The European Anti-Fraud Office (OLAF) 27 June 2014

|

|

|

- Avis McCormick

- 6 years ago

- Views:

Transcription

1 The European Anti-Fraud Office (OLAF) 27 June 2014

2 Institutional History 1988 creation of predecessor UCLAF 1999 creation of OLAF, based in Brussels mandate of F.H. Brüner, the first OLAF Director General 2011 mandate of G. Kessler, OLAF Director General OLAF is the French acronym of the Office Européen de Lutte Anti-Fraude 27 MARKED June 2014 NOT PROTECTIVELY MARKED 2

3 OLAF Mission to protect the financial interests of the European Union (EU) by investigating fraud, corruption and any other illegal activities; to detect and investigate serious matters relating to the discharge of professional duties by members and staff of the EU institutions and bodies that could result in disciplinary or criminal proceedings; to support the EU institutions, in particular the European Commission in the development and implementation of anti-fraud legislation and policies. 27 MARKED June 2014 NOT PROTECTIVELY MARKED 3

4 Status 1. INVESTIGATIONS: fully independent Director-General of OLAF: appointed by the European Commission after consultations with the European Parliament and the Council for a seven-year term, not renewable; may neither seek nor accept instructions from any government or any institution, body, office or agency; entitled to bring an action against the Commission before the European Court of Justice. Supervisory Committee: made up of 5 outside independent experts who ensure/reinforce the Office's independence. 2. POLICY: administratively part of the European Commission 27 MARKED June 2014 NOT PROTECTIVELY MARKED 4

5 27 MARKED June 2014 NOT PROTECTIVELY MARKED 5

6 OLAF's Human Resources STAFF 2013: 440 staff members (2012: 435) Many with prior professional experience as: Magistrates or prosecutors Customs officers Police officers Tax inspectors Financial controllers Auditors Intelligence experts. 27 MARKED June

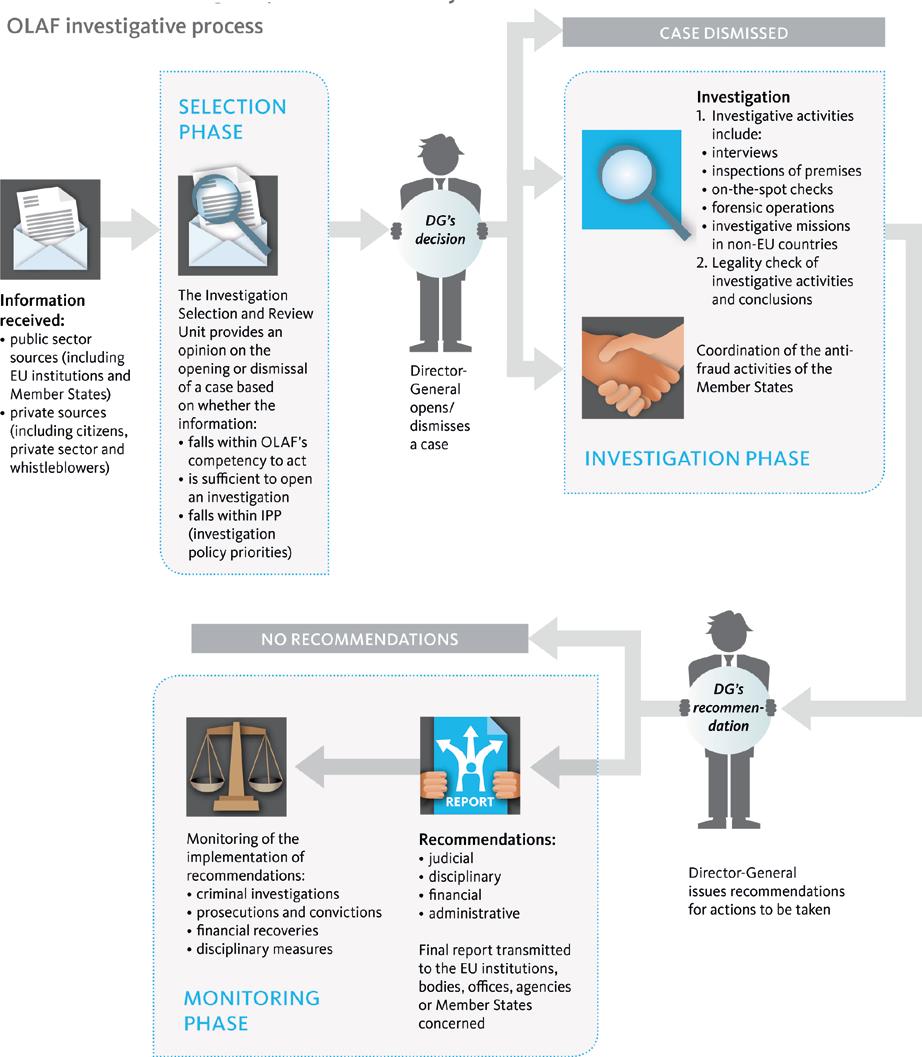

7 OLAF Investigates under administrative law Seeks evidence for and against the suspect (à charge et à décharge) Under a range of legal bases (Regulation 883/2013, Regulation 2185/1996, Customs law, Mutual Assistance agreements) Produces recommendations to national judiciaries and EU disciplinary authorities. They prosecute, we don t! 7

8 What is fraud affecting the European Communities' financial interests? Any intentional act or omission relating to: in respect of expenditure: the use or presentation of false, incorrect or incomplete statements or documents, which has as its effect the misappropriation or wrongful retention of funds from the general budget of the European Communities or budgets managed by, or on behalf of, the European Communities, the misapplication of such funds for purposes other than those for which they were originally granted; In respect of revenue: the use or presentation of false, incorrect or incomplete statements or documents, which has as its effect the illegal diminution of the resources of the general budget of the European Communities or budgets managed by, or on behalf of, the European Communities, misapplication of a legally obtained benefit, with the same effect. non-disclosure of information in violation of a specific obligation, with the same effect. 8

9 Examples of fraud and Embezzled construction aid for bridges and power stations Fiddling in public contract processes Non-payment of import levies on bicycles, televisions, energysaving lamps, sugar Tax evasion caused by cigarette smuggling and contraband goods Financing for fruit juice that is never produced, trees that are never planted, fruit that never exist Corruption inside the EU institutions, bodies and agencies Importing goods via third countries in order to avoid taxes 9

10 Consequences for the European citizen Waste of public money Reduction of EU purchasing power EU businesses are harmed by illegal imports European projects fall into disrepute Less EU support for genuinely deserving projects 10

11 11

12 Selection of cases - criteria OLAF s competency (financial and other interests of the EU) Information is sufficient (reliability of the source, credibility of the allegation) Information falls within OLAF s Investigative Policy Priorities: Proportionality (expected results vs resources; likelihood of recovery/prosecution ) Efficient use of investigative resources (workload, priorities, expertise ) Subsidiarity/added value (OLAF s sole competence ) Special Policy Objectives Financial impact 12

13 Investigative tools legality check Legality check during the investigation Interviews with persons concerned Inspection of premises On-the-spot checks Forensic operations Checks and inspections under sectoral rules Missions in third countries 13

14 Intelligence capability Forensic acquisition Open source intelligence s Data mining Text mining Relationships 27 MARKED June 2014 NOT PROTECTIVELY MARKED 14

15 Can OLAF punish perpetrators? OLAF has no judicial power OLAF may request EU and national authorities to cooperate OLAF can only make recommendations following its investigations 15

16 Outcome of investigations OLAF investigations lead to recommendations: Financial: OLAF and the European Commission can decide to ask for a recovery of the misused funds Judicial: OLAF will send its report to the relevant national authorities recommending legal action Disciplinary: the case is referred to the authority having disciplinary powers in the relevant EU institution. The European Commission operates a zero-tolerance policy Administrative: OLAF can recommend changes to procedures (and to the EWS) to prevent fraud being repeated Authorities of Member States shall inform the Office in due time of the actions taken on the basis of the information transmitted to them by OLAF (Article 12.3 of Regulation n 883/2013) 16

17 Cooperation with national partners in Member States Regular meetings and contacts with national control bodies like: AFCOS (Anti-Fraud Coordination Services) in the Member States and Candidate Countries Attorney General s and other Public Prosecutor s Offices Anti-Corruption Commissions Specialised fraud squads in the police Auditors General s Offices National Customs Authorities 17

18 Cooperation with national partners in non-eu countries A growing number of national control bodies (such as General State Inspectorates, Anti-Corruption Commissions, Public Prosecutor s Offices etc.) which: assist OLAF in carrying out inspections and on-the-spot checks in non-eu countries share information and expertise sign Administrative Cooperation Arrangements in order to facilitate practical aspects of the cooperation 18

19 Cooperation with other European bodies and international organisations Europol Eurojust International Organisations and Financial Institutions UN WCO World Bank WHO Interpol OECD 19

20 Cooperation with national and international partners Define together the needs and solutions Training Technical assistance Investigate in joint teams Provide all the assistance required to OLAF teams or vice versa 20

21 Thank you OLAF website: 27 MARKED June 2014 NOT PROTECTIVELY MARKED 21

European Anti-Fraud Office (OLAF) 18 June Neil RITCHIE, Head of Sector Directorate A Investigations I Centralised Expenditure A.

18 June Neil RITCHIE, Head of Sector Directorate A Investigations I Centralised Expenditure A.") European Anti-Fraud Office (OLAF) 18 June 2018 Neil RITCHIE, Head of Sector Directorate A Investigations I Centralised Expenditure A.3 A little history 1988 creation of OLAF predecessor, UCLAF 1999 creation

European Anti-Fraud Office (OLAF) 18 June 2018 Neil RITCHIE, Head of Sector Directorate A Investigations I Centralised Expenditure A.3 A little history 1988 creation of OLAF predecessor, UCLAF 1999 creation

The fight against fraud - the European Union perspective

The fight against fraud - the European Union perspective ACFE - European Fraud Conference Prague, 19 March 2013 Giovanni Kessler Director-General European Anti-Fraud Office (OLAF) OLAF - EUROPEAN ANTI-FRAUD

The fight against fraud - the European Union perspective ACFE - European Fraud Conference Prague, 19 March 2013 Giovanni Kessler Director-General European Anti-Fraud Office (OLAF) OLAF - EUROPEAN ANTI-FRAUD

INTERREG - IPA CBC ROMANIA-SERBIA PROGRAMME

ANTI-FRAUD STRATEGY INTERREG - IPA CBC ROMANIA-SERBIA PROGRAMME VERSION 2016 1 TABLE OF CONTENTS PRINCIPLE 4 FOREWORD 4 LEGAL BASIS 4 DEFINITIONS 5 I. GENERAL CONSIDERATIONS 5 I.1. AIM 5 I.2. MISSION 6

ANTI-FRAUD STRATEGY INTERREG - IPA CBC ROMANIA-SERBIA PROGRAMME VERSION 2016 1 TABLE OF CONTENTS PRINCIPLE 4 FOREWORD 4 LEGAL BASIS 4 DEFINITIONS 5 I. GENERAL CONSIDERATIONS 5 I.1. AIM 5 I.2. MISSION 6

Report of the European Anti-Fraud Office. Summary version. Eighth Activity Report for the period 1 January 2007 to 31 December 2007

Report of the European Anti-Fraud Office Summary version Eighth Activity Report for the period 1 January 2007 to 31 December 2007 Rue Joseph II 30 B-1000 Bruxelles Internet : http://ec.europa.eu/olaf Note

Report of the European Anti-Fraud Office Summary version Eighth Activity Report for the period 1 January 2007 to 31 December 2007 Rue Joseph II 30 B-1000 Bruxelles Internet : http://ec.europa.eu/olaf Note

ANTI-FRAUD STRATEGY INTERREG IPA CBC PROGRAMMES BULGARIA SERBIA BULGARIA THE FORMER YUGOSLAV REPUBLIC OF MACEDONIA BULGARIA TURKEY

ANTI-FRAUD STRATEGY INTERREG IPA CBC PROGRAMMES 2014-2020 BULGARIA SERBIA BULGARIA THE FORMER YUGOSLAV REPUBLIC OF MACEDONIA BULGARIA TURKEY VERSION NOVEMBER 2016 1 TABLE OF CONTENTS PRINCIPLE 3 FOREWORD

ANTI-FRAUD STRATEGY INTERREG IPA CBC PROGRAMMES 2014-2020 BULGARIA SERBIA BULGARIA THE FORMER YUGOSLAV REPUBLIC OF MACEDONIA BULGARIA TURKEY VERSION NOVEMBER 2016 1 TABLE OF CONTENTS PRINCIPLE 3 FOREWORD

José Lopes da Mota Deputy Prosecutor General Former President of Eurojust

* José Lopes da Mota Deputy Prosecutor General Former President of Eurojust 1 2 Fraud and corruption in health care recognised as a global problem Different players (persons, companies, entities) Acting

* José Lopes da Mota Deputy Prosecutor General Former President of Eurojust 1 2 Fraud and corruption in health care recognised as a global problem Different players (persons, companies, entities) Acting

COMMISSIONER ALGIRDAS ŠEMETA TAXATION, CUSTOMS, STATISTICS, AUDIT AND ANTI- FRAUD

COMMISSIONER ALGIRDAS ŠEMETA TAXATION, CUSTOMS, STATISTICS, AUDIT AND ANTI- FRAUD SPEECH AT THE EUROPEAN SERIOUS & ORGANISED CRIME CONFERENCE 2013 WINNING THE FIGHT 28 th February 2013 KEYNOTE SPEECH Ladies

COMMISSIONER ALGIRDAS ŠEMETA TAXATION, CUSTOMS, STATISTICS, AUDIT AND ANTI- FRAUD SPEECH AT THE EUROPEAN SERIOUS & ORGANISED CRIME CONFERENCE 2013 WINNING THE FIGHT 28 th February 2013 KEYNOTE SPEECH Ladies

COMMISSION DECISION. of on technical provisions necessary for the operation of the transition facility in the Republic of Croatia

EUROPEAN COMMISSION Brussels, 13.6.2013 C(2013) 3463 final COMMISSION DECISION of 13.6.2013 on technical provisions necessary for the operation of the transition facility in the Republic of Croatia EN

EUROPEAN COMMISSION Brussels, 13.6.2013 C(2013) 3463 final COMMISSION DECISION of 13.6.2013 on technical provisions necessary for the operation of the transition facility in the Republic of Croatia EN

DG REGIO, DG EMPL and DG MARE in cooperation with OLAF. Joint Fraud Prevention Strategy. for ERDF, ESF, CF and EFF

EUROPEAN COMMISSION REGIONAL POLICY EMPLOYMENT,SOCIAL AFFAIRS AND EQUAL OPPORTUNITIES OLAF MARE DG REGIO, DG EMPL and DG MARE in cooperation with OLAF Joint Fraud Prevention Strategy for ERDF, ESF, CF

EUROPEAN COMMISSION REGIONAL POLICY EMPLOYMENT,SOCIAL AFFAIRS AND EQUAL OPPORTUNITIES OLAF MARE DG REGIO, DG EMPL and DG MARE in cooperation with OLAF Joint Fraud Prevention Strategy for ERDF, ESF, CF

PRESENTATION BY RUMEN PETKOV. Mr. Rumen Petkov, Minister of Interior, delivered his speech:

Mr. Rumen Petkov, Minister of Interior, delivered his speech: Ladies and Gentlemen, Thank you for the opportunity to welcome the participants in the 6 th Training seminar of the OLAF Anti-Fraud Communicators

Mr. Rumen Petkov, Minister of Interior, delivered his speech: Ladies and Gentlemen, Thank you for the opportunity to welcome the participants in the 6 th Training seminar of the OLAF Anti-Fraud Communicators

Member States capabilities in fighting tax crimes

Belgium Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax burden.

Belgium Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax burden.

Fraud Risk Management MANAGING AUTHORITY OF EUROPEAN TERRITORIAL COOPERATION PROGRAMMES-UNIT A'

Fraud Risk Management Starting Point The Rules the Starting Point: The Treaty The Financial Regulation (966/2012) The Common Regulation (1303/2013) Also, The ETC (1299/2013),. Why are the MAs involved

Fraud Risk Management Starting Point The Rules the Starting Point: The Treaty The Financial Regulation (966/2012) The Common Regulation (1303/2013) Also, The ETC (1299/2013),. Why are the MAs involved

Report. M. Simonato, M. Luchtman & J. Vervaele (eds.) March 2018

March 2018") Report Exchange of information with EU and national enforcement authorities Improving OLAF legislative framework through a comparison with other EU authorities (ECN/ESMA/ECB) M. Simonato, M. Luchtman &

Report Exchange of information with EU and national enforcement authorities Improving OLAF legislative framework through a comparison with other EU authorities (ECN/ESMA/ECB) M. Simonato, M. Luchtman &

Anti-corruption Authorities Initiative: Survey on the Effectiveness of Anticorruption

Updated October, 2014 Anti-corruption Authorities Initiative: Survey on the Effectiveness of Anticorruption Background Information 1. Please enter country name in the space below NAMIBIA 2. Name of the

Updated October, 2014 Anti-corruption Authorities Initiative: Survey on the Effectiveness of Anticorruption Background Information 1. Please enter country name in the space below NAMIBIA 2. Name of the

NEW YORK STATE BAR ASSOCIATION INTERNATIONAL SECTION. Dublin 21 April 2017

1 NEW YORK STATE BAR ASSOCIATION INTERNATIONAL SECTION Dublin 21 April 2017 Christophe Jolk Avocat à la Cour (Paris, Luxembourg) Attorney at Law (New York) Outer Temple Chambers 2 Main Criminal Law Aspects

1 NEW YORK STATE BAR ASSOCIATION INTERNATIONAL SECTION Dublin 21 April 2017 Christophe Jolk Avocat à la Cour (Paris, Luxembourg) Attorney at Law (New York) Outer Temple Chambers 2 Main Criminal Law Aspects

COMMISSION OF THE EUROPEAN COMMUNITIES INTERIM REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 12.2.2009 COM(2009) 69 final INTERIM REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL On Progress in Bulgaria under the Co-operation

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 12.2.2009 COM(2009) 69 final INTERIM REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL On Progress in Bulgaria under the Co-operation

Journal of International Relations, Volume 2, Nomor 4, Tahun 2016, hal Online di

Journal of International Relations, Volume 2, Nomor 4, Tahun 2016, hal 241-249 Online di http://ejournal-s1.undip.ac.id/index.php/jihi OLAF S SUITABILITY TO GLOBAL FINANCIAL CRIME GOVERNANCE ON COMBATING

Journal of International Relations, Volume 2, Nomor 4, Tahun 2016, hal 241-249 Online di http://ejournal-s1.undip.ac.id/index.php/jihi OLAF S SUITABILITY TO GLOBAL FINANCIAL CRIME GOVERNANCE ON COMBATING

SOMERVILLE HOUSING AUTHORITY ANTI- FRAUD POLICY. April 3, 2013

SOMERVILLE HOUSING AUTHORITY ANTI- FRAUD POLICY April 3, 2013 Introduction The Board of Commissioners of the Somerville Housing Authority has established an anti-fraud policy to enforce controls and to

SOMERVILLE HOUSING AUTHORITY ANTI- FRAUD POLICY April 3, 2013 Introduction The Board of Commissioners of the Somerville Housing Authority has established an anti-fraud policy to enforce controls and to

Frequently Asked Questions Protection of the euro and other currencies against counterfeiting

EUROPEAN COMMISSION MEMO Brussels, 6 May 2014 Frequently Asked Questions Protection of the euro and other currencies against counterfeiting Why do we need to protect the euro and other currencies? Counterfeiting

EUROPEAN COMMISSION MEMO Brussels, 6 May 2014 Frequently Asked Questions Protection of the euro and other currencies against counterfeiting Why do we need to protect the euro and other currencies? Counterfeiting

The European Social Fund and Risks of Fraud to the Detriment of the European Union

AGAINST FRAUD TO THE DETRIMENT OF THE EU The European Social Fund and Risks of Fraud to the Detriment of the European Union 4. Co-funded by the Prevention of and Fight against Crime Programme of the European

AGAINST FRAUD TO THE DETRIMENT OF THE EU The European Social Fund and Risks of Fraud to the Detriment of the European Union 4. Co-funded by the Prevention of and Fight against Crime Programme of the European

The OLAF report 2015 ISSN

The OLAF report 2015 ISSN 2315-2494 The Fraud Notification System (FNS) is a web-based tool available to any person who seeks to pass on information concerning potential corruption and fraud. http://ec.europa.eu/anti-fraud/olaf-and-you/report-fraud_en

The OLAF report 2015 ISSN 2315-2494 The Fraud Notification System (FNS) is a web-based tool available to any person who seeks to pass on information concerning potential corruption and fraud. http://ec.europa.eu/anti-fraud/olaf-and-you/report-fraud_en

10472/18 JC/NC/jk ECOMP.2.B. Council of the European Union Brussels, 14 September 2018 (OR. en) 10472/18. Interinstitutional File: 2017/0248 (CNS)

10472/18. Interinstitutional File: 2017/0248 (CNS)") Council of the European Union Brussels, 14 September 2018 (OR. en) Interinstitutional File: 2017/0248 (CNS) 10472/18 FISC 276 ECOFIN 667 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: COUNCIL REGULATION

Council of the European Union Brussels, 14 September 2018 (OR. en) Interinstitutional File: 2017/0248 (CNS) 10472/18 FISC 276 ECOFIN 667 LEGISLATIVE ACTS AND OTHER INSTRUMTS Subject: COUNCIL REGULATION

Safeguarding EU funds against fraud & corruption. Jana Mittermaier, Director TI EU Office, Brussels

Safeguarding EU funds against fraud & corruption Jana Mittermaier, Director TI EU Office, Brussels Positive developments + EU anti-corruption report (focus public procurement) + Proposal on fight against

Safeguarding EU funds against fraud & corruption Jana Mittermaier, Director TI EU Office, Brussels Positive developments + EU anti-corruption report (focus public procurement) + Proposal on fight against

PART I - DEFINITIONS & PRINCIPLES. Date 11 May 2015

PART I - DEFINITIONS & PRINCIPLES Date 11 May 2015 secretariat@robertcarrfund.org Fund Management Agent: Aids Fonds Keizersgracht 392 1016 GB Amsterdam +31 (0)206262669 secretariat@robertcarrfund.org www.robertcarrfund.org

PART I - DEFINITIONS & PRINCIPLES Date 11 May 2015 secretariat@robertcarrfund.org Fund Management Agent: Aids Fonds Keizersgracht 392 1016 GB Amsterdam +31 (0)206262669 secretariat@robertcarrfund.org www.robertcarrfund.org

ANTI-FRAUD POLICY. Reference No: ANTIFP-251. Policy Type: Governance. Directorate Area: All Directorates. Policy Author / Champion: Maurice Atkinson

ANTI-FRAUD POLICY Reference No: ANTIFP-251 Policy Type: Directorate Area: Policy Author / Champion: Governance All Directorates Maurice Atkinson Date(s) Equality Screened: 21 July 2017 Date(s) Approved

ANTI-FRAUD POLICY Reference No: ANTIFP-251 Policy Type: Directorate Area: Policy Author / Champion: Governance All Directorates Maurice Atkinson Date(s) Equality Screened: 21 July 2017 Date(s) Approved

DG AGRI Seminar. Fraud in the CAP

DG AGRI Seminar Fraud in the CAP June 2011 Anti-fraud Strategy European Commission 3 DG AFS AGRI DG AFS DG AFS DG AFS DG AFS DG 12/09/2012 4 Seminar: 4 Chapters 1. Fraud prevention and detection by Paying

DG AGRI Seminar Fraud in the CAP June 2011 Anti-fraud Strategy European Commission 3 DG AFS AGRI DG AFS DG AFS DG AFS DG AFS DG 12/09/2012 4 Seminar: 4 Chapters 1. Fraud prevention and detection by Paying

MEASURES TO COMBAT ECONOMIC CRIME

MEASURES TO COMBAT ECONOMIC CRIME Erasmus Makodza* I. INTRODUCTION The Land Reform Programme adopted by the Zimbabwe Government in the year 2000 and the subsequent smart sanctions imposed by the Western

MEASURES TO COMBAT ECONOMIC CRIME Erasmus Makodza* I. INTRODUCTION The Land Reform Programme adopted by the Zimbabwe Government in the year 2000 and the subsequent smart sanctions imposed by the Western

APPENDIX 2 CORPORATE ANTI-FRAUD AND CORRUPTION STRATEGY

APPENDIX 2 CORPORATE ANTI-FRAUD AND CORRUPTION STRATEGY January 2017 CONTENTS Section Page 1 Introduction 3 2 Definition of Fraud 3 3 Standards 4 4 Corporate Framework and Culture 4 5 Roles and Responsibilities

APPENDIX 2 CORPORATE ANTI-FRAUD AND CORRUPTION STRATEGY January 2017 CONTENTS Section Page 1 Introduction 3 2 Definition of Fraud 3 3 Standards 4 4 Corporate Framework and Culture 4 5 Roles and Responsibilities

QUESTIONNAIRE Country self-assessment report on implementation and enforcement of G20 commitments on foreign bribery

QUESTIONNAIRE Country self-assessment report on implementation and enforcement of G20 commitments on foreign bribery G20 countries are invited to complete the questionnaire, below, on the implementation

QUESTIONNAIRE Country self-assessment report on implementation and enforcement of G20 commitments on foreign bribery G20 countries are invited to complete the questionnaire, below, on the implementation

Partners and FLC Info day. Madrid, 22/06/2017

Partners and FLC Info day Madrid, 22/06/2017 Fraud and conflict of Interest Fraud and conflict of interest. Definitions. Prevention & sensibilisation. Detection. Reporting. Correction Conflict of interest

Partners and FLC Info day Madrid, 22/06/2017 Fraud and conflict of Interest Fraud and conflict of interest. Definitions. Prevention & sensibilisation. Detection. Reporting. Correction Conflict of interest

COMMISSION DECISION. of adopting the PERICLES annual work programme 2013 serving as a financing decision for 2013

Ref. Ares(2013)293691-06/03/2013 EUROPEAN COMMISSION Brussels, 5.2.2013 C(2013) 544 final COMMISSION DECISION of 5.2.2013 adopting the PERICLES annual work programme 2013 serving as a financing decision

Ref. Ares(2013)293691-06/03/2013 EUROPEAN COMMISSION Brussels, 5.2.2013 C(2013) 544 final COMMISSION DECISION of 5.2.2013 adopting the PERICLES annual work programme 2013 serving as a financing decision

TEXAS WORKFORCE COMMISSION LETTER. ID/No: Regulatory Integrity Date: August 17, 2009

TEXAS WORKFORCE COMMISSION LETTER ID/No: Regulatory Integrity 04-09 Date: August 17, 2009 TO: FROM: Executive Director Deputy Executive Director Commission Executive Staff Department Heads LWDB Executive

TEXAS WORKFORCE COMMISSION LETTER ID/No: Regulatory Integrity 04-09 Date: August 17, 2009 TO: FROM: Executive Director Deputy Executive Director Commission Executive Staff Department Heads LWDB Executive

Recommendation of the Council for Further Combating Bribery of Foreign Public Officials in International Business Transactions

Working Group on Bribery in International Business Transactions Recommendation of the Council for Further Combating Bribery of Foreign Public Officials in International Business Transactions 26 NOVEMBER

Working Group on Bribery in International Business Transactions Recommendation of the Council for Further Combating Bribery of Foreign Public Officials in International Business Transactions 26 NOVEMBER

ANTI FRAUD POLICY AND FRAUD RESPONSE PLAN

ANTI FRAUD POLICY ANTI FRAUD POLICY AND FRAUD RESPONSE PLAN 1. Introduction 1.1 This paper sets out the Trust strategies for minimising the risk of fraud, corruption and other irregularity and the plan

ANTI FRAUD POLICY ANTI FRAUD POLICY AND FRAUD RESPONSE PLAN 1. Introduction 1.1 This paper sets out the Trust strategies for minimising the risk of fraud, corruption and other irregularity and the plan

FRAUD EXAMINERS MANUAL INTERNATIONAL EDITION

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

TABLE OF CONTENTS VOLUME I SECTION 1 FINANCIAL TRANSACTIONS AND FRAUD SCHEMES ACCOUNTING CONCEPTS Accounting Basics... 1.101 Financial Statements... 1.105 Generally Accepted Accounting Principles (GAAP)...

ANTI- FRAUD & WHISTLE-BLOWING POLICY November 2017

ANTI- FRAUD & WHISTLE-BLOWING POLICY November 2017 1. Introduction Concern is committed to the highest possible standards of openness, transparency and accountability in all its affairs. We wish to promote

ANTI- FRAUD & WHISTLE-BLOWING POLICY November 2017 1. Introduction Concern is committed to the highest possible standards of openness, transparency and accountability in all its affairs. We wish to promote

European Commission proposal for a Council Regulation on the establishment of the European Public Prosecutor's Office

Initial appraisal of a European Commission Impact Assessment European Commission proposal for a Council Regulation on the establishment of the European Public Prosecutor's Office Impact Assessment (SWD

Initial appraisal of a European Commission Impact Assessment European Commission proposal for a Council Regulation on the establishment of the European Public Prosecutor's Office Impact Assessment (SWD

Screening report Serbia

[date] Screening report Serbia Chapter 32 Financial control Date of screening meetings: Explanatory meeting: 17 October 2013 Bilateral meeting: 26 November 2013 I. CHAPTER CONTENT This chapter contains

[date] Screening report Serbia Chapter 32 Financial control Date of screening meetings: Explanatory meeting: 17 October 2013 Bilateral meeting: 26 November 2013 I. CHAPTER CONTENT This chapter contains

Identifying and preventing fraud & corruption in ESI Funds. Fraud prevention: Audit and control systems; Reporting fraud; Fraud indicators.

Fraud prevention: Audit and control systems; Reporting fraud; Fraud indicators. Dermot Byrne, Head of Authority Identifying and preventing fraud & corruption in ESI Funds ERDF Audit Authority, Ireland

Fraud prevention: Audit and control systems; Reporting fraud; Fraud indicators. Dermot Byrne, Head of Authority Identifying and preventing fraud & corruption in ESI Funds ERDF Audit Authority, Ireland

Whistle-Blowing Policy

2017 Ithmaar Bank Human Resources Department Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 3.0- Actions Constituting Fraud 3.1- Criminal / Unethical Conduct 3.2-

2017 Ithmaar Bank Human Resources Department Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 3.0- Actions Constituting Fraud 3.1- Criminal / Unethical Conduct 3.2-

Anti-Money Laundering Law of the People's Republic of China

Anti-Money Laundering Law of the People's Republic of China Adopted at the 24th Session of the Standing Committee of the 10th National People's Congress on 31 October 2006 Table of Contents Chapter I General

Anti-Money Laundering Law of the People's Republic of China Adopted at the 24th Session of the Standing Committee of the 10th National People's Congress on 31 October 2006 Table of Contents Chapter I General

Member States capabilities in fighting tax crimes

United Kingdom Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax

United Kingdom Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax

REPUBLIC OF NAMIBIA NATIONAL STRATEGY ANTI-MONEY LAUNDERING COMBATTING THE FINANCING OF TERRORISM

REPUBLIC OF NAMIBIA NATIONAL STRATEGY ON ANTI-MONEY LAUNDERING AND COMBATTING THE FINANCING OF TERRORISM 2 GLOSSARY AND ABBREVIATIONS ACC AML AMLAC BoN CFT DNFBPs ESAAMLG FATF FI Anti-Corruption Commission

REPUBLIC OF NAMIBIA NATIONAL STRATEGY ON ANTI-MONEY LAUNDERING AND COMBATTING THE FINANCING OF TERRORISM 2 GLOSSARY AND ABBREVIATIONS ACC AML AMLAC BoN CFT DNFBPs ESAAMLG FATF FI Anti-Corruption Commission

Anti-Fraud Policy. Version: 8.0 Approval Status: Approved. Document Owner: Graham Feek. Review Date: 07/12/2018

Anti-Fraud Policy Version: 8.0 Approval Status: Approved Document Owner: Graham Feek Classification: External Review Date: 07/12/2018 Last Reviewed: 09/12/2016 Table of Contents 1. Policy Statement...

Anti-Fraud Policy Version: 8.0 Approval Status: Approved Document Owner: Graham Feek Classification: External Review Date: 07/12/2018 Last Reviewed: 09/12/2016 Table of Contents 1. Policy Statement...

GAO Fraud Risk Framework Rebecca Shea, Director Forensic Audits and Investigative Services

GAO Fraud Risk Framework Rebecca Shea, Director Forensic Audits and Investigative Services Page 1 Agenda GAO s mission and organization (8:30-8:40) GAO s Mission and Values Fundamentals of GAO s Independence

GAO Fraud Risk Framework Rebecca Shea, Director Forensic Audits and Investigative Services Page 1 Agenda GAO s mission and organization (8:30-8:40) GAO s Mission and Values Fundamentals of GAO s Independence

EJTN CRIMINAL JUSTICE SEMINAR

18-19 JUNE 2018 Riga-LATVIA Latvian Judicial Training Centre (LJTC) Mārstalu street 19. Riga, Latvia, 3rd floor EJTN CRIMINAL JUSTICE SEMINAR THE PROTECTION OF THE FINANCIAL INTERESTS OF THE EU With financial

18-19 JUNE 2018 Riga-LATVIA Latvian Judicial Training Centre (LJTC) Mārstalu street 19. Riga, Latvia, 3rd floor EJTN CRIMINAL JUSTICE SEMINAR THE PROTECTION OF THE FINANCIAL INTERESTS OF THE EU With financial

University Fraud Policy

Section 1 University Fraud Policy 1. Introductory Statement The University is committed to the application of the Seven Principles of Public Life commended by the Committee for Standards in Public Life,

Section 1 University Fraud Policy 1. Introductory Statement The University is committed to the application of the Seven Principles of Public Life commended by the Committee for Standards in Public Life,

Whistleblowers Protection Act 2001 Policy and Procedures ABN

Whistleblowers Protection Act 2001 Policy and Procedures ABN 89 066 902 547 Contents 1. Statement of support to whistleblowers... 4 2. Purpose of policy and procedures... 4 3. Objects of the Act... 4 4.

Whistleblowers Protection Act 2001 Policy and Procedures ABN 89 066 902 547 Contents 1. Statement of support to whistleblowers... 4 2. Purpose of policy and procedures... 4 3. Objects of the Act... 4 4.

(Legislative acts) REGULATIONS

REGULATIONS") 1.11.2011 Official Journal of the European Union L 286/1 I (Legislative acts) REGULATIONS REGULATION (EU) No 1077/2011 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 25 October 2011 establishing a European

1.11.2011 Official Journal of the European Union L 286/1 I (Legislative acts) REGULATIONS REGULATION (EU) No 1077/2011 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 25 October 2011 establishing a European

Heerema Marine Contractors

Heerema Marine Contractors ANTI-FRAUD POLICY Date of issue September 2012 Version 2012.02 Document HMC L055 Summary HMC requires its staff at all times to act honestly and with integrity in order to safeguard

Heerema Marine Contractors ANTI-FRAUD POLICY Date of issue September 2012 Version 2012.02 Document HMC L055 Summary HMC requires its staff at all times to act honestly and with integrity in order to safeguard

Council of the European Union Brussels, 14 February 2017 (OR. en)

") Council of the European Union Brussels, 14 February 2017 (OR. en) 6128/1/17 REV 1 COVER NOTE From: To: General Secretariat of the Council Delegations No. prev. doc.: 11501/16 Subject: Joint Investigation

Council of the European Union Brussels, 14 February 2017 (OR. en) 6128/1/17 REV 1 COVER NOTE From: To: General Secretariat of the Council Delegations No. prev. doc.: 11501/16 Subject: Joint Investigation

Law on. Combating Money Laundering and Terrorism Financing LAW ON COMBATING MONEY LAUNDERING AND TERRORISM FINANCING

LAW ON COMBATING MONEY LAUNDERING AND TERRORISM FINANCING Law on Combating Money Laundering and Terrorism Financing PUBLISHED BY: AL ALAWI & CO., ADVOCATES & LEGAL CONSULTANTS CORPORATE ADVISORY GROUP

LAW ON COMBATING MONEY LAUNDERING AND TERRORISM FINANCING Law on Combating Money Laundering and Terrorism Financing PUBLISHED BY: AL ALAWI & CO., ADVOCATES & LEGAL CONSULTANTS CORPORATE ADVISORY GROUP

Eastern Band of Cherokee Indians Fraud Policy

Article I. BACKGROUND According to Management Antifraud Programs and Controls, released in 2002 as an exhibit to Statement on Auditing Standards No. 99 Consideration of Fraud in a Financial Statement Audit,

Article I. BACKGROUND According to Management Antifraud Programs and Controls, released in 2002 as an exhibit to Statement on Auditing Standards No. 99 Consideration of Fraud in a Financial Statement Audit,

EUROPEAN ANTI-FRAUD OFFICE (OLAF)

") EUROPEAN ANTI-FRAUD OFFICE (OLAF) Management Plan 1 Contents PART 1. MISSION STATEMENT... 3 PART 2. THIS YEAR S CHALLENGES... 4 PART 3. GENERAL OBJECTIVES OF THE POLICY... 6 PART 4. SPECIFIC OBJECTIVES

EUROPEAN ANTI-FRAUD OFFICE (OLAF) Management Plan 1 Contents PART 1. MISSION STATEMENT... 3 PART 2. THIS YEAR S CHALLENGES... 4 PART 3. GENERAL OBJECTIVES OF THE POLICY... 6 PART 4. SPECIFIC OBJECTIVES

EJTN STUDY VISITS PRESENTATION, CALENDARS AND REQUIREMENTS 1. STUDY VISIT AT THE EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA)

") EJTN STUDY VISITS PRESENTATION, CALENDARS AND REQUIREMENTS 1. STUDY VISIT AT THE EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA) The study visit will be organized at the European Union Agency for Fundamental

EJTN STUDY VISITS PRESENTATION, CALENDARS AND REQUIREMENTS 1. STUDY VISIT AT THE EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA) The study visit will be organized at the European Union Agency for Fundamental

COMMISSION STAFF WORKING DOCUMENT. Methodology regarding the statistical evaluation of reported irregularities for Accompanying the document

EUROPEAN COMMISSION Brussels, 14.7.2016 SWD(2016) 237 final COMMISSION STAFF WORKING DOCUMENT Methodology regarding the statistical evaluation of reported irregularities for 2015 Accompanying the document

EUROPEAN COMMISSION Brussels, 14.7.2016 SWD(2016) 237 final COMMISSION STAFF WORKING DOCUMENT Methodology regarding the statistical evaluation of reported irregularities for 2015 Accompanying the document

Regulation (2007:972) with instruction for the Swedish Economic Crime Authority

with instruction for the Swedish Economic Crime Authority") SFS no: 2007:972 Department/authority: Ministry of Justice Å Issued: 22/11/2007 Changed: up to SFS 2008:1398 Regulation (2007:972) with instruction for the Swedish Economic Crime Authority Tasks 1 The

SFS no: 2007:972 Department/authority: Ministry of Justice Å Issued: 22/11/2007 Changed: up to SFS 2008:1398 Regulation (2007:972) with instruction for the Swedish Economic Crime Authority Tasks 1 The

France. Parliament has fully informed its members (MPs) on the issue. The associations of local authorities have largely disclosed the information.

on the issue. The associations of local authorities have largely disclosed the information.") France 1. Fair Regulatory framework Outreach to public officials about The current regulatory framework includes: Article 23 of the Constitution Articles 432-12 to 432-13 of the criminal code on illegal

France 1. Fair Regulatory framework Outreach to public officials about The current regulatory framework includes: Article 23 of the Constitution Articles 432-12 to 432-13 of the criminal code on illegal

topic: Introduce of BAK, current cases of BAK and the main - problems of corruption/economic - investigations (for an European/Austrian investigator)

") Republic of Austria Federal Ministry of the Interior Federal Bureau of Anti-Corruption (BAK) Robert KALENSKY for white collar - crime investigations BAK Investigator topic: Introduce of BAK, current cases

Republic of Austria Federal Ministry of the Interior Federal Bureau of Anti-Corruption (BAK) Robert KALENSKY for white collar - crime investigations BAK Investigator topic: Introduce of BAK, current cases

Insurance Fraud Enforcement Department. Referral guide

Insurance Fraud Enforcement Department Referral guide Published 1 April 2016. Version 1.0. Foreword The Insurance Fraud Enforcement Department (IFED) is a specialist police unit which was established in

Insurance Fraud Enforcement Department Referral guide Published 1 April 2016. Version 1.0. Foreword The Insurance Fraud Enforcement Department (IFED) is a specialist police unit which was established in

Double Jeopardy in Investigations and Prosecutions: Risks and Best Practices for companies and individuals

Double Jeopardy in Investigations and Prosecutions: Risks and Best Practices for companies and individuals A sketch of the legal framework IBA - Anti-Corruption Conference, OECD Paris 15 June 2016 - Double

Double Jeopardy in Investigations and Prosecutions: Risks and Best Practices for companies and individuals A sketch of the legal framework IBA - Anti-Corruption Conference, OECD Paris 15 June 2016 - Double

CONTINENTAL REINSURANCE ANTI-BRIBERY & CORRUPTION POLICY COMPLIANCE AND SUPERVISORY PROCEDURES

CONTINENTAL REINSURANCE ANTI-BRIBERY & CORRUPTION POLICY COMPLIANCE AND SUPERVISORY PROCEDURES 1 INTRODUCTION The Board of Directors ( the Board ) has determined that it is the policy of Continental Reinsurance

CONTINENTAL REINSURANCE ANTI-BRIBERY & CORRUPTION POLICY COMPLIANCE AND SUPERVISORY PROCEDURES 1 INTRODUCTION The Board of Directors ( the Board ) has determined that it is the policy of Continental Reinsurance

FRAUD A MULTIFACETED PHENOMENON TYPES OF FRAUD PREVENTION AND PROTECTION

FRAUD A MULTIFACETED PHENOMENON TYPES OF FRAUD PREVENTION AND PROTECTION Vadym NESTERCHUK Chairman, Director, Optima-leasing /SIXT Oleksandr SHAPOVALOV Authorised Operation Officer Organised Crime Control

FRAUD A MULTIFACETED PHENOMENON TYPES OF FRAUD PREVENTION AND PROTECTION Vadym NESTERCHUK Chairman, Director, Optima-leasing /SIXT Oleksandr SHAPOVALOV Authorised Operation Officer Organised Crime Control

AIG Financial Lines. Claims Intelligence Report

AIG Financial Lines Claims Intelligence Report Part 1 - Directors and Officers May 2012 D&O Claims Introduction There is plenty of speculation and hypotheses around corporate and individual risks, such

AIG Financial Lines Claims Intelligence Report Part 1 - Directors and Officers May 2012 D&O Claims Introduction There is plenty of speculation and hypotheses around corporate and individual risks, such

FRAUD POLICY. Fraud Policy-001

Effective Date: March 28, 2018 Owned by: Fraud Committee Review Cycle: Biennial Last Approved: March 28, 2018 Approved By: Executive Management Committee Revision History Revisions to Policy documents

Effective Date: March 28, 2018 Owned by: Fraud Committee Review Cycle: Biennial Last Approved: March 28, 2018 Approved By: Executive Management Committee Revision History Revisions to Policy documents

Speech at the Public Hearing "Public Procurement: costs we pay for corruption"

EUROPEAN COMMISSION Algirdas Šemeta Commissioner responsible for Taxation and Customs Union, Statistics, Audit and Anti-fraud Speech at the Public Hearing "Public Procurement: costs we pay for corruption"

EUROPEAN COMMISSION Algirdas Šemeta Commissioner responsible for Taxation and Customs Union, Statistics, Audit and Anti-fraud Speech at the Public Hearing "Public Procurement: costs we pay for corruption"

PROGRAMME OF THE 1 st EuroMed Forum of the Prosecutors General

DRAFT PROGRAMME OF THE 1 st EuroMed Forum of the Prosecutors General 23 JANUARY 2018 MADRID, SPAIN 1 THE 1 st EUROMED FORUM OF THE PROSECUTORS GENERAL GENERAL PRESENTATION The First EuroMed Forum of the

DRAFT PROGRAMME OF THE 1 st EuroMed Forum of the Prosecutors General 23 JANUARY 2018 MADRID, SPAIN 1 THE 1 st EUROMED FORUM OF THE PROSECUTORS GENERAL GENERAL PRESENTATION The First EuroMed Forum of the

Justice Committee evidence session: The Work of the Serious Fraud Office (SFO) Pre-hearing memorandum from the Serious Fraud Office

Pre-hearing memorandum from the Serious Fraud Office") Justice Committee evidence session: The Work of the Serious Fraud Office (SFO) Pre-hearing memorandum from the Serious Fraud Office 1 Summary 1.1 This memorandum provides high-level and summary information

Justice Committee evidence session: The Work of the Serious Fraud Office (SFO) Pre-hearing memorandum from the Serious Fraud Office 1 Summary 1.1 This memorandum provides high-level and summary information

Foreign Corrupt Practices Act Policy

I. POLICY/PURPOSE Denny s is committed to conducting its business ethically and in compliance with all applicable laws and regulations, including the U.S. Foreign Corrupt Practices Act (FCPA) and other

I. POLICY/PURPOSE Denny s is committed to conducting its business ethically and in compliance with all applicable laws and regulations, including the U.S. Foreign Corrupt Practices Act (FCPA) and other

Official Journal of the European Union L 256/63. (Acts adopted under Title VI of the Treaty on European Union)

") 1.10.2005 Official Journal of the European Union L 256/63 (Acts adopted under Title VI of the Treaty on European Union) COUNCIL DECISION 2005/681/JHA of 20 September 2005 establishing the European Police

1.10.2005 Official Journal of the European Union L 256/63 (Acts adopted under Title VI of the Treaty on European Union) COUNCIL DECISION 2005/681/JHA of 20 September 2005 establishing the European Police

Anti-Money Laundering and Combating Financing of Terrorism Framework 17 January 2018

Anti-Money Laundering and Combating Financing of Terrorism Framework 17 January 2018 Anti-Money Laundering and Combating Financing of Terrorism Framework ( EIB Group AML-CFT Framework ) Revised version:

Anti-Money Laundering and Combating Financing of Terrorism Framework 17 January 2018 Anti-Money Laundering and Combating Financing of Terrorism Framework ( EIB Group AML-CFT Framework ) Revised version:

I. Introduction. 1 Agreement between the European Union and the United States of America on the processing and transfer of

EDPS comments on the Communication from the Commission to the European Parliament and the Council on a European Terrorist Finance Tracking System (TFTS) and on the Commission Staff Working Document - Impact

EDPS comments on the Communication from the Commission to the European Parliament and the Council on a European Terrorist Finance Tracking System (TFTS) and on the Commission Staff Working Document - Impact

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen:

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

Town of Cohasset FRAUD RISK POLICY Adopted by Board of Selectmen: The Town of Cohasset is committed to protecting its revenue, property, information, and other assets from any attempt, either by members

***I DRAFT REPORT. EN United in diversity EN. European Parliament 2018/0250(COD)

") European Parliament 2014-2019 Committee on Civil Liberties, Justice and Home Affairs 2018/0250(COD) 12.11.2018 ***I DRAFT REPORT on the proposal for a regulation of the European Parliament and of the Council

European Parliament 2014-2019 Committee on Civil Liberties, Justice and Home Affairs 2018/0250(COD) 12.11.2018 ***I DRAFT REPORT on the proposal for a regulation of the European Parliament and of the Council

Suspected fraudulent acts by partner

[CBPF Form 22.a] Suspected fraudulent acts by partner SCOPE This form is to be used to support the reporting and follow up to cases of suspicion of fraud involving CBPF project partners including Partner

[CBPF Form 22.a] Suspected fraudulent acts by partner SCOPE This form is to be used to support the reporting and follow up to cases of suspicion of fraud involving CBPF project partners including Partner

Approval version. G l o b a l P o l i c y : F r a u d R e s p o n s e a n d W h i s t l e b l o w i n g P o l i c y. Board of Directors.

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

Approval version G l o b a l P o l i c y : Issuer Author Approved by Board of Directors Group Legal Department Board of Directors Issue date July 01 2013 Revision history Publication via n/a BCnet Limitations

9228/18 SBC/sr 1 DGG 1A

Council of the European Union Brussels, 24 May 2018 (OR. en) Interinstitutional File: 2018/0058 (COD) 9228/18 'I' ITEM NOTE From: General Secretariat of the Council ECOFIN 477 CODEC 826 RELEX 443 COEST

Council of the European Union Brussels, 24 May 2018 (OR. en) Interinstitutional File: 2018/0058 (COD) 9228/18 'I' ITEM NOTE From: General Secretariat of the Council ECOFIN 477 CODEC 826 RELEX 443 COEST

Liechtenstein. I. Brief Introduction to the Legal System of Liechtenstein

Liechtenstein I. Brief Introduction to the Legal System of Liechtenstein As Liechtenstein is a very small country and has always been greatly affected by Austrian history, both Liechtenstein s legal system

Liechtenstein I. Brief Introduction to the Legal System of Liechtenstein As Liechtenstein is a very small country and has always been greatly affected by Austrian history, both Liechtenstein s legal system

ARTICLE 29 Data Protection Working Party

ARTICLE 29 Data Protection Working Party 00195/06/EN WP 117 Opinion 1/2006 on the application of EU data protection rules to internal whistleblowing schemes in the fields of accounting, internal accounting

ARTICLE 29 Data Protection Working Party 00195/06/EN WP 117 Opinion 1/2006 on the application of EU data protection rules to internal whistleblowing schemes in the fields of accounting, internal accounting

Code of Conduct. This Code of Conduct covers all associates. When appropriate, it also covers all members of the Company's Board of Directors.

Code of Conduct This Code of Conduct has been adopted for the purpose of ensuring that the Company's "Associates" (Officers and Employees) conduct themselves and operate the Company's business in accordance

Code of Conduct This Code of Conduct has been adopted for the purpose of ensuring that the Company's "Associates" (Officers and Employees) conduct themselves and operate the Company's business in accordance

THE KINGDOM OF LESOTHO ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM REGIME

THE KINGDOM OF LESOTHO ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM REGIME ----------------------------------------------------------------- NATIONAL STRATEGY JANUARY 2010 1 TABLE OF

THE KINGDOM OF LESOTHO ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM REGIME ----------------------------------------------------------------- NATIONAL STRATEGY JANUARY 2010 1 TABLE OF

Ampco-Pittsburgh Corporation

Ampco-Pittsburgh Corporation CODE OF BUSINESS CONDUCT AND ETHICS For Directors, Officers, Employees and Business Partners of Ampco-Pittsburgh Corporation and its subsidiaries Adopted on December 14, 2004

Ampco-Pittsburgh Corporation CODE OF BUSINESS CONDUCT AND ETHICS For Directors, Officers, Employees and Business Partners of Ampco-Pittsburgh Corporation and its subsidiaries Adopted on December 14, 2004

ANTI-CORRUPTION POLICY

ANTI-CORRUPTION POLICY BACKGROUND: Alcoa Corporation ( Alcoa ) and its management are committed to conducting all of it operations around the globe, ethically and in compliance with all applicable laws.

ANTI-CORRUPTION POLICY BACKGROUND: Alcoa Corporation ( Alcoa ) and its management are committed to conducting all of it operations around the globe, ethically and in compliance with all applicable laws.

ANTI-BRIBERY POLICY AND ANTI-FRAUD POLICY AND RESPONSE PLAN

University for the Creative Arts Financial Regulations: Appendix K ANTI-BRIBERY POLICY AND ANTI-FRAUD POLICY AND RESPONSE PLAN INDEX 1. Introduction 2. Definitions 3. Culture 4. Responsibilities and Reporting

University for the Creative Arts Financial Regulations: Appendix K ANTI-BRIBERY POLICY AND ANTI-FRAUD POLICY AND RESPONSE PLAN INDEX 1. Introduction 2. Definitions 3. Culture 4. Responsibilities and Reporting

ANTI-FRAUD AND CORRUPTION POLICY

ANTI-FRAUD AND CORRUPTION POLICY AIM/PURPOSE 1.1 Trinity Church of England High School (Academy) is committed to ensuring that it acts with integrity and has high standards. Everyone involved with the

ANTI-FRAUD AND CORRUPTION POLICY AIM/PURPOSE 1.1 Trinity Church of England High School (Academy) is committed to ensuring that it acts with integrity and has high standards. Everyone involved with the

Global Policy on Anti-Bribery and Anti-Corruption

1 Global Policy on Anti-Bribery and Anti-Corruption OUR GLOBAL POLICY ON ANTI-BRIBERY AND ANTI-CORRUPTION Did You know?? PolyOne is committed to the prevention, deterrence and detection of fraud, bribery

1 Global Policy on Anti-Bribery and Anti-Corruption OUR GLOBAL POLICY ON ANTI-BRIBERY AND ANTI-CORRUPTION Did You know?? PolyOne is committed to the prevention, deterrence and detection of fraud, bribery

Anti-Fraud Policy Date: Version: Review Date:

Anti-Fraud Policy Date: July 2017 Version: 4.0 Review Date: July 2019 Policy Title Anti-Fraud Policy Policy Number: POL 022 Version 4.0 Policy Sponsor Policy Owner Committee Chief Executive Director of

Anti-Fraud Policy Date: July 2017 Version: 4.0 Review Date: July 2019 Policy Title Anti-Fraud Policy Policy Number: POL 022 Version 4.0 Policy Sponsor Policy Owner Committee Chief Executive Director of

ADVISORY White Collar

ADVISORY White Collar April 15, 2010 THE BRIBERY ACT 2010 - A BRAVE NEW WORLD FOR BUSINESS? Summary On 8 April 2010, the UK Bribery Bill received Royal Assent as the Bribery Act 2010 (the Act ). The Act,

ADVISORY White Collar April 15, 2010 THE BRIBERY ACT 2010 - A BRAVE NEW WORLD FOR BUSINESS? Summary On 8 April 2010, the UK Bribery Bill received Royal Assent as the Bribery Act 2010 (the Act ). The Act,

Tudor Grange Academies Trust Financial Procedures Handbook Publication Date: June 2013 Version 01. Anti Bribery Policy. Page 1

Anti Bribery Policy Page 1 1. INTRODUCTION 1.1 This document sets out the Tudor Grange Academy Trust s policy and advice to employees in dealing with bribery or suspected bribery. This policy details the

Anti Bribery Policy Page 1 1. INTRODUCTION 1.1 This document sets out the Tudor Grange Academy Trust s policy and advice to employees in dealing with bribery or suspected bribery. This policy details the

ANTI-FRAUD POLICY AND RESPONSE PLAN FOR BARLOWORLD LIMITED

ANTI-FRAUD POLICY AND RESPONSE PLAN FOR BARLOWORLD LIMITED Table of Contents GLOSSARY OF TERMS... 3 1. BACKGROUND... 3 2. ETHICS... 4 3. SCOPE OF THE POLICY... 4 4. THE POLICY... 4 5. REPORTING PROCEDURES

ANTI-FRAUD POLICY AND RESPONSE PLAN FOR BARLOWORLD LIMITED Table of Contents GLOSSARY OF TERMS... 3 1. BACKGROUND... 3 2. ETHICS... 4 3. SCOPE OF THE POLICY... 4 4. THE POLICY... 4 5. REPORTING PROCEDURES

Counterfeiting of Euro (penal aspects) Ministry of Interior General Police Directorate Criminal Police Directorate

Ministry of Interior General Police Directorate Criminal Police Directorate") Counterfeiting of Euro (penal aspects) Ministry of Interior General Police Directorate Criminal Police Directorate Overview of the legislation National legislation Constitution Criminal Code Criminal Procedure

Counterfeiting of Euro (penal aspects) Ministry of Interior General Police Directorate Criminal Police Directorate Overview of the legislation National legislation Constitution Criminal Code Criminal Procedure

L 145/30 Official Journal of the European Union

L 145/30 Official Journal of the European Union 31.5.2011 REGULATION (EU) No 513/2011 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 11 May 2011 amending Regulation (EC) No 1060/2009 on credit rating

L 145/30 Official Journal of the European Union 31.5.2011 REGULATION (EU) No 513/2011 OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 11 May 2011 amending Regulation (EC) No 1060/2009 on credit rating

Recent developments and proposed reforms affecting the legal profession in Portugal

Recent developments and proposed reforms affecting the legal profession in Portugal ECBA Spring Conference Budapest May 7 2011 Carlos Pinto de Abreu e Associados Sociedade de Advogados, RL. Alameda Quinta

Recent developments and proposed reforms affecting the legal profession in Portugal ECBA Spring Conference Budapest May 7 2011 Carlos Pinto de Abreu e Associados Sociedade de Advogados, RL. Alameda Quinta

COMMISSION OF THE EUROPEAN COMMUNITIES REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 16.10.2009 COM(2009)526 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT on the follow-up to 2007 Discharge Decisions (Summary) - European

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 16.10.2009 COM(2009)526 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT on the follow-up to 2007 Discharge Decisions (Summary) - European

Whistle-Blowing Policy

2011 Ithmaar Bank Risk Management & Compliance Division 21-Oct-11 Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 4 3.0- Actions Constituting Fraud 4 3.1- Criminal

2011 Ithmaar Bank Risk Management & Compliance Division 21-Oct-11 Table of Contents Table of Contents 2 1.0- Statement of Purpose: 3 2.0- Responsibilities 4 3.0- Actions Constituting Fraud 4 3.1- Criminal

The Co-operative Academies Trust Anti-Fraud and Anti-Bribery Policy. Approved by the Trust Board on 21 April 2016 Implementation from 22 April 2016

The Co-operative Academies Trust Anti-Fraud and Anti-Bribery Policy Approved by the Trust Board on 21 April 2016 Implementation from 22 April 2016 April 2016 1 Anti-Fraud and Anti-Bribery Policy Contents

The Co-operative Academies Trust Anti-Fraud and Anti-Bribery Policy Approved by the Trust Board on 21 April 2016 Implementation from 22 April 2016 April 2016 1 Anti-Fraud and Anti-Bribery Policy Contents

Council of Europe COMMITTEE OF MINISTERS

Word FranГais Explanatory Memorandum Council of Europe COMMITTEE OF MINISTERS Recommendation Rec(2001)11 of the Committee of Ministers to member states concerning guiding principles on the fight against

Word FranГais Explanatory Memorandum Council of Europe COMMITTEE OF MINISTERS Recommendation Rec(2001)11 of the Committee of Ministers to member states concerning guiding principles on the fight against

FCPA, UK Bribery Act interpreted from a EU non-us/uk perspective

NYSBA Prague Regional Meeting 2012 Friday, 9th of March FCPA, UK Bribery Act interpreted from a EU non-us/uk perspective Otto Waechter, Philip Rosenauer NYSBA Prague Regional Meeting 2012 Friday, 9th of

NYSBA Prague Regional Meeting 2012 Friday, 9th of March FCPA, UK Bribery Act interpreted from a EU non-us/uk perspective Otto Waechter, Philip Rosenauer NYSBA Prague Regional Meeting 2012 Friday, 9th of

Member States capabilities in fighting tax crimes

Latvia Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax burden.

Latvia Tax avoidance is understood as a legal act - unless deemed illegal by the tax authorities or, ultimately, by the courts - of using tax regimes to one's own advantage to reduce one's tax burden.

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of

Fraud Risk Assessment CARRIE KENNEDY, PARTNER DUSTIN BIRASHK, PARTNER Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed as advice of