For personal use only

|

|

|

- Stephen Whitehead

- 5 years ago

- Views:

Transcription

1 Demerger Scheme Booklet for a scheme of arrangement and reduction of capital in relation to the proposed demerger of Talon Petroleum Limited (ABN ) from Texon Petroleum Ltd (ABN ) A Notice of General Meeting and a Notice of Demerger Scheme Meeting are included as Appendix 6 and Appendix 7 to this Demerger Scheme Booklet. Proxy forms for the meetings accompany this Demerger Scheme Booklet. The Demerger Scheme Meeting will be held at the offices of Minter Ellison Lawyers, Level 22, Waterfront Place, 1 Eagle Street, Brisbane on 25 February 2013 at 11.30am. The General Meeting will be held at the same venue at 1.30pm on 25 February 2013 (or as soon thereafter as the Acquisition Scheme Meeting has been concluded or adjourned). THE TEXON DIRECTORS UNANIMOUSLY RECOMMEND THAT YOU VOTE IN FAVOUR OF THE DEMERGER SCHEME AND THE CAPITAL REDUCTION, IN THE ABSENCE OF A SUPERIOR PROPOSAL. THIS IS AN IMPORTANT DOCUMENT AND REQUIRES YOUR URGENT ATTENTION. If you are in any doubt as to how to deal with this Demerger Scheme Booklet, please consult your legal, financial, taxation or other professional adviser immediately. If, after reading this Demerger Scheme Booklet, you have any questions about the Demerger Scheme or the Capital Reduction, please call the Texon Shareholder Information Line on (within Australia) or (outside Australia) Monday to Friday between 8.30am and 5.00pm (Brisbane, Australia time). If you have recently sold all of your Texon Shares, please disregard all enclosed documents. Legal Adviser to Texon Financial Adviser to Texon

2 Important notices General You should read this Demerger Scheme Booklet in its entirety before making a decision on how to vote on the resolution to be considered at the Demerger Scheme Meeting and the General Meeting. The notice convening the General Meeting is contained in Appendix 6 to this Demerger Scheme Booklet. The notice convening the Demerger Scheme Meeting is contained in Appendix 7 to this Demerger Scheme Booklet. Proxy forms for the General Meeting and the Demerger Scheme Meeting are provided with this Demerger Scheme Booklet. Defined terms Capitalised terms in this Demerger Scheme Booklet are defined either in the Glossary in Section 10 or where the relevant term is first used. Purposes of this Demerger Scheme Booklet This explanatory statement has been prepared pursuant to section 412(1) of the Corporations Act to: (a) explain the terms and effect of the Demerger Scheme to Texon Shareholders; (b) explain the manner in which the Demerger Scheme will be considered and, if approved, implemented; (c) state any material interests of the Texon Directors, whether as directors, members or creditors of Texon or otherwise and the effect on those interests of the Demerger Scheme as far as that effect is different from the effect on similar interests of other persons; and (d) provide such information as is prescribed by the Corporations Act and the Corporations Regulations or as is otherwise material to the decision of Texon Shareholders whether to approve the Demerger Scheme. This Demerger Scheme Booklet is not a disclosure document lodged under Chapter 6D of the Corporations Act. ASIC and ASX A copy of this Demerger Scheme Booklet has been examined by ASIC for the purpose of section 411(2) of the Corporations Act and registered by ASIC for the purpose of section 412(6) of the Corporations Act. ASIC will be requested to provide a statement, in accordance with section 411(17)(b) of the Corporations Act, that ASIC has no objection to the Demerger Scheme. If ASIC provides that statement, it will be produced to the Court at the time of the Court hearing to approve the Demerger Scheme. Neither ASIC nor any of its officers take any responsibility for the contents of this Demerger Scheme Booklet. A copy of this Demerger Scheme Booklet has been lodged with the ASX. Neither the ASX nor any of its officers take any responsibility for the contents of this Demerger Scheme Booklet. Input from other parties The Independent Expert, BDO Corporate Finance (QLD) Ltd, has prepared the Independent Expert s Report in relation to the Demerger Scheme in Appendix 1 to this Demerger Scheme Booklet and takes responsibility for that report. Texon, its Related Bodies Corporate and their respective directors, officers, employees, advisers and agents do not assume any responsibility, and they are not responsible, for the accuracy or completeness of the Independent Expert s Report. Other than in respect of the information provided by the Independent Expert as identified above, the information contained in the remainder of this Demerger Scheme Booklet has been prepared by Texon and is the responsibility of Texon. Texon Shareholders outside of Australia This Demerger Scheme Booklet has been prepared having regard to Australian disclosure requirements. These requirements may be different from those in other jurisdictions. The financial information in this Demerger Scheme Booklet has also been prepared in accordance with Australian equivalents of International Financial Reporting Standards (AIFRS), which may differ from generally accepted accounting principles in other jurisdictions. This Demerger Scheme Booklet does not constitute an offer to Texon Shareholders or a solicitation in any jurisdiction in which, or to any person to whom, it would not be lawful to make such an offer or solicitation. Restrictions in jurisdictions outside Australia and its external territories, New Zealand, the United Kingdom, the United States of America, Singapore and Hong Kong may make it impractical or unlawful for Talon Shares to be transferred under a scheme of arrangement to, or be received under a scheme of arrangement by, Texon Shareholders in those jurisdictions. New Zealand The offer of Talon Shares pursuant to the Demerger Scheme is being made to Texon Shareholders in New Zealand pursuant to the Securities Act (Overseas Companies) Exemption Notice 2002 (New Zealand). This Demerger Scheme Booklet is not a New Zealand prospectus or an investment statement and it has not been registered, filed with or approved by any New Zealand regulatory authority under or in accordance with the Securities Act 1978 (New Zealand) or any other relevant law in New Zealand. This Demerger Scheme Booklet may not contain all of the information that a prospectus or an investment statement under New Zealand law is required to contain. United Kingdom This Demerger Scheme Booklet is not a prospectus, and no such prospectus is required for the purposes of the European Union s Prospectus Directive as implemented by the Financial Services and Markets Act 2000 (United Kingdom) and the Prospectus Rules of the Financial Services Authority in the United Kingdom. Hong Kong WARNING The contents of this Demerger Scheme Booklet have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to any Talon Shares that may be transferred to you. If you are in doubt about any of the contents of this document, you should obtain independent professional advice. The Demerger Scheme and this Demerger Scheme Booklet do not constitute an offer or invitation to the public in Hong Kong within the meaning of the Hong Kong Companies Ordinance or the Hong Kong Securities and Futures Ordinance. Accordingly, unless permitted by the securities laws of Hong Kong, no person may issue or have in its possession for the purposes of issue, this Demerger Scheme Booklet or any invitation or document relating to the Demerger Scheme, whether in Hong Kong or elsewhere, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong other than in circumstances which do not constitute an offer or an invitation to the public for the purposes of the Hong Kong Companies Ordinance or the Hong Kong Securities and Futures Ordinance. However, numbered copies of this Demerger Scheme Booklet may be issued to a limited number of shareholders in Hong Kong in a manner which does not constitute an issue, circulation or distribution of this Demerger Scheme Booklet, or any offer or invitation in respect of the Talon Shares, to the public in Hong Kong. Only the person to whom a numbered copy of this Demerger Scheme Booklet has been issued may take action in response to this Demerger Scheme Booklet. No person to whom a numbered copy of this Demerger Scheme Booklet is issued may issue, circulate or distribute this Demerger Scheme Booklet in Hong Kong or make or give a copy of this Demerger Scheme Booklet to any other person. Singapore The transfer of Talon Shares under the Demerger Scheme is being made to Texon Shareholders based in Singapore on the basis that no prospectus has been or will be registered in Singapore and under the applicable exemptions provided in the Singapore Securities and Futures Act (Cap 289). The Talon Shares will be transferred to Texon Shareholders based in Singapore solely as a consequence of their shareholding in Texon, and is not being made with a view to them subsequently offering the shares for sale to any other parties. United States The Talon Shares to be issued or transferred pursuant to the Demerger Scheme have not been, and will not be, registered under the United States Securities Act of 1933 (U.S. Securities Act), or the securities laws of any other jurisdiction, and may not be offered or sold in the U.S. or to U.S. Persons (as defined in Regulation S under the Securities Act) (U.S. Persons) unless they are registered under the U.S. Securities Act, or an exemption from the registration requirements of the U.S. Securities Act is available. Any Talon Shares issued or transferred to persons in the United States under the Demerger Scheme will be issued or transferred in reliance on the exemption from the registration

3 Demerger Scheme Booklet 1 requirements of the U.S. Securities Act provided by Section 3(a)(10) thereof, based on the approval of the Demerger Scheme by the Court. Talon Shares received under the Demerger Scheme by any person who is deemed to be an affiliate of Talon under Rule 145 under the U.S. Securities Act, including, without limitation, directors and certain executive officers, may not be resold in the United States or to a U.S. Person except in accordance with the provisions of Rule 144 under the U.S. Securities Act, outside of the United States in reliance upon Regulation S under the U.S. Securities Act, or as otherwise permitted by the U.S. Securities Act. Texon Shareholders in the United States should note that this Demerger Scheme Booklet has been prepared in accordance with Australian disclosure requirements, which are different to those that would apply to a disclosure document prepared in accordance with the rules of the U.S. Securities Exchange Commission (SEC). The SEC has not reviewed or approved the contents of this Demerger Scheme Booklet. In particular, Texon Shareholders should note that the pro forma financial information included in this Demerger Scheme Booklet does not purport to comply with the requirements of Article 11 of Regulation S-X of the rules and regulations of the SEC. Texon Shareholders should note that the petroleum reserve and resource reporting systems of different jurisdictions employ different definitions and permit or require different assumptions, and that identical geological and engineering data can produce different results under different reporting systems. Texon provides no assurance that the reserves and resources stated in this Demerger Scheme Booklet would be equivalent to the reserves and resources it would be required or permitted to state under any other reporting system. In particular, Texon Shareholders in the United States are cautioned that the methodologies used to estimate the reserve and resource quantities reported in this Demerger Scheme Booklet vary in certain respects from those required to be used by SEC reporting companies, including the reporting requirements set out in SEC Industry Guide 2, Regulations S-K and S-X and related SEC disclosure requirements. Investment decisions This Demerger Scheme Booklet does not take into account the investment objectives, financial situation or particular needs of any Texon Shareholder or any other person. Texon is not licensed to provide financial product advice in relation to Texon Shares. This Demerger Scheme Booklet should not be relied on as the sole basis for any investment decision in relation to Texon Shares or the decision by Texon Shareholders to vote in relation to the Demerger Scheme. Independent financial and taxation advice should be sought before making any decision in relation to the Demerger Scheme. Forward looking statements Certain statements in this Demerger Scheme Booklet (including in the Independent Expert s Report) relate to the future. Forward looking statements can be identified by the use of forward looking words such as may, should, expect, anticipate, estimate, scheduled, believe or continue, their negative equivalent or comparable terminology. Similarly, statements that describe Texon s or Talon s objectives, plans, goals or expectations are or may be forward looking statements. The statements contained in this Demerger Scheme Booklet about the impact that the Demerger Scheme may have on the results of Texon s or Talon s operations and the advantages and disadvantages anticipated to result from the Demerger Scheme, are also forward looking statements. Such statements involve known and unknown risks, uncertainties and other important factors that could cause the actual results, performance or achievements of Texon or Talon to be materially different from expected future results, performance or achievements expressed, projected or implied by such statements. Such risks, uncertainties and other important factors include among other things, general economic conditions, specific market conditions, exchange rates, interest rates and regulatory changes. The risk factors described in Section 6 of this Demerger Scheme Booklet could affect future results, causing these results to differ materially from those expressed, projected or implied in any forward looking statements. These factors are not necessarily all of the important factors that could cause actual results to differ materially from those expressed, projected or implied in any forward looking statement. Other unknown or unpredictable factors could also have a material adverse effect on future results of Texon and Talon. Forward looking statements included in this Demerger Scheme Booklet reflect the expectations of relevant parties views only as of the date of this Demerger Scheme Booklet. Each of Texon and Talon has no obligation to disseminate, after the date of this Demerger Scheme Booklet, any updates or revisions to any such statements to reflect any change in expectations in relation to those statements or any change in events, conditions or circumstances on which any of those statements is based unless it is required to do so pursuant to its continuous disclosure obligations under the Corporations Act and the Listing Rules or by an order of the Court. Texon and Talon and their officers, and any persons named in this Demerger Scheme Booklet with their consent or any person involved in the preparation of this Demerger Scheme Booklet, make no representation or warranty and give no assurance or guarantee that the occurrence of the events or the accuracy of achievement of results expressed, projected or implied in any forward looking statements (except to the extent required by law) will actually occur. You are cautioned not to rely on any forward looking statement. Rounding of numerical information Any discrepancies between totals in tables and sums of components contained in this Demerger Scheme Booklet and between those figures and figures referred to in other parts of this Demerger Scheme Booklet are due to rounding. All rounded numbers have been rounded either to one decimal place or to the nearest whole number. Privacy statement Texon collects personal information about its shareholders holdings of Texon Shares in accordance with the Corporations Act. Texon will share that personal information with its advisers and service providers in connection with the Demerger Scheme. Shareholders can contact the Texon Registry, Computershare Investor Services Pty Limited, on (within Australia) or (outside Australia) if they have questions about their personal information. No internet site is part of this Demerger Scheme Booklet Texon maintains an internet site at com.au. Any references in this Demerger Scheme Booklet to an internet site are textual references for information only and no information in any internet site forms part of this Demerger Scheme Booklet. Important notice associated with Court order under section 411(1) of the Corporations Act The fact that under section 411(1) of the Corporations Act the Court ordered that a meeting of Texon Shareholders be convened by Texon to consider and vote on the Demerger Scheme and has approved this Demerger Scheme Booklet does not mean that the Court: (a) has formed any view as to the merits of the proposed Demerger Scheme or as to how Texon Shareholders should vote (on this matter, Texon Shareholders must reach their own decision); or (b) has prepared, or is responsible for, the content of this Demerger Scheme Booklet. References to time All references to time in this Demerger Scheme Booklet are references to Brisbane, Australia time unless otherwise stated. Currency All references in this Demerger Scheme Booklet to $, A$ and cents are references to Australian currency, unless otherwise specified. All references in this Demerger Scheme Booklet to US$ and US dollars are references to United States currency, unless otherwise specified. Date of this Demerger Scheme Booklet This Demerger Scheme Booklet is dated 22 January 2013.

4 2 Letter from the Chairman of Texon Dear Texon Shareholder On 13 November 2012, Texon announced two separate transactions under which Texon would create a new listed petroleum exploration company, Talon Petroleum Limited, through a demerger of certain assets by implementation of the Demerger Scheme and the acquisition by Sundance of all of your post Demerger Texon Shares, pursuant to the Acquisition Scheme. The acquisition of your Texon Shares by Sundance is conditional upon the implementation of the Demerger, but, subject to obtaining relevant approvals, the Demerger Scheme will proceed even if the Acquisition Scheme does not. I am pleased to provide this Demerger Scheme Booklet to you which sets out the detail of the Demerger Scheme and the formation of Talon. You will also receive a separate Acquisition Scheme Booklet which sets out the detail of the Acquisition Scheme. Talon will be an exploration and appraisal focussed oil and gas company, with a portfolio that includes a mix of production, development, appraisal and exploration assets. Talon will continue to seek to participate in low risk oil prospects, located in mature, well serviced areas, that can readily be commercialised. The Texon Directors unanimously recommend that, in the absence of a Superior Proposal, you vote in favour of the Demerger Scheme Resolution at the Demerger Scheme Meeting and the Capital Reduction Resolution at the General Meeting to be held on 25 February The Texon Directors who hold or control Texon Shares intend to vote in favour of the Demerger Scheme Resolution and the Capital Reduction Resolution in respect of all their Texon Shares, in the absence of a Superior Proposal. As at the date of this Demerger Scheme Booklet, the Texon Directors hold or control approximately 11.2 million Texon Shares, representing approximately 4.6% of Texon s share capital. Please read this Demerger Scheme Booklet carefully as it contains important information in relation to the Demerger Scheme, including the reasons for the Texon Directors recommendation and the Independent Expert s Report prepared by BDO Corporate Finance (QLD) Ltd. The Independent Expert has concluded that, on balance, the advantages of the Demerger Scheme outweigh the disadvantages of the Demerger Scheme and that, in the absence of any other information or a superior proposal, it is in the best interests of Texon Shareholders. The Independent Expert s Report is included in Appendix 1 of this Demerger Scheme Booklet and I encourage you to read it before voting on the Demerger Scheme. If you have any questions, please call the Texon Shareholder Information Line on (within Australia) or (outside Australia) Monday to Friday between 8.30am and 5.00pm (Brisbane, Australia time). Alternatively, contact your legal, financial, taxation or other professional adviser. Your vote is important regardless of how many Texon Shares you own. If you are unable to attend the Demerger Scheme Meeting in person, I encourage you to vote by completing your personalised proxy form which is enclosed with this Demerger Scheme Booklet and returning it in accordance with the directions on the form so it is received by 1.30pm (Brisbane time) on Saturday, 23 February On behalf of the Texon Directors, I would like to take this opportunity to thank you for your support of Texon. Yours sincerely, John Armstrong Chairman

5 Demerger Scheme Booklet 3 Overview of this Demerger Scheme Booklet What is this Demerger Scheme Booklet for? On 13 November 2012, Texon announced a series of transactions to deliver to all Texon Shareholders: (a) one share in a new entity to be listed on ASX, Talon Petroleum Limited, for every Texon Share held on the Demerger Record Date; 1 and (b) one New Sundance Share for every two Texon Shares pursuant to the Acquisition Scheme, 2 subject to and following the implementation of the Demerger Scheme. Since the announcement of the Demerger Scheme, Texon has determined that under the Demerger Scheme Eligible Scheme Shareholders will be entitled to receive two Talon Shares for every five Texon Shares held on the Demerger Record Date (giving the same percentage interest for the shareholder in Talon as the shareholder held in Texon prior to the Demerger). The Demerger Scheme and the Acquisition Scheme will be effected by two separate schemes of arrangement, both of which you will be entitled to vote on. The Acquisition Scheme is conditional on, and therefore will not proceed unless, the Demerger Scheme is approved and implemented. The Demerger Scheme is not conditional on whether the Acquisition Scheme is approved or implemented but is subject to a number of conditions, details of which are set out in Section 1.5. For the Demerger Scheme to be implemented, Texon Shareholders will need to approve the Demerger Scheme Resolution at the Demerger Scheme Meeting and Capital Reduction Resolution at a general meeting of Texon Shareholders, which is separate to the Demerger Scheme Meeting. If the Demerger Scheme is approved by Texon Shareholders, the Capital Reduction Amount will be applied by Texon as consideration for the acquisition of Talon Shares. Accordingly, Eligible Scheme Shareholders will not receive a cash payment for the Capital Reduction Amount, but will instead receive two Talon Shares for every five Texon Shares they hold on the Demerger Record Date. 3 Texon Shareholders will also be asked at the General Meeting to approve the issue of Talon Shares to Wandoo under the Wandoo Interest Acquisition Agreement (described in Section 4.8(b)(ii) of this Demerger Scheme Booklet). Sundance entered into the Scheme Implementation Agreement and agreed to proceed with the Acquisition Scheme on the basis that this transaction would take place. Further detailed discussion of matters relating to this resolution may be found in the Notice of General Meeting included as Appendix 6 and in the value analysis in relation to the Wandoo Interest Acquisition Agreement included as Appendix 8 to this Demerger Scheme Booklet. This Demerger Scheme Booklet contains information to assist you to decide how to vote on the Demerger Scheme at the Demerger Scheme Meeting to be held at the offices of Minter Ellison Lawyers, Level 22, Waterfront Place, 1 Eagle Street, Brisbane on 25 February 2013 at 11.30am. Further information regarding the Capital Reduction Resolution and other resolutions to be considered at the General Meeting is set out in the Notice of General Meeting included as Appendix 6 to this Demerger Scheme Booklet. For more information on the Acquisition Scheme, you should refer to the Acquisition Scheme Booklet which you should receive from Texon at about the same time as you receive this Demerger Scheme Booklet. 1 Note that if you are an Ineligible Foreign Shareholder, the Talon Shares that you would otherwise have received under the Demerger Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive under the Demerger Scheme, please refer to Section 8.9(d). 2 Note that if you are an Ineligible Foreign Shareholder (as defined in the Acquisition Scheme Booklet), the New Sundance Shares that you would otherwise have received under the Acquisition Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive under the Acquisition Scheme, please refer to the Acquisition Scheme Booklet. 3 Note that if you are an Ineligible Foreign Shareholder, the Talon Shares that you would have otherwise received under the Demerger Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive, see Section 8.9(d).

6 4 Why should you vote? For the Demerger Scheme to be implemented, the Demerger Scheme Resolution must be approved by Texon Shareholders at the Demerger Scheme Meeting and the Capital Reduction Resolution must be approved by Texon Shareholders at the General Meeting. For the Demerger Scheme to proceed, the Demerger Scheme Resolution must be approved by: a majority in number (more than 50%) of Texon Shareholders present and voting on the Demerger Scheme Resolution (whether in person, by proxy or attorney or, in the case of a corporate Texon Shareholder or proxy, by corporate representative); 4 and at least 75% of the total number of votes cast on the Demerger Scheme Resolution by Texon Shareholders (whether in person or by proxy, attorney or, in the case of a corporate Texon Shareholder or proxy, by corporate representative). The Demerger Scheme Meeting will be held at the offices of Minter Ellison Lawyers, Level 22, Waterfront Place, 1 Eagle Street, Brisbane on 25 February The Demerger Scheme Meeting will commence at 11.30am. The notice convening the Demerger Scheme Meeting is attached at Appendix 7 to this Demerger Scheme Booklet. For the Capital Reduction Resolution to be passed, votes in favour of that resolution must be received from a simple majority of Texon Shareholders. The General Meeting will be held at the same venue as the Demerger Scheme Meeting on 25 February The General Meeting will commence at 1.30pm or as soon thereafter as the Acquisition Scheme Meeting has been concluded or adjourned. The notice convening the General Meeting is in Appendix 6. The Texon Directors urge all Texon Shareholders to vote at the Demerger Scheme Meeting and the General Meeting. The matters to be decided at these meetings affects your shareholding and your vote at the meetings is important in determining whether the Demerger Scheme proceeds. What you should do next Read this Demerger Scheme Booklet and consider the Demerger Scheme You should read and carefully consider the information included in this Demerger Scheme Booklet to help you make an informed decision. Answers to some frequently asked questions are included in this booklet (commencing on page 17). If you have any doubts as to what action you should take, you should consult your legal, financial, taxation or other professional adviser before making any decision in relation to your Texon Shares and how to vote at the Demerger Scheme Meeting and the General Meeting. Consider your decision Texon Shareholders should refer to Section 3 for further information on the expected advantages and possible disadvantages of the Demerger Scheme. However, this Demerger Scheme Booklet does not take into account the investment objectives, financial situation and particular needs of any Texon Shareholder. You should read this Demerger Scheme Booklet in its entirety and contact your legal, financial, taxation, investment or other professional adviser if you require further advice in relation to the Demerger Scheme. 4 The Court has a discretion to approve the Acquisition Scheme where it is approved by at least 75% of all votes cast on the resolution to approve the Acquisition Scheme but not by a majority in number of Texon Shareholders voting on the resolution to approve the Acquisition Scheme: refer to section 411(4)(a)(ii)(A) of the Corporations Act.

7 Demerger Scheme Booklet 5 Vote on the Demerger Scheme and Capital Reduction As a Texon Shareholder, it is your right to vote on whether the Demerger Scheme should proceed. You are also entitled to vote on the resolutions to be considered at the General Meeting. If you wish to vote in person at the Demerger Scheme Meeting or the General Meting, then you must attend the relevant meeting. If you cannot attend the Demerger Scheme Meeting or the General Meeting, you may vote by proxy, attorney or if you are a body corporate, by appointing a corporate representative. Attorneys who plan to attend the Demerger Scheme Meeting or the General Meeting should bring with them the original or a certified copy of the power of attorney under which they have been authorised to attend and vote at the Demerger Scheme Meeting or the General Meeting. A body corporate which is a Texon Shareholder may appoint an individual to act as its corporate representative. The appointment must comply with the requirements of section 250D of the Corporations Act. The representative should bring to the Demerger Scheme Meeting or the General Meeting evidence of his or her appointment, including any authority under which it is signed. If you wish to vote by proxy, your proxy form must be received by the Texon Registry (whether through the InvestorVote website, by mail or by fax) before the relevant cut-off time on 23 February For further details, please refer to the Notice of Demerger Scheme Meeting and the Notice of General Meeting. Is the Demerger Scheme in the best interests of Texon Shareholders? The Independent Expert has concluded in the Independent Expert s Report that, on balance, the advantages of the Demerger Scheme outweigh the disadvantages of the Demerger Scheme and that the Demerger Scheme is, in the absence of any other information or a superior proposal, fair and reasonable and in the best interests of Texon Shareholders. What do the Texon Directors recommend? The Texon Directors UNANIMOUSLY RECOMMEND that you vote IN FAVOUR of the Demerger Scheme and the Capital Reduction Resolution, in the absence of a Superior Proposal. The Texon Directors intend to vote all Texon Shares they hold or control IN FAVOUR of the Demerger Scheme and the Capital Reduction Resolution, in the absence of a Superior Proposal.

8 6 Important dates and times Key events and the expected timing in relation to the approval and implementation of the Demerger Scheme are set out in the table below. Event Last time and date for proxy forms for the Demerger Scheme Meeting and General Meeting to be received by the Texon Registry (whether through the InvestorVote website, by mail or by fax) Time and date for determining eligibility to vote at the Demerger Scheme Meeting Demerger Scheme Meeting to be held at the offices of Minter Ellison Lawyers, Level 22, Waterfront Place, 1 Eagle Street, Brisbane General Meeting to be held at the same venue as the Demerger Scheme Meeting Date (and time) 1.30pm on 23 February pm on 23 February am on 25 February pm on 25 February 2013, or as soon thereafter as the Acquisition Scheme Meeting has been concluded or adjourned If the Texon Shareholders approve the Demerger Scheme at the Demerger Scheme Meeting and the Capital Reduction Resolution at the General Meeting Second Court Hearing to obtain orders approving the Demerger Scheme Lodgement by Texon of the Court orders with ASIC (Effective Date) Last day of trading in Texon Shares on the ASX with an entitlement to participate in the Demerger Scheme Commencement of trading on the ASX of Texon Shares without an entitlement to participate in the Demerger Scheme 5 27 February February February February 2013 Commencement of trading on the ASX of Talon Shares transferred under the Demerger Scheme on a deferred settlement basis Time and date for determining entitlements to Talon Shares under the Demerger Scheme (Demerger Record Date) Capital Reduction and transfer of Talon Shares to Eligible Scheme Shareholders (Implementation Date) Expected date of dispatch of written advices confirming the issue of, and last day of deferred settlement trading in, Talon Shares transferred under the Demerger Scheme Commencement of normal trading in Talon Shares transferred under the Demerger Scheme 6.00pm on 6 March March March March This will only occur if the Acquisition Scheme is not approved. If the Acquisition Scheme is approved, Texon Shares will be suspended from close of trading on 27 February 2013

9 Demerger Scheme Booklet 7 These dates and times are indicative only. Texon has the right to vary any or all of these dates and times and will provide notice of any such variation. Certain dates and times are conditional on the approval of the Demerger Scheme by Texon Shareholders and by the Court. Any variations to the above dates and times will be announced to the ASX (and accordingly, details will be available on the ASX s website ( and will be published on Texon s website ( Questions About The Demerger Scheme If, after reading this Demerger Scheme Booklet, you have any questions about the Demerger Scheme, please call the Texon Shareholder Information Line on (within Australia) or (outside Australia) Monday to Friday between 8.30am and 5.00pm (Brisbane, Australia time). The Texon Directors recommend that you consult your legal, financial, taxation or other professional adviser concerning the impact your decision may have on your own circumstances.

10 8 Table of Contents Important notices IFC Letter from the Chairman of Texon 2 Overview of this Demerger Scheme Booklet 3 Important dates and times 6 Section 1 Summary of the Demerger Scheme 9 Section 2 Frequently asked questions 14 Section 3 Key reasons to vote in favour of or against the Demerger Scheme 23 Section 4 Information on Talon if the Demerger is implemented 30 Section 5 Information on Texon if the Demerger is implemented (but the Acquisition Scheme is not implemented) 44 Section 6 Risk factors 52 Section 7 What if the Demerger Scheme and/or Acquisition Scheme is not implemented? 60 Section 8 Implementation of the Demerger 63 Section 9 Additional information 69 Section 10 Glossary 80 Appendix 1 Independent Expert s Report 86 Appendix 2 Tax Implications for Texon Shareholders 163 Appendix 3 Demerger Scheme 167 Appendix 4 Demerger Scheme Deed Poll 177 Appendix 5 Summary of material agreements relating to the Demerger 183 Appendix 6 Notice of General Meeting 190 Appendix 7 Notice of Demerger Scheme Meeting 196 Appendix 8 Value analysis in relation to the Wandoo Interest Acquisition Agreement 201 Corporate directory 212

11 Demerger Scheme Booklet 9 1SECTION 1 Summary of the Demerger Scheme

12 10 SECTION 1 Summary of the Demerger Scheme Summary of the Demerger Scheme 1.1 Introduction On 13 November 2012, Texon announced a series of transactions to deliver to all Texon Shareholders: one share in a new listed entity, Talon, for every Texon Share held on the Demerger Record Date; 6 and one New Sundance Share for every two Texon Shares pursuant to the Acquisition Scheme, 7 subject to and following the implementation of the Demerger Scheme. Since the announcement of the Demerger Scheme, Texon has determined that under the Demerger Scheme Eligible Scheme Shareholders will be entitled to receive two Talon Shares for every five Texon Shares held on the Demerger Record Date (giving the same percentage interest for the shareholder in Talon as the shareholder held in Texon prior to the Demerger). The Acquisition Scheme is conditional upon the implementation of the Demerger Scheme, but, subject to obtaining the relevant approvals, the Demerger Scheme will proceed even if the Acquisition Scheme does not. A copy of the Demerger Scheme is set out in Appendix 3 to this Demerger Scheme Booklet. 1.2 What you will receive If the Demerger Scheme is approved and implemented, Eligible Scheme Shareholders will each receive on the Implementation Date two Talon Shares for every five Texon Shares held as at the Demerger Record Date. Ineligible Foreign Shareholders will not receive Talon Shares on the Implementation Date. Instead, the Talon Shares to which the Ineligible Foreign Shareholders would otherwise have been entitled will be sold and the proceeds (less costs) will be remitted to them. More information regarding the entitlements of Ineligible Foreign Shareholders can be found in Section Where the calculation of the number of Talon Shares to be transferred to a particular Eligible Scheme Shareholder (or to be sold in respect of a particular Ineligible Foreign Shareholder) would result in an entitlement that is not a whole number, the fractional entitlement will be rounded down to the nearest whole number of Talon Shares and the fractional entitlement will be disregarded. 1.3 Texon Directors recommendations and intentions The Texon Directors as at the date of this Demerger Scheme Booklet are John Armstrong, Bernard Rowley and David Mason. The Texon Directors unanimously recommend that you vote in favour of the Demerger Scheme Resolution and the Capital Reduction Resolution, in the absence of a Superior Proposal. The Texon Directors have carefully considered the potential advantages and disadvantages of the Demerger Scheme, as set out in Section 3, and believe that the Demerger Scheme is in the best interests of Texon Shareholders, in the absence of a Superior Proposal. If a Superior Proposal emerges, this will be announced to ASX and the Directors will carefully reconsider the Demerger Scheme and advise you of their recommendation. The Texon Directors who hold or control Texon Shares intend to vote in favour of the Demerger Scheme Resolution and the Capital Reduction Resolution in respect of all their Texon Shares, in the absence of a Superior Proposal. As at the date of this Demerger Scheme Booklet, the Texon Directors hold or control approximately 11.2 million Texon Shares, representing approximately 4.6% of Texon s share capital. For details on the Texon Directors interests in Texon Shares, refer to Section Note that if you are an Ineligible Foreign Shareholder, the Talon Shares that you would otherwise have received under the Demerger Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive under the Demerger Scheme, please refer to Section 8.9(d). 7 Note that if you are an Ineligible Foreign Shareholder (as defined in the Acquisition Scheme Booklet), the New Sundance Shares that you would otherwise have received under the Acquisition Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive under the Acquisition Scheme, please refer to the Acquisition Scheme Booklet.

13 Demerger Scheme Booklet Independent Expert s conclusions The Texon Directors commissioned BDO Corporate Finance (QLD) Ltd to provide an Independent Expert s Report including an opinion as to whether the Demerger Scheme is in the best interests of Texon Shareholders. The Independent Expert has concluded in the Independent Expert s Report that, on balance, the advantages of the Demerger Scheme outweigh the disadvantages and that, in the absence of any other information or a superior proposal, the Demerger Scheme is fair and reasonable and in the best interests of Texon Shareholders. The Independent Expert s Report is included in Appendix 1 to this Demerger Scheme Booklet and you are encouraged to read it. 1.5 Key conditions precedent Implementation of the Demerger Scheme is subject to a number of conditions precedent. The Demerger Scheme will become binding on Texon and Texon Shareholders only if the following conditions precedent in the Demerger Scheme and Demerger Deed are satisfied (or, in some cases, waived by Texon): before 7.00 am on the Second Court Date, ASIC and the ASX issue or provide such consents, approvals or waivers or do such other acts which Texon determines are necessary or desirable to implement the Demerger on the terms and conditions set out in this deed, including in the case of ASIC, providing the statement required under section 411(17)(b) of the Corporations Act; the Independent Expert issues its report which concludes that the Demerger Scheme is in the best interests of Scheme Shareholders before the date on which the Demerger Scheme Booklet is registered by ASIC under the Corporations Act and the Independent Expert does not change its conclusions or withdraw its report prior to 7.00 am on the Second Court Date; Texon Shareholders approve the Demerger Scheme by the necessary majorities under the Corporations Act; Texon Shareholders approve the Capital Reduction Resolution by the necessary majority under the Corporations Act and the constitution of Texon before the Second Court Date; the Court approves the Scheme under section 411(4)(b) of the Corporations Act and an office copy of the Scheme Order is lodged with ASIC by the Effective Date as contemplated by section 411(10) of the Corporations Act; as at 7.00 am on the Second Court Date, no temporary restraining order, preliminary or permanent injunction or other order or decision by a court of competent jurisdiction or other regulatory authority is in effect and there is no other legal restraint or prohibition in effect preventing the consummation of any aspect of the Demerger on the Implementation Date; before 7.00 am on the Second Court Date, Texon obtaining relief from any Australian capital gains tax that may arise from the transfer of shares in Talon to Eligible Scheme Shareholders and confirmation from the ATO that no amount deemed to be paid as part of the Capital Reduction will be an assessable dividend; and before 7.00 am on the Second Court Date, ASX agrees in principle to the admission of Talon to the official list on the ASX subject only to the Demerger Scheme becoming Effective and other customary pre-quotation conditions (including the provision of information required by ASX) or on any other conditions acceptable to Texon, acting reasonably. The Demerger Scheme is attached as Appendix 3. A summary of the Demerger Deed is contained in Section 1 of Appendix 5. The conditions under the Demerger Scheme are for the benefit of Texon and only Texon may waive any one or more of the conditions. Texon will provide a certificate to the Court at the Second Court Hearing confirming whether the conditions (other than the condition relating to approval by the Court) have been satisfied or waived. Application for the admission of Talon to the official list on the ASX is to be lodged with ASX before the Second Court Hearing. This application follows preliminary discussions that Texon had with ASX about Talon s proposed listing on the ASX. At the date of this Demerger Scheme Booklet Texon is not aware of any reason why the condition referred to above about ASX listing will not be satisfied before the Second Court Date. SECTION 1 Summary of the Demerger Scheme

14 12 SECTION 1 Summary of the Demerger Scheme If the Effective Date does not occur on or before the End Date (or such later date as Texon determines), the Demerger Scheme will lapse and the Demerger will not be implemented. 1.6 Demerger Scheme Meeting On 22 January 2013, the Court ordered that the Demerger Scheme Meeting be convened in accordance with the Notice of Demerger Scheme Meeting. The Demerger Scheme Meeting will be held at the offices of Minter Ellison Lawyers, Level 22, Waterfront Place, 1 Eagle Street, Brisbane on 25 February 2013 at 11.30am. Each Texon Shareholder who is registered on the Texon Share Register as the holder of a Texon Share at 6.00pm on 23 February 2013 is entitled to attend and vote, in person, by attorney, by proxy or, in the case of corporate Texon Shareholders or proxies, by corporate representative, at the Demerger Scheme Meeting. Further details on how to vote are provided in the Notice of Demerger Scheme Meeting attached as Appendix 7 to this Demerger Scheme Booklet. For the Demerger Scheme to proceed, the Demerger Scheme Resolution must be approved by: a majority in number (more than 50%) of Texon Shareholders present and voting on the Demerger Scheme Resolution (whether in person, by proxy or attorney or, in the case of corporate Texon Shareholders or proxies, by corporate representative); 8 and at least 75% of the votes cast on the Demerger Scheme Resolution by Texon Shareholders (in person or by proxy, attorney or, in the case of corporate Texon Shareholders or proxies, by corporate representative). The fact that the Court has ordered that the Demerger Scheme Meeting be convened is no indication that the Court has a view as to the merits of the Demerger Scheme or as to how Texon Shareholders should vote at the Demerger Scheme Meeting. On these matters, Texon Shareholders must reach their own decision. 1.7 General Meeting The General Meeting will be convened in accordance with the Notice of General Meeting and will be held at the offices of Minter Ellison Lawyers, Level 22, Waterfront Place, 1 Eagle Street, Brisbane on 25 February 2013 at 1.30pm or as soon thereafter as the Acquisition Scheme Meeting has been concluded or adjourned. Each Texon Shareholder who is registered on the Texon Share Register as the holder of a Texon Share at 6.00pm on 23 February 2013 is entitled to attend and vote, in person, by attorney, by proxy or, in the case of corporate Texon Shareholders or proxies, by corporate representative, at the General Meeting. The Capital Reduction Resolution and other resolutions to be considered at the General Meeting are set out in the Notice of General Meeting. These resolutions will be passed with the approval of a simple majority of Texon Shareholders. 1.8 Demerger Scheme Consideration If the Demerger Scheme is approved then, subject to the arrangements for Ineligible Foreign Shareholders described in Section 1.11, the Eligible Scheme Shareholders will be entitled to receive the Demerger Scheme Consideration. In this regard: Texon is required to transfer the relevant number of Talon Shares to you on the Implementation Date; and a written advice confirming the number of Talon Shares will be sent by prepaid post to your address on the Texon Share Register (as at the Demerger Record Date) and the Computershare Investor Centre website will carry details of the Talon Shares issued to your holding. 1.9 Tax consequences Australian tax considerations for Texon Shareholders are discussed in Appendix 2 (Tax Implications for Texon Shareholders). 8 The Court has a discretion to approve the Demerger Scheme where it is approved by at least 75% of all votes cast on the resolution to approve the Demerger Scheme but not by a majority in number of Texon Shareholders voting on the resolution to approve the Demerger Scheme: refer to section 411(4)(a)(ii)(A) of the Corporations Act.

15 Demerger Scheme Booklet Demerger Scheme Deed Poll Talon has executed the Demerger Scheme Deed Poll under which it agreed, subject to the Demerger Scheme becoming Effective, to comply with all of the obligations attributed to it under the Demerger Scheme. A copy of the Demerger Scheme Deed Poll is attached at Appendix 4 to this Demerger Scheme Booklet Ineligible Foreign Shareholders Any Texon Shareholder whose address as shown in the Texon Share Register as outside Australia and its external territories, New Zealand, the United States of America, the United Kingdom, Singapore and Hong Kong will be regarded as an Ineligible Foreign Shareholder for the purpose of the Demerger Scheme, unless Texon determines that it is lawful and not unduly onerous or impracticable to provide that Scheme Shareholder with Talon Shares when the Demerger Scheme becomes Effective Existing Options Texon has procured all of the holders of the Existing Options at the date of this Demerger Scheme Booklet to enter into deeds under which their Existing Options will be cancelled for no consideration as at 5.00pm on the Effective Date, if those Existing Options have not been exercised on or before that date. This will mean that at 5.00pm on the Effective Date, Texon will have no options on issue to acquire Texon Shares. The Demerger Scheme will extend to Texon Shares that are issued on the exercise of any of the Existing Options between the date of this Demerger Scheme Booklet and the Effective Date. SECTION 1 Summary of the Demerger Scheme Ineligible Foreign Shareholders may vote at the Demerger Scheme Meeting and participate in the Demerger Scheme as Scheme Shareholders. However, Ineligible Foreign Shareholders will not be entitled to receive the Talon Shares transferred under the Demerger Scheme. If the Demerger Scheme is approved and implemented, the Talon Shares that would otherwise have been transferred to an Ineligible Foreign Shareholder will be transferred to the Sale Agent (and/or to a nominee of the Sale Agent) on the Implementation Date and sold with the net sale proceeds to be remitted to the Ineligible Foreign Shareholder. For detailed information regarding Ineligible Foreign Shareholders and how the proceeds of the Demerger Scheme Consideration will be provided to them, refer to Section 8.9(d).

16 14 2SECTION 2 Frequently asked questions

17 Demerger Scheme Booklet 15 Frequently asked questions Set out below are summary answers to some questions that Texon Shareholders may have in relation to the Demerger Scheme. This information should be read in conjunction with the remainder of this Demerger Scheme Booklet. QUESTION Why have I received this Demerger Scheme Booklet? SECTION All SECTION 2 Frequently asked questions This Demerger Scheme Booklet has been sent to you because you are a Texon Shareholder and Texon Shareholders are being asked to vote on the Demerger Scheme. If approved and implemented, the Demerger Scheme will result in the demerger and separate ASX listing of a public company, Talon, which is currently a wholly owned subsidiary of Texon and which will hold Texon s non-efs assets. This Demerger Scheme Booklet is intended to help you to decide how to vote on: the Demerger Scheme Resolution which needs to be passed at the Demerger Scheme Meeting to allow the Demerger Scheme to proceed; the Capital Reduction Resolution to be considered at the General Meeting which also needs to be passed to allow the Demerger Scheme to proceed. The Texon Directors recommend that you read the Demerger Scheme Booklet and, if necessary, consult your financial, legal, taxation, investment or other professional adviser before voting on the Demerger Scheme Resolution and Capital Reduction Resolution. What is the Demerger Scheme? The Demerger Scheme involves the demerger and separate ASX listing of a public company, Talon, which is currently a wholly owned subsidiary of Texon. Talon will hold Texon s non-efs assets. The Demerger Scheme is not conditional on whether the Acquisition Scheme is approved or implemented but is subject to a number of conditions, details of which are set out in Section 1.5. Section 1 and Section 8 For the Demerger Scheme to be implemented, Texon Shareholders will also need to approve the Capital Reduction Resolution at a general meeting of Texon Shareholders, which is separate to the meeting of Texon Shareholders convened to approve the Demerger Scheme. If the Demerger Scheme is approved by Texon Shareholders, the Capital Reduction Amount will be applied by Texon as consideration for the acquisition of Talon Shares. Accordingly, Texon Shareholders will not receive a cash payment for the Capital Reduction Amount, but instead they will receive two Talon Shares for every five Texon Shares they hold on the Demerger Record Date. 9 9 Note that if you are an Ineligible Foreign Shareholder, the Talon Shares that you would have otherwise received under the Demerger Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive, see Section 8.9(d).

18 16 SECTION 2 Frequently asked questions QUESTION What is the Acquisition Scheme? On 13 November 2012, Texon and Sundance announced the Acquisition Scheme to ASX. The Acquisition Scheme involves an offer by Sundance to acquire all Texon Shares held by Texon Shareholders in return for: Eligible Scheme Shareholders receiving one New Sundance Share for every two Texon Shares held at the Record Date (as defined in the Acquisition Scheme Booklet); and Ineligible Foreign Shareholders receiving the net proceeds of the sale of the New Sundance Shares to which they would otherwise have been entitled under the Acquisition Scheme, conditional on, among other things, the prior implementation of the Demerger Scheme. SECTION Acquisition Scheme Booklet The Acquisition Scheme will not be implemented if the Demerger Scheme is not approved and implemented. For details of the Acquisition Scheme, Texon Shareholders should refer to the Acquisition Scheme Booklet, which was sent at the same time as this Demerger Scheme Booklet. What will I receive if the Demerger proceeds? If the Demerger proceeds, you will: receive two Talon Shares for every five Texon Shares you hold on the Demerger Record Date (unless you are an Ineligible Foreign Shareholder). You will not be required to pay any cash for the Talon Shares that you receive in connection with the Demerger Scheme. Instead, you will be credited with the Capital Reduction Amount for each Texon Share you hold on the Demerger Record Date and those amounts will be applied as consideration for the Talon Shares you receive under the Demerger Scheme; if you are an Ineligible Foreign Shareholder, the Talon Shares that you would have received under the Demerger Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale being remitted to you, as further described in Section 8.9(d); if you become entitled to a fractional entitlement in a Talon Share, then your entitlement to Talon Shares will be rounded down to the nearest whole number, and the fractional entitlement will be ignored; and unless and until the Acquisition Scheme is implemented or you dispose of them in some other way, continue to hold the Texon Shares you held on the Demerger Record Date. Why is Texon proposing the Demerger Scheme? The principal objective of the Texon Directors in proposing the Demerger is to create value for Texon Shareholders. Following the implementation of the Demerger, Texon Shareholders are expected to realise the benefits set out in Section 3.1(a), which the Texon Directors believe should provide a superior long term outcome than what would be achieved if Talon were to remain part of Texon. The other reasons for the Texon Directors recommendation of the Demerger are set out in Section 3. Section 1 Section 3

19 Demerger Scheme Booklet 17 QUESTION What is Talon? Talon which is wholly owned by Texon, holds and will continue to hold after the Demerger is implemented, Texon s non-efs assets including: oil production from a well in the Olmos reservoir in its Mosman-Rockingham Olmos oil project, and also from a well in the Wilcox reservoir, in McMullen County, Texas; 29 undeveloped Olmos reservoir well locations within its Mosman-Rockingham Olmos oil project in McMullen County, Texas; a 47.4% Working Interest in the Roundhouse oil project; oil and gas leases located in East Texas; and access to 180 3D seismic surveys covering an area of 82,000 square miles in Southeast Texas. SECTION Section 4 SECTION 2 Frequently asked questions If the Demerger is implemented, Talon will be primarily focussed on exploration and development of oil and gas leases in Texas. For more information on Talon, see Section 4. Who can vote at the General Meeting and Demerger Scheme Meeting? Each Texon Shareholder who is registered on the Texon Share Register at 6.00pm on 23 February 2013 is entitled, in person, by attorney, by proxy or, in the case of corporate Texon Shareholders or proxies, by corporate representative, to attend and vote at the General Meeting and Demerger Scheme Meeting. How do I vote? Voting at the General Meeting and Demerger Scheme Meeting may be in person, by attorney, by proxy or, in the case of corporations, by corporate representative. If you wish to vote in person, you must attend the Demerger Scheme Meeting and General Meeting. If you cannot attend the Demerger Scheme Meeting or General Meeting, you may vote by proxy, attorney or, if you are a body corporate, by appointing a corporate representative. Please refer to the notices of meeting in Appendix 6 and Appendix 7 to this Demerger Scheme Booklet for further information on voting procedures and details of the resolutions to be voted on at the Meetings. Section 8 Appendix 6 and Appendix 7

20 18 SECTION 2 Frequently asked questions QUESTION Do the Texon Directors recommend the Demerger Scheme? The Texon Directors unanimously recommend that, in the absence of a Superior Proposal, you vote in favour of the Demerger Scheme Resolution at the Demerger Scheme Meeting and the Capital Reduction Resolution at the General Meeting to be held on 25 February SECTION Section 3 The Texon Directors make these recommendations for the following reasons: the separation of Texon s non-efs assets from its EFS assets has the potential to unlock value currently not being reflected in the Texon share price; whilst the Demerger Scheme is not conditional on the Acquisition Scheme and can proceed independently, if the Demerger Scheme is not approved, the Acquisition Scheme cannot proceed and so Texon Shareholders would not receive the Acquisition Scheme consideration of one New Sundance Share for every two Texon Shares under the Acquisition Scheme; Talon has potential to deliver value for Talon Shareholders; the Independent Expert has concluded that, in the absence of any other information or a superior proposal, that the Demerger Scheme is in the best interests of Texon Shareholders; and the Demerger Scheme provides investors with greater choice regarding the level of exposure they wish to have to the Texon and Talon businesses. The reasons for the Texon Directors unanimous recommendation are set out in more detail in Section 3. How are the Texon Directors intending to vote? The Texon Directors who hold or control Texon Shares intend to vote in favour of the Demerger Scheme Resolution and the Capital Reduction Resolution in respect of all their Texon Shares, in the absence of a Superior Proposal. What is the Independent Expert s opinion on the Demerger Scheme? The Texon Directors commissioned BDO Corporate Finance (QLD) Ltd to provide an Independent Expert s Report including an opinion as to whether the Demerger is in the best interests of Texon Shareholders. A complete copy of the Independent Expert s Report is contained in Appendix 1 of this Demerger Scheme Booklet. Texon Shareholders are encouraged to read the Independent Expert s Report in full. In summary, the Independent Expert has concluded that, on balance, the advantages of the Demerger Scheme outweigh the disadvantages of the Demerger Scheme and that, in the absence of any other information or a superior proposal, the Demerger Scheme is in the best interests of Texon Shareholders. Section 1.3 Appendix 1

21 Demerger Scheme Booklet 19 QUESTION Why might I vote against the Demerger Scheme? There are a number of reasons as to why you may vote against the Demerger including: Talon will, in comparison to Texon prior to the Demerger, be a much smaller company initially with production from only two wells and focused mostly on drilling new projects; Talon will no longer have the financial capacity of Texon; the size and diversification of both Texon and Talon will be reduced; Talon could in due course need to access new funding and raise new capital, including from its shareholders, after Talon is listed on the ASX; and the implementation of the Demerger will result in additional ongoing costs for Talon. SECTION Section 3 SECTION 2 Frequently asked questions For more information on the reasons why you may consider voting against the Demerger, see Section 3.1(b). What are the risks associated with the Demerger Scheme? The risks associated with the implementation of the Demerger Scheme include: the combined market value of Texon Shares and Talon Shares after the implementation of the Demerger Scheme may be less than the market value of Texon Shares prior to the implementation of the Demerger Scheme; there may be a volatile market for Talon Shares after the implementation of the Demerger Scheme; the Court may not approve the Demerger Scheme or that approval may be delayed; and any necessary third party consents may not be able to be obtained in a timely manner or at all. A discussion of these risks and other risks is set out in Section 6. When will I receive my Talon Shares? Provided the Demerger Scheme becomes Effective, Texon Shareholders on the Register at 6.00pm on the Demerger Record Date (other than Ineligible Foreign Shareholders) will receive on the Implementation Date two Talon Shares for every five Texon Shares held on the Demerger Record Date. 10 The expected date of dispatch of written advices confirming these holdings is 13 March The Computershare Investor Centre website will display the issue of Talon Shares from the Implementation Date. The sale of the Talon Shares that would have otherwise been issued to Ineligible Foreign Shareholders and the remittance of any proceeds of that sale to Ineligible Foreign Shareholders will occur within 30 Business Days after the Implementation Date. Section 6 Section 8 10 Note that if you are an Ineligible Foreign Shareholder, the Talon Shares that you would otherwise have received under the Demerger Scheme will be transferred to and sold by the Sale Agent with the net proceeds of sale remitted to you. For more information on what Ineligible Foreign Shareholders will receive, see Section 8.9(d). Fractional entitlements will be ignored.

22 20 SECTION 2 Frequently asked questions QUESTION When can I start trading my Talon Shares? You can start trading any Talon Shares issued to you as Demerger Scheme Consideration on a deferred settlement basis from 28 February It is the responsibility of Scheme Shareholders to confirm their entitlement to Talon Shares under the Demerger Scheme before trading those shares to avoid the risk of selling shares they do not own. SECTION Section 3.4(b) Scheme Shareholders who trade Talon Shares before receiving written confirmation of their entitlements do so at their own risk. Talon, Texon and the Talon Registry disclaim all liability (to the maximum extent permitted by law) to persons who trade Talon Shares before receiving this written confirmation, whether on the basis of confirmation of the allocation provided by Texon, Talon or the Talon Registry. How will the Demerger Scheme be implemented? The mechanics for implementing the Demerger are summarised in Section 8. However, in order for the Demerger to be implemented it is necessary for Texon Shareholders to approve the Demerger Resolution at the Demerger Scheme Meeting and the Capital Reduction Resolution at the General Meeting. The required voting majorities for these resolutions are summarised in Sections 8.4 and 8.5. In addition, the Court must approve the Demerger Scheme following the Texon Shareholders approving the resolutions referred to above, which it will be requested to do on the Second Court Date. Are there any conditions that must be satisfied in order for the Demerger Scheme to be implemented? Yes there are. Key conditions which remain outstanding at the date of this Demerger Scheme Booklet include: Texon Shareholders pass the Demerger Scheme Resolution at the Demerger Scheme Meeting by the required majority; Texon Shareholders pass the Capital Reduction Resolution at the General Meeting by the required majority; ASX approves the admission of Talon to the official list of ASX and grants permission for official quotation of the Talon Shares on ASX, subject only to the Demerger Scheme becoming Effective and other customary pre-quotation conditions (including the provision of information required by ASX); no temporary restraining order, preliminary or permanent injunction or other order is issued by any court of competent jurisdiction or other legal restraint or prohibition preventing the Demerger is in effect at 7.00am on the Second Court Date; and the Court approves the Demerger Scheme in accordance with section 411(4)(b) of the Corporations Act and an office copy of the order of the Court is lodged with ASIC. Further information about these conditions is provided in Section 1.5. Section 8 Section 1.5

23 Demerger Scheme Booklet 21 QUESTION What happens if these conditions are not satisfied? If the conditions to the Demerger Scheme are not satisfied or (where applicable) waived, the Demerger Scheme will not proceed and Texon will continue to own Talon and the non-efs assets and you will not receive any shares in Talon. In these circumstances: Texon Shareholders will not be able to realise the expected benefits of the Demerger Scheme; the Acquisition Scheme will not proceed (which means, among other things, that Texon Shareholders will not receive the Acquisition Scheme consideration of one New Sundance Share for every two Texon Shares they hold on the Record Date (as defined in the Acquisition Scheme Booklet) under the Acquisition Scheme and Texon would remain responsible for repayment of the principle and interest relating to the Loan Notes); and the market price of Texon Shares may fall. SECTION Section 5.6, Section 6.4(c) and Section 7 SECTION 2 Frequently asked questions For more information on the Loan Notes and the risks associated with them, please see Sections 5.6 and 6.4(c). For more information on what happens if the Demerger is not implemented, please see Section 7. What happens if the Demerger Scheme is approved, all conditions are satisfied and it is implemented? For every five Texon Shares held as at the Demerger Record Date, each Scheme Shareholder will receive two Talon Shares (or, in the case of an Ineligible Foreign Shareholder, the net cash proceeds of the sale by the Sale Agent of Talon Shares as described in Section 8.9(d)). If you become entitled to a fractional entitlement in a Talon Share, then your entitlement to Talon Shares will be rounded down to the nearest whole number, and the fractional entitlement will be ignored. Section 8 also provides information about the timing for transfer of Talon Shares to Texon Shareholders under the Demerger Scheme and trading of Talon Shares on the ASX. What are the tax consequences of receiving the Scheme Consideration? The taxation consequences of the Demerger being approved and implemented for Texon Shareholders will depend on the specific taxation circumstances of each Texon Shareholder. However, general information about the likely Australian taxation consequences of the Demerger is set out in Appendix 2 (Taxation Implications for Texon Shareholders). Texon Shareholders should consult their own taxation adviser about the taxation consequences for them if the Demerger Scheme is implemented. Section 8 Appendix 2

24 22 SECTION 2 Frequently asked questions QUESTION What is the Wandoo Interest Acquisition Agreement? The Wandoo Interest Acquisition Agreement is an agreement whereby the Texon Group will acquire certain carried working and royalty interests in the EFS assets from Wandoo, a company associated with Texon Director David Mason. The acquisition is subject to the implementation of the Demerger Scheme and Acquisition Scheme. The consideration is US$1.2 million cash payable in four equal quarterly instalments by Texoz E & P II, Inc (which will become a subsidiary of Sundance upon the implementation of the Acquisition Scheme), the first payable three months after completion of the demerger and 4,480,000 Talon Shares. The consideration is subject to adjustment downwards to US$1 million and 4,000,000 Talon Shares if binding agreements with certain landowners are not entered into within 12 months. SECTION Appendix 8 Appendix 8 contains a value analysis by the Independent Expert of the value of both the interests being acquired (as being in the range of $4 million to $4.7 million) and the consideration payable under the Wandoo Interest Acquisition Agreement (as being in the range of $1.9 million to $2.1 million). Because the value of the interests to be acquired exceeds the consideration payable, the Texon Directors (other than David Mason) have determined that it is not inappropriate that David Mason provides a recommendation in relation to the Demerger Scheme and the Acquisition Scheme. What if I want further information? If you have any questions about the Demerger Scheme or you would like additional copies of this Demerger Scheme Booklet, please call the Texon Shareholder Information Line on (within Australia) or (outside Australia) Monday to Friday between 8.30am and 5.00pm (Brisbane, Australia time). For information about your individual financial or taxation circumstances please consult your financial, legal, taxation or other professional adviser.

25 Demerger Scheme Booklet 23 3SECTION 3 Key reasons to vote in favour of or against the Demerger Scheme

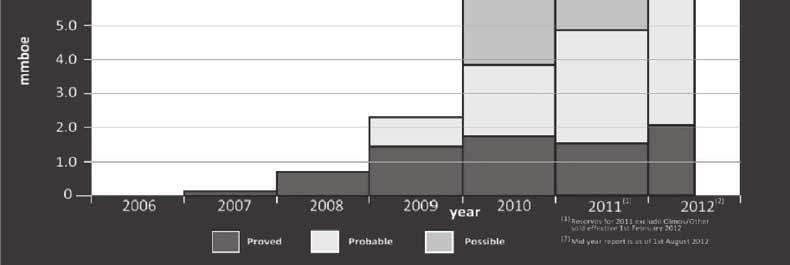

26 24 SECTION 3 Key reasons to vote in favour of or against the Demerger Scheme Key reasons to vote in favour of or against the Demerger Scheme 3.1 Summary (a) Advantages of the Demerger Scheme (i) The separation of Texon s non-efs assets from its EFS assets has the potential to unlock value currently not being reflected in the Texon share price; (ii) Whilst the Demerger Scheme is not conditional on the Acquisition Scheme and can proceed independently, if the Demerger Scheme is not approved, the Acquisition Scheme cannot proceed and so Texon Shareholders would not receive the Acquisition Scheme consideration of one New Sundance Share for every two Texon Shares under the Acquisition Scheme; (iii) Talon has potential to deliver value for Talon Shareholders; (iv) The Independent Expert has concluded that the Demerger Scheme is in the best interests of Texon Shareholders; and (v) The Demerger Scheme provides investors with greater choice regarding the level of exposure they wish to have to the Texon and Talon businesses. (b) Disadvantages of the Demerger Scheme (i) Talon will, in comparison to Texon prior to the Demerger, be a much smaller company initially with production from only two wells and focused mostly on drilling new projects; (ii) Talon will no longer have the financial capacity of Texon; (iii) The size and diversification of both Texon and Talon will be reduced; (iv) Talon could in due course need to access new funding and raise new capital, including from its shareholders, after Talon is listed on the ASX; and (v) The implementation of the Demerger will result in additional ongoing costs for Talon. 3.2 Advantages of the Demerger Scheme (a) The separation of Texon s non-efs assets from its EFS assets has the potential to unlock value currently not being reflected in the Texon share price The Texon Directors believe that the potential value of Talon s assets is not being reflected in the Texon share price and that the Demerger Scheme represents an opportunity for the potential value in Talon s assets to be realised. Some of the key factors in forming this view included the following: (1) Talon s assets have significant exploration potential The Demerger Scheme provides a mechanism for Texon shareholders to retain their interest in Texon s non-efs assets via a shareholding in Talon. The Texon Directors believe the non-efs assets have significant exploration potential. (2) Development of Talon s assets has been impeded by the financing requirements of Texon s EFS assets The development of Texon s EFS assets has required significant capital and this has meant that the development of Talon s assets has been, to a large extent, delayed. After the conclusion of the restructure to be undertaken under the Demerger Deed and any adjustments made under the Scheme Implementation Agreement, Talon is expected to have cash reserves of approximately $8.8 million if the Acquisition Scheme is not implemented or $7.8 million 11 if the Acquisition Scheme is implemented. If the Demerger Scheme is implemented, this capital will fund the committed portion of Talon s exploration and development plan (as described in Sections 3.2(c) and 4.5 below) for the following 12 months. Talon intends to obtain additional funds to fulfil an expanded plan by pursuing sell down and joint venture arrangements in respect of its Olmos, Roundhouse and other East Texas 11 This figure includes an amount of $1.5 million, which is required to be held in escrow for at least six months after the date on which the Acquisition Scheme is implemented.

27 Demerger Scheme Booklet 25 prospects. The Texon Directors believe that the exploration and development of Talon s assets will be significantly improved by way of the Demerger Scheme. (b) Whilst the Demerger Scheme is not conditional on the Acquisition Scheme and can proceed independently, if the Demerger Scheme is not approved, the Acquisition Scheme cannot proceed and so Texon Shareholders would not receive the Acquisition Scheme consideration The Acquisition Scheme provides Texon Shareholders with what the Texon Directors believe is an attractive opportunity to receive the Acquisition Scheme consideration of one New Sundance Share for every two Texon Shares held. The implied value of the Acquisition Scheme consideration per Texon Share is $ Texon Shareholders should note that the implied value of the Acquisition Scheme consideration will change from time to time based on movements in the Sundance Share price. Based on the closing Sundance Share price on the ASX of $0.88 on Monday, 21 January 2013, being the last practicable date prior to the finalisation of this Demerger Scheme Booklet, the implied value of the Acquisition Scheme consideration was $0.44 per Texon Share. As this consideration does not include a value for the Talon business, the Acquisition Scheme is conditional upon implementation of the Demerger Scheme. If the Demerger Scheme does not proceed, Texon Shareholders will not have the opportunity to receive New Sundance Shares for their Texon Shares under the Acquisition Scheme. The Texon Directors have recommended that Texon Shareholders vote in favour of the Acquisition Scheme. The reasons why the Texon Directors recommend Texon Shareholders vote in favour of the Acquisition Scheme are set out in detail in the Acquisition Scheme Booklet. (c) Talon has an attractive portfolio of exploration and appraisal projects that have the potential to deliver value for Talon Shareholders Talon has potential to deliver value for Talon Shareholders from its portfolio of projects which includes the following: South Texas Projects: Olmos Talon s Mosman-Rockingham Olmos oil project in McMullen County, Texas currently has Proved, Probable and Possible reserves of 1.3 MMBOE with a resource potential for 3 MMBOE. This prospect is defined by 3D seismic data and, based on 40 acre spacing, holds up to 29 well locations for the Olmos reservoir. Additional upside may be developed utilising horizontal drilling and fracturing technologies. East Texas Projects: Roundhouse Talon s Roundhouse oil project is located in East Texas and is a north-eastern extension of Cheneyboro oil field in Navarro County, Texas. It is a moderate to low risk prospect with potential for MMBOE. Talon holds 3,510 net Working Interest acres (which equates to a 47.4% Working Interest) in the Roundhouse (Cotton Valley Lime Reservoir) prospect and a test well is planned for drilling in mid Red Fish, Catfish Creek and East Banks Talon has leased 2,917 net Working Interest acres 13 targeting shallow oil reservoirs previously produced in old vertical wells with little or no reservoir stimulation defined by 2D seismic data and historical production data. Based on 80 acre spacing and Talon s current 2,917 net Working Interest acres, there are 36 locations that between them have gross potential of 4.8 MMBOE. Talon has set a target of leasing 20,000 net Working Interest acres in these prospects and, if successful, there may be up to 250 locations with a gross potential of 33 MMBOE. SECTION 3 Key reasons to vote in favour of or against the Demerger Scheme 12 The Acquisition Scheme Consideration comprises one New Sundance Share for every two Texon Shares. For illustrative purposes, the implied value of the Acquisition Scheme Consideration is $0.41 per Texon Share, based on the closing share prices of Sundance Shares on 12 November 2012, being the day immediately preceding announcement of the Acquisition Scheme. The value of the Acquisition Scheme Consideration will fluctuate and will be determined by the price at which New Sundance Shares trade. New Sundance Shares are likely to trade at prices that are different to the prices used in calculating the implied value of the Acquisition Scheme Consideration. 13 Under the Prospect Generation Agreement, Wandoo has the right to acquire up to 3% of this Working Interest. For more information on the Prospect Generation Agreement, please see Section 4.4(f).