Completing IRS Form 1040NR-EZ for 2015

|

|

|

- Byron Rice

- 6 years ago

- Views:

Transcription

1 Completing IRS Form 1040NR-EZ for 2015 Note: If you had income other than wages and taxable scholarship (e.g., interest, dividends, capital gains), you must complete Form 1040NR, rather than Form 1040NR-EZ. In the following, references to comparable lines of Form 1040NR are given in parentheses. Form 1040NR-EZ, Page 1 Enter your name and identifying number (social security number or Individual Tax Identification Number [ITIN]) at the top of the form. List your Amherst College address as the Present home address and City, town or post office, state, and ZIP code on the second and third lines. Country on the fourth line may be left blank or U.S.A. may be entered. Boxes 1 and 2 (Form 104NR, Boxes 1-6, as appropriate). Check your filing status as single or married, as appropriate. Line 3 (Form 104NR, Line 8). Enter the total of your wages, salaries, tips, etc. (if any) reported in Box 1 of your W-2 form(s) for (Form 1040NR, Lines 9a, 9b, 10a, and 10b. Enter appropriate interest and dividend information.) Line 4 (Form 1040NR, Line 11). If you had a refund in 2014 from state taxes (not federal taxes) withheld in a previous year, enter the amount. Line 5 (Form 1040NR, Line 12). If there is a relevant tax treaty between your home country and the United States (see list on page 5), skip to Line 6. (See Form 1040NR, Line 22). Otherwise, determine the amount of taxable scholarship from Form 1042-S for Enter the amount from Box 2 ( gross income ). A copy of your Form 1042-S will suffice for the explanation to be attached. Line 6 (Form 104NR, Line 22). If there is no relevant tax treaty between your home country and the United States (your country is not listed on page 5), leave this line blank, and go on to line 7. If there is a relevant treaty, enter the amount from Box 2 of Form 1042-S, but not more than the maximum amount in the tax treaty listing. If the amount from Form 1042-S is greater than the maximum amount, enter the maximum amount in line 6 and any excess amount in line 5. Line 7. Enter the sum of lines 3, 4, and 5. Line 10 (Form 1040NR, Line 36). Repeat line 7. Line 11 (Form 1040NR. Line 38). If you had state and/or local income taxes withheld in 2015, enter the sum of the amounts from Form W-2, Boxes 17 and 19. If you are a resident of India, note that a special tax-treaty provision allows students to subtract the standard deduction that usually applies to U.S. tax residents. Enter the standard deduction amount ($6,300 for a single person for 2015). Line 12 (Form 1040NR, Line 39). Subtract line 11 from line 10. If the result is negative, enter zero. 1

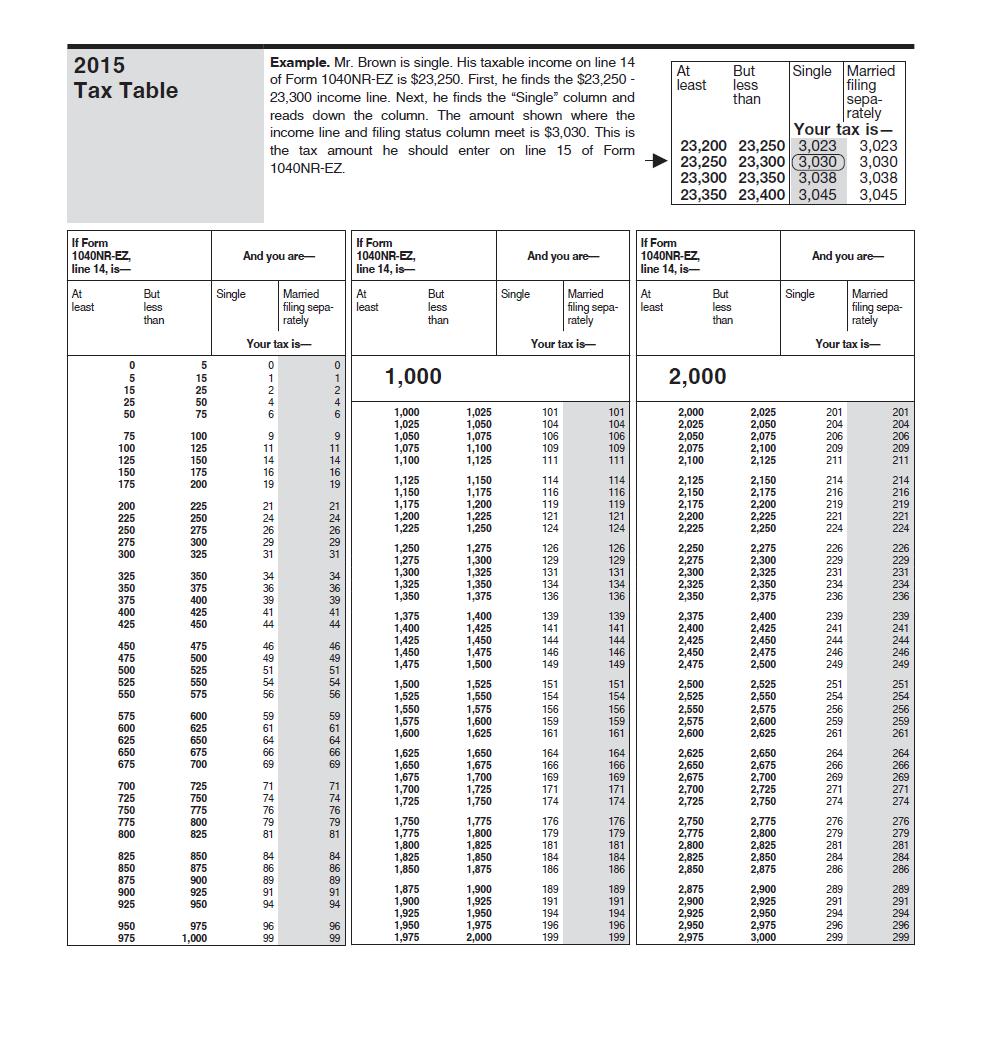

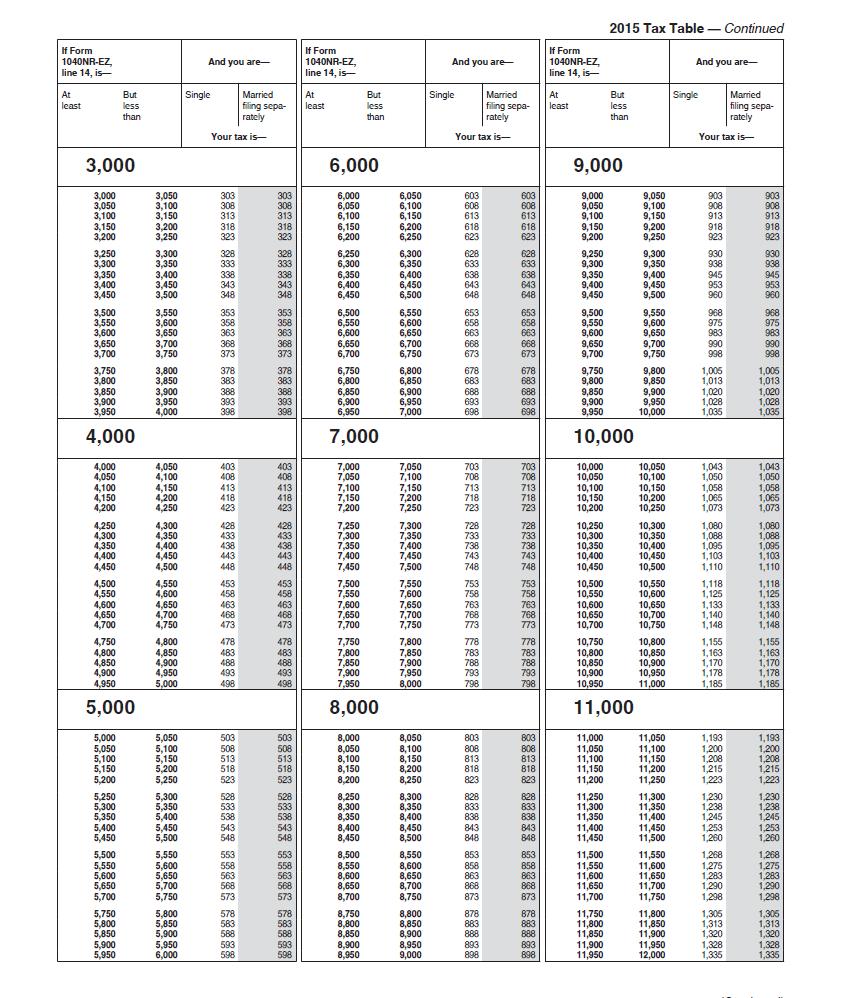

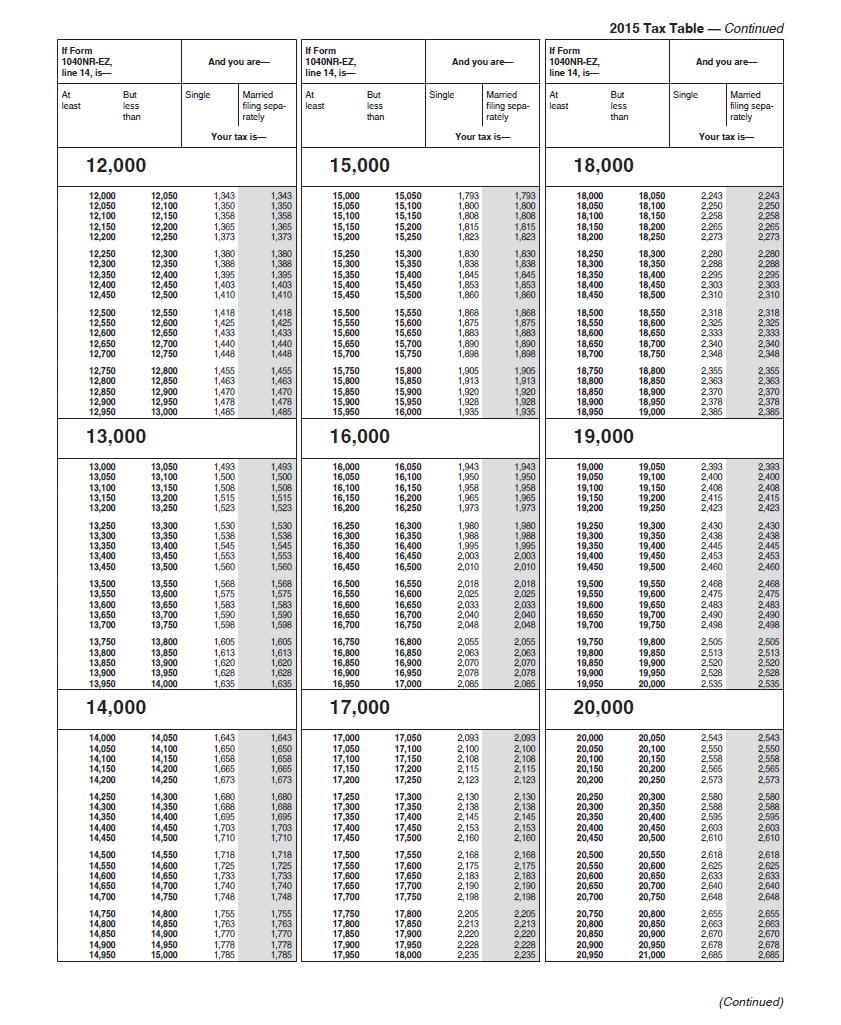

2 Line 13 (Form 104NR, Line 40). Enter $4,000 (the personal exemption for 2015). Line 14 (Form 1040NR, Line 41). Subtract line 13 from line 12. If the result is negative, enter zero. Line 15 (Form 1040NR, Line 42). Enter your income tax from the attached 2015 tax table. Line 17 (Form 1040NR, Line 61). Repeat line 15. Lines 18a and 18b (Form 1040NR, Lines 62a through 62d). Enter the sum of any amounts of U.S. federal tax withheld from wages (Form W-2, Box 2) in line 18a and from taxable scholarship (Form 1042-S, Box 7) in line 18b. Line 21 (Form 1040NR, Line 71). Enter the sum of lines 18a through 20. Line 22 (Form 1040NR, Line 72). If line 21 is greater than line 17, enter the difference of the entries for lines 17 and 21. Your tax payment (withholding) exceeds the tax on your income; you are due a refund. Proceed to lines 23a-23d. Lines 23a-23e (Form 1040NR, Lines 73a-73e). If you are due a refund, you may enter the requested information in items 23b, c, and d in order to have your refund deposited directly into your checking or savings account. If you have a refund due and do not enter this information, a paper check will be sent to the present home address you entered at the top of the form. If you want a paper check sent to an address outside of the United States, enter the address in item 23e. Line 25 (Form 1040NR, Line 75). If line 17 is more than line 21, enter the difference of the entries for lines 17 and 21. Your tax payment (withholding) is less than the tax on your income; you owe additional taxes. Send a check for this amount to the Internal Revenue Service with your tax return. Make the check payable to United States Treasury. Sign Here. Sign and date your form, and enter your occupation as Student. 2

3 Form 1040NR-EZ, Page 2 (Form 1040NR, Page 5), Schedule OI Other Information Lines A through D. Respond to the questions. Line E. Enter your visa type (typically F-1 ). Line F. Respond to the question(s). Line G. List the dates you entered and left the United States in 2015, including dates for the beginning or the ending of the year if you were present in the U.S. on either date. Lines H and I. Respond to the questions. Line J 1. A list is attached that records the countries with which the United States has a treaty that pertains to scholarship aid. If you are exempt from taxation of your scholarship because of a tax treaty between the United States and your home country, complete the information requested; otherwise, enter N/A. The number entered in column (c) should equal the number of months that you claimed exemption for scholarship aid in 2015 and previous years. The amount entered in column (d) should be the same amount you entered in line 6 on the front of the form. Enter the total of entries in column (d) on line J 1 (e). For most students there is only one set of information in columns (a) through (d). Line J 2. Check the appropriate box to indicate whether any treaty-exempt income is taxable in your home country. (Form 1040NR, Schedule OI, Lines K and L. Respond to the questions.) Form 8843 Part I Part III Enter your name and social security number (or Individual Tax Identification Number [ITIN]) at the top of the form, and complete only Parts I and III. Complete the address information only if you are filing Form 8843 by itself because you have no income to report on Form 1040NR-EZ. Lines 1a and b. Enter your visa type (the same information as in Form 1040NR-EZ, Schedule OI, line E) and the date you first entered the United States under this visa. Line 1b. Enter Student visa issued [date], including the date your visa was issued. Lines 2 and 3a-3b. Respond to the questions. Line 4a. Respond to the questions. The entries should correspond with the entries in Form 1040NR-EZ, Schedule OI, line H. Note that the dates are in reverse sequence from Form 1040NR-EZ. Line 4b. Enter the same number as your entry for 2015 in line 4a. Line 9. Enter Amherst College, P.O. Box 5000, Amherst, MA 01002, (413) Line 10. Enter Catherine Epstein, Dean of the Faculty, Amherst College, P.O. Box 5000, Amherst, MA 01002, (413)

4 Line 11. Enter your visa type for any year in which you held an F, J, M, or Q visa. Enter N/A for any year that does not apply to you. Line 12. Respond to the question. If your answer is Yes, attach a brief explanation with your tax return. On any attachment, include your name, address, social security number, and the form and line to which your explanation pertains. Line 13. Respond to the question. Line 14. If your answer to line 13 is Yes, add a brief note of explanation. Filing Your Return Send your Signed and completed Form 1040NR-EZ (or 1040NR) Completed Form 8843 The federal copy of your Form(s) W-2 (attached to the front of Form1040NR-EZ or 1040NR) The federal copy of your Form 1042-S (attached to the front of Form 1040NR-EZ or 1040NR) If additional taxes are due, a check for the amount due payable to United States Treasury To (if you are not enclosing a payment): Department of the Treasury Internal Revenue Service Center Austin, TX U.S.A. If enclosing a payment, mail your return to: Internal Revenue Service P.O. Box 1303 Charlotte, NC Make a copy of your return for your files and, if you are applying for renewal of financial aid, a copy for the Office of Financial Aid. 4

5 TAX TREATY EXEMPTION OF SCHOLARSHIP AID Country Category Maximum Presence in U.S. Payer Maximum Amount Bangladesh Scholarship 2 years U.S. or foreign No limit 21(2) China Scholarship No limit U.S. or foreign No limit 20(b) Commonwealth of Independent States (with no separate treaty) Scholarship 5 years U.S. or foreign $9, VI(1) Cyprus Scholarship Generally 5 U.S. or foreign No limit 21(1) years Czech Republic Scholarship 5 years U.S. or foreign No limit 21(1) Egypt Scholarship Generally 5 U.S. or foreign No limit 23(1) years Estonia Scholarship 5 years U.S. or foreign No limit 20(1) France Scholarship 5 years U.S. or foreign No limit 21(1) Germany Scholarship No limit U.S. or foreign No limit 20(3) Iceland Scholarship 5 years U.S. or foreign No limit 19(1) Indonesia Scholarship 5 years U.S. or foreign No limit 19(1) Israel Scholarship 5 years U.S. or foreign No limit 24(1) Kazakhstan Scholarship 5 years U.S. or foreign No limit 19 Korea, South Scholarship 5 years U.S. or foreign No limit 21(1) Latvia Scholarship 5 years U.S. or foreign No limit 20(1) Lithuania Scholarship 5 years U.S. or foreign No limit 20(1) Morocco Scholarship 5 years U.S. or foreign No limit 18 Netherlands Scholarship 3 years U.S. or foreign No limit 22(2) Norway Scholarship 5 years U.S. or foreign No limit 16(1) Pakistan Scholarship No limit Pakistani nonprofit No limit XIII(1) organization Philippines Scholarship 5 years U.S. or foreign No limit 22(1) Poland Scholarship 5 years U.S. or foreign No limit 18(1) Portugal Scholarship 5 years U.S. or foreign No limit 23(1) Romania Scholarship 5 years U.S. or foreign No limit 20(1) Russia Scholarship 5 years U.S. or foreign No limit 18 Slovak Republic Scholarship 5 years U.S. or foreign No limit 21(1) Slovenia Scholarship 5 years U.S. or foreign No limit 20(1) Spain Scholarship 5 years U.S. or foreign No limit 22(1) Thailand Scholarship 5 years U.S. or foreign No limit 22(1) Trinidad and Scholarship 5 years U.S. or foreign No limit 19(1) Tobago Tunisia Scholarship 5 years U.S. or foreign No limit 20 Ukraine Scholarship 5 years U.S. or foreign No limit 20 Venezuela Scholarship 5 years U.S. or foreign No limit 21(1) Treaty Article 5

6 6

7 7

8 8

AMHERST COLLEGE Office of Financial Aid

AMHERST COLLEGE Office of Financial Aid B-5 Converse Hall P.O. Box 5000 Telephone (413) 542-2296 Amherst, Massachusetts 01002-5000 Facsimile (413) 542-2628 M E M O R A N D U M DATE: February 2009 TO: International

AMHERST COLLEGE Office of Financial Aid B-5 Converse Hall P.O. Box 5000 Telephone (413) 542-2296 Amherst, Massachusetts 01002-5000 Facsimile (413) 542-2628 M E M O R A N D U M DATE: February 2009 TO: International

2016 Publication 4011

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

016 Publication 4011 Foreign Student and Scholar Volunteer Resource Guide For Use in Preparing Tax Year 016 Returns»» Volunteer Income Tax Assistance (VITA)»» Tax Counseling for the Elderly (TCE) For the

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

This Chief Counsel Advice responds to your request for assistance. This advice may not be used or cited as precedent.

Office of Chief Counsel Internal Revenue Service memorandum CC:INTL:B06:APShelburne POSTU-105946-08 UILC: 864.01-01, 864.01-03, 1441.00-00, 1441.02-00, 1441.02-02 date: March 22, 2011 to: Stephen A. Whitlock

Office of Chief Counsel Internal Revenue Service memorandum CC:INTL:B06:APShelburne POSTU-105946-08 UILC: 864.01-01, 864.01-03, 1441.00-00, 1441.02-00, 1441.02-02 date: March 22, 2011 to: Stephen A. Whitlock

Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation

Arm s Length Standard Global views within reach. Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation Transfer pricing continues to be the top enforcement

Arm s Length Standard Global views within reach. Deadlines to preserve taxpayer rights to request competent authority assistance to relieve double taxation Transfer pricing continues to be the top enforcement

NOTE: In August 2011, you will receive a pro-rated stipend amount of $2,101.45, as your August start date is 8/4.

August 31, 2011 Dear Combined Degree Students, There is some confusion regarding the years of the program in which you have no taxes withheld from your stipend check, and need to file estimated taxes and

August 31, 2011 Dear Combined Degree Students, There is some confusion regarding the years of the program in which you have no taxes withheld from your stipend check, and need to file estimated taxes and

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

TAX POLICY AND PROCEDURE GUIDE FOR INCOME PAYMENTS TO ALIEN INDIVIDUALS Revised as of November 2007 University of Alabama at Birmingham Revision Date: November 2007 PREFACE The Tax Policy and Procedure

Withholding Tax Handbook BELGIUM. Version 1.2 Last Updated: June 20, New York Hong Kong London Madrid Milan Sydney

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

In year 1 you may be supported in one of the following ways:

October 1 st 2015 Dear BGS Students, There is some confusion regarding the years of the program in which you get no taxes withheld from your stipend check, and need to file estimated taxes and the years

October 1 st 2015 Dear BGS Students, There is some confusion regarding the years of the program in which you get no taxes withheld from your stipend check, and need to file estimated taxes and the years

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

TAX POLICY AND PROCEDURE GUIDE FOR PAYMENTS TO ALIEN INDIVIDUALS Revised as of July 2017 University of Alabama at Birmingham PREFACE The Tax Policy and Procedure Guide for Income Payments to Alien Individuals

Federal Taxation of Aliens Working in the United States

Federal Taxation of Aliens Working in the United States Erika K. Lunder Legislative Attorney May 18, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

Federal Taxation of Aliens Working in the United States Erika K. Lunder Legislative Attorney May 18, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional Research

US Tax: Corporate Members Eligibility for Treaty Benefits

market bulletin From Senior Tax Manager Taxation (extn 6839) Date 10 November 2005 Reference Subject Y3668 US Tax: Corporate Members Eligibility for Treaty Benefits Subject areas US Tax: Corporate Members

market bulletin From Senior Tax Manager Taxation (extn 6839) Date 10 November 2005 Reference Subject Y3668 US Tax: Corporate Members Eligibility for Treaty Benefits Subject areas US Tax: Corporate Members

(of 19 March 2013) Valid from 1 January A. Taxpayers

Valid from 1 January A. Taxpayers") Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

MIT U.S. Income Tax Presenta3on Interna3onal Scholars, Nonresidents for Tax Purposes

MIT U.S. Income Tax Presenta3on Interna3onal Scholars, Nonresidents for Tax Purposes PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Who are Scholars Postdoctoral Associates and Fellows Lecturers Visi3ng

MIT U.S. Income Tax Presenta3on Interna3onal Scholars, Nonresidents for Tax Purposes PwC Boston Nabih Daaboul Carol McNeil Rich Wagman 1 Who are Scholars Postdoctoral Associates and Fellows Lecturers Visi3ng

Federal Tax Information Session For International Scholars

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

Federal Tax Information Session For International Scholars Agenda Tax Basics Forms You RECEIVE Forms You COMPLETE Tax Residency Status Tax Filing Information for Non-residents Treaty Information Filling

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

Payments Made to Nonresident Aliens

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Payments Made to Nonresident Aliens A Policies and Procedures Manual This Procedures for Payments Made to Nonresident Aliens guide was prepared by Arctic International LLC in connection with Occidental

Other Tax Rates. Non-Resident Withholding Tax Rates for Treaty Countries 1

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Other Tax Rates Non-Resident Withholding Tax Rates for Treaty Countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15

Non-resident withholding tax rates for treaty countries 1

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

Non-resident withholding tax rates for treaty countries 1 Country 2 Interest 3 Dividends 4 Royalties 5 Annuities 6 Pensions/ Algeria 15% 15% 0/15% 15/25% Argentina 7 12.5 10/15 3/5/10/15 15/25 Armenia

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

APA & MAP COUNTRY GUIDE 2017 UNITED STATES

APA & MAP COUNTRY GUIDE 2017 UNITED STATES Managing uncertainty in the new tax environment UNITED STATES KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance

APA & MAP COUNTRY GUIDE 2017 UNITED STATES Managing uncertainty in the new tax environment UNITED STATES KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR

Session 2017 Tax Year Georgia Form 500 with Form 1040NR") Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

Volunteer Income Tax Assistance (VITA) Session 2017 Tax Year Georgia Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance

ORD ISIN: DE / CINS CUSIP: D (ADR: / US )

") The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

Gerry Weber International AG

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

INTERNATIONAL JOURNAL OF RESEARCH AND ANALYSIS VOLUME 5 ISSUE 2 ISSN

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

Contents. Andreas Athinodorou Managing Director International Tax Planning

Seize the advantage of our expertise Technical Newsletter This publication should be used as a source of general information only. For the specific applications of the Law, professional advice should be

Seize the advantage of our expertise Technical Newsletter This publication should be used as a source of general information only. For the specific applications of the Law, professional advice should be

Valid from 1 January A. Taxpayers

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Leaflet. 29/410 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under public law for persons without domicile or in Switzerland (of 19 March 2013) Valid from 1 January 2013

Withholding Tax Rate under DTAA

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

If you do not have all of the above forms, please call Junn De Guzman at (732)

") To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

To: Non-Resident Aliens Requesting Special Tax Treatment From: Junn De Guzman, Sr. Accountant Payroll Department Date: December 31, 2011 Re: Requirements for Tax Benefits for Calendar Year 2012 Enclosed

Sweden Country Profile

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH BOWEN & GREEN, CPA s 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com WEBB PAGE

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH BOWEN & GREEN, CPA s 5010 Centennial Commons Dr NW Acworth, GA 30102-2181 Phone (770) 529-4394 EMAIL taxman@regreencpa.com WEBB PAGE

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

INTERNATIONAL STUDENTS TAX WORKSHOP 2018

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

INTERNATIONAL STUDENTS TAX WORKSHOP 2018 INTRODUCTORY ITEMS Did you have health insurance you purchased from the Health Insurance Marketplace? INTRODUCTORY ITEMS Entered the U.S. in 2018? What country

Section 872. Gross Income. Rev. Rul

Section 872. Gross Income (Also sections 883, 894.) 26 CFR 1.872 2: Exclusions from gross income of nonresident alien individuals. (Also 26 CFR 1.883 1.) This revenue ruling updates the list of countries

Section 872. Gross Income (Also sections 883, 894.) 26 CFR 1.872 2: Exclusions from gross income of nonresident alien individuals. (Also 26 CFR 1.883 1.) This revenue ruling updates the list of countries

Withholding tax rates 2016 as per Finance Act 2016

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Table of Contents. 1 created by

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Non-Resident Alien Frequently Asked Questions

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Materials Management: Payroll Time and Attendance Unit Non-Resident Alien Frequently Asked Questions TAX FILING: DO I NEED TO FILE / WHEN DO I FILE? What happens if I fail to file my taxes? If you owe

Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%

![Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%](/thumbs/88/116150947.jpg "Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%") Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Finland Country Profile

Finland Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Finland EU Member State Double Tax Treaties With: Argentina Armenia Australia

Finland Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Finland EU Member State Double Tax Treaties With: Argentina Armenia Australia

Tax Newsflash January 31, 2014

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Definition of international double taxation

Definition of international double taxation Juridical double taxation: imposition of comparable taxes in two (or more) States on the same taxpayer in respect of the same subject matter and for identical

Definition of international double taxation Juridical double taxation: imposition of comparable taxes in two (or more) States on the same taxpayer in respect of the same subject matter and for identical

To Brokers, Dealers, Commercial Banks, Trust Companies and Other Nominees:

August 31, 2011 To Brokers, Dealers, Commercial Banks, Trust Companies and Other Nominees: We have been appointed by CSR plc, a company organized under the laws of England and Wales ( CSR ), as Exchange

August 31, 2011 To Brokers, Dealers, Commercial Banks, Trust Companies and Other Nominees: We have been appointed by CSR plc, a company organized under the laws of England and Wales ( CSR ), as Exchange

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

APA & MAP COUNTRY GUIDE 2017 DENMARK

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

Canadian Residents Abroad

Canadian Residents Abroad T4131(E) Rev. 12 Is this pamphlet for you? T his pamphlet is for you if you left Canada in the year to travel or live abroad. This pamphlet will help you determine your residency

Canadian Residents Abroad T4131(E) Rev. 12 Is this pamphlet for you? T his pamphlet is for you if you left Canada in the year to travel or live abroad. This pamphlet will help you determine your residency

Instructions for Form 8802 (December 2003)

") Instructions for Form 8802 (December 2003) Application for United States Residency Certification Section references are to the Internal Revenue Code. Department of the Treasury Internal Revenue Service

Instructions for Form 8802 (December 2003) Application for United States Residency Certification Section references are to the Internal Revenue Code. Department of the Treasury Internal Revenue Service

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Following our Announcement A10025, dated 15 February 2010, effective. 1 March 2010

Announcement Tax A10033 Bulgaria: Tax relief procedure for Bulgarian securities Following our Announcement A10025, dated 15 February 2010, effective 1 March 2010 final beneficial owners can use the procedure

Announcement Tax A10033 Bulgaria: Tax relief procedure for Bulgarian securities Following our Announcement A10025, dated 15 February 2010, effective 1 March 2010 final beneficial owners can use the procedure

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH BOWEN & GREEN, CPA s 2645 Dallas Highway Suite 200 Marietta, GA 30064 Main Office Phone (770) 514-8927 EMAIL Bowen - jodeecpa@comcast.net

TAX TIPS FOR FOREIGN MISSIONARIES OF THE SEVENTH-DAY ADVENTIST CHURCH BOWEN & GREEN, CPA s 2645 Dallas Highway Suite 200 Marietta, GA 30064 Main Office Phone (770) 514-8927 EMAIL Bowen - jodeecpa@comcast.net

Real Estate & Private Equity workshop

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Slovakia Country Profile

Slovakia Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Slovakia EU Member State Double Tax Treaties Yes With: Australia Austria Belarus

Slovakia Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Slovakia EU Member State Double Tax Treaties Yes With: Australia Austria Belarus

ALI-ABA Course of Study International Trust and Estate Planning. August 16-17, 2007 Chicago, Illinois

35 ALI-ABA Course of Study International Trust and Estate Planning August 16-17, 2007 Chicago, Illinois Basic U.S. Transfer and Income Tax Rules Applicable to Non-Resident Aliens By Virginia F. Coleman

35 ALI-ABA Course of Study International Trust and Estate Planning August 16-17, 2007 Chicago, Illinois Basic U.S. Transfer and Income Tax Rules Applicable to Non-Resident Aliens By Virginia F. Coleman

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Belgium Country Profile

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

FOREWORD. Services provided by member firms include:

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

2016/17 FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Romania Country Profile

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Lithuania Country Profile

Lithuania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Lithuania EU Member State Yes Double Tax Treaties With: Armenia Austria Azerbaijan

Lithuania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Lithuania EU Member State Yes Double Tax Treaties With: Armenia Austria Azerbaijan

Austria Country Profile

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500

Session 2015 Tax Year GA Form 500") Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Volunteer Income Tax Assistance (VITA) Session 2015 Tax Year GA Form 500 Controller s Office International Student and Scholar Services Disclosure The Volunteer Income Tax Assistance (VITA) Program is

Foreign Nationals Financial Professional Guide

Foreign Nationals Financial Professional Guide Policies issued by American General Life Insurance Company (AGL) except in New York, where issued by The United States Life Insurance Company in the City

Foreign Nationals Financial Professional Guide Policies issued by American General Life Insurance Company (AGL) except in New York, where issued by The United States Life Insurance Company in the City

Romania Country Profile

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Romania Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Romania EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

FOREWORD. Denmark. Services provided by member firms include:

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there

Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

Norway Country Profile

rway Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving rway EU Member State Double Tax Treaties With: Albania Argentina Australia Austria

rway Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving rway EU Member State Double Tax Treaties With: Albania Argentina Australia Austria

wts study Global WTS PE Study A high-level overview of most discussed PE issues in EU, OECD and BRICS countries

wts study Global WTS PE Study A high-level overview of most discussed PE issues in EU, OECD and BRICS countries Table of Contents Preface 3 Conclusions at a glance 4 Summary from the survey 5 Detailed

wts study Global WTS PE Study A high-level overview of most discussed PE issues in EU, OECD and BRICS countries Table of Contents Preface 3 Conclusions at a glance 4 Summary from the survey 5 Detailed

Request to accept inclusive insurance P6L or EASY Pauschal

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

5002001020 page 1 of 7 Request to accept inclusive insurance P6L or EASY Pauschal APPLICANT (INSURANCE POLICY HOLDER) Full company name and address WE ARE APPLYING FOR COVER PRIOR TO DELIVERY (PRE-SHIPMENT

DOING BUSINESS IN PORTUGAL INCORPORATING A COMPANY I - CORPORATE FORMS & INCORPORATION. 1. Legal Structure of Companies: # May 2008

# May 2008 DOING BUSINESS IN PORTUGAL I - CORPORATE FORMS & INCORPORATION 1. Legal Structure of Companies: Among the various legal structures available according to Portuguese Companies Code (Código das

# May 2008 DOING BUSINESS IN PORTUGAL I - CORPORATE FORMS & INCORPORATION 1. Legal Structure of Companies: Among the various legal structures available according to Portuguese Companies Code (Código das

Denmark Country Profile

Denmark Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax With: Treaties Argentina Armenia Australia

Denmark Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax With: Treaties Argentina Armenia Australia

Turkey Country Profile

Turkey Country Profile EU Tax Centre June 2018 EU Tax Centre June 2018 Turkey Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties No

Turkey Country Profile EU Tax Centre June 2018 EU Tax Centre June 2018 Turkey Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties No

Campus Finance and Administration Representative Meeting. March 21, 2013

Campus Finance and Administration Representative Meeting March 21, 2013 Agenda Bringing Foreign Nationals to Wake Forest Presenter: Anne Davenport, Director, Tax Human Resources Update Presenter: Gary

Campus Finance and Administration Representative Meeting March 21, 2013 Agenda Bringing Foreign Nationals to Wake Forest Presenter: Anne Davenport, Director, Tax Human Resources Update Presenter: Gary

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

E 4 ALBERT EMBANKMENT LONDON SE1 7SR Telephone: +44 (0)20 7735 711 Fax: +44 (0)20 7587 3210 1 January 2019 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS

TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017

(CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017") Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Volunteer Income Tax Assistance 2016 Tax Year GA Form 500 with Form 1040NR

Volunteer Income Tax Assistance 2016 Tax Year GA Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure Tax year 2016 The Volunteer Income Tax Assistance (VITA)

Volunteer Income Tax Assistance 2016 Tax Year GA Form 500 with Form 1040NR Controller s Office International Student and Scholar Services Disclosure Tax year 2016 The Volunteer Income Tax Assistance (VITA)

Q&A. 1. Q: Why did the company feel the need to move to Ireland?

Q&A 1. Q: Why did the company feel the need to move to Ireland? A: As we continue to grow the international portion of our business, we believe that moving to a member state of the European Union (EU)

Q&A 1. Q: Why did the company feel the need to move to Ireland? A: As we continue to grow the international portion of our business, we believe that moving to a member state of the European Union (EU)

World Consumer Income and Expenditure Patterns

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

Turkey Country Profile

Turkey Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties With: Albania Algeria Australia Austria

Turkey Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Turkey EU Member State Double Tax Treaties With: Albania Algeria Australia Austria

Madeira: Global Solutions for Wise Investments

Madeira: Global Solutions for Wise Investments Double Taxation Treaties Document downloaded from www.ibc-madeira.com DOUBLE TAXATION TREATIES RATIFIED BY PORTUGAL Europe RATIFICATION/ENTRY INTO FORCE AUSTRIA

Madeira: Global Solutions for Wise Investments Double Taxation Treaties Document downloaded from www.ibc-madeira.com DOUBLE TAXATION TREATIES RATIFIED BY PORTUGAL Europe RATIFICATION/ENTRY INTO FORCE AUSTRIA

INGERSOLL-RAND COMPANY LIMITED (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 Date of Report - March 6, 2009

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 8-K/A CURRENT REPORT Pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934 Date of Report - March 6, 2009

U.S. Nonresident Alien Income Tax Return

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Form 1040NR U.S. Nonresident Alien Income Tax Return OMB No. 1545-0074 For the year January 1 December 31, 2011, or other tax year Department of the Treasury Internal Revenue Service beginning, 2011, and

Hannover Rueckversicherung AG

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

The German Tax Agency (the BZSt) offers an electronic tax relief program (the DTV) designed to facilitate and accelerate German tax reclaims on equities by financial institutions. Acupay provides custodian

Investing In and Through Singapore

Investing In and Through Singapore Shanker Iyer 17 May 2012 Contents Benefits of Singapore Setting Up and Ongoing Requirements Territorial Tax System Taxation of Passive Income and Other income Tax Incentives

Investing In and Through Singapore Shanker Iyer 17 May 2012 Contents Benefits of Singapore Setting Up and Ongoing Requirements Territorial Tax System Taxation of Passive Income and Other income Tax Incentives

Denmark Country Profile

Denmark Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax Treaties With: Argentina Armenia Australia

Denmark Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Denmark EU Member State Double Tax Treaties With: Argentina Armenia Australia

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

IMPORTANT TAX INFORMATION

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Certain Cash Contributions for Typhoon Haiyan Relief Efforts in the Philippines Can Be Deducted on Your 2013 Tax Return A new law allows you to choose to deduct certain charitable contributions of money

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Luxembourg Country Profile

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

TAX INFORMATION PORTUGUESE INTERNATIONAL DOUBLE TAXATION TREATIES. PLMJ Sharing Expertise. Innovating Solutions. April 2011

TAX INFORMATION PLMJ April 2011 PORTUGUESE INTERNATIONAL DOUBLE TAXATION TREATIES International double taxation is an obstacle to trade relations and to the free movement of goods, services, people and

TAX INFORMATION PLMJ April 2011 PORTUGUESE INTERNATIONAL DOUBLE TAXATION TREATIES International double taxation is an obstacle to trade relations and to the free movement of goods, services, people and