Rectification Manual. Submitting Online Rectification Request. rectify intimation order issued under section 143 (1)

|

|

|

- Abner Simmons

- 6 years ago

- Views:

Transcription

1 Rectification Manual Submitting Online Rectification Request to rectify intimation order issued under section 143 (1) by Centralized Processing Center, Bangalore.

2 If you are thinking of seeking rectification of the intimation issued by Centralized Processing Center at Bangalore, then you must carefully review the Common Error Guide and the typical causes of error presented below in order to prepare an accurate rectification request and thereby ensure that you get a proper resolution from CPC in the form of an rectification order. Please do not jump into conclusions or get misguided by others that there are mistakes in processing software; more likely than not the data in the e-return submitted by you was either incomplete or incorrect resulting in calculation different than what is expected by you. For every variation between what you have computed as your tax liability and your refund and what was finally the outcome of processing at CPC there is a logical explanation and therefore, a possible resolution.

3 Sl Symptom and issue Probable reason and Resolution 1 Salary income shown at higher figure than entered In Salary Schedule higher figure is reported under Gross salary which should be excluding Exempt income (such as transport allowance etc). Taxpayer may have mentioned Transport allowance in Exempt Income and may have deducted the same to arrive at a lower net figure in the final calculation. However, the Exempt income is to be mentioned only for reporting purposes and should not be used in any calculation. 2 Loss under House Property due to Interest paid on loans is not allowed In the House property Schedule the Interest paid value is not entered. Instead only the loss figure is mentioned in the final total. The totals are re-calculated while processing the return from the basic values provided. If the break up values are not provided then the total will be calculated as zero. The other possibility is that even if the House Property Schedule was correctly filled, the taxpayer has not claimed the loss in Schedule CYLA. Therefore, even if loss is correctly shown in Sch HP, the adjustment of this loss is not automatic. It has to be entered in the first row against Salary Income as shown to indicate that this loss is adjusted against salary income. 3 Tax payment is not allowed BSR code, Challan number and date of deposit may have been incorrect since any mismatch may lead to rejection of tax payment. Date of deposit of challan cannot be beyond or after date of filing of return. Taxpayer should NOT report tax payments made by Deductors as given in Form 16 or Form 16A as their own payment under Schedule IT. This is meant ONLY to enter tax payments DIRECTLY made by taxpayer himself. 4 TDS credit is not allowed Taxpayer should ensure that the TAN number is valid and as per the Form 16A issued by Deductor. PAN number of Deductor should NOT be mentioned in place of TAN. In many cases Deductors may have given TDS certificate with certain TAN but submitted TDS return to Department under different TAN. This may happen where many group concerns operate in a flexible manner. This should be verified by cross-checking against the 26AS statement for the taxpayer which is available through NSDL or at the e-filing website. Any error by Deductor should be immediately pointed out and correction ensured 5 Chapter VI A deduction specially 80C deduction is not allowed While filling in Deductions in Chapter VI A, taxpayer must ensure to fill up the breakup showing all individual Section-wise deductions such as 80 C etc, and then mention the Total Deduction claimed. At the time of processing, it is not clear under what section is the deduction claimed if details are not given. Since each deduction has different limits and eligibility, it is not possible to allow deduction only from the total.

4 6 Deduction under Chapter 80G or 80IA etc is not allowed. Details u/s 80G in Sch 80G (where the Schedule is available in the return- ITR 4, 5 and 6) along with correct totals may not have been entered, before claiming the total in Chapter VI-A. Similarly, other schedules such as 80IA/IB etc must also be filled in where relevant schedules are in the ITR, before claiming Deductions in Chapter VI-A. Mentioning only the final total values in Chapter VI A Schedule or the total Deduction is not sufficient. 7 8 Tax Rate applied by CPC is not as per rates for Female Taxpayers or Senior citizens or for firms or domestic company. MAT is applied Income from Business is not correctly computed Taxpayer may have entered Gender as Male or entered date of birth incorrectly. Alternatively, taxpayer may have entered these details correctly but the details are different in PAN database, in which case the data in PAN database has to be corrected by taxpayer by giving proof and details. For assessee filing return ITR 5, Status (such as Cooperative Society, Firm, etc) in the General Information Portion may not have been selected correctly. Incorrect status selection can lead to taxation at higher rate or disallowance on specific deductions like 80P, etc. For taxpayers filing ITR 6, the correct selection while opting for item under General Information relating to If a Domestic Company must be made. Domestic companies MUST NOT select "N" here which implies that taxpayer is stating that company is a Foreign Company. When N is selected the tax rate applicable to Foreign Companies will be applied, leading to higher taxation. Schedule MAT MUST be filled by all taxpayers filing ITR 6 irrespective of whether the book profit calculations result in application of provisions of MAT. Taxpayer may not have calculated MAT. There are many reasons for variation in Income From Business: While entering Totals (for ex Total Duties and Taxes etc), breakup is not given. Value entered in Sl no 42 (Depreciation) (where Books of Accounts are maintained) should match the value in Sch BP: Sl no 11 (Depreciation debited to P&L Account) Profit Before Tax (and not Profit After Tax) should be entered in item 1of Sch BP. Depreciation allowable under IT Act u/s 32(1) (ii) must be as per Sch DEP. When Schedule Profit and Loss is filled with a claim for depreciation but depreciation amount is either not added back at item A11 in Schedule BP or details of depreciation in plant and machinery and other assets are not filled by the assessee in Schedule DPM, DOA and Schedule DEP, this may lead to disallowance of depreciation. Schedule DPM, DOA and DEP should NOT be left blank if Depreciation is being claimed. Entering total value of Depreciation in Sl A12 in Schedule BP WITHOUT entering DPM, DOA, DEP will lead to disallowance of Depreciation. Where block ceases to exist, enter correct value in Cap.Gains / Loss u/s 50. Under NO OTHER CIRCUMSTANCE should item 16 be filled. Negative value, if entered in Sl 16, implies that block ceased to exist and then no Depreciation will be allowed for that block. Where P&L account is filled and includes Deemed income u/s 44AD, 44AE 44AF etc, ensure that relevant figures in A4 and A33 in Sch BP are correctly filled Total of Deemed Income (IF NON ZERO) under Sections 44AD, 44AE, 44AF, 44B, 44BB, 44BBA, 44BBB, 44D, 44DA, Chapter XII-G and First Sch

5 of IT Act as per Sl no 33 of Sch BP) should not be hence lower than Sl no 4 of Sch BP. In case nature of business does not include Tea/Coffee/Rubber, the net profit or loss from business or profession after applying Rule 7A,7B, 7C in A37 should be entered as the same value as arrived in Sl no 36 of Sch BP. Where Schedule OI is filled with details of disallowances or amounts which are to be added back to income due to the provisions like 36, 37, 40, 40A, 43B, assessee must fill in the details in Schedule BP in arriving at the income from Business and Profession. This is because at the time of processing these disallowances are taken from Schedule OI and applied to relevant items in Sch BP. This will result in increase of Income under Business due to these disallowances Losses brought forward from previous years has not been allowed Capital Gain is not correctly calculated Before claiming adjustments in Sch BFLA, ensure that Schedule CFL is not left empty. The correct breakup of the losses claimed for setoff must be filled in Sch CFL which alone will be considered for Schedule BFLA. Direct entries in Schedule BFLA without any entry in Schedule CFL will not be entertained, thus leading to demand due to disallowance of claim for adjustment of brought forward loss. Unabsorbed depreciation loss MUST be included in CFL against appropriate year or in case it relates to prior to AY period then it MUST be entered in the row relating to AY ONLY if the unabsorbed Depreciation is entered in CFL, then it will be allowed in Sch BFLA calculation. In Sch BFLA, enter all adjustments correctly. Do not leave blank as system will not allow adjustments of brought forward loss unless claimed in Sch BFLA. Start from full value of consideration in Capital Gain schedule. DO NOT ENTER ONLY FINAL VALUES. Enter the correct breakup to arrive at STCG and LTCG values. Do not leave blank any intermediate figures such as Full Value of Consideration etc. Ensure that the value entered in Sch CG under LTCG Proviso (option under proviso to S.112(1) is exercised) is also correctly entered in Sch SI under LTCG proviso (Section 22). All Capital gain tax calculations are as per special rates given in Schedule SI. In case this is not correctly entered then the calculation may differ. In most cases taxpayers have entered capital gains in CG schedule at 20% tax rate, but in Schedule SI entered in code corresponding to 10% rate by mistake. In such cases tax may be calculated at both these tax rates. Verify that correct quarterly breakups for LTCG and STCG are provided in Sch CG and the total of the quarterly breakups match with the respective values in Sch SI (taxable Income after adjusting Min Chargeable to Tax) after set off of all losses. Ensure that the value entered in Sch CG under STCG 111A is also correctly entered in Sch SI under STCG 111A (Section 1A) Enter correct breakup of STCG 111A and other than 111A in Sch CG.

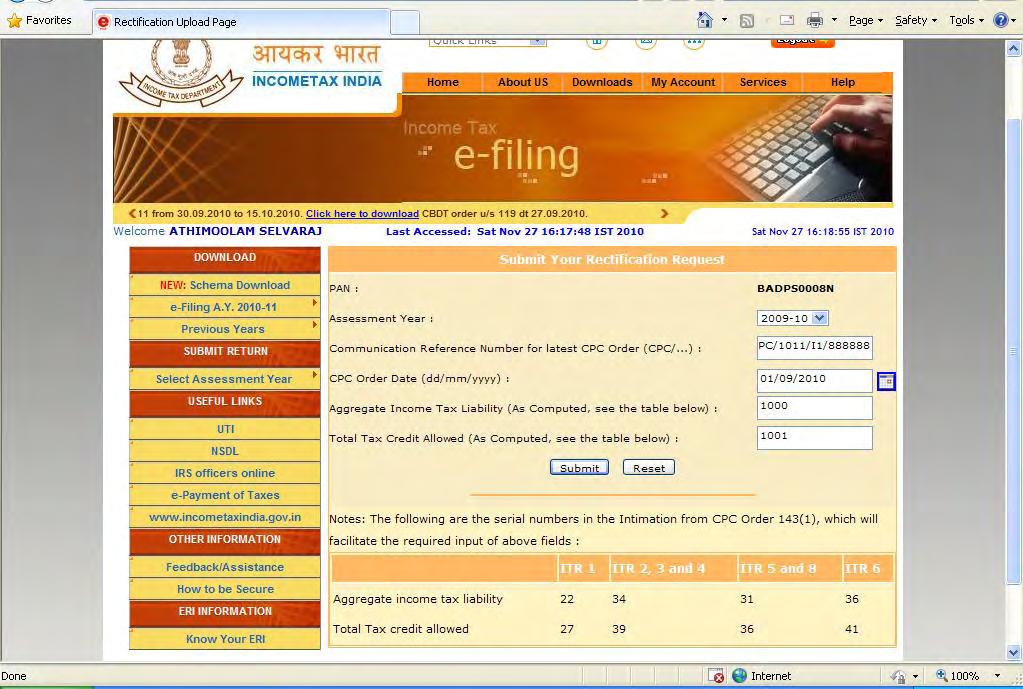

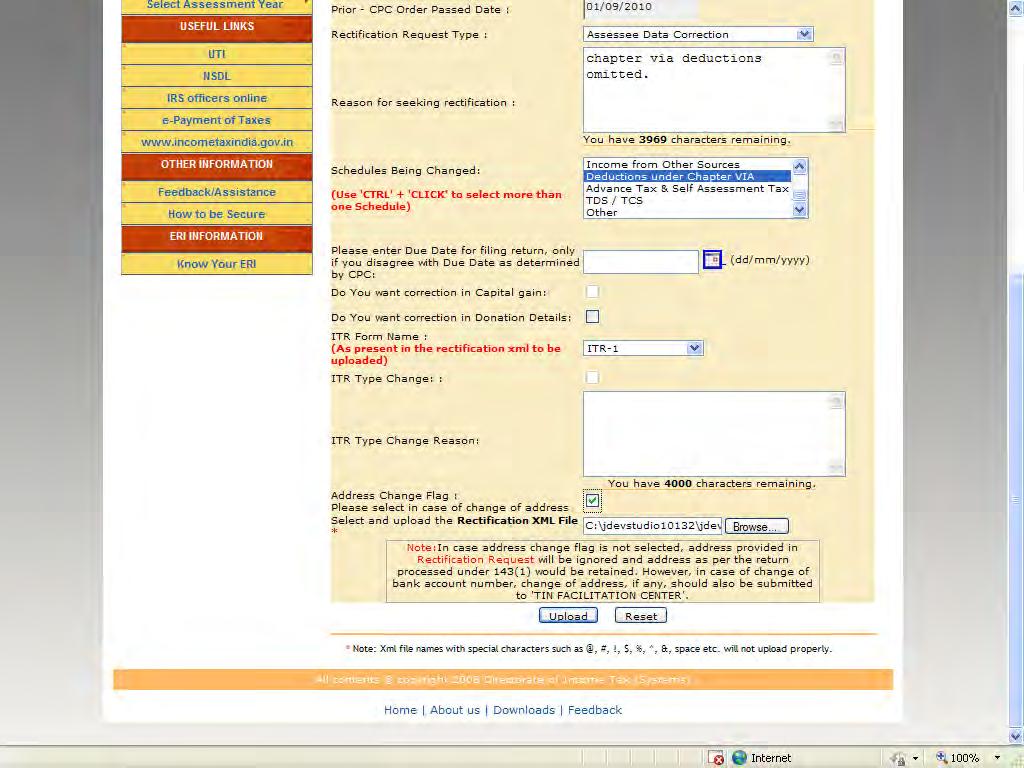

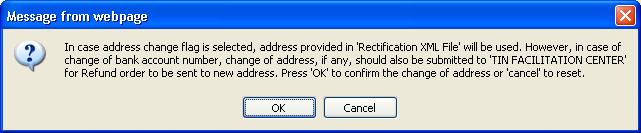

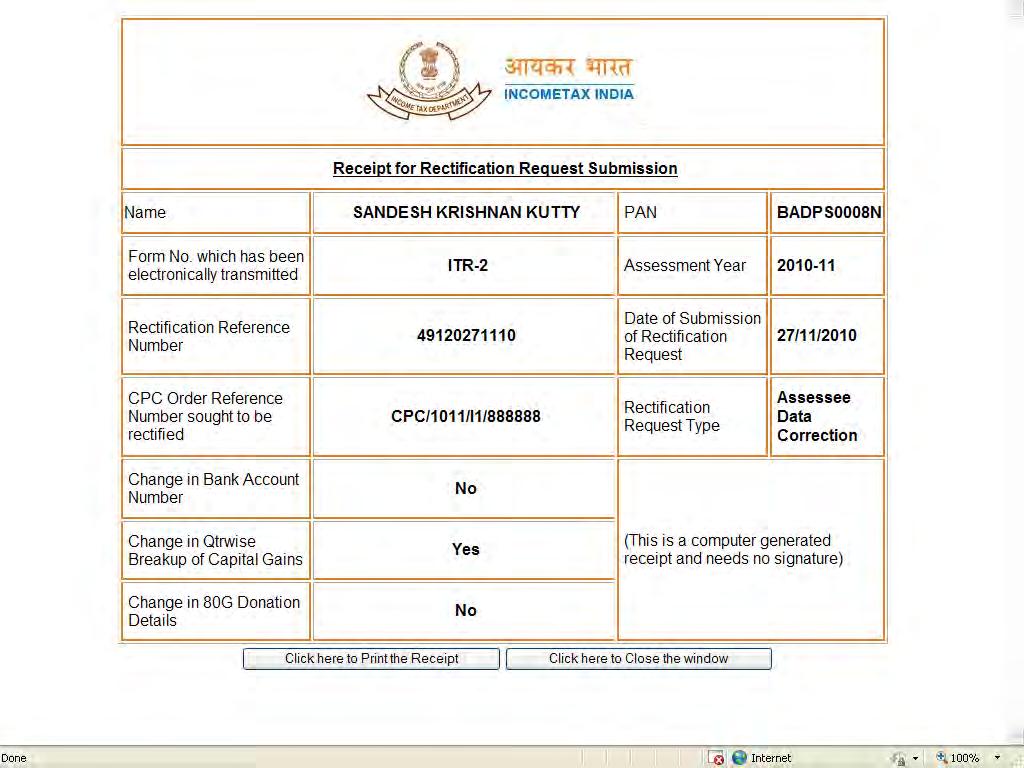

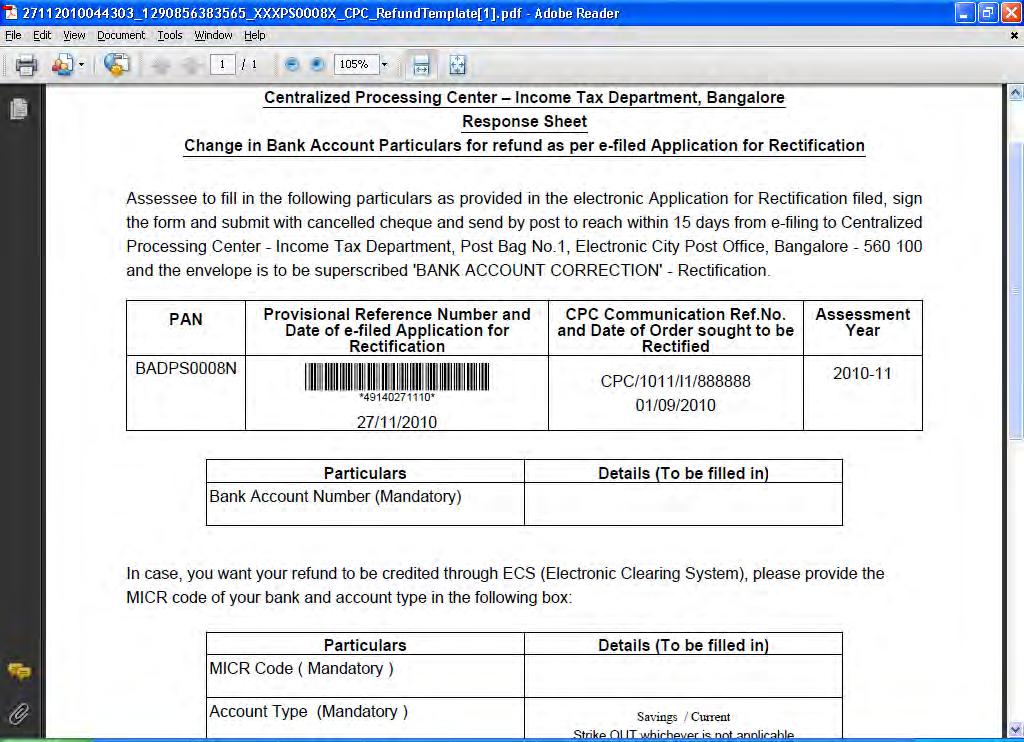

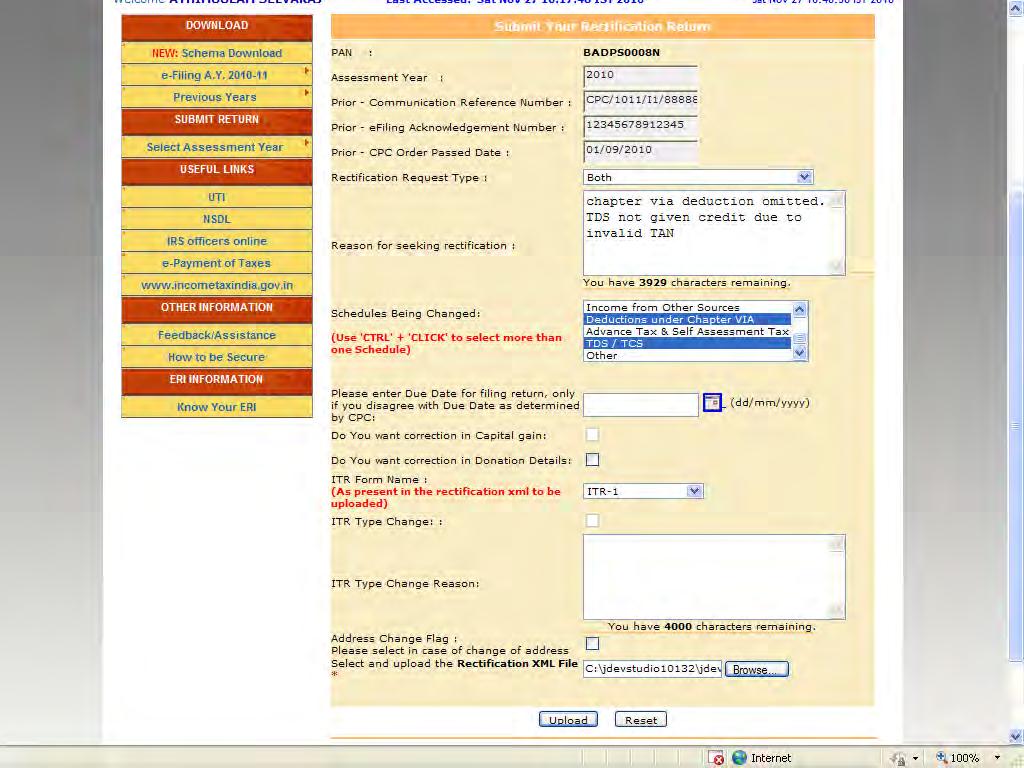

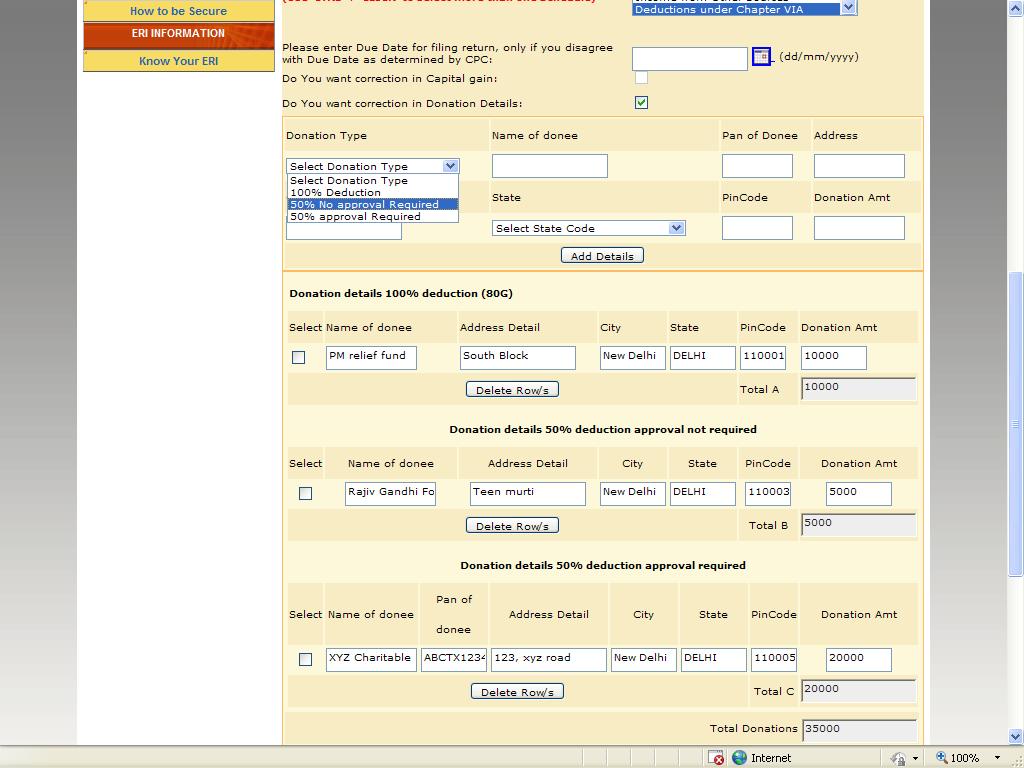

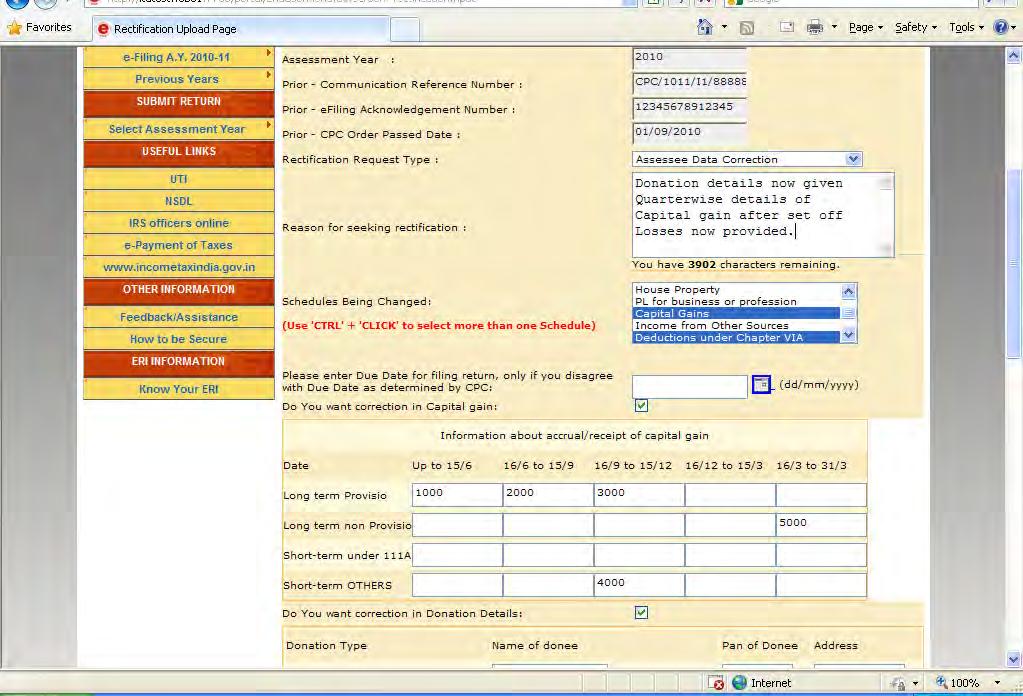

6 How to submit an Online Rectification request Step 1: Make sure you have received an intimation under section 143 (1) from CPC Bangalore for the E-returns filed by you for AY or later. Step 2: Carefully examine the intimation to see if the computation by CPC is correct even if different from what was expected by you. It may be that you may have computed tax liability or interest incorrectly. Step 3: Carefully review the Common Error guide and the table above to understand as the basic reason for the variation. Step 4: Since the Rectification Request is to be submitted by uploading the complete xml file similar to uploading the original return, it may be preferable to start with the saved e-return data that was prepared by the return preparation utility/software (Department provided excel software or other software), in case it is available with the taxpayer. Step 5: All errors in data entry should be completely corrected and schedules or fields left blank should be filled accurately as explained in the guide. The complete return should be filled including TDS and Tax payment schedules and not only schedules that need change or the fields that need correction. This is because the entire return with corrected data would be re-processed under rectification. However, there should not be any revision in income figures or new claims since then the rectification request would be rejected or rectification would be delayed. It may be clearly noted that this facility is only for correcting mistakes apparent from record. Step 6: After the Return data is corrected then the xml can be generated. This is the Rectification XML file. Step 7: Log in to and go to My Account-> Rectification-> Rectification upload Step 8: Fill in details from the intimation sheet which will be verified to ascertain that only the taxpayer in possession of the Intimation from CPC would be able to submit a rectification request. Step 9: Fill in details of Schedules where changes have been made and reasons for seeking rectification. Fill in due date for filing return, if incorrect as per intimation sheet. Leave blank if not applicable. Fill in details which are not available in the return form such as details of 80G donations (not available in ITR forms for 1, 2 and 3) and Quarter-wise details of Capital Gains (all four types- which is not available in ITRs 2, 3, 4, 5 and 6 for AY ) only if applicable. Leave blank if not applicable Please note if your address has been changed in the rectification XML file, you should check the address changed checkbox to ensure that the new address is updated else the old address as per e-return only will be used. Step 10: Now upload the Rectification XML file. Validations will be done to ascertain that only mistakes apparent from record are sought to be rectified Step 11: Upon successful upload, Rectification Request number and acknowledgement will be displayed.

7 In case Bank Account Number is changed in rectification XML as compared to Bank Account number as per e- return then the rectification request is only PROVISIONALLY uploaded. A response sheet will be displayed, which has to be filled and a cancelled cheque attached and sent to CPC Bangalore. Only upon receipt of this response sheet at CPC Bangalore will the Rectification Request be finally accepted and acknowledgement generated. Step 12: The rectification request can be withdrawn within 7 days if uploaded by mistake or the request needed to be amended. Only one rectification request can be submitted at any time. Any rectification request after submission has to be processed at CPC before the next rectification request for the same PAN and AY can be submitted. Step 13: The rectification request will be processed at CPC and either the rectification order under Section 154 will be issued or the request would be rejected.

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

Common Errors made while filling Income Tax returns explained

Common Errors made while filling Income Tax returns explained For AY 2009-10 onwards, E-returns are being processed u/s143 (1) at CPC Bangalore. In some cases, taxpayers have requested for rectification

Common Errors made while filling Income Tax returns explained For AY 2009-10 onwards, E-returns are being processed u/s143 (1) at CPC Bangalore. In some cases, taxpayers have requested for rectification

JB NAGAR STUDY CIRCLE OF WIRC

JB NAGAR STUDY CIRCLE OF WIRC ISSUES ON REVISED AND RECTIFICATION OF ONLINE FILED INCOME TAX RETURNS Compiled by CA Avinash Some Provisions of the Income Tax Act If a person has filed his return of Income

JB NAGAR STUDY CIRCLE OF WIRC ISSUES ON REVISED AND RECTIFICATION OF ONLINE FILED INCOME TAX RETURNS Compiled by CA Avinash Some Provisions of the Income Tax Act If a person has filed his return of Income

List of Issues raised by BCAS for discussion on 26/07/2017

List of Issues raised by BCAS for discussion on 26/07/2017 1 Difference in the fields in ITR form as notified by the CBDT and as put up in the utility on the e-filing site: In ITR 5, in Part B TTI, in

List of Issues raised by BCAS for discussion on 26/07/2017 1 Difference in the fields in ITR form as notified by the CBDT and as put up in the utility on the e-filing site: In ITR 5, in Part B TTI, in

MINUTES OF MEETING HELD AT CENTRAL PROCESSING CENTRE OF INCOME-TAX DEPARTMENT AT BENGALURU

MINUTES OF MEETING HELD AT CENTRAL PROCESSING CENTRE OF INCOME-TAX DEPARTMENT AT BENGALURU Present: From CPC: Mr. Sanjai Kumar Verma, CIT Mr. B.K. Panda, Addl. CIT Mr. Satish Goyal, Addl. CIT Mr. R.K.

MINUTES OF MEETING HELD AT CENTRAL PROCESSING CENTRE OF INCOME-TAX DEPARTMENT AT BENGALURU Present: From CPC: Mr. Sanjai Kumar Verma, CIT Mr. B.K. Panda, Addl. CIT Mr. Satish Goyal, Addl. CIT Mr. R.K.

BCAS LECTURE MEETING 20 st May by CA Raman Jokhakar B. D. Jokhakar & Co.

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

BCAS LECTURE MEETING 20 st May 2008 by CA Raman Jokhakar B. D. Jokhakar & Co. Who is required to file a return When is it required to be filed Which form is required to be used How is the return to be

For J B Nagar Study Circle Meeting

For J B Nagar Study Circle Meeting Nature of income Individual and HUF ITR 1* (Sahaj) ITR 2 ITR 3 ITR 4 Income from salary/pension (for ordinarily resident person) Income from salary/pension (for not ordinarily

For J B Nagar Study Circle Meeting Nature of income Individual and HUF ITR 1* (Sahaj) ITR 2 ITR 3 ITR 4 Income from salary/pension (for ordinarily resident person) Income from salary/pension (for not ordinarily

E-TDS FILING PRESENTED BY. Vinod Kumar Jain FCA

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

E-TDS FILING PRESENTED BY Vinod Kumar Jain FCA What is E- TDS? E-TDS stands for Electronic Tax Deducted at Source introduced by the IT department. Filing e TDS return is compulsory for all assessee and

IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY by CA Sudin Sabnis

FORMS FOR AY by CA Sudin Sabnis") IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY 2018-19 by CA Sudin Sabnis Why filing correct Income Tax Return is important Law of the land Losses and Tax holiday Refunds Stich in time saves

IMPORTANT CHANGES IN INCOME TAX RETURN (ITR) FORMS FOR AY 2018-19 by CA Sudin Sabnis Why filing correct Income Tax Return is important Law of the land Losses and Tax holiday Refunds Stich in time saves

CHANGES IN INCOME TAX RETURN FORMS RELEVANT FOR A.Y

CHANGES IN INCOME TAX RETURN FORMS RELEVANT FOR A.Y.2018-19 Subscribe to webcast https://www.youtube.com/channel/ucbmk3daybl-6unknzthwflq ASSESSMENT YEAR 2018-19 Matters which you must understand before

CHANGES IN INCOME TAX RETURN FORMS RELEVANT FOR A.Y.2018-19 Subscribe to webcast https://www.youtube.com/channel/ucbmk3daybl-6unknzthwflq ASSESSMENT YEAR 2018-19 Matters which you must understand before

By CA. HARANAATH BAABU A.V. Chartered Accountant Partner Haranath & Associates 7/1 Arundelpet Guntur

By CA. HARANAATH BAABU A.V. Chartered Accountant Partner Haranath & Associates 7/1 Arundelpet Guntur 9885678619 sriharipriyawithu@gmail.com 1 NAVIGATION 1) Importance for CORRECT filing of ITR 2) ITR Forms

By CA. HARANAATH BAABU A.V. Chartered Accountant Partner Haranath & Associates 7/1 Arundelpet Guntur 9885678619 sriharipriyawithu@gmail.com 1 NAVIGATION 1) Importance for CORRECT filing of ITR 2) ITR Forms

WESTERN INDIA REGIONAL COUNCIL OF ICAI

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

1 WESTERN INDIA REGIONAL COUNCIL OF ICAI E-Filing of Income Tax Returns PDF processed with CutePDF evaluation edition www.cutepdf.com Endeavor of CPC to promote voluntary compliance; to educate tax payers

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for filling out FORM ITR-2 1. Legal status of instructions These instructions though stated to be non-statutory, may be taken as guidelines for filling the particulars in this Form. In case

Instructions for SUGAM Income Tax Return AY

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for SUGAM Income Tax Return AY 2016-17 1. General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

A23 A24 A25 A26 B1 B2 B3 B5 In response to notice under section In response to notice under section 153A/ 153C 7 In pursuance of an order of the

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Every firm shall furnish the return where income from business or profession is computed in accordance with section 44AD, 44ADA or 44AE. Item by Item Instructions Item A1-A3 A4 A5 A6 A7 A8-A14 A15 A16

Instructions for filling out FORM ITR-3

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-3 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

Instructions for filling out FORM ITR-2

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

1. Tax on accumulated balance of recognised provident fund 111 To be computed in accordance with rule 9(1) of Part A of fourth Schedule 2. Short term

of Part A of fourth Schedule 2. Short term") Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-2 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-6 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-6 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-5

Instructions for filling out FORM ITR-5 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-5 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No.3 for assessment year 2006-07, having the following particulars. (a) (b) (c) (d) (e) PAN

Rajesh Kothari Pinakin Desai. Niraj Bajaj. Kishor Karia President Chairman-Direct Taxation Comt.

BOMBAY CHARTERED ACCOUNTANTS SOCIETY Jolly Bhavan 2, 7,New Marine Lines, Churchgate, Mumbai400020. Tel. : 66595601/2/3/4/5 Fax : 66595606 Email: bca@bcasonline.org; Web :www.bcasonline.org INDIAN MERCHANTS

BOMBAY CHARTERED ACCOUNTANTS SOCIETY Jolly Bhavan 2, 7,New Marine Lines, Churchgate, Mumbai400020. Tel. : 66595601/2/3/4/5 Fax : 66595606 Email: bca@bcasonline.org; Web :www.bcasonline.org INDIAN MERCHANTS

INDIAN INCOME TAX RETURN. Assessment Year FORM

INDIAN INCOME TAX RETURN Assessment Year FORM ITR-7 For persons including companies required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) (Please see

INDIAN INCOME TAX RETURN Assessment Year FORM ITR-7 For persons including companies required to furnish return under section 139(4A) or section 139(4B) or section 139(4C) or section 139(4D) (Please see

Instructions for filling ITR-4 SUGAM A.Y

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-4 SUGAM A.Y. 2017-18 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Changes in ITR Forms A.Y

Changes in ITR Forms A.Y. 2018-19 CA PRERNA PESHORI Obligation to file ROI Who is obliged? Who is not obliged? Company Firm a person other than a company or a firm, if his total income (without giving

Changes in ITR Forms A.Y. 2018-19 CA PRERNA PESHORI Obligation to file ROI Who is obliged? Who is not obliged? Company Firm a person other than a company or a firm, if his total income (without giving

Area/locality; Town/City/District; State; Country. Pin code is mandatory. Tick mark the appropriate box for residential status. For non-residents cert

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

(ii) (iii) (iv) by furnishing the return electronically under digital signature; by transmitting the data in the return electronically under electronic verification code; by transmitting the data in the

Instructions for filling out FORM ITR-4

Instructions for filling out FORM ITR-4 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-4 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

E-FILING of Income Tax Return

E-FILING of Income Tax Return AY : 2018-19 1. Log into pop.ksfe.com/downloadcenter/ using Employee code as Username 2. Download FORM 16 from the Download Link 2. Login to E-FILING website of Income Tax

E-FILING of Income Tax Return AY : 2018-19 1. Log into pop.ksfe.com/downloadcenter/ using Employee code as Username 2. Download FORM 16 from the Download Link 2. Login to E-FILING website of Income Tax

Product Features. TaxPro IT. Chartered Information Systems Pvt. Ltd.

Product Features TaxPro IT Chartered Information Systems Pvt. Ltd. TaxPro Income Tax Computation Software: Product Highlights Apart from the features like Assessee Master Data Management; in-depth coverage

Product Features TaxPro IT Chartered Information Systems Pvt. Ltd. TaxPro Income Tax Computation Software: Product Highlights Apart from the features like Assessee Master Data Management; in-depth coverage

ASSESSMENT YEAR

Final Income Tax Return ASSESSMENT YEAR 008-09 This is your final income tax return. It consists of: 1. Acknowledgement. This Form will be acknowledged by the person who will receive your income tax return

Final Income Tax Return ASSESSMENT YEAR 008-09 This is your final income tax return. It consists of: 1. Acknowledgement. This Form will be acknowledged by the person who will receive your income tax return

NEWSLETTER. M. V. DAMANIA & Co. Chartered Accountants CONTENTS

NEWSLETTER M. V. DAMANIA & Co. Chartered Accountants CONTENTS INTERNATIONAL TAX Allen & Hamilton & Co. - Mumbai Tribunal Bosch Ltd. - Bangalore Tribunal DIRECT TAX J.V.Krishna Rao - Hyderabad Tribunal

NEWSLETTER M. V. DAMANIA & Co. Chartered Accountants CONTENTS INTERNATIONAL TAX Allen & Hamilton & Co. - Mumbai Tribunal Bosch Ltd. - Bangalore Tribunal DIRECT TAX J.V.Krishna Rao - Hyderabad Tribunal

CHANGES IN ITR FORMS FOR A.Y Presented by: CA. Sanjay K. Agarwal

CHANGES IN ITR FORMS FOR A.Y. 2018-19 1 Presented by: CA. Sanjay K. Agarwal Email: agarwal.s.ca@gmail.com TYPES OF INCOME TAX FORMS: FORM(s) ITR 1 ITR 2 ITR 3 ITR 4 PARTICULAR For individuals being a resident

CHANGES IN ITR FORMS FOR A.Y. 2018-19 1 Presented by: CA. Sanjay K. Agarwal Email: agarwal.s.ca@gmail.com TYPES OF INCOME TAX FORMS: FORM(s) ITR 1 ITR 2 ITR 3 ITR 4 PARTICULAR For individuals being a resident

Instructions for filling ITR-3 (AY )

") 1. General Instructions Instructions for filling ITR-3 (AY 2017-18) These instructions are guidelines for filling the particulars in Income Tax Return (ITR) 3. In case of any doubt, please refer to relevant

1. General Instructions Instructions for filling ITR-3 (AY 2017-18) These instructions are guidelines for filling the particulars in Income Tax Return (ITR) 3. In case of any doubt, please refer to relevant

However, a firm whose accounts are liable to audit under section 44AB shall compulsorily furnish the return in the manner mentioned at (i) above.

above.") Instructions for filling out FORM ITR-5 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-5 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

To, July 17, 2007 Mr. P. Chidambaram The Hon ble Finance Minister Government of India, North Block, Vijay Chowk, NEW DELHI

To, July 17, 2007 Mr. P. Chidambaram The Hon ble Finance Minister Government of India, North Block, Vijay Chowk, NEW DELHI 110 001. Re : Discrepancies in quarterly e-tds Statements multiple notices issued

To, July 17, 2007 Mr. P. Chidambaram The Hon ble Finance Minister Government of India, North Block, Vijay Chowk, NEW DELHI 110 001. Re : Discrepancies in quarterly e-tds Statements multiple notices issued

Answer_MTP_ Inter _Syllabus 2016_ Dec 2017_Set 2 Paper 7 Direct Taxation

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

Paper 7 Direct Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 7 Direct Taxation Time Allowed: 3 Hours Full Marks: 100

- Assessee communicate

- Assessee communicate - Income, deduction, exemption, tax, refund, loss, etc - to the department - through the form called return of income - Filled manually or through online - within time specified

- Assessee communicate - Income, deduction, exemption, tax, refund, loss, etc - to the department - through the form called return of income - Filled manually or through online - within time specified

INDIAN INCOME TAX RETURN

FORM ITR-4 INDIAN INCOME TAX RETURN ( For individuals and HUFs having income from a proprietory business or profession) (Please see rule 12 of the Income-tax Rules,1962) Assessment Year (Also see attached

FORM ITR-4 INDIAN INCOME TAX RETURN ( For individuals and HUFs having income from a proprietory business or profession) (Please see rule 12 of the Income-tax Rules,1962) Assessment Year (Also see attached

Instructions for filling ITR-5 (AY )

") 1. General Instructions Instructions for filling ITR-5 (AY 2017-18) These instructions are guidelines for filling the particulars in Income Tax Return (ITR) 5. In case of any doubt, please refer to relevant

1. General Instructions Instructions for filling ITR-5 (AY 2017-18) These instructions are guidelines for filling the particulars in Income Tax Return (ITR) 5. In case of any doubt, please refer to relevant

Instructions for filling out FORM ITR-4

Instructions for filling out FORM ITR-4 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Instructions for filling out FORM ITR-4 These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant provisions of the Income-tax Act,

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No. 3 for assessment year, having the following particulars. (a) PAN (b) Gross Total Income

Government of India INCOME-TAX DEPARTMENT ACKNOWLEDGEMENT Received with thanks from a return of income in Form No. 3 for assessment year, having the following particulars. (a) PAN (b) Gross Total Income

Instructions for filling ITR-1 SAHAJ A.Y

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

Instructions for filling ITR-1 SAHAJ A.Y. 2018-19 General Instructions These instructions are guidelines for filling the particulars in this Return Form. In case of any doubt, please refer to relevant

FORM NO. 2 [See rule 12(1)(b)(i) of Income-tax Rules,1962]

![FORM NO. 2 [See rule 12(1)(b)(i) of Income-tax Rules,1962]](/thumbs/75/72089576.jpg "FORM NO. 2 [See rule 12(1)(b)(i) of Income-tax Rules,1962]") FORM NO. 2 [See rule 12(1)(i) of Income-tax Rules,1962] RETURN OF INCOME SARAL ITS-2 For Non-Corporate assessees not claiming exemption u/s 11 and having income from ACKNOWLEDGEMENT business or profession)

FORM NO. 2 [See rule 12(1)(i) of Income-tax Rules,1962] RETURN OF INCOME SARAL ITS-2 For Non-Corporate assessees not claiming exemption u/s 11 and having income from ACKNOWLEDGEMENT business or profession)

Tax Audits. Tax Audit Reports U/s. 44AB; Form 3CA, 3CB and Form 3CD. August 2011

Tax Audits Tax Audit Reports U/s. 44AB; Form 3CA, 3CB and Form 3CD August 2011 Slide 2 Objectives Participants will be able to understand: Nature and need for tax audits. Form 3CD,clauses and Annexure.

Tax Audits Tax Audit Reports U/s. 44AB; Form 3CA, 3CB and Form 3CD August 2011 Slide 2 Objectives Participants will be able to understand: Nature and need for tax audits. Form 3CD,clauses and Annexure.

Two Ids can now be given in the Return; Mobile Number of the Assessee made mandatory and can be upto 2;

Modification in New Returns Two E-mail Ids can now be given in the Return; Mobile Number of the Assessee made mandatory and can be upto 2; Drop Down Box provided for Section wise Return; 36 Compiled by

Modification in New Returns Two E-mail Ids can now be given in the Return; Mobile Number of the Assessee made mandatory and can be upto 2; Drop Down Box provided for Section wise Return; 36 Compiled by

DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Page 1 of 8 DUTIES & RESPONSIBILITIES OF TAX DEDUCTOR UNDER THE GOODS AND SERVICES TAX ACTS What is GST? Goods and Services Tax (GST) is one indirect tax for the whole Nation, which will make India one

Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB)

and Rule 31AB)") Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB) PDF generated on 18-12-2012 Annual Tax Statement under section 203AA Permanent Account Number: AJQPP9482N Financial

Form No. 26AS (See Section 203AA and second provisio to Section 206C(5) and Rule 31AB) PDF generated on 18-12-2012 Annual Tax Statement under section 203AA Permanent Account Number: AJQPP9482N Financial

NATURE & REMEDIES. A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI

2(4), MUMBAI") NATURE & REMEDIES A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI DEFAULTs u/s. 201(1) & MISMATCHEs u/s. 200A Reasons for Default Types of Default How to Correct? What is the Advantage? Show Cause

NATURE & REMEDIES A Presentation by K.M. SHAHI, ITO(TDS) 2(4), MUMBAI DEFAULTs u/s. 201(1) & MISMATCHEs u/s. 200A Reasons for Default Types of Default How to Correct? What is the Advantage? Show Cause

The Empowered Committee of State Finance Ministers have worked out a dual GST model for India. In

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

GST is proposed to be a comprehensive indirect tax levy on manufacture, sale and consumption of goods as well as on the services at a national level. In an utopian situation, the tax has to be a singular

DIRECT TAX. E TAXATION August Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D.

does not includes : A. Wages B. Pension C. Interest D.") 1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

1 DIRECT TAX 1 Salary Under Section 17(1) does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary : A. Conveyance allowance B. Dearness Allowances C. Children education

BUSINESS PROCESSES ON GST RETURN

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Content provided by Mr. Vineet Bhatia, Advocate BUSINESS PROCESSES ON GST RETURN Proposed returns in the GST regime are quite detailed in nature, with emphasis on cross-matching of data submitted by various

Key Changes In ITR Forms For Assessment Year

Key Changes In ITR For Assessment Year 2017-18 Background The Central Board of Direct Taxes (CBDT) has notified revised Income-tax Returns (ITR) forms for Assessment Year (AY) 2017-18 on 31 st March 2017.

Key Changes In ITR For Assessment Year 2017-18 Background The Central Board of Direct Taxes (CBDT) has notified revised Income-tax Returns (ITR) forms for Assessment Year (AY) 2017-18 on 31 st March 2017.

CA. Mehul Shah. Payment to Transport Contractors implications under the Income-tax Act Overview of Companies Act Care, Pair, and Share

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

Payment to Transport Contractors implications under the Income-tax Act 1961 Overview of Companies Act 2013 CA. Mehul Shah B. Com, F.C.A., DISA (ICAI). Care, Pair, and Share The way s not Smooth 03/06/2015

MAJOR Income Tax Proposals in UNION BUDGET 2017

MAJOR Income Tax Proposals in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 3 rd February 2017, Nehru Place CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No

MAJOR Income Tax Proposals in UNION BUDGET 2017 LUNAWAT & CO. Chartered Accountants 3 rd February 2017, Nehru Place CA. PRAMOD JAIN FCA, FCS, FCMA, LL.B, MIMA, DISA THE CRUX TIMELY FILING OF RETURNS No

Arrear Demand Upload: Salient points

Page 1 of 6 CPC AST> IRLA AO All demand generated on AST till 31.03.2010 needs to be uploaded by AO. Any demand generated on AST from 01.04.2010 is received at CPC automatically. No action is required

Page 1 of 6 CPC AST> IRLA AO All demand generated on AST till 31.03.2010 needs to be uploaded by AO. Any demand generated on AST from 01.04.2010 is received at CPC automatically. No action is required

HIGH COURT OF DELHI. Court on Its Own Motion. Commissioner of Income-tax. W.P.(C) No OF 2012

No OF 2012") PIL on problem of denial of TDS credit by CPC Bangalore on trivial reasons in refund adjustment in violation of section 245: Interim directions to Revenue 31.8.2012 (CBDT directed to urgently look into

PIL on problem of denial of TDS credit by CPC Bangalore on trivial reasons in refund adjustment in violation of section 245: Interim directions to Revenue 31.8.2012 (CBDT directed to urgently look into

CA. PRAMOD JAIN. B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018

, FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018") Union Budget 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018 INCOME TAX PROPOSALS TAX RATES No change in tax

Union Budget 2018 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA Shared at Laxmi Nagar CPE Study Circle of NIRC of ICAI 16 th February 2018 INCOME TAX PROPOSALS TAX RATES No change in tax

Issues in E-filing of Tax Audit Report. Bombay Chartered Accountants Society

Issues in E-filing of Tax Audit Report Bombay Chartered Accountants Society 8 th November, 2014 AMEET N. PATEL Partner Sudit K Parekh & Co. Chartered Accountants Mumbai Pune Hyderabad New Delhi Bangalore

Issues in E-filing of Tax Audit Report Bombay Chartered Accountants Society 8 th November, 2014 AMEET N. PATEL Partner Sudit K Parekh & Co. Chartered Accountants Mumbai Pune Hyderabad New Delhi Bangalore

Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues and Challenges"

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues

The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A Points of discussion with the Group of Ministers on 17th April 2018 on " Return filing under GST-Issues

RETURN FILING UNDER GST ISSUES AND CHALLENGES

RETURN FILING UNDER GST ISSUES AND CHALLENGES TEAM TRD The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A A) Jurisdiction of Tax Payer. Points of discussion

RETURN FILING UNDER GST ISSUES AND CHALLENGES TEAM TRD The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Annexure - A A) Jurisdiction of Tax Payer. Points of discussion

In the Financial World TDS is Tax deducted at. TDS contributes 40% to the gross direct tax

In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance.

In the Financial World TDS is Tax deducted at Source TDS contributes 40% to the gross direct tax collections It has been brought with the principle of Pay As you Earn i.e. Collection of Tax in Advance.

Interim Union Budget 2019 & Important changes for AY CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP

, FCA, FCS, FCMA, LL.B, MIMA, DISA, IP") Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME

Interim Union Budget 2019 & Important changes for AY 2019-20 CA. PRAMOD JAIN B. COM (H), FCA, FCS, FCMA, LL.B, MIMA, DISA, IP Shared at Nehru Place CPE Study Circle of NIRC of ICAI 7 th February 2019 INCOME

Tax Liability Ledger, will reflect the total tax liability of a tax payer (after netting) for the particular month.

for the particular month.") ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

ELECTRONIC LEDGERS & PAYMENTS Once a tax payer is registered on the common portal GSTN, two e-ledgers Cash Ledger & Input Tax Credit Ledger and an Electronic Tax liability ledger will be automatically

The Centre of Excellence for GST. GST: Returns. JULY 09, 2017 ICAI Tower, BKC MUMBAI. CA. Hemant P. Vastani. The Centre of Excellence for GST

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

GST: Returns JULY 09, 2017 ICAI Tower, BKC MUMBAI CA. Hemant P. Vastani 1 Sections Covering Returns 37. Furnishing details of outward supplies. 38. Furnishing details of inward supplies. 39. Furnishing

TRACES Site and Issues in Deemed, Recovery & online resolution

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

TRACES Site and Issues in Deemed, Recovery & online resolution The material contained in the ensuing slides is for general information, compilation is from various websites, views of the experts and the

e- filing of Income Tax Returns- An Overview

e- filing of Income Tax Returns- An Overview Presented by CA Sanjeev Soota catch me at www.caindelhi.co.in www.casanjeevsoota.com Notification No. 34/2013 dated 1 st May, 2013 Rule 12 of the Income Tax

e- filing of Income Tax Returns- An Overview Presented by CA Sanjeev Soota catch me at www.caindelhi.co.in www.casanjeevsoota.com Notification No. 34/2013 dated 1 st May, 2013 Rule 12 of the Income Tax

.m<:rcr" ~m;n:r (~) DIRECTORATEOF INCOMETAX (SYSTEM) "Cr 3ffi" "Cr. m, 31-(f(>f, t-2 $'i gem>! Ia=t l!crf

DIRECTORATEOF INCOMETAX (SYSTEM) Cr 3ffi Cr. m, 31-(f(>f, t-2 $'i gem>! Ia=t l!crf") .mf, t-2 $'i gem>! Ia=t l!crf ARACenter, Ground Floor, "- E-2, Jhandewalan Extension, ~;mm ~ ~ _ 110055, New Delhi - 110055 F.No.

.mf, t-2 $'i gem>! Ia=t l!crf ARACenter, Ground Floor, "- E-2, Jhandewalan Extension, ~;mm ~ ~ _ 110055, New Delhi - 110055 F.No.

INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For firms, AOPs and BOIs] (Please see rule 12 of the Income-tax Rules,1962)

![INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For firms, AOPs and BOIs] (Please see rule 12 of the Income-tax Rules,1962)](/thumbs/85/91382480.jpg "INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For firms, AOPs and BOIs] (Please see rule 12 of the Income-tax Rules,1962)") FORM ITR-5 INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For firms, AOPs and BOIs] (Please see rule 12 of the Income-tax Rules,1962) Assessment Year (Also see attached instructions)

FORM ITR-5 INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For firms, AOPs and BOIs] (Please see rule 12 of the Income-tax Rules,1962) Assessment Year (Also see attached instructions)

Overview of Income-tax Return Forms

Overview of Income-tax Return Forms Seminar Organized by Members of International Tax CA. Group August 08, 2015 Presented by: CA. Ashish Garg Email: citycaashish@gmail.com Mobile No.: +919873467270 August

Overview of Income-tax Return Forms Seminar Organized by Members of International Tax CA. Group August 08, 2015 Presented by: CA. Ashish Garg Email: citycaashish@gmail.com Mobile No.: +919873467270 August

DIRECT TAX PROPOSALS OF UNION BUDGET 2012

DIRECT TAX PROPOSALS OF UNION BUDGET 2012 WWW.ITRVAULT.IN ITR VAULT is your one stop solution to store, save, extract, send and print all your important documents. Searching for the required documents

DIRECT TAX PROPOSALS OF UNION BUDGET 2012 WWW.ITRVAULT.IN ITR VAULT is your one stop solution to store, save, extract, send and print all your important documents. Searching for the required documents

Recent changes in Rule 12, Income tax return forms for AY & EVC. dk bholusaria

Recent changes in Rule 12, Income tax return forms for AY 2015-16 & EVC dk bholusaria dk@bholusaria.com Today s agenda Highlights of changes in rule 12. Assessee, applicable return and mode of filing for

Recent changes in Rule 12, Income tax return forms for AY 2015-16 & EVC dk bholusaria dk@bholusaria.com Today s agenda Highlights of changes in rule 12. Assessee, applicable return and mode of filing for

Issues in filing TDS returns

Issues in filing TDS returns Contents Components of TIN Correction statement Consolidated TDS/TCS statement Online TAN registration Annual Tax Statement New @ TIN FILER DEDUCTOR TAX PAYER TIN FC ERACS

Issues in filing TDS returns Contents Components of TIN Correction statement Consolidated TDS/TCS statement Online TAN registration Annual Tax Statement New @ TIN FILER DEDUCTOR TAX PAYER TIN FC ERACS

Q & A_MTP_ Final _Syllabus 2016_ June 2017_Set 1 Paper 16 Direct Tax Laws And International Taxation

Paper 16 Direct Tax Laws And International Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 16 Direct Tax Laws and International

Paper 16 Direct Tax Laws And International Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 16 Direct Tax Laws and International

Note on Tax Deduction at Source

www.legale-services.com Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting

www.legale-services.com Note on Tax Deduction at Source What is Tax Deduction at Source (TDS)? TDS is a way by which a certain percentage of amounts are deducted by a person at the time of making/crediting

TDS & TCS Recent Updates & Amendments.

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

TDS & TCS Recent Updates & Amendments. By. CA. Tarun Jain. B.com, FCA. Synopsis of Discussion Amendments in Finance act 2016. Amendment to Section 206AA New provisions relating to TCS Other Miscellaneous

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. New Delhi, the 21 st May, 2009 Subject:- New TDS and TCS payment and information reporting

F.No. 142/22/2008-TPL Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes. New Delhi, the 21 st May, 2009 Subject:- New TDS and TCS payment and information reporting

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS 1 The material contained in the ensuing slides is for general information, compilation and the views of the speaker and is purely for general discussion at the

CONSEQUENCES OF DEFAULTS IN e-tds RETURNS 1 The material contained in the ensuing slides is for general information, compilation and the views of the speaker and is purely for general discussion at the

Electronic Tax Liability Register of Taxpayer (Part I: Return related liabilities)

") GST Payment of Tax Rule Sr # Form # Payment of Tax Rules Title of Form Analysis 1 Form GST 1) Electronic Tax Liability Register PMT-01 (1) The electronic tax liability register under sub-section (7) of

GST Payment of Tax Rule Sr # Form # Payment of Tax Rules Title of Form Analysis 1 Form GST 1) Electronic Tax Liability Register PMT-01 (1) The electronic tax liability register under sub-section (7) of

Free of Cost ISBN: CS Executive Programme Module-I (Solution upto June & Questions of Dec Included)

") Free of Cost ISBN: 978-93-5034-584-9 Appendix CS Executive Programme Module-I (Solution upto June - 2013 & Questions of Dec - 2013 Included) Paper - 3: Tax Laws Chapter - 3: Basis of Charge and Scope of

Free of Cost ISBN: 978-93-5034-584-9 Appendix CS Executive Programme Module-I (Solution upto June - 2013 & Questions of Dec - 2013 Included) Paper - 3: Tax Laws Chapter - 3: Basis of Charge and Scope of

Chapter 1 : Income Tax Concept and Computation of Income Tax

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Chapter 1 : Income Tax Concept and Computation of Income Tax This Chapter includes : I. Taxation in India 1. Taxes and its levying authority 2. Tax Structure 3. Hierarchy of Taxes levied and collected

Tax Deduction at Source FY (AY )

") Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

Tax Deduction at Source FY 2017-18 (AY 2018-19) CA Pranjal Joshi M.com, F.C.A., DipIFR (ACCA-UK), Cert. Business Valuation (ICAI) M/s Pranjal Joshi & Co Chartered Accountants TDS introduction - Income

Income Tax Reckoner AY:

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

1. Rates of Income Tax Individuals having income > 5 Lacs* Individuals & Charitable Trust Senior Citizen (60 to 79) Very Senior citizen (80 and above) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to `

CA Final Paper 3 Advance Auditing & Professional Ethics Chapter 15. CA.Saubhik Sarkar

CA Final Paper 3 Advance Auditing & Professional Ethics Chapter 15 CA.Saubhik Sarkar 1. Introduction 2. Audit of Public Trust 3. Audit for claiming deduction under Section 35 D & 35E 4. Tax Audit under

CA Final Paper 3 Advance Auditing & Professional Ethics Chapter 15 CA.Saubhik Sarkar 1. Introduction 2. Audit of Public Trust 3. Audit for claiming deduction under Section 35 D & 35E 4. Tax Audit under

INCOME TAX: SET OFF AND CARRY FORWARD OF LOSSES

35 INCOME TAX: SET OFF AND CARRY FORWARD OF LOSSES CHAPTER We have studied so far that income tax is to be computed under five different heads, salary, income from house property, income from business

35 INCOME TAX: SET OFF AND CARRY FORWARD OF LOSSES CHAPTER We have studied so far that income tax is to be computed under five different heads, salary, income from house property, income from business

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, Amendments w.e.f

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, 1961 Amendments w.e.f 1.4.2015 SN Section Provision 1 4(1) {r/w Sec. 2(4) of the Finance Act, 2015} {Surcharge} In cases in which tax

GLIMPSE INTO AMENDMENTS BY THE FINANCE ACT, 2015 TO INCOME TAX ACT, 1961 Amendments w.e.f 1.4.2015 SN Section Provision 1 4(1) {r/w Sec. 2(4) of the Finance Act, 2015} {Surcharge} In cases in which tax

(Also see attached instructions) Road/Street/Post Office Area/Locality If a domestic company (Tick) (STD code)-phone Number ( )

Road/Street/Post Office Area/Locality If a domestic company (Tick) (STD code)-phone Number ( )") FORM ITR-6 INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For Companies other than companies claiming exemption under section 11] (Please see rule 12 of the Income-tax Rules,1962) Assessment

FORM ITR-6 INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For Companies other than companies claiming exemption under section 11] (Please see rule 12 of the Income-tax Rules,1962) Assessment

Changes in ITR for AY

Changes in ITR for AY 2018-2019 Disclaimer This presentation has been prepared for academic use only for sharing knowledge on the subject. Though every effort has been made to avoid errors or omissions

Changes in ITR for AY 2018-2019 Disclaimer This presentation has been prepared for academic use only for sharing knowledge on the subject. Though every effort has been made to avoid errors or omissions

FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962]

![FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962]](/thumbs/89/98100419.jpg "FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962]") FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962] RETURN OF INCOME SARAL ITS-3 (For Non-Corporate assessees not claiming exemption u/s 11 and not having income from ACKNOWLEDGEMENT business

FORM NO. 3 [See rule 12(1)(b)(iii) of Income-tax Rules, 1962] RETURN OF INCOME SARAL ITS-3 (For Non-Corporate assessees not claiming exemption u/s 11 and not having income from ACKNOWLEDGEMENT business

(Also see attached instructions) Road/Street/Post Office Area/Locality If a domestic company (Tick) (STD code)-phone Number ( )

Road/Street/Post Office Area/Locality If a domestic company (Tick) (STD code)-phone Number ( )") FORM ITR-6 INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For Companies other than companies claiming exemption under section 11] (Please see rule 12 of the Income-tax Rules,1962) Assessment

FORM ITR-6 INDIAN INCOME TAX RETURN ( Including Fringe Benefit Tax Return) [For Companies other than companies claiming exemption under section 11] (Please see rule 12 of the Income-tax Rules,1962) Assessment

Registration. Chapter IV. FAQ s. Registration (Section 22 to 30)

") Chapter IV Registration FAQ s Registration (Section 22 to 30) Section 22 to 30 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of the UTGST

Chapter IV Registration FAQ s Registration (Section 22 to 30) Section 22 to 30 of the CGST Act, 2017 made applicable to IGST vide Section 20 of the IGST Act, 2017 and UTGST vide Section 21 of the UTGST

2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed

![2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed](/thumbs/84/90875315.jpg "2.f List of benefits available to Small Businessmen [AY ] S.N. Particulars Section Benefits/Deductions allowed") 2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

2.f List of benefits available to Small Businessmen [AY 2017 18] S.N. Particulars Section Benefits/Deductions allowed A. Presumptive Taxation Scheme 1. Computation of income from eligible business on presumptive

ALL GUJARAT FEDERATION OF TAX CONSULTANTS

ALL GUJARAT FEDERATION OF TAX CONSULTANTS PRE-BUDGET MEMORANDUM FOR 2015-16 1. Section 2(22)(e) : Deemed Dividend As per the present provision, even if advance or loan is given to a share holder for one

ALL GUJARAT FEDERATION OF TAX CONSULTANTS PRE-BUDGET MEMORANDUM FOR 2015-16 1. Section 2(22)(e) : Deemed Dividend As per the present provision, even if advance or loan is given to a share holder for one

Registration. Chapter IV FAQS. Registration (Section 22 to 30)

") Chapter IV Registration FAQS Registration (Section 22 to 30) Q1. If a person is operating in different states, with the same PAN number, can he operate with a single Registration? Ans. No. Every person

Chapter IV Registration FAQS Registration (Section 22 to 30) Q1. If a person is operating in different states, with the same PAN number, can he operate with a single Registration? Ans. No. Every person

Income Tax Reckoner AY:

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

General* 1. Rates of Income Tax Individuals & Charitable Trust, Senior Citizen (60 to 79) Very Senior citizen (80 and above) (Amount in `) Rates Up to ` 2.00 Lacs Up to ` 2.50 Lacs Up to ` 5.00 Lacs Nil

2. Delay in updation of TDS credit in Form No. 26AS of the taxpayer and approaching due date of TDS statement filing for first quarter

Although the ITR forms for AY 2018-19 were notified on 3 rd April, 2018 vide Notification No. 16/2018, the ITR Form utilities in Java and Excel were released much later in the month of May, 2018(except

Although the ITR forms for AY 2018-19 were notified on 3 rd April, 2018 vide Notification No. 16/2018, the ITR Form utilities in Java and Excel were released much later in the month of May, 2018(except

April 2017 CA K Prasanna and ca Abhinaya Ramanujam

Assessment Procedure April 2017 CA K Prasanna and ca Abhinaya Ramanujam Topics Covered Return of Income Self-Assessment (S 140A) Enquiry before Assessment (S 142(1)) Summary Assessment (S 143(1)) Scrutiny

Assessment Procedure April 2017 CA K Prasanna and ca Abhinaya Ramanujam Topics Covered Return of Income Self-Assessment (S 140A) Enquiry before Assessment (S 142(1)) Summary Assessment (S 143(1)) Scrutiny

Form 26AS. Annual Tax Statement under Section 203AA of the Income Tax Act, 1961

Data updated till 14Feb2013 Form 26AS Annual Tax Statement under Section 203AA of the Income Tax Act, 1961 Permanent Account Number Name of Assessee Address of Assessee AANPK4324N Financial Year 201213

Data updated till 14Feb2013 Form 26AS Annual Tax Statement under Section 203AA of the Income Tax Act, 1961 Permanent Account Number Name of Assessee Address of Assessee AANPK4324N Financial Year 201213

CA RAKESH M. VORA. R P J & ASSOCIATES Chartered Accountants

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

CA RAKESH M. VORA R P J & ASSOCIATES Chartered Accountants Thursday - 8th March, 2018 1 INDEX Introduction to TDS Compliance Provisions Important Payments covered under the scheme of TDS. Details of TDS

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS 1 List of Forms Sr. No. Form No. Title of the Form 1 2 3 1. GSTR-1 2. GSTR-1A 3. GSTR-2 4. GSTR-2A 5. GSTR-3 6. GSTR-3A Details of outwards supplies of

GOODS AND SERVICES TAX RULES, 2017 RETURN FORMATS 1 List of Forms Sr. No. Form No. Title of the Form 1 2 3 1. GSTR-1 2. GSTR-1A 3. GSTR-2 4. GSTR-2A 5. GSTR-3 6. GSTR-3A Details of outwards supplies of

Time allowed : 3 hours Maximum marks : 100. Total number of questions : 8 Total number of printed pages : 6

: 1 : 223 RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 6 NOTE : All references to sections mentioned in Part-A of the Question Paper

: 1 : 223 RollNo... Time allowed : 3 hours Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 6 NOTE : All references to sections mentioned in Part-A of the Question Paper