Advanced Course Scenarios and Test Questions

|

|

|

- Scot Curtis

- 5 years ago

- Views:

Transcription

1 Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource materials to answer the questions after the scenarios. Advanced Scenario 1: Darcy and Chris Tabor Interview Notes Darcy is 45 years old, single, and a U.S. citizen with a valid Social Security number. She had $45,000 in wages. During the interview with Darcy, you determine the following facts: Darcy s son Chris, age 21, is unmarried and was a full-time student working on a degree in accounting during Chris income was $8,500 in wages, which he used to pay his tuition. He did not provide more than half his own support. Chris lived on campus during the school year, but came home on breaks and for the summer. Chris is in his third year of college. Chris has never had a felony drug conviction. Chris is a U.S. citizen with a valid Social Security number. Advanced Scenario 1: Test Questions 1. Who can claim Chris personal or dependency exemption? a. Chris can claim his personal exemption because he had earned income. b. Chris can claim his personal exemption if Darcy does not to claim him. c. Chris does not have a filing requirement so he cannot claim a personal exemption. d. Chris must file a tax return and claim zero personal exemptions because Darcy can claim him as a dependent on her tax return. 2. Darcy can claim the expenses Chris paid as qualifying expenses for the American opportunity credit if Darcy claims Chris as a dependent on her return. Advanced Scenarios 67

2 Advanced Scenario 2: Mike Hastings Interview Notes Mike is 50 and made $36,000 in wages in He is single and pays all the cost of keeping up his home. Mike s daughter, Brittany, lived with Mike all year. Brittany s son, Hayden, was born in November Hayden lived in Mike s home since birth. Brittany is 25, single, and had $1,500 in wages in She is not disabled. Mike provides more than half of the support for both Brittany and Hayden. Mike, Brittany, and Hayden are all U.S. citizens with valid Social Security numbers. Advanced Scenario 2: Test Questions 3. Who can claim Hayden as a dependent? a. No one can claim Hayden because he was not a member of the household for more than six months. b. Mike cannot claim Hayden because Hayden is not Mike s child. c. Brittany can claim Hayden because she is his parent. d. Mike can claim Hayden; Brittany cannot claim Hayden because Brittany qualifies as Mike s dependent. 4. Who can Mike claim as a qualifying child(ren) for the earned income credit? a. Mike has no qualifying children. b. Mike can claim Brittany, but not Hayden. c. Mike can claim Hayden, but not Brittany. d. Mike can claim both Brittany and Hayden. 5. Mike s most advantageous filing status is Single. 68 Advanced Scenarios

3 Advanced Scenario 3: Henry and Claudia Oberlin Interview Notes Henry and Claudia are married and want to file a joint return. They have one child, Alyssa, who is 5 years old and lived with them all year. Henry, Claudia, and Alyssa lived in the U.S. all year and all have Individual Taxpayer Identification Numbers (ITINs). Henry earned $37,000 in wages. Claudia had $5,000 in wage income. They had no other income. Henry and Claudia provided all the support for Alyssa. Advanced Scenario 3: Test Questions 6. Are Henry and Claudia eligible to claim the earned income credit? a. No, because Henry and Claudia s income is too high. b. No, because they all have ITINs. c. Yes, because Alyssa is their qualifying child for EIC. d. Yes, but only if they file a joint return. 7. Henry and Claudia can claim Alyssa for which tax benefit(s)? a. Dependency exemption and the child tax credit b. Dependency exemption only c. Child tax credit only d. Neither dependency exemption nor child tax credit Advanced Scenarios 69

4 Advanced Scenario 4: Martin Huron Interview Notes Martin is married, but did not live with or have contact with his spouse in He does not know where she is. He indicated on the intake sheet that he is not legally separated. Martin does not have children or any other dependents Martin worked as a clerk and earned $36,000 in wages. He had no other income. In 2017, he took a computer class at the local university to improve his job skills. Martin has a receipt showing he paid $1,200 for tuition. He paid for all his educational expenses and did not receive any assistance or reimbursement. He paid $400 for course books from an online bookseller. Martin paid $150 for a parking permit. It was not a requirement of enrollment. Martin does not have enough deductions to itemize. He is a U.S. citizen with a valid Social Security number. Advanced Scenario 4: Test Questions 8. What is Martin s most advantageous allowable filing status? a. Married Filing Separately b. Head of Household c. Single d. Qualifying Widower 9. Considering Martin s filing status and using Publication 4012, Tab J, Education Benefits, which education benefit is Martin eligible to claim? a. American opportunity credit b. He does not qualify for any education benefit c. Lifetime learning credit d. Tuition and fees deduction 70 Advanced Scenarios

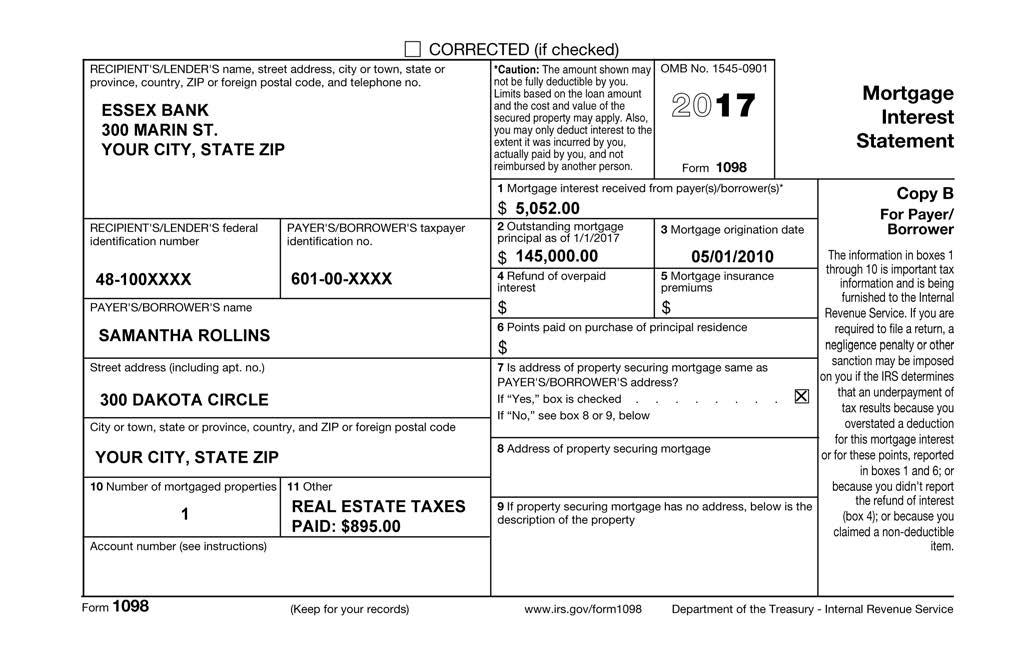

5 Advanced Scenario 5: Samantha Rollins Directions Interview Notes Using the tax software, complete the tax return, including Form 1040 and all appropriate forms, schedules, or worksheets. Answer the questions following the scenario. Note: When entering Social Security numbers (SSNs) or Employer Identification Numbers (EINs), replace the Xs as directed, or with any four digits of your choice. Samantha s husband died in March Samantha filed a joint return with her husband for She has not remarried. In September 2017, Samantha s daughter, Meredith, enrolled in college to pursue a bachelor s degree. She had no previous post-secondary education. Yuma College is a qualified educational institution. Meredith does not have a felony drug conviction. Samantha brought a Form 1098-T and an account statement from the college. Meredith s purchases at the college bookstore were for course-related books. The terms of Meredith s scholarship require that it be used to pay for tuition. Samantha took a distribution from her IRA and used all of the distribution to pay for some of Meredith s education expenses. All her IRA contributions were deductible in the year she made them. Samantha provided the entire cost of maintaining the household and all the support for her children, Meredith and Oliver, in Samantha s older brother, Howard, lives with her and is permanently and totally disabled. He received disability income which he used to provide more than half of his own support. Samantha lost her job in December She received unemployment for two weeks in 2017 until she found a new job. Samantha provides translation services to earn extra income. She received a Form 1099-MISC for all of the translation income. Her only expense related to this income was $150 in office supplies. Oliver attended day care while Samantha worked. Samantha received a Form 1099-C for cancelled credit card debt. Using the insolvency determination worksheet in Publication 4012, you helped Samantha determine the value of her assets exceeded her liabilities and that she was solvent at the time the credit card debt was cancelled. Samantha, Meredith, and Oliver had MEC all year through Samantha s employer. Howard also had MEC all year. Advanced Scenarios 71

6 72 Advanced Scenarios

7 Advanced Scenarios 73

8 74 Advanced Scenarios

9 Advanced Scenarios 75

10 76 Advanced Scenarios

11 Advanced Scenarios 77

12 78 Advanced Scenarios

13 Advanced Scenarios 79

14 80 Advanced Scenarios

15 Advanced Scenario 5: Test Questions 10. Which allowable filing status is most advantageous to Samantha? a. Qualifying Widow b. Single c. Married Filing Separately d. Head of Household 11. Howard is Samantha s qualifying person for which of the following benefits? a. Dependency exemption b. Child tax credit c. Earned income credit d. All of the above 12. What is the credit for child and dependent care expenses shown in the tax and credits section of Samantha s tax return? a. $840 b. $882 c. $630 d. $ What is the total amount of qualified educational expenses used in the calculation of Samantha s American opportunity credit? $. 14. What is the amount of self-employment tax in the Other Taxes section of Samantha s Form 1040, page 2? a. $0 b. $74 c. $148 d. $ Samantha s unemployment income does not need to be reported on her tax return. 16. Where is the cancelled debt from Form 1099-C reported on Samantha s tax return? a. It is not reported on the return b. On Form 1040, line 7 as wages c. On Form 1040, line 21 as other income d. On Schedule A as a miscellaneous deduction Advanced Scenarios 81

16 17. Samantha qualifies for an exception to the 10% additional tax on the early distribution from her IRA. 82 Advanced Scenarios

17 Advanced Scenario 6: Quincy and Marian Pike Directions Interview Notes Using the tax software, complete the tax return, including Form 1040 and all appropriate forms, schedules, or worksheets. Answer the questions following the scenario. Note: When entering Social Security numbers (SSNs) or Employer Identification Numbers (EINs), replace the Xs as directed, or with any four digits of your choice. Quincy retired and began receiving retirement income on April 1, No distributions were received prior to his retirement. Quincy selected a joint survivor annuity for these payments. Quincy brought last year s tax return. It includes a capital loss carryover worksheet. Quincy and Marian are married and want to file a joint return. They provided all the cost of keeping up the home and all of the support for their son Lucas. Lucas has no income and no filing requirement. Quincy was covered by Medicare all year. Marian and Lucas had MEC through Marian s employer all year. Advanced Scenarios 83

18 84 Advanced Scenarios

19 Advanced Scenarios 85

20 86 Advanced Scenarios

21 Advanced Scenarios 87

22 88 Advanced Scenarios

23 Advanced Scenarios 89

24 ABC INVESTMENTS 456 Pima Plaza Your City, YS ZIP 2017 TAX REPORTING STATEMENT Quincy and Marian Pike 388 Noble Circle Your City, YS ZIP Account No Recipient ID No XXXX Payer s Fed ID Number: XXXX Form 1099-DIV* 2017 Dividends and Distributions Copy B for Recipient (OMB NO ) 1a Total Ordinary Dividends b Qualified Dividends a Total Capital Gain Distributions (Includes 2b- 2d) b Capital Gains that represent Unrecaptured 1250 Gain c Capital Gains that represent Section 1202 Gain d Capital Gains that represent Collectibles (28%) Gain Nondividend Distributions Federal Income Tax Withheld Investment Expenses Foreign Tax Paid Foreign Country or U.S. Possession Cash Liquidation Distributions Non-Cash Liquidation Distributions Exempt Interest Dividends Specified Private Activity Bond Interest Dividends State State Identification No State Tax Withheld Form 1099-MISC* 2017 Miscellaneous Income Copy B for Recipient (OMB NO ) 2 Royalties Federal Income Tax Withheld Substitute Payments in Lieu of Dividends or Interest State Tax Withheld State/ Payer s State No State Income Form 1099-INT* 2017 Interest Income Copy B for Recipient (OMB NO ) 1 Interest Income Early Withdrawal Penalty Interest on U.S. Savings Bonds and Treas. Obligations Federal Income Tax Withheld Investment Expenses Foreign Tax Paid Foreign Country or U.S. Possession Tax-Exempt Interest Specified Private Activity Bond Interest Tax-Exempt Bond CUSIP No... Summary of 2017 Proceeds From Broker and Barter Exchange Transactions Sales Price of Stocks, Bonds, etc , Federal Income Tax Withheld Gross Proceeds from each of your security transactions are reported individually to the IRS. Refer to the Form 1099-B section of this statement. Report gross proceeds individually for each security on the appropriate IRS tax return. Do not report gross proceeds in aggregate. Page 1 of 2 90 Advanced Scenarios

25 ABC INVESTMENTS 456 Pima Plaza Your City, YS ZIP 2017 TAX REPORTING STATEMENT Quincy and Marian Pike 388 Noble Circle Your City, YS ZIP Account No Recipient ID No XXXX Payer s Fed ID Number: XXXX FORM 1099-B* 2017 Proceeds from Broker and Barter Exchange Transactions Copy B for Recipient OMB NO Short-term transactions for which basis is reported to the IRS Report on Form 8949 with Box A checked and/or Schedule D, Part I (This Label is a Substitute for Boxes 1c & 6) 8 Description, 1d Stock or Other Symbol, CUSIP (IRS Form 1099-B box numbers are shown below in bold type) Action 1a Date of 1b Date of 1e Quantity 2a Sales Price 3 Cost or Gain / Loss (-) 5 Wash Sale 4 Federal Income State Tax Sale or Acquisition Sold of Stocks, Other Basis (b) Loss Disallowed Tax Withheld State Withheld Exchange Bonds, etc. (a) Dakota Co. Common Stock Sale 03/01/ /01/ , , , TOTALS 3, , FORM 1099-B* 2017 Proceeds from Broker and Barter Exchange Transactions Copy B for Recipient OMB NO Long-term transactions for which basis is not reported to the IRS Report on Form 8949 with Box E checked and/or Schedule D, Part II (This Label is a Substitute for Boxes 1c & 6) 8 Description, 1d Stock or Other Symbol, CUSIP (IRS Form 1099-B box numbers are shown below in bold type) Action 1a Date of 1b Date of 1e Quantity 2a Sales Price 3 Cost or Gain / Loss (-) 5 Wash Sale 4 Federal Income State Tax Sale or Acquisition Sold of Stocks, Other Basis (b) Loss Disallowed Tax Withheld State Withheld Exchange Bonds, etc. (a) Iowa Co. Common Stock Sale 02/01/ /23/ , , TOTALS 3, , This is important tax information and is being furnished to the Internal Revenue Service. If you are required to file a return, a negligence penalty or other sanction may be imposed on you if this income is taxable and the IRS determines that it has not been reported. Page 2 of 2 Advanced Scenarios 91

26 92 Advanced Scenarios

27 Advanced Scenario 6: Test Questions 18. What is the total taxable interest income shown on Line 8a of Form 1040? a. $80 b. $110 c. $150 d. $ How does the code Q on Quincy s Form 1099-R from Essex Bank affect the return? a. The entire distribution is not taxable. b. Half of the distribution is taxable. c. The entire distribution is taxable. d. There is no such code. The taxpayer must get a corrected Form 1099-R from the bank. 20. What is the amount shown on Form 1040, Line 13 Capital gain or loss? a. $1,916 b. $2,451 c. $2,366 d. $2, How much of the $17,500 gross distribution reported on Form 1099-R is taxable in 2017? $. 22. Is Quincy s Social Security income taxable? a. Yes, a portion of the Social Security income is taxable. b. Yes, all of the Social Security income is taxable. c. No, because their total income is less than $32,000. d. No, Social Security benefits are never taxable. 23. Are the Pikes entitled to claim an earned income credit for 2017? a. No, because their investment income exceeds the amount allowed to claim. b. No, Quincy is over the age of 65. c. No, Lucas is not a qualifying child for purposes of the EIC. d. Yes, they are eligible for the credit. 24. What is the total income tax withholding on the tax return? $ Advanced Scenarios 93

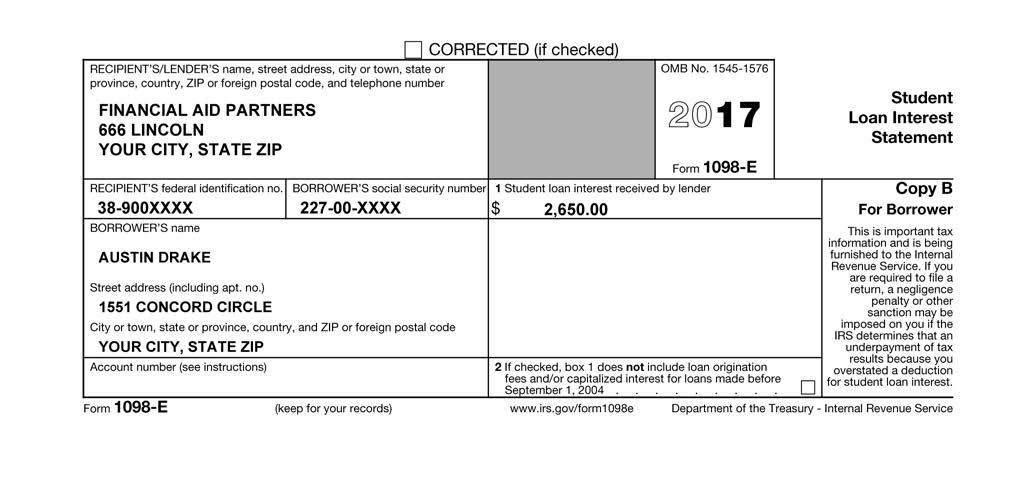

28 Advanced Scenario 7: Austin Drake Directions Interview Notes Using the tax software, complete the tax return, including Form 1040 and all appropriate forms, schedules, or worksheets. Answer the questions following the scenario. Note: When entering Social Security numbers (SSNs) or Employer Identification Numbers (EINs), replace the Xs as directed, or with any four digits of your choice. Austin works as a customer service employee during the day. He also has a business as a personal trainer and fitness instructor, called Austin s Abs. After work, he travels to teach classes at the gym five days a week. Austin is a cash-basis taxpayer who materially participates in the operation of his business. He did not make any payments that would require him to file Form Austin uses business code He received Form 1099-MISC for classes he taught at the gym. He had an additional $4,290 cash income in payments from individual clients not included on the Form 1099-MISC. He has a written mileage log showing the following miles for All his travel is within his local commuting area. 3,750 miles from home to his main job 2,850 miles from his main job to the gym where he taught classes and met individual clients 1,300 miles from the gym each day to his home The total mileage on his car for 2017 was 11,230 miles. He placed his car in service on January 6, He always takes the standard mileage rate. This is Austin s only car and it was available for personal use. Austin has records for other expenses relating to his business: Advertising: $300 Supplies: $1,000 Nutritional supplements for his own consumption: $675 Business liability insurance: $610 Business license: $150 Austin has a statement from his church stating he donated $650 on December 1, Austin also brought his Form 1098 showing the mortgage interest and real estate tax he paid. Austin has receipts for an eye exam for $80 and prescription contact lenses for $300. Austin donated $100 to a friend in need through a social networking site. 94 Advanced Scenarios

29 This year, Austin will deduct state income tax on Schedule A. Last year, he did not itemize. Austin s school loan was for qualified education expenses at an eligible institution. Austin has never taken a distribution from a retirement account and he was not a full-time student during Austin had health insurance all year through his employer. The insurance qualifies as MEC. Advanced Scenarios 95

30 96 Advanced Scenarios

31 Advanced Scenarios 97

32 98 Advanced Scenarios

33 Advanced Scenarios 99

34 100 Advanced Scenarios

35 Advanced Scenarios 101

36 Advanced Scenario 7: Test Questions 25. What income must Austin report for his business on Schedule C-EZ or C? a. Income reported on Form 1099-MISC for classes he taught at the gym. b. Cash income in payments from individual clients. c. None. He must report all income from his personal training business on Line 21, Other income. d. Both his income reported on the Form 1099-MISC and the cash income from his clients. 26. What is Austin s mileage expense deduction (at the standard mileage rate) for his business as a personal trainer? a. $1,525 b. $2,220 c. $3,531 d. $4, Which item(s) cannot be deducted by Austin as a business expense? (Select all that apply.) a. Business license b. Business liability insurance c. Advertising d. Nutritional supplements 28. How does Austin s self-employment tax affect his tax return? a. Austin s self-employment tax is not reported anywhere on Form b. A portion of the self-employment tax is deducted as a business expense on Schedule C-EZ or C. c. The self-employment tax is shown on Form 1040, Other Taxes section, and the full amount is deducted on Schedule A, Taxes You Paid section. d. The self-employment tax is shown on Form 1040, Other Taxes section, and the deductible part is an adjustment on Form 1040, page What is the amount Austin can take as a student loan interest deduction? $. 30. What are Austin s total itemized deductions on Schedule A, line 29? a. $6,856 b. $8,056 c. $8,156 d. $8, Advanced Scenarios

37 31. The amount of Austin s retirement savings contributions credit in the Tax and Credits section of Form 1040 is $ Austin is not able to pay the entire balance due by the due date of the return (without extensions). What are his options? a. He can submit a Form 9465, Installment Agreement Request. b. He can contact the IRS for a full pay 120-day agreement. c. He can pay using his credit card. d. Any of the above. Advanced Scenarios 103

38 Advanced Scenario 8: Robert Wharton Interview Notes Robert, age 33, lived and worked in the U.S. all year. He is single and has no dependents. Robert is not lawfully present in the U.S. and has an Individual Taxpayer Identification Number (ITIN). Robert had wages of $19,000. He had no other income. He did not have any health insurance for all of If he gets a refund, Robert would like to split it between two separate bank accounts. Advanced Scenario 8: Test Questions 33. What form must be used to split Robert s refund? a. Form 8888 b. Form 8880 c. Form 8862 d. There is no form. A refund can t be split. 34. Which health coverage exemption does Robert quality for? a. Short Coverage Gap b. Income below the filing threshold c. Not lawfully present in the U.S. and not a U.S. citizen d. None, Robert doesn t qualify for an exemption 35. Refer to Publication 4012, Tab H. Which of the following qualify as minimum essential coverage? a. Medicare Advantage plans b. COBRA coverage c. Employer-sponsored coverage under a group health plan d. All of the above e. A and C only 104 Advanced Scenarios Retest Questions

39 Advanced Course Retest Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource materials to answer the questions after the scenarios. Advanced Scenario 1: Darcy and Chris Tabor Interview Notes Darcy is 45 years old, single, and a U.S. citizen with a valid Social Security number. She had $45,000 in wages. During the interview with Darcy, you determine the following facts: Darcy s son Chris, age 21, is unmarried and was a full-time student working on a degree in accounting during Chris income was $8,500 in wages, which he used to pay his tuition. He did not provide more than half his own support. Chris lived on campus during the school year, but came home on breaks and for the summer. Chris is in his third year of college. Chris has never had a felony drug conviction. Chris is a U.S. citizen with a valid Social Security number. Advanced Scenario 1: Retest Questions 1. Chris can claim his own personal exemption if his mother decides not to claim him as a dependent. 2. If Darcy claims Chris as a dependent on her return, Darcy cannot claim the American opportunity credit because Chris paid his own tuition. Advanced Scenarios Retest Questions 105

40 Advanced Scenario 2: Mike Hastings Interview Notes Mike is 50 and made $36,000 in wages in He is single and pays all the cost of keeping up his home. Mike s daughter, Brittany, lived with Mike all year. Brittany s son, Hayden, was born in November Hayden lived in Mike s home since birth. Brittany is 25, single, and had $1,500 in wages in She is not disabled. Mike provides more than half of the support for both Brittany and Hayden. Mike, Brittany, and Hayden are all U.S. citizens with valid Social Security numbers. Advanced Scenario 2: Retest Questions 3. Can Brittany claim Hayden as a dependent? a. No, because Hayden didn t live with Brittany for more than 6 months. b. No, because Brittany qualifies as Mike s dependent. c. Yes, because Brittany had earned income. d. Yes, because Brittany is Hayden s mother. 4. How many qualifying children does Mike have for the earned income credit? a. 0 b. 1 c Mike s most advantageous filing status is Head of Household. 106 Advanced Scenarios Retest Questions

41 Advanced Scenario 3: Henry and Claudia Oberlin Interview Notes Henry and Claudia are married and want to file a joint return. They have one child, Alyssa, who is 5 years old and lived with them all year. Henry, Claudia, and Alyssa lived in the U.S. all year and all have Individual Taxpayer Identification Numbers (ITINs). Henry earned $37,000 in wages. Claudia had $5,000 in wage income. They had no other income. Henry and Claudia provided all the support for Alyssa. Advanced Scenario 3: Retest Questions 6. Henry and Claudia are eligible to claim the earned income credit. 7. Henry and Claudia can claim Alyssa as a dependent, but not for the child tax credit. Advanced Scenarios Retest Questions 107

42 Advanced Scenario 4: Martin Huron Interview Notes Martin is married, but did not live with or have contact with his spouse in He does not know where she is. He indicated on the intake sheet that he is not legally separated. Martin does not have children or any other dependents. Martin worked as a clerk and earned $36,000 in wages. He had no other income. In 2017, he took a computer class at the local university to improve his job skills. Martin has a receipt showing he paid $1,200 for tuition. He paid for all his educational expenses and did not receive any assistance or reimbursement. He paid $400 for course books from an online bookseller. Martin paid $150 for a parking permit. It was not a requirement of enrollment. Martin does not have enough deductions to itemize. He is a U.S. citizen with a valid Social Security number. Advanced Scenario 4: Retest Questions 8. Martin s most advantageous allowable filing status is Single. 9. Considering Martin s filing status and using Publication 4012, Tab J, Education Credits, Martin is eligible to claim the lifetime learning credit. 108 Advanced Scenarios Retest Questions

43 Advanced Scenario 5: Retest Questions Directions Read the information for Samantha Rollins beginning on page Head of Household is the most advantageous allowable filing status Samantha can use. 11. How many qualifying persons does Samantha have for the earned income credit? a. 0 b. 1 c. 2 d What is the credit for child and dependent care expenses in the tax and credits section of Samantha s Form 1040? $. 13. The total amount of qualified educational expenses used in the calculation of Samantha s 2017 American opportunity credit is: a. $3,300 b. $3,800 c. $4,000 d. $4, What is the amount of Samantha s self-employment tax in the Other Taxes section of Form 1040, page 2? $. 15. Where is Samantha s unemployment income reported? a. Form 1040, Line 19 b. Form 1040, Line 7 c. Unemployment income does not need to be reported d. Form 1040, Line Samantha s cancelled debt from Form 1099-C must be included on her federal income tax return, Line 21, as other income. Advanced Scenarios Retest Questions 109

44 17. Which exception can Samantha use to avoid the 10% additional tax on the early distribution from her IRA on Form 5329? a. She does not qualify for an exception b. Distribution made for higher education expenses c. Distribution made for purchase of a first home d. Distribution due to total and permanent disability 110 Advanced Scenarios Retest Questions

45 Advanced Scenario 6: Retest Questions Directions Refer to the scenario information for Quincy and Marian Pike, beginning on page The total amount of taxable interest income shown on Line 8a is $ Quincy s entire $4,500 Roth IRA distribution is taxable. 20. The net capital gain or loss reported on Form 1040, Line 13 is a gain of $2, How much of the $17,500 gross distribution reported on Form 1099-R from Hickory Corporation is taxable in 2017? a. $17,500 b. $17,137 c. $17,067 d. $16, A portion of Quincy s Social Security income is taxable. 23. The Pikes are entitled to an earned income credit for The total withholding on the tax return is $2,200. Advanced Scenarios Retest Questions 111

46 Advanced Scenario 7: Retest Questions Directions Refer to the scenario information for Austin Drake, beginning on page Austin must report the income on Form 1099-MISC and the cash income from his clients on Form 1040, Line 21, Other income. 26. What is Austin s mileage expense deduction (at the standard mileage rate) for his business as a personal trainer? $. 27. Austin cannot deduct the amount he pays for nutritional supplements. 28. The full amount of the self-employment tax is deducted on Schedule A, in the Taxes You Paid section. 29. Austin can take a student loan interest deduction of $2, What is Austin s total itemized deductions on Schedule A, line 29? $. 31. What is the amount of Austin s retirement savings contributions credit? $. 32. Austin wants to pay his balance due with his credit card. Can he do that? a. Yes b. No 112 Advanced Scenarios

47 Advanced Scenario 8: Robert Wharton Interview Notes Robert, age 33, lived and worked in the U.S. all year. He is single and has no dependents. Robert is not lawfully present in the U.S. and has an Individual Taxpayer Identification Number (ITIN). Robert had wages of $19,000. He had no other income. He did not have any health insurance for all of If he gets a refund, Robert would like to split it between two separate bank accounts. Advanced Scenario 8: Retest Questions 33. Robert must use Form 8888 to split his refund between his two bank accounts. 34. Robert does not qualify for a coverage exemption, and will need to make a shared responsibility payment (SRP) when filing his tax return. 35. Refer to Publication 4012, Tab H. Which of the following coverages do not qualify as minimum essential coverage? a. Medicare Advantage plans b. COBRA coverage c. Dental insurance d. Employer-sponsored coverage under a group health plan Advanced Scenarios 113

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Scenario 5: Samantha Rollins

Advanced Scenario 5: Samantha Rollins Directions Interview Notes Using the tax software, complete the tax return, including Form 1040 and all appropriate forms, schedules, or worksheets. Answer the questions

Advanced Scenario 5: Samantha Rollins Directions Interview Notes Using the tax software, complete the tax return, including Form 1040 and all appropriate forms, schedules, or worksheets. Answer the questions

Advanced Course Scenarios and Test Questions

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Advanced Course Scenarios and Test Questions Directions The first four scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and

Basic Course Scenarios and Test Questions

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

2017 Advanced Certification Study and Reference Guide

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

2017 Advanced Certification Study and Reference Guide Note: Where used in the following, QRG means Quick Reference Guide ( mini manual ); Manual means the Ladder Up Volunteer Training Manual; in both cases

2017 Form 6744 VITA/TCE Volunteer Assistor s Test/Retest

2017 Form 6744 VITA/TCE Volunteer Assistor s Test/Retest 91 No change Form 6744 92 This page was unintentionally left blank in the printed version. Please replace with Schedule D Worksheet for Capital

2017 Form 6744 VITA/TCE Volunteer Assistor s Test/Retest 91 No change Form 6744 92 This page was unintentionally left blank in the printed version. Please replace with Schedule D Worksheet for Capital

Basic Course Scenarios and Test Questions

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E I R S A D V A N C E D C E R T I F I C A T I O N E X A M

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 7 I R S A D V A N C E D C E R T I F I C A T I O N E X A M OUT OF S COPE FOR S AV EFIRST INTERMEDIATE VOLUNTEERS AT TAX PR EPAR

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 7 I R S A D V A N C E D C E R T I F I C A T I O N E X A M OUT OF S COPE FOR S AV EFIRST INTERMEDIATE VOLUNTEERS AT TAX PR EPAR

Helpful Tips. for Out of Scope Topics. on the 2014 IRS Advanced Certification Exam

Helpful Tips for Out of Scope Topics on the 2014 IRS Advanced Certification Exam HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON 2014 IRS ADVANCED CERTIFICATION EXAM (Out Of Scope For SaveFirst Intermediate Volunteer

Helpful Tips for Out of Scope Topics on the 2014 IRS Advanced Certification Exam HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON 2014 IRS ADVANCED CERTIFICATION EXAM (Out Of Scope For SaveFirst Intermediate Volunteer

Basic Course Scenarios and Test Questions

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

Basic Course Scenarios and Test Questions Directions The first six scenarios do not require you to prepare a tax return. Read the interview notes for each scenario carefully and use your training and resource

TY2018 VITA Advanced Certification Test - Study Guide

Scenario 1: Smith TY2018 VITA Advanced Certification Test - Study Guide Issue #1 Qualified Education Expenses, Taxable Scholarships (p4012 Tab J) When a taxpayer has more scholarships than Qualified Educational

Scenario 1: Smith TY2018 VITA Advanced Certification Test - Study Guide Issue #1 Qualified Education Expenses, Taxable Scholarships (p4012 Tab J) When a taxpayer has more scholarships than Qualified Educational

HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON THE 2016 IRS BASIC CERTIFICATION EXAM

HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON THE 2016 IRS BASIC CERTIFICATION EXAM + H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 6 I R S B A S I C C E R T I F I C A T I O N E

HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON THE 2016 IRS BASIC CERTIFICATION EXAM + H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 6 I R S B A S I C C E R T I F I C A T I O N E

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

Department of the Treasury - Internal Revenue Service Intake/Interview & Quality Review Sheet

Form 13614-C (October 2017) You will need: Tax Information such as Forms W-2, 1099, 1098, 1095. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's

Form 13614-C (October 2017) You will need: Tax Information such as Forms W-2, 1099, 1098, 1095. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Personal Information

Form ID: 1040 Personal Information 1 Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er)) Mark if you were married

Form ID: 1040 Personal Information 1 Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er)) Mark if you were married

Federal Income Taxes. Today s Approach. Your Tax Knowledge. Process. Process Continued. Filing Requirements. Fall 2014 VITA Training

Federal Income Taxes Fall 2014 VITA Training Dr. Cathy Bowen Dr. Barbara Yener Today s Approach Use Form 1040 and common tax forms to discuss key areas of completing a tax return for VITA taxpayers. Not

Federal Income Taxes Fall 2014 VITA Training Dr. Cathy Bowen Dr. Barbara Yener Today s Approach Use Form 1040 and common tax forms to discuss key areas of completing a tax return for VITA taxpayers. Not

TY2018 VITA Basic Certification Test - Study Guide

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Arnold TY2018 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Department of the Treasury - Internal Revenue Service Intake/Interview & Quality Review Sheet

Form 13614-C (October 2017) You will need: Tax Information such as Forms W-2, 1099, 1098, 1095. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's

Form 13614-C (October 2017) You will need: Tax Information such as Forms W-2, 1099, 1098, 1095. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's

TY2017 VITA Basic Certification Test - Study Guide

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Scenario 1: Albright TY2017 VITA Basic Certification Test - Study Guide Issue #1 Minimum Essential Coverage (MEC) (p4012 Tab H) See p4012 s ACA tab for a list of what counts as MEC Issue #2 Penalties for

Determining your 2016 stock plan tax requirements a step-by-step guide

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

Determining your 2016 stock plan tax requirements a step-by-step guide INSIDE How to use the Supplemental Form to avoid overpaying taxes Upon selling shares acquired from a nonqualified employee stock

3. Mailing address Apt # City State ZIP code 516 FREMONT ROAD YOUR CITY YS YOUR ZIP CD

Form 13614-C (October 2014) You will need: Tax Information such as Forms W-2, 1099, 1098. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's license)

Form 13614-C (October 2014) You will need: Tax Information such as Forms W-2, 1099, 1098. Social security cards or ITIN letters for all persons on your tax return. Picture ID (such as valid driver's license)

Practice Scenario 12. Client Information

Practice Scenario 12 Use the taxpayer information provided in the following section to prepare a tax return. After you complete the return, review the Lessons Learned section to see how you did. Client

Practice Scenario 12 Use the taxpayer information provided in the following section to prepare a tax return. After you complete the return, review the Lessons Learned section to see how you did. Client

This is a list of items you should gather for the Income Tax Preparation

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

This is a list of items you should gather for the Income Tax Preparation 1. Social Security Card(s) - Your Social Security number, which is your taxpayer identification number, is printed on your Social

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Campus Fellow Summary Chart

Campus Fellow Summary Chart Line Description Taxpayer s Forms Directions Instructions and Special Notes 1-5 Filing Status Social Security Cards (or SSA-1099, SS letter, ITIN) Choose filing status in interview

Campus Fellow Summary Chart Line Description Taxpayer s Forms Directions Instructions and Special Notes 1-5 Filing Status Social Security Cards (or SSA-1099, SS letter, ITIN) Choose filing status in interview

Personal Information. Present Mailing Address. Dependent Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Determining your 2017 stock plan tax requirements a step-by-step guide

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Determining your 2017 stock plan tax requirements a step-by-step guide Alert: The tax-reform legislation adopted in December 2017 does not affect the 2017 tax year or the federal tax return for 2017 that

Bob Smith Betty Smith Home address (number and street). If you have a P.O.box, see instructions. J Important!

. If you have a P.O.box, see instructions. J Important!") Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

Presidential Lakeview WA 99999 Election Campaign Note: Checking Yes will not change your tax or reduce your refund. You Spouse (See instructions.) A Do you, or your spouse if filing a joint return, want

VITA/TCE Training. Preparing a Return in Practice Lab

The National Tax Training Committee has modified this manual to more accurately reflect Tax-Aide policies and scope and to clarify instructions that relate to Practice Lab versus the desktop version of

The National Tax Training Committee has modified this manual to more accurately reflect Tax-Aide policies and scope and to clarify instructions that relate to Practice Lab versus the desktop version of

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

ADVANCED CERTIFICATION STUDY GUIDE Tax Year 2018 Table of Contents ADVANCED SCENARIO 1: Aiden Smith... 1 ADVANCED SCENARIO 2: Sean Yale... 2 ADVANCED SCENARIO 3: Tom and Carol Baker... 3 ADVANCED SCENARIO

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Form 1040-V. Department of the Treasury. Internal Revenue Service $ 3, Dave Dave Sarah Sarah Terrace Glenview, IL 60001

2006 Form 040-V Department of the Treasury Internal Revenue Service For Privacy Act and Paperwork Reduction Act tice, see separate instructions. DETACH HERE Form 040 (2006) Department of the Treasury Internal

2006 Form 040-V Department of the Treasury Internal Revenue Service For Privacy Act and Paperwork Reduction Act tice, see separate instructions. DETACH HERE Form 040 (2006) Department of the Treasury Internal

Standard Deductions. MACRS Recovery Periods. Tax Preparers Due Diligence Requirements for EITC Medical Savings Accounts (MSA)

") Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

Tax Preparers Due Diligence Requirements for EITC Paid preparers who file EITC returns or claims for refunds for clients must meet four due diligence requirements. Those who fail to do so can be assessed

Tax Determination, Payments, and Reporting Procedures

CCH Essentials of Federal Income Taxation Tax Determination, Payments, and Reporting Procedures 2002, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Taxpayer Filing

CCH Essentials of Federal Income Taxation Tax Determination, Payments, and Reporting Procedures 2002, CCH INCORPORATED 4025 West Peterson Ave. Chicago, IL 60646-6085 http://tax.cchgroup.com Taxpayer Filing

Individual Income Tax Organizer 2016

MICHAEL R. ANLIKER, CPA, P.C. 5348 Twin Hickory Rd. Glen Allen, VA 23059 TELEPHONE: (804) 237-6044 FAX: (804) 237-6064 www.anlikerfinancial.com Individual Income Tax Organizer 2016 This Tax Organizer is

MICHAEL R. ANLIKER, CPA, P.C. 5348 Twin Hickory Rd. Glen Allen, VA 23059 TELEPHONE: (804) 237-6044 FAX: (804) 237-6064 www.anlikerfinancial.com Individual Income Tax Organizer 2016 This Tax Organizer is

Tax Return Questionnaire Tax Year

Print this form out & use it to organize your documents prior to coming to our office. It will help you remember all of the things you should bring to the meeting. Tax Return Questionnaire - 2018 Tax Year

Print this form out & use it to organize your documents prior to coming to our office. It will help you remember all of the things you should bring to the meeting. Tax Return Questionnaire - 2018 Tax Year

2017 Tax Return Questionnaire

2017 Tax Return Questionnaire Directions: Print and complete this form prior to your consultation. Bring it with you when you come to the office or contact us for email or fax instructions. Preparing this

2017 Tax Return Questionnaire Directions: Print and complete this form prior to your consultation. Bring it with you when you come to the office or contact us for email or fax instructions. Preparing this

Tax Preparation Checklist - Form 1040

Tax Preparation Checklist - Form 1040 Note: This organizer will help us to better serve you as a client by providing the information we will need in order to prepare your return. I. Personal Information

Tax Preparation Checklist - Form 1040 Note: This organizer will help us to better serve you as a client by providing the information we will need in order to prepare your return. I. Personal Information

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

BYRT CPAs, LLC Tax Organizer

BYRT CPAs, LLC 2017 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

BYRT CPAs, LLC 2017 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

Please provide us with the following information: If you need more space use pg. 4 or add a page. Date of Birth: SSN: Date of Birth:

1 Please provide us with the following information: If you need more space use pg. 4 or add a page. Personal Information Name: Spouse name: SSN: Date of Birth: SSN: Date of Birth: Address: City:, State:

1 Please provide us with the following information: If you need more space use pg. 4 or add a page. Personal Information Name: Spouse name: SSN: Date of Birth: SSN: Date of Birth: Address: City:, State:

WAHL, WILLEMSE & WILSON, LLP CERTIFIED PUBLIC ACCOUNTANTS 2018 TAX ORGANIZER

FILING STATUS FILING STATUS (See table) Filing Status MARRIED FILING SEPARATE AND LIVED WITH SPOUSE? 1 = Single SPOUSE'S DATE OF DEATH (mm/dd/yy), IF QUALIFYING WIDOW(ER) - 2017 or 2018 2 = Married filing

FILING STATUS FILING STATUS (See table) Filing Status MARRIED FILING SEPARATE AND LIVED WITH SPOUSE? 1 = Single SPOUSE'S DATE OF DEATH (mm/dd/yy), IF QUALIFYING WIDOW(ER) - 2017 or 2018 2 = Married filing

2017 Income Tax Data-Itemizer

Documents Used to Verify Primary Taxpayer Identity: (select one) Driver's License (complete detail below) State issued identification card (complete detail below) Passport IDENTITY VERIFICATION WORKSHEET

Documents Used to Verify Primary Taxpayer Identity: (select one) Driver's License (complete detail below) State issued identification card (complete detail below) Passport IDENTITY VERIFICATION WORKSHEET

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2017 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Taxpayer Name SS# Occupation Birth Date Spouse

TAX ORGANIZER Page 3

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

TAX ORGANIZER Page Basic Taxpayer Information Taxpayer Spouse Taxpayer Spouse First Name Initial Last Name Social Security No. Check if Date of Occupation Dependent Presidential Birth Disabled Blind of

Social Security Card(s) or Numbers for all family members listed on return.

or Numbers for all family members listed on return.") Social Security Card(s) or Numbers for all family members listed on return. If you have your Social Security card, bring it with you to the appointment. If you have changed your name (due to marriage,

Social Security Card(s) or Numbers for all family members listed on return. If you have your Social Security card, bring it with you to the appointment. If you have changed your name (due to marriage,

Tax Organizer For 2014 Income Tax Return

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

Prepared By: Tax Organizer For 2014 Income Tax Return Prepared For: This Tax Organizer can be used to help identify information needed to prepare your 2014 income tax return. Enter your 2014 tax information

2015 Client Organizer

Prepared By: Davis & Associates, CPA 425 Creekstone Rdg Woodstock, GA 30188-3746 Prepared For: 2015 Client Organizer From: To: Davis & Associates, CPA 425 Creekstone Rdg Woodstock, GA 30188-3746 2015 Client

Prepared By: Davis & Associates, CPA 425 Creekstone Rdg Woodstock, GA 30188-3746 Prepared For: 2015 Client Organizer From: To: Davis & Associates, CPA 425 Creekstone Rdg Woodstock, GA 30188-3746 2015 Client

Income. Taxwise Online. IRS Training Workbook

Income Taxwise Online IRS Training Workbook I N C O ME IRS Training Workbook 2012 CCH Small Firm Services. All rights reserved. 225 Chastain Meadows Court NW Suite 200 Kennesaw, Georgia 30144 Information

Income Taxwise Online IRS Training Workbook I N C O ME IRS Training Workbook 2012 CCH Small Firm Services. All rights reserved. 225 Chastain Meadows Court NW Suite 200 Kennesaw, Georgia 30144 Information

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

Personal Legal Plans Client Organizer 2018

TAXPAYER NAME SOCIAL SECURITY NUMBER OCCUPATION DATE OF BIRTH EMAIL ADDRESS CELL PHONE SPOUSE Address: Home Phone: City: State: Zip: County: DEPENDENT CHILDREN & OTHER DEPENDENTS NAME SOCIAL SECURITY NUMBER

TAXPAYER NAME SOCIAL SECURITY NUMBER OCCUPATION DATE OF BIRTH EMAIL ADDRESS CELL PHONE SPOUSE Address: Home Phone: City: State: Zip: County: DEPENDENT CHILDREN & OTHER DEPENDENTS NAME SOCIAL SECURITY NUMBER

Basic Certification Test: Study Guide for Tax Year 2017

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Basic Certification Test: Study Guide for Tax Year 2017 TRAINING PRACTICE PROBLEMS 2018 i The items in parentheses refer to sections or page numbers in Publication 4012, Volunteer Resource Guide. It s

Personal Information 3

Personal Information 3 Taxpayer: First Name and Initial Last Name Social Security Number Occupation Date of Birth (Mo/Da/Yr) Date of Death (Mo/Da/Yr) Spouse: First Name and Initial Last Name Social Security

Personal Information 3 Taxpayer: First Name and Initial Last Name Social Security Number Occupation Date of Birth (Mo/Da/Yr) Date of Death (Mo/Da/Yr) Spouse: First Name and Initial Last Name Social Security

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

217 Medical Savings Accounts (MSA) 217 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,5-6,75 Maximum Out of Pocket Self-Only Coverage 4,5 Family Coverage 8,25 STANDARD DEDUCTIONS

1040 US Tax Organizer

40 US Tax Organizer Page 1 CLIENT INFORMATION First name and initial..... Last name............... Title/suffix............... Social security number... Occupation.............. Date of birth (m/d/y)......

40 US Tax Organizer Page 1 CLIENT INFORMATION First name and initial..... Last name............... Title/suffix............... Social security number... Occupation.............. Date of birth (m/d/y)......

2017 Basic Certification Study and Reference Guide

2017 Basic Certification Study and Reference Guide 1 P age Basic Scenario 1: Calvin and Betty Albright 1. Qualifying health insurance coverage also known as minimum essential coverage or MEC under the

2017 Basic Certification Study and Reference Guide 1 P age Basic Scenario 1: Calvin and Betty Albright 1. Qualifying health insurance coverage also known as minimum essential coverage or MEC under the

Income Tax Guide and Client Organizer

Income Tax Guide and Client Organizer Income Tax Guide and Client Organizer Tax Year For My income tax appointment is: date day of week time PROVIDED BY: This booklet is provided to assist you in assembling

Income Tax Guide and Client Organizer Income Tax Guide and Client Organizer Tax Year For My income tax appointment is: date day of week time PROVIDED BY: This booklet is provided to assist you in assembling

, ending. child tax credit (1) First name Last name

First name Last name") Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return 2016 OMB No. 1545-0074 For the year Jan. 1-Dec. 31, 2016, or other tax year beginning, ending Form Your first

BYRT CPAs, LLC Tax Organizer

BYRT CPAs, LLC 2016 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

BYRT CPAs, LLC 2016 Tax Organizer General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household,

Atwood Tax Client Organizer Taxpayer Information

Atwood Tax Client Organizer Taxpayer Information First Name: ( ) Initial: ( ) Last Name: ( ) Date of Birth: ( / / ) SSN: ( - - ) Occupation: ( ) Address: ( ) State: ( ) Zip: ( ) City: ( ) Daytime phone:

Atwood Tax Client Organizer Taxpayer Information First Name: ( ) Initial: ( ) Last Name: ( ) Date of Birth: ( / / ) SSN: ( - - ) Occupation: ( ) Address: ( ) State: ( ) Zip: ( ) City: ( ) Daytime phone:

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

TAX ORGANIZER. If you answer 'Yes' to any of the General Business and Investment questions, please provide detailed information with your answer.

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2011. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

TAX ORGANIZER Enclosed is your Tax Organizer for tax year 2011. Your Organizer contains several sections that include common expenses and deductions that many taxpayers overlook. Please review these sections

JOYNER, KIRKHAM, KEEL & ROBERTSON, P.C INDIVIDUAL TAX ORGANIZER

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Please provide a copy of your 2013 federal and state tax returns, and complete pages 1 through 3. Other pages: complete only those sections that apply to you. Your Name SS# Occupation Birth Date Spouse

Who wants to tell us. Why do Tax Credits matter?

Who wants to tell us Why do Tax Credits matter? Non-Refundable Credits Non-Refundable Credits Other Dependent Credit Lifetime Learning (Education) Credit Credit for Child and Dependent Care Retirement

Who wants to tell us Why do Tax Credits matter? Non-Refundable Credits Non-Refundable Credits Other Dependent Credit Lifetime Learning (Education) Credit Credit for Child and Dependent Care Retirement

DONALD A. DEVLIN & ASSOCIATES, PC

DONALD A. DEVLIN & ASSOCIATES, PC 807 Bay Avenue Somers Point, NJ 08244 (P) 609-926-6400 (F) 609-926-6426 IDENTITY AUTHENTICATION Driver s License or State Issued Identification Government agencies are

DONALD A. DEVLIN & ASSOCIATES, PC 807 Bay Avenue Somers Point, NJ 08244 (P) 609-926-6400 (F) 609-926-6426 IDENTITY AUTHENTICATION Driver s License or State Issued Identification Government agencies are

Personal Information

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

General: 1040 Personal Information GENERAL INFORMATION Filing (Marital) status code (1 = Single, 2 = Married filing joint, 3 = Married filing separate, 4 = Head of household, 5 = Qualifying widow(er))

1040 Department of the Treasury Internal Revenue Service (99)

") 1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 2016, or

1040 Department of the Treasury Internal Revenue Service (99) U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 2016, or

Volunteer Income Tax Assistance (VITA) Advance Scenarios 1-4.

Advance Scenarios 1-4.") Volunteer Income Tax Assistance (VITA) Advance Scenarios 1-4 www.cwfphilly.org The Campaign for Working Families, Inc. (CWFI) is a non-profit organization committed to helping working families and individuals

Volunteer Income Tax Assistance (VITA) Advance Scenarios 1-4 www.cwfphilly.org The Campaign for Working Families, Inc. (CWFI) is a non-profit organization committed to helping working families and individuals

TAX PRIMER FOR PARENTS COMPLETING A PFS

TAX PRIMER FOR PARENTS Use this primer to get an understanding of which few tax forms will be most helpful to you as you complete your PFS. This primer doesn t provide an overview of every possible tax

TAX PRIMER FOR PARENTS Use this primer to get an understanding of which few tax forms will be most helpful to you as you complete your PFS. This primer doesn t provide an overview of every possible tax

Military Scenario Tax Year 2016 Interview Notes

Military Training Tax Year 2016 Military Scenario Tax Year 2016 Interview Notes Michael and Jessica Williams are married and want to file a joint return. They do not have any dependents. Michael is active

Military Training Tax Year 2016 Military Scenario Tax Year 2016 Interview Notes Michael and Jessica Williams are married and want to file a joint return. They do not have any dependents. Michael is active

Kyle and Kory Kent Advanced Training Exercise

Kyle and Kory Kent Advanced Training Exercise Kyle and Kory Kent were married, full time residents of [your state].unfortunately, Kory passed away on December 12 of the tax year. Kyle isn t sure how he

Kyle and Kory Kent Advanced Training Exercise Kyle and Kory Kent were married, full time residents of [your state].unfortunately, Kory passed away on December 12 of the tax year. Kyle isn t sure how he

1040 U.S. Individual Income Tax Return 2017

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 17 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 17,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 17 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 17,

TAX ORGANIZER. P.O. Box 130, Newburyport, MA Office: Fax: Website:

TAX ORGANIZER P.O. Box 130, Newburyport, MA 01950 Office: 978-499-1888 Fax: 978-499-4988 Email: craig@skytax.net Website: www.skytax.net FEE STRUCTURE Pricing includes: Federal Form 1040, Schedules A &

TAX ORGANIZER P.O. Box 130, Newburyport, MA 01950 Office: 978-499-1888 Fax: 978-499-4988 Email: craig@skytax.net Website: www.skytax.net FEE STRUCTURE Pricing includes: Federal Form 1040, Schedules A &

Income Tax Organizer Instructions

Income Tax Organizer Instructions Our Tax Organizer is designed to help you gather the proper tax information required to prepare your tax return. Please fill out completely all areas that pertain to you.

Income Tax Organizer Instructions Our Tax Organizer is designed to help you gather the proper tax information required to prepare your tax return. Please fill out completely all areas that pertain to you.

STANDARD DEDUCTIONS MACRS RECOVERY PERIODS

216 Medical Savings Accounts (MSA) 216 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,45-6,7 Maximum Out of Pocket Self-Only Coverage 4,45 Family Coverage 8,15 STANDARD DEDUCTIONS

216 Medical Savings Accounts (MSA) 216 Annual Deductible Range Self-Only Coverage 2,25-3,35 Family Coverage 4,45-6,7 Maximum Out of Pocket Self-Only Coverage 4,45 Family Coverage 8,15 STANDARD DEDUCTIONS

TAX PRIMER FOR PARENTS COMPLETING A PFS

FOR PARENTS Use this primer to get an understanding of which few tax forms will be most helpful to you as you complete your PFS. This primer doesn t provide an overview of every possible tax form you might

FOR PARENTS Use this primer to get an understanding of which few tax forms will be most helpful to you as you complete your PFS. This primer doesn t provide an overview of every possible tax form you might

PERSONAL INFORMATION ORGANIZER Please complete this Organizer before your appointment.

1. PERSONAL INFORMATION PERSONAL INFORMATION ORGANIZER Name SSN or ITIN Date of Birth Date of Death Occupation Blind Disabled Taxpayer Spouse Street Address Apt. City or town State Zip Code County Foreign

1. PERSONAL INFORMATION PERSONAL INFORMATION ORGANIZER Name SSN or ITIN Date of Birth Date of Death Occupation Blind Disabled Taxpayer Spouse Street Address Apt. City or town State Zip Code County Foreign

FOR THE TAX YEAR 20 COMPLIMENTARY TAX ORGANIZER FOR PERSONAL PREPARE TODAY TO SAVE TOMORROW www.nevadalegalforms.com PLEASE PROVIDE A COPY OF YOUR PRIOR YEARS FEDERAL AND STATE RETURN IF WE DID NOT PREPARE

FOR THE TAX YEAR 20 COMPLIMENTARY TAX ORGANIZER FOR PERSONAL PREPARE TODAY TO SAVE TOMORROW www.nevadalegalforms.com PLEASE PROVIDE A COPY OF YOUR PRIOR YEARS FEDERAL AND STATE RETURN IF WE DID NOT PREPARE

1040 U.S. Individual Income Tax Return 2017

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 217 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

F or Department of the Treasury Internal Revenue Service (99) 14 U.S. Individual Income Tax Return 217 m OMB No. 1545-74 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31,

You are responsible for the information on your return. Please provide complete and

Military Comprehensive Problem Problem C Brooks Intake and Interview Sheet, page 1 of 2 Form 13614-C (October 2013) You will need: Tax Information such as Forms W-2, 1099, 1098. Social security cards or

Military Comprehensive Problem Problem C Brooks Intake and Interview Sheet, page 1 of 2 Form 13614-C (October 2013) You will need: Tax Information such as Forms W-2, 1099, 1098. Social security cards or

Tax Organizer. Please Complete And Bring This Organizer To Your Tax Appointment. Tax Year

Affix Address Label Tax Organizer Tax Year Please Complete And Bring This Organizer To Your Tax Appointment We are pleased to have you joining us this tax season. Thank you for completing your tax organizer,

Affix Address Label Tax Organizer Tax Year Please Complete And Bring This Organizer To Your Tax Appointment We are pleased to have you joining us this tax season. Thank you for completing your tax organizer,

1040 US Miscellaneous Questions

1040 US Miscellaneous Questions Page 8 If any of the following items pertain to you or your spouse for, please check the appropriate box and provide additional information if necessary. YES NO Did your

1040 US Miscellaneous Questions Page 8 If any of the following items pertain to you or your spouse for, please check the appropriate box and provide additional information if necessary. YES NO Did your

LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 20 SOCIAL SECURITY BENEFITS

LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 20 SOCIAL SECURITY BENEFITS") LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 15 IRA DISTRIBUTIONS LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 19 UNEMPLOYMENT LINE 20 SOCIAL SECURITY BENEFITS LINE 21

LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 15 IRA DISTRIBUTIONS LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 19 UNEMPLOYMENT LINE 20 SOCIAL SECURITY BENEFITS LINE 21

SALLY W EMANUEL If a joint return, spouse's first name M.I. Last name Suffix Spouse's social security number

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 2011, or

Department of the Treasury Internal Revenue Service (99) 1040 U.S. Individual Income Tax Return OMB No. 1545-0074 IRS Use Only Do not write or staple in this space. For the year Jan. 1 Dec. 31, 2011, or

Taxpayer Questionnaire

First : Last : Taxpayer Questionnaire PERSONAL INFORMATION Primary Taxpayer M.I.: S.S.N. : Birthdate: Taxpayer's PIN: Home Phone: Work Phone: Cell Phone: Occupation: Email Address: Dependent on another

First : Last : Taxpayer Questionnaire PERSONAL INFORMATION Primary Taxpayer M.I.: S.S.N. : Birthdate: Taxpayer's PIN: Home Phone: Work Phone: Cell Phone: Occupation: Email Address: Dependent on another

1040 US Client Information 1

Page 1 1040 US Client Information 1 Coleman Tax & Bookkeeping P.O. Box 843 Weaverville, CA 96093 Telephone number: Fax number: E-mail address: (530) 623-4787 (530) 623-4560 ccoleman@velotech.net Tax Return

Page 1 1040 US Client Information 1 Coleman Tax & Bookkeeping P.O. Box 843 Weaverville, CA 96093 Telephone number: Fax number: E-mail address: (530) 623-4787 (530) 623-4560 ccoleman@velotech.net Tax Return

2016 TAX ORGANIZER. This tax organizer has been prepared for your use in gathering the information needed for your 2016 tax return.

F R O M 2016 TAX ORGANIZER T O This tax organizer has been prepared for your use in gathering the information needed for your 2016 tax return. To save you time, selected information from your 2015 tax

F R O M 2016 TAX ORGANIZER T O This tax organizer has been prepared for your use in gathering the information needed for your 2016 tax return. To save you time, selected information from your 2015 tax