Guidance for Taxpayers on the Mutual Agreement Procedure (Q&A)

|

|

|

- Darren French

- 6 years ago

- Views:

Transcription

1 Guidance for Taxpayers on the Mutual Agreement Procedure (Q&A) July, 2017 Office of the Mutual Agreement Procedure National Tax Agency, Japan This guidance is to complement the contents of the Commissioner s Directive on the Mutual Agreement Procedure (Administrative Guidelines) *1. This provides clear MAP guidance to taxpayers required by the recommendation of the BEPS Action14 Final Report *2 published in October, For further information about the Mutual Agreement Procedure, please refer to the Commissioner s Directive on the Mutual Agreement Procedure (Administrative Guidelines). *1 Amended on June 30, *2 The BEPS Action14 Final Report: Element 2.1 Countries should publish rules, guidelines and procedures to access and use the MAP and take appropriate measures to make such information available to taxpayers. Countries should ensure that their MAP guidance is clear and easily accessible to the public.

2 Table of Contents 1. The Outline of the Mutual Agreement Procedure (MAP) Q1-1 What is a MAP? Q1-2 What is the purpose of MAP? Q1-3 Which provision of a tax treaty allows a MAP? Q1-4 How many MAP cases are there in Japan each year? Q1-5 With which jurisdiction is Japan able to provide a MAP? Q1-6 What is the international situation surrounding MAP? Q1-7 How long does it take to resolve a MAP case after its request is made? Q1-8 What are the issues a taxpayer should pay attention to for a MAP request? 2. Common issues of proceeding a MAP Q2-1 Who can request MAP assistance? Q2-2 What are the procedures for requesting MAP assistance? Q2-3 Can a taxpayer consult with the NTA before requesting MAP assistance? Q2-4 Is there a deadline for a pre-filing consultation? Q2-5 What kind of documents should a taxpayer prepare for a pre-filing consultation? Q2-6 Please provide the application form for requesting MAP assistance. Q2-7 What kind of materials should be attached to the application for a MAP? Q2-8 Does the NTA charge for a MAP request? Q2-9 Is there any deadline for a MAP request? Q2-10 Please provide the examples of the cases which a MAP request can be made. Q2-11 There is taxation which is not in accordance with the provisions of the applicable tax treaty and I am going to file an administrative appeal regarding such taxation in accordance with the domestic law of the country in which such taxation was made. Is it possible to request a MAP assistance in addition to this appeal? Q2-12 After submission of a MAP request, I have detected some deficiencies in the content. How can they be corrected? Q2-13 What procedure should be taken when a taxpayer would like to make a MAP request regarding an APA?

3 Q2-14 Q2-15 Q2-16 Q2-17 Q2-18 Q2-19 Q2-20 Are there any cases where a MAP consultation will not start even if a MAP request has been made? Our company decided to join a consolidated corporation group after requesting a MAP. What procedure should be followed in such a case? What kind of cooperation is necessary by the applicant in relation to a MAP? What kind of notification will be provided from the MAP Office, when both competent authorities are going to reach an agreement to resolve a case? What kind of procedure should a taxpayer follow after receipt of Notification That a Mutual Agreement Has been Reached from the MAP Office? Are there any cases where a mutual agreement will not be reached? There is no necessity for us to continue a MAP anymore. What kind of procedure should a taxpayer follow to withdraw a MAP request?

4 1. The Outline of the Mutual Agreement Procedure (MAP) Q1-1 What is a MAP? A MAP is a procedure between the competent authorities of Japan and treaty partners pursuant to the provisions of the tax treaties, to resolve disputes relating to cases, such as: 1 Taxation not in accordance with the provisions of tax treaties resulting from the actions of one or both of the contracting states Taxation Case ; 2 An advance pricing arrangement (APA) to determine an appropriate set of criteria (e.g. method, comparable and appropriate thereto) for determination of the transfer pricing for controlled transactions APA Case. (A basic MAP process flowchart Taxation Case ) Pre-filing consultation MAP request from a taxpayer MAP consultation between Japan and treaty partner Taxpayer's acceptance of contents of draft agreement Agreement reached between Japan and treaty partner Implementation of an adjustment based on the agreement * For further information, please see Commissioner s Directive on the Mutual Agreement Procedure (Administrative Guidelines) ( A basic MAP process flowchart APA Case Pre-filing consultation MAP request and APA request from a taxpayer Review of APA request by RTB MAP consultation between Japan and treaty partner Agreement reached between Japan and treaty partner RTB's notification to taxpayer of APA confirmation based on the agreement * For further information, please see Commissioner s Directive on the Operation of Transfer Pricing (Administrative Guidelines) 1

5 Q1-2 What is the purposes of MAP? One of the purposes of a tax treaty is to eliminate double taxation. To this end, a tax treaty provides rules. However, even if a treaty is concluded, international double taxations may occur by the actions of one or both of the contracting states that result in taxation not in accordance with provisions of an applicable tax treaty. A MAP is mainly aiming at eliminating such double taxation. Q1-3 Which provision of a tax treaty allows a MAP? Generally, there are provisions prescribing a MAP (MAP provisions) in a tax treaty. The MAP provisions allow competent authorities to implement a MAP. For instance, Article 25 contains the MAP provisions under the Convention between the Government of Japan and the Government of the United States of America for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income. (Note) Japan s tax treaties basically adopt the wording of provisions in the Model Tax Convention developed by the Organization for Economic Co-operation and Development (OECD) which includes the following MAP provisions: Article 25 of the OECD Model Tax Convention (MUTUAL AGREEMENT PROCEDURE) 1. Where a person considers that the actions of one or both of the Contracting States result or will result for him in taxation not in accordance with the provisions of this Convention, he may, irrespective of the remedies provided by the domestic law of those States, present his case to the competent authority of either Contracting State. The case must be presented within three years from the first notification of the action resulting in taxation not in accordance with the provisions of the Convention. 2. The competent authority shall endeavour, if the objection appears to it to be justified and if it is not itself able to arrive at a satisfactory solution, to resolve the case by mutual agreement with the competent authority of the other Contracting State, with a view to the avoidance of taxation which is not in accordance with the Convention. Any agreement reached shall be implemented notwithstanding any time limits in the domestic law of the Contracting States. 3. The competent authorities of the Contracting States shall endeavour to resolve by mutual agreement any difficulties or doubts arising as to the interpretation or 2

6 application of the Convention. They may also consult together for the elimination of double taxation in cases not provided for in the Convention. 4. The competent authorities of the Contracting States may communicate with each other directly, including through a joint commission consisting of themselves or their representatives, for the purpose of reaching an agreement in the sense of the preceding paragraphs. 5. Where, a) under paragraph 1, a person has presented a case to the competent authority of a Contracting State on the basis that the actions of one or both of the Contracting States have resulted for that person in taxation not in accordance with the provisions of this Convention, and b) the competent authorities are unable to reach an agreement to resolve that case pursuant to paragraph 2 within two years from the date when all the information required by the competent authorities in order to address the case has been provided to both competent authorities, any unresolved issues arising from the case shall be submitted to arbitration if the person so requests in writing. These unresolved issues shall not, however, be submitted to arbitration if a decision on these issues has already been rendered by a court or administrative tribunal of either State. Unless a person directly affected by the case does not accept the mutual agreement that implements the arbitration decision, that decision shall be binding on both Contracting States and shall be implemented notwithstanding any time limits in the domestic laws of these States. The competent authorities of the Contracting States shall by mutual agreement settle the mode of application of this paragraph. Q1-4 How many MAP cases are there in Japan each year? The number of MAP cases (the number of MAP requests made to Japan and proposals (opening letters) to initiate MAP consultation received from the competent authority of a treaty partner) in Japan is increasing in recent years. Please see the NTA s MAP report (MAP report). Q1-5 With which jurisdiction is Japan able to provide a MAP? Japan has more than 60 treaties which include MAP provisions. Please see Japan s Tax Conventions Including MAP Provisions for further information. 3

7 Q1-6 What is the international situation surrounding MAP? The number of MAP cases is increasing around the world in recent years. It is important to make efforts not only bilaterally but also multilaterally in order to deal with those increasing MAP cases effectively and efficiently. In the Base Erosion and Profit Shifting (BEPS) project launched by OECD in 2012, the measures are developed to strengthen the effectiveness of MAP mechanisms resolving a dispute relating to a tax treaty, in order to eliminate uncertainty of unintended double taxation and ensure predictabilities. The Action 14 final report published in September 2015 contains the minimum standard which each jurisdiction commits to implement. Jurisdictions compliance with the minimum standard is reviewed and monitored, in order to ensure its implementation of the minimum standard. This review and monitoring process is conducted by the Forum on Tax Administration MAP Forum (the FTA MAP Forum). It has been started since December The BEPS Action14 final report 1.3 Countries should commit to a timely resolution of MAP cases: Countries commit to seek to resolve MAP cases within an average timeframe of 24 months. Countries progress toward meeting that target will be periodically reviewed on the basis of the statistics prepared in accordance with the agreed reporting framework referred to in element Countries should commit to have their compliance with the minimum standard reviewed by their peers in the context of the FTA MAP Forum. 2.1 Countries should publish rules, guidelines and procedures to access and use the MAP and take appropriate measures to make such information available to taxpayers. Countries should ensure that their MAP guidance is clear and easily accessible to the public. * Action14: the 2015 Final Report (OECD website) Q1-7 How long does it take to resolve a MAP case after its request is made? The timeframe necessary for resolving a MAP case varies depending on the complexity of the case, the state of submission of documents by an applicant, the tax administrative system of a treaty partner, and so forth. Therefore it is not necessarily appropriate to provide a general timeframe. However, according to the actual statistics so far, it can be said that an average of two years is taken for resolving one case. 4

8 Please see the MAP report. The BEPS Action14 final report recommends that countries should commit to seek to resolve MAP cases within an average timeframe of 24 months. The NTA also targets the same timeframe for MAP cases. The BEPS Action14 final report: Element 1.3 Countries should commit to a timely resolution of MAP cases: Countries commit to seek to resolve MAP cases within an average timeframe of 24 months. Countries progress toward meeting that target will be periodically reviewed on the basis of the statistics prepared in accordance with the agreed reporting framework referred to in element 1.5. Q1-8 What are the issues a taxpayer should pay attention to for a MAP request? 1) The pre-filing consultation Whether a MAP case can be resolved in an effective and efficient manner depends on various elements, such as the particularity and complexity of the case, tax administrative systems of the treaty partner of the case, its MAP experiences, its domestic laws and the way of taxation, and its other domestic remedies. Those elements must be taken into account in proceeding a MAP and accordingly, the NTA strongly recommends that a taxpayer considering to submit a MAP request has a prefiling consultation before its submission. (See Q2-3 ~Q2-5) 2) Timely contact and submission of materials Please contact with the NTA officer in charge of a MAP case in a timely manner in order to keep the MAP process effectively and efficiently. The NTA officer in charge of a MAP or APA case may request the taxpayer who made the MAP request to submit materials necessary for determining an objection made by the taxpayer in the MAP request is justified, for proceeding the MAP consultation or for reviewing the APA request. In such a case, please submit those requested materials in a timely manner. The documents necessary for resolving MAP cases may be requested by the tax authority of a treaty partner through a foreign affiliated corporation. Please share those submitted materials with the NTA officer in charge. Please note that the failure of providing or updating significant information regarding a MAP case in a timely manner may create a serious impediment for resolving the MAP case. 5

9 3) Contents of the required documents There are cases (e.g. transfer pricing cases or APA cases) in which an applicant and its foreign affiliated corporation have to submit a MAP request with required materials to both Japanese and its treaty partner s tax authorities. In such cases, any serious inconsistency in explanation (including description in the MAP request and the required materials) or the significant timing gap of such explanation to both competent authorities may give rise to confusion in the MAP consultation and distract its efficient resolution. Especially, if a MAP request submitted to a treaty partner has significant difference in its contents from the one submitted to the NTA, this inconsistency may create a serious impediment for resolving the MAP case. 6

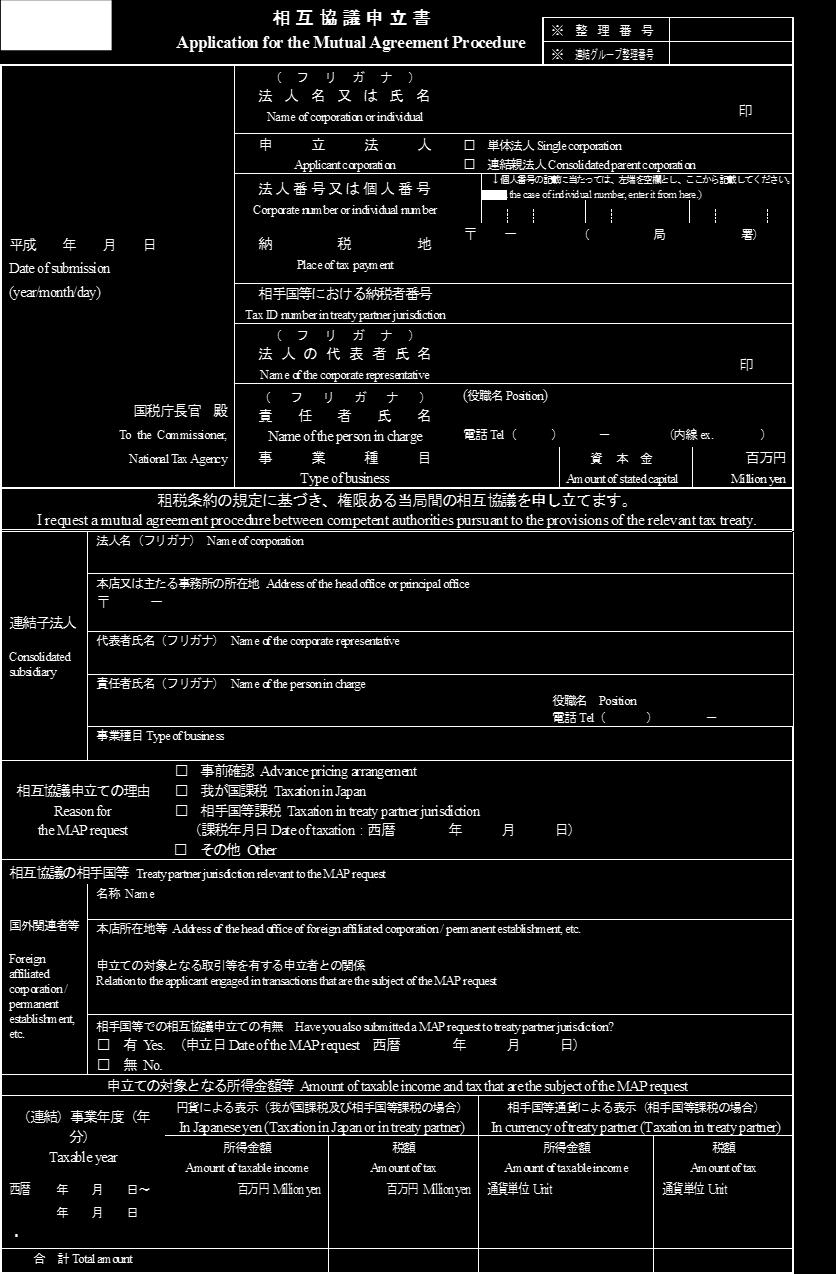

10 2. Common issues of proceeding a MAP Q2-1 Who can request MAP assistance? The following person can request MAP assistance pursuant to an applicable tax treaty, if such a person has been, or will be subject to taxation not in accordance with the provisions of a tax treaty: 1 Resident, 2 Domestic corporation, 3 Non-resident* and, 4 Foreign corporation*. * Non-resident and foreign corporation can make a request for MAP assistance only if such a request is allowed in an applicable tax treaty. A request for MAP assistance (MAP request) regarding an APA can be made by a taxpayer who made, or will make an APA request in accordance with the Commissioner s Directive on the Operation of Transfer Pricing. Q2-2 What are the procedures for requesting MAP assistance? A MAP request shall be made by submitting a The Application for the Mutual Agreement Procedure (Form1) with attachments (See Q2-7) to the Office of Mutual Agreement Procedures (the MAP Office). If the covered transactions of a MAP request is regarding a consolidated subsidiary, its consolidated parent corporation shall submit an application with attachments. (For submission) The MAP Office Contact details: 0081-(0) (ex. 3715) In the case of requesting MAP assistance for an APA, in addition to submitting a MAP request to the MAP office, an APA request shall be made to the Regional Taxation Bureau (RTB) relevant to the place of tax payment of a taxpayer in accordance with the Commissioner s Directives on the Operation regarding transfer pricing, etc. A pre-filing consultation for a MAP request is available. (See Q1-8) 7

11 (The Pre-filing Consultation) Q2-3 Can a taxpayer consult with the NTA before requesting MAP assistance? The MAP Office accepts a pre-filing consultation from a taxpayer who considers requesting MAP assistance, and the NTA strongly recommends usage of such consultation. An anonymous consultation through an agent is also available. A taxpayer who is willing to hold the consultation is required to make an appointment with the MAP Office (An appointment for the consultation regarding an APA can be also made through the relevant divisions in RTBs in charge). Q2-4 Is there a deadline for a pre-filing consultation? There is no deadline for a pre-filing consultation. However, the NTA recommends an earlier consultation when actions of one or both of the contracting states result or will result in taxation not in accordance with the provisions of tax treaties, in order to proceed the MAP consultation in an effective and efficient manner. It should be noted that some tax treaties have time limits for submitting a MAP request. Please be aware that there is a deadline for submitting an APA request in Japan. Q2-5 What kind of documents should a taxpayer prepare for a pre-filing consultation? Please prepare documents providing a summary of the taxation that is the subject of a MAP request, facts led to such taxation and the reason for the MAP request, in order to do the pre-filing consultation smoothly. As for a pre-filing consultation for an APA request, taxpayers are requested to prepare documents describing outlines of the covered transactions and the organization which conducts such transactions and materials explaining the capital relationships with its affiliated corporation. If the documents are in language other than Japanese, please attach Japanese translations of them. (The procedure of MAP request) Q2-6 Please provide the application form for requesting MAP assistance. Please see Application for the Mutual Agreement Procedure. 8

12 9

13 Q2-7 What kind of materials should be attached to the application for a MAP? Taxpayers requesting a MAP are required to attach the following materials to the application: 1 If the request is regarding taxation in Japan or in a treaty partner: (Cases where the taxation has occurred) A copy of the letter of the assessment that proves such taxation. A written description of the details of the facts related to the taxation and an outline of the position of the applicant or its foreign affiliated corporation to such taxation. (Case where the taxation has not yet occurred) A written description of the details of the facts which will result in taxation and an outline of the position of the applicant or its foreign affiliated corporation to such taxation. 2 If the request is regarding taxation in Japan or in a treaty partner, and the applicant or its foreign affiliated corporation has presented the case to an administrative tribunal or a court: Documents indicating that an administrative appeal or a lawsuit regarding the taxation has been filed, and an outline of the position of the applicant or its foreign affiliated corporation to such taxation. A copy of the complaint for an administrative appeal or a lawsuit. 3 If the request is regarding transfer pricing taxation in Japan or in a treaty partner: Documents describing the direct or indirect capital relationship or the de facto control relationship between the parties involved in the transactions that are the subject of the MAP request. 4 If the request is related to Article 13 of the Ministerial Ordinance (Income Tax Convention), and if an applicable tax treaty or intergovernmental agreements appended to the tax treaty provide items that should be considered in the MAP: Documents relating to those items. 5 If the applicant or its foreign affiliated corporation has made a MAP request to the competent authority of the treaty partner: A copy of documents explaining that fact. 6 Other documents that are relevant to the MAP If a MAP request is regarding an APA, it is not necessary for a taxpayer to submit the required attachments to the MAP application, as the APA request or the APA request 10

14 regarding consolidated companies, together with its attachments, submitted to the relevant RTB will be circulated to the MAP Office. If the attachments are in languages other than Japanese, please attach Japanese translations of them. The MAP Office may request additional materials not listed above necessary for determining the objection made by the taxpayer in the MAP request is justified or for proceeding MAP consultation. In that case, please submit those materials in a timely manner. Q2-8 Does the NTA charge for a MAP request? The MAP Office does not charge for a MAP request and a pre-filing consultation. Q2-9 Is there any deadline for a MAP request? In Article 25 of the OECD Model Tax Convention, there is the provision that stipulates a MAP request must be made within three years from the first notification of the action resulting in taxation not in accordance with the provisions of the Convention. Many tax treaties which Japan has concluded contain the similar provision. However, please check the provision of an applicable tax treaty, as the provision may differ treaty by treaty. Article 25 of the OECD Model Tax Convention (MUTUAL AGREEMENT PROCEDURE) 1. Where a person considers that the actions of one or both of the Contracting States result or will result for him in taxation not in accordance with the provisions of this Convention, he may, irrespective of the remedies provided by the domestic law of those States, present his case to the competent authority of either Contracting State. The case must be presented within three years from the first notification of the action resulting in taxation not in accordance with the provisions of the Convention. Q2-10 Please provide the examples of the cases which a MAP request can be made? For example, MAP requests can be made in the following cases: 1 Cases where a domestic corporation requests MAP assistance on the grounds that the corporation has been, or will be subject to transfer pricing taxation in Japan 11

15 or in a treaty partner regarding transactions between the domestic corporation and its foreign affiliated corporation. 2 Cases where a domestic corporation requests MAP assistance with regard to the transactions between the domestic corporation and its foreign affiliated corporation, with a request for an APA in accordance with the Commissioner s Directive on the Operation of Transfer Pricing. 3 Cases where a resident or a domestic corporation requests MAP assistance on the grounds that the resident or the domestic corporation has been, or will be subject to taxation not in accordance with the provisions of the applicable tax treaty regarding the presence of its permanent establishment in a treaty partner, or regarding the amount of profit attributable to the permanent establishment. 4 Cases where a domestic corporation requests MAP assistance with regard to its APA request made in accordance with the Commissioner s Directive on the Operation of Auditing, etc. for Income Attributable to Permanent Establishments. 5 Cases where a resident or a domestic corporation requests MAP assistance on the grounds that the resident or the domestic corporation has been, or will be subject to taxation not in accordance with the provisions of the applicable tax treaty regarding income tax withheld in the treaty partner. 6 Cases where a non-resident who has Japanese nationality requests MAP assistance on the grounds that the person has been, or will be subject to more burdensome taxation or requirements in a treaty partner than the taxation or requirements applied to the nationals of the treaty partner. 7 Cases where a Japanese resident individual who is also regarded as a resident of a treaty partner under laws of the treaty partner requests MAP assistance in order to determine the nation of which the individual is to be deemed to be a resident under the applicable tax treaty. With regard to 1 or 3 above, a taxpayer may request MAP assistance in the cases of bona fide taxpayer-initiated foreign adjustments * 1 or multiple MAP cases* 2. *1 Cases regarding taxpayer-initiated adjustments permitted under the domestic laws of a treaty partner which allow a taxpayer under appropriate circumstances to amend a previously-filed tax return to adjust (i) the price for a transaction between associated enterprises or (ii) the profits attributable to a permanent establishment. *2 Cases regarding multi-jurisdictional tax disputes. A taxpayer may request MAP assistance in cases in which there is a disagreement between the taxpayer and the tax authorities making adjustment as to whether the conditions for the application of a treaty anti-abuse provision have been met or as to 12

16 whether the application of a domestic law anti-abuse provision is in conflict with the provision of a treaty. Q2-11 There is taxation which is not in accordance with the provisions of the applicable tax treaty and I am going to file an administrative appeal regarding such taxation in accordance with the domestic law of the country in which such taxation was made. Is it possible to request a MAP assistance in addition to this appeal? Taxpayers may request MAP assistance even if they have presented their cases to an administrative tribunal or court. In this case, in addition to the other necessary attachments, the taxpayers are required to submit the documents indicating that an administrative appeal or a lawsuit has been filed, and an outline of the position of the applicant or its foreign affiliated corporation to the case, together with a copy of the complaint for the administrative appeal or the lawsuit. A decision on these issues has already been rendered by an administrative tribunal or court in Japan, the MAP office will follow those decisions. Q2-12 After submission of a MAP request, I have detected some deficiencies in the content. How can they be corrected? Please contact the MAP Office without delay if the applicant detects an error or would like to make any significant changes in the application, its attachments or any other documents. If the MAP Office detects deficiencies in the content, the MAP Office will request the applicant to correct them. If the applicant will not cooperate to respond to the request, the MAP Office will inform the tax administration of the treaty partner that the NTA will not initiate the MAP consultation. Q2-13 What procedure should be taken when a taxpayer would like to make a MAP request regarding an APA? The procedure of a MAP request regarding an APA is the same as the other MAP cases. However, the APA request prescribed in the Commissioner s Directive on the Operation of Transfer Pricing (Administrative Guidelines) shall be made before or together with the MAP request. 13

17 The MAP process will terminate in the case where the taxpayer doesn t submit the application for APA or withdraws such application, as it is not justifiable to start or continue the MAP consultation in such case. (The procedure after a MAP request) Q2-14 Are there any cases where a MAP consultation will not start even if a MAP request has been made? After an objection made by a taxpayer is justified (If a MAP request is regarding an APA, after being informed of the completion of the APA review by the RTB concerned), the MAP Office will propose the initiation of the MAP consultation to the competent authority of a treaty partner. However, such proposal will not be made in the following cases: 1 Cases where an applicant does not correct deficiencies in the contents of its Application for the Mutual Agreement Procedure or attachments despite the MAP Office s request. 2 Cases where an applicant does not make an APA request in accordance with the provisions of the Commissioner s Directive on the Operation of Transfer Pricing despite the fact that the MAP request is regarding an APA (including the case where the applicant has withdrawn the request). 3 Cases where an applicant doesn t submit the documents necessary for determining whether the objection made by the applicant in the MAP request is justified despite the MAP Office s request. 4 Cases where the objection made by an applicant in a MAP request is not justified (If the MAP request is regarding an APA, the case where the request is not able to be the subject of the APA prescribed in the Commissioner s Directive on the Operation of Transfer Pricing). Q2-15 Our company decided to join a consolidated corporation group after requesting a MAP. What procedure should be followed in such a case? You are required to submit Notification of Becoming or Joining a Consolidated Corporation Group, etc. and Continuing a Request for a Mutual Agreement Procedure or Notification of Seceding from a Consolidated Corporation Group, etc. and Continuing a Request for a Mutual Agreement Procedure to the MAP Office without delay; 14

18 1 in the cases where a corporation becomes a consolidated corporation after submitting the application for a MAP, 2 in the cases where a consolidated corporation engaged in transactions that are the subject of a MAP request joins another consolidated corporation group, 3 in the cases where a consolidated corporation engaged in transactions that are the subject of a MAP request becomes a corporation other than consolidated corporations. In the case of 1 or 2 above, the corporation which becomes a consolidated parent corporation shall submit the notification to the MAP Office. In the case of 3 above, the corporation which engages transactions which are the subject of the MAP request shall submit the notification to the MAP Office. Q2-16 What kind of cooperation is necessary by the applicant in relation to a MAP? The MAP Office may request additional materials necessary for determining an objection made by a taxpayer in a MAP request is justified or for proceeding a MAP consultation, or an APA review. In those cases, please submit the requested materials in a timely manner. The documents necessary for resolving MAP cases may be requested by the tax administration of the treaty partner through foreign affiliated corporation. Taxpayers are requested to share those submitted materials with the NTA officer in charge. In addition, in the case where you submit them to the tax administration, please note that consistent explanation should be provided to both competent authorities. Q2-17 What kind of notification will be provided from the MAP Office, when both competent authorities are going to reach an agreement to resolve a case? Before reaching an agreement to resolve a case, the MAP Office will propose the draft of the agreement in writing to the applicant of the case, and ask whether the applicant accepts the proposal. After the applicant s acceptance is confirmed, the MAP Office will formally reach the agreement with the competent authority of the treaty partner. If a mutual agreement has been reached on a case, the MAP Office will notify the date and contents of the agreement to the applicant of the case by sending Notification That a Mutual Agreement Has Been Reached. 15

19 Q2-18 What kind of procedure should a taxpayer follow after receipt of Notification That a Mutual Agreement Has been Reached from the MAP Office? After a mutual agreement is reached on a case, the mutual agreement will be implemented by the following procedures: (Taxation case other than withholding taxation case) In cases where a mutual agreement has been reached on a case regarding taxation initiated by Japan other than withholding taxation, and resulted in reducing the amount of income and/or tax of the applicant s filed tax return, the Japanese tax authority will make a correction to the applicant s filed tax return pursuant to Article 26 of the Act on General Rules for National Taxes. Accordingly, the applicant does not have to make a request for reassessment of its filed tax return. In cases where a mutual agreement has been reached on a case regarding taxation initiated by a treaty partner other than withholding taxation, and resulted in reducing the amount of income and/or tax of the applicant s filed tax return, the applicant has to make a request for reassessment of its filed tax return which is prescribed in paragraph 1 or 2 of Article 23 of the Act on General Rules for National Taxes, within 2 months from the date of the mutual agreement so that the mutual agreement will be reflected in its return: pursuant to Article 7 of the Act on Special Provisions regarding the Application of Tax Treaties. (Withholding taxation case) In cases where a mutual agreement has been reached on a case regarding withholding taxation and resulted in refunding all or a part of the amount of income tax and special income tax for reconstruction withheld by a withholding tax agent in Japan voluntarily, that withholding tax agent will be required to submit a Request for a Refund of Overpaid Withholding Income Taxes and Special Income Tax for Reconstruction to the Japanese tax authority without delay. In cases where a mutual agreement has been reached on a case regarding withholding taxation and resulted in refunding all or a part of the amount of income tax and special income tax for reconstruction withheld by a withholding tax agent in Japan based on a notification requiring payment of such taxes, the Japanese tax authority will refund such an amount to the withholding tax agent. Accordingly, that withholding tax agent need not to submit a Request for a Refund of Overpaid Withholding Income Taxes and Special Income Tax for Reconstruction. In cases where a mutual agreement has been reached on a case regarding withholding taxation and resulted in refunding the amount of income tax withheld by a 16

20 withholding tax agent in a treaty partner from the payment which is received by a resident or domestic corporation in Japan from a resident or corporation in the treaty partner, the applicant must request such refund in accordance with the relevant procedures in the treaty partner. (APA case) In cases where a mutual agreement has been reached on an APA case, an applicant has to revise its filed APA request to comply with the mutual agreement, if necessary. Based on the revised APA request, the fact that the APA request is confirmed will be notified in writing to the applicant by the District Director of the Tax Office relevant to the place of tax payment of the applicant. In cases where the amount of income in the applicant s filed tax return for an APA year has proved to be understated for the reason that the price for the covered transactions in the APA request has not been in accordance with the mutual agreement, the applicant has to voluntarily file an amended tax return to correct such understatement without delay. Such an amended tax return filed before the Japanese tax authority points out such understatement will not be treated as the amended tax return which is filed foreknowing that correction would be made otherwise as prescribed in paragraph 1 and 5 of Article 65 of the Act on General Rules for National Taxes. Moreover, in cases where an amended tax return which is voluntarily filed to comply with the APA is filed after the Japanese tax authority notifies the applicant of the initiation of an audit, such an amended tax return will be treated as the tax return filed before receiving a notification regarding the initiation of an audit as prescribed paragraph 5 of Article 65 of the Act on General Rules for National Taxes. Accordingly, any additional tax for understatement will not be imposed on such an amended tax return*. * This treatment only applies to the additional tax with regard to correction made in the amended tax return to comply with a mutual agreement on an APA case. Thus, even in such a case, the applicant has to pay the increased amount of tax in the amended tax return, and an additional tax may be imposed on any amount of tax increased by other reasons than complying with the mutual agreement on the APA case. In cases where the amount of income in the applicant s filed tax return for an APA year has proved to be overstated for the reason that the price for the covered transactions in the APA request has not been in accordance with the mutual agreement, the applicant has to make a request for reassessment of its filed tax return to comply with the mutual agreement within 2 months from the date of the mutual agreement pursuant to paragraphs 1 or 2 of Article 23 of the Act on General Rules for 17

21 National Taxes. If a mutual agreement on a case results in changing an amount of income tax or corporation tax to be paid, an amount of the local taxes to be paid will also be changed accordingly. For the procedures to be taken for such an amendment, please ask the tax authority for the local tax relevant to your place of tax payment. Q2-19 Are there any cases where a mutual agreement will not be reached. If the objection made by a taxpayer in a MAP request is justified, the competent authorities of Japan and a treaty partner should endeavor to resolve the case by mutual agreement under the provisions of a tax treaty. However, the MAP Office will propose termination of a MAP consultation to the competent authority of a treaty partner if there is no appropriate reason for continuing the MAP consultation; for instance, if it has found that the issue regarding a MAP request is not the subject of the MAP provisions under an applicable tax treaty after the MAP consultation has started. In addition, the termination of a MAP consultation will be proposed to the competent authority of a treaty partner after deliberate consideration: 1 where an applicant does not cooperate in providing the documents necessary for a MAP consultation; 2 where an applicant does not accept the draft of an agreement proposed by the MAP Office before both competent authorities reach an agreement to resolve a case; 3 where significant inconsistency between the contents explained by an applicant or its foreign affiliated corporation for each competent authority (including description in a MAP request or required materials) create a serious influence on a MAP consultation; 4 where continuation of a MAP consultation will reach no appropriate solution. If the competent authority of a treaty partner accepts termination of a MAP consultation proposed by the MAP Office, the MAP will be terminated and the MAP Office will notify the applicant of that fact by sending a Notification That a Mutual Agreement Procedure Has been Terminated. Please note that the MAP will be terminated also in cases where the competent authority of a treaty partner proposes termination of a MAP consultation to the MAP Office and the MAP Office accepts such a proposal. 18

22 Q2-20 There is no necessity for us to continue a MAP anymore. What kind of procedure should a taxpayer follow to withdraw a MAP request? After submitting a MAP request, an applicant can withdraw a MAP request any time before receiving a Notification That the Initiation of a Mutual Agreement Procedure Consultation Will not be Proposed, a Notification That a Mutual Agreement Has been Reached or a Notification That a Mutual Agreement Procedure Has been Terminated. In such case, submit Notification of the Withdrawal of a Request for a Mutual Agreement Procedure to the MAP Office. 19

Commissioner s Directive on the Mutual Agreement Procedure (Administrative Guidelines)

") This document is a translation of the original Japanese-language Directive. The Japanese original is the official text. Document ID: Office of Mutual Agreement Procedures 8-7 International Operations Division

This document is a translation of the original Japanese-language Directive. The Japanese original is the official text. Document ID: Office of Mutual Agreement Procedures 8-7 International Operations Division

Maldives Dispute Resolution Profile. (Last updated: 29 November 2018) General Information

General Information") 1 Maldives Dispute Resolution Profile (Last updated: 29 November 2018) General Information Maldives tax treaties are available at: https://www.mira.gov.mv/tax_treaties.aspx MAP requests should be made

1 Maldives Dispute Resolution Profile (Last updated: 29 November 2018) General Information Maldives tax treaties are available at: https://www.mira.gov.mv/tax_treaties.aspx MAP requests should be made

Republic of Korea Dispute Resolution Profile. (Last updated: 30 August 2017) General Information

General Information") 1 Republic of Korea Dispute Resolution Profile (Last updated: 30 August 2017) General Information Korea tax treaties are available at: www.nts.go.kr/eng/ [Please see Resources-Tax Law/Treaty] MAP request

1 Republic of Korea Dispute Resolution Profile (Last updated: 30 August 2017) General Information Korea tax treaties are available at: www.nts.go.kr/eng/ [Please see Resources-Tax Law/Treaty] MAP request

SOME RELEVANT TREATY ISSUES

SOME RELEVANT TREATY ISSUES Rahul Charkha August 29, 2018 CONTENT Sr. No. Topic 1 Glossary 2 Most Favoured Nation Principle 3 Tax Credit 4 Mutual Agreement Procedures 5 Annexure - 1 6 Our Team GLOSSARY

SOME RELEVANT TREATY ISSUES Rahul Charkha August 29, 2018 CONTENT Sr. No. Topic 1 Glossary 2 Most Favoured Nation Principle 3 Tax Credit 4 Mutual Agreement Procedures 5 Annexure - 1 6 Our Team GLOSSARY

Thailand Dispute Resolution Profile. (Last updated: 18 September 2017) General Information

General Information") Thailand Dispute Resolution Profile (Last updated: 18 September 2017) General Information Thailand s tax treaties are available at: http://www.rd.go.th/publish/766.0.html MAP request should be made to:

Thailand Dispute Resolution Profile (Last updated: 18 September 2017) General Information Thailand s tax treaties are available at: http://www.rd.go.th/publish/766.0.html MAP request should be made to:

St. Kitts and Nevis Dispute Resolution Profile. (Last updated: 09 May 2018) General Information

General Information") 1 St. Kitts and Nevis Dispute Resolution Profile (Last updated: 09 May 2018) General Information St. Kitts and Nevis tax treaties are available at: http://www.mof.govt.kn MAP requests should be made to:

1 St. Kitts and Nevis Dispute Resolution Profile (Last updated: 09 May 2018) General Information St. Kitts and Nevis tax treaties are available at: http://www.mof.govt.kn MAP requests should be made to:

Korea Dispute Resolution Profile. (Last updated: 02 April 2018) General Information

General Information") 1 Korea Dispute Resolution Profile (Last updated: 02 April 2018) General Information Korea tax treaties are available at: www.nts.go.kr/eng: Please see ResourcesTax Law/Treaty MAP request should be made

1 Korea Dispute Resolution Profile (Last updated: 02 April 2018) General Information Korea tax treaties are available at: www.nts.go.kr/eng: Please see ResourcesTax Law/Treaty MAP request should be made

Paraguay Dispute Resolution Profile. (Last updated: 27 June 2017)

") 1 Paraguay Dispute Resolution Profile (Last updated: 27 June 2017) General Information Paraguay tax treaties are available at: Under request at the Ministry of Foreign Affairs. MAP request should be made

1 Paraguay Dispute Resolution Profile (Last updated: 27 June 2017) General Information Paraguay tax treaties are available at: Under request at the Ministry of Foreign Affairs. MAP request should be made

Guide for mutual agreement procedure pursuant to tax treaties (MAP) Contents

Contents") Guide for mutual agreement procedure pursuant to tax treaties (MAP) Contents 1 General information about mutual agreement procedures (MAP)... 2 2 Access to MAP... 2 3 Where shall a taxpayer submit a MAP

Guide for mutual agreement procedure pursuant to tax treaties (MAP) Contents 1 General information about mutual agreement procedures (MAP)... 2 2 Access to MAP... 2 3 Where shall a taxpayer submit a MAP

Thailand Dispute Resolution Profile. (Last updated: 12 June 2018) General Information

General Information") 1 Thailand Dispute Resolution Profile (Last updated: 12 June 2018) General Information Thailand tax treaties are available at: http://www.rd.go.th/publish/766.0.html MAP requests should be made to: Mr.

1 Thailand Dispute Resolution Profile (Last updated: 12 June 2018) General Information Thailand tax treaties are available at: http://www.rd.go.th/publish/766.0.html MAP requests should be made to: Mr.

OECD releases Luxembourg peer review report on implementation of Action 14 Minimum Standards

22 December 2017 Global Tax Alert OECD releases Luxembourg peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY

22 December 2017 Global Tax Alert OECD releases Luxembourg peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY

Switzerland Dispute Resolution Profile. (Last updated: 24 August 2018)

") 1 Switzerland Dispute Resolution Profile (Last updated: 24 August 2018) General Information Switzerland tax treaties are available at: https://www.admin.ch/opc/fr/classifiedcompilation/0.67.html#0.67 (in

1 Switzerland Dispute Resolution Profile (Last updated: 24 August 2018) General Information Switzerland tax treaties are available at: https://www.admin.ch/opc/fr/classifiedcompilation/0.67.html#0.67 (in

Bulgaria Dispute Resolution Profile. (Last updated: 16 December 2016)

") 1 Bulgaria Dispute Resolution Profile (Last updated: 16 December 2016) General Information Bulgaria tax treaties are available at: http://nra.bg/page?id=427 (Bulgarian) http://www.nap.bg/en/page?id=530

1 Bulgaria Dispute Resolution Profile (Last updated: 16 December 2016) General Information Bulgaria tax treaties are available at: http://nra.bg/page?id=427 (Bulgarian) http://www.nap.bg/en/page?id=530

Switzerland Dispute Resolution Profile. (Last updated: 1 September 2016) General Information

General Information") 1 Switzerland Dispute Resolution Profile (Last updated: 1 September 2016) General Information Switzerland tax treaties are available at: https://www.admin.ch/opc/fr/classifiedcompilation/0.67.html#0.67

1 Switzerland Dispute Resolution Profile (Last updated: 1 September 2016) General Information Switzerland tax treaties are available at: https://www.admin.ch/opc/fr/classifiedcompilation/0.67.html#0.67

Austria Dispute Resolution Profile. (Last updated: 31 October 2017) General Information

General Information") 1 Austria Dispute Resolution Profile (Last updated: 31 October 2017) General Information Austria s tax treaties are available at: https://english.bmf.gv.at/taxation/theaustriantaxtreatynetwork.html MAP

1 Austria Dispute Resolution Profile (Last updated: 31 October 2017) General Information Austria s tax treaties are available at: https://english.bmf.gv.at/taxation/theaustriantaxtreatynetwork.html MAP

Macau (China) Dispute Resolution Profile. (Last updated: 29 June 2017) General Information

Dispute Resolution Profile. (Last updated: 29 June 2017) General Information") 1 Macau (China) Dispute Resolution Profile (Last updated: 29 June 2017) General Information Macau (China) tax treaties are available at: http://www.dsf.gov.mo/download/tax/e_prb_tax_content.html http://www.dsf.gov.mo/download/tax/p_lei_106_99_m.html

1 Macau (China) Dispute Resolution Profile (Last updated: 29 June 2017) General Information Macau (China) tax treaties are available at: http://www.dsf.gov.mo/download/tax/e_prb_tax_content.html http://www.dsf.gov.mo/download/tax/p_lei_106_99_m.html

OECD releases France peer review report on implementation of Action 14 Minimum Standards

26 December 2017 Global Tax Alert OECD releases France peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY Global

26 December 2017 Global Tax Alert OECD releases France peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY Global

OECD releases Italy peer review report on implementation of Action 14 Minimum Standards

22 December 2017 Global Tax Alert OECD releases Italy peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY Global

22 December 2017 Global Tax Alert OECD releases Italy peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY Global

OECD releases Switzerland s peer review report on implementation of BEPS Action 14 minimum standards

19 October 2017 Global Tax Alert OECD releases Switzerland s peer review report on implementation of BEPS Action 14 minimum standards EY Global Tax Alert Library Access both online and pdf versions of

19 October 2017 Global Tax Alert OECD releases Switzerland s peer review report on implementation of BEPS Action 14 minimum standards EY Global Tax Alert Library Access both online and pdf versions of

SP1/11 Transfer pricing, mutual agreement procedure and arbitration

SP1/11 Transfer pricing, mutual agreement procedure and arbitration 1. This statement describes the UK s practice in relation to methods for reducing or preventing double taxation and supersedes Tax Bulletins

SP1/11 Transfer pricing, mutual agreement procedure and arbitration 1. This statement describes the UK s practice in relation to methods for reducing or preventing double taxation and supersedes Tax Bulletins

BEPS Action 14: Making dispute resolution mechanisms more effective

BEPS Action 14: Making dispute resolution mechanisms more effective The Panel Achim Pross, Head, International Cooperation and Tax Administration Division, OECD Doug O Donnell, LB&I Commissioner, IRS Martin

BEPS Action 14: Making dispute resolution mechanisms more effective The Panel Achim Pross, Head, International Cooperation and Tax Administration Division, OECD Doug O Donnell, LB&I Commissioner, IRS Martin

OECD releases Germany peer review report on implementation of Action 14 Minimum Standards

21 December 2017 Global Tax Alert OECD releases Germany peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY Global

21 December 2017 Global Tax Alert OECD releases Germany peer review report on implementation of Action 14 Minimum Standards EY Global Tax Alert Library Access both online and pdf versions of all EY Global

Bilateral Advance Pricing Agreement Guidelines

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

September 2016 Bilateral Advance Pricing Agreement Guidelines Page 1 Contents PART 1 INTRODUCTION...5 PART 2 BILATERAL APA PROGRAMME OVERVIEW...5 PART 3 PURPOSE AND SCOPE OF APA...7 What is an APA?...7

Georgia Dispute Resolution Profile. (Last updated: 16 December 2016)

") 1 Georgia Dispute Resolution Profile (Last updated: 16 December 2016) General Information Georgia tax treaties are available at: http://mof.gov.ge/en/4681 MAP request should be made to: Mr. Giorgi Pataridze

1 Georgia Dispute Resolution Profile (Last updated: 16 December 2016) General Information Georgia tax treaties are available at: http://mof.gov.ge/en/4681 MAP request should be made to: Mr. Giorgi Pataridze

Saudi Arabia Dispute Resolution Profile. (Last updated: 25 January 2017)

") 1 Saudi Arabia Dispute Resolution Profile (Last updated: 25 January 2017) General Information Saudi Arabia s tax treaties are available at: www.gatz.gov.sa MAP request should be made to: Tareq AlSadhan

1 Saudi Arabia Dispute Resolution Profile (Last updated: 25 January 2017) General Information Saudi Arabia s tax treaties are available at: www.gatz.gov.sa MAP request should be made to: Tareq AlSadhan

APA Program Report. National Tax Agency. Office of Mutual Agreement Procedures. September 2003

APA Program Report September 2003 National Tax Agency Office of Mutual Agreement Procedures Contents Foreword 1 What is Advance Pricing Arrangement (APA)? 2 Background of APA in Japan and the World 3 APA

APA Program Report September 2003 National Tax Agency Office of Mutual Agreement Procedures Contents Foreword 1 What is Advance Pricing Arrangement (APA)? 2 Background of APA in Japan and the World 3 APA

The Independent State of Papua New Guinea Dispute Resolution Profile. (Last updated: )

") 1 The Independent State of Papua New Guinea Dispute Resolution Profile (Last updated: 16.10.2017) General Information Papua New Guinea tax treaties are available: On request by emailing irclegal@irc.gov.pg.

1 The Independent State of Papua New Guinea Dispute Resolution Profile (Last updated: 16.10.2017) General Information Papua New Guinea tax treaties are available: On request by emailing irclegal@irc.gov.pg.

Kenya Dispute Resolution Profile. (Last updated: 15 February 2018) General Information

General Information") 1 Kenya Dispute Resolution Profile (Last updated: 15 February 2018) General Information Kenya s tax treaties are available at: http://www.treasury.go.ke/avoidanceofdoubletaxation.html MAP request should

1 Kenya Dispute Resolution Profile (Last updated: 15 February 2018) General Information Kenya s tax treaties are available at: http://www.treasury.go.ke/avoidanceofdoubletaxation.html MAP request should

Mauritius Dispute Resolution Profile. (Last updated: 19 April 2017) General Information

General Information") 1 Mauritius Dispute Resolution Profile (Last updated: 19 April 2017) General Information Mauritius tax treaties are available at: http://www.mra.mu/index.php/taxes-duties/double-taxation-agreements MAP

1 Mauritius Dispute Resolution Profile (Last updated: 19 April 2017) General Information Mauritius tax treaties are available at: http://www.mra.mu/index.php/taxes-duties/double-taxation-agreements MAP

Slovenia Dispute Resolution Profile. (Last updated: 01 May 2018) General Information

General Information") 1 Slovenia Dispute Resolution Profile (Last updated: 01 May 2018) General Information Slovenia tax treaties are available at: The list of tax treaties, including the number of relevant Official Gazette

1 Slovenia Dispute Resolution Profile (Last updated: 01 May 2018) General Information Slovenia tax treaties are available at: The list of tax treaties, including the number of relevant Official Gazette

BEPS Action 14: Make Dispute Resolution Mechanisms More Effective

BEPS Action 14: Make Dispute Resolution Mechanisms More Effective The Organization for Economic Cooperation and Development on December 18, 2014, released a public discussion draft pursuant to Action 14,

BEPS Action 14: Make Dispute Resolution Mechanisms More Effective The Organization for Economic Cooperation and Development on December 18, 2014, released a public discussion draft pursuant to Action 14,

Photo credits: Cover Rawpixel.com - Shutterstock.com

Photo credits: Cover Rawpixel.com - Shutterstock.com TABLE OF CONTENTS 5 Table of contents Abbreviations and acronyms... 7 Introduction... 9 Part A Preventing Disputes... 11 [BP.1] Implement bilateral

Photo credits: Cover Rawpixel.com - Shutterstock.com TABLE OF CONTENTS 5 Table of contents Abbreviations and acronyms... 7 Introduction... 9 Part A Preventing Disputes... 11 [BP.1] Implement bilateral

The Government of the Kingdom of the Netherlands. And. The Government of the Isle of Man

Agreement between the Kingdom of the Netherlands and the Isle of Man on the access to mutual agreements procedures in connection with the adjustment of profits of associated enterprises and the application

Agreement between the Kingdom of the Netherlands and the Isle of Man on the access to mutual agreements procedures in connection with the adjustment of profits of associated enterprises and the application

Photo credits: Cover Rawpixel.com - Shutterstock.com

Photo credits: Cover Rawpixel.com - Shutterstock.com TABLE OF CONTENTS 5 Table of contents Abbreviations and acronyms... 7 Introduction... 9 Part A Preventing Disputes... 11 [BP.1] Implement bilateral

Photo credits: Cover Rawpixel.com - Shutterstock.com TABLE OF CONTENTS 5 Table of contents Abbreviations and acronyms... 7 Introduction... 9 Part A Preventing Disputes... 11 [BP.1] Implement bilateral

Dispute Resolution: the Mutual Agreement Procedure

Papers on Selected Topics in Administration of Tax Treaties for Developing Countries Paper No. 8-A May 2013 Dispute Resolution: the Mutual Agreement Procedure Hugh Ault Professor Emeritus of Tax Law, Boston

Papers on Selected Topics in Administration of Tax Treaties for Developing Countries Paper No. 8-A May 2013 Dispute Resolution: the Mutual Agreement Procedure Hugh Ault Professor Emeritus of Tax Law, Boston

OECD releases Singapore s peer review report on implementation of Action 14 minimum standard

Transfer Pricing Alert Issue 18 04 April 2018 OECD releases Singapore s peer review report on implementation of Action 14 minimum standard Executive summary On 12 March 2018, the Organisation for Economic

Transfer Pricing Alert Issue 18 04 April 2018 OECD releases Singapore s peer review report on implementation of Action 14 minimum standard Executive summary On 12 March 2018, the Organisation for Economic

Global Transfer Pricing Review

GLOBAL TRANSFER PRICING SERVICES Global Transfer Pricing Review Czech United Republic Kingdom kpmg.com/gtps TAX 2 Global Transfer Pricing Review United Kingdom KPMG observation HMRC supports the Organisation

GLOBAL TRANSFER PRICING SERVICES Global Transfer Pricing Review Czech United Republic Kingdom kpmg.com/gtps TAX 2 Global Transfer Pricing Review United Kingdom KPMG observation HMRC supports the Organisation

Argentina Dispute Resolution Profile. (Last updated: 1 September 2016) General Information

General Information") 1 Argentina Dispute Resolution Profile (Last updated: 1 September 2016) General Information Argentina s tax treaties are available at: www.afip.gov.ar/institucional/acuerdos.asp MAP request should be made

1 Argentina Dispute Resolution Profile (Last updated: 1 September 2016) General Information Argentina s tax treaties are available at: www.afip.gov.ar/institucional/acuerdos.asp MAP request should be made

Egypt Dispute Resolution Profile. (Last updated: 16 October 2018) General Information

General Information") 1 Egypt Dispute Resolution Profile (Last updated: 16 October 2018) General Information Egypt tax treaties are available at: http://www.incometax.gov.eg/treaties.asp MAP requests should be made to: Ms.

1 Egypt Dispute Resolution Profile (Last updated: 16 October 2018) General Information Egypt tax treaties are available at: http://www.incometax.gov.eg/treaties.asp MAP requests should be made to: Ms.

Curaçao (submitted by the Kingdom of the Netherlands on behalf of Curaçao)

") Curaçao (submitted by the Kingdom of the Netherlands on behalf of Curaçao) Status of List of s and Notifications This document contains a provisional list of expected reservations and notifications to

Curaçao (submitted by the Kingdom of the Netherlands on behalf of Curaçao) Status of List of s and Notifications This document contains a provisional list of expected reservations and notifications to

THE JAPAN COMMERCIAL ARBITRATION ASSOCIATION COMMERCIAL ARBITRATION RULES. CHAPTER General Provisions

THE JAPAN COMMERCIAL ARBITRATION ASSOCIATION COMMERCIAL ARBITRATION RULES As Amended and Effective on January 1, 2008 CHAPTER General Provisions Rule 1. Purpose The purpose of these Rules shall be to provide

THE JAPAN COMMERCIAL ARBITRATION ASSOCIATION COMMERCIAL ARBITRATION RULES As Amended and Effective on January 1, 2008 CHAPTER General Provisions Rule 1. Purpose The purpose of these Rules shall be to provide

Brazil Dispute Resolution Profile. (Last updated: 13 February 2019) General Information

General Information") 1 Brazil Dispute Resolution Profile (Last updated: 13 February 2019) General Information Brazil s tax treaties are available at: http://idg.receita.fazenda.gov.br/acesso-rapido/legislacao/acordos-internacionais/acordos-para-evitar-a-dupla-tributacao/acordospara-evitar-a-dupla-tributacao

1 Brazil Dispute Resolution Profile (Last updated: 13 February 2019) General Information Brazil s tax treaties are available at: http://idg.receita.fazenda.gov.br/acesso-rapido/legislacao/acordos-internacionais/acordos-para-evitar-a-dupla-tributacao/acordospara-evitar-a-dupla-tributacao

NOTE ON DISPUTE RESOLUTION: PROPOSED NEW ARTICLE 25 COMMENTARY

Distr.: General 11 October 2011 Original: English Committee of Experts on International Cooperation in Tax Matters Seventh session Geneva, 24-28 October 2011 Item 5 (b) of the provisional agenda Dispute

Distr.: General 11 October 2011 Original: English Committee of Experts on International Cooperation in Tax Matters Seventh session Geneva, 24-28 October 2011 Item 5 (b) of the provisional agenda Dispute

KPMG Japan tax newsletter

Japan tax newsletter KPMG Tax Corporation 24 December 2015 KPMG Japan tax newsletter Amended Japan-Germany Tax Treaty 1. Preamble... 2 2. Hybrid Entities (Article 1)... 2 3. Business Profits (Article 7)...

Japan tax newsletter KPMG Tax Corporation 24 December 2015 KPMG Japan tax newsletter Amended Japan-Germany Tax Treaty 1. Preamble... 2 2. Hybrid Entities (Article 1)... 2 3. Business Profits (Article 7)...

IFA MUNICH. Strategic Approaches to Global Transfer Pricing Risk: the use of tax treaties through APA and MAP. 18 January 2018

IFA MUNICH Strategic Approaches to Global Transfer Pricing Risk: the use of tax treaties through APA and MAP 18 January 2018 www.dlapiper.com 86879547 18 January 2018 0 Agenda Current Environment / Current

IFA MUNICH Strategic Approaches to Global Transfer Pricing Risk: the use of tax treaties through APA and MAP 18 January 2018 www.dlapiper.com 86879547 18 January 2018 0 Agenda Current Environment / Current

Norway Dispute Resolution Profile. (Last updated: 30 September 2017) General Information

General Information") 1 Norway Dispute Resolution Profile (Last updated: 30 September 2017) General Information Norway's tax treaties are available at: https://www.regjeringen.no/no/tema/okonomiogbudsjett/skatterogavgifter/skatteavtalermellomnorgeogandrestat/id417330/

1 Norway Dispute Resolution Profile (Last updated: 30 September 2017) General Information Norway's tax treaties are available at: https://www.regjeringen.no/no/tema/okonomiogbudsjett/skatterogavgifter/skatteavtalermellomnorgeogandrestat/id417330/

Release of BEPS discussion draft: Make Dispute Resolution Mechanisms More Effective

from Tax Controversy and Dispute Resolution Release of BEPS discussion draft: Make Dispute Resolution Mechanisms More Effective December 22, 2014 In brief On December 18, 2014, the Organisation for Economic

from Tax Controversy and Dispute Resolution Release of BEPS discussion draft: Make Dispute Resolution Mechanisms More Effective December 22, 2014 In brief On December 18, 2014, the Organisation for Economic

ANNEX II CHANGES TO THE UN MODEL DERIVING FROM THE REPORT ON BEPS ACTION PLAN 14

E/C.18/2017/CRP.4.Annex 2 Distr.: General 28 March 2017 Original: English Committee of Experts on International Cooperation in Tax Matters Fourteenth Session New York, 3-6 April 2017 Agenda item 3 (b)

E/C.18/2017/CRP.4.Annex 2 Distr.: General 28 March 2017 Original: English Committee of Experts on International Cooperation in Tax Matters Fourteenth Session New York, 3-6 April 2017 Agenda item 3 (b)

Selected Issues in Tax Administration of Japan

Selected Issues in Tax Administration of Japan Mr. Eimon UEDA Deputy Commissioner (International Affairs) National Tax Agency, JAPAN The Fourth IMF-Japan High Level Tax Conference For Asian Countries in

Selected Issues in Tax Administration of Japan Mr. Eimon UEDA Deputy Commissioner (International Affairs) National Tax Agency, JAPAN The Fourth IMF-Japan High Level Tax Conference For Asian Countries in

Pakistan. Total MAP Caseload. Average time needed to close MAP cases (in months) n.a. n.a n.a. n.a. n.a. n.a. n.a. n.a.

n.a. n.a n.a. n.a. n.a. n.a. n.a. n.a.") Pakistan 2 Total MAP Caseload Cases started before 1 January 2016 2017 start inventory Cases started Cases closed 2017 end inventory 0 0 0 0 0 0 0 0 1 Cases started as from 1 January 2016 2017 start inventory

Pakistan 2 Total MAP Caseload Cases started before 1 January 2016 2017 start inventory Cases started Cases closed 2017 end inventory 0 0 0 0 0 0 0 0 1 Cases started as from 1 January 2016 2017 start inventory

Consultation paper Introduction of a mechanism for eliminating double imposition of VAT in individual cases

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION INDIRECT TAXATION AND TAX ADMINISTRATION VAT and other turnover taxes TAXUD/D1/. 5 January 2007 Consultation paper Introduction of a mechanism

EUROPEAN COMMISSION DIRECTORATE-GENERAL TAXATION AND CUSTOMS UNION INDIRECT TAXATION AND TAX ADMINISTRATION VAT and other turnover taxes TAXUD/D1/. 5 January 2007 Consultation paper Introduction of a mechanism

DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 45 RELIEF FROM DOUBLE TAXATION DUE TO TRANSFER PRICING OR PROFIT REALLOCATION ADJUSTMENTS

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 45 RELIEF FROM DOUBLE TAXATION DUE TO TRANSFER PRICING OR PROFIT REALLOCATION ADJUSTMENTS These notes are issued for

Inland Revenue Department Hong Kong DEPARTMENTAL INTERPRETATION AND PRACTICE NOTES NO. 45 RELIEF FROM DOUBLE TAXATION DUE TO TRANSFER PRICING OR PROFIT REALLOCATION ADJUSTMENTS These notes are issued for

Contents. Introduction. International Transfer Pricing: Advance Pricing Arrangements (APAs)

") NO.: 94-4R DATE: March 16, 2001 SUBJECT: International Transfer Pricing: Advance Pricing Arrangements (APAs) This circular cancels and replaces Information Circular 94-4, dated December 30, 1994. This

NO.: 94-4R DATE: March 16, 2001 SUBJECT: International Transfer Pricing: Advance Pricing Arrangements (APAs) This circular cancels and replaces Information Circular 94-4, dated December 30, 1994. This

Increased taxpayer rights for tax dispute resolution under new EU Directive

from Tax Controversy and Dispute Resolution Increased taxpayer rights for tax dispute resolution under new EU Directive November 2, 2017 In brief The European Union is taking an important step forward

from Tax Controversy and Dispute Resolution Increased taxpayer rights for tax dispute resolution under new EU Directive November 2, 2017 In brief The European Union is taking an important step forward

Transfer Pricing Country Summary Switzerland

Page 1 of 6 Transfer Pricing Country Summary Switzerland July 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines There are no specific transfer pricing regulations. However, legal

Page 1 of 6 Transfer Pricing Country Summary Switzerland July 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines There are no specific transfer pricing regulations. However, legal

PERMANENT COURT OF ARBITRATION ARBITRATION RULES 2012

PERMANENT COURT OF ARBITRATION ARBITRATION RULES 2012 Effective December 17, 2012 TABLE OF CONTENTS Section I. Introductory rules...5 Scope of application Article 1...5 Article 2...5 Notice of arbitration

PERMANENT COURT OF ARBITRATION ARBITRATION RULES 2012 Effective December 17, 2012 TABLE OF CONTENTS Section I. Introductory rules...5 Scope of application Article 1...5 Article 2...5 Notice of arbitration

Global Transfer Pricing Review

GLOBAL TRANSFER PRICING SERVICES Global Transfer Pricing Review Hong Kong kpmg.com/gtps TAX 2 Global Transfer Pricing Review Hong Kong KPMG observation The Hong Kong Inland Revenue Department (IRD) released

GLOBAL TRANSFER PRICING SERVICES Global Transfer Pricing Review Hong Kong kpmg.com/gtps TAX 2 Global Transfer Pricing Review Hong Kong KPMG observation The Hong Kong Inland Revenue Department (IRD) released

Arbitration Act (Tentative translation)

") Arbitration Act (Tentative translation) (Act No. 138 of August 1, 2003) Table of Contents Chapter I General Provisions (Articles 1 to 12) Chapter II Arbitration Agreement (Articles 13 to 15) Chapter III

Arbitration Act (Tentative translation) (Act No. 138 of August 1, 2003) Table of Contents Chapter I General Provisions (Articles 1 to 12) Chapter II Arbitration Agreement (Articles 13 to 15) Chapter III

Transfer Pricing Country Summary Ivory Coast

Page 1 of 6 Transfer Pricing Country Summary Ivory Coast July 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On 2 November 2016, Ivory Coast officially joined the Inclusive

Page 1 of 6 Transfer Pricing Country Summary Ivory Coast July 2018 Page 2 of 6 Legislation Existence of Transfer Pricing Laws/Guidelines On 2 November 2016, Ivory Coast officially joined the Inclusive

Denmark Dispute Resolution Profile. (Last updated: 20 June 2017) General Information

General Information") Denmark Dispute Resolution Profile (Last updated: 20 June 2017) 1 General Information Denmark tax treaties are available at: http://www.skm.dk/love/internationalt/dobbeltbeskatningsoverenskomster SKAT's

Denmark Dispute Resolution Profile (Last updated: 20 June 2017) 1 General Information Denmark tax treaties are available at: http://www.skm.dk/love/internationalt/dobbeltbeskatningsoverenskomster SKAT's

SEC. 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

26 CFR 601.201: Rulings and determination letters. Rev. Proc. 96 13 OUTLINE SECTION 1. PURPOSE OF MUTUAL AGREEMENT PROCESS SEC. 2. SCOPE Suspension.02 Requests for Assistance.03 U.S. Competent Authority.04

Global Transfer Pricing Review

Global Transfer Pricing Review Taiwan Czech Republic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Taiwan KPMG observation The Taiwan Transfer Pricing Regulations came into effect in 2005 and are

Global Transfer Pricing Review Taiwan Czech Republic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Taiwan KPMG observation The Taiwan Transfer Pricing Regulations came into effect in 2005 and are

Global Transfer Pricing Review kpmg.com/gtps

Global Transfer Pricing Review Czech FinlandRepublic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Finland KPMG observation The Finnish tax authority continues to pay attention to transfer pricing

Global Transfer Pricing Review Czech FinlandRepublic kpmg.com/gtps TAX 2 Global Transfer Pricing Review Finland KPMG observation The Finnish tax authority continues to pay attention to transfer pricing

BEPS - Current Status of Implementation in EU Countries. Prof. Guglielmo Maisto 1 March 2019

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

BEPS - Current Status of Implementation in EU Countries Prof. Guglielmo Maisto 1 March 2019 1 Pillar I COHERENCE Action 2 Neutralizing Hybrid Mismatch Arrangements Action 3 CFC Rules Action 4 Interest

E/C.18/2016/CRP.2 Attachment 9

Distr.: General * October 2016 Original: English Committee of Experts on International Cooperation in Tax Matters Twelfth Session Geneva, 11-14 October 2016 Agenda item 3 (b) (i) Update of the United Nations

Distr.: General * October 2016 Original: English Committee of Experts on International Cooperation in Tax Matters Twelfth Session Geneva, 11-14 October 2016 Agenda item 3 (b) (i) Update of the United Nations

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15. Mr. S.P. Singh, Ex-IRS 7th November, 2015

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15 Mr. S.P. Singh, Ex-IRS 7th November, 2015 Contents Action 11 - Establishing Methodologies to Collect and Analyze Data on BEPS Action 12 Requiring

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15 Mr. S.P. Singh, Ex-IRS 7th November, 2015 Contents Action 11 - Establishing Methodologies to Collect and Analyze Data on BEPS Action 12 Requiring

Desiring to further develop their economic relationship and to enhance their co-operation in tax matters,

CONVENTION BETWEEN JAPAN AND THE REPUBLIC OF SLOVENIA FOR THE ELIMINATION OF DOUBLE TAXATION WITH RESPECT TO TAXES ON INCOME AND THE PREVENTION OF TAX EVASION AND AVOIDANCE Japan and the Republic of Slovenia,

CONVENTION BETWEEN JAPAN AND THE REPUBLIC OF SLOVENIA FOR THE ELIMINATION OF DOUBLE TAXATION WITH RESPECT TO TAXES ON INCOME AND THE PREVENTION OF TAX EVASION AND AVOIDANCE Japan and the Republic of Slovenia,

NETHERLANDS - ARBITRATION ACT DECEMBER 1986 CODE OF CIVIL PROCEDURE - BOOK IV: ARBITRATION TITLE ONE - ARBITRATION IN THE NETHERLANDS

NETHERLANDS - ARBITRATION ACT DECEMBER 1986 CODE OF CIVIL PROCEDURE - BOOK IV: ARBITRATION TITLE ONE - ARBITRATION IN THE NETHERLANDS SECTION ONE - ARBITRATION AGREEMENT AND APPOINTMENT OF ARBITRATOR Article

NETHERLANDS - ARBITRATION ACT DECEMBER 1986 CODE OF CIVIL PROCEDURE - BOOK IV: ARBITRATION TITLE ONE - ARBITRATION IN THE NETHERLANDS SECTION ONE - ARBITRATION AGREEMENT AND APPOINTMENT OF ARBITRATOR Article

BEPS ACTION 15. Development of a Multilateral Instrument to Implement the Tax Treaty related BEPS Measures

BEPS ACTION 15 Development of a Multilateral Instrument to Implement the Tax Treaty related BEPS Measures REQUEST FOR INPUT ON THE DEVELOPMENT OF A MULTILATERAL INSTRUMENT TO IMPLEMENT THE TAX TREATY-RELATED

BEPS ACTION 15 Development of a Multilateral Instrument to Implement the Tax Treaty related BEPS Measures REQUEST FOR INPUT ON THE DEVELOPMENT OF A MULTILATERAL INSTRUMENT TO IMPLEMENT THE TAX TREATY-RELATED

ROMANIA TRANSFER PRICING COUNTRY PROFILE

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle Latest update April 2018 The arm's length principle was introduced in the domestic tax law in 1994 and is applicable

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle Latest update April 2018 The arm's length principle was introduced in the domestic tax law in 1994 and is applicable

SECTION 5. SMALL CASE PROCEDURE FOR REQUESTING COMPETENT AUTHORITY ASSISTANCE.01 General.02 Small Case Standards.03 Small Case Filing Procedure

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Rev. Proc. 2002 52 SECTION 1. PURPOSE OF THE REVENUE PROCEDURE SECTION 2. SCOPE.01 In General.02 Requests for Assistance.03 Authority of the U.S. Competent Authority.04 General Process.05 Failure to Request

Arbitration under Tax Treaties

Arbitration under Tax Treaties International Fiscal Association India Branch Northern Region Chapter Delhi 11 February 2012 Marcus Desax Walder Wyss Ltd. Overview of presentation The need for tax treaty

Arbitration under Tax Treaties International Fiscal Association India Branch Northern Region Chapter Delhi 11 February 2012 Marcus Desax Walder Wyss Ltd. Overview of presentation The need for tax treaty

Norway signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

18 August 2017 Global Tax Alert Norway signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

18 August 2017 Global Tax Alert Norway signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

Chapter 1 GENERAL PROVISIONS. Article 1 GENERAL DEFINITIONS. 1. For the purposes of this Agreement, unless the context otherwise requires:

AGREEMENT BETWEEN THE GOVERNMENT OF JAPAN AND THE GOVERNMENT OF BERMUDA FOR THE EXCHANGE OF INFORMATION FOR THE PURPOSE OF THE PREVENTION OF FISCAL EVASION AND THE ALLOCATION OF RIGHTS OF TAXATION WITH

AGREEMENT BETWEEN THE GOVERNMENT OF JAPAN AND THE GOVERNMENT OF BERMUDA FOR THE EXCHANGE OF INFORMATION FOR THE PURPOSE OF THE PREVENTION OF FISCAL EVASION AND THE ALLOCATION OF RIGHTS OF TAXATION WITH

HONG KONG. 1. Introduction. Contact Information Henry Fung Candice Ng

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

HONG KONG Contact Information Henry Fung +852 2969 4054 hernyfung@pkf-hk.com Candice Ng +852 2969 4016 candiceng@pkf-hk.com 1. Introduction 1.1. Legal context Currently, the Hong Kong Inland Revenue Ordinance

ROMANIA. minimum of 25% of the number/value of shares or voting rights in the two entities.

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle The arm's length principle was introduced in the domestic tax law in 1994 and is applicable to all related party transactions,

ROMANIA TRANSFER PRICING COUNTRY PROFILE 1. Reference to the Arm s Length Principle The arm's length principle was introduced in the domestic tax law in 1994 and is applicable to all related party transactions,

Foundation for International Taxation Jubilee Conference

Minimising and Resolving International Tax Disputes post-beps Foundation for International Taxation Jubilee Conference Professor Richard Vann Sydney Law School The University of Sydney Page 1 Topics Will

Minimising and Resolving International Tax Disputes post-beps Foundation for International Taxation Jubilee Conference Professor Richard Vann Sydney Law School The University of Sydney Page 1 Topics Will