IMPORTANT NOTICE v

|

|

|

- Leo Gordon

- 5 years ago

- Views:

Transcription

1 IMPORTANT NOTICE THE ATTACHED BASE PROSPECTUS IS AVAILABLE ONLY TO INVESTORS WHO ARE EITHER: (1) QIBs (AS DEFINED BELOW) THAT ARE ALSO QPs (AS DEFINED BELOW); OR (2) NOT U.S. PERSONS (AS DEFINED IN REGULATION S (AS DEFINED BELOW)). IMPORTANT: You must read the following before continuing. The following applies to the attached base prospectus (the "Base Prospectus") and you are therefore advised to read this carefully before reading, accessing or making any other use of the attached Base Prospectus. In accessing the attached Base Prospectus, you agree to be bound by the following terms and conditions, including any modifications to them any time you receive any information from the Trustee, KFH, the Arrangers and the Dealers (each as defined below) as a result of such access. NOTHING IN THIS ELECTRONIC TRANSMISSION CONSTITUTES AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO BUY THE SECURITIES IN THE UNITED STATES OR IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO. THE SECURITIES DESCRIBED IN THE ATTACHED BASE PROSPECTUS HAVE NOT BEEN AND WILL NOT BE, REGISTERED UNDER THE U.S. SECURITIES ACT OF 1933, AS AMENDED (THE "SECURITIES ACT"), OR THE SECURITIES LAWS OF ANY STATE OF THE U.S. OR OTHER JURISDICTIONS, NOR MAY THEY BE OFFERED OR SOLD WITHIN THE UNITED STATES OR TO, OR FOR THE ACCOUNT OR BENEFIT OF, U.S. PERSONS (AS DEFINED IN REGULATION S UNDER THE SECURITIES ACT ("REGULATION S")), EXCEPT (1) IN ACCORDANCE WITH RULE 144A UNDER THE SECURITIES ACT TO PERSONS REASONABLY BELIEVED TO BE "QUALIFIED INSTITUTIONAL BUYERS" ("QIBs") WITHIN THE MEANING OF RULE 144A WHO ARE ALSO QUALIFIED PURCHASERS AS DEFINED IN SECTION 2(A)(51)(A) OF THE U.S. INVESTMENT COMPANY ACT OF 1940, AS AMENDED (EACH A "QP") WHO REPRESENT THAT: (A) THEY ARE QPS WHO ARE QIBS WITHIN THE MEANING OF RULE 144A; (B) THEY ARE NOT BROKER DEALERS WHO OWN AND INVEST ON A DISCRETIONARY BASIS LESS THAN U.S.$25 MILLION IN SECURITIES OF UNAFFILIATED ISSUERS; (C) THEY ARE NOT A PARTICIPANT DIRECTED EMPLOYEE PLAN, SUCH AS A 401(K) PLAN; (D) THEY ARE ACTING FOR THEIR OWN ACCOUNT, OR THE ACCOUNT OF ONE OR MORE QIBS, EACH OF WHICH IS ALSO A QP; (E) THEY ARE NOT FORMED FOR THE PURPOSE OF INVESTING IN THE SECURITIES OR THE TRUSTEE; (F) THEY UNDERSTAND THAT THE TRUSTEE MAY RECEIVE A LIST OF PARTICIPANTS HOLDING POSITIONS IN ITS SECURITIES FROM ONE OR MORE BOOK ENTRY DEPOSITORIES; AND (G) THEY WILL PROVIDE NOTICE OF THESE TRANSFER RESTRICTIONS TO ANY SUBSEQUENT TRANSFEREES; OR (2) IN AN OFFSHORE TRANSACTION TO A PERSON THAT IS NOT A U.S. PERSON IN ACCORDANCE WITH RULE 903 OR RULE 904 OF REGULATION S UNDER THE SECURITIES ACT. THE DISTRIBUTION IN THE UK OF THE BASE PROSPECTUS, ANY FINAL TERMS AND ANY OTHER MARKETING MATERIALS RELATING TO THE SECURITIES IS BEING ADDRESSED TO, OR DIRECTED AT: (A) IF THE SECURITIES ARE "ALTERNATIVE FINANCE INVESTMENT BONDS" ("AFIBS") AND THE DISTRIBUTION IS BEING EFFECTED BY A PERSON WHO IS NOT AN AUTHORISED PERSON UNDER THE FINANCIAL SERVICES AND MARKETS ACT 2000 (THE "FSMA"), ONLY THE FOLLOWING PERSONS: (I) PERSONS WHO ARE INVESTMENT PROFESSIONALS AS DEFINED IN ARTICLE 19(5) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (FINANCIAL PROMOTION) ORDER 2005 (THE "FINANCIAL PROMOTION ORDER"); (II) PERSONS FALLING WITHIN ANY OF THE CATEGORIES OF PERSONS DESCRIBED IN ARTICLE 49 (HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, ETC.) OF THE FINANCIAL PROMOTION ORDER; AND (III) ANY OTHER PERSON TO WHOM IT MAY OTHERWISE LAWFULLY BE MADE IN ACCORDANCE WITH THE FINANCIAL PROMOTION ORDER; AND (B) IF THE SECURITIES ARE NOT AFIBS AND THE DISTRIBUTION IS EFFECTED BY A PERSON WHO IS AN AUTHORISED PERSON UNDER THE FSMA, ONLY THE FOLLOWING PERSONS: (I) PERSONS FALLING WITHIN ONE OF THE CATEGORIES OF INVESTMENT PROFESSIONAL AS DEFINED IN ARTICLE 14(5) OF THE FINANCIAL SERVICES AND MARKETS ACT 2000 (PROMOTION OF COLLECTIVE INVESTMENT SCHEMES) (EXEMPTIONS) ORDER 2001 (THE "PROMOTION OF CISS ORDER"); (II) PERSONS FALLING WITHIN ANY OF THE CATEGORIES OF PERSON DESCRIBED IN ARTICLE 22 (HIGH NET WORTH COMPANIES, UNINCORPORATED ASSOCIATIONS, ETC.) OF THE PROMOTION OF CISS ORDER; AND (III) ANY OTHER PERSON TO WHOM IT MAY OTHERWISE LAWFULLY BE MADE IN ACCORDANCE WITH THE v

2 PROMOTION OF CISS ORDER (ALL SUCH PERSONS TOGETHER BEING REFERRED TO AS "RELEVANT PERSONS"). THE ATTACHED BASE PROSPECTUS MAY NOT BE FORWARDED OR DISTRIBUTED TO ANY OTHER PERSON AND MAY NOT BE REPRODUCED IN ANY MANNER WHATSOEVER. ANY FORWARDING, DISTRIBUTION OR REPRODUCTION OF THE ATTACHED BASE PROSPECTUS IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO COMPLY WITH THIS DIRECTIVE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER JURISDICTIONS. IF YOU HAVE GAINED ACCESS TO THIS TRANSMISSION CONTRARY TO ANY OF THE FOREGOING RESTRICTIONS, YOU ARE NOT AUTHORISED, AND WILL NOT BE ABLE, TO PURCHASE ANY OF THE SECURITIES DESCRIBED THEREIN. CONFIRMATION OF YOUR REPRESENTATION: In order to be eligible to view the attached Base Prospectus or make an investment decision with respect to the Certificates (as defined in the attached Base Prospectus), an investor must be: (i) a person that is outside the United States and is not a U.S. person (within the meaning of Regulation S); or (ii) a person that is a "qualified institutional buyer" ("QIBs") (within the meaning of Rule 144A under the Securities Act ("Rule 144A")) that is also a "qualified purchaser" (each a "QP") (within the meaning of Section 2(a)(51)(A) of the U.S. Investment Company Act of 1940, as amended (the "Investment Company Act")), and the rules and regulations thereunder. The attached Base Prospectus is being sent at your request and by accepting the and accessing the attached Base Prospectus, you shall be deemed to have represented to Kuwait Finance House K.S.C.P. ("KFH"), KFH Sukuk Company SPC Limited (the "Trustee"), KFH Capital Investment Company K.S.C.C. and Standard Chartered Bank (the "Arrangers") and each of KFH Capital Investment Company K.S.C.C., Standard Chartered Bank and any other dealers appointed under the Programme (as defined herein) from time to time by KFH and the Trustee, which appointment may be for a specific issue of securities or on an ongoing basis (together, the "Dealers") that: (a) you and any customers you represent are either: (1) persons other than U.S. persons (within the meaning of Regulation S); or (2) QIBs that are also QPs; (b) you are a person who is permitted under applicable law and regulation to receive the attached Base Prospectus; and (c) you consent to delivery of the attached Base Prospectus and any amendments or supplements thereto by electronic transmission. By accessing the attached Base Prospectus you further confirm to us that: (i) you understand and agree to the terms set out herein; (ii) you will not transmit the attached Base Prospectus (or any copy of it or part thereof) or disclose, whether orally or in writing, any of its contents to any other person; and (iii) you acknowledge that you will make your own assessment regarding any credit, investment, legal, taxation or other economic considerations with respect to your decision to subscribe or purchase any of the Certificates. You are reminded that the attached Base Prospectus has been delivered to you on the basis that you are a person into whose possession the attached Base Prospectus may be lawfully delivered in accordance with the laws of the jurisdiction in which you are located and you may not, nor are you authorised to, deliver the attached Base Prospectus to any other person. Failure to comply with this directive may result in a violation of the Securities Act or the applicable laws of other jurisdictions. The attached Base Prospectus does not constitute, and may not be used in connection with, an offer or solicitation in any place where offers or solicitations are not permitted by law. If a jurisdiction requires that an offering of securities described herein be made by a licensed broker or dealer and the Arrangers and any Dealer or any affiliate of the Arrangers or the relevant Dealer is a licensed broker or dealer in that jurisdiction, the offering shall be deemed to be made by such Arranger or Dealer or such affiliate on behalf of the Trustee or holders of the applicable securities in such jurisdiction. Under no circumstances shall the attached Base Prospectus constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of the securities described herein in any jurisdiction in which such offer, solicitation or sale would be unlawful. Recipients of the attached Base Prospectus who intend to subscribe for or purchase the Certificates are reminded that any subscription or purchase may only be made on the basis of the information contained in the attached Base Prospectus as completed by the applicable Final Terms and/or supplement(s) to the Base Prospectus (if any). The attached Base Prospectus may only be communicated to persons in the United Kingdom in circumstances where Section 21(1) of the Financial Services and Markets Act 2000, as amended does not apply v

3 The distribution of the attached Base Prospectus in certain jurisdictions may be restricted by law. Persons into whose possession the attached Base Prospectus comes are required by the Trustee, KFH, the Arrangers and the Dealers to inform themselves about, and to observe, any such restrictions. The attached Base Prospectus has been sent to you in an electronic form. You are reminded that documents transmitted via this medium may be altered or changed during the process of electronic transmission and consequently neither the Trustee, KFH, the Arrangers and Dealers nor any person who controls them nor any director, officer, employee nor agent of them or affiliate of any such person accepts any liability or responsibility whatsoever in respect of any difference between the Base Prospectus distributed to you in electronic format and the hard copy version available to you on request from the Trustee, KFH, the Arrangers and the Dealers. Please ensure that your copy is complete. If you received the Base Prospectus by , you should not reply by to this announcement. Any reply communications, including those you generate by using the "reply" function on your software, will be ignored or rejected. You are responsible for protecting against viruses and other destructive items. Your use of this is at your own risk, and it is your responsibility to take precautions to ensure that it is free from viruses and other items of a destructive nature v

described in this base prospectus (the \"Base Prospectus\"), KFH Sukuk Company SPC Limited (in its capacity as issuer and as")

(as defined below). The maximum aggregate face amount of all Certificates outstanding from time to time will not be more than U.S.")

4 BASE PROSPECTUS KFH SUKUK COMPANY SPC LIMITED (incorporated in the Dubai International Financial Centre as a Special Purpose Company) U.S.$3,000,000,000 Trust Certificate Issuance Programme Under the U.S.$3,000,000,000 trust certificate issuance programme (the "Programme") described in this base prospectus (the "Base Prospectus"), KFH Sukuk Company SPC Limited (in its capacity as issuer and as trustee, the "Trustee"), subject to compliance with all relevant laws, regulations and directives, may from time to time issue trust certificates (the "Certificates") denominated in any currency agreed between the Trustee and the relevant Dealer(s) (as defined below). The maximum aggregate face amount of all Certificates outstanding from time to time will not be more than U.S.$3,000,000,000 (or its equivalent in other currencies calculated as described in the Programme Agreement described herein), subject to any increase as described herein. Each Tranche (as defined in "Terms and Conditions of the Certificates" (the "Conditions")) of Certificates issued under the Programme will be constituted by: (i) a master declaration of trust dated 16 May 2018 (the "Master Declaration of Trust") entered into between the Trustee, Kuwait Finance House K.S.C.P. ("KFH") and Citibank, N.A., London Branch as delegate of the Trustee (in such capacity, the "Delegate"); and (ii) a supplemental declaration of trust in relation to the relevant Series (each a "Supplemental Declaration of Trust" and together with the Master Declaration of Trust, each a "Declaration of Trust"). Certificates of each Tranche confer on the holders of the Certificates from time to time (the "Certificateholders") the right to receive certain payments (as more particularly described herein) arising from a pro rata ownership interest in the assets of a trust declared by the Trustee in relation to the relevant Series (the "Trust") over the Trust Assets (as defined herein). Certificates may only be issued in registered form. The Certificates may be issued on a continuing basis to one or more of the Dealers specified under "Overview of the Programme" and any additional Dealer appointed under the Programme from time to time (each a "Dealer" and together, the "Dealers"), which appointment may be for a specific issue or on an ongoing basis. References in this Base Prospectus to the "relevant Dealer" shall, in the case of an issue of Certificates being (or intended to be) subscribed by more than one Dealer, be to all Dealers agreeing to subscribe for such Certificates. The Certificates will be limited recourse obligations of the Trustee. An investment in Certificates issued under the Programme involves certain risks. For a discussion of certain of these risks, please see "Risk Factors" on page 9. This Base Prospectus has been approved by the Central Bank of Ireland (the "Central Bank") as competent authority under Directive 2003/71/EC, as amended, and includes any relevant implementing measure in a relevant Member State of the European Economic Area (for the purposes of this Base Prospectus, the "Prospectus Directive"). The Central Bank only approves this Base Prospectus as meeting the requirements imposed under Irish and European Union ("EU") law pursuant to the Prospectus Directive. Application has been made to the Irish Stock Exchange plc, trading as Euronext Dublin ("Euronext Dublin") for Certificates issued under this Programme during the period of 12 months from the date of this Base Prospectus to be admitted to the official list (the "Official List") and to trading on its regulated market (the "Main Securities Market"). The Main Securities Market is a regulated market for the purposes of the Markets in Financial Instruments Directive (Directive 2014/65/EU) ("MiFID II"). Such approval relates only to Certificates which are to be admitted to trading on a regulated market for the purposes of MiFID II and/or which are to be offered to the public in any Member State of the European Economic Area. References in this Base Prospectus to Certificates (other than Non-PD Certificates (as defined below)) being "listed" (and all related references) shall mean that such Certificates have been admitted to trading on the Main Securities Market and have been admitted to the Official List. Notice of the aggregate face amount of the Certificates, profit (if any) payable in respect of the Certificates, the issue price of the Certificates and certain other terms and conditions not contained herein which are applicable to each Tranche of Certificates (other than Non-PD Certificates) will be set out in the applicable final terms (the "Final Terms") which will be delivered to the Central Bank and Euronext Dublin. The Programme also permits Certificates to be issued on the basis that they will not be admitted to listing, trading on a regulated market for the purposes of the Markets in Financial Instruments Directive in the European Economic Area and/or quotation by any competent authority, stock exchange and/or quotation system or may be admitted to listing, trading and/or quotation by such other or further competent authorities, stock exchanges and/or quotation systems as may be agreed between the Trustee, KFH and the relevant Dealer ("Non-PD Certificates"). The Certificates have not been and will not be registered under the U.S. Securities Act of 1933, as amended (the "Securities Act"), or any U.S. state securities laws and subject to certain exceptions, the Certificates may not be offered or sold in the United States or to, or for the account or the benefit of, U.S. persons (as defined in Regulation S under the Securities Act ("Regulation S")). The Certificates are being offered and sold outside the United States to persons who are not U.S. persons in reliance on Regulation S and within the United States only to persons who are reasonably believed to be "qualified institutional buyers" ("QIBs") in reliance on Rule 144A under the Securities Act ("Rule 144A") that are also "qualified purchasers" (each a "QP") within the meaning of Section 2(a)(51)(A) of the U.S. Investment Company Act of 1940, as amended (the "Investment Company Act"), and the rules and regulations thereunder. Please see "Form of Certificates" for a description of the manner in which Certificates will be issued. Certificates are subject to certain restrictions on transfer. Please see "Subscription and Sale and Transfer and Selling Restrictions". Prospective purchasers are hereby notified that sellers of the Certificates may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. The Trustee is a "covered fund" for the purposes of the "Volcker Rule" contained in Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Volcker Rule"). The acquisition of the Certificates is likely to be considered an acquisition of an "ownership interest" (as that term is used in the Volcker Rule) in a "covered fund". Accordingly, entities that may be "banking entities" for the purposes of the Volcker Rule, which is broadly defined to include U.S. banks and bank holding companies and many non-u.s. banking entities, together with their respective subsidiaries and other affiliates, may be restricted from holding the Certificates. Any prospective investor in the Certificates, including a U.S. or foreign bank or a subsidiary should consult its own legal advisors regarding such matters and other effects of the Volcker Rule. For further information, see "Important Notices". KFH has been assigned a long-term foreign currency issuer default rating of A+ with a stable outlook from Fitch Ratings Limited ("Fitch") and a long-term bank deposits rating of A1 with a negative outlook from Moody's Investors Service Ltd. ("Moody's"). Each of Fitch and Moody's has also rated the Trustee's Programme at A+ and A1, respectively. The rating of certain Series of Certificates to be issued under the Programme and the credit rating agency issuing such rating may be specified in the applicable Final Terms. Where an issue of Certificates is rated, its rating will not necessarily be the same as the rating applicable to the Programme. Each of Fitch and Moody's is established in the European Union and is registered under the Regulation (EC) No. 1060/2009 (as amended) (the "CRA Regulation"). As such, each of Fitch and Moody's is included in the list of credit rating agencies published by the European Securities and Markets Authority on its website in accordance with the CRA Regulation. A security rating is not a recommendation to buy, sell or hold securities and may be subject to suspension, reduction or withdrawal at any time by the assigning rating agency. The transaction structure relating to the Certificates (as described in this Base Prospectus) has been approved by the KFH Capital Shari'a Committee and the Shariah Supervisory Committee of Standard Chartered Bank. Prospective Certificateholders should not rely on the approval referred to above in deciding whether to make an investment in the Certificates and should consult their own Shari'a advisors as to whether the proposed transaction described in the approval referred to above is in compliance with their individual standards of compliance with Shari'a principles. Arrangers KFH Capital KFH Capital Dealers Standard Chartered Bank Standard Chartered Bank The date of this Base Prospectus is 16 May v

5 IMPORTANT NOTICES This Base Prospectus comprises a base prospectus for the purposes of Article 5.4 of the Prospectus Directive and for the purpose of giving information with regard to the Trustee, KFH, the Group (as defined below) and the Certificates which, according to the particular nature of the Trustee, KFH, the Group and the Certificates, is necessary to enable investors to make an informed assessment of the assets and liabilities, financial position, profit and losses and prospects of the Trustee, KFH and the Group. The Trustee and KFH accept responsibility for the information contained in this Base Prospectus and the applicable Final Terms for each Series of Certificates issued under the Programme. To the best of the knowledge of the Trustee and KFH (each having taken all reasonable care to ensure that such is the case) the information contained in this Base Prospectus is in accordance with the facts and does not omit anything likely to affect the import of such information. Each Tranche of Certificates will be issued on the terms set out herein under "Terms and Conditions of the Certificates" as completed by the applicable Final Terms. This Base Prospectus must be read and construed together with any amendments or supplements hereto and with any information incorporated by reference herein and, in relation to any Tranche of Certificates which is the subject of the Final Terms, must be read and construed together with the applicable Final Terms. The only persons authorised to use this Base Prospectus in connection with an offer of Certificates are the relevant Dealers or the Managers (as identified in the relevant subscription agreement), as the case may be. Copies of the applicable Final Terms will be available from the registered office of the Trustee and the specified office of each of the Paying Agents (as defined in "Terms and Conditions of the Certificates"). Certain statistical information included in this Base Prospectus has been extracted from official public sources (see further, "Presentation of Financial and other Information Presentation of Statistical Information"). Certain information appearing on pages 171 to 174 (inclusive) of this Base Prospectus under the heading "Book-Entry Clearance Systems" has been obtained from the clearing systems referred to herein. The Trustee and KFH confirms that all third party information contained in this Base Prospectus has been accurately reproduced and that, so far as it is aware and is able to ascertain from information published by the relevant third parties, no facts have been omitted which would render the reproduced information inaccurate or misleading. The source of any third party information contained in this Base Prospectus is stated where such information appears in this Base Prospectus. No person is or has been authorised by the Trustee or KFH to give any information or to make any representation not contained in or not consistent with this Base Prospectus or any other document entered into in relation to the Programme or any other information supplied by the Trustee or KFH or such other information as is in the public domain in connection with the Programme or the Certificates and, if given or made, such information or representation must not be relied upon as having been authorised by the Trustee, KFH or the Arrangers or any Dealers. To the fullest extent permitted by law, neither the Arrangers, the Delegate, the Agents nor any of the Dealers accept (1) any responsibility for (i) the contents of this Base Prospectus or (ii) any information incorporated by reference into this document or (iii) for any other statement made, or purported to be made, by the Arrangers or any Dealer or on any of their affiliates on their behalf or (2) any responsibility for any acts or omissions of the Trustee, KFH or any other person (other than the relevant Arranger or Dealer), in connection with the Trustee, KFH, or the issue and offering of the Certificates. The Arrangers, the Delegate, the Agents and each Dealer accordingly disclaims all and any liability whether arising in tort or contract or otherwise which it might otherwise have in respect of this Base Prospectus or any such statement. Neither this Base Prospectus, any Final Terms nor any other information supplied in connection with the Programme or any Certificates: (i) is intended to provide the basis of any credit or other evaluation; or (ii) should be considered as a recommendation by the Trustee, KFH, the Arrangers, v i

6 the Dealers, the Delegate or the Agents that any recipient of this Base Prospectus, any Final Terms or any other information supplied in connection with the Programme or any Certificates should purchase any Certificates. Each investor contemplating purchasing any Certificates should make its own independent investigation of the financial condition and affairs, and its own appraisal of the creditworthiness, of the Trustee and/or KFH. Neither this Base Prospectus, any Final Terms nor any other information supplied in connection with the Programme or the issue of any Certificates constitutes an offer or invitation by or on behalf of the Trustee, KFH, the Arrangers, the Delegate, the Agents or any of the Dealers to any person to subscribe for or to purchase any Certificates. The only persons authorised to use this Base Prospectus in connection with an offer of Certificates are the persons named in the relevant subscription agreement as the relevant Managers. Neither the delivery of this Base Prospectus, any Final Terms nor the offering, sale or delivery of any Certificates shall in any circumstances imply that the information contained herein concerning the Trustee and/or KFH is correct at any time subsequent to the date hereof or that any other information supplied in connection with the Programme is correct as of any time subsequent to the date indicated in the document containing the same. The Arrangers, the Delegate, the Agents and the Dealers expressly do not undertake to review the financial condition or affairs of the Trustee or KFH during the life of the Programme or to advise any investor in the Certificates of any information coming to their attention. USE OF BENCHMARK Amounts payable under the Certificates may be calculated by reference to: EURIBOR (as defined in the Conditions), which is provided by the European Money Markets Institute; and LIBOR (as defined in the Conditions), which is provided by the ICE Benchmark Administration, each such provider together referred to as the "Administrators". As at the date of this Base Prospectus, the Administrators do not appear on the register of administrators and benchmarks established and maintained by the European Securities and Markets Authority ("ESMA") pursuant to article 36 of the Benchmark Regulation (Regulation (EU) 2016/1011) (the "Benchmark Regulations"). As far as the Trustee and KFH are aware, the transitional provisions in Article 51 of the Benchmark Regulations apply, such that the Administrators are not currently required to obtain authorisation or registration (or, if located outside the European Union, recognition, endorsement or equivalence). This Base Prospectus does not constitute an offer to sell or the solicitation of an offer to buy any Certificates in the United States or in any jurisdiction, in each case, to any person to whom it is unlawful to make the offer or solicitation in such jurisdiction. The distribution of this Base Prospectus and the offer or sale of Certificates may be restricted by law in certain jurisdictions. None of the Trustee, KFH, the Arrangers, the Delegate, the Agents or the Dealers represent that this Base Prospectus may be lawfully distributed, or that any Certificates may be lawfully offered, in compliance with any applicable registration or other requirements in any such jurisdiction, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any such distribution or offering. In particular, no action has been taken by the Trustee, KFH, the Arrangers, the Delegate, the Agents or the Dealers which is intended to permit a public offering of any Certificates or distribution of this Base Prospectus in any jurisdiction where action for that purpose is required. Accordingly, no Certificates may be offered or sold, directly or indirectly, and neither this Base Prospectus nor any advertisement or other offering material may be distributed or published in any jurisdiction, except under circumstances that will result in compliance with any applicable laws and regulations. Persons into whose possession this Base Prospectus or any Certificates may come must inform themselves about, and observe, any such restrictions on the distribution of this Base Prospectus and the offering and sale of Certificates. In particular, there are restrictions on the distribution of this Base Prospectus and the offer, sale or transfer of v ii

7 Certificates in the Dubai International Financial Centre, the European Union, Hong Kong, Japan, Malaysia, the Kingdom of Bahrain, the Kingdom of Saudi Arabia, Singapore, the State of Kuwait, the State of Qatar, the United Arab Emirates (the "UAE") (excluding the Dubai International Financial Centre), the United Kingdom and the United States. Please see "Subscription and Sale and Transfer and Selling Restrictions". The Certificates may not be a suitable investment for all investors. Each potential investor in the Certificates must determine the suitability of that investment in light of its own circumstances. In particular, each potential investor should: have sufficient knowledge and experience to make a meaningful evaluation of the Certificates, the merits and risks of investing in the Certificates and the information contained or incorporated by reference in this Base Prospectus or any applicable supplement; have access to, and knowledge of, appropriate analytical tools to evaluate, in the context of its particular financial situation, an investment in the Certificates and the impact such investment will have on its overall investment portfolio; have sufficient financial resources and liquidity to bear all of the risks of an investment in the Certificates, including Certificates with principal or profit payable in one or more currencies, or where the currency for principal or profit payments is different from the potential investor's currency; understand thoroughly the terms of the Certificates and be familiar with the behaviour of any relevant indices and financial markets; and be able to evaluate (either alone or with the help of a financial advisor) possible scenarios for economic, profit rate and other factors that may affect its investment and its ability to bear the applicable risks. Some Certificates may be complex financial instruments. Sophisticated institutional investors generally do not purchase complex financial instruments as stand-alone investments. They generally purchase complex financial instruments as a way to reduce risk or enhance yield with an understood, measured and appropriate addition of risk to their overall portfolios. A potential investor should not invest in an issue of Certificates which are complex financial instruments unless it has the expertise (either alone or with a financial advisor) to evaluate how the Certificates will perform under changing conditions, the resulting effects of the value of the Certificates and the impact this investment will have on the potential investor's overall investment portfolio. In the case of any Certificates which are to be admitted to trading on a regulated market within the European Economic Area or offered to the public in a Member State of the European Economic Area in circumstances which require the publication of a prospectus under the Prospectus Directive, the minimum specified denomination shall be 100,000 (or its equivalent in any other currency as of the date of issue of the Certificates). None of the Trustee, KFH, the Arrangers, the Delegate, the Agents or the Dealers has authorised, nor do they authorise, the making of any offer of Certificates in circumstances in which an obligation arises for the Trustee, KFH or any Dealer to publish or supplement a prospectus for such offer. In making an investment decision, investors must rely on their own independent examination of the Trustee and KFH and the terms of the Certificates being offered, including the merits and risks involved. None of the Trustee, KFH, the Arrangers, the Delegate, the Agents or the Dealers makes any representation to any investor in the Certificates regarding the legality of its investment under any applicable laws. Any investor in the Certificates should be able to bear the economic risk of an investment in the Certificates for an indefinite period of time v iii

8 Legal investment considerations may restrict certain investments. The investment activities of certain investors are subject to legal investment laws and regulations, or review or regulation by certain authorities. Each potential investor should consult its legal advisors to determine whether and to what extent: (i) the Certificates constitute legal investments for it; (ii) the Certificates can be used as collateral for various types of borrowing; and (iii) other restrictions apply to any purchase or pledge of any Certificates by the investor. Financial institutions should consult their legal advisors or the appropriate regulations to determine the appropriate treatment of the Certificates under any applicable risk-based capital or similar rules and regulations. The requirement to publish a base prospectus under the Prospectus Directive only applies to Certificates which are to be admitted to trading on a regulated market for the purposes of MiFID II in the European Economic Area and/or offered to the public in the European Economic Area other than in circumstances where an exemption is available under Article 3.2 of the Prospectus Directive (as implemented in the relevant Member State(s)). References in this Base Prospectus to "Non-PD Certificates" are to Certificates issued by the Trustee for which no base prospectus is required to be published under the Prospectus Directive. The Central Bank of Ireland has neither approved nor reviewed information contained in this Base Prospectus in connection with Non-PD Certificates. U.S. INFORMATION This Base Prospectus is being provided on a confidential basis in the United States to a limited number of QIBs who are also QPs for informational use solely in connection with the consideration of the purchase of certain Certificates issued under the Programme. Its use for any other purpose in the United States is not authorised. It may not be copied or reproduced in whole or in part nor may it be distributed or any of its contents disclosed to anyone other than the prospective investors to whom it is originally provided. Certificates may only be offered or sold only to persons who are not U.S. persons, or to persons who are QIBs that are also QPs, in transactions exempt from registration under the Securities Act. The Certificates are being offered and sold in the United States in reliance upon an exemption from registration under the Securities Act for an offer and sale of the Certificates which does not involve a public offering. Prospective purchasers are hereby notified that sellers of the Certificates may be relying on the exemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. THE CERTIFICATES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE U.S. SECURITIES AND EXCHANGE COMMISSION, ANY SECURITIES COMMISSION OF ANY STATE IN THE UNITED STATES OR ANY OTHER U.S. REGULATORY AUTHORITY, NOR HAS ANY OF THE FOREGOING AUTHORITIES PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OF CERTIFICATES OR THE ACCURACY OR THE ADEQUACY OF THIS BASE PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENCE IN THE UNITED STATES. Each purchaser or holder of Individual Certificates (as defined herein), Certificates represented by a Restricted Global Certificate (as defined herein) or any Certificates issued in registered form in exchange or substitution therefor (together "Legended Certificates") will be deemed, by its acceptance or purchase of any such Legended Certificates, to have made certain representations and agreements intended to restrict the resale or other transfer of such Certificates as set out in "Subscription and Sale and Transfer and Selling Restrictions". Unless otherwise stated, terms used in this paragraph have the meanings given to them in "Form of Certificates". VOLCKER RULE The Trustee is a "covered fund" for the purposes of the "Volcker Rule" contained in Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The definition of "covered fund" in the Volcker Rule includes (generally) any entity that would be an investment company under the Investment Company Act, but for the exemption provided under Section 3(c)(1) or 3(c)(7) thereunder. Because the Trustee intends to rely on Section 3(c)(7) of the Investment Company Act for its exemption from registration thereunder, (which limits sales of the Certificates to QPs), it is considered to be a covered v iv

9 fund. The Volcker Rule generally prohibits "banking entities" (which is broadly defined to include U.S. banks and bank holding companies and many non-u.s. banking entities, together with their respective subsidiaries and other affiliates) from: (i) engaging in proprietary trading; (ii) acquiring or retaining an ownership interest in or sponsoring a "covered fund"; and (iii) entering into certain relationships with such funds. "Ownership interest" under the Volcker Rule is defined broadly to include any participation or other interest that entitles the holder of such interest to, amongst other things: (i) vote to remove management or otherwise, other than as a creditor exercising remedies upon an event of default, (ii) share in the income, gains, profits or excess spread of the covered fund or (iii) receive underlying assets of the covered fund. Any prospective investor in the Certificates, including a U.S. or foreign bank or a subsidiary or other affiliate thereof, should consult its own legal advisors regarding such matters and other effects of the Volcker Rule. AVAILABLE INFORMATION To permit compliance with Rule 144A in connection with any resales or other transfers of Certificates that are "restricted securities" within the meaning of Rule 144(a)(3) of the Securities Act, the Trustee (failing which, KTH) has undertaken in the Master Declaration of Trust to furnish, upon the request of a holder of such Certificates or any beneficial interest therein, to such holder or to a prospective purchaser designated by such holder or beneficial owner, the information specified in, and meeting the requirements of, Rule 144A(d)(4) under the Securities Act if, at the time of the request, any of the Certificates remain outstanding as "restricted securities" within the meaning of Rule 144(a)(3) of the Securities Act and the Trustee is neither subject to Sections 13 or 15(d) of the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act") nor exempt from reporting requirements pursuant to and in compliance with Rule 12g3-2(b) under the Exchange Act. SERVICE OF PROCESS AND ENFORCEMENT OF CIVIL LIABILITIES The Trustee is a special purpose company incorporated in the Dubai International Financial Centre (the "DIFC") and KFH is a Public Kuwaiti Shareholding Company incorporated in Kuwait. All of the officers and directors of the Trustee and KFH named herein reside outside the United States and all or a substantial portion of the assets of each of the Trustee and KFH and its officers and directors are located outside the United States. As a result: it may not be possible for investors to effect service of process outside the DIFC upon the Trustee or its officers and directors, or to enforce judgments against them predicated upon United States federal securities laws; and it may not be possible for investors to effect service of process outside the State of Kuwait upon KFH or its officers and directors, or to enforce judgments against them predicated upon United States federal securities laws. The Certificates and the Transaction Documents (excluding the Master Purchase Agreement as supplemented by the applicable Supplemental Purchase Agreement (which are governed by Kuwaiti law)) are governed by English law and disputes in respect of them may be settled under the Arbitration Rules of the London Court of International Arbitration (the "LCIA Rules") in London, England. Investors may have difficulties in enforcing any arbitration award against the Trustee or KFH in the courts of Kuwait. In addition, even if English law is accepted as the governing law, this will only be applied to the extent that it is compatible with the mandatory rules of Kuwaiti law and public policy. Moreover, judicial precedent in Kuwait has no binding effect on subsequent decisions and there is no formal system of reporting court decisions in Kuwait. These factors create greater judicial uncertainty than would be expected in certain other jurisdictions. See "Risk Factors Risks Relating to Enforcement Certificateholders will only be able to enforce their contractual rights under the Certificates through arbitration before the London Court of International Arbitration ("LCIA") and LCIA awards relating to disputes arising under the Certificates may not be enforceable in Kuwait". NOTICE TO RESIDENTS OF THE KINGDOM OF BAHRAIN In relation to investors in the Kingdom of Bahrain, Certificates issued in connection with this Base Prospectus and related offering documents may only be offered in registered form to existing accountholders and accredited investors as defined by the Central Bank of Bahrain ("CBB") in the v v

10 Kingdom of Bahrain where such investors make a minimum investment of at least U.S.$100,000 or the equivalent amount in any other currency or such other amount as the CBB may determine. This Base Prospectus does not constitute an offer of securities in the Kingdom of Bahrain pursuant to the terms of Article (81) of the Central Bank and Financial Institutions Law 2006 (decree Law No. 64 of 2006). This Base Prospectus and related offering documents have not been and will not be registered as a prospectus with the CBB. Accordingly, no Certificates may be offered, sold or made the subject of an invitation for subscription or purchase nor will this Base Prospectus or any other related document or material be used in connection with any offer, sale or invitation to subscribe or purchase Certificates, whether directly or indirectly, to persons in the Kingdom of Bahrain, other than to accredited investors for an offer outside the Kingdom of Bahrain. The CBB has not reviewed, approved or registered this Base Prospectus or related offering documents and it has not in any way considered the merits of the Certificates to be offered for investment, whether in or outside the Kingdom of Bahrain. Therefore, the CBB assumes no responsibility for the accuracy and completeness of the statements and information contained in this Base Prospectus and expressly disclaims any liability whatsoever for any loss howsoever arising from reliance upon the whole or any part of the content of this Base Prospectus. No offer of securities will be made to the public in the Kingdom of Bahrain and this Base Prospectus must be read by the addressee only and must not be issued, passed to, or made available to the public generally. NOTICE TO RESIDENTS OF THE KINGDOM OF SAUDI ARABIA This Base Prospectus may not be distributed in the Kingdom of Saudi Arabia except to such persons as are permitted under the Rules on the Offer of Securities and Continuing Obligations issued by the Capital Market Authority of the Kingdom of Saudi Arabia (the "Capital Market Authority"). The Capital Market Authority does not make any representations as to the accuracy or completeness of this Base Prospectus and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this Base Prospectus. Prospective purchasers of Certificates should conduct their own due diligence on the accuracy of the information relating to the Certificates. If a prospective purchaser does not understand the contents of this Base Prospectus, he or she should consult an authorised financial advisor. NOTICE TO RESIDENTS OF THE STATE OF QATAR The Certificates will not be offered, sold or delivered, at any time, directly or indirectly, in the State of Qatar (including the Qatar Financial Centre) in a manner that would constitute a public offering. This Base Prospectus has not been and will not be reviewed or approved by or registered with the Qatar Central Bank, the Qatar Exchange, the Qatar Financial Centre Regulatory Authority or the Qatar Financial Markets Authority in accordance with their regulations or any other regulations in the State of Qatar. The Certificates are not and will not be traded on the Qatar Exchange. NOTICE TO RESIDENTS OF THE STATE OF KUWAIT Unless all necessary approvals from the Kuwait Capital Markets Authority (the "CMA") pursuant to Law No. 7 of 2010, and its executive bylaws (each as amended) (the "CML Rules") together with the various resolutions, regulations, directives and instructions issued pursuant thereto, or in connection therewith (regardless of nomenclature) or any other applicable law or regulation in Kuwait, have been given in respect of the marketing and sale of the Certificates, the Certificates may not be offered for sale, nor sold, in Kuwait. This Base Prospectus is not for general circulation to the public in Kuwait nor will the Certificates be sold by way of a public offering in Kuwait. In the event where the Certificates are intended to be purchased onshore in Kuwait, the same may only be so purchased through a licensed person duly authorised to undertake such activity pursuant to the CML Rules. Investors from Kuwait acknowledge that the CMA and all other regulatory bodies in Kuwait assume no responsibility whatsoever for the contents of this Base Prospectus and do not approve the contents thereof or verify the validity and accuracy of its contents. The CMA, and all other regulatory bodies in Kuwait, assume no responsibility whatsoever for any damages that may result from relying (in whole or in part) on the contents of this Base Prospectus. Prior to purchasing any Certificates, it is recommended that a prospective holder of any Certificates seeks professional advice from its advisors in respect to the contents of this Base Prospectus so as to determine the suitability of purchasing the Certificates v vi

11 NOTICE TO RESIDENTS OF MALAYSIA The Certificates may not be issued, offered or sold and no invitation to subscribe for or purchase the Certificates in Malaysia may be made, directly or indirectly, and any document or other materials in connection therewith may not be distributed in Malaysia other than to persons falling within the categories set out in Schedule 6 or Section 229(1)(b) and Schedule 8 or Section 257(3) and Schedule 7 or Section 230(1)(b), read together with Schedule 9 or Section 257(3) of the Capital Market and Services Act 2007 of Malaysia ("CMSA"). The Securities Commission of Malaysia shall not be liable for any non-disclosure on the part of the Trustee or KFH and assumes no responsibility for the correctness of any statements made or opinions or reports expressed in this Base Prospectus. NOTICE TO UK RESIDENTS Any Certificates to be issued under the Programme which do not constitute "alternative finance investment bonds" ("AFIBs") within the meaning of Article 77A of the Financial Services and Markets Act 2000 (Regulated Activities) (Amendment) Order 2010 will represent interests in a collective investment scheme (as defined in the Financial Services and Markets Act 2000, as amended (the "FSMA")) which has not been authorised, recognised or otherwise approved by the United Kingdom Financial Conduct Authority. Accordingly, this Base Prospectus is not being distributed to, and must not be passed on to, the general public in the United Kingdom. The distribution in the United Kingdom of this Base Prospectus, any applicable Final Terms and any other marketing materials relating to the Certificates is being addressed to, or directed at: (A) if the Certificates are AFIBs and the distribution is being effected by a person who is not an authorised person under the FSMA, only the following persons: (i) persons who are Investment Professionals as defined in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Financial Promotion Order"); (ii) persons falling within any of the categories of persons described in Article 49 (high net worth companies, unincorporated associations, etc.) of the Financial Promotion Order; and (iii) any other person to whom it may otherwise lawfully be made in accordance with the Financial Promotion Order; and (B) if the Certificates are not AFIBs and the distribution is effected by a person who is an authorised person under the FSMA, only the following persons: (i) persons falling within one of the categories of Investment Professional as defined in Article 14(5) of the Financial Services and Markets Act 2000 (Promotion of Collective Investment Schemes) (Exemptions) Order 2001 (the "Promotion of CISs Order"); (ii) persons falling within any of the categories of person described in Article 22 (high net worth companies, unincorporated associations, etc.) of the Promotion of CISs Order; and (iii) any other person to whom it may otherwise lawfully be made in accordance with the Promotion of CISs Order. Persons of any other description in the United Kingdom may not receive and should not act or rely on this Base Prospectus, any applicable Final Terms or any other marketing materials in relation to the Certificates. Potential investors in the United Kingdom in any Certificates which are not AFIBs are advised that all, or most, of the protections afforded by the United Kingdom regulatory system will not apply to an investment in such Certificates and that compensation will not be available under the United Kingdom Financial Services Compensation Scheme. Any individual intending to invest in any investment described in this Base Prospectus should consult his professional advisor and ensure that he fully understands all the risks associated with making such an investment and that he has sufficient financial resources to sustain any loss that may arise from such investment. MIFID II PRODUCT GOVERNANCE / TARGET MARKET The Final Terms in respect of any Certificates may include a legend entitled "MiFID II Product Governance" which will outline the target market assessment in respect of the Certificates and which channels for distribution of the Certificates are appropriate. Any person subsequently offering, selling or recommending the Certificates (a "distributor") should take into consideration the target market assessment; however, a distributor subject to MiFID II is responsible for undertaking its own target market assessment in respect of the Certificates (by either adopting or refining the target market assessment) and determining appropriate distribution channels v vii

12 A determination will be made in relation to each issue about whether, for the purpose of the MiFID II Product Governance rules under EU Delegated Directive 2017/593 (the "MiFID II Product Governance Rules"), any Dealer subscribing for any Certificates is a manufacturer in respect of such Trust Certificates, but otherwise neither the Arrangers nor the Dealers nor any of their respective affiliates will be a manufacturer for the purpose of the MiFID Product Governance Rules. IMPORTANT EEA RETAIL INVESTORS If the applicable Final Terms in respect of any Certificates includes a legend entitled "Prohibition of Sales to EEA Retail Investors", the Certificates, from the date of application of Regulation (EU) No 1286/2014 (the "PRIIPs Regulation"), are not intended to be offered, sold or otherwise made available to and, with effect from such date, should not be offered, sold or otherwise made available to any retail investor in the European Economic Area ("EEA"). For these purposes, a retail investor means a person who is one (or more) of: (i) a retail client as defined in point (11) of Article 4(1) of MiFID II; (ii) a customer within the meaning of Directive 2002/92/EC ("IMD"), where that customer would not qualify as a professional client as defined in point (10) of Article 4(1) of MiFID II; or (iii) not a qualified investor as defined in the Prospectus Directive. Consequently, no key information document required by the PRIIPs Regulation for offering or selling the Certificates or otherwise making them available to retail investors in the EEA has been prepared and therefore offering or selling the Certificates or otherwise making them available to any retail investor in the EEA may be unlawful under the PRIIPs Regulation. SUPPLEMENTARY PROSPECTUS Following the publication of this Base Prospectus, a supplement may be prepared by the Trustee and approved by the Central Bank in accordance with Article 16 of the Prospectus Directive. Statements contained in any such supplement shall, to the extent applicable (whether expressly, by implication or otherwise), be deemed to modify or supersede statements contained in this Base Prospectus. Any statement so modified or superseded shall not, except as so modified or superseded, constitute a part of this Base Prospectus. The Trustee and KFH have given an undertaking to the Arrangers and Dealers that if at any time during the duration of the Programme there is a significant new factor, material mistake or inaccuracy relating to information contained in this Base Prospectus which is capable of affecting the assessment of any Certificates and whose inclusion in or removal from this Base Prospectus is necessary for the purpose of allowing an investor to make an informed assessment of the assets and liabilities, financial position, profits and losses and prospects of the Trustee and KFH, and the rights attaching to the Certificates, the Trustee shall prepare an amendment or supplement to this Base Prospectus or publish a replacement Base Prospectus for use in connection with any subsequent offering of the Certificates and shall supply to the Arrangers and each Dealer such number of copies of such supplement hereto as the Arrangers and/or such Dealer may reasonably request. STABILISATION IN CONNECTION WITH THE ISSUE OF ANY TRANCHE OF CERTIFICATES, ONE OR MORE RELEVANT DEALERS (THE "STABILISATION MANAGER(S)") (OR ANY PERSON ACTING ON BEHALF OF ANY STABILISATION MANAGER(S)) MAY OVER-ALLOT CERTIFICATES OR EFFECT TRANSACTIONS WITH A VIEW TO SUPPORTING THE MARKET PRICE OF THE CERTIFICATES AT A LEVEL HIGHER THAN THAT WHICH MIGHT OTHERWISE PREVAIL. HOWEVER, STABILISATION MAY NOT NECESSARILY OCCUR. ANY STABILISATION ACTION MAY BEGIN ON OR AFTER THE DATE ON WHICH ADKFH PUBLIC DISCLOSURE OF THE TERMS OF THE OFFER OF THE RELEVANT TRANCHE IS MADE AND, IF BEGUN, MAY CEASE AT ANY TIME, BUT IT MUST END NO LATER THAN THE EARLIER OF 30 DAYS AFTER THE ISSUE DATE OF THE RELEVANT TRANCHE AND 60 DAYS AFTER THE DATE OF THE ALLOTMENT OF THE RELEVANT TRANCHE. ANY STABILISATION ACTION OR OVER-ALLOTMENT MUST BE CONDUCTED BY THE RELEVANT STABILISATION MANAGER(S) (OR PERSONS ON BEHALF OF ANY STABILISATION MANAGER(S)) IN ACCORDANCE WITH ALL APPLICABLE LAWS AND RULES v viii

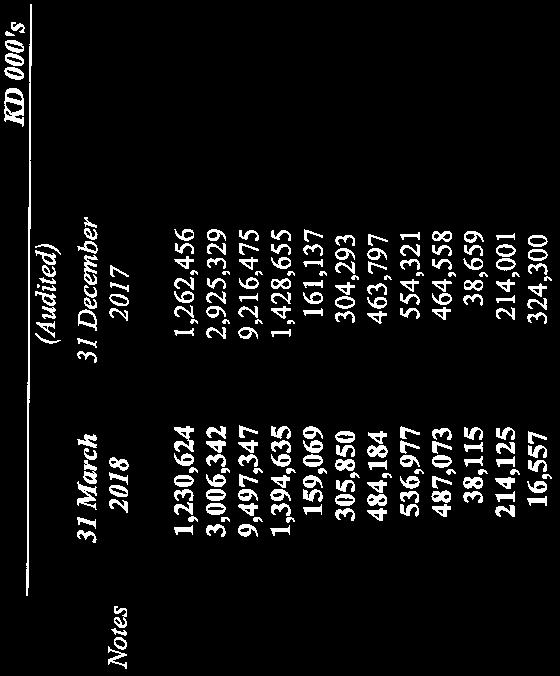

13 PRESENTATION OF FINANCIAL AND OTHER INFORMATION Presentation of Financial Information This Base Prospectus contains the audited consolidated financial statements of the Group as at and for the year ended 31 December 2017 (with comparative data for the year ended 31 December 2016) (the "2017 Consolidated Financial Statements") and the audited consolidated financial statements of the Group as at and for the year ended 31 December 2016 (with comparative data for the year ended 31 December 2015) (the "2016 Consolidated Financial Statements" and, together with the 2017 Consolidated Financial Statements, the "Financial Statements"). Except where explicitly disclosed, the financial data relating to KFH and its financial position presented in this Base Prospectus and relating to the financial information as at and for the year ended 31 December 2017 is derived from the 2017 Consolidated Financial Statements and relating to the financial information as at and for the year ended 31 December 2016 is derived from the comparative financial information as at and for the year ended 31 December 2016 included in the 2017 Consolidated Financial Statements. The financial data relating to KFH and its financial position presented in this Base Prospectus and relating to the financial information as at and for the year ended 31 December 2015 is derived from comparative financial information as at and for the year ended 31 December 2015 included in the 2016 Consolidated Financial Statements. The Financial Statements have been prepared in accordance with International Financial Reporting Standards ("IFRS"), as adopted for use in the State of Kuwait for financial services institutions regulated by the CBK, as further described in Note 2.1 (Basis of Preparation) to the 2017 Consolidated Financial Statements and Note 2.1 (Basis of Preparation) to the 2016 Consolidated Financial Statements. The Financial Statements have been jointly audited by Ernst & Young Al Aiban, Al Osaimi & Partners with license no. 68A ("EY") and Deloitte & Touche Al Wazzan & Co. with license no. 62A ("Deloitte") in accordance with International Standards on Auditing ("ISAs") as stated in their audit reports included therein. The CBK regulations require the adoption of all IFRS requirements except the IAS 39 "Financial Instruments: Recognition and Measurement" requirement for collective provision on credit facilities, which has been replaced by the CBK's requirement for a minimum general provision to be made on all applicable credit facilities that are not impaired (net of certain categories of collateral). Therefore, the Group's policy for the calculation of collective provision on credit facilities complies in all material respects with the relevant requirements of the CBK. For further information, see Note 2.1 (Basis of Preparation) to the 2017 Consolidated Financial Statements and Note 2.1 (Basis of Preparation) to the 2016 Consolidated Financial Statements. The Group's financial year ends on 31 December and references in this Base Prospectus to any specific year are to the 12-month period ended on 31 December of such year. The Group publishes its financial statements in Kuwaiti dinars. Any financial information regarding the Group in this Base Prospectus labelled as "unaudited" has not been extracted from the Financial Statements, but has been extracted or derived from interim financial statements or from the KFH's, the Group's or any Subsidiaries' unaudited management accounts based on accounting records of the relevant entity, as applicable, or is based on calculations of figures from interim financial statements and/or unaudited management accounts. This Base Prospectus contains the interim condensed consolidated financial information (unaudited) of the Group as of and for the three months ended 31 March 2018 and the notes thereto set forth elsewhere herein (the "2018 Interim Financial Statements"). Certain numerical figures set out in this Base Prospectus, including financial and operating data have been subject to rounding adjustments and some of these and other figures are also presented in KD millions or KD billions rather than in KD thousands as in the Financial Statements. Therefore, the sums of amounts given in some columns or rows in the tables and other lists presented in this Base Prospectus may slightly differ from the totals specified for such columns or rows. Similarly, some percentage values presented in the tables in this Base Prospectus have been subject to rounding adjustments and the totals specified in such tables may not add up to 100 per cent. Percentages and amounts reflecting changes over time periods relating to financial and other data are calculated using the numerical data in the relevant Financial Statements and not using the numerical data in the narrative description thereof v ix

14 The financial information included in this Base Prospectus is not intended to comply with the applicable accounting requirements of the Securities Act and the related rules and regulations which would apply if the Certificates were being registered with the U.S. Securities and Exchange Commission (the "SEC"). The information with respect to the Group has not been prepared in accordance with, and is not intended to comply with, the applicable accounting requirements of the Securities Act and the related rules and regulations of the SEC which would apply if the Certificates were being registered with the SEC. In particular, the average balances and related data are based on materially less frequent averaging methods than those used by other banks in the United States, Western Europe and other jurisdictions in connection with similar offers of securities. Prospective investors should be aware that the results of the analysis for the Group would likely be different, if alternative or more frequent averaging methods were used and such differences could be material. Certain Reclassifications In the 2017 Consolidated Financial Statements certain reclassifications to the comparative financial information as at and for the year ended 31 December 2016 have been made to conform to the presentation of such financial information adopted in the 2017 Consolidated Financial Statements. These reclassifications were made to more appropriately present certain items of consolidated statement of financial position, consolidated statement of income, consolidated cash flow statement and disclosures. Since these reclassifications are not reflected in the 2016 Consolidated Financial Statements (which contain financial information as at and for the year ended 31 December 2016 as well as the comparative financial information as at and for the year ended 31 December 2015) due to the fact that the 2016 Consolidated Financial Statements have not been so restated, investors should be aware that financial information contained in the 2016 Consolidated Financial Statements is not comparable in all respects with that contained in the 2017 Consolidated Financial Statements. The key reclassifications are summarized below: the "investment in sukuk" asset line item, as set out in the Consolidated Statement of Financial Position of the Group on page 103 of the Base Prospectus, has been presented as a separate asset line item as at 31 December 2017 and as at 31 December As at 31 December 2015, "investment in sukuk" were not set out as a separate asset line item and instead were aggregated together within the "investments" asset line item which comprised of "investment in sukuk" and other investments. A separate line item was put in place in the 2017 Consolidated Financial Statements for "investment in sukuk" given they were a major component of "investments" for the Group as at 31 December 2017 and as at 31 December This reclassification was done for better financial data presentation and to match industry presentation benchmarks; the "sukuk payables" liabilities line item, as set out in the Consolidated Statement of Financial Position of the Group on page 103 of the Base Prospectus, has been presented as a separate liabilities line item as at 31 December 2017 and as at 31 December As at 31 December 2015, "sukuk payables" were not set out as a separate liabilities line item and instead were aggregated together within the "due to banks and other financial institutions" liabilities line item which comprised of "sukuk payables" and other dues to banks and other financial institutions. A separate line item was put in place in the 2017 Consolidated Financial Statements for "sukuk payables" given they were a major component of "due to banks and other financial institutions" for the Group as at 31 December 2017 and as at 31 December This reclassification was done for better financial data presentation and to match industry presentation benchmarks; Consolidated Statement of Income of the Group on page 102 of the Base Prospectus reflects certain reclassifications with respect to some of the figures relating to the year ended 31 December "(Loss)/Profit after tax for the year from discontinued operations" for the year ended 31 December 2015 was presented below the line item Profit for the year from continuing operations" in the 2016 Consolidated Financial Statements. This has been moved above the line item "Profit before taxation and proposed directors' fees" as "(Loss)/Profit for the year from discontinued operations" on page 105 of the Base Prospectus to ensure consistency with the presentation in the 2017 Consolidated Financial Statements. On account of the change, "(Loss)/Profit after tax for the year from discontinued operations has been renamed to "(Loss)/Profit for the year from discontinued operations and the figure has changed from KD 21.9 million to KD 22.7 million, Profit before taxation and proposed directors fees has changed from KD million to KD million and taxation has changed from KD 20.4 million to KD 21.2 million for the year ended 31 December v x

15 This amendment in presentation does not change the overall Profit for the year amount with respect to the year ended 31 December Investors should be aware that, to the limited extent identified above, the financial information as at 31 December 2017 and 31 December 2016 contained in the 2017 Consolidated Financial Statements is not comparable with that contained in the 2016 Consolidated Financial Statements. Alternative Performance Measures Certain financial measures included in this Base Prospectus are not defined in accordance with IFRS accounting standards. KFH believes that these non-ifrs measures and alternative performance measures (as defined in the European Securities and Markets Authority guidelines (the "ESMA Guidelines") on Alternative Performance Measures ("APMs")) provide useful supplementary information to both investors and to KFH's management as they facilitate the evaluation of underlying operating performance and financial position across financial reporting periods. However, investors should note that, since not all companies calculate non-ifrs financial measurements (such as the APMs presented by KFH in this Base Prospectus) in the same manner, these are not always directly comparable to performance metrics used by other companies. Such non-ifrs measures should not be considered in isolation and are not measures of financial performance or liquidity under IFRS. Accordingly, these non-ifrs measures should not be considered as an alternative to revenues, profit or loss for the period or any other performance measures derived in accordance with IFRS or as an alternative to cash flow from operating, investing or financing activities or any other measure of liquidity derived in accordance with IFRS. Non-IFRS measures do not necessarily indicate whether cash flow will be sufficient or available for cash requirements and may not be indicative of actual results of operations. In addition, the APMs presented by KFH in this Base Prospectus may not be comparable to other similarly titled measures used by other companies. Because of the discretion that KFH and other companies have in defining these measures and calculating the reported amounts, care should be taken in comparing these various measures with similar measures used by other companies. Additionally, the APMs presented by KFH in this Base Prospectus are unaudited and have not been prepared in accordance with IFRS or any other accounting standards. Accordingly, these financial measures should not be seen as a substitute for measures defined according to IFRS. KFH considers that the following metrics (which are set out below along with their reconciliation with the Financial Statements (to the extent that such information is not defined according to IFRS and not included in the Financial Statements included elsewhere in this Base Prospectus)) presented in this Base Prospectus constitute APMs for the purposes of the ESMA Guidelines: APM Method of Calculation Reconciliation with Financial Statements Return on average assets Return on average equity Profit for the year divided by average assets for the year. Profit for the year attributable to shareholders of KFH divided by average shareholders' equity for the year. Profit for the year (as set out in the consolidated statement of income in the Financial Statements) divided by the average assets for the year. Average asset is the sum of total assets at the beginning of the year and at the end of each quarter divided by five. Refers to the same concept/figure as total assets (as set out in the consolidated statement of financial position in the Financial Statements). Profit for the year attributable to shareholders of the bank (as set out in the consolidated statement of income in the Financial Statements) divided by the average shareholders' equity for the year. Average shareholders' equity is the sum of total equity attributable to the shareholders of the bank at the beginning of the year and at the end of each quarter divided by five. Refers to the same concept/figure as total equity attributable to the shareholders of the bank (as set out in the consolidated statement of financial position in the v xi

16 APM Method of Calculation Reconciliation with Financial Statements Financial Statements). Cost to income ratio Net profit margin Total operating expenses for the year divided by the total operating income for the year. Profit for the year attributable to shareholders of KFH divided by the total operating income for the year. Total operating expenses for the year (as set out in the consolidated statement of income in the Financial Statements) divided by the total operating income for the year (as set out in the consolidated statement of income in the Financial Statements). Profit for the year attributable to shareholders of the bank (as set out in the Consolidated Statement of Income in the Financial Statements) divided by the total operating income for the year (as set out in the Consolidated Statement of Income in the Financial Statements). Impaired ratio Provision coverage ratio Liquidity coverage ratio Loans to total deposits ratio CET 1 capital adequacy ratio Non-performing financing (net of deferred and suspended profit) divided by financing receivables (net of deferred and suspended profit). Impairment for financing receivables divided by non-performing cash finance facilities before impairment (net of deferred and suspended profit). Calculated and disclosed as daily averages of the ratio components for the corresponding quarterend in accordance with the requirements of CBK Circular number 2/IBS/346/2014 dated 23 December Total financing receivables divided by total depositors' accounts. CET 1 capital divided by risk-weighted assets at a given date. Calculated in accordance with the requirements of the CBK and the capital adequacy regulations issued by the CBK as stipulated in CBK Circular number 2/RB, RBA/A336/2014 dated 24 June Non-performing cash finance facilities before impairment (net of deferred and suspended profit) (as set out in Note 10 (Financing Receivables) to the 2017 Consolidated Financial Statements and Note 10 (Financing Receivables) to the 2016 Consolidated Financial Statements) divided by financing receivables (net of deferred and suspended profit) (as set out in Note 10 (Financing Receivables) to the 2017 Consolidated Financial Statements and Note 10 (Financing Receivables) to the 2016 Consolidated Financial Statements). Impairment for financing receivables (as set out in Note 10 (Financing Receivables) to the 2017 Consolidated Financial Statements and Note 10 (Financing Receivables) to the 2016 Consolidated Financial Statements) divided by nonperforming cash finance facilities before impairment (net of deferred and suspended profit) (as set out in Note 10 (Financing Receivables) to the 2017 Consolidated Financial Statements and Note 10 (Financing Receivables) to the 2016 Consolidated Financial Statements). Calculated as stipulated in accordance with the requirements of CBK Circular number 2/IBS/346/2014 dated 23 December Financing receivables for the year (as set out in the consolidated statement of financial position in the Financial Statements) divided by depositors' accounts for the year (as set out in the consolidated statement of financial position in the Financial Statements). CET 1 capital calculated in accordance with the requirements of the CBK and the capital adequacy regulations issued by the CBK as stipulated in CBK Circular number 2/RB, RBA/A336/2014 dated 24 June 2014 divided by risk-weighted assets (as set out in Note 32 (Capital Management) to the 2017 Consolidated Financial Statements and Note 32 (Capital Management) to the 2016 Consolidated Financial Statements) v xii

17 APM Method of Calculation Reconciliation with Financial Statements Tier 1 capital adequacy ratio Total capital adequacy ratio Leverage ratio Tier 1 capital resources divided by risk-weighted assets at a given date. Calculated in accordance with the requirements of the CBK and the capital adequacy regulations issued by the CBK as stipulated in CBK Circular number 2/RB, RBA/A336/2014 dated 24 June Total capital resources divided by risk-weighted assets at a given date. Calculated in accordance with the requirements of the CBK and the capital adequacy regulations issued by the CBK as stipulated in CBK Circular number 2/RB, RBA/A336/2014 dated 24 June "Capital" measure (being Tier 1 capital) divided by the "exposure" measure (being the sum of onbalance sheet assets, derivative exposures and off-balance sheet exposures). Calculated in accordance with the requirements of CBK Circular number 2/BS/342/2014 dated 21 October As set out in Note 32 (Capital Management) to the 2017 Consolidated Financial Statements and Note 32 (Capital Management) to the 2016 Consolidated Financial Statements. Calculated in accordance with the requirements of the CBK and the capital adequacy regulations issued by the CBK as stipulated in CBK Circular number 2/RB, RBA/A336/2014 dated 24 June As set out in Note 32 (Capital Management) to the 2017 Consolidated Financial Statements and Note 32 (Capital Management) to the 2016 Consolidated Financial Statements. Calculated in accordance with the requirements of the CBK and the capital adequacy regulations issued by the CBK as stipulated in CBK Circular number 2/RB, RBA/A336/2014 dated 24 June Tier 1 capital (as set out in Note 32 (Capital Management) to the 2017 Consolidated Financial Statements and Note 32 (Capital Management) to the 2016 Consolidated Financial Statements) divided by total exposure (as set out in Note 32 (Capital Management) to the 2017 Consolidated Financial Statements and Note 32 (Capital Management) to the 2016 Consolidated Financial Statements). Calculated in accordance with the requirements of CBK Circular number 2/BS/342/2014 dated 21 October Presentation of Statistical Information Certain statistical information included in this Base Prospectus (including in "Overview of Kuwait" and "Banking Industry and Regulation in Kuwait") has been derived from official public sources, including the CBK, the IMF, the Kuwait Public Authority for Civil Information, OPEC and the Statistics Bureau. All such statistical information may differ from that stated in other sources for a variety of reasons, including the fact that the underlying assumptions and methodology (including definitions and cut-off times) may vary from source to source. This data may subsequently be revised as new data becomes available and any such revised data will not be circulated by KFH to investors who have purchased any Certificates. The statistical information in this Base Prospectus, including in relation to GDP and revenues of Kuwait, have been obtained from public sources identified in this Base Prospectus. All statistical information provided in this Base Prospectus, and the component data on which it is based, may not have been compiled in the same manner as data provided, and may be different from statistics published, by other sources. Accordingly, the statistical data contained in this Base Prospectus should be treated with caution by prospective investors. Where information has not been independently sourced, it is KFH's own information. Presentation of Other Information Certain Definitions Capitalised terms which are used but not defined in any section of this Base Prospectus will have the meaning attributed thereto in the Conditions or any other section of this Base Prospectus. In addition, the following terms as used in this Base Prospectus have the meanings defined below: "Boursa Kuwait" means the Kuwait Stock Exchange; v xiii