SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA

|

|

|

- Bartholomew Wheeler

- 6 years ago

- Views:

Transcription

1 SEMINAR ON TAX DEDUCTED AT SOURCE PRESENTED BY CA B. D SOUZA

2 IS TDS TEDIOUS???

3 SET UP OF TDS

which is a ten digit alpha numeric number.")

4 TAN (TAX DEDUCTION ACCOUNT NUMBER) Every deductor is required to obtain a unique identification number called TAN (Tax Deduction Account Number) which is a ten digit alpha numeric number. This number has to be quoted by the deductor in every correspondence related to TDS

5 PAYMENTS COVERED UNDER SCHEME OF TDS (FOR CHARITABLE TRUSTS) Salary (Sec.192) Payments to Contractors and Subcontractors (Sec.194C) Commission or Brokerage (Sec. 194H) Rent (Sec. 194I) Payment on transfer of Certain immovable property other than Agricultural Land (Sec.194IA) Fees for Technical or Professional Services (Sec. 194J)

6 SALARY (Section. 192 (B)) Payer Employer Who is the payer Employer Who is the recipient Recipient Employee Employee Payment Covered Payment Taxable Salary Covered of the employee Taxable Salary of the employee At what time TDS to be deducted At the time of payment TDS Maximum to be amount deducted which can be paid without tax At deduction the time of payment The amount of exemption limit (i.e.,rs /190000/ for A.Y ) Rate at which tax to be deducted. Maximum As per Calculation amount which can be The amount of exemption limit paid When without the provisions tax deduction are not applicable (i.e.,rs.250,000 for A.Y ) -- if the total income is less than Is it possible to get the payment without tax deduction or with lower tax deduction The employee can make application in Form No , to the Assessing then Officer the to get exemption the certificate of lower tax deduction or no tax deduction. Rate at which tax to be deducted. limit is Rs. 300, As per Calculation

7 PAYMENTS TO CONTRACTORS (Section. 194 (C)) Payer Recipient Rate of TDS Payments Covered under the Section Basic Limit Point of Deduction Specified Person Any Resident Person 2% for persons other than individuals 1% for Individuals All types of Contract works i.e. Payments to civil contractors, printers, caterers, tour operators, advertisements, decorators etc. Rs. 30, incase of single payment; or Rs. 1,00, incase of series of payment (i.e. aggregate of all payments) throughout the year. At the time of payment OR at the time of credit (Even advances are considered as payments)

or H ( then the contractor")

8 HOW TO FIND WHETHER THE CONTRACTOR IS AN INDIVIDUAL OF HUF If the 4 letter of the PAN of Contractor is P (as shown below then the Contractor is an individual) or H ( then the contractor is an HUF)

9 RENT (Section. 194 (I)) Payer Recipient Rate of TDS 10% Payments Covered under the Section Basic Limit Point of Deduction Any Person paying Rent(other than individual and HUF) Any Resident Person Rent rent includes all payments for use of Land, Building, Machinery, Plant, equipments, Furniture and Fittings Rs. 180, either through single payment or through series of payments in a financial year At the time of payment or at the time of credit (Even advances are considered as payments)

10 PAYMENT ON TRANSFER OF CERTAIN IMMOVABLE PROPERTY OTHER THAN AGRICULTURAL LAND (Section. 194 (IA)) Payer Recipient Rate of TDS 1% Payments Covered under the Section Any Person Purchasing Land or Buildings other than agricultural Land Any person who is transferring the Immovable Property Basic Limit Rs. 50,00, Point of Deduction Sale of all immovable property other than Agricultural Land At the time of payment or at the time of credit (Even advances are considered as payments if exceeding the limit)

11 FEES FOR PROFESSIONAL OR TECHNICAL SERVICES (Section. 194 (J)) Payer Recipient Rate of TDS 10% Payments Covered under the Section Basic Limit Point of Deduction All persons other than individual and HUF Any Resident Person All types of Payments for Professional and Technical Services Professionals includes Advocates, Chartered Accountants, Doctors, Architects and Engineers etc. Technical Services Includes Smart Class Payments, Royalty, software Development etc. Rs. 30, per Year At the time of payment OR at the time of credit (Even advances are considered as payments)

12 FEES FOR TECHNICAL SERVICES - SMART CLASSES (Section. 194 (J)) Payer Recipient Rate of TDS 10% Payments Covered under the Section Basic Limit Point of Deduction All persons other than individual and HUF Any Resident Person All types of Payments for smart classes for the content and services (including installation charges). Payments for Hardware portion does not attract TDS provided VAT paid separate bills are obtained. Rs. 30, per Year At the time of payment OR at the time of credit (Even advances are considered as payments)

13 OTHER PROVISIONS If PAN is not provided/or if the deductee does not have PAN then Tax has to deducted at the rate of 20%.

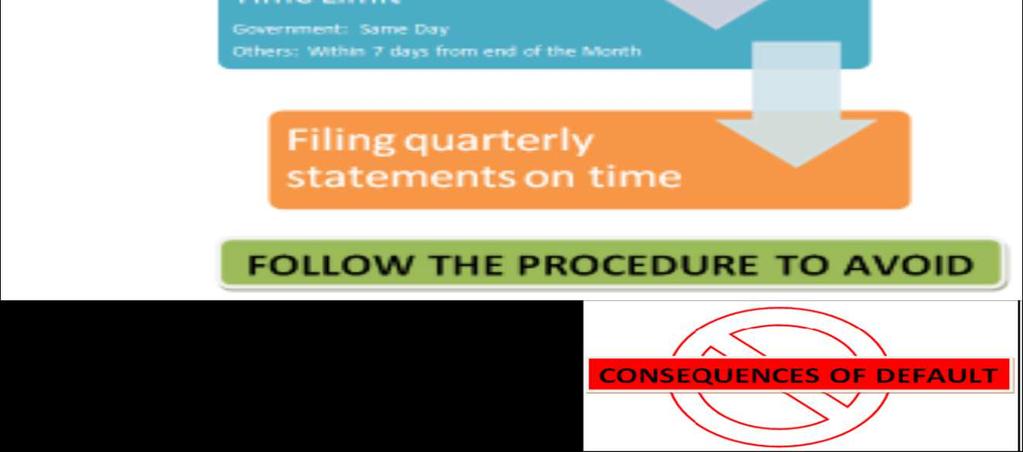

14 TIME LIMIT FO PAYMENT OF TAX DEDUCTED AT SOURCE DEDUCTOR APRIL TO FEBRUARY MARCH Government All other Persons On or before 7 th of Next month for Salary and On the same day for other than salary On or before 7 th of Next month in which tax was deducted On or before 7 th of April On or before 30 th of April

15 CHALLAN FOR PAYMENT OF TAX DEDUCTED AT SOURCE (ITNS 281)

16 RETURN TYPE RETURN TYPE Salary Returns Returns other than salary Returns PERIODICITY Quarterly in Form No. 24Q Quarterly in Form No. 26Q

17 TIME LIMIT FOR PAYMENT OF FILING OF TDS RETURNS Quarter - 1 (April to June) QUARTER Quarter 2 (July to September) DUEDATE FOR FILING QUARTERLY RETURN On or before 15 th July On or before 15 th October Quarter 3 (October to December) Quarter 4 (January to March) On or before 15 th January On or before 15 th May

18 TIME LIMIT FOR ISSUE OF TDS CERTIFICATES (Sec. 203) Form No. 16 CERTIFICATE 31 st May DUEDATE FOR ISSUE Form No. 16A Within 15 days from the date of filing the Form 26Q

19 PENAL PROVISIONS NATUREOF DEFAULT Failure to Deduct Tax (Sec.201 (1)) Failure to Deposit the tax deducted at source (Sec.201(1A) and Sec.276B) Failure to Apply for TAN (Tax Deduction Account Number) (Sec.203A and Sec.272BB) INTEREST, PENALTY AND PROSECUTION Penalty : Amount equal to tax not deducted Interest : 1% per month from the date from which tax is not deducted till the date deduction. Interest : 1.5% per month from the date of deduction till the date of Deposit. Prosecution : Rigorous Imprisonment for a term which shall not less than 3 months but may extend to 7 years with Fine Penalty : Rs. 10,000.00

20 PENAL PROVISIONS CONTINUED. NATUREOF DEFAULT Failure to Furnish Returns within due date (Sec. 200(3) and Sec. 272A(2)(k)) Failure to issue TDS certificates within the time limit prescribed (Sec.272A(2)(g)) INTEREST, PENALTY AND PROSECUTION Penalty : Rs per day during which the failure continues subject to maximum of TDS amount Penalty : Rs per day during which the failure continues subject to maximum of TDS amount

21 SO TDS IS TEDIOUS UNLESS COMPLIED

22 QUESTIONS???

23 THANK YOU

TDS Seminar for Residents Welfare Associations

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

TDS Seminar for Residents Welfare Associations 27 th July 2018 What is TDS? Mode of quick and efficient collection of taxes Tax deducted at the point of generation of income Tax deducted by the payer &

CA RAKESH M. VORA. R P J & ASSOCIATES Chartered Accountants

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

PENALTY, INTEREST & SURVEY (TDS) 12/02/2011 SANGHVI SANGHVI & SANGHVI

12/02/2011 SANGHVI SANGHVI & SANGHVI") 12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

12/02/2011 SANGHVI SANGHVI & SANGHVI 1 PENAL AND OTHER CONSEQUENCES FOR NON- COMPLIANCE WITH THE PROVISIONS OF TDS DISALLOWANCE OF EXPENDITURE Sec. 40(a)(i) : Expenditure in respect of certain payments

T.D.S/T.C.S AT GLANCE FOR A.Y

T.D.S/T.C.S AT GLANCE FOR A.Y. 2012-2013 Tax Deducted at Source (TDS) was introduced to facilitate the payment of Tax while receiving the income and it follows the concept Pay as you Earn. The tax deducted

T.D.S/T.C.S AT GLANCE FOR A.Y. 2012-2013 Tax Deducted at Source (TDS) was introduced to facilitate the payment of Tax while receiving the income and it follows the concept Pay as you Earn. The tax deducted

Tax Deduction at Source FY (AY )

") Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

CA. Mehul Shah. Payment to Transport Contractors implications under the Income-tax Act Overview of Companies Act Care, Pair, and Share

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

PUNJAB STATE TRANSMISSION CORPORATION LIMITED

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

PUNJAB STATE TRANSMISSION CORPORATION LIMITED (Regd. Office: PSEB, Head Office, The Mall, Patiala-147001, Punjab, India) Corporate Identity Number - U40109PB2010SGC033814, Office of CFO, AO/Taxation, Shakti

TDS & TCS Recent Updates & Amendments.

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

E-TDS FILING PRESENTED BY. Vinod Kumar Jain FCA

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

Practical difficulties for TDS returns & Previous year defaults.

Practical difficulties for TDS returns & Previous year defaults. Topics covered Basics of TDS TRACES introduction Procedure of TDS return Revision of TDS return Notice and reasons for defaults Causes of

Practical difficulties for TDS returns & Previous year defaults. Topics covered Basics of TDS TRACES introduction Procedure of TDS return Revision of TDS return Notice and reasons for defaults Causes of

Taxation Laws & Property

& Property Service Tax Applicable only on purchase of under construction properties w.e.f. 1.7.2010 Property is under construction till builder receives Completion Certificate (CC). Service Tax NA if full

& Property Service Tax Applicable only on purchase of under construction properties w.e.f. 1.7.2010 Property is under construction till builder receives Completion Certificate (CC). Service Tax NA if full

DEDUCTION, COLLECTION AND RECOVERY OF TAX

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

DEDUCTION, COLLECTION AND RECOVERY OF TAX Section Particulars 190 different modes of payment of tax: tds, tcs, advance tax, tax u/s 192(1A) 191 failure to deduct tax, and direct payment of tax 192 tds

Note on Tax Deduction at Source

www.legale-services.com Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting

www.legale-services.com Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting

Presentation on TDS Salary & TDS in respect of Residents

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

Presentation on TDS Salary & TDS in respect of Residents R. J. Soni & Associates Corporate Office: MUMBAI Kamla Niwas Plot No. 136/141 Gorai-1 Borivali (W) Mumbai-091. Offices:- MUMBAI JAIPUR PUNE AHEMDABAD

In the Financial World TDS is Tax deducted at. TDS contributes 40% to the gross direct tax

In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance.

In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance.

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f. 01.06.2016 There are continuous changes in the Tax Deduction at Source/Tax Collection at source provisions of Income tax Act from year to year. During this year

RECENT AMENDMENTS REGARDING TDS/TCS w.e.f. 01.06.2016 There are continuous changes in the Tax Deduction at Source/Tax Collection at source provisions of Income tax Act from year to year. During this year

UNION BUDGET

UNION BUDGET 2017-18 Hon ble Prime Minister Narendra Modi has shown his determination to come heavily on tax evaders. He has also shown his commitment to eliminate high value cash transactions from the

UNION BUDGET 2017-18 Hon ble Prime Minister Narendra Modi has shown his determination to come heavily on tax evaders. He has also shown his commitment to eliminate high value cash transactions from the

Amendments. in Withholding Taxes in India ( )

") Amendments in Withholding Taxes in India (009-) TM About Floraison floraison in French means 'flowering'. The name reflects our objective of Accelerating Growth. Floraison India Compliances Private Limited

Amendments in Withholding Taxes in India (009-) TM About Floraison floraison in French means 'flowering'. The name reflects our objective of Accelerating Growth. Floraison India Compliances Private Limited

F6 PKN TAX RATES AND ALLOWANCES JUNE AND DECEMBER 2016

F6 PKN TAX RATES AND ALLOWANCES JUNE AND DECEMBER 2016 The following tax rates and allowances for the tax year 2016 are to be used in answering the questions. A. Tax rates for salaried individuals where

F6 PKN TAX RATES AND ALLOWANCES JUNE AND DECEMBER 2016 The following tax rates and allowances for the tax year 2016 are to be used in answering the questions. A. Tax rates for salaried individuals where

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

TRACES Site and Issues in Deemed, Recovery & online resolution

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

VAT IMPLICATIONS ON REAL ESTATE TRANSACTIONS UNDER DELHI VAT ACT, 2004 BY

VAT IMPLICATIONS ON REAL ESTATE TRANSACTIONS UNDER DELHI VAT ACT, 2004 BY CA. H.L. MADAN Former Vice President Sales Tax Bar Association, Delhi General Secretary All India Federation of Tax Practitioners

VAT IMPLICATIONS ON REAL ESTATE TRANSACTIONS UNDER DELHI VAT ACT, 2004 BY CA. H.L. MADAN Former Vice President Sales Tax Bar Association, Delhi General Secretary All India Federation of Tax Practitioners

TDS & TCS RATE CHART FY

TDS & TCS RATE CHART FY 2017-18 Sl. No Section Of Act Nature of Payment in brief Threshold Limit Rate % From 01.04.17 to 31.03.18 HUF/IND Others 1 192 Salaries Salary income must be more than exemption

TDS & TCS RATE CHART FY 2017-18 Sl. No Section Of Act Nature of Payment in brief Threshold Limit Rate % From 01.04.17 to 31.03.18 HUF/IND Others 1 192 Salaries Salary income must be more than exemption

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Tax deducted at source For the Financial year

Tax deducted at source For the Financial year 2016-17 A summary list of tax deductible from a resident, a nonresident and other persons CA K. Balachandran FCA, Coimbatore TDS summary for the AY 2017-18

Tax deducted at source For the Financial year 2016-17 A summary list of tax deductible from a resident, a nonresident and other persons CA K. Balachandran FCA, Coimbatore TDS summary for the AY 2017-18

NEWSLETTER. M. V. DAMANIA & Co. Chartered Accountants CONTENTS

NEWSLETTER M. V. DAMANIA & Co. Chartered Accountants CONTENTS INTERNATIONAL TAX Allen & Hamilton & Co. - Mumbai Tribunal Bosch Ltd. - Bangalore Tribunal DIRECT TAX J.V.Krishna Rao - Hyderabad Tribunal

NEWSLETTER M. V. DAMANIA & Co. Chartered Accountants CONTENTS INTERNATIONAL TAX Allen & Hamilton & Co. - Mumbai Tribunal Bosch Ltd. - Bangalore Tribunal DIRECT TAX J.V.Krishna Rao - Hyderabad Tribunal

BCAS LECTURE MEETING 20 st May by CA Raman Jokhakar B. D. Jokhakar & Co.

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST

TDS MECHANISM UNDER GST") GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST Tax Deduction at Source (TDS) is a system, initially introduced by the Income Tax Department. It is one of the modes/methods to collect tax, under which,

GST (GOODS AND SERVICES TAX) TDS MECHANISM UNDER GST Tax Deduction at Source (TDS) is a system, initially introduced by the Income Tax Department. It is one of the modes/methods to collect tax, under which,

As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017.

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

A BUDGET FOR A Y From the desk of - B.L. Tulsian Advocate. R. Tulsian & Co LLP Chartered Accountants.

A BUDGET A N A L Y S I S FOR A Y 2020-21 From the desk of - B.L. Tulsian Advocate R. Tulsian & Co LLP Chartered Accountants www.rtulsian.com Page2 Contents Amendment of Section 16... 3 Amendment to Section

A BUDGET A N A L Y S I S FOR A Y 2020-21 From the desk of - B.L. Tulsian Advocate R. Tulsian & Co LLP Chartered Accountants www.rtulsian.com Page2 Contents Amendment of Section 16... 3 Amendment to Section

WESTERN INDIA REGIONAL COUNCIL OF ICAI

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

16. TAX DEDUCTED AT SOURCE PROBLEM NO: 1

SOLUTIONS TO PROBLEMS FOR CLASSROOM DISCUSSION 16. TAX DEDUCTED AT SOURCE PROBLEM NO: 1 In this case, the individual contract payments made to Mr. X does not exceed Rs. 30,000. However, since the aggregate

SOLUTIONS TO PROBLEMS FOR CLASSROOM DISCUSSION 16. TAX DEDUCTED AT SOURCE PROBLEM NO: 1 In this case, the individual contract payments made to Mr. X does not exceed Rs. 30,000. However, since the aggregate

As approved by Income Tax Department

As approved by Income Tax Department "Form No. 26Q [See section 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, 194LA, and rule 31A] Quarterly statement of deduction of tax

As approved by Income Tax Department "Form No. 26Q [See section 193, 194, 194A, 194B, 194BB, 194C, 194D, 194EE, 194F, 194G, 194H, 194I, 194J, 194LA, and rule 31A] Quarterly statement of deduction of tax

Income Tax Reckoner AY:

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS Gautam Nayak Chartered Accountant BCAS Seminar 29 th August 2009 Rates of Taxes Substantial increase

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS Gautam Nayak Chartered Accountant BCAS Seminar 29 th August 2009 Rates of Taxes Substantial increase

FINANCE BILL He has proposed to revise the tax slabs upwards as under:

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

TDS / TCS IMPLICATIONS ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS

TDS / TCS IMPLICATIONS Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

TDS / TCS IMPLICATIONS Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

TAXATION ON SALE AND PURCHASE OF PROPERTY REAL ESTATE SUMMIT 2016

TAXATION ON SALE AND PURCHASE OF PROPERTY BRIEF INTRODUCTION Service tax is presently calculated at the rate of 15% of the gross value of the property. But as there is a government abatement of 75% (increased

TAXATION ON SALE AND PURCHASE OF PROPERTY BRIEF INTRODUCTION Service tax is presently calculated at the rate of 15% of the gross value of the property. But as there is a government abatement of 75% (increased

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED

![NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED](/thumbs/78/78635266.jpg "NOTIFICATION NO. 31/2009[F.NO.142/22/2008-TPL]/S.O.858(E), DATED") INCOME-TAX (EIGHT AMENDMENT) RULES, 2009 - AMENDMENT IN RULES 24Q AND 26Q; SUBSTITUTION OF RULES 30, 31, 31A, 31AA, 37CA, 37D AND FORMS 16, 16A, 16AA, 27D, 27Q AND 27EQ; INSERTION OF FORM 24C; OMISSION

INCOME-TAX (EIGHT AMENDMENT) RULES, 2009 - AMENDMENT IN RULES 24Q AND 26Q; SUBSTITUTION OF RULES 30, 31, 31A, 31AA, 37CA, 37D AND FORMS 16, 16A, 16AA, 27D, 27Q AND 27EQ; INSERTION OF FORM 24C; OMISSION

SyNoPSIS of the FINaNce BILL, 2017

SyNoPSIS of the FINaNce BILL, 2017 By PaRaS KocHaR, advocate The following changes in the finance bill has been proposed by the Hon ble Finance Minister to the Income Tax Act, 1961 from 01-04-2017 TAX

SyNoPSIS of the FINaNce BILL, 2017 By PaRaS KocHaR, advocate The following changes in the finance bill has been proposed by the Hon ble Finance Minister to the Income Tax Act, 1961 from 01-04-2017 TAX

CHANGES IN INCOME TAX BY UNION BUDGET 2017

CHANGES IN INCOME TAX BY UNION BUDGET 2017 CA SOHRABH JINDAL The Hon ble Finance Minister has announced the Union Budget 2017 on 1-2-2017. There are various changes in Law related to Income Tax. I have

CHANGES IN INCOME TAX BY UNION BUDGET 2017 CA SOHRABH JINDAL The Hon ble Finance Minister has announced the Union Budget 2017 on 1-2-2017. There are various changes in Law related to Income Tax. I have

TDS Provisions and Compliances under GST

GST Alert 09/2018-19 Date 15.09.2018 TDS Provisions and Compliances under GST Government vide Notification No. 33/2017-Central Tax dated 15.09.2017 had notified Section 51 of CGST Act, 2017 relating Tax

GST Alert 09/2018-19 Date 15.09.2018 TDS Provisions and Compliances under GST Government vide Notification No. 33/2017-Central Tax dated 15.09.2017 had notified Section 51 of CGST Act, 2017 relating Tax

CONTENTS CONTENTS BOOK ONE : DEDUCTION OF TAX AT SOURCE DEDUCTION OF TAX AT SOURCE FROM SALARY

CONTENTS Chapter-heads I-7 BOOK ONE : DEDUCTION OF TAX AT SOURCE 1 DEDUCTION OF TAX AT SOURCE FROM SALARY 1.1 Who is responsible to deduct tax at source in case of income from salary 4 1.1-1 Where salary

CONTENTS Chapter-heads I-7 BOOK ONE : DEDUCTION OF TAX AT SOURCE 1 DEDUCTION OF TAX AT SOURCE FROM SALARY 1.1 Who is responsible to deduct tax at source in case of income from salary 4 1.1-1 Where salary

Dr. BashirAhmad Joo. Human Resource Development Center University of Kashmir. The Business School University Of Kashmir.

Management of Tax Liability for Salaried Individuals Presentation By Dr. BashirAhmad Joo Professor The Business School University Of Kashmir 0n 11 th March, 2017 Human Resource Development Center University

Management of Tax Liability for Salaried Individuals Presentation By Dr. BashirAhmad Joo Professor The Business School University Of Kashmir 0n 11 th March, 2017 Human Resource Development Center University

The Central Goods and Services Tax Bill, Returns. Arun Kumar Agarwal. 5-May-17

The Central Goods and Services Tax Bill, 2017 Returns Arun Kumar Agarwal info@arsconsultants.net www.arsconsultants.net 1 Statutory Provisions: Chapter Sections 37 to 48 VIII info@arsconsultants.net www.arsconsultants.net

The Central Goods and Services Tax Bill, 2017 Returns Arun Kumar Agarwal info@arsconsultants.net www.arsconsultants.net 1 Statutory Provisions: Chapter Sections 37 to 48 VIII info@arsconsultants.net www.arsconsultants.net

Budget 2017 Synopsis Part II Analysis of Rupiya

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

ALL GUJARAT FEDERATION OF TAX CONSULTANTS Seminar on 14/9/2011

ALL GUJARAT FEDERATION OF TAX CONSULTANTS Seminar on 14/9/2011 PRESUMPTIVE TAXATION U/S 44AD OF THE ACT - CA Sanjay R. Shah, Ahmedabad (1) (a) Section 44AD : Upto Assessment Year 2010-11 (1) Applicable

ALL GUJARAT FEDERATION OF TAX CONSULTANTS Seminar on 14/9/2011 PRESUMPTIVE TAXATION U/S 44AD OF THE ACT - CA Sanjay R. Shah, Ahmedabad (1) (a) Section 44AD : Upto Assessment Year 2010-11 (1) Applicable

RATES OF INCOME-TAX. Nil

1 of 33 07-Oct-11 2:10 AM CIRCULAR INCOME-TAX ACT Section 192 of the Income-tax Act, 1961 - Deduction of tax at source - Salaries - Income-tax deduction from salaries during the financial year 2010-11

1 of 33 07-Oct-11 2:10 AM CIRCULAR INCOME-TAX ACT Section 192 of the Income-tax Act, 1961 - Deduction of tax at source - Salaries - Income-tax deduction from salaries during the financial year 2010-11

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime

Provisions in GST Regime") Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Webinar on Tax Deduction at Source (TDS) Provisions in GST Regime Mr Rajeev Agarwal, IRS Sr.VP, GSTN In association with National e Governance Division, Department of Electronics & Information Technology

Income Tax Frequently Asked Questions

Income Tax Frequently Asked Questions A. General 1. What is Income Tax? It is a tax imposed by the Government of India on any body who earns income in India. This tax is levied on the strength of an Act

Income Tax Frequently Asked Questions A. General 1. What is Income Tax? It is a tax imposed by the Government of India on any body who earns income in India. This tax is levied on the strength of an Act

INDIA BUDGET,2009 Analysis of important provisions July 13, 2009 (Budget presented on 6 th July 2009)

") INDIA BUDGET,2009 Analysis of important provisions July 13, 2009 (Budget presented on 6 th July 2009) Doing common things, Uncommonly well. July 13 2009 A Finance & Accounts Outsourcing Company A Finance

INDIA BUDGET,2009 Analysis of important provisions July 13, 2009 (Budget presented on 6 th July 2009) Doing common things, Uncommonly well. July 13 2009 A Finance & Accounts Outsourcing Company A Finance

EXECUTIVE SUMMARY FEMA Regulations

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

Doha Chapter of ICAI 5 th January 2014 Relevant Changes in FEMA regulations and Direct & Indirect Taxation affecting Real Estate Transactions, with reference to NRI by CA R.BUPATHY PAST PRESIDENT - ICAI

Annexure to Circular No. CTD/Circ./TDS/ /01 dated

OIL AND NATURAL GAS CORPORATION LTD. CORPORATE TAX DIVISION Old Secretariat Building, Tel Bhawan Dehra Dun- 248 003 Tel: 0135-2793833 Fax: 0135-2758518 Annexure to Circular No. CTD/Circ./TDS/2017-18/01

OIL AND NATURAL GAS CORPORATION LTD. CORPORATE TAX DIVISION Old Secretariat Building, Tel Bhawan Dehra Dun- 248 003 Tel: 0135-2793833 Fax: 0135-2758518 Annexure to Circular No. CTD/Circ./TDS/2017-18/01

Who can use this form Who cannot use this form Mode of filing. Individuals whose total income includes:

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y. 2013-2014 AMENDMENTS IN FINANCE ACT, 2012 HAVING IMPACT ON TAX AUDIT REPORT Rule 12 From A.Y. 2013-14 inter-alia e-filing of Audit Reports u/s. 44AB (Tax Audit

CHANGES IN 3CD TAX AUDIT REPORT FOR THE A.Y. 2013-2014 AMENDMENTS IN FINANCE ACT, 2012 HAVING IMPACT ON TAX AUDIT REPORT Rule 12 From A.Y. 2013-14 inter-alia e-filing of Audit Reports u/s. 44AB (Tax Audit

IMPORTANT AMENDMENTS OF THE FINANCE ACT, /6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

IMPORTANT AMENDMENTS OF THE FINANCE ACT,2010 22/6/2011 Lecture Meeting of BCAS - C.A.Vipul Gandhi 1 TAX RATES AND SLABS OF INCOME TAX RATES FOR INDIVIDUAL,HUF,AOP & BOI, ARTIFICIAL JUDICIAL PERSON U/S

Tax Audit Series 9 S. No. 21

Namaste In series - 9 we would discuss the Particulars of Form 3CD Part B S. No. 21. S. No. 21: Amount Debited to Profit & Loss Account S. No. 21 (a) - Furnish the details of amounts debited to the profit

Namaste In series - 9 we would discuss the Particulars of Form 3CD Part B S. No. 21. S. No. 21: Amount Debited to Profit & Loss Account S. No. 21 (a) - Furnish the details of amounts debited to the profit

Instructions for filling ITR-1 SAHAJ A.Y

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

TDS Provisions on Pension Payments CA Pranjal Joshi

TDS Provisions on Pension Payments CA Pranjal Joshi Introduction TDS is the best medium of collecting tax from the citizens without much of hassles, as the responsibility to deduct tax is not on the government,

TDS Provisions on Pension Payments CA Pranjal Joshi Introduction TDS is the best medium of collecting tax from the citizens without much of hassles, as the responsibility to deduct tax is not on the government,

Income Tax Act DIVISION ONE 1 DIVISION TWO 2

Income Tax Act SECTION DIVISION ONE 1 Income-tax Act, 1961 Arrangement of Sections I-3 Text of the Income-tax Act, 1961 as amended by the Finance (No. 2) Act, 2014 1.1 Appendix : Text of remaining provisions

Income Tax Act SECTION DIVISION ONE 1 Income-tax Act, 1961 Arrangement of Sections I-3 Text of the Income-tax Act, 1961 as amended by the Finance (No. 2) Act, 2014 1.1 Appendix : Text of remaining provisions

LATEST IN INCOME TAX. LUNAWAT & CO. Chartered Accountants CA. PRAMOD JAIN. (From Businessmen s Point of View) 3 rd June, Phagwara

3 rd June, Phagwara") LATEST IN INCOME TAX (From Businessmen s Point of View) LUNAWAT & CO. Chartered Accountants 3 rd June, Phagwara CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA Lunawat & Co. PAN Quoting AIR Reporting

LATEST IN INCOME TAX (From Businessmen s Point of View) LUNAWAT & CO. Chartered Accountants 3 rd June, Phagwara CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA AGENDA Lunawat & Co. PAN Quoting AIR Reporting

ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE::KADAPA

[ 2) ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE::KADAPA Cir.No.90-2006-BC-STF Date: 29.9.06 INCOME TAX e FILING OF TDS RETURNS REF: 1) Cir.No.28-2006-BC-STF, dt.14.7.06, Cir.No.41-2006-BC-STF,dt.31.7.06

[ 2) ANDHRA PRAGATHI GRAMEENA BANK HEAD OFFICE::KADAPA Cir.No.90-2006-BC-STF Date: 29.9.06 INCOME TAX e FILING OF TDS RETURNS REF: 1) Cir.No.28-2006-BC-STF, dt.14.7.06, Cir.No.41-2006-BC-STF,dt.31.7.06

2. Delay in updation of TDS credit in Form No. 26AS of the taxpayer and approaching due date of TDS statement filing for first quarter

Although the ITR forms for AY 2018-19 were notified on 3 rd April, 2018 vide Notification No. 16/2018, the ITR Form utilities in Java and Excel were released much later in the month of May, 2018(except

Although the ITR forms for AY 2018-19 were notified on 3 rd April, 2018 vide Notification No. 16/2018, the ITR Form utilities in Java and Excel were released much later in the month of May, 2018(except

Tax Liability Ledger, will reflect the total tax liability of a tax payer (after netting) for the particular month.

for the particular month.") ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

Tax Deduction and Collection at Source

(iii) Ravi Kumar aged 67 years derived ` 6,00,000 as salary from his employer, XYZ Ltd. for the year ended 31-03- 2019. The following details are provided by him to the employer: Particulars ` Loss from

(iii) Ravi Kumar aged 67 years derived ` 6,00,000 as salary from his employer, XYZ Ltd. for the year ended 31-03- 2019. The following details are provided by him to the employer: Particulars ` Loss from

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

The Simple Guide to Taxes for. Freelancers

The Simple Guide to Taxes for Freelancers WWW.CLEARTAX.COM/BUSINESS CONTENTS Should I form a company or can I begin solo?... 1 How do I compute my freelancing income?... 2 Domestic Clients... 3 Foreign

The Simple Guide to Taxes for Freelancers WWW.CLEARTAX.COM/BUSINESS CONTENTS Should I form a company or can I begin solo?... 1 How do I compute my freelancing income?... 2 Domestic Clients... 3 Foreign

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 PREFACE The provisions of the

Tax Payers Information Series - 35 TDS ON SALARIES INCOME TAX DEPARTMENT Directorate of Income Tax (PR, PP & OL) 6 th Floor, Mayur Bhawan, Connaught Circus New Delhi-110001 PREFACE The provisions of the

Rates for tax deduction at source (TDS)

") Rates for tax deduction at source (TDS) [For Assessment year 18-19] Particulars 1. In the case of a person other than a company 1.1 where the person is resident in India- Section 192: Payment of salary

Rates for tax deduction at source (TDS) [For Assessment year 18-19] Particulars 1. In the case of a person other than a company 1.1 where the person is resident in India- Section 192: Payment of salary

Rate of Tax Deducted at source

Rate of Tax Deducted at source During the financial year 2009-, tax is to be deducted at source at the following rate:- Sectio n Nature of Payment TDS [SC- Nil, EC- Nil, SHEC- Nil] 192 Payment of salary

Rate of Tax Deducted at source During the financial year 2009-, tax is to be deducted at source at the following rate:- Sectio n Nature of Payment TDS [SC- Nil, EC- Nil, SHEC- Nil] 192 Payment of salary

Chapter 1 : Income Tax Concept and Computation of Income Tax

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Analysis of new system for TDS -TCS payment and information reporting

Analysis of new system for TDS -TCS payment and information reporting Income Tax Department has introduced a scheme for centralized processing of annual income-tax returns which envisages no interface

Analysis of new system for TDS -TCS payment and information reporting Income Tax Department has introduced a scheme for centralized processing of annual income-tax returns which envisages no interface

Budget Highlights

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Budget Highlights 2018-19 DIRECT TAX PROPOSALS Chartered Accountants 1 st Floor, Sapphire Business Centre, Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad-380013 Email: apcca@apcca.com Website:

Form 26AS. Annual Tax Statement under Section 203AA of the Income Tax Act, 1961

Data updated till 14Feb2013 Form 26AS Annual Tax Statement under Section 203AA of the Income Tax Act, 1961 Permanent Account Number Name of Assessee Address of Assessee AANPK4324N Financial Year 201213

Data updated till 14Feb2013 Form 26AS Annual Tax Statement under Section 203AA of the Income Tax Act, 1961 Permanent Account Number Name of Assessee Address of Assessee AANPK4324N Financial Year 201213

Income Tax Reckoner AY:

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

W S & Co. Contact us FCA Shipra Walia Domestic & International Tax Advisor

Contact us FCA Shipra Walia Domestic & International Tax Advisor www.wsco.in www.shiprawalia.in mail:info@wsco.in Individuals, HUF, AOP, BOI 1. No change in Tax Rate (a) For a resident senior citizen (who

Contact us FCA Shipra Walia Domestic & International Tax Advisor www.wsco.in www.shiprawalia.in mail:info@wsco.in Individuals, HUF, AOP, BOI 1. No change in Tax Rate (a) For a resident senior citizen (who

MONTHLY COMMUNIQUÉ JUNE 2011

INCOME TAX Income Tax Issuance and Authentication of Form 16A: Presently, in relation to withholding Service Tax taxes/tds, the certificate in Form 16A is generated by the deductors and issued to FEMA

INCOME TAX Income Tax Issuance and Authentication of Form 16A: Presently, in relation to withholding Service Tax taxes/tds, the certificate in Form 16A is generated by the deductors and issued to FEMA

CIRCULAR NO. 8/2012, Dated: October 5, 2012

CIRCULAR NO. 8/2012, Dated: October 5, 2012 Suject: Income Tax Deduction From Salaries during the Financial Year 2012-2013 under Section 192 of The Income Tax Act, 1961. Reference is invited to Circular

CIRCULAR NO. 8/2012, Dated: October 5, 2012 Suject: Income Tax Deduction From Salaries during the Financial Year 2012-2013 under Section 192 of The Income Tax Act, 1961. Reference is invited to Circular

INPUT TAX CREDIT (ITC) PROVISIONS. CA Nammitta Gangwal Nilange LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant

PROVISIONS. CA Nammitta Gangwal Nilange LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant") INPUT TAX CREDIT (ITC) PROVISIONS LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant WHAT SHOULD WE KNOW UNDER ITC? Sec. 16 Eligibility & Conditions for taking ITC Sec. 19 Taking ITC in respect

INPUT TAX CREDIT (ITC) PROVISIONS LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant WHAT SHOULD WE KNOW UNDER ITC? Sec. 16 Eligibility & Conditions for taking ITC Sec. 19 Taking ITC in respect

TaxPro. Key Features File Validation Utility (FVU) version 5.7

version 5.7") TaxPro Key Features File Validation Utility (FVU) version 5.7 In case of non-availability of PAN of deductee for Form 27EQ, two new fields are introduced under deductee details which are as below: Field

TaxPro Key Features File Validation Utility (FVU) version 5.7 In case of non-availability of PAN of deductee for Form 27EQ, two new fields are introduced under deductee details which are as below: Field

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS.

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS. Income Tax Amendment - Personal SN Description Impact Author remarks 1 For Income more than one crore surcharge Negative More tax from super

INDIA BUDGET 2016 SUMMARY OF IMPORTANT PROPOSED AMENDMENTS. Income Tax Amendment - Personal SN Description Impact Author remarks 1 For Income more than one crore surcharge Negative More tax from super

Payment of tax, interest, penalty and other amounts (Section 49)

") FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

FAQ s Chapter VIII Payment of Tax Payment of tax, interest, penalty and other amounts (Section 49) Section 49 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Guidelines for reporting TDS transactions where amount paid to deductee has not exceeded the threshold limit

Twitter Linkedin RSS Facebook Corporate Law FEMA Finance General Info Government Policy IRDA Articles News Notifications/Circulars Home Income Tax ITR 11-12 Service Tax Excise C. Law Judiciary DGFT GST

Twitter Linkedin RSS Facebook Corporate Law FEMA Finance General Info Government Policy IRDA Articles News Notifications/Circulars Home Income Tax ITR 11-12 Service Tax Excise C. Law Judiciary DGFT GST

HIGHLIGHTS OF BUDGET

HIGHLIGHTS OF BUDGET 2009 10 No.103, Brigade Links, No.54/1, 1st Main Road, Seshadripuram, Bangalore 560 020 Phone: 080-2344 1114 / 2334 3014 www.nprca.in DIRECT TAXES: Tax Rates for FY 2009-10 All (except

HIGHLIGHTS OF BUDGET 2009 10 No.103, Brigade Links, No.54/1, 1st Main Road, Seshadripuram, Bangalore 560 020 Phone: 080-2344 1114 / 2334 3014 www.nprca.in DIRECT TAXES: Tax Rates for FY 2009-10 All (except

DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Form No. 24Q. 1 ( a ) Tax Deduction Account No ( d ) Assessment year

Tax Deduction Account No ( d ) Assessment year") Form No. 24Q (See section 192 and rule 31A) Quarterly statement of deduction of tax under sub section ( 3 ) of section 200 of the Income tax Act, 1961 in respect of Salary for the quarter ended June /

Form No. 24Q (See section 192 and rule 31A) Quarterly statement of deduction of tax under sub section ( 3 ) of section 200 of the Income tax Act, 1961 in respect of Salary for the quarter ended June /

Marking Scheme. Session TAXATION (782) CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income

CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income") Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Rates for tax deduction at source

Rates for tax deduction at source Particulars 1. In the case of a person other than a company 1.1 where the person is resident in India- Section 192: Payment of salary Section 192A: Payment of accumulated

Rates for tax deduction at source Particulars 1. In the case of a person other than a company 1.1 where the person is resident in India- Section 192: Payment of salary Section 192A: Payment of accumulated

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

A23 A24 A25 A26 B1 B2 B3 B5 In response to notice under section In response to notice under section 153A/ 153C 7 In pursuance of an order of the

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

SURENDER KR. SINGHAL & CO

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

MTP_ Inter _Syllabus 2016_ June 2018_Set 1 Paper 7 Direct Taxation (DTX)

") Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

Paper 7 Direct Taxation (DTX) Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks:

ISSUES IN E-FILING UNDER MVAT ACT

ISSUES IN E-FILING UNDER MVAT ACT Presentation by CA PRANAV KAPADIA For Seminar on e-filing by The Chamber of Tax Consultants 17-08-2013 CA PRANAV KAPADIA 1 E-Services under MVAT Registration Returns &

ISSUES IN E-FILING UNDER MVAT ACT Presentation by CA PRANAV KAPADIA For Seminar on e-filing by The Chamber of Tax Consultants 17-08-2013 CA PRANAV KAPADIA 1 E-Services under MVAT Registration Returns &

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

Shah & Savla Chartered Accountants

1 Reverse Charge Mechanism & Valuation Rules J. B. Nagar CPE Study Circle CA Ashit Shah Chartered Accountants 2 Matters to be covered Notices: Reverse Charge Mechanism of Taxation [N. No. 30/2012 dated

1 Reverse Charge Mechanism & Valuation Rules J. B. Nagar CPE Study Circle CA Ashit Shah Chartered Accountants 2 Matters to be covered Notices: Reverse Charge Mechanism of Taxation [N. No. 30/2012 dated