Transfer Pricing based on HFM and TPH (Transfer Pricing for Hyperion) Matthew Prior & Neil Weller AMOSCA

|

|

|

- Susanna Parrish

- 6 years ago

- Views:

Transcription

1 Transfer Pricing based on HFM and TPH (Transfer Pricing for Hyperion) Matthew Prior & Neil Weller AMOSCA

2 Agenda Transfer Pricing» Background and context Introducing TPH (Transfer Pricing for Hyperion)» An overview» Demo» Features and benefits

3 Transfer Pricing Background and Context

4 Transfer Pricing In taxation and accounting, transfer pricing refers to the rules and methods for pricing transactions between enterprises under common ownership or control.

5 Fundamental Concepts The cornerstone of transfer pricing is the arm s length principle The amount of profit on transactions between connected parties should for tax purposes be the amount of profit that would have arisen if the same transactions had been executed by unconnected parties This principle is enshrined in OECD guidelines and followed by the tax authorities of most OECD members Many countries require MNE s (Multi National Enterprises) to maintain documentation to demonstrate inter-company transactions are at arm s length» Typically requires extensive analysis and benchmarking of comparables Advance Pricing Agreements can be negotiated with some tax authorities

6 How to determine arm s length pricing Five methods for determining arms length pricing are recognised in the OECD guidelines and US transfer pricing regulations: Comparable uncontrolled price - CUP» Price of comparable transaction between independent parties Resale price method - resale minus» Purchase price of goods for sales and distribution entities Cost plus» Sale price of goods for manufacturers, pricing of intra-group services Transactional Net Margin TNMM» Compare with the return earned by comparable independent enterprise Comparable profits CPM» As TNMM Profit split PSM» Not a recognised method but often asserted or resorted to in disputes

7 Why transfer pricing is important

8 BEPS (Base Erosion & Profit Shifting) The Inclusive Framework on BEPS brings together over 100 countries and jurisdictions to collaborate on the implementation of the OECD/ G20 Base Erosion and Profit Shifting (BEPS) Package. BEPS refers to tax planning strategies that exploit gaps and mismatches in tax rules to artificially shift profits to low or no-tax locations where there is little or no economic activity. Although some of the schemes used are illegal, most are not. This undermines the fairness and integrity of tax systems because businesses that operate across borders can use BEPS to gain a competitive advantage over enterprises that operate at a domestic level.

9 BEPS Action 13 CbC Reporting

10 In the last month alone

11 Introducing Transfer Pricing for Hyperion

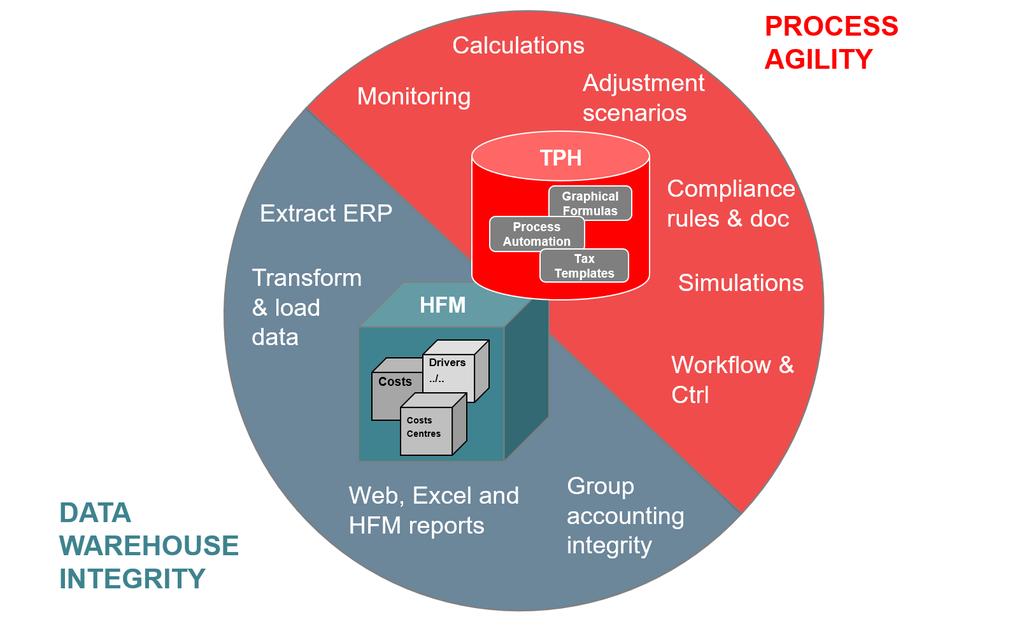

12 HFM and TPH HFM the world s best aggregation and reporting engine» Financial logic» Development capabilities practically unlimited» Range of reporting options and capabilities» Integration utilities» Availability of skills

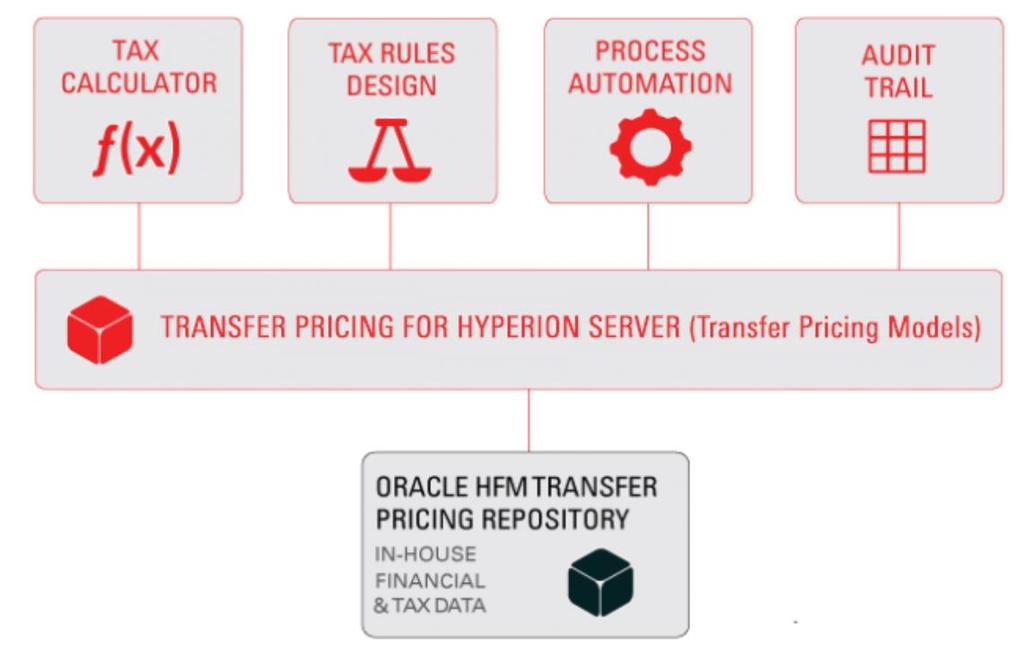

13 HFM and TPH TPH = Transfer Pricing for HFM» Graphical tax calculator» Transfer pricing rules editor» Process automation» Audit trail» HFM transfer pricing application Developed by PebbleAge, Swiss specialists in corporate tax and finance software solutions» Operational Transfer Pricing» Financial Agility» Hyperion Financial Management» Strategic Planning

14 HFM & TPH

15 System landscape of TPH

16

17 Tax calculations

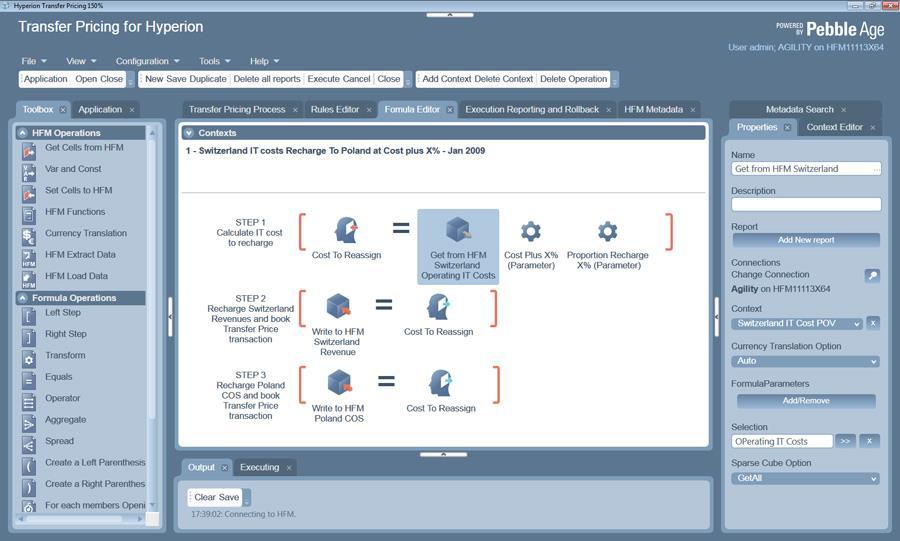

18 Additional functionality added to HFM Drag & drop graphical HFM formula editor

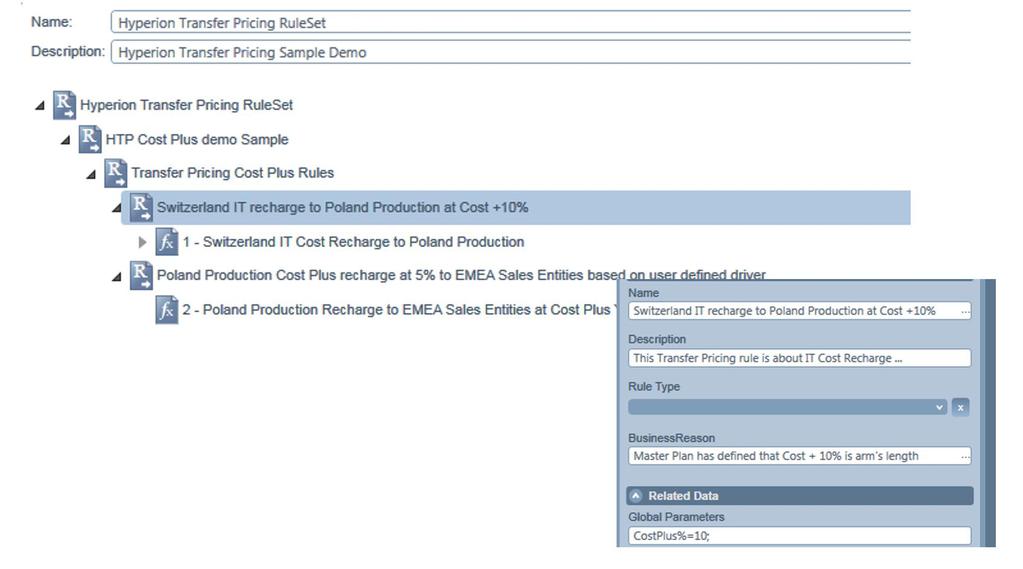

19 Rules repository

20 Process Design

21 Process automation and co-ordination

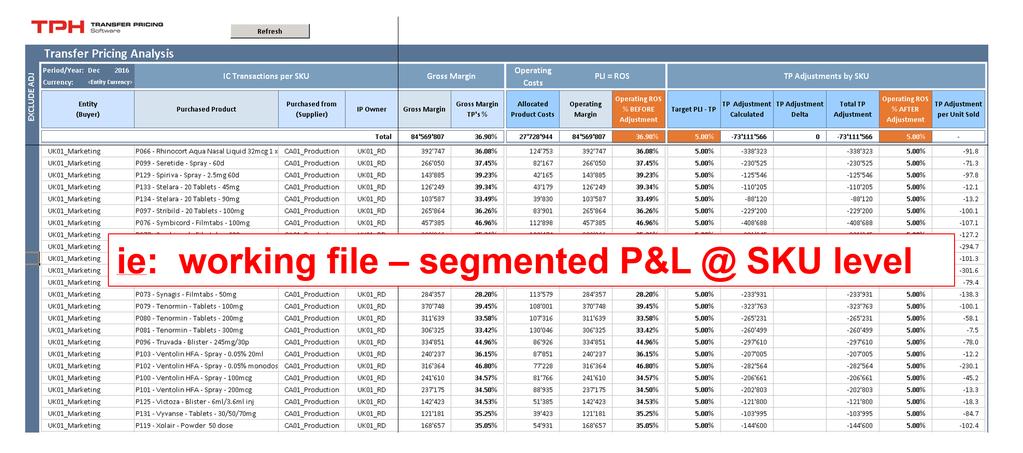

22 Reports SKU analysis

23 Reports SKU analysis

24 Reports

25 Reports

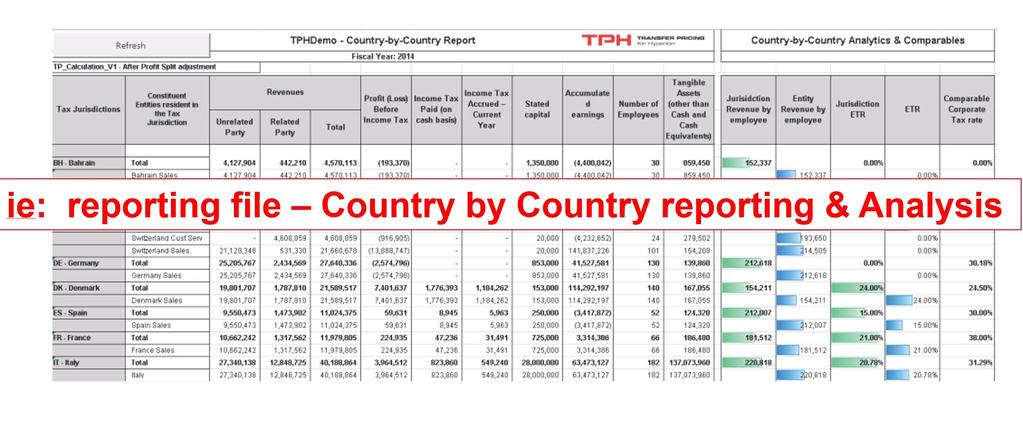

26 Reports P&L Segmentation Analysis per IP Owner & per Supplier

27 Reports P&L Summary for All Legal Entities

28 Transfer Pricing Adjustment Validation

29 Generate profit split transactions

30 Audit Trail

31 Benefits of TPH Monitoring» Monitoring & Co-ordination» Integrated Audit Trail» Tax & Finance data aligned Optimise Tax Return» Proactive Transfer Pricing management» Full financial simulations prior to execution» Measure the bottoem line impact Save operational costs» Full automation of manual procedures» Avoidance of spreadsheet nightmare» Reduce consulting and audit fees

32 Features & Benefits of TPH

33 Thank you

IBFD Course Programme Principles of Transfer Pricing

IBFD Course Programme Principles of Transfer Pricing Overview and Learning Objectives On 5 October 2015, the OECD published its reports addressing base erosion and profit shifting (BEPS). This new guidance

IBFD Course Programme Principles of Transfer Pricing Overview and Learning Objectives On 5 October 2015, the OECD published its reports addressing base erosion and profit shifting (BEPS). This new guidance

IBFD Course Programme Principles of Transfer Pricing

IBFD Course Programme Principles of Transfer Pricing Price: 1,300 (US$ 1560) Price for full IBFD Members: 1,040 (US$ 1,248) Early Bird Discount: A 30% discount will be applied to registrations for this

IBFD Course Programme Principles of Transfer Pricing Price: 1,300 (US$ 1560) Price for full IBFD Members: 1,040 (US$ 1,248) Early Bird Discount: A 30% discount will be applied to registrations for this

Transfer Pricing Principles By Wilfred Alambo KPMG Advisory Services Limited

Transfer Pricing Principles By Wilfred Alambo KPMG Advisory Services Limited Introduction, African overview and TP methods Table of contents 1. Background & introduction 2. Overview TP in Africa 3. TP

Transfer Pricing Principles By Wilfred Alambo KPMG Advisory Services Limited Introduction, African overview and TP methods Table of contents 1. Background & introduction 2. Overview TP in Africa 3. TP

SEMINAR ON TRANSFER PRICING 23rd September, Valuation Approaches and their applicability under Transfer Pricing. CA Siddharth Banwat

SEMINAR ON TRANSFER PRICING 23rd September, 2017 Valuation Approaches and their applicability under Transfer Pricing WHAT IS VALUATION? WHAT IS VALUE? A value in exchange is a hypothetical price and the

SEMINAR ON TRANSFER PRICING 23rd September, 2017 Valuation Approaches and their applicability under Transfer Pricing WHAT IS VALUATION? WHAT IS VALUE? A value in exchange is a hypothetical price and the

Tax Seminar: Transfer Pricing A Customs Perspective. Peter Caxton Kinuthia Director, Tax Services KPMG Kenya. 30 April 2015

Tax Seminar: Transfer Pricing A Customs Perspective Peter Caxton Kinuthia Director, Tax Services KPMG Kenya 30 April 2015 Presentation Outline Background TP and Customs Valuation Worldwide Developments

Tax Seminar: Transfer Pricing A Customs Perspective Peter Caxton Kinuthia Director, Tax Services KPMG Kenya 30 April 2015 Presentation Outline Background TP and Customs Valuation Worldwide Developments

OECD Tax Treaties and Transfer Pricing Division 2, rue André Pascal Paris Per

OECD Tax Treaties and Transfer Pricing Division 2, rue André Pascal 75775 Paris Per e-mail: TransferPricing@oecd.org Basel, 20 June 2018 St. 001 SMA +41 61 295 92 80 SBA Submission: OECD Request for Public

OECD Tax Treaties and Transfer Pricing Division 2, rue André Pascal 75775 Paris Per e-mail: TransferPricing@oecd.org Basel, 20 June 2018 St. 001 SMA +41 61 295 92 80 SBA Submission: OECD Request for Public

Introduction to Transfer Pricing. Presented by Ziad Rahman APTP

Introduction to Transfer Pricing Presented by Ziad Rahman APTP What is Transfer Pricing? Arm s Length Principle. Transfer Pricing Documentation. Transfer Pricing Methodologies. Benchmarking. Transfer Pricing

Introduction to Transfer Pricing Presented by Ziad Rahman APTP What is Transfer Pricing? Arm s Length Principle. Transfer Pricing Documentation. Transfer Pricing Methodologies. Benchmarking. Transfer Pricing

Principles of Transfer Pricing

Summary This intermediate-level five-day course introduces participants to transfer pricing principles and methodologies and then covers the application of these principles and methodologies to specific

Summary This intermediate-level five-day course introduces participants to transfer pricing principles and methodologies and then covers the application of these principles and methodologies to specific

THE OECD BEPS ACTION PLAN

THE OECD BEPS ACTION PLAN Intangibles and Services Seminar 28-03-2017 INTRODUCTION TO COPENHAGEN ECONOMICS IP Valuation & Transfer Pricing We help our clients by quantifying the economic value of various

THE OECD BEPS ACTION PLAN Intangibles and Services Seminar 28-03-2017 INTRODUCTION TO COPENHAGEN ECONOMICS IP Valuation & Transfer Pricing We help our clients by quantifying the economic value of various

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

TRANSFER PRICING UNDER INCOME TAX ACT, N.Madhan B.Com., CA & Grad CWA. 22 August 2015

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

TRANSFER PRICING UNDER INCOME TAX ACT, 1961 N.Madhan B.Com., CA & Grad CWA 1 22 August 2015 Contents Concept of Transfer Pricing Important Terminologies Nature of Methods & its Applicability Importance

Transfer pricing of intangibles

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

Transfer Pricing Country Summary Ghana

Page 1 of 6 Transfer Pricing Country Summary Ghana September 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines Ghana published the Transfer Pricing Regulations, 2012 (L.I 2188)

Page 1 of 6 Transfer Pricing Country Summary Ghana September 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines Ghana published the Transfer Pricing Regulations, 2012 (L.I 2188)

Chapter -1. An Introduction to Transfer Pricing

United Nations Geneva Meeting 16 th October 2012 Chapter -1 An Introduction to Transfer Pricing - Mr. T. P. Ostwal (India) October 2012 1 SYNOPSIS Section No. Title 1 What is Transfer Pricing? 2 Basic

United Nations Geneva Meeting 16 th October 2012 Chapter -1 An Introduction to Transfer Pricing - Mr. T. P. Ostwal (India) October 2012 1 SYNOPSIS Section No. Title 1 What is Transfer Pricing? 2 Basic

Transfer Pricing Country Summary Russia

Page 1 of 6 Transfer Pricing Country Summary Russia 16 November 2015 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines The TP rules are fixed in the Russian Tax Code (Part 1). Furthermore,

Page 1 of 6 Transfer Pricing Country Summary Russia 16 November 2015 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines The TP rules are fixed in the Russian Tax Code (Part 1). Furthermore,

Transfer Pricing. General Department of Taxation. Presented by: Mr.Traing Lay Mr. Chea Chantra. 18 January 2018

General Department of Taxation Transfer Pricing Presented by: Mr.Traing Lay Mr. Chea Chantra 18 January 2018 All rights reserved by General Department of Taxation 1 Content 1- Overview of Transfer Pricing

General Department of Taxation Transfer Pricing Presented by: Mr.Traing Lay Mr. Chea Chantra 18 January 2018 All rights reserved by General Department of Taxation 1 Content 1- Overview of Transfer Pricing

Issues Involving Comparability and Profit Based Methods in Transfer Pricing

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

G L O B A L T R A N S F E R P R I C I N G S E R V I C E S Issues Involving Comparability and Profit Based Methods in Transfer Pricing International Taxation Conference 2008 December 5, 2008 T A X Uday

Transfer Pricing Country Summary Pakistan

Page 1 of 7 Transfer Pricing Country Summary Pakistan July 2018 Page 2 of 7 Legislation Existence of Transfer Pricing Laws/Guidelines There is a general anti-avoidance rule in the Pakistani tax law that

Page 1 of 7 Transfer Pricing Country Summary Pakistan July 2018 Page 2 of 7 Legislation Existence of Transfer Pricing Laws/Guidelines There is a general anti-avoidance rule in the Pakistani tax law that

TPA Global. Top-10 Solutions. tpa-global.com

TPA Global Top-10 Solutions 1 Top Ten TP Specific Solutions - Overview 2 1 Are you in control on tax/tp? TPA offers a solution to MNEs to be in control of their organizational and operational aspects of

TPA Global Top-10 Solutions 1 Top Ten TP Specific Solutions - Overview 2 1 Are you in control on tax/tp? TPA offers a solution to MNEs to be in control of their organizational and operational aspects of

Internal or external comparables can be used to determine the gross profit margin.

Question 1 Part 1 The Resale Price Minus Method(RPM) is a transfer pricing method use generally by distribution companies in order to determine the arm's length price of transactions with related parties.

Question 1 Part 1 The Resale Price Minus Method(RPM) is a transfer pricing method use generally by distribution companies in order to determine the arm's length price of transactions with related parties.

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Transfer Pricing Country Summary Russia

Page 1 of 6 Transfer Pricing Country Summary Russia March 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines The Transfer pricing ( TP ) rules are fixed in the Russian Tax Code

Page 1 of 6 Transfer Pricing Country Summary Russia March 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines The Transfer pricing ( TP ) rules are fixed in the Russian Tax Code

IBFD Course Programme Principles of Transfer Pricing

IBFD Course Programme Principles of Transfer Pricing Price: 1,875 (US$ 2,415) Price for full IBFD Members: 1,500 (US$ 1,932) Early Bird Discount: A 30% discount will be applied to registrations for this

IBFD Course Programme Principles of Transfer Pricing Price: 1,875 (US$ 2,415) Price for full IBFD Members: 1,500 (US$ 1,932) Early Bird Discount: A 30% discount will be applied to registrations for this

KIRKLAND ALERT. e First BEPS Changes Come to the U.S.: e IRS Issues Proposed Regulations on Country-by-Country Reporting. Attorney Advertising

KIRKLAND ALERT January 2016 e First BEPS Changes Come to the U.S.: e IRS Issues Proposed Regulations on Country-by-Country Reporting On December 21, 2015, the U.S. Treasury and the Internal Revenue Service

KIRKLAND ALERT January 2016 e First BEPS Changes Come to the U.S.: e IRS Issues Proposed Regulations on Country-by-Country Reporting On December 21, 2015, the U.S. Treasury and the Internal Revenue Service

IBFD Course Programme Principles of International Taxation

IBFD Course Programme Principles of International Taxation Need a good base to start your career in international tax? This course will provide the essential knowledge you need and give you the confidence

IBFD Course Programme Principles of International Taxation Need a good base to start your career in international tax? This course will provide the essential knowledge you need and give you the confidence

Transfer Pricing Country Summary Tanzania

Page 1 of 6 Transfer Pricing Country Summary Tanzania August 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines Section 33 of the Income Tax Act, Chapter 332 ( The Act ) sets out

Page 1 of 6 Transfer Pricing Country Summary Tanzania August 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines Section 33 of the Income Tax Act, Chapter 332 ( The Act ) sets out

KPMG s general comments on the Discussion Draft are as follows:

KPMG International To Andrew Hickman Head of Transfer Pricing Unit Centre for Tax Policy and Administration OECD From KPMG Date Ref Comments to the OECD: BEPS Action 10 Discussion Draft on the Transfer

KPMG International To Andrew Hickman Head of Transfer Pricing Unit Centre for Tax Policy and Administration OECD From KPMG Date Ref Comments to the OECD: BEPS Action 10 Discussion Draft on the Transfer

Principles of International Taxation

Overview and Learning Objectives This tax course is designed to provide participants with the essentials of international taxation. The first three days are dedicated to the fundamental concepts relevant

Overview and Learning Objectives This tax course is designed to provide participants with the essentials of international taxation. The first three days are dedicated to the fundamental concepts relevant

Arm s Length Principle. Kavita Sethia Gambhir

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

Institute of Certified Public Accountants Transfer Pricing Workshop

Institute of Certified Public Accountants Transfer Pricing Workshop Transfer Pricing Post BEPS by Antony Munanda Ag. Manager, International Tax Office, KRA. 6 th June 2018 1 www.kra.go.ke 08/06/2018 Outline

Institute of Certified Public Accountants Transfer Pricing Workshop Transfer Pricing Post BEPS by Antony Munanda Ag. Manager, International Tax Office, KRA. 6 th June 2018 1 www.kra.go.ke 08/06/2018 Outline

Introduction to Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Introduction to Transfer Pricing Regulations January 24, 2015 Vispi T. Patel Vispi T. Patel & Associates 1 Agenda Transfer Pricing Regulations in India Practical applicability of Transfer Pricing Regulations

Base erosion & profit shifting (BEPS) 25 May 2016

25 May 2016") Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

TRANSFER PRICING DATED CA. Ashwani Rastogi, New Delhi

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

TRANSFER PRICING DATED 8.6.2017 1 India has signed the historic multilateral convention to implement tax treaty related measures to prevent Base Erosion and Profit Shifting (BEPS), at Paris with More than

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

Transfer Pricing Country Summary Israel

Page 1 of 11 Transfer Pricing Country Summary Israel September 2018 Page 2 of 11 Legislation Existence of Transfer Pricing Laws/Guidelines The current legal framework in Israel is based mainly upon Section

Page 1 of 11 Transfer Pricing Country Summary Israel September 2018 Page 2 of 11 Legislation Existence of Transfer Pricing Laws/Guidelines The current legal framework in Israel is based mainly upon Section

DECEMBER Update on Transfer Pricing: Compliance Requirements and the Changing Landscape

DECEMBER 2018 Update on Transfer Pricing: Compliance Requirements and the Changing Landscape Outline Sections 1 Objectives 2 Overview of transfer pricing concepts 3 Legal basis for transfer pricing in

DECEMBER 2018 Update on Transfer Pricing: Compliance Requirements and the Changing Landscape Outline Sections 1 Objectives 2 Overview of transfer pricing concepts 3 Legal basis for transfer pricing in

Egypt updates Transfer Pricing Guidelines

Egypt updates Transfer Pricing Guidelines October 2018 In brief On 23 October 2018, the Egyptian Tax Authority ( ETA ) published an update to the Egyptian Transfer Pricing Guidelines ( ETPG ) which were

Egypt updates Transfer Pricing Guidelines October 2018 In brief On 23 October 2018, the Egyptian Tax Authority ( ETA ) published an update to the Egyptian Transfer Pricing Guidelines ( ETPG ) which were

Introduction to Transfer Pricing Regulations BCA. Vispi T. Patel. Vispi T. Patel & Associates

Introduction to Transfer Pricing Regulations BCA Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Regulation in India Practical applicability of the Transfer Pricing Regulation and Case

Introduction to Transfer Pricing Regulations BCA Vispi T. Patel Vispi T. Patel & Associates Agenda Transfer Pricing Regulation in India Practical applicability of the Transfer Pricing Regulation and Case

Transfer Pricing Country Summary Romania

Page 1 of 8 Transfer Pricing Country Summary Romania June 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines Overview General Transfer Pricing rules have been implemented in Romanian

Page 1 of 8 Transfer Pricing Country Summary Romania June 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines Overview General Transfer Pricing rules have been implemented in Romanian

Korean Tax Update BEPS Implementation

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Transfer Pricing Country Summary The Netherlands

Page 1 of 6 Transfer Pricing Country Summary The Netherlands June 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On 11 May 2018 the Dutch Ministry of Finance published a new

Page 1 of 6 Transfer Pricing Country Summary The Netherlands June 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On 11 May 2018 the Dutch Ministry of Finance published a new

International Transfer Pricing Framework

Are you ready for transfer pricing? Seminar on November 28th, 2005 Swissotel, Istanbul International Framework Marc Diepstraten, Partner, PwC Amsterdam, +31 20 568 64 76 PwC Agenda Transfer pricing environment

Are you ready for transfer pricing? Seminar on November 28th, 2005 Swissotel, Istanbul International Framework Marc Diepstraten, Partner, PwC Amsterdam, +31 20 568 64 76 PwC Agenda Transfer pricing environment

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

Taxing and Pricing of Intangibles. Alan Ross

SMU-TA Centre for Excellence in Taxation Inaugural Conference 2015 Taxing and Pricing of Intangibles Alan Ross 17 September 2015 2 Outline of Discussion Areas Today Address the various BEPS documents impacting

SMU-TA Centre for Excellence in Taxation Inaugural Conference 2015 Taxing and Pricing of Intangibles Alan Ross 17 September 2015 2 Outline of Discussion Areas Today Address the various BEPS documents impacting

BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

CONTENTS BOOK ONE GENERAL PRINCIPLES OF TRANSFER PRICING CHAPTER 1 : INTRODUCTION 3 CHAPTER 2 : FEATURES OF THE TRANSFER PRICING REGIME UNDER CHAPTER X 10 CHAPTER 3 : TRANSFER PRICING PROVISIONS OF CHAPTER

Engaging title in Green Descriptive element in Blue 2 lines if needed

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting

5 January 2018 Global Tax Alert Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting EY Global Tax Alert Library Access both online and pdf versions of

5 January 2018 Global Tax Alert Hong Kong introduces tax and transfer pricing legislation to counter Base Erosion and Profit Shifting EY Global Tax Alert Library Access both online and pdf versions of

Revised Guidance on the Application of the Transactional Profit Split Method INCLUSIVE FRAMEWORK ON BEPS: ACTIONS 10

Revised Guidance on the Application of the Transactional Profit Split Method INCLUSIVE FRAMEWORK ON BEPS: ACTIONS 10 June 2018 OECD/G20 Base Erosion and Profit Shifting Project Revised Guidance on the

Revised Guidance on the Application of the Transactional Profit Split Method INCLUSIVE FRAMEWORK ON BEPS: ACTIONS 10 June 2018 OECD/G20 Base Erosion and Profit Shifting Project Revised Guidance on the

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud

and EU measures against aggressive tax planning and tax fraud") The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The transfer pricing rules apply for transactions between resident persons, as well as for transactions between resident persons and non-residents.

18. Bulgaria Introduction The Bulgarian tax legislation requires that taxpayers determine their taxable profits and income by applying the arm s-length principle to the prices for which they exchange goods,

18. Bulgaria Introduction The Bulgarian tax legislation requires that taxpayers determine their taxable profits and income by applying the arm s-length principle to the prices for which they exchange goods,

OECD releases final BEPS package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

International Tax Primer. Third Edition. Brian J. Arnold

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

BEPS: What does it mean for funds and asset managers?

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

Effects of Transfer Pricing in developing countries: Cases in Africa

ACCOUNTANTS ANNUAL CONFERENCE 2016 Effects of Transfer Pricing in developing countries: Cases in Africa APC- Bunju 3 rd December, 2016 CPA Ahmad Mohamed (MARLA, ADA, Dip-Edu) Disclaimer This presentation

ACCOUNTANTS ANNUAL CONFERENCE 2016 Effects of Transfer Pricing in developing countries: Cases in Africa APC- Bunju 3 rd December, 2016 CPA Ahmad Mohamed (MARLA, ADA, Dip-Edu) Disclaimer This presentation

Keywords: arm s length principle, transfer pricing, MNE economic rent, BEPS

Crawford School of Public Policy TTPI Tax and Transfer Policy Institute TTPI - Working Paper 7/2016 September 2016 Melissa Ogier Abstract Multinational enterprises (MNEs) operating by way of wholly owned

Crawford School of Public Policy TTPI Tax and Transfer Policy Institute TTPI - Working Paper 7/2016 September 2016 Melissa Ogier Abstract Multinational enterprises (MNEs) operating by way of wholly owned

CA T. P. OSTWAL. T. P. Ostwal & Associates LLP

CA T. P. OSTWAL BEPS strategies may not necessarily be illegal Increased globalisation enables companies to exploit gaps arising on interaction of domestic tax systems and treaty rules within the boundary

CA T. P. OSTWAL BEPS strategies may not necessarily be illegal Increased globalisation enables companies to exploit gaps arising on interaction of domestic tax systems and treaty rules within the boundary

Intra-Group Services & Intangibles

Intra-Group Services & Intangibles Mbiki Kamanjiri @ 2016 Grant Thornton All rights reserved. What is covered under Intangible Property Definition: Property with no physical existence but whose value depends

Intra-Group Services & Intangibles Mbiki Kamanjiri @ 2016 Grant Thornton All rights reserved. What is covered under Intangible Property Definition: Property with no physical existence but whose value depends

Transfer Pricing Country Summary Turkey

Page 1 of 8 Transfer Pricing Country Summary Turkey August 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines Formal transfer pricing rules were introduced in Turkey on 21 June

Page 1 of 8 Transfer Pricing Country Summary Turkey August 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines Formal transfer pricing rules were introduced in Turkey on 21 June

Russian Federation. Transfer Pricing Country Profile. Updated October The Arm s Length Principle

Russian Federation Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle?

Russian Federation Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle?

On October , the OECD released its final report on

New TP documentation rules: update and CbCR example Maik Heggmair and Tobias Faltlhauser of WTS summarise the new transfer pricing (TP) documentation rules to be implemented in Germany and provide an example

New TP documentation rules: update and CbCR example Maik Heggmair and Tobias Faltlhauser of WTS summarise the new transfer pricing (TP) documentation rules to be implemented in Germany and provide an example

B.4. Intra-Group Services

B.4. Intra-Group Services Introduction B.4.1. This chapter considers the transfer prices for intra-group services within an MNE group. Firstly, it considers the tests for determining whether chargeable

B.4. Intra-Group Services Introduction B.4.1. This chapter considers the transfer prices for intra-group services within an MNE group. Firstly, it considers the tests for determining whether chargeable

Veronica Vragaleva Scientific researcher, Ph.D student, The Institute of Economy, Finance and Statistics, Republic of Moldova

TAX ASPECTS OF TRANSFER PRICE REGULATION: PERSPECTIVE OF IMPLEMENTATION IN THE REPUBLIC OF MOLDOVA Veronica Vragaleva Scientific researcher, Ph.D student, The Institute of Economy, Finance and Statistics,

TAX ASPECTS OF TRANSFER PRICE REGULATION: PERSPECTIVE OF IMPLEMENTATION IN THE REPUBLIC OF MOLDOVA Veronica Vragaleva Scientific researcher, Ph.D student, The Institute of Economy, Finance and Statistics,

Aligning Transfer Pricing Outcomes with Value

OECD/G20 Base Erosion and Profit Shifting Project Aligning Transfer Pricing Outcomes with Value Creation ACTIONS 8-10: 2015 Final Reports OECD/G20 Base Erosion and Profit Shifting Project Aligning Transfer

OECD/G20 Base Erosion and Profit Shifting Project Aligning Transfer Pricing Outcomes with Value Creation ACTIONS 8-10: 2015 Final Reports OECD/G20 Base Erosion and Profit Shifting Project Aligning Transfer

Examining the impact of BEPS on the life sciences sector. Overview of select BEPS final reports and timing of implementation

Examining the impact of BEPS on the life sciences sector Overview of select BEPS final reports and timing of implementation Contents Overview of BEPS 1 Impact of BEPS final reports on the life sciences

Examining the impact of BEPS on the life sciences sector Overview of select BEPS final reports and timing of implementation Contents Overview of BEPS 1 Impact of BEPS final reports on the life sciences

Transfer Pricing Methods. Transactional Net Margin Method. Presented by: Suchint Majmudar. Date. Agenda

Transfer Pricing Methods Transactional Net Margin Method Presented by: Suchint Majmudar Agenda Introduction Transactional Net Margin Method TNMM CPM Slide 2 1 Most Appropriate Method OECD advocates the

Transfer Pricing Methods Transactional Net Margin Method Presented by: Suchint Majmudar Agenda Introduction Transactional Net Margin Method TNMM CPM Slide 2 1 Most Appropriate Method OECD advocates the

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Summary This intermediate-level course provides participants with an in-depth understanding of the current discussions relating to international

IBFD Course Programme Current Issues in International Tax Planning Summary This intermediate-level course provides participants with an in-depth understanding of the current discussions relating to international

Value chain perspectives and their increased importance under BEPS, tax policy and technological change

Value chain perspectives and their increased importance under BEPS, tax policy and technological change February 22, 2017 FOR DISCUSSION PURPOSES ONLY Disclaimer This material has been prepared for general

Value chain perspectives and their increased importance under BEPS, tax policy and technological change February 22, 2017 FOR DISCUSSION PURPOSES ONLY Disclaimer This material has been prepared for general

OECD TP Guidelines July 2017 Brief synopsis

OECD TP Guidelines July 2017 Brief synopsis Introduction to the OECD TP Guidelines Snapshot OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations Commonly referred to as

OECD TP Guidelines July 2017 Brief synopsis Introduction to the OECD TP Guidelines Snapshot OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations Commonly referred to as

Transfer Pricing in a Post -BEPS World

Transfer Pricing in a Post -BEPS World Intangibles Perspective Ajit Kumar Jain About the Author Ajit is a Chartered Accountant and Company Secretary. He has done his graduation from Jai Narayan Vyas University,

Transfer Pricing in a Post -BEPS World Intangibles Perspective Ajit Kumar Jain About the Author Ajit is a Chartered Accountant and Company Secretary. He has done his graduation from Jai Narayan Vyas University,

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel 19th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations v OECD

MP&S DECOSIMO GLOBAL TRANSFER PRICING DOCUMENTATION, CONSULTING AND ARMS-LENGTH PRICE DETERMINATION

TRANSFER PRICING DOCUMENTATION, CONSULTING AND ARMS-LENGTH PRICE DETERMINATION Transforming global problems into global solutions Transfer pricing is a term used to describe all aspects of intercompany

TRANSFER PRICING DOCUMENTATION, CONSULTING AND ARMS-LENGTH PRICE DETERMINATION Transforming global problems into global solutions Transfer pricing is a term used to describe all aspects of intercompany

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

TRAINING ON TRANSFER PRICING. Income Tax Workshop DATE: 12th 13th April 2018 VENUE: Grand Regency Hotel Nairobi

TRAINING ON TRANSFER PRICING Income Tax Workshop DATE: 12th 13th April 2018 VENUE: Grand Regency Hotel Nairobi 1 www.kra.go.ke 18/04/2018 INTRODUCTION TO TRANSFER PRICING What is Transfer Pricing? Prices

TRAINING ON TRANSFER PRICING Income Tax Workshop DATE: 12th 13th April 2018 VENUE: Grand Regency Hotel Nairobi 1 www.kra.go.ke 18/04/2018 INTRODUCTION TO TRANSFER PRICING What is Transfer Pricing? Prices

Country by Country Reporting & Tax Footprint Jarno Siivola Vice President, Tax Metso Corporation

Country by Country Reporting & Tax Footprint Jarno Siivola Vice President, Tax Metso Corporation Metso in brief Metso a focused industrial company We are dedicated to delivering solutions: Processing equipment,

Country by Country Reporting & Tax Footprint Jarno Siivola Vice President, Tax Metso Corporation Metso in brief Metso a focused industrial company We are dedicated to delivering solutions: Processing equipment,

Post-BEPS application of the arm s length principle: India charts a new course

Post-BEPS application of the arm s length principle: India charts a new course India Tax Insights Rajendra Nayak Partner Tax & Regulatory Services, EY India An updated version of the United Nations Transfer

Post-BEPS application of the arm s length principle: India charts a new course India Tax Insights Rajendra Nayak Partner Tax & Regulatory Services, EY India An updated version of the United Nations Transfer

14.01 TRANSFER PRICING IN MEXICO

Yoshio Uehara & Gustavo Méndez * 14.01 TRANSFER PRICING IN MEXICO Recent efforts of the Organization for Economic Cooperation and Development ( OECD ) 1 members in the tax area is to prevent that multinational

Yoshio Uehara & Gustavo Méndez * 14.01 TRANSFER PRICING IN MEXICO Recent efforts of the Organization for Economic Cooperation and Development ( OECD ) 1 members in the tax area is to prevent that multinational

Transfer Pricing Country Profile (to be posted on the OECD Internet site

Transfer Pricing Country Profile (to be posted on the OECD Internet site www.oecd.org/taxation) Name of Country: Australia Date of profile: November 2006 No. Item Reference to and wherever possible text

Transfer Pricing Country Profile (to be posted on the OECD Internet site www.oecd.org/taxation) Name of Country: Australia Date of profile: November 2006 No. Item Reference to and wherever possible text

FINAL PACKAGE OF MEASURES UNDER THE BASE EROSION AND PROFIT SHIFTING ( BEPS ) PROJECT An Indian Perspective

PROJECT An Indian Perspective") FINAL PACKAGE OF MEASURES UNDER THE BASE EROSION AND PROFIT SHIFTING ( BEPS ) PROJECT An Indian Perspective TABLE OF CONTENTS 02 1. Background 03 2. Action 1: Addressing the tax challenges of the digital

FINAL PACKAGE OF MEASURES UNDER THE BASE EROSION AND PROFIT SHIFTING ( BEPS ) PROJECT An Indian Perspective TABLE OF CONTENTS 02 1. Background 03 2. Action 1: Addressing the tax challenges of the digital

Turkey amends transfer pricing legislation

19 August 2016 Global Tax Alert News from Transfer Pricing Turkey amends transfer pricing legislation EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into

19 August 2016 Global Tax Alert News from Transfer Pricing Turkey amends transfer pricing legislation EY Global Tax Alert Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into

Transfer Pricing Country Summary Belgium

Page 1 of 8 Transfer Pricing Country Summary Belgium July 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines The arm s length principle is codified in Article 185, Par 2, of the

Page 1 of 8 Transfer Pricing Country Summary Belgium July 2018 Page 2 of 8 Legislation Existence of Transfer Pricing Laws/Guidelines The arm s length principle is codified in Article 185, Par 2, of the

INTERSECTION OF TRANSFER PRICING AND CUSTOMS VALUATION: OPPORTUNITIES & CHALLENGES

INTERSECTION OF TRANSFER PRICING AND CUSTOMS VALUATION: OPPORTUNITIES & CHALLENGES SPEAKERS: Ian Cremer, Senior Technical Officer, World Customs Organization Damon V. Pike, President, The Pike Law Firm,

INTERSECTION OF TRANSFER PRICING AND CUSTOMS VALUATION: OPPORTUNITIES & CHALLENGES SPEAKERS: Ian Cremer, Senior Technical Officer, World Customs Organization Damon V. Pike, President, The Pike Law Firm,

An overview of Transfer Pricing

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

An overview of Transfer Pricing Vispi T. Patel Vispi T. Patel & Associates March 14, 2015 1 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer Pricing Regulations

Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

CA. Vispi T. Patel, CA. Rajiv Shah and CA.Kejal Visharia Broad Overview of Transfer Pricing Provisions in India and Current Key Issues faced by Tax-payer INTERNATIONAL PRICING PROVISIONS TRANSFER Introduction

Domestic Fiscal System and International

Lorenzo Riccardi Vietnam Tax Guide Domestic Fiscal System and International Treaties ^ Springer Part I Vietnamese Tax System 1 Introduction to the Vietnamese Tax System 3 1.1 Legislative Background and

Lorenzo Riccardi Vietnam Tax Guide Domestic Fiscal System and International Treaties ^ Springer Part I Vietnamese Tax System 1 Introduction to the Vietnamese Tax System 3 1.1 Legislative Background and

MALAYSIA TRANSFER PRICING LANDSCAPE

MALAYSIA TRANSFER PRICING LANDSCAPE 1967: Introduced general anti-avoidance through Section 140 of the Malaysian Income Tax Act, 1967. July 2003: Transfer pricing guidelines were introduced by the Internal

MALAYSIA TRANSFER PRICING LANDSCAPE 1967: Introduced general anti-avoidance through Section 140 of the Malaysian Income Tax Act, 1967. July 2003: Transfer pricing guidelines were introduced by the Internal

OECD/G20 Base Erosion and Profit Shifting Project

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

THE OECD 2017 TRANSFER PRICING GUIDELINES AN INDIAN PERSPECTIVE

THE OECD 2017 TRANSFER PRICING GUIDELINES AN INDIAN PERSPECTIVE FROM OUR CEO The Organisation for Economic Co-operation and Development ( OECD ) on July 10, 2017, released the updated OECD Transfer Pricing

THE OECD 2017 TRANSFER PRICING GUIDELINES AN INDIAN PERSPECTIVE FROM OUR CEO The Organisation for Economic Co-operation and Development ( OECD ) on July 10, 2017, released the updated OECD Transfer Pricing

Transfer Pricing Backdrop in. Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

Transfer Pricing Backdrop in India Glimpse on International Transactions CA Utpal Doshi and CA Harshil Shah 9 October, 2016 Presentation Outline Introduction ti Transfer Pricing Regulations in India Arms

Global FS view on BEPS latest developments for asset managers. Event Date: Thursday 22 October Event Time: 9am EDT/3pm CET

Global FS view on BEPS latest developments for asset managers Event Date: Thursday 22 October Event Time: 9am EDT/3pm CET Notice The following information is not intended to be written advice concerning

Global FS view on BEPS latest developments for asset managers Event Date: Thursday 22 October Event Time: 9am EDT/3pm CET Notice The following information is not intended to be written advice concerning

[2012] 18 taxmann.com 256 (Article)

![[2012] 18 taxmann.com 256 (Article)](/thumbs/75/72354143.jpg "[2012] 18 taxmann.com 256 (Article)") [2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

[2012] 18 taxmann.com 256 (Article) Convergence between Transfer Pricing and Customs Valuation in the Indian context Introduction KARTHIK SUNDARAM Advocate - Madras High Court 1 1. Transactions globally

Newsletter No. 93 (EN) Synopsis on Transfer Pricing in Hong Kong, Thailand and Vietnam

Synopsis on Transfer Pricing in Hong Kong, Thailand and Vietnam") Synopsis on Transfer Pricing in Hong Kong, Thailand and Vietnam March 2016 All r ig ht s r e ser ved Lo r e nz & P art ner s 2016 Although Lorenz & Partners always pays great attention on updating information

Synopsis on Transfer Pricing in Hong Kong, Thailand and Vietnam March 2016 All r ig ht s r e ser ved Lo r e nz & P art ner s 2016 Although Lorenz & Partners always pays great attention on updating information

Transfer Pricing Country Summary Austria

Page 1 of 6 Transfer Pricing Country Summary Austria April 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On July 6, 2016, the Transfer Pricing Documentation Act (TPDA) has

Page 1 of 6 Transfer Pricing Country Summary Austria April 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On July 6, 2016, the Transfer Pricing Documentation Act (TPDA) has

New Zealand. Transfer Pricing Country Profile. Updated October The Arm s Length Principle

New Zealand Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle?

New Zealand Transfer Pricing Country Profile Updated October 2017 SUMMARY REFERENCE The Arm s Length Principle 1 Does your domestic legislation or regulation make reference to the Arm s Length Principle?

BEPS Country-by-Country Reporting Rules and New Documentation Requirements

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

SRI LANKA TRANSFER PRICING LANDSCAPE

SRI LANKA TRANSFER PRICING LANDSCAPE March 2006: Transfer pricing provisions were introduced for the first time in March 2006 under section 104 of the Inland Revenue Act (IRA) of Sri Lanka. April 2008:

SRI LANKA TRANSFER PRICING LANDSCAPE March 2006: Transfer pricing provisions were introduced for the first time in March 2006 under section 104 of the Inland Revenue Act (IRA) of Sri Lanka. April 2008:

India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries

14 November 2016 Global Tax Alert News from Transfer Pricing India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries EY Global Tax Alert Library

14 November 2016 Global Tax Alert News from Transfer Pricing India revises Country Chapter comments in UN Practical Manual on Transfer Pricing Issues for Developing Countries EY Global Tax Alert Library

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Fundamental principles of Transfer Pricing and Transfer Pricing audit under the Income-tax Act, 1961 Borivali (Central) CPE Study Circle of WIRC of The Institute Of Chartered Accountants Of India Vispi

Transfer Pricing Methods and Selection of Most Appropriate Method. Vaishali Mane Partner Grant Thornton India LLP Mumbai

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

Transfer Pricing Methods and Selection of Most Appropriate Method Vaishali Mane Partner Grant Thornton India LLP Mumbai Agenda Transfer Pricing Quick background Arm's Length Principle Overview of Methods

An overview of Transfer Pricing

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

An overview of Transfer Pricing WIRC of ICAI Vispi T. Patel Vispi T. Patel & Associates 19 th June, 2013 Agenda Transfer Pricing Origin, Evolution and Basic Concepts TP Indian Perspective Indian Transfer

o Interpretation of Article 9 of the OECD, UN and US Models: - Primary adjustment - Corresponding adjustments - Secondary adjustment

Program content Draft program: Subject to changes B Basic level course / I Intermediate level course / A Advanced level course April 2019 1 st day of class with welcome and Graduation ceremony for the

Program content Draft program: Subject to changes B Basic level course / I Intermediate level course / A Advanced level course April 2019 1 st day of class with welcome and Graduation ceremony for the