GST SEMINAR FOR FOMFEIA

|

|

|

- Emmeline Cole

- 6 years ago

- Views:

Transcription

1 GST SEMINAR FOR FOMFEIA Accounting For Tax 1 April am -2.30pm New York Hotel, Johor Bahru Norlela Hj Ismail Unit GST, Putrajaya PEJABAT PELAKSANAAN GST KEMENTERIAN KEWANGAN

2 Briefing Agenda 1. Charging Output Tax 2. Entitlement of Input Tax 3. Apportionment Rules 4. GST Adjustments 5. Taxable period 6. Submission of GST Return 7. Payment of Tax 2

3 1 3

4 Input tax and Output tax INPUT Goods (raw materials, machines and other goods) Services (rental telephone and insurance) Utilities (electricity and water) GST on inputs = Input tax Business Claimed input tax GST on outputs = Output tax OUTPUT Goods (e.g. furniture, tableware, television) Services ( e.g. loan of mould 4

5 Output Tax Scope and charge GST is charged on the taxable supply of goods and services made by a taxable person in the course or furtherance of business in Malaysia GST is charged on imported goods 5

6 Output Tax GST charged on taxable supplies (sales of goods / services) deemed supplies disposal of business assets private use of business asset imported services payment not paid to taxable person for purchases made after 6 months gifts costing more than RM 500 6

7 Disposal of Assets Sale of capital assets, other than TOGC subject to GST Sale of assets as TOGC not subject to GST (not a supply) Given free the value will be the open market value subject to GST (>RM500) Sell as scrap the value will be the sale value of scrap subject to GST 7

8 Imported Services Malaysia IT Tex_.UK ABC Sdn.Bhd (Taxable person) Value of Services = RM10, GST = 6% X RM10,000 = RM600 GST-03 OUTPUT TAX = RM600 Port overseas INPUT TAX = RM600 8

9 Output Tax Supplies which may not be subject to GST cash donation or grants where a person does not get benefits compensation or liquidated damages disbursements, dividends, loan repayments or capital injection transfer of going concern (TOGC) contribution to pension, provident or social security fund supplies by any society or similar organisation supplies excluded from input tax credit 9

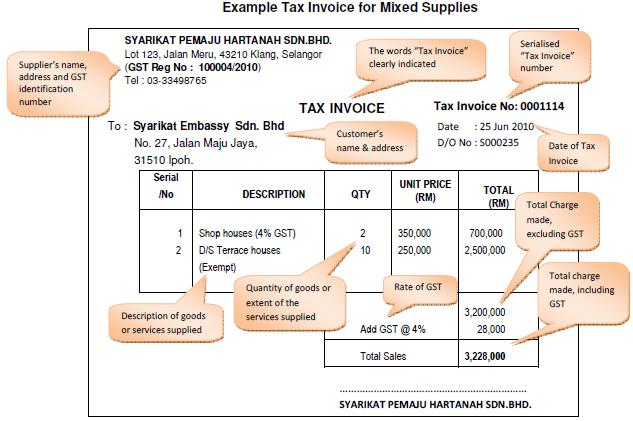

10 Issuance of Tax Invoice Types of tax invoice when making taxable supplies full tax invoice simplified tax invoice 10

11 Serial number Supplier, name, address & Identification number The words tax invoice in a prominent place Date of invoice Name and address of person being supplied Sufficient description The total amount payable excluding tax, the rate of tax and the total tax chargeable shown as a separate amount. The total amount payable including the total tax chargeable

12 1 2

13 Simplified Tax Invoice Statement Price inclusive of GST 6% need to be printed here The total amount payable including GST 6% 13

14 More sample Supplier Identification? Date of invoice Sufficient description The total amount payable including tax 14

15 2 15

16 Supplies taxable supplies Allowable Input Tax standard rated or zero rated supplies disregarded supplies (supplies within group, supplies made in warehouse) supplies made outside Malaysia which would be taxable supplies if made in Malaysia any other prescribed supply (Fixed Input Tax Recovery) 16

17 Group Registration Inputs: Raw materials, Utilities, commercial buildings Supplies to any members are treated as supplies to representative member Group member Supplies between groups are disregarded Group Representative Submission of GST return and payment to Authority Group member Group Registration 17

18 Warehousing Scheme A Inputs: Forklift charges, storage charges C Declares supply and pays GST B 18

19 Supplies Made Outside Malaysia B Factory Inputs: office rental, utilities, office furniture Purchase clothes A Operational Headquarters Supplies clothes issue invoices C 19

Input tax based on fixed rate")

20 Fixed Input Tax Recovery computer, commercial buildings, office furniture Exempt supplies (business) Input tax based on fixed rate Recovery Taxable supplies (fee based services) utilities, audit, telecommunication security services, Exempt supplies (non business) 20

21 Allowable Input Tax Incidental financial supplies: deposit of money exchange of currency holding of bonds or other debt securities transfer of ownership of securities provision of loans, advance or credit to employees or connected persons assignment of provision of trade receivables holding or transfer of trust unit hedging of interest, commodity, utility or freight risk 21

22 Incidental Financial Supplies Special tax treatment does not apply to: commercial or investment bank or money broker development financial institutions or money lenders insurance company stock or futures brokers pawn broker or hire purchase companies debt factor or credit or debit card companies investment or unit trust or venture capital company 22

23 Input Tax Credit Prerequisite for ITC: Claimant must be a taxable person Must have a valid tax invoice full tax invoice simplified tax invoice - claim the input tax up to a limit of RM30.00 if name and address of recipient is not stated in invoice (GST at 6%) invoice issued by approved person under Flat Rate Scheme Customs No 1 /Customs 9 (imported goods) document to show claimant pays imported services Invoice issued under the name of the claimant Goods and services acquired are not subject to any input tax restriction e.g., motorcars Good and services are acquired for the purpose of making taxable supply 23

24 Input Tax Mechanism Input Tax Credit Tax paid on inputs to be offset against the output tax in the relevant taxable period Subject to a time limit of 6 years from the date of return required to be made Apportionment rule to apply for a mixed supply Refund to be offset against other unpaid GST, customs and excise duties Net tax to be refunded within 14 working days for on-line submission 28 working days for manual submission 24

25 Non Allowable Input Tax Blocked input tax passenger motor cars including hiring of car family benefits club subscription fee medical and personal accident insurance medical expenses entertainment expenses for family members and potential clients 25

26 Blocked Input Tax Passenger motor car adapted for carrying not more than 9 passengers including the driver unladen weight of which does not exceed 3000kg Exclusion public service or tourism motor cars hire and drive cars or cars for sale by second hand dealers cars used for driving instructional purposes cars forming part of stock in trade cars used exclusively for business purposes approved by Director General 26

27 Blocked Input Tax Family benefits any benefits (including hospitality of any kind) provided by the taxable person for the benefit of any person who is the wife, husband, child or relative of any person employed by the taxable person for the purposes of any business carried on or to be carried on by the taxable person 27

28 Blocked Input Tax Club subscription fee any joining fee, subscription fee, membership fee, transfer fee or other consideration charged by any club, association, society or organization established principally for recreational or sporting purposes or by the transferor of the membership or such club, association, society or organization 28

29 Blocked Input Tax Medical and personal accident insurance Any payment or contribution for insurance contracts:- To insure and cover the cost of medical treatment as well as cost of personal accident in which the insured is any person employed by the taxable person 29

30 Blocked Input Tax Medical expenses any medical expenses in connection with the provision of medical treatment to any person employed by a taxable person Entertainment expenses Spouse or family members Potential clients Employees Clients 30

31 3 31

32 Apportionment Rules Apportionment rules (first level) Apportionment between business and non-business Apportionment rules (second level): Applicable when goods and services are used for both taxable and exempt supplies (mixed supplier) 32

33 Apportionment Rules No apportionment if can attribute wholly full input tax if wholly attributable to taxable supplies no input tax if wholly attributable to exempt supplies Apportionment rules applicable when goods and services are used for both taxable and non-taxable supplies 33

34 Apportionment Rules Inputs used Wholly attributable to taxable supplies Wholly attributable to exempt supplies Claim 100% input tax Attributable to both taxable and exempt supplies Cannot claim input tax Apportionment rules apply 34

35 Apportionment Rules Mechanism for input tax apportionment Turnover-based method as a standard method for apportioning any residual input Taxable portion = Value of taxable supplies Value of all supplies round up or down to the nearest two decimal places Input tax claimable = Taxable portion X Residual input tax 35

36 Apportionment Rules Example: Taxable supplies = RM300,000 Exempt supplies = RM250,000 Residual input tax = RM8,000 RM300,000 Taxable portion = RM300,000 + RM250,000 = % = 54.55% (2 decimal places) Input tax claimable = 54.55% X RM8,000 = RM4,364 36

37 Apportionment Rules Standard method must reflect correct proportion to which the inputs are put to use if does not reflect correct proportion, use alternative methods floor space method transaction based method input based method cost centre accounting method employee time method use of alternative methods requires prior approval 37

38 Apportionment Rules Example: A finance company Arus Sdn Bhd. deals in taxable leasing and exempt personal loans services. The value and number of transaction of taxable and exempt supplies are as follows: Activities No. of Transactions % Value (RM) % Leasing agreements entered into , Personal loans entered into ,000, TOTAL ,750,

39 Apportionment Rules De Minimis Limit Exempt input tax can be recovered in full if the total value of exempt supply is less than a prescribed amount Prescribed amount total value of the exempt supplies does not exceed Example: an average of RM5,000 per month and not exceeding 5% of the total value of total supplies (all taxable and exempt supplies) made in that period Factory provides transport (workers bus) to his workers for a charge 39

40 De Minimis Limit Example 1 : A manufacturing company provides bus transportation to its workers and charges them. Activity Taxable Exempt % Value (RM) 150,000 4, Full recovery of input tax allowed 40

41 De Minimis Limit Example 2 : A manufacturing company provides bus transportation to its workers and charges them. Activity Taxable Exempt % Value (RM) 500,000 10, Full recovery of input tax are not allowed, have to apply apportionment rule on ITC Residual Input Tax Taxable Supplies Exempted Supplies ITC Claimable Total Input Tax RM500 RM500,000 RM10,000 98% RM

42 4 42

43 Adjustments Adjustments to input tax and output tax when the taxable person issues debit notes or credit notes payment not received after 6 months (bad debts) debtor has become insolvent before expiry of 6 months payment not made for supply after six months 43

44 Adjustments Credit note & Debit note Adjustments due to credit note issued credit note is issued when the amount previously invoiced is reduced or a transaction is cancelled Supplier, already accounted for output tax, reduces output tax in the return for the taxable period in which the credit note was issued buyer, already claimed input tax, reduces input tax in the return for the taxable period in which he received the credit note Adjustments due to debit note issued debit note is issued when the amount previously invoiced is increased supplier has to increase output tax in the return for the taxable period in which the debit note was issued buyer has to increase input tax in the return for the taxable period in which he received the debit note 44

45 Credit note & Debit note adjustment Adjustment Supplier Recipient In relation to Adjustment method When: In GST Return for Adjustment method When: In GST Return for Credit note Reduce output tax The taxable period where CN is issued Reduce input tax Taxable period where CN is issued Debit note Increase output tax The taxable period where DN is issued Increase input tax Taxable period where DN is issued 45

46 Bad debt Bad Debt Relief entitle to relief on bad debts if the taxable person has not received any payment or part of payment in respect of the taxable supplies Conditions to apply relief GST has been paid has not received any payment or part payment 6 months from the date of supply or the debtor has become insolvent before the period of 6 months has elapsed sufficient efforts have been made to recover the debt 46

47 Adjustments Bad debts Adjustments due to payment not received supplier is entitled to bad debts relief supplier claims as input tax in the return for the taxable period in which the bad debts are given relief output tax paid, claim as A1 input tax = x C B where A1 is the payment not received in respect of the taxable supply B is the consideration for the taxable supply C is the tax due and payable on the taxable supply customer account as output tax in the return for the taxable period in which the bad debts are given relief 47

48 Adjustments Bad debts Adjustments due to payment received in respect of bad debts supplier has made the claim for bad debt relief subsequently customer paid the debt supplier accounts as output tax in the return for the taxable period in which the payment is made output tax amount to account A2 output tax = x C B where A2 is the payment received in respect of the taxable supply B is the consideration for the taxable supply C is the tax due and payable on the taxable supply customer claim as input tax in the return for the taxable period in which the payment is made 48

49 Adjustments Bad debts Adjustment Supplier Recipient In relation to Adjustment method When: In GST Return for Adjustment method When: In GST Return for Bad debt relief (Payment NOT received) Increase input tax The taxable period when bad debt relief is claimed Increase output tax The taxable period where the 6 th months from time of supply occurred Recovery of bad debt (Payment received) Increase output tax The taxable period when payment is received Increase input tax The taxable period when payment is made 49

50 Other Adjustment Capital Goods adjustment Applicable for mixed suppliers only Criteria : Value of the goods (exclusive of tax) RM100,000 Used in the course or furtherance of a business The goods can be capitalised under GAAP goods other than properties = 5 successive intervals Properties = 10 successive intervals First interval commence on the day of supply and end on the last day of that tax year Subsequent interval correspond with the tax year *Tax year is the financial year of the taxable person 50

51 5 51

52 Taxable period Regular interval period where a taxable person accounts and pays GST to the government The taxable period will be determined at the time when the GST registration is approved quarterly basis for businesses with annual turnover not exceeding RM5 million monthly basis for businesses with annual turnover exceeding RM5 million A taxable person may apply to be placed in any other category other than his pre-determined taxable period 52

53 6 53

54 Submission of GST Returns Filing of Returns GST returns and payments must be submitted not later than the last day of the month following the end of the taxable period Electronic filing is encouraged 54

55 Submission of GST Returns GST Return must be submitted for any condition as follows: Payment : output tax > input tax Refund : output tax < input tax No payment : output tax = input tax no output tax, no input tax (nil return) Return not submitted an offence 55

56 Submission of Tax Return 56

57 Submission of GST Returns When to submit GST Return monthly taxable period quarterly taxable period 57

58 Submission of GST Returns GST charged on taxable supplies less GST paid on business purchases equal Output Tax Input Tax minus (-) Net GST plus (+) Refund to taxable person Pay GST to Government 58

59 Submission of GST Returns Sample of GST Return Calculation of output tax Value of taxable supplies made Output tax Calculation of input tax Value of taxable supplies received Input tax Net tax payable/refundable GST payable (2 4) GST refundable (4 2) RM1,000,000 1 RM 40,000 2 RM 600,000 3 RM 24,000 4 RM 16,

60 Submission of GST Returns Sample of GST Return Calculation of output tax Value of taxable supplies made Output tax Calculation of input tax Value of taxable supplies received Input tax RM1,000,000 1 RM 40,000 2 RM1, 600,000 3 RM 64,000 4 Net tax payable/refundable GST payable (2 4) 5 GST refundable (4 2) RM 24,

61 7 61

62 payments must be submitted not later than the last day of the month following the end of the taxable period Payment of tax may be made at JKDM office, in person cheque, bank draft, postal order, money order 62

63 Cont.. Payment of tax may be made.. over the counter at dedicated bank cheque, bank draft by post cheque, bank draft, postal order by electronic means Internet banking, FPX (financial processing exchange) 63

64 Thank You Pejabat Pelaksanaan GST Kementerian Kewangan Malaysia Norlela Hj Ismail GST Unit Royal Malaysian Customs

GST SEMINAR: FOMFEIA. Accounting For Tax. ate : 4 Mac 2014 lace: Hotel Hatten Melaka

GST SEMINAR: FOMFEIA Accounting For Tax ate : 4 Mac 2014 lace: Hotel Hatten Melaka Briefing Agenda 1. Charging Output Tax 2. Entitlement of Input Tax 3. Apportionment Rules 4. GST Adjustments 5. Taxable

GST SEMINAR: FOMFEIA Accounting For Tax ate : 4 Mac 2014 lace: Hotel Hatten Melaka Briefing Agenda 1. Charging Output Tax 2. Entitlement of Input Tax 3. Apportionment Rules 4. GST Adjustments 5. Taxable

Getting prepared for GST 5 June 2014

www.pwc.com Getting prepared for GST Agenda GST in a nutshell Impact of GST on businesses Challenges of GST Implementation Steps to be GST compliant 2 GST in a nutshell 3 GST headlines Standard rate: 6%

www.pwc.com Getting prepared for GST Agenda GST in a nutshell Impact of GST on businesses Challenges of GST Implementation Steps to be GST compliant 2 GST in a nutshell 3 GST headlines Standard rate: 6%

Contents. Salient Features of GST

Contents Salient Features of GST 1 What is GST? 1 2 Proposed GST model 4 3 Basic elements of GST 17 4 Registration for GST 35 Contents Accounting For Tax 1 Charging Output Tax 51 2 Entitlement of Input

Contents Salient Features of GST 1 What is GST? 1 2 Proposed GST model 4 3 Basic elements of GST 17 4 Registration for GST 35 Contents Accounting For Tax 1 Charging Output Tax 51 2 Entitlement of Input

FREQUENTLY ASKED QUESTIONS (FAQ) TRANSITIONAL 6% - 0%

TRANSITIONAL 6% - 0%") Without prejudice. FREQUENTLY ASKED QUESTIONS (FAQ) TRANSITIONAL 6% - 0% Note: The FAQ dated 17 May 2018 is cancelled. 1. STATUS OF GST 1.1. S : What does the MOF statement mean / What happens to GST?

Without prejudice. FREQUENTLY ASKED QUESTIONS (FAQ) TRANSITIONAL 6% - 0% Note: The FAQ dated 17 May 2018 is cancelled. 1. STATUS OF GST 1.1. S : What does the MOF statement mean / What happens to GST?

GST SEMINAR MALAYSIA AUTOMOTIVE INSTITUTE (MAI) BUSINESS PREPARATION. Date : 19th. June 2014 Place: Hotel Ixora Seberang Prai Penang

BUSINESS PREPARATION. Date : 19th. June 2014 Place: Hotel Ixora Seberang Prai Penang") GST SEMINAR MALAYSIA AUTOMOTIVE INSTITUTE (MAI) BUSINESS PREPARATION Date : 19th. June 2014 Place: Hotel Ixora Seberang Prai Penang Briefing Agenda 1. Supplies Spanning GST 2. Non Reviewable Contract 3.

GST SEMINAR MALAYSIA AUTOMOTIVE INSTITUTE (MAI) BUSINESS PREPARATION Date : 19th. June 2014 Place: Hotel Ixora Seberang Prai Penang Briefing Agenda 1. Supplies Spanning GST 2. Non Reviewable Contract 3.

GST TREATMENT ON MANUFACTURING AND RETAIL SECTOR

GST TREATMENT ON MANUFACTURING AND RETAIL SECTOR Venue : KLSFEA Shah Alam Date : 26 February 2014 Organised by: KLSFEA Presenter: Sabariah Md Yusof ROYAL MALAYSIAN CUSTOMS FIZ & LMW Concept Current treatments

GST TREATMENT ON MANUFACTURING AND RETAIL SECTOR Venue : KLSFEA Shah Alam Date : 26 February 2014 Organised by: KLSFEA Presenter: Sabariah Md Yusof ROYAL MALAYSIAN CUSTOMS FIZ & LMW Concept Current treatments

SEMINAR GST UNTUK PERSATUAN VETERINAR MALAYSIA (VAM) ACCOUNTING FOR GST

ACCOUNTING FOR GST") SEMINAR GST UNTUK PERSATUAN VETERINAR MALAYSIA (VAM) ACCOUNTING FOR GST Presenter :SABARIAH BINTI MD YUSOF Venue : Holiday Villa Subang Date : 20 November 2014 1 2 Responsibilities and Obligations As a

SEMINAR GST UNTUK PERSATUAN VETERINAR MALAYSIA (VAM) ACCOUNTING FOR GST Presenter :SABARIAH BINTI MD YUSOF Venue : Holiday Villa Subang Date : 20 November 2014 1 2 Responsibilities and Obligations As a

INCOME TAX ISSUES ARISING FROM THE IMPLEMENTATION OF GOODS AND SERVICES TAX

INCOME TAX ISSUES ARISING FROM THE IMPLEMENTATION OF GOODS AND SERVICES TAX Prepared by: Technical Committee Direct Tax (I) [TC-DT (I)] (6 March 2015) INCOME TAX ISSUES ARISING FROM THE IMPLEMENTATION

INCOME TAX ISSUES ARISING FROM THE IMPLEMENTATION OF GOODS AND SERVICES TAX Prepared by: Technical Committee Direct Tax (I) [TC-DT (I)] (6 March 2015) INCOME TAX ISSUES ARISING FROM THE IMPLEMENTATION

Goods and Services Tax

Goods and Services Tax Document Information Document Title : Self Review Check List for GST 03 Issuance Date : November 21, 2015 (Version 4) Purpose : This checklist serves as a guide for you to assess

Goods and Services Tax Document Information Document Title : Self Review Check List for GST 03 Issuance Date : November 21, 2015 (Version 4) Purpose : This checklist serves as a guide for you to assess

75% of aggregate costs 345,000 ½

Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Section B September/December 07 Sample Answers and Marking Scheme (a) Delia Spa Sdn Bhd Capital allowances () Doors are part

Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Section B September/December 07 Sample Answers and Marking Scheme (a) Delia Spa Sdn Bhd Capital allowances () Doors are part

QNE SOFTWARE SDN. BHD. ( V)

") New Tax Code Update Once you upgrade QNE Optimum from old version to new version, the follow tax code will be updated Or click on GST Tax Codes Search Click Tax Codes Update Wizard, the tax code update

New Tax Code Update Once you upgrade QNE Optimum from old version to new version, the follow tax code will be updated Or click on GST Tax Codes Search Click Tax Codes Update Wizard, the tax code update

SST ROADSHOWS BY YEOH CHENG GUAN DATE : 25 AUGUST 2018 VENUE : SENG PENG HALL OF WISMA CHINESE CHAMBER, KUALA LUMPUR

SST ROADSHOWS BY YEOH CHENG GUAN DATE : 25 AUGUST 2018 VENUE : SENG PENG HALL OF WISMA CHINESE CHAMBER, KUALA LUMPUR SALES AND SERVICE TAX (SST 2.0) Sales tax and Service tax (SST) 31 st July 2018 7&8

SST ROADSHOWS BY YEOH CHENG GUAN DATE : 25 AUGUST 2018 VENUE : SENG PENG HALL OF WISMA CHINESE CHAMBER, KUALA LUMPUR SALES AND SERVICE TAX (SST 2.0) Sales tax and Service tax (SST) 31 st July 2018 7&8

GST SEMINAR: IMPLEMENTATION OF GST AND BUSINESS PREPARATION

GST SEMINAR: IMPLEMENTATION OF GST AND BUSINESS PREPARATION 1 Briefing Agenda 1. Supplies Spanning GST 2. Non Reviewable Contract 3. Special Refund 4. Registration 5. Business Preparation for GST 2 1 3

GST SEMINAR: IMPLEMENTATION OF GST AND BUSINESS PREPARATION 1 Briefing Agenda 1. Supplies Spanning GST 2. Non Reviewable Contract 3. Special Refund 4. Registration 5. Business Preparation for GST 2 1 3

Director General s Decision: ( )

") DECISION BY DIRECTOR GENERAL OF ROYAL MALAYSIAN CUSTOMS 1. Small Office Home Office (SOHO) The classification of residential property will be based on the design features and essential characteristics

DECISION BY DIRECTOR GENERAL OF ROYAL MALAYSIAN CUSTOMS 1. Small Office Home Office (SOHO) The classification of residential property will be based on the design features and essential characteristics

Responsibilities of GST-Registered Businesses. Key GST Concepts & Common GST Errors

Responsibilities of GST-Registered Businesses Key GST Concepts & Common GST Errors 1 Responsibilities of a GST- Registered Business Collect and account GST On all taxable supplies of goods and services

Responsibilities of GST-Registered Businesses Key GST Concepts & Common GST Errors 1 Responsibilities of a GST- Registered Business Collect and account GST On all taxable supplies of goods and services

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON PAYMENT BASIS

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON PAYMENT BASIS Publication Date Published: 10 December 2015. The Guide on Payment Basis as at 30 January 2014 is withdrawn and replaced by the Guide

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON PAYMENT BASIS Publication Date Published: 10 December 2015. The Guide on Payment Basis as at 30 January 2014 is withdrawn and replaced by the Guide

Chart of Accounts Analysis for GST Supply

Chart of Accounts Analysis for GST Supply GST Output Tax Code Adjustment Description SR ZRL ZRE DS ES ES43 RS OS GS Note AJP AJS Assets Accounts Receivable Debtors Current Account Employee Advance Funds

Chart of Accounts Analysis for GST Supply GST Output Tax Code Adjustment Description SR ZRL ZRE DS ES ES43 RS OS GS Note AJP AJS Assets Accounts Receivable Debtors Current Account Employee Advance Funds

Paper F6 (MYS) Taxation (Malaysia) Tuesday 12 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Malaysia) Tuesday 12 June Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Malaysia) Tuesday 12 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Fundamentals Level Skills Module Taxation (Malaysia) Tuesday 12 June 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

QNE SOFTWARE SDN. BHD. ( V)

") New Tax Code Update With upgrading to version 730 onward 1) GST GST Code Click on Update GST Tax Code Wizard Click Next to Update new Tax Code. 1 2) Click Update for Tax Code AJP, AJS, GS, IM, TX-RE &

New Tax Code Update With upgrading to version 730 onward 1) GST GST Code Click on Update GST Tax Code Wizard Click Next to Update new Tax Code. 1 2) Click Update for Tax Code AJP, AJS, GS, IM, TX-RE &

2017 Basic tax information in Malaysia

2017 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. ly income that is accrued or derived from

2017 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. ly income that is accrued or derived from

CONSOLIDATED TO 1 DECEMBER 2014 LAWS OF SEYCHELLES

CONSOLIDATED TO 1 DECEMBER 2014 LAWS OF SEYCHELLES VALUE ADDED TAX ACT [1st January, 2013] Act 35of 2010 Act 3 of 2012 Act 13 of 2012 S.I. 62 of 2012 S.I. 65 of 2012 S.I. 33 of 2013 S.I. 34 of 2013 S.I.

CONSOLIDATED TO 1 DECEMBER 2014 LAWS OF SEYCHELLES VALUE ADDED TAX ACT [1st January, 2013] Act 35of 2010 Act 3 of 2012 Act 13 of 2012 S.I. 62 of 2012 S.I. 65 of 2012 S.I. 33 of 2013 S.I. 34 of 2013 S.I.

Paper P6 (MYS) Advanced Taxation (Malaysia) Monday 7 June Professional Level Options Module. The Association of Chartered Certified Accountants

Advanced Taxation (Malaysia) Monday 7 June Professional Level Options Module. The Association of Chartered Certified Accountants") Professional Level Options Module Advanced Taxation (Malaysia) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Monday 7 June 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

CAPITAL GOODS ADJUSTMENT

CAPITAL GOODS ADJUSTMENT 1 AGENDA 2 INTRODUCTION 3 1. BASIC CGA I. What is CGA? INTRODUCTION Adjustments to be made to the initial amount of input tax claimed, during a specified period. II. III. Who need

CAPITAL GOODS ADJUSTMENT 1 AGENDA 2 INTRODUCTION 3 1. BASIC CGA I. What is CGA? INTRODUCTION Adjustments to be made to the initial amount of input tax claimed, during a specified period. II. III. Who need

Accountability for GST Parameter. GST Check List. GST IRR Purchases. GST Additional Information. List

Stanley Wong Stanley.Wong@swprojectconsulting.com.my Parameter Business Unit Name: SSPM Registration Number: 000123456789 Taxable Period From: 01/04/2015 Taxable Period To: 30/06/2015 Submission Date:

Stanley Wong Stanley.Wong@swprojectconsulting.com.my Parameter Business Unit Name: SSPM Registration Number: 000123456789 Taxable Period From: 01/04/2015 Taxable Period To: 30/06/2015 Submission Date:

Recommended GST Tax Code Listings for Purchase and Supply

APPENDIX 3 Introduction Recommended GST Tax Code Listings for Purchase and Supply This section provides a list of GST tax codes for Purchase and Supply. These tax code listings are recommendation to allow

APPENDIX 3 Introduction Recommended GST Tax Code Listings for Purchase and Supply This section provides a list of GST tax codes for Purchase and Supply. These tax code listings are recommendation to allow

GUIDE ON: HIRE PASSENGER VEHICLES SERVICES

SERVICE TAX 2018 GUIDE ON: HIRE PASSENGER VEHICLES SERVICES Published by : Royal Malaysian Customs Department Internal Tax Division Putrajaya 21 August 2018 Publication Date: 21 August 2018. Copyright

SERVICE TAX 2018 GUIDE ON: HIRE PASSENGER VEHICLES SERVICES Published by : Royal Malaysian Customs Department Internal Tax Division Putrajaya 21 August 2018 Publication Date: 21 August 2018. Copyright

GST Awareness Briefing 消费税简介. 17 th July 2014

GST Awareness Briefing 消费税简介 17 th July 2014 Agenda Basics and Fundamentals of GST Supply Transitional Provisions (Supply) Acquisition Transitional Provisions (Acquisition) Impacts on Fringe Benefits Registration,

GST Awareness Briefing 消费税简介 17 th July 2014 Agenda Basics and Fundamentals of GST Supply Transitional Provisions (Supply) Acquisition Transitional Provisions (Acquisition) Impacts on Fringe Benefits Registration,

TRANSITIONAL GUIDE TRANSITIONAL RULES. Published by: Royal Malaysia Customs Department Sales & Service Tax Division Putrajaya

TRANSITIONAL GUIDE TRANSITIONAL RULES Published by: Royal Malaysia Customs Department Sales & Service Tax Division Putrajaya 5 September 2018 Publication Date: 5 September 2018. The Guide on Transitional

TRANSITIONAL GUIDE TRANSITIONAL RULES Published by: Royal Malaysia Customs Department Sales & Service Tax Division Putrajaya 5 September 2018 Publication Date: 5 September 2018. The Guide on Transitional

South Africa: VAT essentials

South Africa: VAT essentials Essential information regarding VAT as it applies in South Africa. Scope and Rates Registration VAT grouping Returns VAT recovery International Supplies of Goods and Services

South Africa: VAT essentials Essential information regarding VAT as it applies in South Africa. Scope and Rates Registration VAT grouping Returns VAT recovery International Supplies of Goods and Services

Malaysian GST: Turning Promises into Hard Realities by April March 2014 Host: Robert Tsang Presenter: Kah Seong Fan

Q&A Report Malaysian GST: Turning Promises into Hard Realities by April 2015 27 March 2014 Host: Robert Tsang Presenter: Kah Seong Fan 1. Does the Goods and Services Tax (GST) identification number of

Q&A Report Malaysian GST: Turning Promises into Hard Realities by April 2015 27 March 2014 Host: Robert Tsang Presenter: Kah Seong Fan 1. Does the Goods and Services Tax (GST) identification number of

Paper FTX (MYS) Foundations in Taxation (Malaysia) FOUNDATIONS IN ACCOUNTANCY. Monday 11 June The Association of Chartered Certified Accountants

Foundations in Taxation (Malaysia) FOUNDATIONS IN ACCOUNTANCY. Monday 11 June The Association of Chartered Certified Accountants") FOUNDTIONS IN CCOUNTNCY Foundations in Taxation (Malaysia) Monday 11 June 2012 Time allowed: 2 hours This paper is divided into two sections: Section LL TEN questions are compulsory and MUST be attempted

FOUNDTIONS IN CCOUNTNCY Foundations in Taxation (Malaysia) Monday 11 June 2012 Time allowed: 2 hours This paper is divided into two sections: Section LL TEN questions are compulsory and MUST be attempted

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON CONSTRUCTION INDUSTRY

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON CONSTRUCTION INDUSTRY TABLE OF CONTENTS INTRODUCTION... 1 Overview of Goods and Services Tax (GST)... 1 GENERAL OPERATION OF THE INDUSTRY... 1 FREQUENTLY

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON CONSTRUCTION INDUSTRY TABLE OF CONTENTS INTRODUCTION... 1 Overview of Goods and Services Tax (GST)... 1 GENERAL OPERATION OF THE INDUSTRY... 1 FREQUENTLY

First floor 400,000 Second floor 200, ,000 Total for three floors 1,200,000 Portion exempt (600,000/1,200,000) 50%

50%") Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Section B March/June 07 Sample Answers and Marking Scheme (a) Adora and Zizan Real property gains tax (RPGT) (i) Adora will

Answers Fundamentals Level Skills Module, Paper F6 (MYS) Taxation (Malaysia) Section B March/June 07 Sample Answers and Marking Scheme (a) Adora and Zizan Real property gains tax (RPGT) (i) Adora will

IRAS e-tax Guide. GST: General Guide for Businesses (Sixth edition)

") IRAS e-tax Guide GST: General Guide for Businesses (Sixth edition) Published by Inland Revenue Authority of Singapore Published on 5 Jul 2017 First Edition on 8 Oct 2014 Second Edition on 1 Apr 2015 Third

IRAS e-tax Guide GST: General Guide for Businesses (Sixth edition) Published by Inland Revenue Authority of Singapore Published on 5 Jul 2017 First Edition on 8 Oct 2014 Second Edition on 1 Apr 2015 Third

ASQ Basic tax information in Malaysia

ASQ 2016 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. Only income that is accrued or derived

ASQ 2016 Basic tax information in Malaysia INCOME TAX Direct taxation in Malaysia is based on the unitary system and the basis of taxation is territorial in nature. Only income that is accrued or derived

MALAYSIAN GST MECHANISM AND ITS IMPACT ON BUSINESS AND FINANCIAL PLANNING

HRDF APPROVED SMETAP Programme Malaysian Export Academy (PSMB Registered Class A Training Provider - SBL Claimable) presents MALAYSIAN GST MECHANISM AND ITS IMPACT ON BUSINESS AND FINANCIAL PLANNING 4

HRDF APPROVED SMETAP Programme Malaysian Export Academy (PSMB Registered Class A Training Provider - SBL Claimable) presents MALAYSIAN GST MECHANISM AND ITS IMPACT ON BUSINESS AND FINANCIAL PLANNING 4

Good & Service Tax. Salient Features of GST. Presented by. Goh Kin Siang Deputy Director of Customs rtd ITS Management Sdn Bhd

Good & Service Tax Salient Features of GST Presented by Goh Kin Siang Deputy Director of Customs rtd ITS Management Sdn Bhd Agenda: Why GST? What is GST? GST Models Basic Elements of GST Registration Why

Good & Service Tax Salient Features of GST Presented by Goh Kin Siang Deputy Director of Customs rtd ITS Management Sdn Bhd Agenda: Why GST? What is GST? GST Models Basic Elements of GST Registration Why

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON DESIGNATED AREA

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON DESIGNATED AREA Publication Date Published: 12 January 2016. The Guide on Designated Area as at 5 January 2016 is withdrawn and replaced by the Guide

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON DESIGNATED AREA Publication Date Published: 12 January 2016. The Guide on Designated Area as at 5 January 2016 is withdrawn and replaced by the Guide

Input Tax 6% To Make Taxable Supplies (standard rated) Input Tax 6% To Make Taxable Supplies (zero rated)

Input Tax 6% To Make Taxable Supplies (zero rated)") Tax Code Listing S/P UD Tax Code RMCD Tax Code Tax Rate Description / GL Acc Note P TX-S TX 6% 6% To Make Taxable Supplies (standard rated) Goods and services purchased from GST registered suppliers and

Tax Code Listing S/P UD Tax Code RMCD Tax Code Tax Rate Description / GL Acc Note P TX-S TX 6% 6% To Make Taxable Supplies (standard rated) Goods and services purchased from GST registered suppliers and

Paper P6 (MYS) Advanced Taxation (Malaysia) March/June 2017 Sample Questions. Professional Level Options Module

Advanced Taxation (Malaysia) March/June 2017 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) March/June 2017 Sample Questions Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section A BOTH questions

Professional Level Options Module Advanced Taxation (Malaysia) March/June 2017 Sample Questions Time allowed: 3 hours and 15 minutes This question paper is divided into two sections: Section A BOTH questions

TAXABLE PERSON GUIDE FOR VALUE ADDED TAX. Issue 1/March 2018

TAXABLE PERSON GUIDE FOR VALUE ADDED TAX Issue 1/March 2018 Contents 1. Introduction... 5 1.1. Purpose of this guide... 5 1.2. Changes to the previous version of the guide... 5 1.3. Who should read this

TAXABLE PERSON GUIDE FOR VALUE ADDED TAX Issue 1/March 2018 Contents 1. Introduction... 5 1.1. Purpose of this guide... 5 1.2. Changes to the previous version of the guide... 5 1.3. Who should read this

Paper F6 (MYS) Taxation (Malaysia) Tuesday 4 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Malaysia) Tuesday 4 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Malaysia) Tuesday 4 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (Malaysia) Tuesday 4 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON PAWNBROKING

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON PAWNBROKING CONTENTS INTRODUCTION... 1 Overview of Goods and Services Tax (GST)... 1 GST TREATMENT ON PAWNBROKING... 1 Provision of Pledge... 1 Accounting

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON PAWNBROKING CONTENTS INTRODUCTION... 1 Overview of Goods and Services Tax (GST)... 1 GST TREATMENT ON PAWNBROKING... 1 Provision of Pledge... 1 Accounting

Section A. 2 B Petrol and insurance RM36 ( ) x 6/106

x 6/106") Answers Applied Skills, TX MYS Taxation Malaysia (TX MYS) September/December 208 Sample Answers and Marking Scheme Section A B A non-resident employee, with the same employer for 2 months, may elect not

Answers Applied Skills, TX MYS Taxation Malaysia (TX MYS) September/December 208 Sample Answers and Marking Scheme Section A B A non-resident employee, with the same employer for 2 months, may elect not

ICC UAE VAT RETURNS WORKSHOP. 29 th March 2018 Dubai Chamber of Commerce & Industry

ICC UAE VAT RETURNS WORKSHOP 29 th March 2018 Dubai Chamber of Commerce & Industry OVERVIEW OF VAT Direct Tax The person paying the tax to the Government directly bears the incidence of tax It is progressive

ICC UAE VAT RETURNS WORKSHOP 29 th March 2018 Dubai Chamber of Commerce & Industry OVERVIEW OF VAT Direct Tax The person paying the tax to the Government directly bears the incidence of tax It is progressive

VAT in the European Community APPLICATION IN THE MEMBER STATES, FACTS FOR USE BY ADMINISTRATIONS/TRADERS INFORMATION NETWORKS ETC.

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes Brussels, October 2010 TAXUD/C/1 VAT in the European Community APPLICATION

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION Indirect Taxation and Tax administration VAT and other turnover taxes Brussels, October 2010 TAXUD/C/1 VAT in the European Community APPLICATION

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON FUND MANAGEMENT

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON FUND MANAGEMENT Publication Date Published: 11 April 2016. The Guide on Fund Management revised as at 27 October 2013 is withdrawn and replaced by

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON FUND MANAGEMENT Publication Date Published: 11 April 2016. The Guide on Fund Management revised as at 27 October 2013 is withdrawn and replaced by

Paper F6 (MYS) Taxation (Malaysia) March/June 2018 Sample Questions. Fundamentals Level Skills Module

Taxation (Malaysia) March/June 2018 Sample Questions. Fundamentals Level Skills Module") Fundamentals Level Skills Module Taxation (Malaysia) March/June 2018 Sample Questions F6 MYS ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions

Fundamentals Level Skills Module Taxation (Malaysia) March/June 2018 Sample Questions F6 MYS ACCA Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions

CHAPTER 1 VAT GENERAL PRINCIPLES

CHAPTER 1 VAT GENERAL PRINCIPLES 1.1 VAT legislation and interpretation Value added tax (VAT) was introduced in the UK on 1 April 1973 by the Finance Act 1972. Successive Finance Acts have made amendments

CHAPTER 1 VAT GENERAL PRINCIPLES 1.1 VAT legislation and interpretation Value added tax (VAT) was introduced in the UK on 1 April 1973 by the Finance Act 1972. Successive Finance Acts have made amendments

1 TAX SEPTEMBER 2017

1 TAX SEPTEMBER 2017 SUGGESTED SOLUTION SET1 SOLUTION 1 MM Manufacturing Sdn Bhd Tax computation for the year of assessment 2017 Add (+) Ded (-) Note 000 000 000 Business income Profit before taxation

1 TAX SEPTEMBER 2017 SUGGESTED SOLUTION SET1 SOLUTION 1 MM Manufacturing Sdn Bhd Tax computation for the year of assessment 2017 Add (+) Ded (-) Note 000 000 000 Business income Profit before taxation

Goods and Services Tax Act 2014

Goods and Services Tax Act 2014 Please be informed that Citibank Berhad is a GST-registered person with GST registration number 000 958 922 752, and therefore our fees and charges for all applicable products

Goods and Services Tax Act 2014 Please be informed that Citibank Berhad is a GST-registered person with GST registration number 000 958 922 752, and therefore our fees and charges for all applicable products

VALUE ADDED TAX (VAT) RETURNS USER GUIDE

RETURNS USER GUIDE") VALUE ADDED TAX (VAT) RETURNS USER GUIDE February 2018 1 Contents 1. Brief overview of this user guide... 3 2. Important notes about the VAT Return... 3 3. Completing and Submitting the VAT Return Form...

VALUE ADDED TAX (VAT) RETURNS USER GUIDE February 2018 1 Contents 1. Brief overview of this user guide... 3 2. Important notes about the VAT Return... 3 3. Completing and Submitting the VAT Return Form...

Broking breakfast briefing

Broking breakfast briefing VAT for broker accounts staff 18 June 2010 VAT for broker accounts staff Introduction to VAT basic principles Partial exemption Group registration The liability of insurance

Broking breakfast briefing VAT for broker accounts staff 18 June 2010 VAT for broker accounts staff Introduction to VAT basic principles Partial exemption Group registration The liability of insurance

ROYAL CUSTOMS DEPARTMENT

ROYAL CUSTOMS DEPARTMENT GOODS AND SERVICES TAX GUIDE ON DEVELOPMENT FINANCIAL INSTITUTION TABLE OF CONTENTS INTRODUCTION... 1 GENERAL OPERATION OF GOODS AND SERVICES TAX (GST)... 1 OVERVIEW GENERAL OPERATIONS

ROYAL CUSTOMS DEPARTMENT GOODS AND SERVICES TAX GUIDE ON DEVELOPMENT FINANCIAL INSTITUTION TABLE OF CONTENTS INTRODUCTION... 1 GENERAL OPERATION OF GOODS AND SERVICES TAX (GST)... 1 OVERVIEW GENERAL OPERATIONS

SEMINAR GST SEMINAR GST FEDERATION OF LIVESTOCK FARMERS ASSOCIATION OF MALAYSIA. Tempat : Holiday 20 Inn November Villa, Subang 2014 Jaya

SEMINAR GST SEMINAR GST FEDERATION OF LIVESTOCK FARMERS ASSOCIATION OF MALAYSIA Tarikh Holiday : 20 November Inn Villa, Shah 2014 Alam Tempat : Holiday 20 Inn November Villa, Subang 2014 Jaya AMINAH ABDUL

SEMINAR GST SEMINAR GST FEDERATION OF LIVESTOCK FARMERS ASSOCIATION OF MALAYSIA Tarikh Holiday : 20 November Inn Villa, Shah 2014 Alam Tempat : Holiday 20 Inn November Villa, Subang 2014 Jaya AMINAH ABDUL

Commissioner. The VAT legislation stipulates following ways in which you should account for the tax:

ACCOUNTING FOR VAT After charging VAT, you are required to account for it to the Commissioner. The VAT legislation stipulates following ways in which you should account for the tax: a) Issuing a Tax Invoice

ACCOUNTING FOR VAT After charging VAT, you are required to account for it to the Commissioner. The VAT legislation stipulates following ways in which you should account for the tax: a) Issuing a Tax Invoice

Paper P6 (MYS) Advanced Taxation (Malaysia) Friday 7 December Professional Level Options Module

Advanced Taxation (Malaysia) Friday 7 December Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Friday 7 December 2012 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Sage Malaysia Tax Reports Implementation Guide. Version TM 6.6A

Sage 300 2019 Malaysia Reports Implementation Guide Version TM 6.6A This is a publication of Sage Software, Inc. 2018 The Sage Group plc or its licensors. All rights reserved. Sage, Sage logos, and Sage

Sage 300 2019 Malaysia Reports Implementation Guide Version TM 6.6A This is a publication of Sage Software, Inc. 2018 The Sage Group plc or its licensors. All rights reserved. Sage, Sage logos, and Sage

CHARTERED TAX INSTITUTE OF MALAYSIA ( T) (Institut Percukaian Malaysia) PROFESSIONAL EXAMINATIONS. Date

(Institut Percukaian Malaysia) PROFESSIONAL EXAMINATIONS. Date") CHARTERED TAX INSTITUTE OF MALAYSIA (225750 T) (Institut Percukaian Malaysia) PROFESSIONAL EXAMINATIONS INTEEDIATE LEVEL BUSINESS TAXATION JUNE 2015 Student Registration No. Desk No. Date Examination Centre

CHARTERED TAX INSTITUTE OF MALAYSIA (225750 T) (Institut Percukaian Malaysia) PROFESSIONAL EXAMINATIONS INTEEDIATE LEVEL BUSINESS TAXATION JUNE 2015 Student Registration No. Desk No. Date Examination Centre

TAX MARCH 2016 TAXATION MARCH 2016 SUGGESTED SOLUTION. Answer 1 PL Adjustment

TAXATION MARCH 2016 SUGGESTED SOLUTION Answer 1 PL Adjustment Musa Engineering Sdn Bhd Tax computation for the year of assessment 2015 Add (+) Ded (-) Note 000 000 000 Business income Profit before taxation

TAXATION MARCH 2016 SUGGESTED SOLUTION Answer 1 PL Adjustment Musa Engineering Sdn Bhd Tax computation for the year of assessment 2015 Add (+) Ded (-) Note 000 000 000 Business income Profit before taxation

Goods and Services Tax (GST)

") Back to Basics: Goods and Services Tax (GST) Lorraine Parkin, Nicole Baxter & Ankit Dashora Grant Thornton Singapore Agenda GST compliance obligations GST classification types of supply Output tax Input

Back to Basics: Goods and Services Tax (GST) Lorraine Parkin, Nicole Baxter & Ankit Dashora Grant Thornton Singapore Agenda GST compliance obligations GST classification types of supply Output tax Input

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON INSURANCE AND TAKAFUL TABLE OF CONTENTS INTRODUCTION... 1 Overview Of Goods And Services Tax (GST)... 1 OVERVIEW GENERAL OPERATIONS OF THE INDUSTRY...

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON INSURANCE AND TAKAFUL TABLE OF CONTENTS INTRODUCTION... 1 Overview Of Goods And Services Tax (GST)... 1 OVERVIEW GENERAL OPERATIONS OF THE INDUSTRY...

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON INSURANCE AND TAKAFUL CONTENTS INTRODUCTION... 1 Overview Of Goods And Services Tax (GST)... 1 OVERVIEW GENERAL OPERATIONS OF THE INDUSTRY... 1 GST

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON INSURANCE AND TAKAFUL CONTENTS INTRODUCTION... 1 Overview Of Goods And Services Tax (GST)... 1 OVERVIEW GENERAL OPERATIONS OF THE INDUSTRY... 1 GST

Paper F6 (CHN) Taxation (China) Monday 6 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (China) Monday 6 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (China) Monday 6 December 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Fundamentals Level Skills Module Taxation (China) Monday 6 December 2010 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Good & Service Tax. Salient Features of GST. Presented by. Goh Kin Siang Deputy Director of Customs rtd ITS Management Sdn Bhd

Good & Service Tax Salient Features of GST Presented by Goh Kin Siang Deputy Director of Customs rtd ITS Management Sdn Bhd Agenda: Why GST? What is GST? GST Models Basic Elements of GST Registration Why

Good & Service Tax Salient Features of GST Presented by Goh Kin Siang Deputy Director of Customs rtd ITS Management Sdn Bhd Agenda: Why GST? What is GST? GST Models Basic Elements of GST Registration Why

ACCA Certified Accounting Technician Examination Paper T9 (MYS) Preparing Taxation Computations (Malaysia)

Preparing Taxation Computations (Malaysia)") Answers ACCA Certified Accounting Technician Examination Paper T9 (MYS) Preparing Taxation Computations (Malaysia) December 2009 Answers and Marking Scheme Notes: () All references to legislation or public

Answers ACCA Certified Accounting Technician Examination Paper T9 (MYS) Preparing Taxation Computations (Malaysia) December 2009 Answers and Marking Scheme Notes: () All references to legislation or public

Paper F6 (CYP) Taxation (Cyprus) Tuesday 3 December Fundamentals Level Skills Module. Time allowed

Taxation (Cyprus) Tuesday 3 December Fundamentals Level Skills Module. Time allowed") Fundamentals Level Skills Module Taxation (Cyprus) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

Fundamentals Level Skills Module Taxation (Cyprus) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax rates

6. Salary costs 8,000 Not a supply Cosmetics purchased from a supplier in Korea and imported into Singapore

Answers Fundamentals Level Skills Module, Paper F6 (SGP) Taxation (Singapore) Section B March/June 208 Sample Answers and Marking Scheme Cosmetic Pte Ltd (a) In order to claim the pre-registration goods

Answers Fundamentals Level Skills Module, Paper F6 (SGP) Taxation (Singapore) Section B March/June 208 Sample Answers and Marking Scheme Cosmetic Pte Ltd (a) In order to claim the pre-registration goods

09/05/2018. LEADER IN NURTURING CHARTERED ACCOUNTANTS Prepared By: Zvino L Mapetere CA(Z)

") 09/05/2018 LEADER IN NURTURING CHARTERED ACCOUNTANTS 2 LEARNING OUTCOMES 1. Determining whether or not VAT should be levied in a transaction s6 2. Classifying supplies for VAT s10 and s11 3. Time of Supply

09/05/2018 LEADER IN NURTURING CHARTERED ACCOUNTANTS 2 LEARNING OUTCOMES 1. Determining whether or not VAT should be levied in a transaction s6 2. Classifying supplies for VAT s10 and s11 3. Time of Supply

TaXavvy Stay current. Be tax savvy.

27 March 2015 Issue 6-2015 TaXavvy Stay current. Be tax savvy. Director General of Custom s decision on GST frequently asked issues 2/2015 and decision amendment 1/2015 www.pwc.com/my 2 Director General

27 March 2015 Issue 6-2015 TaXavvy Stay current. Be tax savvy. Director General of Custom s decision on GST frequently asked issues 2/2015 and decision amendment 1/2015 www.pwc.com/my 2 Director General

GST in INDIA. Input Tax Credit

GST in INDIA Input Tax Credit 1 COMPONENTS Legal Frame work Eligible & Ineligible credit Conditions and Restrictions ITC ITC in specific circumstances Input Service Distribution Recovery of erroneous credit

GST in INDIA Input Tax Credit 1 COMPONENTS Legal Frame work Eligible & Ineligible credit Conditions and Restrictions ITC ITC in specific circumstances Input Service Distribution Recovery of erroneous credit

GOODS & SERVICES TAX (GST) Malaysia

Malaysia") 1 GOODS & SERVICES TAX (GST) Malaysia 9. Tips on Compliance CONTENTS 2 1. Latest GST Developments in Malaysia 2. Introduction to GST 3. GST Mechanism Supplies 4. GST Registration & Liability to Register

1 GOODS & SERVICES TAX (GST) Malaysia 9. Tips on Compliance CONTENTS 2 1. Latest GST Developments in Malaysia 2. Introduction to GST 3. GST Mechanism Supplies 4. GST Registration & Liability to Register

Paper P6 (ZAF) Advanced Taxation (South Africa) Friday 5 June Professional Level Options Module

Advanced Taxation (South Africa) Friday 5 June Professional Level Options Module") Professional Level Options Module Advanced Taxation (South Africa) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (South Africa) Friday 5 June 2015 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

4. Interest income from a Singapore 10,000 Exempt supply 0 1 bank 5. Trading stock bought from a supplier 300,000 Standard-rated 21,

Answers Fundamentals Level Skills Module, Paper F6 (SGP) Taxation (Singapore) Section B September/December 207 Sample Answers and Marking Scheme Pluto Pte Ltd (PPL) (a) Goods and services tax (GST) return

Answers Fundamentals Level Skills Module, Paper F6 (SGP) Taxation (Singapore) Section B September/December 207 Sample Answers and Marking Scheme Pluto Pte Ltd (PPL) (a) Goods and services tax (GST) return

Section A 2 C 10 C $49,000 (102,000/3 + 15,000)

") Answers Applied Skills, TX SGP Taxation Singapore (TX SGP) September/December 2018 Sample Answers and Marking Scheme Section A 1 B The input tax based on the Singapore dollar amounts shown on the import

Answers Applied Skills, TX SGP Taxation Singapore (TX SGP) September/December 2018 Sample Answers and Marking Scheme Section A 1 B The input tax based on the Singapore dollar amounts shown on the import

Paper F6 (CHN) Taxation (China) Monday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (China) Monday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (China) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. s of tax

Fundamentals Level Skills Module Taxation (China) Monday 3 December 2007 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. s of tax

VALUE ADDED TAX GUIDE

FormoreinformationcontacttheSRA ContactCentreon: Tel :+26824064050 Email :info@sra.org.sz AlternativelyvisittheSRA websiteonwww.sra.org.sz Page 1 TABLE OF CONTENTS PART PART ONE Page Number 1.0 Introduction

FormoreinformationcontacttheSRA ContactCentreon: Tel :+26824064050 Email :info@sra.org.sz AlternativelyvisittheSRA websiteonwww.sra.org.sz Page 1 TABLE OF CONTENTS PART PART ONE Page Number 1.0 Introduction

FOUNDATIONS IN ACCOUNTANCY Paper FTX (MYS)

") Answers FOUNDATIONS IN ACCOUNTANCY Paper FTX (MYS) Foundations in Taxation (Malaysia) June 0 Answers and Marking Scheme Notes: () All references to legislation or public rulings shown in square brackets

Answers FOUNDATIONS IN ACCOUNTANCY Paper FTX (MYS) Foundations in Taxation (Malaysia) June 0 Answers and Marking Scheme Notes: () All references to legislation or public rulings shown in square brackets

BUDGET 2016 PROSPERING THE RAKYAT

BUDGET 2016 PROSPERING THE RAKYAT Selected Summary of Malaysia s Tax Budget 2016 CHANGES AFFECTING INDIVIDUAL Review Tax Rate for Individual Resident individual taxpayer: Income tax rate be increased between

BUDGET 2016 PROSPERING THE RAKYAT Selected Summary of Malaysia s Tax Budget 2016 CHANGES AFFECTING INDIVIDUAL Review Tax Rate for Individual Resident individual taxpayer: Income tax rate be increased between

2016/17 GUIDE TO... Value Added Tax. Chartered Accountants Registered Auditors FOR ELECTRONIC USE ONLY

2016/17 GUIDE TO... Value Added Tax Chartered Accountants Registered Auditors 020 8731 0777 www.cohenarnold.com FOR ELECTRONIC USE ONLY YOUR GUIDE TO Value Added Tax Value Added Tax (VAT) is a tax chargeable

2016/17 GUIDE TO... Value Added Tax Chartered Accountants Registered Auditors 020 8731 0777 www.cohenarnold.com FOR ELECTRONIC USE ONLY YOUR GUIDE TO Value Added Tax Value Added Tax (VAT) is a tax chargeable

UK VAT Notices VAT. t&columns=1&id=hmce_cl_ Completing your VAT return. 700/12 Filling in your VAT return

UK VAT Notices VAT Notice title Date of issue Link to Notices Notice Reference VAT Guide 700 The VAT Guide August Completing your VAT return 700/12 Filling in your VAT return April t&columns=1&id=hmce_cl_001596

UK VAT Notices VAT Notice title Date of issue Link to Notices Notice Reference VAT Guide 700 The VAT Guide August Completing your VAT return 700/12 Filling in your VAT return April t&columns=1&id=hmce_cl_001596

15-16 Tax Workshop. for. By Julie Pocock MAAT

15-16 Tax Workshop for By Julie Pocock MAAT What are the deadlines for the 15-16 Tax Year? The 15-16 Tax Year begins on 6 th April 2015 and ends on 5 th April 2016. If you submit a paper tax return, HMRC

15-16 Tax Workshop for By Julie Pocock MAAT What are the deadlines for the 15-16 Tax Year? The 15-16 Tax Year begins on 6 th April 2015 and ends on 5 th April 2016. If you submit a paper tax return, HMRC

Paper F6 (SGP) Taxation (Singapore) September/December 2017 Sample Questions. Fundamentals Level Skills Module. Time allowed: 3 hours 15 minutes

Taxation (Singapore) September/December 2017 Sample Questions. Fundamentals Level Skills Module. Time allowed: 3 hours 15 minutes") Fundamentals Level Skills Module Taxation (Singapore) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions

Fundamentals Level Skills Module Taxation (Singapore) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A ALL 15 questions

1. In this Act "the Principal Act" means the Value-Added Tax Act, Section 1 of the Principal Act is hereby amended by

VALUE-ADDED TAX (AMENDMENT) ACT 1978 VALUE-ADDED TAX (AMENDMENT) ACT 1978 - LONG TITLE AN ACT TO AMEND THE VALUE-ADDED TAX ACT, 1972, AND THE ACTS AMENDING THAT ACT AND TO PROVIDE FOR RELATED MATTERS.

VALUE-ADDED TAX (AMENDMENT) ACT 1978 VALUE-ADDED TAX (AMENDMENT) ACT 1978 - LONG TITLE AN ACT TO AMEND THE VALUE-ADDED TAX ACT, 1972, AND THE ACTS AMENDING THAT ACT AND TO PROVIDE FOR RELATED MATTERS.

STATUTORY INSTRUMENTS. S.I. No. 639 of 2010 VALUE-ADDED TAX REGULATIONS 2010

STATUTORY INSTRUMENTS. S.I. No. 639 of 2010 VALUE-ADDED TAX REGULATIONS 2010 (Prn. A10/1928) 2 [639] S.I. No. 639 of 2010 VALUE-ADDED TAX REGULATIONS 2010 1. Citation and commencement 2. Interpretation

STATUTORY INSTRUMENTS. S.I. No. 639 of 2010 VALUE-ADDED TAX REGULATIONS 2010 (Prn. A10/1928) 2 [639] S.I. No. 639 of 2010 VALUE-ADDED TAX REGULATIONS 2010 1. Citation and commencement 2. Interpretation

Fundamentals Level Skills Module, Paper F6 (HKG)

") Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 200 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Answers Fundamentals Level Skills Module, Paper F6 (HKG) Taxation (Hong Kong) June 200 Answers and Marking Scheme Cases are given in the answers for educational purposes. Unless specifically requested,

Fundamentals Level Skills Module, Paper F6 (SGP)

") Answers Fundamentals Level Skills Module, Paper F6 (SGP) Taxation (Singapore) December 2010 Answers 1 (a) The Income Tax Act defines a company to be resident in Singapore if the control and management

Answers Fundamentals Level Skills Module, Paper F6 (SGP) Taxation (Singapore) December 2010 Answers 1 (a) The Income Tax Act defines a company to be resident in Singapore if the control and management

Paper P6 (MYS) Advanced Taxation (Malaysia) September/December 2017 Sample Questions. Professional Level Options Module

Advanced Taxation (Malaysia) September/December 2017 Sample Questions. Professional Level Options Module") Professional Level Options Module Advanced Taxation (Malaysia) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) September/December 2017 Sample Questions Time allowed: 3 hours 15 minutes This question paper is divided into two sections: Section A BOTH

Sales Tax and Service Tax ( SST ) Framework Deloitte Analysis and Views

Framework Deloitte Analysis and Views") Sales Tax and Service Tax ( SST ) Framework Deloitte Analysis and Views Overview The proposed taxes are conceptually a re-introduction of the Sales Tax and Service Tax that existed prior to the introduction

Sales Tax and Service Tax ( SST ) Framework Deloitte Analysis and Views Overview The proposed taxes are conceptually a re-introduction of the Sales Tax and Service Tax that existed prior to the introduction

Penalty regime Trade with EU VAT Advice helpline: Adrian Houstoun Gail Pitchley Geraint Lewis

VAT Facts 2013/14 Registration Standard rate = 20% from 4 January 2011 Registration threshold from 1 April 2013: 79,000 Deregistration threshold from 1 April 2013: 77,000 VAT rates and types of supply

VAT Facts 2013/14 Registration Standard rate = 20% from 4 January 2011 Registration threshold from 1 April 2013: 79,000 Deregistration threshold from 1 April 2013: 77,000 VAT rates and types of supply

Release Notes for Sage UBS

Release Notes for Sage UBS Content This release notes covers two sections: 1. Progressive Enhancement (if any) 2. Issues that have been addressed Version 9.9.3.1 Release date: 07 th October 2016 Progressive

Release Notes for Sage UBS Content This release notes covers two sections: 1. Progressive Enhancement (if any) 2. Issues that have been addressed Version 9.9.3.1 Release date: 07 th October 2016 Progressive

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON E-COMMERCE SERVICES

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON E-COMMERCE SERVICES Publication Date Published: 18 December 2015. The Guide on E-Commerce as at 20 August 2015 is withdrawn and replaced by the Guide

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON E-COMMERCE SERVICES Publication Date Published: 18 December 2015. The Guide on E-Commerce as at 20 August 2015 is withdrawn and replaced by the Guide

SARS approach to Government institutions

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

SARS approach to Government institutions 1. SARS focusses on the Tax Compliance of Government Institutions at a National, Provincial and Local Level. 2. SARS Risks that we focus are: Correct Registration,

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE MARCH 2019 VERSION 1.0 Contents Contents 1. Introduction... 5 1.1. Purpose of this Guide... 5 1.2. About the National Bureau for Revenue (NBR)... 5 1.3.

KINGDOM OF BAHRAIN VAT FINANCIAL SERVICES GUIDE MARCH 2019 VERSION 1.0 Contents Contents 1. Introduction... 5 1.1. Purpose of this Guide... 5 1.2. About the National Bureau for Revenue (NBR)... 5 1.3.

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON VALUATION

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON VALUATION Publication Date Published: 30 December 2015. Copyright Notice Copyright 2015 Royal Malaysian Customs Department. All rights reserved.

ROYAL MALAYSIAN CUSTOMS GOODS AND SERVICES TAX GUIDE ON VALUATION Publication Date Published: 30 December 2015. Copyright Notice Copyright 2015 Royal Malaysian Customs Department. All rights reserved.

PROFESSIONAL EXAMINATIONS ADVANCE TAXATION 2 DECEMBER Date

CHARTERED TAX INSTITUTE OF MALAYSIA (225750 T) (Institut Percukaian Malaysia) PROFESSIONAL EXAMINATIONS FINAL LEVEL ADVANCE TAXATION 2 DECEMBER 2015 Student Registration No. Desk No. Date Examination Centre

CHARTERED TAX INSTITUTE OF MALAYSIA (225750 T) (Institut Percukaian Malaysia) PROFESSIONAL EXAMINATIONS FINAL LEVEL ADVANCE TAXATION 2 DECEMBER 2015 Student Registration No. Desk No. Date Examination Centre

Paper P6 (MYS) Advanced Taxation (Malaysia) Monday 6 June Professional Level Options Module. The Association of Chartered Certified Accountants

Advanced Taxation (Malaysia) Monday 6 June Professional Level Options Module. The Association of Chartered Certified Accountants") Professional Level Options Module Advanced Taxation (Malaysia) Monday 6 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

Professional Level Options Module Advanced Taxation (Malaysia) Monday 6 June 2011 Time allowed Reading and planning: Writing: 15 minutes 3 hours This paper is divided into two sections: Section A BOTH

TAX MARCH Answer 1

Answer 1 Menara Manufacturing Sdn Bhd Tax computation for the year of assessment 2016 Add (+) Deduct(-) Note 000 000 000 Business income Profit before taxation 232,850 Cost of sales Less: Dividends-single

Answer 1 Menara Manufacturing Sdn Bhd Tax computation for the year of assessment 2016 Add (+) Deduct(-) Note 000 000 000 Business income Profit before taxation 232,850 Cost of sales Less: Dividends-single

GST - Input Tax Credit. Keval Shah at Bandra Kurla Complex, WIRC of the ICAI. Agenda for the day. Provisions of Input Tax Credit

2 GST - Input Tax Credit Keval Shah at Bandra Kurla Complex, WIRC of the ICAI June 16 2017 Agenda for the day Provisions of Input Tax Credit Concept of Input Service Distributor Transitional provisions

2 GST - Input Tax Credit Keval Shah at Bandra Kurla Complex, WIRC of the ICAI June 16 2017 Agenda for the day Provisions of Input Tax Credit Concept of Input Service Distributor Transitional provisions

Paper F6 (SGP) Taxation (Singapore) Tuesday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants

Taxation (Singapore) Tuesday 3 December Fundamentals Level Skills Module. The Association of Chartered Certified Accountants") Fundamentals Level Skills Module Taxation (Singapore) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax

Fundamentals Level Skills Module Taxation (Singapore) Tuesday 3 December 2013 Time allowed Reading and planning: Writing: 15 minutes 3 hours ALL FIVE questions are compulsory and MUST be attempted. Tax