BLOOD TRIBE AGRICULTURAL PROJECT (1991) COMMUNICATION UPDATE OCTOBER 27, 2016

|

|

|

- Theodora Brown

- 6 years ago

- Views:

Transcription

COMMUNICATION UPDATE OCTOBER")

1 BLOOD TRIBE AGRICULTURAL PROJECT (1991) COMMUNICATION UPDATE OCTOBER 27, 2016

2 BACKGROUND & CO-MANAGEMENT 2 BLOOD TRIBE AGRICULTURAL PROJECT (1991) Effective May 16, 2016, Blood Tribe Agricultural Project (1991) (BTAP) was placed under Co-Management by Blood Tribe Chief & Council/Shareholders to prevent legal action against BTAP for not meeting its financial & management responsibilities. In 2015/2016 Chief and Council were alerted by vendors and companies regarding non-payment of invoices. CO-MANAGEMENT PURPOSE The purpose of Co-Management of BTAP is to assist and ensure that BTAP meets its obligations through the joint management by the Blood Tribe Management Team (BTA), the Co-Management Consultant(s) and BTAP, working with the BTAP Board of Directors. The group is working together towards common goals for the best interest of the Blood Tribe as a whole. CO-MANAGEMENT As at March 31, 2016, the operating entities of BTAP included Blood Tribe Irrigation Management, Blood Tribe Farming Initiative (Blood Band Ranch), Sawkee Feedlot Inc., Blood Band Farms Ltd., and AB Ltd (Blood Tribe Forage Processing Plant) and Aohkii Property Management. Prior to the current Board of Directors, BTAP had an annual operating deficit for 2016 of ($4,945,638) The overall negative cash position for the organization as a whole on March 31, 2016 was ($1,601,568). Outstanding accounts payable at that date totalled $3,657,457 and amounts owing to other Blood Tribe departments / entities totalled $2,188,147, not including any long term loans. Since Co-Management began on May 16, 2016, the team has been working on identifying all potential revenue sources and all additional outstanding payables in each of these divisions, as well as: Inventory valuation BTFPP Inventory valuation cattle Identifying and categorizing capital assets and equipment Bringing all custom work and other contracts up to date Identifying specific contact amounts and reconciling amounts owing to / from BTAP, Blood Tribe Lands, Blood Band Farms, Mataki Farms and West End Big Lease Managing the cash flow to ensure payroll and critical accounts payable are being met Preparing a financial position update for each division separately Reviewing and updating budgets Reviewing internal controls and start addressing the Management Letter points from the audit Implementing internal controls West End Big Lease and Blood Band Farms West End Big Lease consists of 10,782 acres and Blood Band Farms consists of 3,917 acres. For the 2016 crop year, B + D Walters Farms (Ben Walters) has been farming these parcels of land with Blood Band Farms doing custom work alongside, providing training and employment for Blood Band Farm employees. BTAP is in the process of reviewing and preparing contracts for the 2017 crop year.

3 BDO FORENSIC REVIEW OCTOBER On April 19, 2016 the Blood Tribe Chief and Council passed a motion to enter into a Co Management Agreement with the Blood Tribe Agriculture Project (1991) to provide management assistance as a result of the noted concerns, and that a forensic audit of BTAP and its affiliated entities be completed by an independent firm. Unfortunately, the Board of Directors subsequently refused to enter into the Co Management Agreement or conduct a forensic audit as requested by Chief and Council. On May 16, 2016, the Council requisitioned a meeting of the BTAP Shareholders and the BTAP Shareholders replaced four of the Board of Directors for BTAP and its affiliated entities, Frank Black Plume, Al Black Water, Myron Eagle Speaker and Bill Wadsworth (the former Board of Directors) with four alternate Council members Mike Bruised Head, Kyla Crow, Lance Tail Feathers, Franklyn White Quills (the current Board of Directors). The Shareholders reaffirmed the request for a forensic review by an independent firm, BDO Canada LLP (BDO), and entered a Co Management Agreement in response to the concerns expressed by BTAP employees, its vendors, the auditors (MNP LLP), the community and other members of Council with regard to the lack of financial management and cash flow. The forensic review conducted by BDO reviewed and analyzed the banking records including relevant documentation in support of the disbursements made from the following entities: Alberta Ltd/Blood Tribe Forage Processing Plant (including Canadian and US Account) Blood Tribe Farming Initiative (Blood Band Ranch) Blood Band Farms Ltd Sawkee Feedlot Inc Aohkii Investment Property Management and; BTAP/BTIM BDO requested financial information for two fiscal years April March Due to the volume of transactions of this 2 year period, BDO tested a 3 month sample period April 1 June for each of the entities listed above. BDO further reviewed $4.7 million received from Blood Tribe Chief and Council and Blood Tribe Land Management department in December The following points summarize the BDO findings: BTAP had an overall negative cash position during the sample period, and BDO noted that the bank balances of BTAP, specifically BTIM were overdrawn by $1,502, as at April Throughout this sample period, BDO noted that this negative cash position persisted, although total deposits of $3,258, were received, including transfers from other BTAP entities, BTAP disbursed $3,060, and at the end of the sample period the bank balance was overdrawn by $1,304, During the three month sample period it was noted that there were significant weaknesses in internal controls including: (a) (b) (c) A lack of financial policies and procedures; Weak oversight regarding authorizations and approvals for cash disbursements by the former COO/GM and Board members; and Poor internal controls, especially in the areas of record keeping, reconciliations and accounting practices. 2. Significant payments from BTAP for travel and honoraria to the former Board of Directors including: (a) During the three month period of April 1, 2015 to June 30, 2015 the four former Board of Directors received total payments for meeting and travel in the amount of $74, (b) Board expenditures for the two fiscal years ending March 31, 2015 totaled $227,709 and ending March 31, 2016 were over budget by a total of $274,243. (c) No Board meeting minutes have been located for the two year period under review. (d) Honoraria were claimed for travel days and BTAP business meetings of which there were no recorded minutes to verify if the meetings took place. (e) Based upon the recorded payments of honoraria or per diem amount of $250 for attendance at meetings it was calculated that there would have been 71 board meetings in 2014/15 and 87 board meetings in 2015/16. (f) The business purpose for meetings or travel was not clear, especially with regard to travel to the United States.

4 BDO FORENSIC REVIEW OCTOBER (g) (h) (i) Meetings were held at locations away from the reserve and BTAP s main office which resulted in excessive mileage claims, which was contrary to the Travel Policy. Mileage was claimed on trips to the United States versus the more economic option of flying. Claims for accommodation, meals and incidentals were not supported by receipts. 3. The former Chief Operating Officer/General Manager (COO/GM) received payments related to travel expenditures in the amount of $17, during the three month sample period. This included: (a) (b) (c) Mileage of $8, while also driving a BTAP vehicle which was not in compliance with the Travel Policy, and Expense reimbursements without supporting receipts for accommodation, meals and incidentals. Received Vacation payouts that were not in compliance with Policy. 4. BTAP employees requested and received payroll advances of $14,350 during the three month sample period. 5. Donations were made in the amount of $11,400 during the sample period. 6. Crop Advances were made to Blood Tribe Occupants in the amount of $53, during the sample period. The following concerns were noted with respect to these payments: (a) (b) (c) (d) Certain occupants were paid rates of $140 per metric ton and $270 per metric ton which was not in accordance with the stated contract rates of $85 and $40 depending upon the quality of the hay. Accounting records lacked information such as price and quantity relating to the delivery of the products and therefore made it difficult to determine what, if any, product was delivered. Crop advances were paid to some occupants in excess of the product that was delivered to the processing plant. Advances were paid to certain occupant sellers who did not have contracts with the Blood Tribe Forage Processing Plant at the time the advances were paid. 7. Advances on grazing agreements of $45,920 were paid to Blood Tribe members by the Blood Tribe Farming Initiative on behalf of the Blood Band Ranch to graze cattle on lands occupied by them. Concerns surrounding the lack of supporting documentation to show what the agreements were and whether they were fulfilled were noted. 8. Cattle purchases from Band members during the period of review, totaled $54, purchased by Blood Tribe Farming Initiative/Band Ranch and $ purchased by Sawkee Feedlot. BDO noted that the brand of the cattle purchased did not match the registered brand of the band member who had sold the cattle to BTAP, but the brand of another family member. This resulted in questions with regard to who the actual owner of the cattle was at the time BTAP made the cattle purchase. The supporting documentation such as bill of sale, proper invoices or veterinary records were missing at the time of purchase which resulted in issues with the sale of cattle by the Blood Band Ranch. 9. Payments to parties who were related to staff or the former Board of Directors were paid without the necessary supporting documentation. 10. Payments to related parties and immediate family for fencing had no contracts in place, there appeared that no bids were submitted to perform this work, there was no independent approval of invoices, and there were no confirmation that the work had been completed. Several invoices lacked details or were noted as progress payments with no details of work that was being done. The amount paid for year 2014/2015 was $42,763 and for year 2015/2016 was $235, Payments to an acquaintance of former COO/GM, BDO noted total crop advance was $ for the year 2014/2015, BDO further noted a contract was filed with a start date of March the next fiscal year, and there was no recorded deliveries of product therefore it was an overpayment by this amount. In addition, a payment of $2700 was made to the acquaintance regarding the purchase of promotional items such as jewelry and crafts, including a donation to this small business. BDO was not able to determine the business purpose for which these payments were made. 10. Payments were made to Consultants and Contractors for professional services such as legal, accounting IT and consulting in the total amount of $581,126 for 2014/15 and $946,524 in 2015/2016. It was noted that several consultants did not have contracts with BTAP.

5 BDO FORENSIC REVIEW OCTOBER Payments were made to non-blood Tribe members from the Forage Processing Plant US funds for marketing, promotional and consulting purposes which were not related to operations of the processing plant. These payments were in the amount of $28,750 US for the fiscal year of 2014/2015 and $61,064 US for the fiscal year of 2015/ Reconciliation of the $4.7 million received by the Blood Tribe Farming Initiative showed that the funds were used to purchase farming equipment, vehicles, livestock and office supplies. The review noted several payments lacked accounting support such as purchase orders, bills of sale and invoices. BDO also noted that the capital assets were poorly tracked and it was recommended that a complete review of all capital equipment owned by BTAP (and its affiliated entities) be conducted in order to confirm that status and use of the assets. 13. Intermingled funds from the various BTAP entities resulted in payments for goods or services being made from an entity and these purchases did not relate to their operations and expenditures being incorrectly allocated during the Period of Review. 14. Conflicts of interest were noted during the course of the review, including payments to related parties, such as family members, former BTAP board members and friends, as well as the employment of related parties by BTAP during the two year period which could be interpreted as real, potential or apparent conflicts of interest. BDO Conclusion and Recommendations: Throughout the review of the financial records of BTAP, BDO noted poor internal controls and apparent careless accounting practices. Recommendations are being made with respect to addressing the weaknesses in BTAP s internal controls and it is anticipated that these will include the following: Policies 1. Develop, amend and upgrade policies to address the internal concerns surrounding accountability, travel, HR, rates, payroll advances, donations, cell phone usage. Existing policies should be communicated to and followed by the Board of Directors, General Manager and staff. Oversight and Accountability 2. Establish realistic budgets with regard to operations, board expenditures, travel and other related expenditures. 3. Put controls in place to monitor the spending of the Board of Directors and General Manager. 4. Establish spending limits for purchases and contracts. 5. Disclose activities undertaken by the entities, including special projects, to the shareholders on a monthly basis, including accurate financial statements and disclosure on all significant projects. Accounting Practices 6. Ensure that an accounting team with strong leadership is put in place and that there is a separation between the accounting department and management of BTAP to ensure financial resources are safeguarded. 7. Segregate duties within the accounting department. 8. Provide adequate ongoing training to accounting staff to ensure that they perform their duties with due care and minimal error. 9. Conduct a reconciliation of all accounts on a regular basis. Record Keeping 10. Put procedures in place to ensure that all payments are supported by valid invoices and approvals. 11. Ensure all cheques are accounted for. 12. Ensure all backup documentation with respect to the receipt of goods are attached to invoices to ensure that the goods were received and the work performed and verified. 13. Ensure that contracts are in place with all consultants and contractors. 14. Ensure that all meeting minutes are recorded, maintained and submitted to the shareholders on a timely basis. Conflicts of Interest 15. Address the issues that have been identified including payments made to related parties, family members, payments made to employees or Board of Directors which could be interpreted as real, potential or apparent conflict of interest. 16. All situations that give rise to real, potential or apparent conflicts of interests should be reviewed and resolved by an independent committee.

6 6

7 7

8 BLOOD BAND RANCH & FEEDLOT OCTOBER

to perform a review and assessment of the current processes and internal controls in place at the Blood Tribe Forage Processing Plant (BTFPP) as it")

9 BDO INVENTORY REVIEW OF BLOOD TRIBE FORAGE PROCESSING PLANT 9 Review and Assessment of Inventory Process and Controls at the Blood Tribe Forage Processing Plant BDO Canada LLP ( BDO ) was engaged by the Blood Tribe Agricultural Project (BTAP) to perform a review and assessment of the current processes and internal controls in place at the Blood Tribe Forage Processing Plant (BTFPP) as it pertains the handling, processing and shipping of forage inventory. BDO held an on-site visit and conducted discussions / interviews with staff and members of management. Findings include the following: Lack of appropriate review and authorization of contracts Contracts are not housed / maintained at BTAP Administration office Inconsistent tagging procedures Weigh scale tickets can be accessed by many individuals and are not consistently kept in one place Inventory and shipments are not being entered into Quickbooks in a timely manner Chaff bales are not being actively tracked Damaged / rejected inventory product is not being appropriately approved or tracked Lack of consistency among various methods of shipping documentation Lack of consistency among shipping documentation approval Lack of security of the product when left in the field Risk of quality diminishing when product is left in the field Weigh scale tickets are not the source documents for recording accounting and inventory received Accounting for pre-payments to off-project harvesters was done incorrectly Concern over the maintenance and calibration of the weigh scale Concern over reliability / accuracy of the document management system and Quickbooks

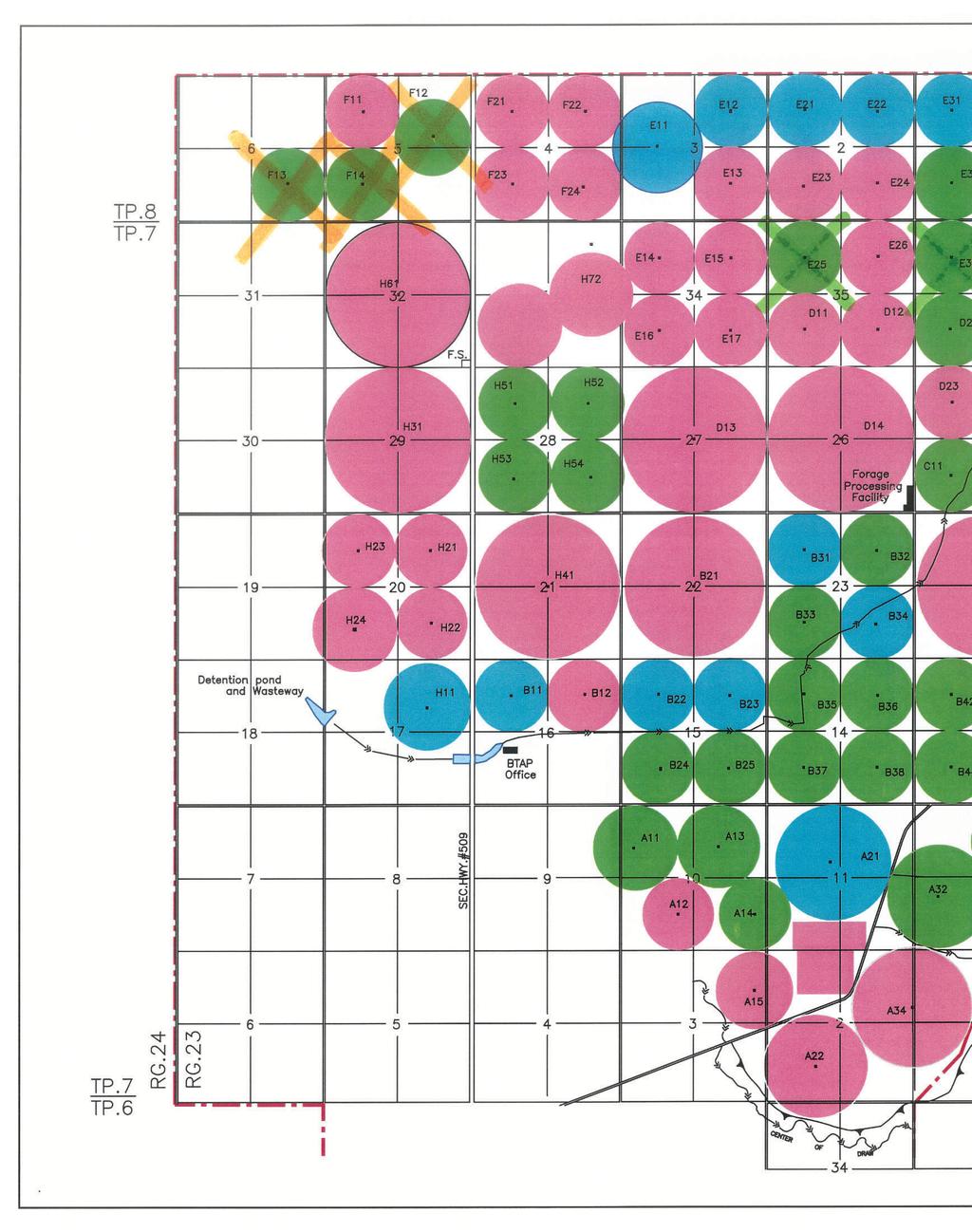

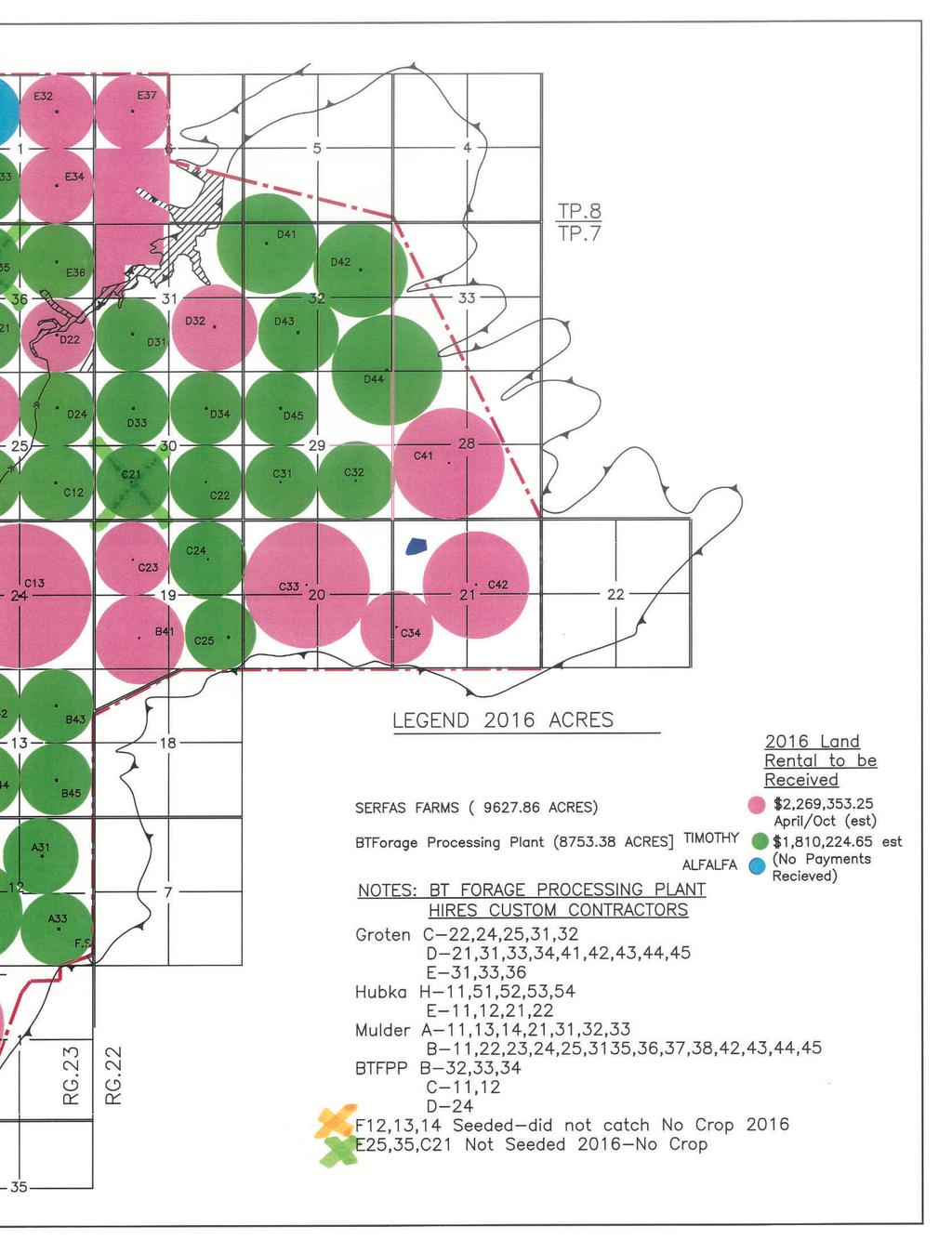

10 PHOTOS 10

11 BTAP AUDITED FINANCIAL SUMMARY 11

12

GLASA. Greater Los Angeles Softball Association. Accounting Policies & Procedures Manual

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

GLASA Greater Los Angeles Softball Association Accounting Policies & Procedures Manual 7/2015 TABLE OF CONTENTS I. General Practices... 1 II. Cash Receipts... 2 III. Cash Disbursements... 3 IV. Other Financial

Mitigation, Prevention, Occupational Health and Safety

Section 1: Program Information Program Purpose: Support the New Brunswick agriculture industry to prevent accidents and promote occupational safety on farms as well as to identify, manage, protect and

Section 1: Program Information Program Purpose: Support the New Brunswick agriculture industry to prevent accidents and promote occupational safety on farms as well as to identify, manage, protect and

CREIA ACCOUNTING POLICIES AND PROCEDURES

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

CREIA ACCOUNTING POLICIES AND PROCEDURES Updated June 2015 1 Table of Contents I. Introduction... 3 II. Division of Responsibilities... 4 Board of Directors... 4 Executive Director/Chief Executive Officer...

Friends of the Library Financial Policies

Note: This may seem to be overkill for such a small organization. The Executive Committee is proposing these policies to ensure that the 501(c)3 status which the IRS has given to the Friends will not be

Note: This may seem to be overkill for such a small organization. The Executive Committee is proposing these policies to ensure that the 501(c)3 status which the IRS has given to the Friends will not be

National Association of Community Health Centers FOM / IT

National Association of Community Health Centers FOM / IT FINANCIAL POLICY CONSIDERATIONS IN PREPARATION FOR HRSA SITE VISITS OCTOBER 29, 2017 David Fields BKD,LLP Partner Catherine Gilpin BKD, LLP Senior

National Association of Community Health Centers FOM / IT FINANCIAL POLICY CONSIDERATIONS IN PREPARATION FOR HRSA SITE VISITS OCTOBER 29, 2017 David Fields BKD,LLP Partner Catherine Gilpin BKD, LLP Senior

Board Policy No

Board Policy No. 2015-16-6 Fiscal Policies and Procedures Handbook Created by: TABLE OF CONTENTS Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Contracts... 2 Accounts Payable... 4 Bank Check

Board Policy No. 2015-16-6 Fiscal Policies and Procedures Handbook Created by: TABLE OF CONTENTS Overview... 1 Annual Financial Audit... 1 Purchasing... 2 Contracts... 2 Accounts Payable... 4 Bank Check

How To Prove Certain Business Expenses...7

Table of Contents Accounting Systems...3 Taxation...3 Fixed Assets...4 Accounting Firms...4 Insurance...4 Corporate Records...4 Payroll...5 Miscellaneous...5 Human Resources...5 Security...5 Legal...6

Table of Contents Accounting Systems...3 Taxation...3 Fixed Assets...4 Accounting Firms...4 Insurance...4 Corporate Records...4 Payroll...5 Miscellaneous...5 Human Resources...5 Security...5 Legal...6

AP 571 PURCHASING CARD COMMERCIAL CREDIT CARD PROGRAM

AP 571 PURCHASING CARD COMMERCIAL CREDIT CARD PROGRAM BACKGROUND This procedure is for the use and control of purchasing cards (a commercial credit card) for the purpose of obtaining goods and services

AP 571 PURCHASING CARD COMMERCIAL CREDIT CARD PROGRAM BACKGROUND This procedure is for the use and control of purchasing cards (a commercial credit card) for the purpose of obtaining goods and services

Account - A record of financial transactions that are similar in terms of a given frame of reference such as purpose, objective, or source.

This section includes definitions of terms used in this guide and additional terms necessary for the understanding of financial accounting procedures for internal funds. Internal funds are defined as all

This section includes definitions of terms used in this guide and additional terms necessary for the understanding of financial accounting procedures for internal funds. Internal funds are defined as all

MINNEAPOLIS PUBLIC SCHOOLS SPECIAL DISTRICT NO. 1 REPORTS ON GOVERNMENT AUDITING STANDARDS, OMB CIRCULAR A-133 SINGLE AUDIT AND LEGAL COMPLIANCE

REPORTS ON GOVERNMENT AUDITING STANDARDS, OMB CIRCULAR A-133 SINGLE AUDIT AND LEGAL COMPLIANCE For the Year Ended TABLE OF CONTENTS SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS... 1 NOTES TO THE SCHEDULE

REPORTS ON GOVERNMENT AUDITING STANDARDS, OMB CIRCULAR A-133 SINGLE AUDIT AND LEGAL COMPLIANCE For the Year Ended TABLE OF CONTENTS SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS... 1 NOTES TO THE SCHEDULE

Updated 07/07/2018 ID 19, Page 1 of 6

Requirement: Frequency: Due Date: Purpose Financial Management Requirements 2 C.F.R., part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; The U.S.

Requirement: Frequency: Due Date: Purpose Financial Management Requirements 2 C.F.R., part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; The U.S.

DISTRICT RESPONSES TO EXTERNAL AUDITOR S OBSERVATIONS & RECOMMENDATIONS

Department of Fiscal Services Internal Accounting Control 1130 Fifth Avenue, Chula Vista, CA 91911-2896 Telephone: (619) 691-5550 FAX: (619) 425-3394 DISTRICT RESPONSES TO EXTERNAL AUDITOR S OBSERVATIONS

Department of Fiscal Services Internal Accounting Control 1130 Fifth Avenue, Chula Vista, CA 91911-2896 Telephone: (619) 691-5550 FAX: (619) 425-3394 DISTRICT RESPONSES TO EXTERNAL AUDITOR S OBSERVATIONS

Cash Disbursement Policy

Policy Number: 4020 Dated: 09/13/2013 Cash Disbursement Policy A. Purpose To establish policy and procedure governing the initiation, authorization, and review of all expenditures of American Leadership

Policy Number: 4020 Dated: 09/13/2013 Cash Disbursement Policy A. Purpose To establish policy and procedure governing the initiation, authorization, and review of all expenditures of American Leadership

Loyola University Maryland Procurement Card Policy & Procedure Revised October 9, 2014

Policy Statement Loyola University Maryland Procurement Card Policy & Procedure Revised October 9, 2014 Procurement Cards are issued by name to individual employees and cannot be transferred to, assigned

Policy Statement Loyola University Maryland Procurement Card Policy & Procedure Revised October 9, 2014 Procurement Cards are issued by name to individual employees and cannot be transferred to, assigned

CITY OF CLARKSVILLE INTERNAL AUDITOR S REPORT

CITY OF CLARKSVILLE INTERNAL AUDITOR S REPORT Clarksville-Montgomery County Regional Airport Authority Review of Expenses and Internal Controls July 1, 2009 June 2, 2010 CITY OF CLARKSVILLE INTERNAL AUDITOR

CITY OF CLARKSVILLE INTERNAL AUDITOR S REPORT Clarksville-Montgomery County Regional Airport Authority Review of Expenses and Internal Controls July 1, 2009 June 2, 2010 CITY OF CLARKSVILLE INTERNAL AUDITOR

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL INTRODUCTION In view of the large amount of monies received from and expended for student/campus activities, the demand has developed for efficient,

OVERTON ISD FUNDRAISER/ACTIVITY FUND & PROCEDURE MANUAL INTRODUCTION In view of the large amount of monies received from and expended for student/campus activities, the demand has developed for efficient,

WASHOE COUNTY Dedicated To Excellence in Public Service

WASHOE COUNTY Dedicated To Excellence in Public Service www.washoecounty.us DATE: November 14, 2016 TO: FROM: STAFF REPORT BOARD MEETING DATE: December 13, 2016 Board of County Commissioners Alison A.

WASHOE COUNTY Dedicated To Excellence in Public Service www.washoecounty.us DATE: November 14, 2016 TO: FROM: STAFF REPORT BOARD MEETING DATE: December 13, 2016 Board of County Commissioners Alison A.

Financial Policies and Procedures

Financial Policies and Procedures It is the intent of these Financial Policies and Procedures to implement both the letter and spirit of all applicable State and Federal regulations regarding the expenditure

Financial Policies and Procedures It is the intent of these Financial Policies and Procedures to implement both the letter and spirit of all applicable State and Federal regulations regarding the expenditure

Minneapolis Public Schools Special District No. 1. Reports on Government Auditing Standards, Uniform Guidance and Legal Compliance.

Reports on Government Auditing Standards, Uniform Guidance and Legal Compliance June 30, 2016 Table of Contents Schedule of Expenditures of Federal Awards 1 Notes to the Schedule of Expenditures of Federal

Reports on Government Auditing Standards, Uniform Guidance and Legal Compliance June 30, 2016 Table of Contents Schedule of Expenditures of Federal Awards 1 Notes to the Schedule of Expenditures of Federal

Financial Policies and Procedures

1.0 Cash Receipts Each day that the Library is open and there is mail delivery, the Library Director or the Circulation Manager check the mail. Checks and credit card payments are either given directly

1.0 Cash Receipts Each day that the Library is open and there is mail delivery, the Library Director or the Circulation Manager check the mail. Checks and credit card payments are either given directly

Lackland ISD Accounts Payable Procedures

Accounts payable checks should be processed on a weekly basis for release by Friday morning, or earlier dependent upon work schedules or holidays. General Instructions: All invoices shall be entered separately

Accounts payable checks should be processed on a weekly basis for release by Friday morning, or earlier dependent upon work schedules or holidays. General Instructions: All invoices shall be entered separately

MINNEAPOLIS PUBLIC SCHOOLS SPECIAL DISTRICT NO. 1 REPORTS ON GOVERNMENT AUDITING STANDARDS, OMB CIRCULAR A-133 SINGLE AUDIT AND LEGAL COMPLIANCE

REPORTS ON GOVERNMENT AUDITING STANDARDS, OMB CIRCULAR A-133 SINGLE AUDIT AND LEGAL COMPLIANCE Year Ended TABLE OF CONTENTS SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS... 1 NOTES TO THE SCHEDULE OF EXPENDITURES

REPORTS ON GOVERNMENT AUDITING STANDARDS, OMB CIRCULAR A-133 SINGLE AUDIT AND LEGAL COMPLIANCE Year Ended TABLE OF CONTENTS SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS... 1 NOTES TO THE SCHEDULE OF EXPENDITURES

The Saskatchewan Feed and Forage Program Regulations

1 FEED AND FORAGE PROGRAM F-8.001 REG 44 The Saskatchewan Feed and Forage Program Regulations being Chapter F-8.001 Reg 44 (effective June 23, 2011; expired December 31, 2013). NOTE: This consolidation

1 FEED AND FORAGE PROGRAM F-8.001 REG 44 The Saskatchewan Feed and Forage Program Regulations being Chapter F-8.001 Reg 44 (effective June 23, 2011; expired December 31, 2013). NOTE: This consolidation

New York City Department of Education

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

O f f i c e o f t h e N e w Y o r k S t a t e C o m p t r o l l e r Division of State Government Accountability New York City Department of Education James Monroe Educational Campus Management of General

Cash Management Policy Knox County Housing Authority 216 W. Simmons St. Galesburg, IL (309)

") Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

Article I. Purpose / Scope of the Policy Cash Management Policy 216 W. Simmons St. Galesburg, IL 61401 (309) 342-8129 Section 1.01 The follows the best practices when it comes to cash management. These

ACCOUNTING POLICIES AND PROCEDURES MANUAL

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

ACCOUNTING POLICIES AND PROCEDURES MANUAL Accounting Policies and Procedures Manual Page 1 Table of Contents Introduction... 3 Division of Responsibilities... 4 Board of Directors... 4 Executive Director...

Sample Fiscal Policies & Procedures Manual

Sample Fiscal Policies & Procedures Manual Legal Disclaimer Please note that TREC does not provide legal advice. This sample Fiscal Policies and Procedures Manual discusses a topic of general interest

Sample Fiscal Policies & Procedures Manual Legal Disclaimer Please note that TREC does not provide legal advice. This sample Fiscal Policies and Procedures Manual discusses a topic of general interest

TOWN OF SOUTHAMPTON, MASSACHUSETTS. Management Letter. For the Year Ended June 30, 2014

TOWN OF SOUTHAMPTON, MASSACHUSETTS Management Letter For the Year Ended June 30, 2014 TABLE OF CONTENTS INTRODUCTORY LETTER 1 PAGE CURRENT YEAR ISSUES 1. Improve Internal Controls Over Payroll Disbursements

TOWN OF SOUTHAMPTON, MASSACHUSETTS Management Letter For the Year Ended June 30, 2014 TABLE OF CONTENTS INTRODUCTORY LETTER 1 PAGE CURRENT YEAR ISSUES 1. Improve Internal Controls Over Payroll Disbursements

Minnesota Veterans Home at Hastings

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA FINANCIAL AUDIT DIVISION REPORT Minnesota Veterans Home at Hastings Internal Control and Compliance Audit July 1, 2006, through March 31, 2009

O L A OFFICE OF THE LEGISLATIVE AUDITOR STATE OF MINNESOTA FINANCIAL AUDIT DIVISION REPORT Minnesota Veterans Home at Hastings Internal Control and Compliance Audit July 1, 2006, through March 31, 2009

HOUSTON LIVESTOCK SHOW and RODEO TM

2016 Record Book Instructions and Guidelines This contest is subject to the Houston Livestock Show and Rodeo General Rules and Regulations, the Junior Show Rules and Regulations and the Special Rules for

2016 Record Book Instructions and Guidelines This contest is subject to the Houston Livestock Show and Rodeo General Rules and Regulations, the Junior Show Rules and Regulations and the Special Rules for

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings. September 30, 2001 and 2000

Schedule of Findings. September 30, 2001 and 2000") GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

GOVERNMENT OF GUAM RETIREMENT FUND (A Public Corporation) Schedule of Findings CURRENT YEAR (2001) FINDINGS Finding No. 2001-1 Verification of Disability Annuitants 4GCA, Chapter 8, Article 1, 8127(a)

2017 Tax Questionnaire Corporate

2017 Tax Questionnaire Corporate Thank you for completing this questionnaire completely and accurately. This is a very important step in analyzing your tax position for the year. By doing so, you provide

2017 Tax Questionnaire Corporate Thank you for completing this questionnaire completely and accurately. This is a very important step in analyzing your tax position for the year. By doing so, you provide

STATE OF MINNESOTA Office of the State Auditor

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

STATE OF MINNESOTA Office of the State Auditor Patricia Anderson State Auditor MANAGEMENT AND COMPLIANCE REPORT PREPARED AS A RESULT OF THE AUDIT OF THE FINANCIAL AFFAIRS OF THE CITY OF GREENFIELD GREENFIELD,

Financial Policies and Procedures Manual

Financial Policies and Manual PTP - Adult Learning and Employment Programs PTP FINANCIAL POLICIES AND PROCEDURES MANUAL Table of Contents Policy 1 Financial Accountability of the Board of Directors...

Financial Policies and Manual PTP - Adult Learning and Employment Programs PTP FINANCIAL POLICIES AND PROCEDURES MANUAL Table of Contents Policy 1 Financial Accountability of the Board of Directors...

RECORD RETENTION SCHEDULES FOR BUSINESSES

RECORD RETENTION SCHEDULES FOR BUSINESSES How to Prove Certain Business Expenses Must keep records that show details on the following: If you have expenses for: Travel Entertainment Gifts Amount Time Place

RECORD RETENTION SCHEDULES FOR BUSINESSES How to Prove Certain Business Expenses Must keep records that show details on the following: If you have expenses for: Travel Entertainment Gifts Amount Time Place

Title Insurance and Settlement Company Best Practices

ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Page 1 of 8 ALTA Best Practices Framework The ALTA Best Practices Framework has been developed to assist lenders in

ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Page 1 of 8 ALTA Best Practices Framework The ALTA Best Practices Framework has been developed to assist lenders in

AIPHS Financial Procedures

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

AIPHS Financial Procedures 1. Bank Accounts Shall remain at Community Bank of the Bay and East West Bank. The Board president along with the Superintendent of AIM Schools, shall have signatory power. 2.

Port Jefferson Union Free School District. Annual Risk Assessment Update Pertaining to the Internal Controls Of District Operations.

Update Pertaining to the Internal Controls Of District Operations INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED UPON PROCEDURES The Board of Education Port Jefferson Union Free School District We have

Update Pertaining to the Internal Controls Of District Operations INDEPENDENT ACCOUNTANTS REPORT ON APPLYING AGREED UPON PROCEDURES The Board of Education Port Jefferson Union Free School District We have

PURCHASING CARD PROCEDURES

EDGEWOOD INDEPENDENT SCHOOL DISTRICT PURCHASING CARD PROCEDURES September 2017 5358 West Commerce Street San Antonio, Texas 78237 Table of Contents Page Table of Contents... 1 Introduction... 2 Card Holder...

EDGEWOOD INDEPENDENT SCHOOL DISTRICT PURCHASING CARD PROCEDURES September 2017 5358 West Commerce Street San Antonio, Texas 78237 Table of Contents Page Table of Contents... 1 Introduction... 2 Card Holder...

AHS Board and Executive Expense Report

Name Andrea Beckwith-Ferraton Title Chief Ethics & Compliance Officer Calgary Expenses submitted during the month of July 208 AHS Board and Executive Expense Report MMM-YY Travel () Source Document Purpose

Name Andrea Beckwith-Ferraton Title Chief Ethics & Compliance Officer Calgary Expenses submitted during the month of July 208 AHS Board and Executive Expense Report MMM-YY Travel () Source Document Purpose

Rockdale ISD Accounts Payable Procedures

Accounts payable checks should be processed on a weekly basis for release by Thursday morning, or earlier dependent upon work schedules or holidays. Cut-off date for weekly processing is noon on Tuesday.

Accounts payable checks should be processed on a weekly basis for release by Thursday morning, or earlier dependent upon work schedules or holidays. Cut-off date for weekly processing is noon on Tuesday.

KASFAA Policy and Procedure Manual. A record of membership dues for the past five years can be found in Appendix D of this manual.

11. Financial 11.1 Membership Dues The Board establishes annual membership dues. This rate is subject to change at the discretion of the Board. Honorary Life Members are not charged membership dues. Membership

11. Financial 11.1 Membership Dues The Board establishes annual membership dues. This rate is subject to change at the discretion of the Board. Honorary Life Members are not charged membership dues. Membership

JCPS Extended Retention Memorandum

JCPS Extended Retention Memorandum Jefferson County Public Schools Archives and Records Center The following series have an extended retention period according to JCPS policy. Records should be managed

JCPS Extended Retention Memorandum Jefferson County Public Schools Archives and Records Center The following series have an extended retention period according to JCPS policy. Records should be managed

Selected Employee Travel Expenses. City University of New York

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Selected Employee Travel Expenses City University of New York Report 2012-S-98 February 2014

New York State Office of the State Comptroller Thomas P. DiNapoli Division of State Government Accountability Selected Employee Travel Expenses City University of New York Report 2012-S-98 February 2014

Office of the City Auditor. Committed to increasing government efficiency, effectiveness, accountability and transparency

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Background...1 Findings &

Office of the City Auditor Committed to increasing government efficiency, effectiveness, accountability and transparency Issue Date: TABLE OF CONTENTS Executive Summary... ii Background...1 Findings &

Fairfield ISD Accounts Payable Procedures

Fairfield ISD Accounts Payable Procedures Revised: January 31, 2017 Contents General Instructions... 2 Compliance with State Law... 3 Verification of Check Transactions... 3 Travel Payments... 3 Construction

Fairfield ISD Accounts Payable Procedures Revised: January 31, 2017 Contents General Instructions... 2 Compliance with State Law... 3 Verification of Check Transactions... 3 Travel Payments... 3 Construction

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

MILWAUKEE PUBLIC SCHOOLS OFFICE OF AUDIT SERVICES. Internal Controls and Other Procedures

MILWAUKEE PUBLIC SCHOOLS OFFICE OF AUDIT SERVICES Internal Controls and Other Procedures School funds are accounted for through the Checkbook Accounting System Headquarters (CASH) and the Integrated Finance

MILWAUKEE PUBLIC SCHOOLS OFFICE OF AUDIT SERVICES Internal Controls and Other Procedures School funds are accounted for through the Checkbook Accounting System Headquarters (CASH) and the Integrated Finance

Schedule of Findings and Questioned Costs For the Year Ended December 31, 2011 SECTION II FINANCIAL STATEMENT FINDINGS

Schedule of Findings and Questioned Costs 2011-FS-1 Preparation of Financial Statements (Repeated from Prior Year) Finding Type. Material Weakness in Internal Control over Financial Reporting. Criteria.

Schedule of Findings and Questioned Costs 2011-FS-1 Preparation of Financial Statements (Repeated from Prior Year) Finding Type. Material Weakness in Internal Control over Financial Reporting. Criteria.

Brownfield ISD Business Office Procedures Manual

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

Brownfield ISD Business Office Procedures Manual Brownfield Independent School District 601 Tahoka Road, Brownfield, Texas 79316 Phone (806) 637-2591 Fax (806) 637-8934 Table of Contents Section 1 Introduction..

Dear Ms. Lawrence and Members of the Board of Commissioners:

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

It was also noted on the bank reconciliations that there was approximately $77,000 of staledated cheques that were not cleared off the outstanding che

August 3, 2017 Chief and Council Montreal Lake Cree Nation Box 106 Montreal Lake, Saskatchewan S0J 1Y0 Dear Chief and Council: 2017 MANAGEMENT LETTER During the course of our audit of Montreal Lake Cree

August 3, 2017 Chief and Council Montreal Lake Cree Nation Box 106 Montreal Lake, Saskatchewan S0J 1Y0 Dear Chief and Council: 2017 MANAGEMENT LETTER During the course of our audit of Montreal Lake Cree

FISCAL POLICIES AND PROCEDURES

FISCAL POLICIES AND PROCEDURES OVERVIEW The Board of Directors of HARRIET TUBMAN VILLAGE SCHOOL has reviewed and adopted the following policies and procedures to ensure the most effective use of the funds

FISCAL POLICIES AND PROCEDURES OVERVIEW The Board of Directors of HARRIET TUBMAN VILLAGE SCHOOL has reviewed and adopted the following policies and procedures to ensure the most effective use of the funds

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

Accounting Policies and Procedures Manual Wake Forest Area Chamber of Commerce Accounting Policies and Procedures Manual Table of Contents Contents Introduction... 3 Division of Duties... 4 Cash Receipts

AUDIT UNDP COUNTRY OFFICE AFGHANISTAN FINANCIAL MANAGEMENT. Report No Issue Date: 10 December 2013

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

UNITED NATIONS DEVELOPMENT PROGRAMME AUDIT OF UNDP COUNTRY OFFICE IN AFGHANISTAN FINANCIAL MANAGEMENT Report No. 1233 Issue Date: 10 December 2013 Table of Contents Executive Summary i I. Introduction

WASHOE COUNTY Integrity Communication Service

WASHOE COUNTY Integrity Communication Service www.washoecounty.us DATE: August 24, 2017 TO: FROM: STAFF REPORT BOARD MEETING DATE: September 26, 2017 Board of County Commissioners Alison Gordon Internal

WASHOE COUNTY Integrity Communication Service www.washoecounty.us DATE: August 24, 2017 TO: FROM: STAFF REPORT BOARD MEETING DATE: September 26, 2017 Board of County Commissioners Alison Gordon Internal

2016 Self-Employment Questionnaire

2016 Self-Employment Questionnaire Thank you for completing this questionnaire completely and accurately. This is a very important step in analyzing your tax position for the year. By doing so, you provide

2016 Self-Employment Questionnaire Thank you for completing this questionnaire completely and accurately. This is a very important step in analyzing your tax position for the year. By doing so, you provide

AUDIT PROCEDURE SCHOOL GENERATED FUNDS AND REVIEW AND INTERNAL CONTROLS

AUDIT PROCEDURE SCHOOL GENERATED FUNDS AND REVIEW AND INTERNAL CONTROLS OBJECTIVE The overall objective of internal review is to assist administrators and support staff charged with financial responsibilities

AUDIT PROCEDURE SCHOOL GENERATED FUNDS AND REVIEW AND INTERNAL CONTROLS OBJECTIVE The overall objective of internal review is to assist administrators and support staff charged with financial responsibilities

Fiscal Policies and Procedures for County Councils. Responsibilities

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

Fiscal Policies and Procedures for County Councils Fiscal management policies established for county outreach and extension councils are based on the Missouri Revised Statutes, University of Missouri policies

26. PURCHASING CARD POLICY

26. PURCHASING CARD POLICY POLICY It is the policy of Scott County to have a Purchasing Card Program. This program is intended to replace blanket purchase orders, purchase orders used to purchase items

26. PURCHASING CARD POLICY POLICY It is the policy of Scott County to have a Purchasing Card Program. This program is intended to replace blanket purchase orders, purchase orders used to purchase items

OFFICE OF THE STATE COMPTROLLER

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

THOMAS P. DiNAPOLI COMPTROLLER STATE OF NEW YORK OFFICE OF THE STATE COMPTROLLER 110 STATE STREET ALBANY, NEW YORK 12236 GABRIEL F. DEYO DEPUTY COMPTROLLER DIVISION OF LOCAL GOVERNMENT AND SCHOOL ACCOUNTABILITY

Allegany County Public Schools

Financial Management Practices Audit Report Allegany County Public Schools January 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Financial Management Practices Audit Report Allegany County Public Schools January 2013 OFFICE OF LEGISLATIVE AUDITS DEPARTMENT OF LEGISLATIVE SERVICES MARYLAND GENERAL ASSEMBLY This report and any related

Cost Control Systems. Conclusion. Overview of Chapter Findings

The Santa Rosa County School District s cost control systems include internal auditing, financial auditing, asset management, inventory management, risk management, financial management, purchasing, and

The Santa Rosa County School District s cost control systems include internal auditing, financial auditing, asset management, inventory management, risk management, financial management, purchasing, and

Review of Audit Opinions and Management Letters

5 Review of Audit Opinions and Management Letters Summary Management letters provided by auditors on completion of annual audits provide a wealth of information on accounting and management issues in entities

5 Review of Audit Opinions and Management Letters Summary Management letters provided by auditors on completion of annual audits provide a wealth of information on accounting and management issues in entities

Agricultural Development Chapter ALABAMA AGRICULTURAL DEVELOPMENT AUTHORITY ADMINISTRATIVE CODE CHAPTER LOAN PROGRAMS

ALABAMA AGRICULTURAL DEVELOPMENT AUTHORITY ADMINISTRATIVE CODE CHAPTER 108-1-3 LOAN PROGRAMS TABLE OF CONTENTS 108-1-3-.01 Cattle Working Facilities Loan Program 108-1-3-.02 Commodity Barn Loan Program

ALABAMA AGRICULTURAL DEVELOPMENT AUTHORITY ADMINISTRATIVE CODE CHAPTER 108-1-3 LOAN PROGRAMS TABLE OF CONTENTS 108-1-3-.01 Cattle Working Facilities Loan Program 108-1-3-.02 Commodity Barn Loan Program

GENERAL ACCOUNTING POLICIES AND PROCEDURES MANUAL

Los Angeles Leadership Academy 2670 Griffin Avenue, Los Angeles, CA 90031 Ph. 213.381.8484 www.laleadership.org GENERAL ACCOUNTING POLICIES AND PROCEDURES MANUAL ACCOUNTING POLICIES Board Approved 09/09/2015

Los Angeles Leadership Academy 2670 Griffin Avenue, Los Angeles, CA 90031 Ph. 213.381.8484 www.laleadership.org GENERAL ACCOUNTING POLICIES AND PROCEDURES MANUAL ACCOUNTING POLICIES Board Approved 09/09/2015

FINANCIAL MANAGEMENT MANUAL

LAKE MICHIGAN AIR DIRECTORS CONSORTIUM FINANCIAL MANAGEMENT MANUAL This manual is the exclusive property of Lake Michigan Air Directors Consortium (LADCO) 2250 East Devon Avenue, Suite 250 Des Plaines,

LAKE MICHIGAN AIR DIRECTORS CONSORTIUM FINANCIAL MANAGEMENT MANUAL This manual is the exclusive property of Lake Michigan Air Directors Consortium (LADCO) 2250 East Devon Avenue, Suite 250 Des Plaines,

State Capitol Building Des Moines, Iowa

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

OFFICE OF AUDITOR OF STATE STATE OF IOWA State Capitol Building Des Moines, Iowa 50319-0006 Mary Mosiman, CPA Auditor of State Telephone (515) 281-5834 Facsimile (515) 242-6134 NEWS RELEASE Contact: Mary

Jefferson County Soil and Water Conservation District

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Jefferson County Soil and Water Conservation District Internal Controls Over Selected Financial Operations

O FFICE OF THE NEW YORK STATE COMPTROLLER DIVISION OF LOCAL GOVERNMENT & SCHOOL ACCOUNTABILITY Jefferson County Soil and Water Conservation District Internal Controls Over Selected Financial Operations

STATE OF NEVADA OFFICE OF LIEUTENANT GOVERNOR

STATE OF NEVADA OFFICE OF LIEUTENANT GOVERNOR AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 4 Background... 4 Scope and Objective... 5 Findings and Recommendations... 6 Financial

STATE OF NEVADA OFFICE OF LIEUTENANT GOVERNOR AUDIT REPORT Table of Contents Page Executive Summary... 1 Introduction... 4 Background... 4 Scope and Objective... 5 Findings and Recommendations... 6 Financial

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

TOWN OF BURLINGTON, MASSACHUSETTS MANAGEMENT LETTER JUNE 30, 2013 To the Honorable Board of Selectmen Town of Burlington, Massachusetts In planning and performing our audit of the financial statements

Tulane Purchasing Card Policies and Procedures

Tulane Purchasing Card Policies and Procedures I. Purpose The Purchasing Card program was established to provide a more efficient and cost-effective method for purchasing and paying for small dollar transactions,

Tulane Purchasing Card Policies and Procedures I. Purpose The Purchasing Card program was established to provide a more efficient and cost-effective method for purchasing and paying for small dollar transactions,

Advances (Including Petty Cash and Accounts Receivable)

") CORNELL UNIVERSITY POLICY LIBRARY Advances (Including Petty Cash and Accounts Receivable) Chapter: 21, Advances Revised: POLICY STATEMENT Cornell University provides advances of cash or other resources

CORNELL UNIVERSITY POLICY LIBRARY Advances (Including Petty Cash and Accounts Receivable) Chapter: 21, Advances Revised: POLICY STATEMENT Cornell University provides advances of cash or other resources

Allen ISD Travel Guidelines

Allen ISD Travel Guidelines 2015-2016 Table of Contents General Guidelines for Employee Travel 2-3 Local Travel 3 Out of District Travel 4 Meals 4-5 Lodging/Hotels 5-6 Air Fare 6 Car Rental/Personal Vehicle

Allen ISD Travel Guidelines 2015-2016 Table of Contents General Guidelines for Employee Travel 2-3 Local Travel 3 Out of District Travel 4 Meals 4-5 Lodging/Hotels 5-6 Air Fare 6 Car Rental/Personal Vehicle

Community Partnerships Program Eligible Costing Rules and Financial Management Guidelines

Community Partnerships Program Eligible Costing Rules and Financial Management Guidelines Top tips when preparing your budget... 2 What are eligible costs?... 3 I. Personnel, Payroll and other Compensation...

Community Partnerships Program Eligible Costing Rules and Financial Management Guidelines Top tips when preparing your budget... 2 What are eligible costs?... 3 I. Personnel, Payroll and other Compensation...

REPORT 2013/142. Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

INTERNAL AUDIT DIVISION REPORT 2013/142 Audit of accounts receivable and payable in the United Nations Operation in Côte d Ivoire Overall results relating to the effective management of accounts receivable

Travel Forms Effective November 1, 2018 Presented by Miranda Salvatore Accounts Payable

Travel Forms Effective November 1, 2018 Presented by Miranda Salvatore Accounts Payable Discussion Highlights New Forms Updated Forms Details of each form Day Travel Expense Form International Travel Request

Travel Forms Effective November 1, 2018 Presented by Miranda Salvatore Accounts Payable Discussion Highlights New Forms Updated Forms Details of each form Day Travel Expense Form International Travel Request

SAMPLE FISCAL POLICIES & PROCEDURES MANUAL: CANADIAN EDITION

SAMPLE FISCAL POLICIES & PROCEDURES MANUAL: CANADIAN EDITION Legal Disclaimer Please note that TREC does not provide legal advice. This sample Fiscal Policies and Procedures Manual discusses a topic of

SAMPLE FISCAL POLICIES & PROCEDURES MANUAL: CANADIAN EDITION Legal Disclaimer Please note that TREC does not provide legal advice. This sample Fiscal Policies and Procedures Manual discusses a topic of

INTERNAL CONTROLS AND OTHER PROCEDURES

MILWAUKEE PUBLIC SCHOOLS OFFICE OF BOARD GOVERNANCE-AUDIT SERVICES INTERNAL CONTROLS AND OTHER PROCEDURES School funds are accounted for through the Integrated Finance and Accounting System (IFAS). The

MILWAUKEE PUBLIC SCHOOLS OFFICE OF BOARD GOVERNANCE-AUDIT SERVICES INTERNAL CONTROLS AND OTHER PROCEDURES School funds are accounted for through the Integrated Finance and Accounting System (IFAS). The

Aphria Inc. CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED FEBRUARY 29, 2016 and FEBRUARY 28, 2015

CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED FEBRUARY 29, 2016 and FEBRUARY 28, 2015 (Unaudited, expressed in Canadian Dollars, unless otherwise noted) Notice of No Auditor

CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED FEBRUARY 29, 2016 and FEBRUARY 28, 2015 (Unaudited, expressed in Canadian Dollars, unless otherwise noted) Notice of No Auditor

Interior Health Authority Board Manual 3.6 DIRECTOR RETAINERS, FEES AND EXPENSES

1. INTRODUCTION (1) The Board of Directors (the Board ) is committed to the responsible use of public funds to support Board operations. This Policy reflects requirements of the Provincial Government,

1. INTRODUCTION (1) The Board of Directors (the Board ) is committed to the responsible use of public funds to support Board operations. This Policy reflects requirements of the Provincial Government,

MOJAVE WATER AGENCY PURCHASING POLICY

MOJAVE WATER AGENCY PURCHASING POLICY PURCHASING POLICY 01/13/2011 TABLE OF CONTENTS SECTION PAGE No. 1.0 INTRODUCTION 1.1 Purpose 1 1.2 Scope and Intent 1 1.3 Authority to Purchase 1 1.4 Ethical Conduct

MOJAVE WATER AGENCY PURCHASING POLICY PURCHASING POLICY 01/13/2011 TABLE OF CONTENTS SECTION PAGE No. 1.0 INTRODUCTION 1.1 Purpose 1 1.2 Scope and Intent 1 1.3 Authority to Purchase 1 1.4 Ethical Conduct

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

OKLAHOMA CITY BOARD OF EDUCATION OKLAHOMA CITY PUBLIC SCHOOLS TRAVEL EXPENSE APPROVAL, DOCUMENTATION, AND REIMBURSEMENT ADMINISTRATIVE REGULATION

OKLAHOMA CITY PUBLIC SCHOOLS TRAVEL EXPENSE APPROVAL, DOCUMENTATION, AND REIMBURSEMENT ADMINISTRATIVE REGULATION SUMMARY AND RESPONSIBILITIES The Board of Education believes that professional growth is

OKLAHOMA CITY PUBLIC SCHOOLS TRAVEL EXPENSE APPROVAL, DOCUMENTATION, AND REIMBURSEMENT ADMINISTRATIVE REGULATION SUMMARY AND RESPONSIBILITIES The Board of Education believes that professional growth is

Eligible Expenses and Cost Instructions

Eligible Expenses and Cost Instructions June 2018 Table of Contents 1 SALARIES, BENEFITS AND LABOUR COSTS... 4 1.1 Salary and Labour... 4 1.2 Employee Benefits... 4 2 INDIRECT AND ADMINISTRATIVE EXPENSES...

Eligible Expenses and Cost Instructions June 2018 Table of Contents 1 SALARIES, BENEFITS AND LABOUR COSTS... 4 1.1 Salary and Labour... 4 1.2 Employee Benefits... 4 2 INDIRECT AND ADMINISTRATIVE EXPENSES...

Delaware Design-Lab High School Accounting Manual

Delaware Design-Lab High School Accounting Manual I. INTRODUCTION This manual sets forth the general budgeting and accounting policies/procedures that are to be followed by Delaware Design Lab High School

Delaware Design-Lab High School Accounting Manual I. INTRODUCTION This manual sets forth the general budgeting and accounting policies/procedures that are to be followed by Delaware Design Lab High School

The 2009 Farm and Ranch Water Infrastructure Program Regulations

Consolidated to March 29, 2011 1 INFRASTRUCTURE PROGRAM F-8.001 REG 38 The 2009 Farm and Ranch Water Infrastructure Program Regulations being Chapter F-8.001 Reg 38 (effective April 30, 2009) as amended

Consolidated to March 29, 2011 1 INFRASTRUCTURE PROGRAM F-8.001 REG 38 The 2009 Farm and Ranch Water Infrastructure Program Regulations being Chapter F-8.001 Reg 38 (effective April 30, 2009) as amended

Audit Report 2018-A-0011 Town of Glen Ridge Revenue and Credit Cards

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Town of Glen Ridge Revenue and Credit Cards July 16, 2018 Insight Oversight

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report Town of Glen Ridge Revenue and Credit Cards July 16, 2018 Insight Oversight

Audit Report 2018-A-0001 City of Lake Worth Water Utility Services

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report City of Lake Worth Water Utility Services December 18, 2017 Insight Oversight

PALM BEACH COUNTY John A. Carey Inspector General Inspector General Accredited Enhancing Public Trust in Government Audit Report City of Lake Worth Water Utility Services December 18, 2017 Insight Oversight

SANTA BARBARA COUNTY EMPLOYEES RETIREMENT SYSTEM TRUSTEE TRAVEL POLICY I. PURPOSE

SANTA BARBARA COUNTY EMPLOYEES RETIREMENT SYSTEM TRUSTEE TRAVEL POLICY I. PURPOSE The purpose of this Trustee Travel Policy is to encourage and facilitate the pursuit of relevant educational and business-related

SANTA BARBARA COUNTY EMPLOYEES RETIREMENT SYSTEM TRUSTEE TRAVEL POLICY I. PURPOSE The purpose of this Trustee Travel Policy is to encourage and facilitate the pursuit of relevant educational and business-related

RECOMMENDED RETENTION PERIOD

TO: CHIEF FINANCIAL OFFICERS - IDA JURISDICTION FIRMS PANEL AUDITORS - IDA JURISDICTION FIRMS May 15, 1992 C-38 RECORD The purpose of this interpretation bulletin is to set out the record retention guidelines

TO: CHIEF FINANCIAL OFFICERS - IDA JURISDICTION FIRMS PANEL AUDITORS - IDA JURISDICTION FIRMS May 15, 1992 C-38 RECORD The purpose of this interpretation bulletin is to set out the record retention guidelines

Spencer CPA & Associates, P.L.L.C.

Spencer CPA & Associates, P.L.L.C. PO Box 2560 74 East Main Street Buckhannon, WV 26201 Buckhannon, WV 26201 Phone: (304)472-1928 Fax: (304)472-1951 Member: American Institute of Certified Public Accountants

Spencer CPA & Associates, P.L.L.C. PO Box 2560 74 East Main Street Buckhannon, WV 26201 Buckhannon, WV 26201 Phone: (304)472-1928 Fax: (304)472-1951 Member: American Institute of Certified Public Accountants

Accounting Records: How They Are Used To Conceal Fraud

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

: How They Are Used To Conceal Fraud ACFE 2012 Canadian Conference October 29, 2012 Rosanne Terhart, CA, CFE Overview Summary of Topics Which records are used to conceal fraud What evidence of fraud do

ASD INTERNAL AUDIT REPORT

ASD INTERNAL AUDIT REPORT 2016-02 July 21, 2016 MUNICIPALITY OF ANCHORAGE Internal Audit Department 632 W 6th Avenue, Suite 600 P.O. Box 196650 Anchorage, Alaska 99519-6650 www.muni.org/departments/intern

ASD INTERNAL AUDIT REPORT 2016-02 July 21, 2016 MUNICIPALITY OF ANCHORAGE Internal Audit Department 632 W 6th Avenue, Suite 600 P.O. Box 196650 Anchorage, Alaska 99519-6650 www.muni.org/departments/intern

The Importance of Sound Financial Policies and Procedures

The Importance of Sound Financial Policies and Procedures Presented by Michael Holton Holton Healthcare Consulting, Inc. Raleigh, NC mholton@holtonhealthcare.com www.holtonhealthcare.com 0 Understand the

The Importance of Sound Financial Policies and Procedures Presented by Michael Holton Holton Healthcare Consulting, Inc. Raleigh, NC mholton@holtonhealthcare.com www.holtonhealthcare.com 0 Understand the

Chapter 3: Results of Audits in the Government Reporting Entity

Chapter 3: Results of Audits in the Government Reporting Entity Why we did this work: To summarize matters reported to management and boards There are about 100 entities outside of core government These

Chapter 3: Results of Audits in the Government Reporting Entity Why we did this work: To summarize matters reported to management and boards There are about 100 entities outside of core government These

OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL

September 4, 2018 AR-01-39-18 THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL AUDIT OF THE ADMINISTRATIVE FUNCTIONS OF THE VIRGIN ISLANDS CASINO CONTROL COMMISSION ILLEGAL

September 4, 2018 AR-01-39-18 THE UNITED STATES VIRGIN ISLANDS OFFICE OF THE VIRGIN ISLANDS INSPECTOR GENERAL AUDIT OF THE ADMINISTRATIVE FUNCTIONS OF THE VIRGIN ISLANDS CASINO CONTROL COMMISSION ILLEGAL

Accounts Payable Policies and Procedures

Accounts Payable Policies and Procedures Updated December 6th, 2018 Table of Contents General Information... 1 1.0 Policies for Allowable Business Expenses... 2 1.1 Business Travel Expenses... 2 1.2 Meals...

Accounts Payable Policies and Procedures Updated December 6th, 2018 Table of Contents General Information... 1 1.0 Policies for Allowable Business Expenses... 2 1.1 Business Travel Expenses... 2 1.2 Meals...

Accounting Policies and Procedures Manual

Accounting Policies and Procedures Manual TABLE OF CONTENTS Page No, INTRODUCTION... 1 FISCAL YEAR OF ORGANIZATION... 1 FINANCIAL OPERATIONS, GENERAL LEDGER AND CHART OF ACCOUNTS... 2 GENERAL LEDGER AND

Accounting Policies and Procedures Manual TABLE OF CONTENTS Page No, INTRODUCTION... 1 FISCAL YEAR OF ORGANIZATION... 1 FINANCIAL OPERATIONS, GENERAL LEDGER AND CHART OF ACCOUNTS... 2 GENERAL LEDGER AND

Stop Fraud in Your Office. Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA

McGarrity, Esq., CPA") Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals

Stop Fraud in Your Office Presented by: Margaret A. (Peggy) McGarrity, Esq., CPA 1 White-Collar Crime EDWIN H. SUTHERLAND 1939 First defined white-collar crime Criminal acts of corporations Individuals