account Tax Compliance Act (FATCA)

") www.pwc.com Foreign Account Tax Compliance Act (FATCA) IRS Revenue Procedure 2014-13 FFI Agreement for Participating FFI and Reporting Model 2 FFI Released December 27, 2013 Formatted redline comparing

www.pwc.com Foreign Account Tax Compliance Act (FATCA) IRS Revenue Procedure 2014-13 FFI Agreement for Participating FFI and Reporting Model 2 FFI Released December 27, 2013 Formatted redline comparing

FATCA: Impact on Mauritius Entities

FATCA: Impact on Mauritius Entities Foreword This publication provides a brief overview of the expected impact on entities resident in the Republic of Mauritius ( Mauritius ) of the foreign account tax

FATCA: Impact on Mauritius Entities Foreword This publication provides a brief overview of the expected impact on entities resident in the Republic of Mauritius ( Mauritius ) of the foreign account tax

SWISS TRUSTEES AND B OARD MEMBERS OF FOUNDATIO NS HAVE TO PREPARE FOR F.A.T.C.A.

SWISS TRUSTEES AND B OARD MEMBERS OF FOUNDATIO NS HAVE TO PREPARE FOR F.A.T.C.A. Authors* Natalie Peter Peter Altenburger Tags F.A.T.C.A. Switzerland U.K. Liechtenstein Natalie Peter (LLM Boston University)

SWISS TRUSTEES AND B OARD MEMBERS OF FOUNDATIO NS HAVE TO PREPARE FOR F.A.T.C.A. Authors* Natalie Peter Peter Altenburger Tags F.A.T.C.A. Switzerland U.K. Liechtenstein Natalie Peter (LLM Boston University)

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. April 2018) Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For

Instructions for the Requester of Forms W 8BEN, W 8BEN E, W 8ECI, W 8EXP, and W 8IMY (Rev. April 2018) Section references are to the Internal Revenue Code unless otherwise noted. Future developments. For

Certain investment entities that do not maintain financial Nonparticipating foreign financial institution (FFI) (including an FFI

(including an FFI") Form W-8IMY (Rev. June 2017) Department of the Treasury Internal Revenue Service Do not use this form for: Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for

Form W-8IMY (Rev. June 2017) Department of the Treasury Internal Revenue Service Do not use this form for: Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for

Implications of FATCA for legal entities

Implications of FATCA for legal entities April 2015 Introduction FATCA and its context Page 3 Section 1 Application variants and entities concerned Page 4 Section 2 Classification of entities under FATCA

Implications of FATCA for legal entities April 2015 Introduction FATCA and its context Page 3 Section 1 Application variants and entities concerned Page 4 Section 2 Classification of entities under FATCA

Tax Compliance: International Exchange of Information Agreement. Tax Residence Self-Certification Form Entities

Tax Compliance: International Exchange of Information Agreement Tax Residence Self-Certification Form Entities Document Guide Part 1: Entity Details Part 2: Current Residence Address Part 3: Jurisdiction

Tax Compliance: International Exchange of Information Agreement Tax Residence Self-Certification Form Entities Document Guide Part 1: Entity Details Part 2: Current Residence Address Part 3: Jurisdiction

Guidelines for Completion of the Form W-8BEN-E and Foreign Account Tax Compliance Act (FATCA) Entity Classification Guide

Entity Classification Guide") Guidelines for Completion of the Form W-8BEN-E and Foreign Account Tax Compliance Act (FATCA) Entity Classification Guide This information is made available for general reference only. It does not constitute

Guidelines for Completion of the Form W-8BEN-E and Foreign Account Tax Compliance Act (FATCA) Entity Classification Guide This information is made available for general reference only. It does not constitute

MSA EMEA ETP Report. Full year 2016 review of ETP trade volumes. February 2017

MSA EMEA ETP Report Full year 2016 review of ETP trade volumes February 2017 2 Market Share Analysis (MSA) Markit s Trading Analytics platform delivers a full suite of tools to facilitate the measurement

MSA EMEA ETP Report Full year 2016 review of ETP trade volumes February 2017 2 Market Share Analysis (MSA) Markit s Trading Analytics platform delivers a full suite of tools to facilitate the measurement

Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches for United States Tax Withholding and Reporting

For. W-8IMY (Rev. April 2014) Department of the Treasury Internal Revenue Service Do not use this form for: Part I Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches

For. W-8IMY (Rev. April 2014) Department of the Treasury Internal Revenue Service Do not use this form for: Part I Certificate of Foreign Intermediary, Foreign Flow-Through Entity, or Certain U.S. Branches

Tax Information Authority

Tax Information Authority CAYMAN ISLANDS GUIDANCE NOTES ON THE INTERNATIONAL TAX COMPLIANCE REQUIREMENTS OF THE INTERGOVERNMENTAL AGREEMENTS BETWEEN THE CAYMAN ISLANDS AND THE UNITED STATES OF AMERICA

Tax Information Authority CAYMAN ISLANDS GUIDANCE NOTES ON THE INTERNATIONAL TAX COMPLIANCE REQUIREMENTS OF THE INTERGOVERNMENTAL AGREEMENTS BETWEEN THE CAYMAN ISLANDS AND THE UNITED STATES OF AMERICA

Tax Year 2016 Form 1042-S FAQs

Tax Year 2016 Form 1042-S FAQs Q: WHY DID I RECEIVE A FORM 1042-S? A: Form 1042-S reports ordinary dividend, long-term capital gain income, and short-term capital gain income earned in accounts by non-resident

Tax Year 2016 Form 1042-S FAQs Q: WHY DID I RECEIVE A FORM 1042-S? A: Form 1042-S reports ordinary dividend, long-term capital gain income, and short-term capital gain income earned in accounts by non-resident

Foreign Account Tax Compliance Act (FATCA) Implications, Considerations and Responses

Implications, Considerations and Responses") Foreign Account Tax Compliance Act (FATCA) Implications, Considerations and Responses The Foreign Account Tax Compliance Act (FATCA) was enacted on March 18, 2010, by the U.S. Congress as part of the Hiring

Foreign Account Tax Compliance Act (FATCA) Implications, Considerations and Responses The Foreign Account Tax Compliance Act (FATCA) was enacted on March 18, 2010, by the U.S. Congress as part of the Hiring

Cayman Islands Mutual Funds

Cayman Islands Mutual Funds Preface This publication has been prepared for the assistance of those who are considering the formation of a mutual fund in the Cayman Islands. It deals in broad terms with

Cayman Islands Mutual Funds Preface This publication has been prepared for the assistance of those who are considering the formation of a mutual fund in the Cayman Islands. It deals in broad terms with

The Foreign Account and Tax Compliance Act (FATCA)

") The Foreign Account and Tax Compliance Act (FATCA) Highlights of the Proposed Regulations Jonathan Sambur Donald Morris + 1 202 263-3256 +1 312 701 7126 jsambur@mayerbrown.com dmorris@mayerbrown.com April

The Foreign Account and Tax Compliance Act (FATCA) Highlights of the Proposed Regulations Jonathan Sambur Donald Morris + 1 202 263-3256 +1 312 701 7126 jsambur@mayerbrown.com dmorris@mayerbrown.com April

Automatic Exchange of Information (AEOI) CRS and FATCA Regulatory Compliance Your Foundation in a Changing World

CRS and FATCA Regulatory Compliance Your Foundation in a Changing World") Automatic Exchange of Information (AEOI) CRS and FATCA Regulatory Compliance Your Foundation in a Changing World An Automated Solution for Global Reporting Compliance Evolving international tax regulations

Automatic Exchange of Information (AEOI) CRS and FATCA Regulatory Compliance Your Foundation in a Changing World An Automated Solution for Global Reporting Compliance Evolving international tax regulations

FORM 2C TRUST ACCOUNT AND ENTITY DECLARATION FORM

TRUST ACCOUNT AND ENTITY DECLARATION FORM Post this form to ANZ Investments, Freepost 324, PO Box 7149, Wellesley Street, Auckland 1141. Under New Zealand law, ANZ Investments must collect a declaration

TRUST ACCOUNT AND ENTITY DECLARATION FORM Post this form to ANZ Investments, Freepost 324, PO Box 7149, Wellesley Street, Auckland 1141. Under New Zealand law, ANZ Investments must collect a declaration

Markit economic overview

Markit Economics Markit economic overview Faltering US economy leads global slowdown March 9 th 2016 Global economic growth slides to weakest for nearly 3 ½ years Global economic growth slowed to near-stagnation

Markit Economics Markit economic overview Faltering US economy leads global slowdown March 9 th 2016 Global economic growth slides to weakest for nearly 3 ½ years Global economic growth slowed to near-stagnation