United States Court of Appeals

|

|

|

- Reginald Booth

- 5 years ago

- Views:

Transcription

1 RECORD NO ORAL ARGUMENT HAS NOT YET BEEN SCHEDULED In The United States Court of Appeals For The District of Columbia Circuit INDIANA BOXCAR CORPORATION, Petitioner, v. RAILROAD RETIREMENT BOARD, Respondent, AMERICAN SHORT LINE AND REGIONAL RAILROAD ASSOCIATION Amicus Curiae for Petitioner. ON APPEAL FROM THE RAILROAD RETIREMENT BOARD FINAL BRIEF OF PETITIONER John D. Heffner STRASBURGER & PRICE, LLP 1700 K Street, N.W. Suite 640 Washington, D.C (202) Counsel for Petitioner THE LEX GROUP DC 1825 K Street, N.W. Suite 103 Washington, D.C (202) (800) Fax: (202)

2 USCA Case # Document # Filed: 05/07/2012 Page 1 of 3

3 USCA Case # Document # Filed: 05/07/2012 Page 2 of 3

4 USCA Case # Document # Filed: 05/07/2012 Page 3 of 3

5 TABLE OF CONTENTS Page TABLE OF CONTENTS... i TABLE OF AUTHORITIES... iii I. JURISDICTIONAL STATEMENT... 1 II. STATEMENT OF THE ISSUES... 2 III. STATUTES AND REGULATIONS... 2 IV. STATEMENT OF THE CASE... 3 V. STATEMENT OF FACTS... 4 VI. SUMMARY OF ARGUMENT VII. STANDING VIII. ARGUMENT A. STANDARD OF REVIEW B. THE BOARD S DECISION LACKS A REASONABLE BASIS AND IS ARBITRARY AND CAPRICIOUS INASMUCH AS IT FAILS TO PROVIDE A REASONED EXPLANATION FOR ITS DEPARTURE FROM LONG ESTABLISHED PRECEDENT C. THE BOARD S DECISION LACKS A REASONABLE BASIS AND IS ARBITRARY AND CAPRICIOUS INASMUCH AS IT IS CONTRARY TO THE PLAIN LANGUAGE OF THE STATUTE AND THE COMMON MEANING OF COMMON CONTROL i

6 D. THE BOARD S DECISION LACKS A REASONABLE BASIS AND IS ARBITRARY AND CAPRICIOUS BECAUSE IT IGNORES THE SUBSTANTIAL EVIDENCE OF RECORD IX. CONCLUSION CERTIFICATE OF COMPLIANCE CERTIFICATE OF FILING AND SERVICE ADDENDUM ii

7 TABLE OF AUTHORITIES Page(s) CASES Anacostia Rail Holdings Company B.C.D (1999) CAGY Industries, Inc. B.C.D (1995) CCP Holdings, Inc. B.C.D (1994) *Chevron U.S.A. v. Natural Res. Def. Council, 467 U.S. 837, 104 S. Ct. 2778, 81 L. Ed. 2d 694, 21 ERC 1049 (1984)... 11, 19 Dean v. United States, U.S., 129 S. Ct. 1849, 2009 LEXIS 3300 (2009) *Delaware Otsego Corporation B.C.D *Delaware Otsego Corporation B.C.D , 18 Holman v. U.S. R.R. Ret. Bd., 253 F.3d 975 (7th Cir. 2001) Housatonic Transportation Company B.C.D (1994) *Interstate Quality Services, Inc. v. Railroad Retirement Board, 83 F.2d 1465 (D.C. Cir. 1996)... 11, 14, 19 *Chief Authorities are Designated with an Asterisk iii

8 *Iowa Pacific Holdings, LLC B.C.D (2004)... 12, 17 *Itel Corporation v. United States Railroad Retirement Board, 710 F.2d 1243 (7th Cir. 1983) KBN, Inc. B.C.D (2001) Kurka v. U.S.R.R. Ret. Bd., 615 F.2d 246 (5th Cir. 1980) Louisiana Pub. Serv. Comm n v. FERC, 337 U.S. App. D.C. 312, 184 F.3d 892 (D.C. Cir. 1999) McDonald v. Thompson, 305 U.S. 263, 59 S. Ct. 176, 83 L. Ed. 164 (1938) Mississippi Central Railroad Co. Change in Operators Exemption Tishomingo Railroad Company, Inc., FD 35258, STB, July 10, Moskal v. United States, 498 U.S. 103, 112 L. Ed. 2d 449, 111 S. Ct. 461 (1990) Motor Vehicle Mfrs. Ass n v. State Farm Mut. Auto. Ins. Co., 463 U.S. 29, 103 S. Ct. 2856, 77 L. Ed. 2d 443 (1983) National Fed n of Fed. Emples., Local 951 v. FLRA, 412 F.3d 119 (D.C. Cir. 2005) *New York Cross Harbor Railroad v. Surface Transportation Board, 374 F.3d 1177 (D.C. Cir. 2004)... 14, 15 North American Railnet, Inc. B.C.D (1997) *Patriot Rail, LLC, et al, Employer Status Determination B.C.D iv

9 S. Dev. Co. v. U.S.R.R. Ret. Bd., 243 F.2d 351 (8th Cir. 1957)... 14, 27 States Rail, Inc. B.C.D (1998) *Union Pacific Corporation v. United States 26 Cl. Ct. 739, 1992 U.S.C. Ct. Lexis 280, aff d, 5 F.3d 523 (Fed. Cir. 1993)... 3, 4, 10, 11, 12, 15, 16, 17, 18, 19, 20, 21, 22, 23, 27 Utah Copper Co. v. Railroad Retirement Bd., cert. denied, 129 F.2d 358 (10th Cir. 1942) 317 U.S. 687, 63 S. Ct. 258, 87 L. Ed. 551 (1942) STATUTES 26 U.S.C U.S.C. 3231(a) U.S.C. 3231(b) U.S.C. 3231(d) U.S.C. 231(a)(1) U.S.C. 231(a)(1)(i) U.S.C. 231(a)(1)(ii)... 8, 9, 21, U.S.C. 231(a)(2) U.S.C. 231(b) U.S.C. 231f(b)(5) U.S.C. 231g... 1, U.S.C. 351(b) v

10 45 U.S.C. 351(d) U.S.C. 355 et seq.... 1, 13 REGULATIONS 20 CFR , 22, CFR , CFR 1201.A OTHER AUTHORITIES Webster s New International Dictionary 539 2d ed. (1951) vi

11 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT Indiana Boxcar Corporation, ) Petitioner ) v. ) United States Railroad ) No Retirement Board, ) Respondent ) ) BRIEF OF PETITIONER-APPELLANT INDIANA BOXCAR CORPORATION I. JURISDICTIONAL STATEMENT The decision under review was issued January 13, 2012, by the United States Railroad Retirement Board ( the Board ) pursuant to the Railroad Retirement Act of (b)(5) ( the RRA ), 45 U.S.C. 231f(b)(5) (2000). That final agency decision is subject to review in this Court. RRA 8, 45 U.S.C. 231g (2000). Indiana Boxcar Corporation (hereinafter IBCX ) filed its Petition for Review in this Court on March 20, 2012, within the ninety-day limit provided for in section 5(f) of the Railroad Unemployment Insurance Act ( RUIA ), which the RRA incorporates by reference. See Petition for Review, at 2 (citing 45 U.S.C. 355 et seq.). 1

12 II. STATEMENT OF THE ISSUES 1. Whether the Railroad Retirement Board s decision finding IBCX to be an employer covered by and subject to the Railroad Retirement Act, the Railroad Unemployment Insurance Act, and the Railroad Retirement Tax Act is contrary to law. 2. Whether the Railroad Retirement Board s decision finding IBCX to be an employer covered by and subject to the Railroad Retirement Act, the Railroad Unemployment Insurance Act, and the Railroad Retirement Tax Act is arbitrary and capricious. 3. Whether the Railroad Retirement Board s decision finding IBCX to be an employer covered by and subject to the Railroad Retirement Act, the Railroad Unemployment Insurance Act, and the Railroad Retirement Tax Act is supported by substantial evidence. III. STATUTES AND REGULATIONS Pertinent statutes and regulations are set forth in the attached addendum: Statutes: 45 U.S.C. 231(a)(1)(i) and (ii) 45 U.S.C. 231(b) 45 U.S.C. 231g 45 U.S.C. 351(b) 2

13 45 U.S.C. 351(d) 45 U.S.C. 355 Regulations: 20 CFR CFR IV. STATEMENT OF THE CASE This is an appeal of the Board s decision on reconsideration dated January 13, 2012 ( the Reconsideration Decision ), 1 holding that IBCX is a covered employer under the RRA, the RUIA, and the Railroad Retirement Tax Act ( RRTA ). 2 The Board conceded that IBCX is clearly not a rail carrier employer under the definition of employer pursuant to subsection (i) of the RRA, 45 U.S.C. 231(a)(1). Nevertheless, it went on to find IBCX a rail carrier affiliate and the services that it was performing for those entities were services in connection with railroad transportation under 231(a)(2); Reconsideration Decision at 1, 2, 6, and 7; J.A. 116, 117, 122. Additionally, the Board rejected IBCX s argument based on Union Pacific Corporation v. United States, 5 F.3d 523 (Fed. Cir. 1993) (hereafter Union Pacific) that it is not under common control with its rail carrier subsidiaries. Reversing without explanation nearly 20 years of 1 2 Management Member Kever dissenting. collectively the Acts 3

14 precedent, the Board reasoned that the Union Pacific ruling should not apply to closely held corporate structures where control of the parent company and subsidiary carrier(s) is clearly concentrated in a few individuals. Reconsideration Decision at 6; J.A The Reconsideration Decision affirmed and adopted the Board s initial decision dated August 11, 2008, cited as Employer Status Determination-Indiana Boxcar Corporation, B.C.D (hereafter the Initial Decision ), but shortened the first coverage period by approximately 29 months. 3 Reconsideration Decision at 9; J.A V. STATEMENT OF FACTS IBCX is a subchapter S corporation established in 1988 for the purpose of acquiring and owning railroad rolling stock. In 1996 IBCX President Powell Felix and his wife obtained control of that company when they acquired the shares of the other stockholders. 4 Historically, IBCX s principal business activities involved owning and leasing rail cars, buying, owning, and leasing locomotives, rerailing 3 Initially the Board found the coverage period extended from January 1, 1997 to April 1, Initial Decision at 4; J.A. 29. On reconsideration it shortened the period to the 10 months between May 28, 1999, and April 1, Reconsideration Decision at 9; J.A IBCX had initially represented to the Board that IBCX was formed in 1988 by Mr. and Mrs. Felix for the purpose of providing services to unaffiliated short line railroads and other parties that own railroad facilities or assets. J.A. 2 and

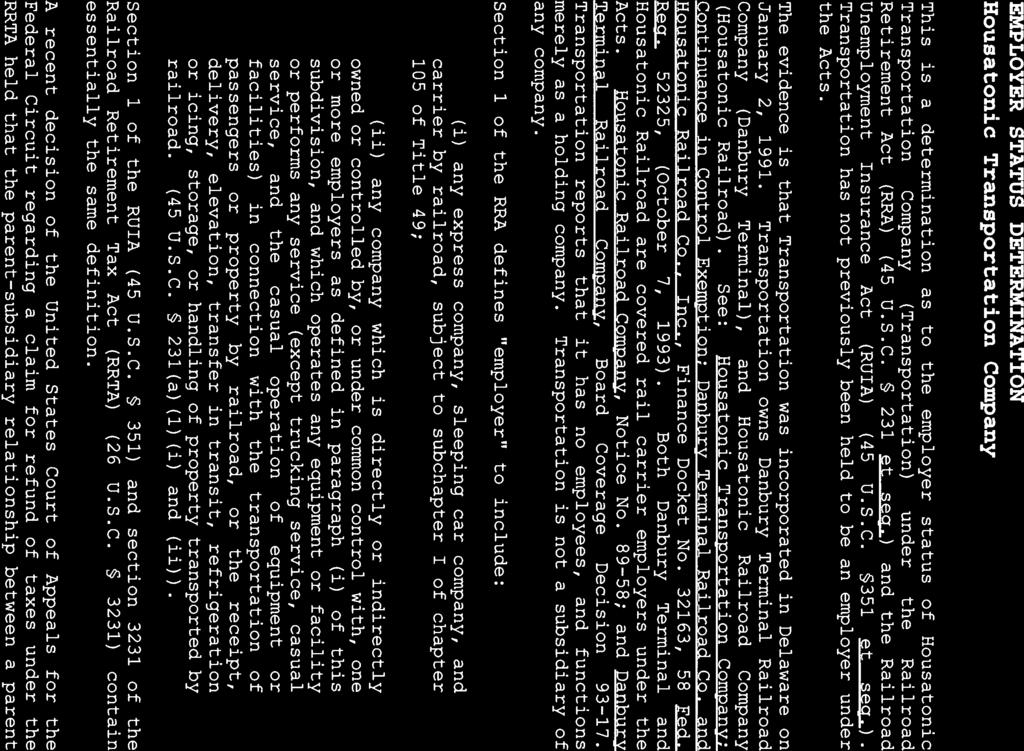

15 derailed rail cars, and performing railroad-related consulting services for unaffiliated clients including short line railroads. 5 No railroads own or have ever owned an interest in IBCX. Conversely, IBCX does not itself own and has never owned any railroad lines or facilities or held itself out as a common carrier to provide transportation for compensation. J.A. 34-6, 39-40; and IBCX did not become a short line railroad holding company until 1999 when it acquired majority control of the Evansville Terminal Railway Company ( EVT ). 6 It subsequently sold its interest in EVT and ceased to be a short line railroad holding company on April 1, J.A. 36 and Starting in 2003, IBCX once again became a short line railroad holding company when it established Vermilion Valley Railroad Company, Inc., as the first of several small carrier subsidiaries it would eventually own. Thereafter, it successively formed the Chesapeake and Indiana Railroad Company, Inc. (August 11, 2004), the 5 Such as rail-served industries, public agencies, and other short line railroads. The Surface Transportation Board ( STB ), the federal agency having jurisdiction over the economic regulation of railroads, classifies railroads according to their revenues. Short lines are generally regarded by the STB as carriers having under $20 million in annual operating revenues. See, 49 CFR Part 1201, Subpart A, 1-1. Short lines typically provide rail service over light density branch lines shed by larger carriers. 6 The Board s Initial Decision erroneously determined that IBCX became subject to the Railroad Retirement Act on January 1, 1997, as a result of its control of EVT. Initial Decision at 4; J.A. 29. In response to IBCXs reconsideration petition, Board corrected its error in the Reconsideration Decision. See footnote 3 on page 4; J.A

16 Tishomingo Railroad Company (April 1, 2006), 7 and the Youngstown & Southeastern Railway Company (December 1, 2006) to operate each of the rail lines that it had been engaged to operate. J.A. 36; Mr. Felix also manages Ohi-Rail, Inc., an unaffiliated Ohio-based short line railroad. J.A and During the periods that IBCX owned no railroads, it continued as an active company serving unaffiliated railroad-related clients. Although IBCX initially had no employees on its payroll, it engaged Mr. Felix as its first employee in J.A. 35 and 51. During the short period that IBCX owned a controlling interest in EVT, IBCX and its railroad subsidiary kept separate books and payrolls, bookkeeping systems, checking accounts, tax returns, and payrolls for each company. Mr. Felix received two pay checks, one subject to Railroad Retirement Tax ( RRTX ) for EVT work and one subject to Social Security tax for IBCX work. J.A. 36 and It discontinued that practice when it sold EVT. J.A. 36 and 53. Upon IBCX s reentering the short line railroad business as a holding company owning carrier subsidiaries, Mr. Felix resumed his former practice of receiving separate compensation from the railroads for railroad work subject to 7 Operations were transferred in 2009 to a railroad owned by short line railroad holding company Pioneer Rail Corporation. See, Mississippi Central Railroad Co. Change in Operators Exemption Tishomingo Railroad Company, Inc., FD 35258, STB served July 10, 2009, copy attached. 8 Neither IBCX nor Mr. Felix own any stock in Ohi-Rail, Inc. J.A. 37 and 58. 6

17 RRTX and one from IBCX for holding company and unaffiliated company work subject to Social Security tax. It did so based upon advice that it received from Board employees. J.A. 37, 43, and Mr. Felix functions as president of each of the subsidiary railroads paid as an employee of the specific carrier. J.A. 47 and 56. Since several of IBCX s railroad subsidiaries have full time managers, the services that Mr. Felix provides at IBCX for the subsidiary railroads are limited to administrative functions such as billing, electronic data transmittal, Federal Railroad Administration rules compliance, accounting and other supervisory duties. J.A. 38 and 58. IBCX represented to the Board that it allocates Mr. Felix s compensation as 27% to IBCX and 73% to the railroad subsidiaries. The vast majority (approaching 90%) of Mr. Felix s compensation and work for IBCX is for its unaffiliated clients. J.A. 38, 44; and Mr. Felix terminated his employment relationship with IBCX as of July 31, 2008, even though he continues to the own the company and direct its activities. J.A. 46 and 57. Since then, Mr. Felix has derived all compensation for railroad work for the IBCX-owned subsidiaries in the form of salary from those companies subject to RRTX. J.A and 56. During the period between 2005 and 2008, IBCX also employed Mr. Felix s daughter, Ms. Kesha Felix Lainhart. She divided her time between performing administrative work and railroad work for the individual subsidiaries. She was 7

18 paid as an employee of IBCX subject to Social Security tax and as an employee of the individual railroad subsidiaries subject to RRTX. More than 50% of Ms. Lainhart s compensation came from the rail carrier subsidiaries. J.A. 37-8, 43; and On August 11, 2008, the Board issued its Initial Decision. 9 It held that [b]ecause Mr. Felix is the president of both [IBCX] and [its short line railroad subsidiaries] the Board finds that [IBCX] is under common control with those railroads within the meaning of section 1(a)(1)(ii) of the RRA and the corresponding section of the RUIA. The Board continued, [t]he evidence of record establishes that [IBCX] does not conduct rail carrier operations itself. [IBCX] has, however, been involved in the operating or management of short line railroads since Accordingly, the Board finds that [IBCX] has been performing services in connection with the transportation of passengers or property by railroad for the period 1997 to 2000 [in connection with its ownership relationship with EVT] and the again from 2003 to the present [in connection with its ownership relationships with its other carrier subsidiaries]. The Board concluded with the statement, [t]he Board holds that [IBCX] became an affiliate employer under the [Acts] effective January 1, 1997, the beginning of the first year 9 Management Member Kever dissenting. 8

19 during which it was under common control with a rail carrier employer. Initial Decision at 4; J.A. 29. IBCX filed its Petition for Reconsideration on August 5, It argued that the Board s ruling contained material errors of both law and fact inasmuch as IBCX was strictly a short line railroad holding company without any railroad operations or common carrier obligations and was therefore not a covered employer. J.A. 34. IBCX noted that even the Board has conceded it is not a rail carrier under the first test of 45 U.S.C. 231(a)(1)(i): [t]he evidence of record establishes that [IBCX] does not conduct rail carrier operations itself. J.A. 40. IBCX asserted that it does not satisfy the second statutory coverage test of 45 U.S.C. 231(a)(1)(ii) as well, as a company which is directly or indirectly owned or controlled by, or under common control with, one or more employers as defined in paragraph (i) of this subdivision, and which operates any equipment or facility or performs any service in connection with the transportation of passengers or property by railroad, because it is not owned or controlled by a railroad common carrier and it is not under common control with one or more railroad common carrier employers, citing 9

20 the lower court s ruling in Union Pacific Corporation v. United States (cited as Union Pacific). 10 J.A. 40. IBCX stressed that the Board s Initial Decision contradicted without explanation or even citation its decision on reconsideration in Delaware Otsego Corporation. 11 J.A. 41. Had the Board applied the Court ruling in Union Pacific and its own ruling on reconsideration to Delaware Otsego, IBCX could not have been found covered because there was no common control relationship between it and its subsidiary railroads. J.A. 43. Finally, IBCX addressed the Board s concern that it was performing services in connection with transportation for its rail carrier subsidiaries, noting that when Mr. Felix and Ms. Lainhart performed services for IBCX subsidiaries they did so as employees of those carriers and were paid by the specific railroad carrier(s) subject to RRTX. As IBCX observed, this practice is totally consistent with the Board s ruling in the second to last paragraph of Delaware Otsego. J.A Cl. Ct. 739, 1992 U.S.C. Ct. Lexis 280, aff d, 5 F.3d 523 (Fed. Cir. 1993) (holding that there is no common control relationship between a holding company parent and its subsidiary companies; common control only exists between corporate siblings). 11 B.C.D (Dec. 24, 2003) (involving a similarly situated entrepreneurowned short line railroad holding company and holding it to be noncovered). 10

21 VI. SUMMARY OF ARGUMENT The Board erred in finding IBCX a covered employer due to common control with its railroad subsidiaries. Where the statute is clear on its face as to the meaning of a term as it is here, the Court need not give any deference to the Board s interpretation of common control. Chevron U.S.A. v. Natural Res. Def. Council, 467 U.S. 837, 842, 104 S. Ct. 2778, 2781 (1984) cited in Interstate Quality Services, Inc. v. Railroad Retirement Board, 83 F.2d 1465 (D.C. Cir. 1996) (standing for the proposition that it is for the court as well as the agency to give effect to the unambiguously expressed intent of Congress). Under controlling precedent including both Union Pacific and numerous Board decisions until now the agency must engage in a two-step analysis to find coverage. First, it must determine whether common control exists. If so, the second step is to ascertain whether an entity is providing services to its affiliates. Absent a common control finding, there is no way the Board could even reach the question of whether services are provided to affiliates. 11

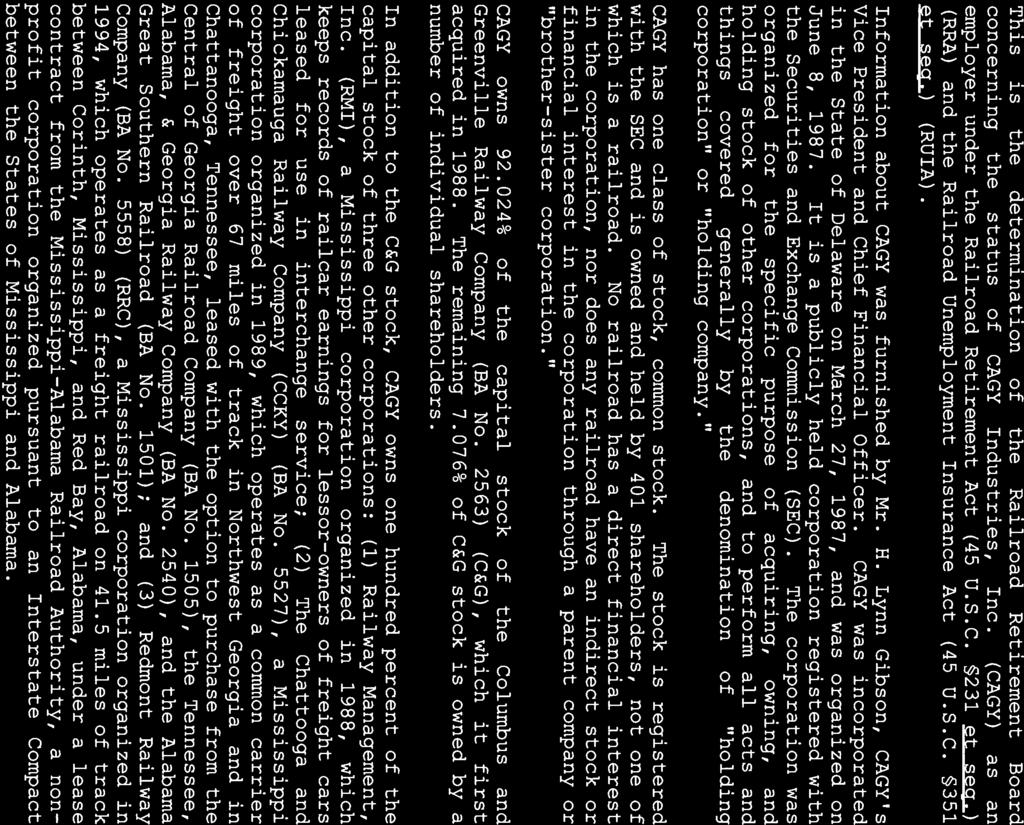

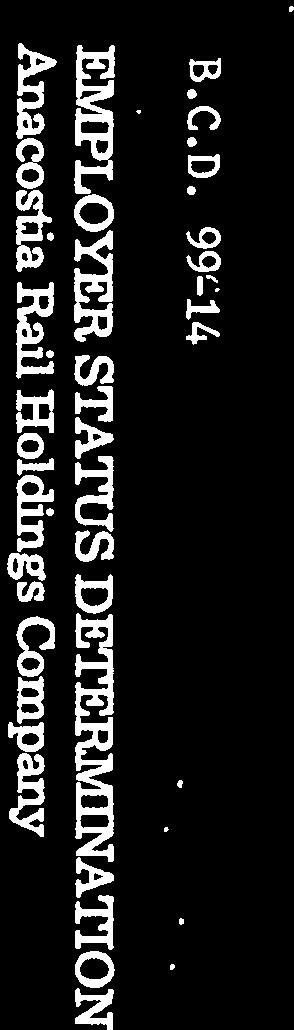

22 The Board s decision is defective in three respects. First, it represents an unexplained departure from a long line of judicial and agency precedent 12 finding that a noncarrier holding company that owns a series of subsidiary railroads is not under common control with those companies for the purpose of establishing coverage under the Acts. The Board s simplistic analysis allowing publicly held railroad holding companies to avoid that coverage while subjecting private, closely held companies to the Board s jurisdiction is arbitrary and capricious. It fails to explain why it is now departing from 20 years of consistent application of Union Pacific to closely held companies. Further, determining tax status and employee benefits based on the number or identity of a holding company s owner(s) bears no relation to Congress intent. In fact, some railroad holding companies have gone from being publicly traded entities to privately held concerns only to have their ownership status change again at a future date. 12 Illustrative Board decisions finding short line railroad holding companies outside the coverage jurisdiction of the Acts include B.C.D (1994), Housatonic Transportation Company; B.C.D (1994), CCP Holdings, Inc.; B.C.D (1995), CAGY Industries, Inc.; B.C.D (1997), North American Railnet, Inc.; B.C.D (1998), States Rail, Inc.; B.C.D (1999), Anacostia Rail Holdings Company; B.C.D (2001), KBN, Inc.; and B.C.D (2004), Iowa Pacific Holdings, LLC. In each case the Board stated a parent corporation which owns a rail carrier subsidiary is not under common control with the subsidiary within the meaning of 3231 of the [RRTX] citing the appeals court s ruling in Union Pacific, and adding [t]he relevant facts of the Union Pacific case are indistinguishable from those presented by the instant case. 12

23 Second, the Board s holding that common control exists between a corporate parent and its subsidiaries violates the plain language of the statute as well as the common dictionary definition of that term. The practical result of the Board s holding is to find that certain services that IBCX provides to its subsidiaries automatically subject it to coverage under the Acts. Finally, the Board s decision ignores the substantial evidence of record insofar as it erroneously treats work performed by individuals Mr. Felix and his daughter Ms. Lainhart for the rail carrier subsidiaries as work performed by the holding company. In fact, the evidence shows that such work was actually performed by Mr. Felix and Ms. Lainhart as carrier employees subject to RRTX and no compensation was paid by IBCX. J.A. 37-8, 43, 46-7, 56, and 58. VII. STANDING Standing to seek review of an order of the Board is conferred by 45 U.S.C. 231g and 45 U.S.C IBCX was a party to an administrative proceeding before the Board, and, as such, it is adversely affected by the Board s ruling. This proceeding challenges the validity of the Board s ruling. 13

24 VIII. ARGUMENT A. STANDARD OF REVIEW In general a Board decision must have a reasonable basis in law, not be based on an error in law, and be supported by substantial evidence. See, e.g., Interstate Quality Services, Inc., supra; Holman v. U.S. R.R. Ret. Bd., 253 F.3d 975, 978 (7th Cir. 2001); S. Dev. Co. v. U.S.R.R. Ret. Bd., 243 F.2d 351, 353 (8th Cir. 1957); and Itel Corporation v. United States Railroad Retirement Board, 710 F.2d 1243 (7th Cir. 1983) (cited as Itel). This Court and others have applied this reasonable basis in the law standard to the Board s interpretation of its statutes and regulations. See, Itel, supra (holding that the Board s interpretation of a statute has no reasonable basis in law when it requires the court to ignore clear statutory language) and Kurka v. U.S.R.R. Ret. Bd., 615 F.2d 246, (5th Cir. 1980) (reversing a Board ruling which misapplied the statutory requirements by ignoring the statutory definition of employee ). Similarly, Courts have held that an agency has not acted reasonably when it departs from established precedent without providing an explanation for its decision. New York Cross Harbor Railroad v. Surface Transportation Board, 374 F.3d 1177 (D.C. Cir. 2004). 14

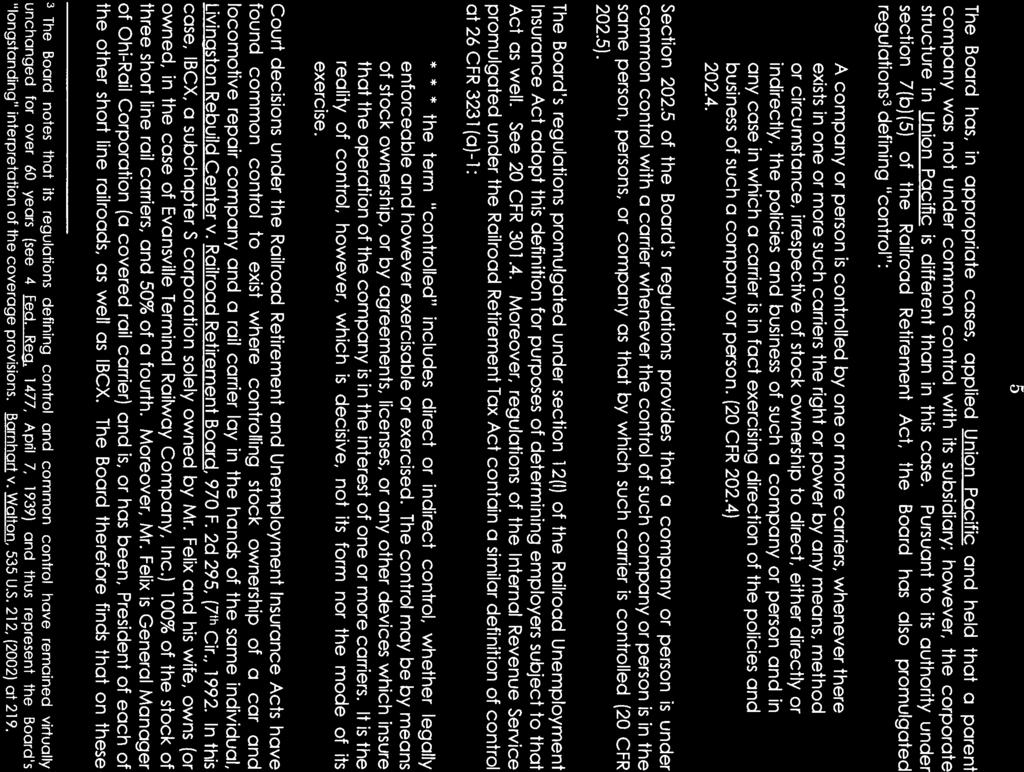

25 B. THE BOARD S DECISION LACKS A REASONABLE BASIS AND IS ARBITRARY AND CAPRICIOUS INASMUCH AS IT FAILS TO PROVIDE A REASONED EXPLANATION FOR ITS DEPARTURE FROM LONG ESTABLISHED PRECEDENT By finding that IBCX could not avail itself of the Federal Circuit s ruling in Union Pacific, which states that a railroad holding company is not under common control with its subsidiary railroad for the purpose of determining coverage under the Acts, the Board violated the basic rule of administrative law that an agency must follow its precedents or provide a reasoned explanation for its departure. National Fed n of Fed. Emples., Local 951 v. FLRA, 412 F.3d 119, 120, 124 (D.C. Cir. 2005). As this Court succinctly stated: An agency acts arbitrarily and capriciously if it reverses its position in the face of a precedent it has not persuasively distinguished, citing Louisiana Pub. Serv. Comm n v. FERC, 337 U.S. App. D.C. 312, 184 F.3d 892, 897 (D.C. Cir. 1999) and Motor Vehicle Mfrs. Ass n v. State Farm Mut. Auto. Ins. Co., 463 U.S. 29, 57, 103 S. Ct. 2856, 77 L. Ed. 2d 443 (1983) ( An agency s view of what is in the public interest may change, either with or without a change in circumstances. But an agency changing its course must supply a reasoned analysis. (internal quotation omitted)), and if it fails to consider all the relevant factors in reaching its decision. New York Cross Harbor Railroad v. Surface Transportation Board, 374 F.3d 1177, 1181 (D.C. Cir. 2004). The Board makes absolutely no attempt to do so here. It summarily rejects 20 years of consistent precedent with the following two statements: The Board has, in appropriate cases, applied [Union Pacific] and held that a parent company was not under common control with its subsidiary; however, the corporate structure in Union Pacific is different than in this case.. 15

26 With respect to IBCX s argument that the Court s holding in [Union Pacific] as previously applied by the Board dictates that IBCX is not under common control with its wholly owned subsidiaries, we note that the Board has declined to follow [Union Pacific] in closely held corporate structures where control of the parent company and subsidiary carrier(s) is clearly concentrated in a few individuals. Review of the [Union Pacific] case indicates that the Court in [Union Pacific] noted that the shareholders of the holding company could exercise some control over the policies of that entity, which, in turn, could exercise some control of the policies of the subsidiary rail carrier. However, the Court did not find that the ultimate authority of the shareholders subjected the holding company and subsidiary rail carrier to common control. We find such a conclusion reasonable in the case of a publicly held corporation, where ownership is so diffuse among a large number of stockholders that any control exercised by shareholders is remote, indirect, and, to a certain extent, nonexistent. However, in the case before us, control of all operations is direct and absolute. Mr. Felix and his wife are sole owners of IBCX, which in turn owns a number of small rail carriers covered under the Acts. Ownership of IBCX and the carriers is concentrated in two individuals. Accordingly, the Board finds on these facts that IBCX is under common control with its rail carrier subsidiaries. Reconsideration Decision at 5-6; J.A The Board s ruling suggests that at some point between the date Union Pacific was issued (1993) and the date the Initial Decision was served (2008), the agency issued one or more decisions declining to allow closely held carriers the benefits of this policy. Reconsideration Decision at 6; J.A However, the Board cited no precedent and IBCX s research has not disclosed any. Rather the Board has issued a long line of decisions exempting from coverage under the Acts privately held short line railroads where the holding company officers, directors, 16

27 and even shareholders have been intimately involved in the day-to-day operations of the subsidiary carriers. 13 In B.C.D , Delaware Otsego Corporation, the Board started to change that policy by ruling that Delaware Otsego Corporation, a short line holding company that controlled two carriers, was under common control with its subsidiaries and subject to coverage under the Acts. However, on reconsideration the Board reversed itself stating that [t]o the extent that those decisions imply that the Board would apply Union Pacific to any case involving a parent with a subsidiary employer without examining the existence of control, the Board rejects that implication. B.C.D , Decision on Reconsideration, Delaware Otsego Corporation, slip op. at 6, served December 24, In one of the only two short line holding company cases decided since then, B.C.D , Iowa Pacific Holdings, LLC, Employer Status Determination, served September 20, 2004, the Board held that neither Iowa Pacific, nor its noncarrier holding company subsidiary, Permian Basin Railways, were covered employers under the Acts. 14 The Board issued this ruling despite the fact that Iowa 13 See, illustrative cases cited in footnote 12 at page The Board would have found Permian Basin covered under the Acts but for the fact that it was a corporate shell with no employees. Id. 17

28 Pacific was a closely held company managed by its shareholder-officers. 15 The Board found that Iowa Pacific had a small staff of seven employees subject to Social Security coverage who performed administrative activities and by implication a larger number of workers covered under the Acts and employed by its carrier subsidiaries who performed railroad-related tasks. In holding Iowa Pacific not subject to coverage, the Board s reasoning cited Union Pacific, The relevant facts of the Union Pacific case are indistinguishable from those presented by Iowa Pacific. Accordingly, the Board determines that Iowa Pacific Holdings, LLC, is not an employer under the Acts as it is not under common control with its rail carrier subsidiaries. IBCX s research has identified only one other short line holding company ruling issued after Delaware Otsego, namely B.C.D , Patriot Rail, LLC, et al, Employer Status Determination. The Board s decision finding two of the three Patriot Rail holding companies not covered focused on the fact that these entities did not provide a service in connection with railroad transportation. Id. at By contrast, IBCX s two employees split their time working part-time for the railroad subsidiaries performing railroad-related duties and receiving pay checks subject to RRTX withholding. To the extent these employees work for IBCX or for unaffiliated clients, they receive separate IBCX checks subject to Social Security tax. See, discussion at pages

29 C. THE BOARD S DECISION LACKS A REASONABLE BASIS AND IS ARBITRARY AND CAPRICIOUS INASMUCH AS IT IS CONTRARY TO THE PLAIN LANGUAGE OF THE STATUTE AND THE COMMON MEANING OF COMMON CONTROL This proceeding involves a basic question of statutory construction: whether common control used in the context of a holding company means the relationship between that company and its subsidiaries or just the relationship between or among various corporate siblings, the subsidiaries. IBCX urges, as a matter of corporate law and statutory construction, it is the latter. As a preliminary matter, the Supreme Court ruled in Chrevon U.S.A. v. Natural Res. Def., Council, supra, that where the statutory language is unambiguous as it is here, there is no need to defer to the Board s interpretation. However, this Court has never specifically resolved the applicability of Chevron in connection with Board coverage decisions. See, Interstate Quality Services, Inc. v. Railroad Retirement Board, supra. Nevertheless, the Union Pacific decision, which the Board so carefully wishes to avoid, speaks directly to this issue: [o]n this question of statutory interpretation, the language of the statute itself governs [u]nless otherwise defined, statutory words carry their ordinary, contemporary, and common meaning. See also, Dean v. United States, U.S., 129 S. Ct. 1849, 1853, 2009 LEXIS 3300 (2009) ( This inquiry necessarily begins with the language of the statute). Where, as here, Congress has directly addressed the precise question at issue, that is the end of the matter. It is for the court as well as the agency to give effect to the unambiguously expressed intent of Congress. Chevron U.S.A. v. Natural Res. Def. Council, 467 U.S. 837, 842-2, 104 S. Ct. 2778, 2781 (1984) cited in Interstate Quality Services, Inc. v. Railroad Retirement Board, 83 F.3d at 1465, supra. 19

30 As the Court stated in Union Pacific, The term under common control does not usually apply to two companies in a parent-subsidiary relationship. These words under common control convey a meaning of mutual subordinance to a controlling principal. A company which controls another is not under common control with its subsidiary. Rather two companies most naturally fit within the term under common control when occupying parallel positions as subsidiaries controlled by a common parent. See, e.g., Utah Copper Co. v. Railroad Retirement Bd., 129 F.2d 358, 363 (10th Cir. 1942) cert. denied, 317 U.S. 687, 63 S. Ct. 258, 87 L. Ed. 551 (1942) (carrier and sibling corporation owned by parent company are under common control ). Within the meaning of section 3231(a), the [lower court] was correct: Necessary to a finding of common control is the existence of corporate entities... which are in parallel position, both controlled by a single additional corporate entity, such as subsidiaries owned by a common parent. Union Pacific, 26 Cl. Ct. at 750. And the Federal Circuit continued, The statutory context of the phrase under common control also informs its meaning. The meaning of statutory terms should not render other words and phrases within the statute superfluous. See, e.g., Moskal v. United States, 498 U.S. 103, , 112 L. Ed. 2d 449, 111 S. Ct. 461 (1990); McDonald v. Thompson, 305 U.S. 263, 59 S. Ct. 176, 83 L. Ed. 164 (1938). In the RRTA, the words under common control appear in the context of a larger phrase any company directly or indirectly owned or controlled by one or more such carriers or under common control therewith. The meaning of under common control should not render meaningless other words within this entire phrase. Therefore, the statute should allow situations where corporate entities are under common control without being directly or indirectly owned by a carrier. Otherwise the terms under common control would encompass, and render needless, the rest of the statutory phrase. If the words under common control covered a parent company s relation to its subsidiary, the statute would have no need for the reference to companies directly or indirectly owned or controlled by one or more such carriers. A parent corporation clearly directly or indirectly owns or controls its subsidiaries. A meaning of under common control that encompassed parent-subsidiary corporate relationships would render other language of the 20

31 RRTA impotent. Thus, this principle of statutory construction also counsels that the words under common control do not include parent-subsidiary relationships. The Reconsideration Decision stated as relevant: because Mr. Felix is the owner and President of IBCX and president of the railroads listed in the preceding paragraph, the Board found that IBCX is under common control with those railroads within the meaning of section 1(a)(1)(ii) of the RRA and the corresponding section of the RUIA. Reconsideration Decision at 4; J.A But that s not what the law says. Citing to the dictionary definition of common control, 16 the Court in Union Pacific held, [a] company which controls another is not under common control with the second company. Necessary to a finding of common control is the existence of corporate entities which exercise shared control over each other, or corporate entities which are in parallel position, both controlled by a single additional corporate entity, such as subsidiaries owned by a common parent. A parent company of a wholly-owned subsidiary clearly does not share control with its subsidiaries. The Board attempts to avoid the holding in Union Pacific by resorting to the definitions of control and common control in its regulations to find an alternative basis for treating IBCX as a covered entity. First, it cited to 20 CFR which states: 16 The phrase under common control does not provide a natural description of a parent and its subsidiary because the word common conveys a sense of equality. For example, Webster s New International Dictionary defines common as shared equally or similarly by two or more individuals. Webster s New International Dictionary 539 2d ed. (1951). 21

32 A company or person is controlled by one or more carriers, whenever there exists in one or more such carriers the right or power by any means, method or circumstance, irrespective of stock ownership to direct, either directly or indirectly, the policies and business of such a company or person and in any case in which a carrier is in fact exercising direction of the policies and business of such a company or person. Reconsideration Decision at 5; J.A Then it quoted its regulations at 20 CFR as an additional basis for finding control: Section of the Board s regulations provides that a company or person is under common control with a carrier whenever the control of such company or person is in the same person, persons, or company as that by which such carrier is controlled. Reconsideration Decision at 5; J.A But these are the very same regulations relied upon by the United States in the Union Pacific case for finding control that the Court explicitly and properly rejected. The Court stated as to 20 CFR that these regulations only apply to situations where a company is controlled by a carrier, not vice versa. Regarding 20 CFR 202.5, the Court observed that the definition of common control included in 20 CFR does not, by its terms, address the parent-subsidiary relationship. Rather, 20 CFR establishes common control between sister corporations, namely a carrier and another corporation, both controlled by a parent 17 The Board noted that its regulations promulgated under section 12(l) of the RUIA adopt this definition and that the regulations of the Internal Revenue Service under the RRTA contain a similar definition of control. Reconsideration Decision at 5; J.A

33 corporation. 26 Cl. Ct. 739, These regulations have not been changed since The Board cannot argue that either of the cited regulations applies to IBCX. Since IBCX is neither a carrier nor a company or person controlled by a carrier, 20 CFR does not apply. Furthermore, 20 CFR cannot apply to IBCX because it only applies to relationships involving corporate siblings, not relationships between a parent and a subsidiary. The Board asserts that the basis for its ability to exercise jurisdiction over IBCX is the fact that this entity provides services in connection the transportation of property by railroad. Specifically, the Board states at page one of the Reconsideration Decision: Accordingly, the Board found that IBCX has been performing services in connection with the transportation of passengers or property by railroad for the period 1997 to 2000, when it had an ownership relationship with Evansville Terminal Railway Company, Inc., and then again from 2003 to the present, when it had ownership relationships with [other subsidiary short line railroads] established after 2003, all of which are covered rail carrier employers. J.A But to do so is to misread the statute. As the Court in Union Pacific has clearly noted, a finding of common control missing here is a prerequisite to the second component to finding jurisdiction over an entity. There the Court concluded, [b]ecause the Corporation and the Railroad are not under common control, this court does not reach the question of whether the Corporation performed services in connection with the transportation of passengers or property by railroad. 5 F.3d at

34 At page two of its Reconsideration Decision, the Board even acknowledged that both criteria must be satisfied before it can find an entity covered under the second common control test at section 1(a)(1)(ii): [u]nder section 1(a)(1)(ii), a company is an employer if it meets both of two criteria: [emphasis supplied] if it is owned by or under common control with a rail carrier employer and [emphasis added] if it provides service in connection with railroad transportation. If it fails to meet either condition, it is not a covered employer within section 1(a)(1)(ii). J.A Because no common control exists between IBCX and its subsidiaries, the Board erred in considering whether IBCX provided any services to its subsidiaries let alone finding it provided such services. D. THE BOARD S DECISION LACKS A REASONABLE BASIS AND IS ARBITRARY AND CAPRICIOUS BECAUSE IT IGNORES THE SUBSTANTIAL EVIDENCE OF RECORD Finally, the Board s decision ignores the substantial evidence of record by treating as work for IBCX work that Mr. Felix and Ms. Lainhart performed for the rail carrier subsidiaries as carrier employees paid by such carrier(s) and subject to RRTX. J.A. 37-8, 43, 46-7, 56, and 58. The RRA and the RUIA both provide that an employee may be covered as an individual in the service of an employer for compensation even if the employer is not covered. See, 45 U.S.C. 231(b) and 45 U.S.C. 351(b). Section 1(d) of the RRA, 45 U.S.C. 351(d) further defines an individual as in the service of an employer when: (i) (A) he is subject to the continuing authority of the employer to supervise and direct the manner of rendition of his service, or (B) he is rendering 24

35 professional or technical services and is integrated into the staff of the employer, or (C) he is rendering, on the property used in the employer s operations, personal services the rendition of which is integrated into the employer s operations; and (ii) he renders such service for compensation. 18 Both Mr. Felix and Ms. Lainhart met that test during those portions of the work day that they performed services for IBCX s rail carrier subsidiaries. The Board was in a position to develop a full and accurate record of the work performed and the compensation received by Mr. Felix and Ms. Lainhart by examining correspondence between Mr. Felix and the Board staff in Specifically, William Wolfe, the chief of the Board s Audit and Compliance Division, had contacted Mr. Felix seeking answers information about IBCX s 19 corporate status, ownership, formation, employees, revenues and services, assets, and contracts, among other matters. J.A After IBCX promptly furnished detailed answers, Mr. Wolf requested additional information. J.A Among other matters, he asked whether the subsidiary railroads were owned by Mr. Felix in his individual capacity or by IBCX, sought more detailed information about the services that IBCX provided for these entities, inquired as to the respective percentages of its total revenues that IBCX received from its affiliated railroads 18 Section 1(e) of the RUIA contains a definition of service substantially identical to the above, as do sections 3231(b) and 3231(d) of the RRTA (26 U.S.C. 3231(b) and (d)). 19 The letter referred to IBCX as IBC. 25

36 and unrelated third parties, requested a more detailed explanation as to who employed Ms. Lainhart and Mr. Felix, and asked whether IBCX was owned by or under common control with any other rail carrier. J.A Mr. Felix answered that he and his wife owned IBCX which in turn owned the various railroad subsidiaries. 20 Mr. Felix identified the specific entities that employed both Ms. Lainhart and himself, summarized the services that each provided for the subsidiary railroads, presented payroll information for each carrier with October 2007 as a typical month, and gave a percentage breakdown of compensation for Ms. Lainhart and himself indicating the figures for both IBCX and the subsidiary railroads as a whole. Finally, he confirmed that IBCX was not owned by or under common control with any other railroad. J.A Engaging in results-oriented decision making, the Board found that Mr. Felix and Ms. Lainhart had provided services for the railroad subsidiaries while in the employ of IBCX. Reconsideration Decision at 3, 4, and 6; J.A , and 121. So anxious to find coverage over IBCX as a result of these services and its perception of common control, the Board artfully twisted the facts to reach that conclusion. The Board s analysis of the pertinent facts in the Initial Decision relating to services performed for various entities was limited to a simple sentence: 20 With the exception of Tishomingo Railroad Company, Inc., IBCX owned 100% of the shares of each. IBCX has no involvement in Ohi-Rail Corporation. J.A. 55 and

37 [IBCX] has, however, been involved in the operating or management of short line railroads since 1997 followed by a list of those carriers. Initial Decision at 4; J.A. 29. In response to IBCX s reconsideration petition, the Board expanded its analysis of work performed by Mr. Felix and Ms. Lainhart. Beginning with lengthy references to or quotations from Mr. Felix s affidavit accompanying the reconsideration petition, the Board concluded contrary to the evidence that IBCX, rather than Mr. Felix and his daughter, is providing services to its subsidiaries in the form of management services such as leasing locomotives and maintenance equipment and maintaining a central corporate office. Reconsideration Decision at 7; J.A Despite evidence provided to Mr. Wolfe that IBCX is not under common control with any other railroad, the Board found otherwise. Reconsideration Decision at 7; J.A. at 122. The Board reasoned that if the operation of a building that housed a railroad s administrative offices constituted services in connection with rail transportation citing a case that long predated Union Pacific, 21 then the sort of services that IBCX provided its subsidiaries must be services in connection with the rail transportation of IBCX s rail carrier subsidiaries as well. But there is no evidence that IBCX performed any service for the railroads. There is no management services agreement and no management fee paid to ICBX. The only 21 S. Dev. Co. v. U.S.R.R. Ret. Bd, supra, cited at page 14 27

38 services were provided personally by Mr. Felix and his daughter and were paid for by the railroads. J.A. 37-8, 46-7, and If there is any issue for the Board to legitimately pursue, it might be whether the allocation of compensation between the railroads and the holding company is appropriate, but there is no basis to conclude that the holding company itself was providing services to the railroads. The services that IBCX performs are limited to management (or the sale of) leased railroad equipment, or the provision of railroad consulting services to unaffiliated clients. Most galling was the Board s discussion of the allocation of time that Mr. Felix and Ms. Lainhart allocated as between work for the rail carrier subsidiaries and administrative work by IBCX for those companies. Reconsideration Decision at 4, 7; J.A. 119 and 122. Totally missing from the Board s discussion is recognition of the fact that Mr. Felix and Ms. Lainhart performed the carrierspecific services while acting as carrier employees with their compensation subject to RRTX. Instead, the Board cavalierly stated, [t]he problem with this argument is that Mr. Felix is equating himself with IBCX. Since Mr. Felix s time is divided as described above, he appears to be arguing that the same division of time and compensation be attributed to IBCX. However, this is not a determination that Mr. Felix is an employer under the Acts, but that IBCX is. Reconsideration Decision at 7; J.A In reality, it is the Board who is equating the work performed by Mr. Felix and his daughter and paid for by the railroads with services provided by IBCX. 28

39 IX. CONCLUSION The Board erred in finding IBCX a covered employer by reason of common control with its railroad subsidiaries because there is no common control between these companies under longstanding precedent and the plain meaning of that term. In making that determination, the Board reversed without explanation 20 years of precedent. Absent the existence of any common control, the Board acted arbitrarily and capriciously ruling that services that IBCX provided its subsidiary railroad rendered it covered under the Acts. Finally, in one last ditch effort to find coverage the Board ignored the substantial evidence of record as to the entity for which services were actually rendered by Mr. Felix and Ms. Lainhart. Accordingly, this IBCX respectfully requests this Court to reverse and remand with instructions the Board s Reconsideration Decision dated January 13, Respectfully submitted, /s/ John D. Heffner John D. Heffner Strasburger & Price, LLP 1700 K Street, N.W. Suite 640 Washington, D.C (202) Date: September 26,

40 CERTIFICATE OF COMPLIANCE 1. This brief complies with the type-volume limitation of Fed. R. App. P. 28.1(e)(2) or 32(a)(7)(B) because: [ X ] this brief contains [7,037] words, excluding the parts of the brief exempted by Fed. R. App. P. 32(a)(7)(B)(iii), or [ ] this brief uses a monospaced typeface and contains [state the number of] lines of text, excluding the parts of the brief exempted by Fed. R. App. P. 32(a)(7)(B)(iii). 2. This brief complies with the typeface requirements of Fed. R. App. P. 32(a)(5) and the type style requirements of Fed. R. App. P. 32(a)(6) because: [ X ] this brief has been prepared in a proportionally spaced typeface using [Microsoft Word 2007] in [14pt Times New Roman]; or [ ] this brief has been prepared in a monospaced typeface using [state name and version of word processing program] with [state number of characters per inch and name of type style]. Dated: September 26, 2012 /s/ John D. Heffner John D. Heffner Counsel for Petitioner

41 CERTIFICATE OF FILING AND SERVICE I hereby certify that on this 26th day of September, 2012, I caused this Final Brief of Petitioner to be filed electronically with the Clerk of the Court using the CM/ECF System, which will send notice of such filing to the following registered CM/ECF users: Karl T. Blank Kelli D. Johnson RAILROAD RETIREMENT BOARD OFFICE OF GENERAL COUNSEL 844 North Rush Street Chicago, Illinois (312) Counsel for Respondent Keith T. Brown AMERICAN SHORT LINE AND REGIONAL RAILROAD ASSOCIATION 50 F Street, N.W. Suite 7020 Washington, D.C (202) Ronald A. Lane FLETCHER & SIPPEL LLC 29 North Wacker Drive Suite 920 Chicago, Illinois (312) Counsel for Amicus Curiae

42 I further certify that on this 26th day of September, 2012, I caused the required copies of the Final Brief of Petitioner to be hand filed with the Clerk of the Court. /s/ John D. Heffner John D. Heffner Counsel for Petitioner

43 ADDENDUM

44 TABLE OF CONTENTS Page 45 U.S.C. 231(a)(1)(i) and (ii)... Add U.S.C. 231(b)... Add U.S.C. 231g... Add U.S.C. 351(b) and (d)... Add U.S.C Add CFR Add CFR Add. 6 Administrative Decisions: B.C.D Add. 7 B.C.D Add. 11 B.C.D Add. 21 B.C.D Add. 25 B.C.D Add. 30 B.C.D Add. 38 B.C.D Add. 41 B.C.D Add. 43 B.C.D Add. 48 B.C.D Add. 50 i

45 B.C.D Add. 52 B.C.D Add. 56 B.C.D Add. 59 Case: Mississippi Central Railroad Co. Change in Operators Exemption Tishomingo Railroad Company, Inc.... Add. 63 ii

46 Add. 1

47 Add. 2

48 Add. 3

49 Add. 4

50 Add. 5

51 Add. 6

52 Add. 7

53 Add. 8

54 Add. 9

55 Add. 10

56 Add. 11

57 Add. 12

58 Add. 13

59 Add. 14

60 Add. 15

61 Add. 16

62 Add. 17

63 Add. 18

64 Add. 19

65 Add. 20

66 Add. 21

67 Add. 22

68 Add. 23

69 Add. 24

70 Add. 25

71 Add. 26

72 Add. 27

73 Add. 28

74 Add. 29

75 Add. 30

76 Add. 31

77 Add. 32

78 Add. 33

79 Add. 34

80 Add. 35

81 Add. 36

82 Add. 37

83 Add. 38

84 Add. 39

85 Add. 40

86 Add. 41

87 Add. 42

88 Add. 43

89 Add. 44

90 Add. 45

91 Add. 46

92 Add. 47

93 Add. 48

94 Add. 49

95 Add. 50

96 Add. 51

97 Add. 52

98 Add. 53

99 Add. 54

100 Add. 55

101 Add. 56

102 Add. 57

103 Add. 58

104 Add. 59

105 Add. 60

106 Add. 61

107 Add. 62

108 Add. 63

109 Add. 64

110 Add. 65

ARTICLE/OP-ED PIECE FOR RAILWAY AGE By John D. Heffner, Attorney with Strasburger & Price, LLP

ARTICLE/OP-ED PIECE FOR RAILWAY AGE By John D. Heffner, Attorney with Strasburger & Price, LLP The United States Court of Appeals for the District of Columbia Circuit is currently considering two significant

ARTICLE/OP-ED PIECE FOR RAILWAY AGE By John D. Heffner, Attorney with Strasburger & Price, LLP The United States Court of Appeals for the District of Columbia Circuit is currently considering two significant

United States Court of Appeals for the Federal Circuit

United States Court of Appeals for the Federal Circuit KELLY L. STEPHENSON, Petitioner, v. OFFICE OF PERSONNEL MANAGEMENT, Respondent. 2012-3074 Petition for review of the Merit Systems Protection Board

United States Court of Appeals for the Federal Circuit KELLY L. STEPHENSON, Petitioner, v. OFFICE OF PERSONNEL MANAGEMENT, Respondent. 2012-3074 Petition for review of the Merit Systems Protection Board

UNITED STATES COURT OF APPEALS FOR THE TENTH CIRCUIT ORDER AND JUDGMENT * Before TYMKOVICH, Chief Judge, KELLY and O BRIEN, Circuit Judges.

MARGARET GRAVES, individually and on behalf of all others similarly situated, UNITED STATES COURT OF APPEALS FOR THE TENTH CIRCUIT FILED United States Court of Appeals Tenth Circuit April 21, 2017 Elisabeth

MARGARET GRAVES, individually and on behalf of all others similarly situated, UNITED STATES COURT OF APPEALS FOR THE TENTH CIRCUIT FILED United States Court of Appeals Tenth Circuit April 21, 2017 Elisabeth

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS TEAM MEMBER SUBSIDIARY, L.L.C., Petitioner-Appellant, UNPUBLISHED September 6, 2011 v No. 294169 Livingston Circuit Court LABOR & ECONOMIC GROWTH LC No. 08-023981-AV

STATE OF MICHIGAN COURT OF APPEALS TEAM MEMBER SUBSIDIARY, L.L.C., Petitioner-Appellant, UNPUBLISHED September 6, 2011 v No. 294169 Livingston Circuit Court LABOR & ECONOMIC GROWTH LC No. 08-023981-AV

Case , Document 87-1, 03/11/2015, , Page1 of 10. (Argued: September 29, 2014 Decided: March 11, 2015)

") Case -0, Document -, 0//0, 0, Page of 0-0-ag Stryker v. Securities and Exchange Commission, 0 0 UNITED STATES COURT OF APPEALS FOR THE SECOND CIRCUIT August Term, 0 (Argued: September, 0 Decided: March,

Case -0, Document -, 0//0, 0, Page of 0-0-ag Stryker v. Securities and Exchange Commission, 0 0 UNITED STATES COURT OF APPEALS FOR THE SECOND CIRCUIT August Term, 0 (Argued: September, 0 Decided: March,

ALABAMA COURT OF CIVIL APPEALS

REL: June 15, 2018 Notice: This opinion is subject to formal revision before publication in the advance sheets of Southern Reporter. Readers are requested to notify the Reporter of Decisions, Alabama Appellate

REL: June 15, 2018 Notice: This opinion is subject to formal revision before publication in the advance sheets of Southern Reporter. Readers are requested to notify the Reporter of Decisions, Alabama Appellate

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS HASTINGS MUTUAL INSURANCE COMPANY, Plaintiff-Appellee, FOR PUBLICATION May 16, 2017 9:15 a.m. v No. 331612 Berrien Circuit Court GRANGE INSURANCE COMPANY OF LC No. 14-000258-NF

STATE OF MICHIGAN COURT OF APPEALS HASTINGS MUTUAL INSURANCE COMPANY, Plaintiff-Appellee, FOR PUBLICATION May 16, 2017 9:15 a.m. v No. 331612 Berrien Circuit Court GRANGE INSURANCE COMPANY OF LC No. 14-000258-NF

In the Supreme Court of the United States

No. 12-1408 In the Supreme Court of the United States UNITED STATES OF AMERICA, PETITIONER v. QUALITY STORES, INC., ET AL. ON PETITION FOR A WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR

No. 12-1408 In the Supreme Court of the United States UNITED STATES OF AMERICA, PETITIONER v. QUALITY STORES, INC., ET AL. ON PETITION FOR A WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR

IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT

USCA Case #17-1271 Document #1714908 Filed: 01/26/2018 Page 1 of 16 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT Appalachian Voices, et al., ) Petitioners, ) ) No. 17-1271

USCA Case #17-1271 Document #1714908 Filed: 01/26/2018 Page 1 of 16 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT Appalachian Voices, et al., ) Petitioners, ) ) No. 17-1271

Is a Horse not a Horse When Entities Incur Investment Advisory Fees?

Is a Horse not a Horse When Entities Incur Investment Advisory Fees? Lou Harrison John Janiga Deductions under Section 67 for Investment Expeneses A colleague of mine, John Janiga, of the School of Business

Is a Horse not a Horse When Entities Incur Investment Advisory Fees? Lou Harrison John Janiga Deductions under Section 67 for Investment Expeneses A colleague of mine, John Janiga, of the School of Business

No. 47,320-CA COURT OF APPEAL SECOND CIRCUIT STATE OF LOUISIANA * * * * * Versus * * * * * * * * * *

Judgment rendered September 20, 2012. Application for rehearing may be filed within the delay allowed by Art. 2166, LSA-CCP. No. 47,320-CA COURT OF APPEAL SECOND CIRCUIT STATE OF LOUISIANA * * * * * RHONDA

Judgment rendered September 20, 2012. Application for rehearing may be filed within the delay allowed by Art. 2166, LSA-CCP. No. 47,320-CA COURT OF APPEAL SECOND CIRCUIT STATE OF LOUISIANA * * * * * RHONDA

IN THE COMMONWEALTH COURT OF PENNSYLVANIA

IN THE COMMONWEALTH COURT OF PENNSYLVANIA Allstate Life Insurance Company, : Petitioner : : v. : No. 89 F.R. 1997 : Commonwealth of Pennsylvania, : Argued: December 9, 2009 Respondent : BEFORE: HONORABLE

IN THE COMMONWEALTH COURT OF PENNSYLVANIA Allstate Life Insurance Company, : Petitioner : : v. : No. 89 F.R. 1997 : Commonwealth of Pennsylvania, : Argued: December 9, 2009 Respondent : BEFORE: HONORABLE

UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE BOARD OF PATENT APPEALS AND INTERFERENCES. Ex parte GEORGE R. BORDEN IV

UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE BOARD OF PATENT APPEALS AND INTERFERENCES Ex parte GEORGE R. BORDEN IV Technology Center 2100 Decided: January 7, 2010 Before JAMES T. MOORE and ALLEN

UNITED STATES PATENT AND TRADEMARK OFFICE BEFORE THE BOARD OF PATENT APPEALS AND INTERFERENCES Ex parte GEORGE R. BORDEN IV Technology Center 2100 Decided: January 7, 2010 Before JAMES T. MOORE and ALLEN

UNITED STATES COURT OF APPEALS FOR THE THIRD CIRCUIT. No

Case: 14-1628 Document: 003112320132 Page: 1 Date Filed: 06/08/2016 UNITED STATES COURT OF APPEALS FOR THE THIRD CIRCUIT No. 14-1628 FREEDOM MEDICAL SUPPLY INC, Individually and On Behalf of All Others

Case: 14-1628 Document: 003112320132 Page: 1 Date Filed: 06/08/2016 UNITED STATES COURT OF APPEALS FOR THE THIRD CIRCUIT No. 14-1628 FREEDOM MEDICAL SUPPLY INC, Individually and On Behalf of All Others

United States Court of Appeals for the Federal Circuit CHICAGO MILWAUKEE CORPORATION, Plaintiff-Appellant, THE UNITED STATES,

United States Court of Appeals for the Federal Circuit 96-5113 CHICAGO MILWAUKEE CORPORATION, Plaintiff-Appellant, v. THE UNITED STATES, Defendant-Appellee. Joel J. Africk, Jenner & Block, of Chicago,

United States Court of Appeals for the Federal Circuit 96-5113 CHICAGO MILWAUKEE CORPORATION, Plaintiff-Appellant, v. THE UNITED STATES, Defendant-Appellee. Joel J. Africk, Jenner & Block, of Chicago,

No IN THE Supreme Court of the United States. UNITED STATES OF AMERICA, Respondent.

No. 17-530 IN THE Supreme Court of the United States WISCONSIN CENTRAL, LTD.; GRAND TRUNK WESTERN RAILROAD COMPANY; AND ILLINOIS CENTRAL RAILROAD COMPANY, v. Petitioners, UNITED STATES OF AMERICA, Respondent.

No. 17-530 IN THE Supreme Court of the United States WISCONSIN CENTRAL, LTD.; GRAND TRUNK WESTERN RAILROAD COMPANY; AND ILLINOIS CENTRAL RAILROAD COMPANY, v. Petitioners, UNITED STATES OF AMERICA, Respondent.

UNITED STATES BANKRUPTCY APPELLATE PANEL FOR THE FIRST CIRCUIT

Case: 12-54 Document: 001113832 Page: 1 Date Filed: 11/20/2012 Entry ID: 2173182 No. 12-054 UNITED STATES BANKRUPTCY APPELLATE PANEL FOR THE FIRST CIRCUIT In re LOUIS B. BULLARD, Debtor LOUIS B. BULLARD,

Case: 12-54 Document: 001113832 Page: 1 Date Filed: 11/20/2012 Entry ID: 2173182 No. 12-054 UNITED STATES BANKRUPTCY APPELLATE PANEL FOR THE FIRST CIRCUIT In re LOUIS B. BULLARD, Debtor LOUIS B. BULLARD,

No IN THE UNITED STATES COURT OF APPEALS FOR THE ELEVENTH CIRCUIT KAWA ORTHODONTICS, LLP, Plaintiff-Appellant,

Case: 14-10296 Date Filed: 04/11/2014 Page: 1 of 8 No. 14-10296 IN THE UNITED STATES COURT OF APPEALS FOR THE ELEVENTH CIRCUIT KAWA ORTHODONTICS, LLP, Plaintiff-Appellant, v. SECRETARY, U.S. DEPARTMENT

Case: 14-10296 Date Filed: 04/11/2014 Page: 1 of 8 No. 14-10296 IN THE UNITED STATES COURT OF APPEALS FOR THE ELEVENTH CIRCUIT KAWA ORTHODONTICS, LLP, Plaintiff-Appellant, v. SECRETARY, U.S. DEPARTMENT

IN THE OREGON TAX COURT MAGISTRATE DIVISION Municipal Tax ) ) I. INTRODUCTION

) I. INTRODUCTION") IN THE OREGON TAX COURT MAGISTRATE DIVISION Municipal Tax JOHN A. BOGDANSKI, Plaintiff, v. CITY OF PORTLAND, State of Oregon, Defendant. TC-MD 130075C DECISION OF DISMISSAL I. INTRODUCTION This matter

IN THE OREGON TAX COURT MAGISTRATE DIVISION Municipal Tax JOHN A. BOGDANSKI, Plaintiff, v. CITY OF PORTLAND, State of Oregon, Defendant. TC-MD 130075C DECISION OF DISMISSAL I. INTRODUCTION This matter

Article. By Richard Painter, Douglas Dunham, and Ellen Quackenbos

Article [Ed. Note: The following is taken from the introduction of the upcoming article to be published in volume 20:1 of the Minnesota Journal of International Law] When Courts and Congress Don t Say

Article [Ed. Note: The following is taken from the introduction of the upcoming article to be published in volume 20:1 of the Minnesota Journal of International Law] When Courts and Congress Don t Say

Illinois Official Reports

Illinois Official Reports Appellate Court Village of Westmont v. Illinois Municipal Retirement Fund, 2015 IL App (2d) 141070 Appellate Court Caption THE VILLAGE OF WESTMONT, Plaintiff-Appellant, v. THE

Illinois Official Reports Appellate Court Village of Westmont v. Illinois Municipal Retirement Fund, 2015 IL App (2d) 141070 Appellate Court Caption THE VILLAGE OF WESTMONT, Plaintiff-Appellant, v. THE

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS DAN M. SLEE, Petitioner-Appellee, UNPUBLISHED September 16, 2008 v No. 277890 Washtenaw Circuit Court PUBLIC SCHOOL EMPLOYEES RETIREMENT LC No. 06-001069-AA SYSTEM, Respondent-Appellant.

STATE OF MICHIGAN COURT OF APPEALS DAN M. SLEE, Petitioner-Appellee, UNPUBLISHED September 16, 2008 v No. 277890 Washtenaw Circuit Court PUBLIC SCHOOL EMPLOYEES RETIREMENT LC No. 06-001069-AA SYSTEM, Respondent-Appellant.

IN THE SUPREME COURT OF FLORIDA CASE NO.: SC SERVICE INSURANCE COMPANY, Appellant, vs. OFFICE OF INSURANCE REGULATION AND

IN THE SUPREME COURT OF FLORIDA CASE NO.: SC11-299 SERVICE INSURANCE COMPANY, Appellant, vs. OFFICE OF INSURANCE REGULATION AND THE FINANCIAL SERVICES COMMISSION, Appellees. BRIEF ON JURISDICTION OF APPELLEES

IN THE SUPREME COURT OF FLORIDA CASE NO.: SC11-299 SERVICE INSURANCE COMPANY, Appellant, vs. OFFICE OF INSURANCE REGULATION AND THE FINANCIAL SERVICES COMMISSION, Appellees. BRIEF ON JURISDICTION OF APPELLEES

ARMED SERVICES BOARD OF CONTRACT APPEALS. Appeal of -- ) ) C. Martin Company, Inc. ) ASBCA No ) Under Contract No. N D-0501 )

) C. Martin Company, Inc. ) ASBCA No ) Under Contract No. N D-0501 )") ARMED SERVICES BOARD OF CONTRACT APPEALS Appeal of -- ) ) C. Martin Company, Inc. ) ASBCA No. 54182 ) Under Contract No. N68711-00-D-0501 ) APPEARANCE FOR THE APPELLANT: APPEARANCES FOR THE GOVERNMENT:

ARMED SERVICES BOARD OF CONTRACT APPEALS Appeal of -- ) ) C. Martin Company, Inc. ) ASBCA No. 54182 ) Under Contract No. N68711-00-D-0501 ) APPEARANCE FOR THE APPELLANT: APPEARANCES FOR THE GOVERNMENT:

UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT. Case No CONFEDERATED TRIBES OF THE CHEHALIS RESERVATION, et al.,

Case: 10-35642 08/27/2013 ID: 8758655 DktEntry: 105 Page: 1 of 14 UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT Case No. 10-35642 CONFEDERATED TRIBES OF THE CHEHALIS RESERVATION, et al., Plaintiffs/Appellants,

Case: 10-35642 08/27/2013 ID: 8758655 DktEntry: 105 Page: 1 of 14 UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT Case No. 10-35642 CONFEDERATED TRIBES OF THE CHEHALIS RESERVATION, et al., Plaintiffs/Appellants,

SUPREME COURT OF THE UNITED STATES

Cite as: U. S. (2000) 1 NOTICE: This opinion is subject to formal revision before publication in the preliminary print of the United States Reports. Readers are requested to notify the Reporter of Decisions,

Cite as: U. S. (2000) 1 NOTICE: This opinion is subject to formal revision before publication in the preliminary print of the United States Reports. Readers are requested to notify the Reporter of Decisions,

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS PAUL JOSEPH STUMPO, Petitioner-Appellant, UNPUBLISHED August 4, 2009 v No. 283991 Tax Tribunal MICHIGAN DEPARTMENT OF TREASURY, LC No. 00-331638 Respondent-Appellee.

STATE OF MICHIGAN COURT OF APPEALS PAUL JOSEPH STUMPO, Petitioner-Appellant, UNPUBLISHED August 4, 2009 v No. 283991 Tax Tribunal MICHIGAN DEPARTMENT OF TREASURY, LC No. 00-331638 Respondent-Appellee.

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION U.S. Department of Energy, Portsmouth/Paducah Project Office Docket No. RC08-5- REQUEST FOR REHEARING AND CLARIFICATION OF THE NORTH

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION U.S. Department of Energy, Portsmouth/Paducah Project Office Docket No. RC08-5- REQUEST FOR REHEARING AND CLARIFICATION OF THE NORTH

Case: Document: Filed: 07/03/2012 Page: 1. NOT RECOMMENDED FOR FULL-TEXT PUBLICATION File Name: 12a0709n.06. No.

Case: 11-1806 Document: 006111357179 Filed: 07/03/2012 Page: 1 NOT RECOMMENDED FOR FULL-TEXT PUBLICATION File Name: 12a0709n.06 UNITED STATES COURT OF APPEALS FOR THE SIXTH CIRCUIT MARY K. HARGROW; M.

Case: 11-1806 Document: 006111357179 Filed: 07/03/2012 Page: 1 NOT RECOMMENDED FOR FULL-TEXT PUBLICATION File Name: 12a0709n.06 UNITED STATES COURT OF APPEALS FOR THE SIXTH CIRCUIT MARY K. HARGROW; M.

IN THE UNITED STATES COURT OF APPEALS FOR THE FIFTH CIRCUIT. Plaintiffs-Appellants, Defendants-Appellees.

Case: 17-10238 Document: 00514003289 Page: 1 Date Filed: 05/23/2017 IN THE UNITED STATES COURT OF APPEALS FOR THE FIFTH CIRCUIT CHAMBER OF COMMERCE OF THE UNITED STATES OF AMERICA, et al., Plaintiffs-Appellants,

Case: 17-10238 Document: 00514003289 Page: 1 Date Filed: 05/23/2017 IN THE UNITED STATES COURT OF APPEALS FOR THE FIFTH CIRCUIT CHAMBER OF COMMERCE OF THE UNITED STATES OF AMERICA, et al., Plaintiffs-Appellants,

119 T.C. No. 5 UNITED STATES TAX COURT. JOSEPH M. GREY PUBLIC ACCOUNTANT, P.C., Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent

119 T.C. No. 5 UNITED STATES TAX COURT JOSEPH M. GREY PUBLIC ACCOUNTANT, P.C., Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 4789-00. Filed September 16, 2002. This is an action

119 T.C. No. 5 UNITED STATES TAX COURT JOSEPH M. GREY PUBLIC ACCOUNTANT, P.C., Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 4789-00. Filed September 16, 2002. This is an action

IN THE SUPREME COURT OF MISSISSIPPI CONTINENTAL CASUALTY COMPANY. v. No CA ALLSTATE PROPERTY AND CASUALTY INSURANCE COMPANY

E-Filed Document Sep 11 2017 10:34:38 2016-CA-00359-SCT Pages: 12 IN THE SUPREME COURT OF MISSISSIPPI CONTINENTAL CASUALTY COMPANY APPELLANT v. No. 2016-CA-00359 ALLSTATE PROPERTY AND CASUALTY INSURANCE

E-Filed Document Sep 11 2017 10:34:38 2016-CA-00359-SCT Pages: 12 IN THE SUPREME COURT OF MISSISSIPPI CONTINENTAL CASUALTY COMPANY APPELLANT v. No. 2016-CA-00359 ALLSTATE PROPERTY AND CASUALTY INSURANCE

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS LARRY JEFFREY, Plaintiff/Third-Party Defendant- Appellee, FOR PUBLICATION July 23, 2002 9:10 a.m. v No. 229407 Ionia Circuit Court TITAN INSURANCE COMPANY, LC No. 99-020294-NF

STATE OF MICHIGAN COURT OF APPEALS LARRY JEFFREY, Plaintiff/Third-Party Defendant- Appellee, FOR PUBLICATION July 23, 2002 9:10 a.m. v No. 229407 Ionia Circuit Court TITAN INSURANCE COMPANY, LC No. 99-020294-NF

COMMISSIONER OF INTERNAL REVENUE, PETITIONER v. NADER E. SOLIMAN 506 U.S. 168; 113 S. Ct. 701

CLICK HERE to return to the home page COMMISSIONER OF INTERNAL REVENUE, PETITIONER v. NADER E. SOLIMAN 506 U.S. 168; 113 S. Ct. 701 January 12, 1993 JUDGES: KENNEDY, J., delivered the opinion of the Court,

CLICK HERE to return to the home page COMMISSIONER OF INTERNAL REVENUE, PETITIONER v. NADER E. SOLIMAN 506 U.S. 168; 113 S. Ct. 701 January 12, 1993 JUDGES: KENNEDY, J., delivered the opinion of the Court,

ORAL ARGUMENT HELD APRIL 12, 2016 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT

USCA Case #15-1177 Document #1653244 Filed: 12/28/2016 Page 1 of 5 ORAL ARGUMENT HELD APRIL 12, 2016 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT PHH CORPORATION, PHH MORTGAGE

USCA Case #15-1177 Document #1653244 Filed: 12/28/2016 Page 1 of 5 ORAL ARGUMENT HELD APRIL 12, 2016 IN THE UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT PHH CORPORATION, PHH MORTGAGE

United States Court of Appeals

United States Court of Appeals FOR THE DISTRICT OF COLUMBIA CIRCUIT Argued May 11, 2017 Decided July 25, 2017 No. 16-5255 ALLINA HEALTH SERVICES, DOING BUSINESS AS UNITED HOSPITAL, DOING BUSINESS AS UNITY

United States Court of Appeals FOR THE DISTRICT OF COLUMBIA CIRCUIT Argued May 11, 2017 Decided July 25, 2017 No. 16-5255 ALLINA HEALTH SERVICES, DOING BUSINESS AS UNITED HOSPITAL, DOING BUSINESS AS UNITY

ORAL ARGUMENT NOT YET SCHEDULED Nos , , , ,

USCA Case #13-1280 Document #1504903 Filed: 07/28/2014 Page 1 of 17 ORAL ARGUMENT NOT YET SCHEDULED Nos. 13-1280, 13-1281, 13-1291, 13-1300, 14-1006 IN THE United States Court of Appeals for the District

USCA Case #13-1280 Document #1504903 Filed: 07/28/2014 Page 1 of 17 ORAL ARGUMENT NOT YET SCHEDULED Nos. 13-1280, 13-1281, 13-1291, 13-1300, 14-1006 IN THE United States Court of Appeals for the District

United States Court of Appeals for the Federal Circuit

United States Court of Appeals for the Federal Circuit BONNIE J. RUSICK, Claimant-Appellant, v. SLOAN D. GIBSON, Acting Secretary of Veterans Affairs, Respondent-Appellee. 2013-7105 Appeal from the United

United States Court of Appeals for the Federal Circuit BONNIE J. RUSICK, Claimant-Appellant, v. SLOAN D. GIBSON, Acting Secretary of Veterans Affairs, Respondent-Appellee. 2013-7105 Appeal from the United

ORAL ARGUMENT NOT YET SCHEDULED UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT. Nos and

USCA Case #12-1008 Document #1400702 Filed: 10/19/2012 Page 1 of 22 ORAL ARGUMENT NOT YET SCHEDULED UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT Nos. 12-1008 and 12-1081 TC RAVENSWOOD,

USCA Case #12-1008 Document #1400702 Filed: 10/19/2012 Page 1 of 22 ORAL ARGUMENT NOT YET SCHEDULED UNITED STATES COURT OF APPEALS FOR THE DISTRICT OF COLUMBIA CIRCUIT Nos. 12-1008 and 12-1081 TC RAVENSWOOD,

IN THE DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT

IN THE DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT NOT FINAL UNTIL TIME EXPIRES TO FILE MOTION FOR REHEARING AND DISPOSITION THEREOF IF FILED MERCURY INSURANCE COMPANY OF FLORIDA, Petitioner,

IN THE DISTRICT COURT OF APPEAL OF THE STATE OF FLORIDA FIFTH DISTRICT NOT FINAL UNTIL TIME EXPIRES TO FILE MOTION FOR REHEARING AND DISPOSITION THEREOF IF FILED MERCURY INSURANCE COMPANY OF FLORIDA, Petitioner,

Case No IN THE UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT. TIMOTHY WHITE, ROBERT L. BETTINGER, and MARGARET SCHOENINGER,

Case: 12-17489 09/22/2014 ID: 9248883 DktEntry: 63 Page: 1 of 12 Case No. 12-17489 IN THE UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT TIMOTHY WHITE, ROBERT L. BETTINGER, and MARGARET SCHOENINGER,

Case: 12-17489 09/22/2014 ID: 9248883 DktEntry: 63 Page: 1 of 12 Case No. 12-17489 IN THE UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT TIMOTHY WHITE, ROBERT L. BETTINGER, and MARGARET SCHOENINGER,

Camico Mutual Insurance Co v. Heffler, Radetich & Saitta

2014 Decisions Opinions of the United States Court of Appeals for the Third Circuit 10-10-2014 Camico Mutual Insurance Co v. Heffler, Radetich & Saitta Precedential or Non-Precedential: Non-Precedential

2014 Decisions Opinions of the United States Court of Appeals for the Third Circuit 10-10-2014 Camico Mutual Insurance Co v. Heffler, Radetich & Saitta Precedential or Non-Precedential: Non-Precedential

STATE OF MICHIGAN COURT OF APPEALS

STATE OF MICHIGAN COURT OF APPEALS PROGRESSIVE MICHIGAN INSURANCE COMPANY, UNPUBLISHED June 17, 2003 Plaintiff-Appellee/Cross-Appellant, v No. 237926 Wayne Circuit Court AMERICAN COMMUNITY MUTUAL LC No.

STATE OF MICHIGAN COURT OF APPEALS PROGRESSIVE MICHIGAN INSURANCE COMPANY, UNPUBLISHED June 17, 2003 Plaintiff-Appellee/Cross-Appellant, v No. 237926 Wayne Circuit Court AMERICAN COMMUNITY MUTUAL LC No.

Employee Relations. A Farewell to Yard-Man. Craig C. Martin and Amanda S. Amert

Employee Relations L A W J O U R N A L ERISA Litigation A Farewell to Yard-Man Electronically reprinted from Summer 2015 Craig C. Martin and Amanda S. Amert In January, the U.S. Supreme Court finally did

Employee Relations L A W J O U R N A L ERISA Litigation A Farewell to Yard-Man Electronically reprinted from Summer 2015 Craig C. Martin and Amanda S. Amert In January, the U.S. Supreme Court finally did

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S DAVID GURSKI, Plaintiff-Appellee, FOR PUBLICATION October 17, 2017 9:00 a.m. v No. 332118 Wayne Circuit Court MOTORISTS MUTUAL INSURANCE LC No.

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S DAVID GURSKI, Plaintiff-Appellee, FOR PUBLICATION October 17, 2017 9:00 a.m. v No. 332118 Wayne Circuit Court MOTORISTS MUTUAL INSURANCE LC No.

v No Court of Claims v No Court of Claims v No Court of Claims

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S ALTICOR, INC., Plaintiff-Appellant, FOR PUBLICATION May 22, 2018 9:05 a.m. v No. 337404 Court of Claims DEPARTMENT OF TREASURY, LC No. 17-000011-MT

S T A T E O F M I C H I G A N C O U R T O F A P P E A L S ALTICOR, INC., Plaintiff-Appellant, FOR PUBLICATION May 22, 2018 9:05 a.m. v No. 337404 Court of Claims DEPARTMENT OF TREASURY, LC No. 17-000011-MT

PETITION OF BROTHERHOOD OF LOCOMOTIVE ENGINEERS AND TRAINMEN AND UNITED TRANSPORTATION UNION TO REVOKE EXEMPTIONS

Before the SURFACE TRANSPORTATION BOARD FINANCE DOCKET NO. 35410 ADRIAN & BLISSFIELD RAIL ROAD COMPANY CONTINUANCE IN CONTROL EXEMPTION FINANCE DOCKET NO. 35411 LEASE AND OPERATION EXEMPTION NORFOLK SOUTHERN

Before the SURFACE TRANSPORTATION BOARD FINANCE DOCKET NO. 35410 ADRIAN & BLISSFIELD RAIL ROAD COMPANY CONTINUANCE IN CONTROL EXEMPTION FINANCE DOCKET NO. 35411 LEASE AND OPERATION EXEMPTION NORFOLK SOUTHERN

United States Small Business Administration Office of Hearings and Appeals

Cite as: Size Appeal of Williams Adley & Company -- DC. LLP, SBA No. SIZ-5341 (2012) United States Small Business Administration Office of Hearings and Appeals SIZE APPEAL OF: Williams Adley & Company

Cite as: Size Appeal of Williams Adley & Company -- DC. LLP, SBA No. SIZ-5341 (2012) United States Small Business Administration Office of Hearings and Appeals SIZE APPEAL OF: Williams Adley & Company

IN THE SUPREME COURT OF FLORIDA. Case No. 1D

IN THE SUPREME COURT OF FLORIDA Case No. 1D07-6027 FLORIDA DEPARTMENT OF FINANCIAL SERVICES, AS RECEIVER FOR AMERICAN SUPERIOR INSURANCE COMPANY, INSOLVENT, vs. Petitioner, IMAGINE INSURANCE COMPANY LIMITED

IN THE SUPREME COURT OF FLORIDA Case No. 1D07-6027 FLORIDA DEPARTMENT OF FINANCIAL SERVICES, AS RECEIVER FOR AMERICAN SUPERIOR INSURANCE COMPANY, INSOLVENT, vs. Petitioner, IMAGINE INSURANCE COMPANY LIMITED

United States Court of Appeals

United States Court of Appeals FOR THE EIGHTH CIRCUIT No. 10-1943 GeoVera Specialty Insurance * Company, formerly known as * USF&G Specialty Insurance * Company, * * Appeal from the United States Appellant,

United States Court of Appeals FOR THE EIGHTH CIRCUIT No. 10-1943 GeoVera Specialty Insurance * Company, formerly known as * USF&G Specialty Insurance * Company, * * Appeal from the United States Appellant,

THE UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION

THE UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Inquiry Regarding the Effect of the Tax Cuts ) and Jobs Act on Commission-Jurisdictional ) Docket No. RM18-12-000 Rates ) MOTION

THE UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Inquiry Regarding the Effect of the Tax Cuts ) and Jobs Act on Commission-Jurisdictional ) Docket No. RM18-12-000 Rates ) MOTION

2011 VT 92. No On Appeal from v. Chittenden Family Court. Alan B. Cote October Term, 2010

Cote v. Cote (2010-057) 2011 VT 92 [Filed 12-Aug-2011] NOTICE: This opinion is subject to motions for reargument under V.R.A.P. 40 as well as formal revision before publication in the Vermont Reports.

Cote v. Cote (2010-057) 2011 VT 92 [Filed 12-Aug-2011] NOTICE: This opinion is subject to motions for reargument under V.R.A.P. 40 as well as formal revision before publication in the Vermont Reports.

ARMED SERVICES BOARD OF CONTRACT APPEALS

ARMED SERVICES BOARD OF CONTRACT APPEALS Appeal of -- ) ) Allison Transmission, Inc. ) ) Under Contract No. DAAE07-99-C-N031 ) APPEARANCES FOR THE APPELLANT: APPEARANCES FOR THE GOVERNMENT: ASBCA No. 59204

ARMED SERVICES BOARD OF CONTRACT APPEALS Appeal of -- ) ) Allison Transmission, Inc. ) ) Under Contract No. DAAE07-99-C-N031 ) APPEARANCES FOR THE APPELLANT: APPEARANCES FOR THE GOVERNMENT: ASBCA No. 59204

United States Court of Appeals

In the United States Court of Appeals For the Seventh Circuit No. 06-1719 IN RE: ABC-NACO, INC., and Debtor-Appellee, OFFICIAL COMMITTEE OF UNSECURED CREDITORS OF ABC-NACO, INC., APPEAL OF: Appellee. SOFTMART,

In the United States Court of Appeals For the Seventh Circuit No. 06-1719 IN RE: ABC-NACO, INC., and Debtor-Appellee, OFFICIAL COMMITTEE OF UNSECURED CREDITORS OF ABC-NACO, INC., APPEAL OF: Appellee. SOFTMART,

Katharine B. Gresham (pro hac vice pending) Hearing Date: February 2, 2010

Hearing Date: February 2, 2010") Katharine B. Gresham (pro hac vice pending) Hearing Date: February 2, 2010 Securities and Exchange Commission Hearing Time: 10:00 a.m 100 F Street, N.E. Washington, D.C. 20548 Telephone: (202) 551-5148

Katharine B. Gresham (pro hac vice pending) Hearing Date: February 2, 2010 Securities and Exchange Commission Hearing Time: 10:00 a.m 100 F Street, N.E. Washington, D.C. 20548 Telephone: (202) 551-5148

In the Supreme Court of the United States

No. 16-757 In the Supreme Court of the United States DOMICK NELSON, PETITIONER v. MIDLAND CREDIT MANAGEMENT, INC. ON PETITION FOR A WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE EIGHTH

No. 16-757 In the Supreme Court of the United States DOMICK NELSON, PETITIONER v. MIDLAND CREDIT MANAGEMENT, INC. ON PETITION FOR A WRIT OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE EIGHTH