IAS 12 Corporation Tax Presentation by: Mbiki Kamanjiri Manager, Tax Consulting Grant Thornton

|

|

|

- Milo McGee

- 5 years ago

- Views:

Transcription

1 IAS 12 Corporation Tax Presentation by: Mbiki Kamanjiri Manager, Tax Consulting Grant Thornton

2 Agenda 01 Introduction 02 Taxation of Corporate entities 03 Transfer pricing 04 Thin Cap and Deemed Interest 05 Tax Planning 06 Consequences and penalties

3 Introduction 3

4 Introduction Pharisees tested Jesus Is it lawful to pay taxes to Ceasar?

5 Introduction

6 Taxation of Corporate Entities Thoughts? 6

7 Taxation of Corporate Entities Resident 30%* Non-resident 37.5% *Reduced corporation tax rates for newly listed companies, approved under the Capital Markets Act (CMA), are available as follows: Shareholding Timelines Rates With 20% issued shares listed First 3 years after listing 27% With 30% issued shares listed First 5 years after listing 25% With 40% issued shares listed First 5 years after listing 20%

First 10 years 10 Next 10 years 15 Thereafter 30")

8 Taxation of Corporate Entities Corporation tax rates for Special Economic Zones Entities Period Rate (%) First 10 years 10 Next 10 years 15 Thereafter 30 Industries

9 Other rates Export processing zone 15% Car manufacturing 15% 400 housing units

10 Payment of taxes Two methods Current year: Four quarterly instalments based on expected profits Penalty if estimation is under 10% of actual profits Prior year: 110% of last years taxes Into four instalments

11 Computation of taxable income

12 Allowable expenses Expenditure wholly and exclusively incurred in the production of income for that year of income Legal expenses and stamp duties on acquiring a lease on premises not exceeding 99 years Legal and other costs in publicly issuing shares and debentures Capital allowances Expenses incurred prior to the commencement of business that would have been deductible if incurred after the date of commencement

13 Allowable expenses Expenditure on agricultural land clearance and planting of semi/permanent crops Cost of structural alterations to premises, incurred by a landlord to maintain the rent (non-capital) Expenses incurred by a lessee, in leasing transactions Interest paid on borrowings made to generate investment income (but restricted to the amount of investment income earned) Expenditure on scientific research

14 Allowable expenses Donations to approved charitable organisations Bad debts written off which satisfy the following: Commissioner s guidelines: The debt was wholly and exclusively incurred in the normal course of business; The debt is not of a capital nature; and The debt has become uncollectable

15 Bad debts A debt is uncollectable where: The creditor loses the contractual right of a debt through a court order; No form of security or collateral is realizable; The securities or collateral realized are unable to cover the entire debt; The debtor is adjudged insolvent or bankrupt by a court of law; The costs of recovering the debt exceeds the debt itself; or Efforts to collect the debt are abandoned for another reasonable cause

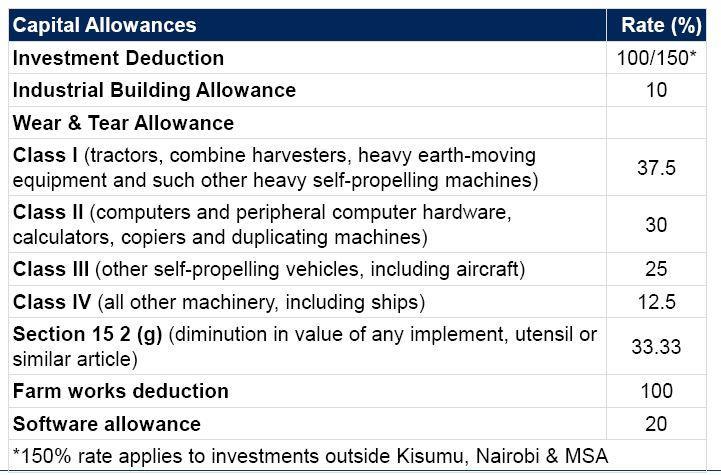

16 Capital Allowances

17 Disallowable Expenditure not wholly and exclusively incurred in the production of income Capital costs and losses Income tax, compensating tax and similar taxes Personal expenses, other than those incurred specifically in the course of business Expenses of non-resident persons relating to certain types of income interest, management fees, royalties etc Pension contributions to unregistered pension schemes

18 Corporation taxes Current year Prior year Estimation of current years tax payable Current year basis is more appropriate where the operating results fluctuate substantially. In case of variance of 10% or more, penalties and interest are levied 25% of 110%of tax assessed for the previous year.

19 Excess pension Section 22A of the ITA KES 20,000 allowed to registered scheme per employee per month Consider the employees contribution first including NSSF Whatever remains can be attributed to employer

20 Transfer Pricing Updates 20

21 Transfer Pricing Definition: the setting of the price for goods and services sold between controlled (or related) legal entities within an enterprise. For example, if a subsidiary company sells goods to a parent company, the cost of those goods paid by the parent to the subsidiary is the transfer price.

22 Transfer Pricing Arm s length price Focus under BEPS [Where] conditions are made or imposed between the two [associated] enterprises in their commercial or financial relations which differ from those which would be made between independent enterprises, then any profits which would, but for those conditions, have accrued to one of the enterprises, but, by reason of those conditions, have not so accrued, may be included in the profits of that enterprise and taxed accordingly Value creation

23 BEPS Developments Work on harmful practices Action 5 Tax treaty abuse Action 6 Action 13 Country by Country Reporting Dispute resolution mechanisms Action 14

24 Thin Cap & Deemed Interest 24

25 Thin Cap & Deemed Interest Thin Cap When a company s* capital is made up of a much greater proportion of debt than equity, i.e. its gearing or leverage, is too high it is said to be thinly capitalised. *Not applicable to financial institutions licensed under Banking Act

26 Thin cap provisions Section 16(2)(j) For purposes of ascertaining the total income of a person, no deduction shall be allowed in respect of interest payments in proportion to the extent that the highest amount of all loans held by the company at any time during the year of income exceeds the greater of: three times the sum of the revenue reserves and the issued and paid up capital of all classes of shares of the company;

27 Deemed interest or an amount of deemed interest where the company is in the control of a non-resident person alone or together with four or fewer other persons and where the company is not a bank or a financial institution licensed under the Banking Act Provided that this paragraph shall also apply to loans advanced to the company by a nonresident associate of the non-resident company controlling the resident company

28 Thin Cap Deemed interest Implications: Mutually exclusive loans, overdrafts, ordinary trade debts, overdrawn current accounts or any other form of indebtedness Restrict interest Restrict forex losses. Pay withholding tax

29 Capital gains tax Gain = Consideration Adjusted cost CGT = 5% of gain Incidental costs may include fees, commission or remuneration to surveyor, valuer, accountant, agent or legal adviser Costs of transfer including Stamp duty and advertising costs *Payable on 20 th day after transfer of property

30 Recent Changes Special economic zones Exempt Withholding Tax on dividends to non residents Reduced Withholding tax on interest from 15% to 5% Reduced management fees and royalties from 20% to 5% Building costs and machinery 100% allowance Exemption from Export duty and Import Declaration Fees Transfer Pricing introduced for transactions between resident entities of the SEZ / EPZ and related entities outside SEZ / EPZ

31 Recent Changes Betting, gaming and Lotteries Gaming tax from 12% to 50% Betting tax 7.5% to 50% Lottery tax from 5% to 50% Prize competitions tax from 15% to 50%

32 Tax planning 32

33 Tax planning Debt as a tool for tax planning Share Capital Debt Capital PBIT 150, ,000 Interest on shareholder's loan - 100,000 Taxable profit 150,000 50,000 45,000 15,000 Dividends 105,000 35,000 Interest - 100,000 Total Shareholders return 105, ,000

34 Tax planning Managem ent fees Dividends Royalties Interest UK 12.5% 10% 15% 15% Germany 15% 10% 15% 15% &Canada Denmark 20% 10% 20% 15% Norway Sweden Zambia India 17.5% 10% 20% 15% France nil 10% 10% 12% Netherlands nil nil* 10% 10% Mauritius^ nil 5%* 10% 10% South Africa nil 10% 10% 10% Italy nil 10% 20% 15%

35 Consequences and penalties of noncompliance 35

36 Cost of getting it wrong Offense Person liable to tax for failing to register for taxes Penalty KES 100,000 per month subject to a maximum of KES 1 million Failure to keep documents KES 100,000 or 10% of the amount of tax payable to which the document relates to Late submission of tax return on account of employment income Late submission of tax return (individuals and corporates) Late submission of tax return on account of Turnover tax Failure to comply with electronic tax systems The higher of 25% of the tax due or KES 10,000 The higher of 5% of the tax due or KES 20,000 KES 5,000 KES 100,000 Tax Avoidance Double the amount of tax Tax refund fraud Two times the amount of the claim

37 Definitions Tax evasion Intentionally failing to disclose taxable income to tax authorities Tax avoidance tax avoidance is the legal use of tax laws to reduce one's tax burden.

38 Tax shortfall Penalty 75% 20% 10% 25% 10% If omission is made deliberately In any other case Increase if second time Increase if third time Decrease on self declaration

39 Q&A 5 th Floor, Avocado Towers, Muthithi Road, Westlands, Nairobi Kenya T F Mbiki Kamanjiri Manager Tax Consulting Services Cell E ; mbiki.kamanjiri@ke.gt.com

Tax Procedures Act Grant Thornton International Ltd. All rights reserved.

Tax Procedures Act 2015 Changes in Tax Administration VAT Act 2013 Finance Act 2016 Tax Appeals Tribunal Act 2013 Tax Procedures Act,, 2015 Finance Act 2017 New Income Tax Act? Excise Duty Act 2015 Tax

Tax Procedures Act 2015 Changes in Tax Administration VAT Act 2013 Finance Act 2016 Tax Appeals Tribunal Act 2013 Tax Procedures Act,, 2015 Finance Act 2017 New Income Tax Act? Excise Duty Act 2015 Tax

Tax Healtchecks. Mbiki 2016 Grant Thornton International Ltd. All rights reserved.

Tax Healtchecks Mbiki Kamanjiri @ 2016 Grant Thornton International Ltd. All rights reserved. Preamble Section 15(2)(g) Then the Pharisees went and plotted how they might entangle Him in His talk.. Is

Tax Healtchecks Mbiki Kamanjiri @ 2016 Grant Thornton International Ltd. All rights reserved. Preamble Section 15(2)(g) Then the Pharisees went and plotted how they might entangle Him in His talk.. Is

CORPORATION TAX Presentation by: Daniel Masaku Senior Tax Consultant, Ernst & Young LLP Thursday, 12 th April Uphold public interest

CORPORATION TAX Presentation by: Daniel Masaku Senior Tax Consultant, Ernst & Young LLP Thursday, 12 th April 2018 Uphold public interest Presentation Outline Taxation of Corporate Entities Allowable &

CORPORATION TAX Presentation by: Daniel Masaku Senior Tax Consultant, Ernst & Young LLP Thursday, 12 th April 2018 Uphold public interest Presentation Outline Taxation of Corporate Entities Allowable &

Nairobi GMT +3. EY +254 (20) Mail address: Fax: +254 (20)

Mail address: Fax: +254 (20)") Kenya 717 ey.com/globaltaxguides ey.com/taxguidesapp Nairobi GMT +3 EY +254 (20) 271-5300 Mail address: Fax: +254 (20) 271-6271 P.O. Box 44286 00100 Email: info@ey.co.ke Nairobi GPO Kenya Street address:

Kenya 717 ey.com/globaltaxguides ey.com/taxguidesapp Nairobi GMT +3 EY +254 (20) 271-5300 Mail address: Fax: +254 (20) 271-6271 P.O. Box 44286 00100 Email: info@ey.co.ke Nairobi GPO Kenya Street address:

FOREWORD. Kenya. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

FOREWORD. Kenya. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Budget Statement 2017 Highlights

Budget Statement 2017 Highlights Mbiki Kamanjiri Manager - Tax Economic Review Global Outlook 1.5% 1.5% 1.7% 3.0% 3.1% 2.7% 6.0% 1.8% 2.9% 4.8% 5.9% African Outlook 4.3% 4.0% 2016 2017 6.6% 6.3% -1.7%

Budget Statement 2017 Highlights Mbiki Kamanjiri Manager - Tax Economic Review Global Outlook 1.5% 1.5% 1.7% 3.0% 3.1% 2.7% 6.0% 1.8% 2.9% 4.8% 5.9% African Outlook 4.3% 4.0% 2016 2017 6.6% 6.3% -1.7%

Global Mobility Services: Taxation of International Assignees Kenya

www.pwc.com/ke/en Global Mobility Services: Taxation of International Assignees Kenya People and Organisation Global Mobility Country Guide (Folio) Last Updated: May 2018 This document was not intended

www.pwc.com/ke/en Global Mobility Services: Taxation of International Assignees Kenya People and Organisation Global Mobility Country Guide (Folio) Last Updated: May 2018 This document was not intended

Morocco Tax Guide 2012

Tax Guide 2012 structure of country descriptions a. taxes payable FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER

Tax Guide 2012 structure of country descriptions a. taxes payable FEDERAL TAXES AND LEVIES COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX SALES TAX/VALUE ADDED TAX FRINGE BENEFITS TAX LOCAL TAXES OTHER

ICPAK Tax Workshop. Employee Taxation. Withholding tax. 24 January /27/2014 1

ICPAK Tax Workshop Employee Taxation Withholding tax 24 January 2014 1/27/2014 1 Employee Taxation The tax year for individuals runs from 1 January to 31 December Chargeable Income: For each year of income

ICPAK Tax Workshop Employee Taxation Withholding tax 24 January 2014 1/27/2014 1 Employee Taxation The tax year for individuals runs from 1 January to 31 December Chargeable Income: For each year of income

ICPAK Annual Tax Conference

ICPAK Annual Tax Conference Income Tax Reforms: Is it time? 20 September 2013 PRESENTER: Francis Kamau, CPA Corporation Tax Determination of a PE Section 2 - defines a permanent establishment ( PE ) as

ICPAK Annual Tax Conference Income Tax Reforms: Is it time? 20 September 2013 PRESENTER: Francis Kamau, CPA Corporation Tax Determination of a PE Section 2 - defines a permanent establishment ( PE ) as

TAXATION OF EMPLOYEE EMOLUMENTS AND WITHHOLDING TAX OBLIGATIONS Presentation by: Mary Weru. Uphold public interest

TAXATION OF EMPLOYEE EMOLUMENTS AND WITHHOLDING TAX OBLIGATIONS Presentation by: Mary Weru Uphold public interest Presentation agenda Employee taxes Basis of taxation Residence rules Income subject to

TAXATION OF EMPLOYEE EMOLUMENTS AND WITHHOLDING TAX OBLIGATIONS Presentation by: Mary Weru Uphold public interest Presentation agenda Employee taxes Basis of taxation Residence rules Income subject to

*Transcending Business Confidence PROVISIONAL AUDITAX TAX GUIDE 2016 /

*Transcending Business Confidence PROVISIONAL AUDITAX TAX GUIDE 2016 / 2017 www.auditaxinternational.com DIRECT TAXES Payroll Taxes Pay As You Earn (PAYE) Monthly Taxable Income Tax Rate Up to TZS. 170,000

*Transcending Business Confidence PROVISIONAL AUDITAX TAX GUIDE 2016 / 2017 www.auditaxinternational.com DIRECT TAXES Payroll Taxes Pay As You Earn (PAYE) Monthly Taxable Income Tax Rate Up to TZS. 170,000

International Tax Kenya Highlights 2019

International Tax Updated February 2019 For the latest tax developments relating to Kenya, see Deloitte tax@hand. Investment basics: Currency Kenyan Shilling (KES) Foreign exchange control No, but banks

International Tax Updated February 2019 For the latest tax developments relating to Kenya, see Deloitte tax@hand. Investment basics: Currency Kenyan Shilling (KES) Foreign exchange control No, but banks

Tax principles workshop : The Building blocks of a sound tax system

Tax principles workshop : The Building blocks of a sound tax system 27 January 2017 CPA Starlings Muchiri Partner East African Tax Consulting Mobile: 0722 33 27 29 Email: starlings@taxeac.com INCOME TAX

Tax principles workshop : The Building blocks of a sound tax system 27 January 2017 CPA Starlings Muchiri Partner East African Tax Consulting Mobile: 0722 33 27 29 Email: starlings@taxeac.com INCOME TAX

FOREWORD. Isle of Man

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Ghana Tax Guide 2012

Ghana Tax Guide 2012 I IMPORTANT DISCLAIMER: No person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice

Ghana Tax Guide 2012 I IMPORTANT DISCLAIMER: No person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice

INCOME TAX BILL, 2018

INCOME TAX BILL, 2018 ALERT ALGERIA BOTSWANA ETHIOPIA GUINEA KENYA MADAGASCAR MALAWI MAURITIUS MOROCCO MOZAMBIQUE NIGERIA RWANDA SUDAN TANZANIA UGANDA ZAMBIA REGIONAL OFFICE: UAE ASSOCIATE FIRM: SOUTH

INCOME TAX BILL, 2018 ALERT ALGERIA BOTSWANA ETHIOPIA GUINEA KENYA MADAGASCAR MALAWI MAURITIUS MOROCCO MOZAMBIQUE NIGERIA RWANDA SUDAN TANZANIA UGANDA ZAMBIA REGIONAL OFFICE: UAE ASSOCIATE FIRM: SOUTH

Tanzania Tax Data 2013/2014

Tanzania tax datacard 2013/2014 Income tax - Corporations Corporation rate Capital deductions Resident corporation 30 Non-resident corporation* 30 Newly listed companies - reduced rate for 3 years** 25

Tanzania tax datacard 2013/2014 Income tax - Corporations Corporation rate Capital deductions Resident corporation 30 Non-resident corporation* 30 Newly listed companies - reduced rate for 3 years** 25

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Withholding Tax Training for NPOs Presentation by:

Withholding Tax Training for NPOs Presentation by: Caleb Mokaya CPA Friday, 12 th May 2017 Presentation Outline 1 2 3 4 5 6 7 8 Overview of Withholding Tax (WHT) Payments Subject to WHT Legal provisions

Withholding Tax Training for NPOs Presentation by: Caleb Mokaya CPA Friday, 12 th May 2017 Presentation Outline 1 2 3 4 5 6 7 8 Overview of Withholding Tax (WHT) Payments Subject to WHT Legal provisions

Excise Duty & Miscellaneous Fees and Levies. Mbiki Kamanjiri

Excise Duty & Miscellaneous Fees and Levies Mbiki Kamanjiri History of Excise 1972 Customs and Excise Act, Cap 472. Excise Regulations 2013 Finance Act 2016 30 Mar 2017 Remission Regulations EACCMA Repeals

Excise Duty & Miscellaneous Fees and Levies Mbiki Kamanjiri History of Excise 1972 Customs and Excise Act, Cap 472. Excise Regulations 2013 Finance Act 2016 30 Mar 2017 Remission Regulations EACCMA Repeals

Intra-Group Services & Intangibles

Intra-Group Services & Intangibles Mbiki Kamanjiri @ 2016 Grant Thornton All rights reserved. What is covered under Intangible Property Definition: Property with no physical existence but whose value depends

Intra-Group Services & Intangibles Mbiki Kamanjiri @ 2016 Grant Thornton All rights reserved. What is covered under Intangible Property Definition: Property with no physical existence but whose value depends

Objection to Commissioner Within 30 days having paid tax not in dispute Commissioner to respond within 60 days

1 Procedure Objection to Commissioner Within 30 days having paid tax not in dispute Commissioner to respond within 60 days High Court If still aggrieved by decision by TAT one may appeal to High Court

1 Procedure Objection to Commissioner Within 30 days having paid tax not in dispute Commissioner to respond within 60 days High Court If still aggrieved by decision by TAT one may appeal to High Court

Recent Updates on Tax Case Law Presentation by: Mbiki Kamanjiri Manager, Tax Consulting Grant Thornton

Recent Updates on Tax Case Law Presentation by: Mbiki Kamanjiri Manager, Tax Consulting Grant Thornton Uphold public interest 1 Objections and Appeals Process Procedure Objection to Commissioner Within

Recent Updates on Tax Case Law Presentation by: Mbiki Kamanjiri Manager, Tax Consulting Grant Thornton Uphold public interest 1 Objections and Appeals Process Procedure Objection to Commissioner Within

T H E C Y P R U S F I N A N C E C O M P A N Y

T H E C Y P R U S F I N A N C E C O M P A N Y The contents of this publication are for information purposes only and can not be construed as providing any advice on matters including, but not restricted

T H E C Y P R U S F I N A N C E C O M P A N Y The contents of this publication are for information purposes only and can not be construed as providing any advice on matters including, but not restricted

Global Mobility Services: Taxation of International Assignees - Zambia

www.pwc.com/zm/en Global Mobility Services: Taxation of International Assignees - Zambia Taxation issues & related matters for employers & employees 2018 Last Updated: May 2018 This document was not intended

www.pwc.com/zm/en Global Mobility Services: Taxation of International Assignees - Zambia Taxation issues & related matters for employers & employees 2018 Last Updated: May 2018 This document was not intended

Tax Card With effect from 1 January 2016 Lithuania. KPMG Baltics, UAB. kpmg.com/lt

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Tax Card 2016 With effect from 1 January 2016 Lithuania KPMG Baltics, UAB kpmg.com/lt CORPORATE INCOME TAX Taxable profit of Lithuanian and foreign corporate taxpayers is subject to a standard (flat) rate

Withholding Tax (WHT) Presentation by: Robert Waruiru Associate Director, KPMG Advisory Services Limited CPA-K April 2018

Presentation by: Robert Waruiru Associate Director, KPMG Advisory Services Limited CPA-K April 2018") Withholding Tax (WHT) Presentation by: Robert Waruiru Associate Director, KPMG Advisory Services Limited CPA-K April 2018 TABLE OF CONTENTS Introduction: What is Withholding Tax? WHT for residents and

Withholding Tax (WHT) Presentation by: Robert Waruiru Associate Director, KPMG Advisory Services Limited CPA-K April 2018 TABLE OF CONTENTS Introduction: What is Withholding Tax? WHT for residents and

Kenya. Individual Taxation. Abbreviations. References. Latest Information: Author Catherine Mutava

Kenya Individual Taxation Author Catherine Mutava Latest Information: This chapter is based on information available up to 4 October 2017. Please find below the main changes made to this chapter up to

Kenya Individual Taxation Author Catherine Mutava Latest Information: This chapter is based on information available up to 4 October 2017. Please find below the main changes made to this chapter up to

Zambia's 2019 National Budget: Tax Data Card. What next? Zambia Budget 2019 Tax Data Card

Zambia's National Budget: Tax Data Card What next? Zambia Budget Tax Data Card www.pwc.com/zm Corporate tax rates Standard rate 3 3 Banks 3 3 Turnover tax levied on business with turnover below 8, Income

Zambia's National Budget: Tax Data Card What next? Zambia Budget Tax Data Card www.pwc.com/zm Corporate tax rates Standard rate 3 3 Banks 3 3 Turnover tax levied on business with turnover below 8, Income

0 Uganda Fiscal Guide 2015/2016. Tax. kpmg.com

0 Uganda Fiscal Guide 2015/2016 Tax kpmg.com 1 Uganda Nigeria Fiscal Guide 2013/2014 2015/2016 INTRODUCTION Uganda Fiscal Guide 2015/2016 2 Basis of taxation Income tax is levied on both companies and

0 Uganda Fiscal Guide 2015/2016 Tax kpmg.com 1 Uganda Nigeria Fiscal Guide 2013/2014 2015/2016 INTRODUCTION Uganda Fiscal Guide 2015/2016 2 Basis of taxation Income tax is levied on both companies and

0 Zimbabwe Fiscal Guide 2015/2016. Tax. kpmg.com

0 Zimbabwe Fiscal Guide 2015/2016 Tax kpmg.com 1 Zimbabwe Nigeria Fiscal Fiscal Guide Guide 2013/2014 2015/2016 INTRODUCTION Zimbabwe Fiscal Guide 2015/2016 2 Business income Tax is levied on a source

0 Zimbabwe Fiscal Guide 2015/2016 Tax kpmg.com 1 Zimbabwe Nigeria Fiscal Fiscal Guide Guide 2013/2014 2015/2016 INTRODUCTION Zimbabwe Fiscal Guide 2015/2016 2 Business income Tax is levied on a source

Chapter 11 Tax System

Chapter 11 Tax System www.pwc.com/mt/doingbusiness Doing Business in Malta Principal taxes The principal taxes under Maltese law are: Income tax, which includes tax on income and on capital gains of individuals,

Chapter 11 Tax System www.pwc.com/mt/doingbusiness Doing Business in Malta Principal taxes The principal taxes under Maltese law are: Income tax, which includes tax on income and on capital gains of individuals,

Finance Bill 2017 Analysis

Finance Bill 2017 Analysis April 2017 Income Tax Changes Focus area Proposed change and KPMG comments Effective Taxation of Islamic Financial Arrangement Proposed amendment to Section 2 The Bill proposes

Finance Bill 2017 Analysis April 2017 Income Tax Changes Focus area Proposed change and KPMG comments Effective Taxation of Islamic Financial Arrangement Proposed amendment to Section 2 The Bill proposes

Tax data card 2018/2019

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

Tax data card 2018/2019 1 Contents 1 Individuals and trusts 4 Companies 5 Capital allowances 6 Capital gains tax 7 Tax Administration Act penalties 8 Value-added tax 8 Other taxes, duties & levies 10 Exchange

IAS 12 Income Tax Presentation by: CPA John Waihenya Senior Associate, Tax Consulting Grant Thornton

IAS 12 Income Tax Presentation by: CPA John Waihenya Senior Associate, Tax Consulting Grant Thornton Introduction 2 Course objectives By the end of this course you should; 1. Know the components making

IAS 12 Income Tax Presentation by: CPA John Waihenya Senior Associate, Tax Consulting Grant Thornton Introduction 2 Course objectives By the end of this course you should; 1. Know the components making

Dar es Salaam GMT +3. EY +255 (22) Mail address: Fax: +255 (22) P.O. Box 2475 Dar es Salaam Tanzania

Mail address: Fax: +255 (22) P.O. Box 2475 Dar es Salaam Tanzania") 1358 ey.com/globaltaxguides ey.com/taxguidesapp Dar es Salaam GMT +3 EY +255 (22) 266-7227 Mail address: Fax: +255 (22) 266-6948 P.O. Box 2475 Dar es Salaam Street address: Utalii House 36 Laibon Road

1358 ey.com/globaltaxguides ey.com/taxguidesapp Dar es Salaam GMT +3 EY +255 (22) 266-7227 Mail address: Fax: +255 (22) 266-6948 P.O. Box 2475 Dar es Salaam Street address: Utalii House 36 Laibon Road

ALBANIA TAX CARD 2017

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

ALBANIA TAX CARD 2017 TAX CARD 2017 ALBANIA Table of Contents 1. Individuals 1.1 Personal Income Tax 1.1.1 Tax Rates 1.1.2 Taxable Income 1.1.3 Exempt Income 1.1.4 Deductible Expenses 1.2 Social Security

Tax Card KPMG in Macedonia. kpmg.com/mk

Tax Card 2016 KPMG in Macedonia kpmg.com/mk TAXATION OF CORPORATE PROFITS Corporate income tax (CIT) is due from profits realized by resident legal entities as well as by non-residents with a permanent

Tax Card 2016 KPMG in Macedonia kpmg.com/mk TAXATION OF CORPORATE PROFITS Corporate income tax (CIT) is due from profits realized by resident legal entities as well as by non-residents with a permanent

FOREWORD. Zimbabwe. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Namibia Tax Reference and Rate card

www.pwc.com/na Namibia Tax Reference and Rate card 2015/2016 Source basis of Income Tax Normal tax is levied on taxable income of companies, trusts and individuals from sources within or deemed to be within

www.pwc.com/na Namibia Tax Reference and Rate card 2015/2016 Source basis of Income Tax Normal tax is levied on taxable income of companies, trusts and individuals from sources within or deemed to be within

FOREWORD. Cyprus. Services provided by member firms include:

216/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

216/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

FOREWORD. Rwanda. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

COMPARISON OF EUROPEAN HOLDING COMPANY REGIMES

COMPARISON OF EUROPEAN HOLDING COMPANY REGIMES This analysis provides an indicative guide only and advice from appropriate country specialists should always be sought. Particular attention should be given

COMPARISON OF EUROPEAN HOLDING COMPANY REGIMES This analysis provides an indicative guide only and advice from appropriate country specialists should always be sought. Particular attention should be given

Taxation of Public Benefit Organizations. Uphold public interest

Taxation of Public Benefit Organizations Uphold public interest Presentation by: Caleb Mokaya Friday, 15 th September 2017 Presentation agenda Introduction Corporate Tax Consideration Tax Obligations General

Taxation of Public Benefit Organizations Uphold public interest Presentation by: Caleb Mokaya Friday, 15 th September 2017 Presentation agenda Introduction Corporate Tax Consideration Tax Obligations General

Paper F6 (CHN) Taxation (China) Tuesday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (China) Tuesday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (China) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Fundamentals Level Skills Module Taxation (China) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

HOSPITALITY INDUSTRY 9 th February 2012

HOSPITALITY INDUSTRY 9 th February 2012 Taxation Julius Mwatu CFO Indigo Telecom Council Member - ICPAK Tax some sort of food? Tax The Tax Structure Tax Direct Taxes Indirect Taxes Income Taxes VAT Personal

HOSPITALITY INDUSTRY 9 th February 2012 Taxation Julius Mwatu CFO Indigo Telecom Council Member - ICPAK Tax some sort of food? Tax The Tax Structure Tax Direct Taxes Indirect Taxes Income Taxes VAT Personal

KPMG Japan tax newsletter

Japan tax newsletter KPMG Tax Corporation 24 December 2015 KPMG Japan tax newsletter Amended Japan-Germany Tax Treaty 1. Preamble... 2 2. Hybrid Entities (Article 1)... 2 3. Business Profits (Article 7)...

Japan tax newsletter KPMG Tax Corporation 24 December 2015 KPMG Japan tax newsletter Amended Japan-Germany Tax Treaty 1. Preamble... 2 2. Hybrid Entities (Article 1)... 2 3. Business Profits (Article 7)...

Oil and gas taxation in Namibia Deloitte taxation and investment guides

Oil and gas taxation in Namibia Deloitte taxation and investment guides Contents 1.0 Summary 1 2.0 Corporate income tax 1 2.1 In general 1 2.2 Rates 1 2.3 Taxable income 1 2.4 Revenue 2 2.5 Deductions

Oil and gas taxation in Namibia Deloitte taxation and investment guides Contents 1.0 Summary 1 2.0 Corporate income tax 1 2.1 In general 1 2.2 Rates 1 2.3 Taxable income 1 2.4 Revenue 2 2.5 Deductions

1993 Income and Capital Gains Tax Convention

1993 Income and Capital Gains Tax Convention Treaty Partners: Ghana; United Kingdom Signed: January 20, 1993 In Force: August 10, 1994 Effective: In Ghana, from January 1, 1995. In the U.K.: income tax

1993 Income and Capital Gains Tax Convention Treaty Partners: Ghana; United Kingdom Signed: January 20, 1993 In Force: August 10, 1994 Effective: In Ghana, from January 1, 1995. In the U.K.: income tax

FOREWORD. Saint Lucia

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

1. GENERAL 2 2. SUMMARY OF THE PRINCIPAL CHANGES INCOME TAX (AMENDMENT) ACT COMMENTARY ON THE INCOME TAX 6-9 (AMENDMENT) ACT 2001

ACT COMMENTARY ON THE INCOME TAX 6-9 (AMENDMENT) ACT 2001") CONTENTS PAGE 1. GENERAL 2 2. SUMMARY OF THE PRINCIPAL CHANGES INCOME TAX (AMENDMENT) ACT 2001 3-4 3. COMMENTARY ON THE INCOME TAX 6-9 (AMENDMENT) ACT 2001 3. OTHER MATTERS 10-11 4. ZAMBIA REVENUE AUTHORITY

CONTENTS PAGE 1. GENERAL 2 2. SUMMARY OF THE PRINCIPAL CHANGES INCOME TAX (AMENDMENT) ACT 2001 3-4 3. COMMENTARY ON THE INCOME TAX 6-9 (AMENDMENT) ACT 2001 3. OTHER MATTERS 10-11 4. ZAMBIA REVENUE AUTHORITY

The UK Holding Company in light of recent developments

The UK Holding Company in light of recent developments Dr. Cristiano Medori ACA ATII ATT Senior International Tax Manager 38 Wigmore Street, London UK Holding Company Equity Debt Interest Upon incorporation

The UK Holding Company in light of recent developments Dr. Cristiano Medori ACA ATII ATT Senior International Tax Manager 38 Wigmore Street, London UK Holding Company Equity Debt Interest Upon incorporation

Mauritius Taxes Overview

Mauritius Taxes Overview Mauritius personal Income Tax Mauritius personal tax rate is a flat 15%. As from 1 January 2010, the fiscal year will be on a calendar year basis. Income Tax is payable by residents

Mauritius Taxes Overview Mauritius personal Income Tax Mauritius personal tax rate is a flat 15%. As from 1 January 2010, the fiscal year will be on a calendar year basis. Income Tax is payable by residents

FOREWORD. Gambia. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Convention. between. New Zealand and Japan. for the. Avoidance of Double Taxation. and the Prevention of Fiscal Evasion

Convention between New Zealand and Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income New Zealand and Japan, Desiring to conclude a new Convention

Convention between New Zealand and Japan for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income New Zealand and Japan, Desiring to conclude a new Convention

Tax Alert. Draft Income Tax Bill, In this bulletin... Introduction 2 Proposed tax rates 3 Capital gains tax 7

Tax Alert Draft Income Tax Bill, 2018 In this bulletin... Introduction 2 Proposed tax rates 3 Capital gains tax 7 May 2018 Taxation of dividends 7 Taxation of debt 8 Loss carry forward period 9 Income

Tax Alert Draft Income Tax Bill, 2018 In this bulletin... Introduction 2 Proposed tax rates 3 Capital gains tax 7 May 2018 Taxation of dividends 7 Taxation of debt 8 Loss carry forward period 9 Income

International Tax Singapore Highlights 2018

International Tax Singapore Highlights 2018 Investment basics: Currency Singapore Dollar (SGD) Foreign exchange control There are no significant restrictions on foreign exchange transactions and capital

International Tax Singapore Highlights 2018 Investment basics: Currency Singapore Dollar (SGD) Foreign exchange control There are no significant restrictions on foreign exchange transactions and capital

Taxation of NGOs Presentation by:

Taxation of NGOs Presentation by: Caleb Mokaya CPA Thursday, 11 th May 2017 Upholding Public Interest Table of contents 1. Background 2. Registration 3. Corporation Tax 4. Value Added Tax 5. Customs and

Taxation of NGOs Presentation by: Caleb Mokaya CPA Thursday, 11 th May 2017 Upholding Public Interest Table of contents 1. Background 2. Registration 3. Corporation Tax 4. Value Added Tax 5. Customs and

Income Tax Act Review Presentation by: Stanley Ngundi Tax Manager, Ernst and Young LLP

Income Tax Act Review Presentation by: Stanley Ngundi Tax Manager, Ernst and Young LLP Its Time! The National Treasury has commenced the review of the present Income Tax Act in order to make it productive,

Income Tax Act Review Presentation by: Stanley Ngundi Tax Manager, Ernst and Young LLP Its Time! The National Treasury has commenced the review of the present Income Tax Act in order to make it productive,

Company Tax Return Preparation Checklist 2017

COMPANY TAX RETURN PREPARATION CHECKLIST 2017 This checklist should be completed in conjunction with the preparation of tax reconciliation return workpapers. The checklist provides a general list of major

COMPANY TAX RETURN PREPARATION CHECKLIST 2017 This checklist should be completed in conjunction with the preparation of tax reconciliation return workpapers. The checklist provides a general list of major

LIST OF ABBREVIATIONS...III LIST OF LEGAL REFERENCES... IV PART I. IMPLEMENTATION OF THE DIRECTIVE... V 1. INTRODUCTION... V

UNITED KINGDOM 535 Page ii OUTLINE LIST OF ABBREVIATIONS...III LIST OF LEGAL REFERENCES... IV PART I. IMPLEMENTATION OF THE DIRECTIVE... V 1. INTRODUCTION... V 1.1. GENERAL INFORMATION ON THE IMPLEMENTATION

UNITED KINGDOM 535 Page ii OUTLINE LIST OF ABBREVIATIONS...III LIST OF LEGAL REFERENCES... IV PART I. IMPLEMENTATION OF THE DIRECTIVE... V 1. INTRODUCTION... V 1.1. GENERAL INFORMATION ON THE IMPLEMENTATION

Direct Tax and Employee Tax Bootcamp

Direct Tax and Employee Tax Bootcamp Deloitte Place, Nairobi November 2016 Contents Corporation Tax Withholding Tax Pay As You Earn 2014 Deloitte & Touche 2 Corporation Tax 2016 Deloitte & Touche 3 Outline

Direct Tax and Employee Tax Bootcamp Deloitte Place, Nairobi November 2016 Contents Corporation Tax Withholding Tax Pay As You Earn 2014 Deloitte & Touche 2 Corporation Tax 2016 Deloitte & Touche 3 Outline

EY +233 (302) , Mail address: Fax: +233 (302) P.O. Box KA KIA Accra Ghana

, Mail address: Fax: +233 (302) P.O. Box KA KIA Accra Ghana") 490 Ghana ey.com/globaltaxguides ey.com/taxguidesapp Accra GMT EY +233 (302) 779-868, 779-223 Mail address: Fax: +233 (302) 778-894 P.O. Box KA 16009 KIA Accra Ghana Street address: G15 White Avenue Airport

490 Ghana ey.com/globaltaxguides ey.com/taxguidesapp Accra GMT EY +233 (302) 779-868, 779-223 Mail address: Fax: +233 (302) 778-894 P.O. Box KA 16009 KIA Accra Ghana Street address: G15 White Avenue Airport

FOREWORD. Uganda. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

FOREWORD. Botswana. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

INTERNATIONAL ASPECTS OF AUSTRALIAN INCOME TAX

INTERNATIONAL ASPECTS OF AUSTRALIAN INCOME TAX Chartered Accountants Business Advisers and Consultants Suite 201, Level 2 65 York Street, Sydney NSW 2000 Australia Telephone: 61+2+9290 1588 Facsimile:

INTERNATIONAL ASPECTS OF AUSTRALIAN INCOME TAX Chartered Accountants Business Advisers and Consultants Suite 201, Level 2 65 York Street, Sydney NSW 2000 Australia Telephone: 61+2+9290 1588 Facsimile:

Paper F6 (CHN) Taxation (China) Monday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (China) Monday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (China) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. s of tax

Fundamentals Level Skills Module Taxation (China) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. s of tax

Table of Contents Personal Income Tax... 3 Tax-Free Savings Account ( TFSA )... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals...

... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals...") 2015 Federal Budget April 21, 2015 Table of Contents Personal Income Tax... 3 Tax-Free Savings Account ( TFSA )... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals... 3 Eligible Dwellings...

2015 Federal Budget April 21, 2015 Table of Contents Personal Income Tax... 3 Tax-Free Savings Account ( TFSA )... 3 Home Accessibility Tax Credit... 3 Qualifying Individuals... 3 Eligible Dwellings...

AFGHANISTAN INCOME TAX LAW

AFGHANISTAN INCOME TAX LAW 2009 An unofficial translation of the Income Tax Law 2009 as published in Official Gazette number 976 dated 18 th March 2009. This translation has been prepared by the Afghanistan

AFGHANISTAN INCOME TAX LAW 2009 An unofficial translation of the Income Tax Law 2009 as published in Official Gazette number 976 dated 18 th March 2009. This translation has been prepared by the Afghanistan

FOREWORD. Jersey. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Mongolia Tax Profile. Produced in conjunction with the KPMG Asia Pacific Tax Centre. Updated: June 2015

Mongolia Tax Profile Produced in conjunction with the KPMG Asia Pacific Tax Centre Updated: June 2015 Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 6 3 Indirect

Mongolia Tax Profile Produced in conjunction with the KPMG Asia Pacific Tax Centre Updated: June 2015 Contents 1 Corporate Income Tax 1 2 Income Tax Treaties for the Avoidance of Double Taxation 6 3 Indirect

OUTLINE LIST OF ABBREVIATIONS... III LIST OF LEGAL REFERENCES...IV PART I. IMPLEMENTATION OF THE DIRECTIVE...V 1. INTRODUCTION...V 2. SCOPE...

CYPRUS 95 Page ii OUTLINE LIST OF ABBREVIATIONS... III LIST OF LEGAL REFERENCES...IV PART I. IMPLEMENTATION OF THE DIRECTIVE...V 1. INTRODUCTION...V 1.1. GENERAL INFORMATION ON THE IMPLEMENTATION OF THE

CYPRUS 95 Page ii OUTLINE LIST OF ABBREVIATIONS... III LIST OF LEGAL REFERENCES...IV PART I. IMPLEMENTATION OF THE DIRECTIVE...V 1. INTRODUCTION...V 1.1. GENERAL INFORMATION ON THE IMPLEMENTATION OF THE

Hong Kong. Investment basics. Currency Hong Kong Dollar (HKD) Foreign exchange control

Foreign exchange control") Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

Hong Kong Linda Ng Director Tel: +1 212 436 2764 ling@deloitte.com Investment basics Currency Hong Kong Dollar (HKD) Foreign exchange control Accounting principles/financial statements Hong Kong Financial

International Tax Germany Highlights 2018

International Tax Germany Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital; however, a declaration must be

International Tax Germany Highlights 2018 Investment basics: Currency Euro (EUR) Foreign exchange control No restrictions are imposed on the import or export of capital; however, a declaration must be

Economic Landscape of South Africa

Economic Landscape of South Africa INTRODUCTION One of the leading economies in Africa, with a well-developed infrastructure and established trade links with the rest of the continent, South Africa is

Economic Landscape of South Africa INTRODUCTION One of the leading economies in Africa, with a well-developed infrastructure and established trade links with the rest of the continent, South Africa is

Tax Letter EMPLOYER-PROVIDED CARS AND TAXABLE BENEFITS. Example. Amount E is then reduced by a reduction factor

Lionel Nolet CPA, CA, Partner Tax Letter Monthly Newsletter July 2017 EMPLOYER-PROVIDED CARS AND TAXABLE BENEFITS If your employer provides you with a car, there are two potential taxable benefits that

Lionel Nolet CPA, CA, Partner Tax Letter Monthly Newsletter July 2017 EMPLOYER-PROVIDED CARS AND TAXABLE BENEFITS If your employer provides you with a car, there are two potential taxable benefits that

International Tax Turkey Highlights 2018

International Tax Turkey Highlights 2018 Investment basics: Currency Turkish Lira (TRY) Foreign exchange control The TRY is fully convertible, at least from the Turkish side, to the extent Turkey is recognized

International Tax Turkey Highlights 2018 Investment basics: Currency Turkish Lira (TRY) Foreign exchange control The TRY is fully convertible, at least from the Turkish side, to the extent Turkey is recognized

Thin Capitalization A Detailed Study

Thin Capitalization A Detailed Study C.A. Divakar Vijayasarathy This paper is a copyright of Divakar Vijayasarathy & Associates. The author and the firm expressly disown their liability on any consequence

Thin Capitalization A Detailed Study C.A. Divakar Vijayasarathy This paper is a copyright of Divakar Vijayasarathy & Associates. The author and the firm expressly disown their liability on any consequence

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Tax Card 2018 Effective from 1 January 2018 The Republic of Estonia KPMG Baltics OÜ kpmg.com/ee CORPORATE INCOME TAX In Estonia, corporate income tax is not levied when profit is earned but when it is

Corporation Tax Deloitte & Touche

Tax Training for Public Sector Entities Mombasa April 2017 Corporation Tax 2 Outline Introduction Imposition of Income Tax Exemption from Income tax Ascertainment of Total Income-Deductions allowed and

Tax Training for Public Sector Entities Mombasa April 2017 Corporation Tax 2 Outline Introduction Imposition of Income Tax Exemption from Income tax Ascertainment of Total Income-Deductions allowed and

Act (1994:1617) on the double taxation treaty between Sweden and the United States

on the double taxation treaty between Sweden and the United States") Act (1994:1617) on the double taxation treaty between Sweden and the United States SFS : 1994:1617 Ministry / Authority : Ministry of Finance S3 Issued : 1994-12- 15 Modified SFS 2011:1368 Amendment Record

Act (1994:1617) on the double taxation treaty between Sweden and the United States SFS : 1994:1617 Ministry / Authority : Ministry of Finance S3 Issued : 1994-12- 15 Modified SFS 2011:1368 Amendment Record

Global Transfer Pricing Review

Global Transfer Pricing Review Czech ZambiaRepublic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Zambia KPMG observation Transfer pricing provisions were written into the Income Tax Act (ITA) in

Global Transfer Pricing Review Czech ZambiaRepublic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Zambia KPMG observation Transfer pricing provisions were written into the Income Tax Act (ITA) in

Mexico has a value added tax that is applied to most products and services. It is 15% in most of the country and 10% in border areas.

Mexico has a value added tax that is applied to most products and services. It is 15% in most of the country and 10% in border areas. PERSONAL CONCLUSION Mexico is modernizing. In the past, the Mexican

Mexico has a value added tax that is applied to most products and services. It is 15% in most of the country and 10% in border areas. PERSONAL CONCLUSION Mexico is modernizing. In the past, the Mexican

FOREWORD. Namibia. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

doing business in Zambia

doing business in Zambia country profile time zone GMT+2 official language English population 17 293 692 currency Kwacha ( ZMW ) government structure economic data Executive: The president is head of state

doing business in Zambia country profile time zone GMT+2 official language English population 17 293 692 currency Kwacha ( ZMW ) government structure economic data Executive: The president is head of state

Form CT1. Pay and File Corporation Tax Return (for accounting periods ending in 2004) Tax Reference Number

Tax Reference Number") TAIN Form CT1 Pay and File Corporation Tax Return 2004 (for accounting periods ending in 2004) Please quote this number in all correspondence or when calling at your Revenue office Tax Reference Number

TAIN Form CT1 Pay and File Corporation Tax Return 2004 (for accounting periods ending in 2004) Please quote this number in all correspondence or when calling at your Revenue office Tax Reference Number

RELATIONAL DIAGRAM OF MAIN CAPABILITIES. The Malaysian tax system (A) Real property gains tax (D)

Real property gains tax (D)") Syllabus (P6) MYS MAIN CAPABILITIES After completing this examination paper students should be able to: A Explain the operation and scope of the tax system AIM (F6) MYS To develop knowledge and skills

Syllabus (P6) MYS MAIN CAPABILITIES After completing this examination paper students should be able to: A Explain the operation and scope of the tax system AIM (F6) MYS To develop knowledge and skills

FOREWORD. Mozambique. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

FOREWORD. Egypt. Services provided by member firms include:

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2015/16 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS.

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS. Income Tax Amendment - Personal SN Description Impact Author remarks 1 For Income more than one crore surcharge Negative More tax from super

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS. Income Tax Amendment - Personal SN Description Impact Author remarks 1 For Income more than one crore surcharge Negative More tax from super

1980 Income and Capital Gains Tax Convention

1980 Income and Capital Gains Tax Convention Treaty Partners: Gambia; United Kingdom Signed: May 20, 1980 In Force: July 5, 1982 Effective: In Gambia, from January 1, 1980. In the U.K.: income tax and

1980 Income and Capital Gains Tax Convention Treaty Partners: Gambia; United Kingdom Signed: May 20, 1980 In Force: July 5, 1982 Effective: In Gambia, from January 1, 1980. In the U.K.: income tax and

CONVENTION. between THE GOVERNMENT OF BARBADOS. and THE GOVERNMENT OF THE REPUBLIC OF GHANA

CONVENTION between THE GOVERNMENT OF BARBADOS and THE GOVERNMENT OF THE REPUBLIC OF GHANA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND ON

CONVENTION between THE GOVERNMENT OF BARBADOS and THE GOVERNMENT OF THE REPUBLIC OF GHANA FOR THE AVOIDANCE OF DOUBLE TAXATION AND THE PREVENTION OF FISCAL EVASION WITH RESPECT TO TAXES ON INCOME AND ON

Film Financing and Television Programming

MEDIA AND ENTERTAINMENT Film Financing and Television Programming A Taxation Guide Sixth Edition kpmg.com Contents Preface 1 Chapter 01 Australia 3 Chapter 02 Austria 30 Chapter 03 Belgium 39 Chapter 04

MEDIA AND ENTERTAINMENT Film Financing and Television Programming A Taxation Guide Sixth Edition kpmg.com Contents Preface 1 Chapter 01 Australia 3 Chapter 02 Austria 30 Chapter 03 Belgium 39 Chapter 04

Income Tax. ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1

ABC of Capital Gains Tax for Companies (Issue 7) 1") Income Tax ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1 Preface ABC of Capital Gains Tax for Companies This guide provides a basic introduction to

Income Tax ABC of Capital Gains Tax for Companies (Issue 7) ABC of Capital Gains Tax for Companies (Issue 7) 1 Preface ABC of Capital Gains Tax for Companies This guide provides a basic introduction to

International Tax Taiwan Highlights 2018

International Tax Taiwan Highlights 2018 Investment basics: Currency Taiwan Dollar (NTD) Foreign exchange control Foreign exchange transactions are administered by the central bank. A limit of USD 50 million

International Tax Taiwan Highlights 2018 Investment basics: Currency Taiwan Dollar (NTD) Foreign exchange control Foreign exchange transactions are administered by the central bank. A limit of USD 50 million

Domestic Fiscal System and International

Lorenzo Riccardi Vietnam Tax Guide Domestic Fiscal System and International Treaties ^ Springer Part I Vietnamese Tax System 1 Introduction to the Vietnamese Tax System 3 1.1 Legislative Background and

Lorenzo Riccardi Vietnam Tax Guide Domestic Fiscal System and International Treaties ^ Springer Part I Vietnamese Tax System 1 Introduction to the Vietnamese Tax System 3 1.1 Legislative Background and

2005 Income and Capital Gains Tax Convention and Notes

2005 Income and Capital Gains Tax Convention and Notes Treaty Partners: Botswana; United Kingdom Signed: September 9, 2005 In Force: September 4, 2006 Effective: In Botswana, from July 1, 2007. In the

2005 Income and Capital Gains Tax Convention and Notes Treaty Partners: Botswana; United Kingdom Signed: September 9, 2005 In Force: September 4, 2006 Effective: In Botswana, from July 1, 2007. In the