US Outbound Investment

|

|

|

- Elijah Richards

- 6 years ago

- Views:

Transcription

1 US Outbound Investment

2 Denise Magyer Senior Vice President Allied Irish Bank

3 Agenda AGENDA 3

U.S.")

4 U.S.Outbound Investment US Outbound Investment = Foreign Direct Investment (FDI) U.S. Outbound Investment: Why Choose Ireland?

5 U.S. Ireland Source: America Ireland Chamber of Commerce US-Ireland Business 2017 U.S. Outbound Investment: Why Choose Ireland?

6 Evolution of FDI in Ireland Source: IDA Ireland Strategy, Horizon 2020 A range of services and incentives, including funding and grants, are available to those considering foreign direct investment in Ireland. These are offered by IDA Ireland, Ireland s inward investment promotion agency, to both new and existing clients. U.S. Outbound Investment Why Choose Ireland?

7

8 Survey Results 86% of companies stated that access to Europe was critical or important REASONS FOR SETTING UP IN IRELAND See our Sector Report, "Why Choose Ireland?" at Source: Ipsos MRBI AIB Foreign Direct Investment Research February 2014 U.S. Outbound Investment: Why Choose Ireland?

9 Access to the European market ECONOMIC SIZE PER CAPITA WEALTH LARGE MARKET FOR US GOODS/SERVICES CHINA $21.3 trillion EU $19.2 China $11,000 US $18.6 INDIA $8.7 JAPAN $ 4.9 EU $35,000 Source: Cia WORLD FACT BOOK U.S. Outbound Investment: Why Choose Ireland?

10 Export Propensity Access to the 500m people in Europe US affiliate sales of goods and services in Ireland totaled $343 billion in 2015 > Greater than US affiliate sales in China ($165bn) and Japan ($108bn). The reason: Export-Propensity. Ireland ranks the number one export platform in the world for U.S. affiliates underscoring the importance of Ireland in the global value chains Source: Bureau of Economic Analysis 2016 based on most recent data U.S. Outbound Investment: Why Choose Ireland?.

11 Ease of Doing Business 1 Source: Ipsos MRBI AIB Foreign Direct Investment Research February 2014 U.S. Outbound Investment: Why Choose Ireland?

12 Education = Talent in Ireland Young, well educated and productive workforce Youngest population in Europe. Currently 1m people in full time education. ICT skills strategy is driving significant increases in graduates with an increase of % by Multi-lingual capabilities. Source:: IDA Ireland is the only English speaking workforce in the Eurozone U.S. Outbound Investment: Why Choose Ireland?

13

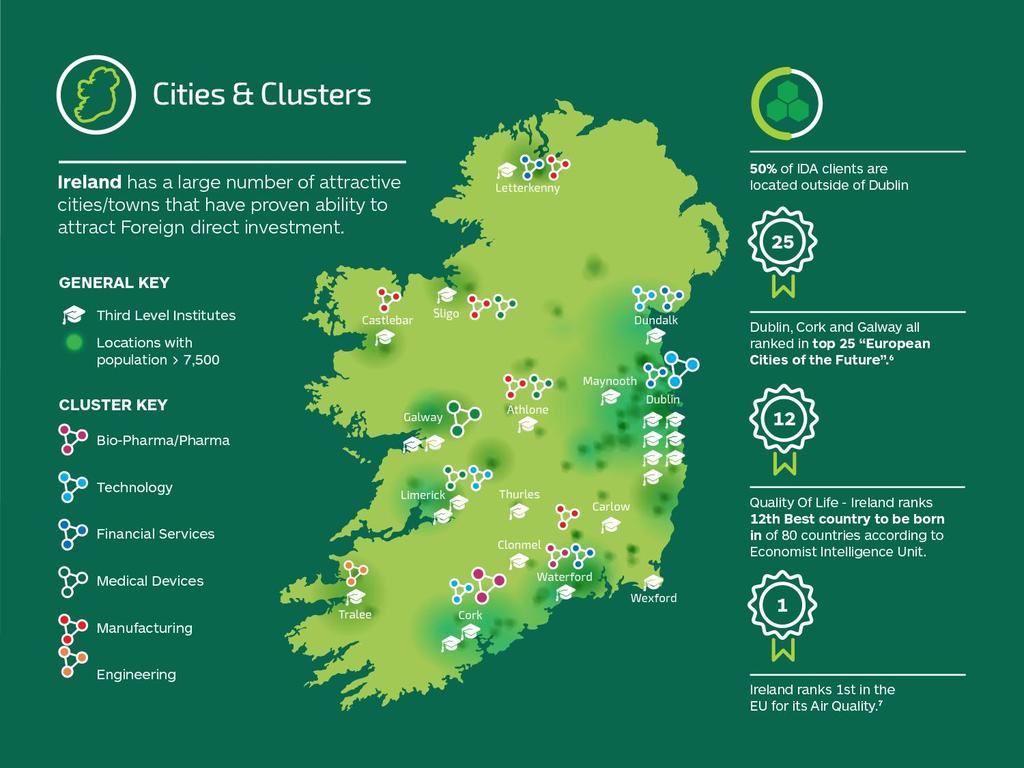

14 Tech Clusters: Dublin

15 Tech Clusters: Galway

16 Track Record

17 Time Zone

Tax Credit An Intellectual Property (IP) regime which provides a tax write-off for broadly defined IP acquisitions.")

18 Tax Regime Corporate tax rate of 12.5% for active business. 25% Research & Development (R&D) Tax Credit An Intellectual Property (IP) regime which provides a tax write-off for broadly defined IP acquisitions. Attractive relief for staff assigned from abroad, key staff working in R&D. Our core offering is a competitive, businessfriendly regime with a rock solid commitment to the 12.5% corporation tax rate Update on Ireland s International Tax Strategy 2016 Minister of Finance, Michael Noonan, TD

19 Why are Companies using Ireland? Supply Chain Management Headquarters & IP Management High Value Manufacturing Global Business Service Centers Research, Development & Innovation

20 Expansion into EMEA Markets Tax efficient supply chain management Arm s length pricing and transfer pricing Operational substance in Ireland Corporate restructuring and inversions into Ireland

21 IRELAND as a Treasury Location IRELAND AS A TREASURY LOCATION Ireland also represents a very attractive and sustainable solution as a corporate treasury center/ group bank. The taxation of interest / treasury income at 12.5% is not targeted by BEPS. 12.5% on treasury trading profit Transparent tax regime aligned to BEPS Extensive tax treaty network & EU Directives Dedicated securitization regime Unilateral credit for foreign withholding taxes Ireland is not a hybrid haven. The taxation of interest / treasury income at 12.5% rate should meet minimum taxation level of unilateral interest base erosion measures. WHT exemption on interest & dividends No CFC or thin capitalization rules OECD based transfer pricing regime No capital duty on shares / loan issuances Published guidance on treasury activities 21 Source: EY U.S. Outbound Investment: Why Choose Ireland?

22 Case Study: The existing business model had many issues and opportunities IP License IP Ownership USP Sales Physical flow & Title US Customers RM Purchases Italy Physical flow & Title Sales Italy Customers Suppliers France France Customers Spain Spain Customers Key to flows: Legal title Physical flow Services Full-fledged entrepreneurs: procurement, manufacturing, distribution, marketing, sales, backoffice support, etc.

23 Real Life Case Study: Centralized model Suppliers Cost-sharing for ROW IP rights RM Title IP Ownership USP IrishCo FG Sale - Mkt price less commission CM fee FG Sale - mkt price Finished good shipped Italy France Spain US Customers RM Physical flow FG Sale mkt price Key to flows: Legal title Physical flow ROW Customers Services

24 Intellectual Property Exploitation Why choose Ireland for IP? Legal framework for IP protection Taxation at 12.5% on trading profits of an active brand management trade Effective tax rate can be as low as 2.5% Amortization for tax purposes R&D credits: close to 40% on the dollar for qualifying R&D spend Ireland: A Platform for Expansion into Europe 24

25 IRELAND as an IP Location Ireland has a very favorable IP regime with a number of large MNE s already choosing to locate their non-us IP in Ireland. Tax amortization available for acquired IP Extensive tax treaty network & EU Directives 25% refundable R&D tax credit Source: EY The royalty income received should be taxable at the 12.5% provided the company has substance in Ireland is actively carrying on an IP type trade. A deduction for tax amortization on acquired IP and interest on borrowings also available which can reduce the company s cash tax rate below the standard 12.5% rate and 0% rate is possible. Currently seeing a huge amount of interest in Ireland as an IP location. 12.5% on IP trading profit WHT exemption on outbound royalties payments Tax free exit available on migration U.S. Outbound Investment: Why Choose Ireland? Credit available for WHT on inbound royalties Interest deduction on borrowings used to acquire IP New OECD compliant patent box No stamp duty on the acquisition of IP 25

26 Ireland is NOT a Tax Haven. The OECD has identified four key indicators of a 1. No or nominal taxes Ireland s corporate tax rate is 12.5% 2 Lack of transparency Ireland s tax regime is fully transparent based on legislation 3. Unwilling to exchange Ireland exchanges information through Tax information tax haven Treaties, Information Exchange Agreements, EU Savings Tax Directive and (proposed) FATCA); 4 No substance requirement The 12.5% tax rate applies to trading activities only which require substance None of which apply to Ireland

27 Base Erosion Profit Shifting BASE EROSION & PROFIT SHIFTING (BEPS) What Is BEPS?. Tax planning strategies that exploit gaps and mismatches in tax rules that artificially shift profits to low or no-tax locations where there is little or no economic activity, resulting in little or no overall corporate tax being paid Stated simply, BEPS arises because under existing rules, it is possible for companies to artificially separate taxable profits from economic activities and value creation Raffaele Russo, Head of BEPS project 27 Source: OECD U.S. Outbound Investment: Why Choose Ireland?

28 What is BEPS All About? 28 Source: EY U.S. Outbound Investment: Why Choose Ireland?

29 A Message From Ireland s Finance Minister: Ireland is committed to the BEPS project Country by Country reporting has been implemented Transparency: Committed to the highest international standards Review of Ireland s tax code in 2017 budget Source: Address by Minister Michael Noonan TD to Irish Times International Tax Event 1/24/17 U.S. Outbound Investment: Why Choose Ireland? 29

30 BEPS impact on Ireland Ireland likely to be the go-to jurisdiction since it already requires substance and has a competitive tax rate. Ireland s Knowledge Development Box was created in accordance with the OECD guidelines. Multi-national companies operating in different jurisdictions will have increased compliance costs. 30 Source: AIB, EY U.S. Outbound Investment: Why Choose Ireland?

31 BEPS impact on Treasury Action 14: Making dispute resolution mechanisms more effective Action 15: Develop of a multilateral instrument for amending bilateral tax treaties Action 11: Establish methodologies to collect and analyse data on BEPS and actions addressing it Action 12: Require taxpayers to disclose their aggressive tax planning arrangements Action 13: Re-examine transfer pricing documentation Action plan on Base Erosion and Profit Shifting (BEPS) Action 8: Consider transfer pricing for intangibles Action 9: Consider transfer pricing for risks and capital Action 10: Consider transfer pricing for other high-risk transactions Action 1: Address the tax challenges of the digital economy Action 2: Neutralise the effects of hybrid mismatch arrangements Action 3: Strengthen CFC rules Action 4: Limit base erosion via interest deductions and other financial payments Action 5: Counter harmful tax practices more effectively, taking into account transparency and substance Action 6: Prevent treaty abuse Action 7: Prevent the artificial avoidance of permanent establishment status 31 Source: EY U.S. Outbound Investment: Why Choose Ireland?

32 BEPS impact on Treasury Action 14: Making dispute resolution mechanisms more effective Action 15: Develop of a multilateral instrument for amending bilateral tax treaties Action 11: Establish methodologies to collect and analyse data on BEPS and actions addressing it Action 12: Require taxpayers to disclose their aggressive tax planning reporting arrangements Action 13: Re-examine transfer pricing documentation Source: EY Double taxation due to conflicting jurisdictions? Increased requirements & audits Action plan on Base Erosion and Profit Shifting (BEPS) Transfer pricing calculations; impact on intercompany financings Action 8: Consider transfer pricing for intangibles Action 9: Consider transfer pricing for risks and capital Action 10: Consider transfer pricing for other high-risk transactions U.S. Outbound Investment: Why Choose Ireland? Action 1: Address the tax challenges of the digital economy Impact sales tax payments- where collected and paid Action 2: Neutralise the effects of hybrid mismatch arrangements Action 3: Strengthen CFC rules Action 4: Limit base erosion via interest deductions and other financial payments Interest deductions & Withholding tax Action 5: Counter harmful tax practices more effectively, taking into account transparency and substance calcs; Req. for substance and shift of trading activity Action 6: Prevent treaty abuse Action 7: Prevent the artificial avoidance of permanent establishment status 32

33 Ireland: Other considerations Brexit US Tax Reform The Apple Case 33 U.S. Outbound Investment: Why Choose Ireland?

should I be in Proc")

34 It s Important to Have a Vision for Your Business Initial expansion planning decisions can have long-term impacts Each business decision drives tax consequences and opportunities What are my financial & regulatory requirements How will I mange foreign currency issues What do I do with cash builtup off-shore What are my income/indirect tax obligations Treas Cash AP Risk Global Business Model AR Legal Mfg What location(s) should I be in Proc IT Sales Fin Acctg What should my legal structure be How do I exploit my Intellectual property How do I fund ongoing R&D How will I distribute finished goods How will I sell & conclude sales outside the US How/where will I bill and collect from clients If/where/how should I manufacture products Anticipating and planning for each decision may help avoid unfavorable default decisions which may negate benefits on an after-tax basis U.S. Outbound Investment: Why Choose Ireland?

35 Some thoughts Be aware of OECD work in progress/areas of focus Choose a structure that best fits your company s risk profile. Hire the appropriate team of consultants and advisors

36 Questions

37 The Irish Advantage It is the combination of factors Highly skilled, knowledge based economy Flexibility, responsiveness & innovation Experience delivering Global Business Services Experienced & Innovative Leaders Excellent Research facilities & capabilities Stable political environment & Respected regulatory regime Irish Government partnering 12.5% CT & extensive tax treaty network The Irish Advantage Unique mix of components Source: IDA Ireland

38 Fun Facts FUN FACTS Ireland produces: % of the world s contact lenses %of ventilators used in acute hospitals worldwide % of the world s stents % of the world s Botox # of Jelly Beans daily % of the world s Tic Tacs 1 in burgers served in European McDonalds is made with Irish beef Driver vision systems technology is manufactured in Galway which can park your car without you being in it.

39 Contacts Denise Magyer Senior Vice President Allied Irish Bank 1345 Avenue of the Americas 10 th Floor New York NY

US Outbound Investment

US Outbound Investment David Evans Managing Director Canyon CTS Denise Magyer Senior Vice President Allied Irish Bank U.S.Outbound Investment US Outbound Investment = Foreign Direct Investment (FDI) U.S.

US Outbound Investment David Evans Managing Director Canyon CTS Denise Magyer Senior Vice President Allied Irish Bank U.S.Outbound Investment US Outbound Investment = Foreign Direct Investment (FDI) U.S.

THE INTERSECTION OF TAX & TREASURY

THE INTERSECTION OF TAX & TREASURY 1 INTRODUCTIONS Denise Magyer Senior Vice President, Allied Irish Bank BEATRIZ SALDIVAR MBA & CTP Consultant & Member of the Federal Reserve Faster Payments Task Force

THE INTERSECTION OF TAX & TREASURY 1 INTRODUCTIONS Denise Magyer Senior Vice President, Allied Irish Bank BEATRIZ SALDIVAR MBA & CTP Consultant & Member of the Federal Reserve Faster Payments Task Force

A small country perspective on international taxation Ann Nolan, Second Secretary General, Ministry of Finance, Ireland Oxford University Centre for

A small country perspective on international taxation Ann Nolan, Second Secretary General, Ministry of Finance, Ireland Oxford University Centre for Business Taxation, Summer Conference, 23 June 2014 Outline

A small country perspective on international taxation Ann Nolan, Second Secretary General, Ministry of Finance, Ireland Oxford University Centre for Business Taxation, Summer Conference, 23 June 2014 Outline

STEP Silicon Valley Ireland: Gateway to Accessing the EU Market

STEP Silicon Valley Ireland: Gateway to Accessing the EU Market Mark O Sullivan and Pat English August 17, 2016 Financial Times 2012-2015 Matheson is ranked in the FT s top 10 European law firms 2015.

STEP Silicon Valley Ireland: Gateway to Accessing the EU Market Mark O Sullivan and Pat English August 17, 2016 Financial Times 2012-2015 Matheson is ranked in the FT s top 10 European law firms 2015.

Irish Government announces Budget 2016 and publishes update on international tax strategy

16 October 2015 EY Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/ Services/Tax/International- Tax/Tax-alert-library#date Irish

16 October 2015 EY Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/ Services/Tax/International- Tax/Tax-alert-library#date Irish

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

BUSINESS MODELS IN THE CURRENT BEPS ENVIRONMENT DO YOU NEED TO CHANGE? Lyndon James, Partner Pete Rhodes, Senior Manager PwC Agenda The current environment and the case for change Australian measures most

Practical Implications of BEPS

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

The OECD s 3 Major Tax Initiatives

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

The OECD s 3 Major Tax Initiatives 1. The Global Forum on Transparency and Exchange of Information for Tax Purposes Peer review of ~ 100 countries International standard for transparency and exchange of

Why invest in Ireland? At a glance

Why invest in Ireland? At a glance Irish snapshot 50% under the age of 34 - youngest population in Europe 10/10 world s top pharma companies based here 13/15 world s top medtech companies #1 in EU for

Why invest in Ireland? At a glance Irish snapshot 50% under the age of 34 - youngest population in Europe 10/10 world s top pharma companies based here 13/15 world s top medtech companies #1 in EU for

The new global tax environment. What the global focus on Base Erosion and Profit Shifting (BEPS) means for your business

means for your business") The new global tax environment What the global focus on Base Erosion and Profit Shifting (BEPS) means for your business Changing business environment Macroeconomic megatrends, mobility of capital and growth

The new global tax environment What the global focus on Base Erosion and Profit Shifting (BEPS) means for your business Changing business environment Macroeconomic megatrends, mobility of capital and growth

Moshe Bina, Senior Manager, International Taxation Department, Deloitte Israel

Moshe Bina, Senior Manager, International Taxation Department, Deloitte Israel Doing business in Japan Tax Aspects and a glance at BEPS Moshe Bina, Adv. September 6 th, 2015 Our main Topics. Country Domestic

Moshe Bina, Senior Manager, International Taxation Department, Deloitte Israel Doing business in Japan Tax Aspects and a glance at BEPS Moshe Bina, Adv. September 6 th, 2015 Our main Topics. Country Domestic

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Summary This intermediate-level course provides participants with an in-depth understanding of the current discussions relating to international

IBFD Course Programme Current Issues in International Tax Planning Summary This intermediate-level course provides participants with an in-depth understanding of the current discussions relating to international

SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018

CPAs & ADVISORS experience direction // SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018 William D. James Principal Transfer Pricing & David H. Whitmer Director Transfer

CPAs & ADVISORS experience direction // SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018 William D. James Principal Transfer Pricing & David H. Whitmer Director Transfer

IBFD Course Programme Current Issues in International Tax Planning

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

IBFD Course Programme Current Issues in International Tax Planning Amsterdam, 14 16 June 2017 Summary This intermediate-level course provides participants with an in-depth understanding of the current

Intellectual property in the age of BEPS

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

Intellectual property in the age of BEPS Tax Executives Institute Michigan Chapter Detroit 28 October 2015 Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms

BEPS and ATAD: Where do we stand?

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

BEPS and ATAD: Where do we stand? by Nicky Gouder Tax Partner Summary Quick Overview of the BEPS Project and ATAD; A Comparison of the BEPS Recommendations and the ATAD obstacles, conflicts. Is harmonious

Base erosion & profit shifting (BEPS) 25 May 2016

25 May 2016") Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

Base erosion & profit shifting (BEPS) 25 May 2016 Introduction Important to distinguish between: Tax avoidance Using legal provisions to minimise tax liability Covers interventions that are referred to

IP BOX TAX REGIMES. Rod Donnelly Thursday, September 14, 2017

IP BOX TAX REGIMES Rod Donnelly Thursday, September 14, 2017 AGENDA 2 IP Box basics Tax sticks and carrots International landscape harmful tax practices OECD BEPS 2015 action final report topics OECD BEPS

IP BOX TAX REGIMES Rod Donnelly Thursday, September 14, 2017 AGENDA 2 IP Box basics Tax sticks and carrots International landscape harmful tax practices OECD BEPS 2015 action final report topics OECD BEPS

OECD meets with business on base erosion and profit shifting action plan

4 October 2013 OECD meets with business on base erosion and profit shifting action plan Executive summary On 1 October 2013, the Organisation for Economic Cooperation and Development (OECD) held a meeting

4 October 2013 OECD meets with business on base erosion and profit shifting action plan Executive summary On 1 October 2013, the Organisation for Economic Cooperation and Development (OECD) held a meeting

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud

and EU measures against aggressive tax planning and tax fraud") The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

The OECD report on base erosion and profit shifting (BEPS) and EU measures against aggressive tax planning and tax fraud Pere M. Pons New York, May 6 th, 2013 Agenda I. Background II. Key pressure areas

Hot topics Treasury seminar

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Hot topics Treasury seminar Treasury in a transparent and new tax world Discover and unlock your potential Program Introduction on BEPS Potential implications for treasury o Interest deduction o Treaty

Recent developments in international tax

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

Recent developments in international tax Disclaimer EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate

BEPS Country-by-Country Reporting Rules and New Documentation Requirements

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

Transfer pricing of intangibles

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

32E30000 - Tax Planning of International Enterprises Transfer pricing of intangibles Aalto BIZ / May 2, 2016 Petteri Rapo Alder & Sound Mannerheimintie 16 A FI-00100 Helsinki firstname.lastname@aldersound.fi

BEPS: What does it mean for funds and asset managers?

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

BEPS: What does it mean for funds and asset managers? Client Seminar Martin Shah René van Eldonk Malcolm Richardson, M&G 10 March 2015 Overview Background to and progress to date of BEPS Action Plan More

Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

www.pwc.com/jg November 2015 Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry Current International Tax Environment 1 2 The current environment The ability to achieve tax certainty

IBFD Course Programme BEPS Country Implementation

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

IBFD Course Programme BEPS Country Implementation Summary On 5 October 2015, the OECD published the final reports of its 15-point base erosion and profit shifting (BEPS) project. A bit more than a year

OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS)

") 22 July 2013 OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS) Executive summary On 19 July 2013, the Organisation for Economic Cooperation and Development (OECD) issued its much-anticipated

22 July 2013 OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS) Executive summary On 19 July 2013, the Organisation for Economic Cooperation and Development (OECD) issued its much-anticipated

תמונת מצב עדכנית ומבט ישראלי - BEPS

תמונת מצב עדכנית ומבט ישראלי - BEPS משה בינה, מנהל בכיר, מחלקת מיסוי בינלאומי, Deloitte Agenda BEPS Background Treaty Related Action Plans Harmful Tax Practices Transfer Pricing Others Next Steps 2017

תמונת מצב עדכנית ומבט ישראלי - BEPS משה בינה, מנהל בכיר, מחלקת מיסוי בינלאומי, Deloitte Agenda BEPS Background Treaty Related Action Plans Harmful Tax Practices Transfer Pricing Others Next Steps 2017

A Transfer Pricing Update BEPS & U.S. Tax Reform

A Transfer Pricing Update BEPS & U.S. Tax Reform JANUARY 17, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

A Transfer Pricing Update BEPS & U.S. Tax Reform JANUARY 17, 2018 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in a group Complete

Why invest in Ireland? At a glance

Why invest in Ireland? At a glance 12.5% corporation tax 15 of the world s top Financial Services companies Home to over 1,200 overseas companies #1 in EU #6 globally for the ease in which a business can

Why invest in Ireland? At a glance 12.5% corporation tax 15 of the world s top Financial Services companies Home to over 1,200 overseas companies #1 in EU #6 globally for the ease in which a business can

Korean Tax Update BEPS Implementation

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Do we have the wrong tax system for the digital economy? Alf Capito, Tax Policy Leader, EY Asia Pacific July 2014

Do we have the wrong tax system for the digital economy? Alf Capito, Tax Policy Leader, EY Asia Pacific July 2014 Key features of the digital economy as seen by the OECD taskforce Mobility Reliance on

Do we have the wrong tax system for the digital economy? Alf Capito, Tax Policy Leader, EY Asia Pacific July 2014 Key features of the digital economy as seen by the OECD taskforce Mobility Reliance on

WELCOME TO OUR WEBINAR

WELCOME TO OUR WEBINAR International Franchise Structures Tuesday, September 15, 2015 1:00 p.m. EDT If you cannot hear us speaking, please make sure you have called into the teleconference number on your

WELCOME TO OUR WEBINAR International Franchise Structures Tuesday, September 15, 2015 1:00 p.m. EDT If you cannot hear us speaking, please make sure you have called into the teleconference number on your

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

Comparison of Key Anti-Base Erosion Rules in the Tax Reform Act of 2017 and under UK Tax Law Calum Dewar, PwC Mike Williams, HM Treasury International Tax Policy Forum and Institute of Economic Law Conference

Intercompany financing facing new challenges. EY Africa Tax Conference September 2014

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Simplifying BEPS Action Plan

Simplifying BEPS Action Plan BEPS and GST Conference 2 nd September 2016 1 About the pic: 16 Nov 2015, In Antalya, Leaders expressed support for the package of measures developed under the G-20/OECD Base

Simplifying BEPS Action Plan BEPS and GST Conference 2 nd September 2016 1 About the pic: 16 Nov 2015, In Antalya, Leaders expressed support for the package of measures developed under the G-20/OECD Base

CPA Esther Wahome. Thursday, 16 August 2018

Current trends in international tax planning (focus on BEPS). Presentation by: CPA Esther Wahome Senior Manager Taxation Services Deloitte & Touche Thursday, 16 August 2018 Uphold public interest Contents

Current trends in international tax planning (focus on BEPS). Presentation by: CPA Esther Wahome Senior Manager Taxation Services Deloitte & Touche Thursday, 16 August 2018 Uphold public interest Contents

M&A OUTLOOK - POST BEPS. International Tax Refresher Course

M&A OUTLOOK - POST BEPS International Tax Refresher Course WHY BEPS? AND BEPS IMPACT Dell case (Spain SC) Restructured to low-risk distribution: FAR transferred to Principal Principal no substance no employees/office

M&A OUTLOOK - POST BEPS International Tax Refresher Course WHY BEPS? AND BEPS IMPACT Dell case (Spain SC) Restructured to low-risk distribution: FAR transferred to Principal Principal no substance no employees/office

The UK as a favoured location for Indian investments

The UK as a favoured location for Indian investments Over the course of multiple parliaments under different political leadership, UK Government policy has consistently aimed at creating the most competitive

The UK as a favoured location for Indian investments Over the course of multiple parliaments under different political leadership, UK Government policy has consistently aimed at creating the most competitive

BEPS Beyond Fortune 1000 October Armanino LLP amllp.com Armanino LLP amllp.com

BEPS Beyond Fortune 1000 October 2016 1 Armanino LLP amllp.com Armanino LLP amllp.com 1 BEPS Overview Timeline Pre-2013 - Organization for Economic Cooperation and Development (OECD) concern that existing

BEPS Beyond Fortune 1000 October 2016 1 Armanino LLP amllp.com Armanino LLP amllp.com 1 BEPS Overview Timeline Pre-2013 - Organization for Economic Cooperation and Development (OECD) concern that existing

Engaging title in Green Descriptive element in Blue 2 lines if needed

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

When The Dust Has Settled (Part 1)

") www.pwc.com/sg When The Dust Has Settled (Part 1) Elaine Ng, Tax Partner 15 August 2017 Let s shake up the dust ITA NOA GST IRAS DTA SDA EEIA 2 Let s shake up the dust CbCR PPT AEOI MAAL BEPS DPT MLI FHTP

www.pwc.com/sg When The Dust Has Settled (Part 1) Elaine Ng, Tax Partner 15 August 2017 Let s shake up the dust ITA NOA GST IRAS DTA SDA EEIA 2 Let s shake up the dust CbCR PPT AEOI MAAL BEPS DPT MLI FHTP

The International Tax Landscape

and EU Tax Reforms How will Ireland, Luxembourg, Netherlands and Switzerland Reform Their Tax Systems to Comply?, Loyens & Loeff NV, PricewatershouseCoopers, PricewaterhouseCoopers 67 th Annual Tax Conference

and EU Tax Reforms How will Ireland, Luxembourg, Netherlands and Switzerland Reform Their Tax Systems to Comply?, Loyens & Loeff NV, PricewatershouseCoopers, PricewaterhouseCoopers 67 th Annual Tax Conference

32nd Annual Asia Pacific Tax Conference November 2016 JW Marriott Hotel Hong Kong

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong The consequences of real transparency: Reporting,documentation and reconsidering your Asian structures in light of

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong The consequences of real transparency: Reporting,documentation and reconsidering your Asian structures in light of

Planning for Intangible Property Migration in an Uncertain Environment. ABA Section of Taxation Mid Year Meeting January 25, 2013

Planning for Intangible Property Migration in an Uncertain Environment ABA Section of Taxation Mid Year Meeting January 25, 2013 1 Presenters Moderator Kenneth Christman, Ernst &Young Panelists Chris Bello,

Planning for Intangible Property Migration in an Uncertain Environment ABA Section of Taxation Mid Year Meeting January 25, 2013 1 Presenters Moderator Kenneth Christman, Ernst &Young Panelists Chris Bello,

VAT The submerged part of the BEPS

www.pwc.com VAT The submerged part of the BEPS Thursday, Geneva Agenda Background Potential VAT impact of BEPS Permanent establishment (PE) issues and threats to commissionaire structures How non-european

www.pwc.com VAT The submerged part of the BEPS Thursday, Geneva Agenda Background Potential VAT impact of BEPS Permanent establishment (PE) issues and threats to commissionaire structures How non-european

BASE EROSION AND PROFIT SHIFTING ISSUES : THAILAND

BASE EROSION AND PROFIT SHIFTING ISSUES : THAILAND ECOSOC Special Meeting on International Cooperation in Tax Matters 5 June 2014 Phensuk Sangasubana The Revenue Department, Thailand CONTENTS Background

BASE EROSION AND PROFIT SHIFTING ISSUES : THAILAND ECOSOC Special Meeting on International Cooperation in Tax Matters 5 June 2014 Phensuk Sangasubana The Revenue Department, Thailand CONTENTS Background

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

32nd Annual Asia Pacific Tax Conference November 2016 JW Marriott Hotel Hong Kong

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong Alternative A: Source country taxation, evolving PE rules and unilateral measures Chair: Gary Sprague, Palo Alto

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong Alternative A: Source country taxation, evolving PE rules and unilateral measures Chair: Gary Sprague, Palo Alto

Ireland update: Considerations for U.S. companies

Ireland update: June 20, 2013 Leading today s discussion Dan Gaffey Julian Caplin Michael Shelley Michael McGivern Partner Partner, Head of International Audit International Tax Partner Corporate Finance

Ireland update: June 20, 2013 Leading today s discussion Dan Gaffey Julian Caplin Michael Shelley Michael McGivern Partner Partner, Head of International Audit International Tax Partner Corporate Finance

TRANSNATIONAL TAX NETWORK 2015 HONG KONG CONFERENCE. Hong Kong 9 February David Russell QC Outer Temple Chambers London and Dubai

TRANSNATIONAL TAX NETWORK 2015 HONG KONG CONFERENCE Hong Kong 9 February 2015 David Russell QC Outer Temple Chambers London and Dubai B.E.P.S. for BEGINNERS OR MISERY LOVES COMPANY A TALE OF TWO CITIES

TRANSNATIONAL TAX NETWORK 2015 HONG KONG CONFERENCE Hong Kong 9 February 2015 David Russell QC Outer Temple Chambers London and Dubai B.E.P.S. for BEGINNERS OR MISERY LOVES COMPANY A TALE OF TWO CITIES

Exploiting Intellectual Property Rights: Key Attractions of Locating Operations in Ireland

Locating Operations in briefing Many of the leading global corporates in the technology, pharma, medical devices, biotech and other sectors involved in the commercialisation of intellectual property have

Locating Operations in briefing Many of the leading global corporates in the technology, pharma, medical devices, biotech and other sectors involved in the commercialisation of intellectual property have

Women in Tax Leaders

www.internationaltaxreview.com Women in Tax Leaders SECOND EDITION The comprehensive guide to the world s leading female tax advisers : An attractive location for investment Lorraine Griffin and Louise

www.internationaltaxreview.com Women in Tax Leaders SECOND EDITION The comprehensive guide to the world s leading female tax advisers : An attractive location for investment Lorraine Griffin and Louise

Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

17 July 2017 Global Tax Alert Ireland signs Multilateral Convention to Implement Tax Treaty Related Measures to Prevent BEPS EY Global Tax Alert Library Access both online and pdf versions of all EY Global

THE NEW IRISH IP REGIME AND OTHER RECENT DEVELOPMENTS

THE NEW IRISH IP REGIME AND OTHER RECENT DEVELOPMENTS 1 RUNNING ORDER 1. Latest developments on Apple and Ireland 1. Irelands Food and Beverage sector An opportunity 1. A location for IP and intangibles

THE NEW IRISH IP REGIME AND OTHER RECENT DEVELOPMENTS 1 RUNNING ORDER 1. Latest developments on Apple and Ireland 1. Irelands Food and Beverage sector An opportunity 1. A location for IP and intangibles

OECD s Base Erosion and Profit Shifting (BEPS) Action Plan

Action Plan") OECD s Base Erosion and Profit Shifting (BEPS) Action Plan Joanne Theodorides Senior Manager Tax Advisory Services, PWC Email: joanne.theodorides@cy.pwc.com OECD s BEPS Action Plan The G20 finance minsters

OECD s Base Erosion and Profit Shifting (BEPS) Action Plan Joanne Theodorides Senior Manager Tax Advisory Services, PWC Email: joanne.theodorides@cy.pwc.com OECD s BEPS Action Plan The G20 finance minsters

INTERNATIONAL TAX STRUCTURING FOR INVESTING ADROAD INTERNATIONAL TAX CONFERENCE

INTERNATIONAL TAX STRUCTURING FOR INVESTING ADROAD December 5, 2009 INTERNATIONAL TAX CONFERENCE - 2009 Shefali Goradia Partner, BMR Advisors OVERSEAS INVESTMENT KEY DRIVERS Access to Global Markets Inorganic

INTERNATIONAL TAX STRUCTURING FOR INVESTING ADROAD December 5, 2009 INTERNATIONAL TAX CONFERENCE - 2009 Shefali Goradia Partner, BMR Advisors OVERSEAS INVESTMENT KEY DRIVERS Access to Global Markets Inorganic

Introduction to Transfer Pricing. Presented by Ziad Rahman APTP

Introduction to Transfer Pricing Presented by Ziad Rahman APTP What is Transfer Pricing? Arm s Length Principle. Transfer Pricing Documentation. Transfer Pricing Methodologies. Benchmarking. Transfer Pricing

Introduction to Transfer Pricing Presented by Ziad Rahman APTP What is Transfer Pricing? Arm s Length Principle. Transfer Pricing Documentation. Transfer Pricing Methodologies. Benchmarking. Transfer Pricing

BEPS Impact on Manufacturing

BEPS Impact on Manufacturing Base Erosion and Profit Shifting India has emerged as the seventh largest economy. Favorable demographics, a burgeoning domestic market and an annual growth rate in excess

BEPS Impact on Manufacturing Base Erosion and Profit Shifting India has emerged as the seventh largest economy. Favorable demographics, a burgeoning domestic market and an annual growth rate in excess

Cyprus Tax Update. Kyiv May 2018

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

Cyprus Tax Update Kyiv May 2018 Today s agenda 1. Snapshot of Cyprus tax system 2. Developments affecting the Cyprus tax regime 3. Selected developments : a) ATAD b) TP 4. Selected structures 5. Expected

International trends in taxation of capital and financial products and the impact on Thai Business

15th Annual Conference Maximise www.pwc.com/th International trends in taxation of capital and financial products and the impact on Thai Business Shareholder Value through Effective TAX Planning 2014 Agenda

15th Annual Conference Maximise www.pwc.com/th International trends in taxation of capital and financial products and the impact on Thai Business Shareholder Value through Effective TAX Planning 2014 Agenda

EU Commission approves enhancements to Madeira International Business Center Tax Regime

3 September 2013 EU Commission approves enhancements to Madeira International Business Center Tax Regime Executive summary On 2 July 2013, the EU Commission issued a decision allowing Portugal to increase

3 September 2013 EU Commission approves enhancements to Madeira International Business Center Tax Regime Executive summary On 2 July 2013, the EU Commission issued a decision allowing Portugal to increase

5. Ireland is Countering Aggressive Tax Planning

CONTENTS 1. Foreword by the Minister for Finance 2. Introduction 3. Ireland s International Tax Charter 4. Ireland s Corporate Tax Strategy 5. Ireland is Countering Aggressive Tax Planning 6. Conclusion

CONTENTS 1. Foreword by the Minister for Finance 2. Introduction 3. Ireland s International Tax Charter 4. Ireland s Corporate Tax Strategy 5. Ireland is Countering Aggressive Tax Planning 6. Conclusion

TAX UPDATE. Geneva, December 16, 2015

TAX UPDATE Geneva, December 16, 1 AGENDA 1. Swiss and international Corporate tax policy update 2. Base Erosion and Profit Shifting 3. Swiss Corporate Tax Reform III 4. Automatic exchange of information

TAX UPDATE Geneva, December 16, 1 AGENDA 1. Swiss and international Corporate tax policy update 2. Base Erosion and Profit Shifting 3. Swiss Corporate Tax Reform III 4. Automatic exchange of information

PwC Tax Panel 18 October 2016

18 th Annual Tax and Legal Conference Maximise Shareholder Value 2017 www.pwc.com/th Tax Panel Agenda Section one - Challenges in the digital economy Section two - Legal perspective for online transactions

18 th Annual Tax and Legal Conference Maximise Shareholder Value 2017 www.pwc.com/th Tax Panel Agenda Section one - Challenges in the digital economy Section two - Legal perspective for online transactions

Value chain perspectives and their increased importance under BEPS, tax policy and technological change

Value chain perspectives and their increased importance under BEPS, tax policy and technological change February 22, 2017 FOR DISCUSSION PURPOSES ONLY Disclaimer This material has been prepared for general

Value chain perspectives and their increased importance under BEPS, tax policy and technological change February 22, 2017 FOR DISCUSSION PURPOSES ONLY Disclaimer This material has been prepared for general

Tax Strategy Group TSG XX/XX Title CORPORATION TAX. Tax Strategy Group TSG 17/ July 2017

Tax Strategy Group TSG XX/XX Title CORPORATION TAX Tax Strategy Group TSG 17/01 25 July 2017 1 TSG 17/01 Tax Strategy Group Corporation Tax Contents Introduction... 3 Recent Domestic Developments... 5

Tax Strategy Group TSG XX/XX Title CORPORATION TAX Tax Strategy Group TSG 17/01 25 July 2017 1 TSG 17/01 Tax Strategy Group Corporation Tax Contents Introduction... 3 Recent Domestic Developments... 5

OECD releases final BEPS package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

6 October 2015 Tax Flash OECD releases final BEPS package On 5 October 2015, the OECD published the final reports of the OECD/G20 Base Erosion and Profit Shifting ( BEPS ) project, which consist of a package

China & Hong Kong Latest Transfer Pricing Developments

www.pwc.com/tp China & Hong Kong Latest Transfer Pricing Developments Navigating through the complexity June 2015 Disclaimer The materials of this seminar/workshop/conference are intended to provide general

www.pwc.com/tp China & Hong Kong Latest Transfer Pricing Developments Navigating through the complexity June 2015 Disclaimer The materials of this seminar/workshop/conference are intended to provide general

A new design for the corporate income tax?

A new design for the corporate income tax? Michael Devereux Paris, October 17, 2013 Three issues 1. Why tax corporate profit, and what economic problems arise in attempting to do so? 2. Defining the domestic

A new design for the corporate income tax? Michael Devereux Paris, October 17, 2013 Three issues 1. Why tax corporate profit, and what economic problems arise in attempting to do so? 2. Defining the domestic

Welcome to the EFS-seminar. BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

Welcome to the EFS-seminar BEPS and transfer pricing, but what about VAT and Customs? Conference Chairman: René van der Paardt Rotterdam February 3, 2016 Agenda Seminar An update on the transfer pricing

Principles of International Tax Planning

Overview and Learning Objectives This course is aimed at analysing the fundamentals of international tax planning in a structured and consistent manner, deepening the knowledge of tax planning techniques

Overview and Learning Objectives This course is aimed at analysing the fundamentals of international tax planning in a structured and consistent manner, deepening the knowledge of tax planning techniques

THE KNOWLEDGE DEVELOPMENT BOX Public Consultation JANUARY 2015

THE KNOWLEDGE DEVELOPMENT BOX Public Consultation JANUARY 2015 Public Consultation Paper: The Knowledge Development Box Department of Finance January 2015 Tax Policy Division Department of Finance Government

THE KNOWLEDGE DEVELOPMENT BOX Public Consultation JANUARY 2015 Public Consultation Paper: The Knowledge Development Box Department of Finance January 2015 Tax Policy Division Department of Finance Government

Turkish Perspective on OECD Action Plan on Base Erosion and Profit Shifting

Turkey Ramazan Biçer and Mehmet Erginay* Turkish Perspective on OECD Action Plan on Base Erosion and Profit Shifting The OECD Action Plan on Base Erosion and Profit Shifting (BEPS) is a focal point of

Turkey Ramazan Biçer and Mehmet Erginay* Turkish Perspective on OECD Action Plan on Base Erosion and Profit Shifting The OECD Action Plan on Base Erosion and Profit Shifting (BEPS) is a focal point of

Outbound investments -Tax issues. 21 April 2012 CA. N.C.Hegde

Outbound investments -Tax issues 21 April 2012 CA. N.C.Hegde Key takeaways of the session Key tax objectives and challenges Scenarios Funds to be repatriated to India Funds not to be repatriated to India

Outbound investments -Tax issues 21 April 2012 CA. N.C.Hegde Key takeaways of the session Key tax objectives and challenges Scenarios Funds to be repatriated to India Funds not to be repatriated to India

CA T. P. OSTWAL. T. P. Ostwal & Associates LLP

CA T. P. OSTWAL BEPS strategies may not necessarily be illegal Increased globalisation enables companies to exploit gaps arising on interaction of domestic tax systems and treaty rules within the boundary

CA T. P. OSTWAL BEPS strategies may not necessarily be illegal Increased globalisation enables companies to exploit gaps arising on interaction of domestic tax systems and treaty rules within the boundary

Exploiting & Protecting IP in Ireland

Exploiting & Protecting IP in Ireland Intellectual Property Framework in Ireland Ireland is a favourable and popular location for holding and exploiting Intellectual Property ( IP ) due to its beneficial

Exploiting & Protecting IP in Ireland Intellectual Property Framework in Ireland Ireland is a favourable and popular location for holding and exploiting Intellectual Property ( IP ) due to its beneficial

Tax footprint report 2017

Tax Footprint 2017 Tax footprint report 2017 This tax footprint report is a non-audited report, where Kemira publishes its global tax policy and key tax figures. Kemira s quantitative tax analysis is prepared

Tax Footprint 2017 Tax footprint report 2017 This tax footprint report is a non-audited report, where Kemira publishes its global tax policy and key tax figures. Kemira s quantitative tax analysis is prepared

To what extent does Cyprus still present advantages in international tax planning? The Switzerland EC savings tax agreement: a positive result?

The following completed extended essays have been submitted by students registered for the ADIT extended essay option, and have been awarded a pass. Successful extended essays are correct to 30 June 2018.

The following completed extended essays have been submitted by students registered for the ADIT extended essay option, and have been awarded a pass. Successful extended essays are correct to 30 June 2018.

Irish Tax Institute Response to public consultation on the review of the corporation tax code

Irish Tax Institute Response to public consultation on the review of the corporation tax code Table of Contents About the Institute... 3 Introduction... 4 Summary of Recommendations... 5 Responses to consultation

Irish Tax Institute Response to public consultation on the review of the corporation tax code Table of Contents About the Institute... 3 Introduction... 4 Summary of Recommendations... 5 Responses to consultation

Next Generation Fund Structuring Are you ready? 10 May 2017

Next Generation Fund Structuring Are you ready? 10 May 2017 Global Private Equity Fundraising Activity Page 2 Agenda and Speakers 1. Fund Level Considerations Adam Williams EY Greater China Private Equity

Next Generation Fund Structuring Are you ready? 10 May 2017 Global Private Equity Fundraising Activity Page 2 Agenda and Speakers 1. Fund Level Considerations Adam Williams EY Greater China Private Equity

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

EUROPEAN COMMISSION PRESENTS ANTI-TAX AVOIDANCE PACKAGE tax.thomsonreuters.com On January 28, 2016, the European Commission presented its Communication on the Anti-Tax Avoidance Package (ATA Package).

Ireland, one of the best places in the world to do business. Q Key Marketplace Messages

, one of the best places in the world to do business. Q1 2013 Key Marketplace Messages Why : Companies are attracted to for a variety reasons: Talent Young, flexible, adaptable, mobile workforce. The median

, one of the best places in the world to do business. Q1 2013 Key Marketplace Messages Why : Companies are attracted to for a variety reasons: Talent Young, flexible, adaptable, mobile workforce. The median

Prior to joining Microsoft, Angel worked for Arthur Andersen in their New York Office.

Steve covers Finance, CELA and Human Resource (HR). The Finance function includes: Purchasing, RE&F, Venture Integration, Corporate Finance, Finance Operations, Physical Security, Treasury, Investor Relations,

Steve covers Finance, CELA and Human Resource (HR). The Finance function includes: Purchasing, RE&F, Venture Integration, Corporate Finance, Finance Operations, Physical Security, Treasury, Investor Relations,

A Guide To Changes In Irish Tax Rules

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

Trends I Netherlands moves away from fiscal offshore industry

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

1 Trends I Netherlands moves away from fiscal offshore industry The Netherlands is slowly but surely steering away from facilitating the use of its corporate income tax system by companies that are set

Country by country (CbC) reporting reaches Indian shores. By Paresh Parekh, Partner, EY March 2, 2016

reporting reaches Indian shores. By Paresh Parekh, Partner, EY March 2, 2016") Country by country (CbC) reporting reaches Indian shores By aresh arekh, artner, EY March 2, 2016 Contents CbC reporting BES Action 13 - background Budget 2016 proposals Global overview age 2 BES - What

Country by country (CbC) reporting reaches Indian shores By aresh arekh, artner, EY March 2, 2016 Contents CbC reporting BES Action 13 - background Budget 2016 proposals Global overview age 2 BES - What

International Tax. international tax developments in the Asia Pacific region. February 2015

International Tax A Hong Kong perspective on key international tax developments in the Asia Pacific region February 2015 An overview of key international tax developments and structuring considerations

International Tax A Hong Kong perspective on key international tax developments in the Asia Pacific region February 2015 An overview of key international tax developments and structuring considerations

BASE EROSION PROFIT SHARING INITIATIVE THE IMPLICATIONS FOR THE BAHAMAS

BASE EROSION PROFIT SHARING INITIATIVE THE IMPLICATIONS FOR THE BAHAMAS By Ryan Pinder Partner, Graham Thompson International Business & Finance Summit (IBFS) March 2, 2018 Baha Mar Convention Centre Nassau,

BASE EROSION PROFIT SHARING INITIATIVE THE IMPLICATIONS FOR THE BAHAMAS By Ryan Pinder Partner, Graham Thompson International Business & Finance Summit (IBFS) March 2, 2018 Baha Mar Convention Centre Nassau,

GILTI WHEN CHARGED? IT S NOT JUST IP THAT S IMPACTED

GILTI WHEN CHARGED? IT S NOT JUST IP THAT S IMPACTED SESSION OVERVIEW GILTI, WHEN CHARGED? IT S NOT JUST IP THAT S IMPACTED Albert Liguori (USA), Benoit Bec (France), Paolo Ruggiero (Italy), Shane Wallace

GILTI WHEN CHARGED? IT S NOT JUST IP THAT S IMPACTED SESSION OVERVIEW GILTI, WHEN CHARGED? IT S NOT JUST IP THAT S IMPACTED Albert Liguori (USA), Benoit Bec (France), Paolo Ruggiero (Italy), Shane Wallace

LIVE WEBCAST UPDATE ON BEPS PROJECT. 26 May :00pm 2:00pm (CEST)

") LIVE WEBCAST UPDATE ON BEPS PROJECT 26 May 2014 1:00pm 2:00pm (CEST) Speakers Pascal Saint-Amans Director, Centre for Tax Policy and Administration Raffaele Russo Head of BEPS Project Marlies de Ruiter

LIVE WEBCAST UPDATE ON BEPS PROJECT 26 May 2014 1:00pm 2:00pm (CEST) Speakers Pascal Saint-Amans Director, Centre for Tax Policy and Administration Raffaele Russo Head of BEPS Project Marlies de Ruiter

Statement for the Record

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Tax Planning in the Middle East

Overview and Learning Objectives This three-day intermediate-level course concentrates on a number of common international tax planning scenarios in the Middle East region. It examines the widely used

Overview and Learning Objectives This three-day intermediate-level course concentrates on a number of common international tax planning scenarios in the Middle East region. It examines the widely used

Roundup of Australia s BEPS developments

TaxTalk Insights Global Tax Roundup of Australia s BEPS developments 12 April 2017 In brief Since its presidency of the G20 in 2014, Australia has been at the forefront of efforts to combat tax avoidance

TaxTalk Insights Global Tax Roundup of Australia s BEPS developments 12 April 2017 In brief Since its presidency of the G20 in 2014, Australia has been at the forefront of efforts to combat tax avoidance

International Tax Primer. Third Edition. Brian J. Arnold

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

International Tax Primer Third Edition Brian J. Arnold Wolters Kluwer Preface xi CHARTER 1 Introduction 1 1.1 Objectives of This Primer 1 1.2 What Is International Tax? 2 1.3 Goals of International Tax

Ireland updates international tax strategy

14 October 2016 Issue 06/2016 Tax alert Ireland Ireland updates international tax strategy Contacts If you require further information, please call your regular contact in EY or contact any of the following:

14 October 2016 Issue 06/2016 Tax alert Ireland Ireland updates international tax strategy Contacts If you require further information, please call your regular contact in EY or contact any of the following:

Transfer Pricing Update

Transfer Pricing Update Ray Brown, Principal Economist, DLA Piper - Los Angeles Mike Patton, Partner, DLA Piper - Los Angeles Eric Ryan, Partner, DLA Piper - Silicon Valley *This presentation is offered

Transfer Pricing Update Ray Brown, Principal Economist, DLA Piper - Los Angeles Mike Patton, Partner, DLA Piper - Los Angeles Eric Ryan, Partner, DLA Piper - Silicon Valley *This presentation is offered