Capital Gains Tax Planning In A World Without Estate Tax

|

|

|

- Cameron Quinn

- 6 years ago

- Views:

Transcription

1 BRUCE GIVNER ( bruce@givnerkaye.com) OWEN D. KAYE ( owen@givnerkaye.com) KATHLEEN GIVNER ( kathy@givnerkaye.com) NEDA BARKHORDAR ( neda@givnerkaye.com) JACQUELINE BURBANK ( jacqueline@givnerkaye.com) LAW OFFICES SUITE WILSHIRE BOULEVARD LOS ANGELES, CALIFORNIA South Bay Estate Planning Council PHONE (310) (818) FAX (310) (818) I. LIKELY MAXIMUM 2017 RATES COMPARED TO MAXIMUM 2016 RATES. Ordinary (Earned) Income. 2016: 39.6% federal plus (13.3% X 60.4% = ) % = % 2017: 33% federal plus 13.3% 1 = 46.3% = 97.2% (a reduction of % in the rate itself). Ordinary (Passive) Income. Capital Gain. 2016: 39.6% federal plus (60.4% x 3.8% = ) % % = % 2017: 33% federal plus 13.3% = 46.3% = 92.73% (a reduction of % in the rate itself) in the A.M.T. 2 Passive. 20% + 3.8% % = 37.1% Materially Participating. 20% % = 33.3% 2017: depends on what rate you believe will be enacted. Compare: Trump 20% % = 33.3% House (1/2 max. pers rate) 16.5% % = 29.8% II. passive will be 33.3% 37.1 = 89.76% or 29.8% 37.1% = 80.3% Materially particip g 33.3% (same) or 29.8% 33.3% = 89.5% LIKELY 2017 NEVADA ADVANTAGE. Ordinary (Earned) Income (Maximum). Before: % vs. 39.6% = 83.14%. An % rate advantage (the deductible California tax rate). Now: 46.3% vs. 33%. 33.3% 46.3% = 72%. A 13.3% rate advantage (California tax no longer deductible). 1 No deduction for state and local taxes. 2 Both President Trump and the Republicans plan eliminate the A.M.T. 3 Can Congress have a transition period of several years in which the A.C.A. stays in existence, while it comes up with a replacement, in which it repeals the 3.8%? If so, that creates a huge hole in the deficit.

2 Page 2 of 33 Capital Gain. Before: Passive: 37.1 vs Nevada was 64% of California tax. Now: Materially Participating: 33.3 vs. 20. Nevada was 60% of California tax. Trump: 33.3% vs. 20%. Nevada will be 60% of California tax. III. GOP: 29.8% vs. 16.5%. Nevada will be 55.4% of California. CAPITAL GAINS TAX PLANNING Preliminary Which Rate Will Prevail? If you think the House rate will prevail, the argument to Pay The Tax And Pocket The Proceeds is stronger than ever as 29.8% is a great rate. If you believe that rate is unattainable, and the rate will be 33.3%, the same analysis applies in 2017 as in 2016: those with large capital gains will want to examine alternatives to paying all of the tax Timing. Timing: the most important element in all tax planning (and asset protection planning). Teaching the client the wisdom of owning nothing, controlling everything. Own Control. Make client comfortable the client can control the children s trust. Maintenance programs Statutory Wealthy real estate families don t do 1031s. IRS: gave up on drop and swap after: Bolker, 760 F2d 1039 (9 th 1985). Magneson, 753 F. 2d 1490 (9 th 1985). FSA : Although we disagree with the conclusion that a taxpayer that receives property subject to a prearranged agreement to immediately transfer the property `holds the property for investment, we are no longer pursuing this position in litigation. FTB Project: drop and swap and swap and drop. Rago Development Corporation, June 23, 2015 SBE upheld swap & drop: Taxpayers held property for 7 months before drop into LLC.

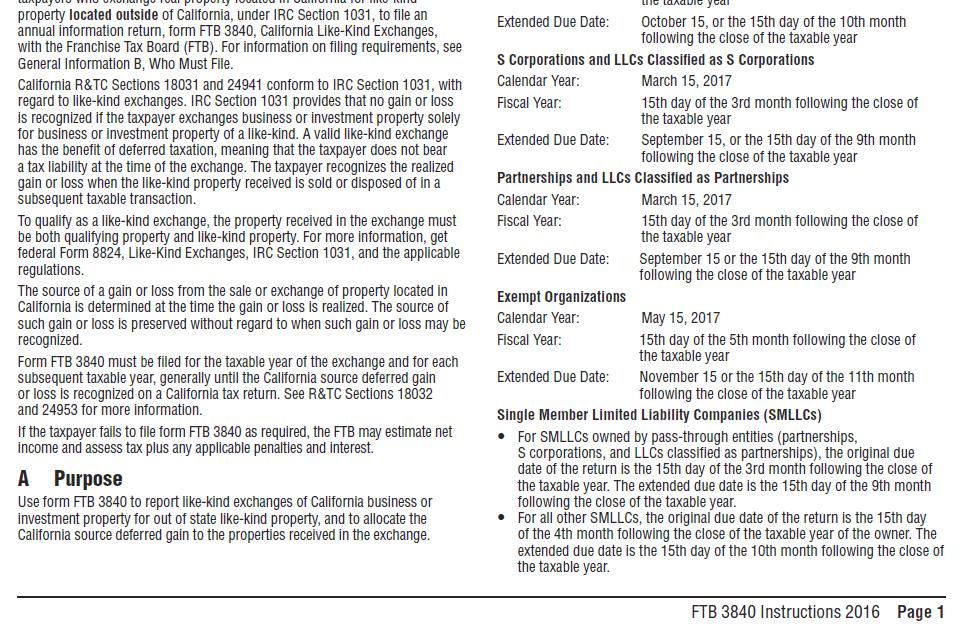

3 Page 3 of 33 Transfer to the LLC was the lender s requirement. See FTB Form 3840 attached (e). The best capital gains tax planning as it is on the face of the Code. See the attached diagram. Problem? Finding taxpayers more than 2 years in advance. Impact of Woelbing and Davidson audits. IRC 453A: $5,000,000 per seller limit. You must pay interest, at the underpayment rate (currently 4%), on the tax inherent in the installment notes A See the four pages comparing countries tax burdens. Mark to market exit tax borrowed from Canada. $699,000 for 2017 is the excluded gain. $164,000 is the average annual net income for the 5 preceding taxable years. $2,000,000 or more is the net worth test to be a covered individual. Security for deferred tax is only a bond or LC. Very restrictive. 30% withholding from a non-grantor trust. No more than 120 days per year to avoid the 7701(a) substantial presence test, but arguably no more than 30 days. Reed Amendment: Any alien who is a former [U.S.] citizen who officially renounces Citizenship and who the Attorney General [determines] to have renounced citizenship for the purpose of avoiding taxation is inadmissible. Gross income of a bona fide resident of the Virgin Islands does not include any amount included in gross income on that person s V.I. income tax return. 932(c)(4). This applies only if the V.I. resident reports all income from all sources on the V.I. return, identifies each item s source and pays the amount determined under 934 as V.I. income tax liability. See Publication 1321 about filing in Puerto Rico. Gross income of a bona fide resident of Puerto Rico, who is a resident for the entire taxable year, does not include income derived from sources within P.R. 933(1). Gross income of a U.S. citizen who has been a bona fide P.R. resident for a period of at least two years before the date on which the P.R. residency ends does not include income derived from sources with P.R. attributable to the period of P.R. residency. 933(2). Neither exclusion applies to amounts paid for services performed as a U.S. or agency employee. Doesn t work with encumbered real estate. Parents plus 3 children works: See diagram and calculations.

4 Page 4 of Others. V. CONCLUSION. On surviving parent s death there is inclusion. Most people simply don t buy life insurance. Doesn t work with a personal residence: must convert to TorB or investment. Doesn t work with S corporations Charitable LLC. See the Jay Adkisson Forbes article. See the diagram and comparative advantage. See IRS Form Sale of LP interests followed by a 754 election. Avoid the 2 year holding period requirement of 453(e). 2/9/06 IRS Redemption Bogus optional basis tax shelter announcement. 4/28/16 SBE s Khoury decision. Michael Hamersley, Esq. Rev. & Tax Code 19774: see attachment Sale to a technically unrelated, but friendly, third party. How does your Uncle come up with 10% down? Your Uncle needs to make a profit. Wait until statute of limitations runs to drop it into an LLC which you manage Use of partnership to move basis from one asset to another. $10,000,000 apartment building with $1,000,000 of basis. In a partnership. Parents have a frozen interest. Children have a zero basis common interest. Partnership buys raw land for $9,000,000 for the next deal. Two years later the partnership redeems out the children s trust Professional third parties. Deferred Sales Trust by Monetized Installment Sale. Stan Crow. See BNA item on January, 2016, ABA meeting in Los Angeles Nevada non-grantor trust. See the FTB Information Letter. See the diagram. There will always be an estate tax. See the final pages about SB 726.

5 Page 5 of 33

6 Page 6 of 33

7 Page 7 of 33

8 Page 8 of 33

9 Page 9 of 33

10 Page 10 of 33 bulgaria-27--corporate-taxes-in-bulgaria-are-just-10-the-same-as-the-maximum-possible-income-taxcharged-to-individuals-in-the-country-that-numbers-is-one-of-the-five-lowest-in-europe-1 The total amount of taxes is the sum of five different types of taxes and contributions payable after accounting for deductions and exemptions: profit or corporate income tax, social contributions, and labour taxes paid by the employer, property taxes, turnover taxes and other small taxes. 29. Bulgaria 27%. 28. Thailand 26.9%. 27. Denmark 26%. 26. Ireland 25.9% 25. Laos 25.8% 24. Botswana 25.3% 23. Mauritius 24.5% 22. Mongolia 24.4% 21. Bosnia/Herzegovina 23.3% 20. Cyprus 23.2% 19. Oman 23% 18. Hong Kong 22.8% 17. Montenegro 22.3% 15. Canada 21% 15. Cambodia 21% 14. Namibia 20.7% 13. Armenia 20.4% 12. Luxembourg 20.2% 11. Croatia 18.8% 10. Singapore 18.4% 9. Georgia 16.4% 7. UAE 14.8% 7. Zambia 14.8% 6. Saudi Arabia 14.5% 5. Lesotho 13.6% 4. Bahrain 13.5% 3. Kuwait 12.8% 2. Qatar 11.3% 1. Macedonia 7.4%

11 Page 11 of 33

12 Page 12 of 33

13 Page 13 of 33

14 Page 14 of 33

15 Page 15 of 33

16 Page 16 of 33

17 Page 17 of 33

18 Page 18 of 33

19 Page 19 of 33

20 Page 20 of 33

21 Page 21 of 33 Charitable Limited Partnership

22 Page 22 of 33

23 Page 23 of 33

24 Page 24 of 33

25 Page 25 of 33 California Revenue & Taxation Code (a) If a taxpayer has a noneconomic substance transaction [ NEST ] understatement for any taxable year, there shall be added to the tax an amount equal to 40% of the amount of that understatement. (b) (1) Subdivision (a) shall be applied by substituting 20% for 40% as to the portion of any NEST understatement as to which the relevant facts affecting the tax treatment of the item are adequately disclosed in the return or a statement attached to the return. (c) For purposes of this section: (1) The term NEST understatement means any amount which would be an understatement under IRC 6662A(b), as modified by (b) if IRC 6662A(b) were applied by taking into account items attributable to NESTs rather than items to which 6662A(b) applies. (2) A NEST includes: (A) The disallowance of any loss, deduction or credit, or addition to income attributable to a determination that the disallowance or addition is attributable to a transaction or arrangement that lacks economic substance including a transaction or arrangement in which an entity is disregarded as lacking economic substance. A transaction shall be treated as lacking economic substance if the taxpayer does not have a valid nontax California business purpose for entering into the transaction. (B) Any disallowance of claimed tax benefits due to a transaction lacking economic substance, within the meaning of IRC 7701(o) relating to clarification of economic substance doctrine except as otherwise provided. (i) For purposes of this subparagraph, the phrase apart from state income tax effects shall be substituted for the phrase apart from Federal income tax effects in each place it appears in IRC 7701(o)(1). (ii) For purposes of this subparagraph, the phrase any federal or local income tax effect which is related to a state income tax effect shall be treated in the same manner as a state income tax effect is substituted for the phrase any State or local income tax effect which is related to a Federal income tax effect shall be treated in the same manner as a Federal income tax effect in IRC 7701(o)(3).

26 Page 26 of 33 (d) (1) If the notice of proposed assessment of additional tax has been sent as to a penalty to which this section applies, only the FTB Chief Counsel may compromise all or any portion of that penalty. (2) The exercise of authority under paragraph (1) shall be at the FTB Chief Counsel s sole discretion and may not be delegated. (3) Despite any other law or rule of law, any determination under this subdivision may not be reviewed in any administrative or judicial proceeding [??!!]. (e) Despite anything to the contrary in this section, if a penalty has been assessed for federal income tax purposes pursuant to IRC Section 6662(b)(6) on an underpayment attributable to the disallowance of claimed tax benefits due to a transaction lacking economic substance, then a penalty shall be imposed under this section for that portion of an understatement attributable to that transaction, and shall not be abated unless the taxpayer can establish that the imposition of the federal penalty under IRC 6662 was clearly erroneous.

27 Page 27 of 33

28 Page 28 of 33

29 Page 29 of 33

30 Page 30 of 33

31 Page 31 of 33

32 Page 32 of 33

33 Page 33 of 33

Tax Planning Right Now Under Trump

BRUCE GIVNER (bruce@givnerkaye.com) OWEN D. KAYE (owen@givnerkaye.com) KATHLEEN GIVNER (kathy@givnerkaye.com) NEDA BARKHORDAR (neda@givnerkaye.com) JACQUELINE BURBANK (jacqueline@givnerkaye.com) SUITE

BRUCE GIVNER (bruce@givnerkaye.com) OWEN D. KAYE (owen@givnerkaye.com) KATHLEEN GIVNER (kathy@givnerkaye.com) NEDA BARKHORDAR (neda@givnerkaye.com) JACQUELINE BURBANK (jacqueline@givnerkaye.com) SUITE

October 19, 2017 CAPITAL GAINS TAX PLANNING PART 1 - INTRODUCTION

BRUCE GIVNER (bruce@givnerkaye.com) OWEN D. KAYE (owen@givnerkaye.com) KATHLEEN GIVNER (kathy@givnerkaye.com) NEDA BARKHORDAR (neda@givnerkaye.com) LAW OFFICES SUITE 445 12100 WILSHIRE BOULEVARD LOS ANGELES,

BRUCE GIVNER (bruce@givnerkaye.com) OWEN D. KAYE (owen@givnerkaye.com) KATHLEEN GIVNER (kathy@givnerkaye.com) NEDA BARKHORDAR (neda@givnerkaye.com) LAW OFFICES SUITE 445 12100 WILSHIRE BOULEVARD LOS ANGELES,

Form Specified Individual. The Instructions to Form 8938 define a Specified Individual as: A U.S. Citizen.

Form 8938 On March 18, 2010, the Foreign Account Tax Compliance Act ( FATCA ) was enacted as part of the Hiring Incentives to Restore Employment ( HIRE ) Act. Section 511 of FATCA creates new Internal

Form 8938 On March 18, 2010, the Foreign Account Tax Compliance Act ( FATCA ) was enacted as part of the Hiring Incentives to Restore Employment ( HIRE ) Act. Section 511 of FATCA creates new Internal

a closer look GLOBAL TAX WEEKLY ISSUE 271 JANUARY 18, 2018

GLOBAL TAX WEEKLY a closer look ISSUE 271 JANUARY 18, 2018 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 271 JANUARY 18, 2018 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Three Reasons International Families Should Consider Qualified Domestic Trusts. John C. Martin 1

Three Reasons International Families Should Consider Qualified Domestic Trusts John C. Martin 1 Martin1 What kind estate planning is advisable for individuals with a non US citizen spouse? In most cases,

Three Reasons International Families Should Consider Qualified Domestic Trusts John C. Martin 1 Martin1 What kind estate planning is advisable for individuals with a non US citizen spouse? In most cases,

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Information Reporting and Civil Penalties (in a Nutshell)

") I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

I. In General Information Reporting and Civil Penalties (in a Nutshell) By Lucy S. Lee, Esq. Caplin & Drysdale, Chartered Washington, D.C. 2008 Lucy S. Lee The Internal Revenue Code (the Code ) 1 generally

Business and Personal Income Tax Planning Under The New Tax Law

BRUCE GIVNER ( bruce@givnerkaye.com) OWEN D. KAYE ( owen@givnerkaye.com) KATHLEEN GIVNER ( kathy@givnerkaye.com) NEDA BARKHORDAR ( neda@givnerkaye.com) JACQUELINE BURBANK ( Jacqueline@GivnerKaye.com) SUITE

BRUCE GIVNER ( bruce@givnerkaye.com) OWEN D. KAYE ( owen@givnerkaye.com) KATHLEEN GIVNER ( kathy@givnerkaye.com) NEDA BARKHORDAR ( neda@givnerkaye.com) JACQUELINE BURBANK ( Jacqueline@GivnerKaye.com) SUITE

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

This notice announces that the Department of the Treasury ( Treasury

Additional Guidance Under Section 965; Guidance Under Sections 62, 962, and 6081 in Connection With Section 965; and Penalty Relief Under Sections 6654 and 6655 in Connection with Section 965 and Repeal

Additional Guidance Under Section 965; Guidance Under Sections 62, 962, and 6081 in Connection With Section 965; and Penalty Relief Under Sections 6654 and 6655 in Connection with Section 965 and Repeal

Ch. 14 Corporate Tax Anti-avoidance Rules

Ch. 14 Corporate Tax Anti-avoidance Rules In the U.S. corporate income tax context U.S. Treasury Department has concerns about: 1) Avoidance of the double tax on corporate/shareholder taxation. 2) Avoiding

Ch. 14 Corporate Tax Anti-avoidance Rules In the U.S. corporate income tax context U.S. Treasury Department has concerns about: 1) Avoidance of the double tax on corporate/shareholder taxation. 2) Avoiding

California Voluntary Compliance Initiative II for Abusive Tax Avoidance Transactions and Offshore Financial Arrangements.

California Voluntary Compliance Initiative II for Abusive Tax Avoidance Transactions and Offshore Financial Arrangements. BY VALERIE DICKERSON & MATTHEW JOHNSON California Voluntary Compliance Initiative

California Voluntary Compliance Initiative II for Abusive Tax Avoidance Transactions and Offshore Financial Arrangements. BY VALERIE DICKERSON & MATTHEW JOHNSON California Voluntary Compliance Initiative

Withholding Tax Rate under DTAA

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

Withholding Tax Rate under DTAA Country Albania 10% 10% 10% 10% Armenia 10% Australia 15% 15% 10%/15% [Note 2] 10%/15% [Note 2] Austria 10% Bangladesh Belarus a) 10% (if at least 10% of recipient company);

If you have foreign accounts, entities, or assets, chances are that you

International Tax Form Filing Guide If you have foreign accounts, entities, or assets, chances are that you will be required to file various forms disclosing them. Some of these forms are filed with your

International Tax Form Filing Guide If you have foreign accounts, entities, or assets, chances are that you will be required to file various forms disclosing them. Some of these forms are filed with your

a closer look GLOBAL TAX WEEKLY ISSUE 254 SEPTEMBER 21, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 254 SEPTEMBER 21, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

GLOBAL TAX WEEKLY a closer look ISSUE 254 SEPTEMBER 21, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%

![Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%](/thumbs/88/116150947.jpg "Albania 10% 10%[Note1] 10% 10% Armenia 10% 10% [Note1] 10% 10% Austria 10% 10% [Note1] 10% 10%") Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

Country Dividend (not being covered under Section 115-O) Withholding tax rates Interest Royalty Fee for Technical Services Albania 10% 10%[Note1] 10% 10% Armenia 10% Australia 15% 15% 10%/15% 10%/15% Austria

MANAGING INTERNATIONAL TAX ISSUES

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

MANAGING INTERNATIONAL TAX ISSUES Starting A Business Retirement Strategies Operating A Business Marriage Investing Tax Smart Estate Planning Ending A Business Off to School Divorce And Separation Travel

Withholding tax rates 2016 as per Finance Act 2016

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Withholding tax rates 2016 as per Finance Act 2016 Sr No Country Dividend Interest Royalty Fee for Technical (not being covered under Section 115-O) Services 1 Albania 10% 10% 10% 10% 2 Armenia 10% 10%

Internal Revenue Code Section 6662(j) Imposition of accuracy-related penalty on underpayments.

Imposition of accuracy-related penalty on underpayments.") Internal Revenue Code Section 6662(j) Imposition of accuracy-related penalty on underpayments. CLICK HERE to return to the home page (a) Imposition of penalty. If this section applies to any portion of

Internal Revenue Code Section 6662(j) Imposition of accuracy-related penalty on underpayments. CLICK HERE to return to the home page (a) Imposition of penalty. If this section applies to any portion of

1031 DROP AND SWAP: BREAKING UP IS HARD TO DO. By: Gary Kravitz, Esq. and Kevin Henry, Esq.

1031 DROP AND SWAP: BREAKING UP IS HARD TO DO By: Gary Kravitz, Esq. and Kevin Henry, Esq. I. THE BASICS OF 1031 EXCHANGES AND THE USE OF LIMITED LIABILITY COMPANIES IN REAL ESTATE ACQUISITIONS A. What

1031 DROP AND SWAP: BREAKING UP IS HARD TO DO By: Gary Kravitz, Esq. and Kevin Henry, Esq. I. THE BASICS OF 1031 EXCHANGES AND THE USE OF LIMITED LIABILITY COMPANIES IN REAL ESTATE ACQUISITIONS A. What

a closer look GLOBAL TAX WEEKLY ISSUE 249 AUGUST 17, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Ireland Country Profile

Ireland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Ireland EU Member State Yes Double Tax Treaties With: Albania Armenia Australia

Ireland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Ireland EU Member State Yes Double Tax Treaties With: Albania Armenia Australia

INTERNATIONAL JOURNAL OF RESEARCH AND ANALYSIS VOLUME 5 ISSUE 2 ISSN

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

CRITICAL ANALYSIS ON DOUBLE TAXATION AVOIDANCE AGREEMENT **AASTHA SUMAN & HIMANSHU SHUKLA The DTAA, or Double countries) so that taxpayers can avoid paying double taxes on their income earned from the

OBAMA'S HIRE ACT -- EXPLAINING THE TAX PROVISIONS

OBAMA'S HIRE ACT -- EXPLAINING THE TAX PROVISIONS Publication OBAMA'S HIRE ACT -- EXPLAINING THE TAX PROVISIONS March 24, 2010 President Obama signed the Hiring Incentives to Restore Employment Act (the

OBAMA'S HIRE ACT -- EXPLAINING THE TAX PROVISIONS Publication OBAMA'S HIRE ACT -- EXPLAINING THE TAX PROVISIONS March 24, 2010 President Obama signed the Hiring Incentives to Restore Employment Act (the

General Rule Capital Gain or Loss. Sec Example 12-1 Sale. General rule: a sale by a partner generates capital gain or loss.

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, August

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, August

Real Estate & Private Equity workshop

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Positions that are the same as or similar to the positions listed in this Notice are

Part III - Administrative, Procedural, and Miscellaneous Frivolous Positions Notice 2007-30 PURPOSE Positions that are the same as or similar to the positions listed in this Notice are identified as frivolous

Part III - Administrative, Procedural, and Miscellaneous Frivolous Positions Notice 2007-30 PURPOSE Positions that are the same as or similar to the positions listed in this Notice are identified as frivolous

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, July 14,

Save up to 74% on U.S. postage.

BRITISH COLUMBIA RATE CARD 2019 Effective January 27 2019 Save up to 74% on U.S. postage. Postage from $2.66 USD Delivery within 4 business days Tracking included Chit Chats Insurance from $0.35 Canada

BRITISH COLUMBIA RATE CARD 2019 Effective January 27 2019 Save up to 74% on U.S. postage. Postage from $2.66 USD Delivery within 4 business days Tracking included Chit Chats Insurance from $0.35 Canada

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA Tel: (310) Fax: (310)

Fax: (310)") Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

Jeffrey P. Geida Weinstock Manion 1875 Century Park East, Suite 2000 Los Angeles, CA 90067 Tel: (310) 553-8844 Fax: (310) 553-5165 jgeida@weinstocklaw.com IRC 170(c), a contribution or gift to or for the

The new rules are generally effective for partnership audits of tax years beginning after December 31, 2017.

Please be aware that the following responses to FAQ s are based upon the statutory legislation and related guidance in the form of enacted and proposed regulations existing as of October 16, 2018. What

Please be aware that the following responses to FAQ s are based upon the statutory legislation and related guidance in the form of enacted and proposed regulations existing as of October 16, 2018. What

SANGAM GLOBAL PHARMACEUTICAL & REGULATORY CONSULTANCY

SANGAM GLOBAL PHARMACEUTICAL & REGULATORY CONSULTANCY Regulatory Affairs Worldwide An ISO 9001:2015 Certified Company Welcome to Sangam Global Pharmaceutical & Regulatory Consultancy (SGPRC) established

SANGAM GLOBAL PHARMACEUTICAL & REGULATORY CONSULTANCY Regulatory Affairs Worldwide An ISO 9001:2015 Certified Company Welcome to Sangam Global Pharmaceutical & Regulatory Consultancy (SGPRC) established

Tax Management International Journal

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 540, 09/12/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

Tax Management International Journal Reproduced with permission from Tax Management International Journal, 43 TMIJ 540, 09/12/2014. Copyright 2014 by The Bureau of National Affairs, Inc. (800-372- 1033)

The Wolfe Law Group Gary S. Wolfe, A Professional Law Corporation. March 18, Expatriation and the Ten Year Rule

The Wolfe Law Group Gary S. Wolfe, A Professional Law Corporation 6303 WILSHIRE BOULEVARD TELEPHONE (323) 782-9139 SUITE 201 FACSIMILE (323) 782-9289 LOS ANGELES, CA 90048 E-MAIL gsw@gswlaw.com March 18,

The Wolfe Law Group Gary S. Wolfe, A Professional Law Corporation 6303 WILSHIRE BOULEVARD TELEPHONE (323) 782-9139 SUITE 201 FACSIMILE (323) 782-9289 LOS ANGELES, CA 90048 E-MAIL gsw@gswlaw.com March 18,

NAVIGATING US TAX REFORM:

NAVIGATING US TAX REFORM: WHAT BUSINESSES NEED TO KNOW State and Local Tax Implications January 17, 2018 Presenters: 2018 Morgan, Lewis & Bockius LLP Donald-Bruce Abrams, Partner Daniel Dixon, Of Counsel

NAVIGATING US TAX REFORM: WHAT BUSINESSES NEED TO KNOW State and Local Tax Implications January 17, 2018 Presenters: 2018 Morgan, Lewis & Bockius LLP Donald-Bruce Abrams, Partner Daniel Dixon, Of Counsel

a closer look GLOBAL TAX WEEKLY ISSUE 255 SEPTEMBER 28, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 255 SEPTEMBER 28, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

GLOBAL TAX WEEKLY a closer look ISSUE 255 SEPTEMBER 28, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

BOARD OF EQUALIZATION STATE OF CALIFORNIA ) ) ) ) ) ) ) )

) ) ) ) ) ) )") STATE BOARD OF EQUALIZATION In the Matter of the Appeal of: PEDRO V. DATING AND SIMONA V. DATING Representing the Parties: For Appellants: For Franchise Tax Board: Counsel for the Board of Equalization:

STATE BOARD OF EQUALIZATION In the Matter of the Appeal of: PEDRO V. DATING AND SIMONA V. DATING Representing the Parties: For Appellants: For Franchise Tax Board: Counsel for the Board of Equalization:

Luxembourg Country Profile

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

Luxembourg Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Luxembourg EU Member State Yes Double Tax Treaties With: Albania (a) Andorra

2011 Year End Income Tax Planning: What Can You Do At This Late Date? Givner & Kaye, A Professional Corporation

2011 Year End Income Tax Planning: What Can You Do At This Late Date? 1 Planning Is Based On Your Predictions: 1. Will rates go up? Down? Stay the same? You must predict the elections. 2. Will client s

2011 Year End Income Tax Planning: What Can You Do At This Late Date? 1 Planning Is Based On Your Predictions: 1. Will rates go up? Down? Stay the same? You must predict the elections. 2. Will client s

Long Association List of Jurisdictions Surveyed for Which a Response Has Been Received

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

Agenda Item 7-B Long Association List of Jurisdictions Surveed for Which a Has Been Received Jurisdictions Region IFAC Largest 29 G10 G20 EU/EEA IOSCO IFIAR Surve Abu Dhabi Member (UAE) Albania Member

Dutch tax treaty overview Q3, 2012

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

Dutch tax treaty overview Q3, 2012 Hendrik van Duijn DTS Duijn's Tax Solutions Zuidplein 36 (WTC Tower H) 1077 XV Amsterdam The Netherlands T +31 888 387 669 T +31 888 DTS NOW F +31 88 8 387 601 duijn@duijntax.com

The Internal Revenue Service is aware that certain promoters are advising

Part I Income Taxes Meritless Filing Position Based on Sections 932(c) and 934(b) Notice 2004-45 The Internal Revenue Service is aware that certain promoters are advising taxpayers to take highly questionable,

Part I Income Taxes Meritless Filing Position Based on Sections 932(c) and 934(b) Notice 2004-45 The Internal Revenue Service is aware that certain promoters are advising taxpayers to take highly questionable,

Table of Contents. 1 created by

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

Table of Contents Overview... 2 Exemption Application Instructions for U.S. Tax Residents Living in the U.S.... 3 Exemption Application Instructions for Tax Residents of European Union Member States (other

H.R. 1 TAX CUT AND JOBS ACT. By: Michelle McCarthy, Esq. and Tyler Murray, Esq.

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Wenzhou-Kean University. Employee Tax Considerations

Wenzhou-Kean University Employee Tax Considerations Chinese Tax Issues China (PRC) has an individual income tax system and assesses income tax on nonresidents and residents of China, regardless of nationality

Wenzhou-Kean University Employee Tax Considerations Chinese Tax Issues China (PRC) has an individual income tax system and assesses income tax on nonresidents and residents of China, regardless of nationality

WHAT MAKES YOU A BONA FIDE RESIDENT OF PUERTO RICO FOR US INCOME TAX PURPOSES, AND ACT 20 AND 22 IMPLICATIONS

WHAT MAKES YOU A BONA FIDE RESIDENT OF PUERTO RICO FOR US INCOME TAX PURPOSES, AND ACT 20 AND 22 IMPLICATIONS By: Ricardo Muñiz W hether you are planning to move to Puerto Rico ( PR ) to enjoy the benefits

WHAT MAKES YOU A BONA FIDE RESIDENT OF PUERTO RICO FOR US INCOME TAX PURPOSES, AND ACT 20 AND 22 IMPLICATIONS By: Ricardo Muñiz W hether you are planning to move to Puerto Rico ( PR ) to enjoy the benefits

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Czech Republic Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Czech Rep. EU Member State Yes Double Tax With: Treaties Albania Armenia

Austria Country Profile

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, December

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, February

Total Imports by Volume (Gallons per Country)

") 5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, July

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, July

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, January

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, January

YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS Short Format UPDATED November 2, 2017 www.cordascocpa.com 2017 YEAR-END INCOME TAX PLANNING FOR INDIVIDUALS INTRODUCTION With year-end approaching, this

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, April

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, April

SUMMARY OF INTERNATIONAL TAX LAW DEVELOPMENTS

SUMMARY OF INTERNATIONAL TAX LAW DEVELOPMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 12, 1998 In the past year there have been many developments affecting the United States taxation of international transactions.

SUMMARY OF INTERNATIONAL TAX LAW DEVELOPMENTS SIMPSON THACHER & BARTLETT LLP FEBRUARY 12, 1998 In the past year there have been many developments affecting the United States taxation of international transactions.

ide: FRANCE Appendix A Countries with Double Taxation Agreement with France

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Fiscal operational guide: FRANCE ide: FRANCE Appendix A Countries with Double Taxation Agreement with France Albania Algeria Argentina Armenia 2006 2006 From 1 March 1981 2002 1 1 1 All persons 1 Legal

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, November

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Wednesday, November

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, October

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Friday, October

EXPAT TAX.A TO Z. ASSETS Anything you own that has value is considered an asset. Bank accounts,

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

EXPAT TAX.A TO Z US tax law is difficult enough to understand without the added burden of trying to understand the overseas side of things. Here is an explanation of expat key words and phrases that will

Tax Issues for Limited Liability Companies

Tax Issues for Limited Liability Companies What You Should Know About Limited Liability Companies... What is a Limited Liability Company? A Limited Liability Company (LLC) is a relatively new business

Tax Issues for Limited Liability Companies What You Should Know About Limited Liability Companies... What is a Limited Liability Company? A Limited Liability Company (LLC) is a relatively new business

a closer look GLOBAL TAX WEEKLY ISSUE 255 SEPTEMBER 28, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 255 SEPTEMBER 28, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

GLOBAL TAX WEEKLY a closer look ISSUE 255 SEPTEMBER 28, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES

Total Imports by Volume (Gallons per Country)

") 10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

Today's CPI data: what you need to know

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, October

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: Consumer Price Index, Producer Price Index Thursday, October

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES AT A GLANCE GEOGRAPHY 77 COUNTRIES COVERED 5 REGIONS Americas Asia Pacific Central & Eastern

HEALTH WEALTH CAREER 2017 WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES WORLDWIDE BENEFIT & EMPLOYMENT GUIDELINES AT A GLANCE GEOGRAPHY 77 COUNTRIES COVERED 5 REGIONS Americas Asia Pacific Central & Eastern

An In-Depth Look at the FBAR (and other foreign account reporting requirements)

") An In-Depth Look at the FBAR (and other foreign account reporting requirements) Pacific Tax Institute November 8, 2011 Bell Harbor International Conference Center Seattle, Washington Amy P. Jetel Schurig

An In-Depth Look at the FBAR (and other foreign account reporting requirements) Pacific Tax Institute November 8, 2011 Bell Harbor International Conference Center Seattle, Washington Amy P. Jetel Schurig

Total Imports by Volume (Gallons per Country)

") 1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

Czech Republic Country Profile

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Czech Republic Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Czech Republic EU Member State Yes Double Tax Treaties With: Albania

Partnership Audit Procedures Under the Bipartisan Budget Act of 2015

Partnership Audit Procedures Under the Bipartisan Budget Act of 2015 INTRODUCTION The Internal Revenue Service ( IRS ) currently audits most partnerships under rules enacted in the Tax Equity and Fiscal

Partnership Audit Procedures Under the Bipartisan Budget Act of 2015 INTRODUCTION The Internal Revenue Service ( IRS ) currently audits most partnerships under rules enacted in the Tax Equity and Fiscal

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

Luxembourg-Kazakhstan business relations A focus on financial services. 2 March 2017

Luxembourg-Kazakhstan business relations A focus on financial services 2 March 2017 Arendt & Medernach s story in Kazakhstan First visit to Kazakhstan in 2011 Moscow office opened in October 2012 Covering

Luxembourg-Kazakhstan business relations A focus on financial services 2 March 2017 Arendt & Medernach s story in Kazakhstan First visit to Kazakhstan in 2011 Moscow office opened in October 2012 Covering

Total Imports by Volume (Gallons per Country)

") 12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

Americans Retiring Abroad

U.S. EXPAT TAX GUIDE FOR Americans Retiring Abroad The most important tax tips to save money with credits, exclusions, and deductions available to Americans retiring abroad Let LOCUS file your taxes this

U.S. EXPAT TAX GUIDE FOR Americans Retiring Abroad The most important tax tips to save money with credits, exclusions, and deductions available to Americans retiring abroad Let LOCUS file your taxes this

Total Imports by Volume (Gallons per Country)

") 2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

Cyprus Country Profile

Cyprus Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Cyprus Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Cyprus EU Member State Yes Double Tax Treaties With: Armenia Austria Bahrain

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Countries with Double Taxation Agreements with the UK rates of withholding tax for the year ended 5 April 2012 This table shows the maximum rates of tax those countries with a Double Taxation Agreement

Total Imports by Volume (Gallons per Country)

") 11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

Total Imports by Volume (Gallons per Country)

") 2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

Total Imports by Volume (Gallons per Country)

") 3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

Total Imports by Volume (Gallons per Country)

") 10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

Partnership Audits. Crowell & Moring, LLP. Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration)

") Partnership Audits Crowell & Moring, LLP Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration) Jennifer Ray, Partner, Crowell & Moring, LLP September 29, 2016

Partnership Audits Crowell & Moring, LLP Gregory Armstrong, Senior Technician Reviewer, Office of Chief Counsel (Procedure & Administration) Jennifer Ray, Partner, Crowell & Moring, LLP September 29, 2016

a closer look GLOBAL TAX WEEKLY ISSUE 271 JANUARY 18, 2018

GLOBAL TAX WEEKLY a closer look ISSUE 271 JANUARY 18, 2018 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 271 JANUARY 18, 2018 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Individual Retirement Custodial Account Agreement

Individual Retirement Custodial Account Agreement Form 5305-A under Section 408(a) of the Internal Revenue Code FORM (Rev. December 2016) The depositor named on the application is establishing a Traditional

Individual Retirement Custodial Account Agreement Form 5305-A under Section 408(a) of the Internal Revenue Code FORM (Rev. December 2016) The depositor named on the application is establishing a Traditional

2017 Year-End Income Tax Planning for Individuals December 2017

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

2017 Year-End Income Tax Planning for Individuals December 2017 9605 S. Kingston Ct., Suite 200 Englewood, CO 80112 T: 303 721 6131 www.richeymay.com Introduction With year-end approaching, this is the

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

United States: Summary of key 2017 and 2018 federal tax rates and limits many changes after tax reform

www.gmsasia.pwc.com United States: Summary of key 2017 and 2018 federal tax rates and limits many changes after tax reform April 2018 In brief The following is a high-level summary of some key individual

www.gmsasia.pwc.com United States: Summary of key 2017 and 2018 federal tax rates and limits many changes after tax reform April 2018 In brief The following is a high-level summary of some key individual

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

AMERICAN CITIZENS ABROAD RESIDENCY-BASED TAXATION: A VANILLA APPROACH TO REPLACING CITIZENSHIP-BASED TAXATION October 15, 2017 Congress and the Administration are expected to consider changes in US tax

YUM! Brands, Inc. Historical Financial Summary. Second Quarter, 2017

YUM! Brands, Inc. Historical Financial Summary Second Quarter, 2017 YUM! Brands, Inc. Consolidated Statements of Income (in millions, except per share amounts) 2017 2016 2015 YTD Q3 Q4 FY FY Revenues Company

YUM! Brands, Inc. Historical Financial Summary Second Quarter, 2017 YUM! Brands, Inc. Consolidated Statements of Income (in millions, except per share amounts) 2017 2016 2015 YTD Q3 Q4 FY FY Revenues Company

INTESA SANPAOLO S.p.A. INTESA SANPAOLO BANK IRELAND p.l.c. 70,000,000,000 Euro Medium Term Note Programme

PROSPECTUS SUPPLEMENT INTESA SANPAOLO S.p.A. (incorporated as a società per azioni in the Republic of Italy) as Issuer and, in respect of Notes issued by Intesa Sanpaolo Bank Ireland p.l.c., as Guarantor

PROSPECTUS SUPPLEMENT INTESA SANPAOLO S.p.A. (incorporated as a società per azioni in the Republic of Italy) as Issuer and, in respect of Notes issued by Intesa Sanpaolo Bank Ireland p.l.c., as Guarantor

Internal Revenue Code Section 1291 Interest on tax deferral

Internal Revenue Code Section 1291 Interest on tax deferral (a) Treatment of distributions and stock dispositions. CLICK HERE to return to the home page (1) Distributions. If a United States person receives

Internal Revenue Code Section 1291 Interest on tax deferral (a) Treatment of distributions and stock dispositions. CLICK HERE to return to the home page (1) Distributions. If a United States person receives

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

SELECTED TAX DEVELOPMENTS

ALI-ABA Video Law Review Limited Liability Entities 2010: New Developments in Limited Liability Companies and Limited Liability Partnerships John Maxfield, Esq Hank Vanderhage, Esq. Holland & Hart LLP

ALI-ABA Video Law Review Limited Liability Entities 2010: New Developments in Limited Liability Companies and Limited Liability Partnerships John Maxfield, Esq Hank Vanderhage, Esq. Holland & Hart LLP

Update on Partnership Audit Provisions and Certain Deductions

Update on Partnership Audit Provisions and Certain Deductions Jennifer O Leary, Philadelphia Office olearyj@pepperlaw.com Ph. 215.981.4184 Annette Ahlers, Los Angeles Office ahlersa@pepperlaw.com Ph. 213.928.9825

Update on Partnership Audit Provisions and Certain Deductions Jennifer O Leary, Philadelphia Office olearyj@pepperlaw.com Ph. 215.981.4184 Annette Ahlers, Los Angeles Office ahlersa@pepperlaw.com Ph. 213.928.9825

FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers

Communication on June 19 th 2014 last update: July 23 rd 2018 FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers Goal and legal framework of FATCA The

Communication on June 19 th 2014 last update: July 23 rd 2018 FATCA, an American law applied starting July 1 st, 2014 to fight offshore tax evasion by US Taxpayers Goal and legal framework of FATCA The

Inflation Guard Annuity Prospectus

Inflation Guard Annuity Prospectus August 8, 2011 SINGLE PAYMENT MODIFIED GUARANTEE DEFERRED ANNUITY NON-PARTICIPATING CONTRACT VALUE INTERESTS Guaranteed as described herein by MANULIFE FINANCIAL CORPORATION

Inflation Guard Annuity Prospectus August 8, 2011 SINGLE PAYMENT MODIFIED GUARANTEE DEFERRED ANNUITY NON-PARTICIPATING CONTRACT VALUE INTERESTS Guaranteed as described herein by MANULIFE FINANCIAL CORPORATION

Sec Imposition of Accuracy-Related Penalty on Underpayments.

Sec. 6662. Imposition of Accuracy-Related Penalty on Underpayments. (a) Imposition of Penalty. If this section applies to any portion of an underpayment of tax required to be shown on a return, there shall

Sec. 6662. Imposition of Accuracy-Related Penalty on Underpayments. (a) Imposition of Penalty. If this section applies to any portion of an underpayment of tax required to be shown on a return, there shall

THE TAXATION OF INDIVIDUALS AND FAMILIES

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE

THE TAXATION OF INDIVIDUALS AND FAMILIES Scheduled for a Public Hearing Before the TAX POLICY SUBCOMMITTEE of the HOUSE COMMITTEE ON WAYS AND MEANS on July 19, 2017 Prepared by the Staff of the JOINT COMMITTEE