Capital Gain or Loss

|

|

|

- Claud Hopkins

- 5 years ago

- Views:

Transcription

1 Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages Pub 4491 Part 3 Lesson 11 The Interview Question 9 in Income section Question 3 in Life Events section 2 1

Government is a profits-only partner!")

2 In Scope Capital Assets Stocks Mutual fund shares Exhange traded funds (ETF) shares Bonds (limited) Personal Residences 3 Sort-of Capital Assets Homes and other non-investment assets Capital assets for gains Personal assets for losses (not deductible) Government is a profits-only partner! 4 2

3 Interview Scope Out of Scope Business Assets Brokerage Sales paid with virtual currencies (e.g. bitcoins) All other asset sales are out of scope 5 When is a Transaction Reported When asset is sold When asset is otherwise disposed, such as When bond is redeemed When it is totally worthless 6 3

4 When Transaction Is Not Reported Not reported if not a sale or exchange A gift is not sale or exchange Donation to charity is not sale or exchange Bequest to heir is not sale or exchange 7 Forms From Client 1099-B Consolidated brokerage statement Non-IRS forms 1099-S 8 4

5 Interview Brokerage or Mutual Fund Statement Review forms with taxpayer Confirm that cost is reported on forms Does taxpayer agree with reported cost? If not, does taxpayer have cost? Only stocks, mutual funds or some bonds 9 Introduction Sale Of Assets Key elements of a sale: When did you buy it What did you pay for it, i.e., cost basis When did you sell it What is the sales price 10 5

6 What is the Basis* of Shares Cost amount originally paid Adjustments to basis* (of shares) Purchase expenses (commissions) Sale expenses, if not already used to reduce proceeds Non-dividend distributions Broker s requirement to report basis * Basis is term generically used for cost or adjusted basis 11 What is the Basis What if basis is unknown Taxpayer could establish basis if know when it was acquired Watch out for dividend reinvestment, intervening splits, mergers, etc. IRS rule: report zero as basis if taxpayer doesn t have any information 12 6

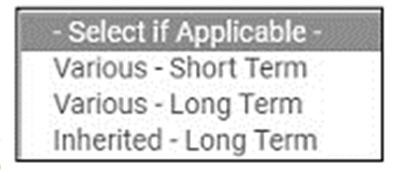

7 What is the Basis Inherited Inherited Property From decedent who died before or after 2010 Fair Market Value (FMV) On date of death -OR- On alternate valuation date, if elected by estate Taxpayer needs to provide basis or be referred to paid preparer Always long term Use Inherited Long Term in TaxSlayer, Date Acquired dropdown selection 13 What is the Basis Inherited Community property states (usually) Basis of 100% of the property is based on the date-of-death value Follow rules for your state. Separate property states (usually) Basis of the decedent s interest is based on the date-of-death value Basis of survivor s interest unchanged 14 7

8 What is the Basis Gifts Property received as gift Must know basis in the hands of donor Must know fair market value on day of gift Which to use? Depends on which is higher and whether computing gain or loss Taxpayer needs to provide basis or be referred to paid preparer 15 Special Situation (Stock Splits) Shareholder receives additional shares, usually no additional cost Basis of old shares is spread over all shares (old and new) Date acquired for new shares is same as for old shares 16 8

9 Stock Split Example Bought 100 shares for $5,000 on 7/1/2006 $50 per share ($5, shares) On 3/1/2014, receives 100 more shares due to stock split Total basis is still $5,000 Now $25 per share ($5, shares) Date acquired for all 200 shares is 7/1/ Special Situation (Dividend Reinvestment) Shareholder receives dividend payment as additional shares, usually no additional cost Broker reinvests new shares (may be fractional amount) Date acquired for new shares is dividend payment date Prior basis adjusted by adding new share purchase cost 18 9

10 Holding Period When did you buy it? When did you sell it? Always use trade date for securities Settlement date will be later Difference between buy date and sell date is the holding period 19 Capital Asset Taxation Capital gain tax rates apply to net long-term gains and qualified dividends Ordinary income rates apply to net short-term gains Capital gains or losses come from the sale of capital assets 20 10

11 Tax Rates Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower 0% for 10 & 15% ordinary rates 15% for 25 to 35% ordinary rates 20% for 39.6% ordinary rate 21 What is the Sales Price? Gross proceeds (sales price) Not reduced for expenses of sale Net proceeds Already reduced for expenses of sale 1099-B specifies method used 22 11

12 Gross or Net Proceeds If gross proceeds are reported on 1099-B Do not adjust proceeds for expenses of sale Instead, make adjustment equal to selling expenses (non-covered only) IRS matches proceeds reported on all Forms 1099-Bs to total proceeds on tax return Don t adjust for covered securities broker has already reflected in basis 23 Entering in TaxSlayer Taxpayer receives substitute Form 1099-B or IRS supplied Form 1099-B There may be corrected forms use last one received (will have date) Follow the statement Unless taxpayer has information that statement is incorrect or incomplete 24 12

Date of transaction Description and quantity of securities sold May need to report more information 26 13")

13 Actual form Many brokers provide a substitute 1099-B B Requirements All Transactions Payer must report: Proceeds (gross or net) Date of transaction Description and quantity of securities sold May need to report more information 26 13

14 1099-B Requirements Covered Transactions Only if securities sold were covered securities (transaction was required to be reported to IRS) Payer must also report: Cost or other basis Whether gain or loss is short-term or long-term A code and adjustment amount, e.g. W for wash sale and amount of loss to disallow Not required for non-covered securities 27 Summarize Broker Transactions per Pub 4012 Tab D Divide the transactions: Short term Basis reported to the IRS Box A Long term Basis reported to the IRS Box D Short term Basis not reported to the IRS Box B Long term Basis not reported to the IRS Box E 28 14

15 Sample Brokerage 1099-B Format varies by brokerage firm Brokers may present transactions subtotaled based on 1099 code 29 TaxSlayer Data Flow Enter transaction details on TaxSlayer Schedule D Capital Gains Input Flows to Forms 8949 Flows to Schedule D Flows to Form 1040 Line 13 TaxSlayer does the flowing 30 15

16 Capital Gains in TaxSlayer Navigation: Federal>Income>Capital Gains and Loses 31 TaxSlayer Input 32 16

17 TaxSlayer Input Enter net adjustment and check allapplicable boxes on screen below Description of codes see PUB 4012 Page D TaxSlayer Input If entering multiple transactions on a single line check code M and enter $0.00 if no other adjustments are required

18 Summarizing Multiple Brokerage Transactions Open Pub 4012 Page D-25: Each brokerage statement divides transactions into four categories: Short term transactions with basis reported to the IRS -categorized as Box A Short term transactions with basis not reported to the IRS - categorized as Box B Long term transactions with basis reported to the IRS -categorized as Box D Long term transactions with basis not reported to the IRS -categorized as Box E 35 Summarizing Multiple Brokerage Transactions - Continued Enter Totals from Statement using the alternate date options shown previously Enter the adjustment total from the statement with all applicable adjustment codes 36 18

19 Reporting Multiple Brokerage Transactions Tax-Aide Policy no longer requires that basis not reported information be sent to IRS using Form 8453 Taxpayer should be advised this information could be requested by IRS Scanned information may be attached as a PDF to the return, but it is not required 37 Wash Sales Sale of securities at a loss -ANDpurchase of same securities within 30 days of sale date (before or after) Result is that loss (in part or in whole) is disallowed... until later In scope only if reported on brokerage or mutual fund statement 38 19

20 Wash Sale What happens to disallowed loss in Wash Sale situation? Basis of new shares is increased by amount of prior disallowed loss Brokers/mutual funds do the accounting! 39 Capital Loss Carryovers For TY2017, review 2016 tax return for the schedule computing capital loss carryover available to 2017 If no loss carryover schedule but 1040 line 13 is exactly -3,000, will need to calculate TaxSlayer will carry forward available capital loss carryovers for returning taxpayers next year 40 20

21 Loss Carryovers Use taxpayers prior return Form 1040 Schedule D Input loss carryover(s) in TaxSlayer Other Capital Gains Data input sheet May need to input state loss carryover 41 Carryover Input Navigation: Federal>Income>Capital Gains and Loses>Other Capital Gains Data Enter long and short term loss carryover from Prior year return 42 21

22 Input is Done? TaxSlayer will Determine whether long/short term Calculate gain/loss Carry data to Form 8949 and Schedule D 43 Capital Gain (Loss) Questions Comments

Capital Gain or Loss. Form 1040 Line 13 Pub 4012 Tab D Pages Pub 4491 Part 3 Lesson 11

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pages 22-27 Pub 4491 Part 3 Lesson 11 Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss. Pub 4012 Tab D Pub 4491 Lesson 11

Capital Gain or Loss Pub 4012 Tab D Pub 4491 Lesson 11 Introduction Ordinary income tax rates range from 10% to 37% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very

Capital Gain or Loss Pub 4012 Tab D Pub 4491 Lesson 11 Introduction Ordinary income tax rates range from 10% to 37% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very

Capital Gain or Loss. Introduction. Capital Asset Taxation. Introduction. Capital Asset Taxation. What is a Capital Asset

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Introduction Capital Gain or Loss Form 1040 Line 13 Pub 4012 Tab D Pub 4491 Part 3 Lesson 11 What is a capital gain? It s the taxpayer s profit when they sell a capital asset for more than they have in

Capital Asset Taxation Introduction

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually 0% or 15% rate Could be 20% rate for very high incomes NTTC Training

Capital Gain or Loss

Capital Gain or Loss Form 1040 Line 13 Pub 4012 D 13 Pub 4491 Page 89 Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Capital Gain or Loss Form 1040 Line 13 Pub 4012 D 13 Pub 4491 Page 89 Capital Asset Taxation Introduction Ordinary income tax rates range from 10% to 39.6% Capital gain tax rates are much lower Usually

Sale of Personal Residence. Form 1040 Line 13 Pub 4012 Tab D Pg Pub 4491 Part 3 Lesson 11

Sale of Personal Residence Form 1040 Line 13 Pub 4012 Tab D Pg 28-32 Pub 4491 Part 3 Lesson 11 The Interview Question 3 in Life Events section COD is out of scope this tax season Home can be a second home

Sale of Personal Residence Form 1040 Line 13 Pub 4012 Tab D Pg 28-32 Pub 4491 Part 3 Lesson 11 The Interview Question 3 in Life Events section COD is out of scope this tax season Home can be a second home

Income Capital Gain or Loss; Form 1040, Line 13

Income Capital Gain or Loss; Form 1040, Line 13 Objectives Capital Gain or Loss Determine if the asset s holding period is long-term or short-term Calculate the taxable gain or deductible loss from the

Income Capital Gain or Loss; Form 1040, Line 13 Objectives Capital Gain or Loss Determine if the asset s holding period is long-term or short-term Calculate the taxable gain or deductible loss from the

Instructions for Form 8949

2012 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

2012 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted.

IRS tax reporting changes for investors

IRS tax reporting changes for investors E*TRADE Financial Corporation and its affiliates do not provide tax advice, and you always should consult your own tax advisor regarding your personal circumstances

IRS tax reporting changes for investors E*TRADE Financial Corporation and its affiliates do not provide tax advice, and you always should consult your own tax advisor regarding your personal circumstances

ICI Webinar on Cost Basis Reporting: Preparing for Tax Reporting Season. July 17, :00 2:30 p.m.

ICI Webinar on Cost Basis Reporting: Preparing for Tax Reporting Season July 17, 2012 1:00 2:30 p.m. Speakers Jeff Cook Director of Regulatory Compliance, DST Systems, Inc. Karen Gibian Associate Counsel,

ICI Webinar on Cost Basis Reporting: Preparing for Tax Reporting Season July 17, 2012 1:00 2:30 p.m. Speakers Jeff Cook Director of Regulatory Compliance, DST Systems, Inc. Karen Gibian Associate Counsel,

Instructions for Form 8949

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2015 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. 2015 Instructions for Form 8949 Sales and Other Dispositions of Capital Assets Department of the

Interest and Dividend Income

Interest and Dividend Income Form 1040 Lines 8 9 Pub 4012 Tab D Pub 4491 Lesson 9 What Is Interest Income? Earnings on Bank, savings, and credit union deposits Certificates of Deposit Bonds (corporate

Interest and Dividend Income Form 1040 Lines 8 9 Pub 4012 Tab D Pub 4491 Lesson 9 What Is Interest Income? Earnings on Bank, savings, and credit union deposits Certificates of Deposit Bonds (corporate

7th Correction Run October 10. ***Prior year corrections are included in the above schedule if requested.

Tax Reporting Q: LPL mails the majority of the 1099-C forms on February 15. Isn t this considered late? A: No. In the fall of 2008, the IRS recognized that there was not sufficient time to make the necessary

Tax Reporting Q: LPL mails the majority of the 1099-C forms on February 15. Isn t this considered late? A: No. In the fall of 2008, the IRS recognized that there was not sufficient time to make the necessary

A Comprehensive Guide to your Composite Tax Statement

A Comprehensive Guide to your Composite Tax Statement Hilltop Securities does not provide tax advice. This material is presented for informational purposes only. You should consult your tax advisor on

A Comprehensive Guide to your Composite Tax Statement Hilltop Securities does not provide tax advice. This material is presented for informational purposes only. You should consult your tax advisor on

Interest and Dividend Income. Form 1040 Lines 8 9 Pub 4012 Tab D Pub 4491 Lesson 9

Interest and Dividend Income Form 1040 Lines 8 9 Pub 4012 Tab D Pub 4491 Lesson 9 Interest Income Income on Bank and credit union deposits Bonds (corporate or government) Money loaned out It is not earned

Interest and Dividend Income Form 1040 Lines 8 9 Pub 4012 Tab D Pub 4491 Lesson 9 Interest Income Income on Bank and credit union deposits Bonds (corporate or government) Money loaned out It is not earned

Small Business Valuation Overview and Analysis

Small Business Valuation Overview and Analysis presented by Tim Mezhlumov, EA, CFP, CLU Business Valuation - Definition The process of determining the economic value or Fair Market Value (FMV) of a company

Small Business Valuation Overview and Analysis presented by Tim Mezhlumov, EA, CFP, CLU Business Valuation - Definition The process of determining the economic value or Fair Market Value (FMV) of a company

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

Form 1041 Schedule D: Reporting Capital Gains for Trusts and Estates FOR LIVE PROGRAM ONLY THURSDAY, SEPTEMBER 13, 2018, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This program is

1998 Instructions for Schedule D, Capital Gains and Losses

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

1998 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report: The sale or exchange of a capital asset (defined on this page). Gains from involuntary conversions (other

KEY IMPACTS OF THE COST BASIS LEGISLATION. Understanding cost basis legislation // How it impacts investors // Things to consider

KEY IMPACTS OF THE COST BASIS LEGISLATION Understanding cost basis legislation // How it impacts investors // Things to consider KEY TAKEAWAYS Raymond James is required to report detailed cost basis information

KEY IMPACTS OF THE COST BASIS LEGISLATION Understanding cost basis legislation // How it impacts investors // Things to consider KEY TAKEAWAYS Raymond James is required to report detailed cost basis information

Helpful Tips. for Out of Scope Topics. on the 2014 IRS Advanced Certification Exam

Helpful Tips for Out of Scope Topics on the 2014 IRS Advanced Certification Exam HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON 2014 IRS ADVANCED CERTIFICATION EXAM (Out Of Scope For SaveFirst Intermediate Volunteer

Helpful Tips for Out of Scope Topics on the 2014 IRS Advanced Certification Exam HELPFUL TIPS FOR OUT OF SCOPE TOPICS ON 2014 IRS ADVANCED CERTIFICATION EXAM (Out Of Scope For SaveFirst Intermediate Volunteer

Interest and Dividend Income. Pub 4012 Tab D Pub 4491 Lesson 9

Interest and Dividend Income Pub 4012 Tab D Pub 4491 Lesson 9 Interest and Dividend Income Interest Income US Savings Bonds and Treasury Obligation Interest Tax exempt interest Interest in a foreign bank

Interest and Dividend Income Pub 4012 Tab D Pub 4491 Lesson 9 Interest and Dividend Income Interest Income US Savings Bonds and Treasury Obligation Interest Tax exempt interest Interest in a foreign bank

2001 Instructions for Schedule D, Capital Gains and Losses

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2001 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Retirement Income: IRAs and Pensions. Pub 4491 Part 3 Pub 4012 Tab D

Retirement Income: IRAs and Pensions Pub 4491 Part 3 Pub 4012 Tab D Types of Retirement Income Individual Retirement Arrangement (IRA) Distributions Pensions Annuities Social Security (covered in a separate

Retirement Income: IRAs and Pensions Pub 4491 Part 3 Pub 4012 Tab D Types of Retirement Income Individual Retirement Arrangement (IRA) Distributions Pensions Annuities Social Security (covered in a separate

See Tax-Aide Scope Summary from OneSupport>Tax Training>Scope for differences between Tax-Aide scope and VITA scope.

This document provides how-to information for those items that are in scope for Tax-Aide but out of scope for VITA (and therefore not covered in Pub 4012.) See Tax-Aide Scope Summary from OneSupport>Tax

This document provides how-to information for those items that are in scope for Tax-Aide but out of scope for VITA (and therefore not covered in Pub 4012.) See Tax-Aide Scope Summary from OneSupport>Tax

2002 Instructions for Schedule D, Capital Gains and Losses

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

2002 Instructions for Schedule D, Capital Gains and Losses Use Schedule D (Form 1040) to report the following. The sale or exchange of a capital asset (defined on this page) not reported on another form

Preparing Taxes with TaxSlayer

Preparing Taxes with TaxSlayer Changes to Tax Law for ty 2017 What we all forget year to year Affordable Care Act New York Returns NJ non-resident returns 1 NTTC Training - TY2016 Review all docs before

Preparing Taxes with TaxSlayer Changes to Tax Law for ty 2017 What we all forget year to year Affordable Care Act New York Returns NJ non-resident returns 1 NTTC Training - TY2016 Review all docs before

Questions and Answers Regarding Form 1099-B and Cost Basis Reporting

Questions and Answers Regarding Form 1099-B and Cost Basis Reporting Cost basis information and this Q and A made available to clients are not intended to be, and should not be construed as, legal or tax

Questions and Answers Regarding Form 1099-B and Cost Basis Reporting Cost basis information and this Q and A made available to clients are not intended to be, and should not be construed as, legal or tax

Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

FOR LIVE PROGRAM ONLY Mastering 1099-B Reporting on Schedule D and Form 8949: Meeting Capital Gains Basis Reporting Challenges TUESDAY, AUGUST 1, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE

Year-End Planning 2017

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

Wealth Management Year-End Planning Executive Summary As we approach the end of, it is time to review traditional year-end planning decisions. We are aware of the significant changes in the tax code currently

January 1, Form 1099-B must include adjusted basis and long-term/short-term

Subject: New Cost Basis Reporting Rules Effective For 2011 (Revised December 28, 2010) Dear Client: The Energy Improvement and Extension Act of 2008 (the Act ), enacted on October 3, 2008, expanded existing

Subject: New Cost Basis Reporting Rules Effective For 2011 (Revised December 28, 2010) Dear Client: The Energy Improvement and Extension Act of 2008 (the Act ), enacted on October 3, 2008, expanded existing

A Comprehensive Guide to Your Composite 1099 Tax Statement

A Comprehensive Guide to Your 2016 Composite 1099 Tax Statement Table of Contents A Note from Hilliard Lyons... 1 Tax Information Reporting and Our Obligation to Clients... 2 What s New This Year and Important

A Comprehensive Guide to Your 2016 Composite 1099 Tax Statement Table of Contents A Note from Hilliard Lyons... 1 Tax Information Reporting and Our Obligation to Clients... 2 What s New This Year and Important

A Comprehensive Reference Guide to Your Consolidated Tax Statement

1099-Consolidated Tax Statement 2014 Guide A Comprehensive Reference Guide to Your 2014 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

1099-Consolidated Tax Statement 2014 Guide A Comprehensive Reference Guide to Your 2014 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

Instructions for Form 1099-B

2013 Instructions for Form 1099-B Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

2013 Instructions for Form 1099-B Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

Frequently Asked Questions

Northwestern Mutual Investment Services (NMIS) is enhancing its cost basis reporting services in preparation for and in response to IRS mandated changes in the Emergency Economic Stabilization Act of 2008.

Northwestern Mutual Investment Services (NMIS) is enhancing its cost basis reporting services in preparation for and in response to IRS mandated changes in the Emergency Economic Stabilization Act of 2008.

Ameriprise certificates tax reporting

Ameriprise certificates tax reporting The Ameriprise Certificate Company issues face-amount certificates which are Securities and Exchange Commission (SEC) registered investments with a stated maturity

Ameriprise certificates tax reporting The Ameriprise Certificate Company issues face-amount certificates which are Securities and Exchange Commission (SEC) registered investments with a stated maturity

Helping You Avoid IRA Distribution Mistakes

Helping You Avoid IRA Distribution Mistakes Provided to you by: Yvette Scanlon President & Financial Advisor 888-551-2133 Helping You Avoid IRA Distribution Mistakes Written by Financial Educators Provided

Helping You Avoid IRA Distribution Mistakes Provided to you by: Yvette Scanlon President & Financial Advisor 888-551-2133 Helping You Avoid IRA Distribution Mistakes Written by Financial Educators Provided

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E I R S A D V A N C E D C E R T I F I C A T I O N E X A M

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 7 I R S A D V A N C E D C E R T I F I C A T I O N E X A M OUT OF S COPE FOR S AV EFIRST INTERMEDIATE VOLUNTEERS AT TAX PR EPAR

H E L P F U L T I P S F O R O U T O F S C O P E T O P I C S O N T H E 2 0 1 7 I R S A D V A N C E D C E R T I F I C A T I O N E X A M OUT OF S COPE FOR S AV EFIRST INTERMEDIATE VOLUNTEERS AT TAX PR EPAR

Tax Year 2017 Form 1099-DIV/B Guide

Tax Year 2017 Form 1099-DIV/B Guide Form 1099 FAQs Q: WHAT SHOULD I DO UPON RECEIVING MY FORM 1099? A: Upon receiving your form please review the data carefully. Also be sure to check the tax identification

Tax Year 2017 Form 1099-DIV/B Guide Form 1099 FAQs Q: WHAT SHOULD I DO UPON RECEIVING MY FORM 1099? A: Upon receiving your form please review the data carefully. Also be sure to check the tax identification

Tax-Aide Supplement to Publication 4012 TY 2016 Version B Print and Replace Whole Pages

Tax-Aide Supplement to Publication 4012 TY 2016 Version B Print and Replace Whole Pages This optional document provides how-to information for those items that are in scope for Tax-Aide but out of scope

Tax-Aide Supplement to Publication 4012 TY 2016 Version B Print and Replace Whole Pages This optional document provides how-to information for those items that are in scope for Tax-Aide but out of scope

Smart IRA withdrawal strategies

Smart IRA withdrawal strategies Fidelity Viewpoints Wednesday, 29 August 2012 Knowing your income needs and options is key. Every year, if you re age 70½ or older, you generally need to withdraw a certain

Smart IRA withdrawal strategies Fidelity Viewpoints Wednesday, 29 August 2012 Knowing your income needs and options is key. Every year, if you re age 70½ or older, you generally need to withdraw a certain

Client Tax Letter. Income Tax Rates Hold Steady. What s Inside. Still a Bargain. April/May/June 2011

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Income Tax Rates Hold Steady April/May/June 2011 Tax legislation passed at the end of 2010 the Tax Relief, Unemployment

Client Tax Letter Tax Saving and Planning Strategies from your Trusted Business Advisor sm Income Tax Rates Hold Steady April/May/June 2011 Tax legislation passed at the end of 2010 the Tax Relief, Unemployment

A Comprehensive Reference Guide to your Consolidated Tax Statement

Formerly Clearview Correspondent Services, LLC. 1099-Consolidated Tax Statement 2012 Guide A Comprehensive Reference Guide to your 2012 1099 Consolidated Tax Statement This comprehensive and informative

Formerly Clearview Correspondent Services, LLC. 1099-Consolidated Tax Statement 2012 Guide A Comprehensive Reference Guide to your 2012 1099 Consolidated Tax Statement This comprehensive and informative

2017 Instructions for Schedule D

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule D Capital Gains and Losses These instructions explain how to complete Schedule D (Form 1040). Complete Form 8949 before

Department of the Treasury Internal Revenue Service 2017 Instructions for Schedule D Capital Gains and Losses These instructions explain how to complete Schedule D (Form 1040). Complete Form 8949 before

Finishing the Return in TaxSlayer. Pub 4012 Tab K Pub 4491 Lesson 31

Finishing the Return in TaxSlayer Pub 4012 Tab K Pub 4491 Lesson 31 Finishing the Return in TaxSlayer E- File Section Screens to Complete Return Type Tax Preparation and E-File Information State Return(s)

Finishing the Return in TaxSlayer Pub 4012 Tab K Pub 4491 Lesson 31 Finishing the Return in TaxSlayer E- File Section Screens to Complete Return Type Tax Preparation and E-File Information State Return(s)

Standard Deduction (4012 Tab F)

") Standard Deduction (4012 Tab F) $$ amount based on Filing Status (1040 Section 1) Subtraction from a taxpayer s AGI The idea is that it s the amount of money the IRS determines you used to live (expenses)

Standard Deduction (4012 Tab F) $$ amount based on Filing Status (1040 Section 1) Subtraction from a taxpayer s AGI The idea is that it s the amount of money the IRS determines you used to live (expenses)

2017 Tax Information Guide

2017 Tax Information Guide Please retain this booklet with your 2017 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information Guide is provided

2017 Tax Information Guide Please retain this booklet with your 2017 tax records. If you use the services of a tax advisor, please furnish this booklet to him or her. This Tax Information Guide is provided

LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 20 SOCIAL SECURITY BENEFITS

LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 20 SOCIAL SECURITY BENEFITS") LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 15 IRA DISTRIBUTIONS LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 19 UNEMPLOYMENT LINE 20 SOCIAL SECURITY BENEFITS LINE 21

LINE 13 CAPITAL GAIN AND LOSSES (SCHEDULE D) LINE 15 IRA DISTRIBUTIONS LINE 16 PENSIONS AND ANNUITIES LINE 17 RENTAL REAL ESTATE, ROYALTIES LINE 19 UNEMPLOYMENT LINE 20 SOCIAL SECURITY BENEFITS LINE 21

Income Tax Changes, Estate Tax Changes And Implications for Charitable Giving Of the Economic Growth and Tax Relief Reconciliation Act of 2001

Income Tax Changes, Estate Tax Changes And Implications for Charitable Giving Of the Economic Growth and Tax Relief Reconciliation Act of 2001 Prepared by Catherine E. Livingston and Beth Shapiro Kaufman

Income Tax Changes, Estate Tax Changes And Implications for Charitable Giving Of the Economic Growth and Tax Relief Reconciliation Act of 2001 Prepared by Catherine E. Livingston and Beth Shapiro Kaufman

Shareholder's Instructions for Schedule K-1 (Form 1120S)

") 2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

2017 Shareholder's Instructions for Schedule K-1 (Form 1120S) Shareholder's Share of Income, Deductions, Credits, etc. (For Shareholder's Use Only) Department of the Treasury Internal Revenue Service Section

Important Notes. Version c May 9, of 57. Presented by: Joseph Davis, CLU, ChFC For Evaluation Purposes Only

Ed and Tina Allen Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com Financial

Ed and Tina Allen Presented by: Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: joseph.davis@aol.com Financial

Year-end Tax Moves for 2017

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

New Federal Tax Legislation. Philip E. Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison

New Federal Tax Legislation Philip E. Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Its Not My Job Award In this day and age of ever increasing departmentalization,

New Federal Tax Legislation Philip E. Harris Department of Agricultural and Applied Economics University of Wisconsin-Madison Its Not My Job Award In this day and age of ever increasing departmentalization,

COST BASIS REPORTING GUIDELINES

COST BASIS REPORTING GUIDELINES VOLUME I Revision 2.0 DECEMBER 3, 2010 ACKNOWLEDGEMENT The STA Cost Basis Sub-Committee has spent many hours, over two years, creating and reviewing the transfer scenarios

COST BASIS REPORTING GUIDELINES VOLUME I Revision 2.0 DECEMBER 3, 2010 ACKNOWLEDGEMENT The STA Cost Basis Sub-Committee has spent many hours, over two years, creating and reviewing the transfer scenarios

Year end tax planning 2017/18

BOND Chartered Accountants KEY GUIDE Year end tax planning 2017/18 Income tax saving for couples If you re in a couple, you might be able to save tax by switching income from one spouse or partner to the

BOND Chartered Accountants KEY GUIDE Year end tax planning 2017/18 Income tax saving for couples If you re in a couple, you might be able to save tax by switching income from one spouse or partner to the

A Comprehensive Reference Guide to Your Consolidated Tax Statement

1099-Consolidated Tax Statement 2015 Guide A Comprehensive Reference Guide to Your 2015 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

1099-Consolidated Tax Statement 2015 Guide A Comprehensive Reference Guide to Your 2015 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

Vanguard mutual fund and brokerage investors 2016 Form 1099-B instructions

Vanguard mutual fund and brokerage investors 206 099-B instructions guide to reporting investment capital gains and losses from your 099-B on your tax return (IRS 040 or 040) When you ll receive your s

Vanguard mutual fund and brokerage investors 206 099-B instructions guide to reporting investment capital gains and losses from your 099-B on your tax return (IRS 040 or 040) When you ll receive your s

FINISHING TOUCHES. Pub 4012 Pages K-16 to K-22 Pub 4491 Lesson 31

FINISHING TOUCHES Pub 4012 Pages K-16 to K-22 Pub 4491 Lesson 31 2 FINISHING UP YOU ARE NOT DONE YET Review intake-interview View return [continue] to e-file Select Federal Return type Select State return

FINISHING TOUCHES Pub 4012 Pages K-16 to K-22 Pub 4491 Lesson 31 2 FINISHING UP YOU ARE NOT DONE YET Review intake-interview View return [continue] to e-file Select Federal Return type Select State return

Estate Taxation Made Simple (?) Monica Haven, E.A.

Monica Haven, E.A.") Estate Taxation Made Simple (?) 061403 Monica Haven, E.A. I. Types of Tax A. Estate Tax Assessed on the value of the decedent s estate on the date of death or the alternate valuation date 6 months later

Estate Taxation Made Simple (?) 061403 Monica Haven, E.A. I. Types of Tax A. Estate Tax Assessed on the value of the decedent s estate on the date of death or the alternate valuation date 6 months later

ESTATE EVALUATION. John and Jane Doe

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

NQ An easy, step-by-step guide

Your Non-Qualified () Stock Options Reporting the exercise and related sale of shares on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements

Your Non-Qualified () Stock Options Reporting the exercise and related sale of shares on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements

Cryptocurrencies as Charitable Gifts: Should Your Charity Say Yes?

With the increased notoriety of cryptocurrencies, many charities are exploring the option of accepting Bitcoin, Ripple, Litecoin and nearly 2,000 other virtual currencies for donations. In fact, Fidelity

With the increased notoriety of cryptocurrencies, many charities are exploring the option of accepting Bitcoin, Ripple, Litecoin and nearly 2,000 other virtual currencies for donations. In fact, Fidelity

A Comprehensive Reference Guide to Your Consolidated Tax Statement

1099-Consolidated Tax Statement 2017 Guide A Comprehensive Reference Guide to Your 2017 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

1099-Consolidated Tax Statement 2017 Guide A Comprehensive Reference Guide to Your 2017 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

Giving is a part of life. Charitable Giving With Life Insurance

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

Giving is a part of life Charitable Giving With Life Insurance If you are interested in giving more to charity, life insurance may be able to help. When properly implemented, a life insurance policy may

NORTHERN FUNDS TA X GUIDE 2O12

NORTHERN FUNDS TA X GUIDE 2O12 Contents 1 Mutual Fund Distributions 2 Forms & Statements 4 Form 1099 DIV 5 Form 1099 B/Cost Basis 6 Form 1099 R 7 Form 1099 Q 8 Form 5498 IRA 9 Form 5498 ESA WELCOME TO

NORTHERN FUNDS TA X GUIDE 2O12 Contents 1 Mutual Fund Distributions 2 Forms & Statements 4 Form 1099 DIV 5 Form 1099 B/Cost Basis 6 Form 1099 R 7 Form 1099 Q 8 Form 5498 IRA 9 Form 5498 ESA WELCOME TO

Internal Revenue Code Section 1296(e) Election of mark to market for marketable stock

Election of mark to market for marketable stock") CLICK HERE to return to the home page Internal Revenue Code Section 1296(e) Election of mark to market for marketable stock (a) General rule. In the case of marketable stock in a passive foreign investment

CLICK HERE to return to the home page Internal Revenue Code Section 1296(e) Election of mark to market for marketable stock (a) General rule. In the case of marketable stock in a passive foreign investment

Don t overpay your taxes. Learn more about tax reporting and cost basis facts for stock plans.

Don t overpay your taxes. Learn more about tax reporting and cost basis facts for stock plans. As a participant in your company s stock plan program and/or employee stock purchase plan (ESPP), it s important

Don t overpay your taxes. Learn more about tax reporting and cost basis facts for stock plans. As a participant in your company s stock plan program and/or employee stock purchase plan (ESPP), it s important

Capital Gains and Losses

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

Capital Gains and Losses Table of Contents Chapter 1: Basis Of Property... 2 I. Introduction... 2 II. Cost Basis... 2 III. Adjusted Basis... 4 IV. Basis Other Than Cost... 5 Chapter 2: Sale Of Property...

2017 Tax Guide FORM 1099-B

2017 Tax Guide FORM 1099-B Table of Contents IRS RESOURCES:... 3 FORM 1099-B: PROCEEDS FROM BROKER & BARTER EXCHANGE TRANSACTIONS... 4 Understanding Form 1099-B... 7 Frequently Asked Questions... 9 Resources

2017 Tax Guide FORM 1099-B Table of Contents IRS RESOURCES:... 3 FORM 1099-B: PROCEEDS FROM BROKER & BARTER EXCHANGE TRANSACTIONS... 4 Understanding Form 1099-B... 7 Frequently Asked Questions... 9 Resources

Chapter 12. Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges

Chapter 12 Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004

Chapter 12 Property Transactions: Determination of Gain or Loss,Basis Considerations, and Nontaxable Exchanges Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004

NTTC Modifications to the IRS Training Guide 2018 Returns Publication 4491

For volunteers using the hard copy of Pub 4491, the following recaps the modifications that were made to the electronic version available on the Volunteer Portal Library. Use this document in conjunction

For volunteers using the hard copy of Pub 4491, the following recaps the modifications that were made to the electronic version available on the Volunteer Portal Library. Use this document in conjunction

Section 2: Short-Term Transactions for which Basis Is Not Reported to the IRS Report on Form 8949, Part 1, with Box B checked.

2017 Tax Form 1099-B Proceeds from Redemptions or Exchange of Securities All redemptions (sales) or exchanges made in non-retirement mutual fund accounts must be reported on Form 1099-B. Form 1099-B reports

2017 Tax Form 1099-B Proceeds from Redemptions or Exchange of Securities All redemptions (sales) or exchanges made in non-retirement mutual fund accounts must be reported on Form 1099-B. Form 1099-B reports

Introduction to Estate and Gift Taxes

Department of the Treasury Internal Revenue Service Publication 950 (Rev. August 2007) Cat. No. 14447X Introduction to Estate and Gift Taxes Get forms and other information faster and easier by: Internet

Department of the Treasury Internal Revenue Service Publication 950 (Rev. August 2007) Cat. No. 14447X Introduction to Estate and Gift Taxes Get forms and other information faster and easier by: Internet

GMS SURGENT 2014 YEAR-END TAX SAVING TIPS

GMS SURGENT 2014 YEAR-END TAX SAVING TIPS As the days on the calendar grow short and the holiday season gets into full swing, we at GMS Surgent would like to provide you with some valuable ideas to reduce

GMS SURGENT 2014 YEAR-END TAX SAVING TIPS As the days on the calendar grow short and the holiday season gets into full swing, we at GMS Surgent would like to provide you with some valuable ideas to reduce

2017 Year-End Tax Reminders

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2017 Year-End Tax Reminders INCOME TAX Wealth Planning Income Tax Rates 1. The following federal tax rates now apply to most types of capital gains for taxpayers in the highest tax brackets: 39.6% (short-term),

2014 Cost Basis Legislation and Tax Reporting

2014 Cost Basis Legislation and Tax Reporting Fixed Income and Options Advisor Toolkit Volume II Table of Contents Introduction....2 NEW Reporting Requirements for Options....19 NEW Form 1099-B....3 NEW

2014 Cost Basis Legislation and Tax Reporting Fixed Income and Options Advisor Toolkit Volume II Table of Contents Introduction....2 NEW Reporting Requirements for Options....19 NEW Form 1099-B....3 NEW

Attention: This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page.

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red,

This form is referenced in an endnote at the Bradford Tax Institute. CLICK HERE to go to the home page. Attention: Copy A of this form is provided for informational purposes only. Copy A appears in red,

Dialogues Year-End Tax Planning Guide WEALTH STRATEGIES FOR DISCUSSION

Dialogues WEALTH STRATEGIES FOR DISCUSSION We can work with you and your tax professional to help you decide which year-end tax strategies may be beneficial to you. FOURTH QUARTER 2010 COURTESY OF THE

Dialogues WEALTH STRATEGIES FOR DISCUSSION We can work with you and your tax professional to help you decide which year-end tax strategies may be beneficial to you. FOURTH QUARTER 2010 COURTESY OF THE

Understanding Required Minimum Distributions for Individual Retirement Accounts

Understanding Required Minimum Distributions for Individual Retirement Accounts What are required minimum distributions (RMDs)? Required minimum distributions, often referred to as RMDs or minimum required

Understanding Required Minimum Distributions for Individual Retirement Accounts What are required minimum distributions (RMDs)? Required minimum distributions, often referred to as RMDs or minimum required

ISO An easy, step-by-step guide

Your Incentive Stock Options () Reporting the exercise and related sale on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements that may apply

Your Incentive Stock Options () Reporting the exercise and related sale on your 2017 tax return A tax This document provides information about US federal income tax reporting requirements that may apply

Let s Talk Taxes! If you have income, the IRS wants their share. We need to follow their rules on how to track and report it and pay taxes on it.

Let s Talk Taxes! If you have income, Why your club files the IRS wants their share. We need to follow their rules on how to track and report it and pay taxes on it. Form 1065 Your investment club is a

Let s Talk Taxes! If you have income, Why your club files the IRS wants their share. We need to follow their rules on how to track and report it and pay taxes on it. Form 1065 Your investment club is a

Let s Talk Taxes! If you have income, the IRS wants their share. We need to follow their rules on how to track and report it and pay taxes on it.

Let s Talk Taxes! If you have income, Why your club files the IRS wants their share. We need to follow their rules on how to track and report it and pay taxes on it. Form 1065 Your investment club is a

Let s Talk Taxes! If you have income, Why your club files the IRS wants their share. We need to follow their rules on how to track and report it and pay taxes on it. Form 1065 Your investment club is a

ESTATE OR TRUST TAX ORGANIZER FORM New Estate or Trust Administrators Information Needed

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

ESTATE OR TRUST TAX ORGANIZER FORM 1041 New Estate or Trust Administrators Information Needed This is a list of information which will be typically needed for us to work with you on tax issues for an estate

FIDUCIARY TAX ORGANIZER (FORM 1041)

") Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

Trust/Estate Name(s) Federal ID# Address City, Town, or Post Office County State ZIP Code Telephone Number Telephone Number Fax Number E-mail Address Home/Mobile Office Fiduciary Name(s) and Title(s) Federal

ALSO IN THIS ISSUE. The 2005 Form 5498, Instructions to the Participant and the Custodian

July 2005 Published Since 1984 ALSO IN THIS ISSUE The 2005 Form 5498, Instructions to the Participant and the Custodian HSAs and FDIC Insurance Not as Simple as It Should Be, Page 4 Form 1099-R For Roth

July 2005 Published Since 1984 ALSO IN THIS ISSUE The 2005 Form 5498, Instructions to the Participant and the Custodian HSAs and FDIC Insurance Not as Simple as It Should Be, Page 4 Form 1099-R For Roth

Business Income. Pub 4012 Tab D Pub 4491 Lesson 10

Business Income Pub 4012 Tab D Pub 4491 Lesson 10 Business Determination There are 3 choices 1. A business 2. Income producing, but not a business 3. Not entered into for profit (e.g. hobby) 2 A Business

Business Income Pub 4012 Tab D Pub 4491 Lesson 10 Business Determination There are 3 choices 1. A business 2. Income producing, but not a business 3. Not entered into for profit (e.g. hobby) 2 A Business

Contacts. Key Dates: BNY Mellon Broker-Dealer Services BNY Mellon Unit Holder Services

Contacts BNY Mellon Broker-Dealer Services 800.545.5256 BNY Mellon Unit Holder Services 800.856.8487 BNY Mellon Tax Information Line 866.568.8985 Price Quotes 800.953.6785 Internal Revenue Service 800.829.1040

Contacts BNY Mellon Broker-Dealer Services 800.545.5256 BNY Mellon Unit Holder Services 800.856.8487 BNY Mellon Tax Information Line 866.568.8985 Price Quotes 800.953.6785 Internal Revenue Service 800.829.1040

Tax-Aide Quality Review Guide For Tax Year 2018

Tax-Aide Quality Review Guide For Tax Year 2018 December 2018 AARP Tax-Aide FL2 District 45 The Villages, Florida This guide focuses on the needs of the FL 2 District 45 Tax-Aide Quality Reviewer, who

Tax-Aide Quality Review Guide For Tax Year 2018 December 2018 AARP Tax-Aide FL2 District 45 The Villages, Florida This guide focuses on the needs of the FL 2 District 45 Tax-Aide Quality Reviewer, who

PRACTICAL TIPS FOR CHARITABLE PLANNING

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

PRACTICAL TIPS FOR CHARITABLE PLANNING CLINT T. SWANSON SWANSON LAW FIRM, PLLC 200 REUNION CENTER NINE EAST FOURTH STREET TULSA, OKLAHOMA 74103 I. CHARITABLE PLANNING A. Importance of Charitable Planning

NOVEMBER 2017 THE CURRENT SHAPE OF TAX REFORM

NOVEMBER 2017 THE CURRENT SHAPE OF TAX REFORM While much remains to be done, the President and the majority of Congress have articulated their plan for tax reform. The draft bill includes significant tax

NOVEMBER 2017 THE CURRENT SHAPE OF TAX REFORM While much remains to be done, the President and the majority of Congress have articulated their plan for tax reform. The draft bill includes significant tax

2018 Consolidated 1099 Tax Statement

2018 Consolidated 1099 Tax Statement Furnished by Edward Jones for Taxable Brokerage Accounts Use this document to help understand your Consolidated 1099 Tax Statement from Edward Jones. The Consolidated

2018 Consolidated 1099 Tax Statement Furnished by Edward Jones for Taxable Brokerage Accounts Use this document to help understand your Consolidated 1099 Tax Statement from Edward Jones. The Consolidated

You re Doing Cost Basis Reporting But Are You Doing It Right?

You re Doing Cost Basis Reporting But Are You Doing It Right? Stevie D. Conlon Senior Director & Tax Counsel, Wolters Kluwer Financial Services Securities Transfer Association Annual Meeting October 21,

You re Doing Cost Basis Reporting But Are You Doing It Right? Stevie D. Conlon Senior Director & Tax Counsel, Wolters Kluwer Financial Services Securities Transfer Association Annual Meeting October 21,

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011 1) Chapter 1 was not assigned! 2) Formation and Capital Structure

Acc. 433, Chapter Outline for use with Prentice Hall's Federal Taxation Corporations Richard B. Malamud, last updates, in part, November, 2011 1) Chapter 1 was not assigned! 2) Formation and Capital Structure

Trusts and Other Planning Tools

Trusts and Other Planning Tools Today, We Will Discuss: Estate planning fundamentals Wills and probate Taxes Trusts Life insurance Alternate decision makers How we can help Preliminary Considerations Ask

Trusts and Other Planning Tools Today, We Will Discuss: Estate planning fundamentals Wills and probate Taxes Trusts Life insurance Alternate decision makers How we can help Preliminary Considerations Ask

Completing the e-file Section

Completing the e-file Section e-file Process When all the data has been enter paper Return Type Tax Preparation and E-File Information State Return(s) Taxpayer Bank Account Information Third Party Designee

Completing the e-file Section e-file Process When all the data has been enter paper Return Type Tax Preparation and E-File Information State Return(s) Taxpayer Bank Account Information Third Party Designee

Tax Planning for the New Tax Year 5th April 2015

ROBINSONS Chartered Accountants 5 Underwood Street, London N1 7LY Tel: Email: Website: 020 7684 0707 Follow us on Twitter: @robinsonslondon Tax Planning for the New Tax Year 5th April 2015 (Your guide

ROBINSONS Chartered Accountants 5 Underwood Street, London N1 7LY Tel: Email: Website: 020 7684 0707 Follow us on Twitter: @robinsonslondon Tax Planning for the New Tax Year 5th April 2015 (Your guide

A Comprehensive Reference Guide to Your Consolidated Tax Statement

1099-Consolidated Tax Statement 2013 Guide A Comprehensive Reference Guide to Your 2013 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

1099-Consolidated Tax Statement 2013 Guide A Comprehensive Reference Guide to Your 2013 1099-Consolidated Tax Statement This comprehensive and informative guide is a tool to assist you and your tax professional

SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS

INVESTMENTS") SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

Mutual Funds Tax Guide 2017

Mutual Funds Tax Guide 2017 A guide to your year-end tax statements and forms When it comes to investing, we at Nuveen work to help investors build and sustain the wealth of a lifetime. For many, that

Mutual Funds Tax Guide 2017 A guide to your year-end tax statements and forms When it comes to investing, we at Nuveen work to help investors build and sustain the wealth of a lifetime. For many, that

Partnership Taxation and the Preparation of Form 1065

AA. Introduction to the Federal Income Tax Issues of Partnership Taxation and the Preparation of Form 1065 Paul La Monaca, CPA, MST NSTP Director of Education Legislative Change Effective for 2016 Form

AA. Introduction to the Federal Income Tax Issues of Partnership Taxation and the Preparation of Form 1065 Paul La Monaca, CPA, MST NSTP Director of Education Legislative Change Effective for 2016 Form

Sale of Personal Residence. Pub 4012 Tab D Pub 4491 Lesson 11

Sale of Personal Residence Pub 4012 Tab D Pub 4491 Lesson 11 The Interview Question 9 in Income section: 9. (A) Income (or loss) from the sale of Stocks, Bonds or Real Estate? (including your home) (Forms

Sale of Personal Residence Pub 4012 Tab D Pub 4491 Lesson 11 The Interview Question 9 in Income section: 9. (A) Income (or loss) from the sale of Stocks, Bonds or Real Estate? (including your home) (Forms