Filing of Service Tax Return

|

|

|

- Gabriella Townsend

- 6 years ago

- Views:

Transcription

Shah Organised by: WIRC-ICAI On: th 10 March,")

1 Filing of Service Tax Return Presented by: CA Prerana (Payal) Shah Organised by: WIRC-ICAI On: th 10 March, 2017

2 2

3 Why is it important to file Service tax returns? 3

4 Bullets Service tax return GST 4

5 Taxability CENVAT Credit Classification Provisions determining liability under Service tax Place of Provision of Services RCM Components & Rate of Service tax Valuation Point of taxation 5

6 ST Return Mr. Samay had delayed ST registration by 1 year. Mr. Samay has deposited ST with interest to Government Treasury. Consequently, Mr. Samay wants to file ST return for the periods prior to registration. Is it possible? Not required No such provision in law Possible Section 73(3) of the FA, 1994 Intimation to be filed with the department No levy of penalty when ST with interest paid before issuance of SCN Pay late filing fees?? 6

7 FORM ST-3 7

8 Form ST

9 Form ST

10 Form ST

11 Form ST

12 Form ST

13 Form ST

14 Form ST

15 Form ST

16 Form ST

17 Form ST

18 Form ST

19 Form ST

20 Form ST

21 Form ST

22 Form ST

23 Form ST

24 Form ST

25 Form ST

26 Form ST

27 Form ST

28 Form ST

29 Form ST

30 Form ST

31 Form ST

32 Form ST

33 Form ST

34 Form ST

35 Form ST

36 Form ST

37 Form ST

38 Form ST

39 Form ST

40 Form ST

41 Form ST

42 Form ST

43 Form ST

44 Form ST

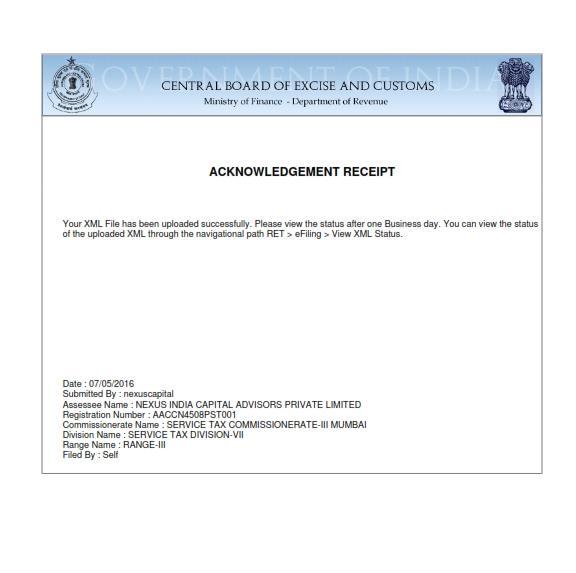

45 ST Return How to fill offline utility of ST return? Offline Utility Uploading procedure Always download new version of ST from Acknowledgement Check after 1 business day Status should be FILED Print acknowledgement receipt Whether online utility available for ST returns. Yes Mandatory e-filing for all assessees 45

46 Service Tax Log-in screen 46

47 .. Form ST

48 .. Form ST

49 Form ST-3 49

50 Form ST-3 50

51 Form ST-3 51

52 Print Acknowledgment Receipt 52

53 Uploaded-Ack. 53

54 Filed-Ack. 54

55 ST Return ST return is filed on 25th April, However, the same got rejected by system due to some technical error. Can it be considered as return filed on time? Circular No. 956/17/2011-ST dated 28th September, 2011 In case a return is rejected by the application, the date of uploading of the rejected return will not be considered as the date of filing, rather the date of uploading of the successfully filed, return (after the assessee carries out necessary corrections and uploads it again) will be considered as the actual date of filing Section 70 of the FA, 1994 read with Rule 7 of STR, 1994 Words used are Furnish ; Submit Whether the above circular is binding on the assessee CCE vs. Ratan Melting and Wire Industries 2008 (12) STR 416 (SC)» Circulars binding on department not on Court» Circulars contrary to statutory provisions has no existence in law 55

Every assessee Para 4.")

56 ST Return Whether the assessee is required to file NIL return in case there is no taxable services provided and no payments received during a return period. Section 70 of the FA, 1994 Every person liable to pay the service tax Rule 7 of the STR, 1994 (1) Every assessee Para 4.9 of the FAQs issued by CBEC & DGST on 1st September, rd Proviso to Rule 7C of STR, 1994 Penalty can be waived if NIL return B & A Multiwall Packaging Ltd. vs. CCE, BBSR I 2006 (3) STR 673 (Tri.-Kolkata) What if the last date for filing is a public holiday? Circular No. 63/12/2003-S.T., dated 14th October,

57 ST Return CENVAT Credit availed shown under Central Excise returns and not under Service tax returns. Whether this is a mistake? No Pipavav Shipyard Ltd. vs. CCE & ST, Bhavnagar 2016 (41) STR 151 (Tri.-Ahmd.) admitted to High Court in 2016 (45) STR J217 (Guj.) What if Service tax return does not match with income tax return? Scrutiny required ALP Management Consultants Pvt. Ltd. vs. Commr. of S. T., Bangalore 2006 (4) STR 21 (Tri.-Bang.) 57

58 ST Return Can the Original Return filed after due date, be revised within the time frame of 90 days? Rule 7B of the STR, 1994 from the date of submission of the return under rule days to be counted from when: From the date of filing original ST return or from the due date of filing original return? Rule 7B of the STR, 1994 from the date of submission of the return under rule 7 What if the assessee realised mistake after 90 days from the date of filing original return? No provision in Law File intimation letter 58

59 ST Return ST RC is surrendered. However, the department has not closed the procedure of surrender. Should the assessee file NIL ST return till the time department accepts surrender of ST RC? No Penalty vs. late filing fees Worded as late filling fees but penalty 3rd Proviso to Rule 7C of the STR, 1994 ST payable NIL + sufficient reason Penalty can be waived 59

60 ST Return Mr. Ghanchakkar was engaged in providing 10 different categories of services Mr. Ghanchakkar got registered under only 1 category of service on time 9 other services were registered after a gap of 6 months He had provided services only under 1 category of services during the period July to September, 2012 Accordingly, he filed return only under such 1 category of service. Whether department can levy Penalty for all other 9 services. Circular No. 76/6/2004-ST dated 3rd March, 2004 Only 1 penalty can be imposed 60

61 ST Return Probable errors while filing Service tax returns Challan does not exist Opening balance of CENVAT Credit Rounding off errors Difference between liability and payment/cenvat utilization Excess Service tax paid Presentation Issue 61

62 Practical Tips Download the latest version of forms from Keep snapshot of each procedure made online Wherever required, file intimations with ST department Be careful in drafting these intimation letters Be extra careful in filing last return under Pre-GST Regime Do not hesitate to contact ST experts Get confirmation from clients before filing applications / forms / letters with the department If wrong ID or password is entered continuously for 5 times, the account gets blocked and the ACES registration procedure needs to be repeated 62

63 63

64 64

65 GST Based on November 2016 Model GST Law 65

66 Case Study Old Credits can be availed under GST? M/s. Forgetful Pvt. Ltd. forgot to avail CENVAT Credit of Service tax paid on various input services such as advertisement, rent etc. amounting to Rs. 1.5 Crore GST regime got implemented While finalising Books of Accounts, M/s. Forgetful Pvt. Ltd. realises the fact of nonavailment of CENVAT Credit Whether M/s. Forgetful Pvt. Ltd. can avail such credits under GST? Most Crucial Return-Last return under old Laws 66

Registered Person (Other than Composition Tax payer under GST Act)")

67 Cenvat Credit admissible as ITC (Sec. 167-CGST) Registered Person (Other than Composition Tax payer under GST Act) Provided that the said credit is admissible under GST Act CENVAT Credit of Earlier Laws carried forward in last return furnished under earlier law Entitled to be credited in Electronic credit Ledger 67

68 Unutilized Cenvat credit of Centralized Registrations (Sec. 191-CGST) Registered taxable person having centralized registration under earlier laws shall be allowed to take credit of cenvat carried forward in last return if: Registered under GST Act Return is filed within 3 months of appointed day Amount of credit as appearing in original return or reduced amount as appearing in revised return Such credit admissible under GST Act Credit may be transferred to taxable person having same PAN and registered under earlier law 68

69 Return filed under earlier laws Revision of Returns (Sec. 185-CGST & SGST) Recover as arrears under GST Act Amount of tax is recoverable or credit is inadmissible No ITC under GST Act Revised after appointed day Amount found to be refundable or credit found admissible If return revised within time limit as prescribed in earlier law Refund in Cash irrespective of provisions of earlier law except 11B (2) (CGST) Refund in accordance with provisions of earlier law (SGST) 69

70 70

71 Believe in self and never ever give up 71

72 Overnight Success??? Hard Work + Determination + Interest + Passion 72

73 73

, Mumbai-400 069.")

74 Our Offices: West Region: 2/19 Nityanand Nagar, Sahar Road, Andheri (East), Mumbai North Region: A-36, First Floor, Ring Road, Adjacent to Raja Garden Flyover, Rajouri Garden, New Delhi East Region: 406A - 406B, 4th Floor, Todi Chamber, 2, Lal Bazar Street, Kolkata preranashah@gscintime.com info@gscintime.com South Region: 64, Thirumalai Pillai Road, T. Nagar, Chennai

E-filing under Service Tax

E-filing under Service Tax Presented by: Ca. Prerana Shah Organised by: WIRC-ICAI Bullets Registrations Payments Returns Misc. 5/7/2016 Ca. Payal (Prerana) Shah 2 REGISTRATION 5/7/2016 Ca. Payal (Prerana)

E-filing under Service Tax Presented by: Ca. Prerana Shah Organised by: WIRC-ICAI Bullets Registrations Payments Returns Misc. 5/7/2016 Ca. Payal (Prerana) Shah 2 REGISTRATION 5/7/2016 Ca. Payal (Prerana)

Update on amendments made in GST Law on 13 th October 2017 in view of various recommendations made by GST Council

Update on amendments made in GST Law on 13 th October in view of various recommendations made by GST Council No Reverse Charge with respect to purchase from unregistered persons till 31 st March 2018:

Update on amendments made in GST Law on 13 th October in view of various recommendations made by GST Council No Reverse Charge with respect to purchase from unregistered persons till 31 st March 2018:

Relief to Exporters by GST Council on 6 th October,

Relief to Exporters by GST Council on 6 th October, 2017 1 GST Council had set up a high power Committee for exports under Revenue Secretary Mr. Hasmukh Adhia in September, 2017 to recommend strategies

Relief to Exporters by GST Council on 6 th October, 2017 1 GST Council had set up a high power Committee for exports under Revenue Secretary Mr. Hasmukh Adhia in September, 2017 to recommend strategies

Service tax. Key Budget Proposals and Amendments. Union Budget

Key Budget Proposals and Amendments Union Budget 2017-2018 2/19, Nitya Priya, Nityanand Nagar, Sahar Road, Andheri (East), Mumbai-400 069. 03/02/2017 Contents 1. Retrospective Amendment in Valuation of

Key Budget Proposals and Amendments Union Budget 2017-2018 2/19, Nitya Priya, Nityanand Nagar, Sahar Road, Andheri (East), Mumbai-400 069. 03/02/2017 Contents 1. Retrospective Amendment in Valuation of

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC 3rd October Presenter CA Mandar Telang

organised by WIRC 3rd October Presenter CA Mandar Telang") Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Beginners Course on GST (Registration, Returns, Payment & Documentation) organised by WIRC Presenter CA Mandar Telang 1 Registration 2 Registration Legal Framework v Taxable Person means a person who carries

Registration, returns & TRANSITIONAL PROVISIONS

1 www.ada.org.in/gstindia.biz Registration, returns & TRANSITIONAL PROVISIONS Ashu Dalmia Partner Ashu Dalmia & Associates FCA,DISA,CISA ICAI Certified-FAFD,ICAI-Certified Arbitrator Special Auditor u/s

1 www.ada.org.in/gstindia.biz Registration, returns & TRANSITIONAL PROVISIONS Ashu Dalmia Partner Ashu Dalmia & Associates FCA,DISA,CISA ICAI Certified-FAFD,ICAI-Certified Arbitrator Special Auditor u/s

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR

TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR") GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GST THIS WEEK. GST Update No. 02/2017/KMS IN THIS UPDATE. 27 th Feb 5 th Mar, 2017

GST Update No. 02/2017/KMS GST THIS WEEK 27 th Feb 5 th Mar, 2017 IN THIS UPDATE Flow chart on tax treatment on services or goods where Tax has been payable under the earlier law & Service Tax credit distributed

GST Update No. 02/2017/KMS GST THIS WEEK 27 th Feb 5 th Mar, 2017 IN THIS UPDATE Flow chart on tax treatment on services or goods where Tax has been payable under the earlier law & Service Tax credit distributed

GST Update. Weekly Update N a t i o n a l A c a d e m y o f C u s t o m s, I n d i r e c t T a x e s a n d N a r c o t i c s ( N A C I N )

") GST Update Weekly Update 02.02.2019 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 26.01.2019.

GST Update Weekly Update 02.02.2019 1 Background This Presentation covers the GST changes / observations/ press releases/ Tweet FAQs/ Sectoral FAQs released by CBEC since the last update on 26.01.2019.

SERVICE TAX REGISTRATION, PAYMENTS & RETURNS

SERVICE TAX REGISTRATION, PAYMENTS & RETURNS Prepared By On Sunday 6 th April, 2014 Organised By INDEX Sl. No. TOPICS PG. NO. 1 Service Tax Registration 2 2 Service Tax Payments 9 3 Service Tax Returns

SERVICE TAX REGISTRATION, PAYMENTS & RETURNS Prepared By On Sunday 6 th April, 2014 Organised By INDEX Sl. No. TOPICS PG. NO. 1 Service Tax Registration 2 2 Service Tax Payments 9 3 Service Tax Returns

Transitional Provisions in GST... by Raman Gupta

Transitional Provisions in GST... by Raman Gupta Section 141- General Provisions Persons working in Service Tax Department, Excise Department, various State VAT Departments and other indirect tax departments

Transitional Provisions in GST... by Raman Gupta Section 141- General Provisions Persons working in Service Tax Department, Excise Department, various State VAT Departments and other indirect tax departments

Invoice, Accounting and TRAN1 form under GST

Invoice, Accounting and TRAN1 form under GST Basic Understanding: 1. GST is leviable on SUPPLY made for CONSIDERATION made at a PLACE on a VALUE at such RATE on such TIME - PLACE: Supply Within State -

Invoice, Accounting and TRAN1 form under GST Basic Understanding: 1. GST is leviable on SUPPLY made for CONSIDERATION made at a PLACE on a VALUE at such RATE on such TIME - PLACE: Supply Within State -

TRANSITIONAL PROVISIONS. CA. PUNEET OBEROI FCA, DISA

TRANSITIONAL PROVISIONS CA. PUNEET OBEROI FCA, DISA 9779344448 puneet@poc-ca.com SCHEME OF TRANSITIONAL PROVISIONS MGL FUNCTIONAL CGST-SEC. 165 TO 197 (Chapter XXVII) IGST- SEC. 21 TRANSITION OF DEPARTMENT

TRANSITIONAL PROVISIONS CA. PUNEET OBEROI FCA, DISA 9779344448 puneet@poc-ca.com SCHEME OF TRANSITIONAL PROVISIONS MGL FUNCTIONAL CGST-SEC. 165 TO 197 (Chapter XXVII) IGST- SEC. 21 TRANSITION OF DEPARTMENT

Transitional Provisions

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

FAQ s Migration of Existing Tax Payers (Section 139) Similar provisions have been specified in the UTGST Act, 2017 Chapter XVIII Transitional Provisions Q1. What is the primary condition for provisional

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

FILING OF RETURNS UNDER GST INCLUDING MATCHING OF INPUT TAX CREDIT DRAFT RETURN FORMS FORM NO DETAILS 1. GSTR 1 Details of outward supplies of taxable goods and/or services effected 2. GSTR 01A Details

The Empowered Committee of State Finance Ministers have worked out a dual GST model for India. In

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

BUSINESS PROCESSES ON GST RETURN

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues and Challenges"

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues

Khandhar Mehta & Shah 1

Khandhar Mehta & Shah 1 KMS Intellectus # 6 TDS under GST Provision on TDS Requirement of TDS Persons liable to deduct TDS Persons not liable to deduct TDS Registration for TDS Payment of TDS TDS Return

Khandhar Mehta & Shah 1 KMS Intellectus # 6 TDS under GST Provision on TDS Requirement of TDS Persons liable to deduct TDS Persons not liable to deduct TDS Registration for TDS Payment of TDS TDS Return

Khandhar Mehta & Shah. Concept of Composition Scheme under GST. KMS Intellectus # 2 KMS/GST/ /02

Khandhar Mehta & Shah 1 KMS Intellectus # 2 Concept of Composition Scheme under GST Basic requirements under Composition Scheme Flow chart to decide eligibility Calculation of Turnover Procedural Requirement

Khandhar Mehta & Shah 1 KMS Intellectus # 2 Concept of Composition Scheme under GST Basic requirements under Composition Scheme Flow chart to decide eligibility Calculation of Turnover Procedural Requirement

Tweet FAQs. The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets.

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 100 tweets. S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include

Tweet FAQs. S. No. Questions / Tweets Received Replies. Registration

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 50 tweets. It should be noted that the tweets received or the replies quoted are only for educational

Tweet FAQs The tweets received by askgst_goi handle were scrutinized and developed into a short FAQ of 50 tweets. It should be noted that the tweets received or the replies quoted are only for educational

A COMPREHENSIVE GST CHECKLIST BEFORE FINALISATION OF BALANCE SHEET FOR THE FY FOR REGISTERED PERSONS - PART 3

A COMPREHENSIVE GST CHECKLIST BEFORE FINALISATION OF BALANCE SHEET FOR THE FY 2017-2018 FOR REGISTERED PERSONS - PART 3 CMA SUSANTA KUMAR SAHA GST Consultant This being the concluding part of this series

A COMPREHENSIVE GST CHECKLIST BEFORE FINALISATION OF BALANCE SHEET FOR THE FY 2017-2018 FOR REGISTERED PERSONS - PART 3 CMA SUSANTA KUMAR SAHA GST Consultant This being the concluding part of this series

Finalisation of Accounts from GST Perspective

Finalisation of Accounts from GST Perspective Ashish Kedia WIRC 7 th July, 2018 Broadly can be divided into 3 broad areas Input, Output and Tax payable Output side requires maintenance of various accounts

Finalisation of Accounts from GST Perspective Ashish Kedia WIRC 7 th July, 2018 Broadly can be divided into 3 broad areas Input, Output and Tax payable Output side requires maintenance of various accounts

IGP-CS CS PROFESSIONAL ADVANCED TAX CA VIVEK GABA GST IN INDIA AN INTRODUCTION SUPPLY UNDER GST

GST IN INDIA AN INTRODUCTION Q1. Discuss how GST resolved the double taxation dichotomy under previous indirect tax laws. Q2. Enumerate the deficiencies of the existing indirect taxes which led to the

GST IN INDIA AN INTRODUCTION Q1. Discuss how GST resolved the double taxation dichotomy under previous indirect tax laws. Q2. Enumerate the deficiencies of the existing indirect taxes which led to the

CENVAT CREDIT Recent Court Rulings Presented by: Ca. Jayesh Gogri

CENVAT CREDIT Recent Court Rulings Presented by: Ca. Jayesh Gogri 7/2/13 CA JAYESH Organised GOGRI by: 1 Wrong availment of CENVAT Credit and interest thereon Mr. Inamdaar was engaged in the manufacture

CENVAT CREDIT Recent Court Rulings Presented by: Ca. Jayesh Gogri 7/2/13 CA JAYESH Organised GOGRI by: 1 Wrong availment of CENVAT Credit and interest thereon Mr. Inamdaar was engaged in the manufacture

Goods and Services Tax CA. Sathish V & CA. Krishna J August 2017

Goods and Services Tax CA. Sathish V & CA. Krishna J August 2017 Slide 1 Table of Contents 1 Input service distribution 2 E-Commerce in GST 3 Job work - an overview 4 Job work procedures in GST 5 Transition

Goods and Services Tax CA. Sathish V & CA. Krishna J August 2017 Slide 1 Table of Contents 1 Input service distribution 2 E-Commerce in GST 3 Job work - an overview 4 Job work procedures in GST 5 Transition

FAQ on filing of Transition form

FAQ on filing of Transition form 1. What is the requirement for filing transition Form GST TRAN - 1? Every registered person in GST would be required to file form GST TRAN-1 to carry forward credit of

FAQ on filing of Transition form 1. What is the requirement for filing transition Form GST TRAN - 1? Every registered person in GST would be required to file form GST TRAN-1 to carry forward credit of

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

Whether supply of goods with transportation services - naturally bundled and treated as composite supply.

25 th J U N E 2018 This alert summaries the following writ petitions & AAR filed and outcome of such petitions. The key issues raised before the courts and Authority for Advance Ruling are : AAR Ruling

25 th J U N E 2018 This alert summaries the following writ petitions & AAR filed and outcome of such petitions. The key issues raised before the courts and Authority for Advance Ruling are : AAR Ruling

GOODS AND SERVICES TAX

GOODS AND SERVICES TAX TRANSITIONAL CREDITS AND DEMONSTRATION OF FILING OF TRAN-1 Two days webcast on GST Organised by: Indirect Taxes Committee GENERAL PRINCIPLES RELATING TO TRANSITION a) Every person

GOODS AND SERVICES TAX TRANSITIONAL CREDITS AND DEMONSTRATION OF FILING OF TRAN-1 Two days webcast on GST Organised by: Indirect Taxes Committee GENERAL PRINCIPLES RELATING TO TRANSITION a) Every person

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act.

of CGST Act.") S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

S. No. Questions / Tweets Received Replies Registration 1. Does aggregate turnover include value of inward supplies Refer Section 2(6) of CGST Act. received on which RCM is payable? Aggregate turnover

GST: Transitional Provisions

GST: Transitional Provisions Edition 1 Contents Administration under GST [S.165] Migration of Existing taxpayers [S.166] Input Tax Credits [S.167 to 172] Goods sent for Job work [S.173 to S.177] 2 Section

GST: Transitional Provisions Edition 1 Contents Administration under GST [S.165] Migration of Existing taxpayers [S.166] Input Tax Credits [S.167 to 172] Goods sent for Job work [S.173 to S.177] 2 Section

CA. Annapurna Kabra

By CA. Annapurna Kabra 9972077441 I) Payment under GST Type of payment Due date Modes of payment with Rules and collection of tax Collection of incorrect amount / rate of GST Omission to collect GST in

By CA. Annapurna Kabra 9972077441 I) Payment under GST Type of payment Due date Modes of payment with Rules and collection of tax Collection of incorrect amount / rate of GST Omission to collect GST in

Refunds. Chapter IX. FAQ s. Refund of tax (Section 54)

") FAQ s Refund of tax (Section 54) Chapter IX Refunds Q1. Is the word refund defined in the CGST Act? Ans. Yes, the word refund is defined in explanation to Section 54 of the CGST Act, 2017. As per the said

FAQ s Refund of tax (Section 54) Chapter IX Refunds Q1. Is the word refund defined in the CGST Act? Ans. Yes, the word refund is defined in explanation to Section 54 of the CGST Act, 2017. As per the said

GST - Input Tax Credit. Keval Shah at Bandra Kurla Complex, WIRC of the ICAI. Agenda for the day. Provisions of Input Tax Credit

2 GST - Input Tax Credit Keval Shah at Bandra Kurla Complex, WIRC of the ICAI June 16 2017 Agenda for the day Provisions of Input Tax Credit Concept of Input Service Distributor Transitional provisions

2 GST - Input Tax Credit Keval Shah at Bandra Kurla Complex, WIRC of the ICAI June 16 2017 Agenda for the day Provisions of Input Tax Credit Concept of Input Service Distributor Transitional provisions

National conclave on GST Transitional Credit Issues and recap of MVAT Audit organized by CPE Committee, ICAI hosted by WIRC of ICAI

National conclave on GST Transitional Credit Issues and recap of MVAT Audit organized by CPE Committee, ICAI hosted by WIRC of ICAI Presentation by Rajat Talati Chartered Accountant On 29 th December 2018

National conclave on GST Transitional Credit Issues and recap of MVAT Audit organized by CPE Committee, ICAI hosted by WIRC of ICAI Presentation by Rajat Talati Chartered Accountant On 29 th December 2018

GSTR - 3B Dec 3B Jan 3B Feb 3B Mar 3B Apr 3B GSTR -1 July to Nov 2017 Dec 2017 Jan 2018 Feb 2018 Mar 2018

Circular No. 26/26/2017-GST F. No. 349/164/2017/-GST Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs GST Policy Wing New Delhi, Dated the 29 th December,

Circular No. 26/26/2017-GST F. No. 349/164/2017/-GST Government of India Ministry of Finance Department of Revenue Central Board of Excise and Customs GST Policy Wing New Delhi, Dated the 29 th December,

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

Chapter IX Returns Statutory Provision 37. Furnishing details of outward supplies (1) Every registered taxable person, other than an input service distributor, a non-resident taxable person and a person

WIRC of ICAI. Understanding Annual Returns & Reconciliation Statement. Presented By CA. Kevin Shah

WIRC of ICAI Understanding Annual Returns & Reconciliation Statement Presented By CA. Kevin Shah STATUTORY PROVISIONS Section 35 (5) of the CGST Act, 2017 (5) Every registered person whose turnover during

WIRC of ICAI Understanding Annual Returns & Reconciliation Statement Presented By CA. Kevin Shah STATUTORY PROVISIONS Section 35 (5) of the CGST Act, 2017 (5) Every registered person whose turnover during

Procedures under GST BY CA LAKSHMI G K. Hiregange & Associates

Procedures under GST BY CA LAKSHMI G K 1 Coverage Procedure to register under GST Procedure to supply goods Books of accounts to be maintained under GST Procedure to pay GST Procedure to file returns under

Procedures under GST BY CA LAKSHMI G K 1 Coverage Procedure to register under GST Procedure to supply goods Books of accounts to be maintained under GST Procedure to pay GST Procedure to file returns under

IGST REFUNDS - EXPORTS ROLE OF CUSTOMS

IGST REFUNDS - EXPORTS ROLE OF CUSTOMS BACKGROUND OF IGST REFUNDS ON EXPORTS Exports : Zero-Rated Supply: Eligible to Claim Refund As per Sec 2(23) of IGST Act: zero-rated supply shall have the meaning

IGST REFUNDS - EXPORTS ROLE OF CUSTOMS BACKGROUND OF IGST REFUNDS ON EXPORTS Exports : Zero-Rated Supply: Eligible to Claim Refund As per Sec 2(23) of IGST Act: zero-rated supply shall have the meaning

100 Issues & solutions in filing GST Returns & TRAN Forms

100 Issues & solutions in filing GST Returns & TRAN s It is seen that industry, trade and professionals have been facing various in filing of GST Returns and transitional forms. Therefore, this article

100 Issues & solutions in filing GST Returns & TRAN s It is seen that industry, trade and professionals have been facing various in filing of GST Returns and transitional forms. Therefore, this article

ITC Concepts. Features of ITC Provisions. ISD & its Features

Legal Provisions ITC Concepts Eligibility for ITC Features of ITC Provisions Transitional Provisions ISD & its Features Cross Utilization Does Law define Input 2 (59) means any goods other than capital

Legal Provisions ITC Concepts Eligibility for ITC Features of ITC Provisions Transitional Provisions ISD & its Features Cross Utilization Does Law define Input 2 (59) means any goods other than capital

FAQ s on Form GSTR-9 Annual Return

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

FAQ s on Form GSTR-9 Annual Return DISCLAIMER The views expressed in this write up are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed

ROUTINE PROCEDURES

A. REGISTRATION ROUTINE PROCEDURES AS SERVICE Procedure, conditions and safeguards for registration under service tax will be as prescribed by CBE&C by order rule 4(9) of Service Tax Rules, inserted w.e.f.

A. REGISTRATION ROUTINE PROCEDURES AS SERVICE Procedure, conditions and safeguards for registration under service tax will be as prescribed by CBE&C by order rule 4(9) of Service Tax Rules, inserted w.e.f.

Transitional Provisions

Chapter XX Transitional Provisions Statutory provision 139. Migration of existing Tax Payers to GST Section (1) On and from the appointed day, every person registered under any of the existing laws and

Chapter XX Transitional Provisions Statutory provision 139. Migration of existing Tax Payers to GST Section (1) On and from the appointed day, every person registered under any of the existing laws and

The Institute of Chartered Accountants of India Western India Regional Council

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

APPLICABILITY OF SERVICE TAX:

SERVICE TAX It is an indirect tax. Service tax is a tax on services provided.the provisions of service tax are contained in chapter V of the Finance Act, 1994 and administered by the Central Excise Department.

SERVICE TAX It is an indirect tax. Service tax is a tax on services provided.the provisions of service tax are contained in chapter V of the Finance Act, 1994 and administered by the Central Excise Department.

REFUND UNDER SERVICE TAX

REFUND UNDER SERVICE TAX (with special reference to Recent Developments) ORGANISED by WIRC OF ICAI CA. NARENDRA SONI 1 Summary of Refund under Service Tax Law Provisions Section 11B of The CE Act, 1944

REFUND UNDER SERVICE TAX (with special reference to Recent Developments) ORGANISED by WIRC OF ICAI CA. NARENDRA SONI 1 Summary of Refund under Service Tax Law Provisions Section 11B of The CE Act, 1944

GST: Transitional Provisions

GST: Transitional Provisions Edition 2 Contents Debit and Credit Notes [S.178] Pending Refunds [S.179 to S.181] Pending Assessments and Appeals [S.182 to S.185] Continuing Contracts [S.186 and S. 187]

GST: Transitional Provisions Edition 2 Contents Debit and Credit Notes [S.178] Pending Refunds [S.179 to S.181] Pending Assessments and Appeals [S.182 to S.185] Continuing Contracts [S.186 and S. 187]

Sampat & Mehta GST - FAQ

Sr. No. Particulars Suggestions 1. What documents are required to accompany movement of Goods outside own premises E Way Bill to be generated from GSTN Portal before or at the time of movement of Goods

Sr. No. Particulars Suggestions 1. What documents are required to accompany movement of Goods outside own premises E Way Bill to be generated from GSTN Portal before or at the time of movement of Goods

Composition. Exports

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.

![[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.](/thumbs/90/103497091.jpg "[Chapter IX] Edition NBC, Chartered Accountants and member of Allinial Global Accounting Association. All Rights Reserved.") [Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

[Chapter IX] Edition 7 Contents Furnishing details of outward supplies [S. 37] Furnishing details of inward supplies [S. 38] Furnishing of Returns [S. 39] First Return [S. 40] Claim of input tax credit

SERVICE TAX IMPACT BEFORE

Service Tax Liability on Land owners share - CA Mahadev R The prohibitive cost of land in major cities means a high investment of monies for developing any property. Finance constraints add to the challenge.

Service Tax Liability on Land owners share - CA Mahadev R The prohibitive cost of land in major cities means a high investment of monies for developing any property. Finance constraints add to the challenge.

Returns, Matching Concept, Accounts & Records, under GST Law. Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017

Returns, Matching Concept, Accounts & Records, under GST Law Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017 Agenda Returns & Matching Concept Accounts & Records

Returns, Matching Concept, Accounts & Records, under GST Law Presentation by CA. Gaurav V Save GST Course for CA Students WIRC of ICAI June 07, 2017 Agenda Returns & Matching Concept Accounts & Records

TRANSITIONAL PROVISIONS

TRANSITIONAL PROVISIONS REGISTRATION Sec Ref Chapter XX Particulars 139 Migration of Existing Tax Payers 140 Input Tax Credit Transition 141 Job work related Transition 142 Miscellaneous Transition provisions

TRANSITIONAL PROVISIONS REGISTRATION Sec Ref Chapter XX Particulars 139 Migration of Existing Tax Payers 140 Input Tax Credit Transition 141 Job work related Transition 142 Miscellaneous Transition provisions

Levy. FAQs. S.No. Query Reply

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Transition Returns. Tran 1 + Tran 2

Transition Returns Tran 1 + Tran 2 1 Transition Returns Tran 1 Entitled to Input tax credit u/140 Final One Time Transition Return Entitled for Actual Credit Tran 2 Not Registered Under Existing Law 140(3)

Transition Returns Tran 1 + Tran 2 1 Transition Returns Tran 1 Entitled to Input tax credit u/140 Final One Time Transition Return Entitled for Actual Credit Tran 2 Not Registered Under Existing Law 140(3)

Transitional Provisions under GST

Introduction: Transitional Provisions under GST Transitional Provisions in GST Act is to clarify as to when and how the operative parts of the enactments are to take effect. The Transitional Provisions

Introduction: Transitional Provisions under GST Transitional Provisions in GST Act is to clarify as to when and how the operative parts of the enactments are to take effect. The Transitional Provisions

INPUT TAX CREDIT (ITC) PROVISIONS. CA Nammitta Gangwal Nilange LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant

PROVISIONS. CA Nammitta Gangwal Nilange LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant") INPUT TAX CREDIT (ITC) PROVISIONS LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant WHAT SHOULD WE KNOW UNDER ITC? Sec. 16 Eligibility & Conditions for taking ITC Sec. 19 Taking ITC in respect

INPUT TAX CREDIT (ITC) PROVISIONS LCS, DISA, GST Faculty R. I. Nilange & Co. Chartered Accountant WHAT SHOULD WE KNOW UNDER ITC? Sec. 16 Eligibility & Conditions for taking ITC Sec. 19 Taking ITC in respect

Draft suggestions on GST -Form GSTR- 9

Draft suggestions on GST -Form GSTR- 9 Indirect es Committee THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA NEW DELHI INTRODUCTION 1. The Institute of Chartered Accountants of India considers it a privilege

Draft suggestions on GST -Form GSTR- 9 Indirect es Committee THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA NEW DELHI INTRODUCTION 1. The Institute of Chartered Accountants of India considers it a privilege

Assessment. Chapter XII

Chapter XII Assessment 59. Self-assessment 60. Provisional assessment 61. Scrutiny of returns 62. Assessment of non-filers of returns 63. Assessment of unregistered persons 64. Summary assessment in certain

Chapter XII Assessment 59. Self-assessment 60. Provisional assessment 61. Scrutiny of returns 62. Assessment of non-filers of returns 63. Assessment of unregistered persons 64. Summary assessment in certain

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

Input Tax Credit (ITC)

") FAQ s Chapter III Input Tax Credit (ITC) Eligibility and Conditions for taking Input Tax Credit (Section 16) Section 16 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017

FAQ s Chapter III Input Tax Credit (ITC) Eligibility and Conditions for taking Input Tax Credit (Section 16) Section 16 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017

E-filing under MVAT & Profession Tax Laws

E-filing under MVAT & Profession Tax Laws Presented by CA Somit Goyal On Sunday 17 th June, 2012 For J. B. Nagar CPE Study Circle of WIRC. 1 E Filing under MVAT Laws E Registration E Enrolment E Payment

E-filing under MVAT & Profession Tax Laws Presented by CA Somit Goyal On Sunday 17 th June, 2012 For J. B. Nagar CPE Study Circle of WIRC. 1 E Filing under MVAT Laws E Registration E Enrolment E Payment

Input Tax Credit. Issues with possible solutions (including cancellation, opt for composition) and other aspects. CA Venugopal Gella

and other aspects. CA Venugopal Gella") Input Tax Credit Availment, Migration Restrictions, to GST Jobwork and other aspects Issues with possible solutions (including cancellation, opt for composition) ICAI Webcast < http://estv.in/icai/08082017/>

Input Tax Credit Availment, Migration Restrictions, to GST Jobwork and other aspects Issues with possible solutions (including cancellation, opt for composition) ICAI Webcast < http://estv.in/icai/08082017/>

Payments under GST DISCLAIMER:

DISCLAIMER: Payments under GST The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

DISCLAIMER: Payments under GST The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

CA. Mehul Shah. Payment to Transport Contractors implications under the Income-tax Act Overview of Companies Act Care, Pair, and Share

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

WEBINAR ON - GST REFUND

WEBINAR ON - GST REFUND Organized by THE CHAMBER OF TAX CONSULTANTS PRESENTED BY RAJIV LUTHIA AN INVESTMENT IN KNOWLEDGE PAYS THE BEST RETURN 11th March, 2018 CA RAJIV LUTHIA 1 Refunds [Chapter XI Sections

WEBINAR ON - GST REFUND Organized by THE CHAMBER OF TAX CONSULTANTS PRESENTED BY RAJIV LUTHIA AN INVESTMENT IN KNOWLEDGE PAYS THE BEST RETURN 11th March, 2018 CA RAJIV LUTHIA 1 Refunds [Chapter XI Sections

CERTIFIED FACILITATION CENTRES UNDER ACES PROJECT OF THE CBEC

CERTIFIED FACILITATION CENTRES UNDER ACES PROJECT OF THE CBEC Frequently Asked Questions (FAQs) Q.1 What is CFC? CFC stands for Certified Facilitation Centre under ACES project of CBEC and is an e-facility,

CERTIFIED FACILITATION CENTRES UNDER ACES PROJECT OF THE CBEC Frequently Asked Questions (FAQs) Q.1 What is CFC? CFC stands for Certified Facilitation Centre under ACES project of CBEC and is an e-facility,

Transition Provisions Revised Model GST Law Hari Ganesh V

Transition Provisions Revised Model GST Law Hari Ganesh V Flow of Taxes Imports BCD CVD Cess SACD BCD IGST Import of Service Service tax IGST IGST (Excise, CST, or Service tax) Outside State Goods and

Transition Provisions Revised Model GST Law Hari Ganesh V Flow of Taxes Imports BCD CVD Cess SACD BCD IGST Import of Service Service tax IGST IGST (Excise, CST, or Service tax) Outside State Goods and

INDIRECT TAXES UPDATE 150

INDIRECT TAXES UPDATE 150 CUSTOMS Implementing Integrated Declaration under the Indian Customs Single Window An 'Indian Customs Single Window Project' facilitates trade where importers and exporters would

INDIRECT TAXES UPDATE 150 CUSTOMS Implementing Integrated Declaration under the Indian Customs Single Window An 'Indian Customs Single Window Project' facilitates trade where importers and exporters would

CENTRAL BOARD OF EXCISE & CUSTOMS

CENTRAL BOARD OF EXCISE & CUSTOMS GST (Goods and Services Tax) www.cbec.gov.in www.aces.gov.in CENTRAL BOARD OF EXCISE & CUSTOMS Concept of GST Registration g ITC Return PRESENTATION PLAN www.cbec.gov.in

CENTRAL BOARD OF EXCISE & CUSTOMS GST (Goods and Services Tax) www.cbec.gov.in www.aces.gov.in CENTRAL BOARD OF EXCISE & CUSTOMS Concept of GST Registration g ITC Return PRESENTATION PLAN www.cbec.gov.in

CA Somit Goyal. 18 th April WIRC of ICAI Jointly with J. B. Nagar CPE Study Circle of WIRC

E-FILING UNDER MVAT ACT By CA Somit Goyal 18 th April 2015 WIRC of ICAI Jointly with J. B. Nagar CPE Study Circle of WIRC Basics 2 VAT is payable on Sale of Goods. VAT is a multistage tax on value added.

E-FILING UNDER MVAT ACT By CA Somit Goyal 18 th April 2015 WIRC of ICAI Jointly with J. B. Nagar CPE Study Circle of WIRC Basics 2 VAT is payable on Sale of Goods. VAT is a multistage tax on value added.

GOODS & SERVICES TAX

GOODS & SERVICES TAX IMPORTANT FACTS ABOUT GST FAQ covers all the commonly asked questions, raised by business owners about the Procedures, challenges of implementation in companies, Preparations of GST.

GOODS & SERVICES TAX IMPORTANT FACTS ABOUT GST FAQ covers all the commonly asked questions, raised by business owners about the Procedures, challenges of implementation in companies, Preparations of GST.

IMPORTANT DATES DIRECT TAXES. TDS / TCS returns are to be filed Quarterly.

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

ELECTRONIC PAYMENT SYSTEM

ELECTRONIC PAYMENT SYSTEM Instructions for DDOs 1. Each payee is required to be got allocated a unique code (UCP) by furnishing bank details in specified format (Annexure I) at the concerned treasury.

ELECTRONIC PAYMENT SYSTEM Instructions for DDOs 1. Each payee is required to be got allocated a unique code (UCP) by furnishing bank details in specified format (Annexure I) at the concerned treasury.

Input Tax Credit. Chapter III FAQS. Eligibility and conditions for taking Input Tax credit (Section 16)

") FAQS Chapter III Input Tax Credit Eligibility and conditions for taking Input Tax credit (Section 16) Section 16 of CGST Act, made applicable to IGST vide Section 20 of IGST Act and Section 21 of UTGST

FAQS Chapter III Input Tax Credit Eligibility and conditions for taking Input Tax credit (Section 16) Section 16 of CGST Act, made applicable to IGST vide Section 20 of IGST Act and Section 21 of UTGST

FAQs. Yes. He is liable for registration as he is engaged in Inter State supplies.

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

FAQs 1. A registered person s business is in many states. All supplies are below 10 lakhs. He makes an Inter State supply from one state. Is he liable for registration? Yes. He is liable for registration

F. No. 137/85/2007-CX. 4 Government of India Ministry of Finance Department of Revenue Central Board of Excise & Customs New Delhi

Cirlcular No. 97/8/2007 F. No. 137/85/2007-CX. 4 Government of India Ministry of Finance Department of Revenue Central Board of Excise & Customs New Delhi Procedural issues in Service Tax-circular-reg.

Cirlcular No. 97/8/2007 F. No. 137/85/2007-CX. 4 Government of India Ministry of Finance Department of Revenue Central Board of Excise & Customs New Delhi Procedural issues in Service Tax-circular-reg.

REPORT THE JOINT COMMITTEE ON BUSINESS PROCESS FOR GST GST RETURN. Empowered Committee of State Finance Ministers. New Delhi.

REPORT OF THE JOINT COMMITTEE ON BUSINESS PROCESS FOR GST ON GST RETURN Empowered Committee of State Finance Ministers New Delhi October, 2015 Table of Contents 1. Introduction... 4 2. Periodicity of Return

REPORT OF THE JOINT COMMITTEE ON BUSINESS PROCESS FOR GST ON GST RETURN Empowered Committee of State Finance Ministers New Delhi October, 2015 Table of Contents 1. Introduction... 4 2. Periodicity of Return

EXPORT BENEFITS UNDER SERVICE TAX CA. MANINDAR KAKARLA

EXPORT BENEFITS UNDER SERVICE TAX CA. MANINDAR KAKARLA 2 Objective: Objective & Coverage To recall various benefits to exporter of goods & services. The conditions/procedures to be complied with. Intricacies

EXPORT BENEFITS UNDER SERVICE TAX CA. MANINDAR KAKARLA 2 Objective: Objective & Coverage To recall various benefits to exporter of goods & services. The conditions/procedures to be complied with. Intricacies

Click to Close. Click to Print. Case Tracker. Passed by the. Date COMMISSIONER MUMBAI-II. Airline

Click to Print Click to Close 2017-TIOL-3894-CESTAT-MUM IN THE CUSTOMS, EXCISE AND SERVICE TAX APPELLATE TRIBUNAL WEST ZONAL BENCH, MUMBAI Case Tracker DHL LOGISTICS PVT LTD Vs CCE [CESTAT] Appeal No.

Click to Print Click to Close 2017-TIOL-3894-CESTAT-MUM IN THE CUSTOMS, EXCISE AND SERVICE TAX APPELLATE TRIBUNAL WEST ZONAL BENCH, MUMBAI Case Tracker DHL LOGISTICS PVT LTD Vs CCE [CESTAT] Appeal No.

GST transitional provisions on credits key issues and challenges. Sagar Shah 17 June 2017

GST transitional provisions on credits key issues and challenges Sagar Shah 17 June 2017 Interpreting the Transition Provisions Obscurity is often caused not by unnecessary complication of language but

GST transitional provisions on credits key issues and challenges Sagar Shah 17 June 2017 Interpreting the Transition Provisions Obscurity is often caused not by unnecessary complication of language but

REGISTRATION. AKOLA Branch of WIRC of ICAI. CA. Dhiraj C Baldota Solapur. June 17, 2017

REGISTRATION June 17, 2017 AKOLA Branch of WIRC of ICAI CA. Dhiraj C Baldota Solapur EXCISE / SERVICE TAX / VAT and on. take taxes but reduce compliance. a smooth n healthy act???? Why Liability to Register

REGISTRATION June 17, 2017 AKOLA Branch of WIRC of ICAI CA. Dhiraj C Baldota Solapur EXCISE / SERVICE TAX / VAT and on. take taxes but reduce compliance. a smooth n healthy act???? Why Liability to Register

GOVERNMENT OF WEST BENGAL DIRECTORATE OF COMMERCIAL TAXES 14, BELIAGHATA ROAD, KOLKATA DATED:

GOVERNMENT OF WEST BENGAL DIRECTORATE OF COMMERCIAL TAXES 14, BELIAGHATA ROAD, KOLKATA-700015 TRADE CIRCULAR No. 23/2018 (Circular No. 26/26/2017-GST) Subject: Filing of Returns under GST DATED: 17.09.2018

GOVERNMENT OF WEST BENGAL DIRECTORATE OF COMMERCIAL TAXES 14, BELIAGHATA ROAD, KOLKATA-700015 TRADE CIRCULAR No. 23/2018 (Circular No. 26/26/2017-GST) Subject: Filing of Returns under GST DATED: 17.09.2018

SUGGESTIONS ON GST Implementation Issues

SUGGESTIONS ON GST Implementation s (AUGUST, 2017 ) Indirect Taxes Committee THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA NEW DELHI INTRODUCTION The Institute of Chartered Accountants of India s on

SUGGESTIONS ON GST Implementation s (AUGUST, 2017 ) Indirect Taxes Committee THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA NEW DELHI INTRODUCTION The Institute of Chartered Accountants of India s on

National Conference RAJKOT BRANCH OF WIRC OF ICAI ICAI BHAWAN 29 th & 30 th Dec 2018

National Conference RAJKOT BRANCH OF WIRC OF ICAI ICAI BHAWAN 29 th & 30 th Dec 2018 Controversies in GST 29th DEC 2018 Ashu Dalmia Coverage of Presentation Initial Preparation for Annual Compliance GSTR-9

National Conference RAJKOT BRANCH OF WIRC OF ICAI ICAI BHAWAN 29 th & 30 th Dec 2018 Controversies in GST 29th DEC 2018 Ashu Dalmia Coverage of Presentation Initial Preparation for Annual Compliance GSTR-9

(Extract) Notification No: 9/ , New Delhi, the 28th May, 2018

Notification No: 9/ , New Delhi, the 28th May, 2018") This column is compiled by Consultant [EXIM Policy] of EPCH. It contains recent Public Notices, Notifications and Circulars of DGFT, CBEC and Department of Revenue. If a handicraft exporter has question[s]

This column is compiled by Consultant [EXIM Policy] of EPCH. It contains recent Public Notices, Notifications and Circulars of DGFT, CBEC and Department of Revenue. If a handicraft exporter has question[s]

Issues relating to SEZ

Issues relating to SEZ DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

Issues relating to SEZ DISCLAIMER The views expressed in this article are of the author(s). The Institute of Chartered Accountants of India may not necessarily subscribe to the views expressed by the author(s).

Returns in goods and services tax

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

Returns in goods and services tax A brief overview by Shri Sunil Lahane, Dy Commissioner, Sales Tax Outline What s special about GST return? Overview of Returns to be submitted by regular tax payers Process

Articles Orientation Programme. The Chamber of Tax Consultants. By CA Amit Purohit. Coverage. Overview of Section 44 AB and its applicability

Articles Orientation Programme The Chamber of Tax Consultants By CA Amit Purohit Purpose of Tax audit Coverage Approaching Tax Audit Overview of Section 44 AB and its applicability Audit report applicability

Articles Orientation Programme The Chamber of Tax Consultants By CA Amit Purohit Purpose of Tax audit Coverage Approaching Tax Audit Overview of Section 44 AB and its applicability Audit report applicability

GST Workshop 9th June 2017

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

GST Workshop 9 th June 2017 GST Model- Basic Features GST is tax on the supply of goods and services, right from the manufacturer/service provider to the consumer. Destination based consumption Tax (Tax

MODEL GST LAW. CA. UPENDER GUPTA, IRS COMMISSIONER (GST), CBEC

, CBEC") MODEL GST LAW CA. UPENDER GUPTA, IRS COMMISSIONER (GST), CBEC upender.gupta@nic.in PRESENTATION PLAN BASIC FEATURES HIGHLIGHTS OF MODEL GST LAW (MGL) MINIMAL HUMAN INTERFACE GST A GAME CHANGER 2 BASIC

MODEL GST LAW CA. UPENDER GUPTA, IRS COMMISSIONER (GST), CBEC upender.gupta@nic.in PRESENTATION PLAN BASIC FEATURES HIGHLIGHTS OF MODEL GST LAW (MGL) MINIMAL HUMAN INTERFACE GST A GAME CHANGER 2 BASIC

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the rate of service tax was reduced to 10% vide Notification

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the rate of service tax was reduced to 10% vide Notification

GST TRANSITION PROVISIONS & GST TRAN 1. CTC Indirect Tax Study Circle Meeting

GST TRANSITION PROVISIONS & GST TRAN 1 CTC Indirect Tax Study Circle Meeting 25 th July 2017 CA Shrenik A Shah Partner Ashwin K Shah & Co LLP 7, Chemox House, Barrack Lane, Mumbai - 400020 Mapping of Statutory

GST TRANSITION PROVISIONS & GST TRAN 1 CTC Indirect Tax Study Circle Meeting 25 th July 2017 CA Shrenik A Shah Partner Ashwin K Shah & Co LLP 7, Chemox House, Barrack Lane, Mumbai - 400020 Mapping of Statutory

Bandra Kurla Complex, Bandra East, CA Naresh Sheth 1. highlight the issues and challenges arising in GST for real estate sector

Western India Regional Council of ICAI Topic : GST implications of Real Estate Date & Day : 22 nd April 2017 Venue : ICAI Tower, Plot No C-40, G Block, Bandra Kurla Complex, Bandra East, Mumbai 400051

Western India Regional Council of ICAI Topic : GST implications of Real Estate Date & Day : 22 nd April 2017 Venue : ICAI Tower, Plot No C-40, G Block, Bandra Kurla Complex, Bandra East, Mumbai 400051

GST on financial services: Frequently Asked Questions

GST on financial services: Frequently Asked Questions GST on financial services Straight answers to nagging questions GST happens to be one of the biggest tax reforms since Independence and is expected

GST on financial services: Frequently Asked Questions GST on financial services Straight answers to nagging questions GST happens to be one of the biggest tax reforms since Independence and is expected

EY Tax Alert. Executive summary

16 March 2016 EY Tax Alert CESTAT allows credit of Service tax on transportation, treating the place where property in goods is transferred in terms of Sale of Goods Act - as Place of removal Executive

16 March 2016 EY Tax Alert CESTAT allows credit of Service tax on transportation, treating the place where property in goods is transferred in terms of Sale of Goods Act - as Place of removal Executive