Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable

|

|

|

- Jeffry Lawrence

- 6 years ago

- Views:

Transcription

1 Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable Presented by Richard S. Lehman, Esq S.W. 18th Street, Suite C-1, Boca Raton, FL Tel: (561) Fax: (561) !

2 Richard S. Lehman, Esq. Masters in Tax Law from New York University Law School ATTORNEY AT LAW Richard S. Lehman, Esq S.W. 18th Street, Suite C-1 Boca Raton, FL Tel: U.S. Tax Court and Internal Revenue Service experience in Washington D.C.» Served as a law clerk to the Honorable William M. Fay, U.S. Tax Court!» Senior Attorney, Interpretative Division, Chief Counsel s Office, Internal Revenue Service, Washington D.C The firm regularly works with law firms, accountants, businesses and individuals struggling to find their way through the complexities of the tax law. With over 38 years as a tax lawyer in Florida, Lehman has built a boutique tax law firm with a national reputation for being able to handle the toughest tax cases, structure the most sophisticated income tax and estate tax plans, and defend clients before the IRS.

3 By the end of this presentation you will better understand how these items relate to ponzi scheme tax loss: THE SAFE HARBOR & The Internal Revenue Procedure THE LAW & The Internal Revenue Ruling TAX PLANNING How the taxpayer will plan and implement his or her Ponzi scheme tax loss for maximum benefits now and in the future.

4 Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable

5 Tax Refunds from Ponzi Scheme Losses Are Extremely Valuable Ordinary Income Loss can be used against all types of income. 3 Year Carry Back Fast Process to Receive Cash Tax Refund and Amended Returns No Litigation Costs or Delays Most Secure Payer United States Government Can be as High as 39.9% Plus 3.8%Return for each Dollar Loss and more for state income tax refunds and due to the absence of deduction limitations Can be a higher value in future with higher taxes 20 Year Carry Forward Possibility of Receiving Interest on Tax Refunds from Prior Years Value Can Be Lost Without Good Professional Advice

6 PROFESSIONAL Tax Planning The final professional product should provide the taxpayer with appropriate projections of the use of the tax losses under differing circumstances that are legally feasible to obtain. The client will be able to understand the financial effect of various options that the tax loss and litigation recoveries may provide for. Since the theft loss may be carried back three years and carried forward 20 years, it is extremely valuable.

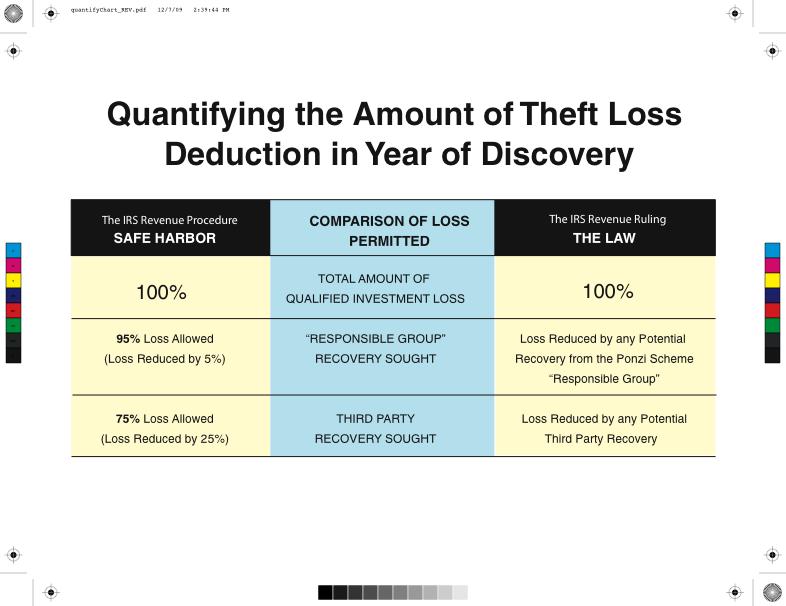

7 The Safe Harbor The IRS Revenue Procedure

8 The Safe Harbor The Safe Harbor requires that the Ponzi scheme victims forego the opportunity to file amended returns for those years that are still open by the statute of limitations. However, by amending a prior return instead of taking a theft loss deduction, a taxpayer can eliminate only the taxpayer s Ponzi scheme phantom income from the taxable income in the prior years. This will typically be the high bracket income.

9 Ponzi Schemes & Theft Loss

10 The Theft Loss allows a deduction for loss sustained during the taxable year and not compensated by insurance or otherwise. For federal income tax purposes, theft is a word of general and broad connotation, covering any criminal appropriation of another s property to the use of the taker, including theft by swindling, false pretenses and any other form of guile. A taxpayer claiming a theft loss must prove that the loss resulted from a taking of property that was illegal under the law of the jurisdiction in which it occurred and was done with criminal intent. However, a taxpayer need not show a conviction for theft.

11 Ponzi Schemes & Theft Loss The Theft Loss Privity of Investor Character of Loss Limitations on Deductions

12 II. Ponzi Schemes & Theft Loss Amount of the Theft Loss Year of Theft Loss Deduction Amount of Theft Loss Deduction in Year of Discovery Amount of Theft Loss Deduction in Later Years and Recoveries in Excess of Theft Loss Deductions

13 The Amount of The Loss (Basis) & Phantom Income Definition of Phantom Income: The Revenue Ruling and the Revenue Procedure both acknowledge that: Theft loss resulting from a Ponzi scheme is generally The initial amount invested in the arrangement plus 2. Any additional investments upon which taxes have been paid, less amounts withdrawn The I.R.S. agrees that if an amount is reported to the investor as income in years prior to the year of discovery of the theft and the investor includes the amount in gross income; then the amount of the theft loss is increased by the purportedly reinvested amount (the Phantom Income ).

14 Year of Discovery Definition of Taxable Year of Discovery any loss arising from theft shall be treated as sustained during the taxable year in which the taxpayer discovers such loss. A loss is considered to be discovered when a reasonable person in similar circumstances would have realized that he or she had suffered an unrecoverable loss. Although a theft loss must be considered as sustained in the year of its discovery, [The code section] does not indicate that discovery of some false representation (even amounting to theft under applicable law) creates a theft loss as of the date of the discovery of the falsity of the representation. The statue refers to the year of discovery of the loss, not of the theft.

15 Year of Discovery The year of discovery is very important and evidence is critical here to show exactly when and how a taxpayer can pin down this time. We look to several examples of CASE LAW to help us to define the year of discovery of a theft loss.

16 The Amount & Timing Of The Theft Loss

17 Reasonable Prospect of Recovery Definition of Reasonable Prospect of Recovery A reasonable prospect of recovery exists when the taxpayer has a bona fide claim for recoupment from third parties or otherwise, and when there is a substantial possibility that such claims will be decided in the taxpayer s favor. The taxpayer is not, however, required to be an incorrigible optimist and claims with only remote or nebulous potential for success will not postpone the deduction.

18 Reasonable Prospect of Recovery 1. In determining the reasonableness of a taxpayer s belief of loss the courts had to be practical and aware of the individual facts of a case. 2. Circumstances are those that are known or reasonably could be known as of the end of the tax year for which the loss deduction is claimed. The only test is foresight, not hindsight. 3. Both objective and subjective factors must be examined.

19 Reasonable Prospect of Recovery The taxpayer s legal rights as of the end of the year of discovery are all important and need to be studied to make a proper decision. One of the facts and circumstances deserving of consideration is the probability of success on the merits of any claim brought by the taxpayer. The filing of a lawsuit may give rise to an inference of a reasonable prospect of recovery. However, the inference is not conclusive nor mandatory. The inquiry should be directed to the probability of recovery as opposed to the mere possibility. A remote possibility of recovery is not enough; there must be a reasonable prospect of recovery at the time the deduction was claimed, not later.

20 Ascertainable Standard Once the taxpayer has deducted all that could be deducted in the year of discovery by reducing the loss for all reasonable prospects of recovery the tax in year two, after the discovery year, from this point on will be able to claim continuing theft loss deductions until the loss is recovered in full. However, at this point the taxpayer cannot deduct any more of his or her un-deducted theft loss unless the deduction can be ascertained with a reasonable certainty. This is a higher standard of proof.

21 Tax Planning The major principle seen in each of the court s decisions is that victims of the fraud who want to take the theft loss deduction in the year of discovery, must be well advised to separately consider each of their potential sources of recovery. Value can be lost without good professional advice.

22 PROFESSIONAL Tax Planning Tax planning should result in a professional work product that will most likely accompany an amended return or similar type of I.R.S. filing. The document will most likely be the work product of at least three of the client s advisors: 1. THEIR ACCOUNTANT 2. A TAX ATTORNEY 3. LITIGATION COUNSEL

23 PROFESSIONAL Tax Planning With the professional team in place, the steps generally will be as follows: 1. Records 2. Basis Calculations 3. Sources of Recovery 4. Loss in Year of Discovery 5. Accounting Schedules and Forecasts These projections will be critical.

24 The Safe Harbor The IRS Revenue Procedure

25 Comparison of Revenue Procedure vs Revenue Ruling

26

27 Other Reductions to Qualified Investment Loss SAME FOR SAFE HARBOR OR THE LAW 1. Loss Reduced by Actual Recovery Received in the year of Discovery 2. Loss Reduced by Insurance policies In the name of the Qualified investor 3. Loss Reduced by Contractual arrangements that guarantees or otherwise protects against loss of the qualified investment 4. Loss Reduced by Certain Amounts Payable from the Securities Investor Protection Corporation (SPIC)

28 Theft Loss vs Amended Returns

29 Amended Returns A deduction obtained from amending tax returns to eliminate only the Ponzi scheme income may be more valuable than a theft loss deduction.

30 Comparison of Revenue Procedure vs Revenue Ruling

31 Comparison of Revenue Procedure vs Revenue Ruling

32

33 Clawbacks

34

35

36

37

38

39

40

41

42

43

44

45 Richard S. Lehman, Esq. TAX ATTORNEY AT LAW 6018 S.W. 18th Street, Suite C-1 Boca Raton, FL Tel: Fax: Value can be lost without good professional advice.

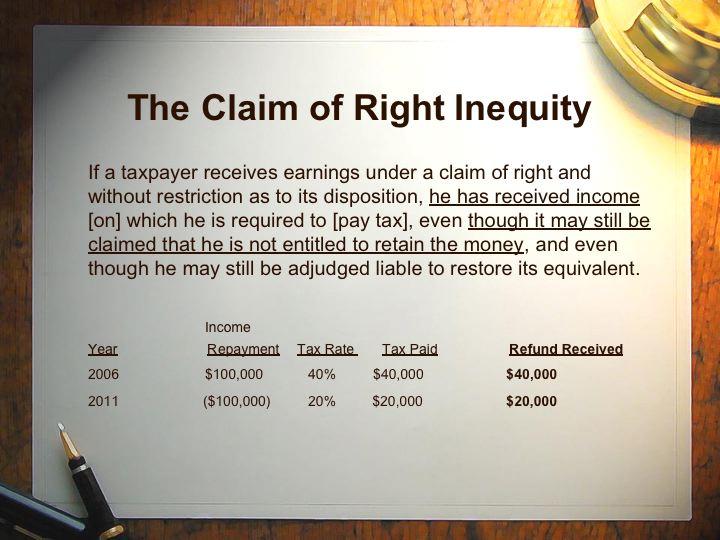

Section 1341 "Claim of Right" Refunds: Calculating Tax Benefits, Avoiding Double Taxation on Repayments and Claw-Backs

Section 1341 "Claim of Right" Refunds: Calculating Tax Benefits, Avoiding Double Taxation on Repayments and Claw-Backs FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 10, 2016, 1:00-2:50 pm Eastern IMPORTANT

Section 1341 "Claim of Right" Refunds: Calculating Tax Benefits, Avoiding Double Taxation on Repayments and Claw-Backs FOR LIVE PROGRAM ONLY THURSDAY, NOVEMBER 10, 2016, 1:00-2:50 pm Eastern IMPORTANT

U.S. Tax Benefits for Exporting

U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton,

U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton,

Revenue Ruling Losses

CLICK HERE to return to the home page Revenue Ruling 2009-9 Losses ISSUES (1) Is a loss from criminal fraud or embezzlement in a transaction entered into for profit a theft loss or a capital loss under

CLICK HERE to return to the home page Revenue Ruling 2009-9 Losses ISSUES (1) Is a loss from criminal fraud or embezzlement in a transaction entered into for profit a theft loss or a capital loss under

(1) Is a loss from criminal fraud or embezzlement in a transaction entered into for

Is a loss from criminal fraud or embezzlement in a transaction entered into for") Part I Section 165. Losses. 26 CFR: 1.165-8: Theft losses. (Also: 63, 67, 68, 172, 1311, 1312, 1313, 1314, 1341) Rev. Rul. 2009-9 ISSUES (1) Is a loss from criminal fraud or embezzlement in a transaction

Part I Section 165. Losses. 26 CFR: 1.165-8: Theft losses. (Also: 63, 67, 68, 172, 1311, 1312, 1313, 1314, 1341) Rev. Rul. 2009-9 ISSUES (1) Is a loss from criminal fraud or embezzlement in a transaction

THE IC-DISC. By Richard S. Lehman, Esq

By Richard S. Lehman, Esq The United States Tax Benefits Of Exporting THE IC-DISC The business world is going to be a tough place for the American exporter in 2012. The dollar will remain strong, keeping

By Richard S. Lehman, Esq The United States Tax Benefits Of Exporting THE IC-DISC The business world is going to be a tough place for the American exporter in 2012. The dollar will remain strong, keeping

Taxation of the Clawback in a Ponzi Scheme Maximum Tax Recovery. Dedicated to Victims and Financial Professionals

Taxation of the Clawback in a Ponzi Scheme Maximum Tax Recovery By Tax Attorney, Richard S. Lehman Esq. This book is not providing any legal advice whatsoever. Each and every taxpayer s situation and potential

Taxation of the Clawback in a Ponzi Scheme Maximum Tax Recovery By Tax Attorney, Richard S. Lehman Esq. This book is not providing any legal advice whatsoever. Each and every taxpayer s situation and potential

Pre-Immigration Tax Planning

Pre-Immigration Tax Planning Safeguarding The Immigrant s Financial Interests Prior to Residency By Richard S. Lehman & Associates Attorneys at Law Pre-Immigration Tax Planning Safeguarding The Immigrant

Pre-Immigration Tax Planning Safeguarding The Immigrant s Financial Interests Prior to Residency By Richard S. Lehman & Associates Attorneys at Law Pre-Immigration Tax Planning Safeguarding The Immigrant

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps By Richard S. Lehman & Associates Attorneys at Law TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps By Richard S. Lehman & Associates Attorneys at Law TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps

Anthony Korda, Atty, The Korda Law Firm, Naples, Fla. Richard S. Lehman, Atty, United States Taxation and Immigration Law, Boca Raton, Fla.

Presenting a live 90-minute webinar with interactive Q&A Pre-Immigration Tax and U.S. Investment Planning for High Net Worth Individuals Navigating the EB-5 Investor's Visa Program, Leveraging Tax Credits

Presenting a live 90-minute webinar with interactive Q&A Pre-Immigration Tax and U.S. Investment Planning for High Net Worth Individuals Navigating the EB-5 Investor's Visa Program, Leveraging Tax Credits

TAX PLANNING. Foreign Investment In United States Real Estate. By Richard S. Lehman, Esq TAX ATTORNEY

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors TAX PLANNING Foreign Investment In United States Real Estate By Richard S. Lehman, Esq TAX ATTORNEY 1 FOREIGN INVESTMENT

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors TAX PLANNING Foreign Investment In United States Real Estate By Richard S. Lehman, Esq TAX ATTORNEY 1 FOREIGN INVESTMENT

2600 N. Military Trail, Suite 206, Boca Raton, Florida Tel

2600 N. Military Trail, Suite 206, Boca Raton, Florida 33431 Tel. 1-561-368-1113 www.lehmantaxlaw.com U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules Tax Planning Before Immigrating

2600 N. Military Trail, Suite 206, Boca Raton, Florida 33431 Tel. 1-561-368-1113 www.lehmantaxlaw.com U.S. Taxation of Foreign Corporations And Nonresident Aliens General Rules Tax Planning Before Immigrating

In c o m e Ta x. Ace t a m i n o p h e n. How Recent IRS Guidance Can Alleviate the Pain Caused by Madoff and Other Ponzi Schemes

In c o m e Ta x Ace t a m i n o p h e n How Recent IRS Guidance Can Alleviate the Pain Caused by Madoff and Other Ponzi Schemes By Stephen A. Beck, J.D., LL.M. 24 Today scpa September/October 2009 The

In c o m e Ta x Ace t a m i n o p h e n How Recent IRS Guidance Can Alleviate the Pain Caused by Madoff and Other Ponzi Schemes By Stephen A. Beck, J.D., LL.M. 24 Today scpa September/October 2009 The

Chapter 14 p.835 Losses

Chapter 14 p.835 Losses 165(a) provides the general rule that a tax deduction is available (1) for any loss sustained during the taxable year and (2) not compensated for by insurance. 165(b) specifies

Chapter 14 p.835 Losses 165(a) provides the general rule that a tax deduction is available (1) for any loss sustained during the taxable year and (2) not compensated for by insurance. 165(b) specifies

1111 Constitution Avenue, NW 1111 Constitution Avenue, NW Washington, DC Washington, DC 20224

Mr. Scott Dinwiddie Mr. John Moriarty June 13, 2018 Page 2 of 2 June 13, 2018 Mr. Scott Dinwiddie Mr. John Moriarty Associate Chief Counsel Deputy Associate Chief Counsel Income Tax & Accounting Income

Mr. Scott Dinwiddie Mr. John Moriarty June 13, 2018 Page 2 of 2 June 13, 2018 Mr. Scott Dinwiddie Mr. John Moriarty Associate Chief Counsel Deputy Associate Chief Counsel Income Tax & Accounting Income

U.S. v. Sulzbach: Government Theories, Potential Defenses, and Lessons Learned

U.S. v. Sulzbach: Government Theories, Potential Defenses, and Lessons Learned Presented By: David O Brien Christine Rinn Michael Paddock HOOPS 2007 - Washington, DC October 15-16 Background June 1994:

U.S. v. Sulzbach: Government Theories, Potential Defenses, and Lessons Learned Presented By: David O Brien Christine Rinn Michael Paddock HOOPS 2007 - Washington, DC October 15-16 Background June 1994:

JUDGE WATSON'S NOTICE OF COMPLIANCE WITH OMNIBUS ORDER ON PENDING MOTIONS DATED DECEMBER 20, 2013

Filing # 8818506 Electronically Filed 01/06/2014 10:45:52 AM RECEIVED, 1/6/2014 10:48:40, John A. Tomasino, Clerk, Supreme Court BEFORE THE FLORIDA JUDICIAL QUALIFICATIONS COMMISSION STATE OF FLORIDA INQUIRY

Filing # 8818506 Electronically Filed 01/06/2014 10:45:52 AM RECEIVED, 1/6/2014 10:48:40, John A. Tomasino, Clerk, Supreme Court BEFORE THE FLORIDA JUDICIAL QUALIFICATIONS COMMISSION STATE OF FLORIDA INQUIRY

NEW JERSEY LAW REVISION COMMISSION. Revised Final Report. Amendments to Uniform Principal and Income Act. July 18, 2013

NEW JERSEY LAW REVISION COMMISSION Revised Final Report Relating to Amendments to Uniform Principal and Income Act July 18, 2013 The work of the New Jersey Law Revision Commission is only a recommendation

NEW JERSEY LAW REVISION COMMISSION Revised Final Report Relating to Amendments to Uniform Principal and Income Act July 18, 2013 The work of the New Jersey Law Revision Commission is only a recommendation

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO CIV-DIMITROULEAS

In re DS Healthcare Group, Inc. Securities Litigation / UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO. 16-60661-CIV-DIMITROULEAS NOTICE OF PENDENCY AND PROPOSED SETTLEMENT OF CLASS

In re DS Healthcare Group, Inc. Securities Litigation / UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF FLORIDA CASE NO. 16-60661-CIV-DIMITROULEAS NOTICE OF PENDENCY AND PROPOSED SETTLEMENT OF CLASS

capital gains and dividend income

capital gains and dividend income Managing capital gains and losses can help you save taxes, defer taxes and obtain the highest after-tax yield on your assets. This planning is very critical when considering

capital gains and dividend income Managing capital gains and losses can help you save taxes, defer taxes and obtain the highest after-tax yield on your assets. This planning is very critical when considering

A Look at the Final Section 2053 Regulations

A PROFESSIONAL CORPORATION ATTORNEYS AT LAW A Look at the Final Section 2053 Regulations 2009 by Jonathan G. Blattmachr & Mitchell M. Gans All Rights Reserved. Introduction As a general rule, expenses

A PROFESSIONAL CORPORATION ATTORNEYS AT LAW A Look at the Final Section 2053 Regulations 2009 by Jonathan G. Blattmachr & Mitchell M. Gans All Rights Reserved. Introduction As a general rule, expenses

CHAPTER 20 - QUESTIONS

CHAPTER 20 - QUESTIONS 1. Does the sale of a business opportunity always require a real estate license? 2. When is a license required? 3. May an unlicensed person receive compensation for the portion of

CHAPTER 20 - QUESTIONS 1. Does the sale of a business opportunity always require a real estate license? 2. When is a license required? 3. May an unlicensed person receive compensation for the portion of

Government Documents Regarding Civil Fraud and White-Collar Offenses

Government Documents Regarding Civil Fraud and White-Collar Offenses U.S. Department of Justice Office of the Deputy Attorney General The Deputy Attorney General Washington, DC 20530 June 3, 1998 MEMORANDUM

Government Documents Regarding Civil Fraud and White-Collar Offenses U.S. Department of Justice Office of the Deputy Attorney General The Deputy Attorney General Washington, DC 20530 June 3, 1998 MEMORANDUM

NORTHERN OIL AND GAS, INC. INSIDER TRADING POLICY. and Guidelines with Respect to Certain Transactions in Company Securities. (Adopted March 12, 2012)

") NORTHERN OIL AND GAS, INC. INSIDER TRADING POLICY and Guidelines with Respect to Certain Transactions in Company Securities (Adopted March 12, 2012) Background Northern Oil and Gas, Inc. (the Company )

NORTHERN OIL AND GAS, INC. INSIDER TRADING POLICY and Guidelines with Respect to Certain Transactions in Company Securities (Adopted March 12, 2012) Background Northern Oil and Gas, Inc. (the Company )

Engagement Terms & Conditions

Engagement Terms & Conditions Under the requirements of our profession, we have prepared this written Engagement Terms & Conditions. Arkin & Associates, P.C. will provide professional accounting services

Engagement Terms & Conditions Under the requirements of our profession, we have prepared this written Engagement Terms & Conditions. Arkin & Associates, P.C. will provide professional accounting services

UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION. v. Case No Honorable Patrick J. Duggan FIRST BANK OF DELAWARE,

Case 2:10-cv-11345-PJD-MJH Document 12 Filed 07/07/10 Page 1 of 7 ANTHONY O. WILSON, Plaintiff, UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION v. Case No. 10-11345 Honorable

Case 2:10-cv-11345-PJD-MJH Document 12 Filed 07/07/10 Page 1 of 7 ANTHONY O. WILSON, Plaintiff, UNITED STATES DISTRICT COURT EASTERN DISTRICT OF MICHIGAN SOUTHERN DIVISION v. Case No. 10-11345 Honorable

Case 2:14-cv Document 1 Filed 05/29/14 Page 1 of 14 UNITED STATES DISTRICT COURT WESTERN DISTRICT OF WASHINGTON AT SEATTLE ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) )") Case :-cv-00 Document Filed 0// Page of 0 0 JOSE SILVA, on behalf of himself and others similarly situated, Plaintiff, vs. UNIFUND CCR, LLC AND PILOT RECEIVABLES MANAGEMENT, LLC Defendants. UNITED STATES

Case :-cv-00 Document Filed 0// Page of 0 0 JOSE SILVA, on behalf of himself and others similarly situated, Plaintiff, vs. UNIFUND CCR, LLC AND PILOT RECEIVABLES MANAGEMENT, LLC Defendants. UNITED STATES

New York State Bar Association Tax Section. Tax Exempt Entities Committee Report on Private Foundation Investors in Ponzi Schemes.

New York State Bar Association Tax Section Tax Exempt Entities Committee Report on Private Foundation Investors in Ponzi Schemes May 7, 2009 Table of Contents Page I. Background...2 A. Overview...2 B.

New York State Bar Association Tax Section Tax Exempt Entities Committee Report on Private Foundation Investors in Ponzi Schemes May 7, 2009 Table of Contents Page I. Background...2 A. Overview...2 B.

ADMINISTRATION OF JUSTICE Homework Exam Review WHITE COLLAR CRIME NAME: PERIOD: ROW:

ADMINISTRATION OF JUSTICE Homework Exam Review WHITE COLLAR CRIME NAME: PERIOD: ROW: UNDERSTANDING WHITE COLLAR CRIME 1. White-collar crime is a broad category of nonviolent misconduct involving and fraud.

ADMINISTRATION OF JUSTICE Homework Exam Review WHITE COLLAR CRIME NAME: PERIOD: ROW: UNDERSTANDING WHITE COLLAR CRIME 1. White-collar crime is a broad category of nonviolent misconduct involving and fraud.

January 16, The Honorable Max Baucus, Chairman Senate Committee on Finance 219 Dirksen Senate Office Building Washington, DC 20510

American Institute of CPAs 1455 Pennsylvania Avenue, NW Washington, DC 20004 The Honorable Max Baucus, Chairman Senate Committee on Finance 219 Dirksen Senate Office Building Washington, DC 20510, Ranking

American Institute of CPAs 1455 Pennsylvania Avenue, NW Washington, DC 20004 The Honorable Max Baucus, Chairman Senate Committee on Finance 219 Dirksen Senate Office Building Washington, DC 20510, Ranking

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW By: Kevin M. Henry, Esq. I. WHERE ARE WE NOW? THE TAX EQUITY AND FISCAL RESPONSIBILITY ACT OF 1982 ( TEFRA ) A. Prior to TEFRA, partnership audits

THE NEW CENTRALIZED PARTNERSHIP AUDIT REGIME: AN OVERVIEW By: Kevin M. Henry, Esq. I. WHERE ARE WE NOW? THE TAX EQUITY AND FISCAL RESPONSIBILITY ACT OF 1982 ( TEFRA ) A. Prior to TEFRA, partnership audits

April 19, (b) Plan Terminations. Dear Assistant Secretary Borzi:

Plan Terminations. Dear Assistant Secretary Borzi:") April 19, 2015 The Honorable Phyllis C. Borzi Assistant Secretary Employee Benefits Security Administration U.S. Department of Labor 200 Constitution Avenue NW Room S-2524 Washington, DC 20210 Re: 403(b)

April 19, 2015 The Honorable Phyllis C. Borzi Assistant Secretary Employee Benefits Security Administration U.S. Department of Labor 200 Constitution Avenue NW Room S-2524 Washington, DC 20210 Re: 403(b)

PETITION FORM IND For Claims By Indirect Investors

PETITION FORM IND For Claims By Indirect Investors MADOFF VICTIM FUND Distribution Vehicle for Forfeited Assets on behalf of the UNITED STATES DEPARTMENT OF JUSTICE Submissions to the Madoff Victim Fund

PETITION FORM IND For Claims By Indirect Investors MADOFF VICTIM FUND Distribution Vehicle for Forfeited Assets on behalf of the UNITED STATES DEPARTMENT OF JUSTICE Submissions to the Madoff Victim Fund

IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF NORTH CAROLINA CHARLOTTE DIVISION ) ) ) No. 3:12-CV-519

) ) No. 3:12-CV-519") IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF NORTH CAROLINA CHARLOTTE DIVISION SECURITIES AND EXCHANGE COMMISSION, Plaintiff, vs. REX VENTURE GROUP, LLC d/b/a ZEEKREWARDS.COM, and PAUL

IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF NORTH CAROLINA CHARLOTTE DIVISION SECURITIES AND EXCHANGE COMMISSION, Plaintiff, vs. REX VENTURE GROUP, LLC d/b/a ZEEKREWARDS.COM, and PAUL

City of Gainesville Consolidated Police Officers and Firefighters Retirement Plan

Name of the Plan City of Gainesville Consolidated Police Officers and Firefighters Retirement Plan Introduction This document is the Summary Plan Description (SPD). The SPD introduces the Plan to you and

Name of the Plan City of Gainesville Consolidated Police Officers and Firefighters Retirement Plan Introduction This document is the Summary Plan Description (SPD). The SPD introduces the Plan to you and

NEW BUSINESS APPLICATION (For Private Companies with up to 250 Employees)

") NEW BUSINESS APPLICATION (For Private Companies with up to 250 Employees) BY COMPLETING THIS NEW BUSINESS APPLICATION THE APPLICANT IS APPLYING FOR COVERAGE WITH FEDERAL INSURANCE COMPANY (THE COMPANY

NEW BUSINESS APPLICATION (For Private Companies with up to 250 Employees) BY COMPLETING THIS NEW BUSINESS APPLICATION THE APPLICANT IS APPLYING FOR COVERAGE WITH FEDERAL INSURANCE COMPANY (THE COMPANY

IN THE SUPREME COURT OF FLORIDA (Before a Referee)

") IN THE SUPREME COURT OF FLORIDA (Before a Referee) THE FLORIDA BAR, Complainant, vs. CARLOS LIDSKY, Supreme Court Case No. SC08-2293 The Florida Bar File No. 2008-70,764(11E) Respondent. / REPORT OF REFEREE

IN THE SUPREME COURT OF FLORIDA (Before a Referee) THE FLORIDA BAR, Complainant, vs. CARLOS LIDSKY, Supreme Court Case No. SC08-2293 The Florida Bar File No. 2008-70,764(11E) Respondent. / REPORT OF REFEREE

EMPLOYEES INVESTMENT RETIREMENT PLAN

The Altamonte Springs Retirement System EMPLOYEES INVESTMENT RETIREMENT PLAN A Retirement Guide for Employees January 2016 Edition TABLE OF CONTENTS Introduction... 3 Basic Plan Information... 4 Membership...

The Altamonte Springs Retirement System EMPLOYEES INVESTMENT RETIREMENT PLAN A Retirement Guide for Employees January 2016 Edition TABLE OF CONTENTS Introduction... 3 Basic Plan Information... 4 Membership...

Tax-Free Exchanges Under IRC 1031

May 17, 2011 Tax-Free Exchanges Under IRC 1031 GKG Law, P.C. Webinar Series Presenter: Keith G. Swirsky President Phone: (202) 342-5251 kswirsky@gkglaw.com www.gkglaw.com Disclaimers This presentation

May 17, 2011 Tax-Free Exchanges Under IRC 1031 GKG Law, P.C. Webinar Series Presenter: Keith G. Swirsky President Phone: (202) 342-5251 kswirsky@gkglaw.com www.gkglaw.com Disclaimers This presentation

MARATHON PATENT GROUP, INC.

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 2549 Amendment No. 3 To SCHEDULE 13G (Rule 13d-12) INFORMATION TO BE INCLUDED IN STATEMENTS FILED PURSUANT TO RULE 13d-1(b) (c), AND (d) AND AMENDMENTS

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 2549 Amendment No. 3 To SCHEDULE 13G (Rule 13d-12) INFORMATION TO BE INCLUDED IN STATEMENTS FILED PURSUANT TO RULE 13d-1(b) (c), AND (d) AND AMENDMENTS

IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF MISSOURI WESTERN DIVISION

IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF MISSOURI WESTERN DIVISION UNITED STATES OF AMERICA, No. Plaintiff, COUNT ONE [Both Defendants] v. 18 U.S.C. 286 (Conspiracy to Defraud the

IN THE UNITED STATES DISTRICT COURT FOR THE WESTERN DISTRICT OF MISSOURI WESTERN DIVISION UNITED STATES OF AMERICA, No. Plaintiff, COUNT ONE [Both Defendants] v. 18 U.S.C. 286 (Conspiracy to Defraud the

POLICE OFFICERS SHARE PLAN

The Altamonte Springs Retirement System POLICE OFFICERS SHARE PLAN A Retirement Guide for Police Officers October 2016 Edition TABLE OF CONTENTS Introduction... 3 Plan Information... 4 Membership... 5

The Altamonte Springs Retirement System POLICE OFFICERS SHARE PLAN A Retirement Guide for Police Officers October 2016 Edition TABLE OF CONTENTS Introduction... 3 Plan Information... 4 Membership... 5

OCWEN FINANCIAL CORPORATION (Name of Issuer)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 SCHEDULE 13G Under the Securities Exchange Act of 1934 (Amendment )* OCWEN FINANCIAL CORPORATION (Name of Issuer) Common Stock, par

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 SCHEDULE 13G Under the Securities Exchange Act of 1934 (Amendment )* OCWEN FINANCIAL CORPORATION (Name of Issuer) Common Stock, par

5 Strategies to Resolve Your IRS Tax Problem. By Nehemiah Jefferson, Esq., EA.

5 Strategies to Resolve Your IRS Tax Problem By Nehemiah Jefferson, Esq., EA This mini book is provided for information purposes only, does not create an attorney-client relationship, and should not be

5 Strategies to Resolve Your IRS Tax Problem By Nehemiah Jefferson, Esq., EA This mini book is provided for information purposes only, does not create an attorney-client relationship, and should not be

MANAGING HOME HEALTH AND HOSPICE REGULATORY RISK IN THE NEW HEALTH CARE ECONOMY

MANAGING HOME HEALTH AND HOSPICE REGULATORY RISK IN THE NEW HEALTH CARE ECONOMY By: Thomas William Baker, Esq. Baker Donelson Bearman Caldwell & Berkowitz, PC (404) 221-6510 (Phone) (404) 238-9640 (Facsimile)

MANAGING HOME HEALTH AND HOSPICE REGULATORY RISK IN THE NEW HEALTH CARE ECONOMY By: Thomas William Baker, Esq. Baker Donelson Bearman Caldwell & Berkowitz, PC (404) 221-6510 (Phone) (404) 238-9640 (Facsimile)

Alphabet Soup for Offers In Compromise (OIC)

") HIGH- STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE 1012 Broad Street, 2nd Fl Bloomfield, NJ 07003 Tel (973) 783-7000 Fax (973) 338-3955 www.deblislaw.com 001612007 Alphabet Soup for Offers In Compromise

HIGH- STAKES TAX DEFENSE & COMPLEX CRIMINAL DEFENSE 1012 Broad Street, 2nd Fl Bloomfield, NJ 07003 Tel (973) 783-7000 Fax (973) 338-3955 www.deblislaw.com 001612007 Alphabet Soup for Offers In Compromise

The only way to get a payment. NO LATER THAN MARCH 10, 2011 EXCLUDE YOURSELF NO LATER THAN MARCH 10, 2011 SUBMIT A CLAIM FORM

United States District Court Southern District Of New York IN RE FUWEI FILMS SECURITIES LITIGATION Case No. 07-CV-9416 (RJS) NOTICE OF PENDENCY AND SETTLEMENT OF CLASS ACTION If you purchased or otherwise

United States District Court Southern District Of New York IN RE FUWEI FILMS SECURITIES LITIGATION Case No. 07-CV-9416 (RJS) NOTICE OF PENDENCY AND SETTLEMENT OF CLASS ACTION If you purchased or otherwise

Conducting Aircraft Tax Free Exchanges

Conducting Aircraft Tax Free Exchanges Webinar Presentation - June 16th, 2010 Presenter: Keith G. Swirsky, President Tel: (202) 342-5251 Fax: (202) 965-5725 kswirsky@gkglaw.com Disclaimers This presentation

Conducting Aircraft Tax Free Exchanges Webinar Presentation - June 16th, 2010 Presenter: Keith G. Swirsky, President Tel: (202) 342-5251 Fax: (202) 965-5725 kswirsky@gkglaw.com Disclaimers This presentation

14 - Court Determines Damages for Willfully Filing a Fraudulent Information Return

14 - Court Determines Damages for Willfully Filing a Fraudulent Information Return Angelopoulo v. Keystone Orthopedic Specialists, S.C., et al., (DC IL 7/9/2018) 122 AFTR 2d 2018-5028 A district court

14 - Court Determines Damages for Willfully Filing a Fraudulent Information Return Angelopoulo v. Keystone Orthopedic Specialists, S.C., et al., (DC IL 7/9/2018) 122 AFTR 2d 2018-5028 A district court

New Proposed Regulations Provide Clarity and Rigidity to Tax-Free Spin- Off Rules

S! ta Tax Alert July 2016 New Proposed Regulations Provide Clarity and Rigidity to Tax-Free Spin- Off Rules If finalized, newly released proposed Treasury regulations may make spin-offs more difficult

S! ta Tax Alert July 2016 New Proposed Regulations Provide Clarity and Rigidity to Tax-Free Spin- Off Rules If finalized, newly released proposed Treasury regulations may make spin-offs more difficult

Defending a Federal (IRS) Income Tax or Excise Tax Audit or a State Sales and Use Tax Audit

Income Tax or Excise Tax Audit or a State Sales and Use Tax Audit") Aviation Tax Law Webinar Defending a Federal (IRS) Income Tax or Excise Tax Audit or a State Sales and Use Tax Audit January 7, 2014 Keith G. Swirsky President GKG Law, P.C. (202) 342-5251 kswirsky@gkglaw.com

Aviation Tax Law Webinar Defending a Federal (IRS) Income Tax or Excise Tax Audit or a State Sales and Use Tax Audit January 7, 2014 Keith G. Swirsky President GKG Law, P.C. (202) 342-5251 kswirsky@gkglaw.com

TABLE OF CONTENTS. 1 Introduction 2 Choosing small claims 4 Going to court 6 Litigation funding 7 Your privacy 8 Further resources

SMALL CLAIMS GUIDE Disclaimer: this Guide is meant to be legal information and not legal advice. Users should not rely on this information but should rather seek independent legal advice regarding their

SMALL CLAIMS GUIDE Disclaimer: this Guide is meant to be legal information and not legal advice. Users should not rely on this information but should rather seek independent legal advice regarding their

"It's Not My Fault": Scope of Reasonable Cause And Good Faith Exception to Tax Penalties

THE UNIVERSITY OF TEXAS SCHOOL OF LAW Presented: 61st Annual Taxation Conference December 4-5, 2013 Austin, Texas "It's Not My Fault": Scope of Reasonable Cause And Good Faith Exception to Tax Penalties

THE UNIVERSITY OF TEXAS SCHOOL OF LAW Presented: 61st Annual Taxation Conference December 4-5, 2013 Austin, Texas "It's Not My Fault": Scope of Reasonable Cause And Good Faith Exception to Tax Penalties

Role Of Advisers In Client Class Action Claims

Investment Adviser Association Compliance Workshop October 26, 2005 Role Of Advisers In Client Class Action Claims Steven W. Stone Partner Morgan, Lewis & Bockius LLP www.morganlewis.com Role Of Advisers

Investment Adviser Association Compliance Workshop October 26, 2005 Role Of Advisers In Client Class Action Claims Steven W. Stone Partner Morgan, Lewis & Bockius LLP www.morganlewis.com Role Of Advisers

The Changing Landscape of Securities Class Actions and Its Impact on Mutual Funds

The Changing Landscape of Securities Class Actions and Its Impact on Mutual Funds November 15, 2017 Presented by: Joseph T. Kelleher Partner Investment Management Litigation Keith R. Dutill Partner Investment

The Changing Landscape of Securities Class Actions and Its Impact on Mutual Funds November 15, 2017 Presented by: Joseph T. Kelleher Partner Investment Management Litigation Keith R. Dutill Partner Investment

YMCA of Metropolitan Denver Volunteer Requirements

YMCA of Metropolitan Denver Volunteer Requirements Thank you for considering volunteering with our YMCA sports program. Listed below is a checklist of what any prospective coach in our program will be

YMCA of Metropolitan Denver Volunteer Requirements Thank you for considering volunteering with our YMCA sports program. Listed below is a checklist of what any prospective coach in our program will be

Notice of Class Action and Proposed Settlement. You may be entitled to receive benefits under this class action settlement.

UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF NEW YORK Notice of Class Action and Proposed Settlement You may be entitled to receive benefits under this class action settlement. This notice

UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF NEW YORK Notice of Class Action and Proposed Settlement You may be entitled to receive benefits under this class action settlement. This notice

) ) ) ) ) ) ) ) ) ) ) ) NOTICE OF PROPOSED CLASS ACTION SETTLEMENT

) ) ) ) ) ) ) ) ) ) ) NOTICE OF PROPOSED CLASS ACTION SETTLEMENT") UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK DANIEL AUDE, Individually and on Behalf of All Others Similarly Situated, vs. Plaintiff, KOBE STEEL, LTD., HIROYA KAWASAKI, YOSHINORI ONOE, AKIRA

UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF NEW YORK DANIEL AUDE, Individually and on Behalf of All Others Similarly Situated, vs. Plaintiff, KOBE STEEL, LTD., HIROYA KAWASAKI, YOSHINORI ONOE, AKIRA

Tax-Free Aircraft Exchanges Under IRC 1031 and Bonus Depreciation Update and Basics

Aviation Tax Law Webinar December 8, 2015 Tax-Free Aircraft Exchanges Under IRC 1031 and Bonus Depreciation Update and Basics Presented by: Keith G. Swirsky Christopher B. Younger GKG Law, P.C. 1055 Thomas

Aviation Tax Law Webinar December 8, 2015 Tax-Free Aircraft Exchanges Under IRC 1031 and Bonus Depreciation Update and Basics Presented by: Keith G. Swirsky Christopher B. Younger GKG Law, P.C. 1055 Thomas

Office of Inspector General. Regional Enforcement Efforts and Priorities in Florida. South Atlantic Regional Conference January 28, 2011

Office of Inspector General Regional Enforcement Efforts and Priorities in Florida Health Care Compliance Association South Atlantic Regional Conference January 28, 2011 Felicia Heimer, Esq. Office of

Office of Inspector General Regional Enforcement Efforts and Priorities in Florida Health Care Compliance Association South Atlantic Regional Conference January 28, 2011 Felicia Heimer, Esq. Office of

Launching a HEDGE FUND in 2017: KEY STRUCTURAL AND OPERATIONAL ISSUES

Launching a HEDGE FUND in 2017: KEY STRUCTURAL AND OPERATIONAL ISSUES FUND FORMATION SERVICES What sort of legal structure should be used? Most domestic hedge funds are organized as limited partnerships

Launching a HEDGE FUND in 2017: KEY STRUCTURAL AND OPERATIONAL ISSUES FUND FORMATION SERVICES What sort of legal structure should be used? Most domestic hedge funds are organized as limited partnerships

Management Alert. How Long and Strong is Trustee Piccard s Claw?

How Long and Strong is Trustee Piccard s Claw? On December 10, 2008, Bernard Madoff confessed to his two sons that he had been running what amounted to a massive Ponzi scheme on the scale of approximately

How Long and Strong is Trustee Piccard s Claw? On December 10, 2008, Bernard Madoff confessed to his two sons that he had been running what amounted to a massive Ponzi scheme on the scale of approximately

DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C

/\ DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 OFFICE OF THE CHIEF COUNSEL July 3, 2014 Received & In.specf Vice-Chair of the Incentive Auction Task Force Federal Communications

/\ DEPARTMENT OF THE TREASURY INTERNAL REVENUE SERVICE WASHINGTON, D.C. 20224 OFFICE OF THE CHIEF COUNSEL July 3, 2014 Received & In.specf Vice-Chair of the Incentive Auction Task Force Federal Communications

Benjamin E. Gurstelle

Shareholder 2200 IDS Center 80 South Eighth Street Minneapolis, MN 55402 p: 612.977.8722 f: 612.977.8650 bgurstelle@briggs.com Ben Gurstelle is a member of the Business Litigation and Financial Institutions

Shareholder 2200 IDS Center 80 South Eighth Street Minneapolis, MN 55402 p: 612.977.8722 f: 612.977.8650 bgurstelle@briggs.com Ben Gurstelle is a member of the Business Litigation and Financial Institutions

CITY OF HOLLYWOOD POLICE OFFICERS RETIREMENT SYSTEM SECURITIES LITIGATION POLICY

CITY OF HOLLYWOOD POLICE OFFICERS RETIREMENT SYSTEM SECURITIES LITIGATION POLICY I. Principles 1. The Board of Trustees manages the assets entrusted to it in accordance with the prudent expert principle

CITY OF HOLLYWOOD POLICE OFFICERS RETIREMENT SYSTEM SECURITIES LITIGATION POLICY I. Principles 1. The Board of Trustees manages the assets entrusted to it in accordance with the prudent expert principle

Amended and Restated Dividend Reinvestment and Common Stock Purchase Plan

Amended and Restated Dividend Reinvestment and Common Stock Purchase Plan TABLE OF CONTENTS PAGE SUMMARY... 1 AVAILABLE INFORMATION... 2 INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE... 3 FORWARD LOOKING

Amended and Restated Dividend Reinvestment and Common Stock Purchase Plan TABLE OF CONTENTS PAGE SUMMARY... 1 AVAILABLE INFORMATION... 2 INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE... 3 FORWARD LOOKING

RISK AND INSURANCE MANAGEMENT POLICY. Policy 576 i

RISK AND INSURANCE MANAGEMENT POLICY Policy 576 Table of Contents.1 PURPOSE AND POLICY... 1.4 PRACTICES AND PROCEDURES... 1 4.1 DIRECTOR RESPONSIBLE FOR RISK MANAGEMENT FUNCTION... 1 4.2 CLAIMS SETTLEMENT

RISK AND INSURANCE MANAGEMENT POLICY Policy 576 Table of Contents.1 PURPOSE AND POLICY... 1.4 PRACTICES AND PROCEDURES... 1 4.1 DIRECTOR RESPONSIBLE FOR RISK MANAGEMENT FUNCTION... 1 4.2 CLAIMS SETTLEMENT

POLICIES & PROCEDURES MANUAL OF [INSERT COLLECTION AGENCY NAME] [INSERT DATE]

![POLICIES & PROCEDURES MANUAL OF [INSERT COLLECTION AGENCY NAME] [INSERT DATE]](/thumbs/76/73597071.jpg "POLICIES & PROCEDURES MANUAL OF [INSERT COLLECTION AGENCY NAME] [INSERT DATE]") WARNING: This is a sample template of what corporate policies and procedures might look like when attempting to comply with the requirements of the Receivables Management Certification Program. The use

WARNING: This is a sample template of what corporate policies and procedures might look like when attempting to comply with the requirements of the Receivables Management Certification Program. The use

Solving Money Problems

Solving Money Problems 14 th Edition Robin Leonard, J.D. Attorney Margaret Reiter Chapter 1 How Much Do You Owe?... 1 Learning Objectives... 1 Introduction... 1 How Much Do You Earn?... 2 How Much Do You

Solving Money Problems 14 th Edition Robin Leonard, J.D. Attorney Margaret Reiter Chapter 1 How Much Do You Owe?... 1 Learning Objectives... 1 Introduction... 1 How Much Do You Earn?... 2 How Much Do You

IN THE CIRCUIT COURT OF THE STATE OF OREGON FOR THE COUNTY OF WASHINGTON

IN THE CIRCUIT COURT OF THE STATE OF OREGON FOR THE COUNTY OF WASHINGTON UNIFUND CCR PARTNERS ) CASE NO CO50 Plaintiffs ) ) DEMAND FOR DEBT vs ) COLLECTORS VERIFICATION ) PER 15 USC 1692(g) PAUL ) Defendant

IN THE CIRCUIT COURT OF THE STATE OF OREGON FOR THE COUNTY OF WASHINGTON UNIFUND CCR PARTNERS ) CASE NO CO50 Plaintiffs ) ) DEMAND FOR DEBT vs ) COLLECTORS VERIFICATION ) PER 15 USC 1692(g) PAUL ) Defendant

2017 Updates on Tax Ethics

2017 Updates on Tax Ethics Frank J. Rooney, Esquire Rooney Law Firm Offices in CO, MD and VA 303-534-1690 Colorado 703-527-2660 Virginia 301-984-7505 Maryland 703-636-4445 Fax www.irsequalizer.com Course

2017 Updates on Tax Ethics Frank J. Rooney, Esquire Rooney Law Firm Offices in CO, MD and VA 303-534-1690 Colorado 703-527-2660 Virginia 301-984-7505 Maryland 703-636-4445 Fax www.irsequalizer.com Course

EXPAT TAX HANDBOOK. Tax Considerations For Remote Workers Living Abroad

EXPAT TAX HANDBOOK Tax Considerations For Remote Workers Living Abroad Tax Year 2017 Expat Tax Handbook Tax Considerations for Remote Workers Living Abroad Table of Contents: Introduction / 3 U.S. Federal

EXPAT TAX HANDBOOK Tax Considerations For Remote Workers Living Abroad Tax Year 2017 Expat Tax Handbook Tax Considerations for Remote Workers Living Abroad Table of Contents: Introduction / 3 U.S. Federal

Employer Considerations When Offering Health Coverage under the SCA or DBA

Employer Considerations When Offering Health Coverage under the SCA or DBA Employers that are subject to the McNamara-O Hara Service Contract Act (SCA), Davis-Bacon Act (DBA), and Davis-Bacon Related Acts

Employer Considerations When Offering Health Coverage under the SCA or DBA Employers that are subject to the McNamara-O Hara Service Contract Act (SCA), Davis-Bacon Act (DBA), and Davis-Bacon Related Acts

The Internal Revenue Service is aware that certain promoters are advising

Part I Income Taxes Meritless Filing Position Based on Sections 932(c) and 934(b) Notice 2004-45 The Internal Revenue Service is aware that certain promoters are advising taxpayers to take highly questionable,

Part I Income Taxes Meritless Filing Position Based on Sections 932(c) and 934(b) Notice 2004-45 The Internal Revenue Service is aware that certain promoters are advising taxpayers to take highly questionable,

Agent Application: 2. Have you ever had your insurance or securities license suspended or revoked?

Agent Application: Date: / / Business Name: Name (as it appears on license): Residence Address: Street: City: State: Zip: _ Business Address: Street: City: State: Zip: _ Residence Phone: ( ) - Business

Agent Application: Date: / / Business Name: Name (as it appears on license): Residence Address: Street: City: State: Zip: _ Business Address: Street: City: State: Zip: _ Residence Phone: ( ) - Business

New Tax Laws Relating to IRS Examination of and Tax Collection from Partnerships: Implications for Existing and Future Partnership and LLC Agreements

New Tax Laws Relating to IRS Examination of and Tax Collection from Partnerships: Implications for Existing and Future Partnership and LLC Agreements Charles M. Ruchelman, Jonathan S. Brenner, and Rachel

New Tax Laws Relating to IRS Examination of and Tax Collection from Partnerships: Implications for Existing and Future Partnership and LLC Agreements Charles M. Ruchelman, Jonathan S. Brenner, and Rachel

Hewitt Money Market Fund (Nasdaq Ticker Symbol: HEWXX) Series of Hewitt Series Trust

Series of Hewitt Series Trust") Hewitt Money Market Fund (Nasdaq Ticker Symbol: HEWXX) Series of Hewitt Series Trust Prospectus April 30, 2017 The Securities and Exchange Commission ( SEC ) has not approved or disapproved these securities

Hewitt Money Market Fund (Nasdaq Ticker Symbol: HEWXX) Series of Hewitt Series Trust Prospectus April 30, 2017 The Securities and Exchange Commission ( SEC ) has not approved or disapproved these securities

The Anesthesia Company Model: Frequently Asked Questions

The Anesthesia Company Model: Frequently Asked Questions 1. What is the situation in Florida? Florida-specific Issues For several years, FSA members have been contacting the society with reports of company

The Anesthesia Company Model: Frequently Asked Questions 1. What is the situation in Florida? Florida-specific Issues For several years, FSA members have been contacting the society with reports of company

U.S. TaxNotesFOR CANADIANS

BRUNTON S U.S. TaxNotesFOR CANADIANS Covering U.S. Aspects of U.S. Citizens or U.S. Residents with Canadian Income or Assets, Canadians with U.S. Income or Assets 4710 NW 2ND AVENUE, #101, BOCA RATON FL

BRUNTON S U.S. TaxNotesFOR CANADIANS Covering U.S. Aspects of U.S. Citizens or U.S. Residents with Canadian Income or Assets, Canadians with U.S. Income or Assets 4710 NW 2ND AVENUE, #101, BOCA RATON FL

TAX & TRANSACTIONS BULLETIN

Volume 7 On October 22, 2004, President Bush signed the American Jobs Creation Act of 2004 ( Act ). The Act s main purpose is to repeal the extraterritorial income exclusion (ETI). To compensate U.S. manufacturers

Volume 7 On October 22, 2004, President Bush signed the American Jobs Creation Act of 2004 ( Act ). The Act s main purpose is to repeal the extraterritorial income exclusion (ETI). To compensate U.S. manufacturers

FORGIVE AND FORGET - - THE CALIFORNIA EMPLOYMENT TAX AMNESTY. By Steven Toscher, Esq. March, 1995

FORGIVE AND FORGET - - THE CALIFORNIA EMPLOYMENT TAX AMNESTY By Steven Toscher, Esq. March, 1995 INTRODUCTION Should a taxing authority be able to forgive and forget - - that is, grant amnesty to taxpayers

FORGIVE AND FORGET - - THE CALIFORNIA EMPLOYMENT TAX AMNESTY By Steven Toscher, Esq. March, 1995 INTRODUCTION Should a taxing authority be able to forgive and forget - - that is, grant amnesty to taxpayers

GDPR Essentials. To Meet the May 25th Deadline. FIA Webinar March 1, 2018

GDPR Essentials To Meet the May 25th Deadline FIA Webinar March 1, 2018 3/1/2018 1 Administrative Items The webinar will be recorded and posted to the FIA website following the conclusion of the live webinar.

GDPR Essentials To Meet the May 25th Deadline FIA Webinar March 1, 2018 3/1/2018 1 Administrative Items The webinar will be recorded and posted to the FIA website following the conclusion of the live webinar.

Power Source SM New Business Application (for private companies with up to 250 employees)

") BY COMPLETING THIS APPLICATION YOU ARE APPLYING FOR COVERAGE WITH EXECUTIVE RISK INDEMNITY INC. (THE COMPANY ) NOTICE: THE LIABILITY COVERAGE SECTIONS OF POWER SOURCE SM PROVIDE CLAIMS MADE COVERAGE, WHICH

BY COMPLETING THIS APPLICATION YOU ARE APPLYING FOR COVERAGE WITH EXECUTIVE RISK INDEMNITY INC. (THE COMPANY ) NOTICE: THE LIABILITY COVERAGE SECTIONS OF POWER SOURCE SM PROVIDE CLAIMS MADE COVERAGE, WHICH

Ethical Behavior Our Common Obligation

Ethical Behavior Our Common Obligation Donald Griswold, Reed Smith LLP Southeastern Association of Tax Administrators Annual Conference White Sulphur Springs, WV 23 July 2012 DOC#109561769 Overview Goals

Ethical Behavior Our Common Obligation Donald Griswold, Reed Smith LLP Southeastern Association of Tax Administrators Annual Conference White Sulphur Springs, WV 23 July 2012 DOC#109561769 Overview Goals

Effective Date: 1/01/07 N/A

North Shore-LIJ Health System is now Northwell Health POLICY TITLE: Detecting and Preventing Fraud, Waste, Abuse and Misconduct POLICY #: 800.09 System Approval Date: 03/30/2017 Site Implementation Date:

North Shore-LIJ Health System is now Northwell Health POLICY TITLE: Detecting and Preventing Fraud, Waste, Abuse and Misconduct POLICY #: 800.09 System Approval Date: 03/30/2017 Site Implementation Date:

Attorney Advertising

Attorney Advertising For half a century, Caplin & Drysdale has been a leading provider of tax and related legal services to businesses, nonprofits, and individuals throughout the United States and around

Attorney Advertising For half a century, Caplin & Drysdale has been a leading provider of tax and related legal services to businesses, nonprofits, and individuals throughout the United States and around

14 - IRS Didn't Prove That Taxpayer Convicted of Filing False Returns Intended to Evade Tax

14 - IRS Didn't Prove That Taxpayer Convicted of Filing False Returns Intended to Evade Tax Mathews, TC Memo 2018-212 The Tax Court has held that, although the taxpayer was convicted of filing false income

14 - IRS Didn't Prove That Taxpayer Convicted of Filing False Returns Intended to Evade Tax Mathews, TC Memo 2018-212 The Tax Court has held that, although the taxpayer was convicted of filing false income

DEVELOPING AND IMPLEMENTING PROCEDURES FOR POST-ISSUANCE TAX COMPLIANCE FOR ISSUERS OF GOVERNMENTAL BONDS GFOA DEBT COMMITTEE

DEVELOPING AND IMPLEMENTING PROCEDURES FOR POST-ISSUANCE TAX COMPLIANCE FOR ISSUERS OF GOVERNMENTAL BONDS GFOA DEBT COMMITTEE AUGUST 2016 DEVELOPING AND IMPLEMENTING PROCEDURES FOR POST-ISSUANCE TAX COMPLIANCE

DEVELOPING AND IMPLEMENTING PROCEDURES FOR POST-ISSUANCE TAX COMPLIANCE FOR ISSUERS OF GOVERNMENTAL BONDS GFOA DEBT COMMITTEE AUGUST 2016 DEVELOPING AND IMPLEMENTING PROCEDURES FOR POST-ISSUANCE TAX COMPLIANCE

AMENDED BRIEF IN SUPPORT OF JURISDICTION

KARIM GHANEM, vs. Petitioner, STATE OF FLORIDA, Respondent. / IN THE SUPREME COURT OF FLORIDA CASE NO. SC05-1860 Lower Tribunal No: 4D03-743 AMENDED BRIEF IN SUPPORT OF JURISDICTION [PETITION FOR WRIT

KARIM GHANEM, vs. Petitioner, STATE OF FLORIDA, Respondent. / IN THE SUPREME COURT OF FLORIDA CASE NO. SC05-1860 Lower Tribunal No: 4D03-743 AMENDED BRIEF IN SUPPORT OF JURISDICTION [PETITION FOR WRIT

PUBLISH UNITED STATES COURT OF APPEALS TENTH CIRCUIT. Plaintiffs - Appellees, v. No UNITED STATES OF AMERICA,

FILED United States Court of Appeals Tenth Circuit July 23, 2010 PUBLISH Elisabeth A. Shumaker Clerk of Court UNITED STATES COURT OF APPEALS TENTH CIRCUIT CARLOS E. SALA; TINA ZANOLINI-SALA, Plaintiffs

FILED United States Court of Appeals Tenth Circuit July 23, 2010 PUBLISH Elisabeth A. Shumaker Clerk of Court UNITED STATES COURT OF APPEALS TENTH CIRCUIT CARLOS E. SALA; TINA ZANOLINI-SALA, Plaintiffs

JACKSONVILLE POLICE AND FIRE PENSION FUND Standard Procedures Manual

15 (b) 1 of 6 to be determined I. Principles 1. The Board of Trustees manages the assets entrusted to it in accordance with the prudent expert principle which requires that the Board act with the care,

15 (b) 1 of 6 to be determined I. Principles 1. The Board of Trustees manages the assets entrusted to it in accordance with the prudent expert principle which requires that the Board act with the care,

Dallas Bar Association Tax Section December 4, New Partnership Audit Rules: What They Mean to Partnerships and Tax Professionals.

Dallas Bar Association Tax Section December 4, 2017 New Partnership Audit Rules: What They Mean to Partnerships and Tax Professionals Copyright All rights reserved. Presented By: Charles D. Pulman, J.D.,

Dallas Bar Association Tax Section December 4, 2017 New Partnership Audit Rules: What They Mean to Partnerships and Tax Professionals Copyright All rights reserved. Presented By: Charles D. Pulman, J.D.,

GEORGIA ATTORNEY PREFERENCE NOTICE

GEORGIA ATTORNEY PREFERENCE NOTICE Borrower (s): Lender: Property Address: Loan Number: Date: I understand that I have the right to select a qualified attorney to conduct the title search and loan closing,

GEORGIA ATTORNEY PREFERENCE NOTICE Borrower (s): Lender: Property Address: Loan Number: Date: I understand that I have the right to select a qualified attorney to conduct the title search and loan closing,

BROAD and CASSEL One Biscayne Tower, 21st Floor 2 South Biscayne Blvd. Miami, Florida

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA FORT MYERS DIVISION CASE NO.: 2:09-CV-229-FTM-29SPC SECURITIES AND EXCHANGE COMMISSION, vs. Plaintiff, FOUNDING PARTNERS CAPITAL MANAGEMENT, and

UNITED STATES DISTRICT COURT MIDDLE DISTRICT OF FLORIDA FORT MYERS DIVISION CASE NO.: 2:09-CV-229-FTM-29SPC SECURITIES AND EXCHANGE COMMISSION, vs. Plaintiff, FOUNDING PARTNERS CAPITAL MANAGEMENT, and

DATE: October 16, 2008 SUBJECT: NCITD Meeting of October 8, 2008

DATE: October 16, 2008 SUBJECT: NCITD Meeting of October 8, 2008 This memorandum summarizes the presentations and discussion at the National Council on International Trade Development ( NCITD ) Trade Compliance

DATE: October 16, 2008 SUBJECT: NCITD Meeting of October 8, 2008 This memorandum summarizes the presentations and discussion at the National Council on International Trade Development ( NCITD ) Trade Compliance

Federal Estate, Gift and GST Tax Exemptions and Exclusions in 2017 and 2018

Six Landmark Square 3001 Tamiami Trail North Stamford, CT 06902 Naples, FL 34103 203.327.1700 Phone 239.262.8311 Phone 203.351.4534 Fax 239.263.07032 Fax Two Greenwich Plaza 8000 Health Center Blvd., Suite

Six Landmark Square 3001 Tamiami Trail North Stamford, CT 06902 Naples, FL 34103 203.327.1700 Phone 239.262.8311 Phone 203.351.4534 Fax 239.263.07032 Fax Two Greenwich Plaza 8000 Health Center Blvd., Suite

NOTICE OF PRIVACY PRACTICES FOR PROTECTED HEALTH INFORMATION

THIS NOTICE DESCRIBES HOW MEDICAL INFORMATION ABOUT YOU MAY BE USED AND DISCLOSED AND HOW YOU CAN GET ACCESS TO THIS INFORMATION, PLEASE REVIEW IT CAREFULLY. This notice is provided to you on behalf of

THIS NOTICE DESCRIBES HOW MEDICAL INFORMATION ABOUT YOU MAY BE USED AND DISCLOSED AND HOW YOU CAN GET ACCESS TO THIS INFORMATION, PLEASE REVIEW IT CAREFULLY. This notice is provided to you on behalf of

Physician Contracts GOVERNANCE THOUGHT LEADERSHIP SERIES

Providing education, resources, leadership development to inspire excellence in health care governance. Hospitals regularly contract for many products and services ranging from the linens used in patient

Providing education, resources, leadership development to inspire excellence in health care governance. Hospitals regularly contract for many products and services ranging from the linens used in patient

100 William Street New Business Application New York, NY 10038

BY COMPLETING THIS APPLICATION YOU ARE APPLYING FOR COVERAGE WITH HUDSON INSURANCE COMPANY (THE COMPANY ) NOTICE: THE LIABILITY COVERAGE PART SECTIONS OF PRIVATE DEFENDER PROVIDE CLAIMS MADE COVERAGE,

BY COMPLETING THIS APPLICATION YOU ARE APPLYING FOR COVERAGE WITH HUDSON INSURANCE COMPANY (THE COMPANY ) NOTICE: THE LIABILITY COVERAGE PART SECTIONS OF PRIVATE DEFENDER PROVIDE CLAIMS MADE COVERAGE,

Fay Servicing, LLC 901 S. 2 nd St., Suite 201 Springfield, IL 62704

RE: Identity Theft Claim You recently notified Fay Servicing, LLC that you are the victim of identity theft with respect to the above referenced loan (also referred to in this notice as the debt or account

RE: Identity Theft Claim You recently notified Fay Servicing, LLC that you are the victim of identity theft with respect to the above referenced loan (also referred to in this notice as the debt or account

FILED: NEW YORK COUNTY CLERK 03/26/ :33 PM INDEX NO /2015 NYSCEF DOC. NO. 1 RECEIVED NYSCEF: 03/26/2015

FILED: NEW YORK COUNTY CLERK 03/26/2015 07:33 PM INDEX NO. 650988/2015 NYSCEF DOC. NO. 1 RECEIVED NYSCEF: 03/26/2015 SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK MACQUARIE CAPITAL (USA) INC.,

FILED: NEW YORK COUNTY CLERK 03/26/2015 07:33 PM INDEX NO. 650988/2015 NYSCEF DOC. NO. 1 RECEIVED NYSCEF: 03/26/2015 SUPREME COURT OF THE STATE OF NEW YORK COUNTY OF NEW YORK MACQUARIE CAPITAL (USA) INC.,