Governor s 2018 Tax Proposals Tax Bill (H.F.4385/S.F.3982) and MinnesotaCare Tax Extension

|

|

|

- Aldous Higgins

- 6 years ago

- Views:

Transcription

1 Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue April 16, 2018 Governor s 2018 Tax Proposals Tax Bill (H.F.4385/S.F.3982) and MinnesotaCare Tax Extension The Governor s 2018 Budget proposes the following tax law changes: Governor s Tax Bill Income Tax -- Personal o Start tax calculations with Federal Adjusted Gross Income rather than Federal Taxable Income. Minnesota will maintain the standard deduction, itemized deductions, and personal and dependent exemptions from prior law. Those claiming the increased federal standard deduction will now be able to claim Minnesota s itemized deductions. o Increase Working Family Credit the rates and thresholds, increase the credit for those with three or more children, and other changes. o Create a new $60 credit for each person on the return. The nonrefundable credit will phase out at higher incomes. o Maintain the itemized deduction for mortgage insurance premiums and the deduction for higher education tuition and fees. Estate Tax: Maintain the exclusion at $2.4 million rather than allowing it to rise to $3 million. Sales Tax: Limit the existing sales tax exemptions for data centers. Cigarette and Tobacco Taxes: Restore indexing of the cigarette tax rate for inflation and the prior-law tax rates on premium cigars. Property Taxes: Restore indexing of the state property tax levy for inflation. Taxes on Business (Corporate and Non-corporate): o Conform to most federal tax changes in the definition of the income. Fully conform to Section 179 expensing. o Five Minnesota-specific provisions that expand the corporate tax base. MinnesotaCare Tax Extension Bill Repeal the sunset of the MinnesotaCare provider taxes, permanently maintaining the tax at its current 2% rate beyond December 31, These tax law changes would modify the burden of state and local taxes compared to what it would be under current law. The budget s impact can be estimated using the database and underlying models developed for the Minnesota Tax Incidence Study. Because the latest study projects income and taxes to calendar year 2019, this analysis generally estimates the impact of law changes in that calendar year. That study s baseline projections of tax burdens to 2019 are reduced by $280 million to account for the state and local tax cuts enacted in It is also adjusted to include the state impact of federal law changes that were included in the February forecast, which increased the resident tax burden by an estimated $96 million.

2 The analysis is limited to permanent changes in tax law. Law changes that are phased in over several years (such as the estate tax) or have a delayed effective date are modeled as if fully effective in Because the MinnesotaCare provider taxes were in effect in calendar year 2019, they were included in the Tax Incidence Study s 2019 baseline tax burdens. To provide clarity, this analysis refers to current 2019 law with MinnesotaCare provider taxes and current 2019 law without MinnesotaCare provider taxes. Impact of Proposals on Minnesota State & Local Tax Burdens on Minnesota Residents GOVERNOR S TAX BILL: The mix of tax cuts and tax increases in the Governor s Tax Bill increases the net tax burden on Minnesota residents by $91.5 million. Income Tax Changes (nonbusiness): Proposed changes in income tax provisions would reduce tax revenue by $324.3 million, reducing the tax burden on Minnesota residents by $318.5 million. The new nonrefundable $60 credit for each taxpayer and dependent reduces resident tax liability by $233.1 million. The expansion of the Working Family Credit reduces resident tax by an additional $49.7 million. Deductions for mortgage insurance and higher education tuition and fees reduce resident tax by $7.6 and $2.3 million respectively. The increase in the federal standard deduction reduces the number of taxpayers who will itemize deductions. Under current Minnesota law, those who claim the standard deduction on their federal return cannot itemize deductions on their Minnesota return. The automatic state tax impact of the federal law change was included in the February forecast (raising state revenue). The Governor s bill will undo this tax increase, reducing Minnesota tax by $25.7 million. The impact of each of these provisions is modeled using the House Income Tax Simulation (HITS) Model for tax year Income Tax Changes on Non-Corporate Businesses (sole proprietors, S-corps, and partnerships): Conforming to most of the changes to the federal tax base will raise taxes on non-corporate business income by $176.8 million, and $161.9 million will be borne by Minnesota residents. Corporate Tax Changes: The burden of the estimated $231.1 million increase in corporate tax is modeled using the corporate tax incidence model. After full adjustment, some of the burden would be borne in higher prices, some in lower wages, and some in lower returns to business owners. Tax burdens for Minnesota residents would rise by an estimated $166.4 million (about 72% of added revenue). The remainder would be borne by nonresidents or the federal government (in lower federal corporate tax revenue). These estimates apply to the long-term burden, after businesses have fully adjusted to the change in tax burdens. 2

3 Property Tax Changes: State property taxes on business property and seasonal recreational property will rise by $21.9 million. The net impact on Minnesota residents is estimated to be $11.2 million. In addition, homeowner property tax refunds will increase, reducing resident tax burdens by $1.1 million. Sales and Excise Tax Changes: Sales taxes on business purchases will rise by $37.9 million, increasing the tax burden on Minnesota residents by $35.5 million. Cigarette and tobacco taxes will rise by $9.6 million, with $9.3 million falling on Minnesota residents. Estate Tax Changes: Taxes on estates will rise by $27.1 million, increasing the tax burden on Minnesota estates by $25.6 million. GOVERNOR S MINNESOTACARE TAX EXTENSION BILL: The full-year impact of the 2% provider taxes in calendar year 2019 is forecast to be $692.1 million, of which $634.5 million is borne by Minnesota residents. Because this tax is still in effect in 2019, the impact of the increase can be shown only by removing the tax from 2019 tax burdens. Even though the repeal of the sunset extends an existing 2019 tax, the baseline 2019 tax is shown as Tax without MinnesotaCare Tax. Law Changes Not Included in this Analysis Temporary changes to the Angel Investment Credit and conformity to several small federal changes. Timing changes to the Historic Preservation Credit and in Minnesota s response to federal changes in bonus depreciation. A small change to the gross premiums tax (less than $0.5 million). Results by Population Decile: Change in Minnesota State and Local Tax Burdens Table 1 shows the effective tax rates in 2019 for each of three tax systems: A: without MnCare Tax. The 2019 tax burdens published in the Tax Incidence Study are adjusted for (1) law changes enacted in 2017 (which reduced the total burden by $184 million) and (2) the impact of the impending sunset of the MinnesotaCare provider taxes. These adjustments make the overall tax system less regressive, the Suits Index rising from what was shown in the Tax Incidence Study (at ) to B: with MnCare Tax. C: with MnCare Tax and the Tax Bill. 3

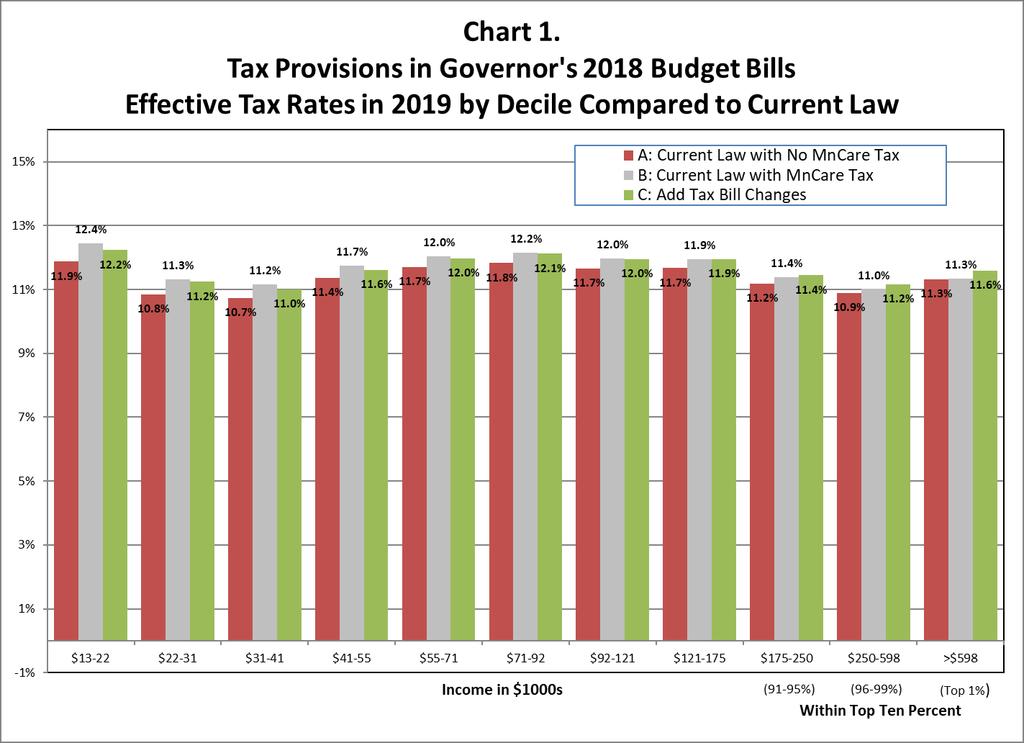

4 2019 Population Decile Income Range Percent of All Households Chart 1. Impact of Governor's Proposed Tax Changes in 2018 Budget Bills (A) (B) (B - A) (B) (C ) (C - B) (A) (C ) C-A without Human Services Bill Alone Tax Bill Alone Both Bills Together with Minnesota State and Local Tax Burden as Percent of Income Change with Tax Bill Plus with Change without Tax Bill Plus with 1 13,418 & under 10% 25.0% 25.8% 0.85% 25.8% 25.6% -0.26% 25.0% 25.6% 0.59% 2 13,419 to 21,894 10% 11.9% 12.4% 0.57% 12.4% 12.2% -0.21% 11.9% 12.2% 0.36% 3 21,895 to 31,391 10% 10.8% 11.3% 0.48% 11.3% 11.2% -0.08% 10.8% 11.2% 0.40% 4 31,392 to 41,344 10% 10.7% 11.2% 0.43% 11.2% 11.0% -0.16% 10.7% 11.0% 0.27% 5 41,345 to 55,093 10% 11.4% 11.7% 0.39% 11.7% 11.6% -0.14% 11.4% 11.6% 0.25% 6 55,094 to 70,943 10% 11.7% 12.0% 0.34% 12.0% 12.0% -0.07% 11.7% 12.0% 0.27% 7 70,944 to 92,150 10% 11.8% 12.2% 0.33% 12.2% 12.1% -0.04% 11.8% 12.1% 0.29% 8 92,151 to 121,494 10% 11.7% 12.0% 0.32% 12.0% 12.0% -0.02% 11.7% 12.0% 0.30% 9 121,495 to 174,624 10% 11.7% 11.9% 0.27% 11.9% 11.9% 0.00% 11.7% 11.9% 0.28% ,625 & over 10% 11.1% 11.2% 0.11% 11.2% 11.4% 0.16% 11.1% 11.4% 0.27% All Households 100% 11.5% 11.7% 0.25% 11.7% 11.8% 0.04% 11.5% 11.8% 0.28% Detail for the 10th Decile Lower Half 174,625 to 250,362 5% 11.2% 11.4% 0.21% 11.4% 11.4% 0.05% 11.2% 11.4% 0.26% Next 4% 250,363 to 598,214 4% 10.9% 11.0% 0.12% 11.0% 11.2% 0.15% 10.9% 11.2% 0.27% Top 1% 598,215 & over 1% 11.3% 11.3% 0.03% 11.3% 11.6% 0.25% 11.3% 11.6% 0.28% Full Decile 174,625 & over 10% 11.1% 11.4% 0.11% 11.4% 11.6% 0.16% 11.1% 11.4% 0.27% Change Tax Incidence Study (A) (B) (B - A) (B) (C ) (C - B) (A) (C ) (C - A) Total Tax Burden ($millions) $30,172 $29,353 $29,988 $635 $29,988 $30,079 $92 $29,353 $30,079 $726 Suits Index * *Generally Suits Indexes are between (most regressive) to (most progressive). However, the Suits Index for changes in tax can sometimes lie outside that range if taxes increase for high income households and decrease for low-income households (as in this case), or visa versa. The Suits Index of in this case reflects the increased tax burden in the 10th decile and decreased burden in the lower deciles. The tax change is highly progressive. 4

5 The Governor s MinnesotaCare Tax Extension Bill changes the tax burden from A to B. The tax burden rises by $635 million, with increases in all deciles. The effective tax rates rise by more in the lower deciles and less in the higher deciles. All deciles except the top decile see the effective tax rates rising by more than the average for all households (0.25%). The Suits Index for the provider tax increase is (quite regressive). It makes the tax system more regressive, raising the tax system Suits Index from to The Governor s Tax Bill changes the burden from B to C. The bill increases the overall tax burden by $92 million, raising the effective tax rate for all households combined by 0.04%. The changes by decile are much larger. The effective tax rate rises by 0.16% in the top decile. It falls for all other deciles, with reductions of 0.10% or more in 4 of the bottom 5 deciles. The bill is highly progressive, with a Suits Index of It raises the tax system Suits Index from to The Governor s bills combined would result in a tax system that has an overall effective tax rate that is 0.04% higher than B (current 2019 law with the MinnesotaCare tax), but the resulting tax system would be just slightly more regressive than A (current 2019 law in the absence of the MinnesotaCare tax). The progressivity of the Tax Bill offsets almost all of the regressivity of the extended MinnesotaCare provider tax. Compared to the 2019 law in effect at the time the Tax Incidence Study was completed, the overall effective tax rate would fall from 11.82% to 11.78% and the tax system Suits Index would rise from to Chart 1 shows the effective tax rates for deciles 2 through 10 under tax systems A, B, and C. The Governor s MinnesotaCare Tax Extension Bill is reflected by the difference between the heights of the first and second bars. The Governor s Tax Bill s impact is the difference between the second and third bar. See note at the bottom of Table 1. 5

6 6

7 Table 2 and Chart 2 show the tax changes by tax type. Table 3 provides more detail of the overall impact of proposals, in the same manner as shown on Table 3-1 in the Tax Incidence Study for all current-law taxes. (See page 44 of that report.) 2019 Population Decile Percent of All Percent of All Property Tax Net of PTR Sales and Excise Taxes MnCare Provider Taxes Percent of Total Change in Income Range Households Income Income Tax Corporate Tax Estate Tax Total Tax Burden 1 $13,418 & under 10% 0.9% ($12,753) $4,414 $263 $2,104 $261 $18,884 $13, % 2 13,419 to 21,894 10% 1.9% (19,216) 5, , ,048 17, % 3 21,895 to 31,391 10% 2.9% (16,845) 7, , ,604 29, % 4 31,392 to 41,344 10% 4.0% (28,430) 8, , ,599 27, % 5 41,345 to 55,093 10% 5.3% (34,140) 10, , ,425 33, % 6 55,094 to 70,943 10% 6.8% (30,508) 12, , ,727 47, % 7 70,944 to 92,150 10% 8.8% (32,371) 16,296 1,159 4,429 1,383 75,148 66, % 8 92,151 to 121,494 10% 11.5% (35,769) 20,505 1,476 5,226 2,789 92,656 86, % 9 121,495 to 174,624 10% 15.7% (37,553) 27,286 1,945 6,500 3, , , % ,625 & over 10% 42.2% 91,051 51,991 4,008 11,456 15, , , % ALL MINNESOTA HOUSEHOLDS Table 2. Change in Minnesota State and Local Tax Burden by Tax Type Impact of Tax Proposals in Governor's 2018 Budget Bills Estimated Calendar Year 2019 Impact, by Tax Type Dollars in $1000s Change in Tax Burden 100% 100.0% ($156,534) $166,351 $11,236 $44,839 $25,637 $634,503 $726, % Detail for the 10th Decile Lower Half $174,625 to 250,362 5% 11.1% ($13,906) $18,141 $1,254 $4,125 $4,288 $60,048 $73, % Next 4% 250,363 to 598,214 4% 15.4% 25,184 21,157 1,531 4,655 6,806 48, , % Top 1% 598,215 & over 1% 15.6% 79,773 12,694 1,224 2,676 4,296 11, , % Full Decile $174,625 & over 10% 42.2% $91,051 $51,991 $4,008 $11,456 $15,389 $119, , % 7

8 Table 3. Impact of Tax Proposals in Governor's 2019 Budget Bills on State and Local Tax Collections and Tax Burdens (Calendar Year 2019) All dollars in millions All dollar values rounded to nearest million dollars. All values that are truly zero are shown as blanks. Suits Index Change in As Imposed After Shifting for Tax Change* Tax Type Collections MN HH's NR Business Minnesota Exported (Full Sample) State Taxes Taxes on Income and Estates Individual income tax ** Corporate franchise tax Estate tax Total Income and Estate Taxes ** Taxes on Consumption Total sales tax General sales tax Sales tax on motor vehicles Motor fuels excise tax Alcoholic beverage excise taxes Cigarette and tobacco excise taxes Insurance premiums taxes Gambling taxes MinnesotaCare taxes Solid waste management taxes Total Consumption Taxes Taxes on Property State property tax Residential recreational property Commercial Industrial Utility Motor vehicle registration tax Mortgage and deed taxes Total Property Taxes Property Tax Refunds Homeowners Renters Total Property Tax Refunds Total State Taxes Local Taxes Property Taxes General Property Tax Homeowners (before PTR) Residential recreational property Commercial Industrial Farm (other than residence) Rental Housing Utility Mining Production Taxes (taconite) Taxes on Consumption Local Sales Taxes Local Gross Earnings Taxes Total Local Taxes Total State and Local Taxes Parts may not sum to totals due to rounding. * Suits indexes for a reduction in regressive taxes (such as the general sales tax) are shown as positive because the tax cut makes the system less regressive. **The net tax change in these cases is very progressive, with tax reductions in deciles 1 through 9 but sizable tax increases in decile 10. As a result, the calculated Suits Index exceeds

9 Appendix 1: Technical Notes A. Assumptions about Changes in Local Property Taxes Local government levies will change in response to changes in state aids and credits. Standard assumptions are used by the Property Tax Division to estimate the magnitude of those changes. (Note: There were no changes in local government levies associated with the Governor s 2018 proposals.) B. Estimating the Incidence of Changes in Business Taxes ( Incremental Incidence ) As explained on pages of the 2017 Tax Incidence Study, the incidence of a change in the level of business taxes ( incremental incidence ) will differ from the incidence of existing business taxes ( average incidence ). Average incidence divides an existing business tax into three parts the national average tax on all capital, the sector differential, and the Minnesota differential. In contrast, a change in the level of a business tax is all treated as a change in the Minnesota differential. If the level of Minnesota business taxes changes, this will generally change the amount of federal tax paid by the business either the federal corporate income tax or the federal individual income tax (for flow-through businesses). For a corporation paying federal tax at the 21% rate, each additional $1000 in Minnesota tax will reduce the federal tax burden by $210. So $210 of the $1000 of Minnesota tax burden is borne by the federal government in foregone tax revenue. The burden of the remaining $790 in tax may be shifted to consumers in higher prices or to workers in lower compensation or it may reduce the after-tax income of the business owner. This analysis assumes federal tax rates of 21% for corporate tax and 17% for individual income tax. The extent to which the tax burden will be shifted to consumers or workers will depend on the nature of the market. Minnesota tax changes are most likely to result in price changes if the market is local and close competitors face the same change in tax. Businesses selling in national or international markets are much less likely to shift the added cost to consumers by raising prices (or reduce their price in response to a tax cut). As in the incidence study, the incidence results assume the market has had time to fully adjust to any tax changes. The incidence of the business tax changes in the bill (as modeled here) is as follows: o Corporate tax increases: 38% shifted to Minnesota consumers, 34% shifted to Minnesota workers, less than 1% borne by Minnesota owners, and 27% borne by nonresidents and the federal government. o Business property tax increases for nonresidential property: 32% of the benefits to Minnesota consumers, 14% to Minnesota workers, 6% to Minnesota owners, and 51% to nonresidents and the federal government. o Individual income tax increases on flow-through income: The burden is assumed to fall on the recipient of the income, as modeled using the House Income Tax Simulation (HITS) Model. 9

Governor s Supplemental Budget Tax Proposals Tax and Transportation Bills

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue May 9, 2017 (REVISED) Governor s Supplemental Budget Tax Proposals Tax and Transportation Bills Including Modifications

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue May 9, 2017 (REVISED) Governor s Supplemental Budget Tax Proposals Tax and Transportation Bills Including Modifications

Laws 2018, Chapter 205 (H.F. 947, 1 st Engrossment) Vetoed Omnibus Tax Bill

Vetoed Omnibus Tax Bill") Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue August 30, 2018 Laws 2018, Chapter 205 (H.F. 947, 1 st Engrossment) Vetoed Omnibus Tax Bill The bill, which

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue August 30, 2018 Laws 2018, Chapter 205 (H.F. 947, 1 st Engrossment) Vetoed Omnibus Tax Bill The bill, which

GOVERNOR S Supplemental Budget Tax Proposals

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue REVISED May 11, 2013 GOVERNOR S Supplemental Budget Tax Proposals HF 677 (Lenczewski) and SF 552 (Skoe) As

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue REVISED May 11, 2013 GOVERNOR S Supplemental Budget Tax Proposals HF 677 (Lenczewski) and SF 552 (Skoe) As

2013 Omnibus Tax Bill

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue June 24, 2013 2013 Omnibus Tax Bill Chapter 143 (H.F. 677 as enacted on May 23, 2013) The 2013 Omnibus Tax

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue June 24, 2013 2013 Omnibus Tax Bill Chapter 143 (H.F. 677 as enacted on May 23, 2013) The 2013 Omnibus Tax

Tax Incidence Analysis First & Second Omnibus Tax Bills

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue June 18, 2014 2014 First & Second Omnibus Tax Bills Chapter 150 (H.F. 1777 as enacted on March 21, 2014) and

Tax Incidence Analysis Prepared by the Tax Research Division, Minnesota Department of Revenue June 18, 2014 2014 First & Second Omnibus Tax Bills Chapter 150 (H.F. 1777 as enacted on March 21, 2014) and

2003 Minnesota Tax Incidence Study

2003 Minnesota Tax Incidence Study (Revised using February 2003 Forecast) An analysis of Minnesota s household and business taxes. March 2003 2003 Minnesota Tax Incidence Study Analysis of Minnesota s

2003 Minnesota Tax Incidence Study (Revised using February 2003 Forecast) An analysis of Minnesota s household and business taxes. March 2003 2003 Minnesota Tax Incidence Study Analysis of Minnesota s

2009 Minnesota Tax Incidence Study

2009 Minnesota Tax Incidence Study (Using November 2008 Forecast) An analysis of Minnesota s household and business taxes. March 2009 For document links go to: Table of Contents 2009 Minnesota Tax Incidence

2009 Minnesota Tax Incidence Study (Using November 2008 Forecast) An analysis of Minnesota s household and business taxes. March 2009 For document links go to: Table of Contents 2009 Minnesota Tax Incidence

2011 Minnesota Tax Incidence Study

2011 Minnesota Tax Incidence Study (Using February 2011 Forecast) An analysis of Minnesota s household and business taxes. March 2011 For document links go to: Table of Contents 2011 Minnesota Tax Incidence

2011 Minnesota Tax Incidence Study (Using February 2011 Forecast) An analysis of Minnesota s household and business taxes. March 2011 For document links go to: Table of Contents 2011 Minnesota Tax Incidence

2007 Minnesota Tax Incidence Study

2007 Minnesota Tax Incidence Study (Using November 2006 Forecast) An analysis of Minnesota s household and business taxes. March 2007 2007 Minnesota Tax Incidence Study Analysis of Minnesota s household

2007 Minnesota Tax Incidence Study (Using November 2006 Forecast) An analysis of Minnesota s household and business taxes. March 2007 2007 Minnesota Tax Incidence Study Analysis of Minnesota s household

2013 Minnesota Tax Incidence Study

Revised April 24, 2013 to correct errors for taxes projected to 2015. Changes were made to each of the following: Executive Summary Chapter 1 Chapter 3 Tables 4-3, 4-4, and 4-5. Please discard earlier

Revised April 24, 2013 to correct errors for taxes projected to 2015. Changes were made to each of the following: Executive Summary Chapter 1 Chapter 3 Tables 4-3, 4-4, and 4-5. Please discard earlier

VIEWPOINT state tax notes

Multi-Tax Incidence Analysis In a Microsimulation Environment by Eric Cook Eric Cook began his career as a revenue estimator with Congress s Joint Committee on Taxation in 1983. He joined PwC in 1987,

Multi-Tax Incidence Analysis In a Microsimulation Environment by Eric Cook Eric Cook began his career as a revenue estimator with Congress s Joint Committee on Taxation in 1983. He joined PwC in 1987,

2013 Supplement to the Minnesota Tax Handbook

2013 Supplement to the Minnesota Tax Handbook This supplement to the 2012 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2013. The page references are to the 2012 Edition.

2013 Supplement to the Minnesota Tax Handbook This supplement to the 2012 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2013. The page references are to the 2012 Edition.

2017 Supplement to the Minnesota Tax Handbook

2017 Supplement to the Minnesota Tax Handbook This supplement to the 2016 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2017. The page references are to the 2016 Edition.

2017 Supplement to the Minnesota Tax Handbook This supplement to the 2016 Edition of the Minnesota Tax Handbook contains the major tax law changes enacted in 2017. The page references are to the 2016 Edition.

Governor s Tax Bill. March 4, 2005

Governor s Tax Bill March 4, 2005 Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie) Analysis Revised for Updated Estimates and February 2005 Forecast Separate Official Fiscal Note

Governor s Tax Bill March 4, 2005 Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie) Analysis Revised for Updated Estimates and February 2005 Forecast Separate Official Fiscal Note

DOR Administrative Costs/Savings Department of Revenue Analysis of H.F (Drazkowski) As Proposed to be Amended (H2716A1 & H2716A2)

As Proposed to be Amended (H2716A1 & H2716A2)") Fair Tax to Replace Income, Sales, and Excise Taxes March 14, 2018 DOR Administrative Costs/Savings Department of Revenue Yes X No Fund Impact F.Y. 2018 F.Y. 2019 F.Y. 2020 F.Y. 2021 (000 s) Individual

Fair Tax to Replace Income, Sales, and Excise Taxes March 14, 2018 DOR Administrative Costs/Savings Department of Revenue Yes X No Fund Impact F.Y. 2018 F.Y. 2019 F.Y. 2020 F.Y. 2021 (000 s) Individual

1999 Minnesota Tax Incidence Study

1999 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1999 MINNESOTA Department of Revenue Tax Research Division Mail Station 2230, St. Paul, MN 55146-2230 (612) 296-3425

1999 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1999 MINNESOTA Department of Revenue Tax Research Division Mail Station 2230, St. Paul, MN 55146-2230 (612) 296-3425

1995 Minnesota Tax Incidence Study

1995 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1995 MINNESOTA Department of Revenue Tax Research Division MINNESOTA Department of Revenue March 1, 1995 To

1995 Minnesota Tax Incidence Study Who pays Minnesota s household and business taxes? March 1995 MINNESOTA Department of Revenue Tax Research Division MINNESOTA Department of Revenue March 1, 1995 To

Corporate Franchise Tax Highway Fuels Excise Tax Deed Transfer Tax Airflight Property Tax

ISSUE BRIEF Tax expenditures The 2010 Tax Expenditure Budget by the Minnesota Department of Revenue (DOR) defines tax expenditure as statutory provisions which reduce the amount of revenue that would otherwise

ISSUE BRIEF Tax expenditures The 2010 Tax Expenditure Budget by the Minnesota Department of Revenue (DOR) defines tax expenditure as statutory provisions which reduce the amount of revenue that would otherwise

Department of Revenue Analysis of S.F. 726 (Chamberlain) As Proposed to be Amended (A )

As Proposed to be Amended (A )") February 7, 2017 Governor s Tax Bill State Taxes Only See Separate Analysis of Property Tax Provisions DOR Administrative Costs/Savings Yes X No Department of Revenue Fund Impact F.Y. 2017 F.Y. 2018 F.Y.

February 7, 2017 Governor s Tax Bill State Taxes Only See Separate Analysis of Property Tax Provisions DOR Administrative Costs/Savings Yes X No Department of Revenue Fund Impact F.Y. 2017 F.Y. 2018 F.Y.

House Taxes Committee. 3/11/2019 One Minnesota revenue.state.mn.us 1

House Taxes Committee 3/11/2019 One Minnesota revenue.state.mn.us 1 Mission/Vision/Values Mission Working together to fund Minnesota s future. Vision Everyone reports, pays, and receives the right amount:

House Taxes Committee 3/11/2019 One Minnesota revenue.state.mn.us 1 Mission/Vision/Values Mission Working together to fund Minnesota s future. Vision Everyone reports, pays, and receives the right amount:

Tax Exemptions & Tax Incidence. A Biennial Report Produced by The Texas Comptroller of Public Accounts

Tax Exemptions & Tax Incidence A Biennial Report Produced by The Texas Comptroller of Public Accounts Presentation by Curtis Toews curtis.toews@cpa.state.tx.us Revenue Estimating Conference Federal of

Tax Exemptions & Tax Incidence A Biennial Report Produced by The Texas Comptroller of Public Accounts Presentation by Curtis Toews curtis.toews@cpa.state.tx.us Revenue Estimating Conference Federal of

Minnesota Biennial Budget

Minnesota Biennial Budget FY 2012 2013 2012 2013 State Taxes and Local Aids and Credits Governor's Budget February 15, 2011 Departm ental Earnings STATE TAXES AND LOCAL AIDS AND CREDITS TABLE OF CONTENTS

Minnesota Biennial Budget FY 2012 2013 2012 2013 State Taxes and Local Aids and Credits Governor's Budget February 15, 2011 Departm ental Earnings STATE TAXES AND LOCAL AIDS AND CREDITS TABLE OF CONTENTS

General Fund Total $761,594 $633,812 $645,863 $657,068. Minnesota Future Resources Fund ($1,022) ($1,055) ($1,001) ($949)

($1,055) ($1,001) ($949)") May 2, 2003 Department of Revenue Analysis of S.F. 1504 (Hottinger), As Amended (A-1) April 30, 2003 Individual Income Tax Corporate Franchise Tax Cigarette and Tobacco Taxes, Others Separate Official

May 2, 2003 Department of Revenue Analysis of S.F. 1504 (Hottinger), As Amended (A-1) April 30, 2003 Individual Income Tax Corporate Franchise Tax Cigarette and Tobacco Taxes, Others Separate Official

Department of Revenue Analysis of S.F (Pogemiller) Revenue Gain or (Loss) F.Y F.Y F.Y F.Y (000 s)

Revenue Gain or (Loss) F.Y F.Y F.Y F.Y (000 s)") Governor's Tax Proposal February 4, 2002 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No X Department of Revenue Analysis of S.F. 3000 (Pogemiller) Revenue

Governor's Tax Proposal February 4, 2002 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No X Department of Revenue Analysis of S.F. 3000 (Pogemiller) Revenue

Supplement Budget Items, Errata and Omissions to the Governor's Biennial Budget - Change Order #2

State of Minnesota Department of Finance 400 Centennial Building 658 Cedar Street St. Paul, Minnesota 55155 Voice: (612) 296-5900 TTY/fDD: (612) 297-5353 or Greater Minnesota 800-627-3529 and ask for 296-5900

State of Minnesota Department of Finance 400 Centennial Building 658 Cedar Street St. Paul, Minnesota 55155 Voice: (612) 296-5900 TTY/fDD: (612) 297-5353 or Greater Minnesota 800-627-3529 and ask for 296-5900

F.Y F.Y F.Y F.Y.

April 16, 2018 State Taxes Only See Separate Analysis for Property Tax Provisions Governor s Tax Bill State Tax Provisions Only DOR Administrative Costs/Savings Yes X No Department of Revenue Fund Impact

April 16, 2018 State Taxes Only See Separate Analysis for Property Tax Provisions Governor s Tax Bill State Tax Provisions Only DOR Administrative Costs/Savings Yes X No Department of Revenue Fund Impact

Notes and Definitions Numbers in the text, tables, and figures may not add up to totals because of rounding. Dollar amounts are generally rounded to t

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2011 Percent 70 60 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2011 Percent 70 60 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Overview of Income, Corporate Franchise, Sales and Other State Taxes

Overview of Income, Corporate Franchise, Sales and Other State Taxes A Presentation to the House Committee on Taxes January 15, 2013 by Andrew Biggerstaff Nina Manzi Joel Michael Pat Dalton Research Department

Overview of Income, Corporate Franchise, Sales and Other State Taxes A Presentation to the House Committee on Taxes January 15, 2013 by Andrew Biggerstaff Nina Manzi Joel Michael Pat Dalton Research Department

Wisconsin Tax Incidence Study: An Overview of Methodology

Wisconsin Tax Incidence Study: An Overview of Methodology by Rebecca Boldt Division of Research and Policy Wisconsin Department of Revenue rboldt@dor.state.wi.us FTA Conference of Revenue Estimating &

Wisconsin Tax Incidence Study: An Overview of Methodology by Rebecca Boldt Division of Research and Policy Wisconsin Department of Revenue rboldt@dor.state.wi.us FTA Conference of Revenue Estimating &

General Sales and Use Tax Transfer of Tax on Motor Vehicle Leases Based on 6.5% Rate Instead of 6.875% $3,800 $4,000 $4,200 $4,200 $4,200

February 17, 2015 State Taxes Only Department of Revenue Analysis of S.F. 826 (Skoe) / H.F. 848 (Davids) Governor s Tax Policy Bill DOR Administrative Costs/Savings Fund Impact F.Y. 2015 F.Y. 2016 F.Y.

February 17, 2015 State Taxes Only Department of Revenue Analysis of S.F. 826 (Skoe) / H.F. 848 (Davids) Governor s Tax Policy Bill DOR Administrative Costs/Savings Fund Impact F.Y. 2015 F.Y. 2016 F.Y.

Tax Incidence of Omnibus Tax Bills: The Minnesota Experience

Tax Incidence of Omnibus Tax Bills: The Minnesota Experience Paul Wilson, Director of Tax Research Minnesota Department of Revenue Federation of Tax Administrators Revenue Analysis and Forecasting Conference

Tax Incidence of Omnibus Tax Bills: The Minnesota Experience Paul Wilson, Director of Tax Research Minnesota Department of Revenue Federation of Tax Administrators Revenue Analysis and Forecasting Conference

Commissioners Schowalter and Frans presentation to the Legislative Commission on Planning and Fiscal Policy

Commissioners Schowalter and Frans presentation to the Legislative Commission on Planning and Fiscal Policy Minnesota Management and Budget, Department of Revenue June 7, 2011 1 One-time stimulus and K-12

Commissioners Schowalter and Frans presentation to the Legislative Commission on Planning and Fiscal Policy Minnesota Management and Budget, Department of Revenue June 7, 2011 1 One-time stimulus and K-12

Property Tax System Overview. Prepared for the Property Tax Working Group

Property Tax System Overview Prepared for the Property Tax Working Group Property Tax Research 9/27/2010 Introduction Property tax in Minnesota is an ad valorem tax. This means that property is taxed

Property Tax System Overview Prepared for the Property Tax Working Group Property Tax Research 9/27/2010 Introduction Property tax in Minnesota is an ad valorem tax. This means that property is taxed

Senate File 1209 (Pogemiller, D-Minneapolis) (passed and laid on the table 03/23/05)

(passed and laid on the table 03/23/05)") Summary of 2005 Tax Provisions (Note: This document will be updated from time to time. Please check back periodically. Currently updated through 05.10.05.) The following tables summarize selected provisions

Summary of 2005 Tax Provisions (Note: This document will be updated from time to time. Please check back periodically. Currently updated through 05.10.05.) The following tables summarize selected provisions

Article 1 Section moves to amend H.F. No as follows: 1.2 Delete everything after the enacting clause and insert: 1.

1.1... moves to amend H.F. No. 2125 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL CONFORMITY 1.5 Section 1. Minnesota Statutes 2018, section 270A.03,

1.1... moves to amend H.F. No. 2125 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL CONFORMITY 1.5 Section 1. Minnesota Statutes 2018, section 270A.03,

METHODOLOGY. Who Pays? A Distributional Analysis of the Tax Systems in All 50 States, 6th Edition

METHODOLOGY The Institute on Taxation & Economic Policy has engaged in research on tax issues since 1980, with a focus on the distributional consequences of both current law and proposed changes. Much

METHODOLOGY The Institute on Taxation & Economic Policy has engaged in research on tax issues since 1980, with a focus on the distributional consequences of both current law and proposed changes. Much

Article 1 Section moves to amend H.F. No as follows: 1.2 Delete everything after the enacting clause and insert: 1.

1.1... moves to amend H.F. No. 4385 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

1.1... moves to amend H.F. No. 4385 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

Tax Cuts and Jobs Act Key Implications for Individuals

Tax Cuts and Jobs Act Key Implications for Individuals Overview The 2017 Tax Reform legislation, the most significant federal tax law reform in over 30 years, was passed by both the House of Representatives

Tax Cuts and Jobs Act Key Implications for Individuals Overview The 2017 Tax Reform legislation, the most significant federal tax law reform in over 30 years, was passed by both the House of Representatives

OFFICE OF THE STATE COMPTROLLER

OFFICE OF THE STATE COMPTROLLER Thomas P. DiNapoli, State Comptroller Comptroller s Fiscal : Results for State Fiscal Year 2014-15 May 2015 Executive Summary New York spent $143.9 billion in State Fiscal

OFFICE OF THE STATE COMPTROLLER Thomas P. DiNapoli, State Comptroller Comptroller s Fiscal : Results for State Fiscal Year 2014-15 May 2015 Executive Summary New York spent $143.9 billion in State Fiscal

Options to Address Minnesota s Budget Deficit

Options to Address Minnesota s Budget Deficit According to the November Forecast, Minnesota faces a deficit of $1.953 billion for the 2002-03 biennium and a structural deficit of $1.234 billion in Fiscal

Options to Address Minnesota s Budget Deficit According to the November Forecast, Minnesota faces a deficit of $1.953 billion for the 2002-03 biennium and a structural deficit of $1.234 billion in Fiscal

The Consequences of Maine s Income Tax Cuts

October 2012 The Consequences of Maine s Income Tax Cuts Introduction Governor LePage and the 125th Maine Legislature used cuts to income, pension, and estate taxes to transfer tens of millions of dollars

October 2012 The Consequences of Maine s Income Tax Cuts Introduction Governor LePage and the 125th Maine Legislature used cuts to income, pension, and estate taxes to transfer tens of millions of dollars

Notes and Definitions Numbers in the text, tables, and figures may not add up to totals because of rounding. Dollar amounts are generally rounded to t

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2013 Percent 70 60 50 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE The Distribution of Household Income and Federal Taxes, 2013 Percent 70 60 50 Shares of Before-Tax Income and Federal Taxes, by Before-Tax Income

The Distribution of Federal Taxes, Jeffrey Rohaly

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

www.taxpolicycenter.org The Distribution of Federal Taxes, 2008 11 Jeffrey Rohaly Overall, the federal tax system is highly progressive. On average, households with higher incomes pay taxes that are a

Overview of Property Taxes. Presentation to House Property and Local Tax Division January 2017

Overview of Property Taxes Presentation to House Property and Local Tax Division January 2017 State and Local Taxes ($32.9 billion in FY 2017) Individual Income 34% Property 28% Other Local Taxes 2% Sales

Overview of Property Taxes Presentation to House Property and Local Tax Division January 2017 State and Local Taxes ($32.9 billion in FY 2017) Individual Income 34% Property 28% Other Local Taxes 2% Sales

Minnesota Tax Handbook

Minnesota Tax Handbook A Profile of State and Local Taxes in Minnesota 2004 Edition Tax Research Division February 2005 The Minnesota Tax Handbook provides general information on Minnesota state and local

Minnesota Tax Handbook A Profile of State and Local Taxes in Minnesota 2004 Edition Tax Research Division February 2005 The Minnesota Tax Handbook provides general information on Minnesota state and local

Department of Revenue Analysis of H.F (Lenczewski) / S.F (Bakk) Fund Impact

/ S.F (Bakk) Fund Impact") 0B U Department Technical Bill February 22, 2010 DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2971 (Lenczewski) / S.F. 2696 (Bakk) Fund Impact UF.Y. 2010U UF.Y. 2011U UF.Y. 2012U

0B U Department Technical Bill February 22, 2010 DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 2971 (Lenczewski) / S.F. 2696 (Bakk) Fund Impact UF.Y. 2010U UF.Y. 2011U UF.Y. 2012U

REVISOR EAP/IL A

1.1... moves to amend H.F. No. 4385, the third engrossment, as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes

1.1... moves to amend H.F. No. 4385, the third engrossment, as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes

Expanded Tax Compliance Initiatives

Expanded Tax Compliance Initiatives Fiscal Year 2011 Report to the Minnesota Legislature March 2011 March 11, 2011 To the members of the legislature of the State of Minnesota: The Minnesota Legislature

Expanded Tax Compliance Initiatives Fiscal Year 2011 Report to the Minnesota Legislature March 2011 March 11, 2011 To the members of the legislature of the State of Minnesota: The Minnesota Legislature

Federal Update: The Tax Cuts and Jobs Act of 2017 As Enacted

Federal Update: The Tax Cuts and Jobs Act of 2017 As Enacted Preliminary Estimates ($000s) Individual Income Tax $8,320 $395,480 $406,820 $492,320 Property Tax Refund $0 $0 $84,410 $84,830 Corporate Franchise

Federal Update: The Tax Cuts and Jobs Act of 2017 As Enacted Preliminary Estimates ($000s) Individual Income Tax $8,320 $395,480 $406,820 $492,320 Property Tax Refund $0 $0 $84,410 $84,830 Corporate Franchise

2017 INDIVIDUAL INCOME TAX LEGISLATIVE BULLETIN

2017 INDIVIDUAL INCOME TAX LEGISLATIVE BULLETIN Bulletin Date: June 27, 2017 Appeals and Legal Services Division 600 North Robert Street Saint Paul, Minnesota 55146-2220 Unless otherwise noted, the provisions

2017 INDIVIDUAL INCOME TAX LEGISLATIVE BULLETIN Bulletin Date: June 27, 2017 Appeals and Legal Services Division 600 North Robert Street Saint Paul, Minnesota 55146-2220 Unless otherwise noted, the provisions

Preliminary Details and Analysis of the Senate s 2017 Tax Cuts and Jobs Act

SPECIAL REPORT No. 240 Nov. 2017 Preliminary Details and Analysis of the Senate s 2017 Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Senate s version of the Tax Cuts and Jobs Act would reform

SPECIAL REPORT No. 240 Nov. 2017 Preliminary Details and Analysis of the Senate s 2017 Tax Cuts and Jobs Act Tax Foundation Staff Key Findings The Senate s version of the Tax Cuts and Jobs Act would reform

Governor s Tax Bill. February 18, Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie)

/ H.F. 660 (Krinkie)") Governor s Tax Bill February 18, 2005 Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie) Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes

Governor s Tax Bill February 18, 2005 Department of Revenue Analysis of S.F. 753 (Ortman)/ H.F. 660 (Krinkie) Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes

Tax Comparisons for Nebraska

Tax Comparisons for John R. Bartle, Dean College of Public Affairs and Community Service University of Omaha December 2013 This policy brief provides two perspectives on taxes. The first is an analysis

Tax Comparisons for John R. Bartle, Dean College of Public Affairs and Community Service University of Omaha December 2013 This policy brief provides two perspectives on taxes. The first is an analysis

Revenue Gain or (Loss) F.Y F.Y F.Y F.Y (000 s) General Fund $0 $0 $0 $0

F.Y F.Y F.Y F.Y (000 s) General Fund $0 $0 $0 $0") Department Technical Bill February 27, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No Department of Revenue Analysis of H.F. 2300 (Abrams) Revenue Gain

Department Technical Bill February 27, 2004 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Yes No Department of Revenue Analysis of H.F. 2300 (Abrams) Revenue Gain

Total state and local business taxes

Total state and local business taxes State-by-state estimates for fiscal year 2014 October 2015 Executive summary This report presents detailed state-by-state estimates of the state and local taxes paid

Total state and local business taxes State-by-state estimates for fiscal year 2014 October 2015 Executive summary This report presents detailed state-by-state estimates of the state and local taxes paid

THE TAX REFORM TRADEOFF: ELIMINATING TAX EXPENDITURES, REDUCING RATES

THE TAX REFORM TRADEOFF: ELIMINATING TAX EXPENDITURES, REDUCING RATES TPC Staff September 13, 2017 ABSTRACT In this exercise, TPC estimates the revenue and distributional effects of proposals that would

THE TAX REFORM TRADEOFF: ELIMINATING TAX EXPENDITURES, REDUCING RATES TPC Staff September 13, 2017 ABSTRACT In this exercise, TPC estimates the revenue and distributional effects of proposals that would

Major State Aids &Taxes DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

Major State Aids &Taxes A COMPARATIVE ANALYSIS, INCLUDING REGIONAL AND COUNTY DATA ON WHERE THE AIDS GO AND WHERE THE TAXES COME FROM Overview of Presentation I will cover three topics or questions: Why

FISCAL FACT No. 516 July, 2016 Director of Federal Projects Key Findings Embargoed

FISCAL FACT No. 516 July, 2016 Details and Analysis of the 2016 House Republican Tax Reform Plan By Kyle Pomerleau Director of Federal Projects Key Findings The House Republican tax reform plan would reform

FISCAL FACT No. 516 July, 2016 Details and Analysis of the 2016 House Republican Tax Reform Plan By Kyle Pomerleau Director of Federal Projects Key Findings The House Republican tax reform plan would reform

Tax Cuts & Jobs Act (TCJA)

") Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

Tax Cuts & Jobs Act (TCJA) Agenda Entity Types and Basis of Accounting TCJA Overview Q&A Learning Objectives: 1) Learn about entity types and basis of accounting for book and tax purposes 2) Develop a

The changes in the bill are not expected to have an impact on state revenues.

Department Technical Bill March 28, 2003 Separate Official Fiscal Note Requested Yes No Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 759 (Abrams)/ S.F. 1007 (Moua)

Department Technical Bill March 28, 2003 Separate Official Fiscal Note Requested Yes No Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 759 (Abrams)/ S.F. 1007 (Moua)

Michigan Tax Revenue. Mary Ann Cleary, Director House Fiscal Agency

Michigan Tax Revenue Mary Ann Cleary, Director Michigan State University Institute for Public Policy and Social Research 2016 Legislative Leadership Program December 5, 2016 Major State Taxes 2 Major State

Michigan Tax Revenue Mary Ann Cleary, Director Michigan State University Institute for Public Policy and Social Research 2016 Legislative Leadership Program December 5, 2016 Major State Taxes 2 Major State

F.Y F.Y F.Y F.Y.

Senate Omnibus Tax Bill May 8, 2018 See Separate Analysis For Property Tax Provisions DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of H.F. 4385 2 nd Unofficial Engrossment Fund

Senate Omnibus Tax Bill May 8, 2018 See Separate Analysis For Property Tax Provisions DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of H.F. 4385 2 nd Unofficial Engrossment Fund

Taxes Primer September 27, 2013

Taxes Primer September 27, 2013 WHERE DOES THE MONEY COME FROM? Each year, some of the revenue the federal government collects comes from various taxes. In 2012, taxpayers paid almost $2.5 trillion, which

Taxes Primer September 27, 2013 WHERE DOES THE MONEY COME FROM? Each year, some of the revenue the federal government collects comes from various taxes. In 2012, taxpayers paid almost $2.5 trillion, which

DIVISION - I. 2. Basic Concepts of Excise Duty Basic Concepts of Customs Duty Basic Concepts of VAT Basic Concepts of CST 146

Contents DIVISION - I 1. Basic Concepts of Indirect Taxes 1 2. Basic Concepts of Excise Duty 11 3. Basic Concepts of Customs Duty 63 4. Basic Concepts of VAT 101 5. Basic Concepts of CST 146 DIVISION -

Contents DIVISION - I 1. Basic Concepts of Indirect Taxes 1 2. Basic Concepts of Excise Duty 11 3. Basic Concepts of Customs Duty 63 4. Basic Concepts of VAT 101 5. Basic Concepts of CST 146 DIVISION -

Federal Update: The Tax Cuts and Jobs Act of 2017 As Enacted

Federal Update: The Tax Cuts and Jobs Act of 2017 As Enacted Preliminary Estimates ($000s) Individual Income Tax ($6,380) $163,980 $194,920 $258,020 Property Tax Refund $0 $0 $84,410 $84,830 Unrelated

Federal Update: The Tax Cuts and Jobs Act of 2017 As Enacted Preliminary Estimates ($000s) Individual Income Tax ($6,380) $163,980 $194,920 $258,020 Property Tax Refund $0 $0 $84,410 $84,830 Unrelated

COUNSEL ESS/NP/JW/JP/RER/GC SCS3982A-3

1.1 Senator... moves to amend S.F. No. 3982 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

1.1 Senator... moves to amend S.F. No. 3982 as follows: 1.2 Delete everything after the enacting clause and insert: 1.3 "ARTICLE 1 1.4 FEDERAL TAX CONFORMITY 1.5 Section 1. Minnesota Statutes 2017 Supplement,

14-1: How Taxes Work NOTES

14-1: How Taxes Work NOTES Learning Target 1. I will demonstrate my understanding of the different types of taxes and what tax revenue is used for. Government Revenue Tax: a mandatory payment to a local,

14-1: How Taxes Work NOTES Learning Target 1. I will demonstrate my understanding of the different types of taxes and what tax revenue is used for. Government Revenue Tax: a mandatory payment to a local,

Fiscal Impacts Appendix

Fiscal Impacts Appendix This chapter focuses on the fiscal impacts to local governments and the State of Alaska resulting from Operation F-35 Beddown at Eielson, which we will hereafter refer to as the

Fiscal Impacts Appendix This chapter focuses on the fiscal impacts to local governments and the State of Alaska resulting from Operation F-35 Beddown at Eielson, which we will hereafter refer to as the

Department of Revenue Analysis of H.F (Marquart) Fund Impact F.Y F.Y F.Y F.Y (000 s) General Fund $0 $0 $0 $0

Fund Impact F.Y F.Y F.Y F.Y (000 s) General Fund $0 $0 $0 $0") Department Policy & Technical Bill March 13, 2019 State Taxes Only See Separate Analysis of Property Tax Provisions DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of H.F. 2169

Department Policy & Technical Bill March 13, 2019 State Taxes Only See Separate Analysis of Property Tax Provisions DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of H.F. 2169

Wisconsin Budget Toolkit

Wisconsin Budget Toolkit INTRODUCTION Updated January 2016 Countless times a day, you are affected by state budget decisions. When you turn on the water, send your child to school, turn on a light, or

Wisconsin Budget Toolkit INTRODUCTION Updated January 2016 Countless times a day, you are affected by state budget decisions. When you turn on the water, send your child to school, turn on a light, or

AP Microeconomics Chapter 16 Outline

I. Learning objectives In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution

I. Learning objectives In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution

MINNESOTA Department of Revenue

MINNESOTA Department of Revenue Department Technical Bill February 1, 2000 Department of Revenue Analysis of S.F. 2693 (Belanger) /H.F. 3024 (Daggett) Revenue Gain or (Loss) F.Y. 2000 F.Y. 2001 Biennium

MINNESOTA Department of Revenue Department Technical Bill February 1, 2000 Department of Revenue Analysis of S.F. 2693 (Belanger) /H.F. 3024 (Daggett) Revenue Gain or (Loss) F.Y. 2000 F.Y. 2001 Biennium

Property Taxes. Property Taxes. Property Taxes: From Levy Certification to Individual Tax Statement

: From Levy Certification to Individual Tax Statement Shelby McQuay Ehlers Andrea Uhl Ehlers May 11, 2017 1 Overview District officials are sometimes expected to explain property taxes in detail: At school

: From Levy Certification to Individual Tax Statement Shelby McQuay Ehlers Andrea Uhl Ehlers May 11, 2017 1 Overview District officials are sometimes expected to explain property taxes in detail: At school

Budget Highlight 2017

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Budget Highlight 2017 Budget Highlights A new top marginal tax rate of 45% on taxable income of above R 1 500 000.00 was introduced The tax threshold increased from R75 000 to R75 750 p.a Dividends tax

Ohio 2020 Tax Policy Commission

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

Ohio 2020 Tax Policy Commission Testimony of Tax Commissioner Joe Testa Department of Taxation October 22, 2015 Co-Chairman Senator Peterson, Co-Chairman Representative McClain, and members of the Tax

NCSL FISCAL BRIEF: PROJECTED STATE TAX GROWTH IN FY 2012 AND BEYOND

NCSL FISCAL BRIEF: PROJECTED STATE TAX GROWTH IN FY 2012 AND BEYOND December 6, 2011 Fiscal year (FY) 2012 marks the second consecutive year state officials are forecasting state tax growth compared with

NCSL FISCAL BRIEF: PROJECTED STATE TAX GROWTH IN FY 2012 AND BEYOND December 6, 2011 Fiscal year (FY) 2012 marks the second consecutive year state officials are forecasting state tax growth compared with

Department of Revenue Analysis of H.F. 751 (Abrams) / S.F. 748 (Belanger) As Proposed to Be Amended

/ S.F. 748 (Belanger) As Proposed to Be Amended") Governor s Tax Bill Original and Supplemental Proposals April 4, 2003 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 751 (Abrams)

Governor s Tax Bill Original and Supplemental Proposals April 4, 2003 Separate Official Fiscal Note Requested Fiscal Impact DOR Administrative Costs/Savings Department of Revenue Analysis of H.F. 751 (Abrams)

2018 Supplement to the Eighth Edition. December 2018

KANSAS TAX FACTS 2018 Supplement to the Eighth Edition December 2018 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181 Topeka, Kansas 66612-1504

KANSAS TAX FACTS 2018 Supplement to the Eighth Edition December 2018 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181 Topeka, Kansas 66612-1504

State Taxes Only See Separate Analysis for Property Taxes and Local Aids

House Omnibus Tax Bill May 9, 2008 State Taxes Only See Separate Analysis for Property Taxes and Local Aids DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of H.F. 3149 (Lenczewski),

House Omnibus Tax Bill May 9, 2008 State Taxes Only See Separate Analysis for Property Taxes and Local Aids DOR Administrative Costs/Savings Yes X No Department of Revenue Analysis of H.F. 3149 (Lenczewski),

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 22, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 22, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

HAWAII INCOME PATTERNS

HAWAII INCOME PATTERNS INDIVIDUALS - 1994 DEPARTMENT OF TAXATION - STATE OF HAWAII STATE OF HAWAII Benjamin J. Cayetano, Governor DEPARTMENT OF TAXATION Ray K. Kamikawa, Director Susan K. Inouye, Deputy

HAWAII INCOME PATTERNS INDIVIDUALS - 1994 DEPARTMENT OF TAXATION - STATE OF HAWAII STATE OF HAWAII Benjamin J. Cayetano, Governor DEPARTMENT OF TAXATION Ray K. Kamikawa, Director Susan K. Inouye, Deputy

Federal Update: The Tax Cuts and Jobs Act of 2017 Generally Effective beginning Tax Year 2019 Retroactive for Select Provisions

Federal Update: The Tax Cuts and Jobs Act of 2017 Generally Effective beginning Tax Year 2019 Retroactive for Select Provisions FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 ($000s) Individual Income Tax ($12,210)

Federal Update: The Tax Cuts and Jobs Act of 2017 Generally Effective beginning Tax Year 2019 Retroactive for Select Provisions FY 2019 FY 2020 FY 2021 FY 2022 FY 2023 ($000s) Individual Income Tax ($12,210)

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

Congress passes 2012 Taxpayer Relief Act and averts fiscal cliff tax consequences Page 1 of 8 In the early morning hours of January 1, 2013, the Senate passed the American Taxpayer Relief Act (the 2012

Most of the provisions discussed below apply beginning in 2018, and many terminate after 2025.

January 26, 2018 To the Clients and Friends of Nathan Wechsler & Company Congress delivered the much-anticipated tax reform bill just before the end of the year. Just as they kept us in suspense as to

January 26, 2018 To the Clients and Friends of Nathan Wechsler & Company Congress delivered the much-anticipated tax reform bill just before the end of the year. Just as they kept us in suspense as to

CHAPTER 13 STATE TAXES

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

Connecticut Budget Act and Pending Tax Legislation

M A Y 2 0 1 1 Connecticut Budget Act and Pending Tax Legislation Facing an estimated $3.5 billion budget deficit, both chambers of the Connecticut General Assembly recently approved a modified version

M A Y 2 0 1 1 Connecticut Budget Act and Pending Tax Legislation Facing an estimated $3.5 billion budget deficit, both chambers of the Connecticut General Assembly recently approved a modified version

Minnesota University Avenue West, Suite 204, Saint Paul, MN

Minnesota 2020 2324 University Avenue West, Suite 204, Saint Paul, MN 55114 www.mn2020.org All work on mn2020.org is licensed under a Creative Commons Attribution-No Derivative Works 3.0 Unported License.

Minnesota 2020 2324 University Avenue West, Suite 204, Saint Paul, MN 55114 www.mn2020.org All work on mn2020.org is licensed under a Creative Commons Attribution-No Derivative Works 3.0 Unported License.

This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16.

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

BUDGET2015 TAX GUIDE This SARS pocket tax guide has been developed to provide a synopsis of the most important tax, duty and levy related information for 2015/16. INCOME TAX: INDIVIDUALS AND TRUSTS Tax

Analysis of Fiscal Policy in Nevada. An Overview of the Approach and Findings of the Governor s Task Force on Tax Policy in Nevada

Analysis of Fiscal Policy in Nevada An Overview of the Approach and Findings of the Governor s Task Force on Tax Policy in Nevada Summary Review ACR 1 s requirements and assumptions provided a general

Analysis of Fiscal Policy in Nevada An Overview of the Approach and Findings of the Governor s Task Force on Tax Policy in Nevada Summary Review ACR 1 s requirements and assumptions provided a general

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 20, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 20, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

H.F Contents. Bill Summary. As amended by H2125DE1. Alexandra Haigler Christopher Kleman Jared Swanson Pat Dalton Sean Williams

Bill Summary Subject Authors Analyst Omnibus Tax Bill Marquart Alexandra Haigler Christopher Kleman Jared Swanson Pat Dalton Sean Williams Date April 8, 2019 Contents Article 1: Federal Conformity... 2

Bill Summary Subject Authors Analyst Omnibus Tax Bill Marquart Alexandra Haigler Christopher Kleman Jared Swanson Pat Dalton Sean Williams Date April 8, 2019 Contents Article 1: Federal Conformity... 2

Kansas Tax Facts Supplement to the Eighth Edition. December 2016

Kansas Tax Facts 2016 Supplement to the Eighth Edition December 2016 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181/FAX (785) 296-3824

Kansas Tax Facts 2016 Supplement to the Eighth Edition December 2016 Kansas Legislative Research Department Room 68-W State Capitol Building 300 SW Tenth Avenue Phone: (785) 296-3181/FAX (785) 296-3824

Table of Contents. A. Income Tax Legislation B. Transaction Privilege ( Sales ) and Use Tax Legislation C. Property Tax Legislation...

and Use Tax Legislation C. Property Tax Legislation...") Important information about this Summary This document briefly summarizes recent substantive changes to Arizona s tax laws. The bills addressed herein were approved by both houses of Arizona s Legislature

Important information about this Summary This document briefly summarizes recent substantive changes to Arizona s tax laws. The bills addressed herein were approved by both houses of Arizona s Legislature

Budget Highlights 2018

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

Budget Highlights 2018 14 March 2018 Budget Highlights Value-Added Tax rate increases from 14% to 15% on 1 April 2018 Limited relief for the effect of inflation in adjusting Personal Income Tax rates resulting

State Taxation. Income Taxes. Upper Income Tax Rate

25 State Taxation The 2005 regular session saw numerous tax changes, ranging from bold reforms to minor, temporary adjustments. As in 2001 and 2003, the General Assembly failed to address its structural

25 State Taxation The 2005 regular session saw numerous tax changes, ranging from bold reforms to minor, temporary adjustments. As in 2001 and 2003, the General Assembly failed to address its structural

April 2004 Memo To: All Tax Clients Re: Stealth Tax The Alternative Minimum Tax ( AMT )

") WILLIAM E. BRYANT CERTIFIED PUBLIC ACCOUNTANT 2524 ELEVENTH AVENUE SOUTH, MINNEAPOLIS, MINNESOTA 55404-4501 TEL. (612) 872-9684 FAX (612) 879-9954 Web Page: http://www.bryant-cpa.com E-mail: web@bryant-cpa.com

WILLIAM E. BRYANT CERTIFIED PUBLIC ACCOUNTANT 2524 ELEVENTH AVENUE SOUTH, MINNEAPOLIS, MINNESOTA 55404-4501 TEL. (612) 872-9684 FAX (612) 879-9954 Web Page: http://www.bryant-cpa.com E-mail: web@bryant-cpa.com

New York State Senate Finance Committee

New York State Senate Finance Committee 2009 Mid Year Report On Receipts and Disbursements Senator Carl Kruger Chair, Senate Finance Committee Senator Liz Krueger Vice-Chair, Senate Finance Committee Joseph

New York State Senate Finance Committee 2009 Mid Year Report On Receipts and Disbursements Senator Carl Kruger Chair, Senate Finance Committee Senator Liz Krueger Vice-Chair, Senate Finance Committee Joseph

State Tax Return. Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

Tax Issues for Possible Consideration by Tax Reform Council

POLICY MEMORANDUM Fiscal Research Center Andrew Young School of Policy Studies Georgia State University SUBJECT: Tax Issues for Possible Consideration by Tax Reform Council Analysis Prepared by: David

POLICY MEMORANDUM Fiscal Research Center Andrew Young School of Policy Studies Georgia State University SUBJECT: Tax Issues for Possible Consideration by Tax Reform Council Analysis Prepared by: David