Important Definitions. Basis of charge & rates of tax. Basic Concepts. Components of Income-tax Law

|

|

|

- Claude Carroll

- 6 years ago

- Views:

Transcription

1 BASICCONCEPTS comprehend the meaning of tax and types of taxes. discern the difference between direct and indirecttaxes. appreciate the components of income-tax law. comprehend the procedure for computation of total income for the purpose of levyof income-tax. comprehend and appreciate the meaning of the important terms used in the Income-taxAct,1961. recognise the previous year and assessment year for the purpose of computing incomechargeableto taxunder the Income-taxAct,1961. explain the circumstances when income of the previous year would be assessed to taxin thepreviousyearitself. apply the rates of tax applicable on different components of total income of a personfor thepurpose of determining the taxliability of such person.

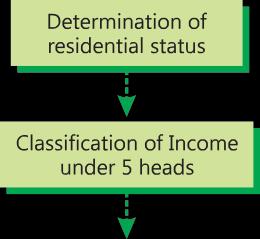

2 Basic Concepts Components of Income-tax Law Steps for computation of total Income(TI) and tax liability Important Definitions Basis of charge & rates of tax Incometax Act, 1961 Annual Finance Act Income tax Rules Determination of residential status Classification of income under different heads Computation of income under each head Assessee Assessment Person Income Charge of Income tax Rates of Income tax Circulars and Notification s Legal decisions Clubbing of income of spouse, minor child etc. Set off or carry forward & set off of losses Computation of Gross total income(gti) Deductions from GTI India Assessment Year Previous Year Maximum Marginal Rate & Average Rate Computation of TI Computation of tax liability

3 What is Tax? Taxis afee charged by agovernment on aproduct, income or activity. Thereare two types of taxes direct taxesand indirect taxes. Direct Taxes: If tax is levied directly on the income or wealth of a person, then, it is a direct taxe.g. income-tax. Indirect Taxes: If tax is levied on the price of a good or service, then, it is an indirect tax e.g. Goods and Services Tax(GST) or Custom Duty. In the case of indirect taxes, the person paying the tax passes on the incidence to another person. INCOME TAX DIRECT TAXES TAX ON UNDISCLOSED FOREIGN INCOME AND ASSETS TYPE OF TAXES GOODS AND SERVICES TAX (GST) INDIRECT TAXES CUSTOMS DUTY

4 Why are Taxes Levied? The reason for levy of taxes is that they constitute the basic source of revenue to the Government. Revenue so raised is utilized for meeting the expenses of Government like defence, provision of education, health-care, infrastructure facilities like roads, dams etc.

5 Overview of Income-tax law in India The income-tax law in India consists of the following components

6 Levy of Income-tax Income-tax is a tax levied on the total income of the previous year of every person (Section 4). A person includes an individual, Hindu Undivided Family (HUF), Association of Persons (AOP), Body of Individuals (BOI), a firm, a company etc. (1) Total Income and Tax Payable Income-tax is levied on an assessee s total income. Such total income has to be computed as per the provisions contained in the Income-tax Act, Let us go step by step to understand the procedure for computation of total income of an individual for the purpose of levy of income-tax Step 1 Determination of residential status The residential status of a person has to be determined to ascertain which income is to be included in computing the total income. Theresidential statusasper the Income-taxAct,1961canbe classifiedasunder

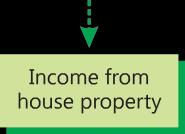

7 Step 2 Classification of income under different heads TheActprescribes five heads of income. Theseare shownbelow There is a charging section under each head of income which defines the scope of income chargeable under that head. These heads of income exhaust all possible types of income that can accrue to or be received by the tax payer. Accordingly, the income is classified as follows: 1. Salary, pension earned is taxable under the head Salaries. 2. Rental income is taxable under the head Income from house property. 3. Income derived from carrying on any business or profession is taxable under the head Profits and gains from business or profession. 4. Profit from sale of a capital asset (like land) is taxable under the head Capital Gains. 5. Thefifth head of income is the residuary head. Theincome whichis not taxable under the first four headswill be taxedunder the head Income from other sources. The tax payer has to classify the income earned under the relevant head of income. Step 3 Computation of income under each head Income is to be computed in accordance with the provisions governing a particular head of income.

8 Exemptions: There are certain incomes which are wholly exempt from income-tax e.g. agricultural income. These incomes have to be excluded and will not form part of Gross Total Income. Also, some incomes are partially exempt from income-tax e.g. House Rent Allowance, Education Allowance. These incomes are excluded only to the extent of the limits specified in the Act. The balance income over and above the prescribed exemption limits would enter computation of total income and have to be classified under the relevant head of income. Deductions: There are deductions and allowances prescribed under each head of income. For example, while calculating income from house property, municipal taxes and interest on loan are allowed as deduction. Similarly, deductions and allowances are prescribed under other heads of income. These deductions etc. have to be considered before arriving atthe net incomechargeable under eachhead. Step 4 Clubbing of income of spouse, minor child etc. In case of individuals, income-tax is levied on a slab system on the total income. The tax system is progressive i.e. as the income increases, the applicable rate of tax increases. Some taxpayers in the higher income bracket have a tendency to divert some portion of their incometo their spouse,minor child etc.to minimize their tax burden. In order to prevent such tax avoidance, clubbing provisions have been incorporated in the Act, under which income arising to certain persons (like spouse, minor child etc.) have to be included in the income of the person who has diverted his income for the purpose of computing taxliability.

9 Step 5 Set-off or carry forward and set-off of losses An assessee may have different sources of income under the same head of income. He might have profit from one source and loss from the other. For instance, an assessee may have profit from his textile business and loss from his printing business. This loss can be set-off against the profits of textile business to arrive at the net income chargeable under the head Profits and gains of business or profession. Similarly, an assessee can have loss under one head of income, say, Income from house property and profits under another head of income, say, profits and gains of business or profession. There are provisions in the Income-tax Act, 1961 for allowing inter-head adjustment in certaincases. However, there are also restrictions in certain cases, like business loss is not allowed to be set-off against salary income. Further, losses which cannot be setoff in the current year due to inadequacy of eligible profits can be carried forward for set-off in the subsequent years as per the provisions contained in the Act. Step 6 Computation of Gross Total Income The final figures of income or loss under each head of income, after allowing the deductions, allowances and other adjustments, are then aggregated, after giving effect to the provisions for clubbing of income and set-off and carry forward of losses,to arrive at the gross totalincome.

10 Step 7 Deductions from Gross Total Income There are deductions prescribed from Gross Total Income. These deductions are of three types DEDUCTIONS FROM GROSS TOTAL INCOME DEDUCTIONS IN RESPECT OF CERTAIN PAYMENTS DEDUCTIONS IN RESPECT OF CERTAIN INCOMES OTHER DEDUCTIONS Examples 1. Life Insurance Premium paid 2. Contribution to Provident Fund/Pension Fund 3. Medical insurance premium paid 4. Payment of interest on loan taken for higher education 5. Rent paid 6. Donation to certain funds, charitable institutions, etc. 7. Contributions to political parties Examples 1. Profits and gains from Industrial undertakings or enterprises engaged in infrastructure development 2. Profits and gains by an undertaking/ enterprise engaged in development of special economic zone. 3. Certain income of cooperative societies 4. Royalty income etc. of authors of certain books other than text-books. 5. Royalty on patents. Examples Deduction in case of a person with disability

11 Step 8 Total income The income arrived at, after claiming the above deductions from the Gross Total Income is known as the Total Income. It should be rounded off to the nearest multiple of ` 10.

12

13 Step 9 Application of the rates of tax on the total income The rates of tax for the different classes of assessees are prescribed by the Annual Finance Act. For individuals, HUFs etc., there is a slab rate and basic exemption limit. At present, the basic exemption limit is ` 2,50,000 for individuals. This means that no taxis payable by individuals with total income of up to ` 2,50,000. Those individuals whose total income is more than ` 2,50,000 but less than ` 5,00,000 have to pay tax on their total income in excess of ` 5%and soon. The highest rate is 30%, which is attracted in respect of income in excess of ` 10,00,000. The tax rates have to be applied on the total income to arrive at the income-tax liability.

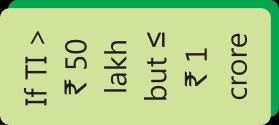

14 Step 10 - Surcharge / Rebate under section 87A Surcharge: Surcharge is an additional tax payable over and above the income-tax. Surcharge is levied as a percentage of income-tax. In case where the total income of an individual/huf/aop/boi exceeds ` 50 lakhs but does not exceed ` 1 crore, surcharge is payable atthe rateof 10% of income-tax and in casetotal income exceeds ` 1 crore,surchargeispayable atthe rateof 15%of income-tax. Rebate under section 87A: In order to provide tax relief to the individual tax payers who are in the 5% tax slab, section 87A provides a rebate from the tax payable by an assessee, being anindividual resident in India, whosetotal incomedoes not exceed ` 3,50,000. The rebate shall be equal to the amount of income-tax payable on the total incomefor anyassessmentyearor anamount of ` 2,500, whichever is less. Level of Total Income Surcharge Rebate u/s 87A ` 3,50,000 Not applicable Income-tax on total income or ` 2,500, whichever is less > ` 3,50,000 ` 50,00,000 Not applicable Not applicable > ` 50,00,000 10% of income-tax Not applicable ` 1,00,00,000 > ` 1,00,00,000 15% of income-tax Not applicable Step 11 Education cess and secondary and higher education cess on income-tax The income-tax, asincreased by the surcharge or asreduced by the rebate under section87a, if applicable, is to be further increased by an additional surcharge called education cess@2% and secondary and higher education cess on of income-tax plus surcharge, if applicable.

15 Step 12 Advance tax and tax deducted at source Although the tax liability of an assessee is determined only at the end of the year, tax is required to be paid in advance in four installments on the basis of estimated income i.e., on or before 15 th June, 15 th September, 15 th December and 15 th March. However, residents opting for presumptive taxation scheme can pay advance taxin one installment on or before 15 th March instead of four installments. In certain cases, tax is required to be deducted at source from the income by the payer at the rates prescribed in the Income-tax Act, 1961 or the Annual Finance Act. Such deduction should be made either at the time of accrualor at the time of payment, asprescribed by the Act. For example, in the case of salary income, the obligation of the employer to deduct tax at source arises only at the time of payment of salary to the employees. However, in respect of other payments like, fees for professional services, fees for technical services, interest made to residents, the person responsible for paying is liable to deduct tax at source at the time of credit of such income to the accounts of the payee or at the time of payment, whichever is earlier. Suchtaxdeducted at source has to be remitted to the credit of the Central Government through any branch of the RBI,SBIor any authorized bank.

16 Step 13: Tax Payable/Tax Refundable After adjusting the advance tax and tax deducted at source, the assessee would arrive at the amount of net tax payable or refundable. Such amount should be rounded off to the nearest multiple of ` 10. The assessee has to pay the amount of tax payable (called self-assessment tax) on or before the due date of filing of the return. Similarly, if any refund is due, assesseewill get the sameafter filing the return of income. (2) Return of Income The Income-tax Act, 1961 contains provisions for filing of return of income. Return of income is the format in which the assessee furnishes information as to his total income and tax payable. The format for filing of returns by different assessees is notified by the CBDT. The particulars of income earned under different heads, gross total income, deductions from gross total income, total income and tax payable by the assessee are required to be furnished in a return of income. In short, a return of income is the declaration of income by the assesseein the prescribed format.

17 IMPORTANT DEFINITIONS 2.1 Assessee [Section 2(7)] Assessee means a person by whom any tax or any other sum of money is payable under this Act. In addition, it includes Every person in respect of whom any proceeding under this Act has been taken for the assessment of his income;or assessment of fringe benefits; or the income of any other person in respect of which he is assessable; or the loss sustained by him or by such other person; or the amount of refund due to him or by such other person. Every person who is deemed to be an assessee under any provision of this Act; Every person who is deemed to be an assessee-in-default under any provision of this Act.

![2. Assessment [Section 2(8)] This is the procedure by which the income of an assessee is determined by the Assessing Officer.](/docs-images/77/75781292/images/18-0.jpg "It may be by way of a normal assessment or by way of reassessment of an income previously assessed. 3.")

18 2. Assessment [Section 2(8)] This is the procedure by which the income of an assessee is determined by the Assessing Officer. It may be by way of a normal assessment or by way of reassessment of an income previously assessed. 3. Person [Section 2(31)] The definition of assessee leads us to the definition of person as the former is closely connected with the latter. The term person is important from another point of view also viz., the charge of income-tax is on every person.

19 PREVIOUS YEAR AND ASSESSMENT YEAR 1. Assessment year The term has been defined under section 2(9). This means a period of 12 months commencing on 1 st April every year. The year in which income is earned is the previous year and such income is taxable in the immediately following year which is the assessment year. Income earned in the previous year istaxablein the assessmentyear Previous year The term has been defined under section 3. It means the financial year immediately preceding the assessmentyear. Asmentioned earlier, the income earned during the previous year is taxable in the assessment year. Business or profession newly set up during the financial year - In such a case, the previous year shall be the period beginning on the date of setting up of the business or profession and ending with31 st Marchof thesaidfinancialyear. Examples: 1. A is running a business from 1993 onwards. Determine the previous year for the assessment year Ans. The previous year will be to A chartered accountant sets up his profession on 1st July, Determine the previous year for the assessment year Ans. The previous year will be from to

20 Previous year for undisclosed sources of income Cash Credits [Section 68] Unexplained Investments [Section 69] Amount borrowed or repaid on hundi [Section 69D] Undisclosed sources of income Unexplained money [Section 69A] Unexplained expenditure [Section 69C] Investment etc. not fully disclosed [Section 69B]

21 There are many occasions when the Assessing Officer detects cash credits, unexplained investments, unexplained expenditure etc, the source for which is not satisfactorily explained by the assessee to the Assessing Officer. The Act contains aseriesof provisions to provide for these contingencies: (i) Cash Credits [Section 68] Where any sum is found credited in the books of the assessee and the assessee offers no explanation about the nature and source or the explanation offered is not satisfactory in the opinion of the Assessing Officer, the sum so credited may be charged as income of the assessee of that previous year. (ii) Unexplained Investments [Section 69] Where in the financial year immediately preceding the assessment year, the assessee has made investments which are not recorded in the books of account and the assessee offers no explanation about the nature and the source of investments or the explanation offered is not satisfactory, the value of the investments are taxed as income of the assessee of such financialyear.

22 (iii)unexplained money etc. [Section 69A] Where in any financial year the assessee is found to be the owner of any money, bullion, jewellery or other valuable article and the same is not recorded in the books of account and the assessee offers no explanation about the nature and source of acquisition of such money, bullion etc. or the explanation offered is not satisfactory, the money and the value of bullion etc. may be deemed to be the income of the assessee for such financial year. Ownership is important and mere possession isnot enough. (iv)amount of investments etc., not fully disclosed in the books of account [Section 69B] Where in any financial year the assessee has made investments or is found to be the owner of any bullion, jewellery or other valuable article and the Assessing Officer finds that the amount spent on making such investments or in acquiring such articles exceeds the amount recorded in the books of account maintained by the assessee and he offers no explanation for the difference or the explanation offered is unsatisfactory, such excess may be deemed to be the income of the assesseefor suchfinancialyear.

23 Example: If the assessee is found to be the owner of say 300 gms of gold (market value of which is ` 25,000) during the financial year ending but he has recorded to have spent ` 15,000 in acquiring it, the Assessing Officer can add ` 10,000 (i.e. the difference of the market value of such gold and ` 15,000) as the income of the assessee, if the assessee offers no satisfactory explanation thereof. (v) Unexplained expenditure [Section 69C] Where in any financial year an assessee has incurred any expenditure and he offers no explanation about the source of such expenditure or the explanation is unsatisfactory the Assessing Officer can treat such unexplained expenditure as the income of the assessee for such financial year. Such unexplained expenditure which is deemed to be the income of the assesseeshallnot be allowedasdeduction under anyhead of income. (vi)amount borrowed or repaid on hundi [Section 69D] Where any amount is borrowed on ahundi or any amount due thereon is repaid other than through an account-payee cheque drawn on a bank, the amount so borrowed or repaid shall be deemed to be the income of the person borrowing or repaying for the previous yearin whichthe amount wasborrowed or repaid, asthe casemay be. However, where any amount borrowed on a hundi has been deemed to be the income of any person, he will not be again liable to be assessed in respect of such amount on repayment of such amount. The amount repaid shall include interest paid on the amount borrowed.

24 Certain cases when income of a previous year will be assessed in the previous year itself General Rule Income of a previous year is assessed in the assessment year following the previous year Exceptions to this rule Cases where income of a previous year is assessed in the previous year itself Shipping business of non-resident Persons leaving India AOP / BOI / Artificial Juridical Person formed for a particular event or purpose Persons likely to transfer property to avoid tax Discontinued business

25 The income of an assessee for a previous year is charged to income-tax in the assessment year following the previous year. For instance, income of previous year is assessed during Therefore, is the assessment year for assessmentof income of the previous year However, in a few cases, this rule does not apply and the income is taxed in the previous year in which it is earned. These exceptions have been made to protect the interests of revenue. Theexceptions are asfollows: (i) Shipping business of non-resident [Section 172] Where a ship, belonging to or chartered by a non-resident, carries passengers, livestock, mail or goods shipped at a port in India, the ship is allowed to leave the port only when the tax has been paid or satisfactory arrangement has been made for payment thereof. 7.5% of the freight paid or payable to the owner or the charterer or to any person on his behalf, whether in India or outside India on account of suchcarriage is deemed to be his income whichis charged to taxin the sameyear in whichit isearned. (ii) Persons leaving India [Section 174] Where it appears to the Assessing Officer that any individual may leave India during the current assessment year or shortly after its expiry and he has no present intention of returning to India, the total income of such individual for the period from the expiry of the respective previous year up to the probable date of his departure from India is chargeable to taxin that assessmentyear.

26 Example: Suppose Mr. X is leaving India for USA on and it appears to the Assessing Officer that he has no intention to return. Before leaving India, Mr. X will be required to pay income tax on the income earned during the P.Y as well as the total income earned during the period to (iii)aop / BOI / Artificial Juridical Person formed for a particular event or purpose [Section 174A] If an AOP/BOI etc. is formed or established for a particular event or purpose and the Assessing Officer apprehends that the AOP/BOI is likely to be dissolved in the same year or in the next year, he can make assessment of the income up to the date of dissolution asincome of the relevant assessment year. (iv)persons likely to transfer property to avoid tax [Section 175] During the current assessment year, if it appears to the Assessing Officer that a person is likely to charge, sell, transfer, dispose of or otherwise part with any of his assets to avoid payment of any liability under this Act, the total income of such person for the period from the expiry of the previous year to the date, when the Assessing Officer commences proceedings under this section is chargeable to tax in that assessment year. (v) Discontinued business [Section 176] Where any business or profession is discontinued in any assessment year, the income of the period from the expiry of the previous year up to the date of such discontinuance may, at the discretion of the Assessing Officer, be charged to tax in that assessment year.

27 Rates of Tax Income-tax is to be charged at the rates fixed for the year by the annual FinanceAct. The slab rates applicable for A.Y are as follows: (1) Individual / Hindu Undivided Family (HUF) / Association of Persons (AOP) / Body of Individuals (BOI) / Artificial Juridical Person. (i) where the total income does not exceed ` 2,50,000 (ii) where the total income exceeds ` 2,50,000but does not exceed ` 5,00,000 (iii) where the total income exceeds ` 5,00,000but does not exceed ` 10,00,000; (iv) where the total income exceeds ` 10,00,00 NIL 5% of the amount by which the total income exceeds ` 2,50,000 ` 12,500 plus 20% of the amount by which the total income exceeds ` 5,00,000 ` 1,12,500 plus 30% of the amount by which the total income exceeds ` 10,00,000

28 ILLUSTRATION 1 Mr. X has a total income of ` 12,00,000 comprising of his salary income and interest on fixed deposit. Compute his tax liability. SOLUTION Computation of Tax liability Tax liability = ` 1,12, % of ` 2,00,000 = `1,72,500 Alternatively: Tax liability: First ` 2,50,000 Next ` 2,50,000 `5,00,000 Next ` 5,00,000 `10,00,000 Balance i.e. ` 12,00,000 minus `10,00,000 - Nil 5% of ` 2,50,000 20% of ` 5,00,000 30% of ` 2,00,000 = ` 12,500 = ` 1,00,000 = ` 60,000 = ` 1,72,500

29 It isto be noted that for asenior citizen(being aresident individual whoisof the age of 60years but not more than 80 years at any time during the previous year), the basic exemption limit is ` 3,00,000. Further, resident individuals of the age of 80 years or more at any time during the previous year,being very senior citizens, would be eligible for ahigher basic exemption limit of ` 5,00,000. Therefore, the tax slabs for these assesseeswould be as follows For senior citizens (being resident individuals of the age of 60 years or more but less than 80 years) (i) where the total income does not exceed ` 3,00,000 (ii) where the total income exceeds ` 3,00,000but does not exceed ` 5,00,000 NIL 5% of the amount by which the total income exceeds ` 3,00,000 (iii) where the total income exceeds ` 5,00,000but does not exceed ` 10,00,000; (iv) where the total income exceeds ` 10,00,00 ` 10,000 plus 20% of the amount by which the total income exceeds ` 5,00,000 ` 1,10,000 plus 30% of the amount by which the total income exceeds ` 10,00,000

30 For resident individuals of the age of 80 years or more at any time during the previous year (i) where the total income does not exceed ` 5,00,000 NIL (ii) where the total income exceeds ` 5,00,000but does not exceed ` 10,00,000; (iv) where the total income exceeds ` 10,00,00 20% of the amount by which the total income exceeds ` 5,00,000 ` 1,00,000 plus 30% of the amount by which the total income exceeds ` 10,00,000

31 (2) Firm/LLP On the whole of the total income (3) Local authority On the whole of the total income (4) Co-operative society (i) Where the total income does not exceed ` 10,000 (ii) Where the total income exceeds ` 10,000 but does not exceed ` 20,000 (iii) Where the total income exceeds ` 20,000 30% 30% 10% of the total income ` 1,000 plus 20% of the amount by which the total income exceeds` 10,000 ` 3,000 plus 30% of the amount by which the total income exceeds` 20,000 (5) Company (i) In the case of a domestic company If the total turnover or gross receipt in the P.Y ` 50 crore: 25% of the total income. In other case: 30% of the total income (ii) In the case of a 40% on the total income company other than a However, specified royalties and fees for rendering technical services (FTS) domestic company received from Government or an Indian concern in pursuance of an approved agreement made by the company with the Government or Indian concern between and (in case of royalties) and between and (in caseof FTS) would be chargeable to

32 The above rates are prescribed by the Finance Act, However, in respect of certain types of income,asmentioned below,the Income-taxAct,1961hasprescribed specific rates S. No. Section Income Rate of Tax (a) 112 Long term capital gains (For details, refer Unit 4 of Chapter 4 on Capital gains ) (b) 111A Short-term capital gains on transfer of Equity shares in a company Unit of an equity oriented fund Unit of business trust The conditions for availing the benefit of this concessional rate are (i)the transaction of sale of such equity share or unit should be entered into on or after and (ii)such transaction should be chargeable to securities transaction tax. (c) 115BB Winning from Lotteries Crossword puzzles Race including horse races Card game and other game of any sort Gambling or betting of any form 20% 15% 30% (d) 115BBDA (See Note 1 Below) Income by way of dividend exceeding ` 10 lakhs in aggregate 10% (e) 115BBE (See Note 2 below) Unexplained money, investment, expenditure, etc. deemed as income under section 68 or section 69 or section 69A or section 69B or section 69C or section 69D 60%

33 Notes: (1) Taxability of dividend under section 115BBDA Section 115BBDA provides that any income by way of aggregate dividend in excess of ` 10 lakh shall be chargeable to tax in the hands of a person other than a domestic company or a fund or institution or trust or any university or other educational institution or any hospital or other medical institution 2 or a trust or institution 3 who is resident in India, at the rate of 10%. Further, the taxation of dividend income in excess` 10 lakh shall be on gross basis i.e., no deduction in respect of any expenditure or allowance or set-off of loss shall be allowed to the assesseein computing the incomeby wayofdividends. (2) Unexplained money, investments etc. to attract [Section 115BBE] (i) In order to control laundering of unaccounted money by availing the benefit of basic exemption limit, the unexplained money, investment, expenditure, etc. deemed as incomeunder section68 or section69 or section69aor section69bor section69cor section 69D would be taxed at the rate of 60% plus of tax. Thus, the effective rate of tax (including surcharge@25% of tax and cess@3% of tax and surcharge)is 77.25%. (ii) No basic exemption or allowance or expenditure shall be allowed to the assesseeunder anyprovision of the Income-taxAct,1961in computing suchdeemedincome. (iii)further, no set off of any loss shall be allowable against income brought to tax under sections68or section69or section69aor section69bor section 69Cor section69d.

34 4.2 Surcharge The rates of surcharge applicable for A.Y are asfollows: (i) Individual/HUF/AOP/BOI/Artificial juridical person (a) Where the total income > ` 50 lakh but is ` 1 crore Where the total income exceeds ` 50 lakh but does not exceed ` 1 crore, surcharge is payable at the rate of 10% of income-tax computed in accordance with the provisions of sub-para (1) of para 4.1 above or section 111A or section112. Marginal relief Marginal relief is available in case of such persons having a total income exceeding ` 50 lakh i.e., the total amount of income-tax payable (together with surcharge) on such income should not exceed the amount of income-tax payable on ` 50 lakh by more than the amount of income that exceeds ` 50 lakh.

35 ILLUSTRATION 2 Compute the tax liability of Mr. A (aged 42), having total income of ` 51 lakhs for the Assessment Year Assume that his total income comprises of Salary income, Income under the head house property and Interest from Saving Bank Account.

36 SOLUTION 2 Computation of tax liability of Mr. A for the A.Y (A) Tax payable including surcharge on total income of ` 51,00,000 ` 2,50,000 ` 5% ` 5,00,000 ` 20% ` 10,00,000 ` 51,00,000@30% Total Add: 10% (B) Tax Payable on total income of ` 50 lakhs (` 12,500 plus `1,00,000 plus ` 12,00,000) (C) Excess tax payable(a)-(b) ` 12,500 ` 1,00,000 ` 12,30,000 ` 13,42,500 (D) Marginal Relief (` 1,64,250 ` 1,00,000, being the amount of income in excess of ` 50,00,000) (E) Tax payable(a)-(d) Add: Education andshec@2% Tax Liability Tax Liability (Rounded off) ` 1,34,250 ` 14,76,750 ` 13,12,500 ` 1,64,250 ` 64,250 ` 14,12,500 ` 42,375 ` 14,54,875 ` 14,54,880

37 (b) Where the total income > ` 1 crore Where the total income exceeds ` 1 crore, surcharge is payable at the rate of 15% of income-tax computed in accordance with the provisions of sub-para (1) of para 4.1 above or section 111A or section 112. Marginal relief Marginal relief is available in case of such persons having a total incomeexceeding ` 1 crore i.e., the total amount of income-tax payable (together with surcharge) should not exceed the amount of income-tax and surcharge payable on total income of ` 1 crore by more than the amount of income that exceeds ` 1 crore. ILLUSTRATION 3 Compute the tax liability of Mr. A (aged 42), having total income of ` 1,01,00,000 for the Assessment Year Assume that his total income comprises of Salary income, Income under the head house property and Interest from fixed deposit Account.

38 SOLUTION 3 Computation of tax liability of Mr. A for the A.Y (A) Tax payable including surcharge on total income of ` 1,01,00,000 ` 2,50,000 ` 5% ` 5,00,000 ` 20% ` 10,00,000 ` 1,01,00,000@30% Total Add: 15% (B) TaxPayable on total income of ` 1 crore [(` 12,500 plus ` 1,00,000 plus ` 27,00,000) plus surcharge@10%] ` 12,500 ` 1,00,000 ` 27,30,000 ` 28,42,500 (C) Excess tax payable(a)-(b) (D) Marginal Relief (` 1,75,125 ` 1,00,000, being the amount of income in excess of ` 1,00,00,000) ` 4,26,375 ` 32,68,875 ` 30,93,750 ` 1,75,125 ` 75,125 (E) Tax payable(a)-(d) ` 31,93,750 Add: Education and SHEC@2% ` 95,813 Tax Liability ` 32,89,563 Tax Liability (Rounded off) ` 32,89,560 (ii) Firm/Limited Liability Partnership/Local Authorities/Co-operative societies Where the total income exceeds ` 1 crore, surcharge is payable at the rate of 12% of income-tax computed in accordance with the provisions of sub-para (2)/(3)/(4) of para 4.1 above or section 111A or section 112. Marginal relief Marginal relief is available in case of such persons i.e. the additional amount of income- tax payable (together with surcharge) on the excessof income over ` 1 crore should not be more than the amount of incomeexceeding` 1 crore.

39 (iii) Domestic company (a) In case of a domestic company, whose total income >` 1 crore but is ` 10 crore Where the total income exceeds ` 1 crore but does not exceed ` 10 crore, surcharge is payable at the rate of 7% of income-tax computed in accordance with the provisions of sub-para (5)(i) of para 4.1 above or section 111A or section 112. Marginal relief Marginal relief is available in case of such companies i.e. the additional amount of income-tax payable (together with surcharge) on the excess of income over ` 1 crore should not be more than the amount of income exceeding ` 1crore. (b) In case of a domestic company, whose total income is > ` 10 crore Where the total income exceeds` 10 crore, surcharge is payable at the rateof 12% of income-tax computed in accordance with the provisions of sub-para (5)(i) of para 4.1 above or section 111A or section 112. Marginal relief Marginal relief is available in case of such companies i.e. the additional amount of income-tax payable (together with surcharge) on the excess of income over ` 10 crore should not be more than the amount of income exceeding ` 10 crore.

40 (iv) Foreign company (a) In case of a foreign company, whose total income > ` 1 crore but is ` 10 crore Where the total income exceeds ` 1 crore but does not exceed ` 10 crore, surcharge is payable at the rate of 2% of income-tax computed in accordance with the provisions of sub-para (5)(ii) of para 4.1 above or section 111A or section 112. Marginal relief Marginal relief is available in case of such companies i.e., the additional amount of income-tax payable (together with surcharge) on the excess of income over ` 1 crore should not be more than the amount of income exceeding ` 1 crore. (b) In case of a foreign company, whose total income is > ` 10 crore Where the total income exceeds ` 10 crore, surcharge is payable at the rate of 5% of income-tax computed in accordance with the provisions of subpara (5)(ii) of para 4.1 above or section 111A or section 112. Marginal relief Marginal relief is available in case of such companies i.e. the additional amount of income-tax payable (together with surcharge) on the excess of income over ` 10 crore should not be more than the amount of income exceeding ` 10 crore.

41

42 Rebate of up to ` 2,500 for resident individuals having total income of up to ` 3.5 lakh [Section 87A] In order to provide taxrelief to the individual taxpayers who are in the 5%taxslab, section 87A provides a rebate from the tax payable by an assessee, being an individual resident in India, whosetotal incomedoes not exceed` 3,50,000. (i) The rebate shall be equal to the amount of income-tax payable on the total income for any assessment year or an amount of ` 2,500, whichever isless. (ii) (iii) Consequently, any individual having total income up to ` 3,00,000 will not be required to pay any tax. Further, every individual having total income of above ` 3,00,000 but not exceeding ` 3,50,000 shall get a tax relief of ` 2,500. In effect, the rebatewould be the taxpayable or ` 2,500, whicheveris less. Further, the aggregate amount of rebate under section 87A shall not exceed the amount of income-tax (as computed before allowing such rebate) on the total income of the assesseewithwhichhe ischargeablefor anyassessment year. Education Cess and Secondary and Higher Education Cess on Income-tax The amount of income-tax as increased by the union surcharge, if applicable, should be further increased by an additional surcharge called the Education cess on income- tax, calculated at the rate of 2% of such income-tax and surcharge, if applicable. Education cess is leviable in the caseof all assessees i.e. individuals, HUF, AOP / BOI, firms, local authorities, co-operative societiesand companies. Further, Secondary and higher education cess on of income-tax plus surcharge, if applicable, is leviable to fulfill the commitment of the Government to provide and financesecondaryand highereducation.

43 Example Mr. Raghav aged 26 years, has a total income of ` 3,40,000, comprising his salary income and interest on bank fixed deposit. Compute his tax liability for A.Y SOLUTION Computation of tax liability of Mr. Raghav for A.Y Particulars ` Tax on total income of ` 3,40,000 Tax@5% of ` 90,000 (` 3,40,000 ` 2,50,000) 4,500 Less: Rebate u/s 87A (Since total income ` 3,50,000) 2,500 2,000 Add: Education cess@2% and SHEC@1% 60 Total tax liability 2,060

CS EXECUTIVE TAX LAWS & PRACTICE CA SACHIN GUPTA

CS EXECUTIVE TAX LAWS & PRACTICE CA SACHIN GUPTA INDEX S.NO. CHAPTER NAME PAGE NO. 1. BASIC CONCEPTS OF INCOME TAX 1 26 2. RESIDENTIAL STATUS 27 47 3. INCOME UNDER HEAD HOUSE PROPERTY 48 75 4. UNDER HEAD

CS EXECUTIVE TAX LAWS & PRACTICE CA SACHIN GUPTA INDEX S.NO. CHAPTER NAME PAGE NO. 1. BASIC CONCEPTS OF INCOME TAX 1 26 2. RESIDENTIAL STATUS 27 47 3. INCOME UNDER HEAD HOUSE PROPERTY 48 75 4. UNDER HEAD

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba 1. Power to impose income tax on agriculture income is with a) Central government b) State government c) Partly with central government and partly with state

IGP-CS Basic Concept M.Test 1 CA Vivek Gaba 1. Power to impose income tax on agriculture income is with a) Central government b) State government c) Partly with central government and partly with state

1.1 Overview of income-tax law in India

1 Basic Concepts 1.1 Overview of income-tax law in India Income-tax is a tax levied on the total income of the previous year of every person. A person includes an individual, Hindu Undivided Family (HUF),

1 Basic Concepts 1.1 Overview of income-tax law in India Income-tax is a tax levied on the total income of the previous year of every person. A person includes an individual, Hindu Undivided Family (HUF),

PREVIOUS YEAR AND ASSESSMENT YEAR

PREVIOUS YEAR AND ASSESSMENT YEAR In this topic we will learn 1) Meaning and relevance of previous year and assessment year 2) Cases when income of the previous year is taxed in the same year itself 3)

PREVIOUS YEAR AND ASSESSMENT YEAR In this topic we will learn 1) Meaning and relevance of previous year and assessment year 2) Cases when income of the previous year is taxed in the same year itself 3)

Circular The Schedule of dates for filing income-tax returns is given below:

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

Circular-2012 To, July 14, 2012 Dear Sir(s)/Madam, Sub: Income-tax, Wealth-tax, Service-tax and TDS returns for Assessment Year 2012-13 and payment of advance-tax for Assessment Year 2013-14 -------------------------------------------------------

SURENDER KR. SINGHAL & CO

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

PROPOSED TAX RATES FOR FINANCIAL YEAR 2016-17 A. Y. 2017-18 Income Tax Rates for Individuals, HUF Individuals, Hindu Undivided Families (HUF) and Artificial Jurisdictional Person: Net Income Range Income

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

R-2. Amendments at a glance

R-2 Amendments at a glance Effected by the Finance ACT, 2018 $ Tax rates 0.11 Tax rates for the assessment years 2018-19 and 2019-20 are given in Referencer 1. 0.11-1 Income-tax - The following are the

R-2 Amendments at a glance Effected by the Finance ACT, 2018 $ Tax rates 0.11 Tax rates for the assessment years 2018-19 and 2019-20 are given in Referencer 1. 0.11-1 Income-tax - The following are the

Income Ta Income Tax (A.Y (A.Y )

") 1 Income Tax (A.Y. 2011-12) 12) What is a Finance Bill? a) The Finance Bill incorporates all the financial proposals of the Government for the following year. b) It is ordinarily introduced in the Lok

1 Income Tax (A.Y. 2011-12) 12) What is a Finance Bill? a) The Finance Bill incorporates all the financial proposals of the Government for the following year. b) It is ordinarily introduced in the Lok

Unit 11: COMPUTATION OF TAX

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

Unit 11: COMPUTATION OF TAX HOW TO COMPUTE TAX PAYABLE Once the net taxable income is computed, the next step is to compute the final tax payable. The final tax payable is computed as follows: (1) Taxable

DEDUCTION OF TAX AT SOURCE

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

DEDUCTION OF TAX AT SOURCE SECTION 190 TO 206AA Section 190 Deduction at source and advance payment Section 191 Direct payment Section 192 Deduction of tax from salary income Section 193 Deduction of tax

Marking Scheme. Session TAXATION (782) CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income

CLASS XII. Total marks: 100 Theory: 60 Marks Practical: 40 Marks. 1 Deduction From Gross Total Income") Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

Marking Scheme Session 2018-19 TAXATION (782) CLASS XII Total marks: 100 Theory: 60 Marks Practical: 40 Marks UNITS UNIT NAME TOTAL 1 Deduction From Gross Total Income 2 Computation Of Ta x Liability Of

INTRODUCTION OF TAX PLANNING

INTRODUCTION OF TAX PLANNING UNIT 1 STRUCTURE OF THE CHAPTER 1.1 Introduction 1.2 Meaning of Planning 1.3 Meaning of Management 1.4 Meaning of Evasion 1.5 Meaning of Avoidance 1.6 Basics 1.7 Summary 1.8

INTRODUCTION OF TAX PLANNING UNIT 1 STRUCTURE OF THE CHAPTER 1.1 Introduction 1.2 Meaning of Planning 1.3 Meaning of Management 1.4 Meaning of Evasion 1.5 Meaning of Avoidance 1.6 Basics 1.7 Summary 1.8

Basics of Income Tax

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

CHAPTER : Basics of Income Tax CONCEPT 1: Short Title, Extent and Commencement [Section 1] a) Short title : Income Tax Act 1961 b) Extent : Whole of India c) Commencement : 1 st April, 1962 CONCEPT 2:

1. Basic concepts of Income Tax

Quick review of the chapter: Sections Particulars Sec. 2(7) Assessee Sec. 2(9) Assessment year Sec. 2(24) Income Sec. 2 (31) Person Sec. 2(34) & 3 "Previous Year" defined Sec. 80B(5) Gross total income

Quick review of the chapter: Sections Particulars Sec. 2(7) Assessee Sec. 2(9) Assessment year Sec. 2(24) Income Sec. 2 (31) Person Sec. 2(34) & 3 "Previous Year" defined Sec. 80B(5) Gross total income

1 Basics of Income Tax Law &

1 Basics of Income Tax Law & Residential Status This Chapter Includes : Basics of Taxation; Direct Taxes & Indirect Taxes; Sources and Authority of Taxes in India; Seventh Schedule of the Constitution;

1 Basics of Income Tax Law & Residential Status This Chapter Includes : Basics of Taxation; Direct Taxes & Indirect Taxes; Sources and Authority of Taxes in India; Seventh Schedule of the Constitution;

1 BASIC CONCEPTS AMENDMENTS BY THE FINANCE ACT, Join with us

1 BASIC CONCEPTS AMENDMENTS BY THE FINANCE ACT, 2015 RATES OF TAX Section 2 of the Finance Act, 2015 read with Part I of the First Schedule to the Finance Act, 2015, seeks to specify the rates at which

1 BASIC CONCEPTS AMENDMENTS BY THE FINANCE ACT, 2015 RATES OF TAX Section 2 of the Finance Act, 2015 read with Part I of the First Schedule to the Finance Act, 2015, seeks to specify the rates at which

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Income-tax and Death are the only two inevitable things in life In India, taxes were levied even in ancient times refer to Manu Smriti & Arthashastra Why to Pay Tax? It was only for the good of his subjects

Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]

![Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]](/thumbs/74/70016057.jpg "Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441]") Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441] Learning Objectives Income from Other Sources Deductions from Income from other Sources Conditions

Chapter 8 : Income from Other Sources (Section 56 to 59) Advance Direct Tax and Service Tax [Sub code : 441] Learning Objectives Income from Other Sources Deductions from Income from other Sources Conditions

Chapter 1 : Income Tax Concept and Computation of Income Tax

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

DIRECT TAX Every bit and piece of my work is dedicated to every sleepless night my mother has spent for me

Part A DIRECT TAX Every bit and piece of my work is dedicated to every sleepless night my mother has spent for me INDEX of Income Tax Amendments by FA, 2016 Chapter 1: Basic Concepts Particulars Rates

Part A DIRECT TAX Every bit and piece of my work is dedicated to every sleepless night my mother has spent for me INDEX of Income Tax Amendments by FA, 2016 Chapter 1: Basic Concepts Particulars Rates

Issues in Taxation of Income (Non-Corporate)

") Issues in Taxation of Income (Non-Corporate) By CA Mahavir Jain B.Com.; DISA; FCA Partner : JMT & Associates Email: jmtca301@gmail.com Issues in Taxation of Non-Corporate Income is a very vast subject.

Issues in Taxation of Income (Non-Corporate) By CA Mahavir Jain B.Com.; DISA; FCA Partner : JMT & Associates Email: jmtca301@gmail.com Issues in Taxation of Non-Corporate Income is a very vast subject.

Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state.

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

1. What is Tax What is Tax? Tax is imposition financial charge or other levy upon a taxpayer by a state or other the functional equivalent of the state. How many Types of Taxes are there and what are they?

Question 1. The Institute of Chartered Accountants of India

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Question 1 PAPER 5 : TAXATION Answer all questions. Working notes should form part of the answer. Wherever necessary suitable assumptions may be made by the candidates. Answer the following with reasons

Instructions for SUGAM Income Tax Return AY

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG

![MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG](/thumbs/73/68647623.jpg "MOCK TEST SOLUTION A.Y Total No. of Question 7] [Total No. of Printed Pages 20 Time Allowed 3 Hours Maximum Marks 100 MKG") MOCK TEST SOLUTION IPC (Intermediate) (Computation of Total Income And Tax Liability, Taxability of Gift, Advance Payment of Tax, Residential Status & Scope of Total Income, House Property, Agricultural

MOCK TEST SOLUTION IPC (Intermediate) (Computation of Total Income And Tax Liability, Taxability of Gift, Advance Payment of Tax, Residential Status & Scope of Total Income, House Property, Agricultural

Most Important Question of INCOME TAX

Most Important Question of INCOME TAX Residential Status 1. In 2 nd additional condition, assessee should have stayed in India for: a) more than 730 days during 7 immediately preceding previous year b)

Most Important Question of INCOME TAX Residential Status 1. In 2 nd additional condition, assessee should have stayed in India for: a) more than 730 days during 7 immediately preceding previous year b)

Assessment Year

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

Assessment Year 2016-2017 Income Income Income Income Income From Salaries from Capital Gains from Business and Profession from House Property from Other Sources Individual/HUF Firm Company Trust AOP/BOI/Co-op

TAX RECKONER

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

TAX RECKONER 2018-19 The rates are applicable for the Financial Year 2018-19 (AY 2019-20) and subject to enactment of the Finance Bill, 2018 Note: The tax rate card will be re-visited post enactment of

Foreign Collaboration

CHAPTER 17 Foreign Collaboration Some Key Points (a) The tax liability of a foreign collaborator and the Indian counter part is dependent on their residential status and the applicable provisions of DTAA,

CHAPTER 17 Foreign Collaboration Some Key Points (a) The tax liability of a foreign collaborator and the Indian counter part is dependent on their residential status and the applicable provisions of DTAA,

A BUDGET FOR A Y From the desk of - B.L. Tulsian Advocate. R. Tulsian & Co LLP Chartered Accountants.

A BUDGET A N A L Y S I S FOR A Y 2020-21 From the desk of - B.L. Tulsian Advocate R. Tulsian & Co LLP Chartered Accountants www.rtulsian.com Page2 Contents Amendment of Section 16... 3 Amendment to Section

A BUDGET A N A L Y S I S FOR A Y 2020-21 From the desk of - B.L. Tulsian Advocate R. Tulsian & Co LLP Chartered Accountants www.rtulsian.com Page2 Contents Amendment of Section 16... 3 Amendment to Section

FINANCE (NO.2) ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT AMENDMENTS AT A GLANCE

ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT AMENDMENTS AT A GLANCE") FINANCE (NO.2) ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT Section/Schedule CIRCULAR NO.1/2015 [F.NO.142/13/2014 TPL], DATED 21 1 2015 AMENDMENTS AT A GLANCE Finance (No.2) Act, 2014 First

FINANCE (NO.2) ACT, 2014 EXPLANATORY NOTES TO THE PROVISIONS OF SAID ACT Section/Schedule CIRCULAR NO.1/2015 [F.NO.142/13/2014 TPL], DATED 21 1 2015 AMENDMENTS AT A GLANCE Finance (No.2) Act, 2014 First

Income Tax Changes made in Income Tax Provisions in the Union Budget which would affect Salaried Class

Income Tax 2013-14 Changes made in Income Tax Provisions in the Union Budget 2013-14 which would affect Salaried Class A. RATES OF INCOME-TAX I. Rates of income-tax in respect of income liable to tax for

Income Tax 2013-14 Changes made in Income Tax Provisions in the Union Budget 2013-14 which would affect Salaried Class A. RATES OF INCOME-TAX I. Rates of income-tax in respect of income liable to tax for

J.M.PATEL COLLEGE OF COMMERCE 1

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 Taxation 2 3 5 4 6 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 Taxation 2 3 5 4 6 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The

UNDERSTANDING-- TAXATION SYSTEM

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 3 5 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The outer effects affecting

UNDERSTANDING-- TAXATION SYSTEM TO UNDERSTAND TAXATION SYSTEM IN TOTALITY ONE HAS TO UNDERSTAND ALL OF THE FOLLOWING The Core 1 3 5 8 7 1. Act 2. Rules 3. Notifications 4. Circulars The outer effects affecting

Jagannath Institute of Management Sciences Lajpat Nagar. BBA Sem V Income Tax

Jagannath Institute of Management Sciences Lajpat Nagar BBA Sem V Income Tax UNIT- 1 Introduction and Important Definitions Introduction Basic concepts of Income Tax Act Income [Section 2(24)] Capital

Jagannath Institute of Management Sciences Lajpat Nagar BBA Sem V Income Tax UNIT- 1 Introduction and Important Definitions Introduction Basic concepts of Income Tax Act Income [Section 2(24)] Capital

EXPLANATORY NOTES TO THE PROVISIONS OF THE FINANCE(No.2) ACT, 2014

ACT, 2014") CIRCULAR NO. 01/2015 F. No. 142/13/2014-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) ******* Dated, the 21st January, 2015 EXPLANATORY NOTES TO THE

CIRCULAR NO. 01/2015 F. No. 142/13/2014-TPL Government of India Ministry of Finance Department of Revenue (Central Board of Direct Taxes) ******* Dated, the 21st January, 2015 EXPLANATORY NOTES TO THE

As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017.

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

Budget 2017-18 Highlights for Non-Residents As proposed in The Finance Bill, 2017 introduced by Finance Minister of India on 1 st February, 2017. The Indian Budget has provisions affecting the taxability

FINANCE BILL He has proposed to revise the tax slabs upwards as under:

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

FINANCE BILL - 2010 The 2 nd budget of the 2 nd UPA Government for the year 2010 2011 was presented by the finance minister on 26 th February 2010. The finance minister has attempted to balance his direct

Rates of Taxes. Rates for deduction of Income

CA Mohan S. Phadke Rates of Taxes I. Rates of Income Tax in respect of income liable to tax for the assessment year 2013-14 a) In respect of income of all categories of assessees liable to tax for the

CA Mohan S. Phadke Rates of Taxes I. Rates of Income Tax in respect of income liable to tax for the assessment year 2013-14 a) In respect of income of all categories of assessees liable to tax for the

Instructions for filling ITR-4 SUGAM A.Y

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

TAX RATES FOR AY ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS

TAX RATES FOR AY 2013-14 Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

TAX RATES FOR AY 2013-14 Compiled by ANUJ PATCHIGAR & ASSOCIATES CHARTERED ACCOUNTANTS DISCLAIMER: Anuj Patchigar & Associates has taken due care and caution in compilation and presenting factually correct

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

CHAPTER 8: RECOVERY OF TAX TAX DEDUCTED AT SOURCE SECTIONS RATE PARTICULARS 192: Deduction of Tax on Slab Every Employer has a liability to deduct TDS on salary on monthly basis on tax from salary Rate

Notes on clauses.

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

52 Notes on clauses Clause 2, read with the First Schedule to the Bill, seeks to specify the rates at which income-tax is to be levied on income chargeable to tax for the assessment year 2009-2010 Further,

Major direct tax proposals in Finance Bill, 2017

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

Major direct tax proposals in Finance Bill, 2017 Member firm Individual, HUF, BOI, AOP, AJP Tax Rates There is no change in the basic exemption limit for individuals/hufs. It is proposed to reduce the

SyNoPSIS of the FINaNce BILL, 2017

SyNoPSIS of the FINaNce BILL, 2017 By PaRaS KocHaR, advocate The following changes in the finance bill has been proposed by the Hon ble Finance Minister to the Income Tax Act, 1961 from 01-04-2017 TAX

SyNoPSIS of the FINaNce BILL, 2017 By PaRaS KocHaR, advocate The following changes in the finance bill has been proposed by the Hon ble Finance Minister to the Income Tax Act, 1961 from 01-04-2017 TAX

UNIT 1 : INCOME TAX LAW : AN INTRODUCTION

1 Basic Concepts Learning Objectives UNIT 1 : INCOME TAX LAW : AN INTRODUCTION After studying this unit, you would be able to - understand the meaning of tax recognize the types of taxes comprehend the

1 Basic Concepts Learning Objectives UNIT 1 : INCOME TAX LAW : AN INTRODUCTION After studying this unit, you would be able to - understand the meaning of tax recognize the types of taxes comprehend the

Budget 2017 Synopsis Part II Analysis of Rupiya

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

Budget 2017 Synopsis Part II Analysis of Rupiya Facts & Findings: Out of 125 crore Indians only 15% ie 19 crore pay income tax % of Taxpayers (Out of 19 Crore) % Contribution To Tax Revenue 01% 26% 1%

INCOME-TAX AND BASED ON FINANCE ACT, FINANCE ACT, 2007 WITH NOTES 49 I.T. NOTES 69 I.T. NOTES 97 I.T. NOTES I.T. NOTES 139 I.T.

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

EHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA S ITRR VG.G.MEHTA S ITRR V.G.MEHTA S ITRR V.G.MEHTA

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

FB.COM/SUPERWHIZZ4U Income Tax Amendment for the Assessment Year 2014-15 - SIPOY SATISH Highlights of Change in Direct Taxes in the Union Budget 2013 1. Rate of Income Tax for Individual a) Slab Rate Assessment

8 Income from other Sources

8 Income from other Sources 8.1 Introduction Any income, profits or gains includible in the total income of an assessee, which cannot be included under any of the preceding heads of income, is chargeable

8 Income from other Sources 8.1 Introduction Any income, profits or gains includible in the total income of an assessee, which cannot be included under any of the preceding heads of income, is chargeable

Appeal, Set comm., DRP Etc Mock Test IGP-CS CA Vivek Gaba

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

1. Taking full advantage of loopholes of law so as to attract least incidence of tax is known as a) Tax planning b) Tax evasion c) Tax avoidance d) Tax management 2. Which is the relevant Form No. for

Chapter 8 Income under the Head "Income from Other Sources"

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

Chapter 8 Income under the Head "Income from Other Sources" 1. Basis of Charge Section 56(1) Income of every kind which is not exempt shall be chargeable to income-tax under the head "Income from Other

A23 A24 A25 A26 B1 B2 B3 B5 In response to notice under section In response to notice under section 153A/ 153C 7 In pursuance of an order of the

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Total turnover/ Gross receipts 30% 30% of FY > Rs 50 Cr No change in rate of Surcharge

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

1. Income Tax Rates: Category of Income New rate of tax Old rate Taxpayer for FY 2017-18 of tax Individuals/ Upto Rs 2.5 L Nil Nil HUF/ BOI/ Rs 2.5 to 5 L 5% 10% AOP/ Rs 5 to 10 L 20% 20% Artificial Above

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year 2013-2014 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Elective Course in Commerce ECO-11 Elements of Income Tax APPENDIX 2014 Assessment Year 2013-2014 School of Management Studies Indira Gandhi National Open University New Delhi 110068 Dear Student, As you

Key Changes In ITR Forms For Assessment Year

Key Changes In ITR For Assessment Year 2017-18 Background The Central Board of Direct Taxes (CBDT) has notified revised Income-tax Returns (ITR) forms for Assessment Year (AY) 2017-18 on 31 st March 2017.

Key Changes In ITR For Assessment Year 2017-18 Background The Central Board of Direct Taxes (CBDT) has notified revised Income-tax Returns (ITR) forms for Assessment Year (AY) 2017-18 on 31 st March 2017.

INCOME FROM OTHER SOURCES. What are the sections which deals with income from Other Sources - Sec. 56 to 59

INCOME FROM OTHER SOURCES What are the sections which deals with income from Other Sources - Sec. 56 to 59 Sec.56(1) : Charging Section This is the last head of income and it is also known as residuary

INCOME FROM OTHER SOURCES What are the sections which deals with income from Other Sources - Sec. 56 to 59 Sec.56(1) : Charging Section This is the last head of income and it is also known as residuary

1 Introduction and Important Definitions

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter Nil j Nil 1 Introduction and Important

Star Rating On the basis of Maximum marks from a chapter On the basis of Questions included every year from a chapter On the basis of Compulsory questions from a chapter Nil j Nil 1 Introduction and Important

Income from Other Sources

Income from Other Sources SECTION 56: INCOME FROM OTHER SOURCES CHARGING SECTION Income from other sources is a residuary head of income i.e. income not chargeable under any other head, and which is not

Income from Other Sources SECTION 56: INCOME FROM OTHER SOURCES CHARGING SECTION Income from other sources is a residuary head of income i.e. income not chargeable under any other head, and which is not

Suggested Answer_Syl12_June 2016_Paper_7 INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper-7: DIRECT TAXATION Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full

INTERMEDIATE EXAMINATION (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS JUNE 2016 Paper-7: DIRECT TAXATION Time Allowed: 3 Hours Full Marks: 100 The figures in the margin on the right side indicate full

UCM 54 INCOME TAX LAW & PRACTICE - I Unit-1 Introduction to Income Tax Act 1961 Type:20% Theory 80% Problem Question & Answers

UCM 54 INCOME TAX LAW & PRACTICE - I Unit-1 Introduction to Income Tax Act 1961 Type:20% Theory 80% Problem Question & Answers PART A 1. What is assessment year? (April 2014, 2013, 2012) ASSESSMENT YEAR

UCM 54 INCOME TAX LAW & PRACTICE - I Unit-1 Introduction to Income Tax Act 1961 Type:20% Theory 80% Problem Question & Answers PART A 1. What is assessment year? (April 2014, 2013, 2012) ASSESSMENT YEAR

Wealth tax notes. Prepared by. Akhil mittal b.com(h), shri ram college of commerce

, shri ram college of commerce") Wealth tax notes Prepared by Akhil mittal b.com(h), shri ram college of commerce 1 C H A P T E R 1 SECTION 3 : CHARGE OF WEALTH TAX Wealth tax shall be charged for every assessment year In respect of the

Wealth tax notes Prepared by Akhil mittal b.com(h), shri ram college of commerce 1 C H A P T E R 1 SECTION 3 : CHARGE OF WEALTH TAX Wealth tax shall be charged for every assessment year In respect of the

INCOMES WHICH DO NOT FORM PART OF TOTAL INCOME

3 INCOMES WHICH DO NOT FORM PART OF TOTAL INCOME Question 1 Choose the correct answer with reference to the provisions of the Income-tax Act, 1961. (i) For an employee in receipt of hostel expenditure

3 INCOMES WHICH DO NOT FORM PART OF TOTAL INCOME Question 1 Choose the correct answer with reference to the provisions of the Income-tax Act, 1961. (i) For an employee in receipt of hostel expenditure

For J B Nagar Study Circle Meeting

For J B Nagar Study Circle Meeting Nature of income Individual and HUF ITR 1* (Sahaj) ITR 2 ITR 3 ITR 4 Income from salary/pension (for ordinarily resident person) Income from salary/pension (for not ordinarily

For J B Nagar Study Circle Meeting Nature of income Individual and HUF ITR 1* (Sahaj) ITR 2 ITR 3 ITR 4 Income from salary/pension (for ordinarily resident person) Income from salary/pension (for not ordinarily

Revisionary Test Paper_Intermediate_Syllabus 2008_Jun2014

Paper 7- Applied Direct Taxation Question 1 Choose the correct answer from the given options in respect of the following: (a) If an assessee fails to furnish return of income under Section 139(1) of the

Paper 7- Applied Direct Taxation Question 1 Choose the correct answer from the given options in respect of the following: (a) If an assessee fails to furnish return of income under Section 139(1) of the

Instructions for filling ITR-1 SAHAJ A.Y

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

UNIT- 1. Computation of Total/Taxable Income And Tax liability of an Individual

UNIT- 1 Computation of Total/Taxable Income And Tax liability of an Individual Steps in computation of total income & tax liability Income-tax is a tax levied on the total income of the previous year of

UNIT- 1 Computation of Total/Taxable Income And Tax liability of an Individual Steps in computation of total income & tax liability Income-tax is a tax levied on the total income of the previous year of

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS Gautam Nayak Chartered Accountant BCAS Seminar 29 th August 2009 Rates of Taxes Substantial increase

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS Gautam Nayak Chartered Accountant BCAS Seminar 29 th August 2009 Rates of Taxes Substantial increase

Basic Concepts of Tax on Income

Basic Concepts of Tax on Income (Taxpayer s Facilitation Guide) September 2011 Revenue Division Federal Board of Revenue Government of Pakistan helpline@fbr.gov.pk 0800-00-227, 051-111-227-227 www.fbr.gov.pk

Basic Concepts of Tax on Income (Taxpayer s Facilitation Guide) September 2011 Revenue Division Federal Board of Revenue Government of Pakistan helpline@fbr.gov.pk 0800-00-227, 051-111-227-227 www.fbr.gov.pk

AMENDMENTS MADE BY FINANCE ACT, RELEVANT FOR MAY 2015/NOV 2015 EXAM

AMENDMENTS MADE BY FINANCE ACT, 2014- RELEVANT FOR MAY 2015/NOV 2015 EXAM FEW AMENDMENTS RELATING TO CAPITAL GAINS 1. SECTION 2(14)-EFFECTIVE FROM A.Y. 2015-16 Income arising from transfer of security

AMENDMENTS MADE BY FINANCE ACT, 2014- RELEVANT FOR MAY 2015/NOV 2015 EXAM FEW AMENDMENTS RELATING TO CAPITAL GAINS 1. SECTION 2(14)-EFFECTIVE FROM A.Y. 2015-16 Income arising from transfer of security

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Paper 7- Direct Taxation

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

Paper 7- Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7- Direct Taxation Full Marks: 100 Time Allowed: 3 hours

As proposed in The Finance Bill, 2016 introduced by Finance Minister of India on 29th February, 2016.

1 Budget 2016-2017 Highlights for Non-Residents As proposed in The Finance Bill, 2016 introduced by Finance Minister of India on 29th February, 2016. The Indian Budget presented by the Finance Minister

1 Budget 2016-2017 Highlights for Non-Residents As proposed in The Finance Bill, 2016 introduced by Finance Minister of India on 29th February, 2016. The Indian Budget presented by the Finance Minister

12 months commencing 1 st April of every day

CHAPTER 1: BASIC CONCEPTS Sr Particulars Explanation 1 Component of Income Tax law 1) Income tax Act, 1961, 2) Finance Act, 3) Income Tax Rules, 1961, 4) Circulars / Notification from CBDT, 5) Supreme

CHAPTER 1: BASIC CONCEPTS Sr Particulars Explanation 1 Component of Income Tax law 1) Income tax Act, 1961, 2) Finance Act, 3) Income Tax Rules, 1961, 4) Circulars / Notification from CBDT, 5) Supreme

Assessment of Various Entities (Revision)

") CA Final Direct Tax 1 Assessment of Various Entities (Revision) Assessment of Companies: Tax on income from life insurance business: (Section 115B) - Profits and gains derived from the business of life

CA Final Direct Tax 1 Assessment of Various Entities (Revision) Assessment of Companies: Tax on income from life insurance business: (Section 115B) - Profits and gains derived from the business of life

Union Budget 2014 Analysis of Major Direct tax proposals

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

RATES OF INCOME TAX Union Budget 2014 Analysis of Major Direct tax proposals Basic exemption limit has been increased from Rs 2 lacs to Rs 2.50 lacs for resident individuals or HUF. Income slabs Income

Web:

PRESENTED ON 1st FEB 2017 HIGHLIGHTS 1 A Rates of Income-tax Rates of income-tax in respect of income liable to tax for the assessment year 2017-18. Rates for deduction of income-tax at source during the

PRESENTED ON 1st FEB 2017 HIGHLIGHTS 1 A Rates of Income-tax Rates of income-tax in respect of income liable to tax for the assessment year 2017-18. Rates for deduction of income-tax at source during the

ARTICLE. On Finance Bill (Budget) Proposals 2013 Income Tax Act, 1961 By CA. SATISH AGARWAL

Proposals 2013 Income Tax Act, 1961 By CA. SATISH AGARWAL") ARTICLE On Finance Bill (Budget) Proposals 0 Income Tax Act, 96 By CA. SATISH AGARWAL Mobile : +99808957 Phone : +95769 Office : 9/4, East Patel Nagar, (Near Jaypee Sidharthe Hotel) New Delhi - 0008 :

ARTICLE On Finance Bill (Budget) Proposals 0 Income Tax Act, 96 By CA. SATISH AGARWAL Mobile : +99808957 Phone : +95769 Office : 9/4, East Patel Nagar, (Near Jaypee Sidharthe Hotel) New Delhi - 0008 :

thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and

![thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and](/thumbs/74/69854896.jpg "thousand rupees of the total income but without being liable to tax], only for the purpose of charging income-tax in respect of the total income; and") ACT FINANCE ACT *Finance Act, 2011 [8 OF 2011] An Act to give effect to the financial proposals of the Central Government for the financial year 2011-2012. BE it enacted by Parliament in the Sixty-second

ACT FINANCE ACT *Finance Act, 2011 [8 OF 2011] An Act to give effect to the financial proposals of the Central Government for the financial year 2011-2012. BE it enacted by Parliament in the Sixty-second

Incomes Which Do Not Form Part of Total Income

3 Incomes Which Do Not Form Part of Total Income Section Key Points Particulars 10(1) Agricultural income is exempt under section 10(1). However, agricultural income has to be aggregated with non-agricultural

3 Incomes Which Do Not Form Part of Total Income Section Key Points Particulars 10(1) Agricultural income is exempt under section 10(1). However, agricultural income has to be aggregated with non-agricultural

BVZ6A,BPG6C Income tax law & practice-ii BVZ6A,BPG6C INCOME TAX LAW & PRACTICE-II. Unit : I - V

BVZ6A,BPG6C Income tax law & practice-ii BVZ6A,BPG6C INCOME TAX LAW & PRACTICE-II Unit : I - V TM BVZ6A,BPG6C Income tax law & practice-ii 02 I UNIT-I SYLLABUS Capital assets Meaning and kind Procedure

BVZ6A,BPG6C Income tax law & practice-ii BVZ6A,BPG6C INCOME TAX LAW & PRACTICE-II Unit : I - V TM BVZ6A,BPG6C Income tax law & practice-ii 02 I UNIT-I SYLLABUS Capital assets Meaning and kind Procedure

Who can use this form Who cannot use this form Mode of filing. Individuals whose total income includes:

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

INCOME TAX: Central Board of Direct Taxes (CBDT) has notified the rules for filing incometax returns for the Assessment Year (AY) 2013-14: Income Tax Service Tax Central Excise Customs FEMA ITR Form Who

Tax Laws 263 NOTE : PART A 263/1