1/25/2018. Disclaimer. Course Objectives. Basic Sales and Use Tax

|

|

|

- Stuart Mathews

- 6 years ago

- Views:

Transcription

1 Basic Sales and Use Tax Minnesota Business Tax Education February 2018 Disclaimer This presentation is for educational purposes only. It is meant to accompany an oral presentation and not to be used as a standalone document. This presentation is based on the facts and circumstances being discussed, and on the laws in effect when it is presented. It does not supersede or alter any provisions of Minnesota laws, administrative rules, court cases, or revenue notices. If you have any questions, contact us at salesuse.edu@state.mn.us, , or (toll-free). Minnesota Business Tax Education Program Providing education opportunities about Minnesota tax laws. 2 Course Objectives After completing this course you will be able to: Apply the basic sales and use tax concepts for Minnesota and its local taxing jurisdictions to your business. Recognize the exceptions to the "rule" and the exemptions available. Identify how to use and when to accept an exemption certificate. Distinguish how sales and use tax law applies to different types of businesses and their business activities. Identify the documentation necessary for sales and use tax records and returns. List several resources that answer your sales and use tax questions. 3 1

2 Sales and Use Tax Basics Part 1 4 Sales and Use Tax Basics Sales and Use Tax Laws are not the same in every state. 5 Sales and Use Tax Basics Five categories of sales Real Property Intangible Property Services Tangible Personal Property (TPP) Digital Products 6 2

3 Sales and Use Tax Basics What are some examples of taxable services in your business? 7 Sales and Use Tax Basics Sales tax = transaction tax 8 Sales and Use Tax Basics Trust tax 1. Collect 2. File 3. Remit 9 3

4 Sales and Use Tax Basics What is a sale? Barter Providing a service Retail Sale Wholesale Lease Rentals 10 Sales and Use Tax Basics What is use tax? Complement to sales tax Self-assessed Paid directly to the state Applies to taxable purchases when sales tax was not charged 11 Sales and Use Tax Basics What is the tax rate? 6.875% 12 4

5 Sales and Use Tax Basics Sourcing determines where the sale takes place and which taxes are imposed on the sale. 1. Seller s Address (if that s where title to or possession of item takes place) 2. Delivery Address (if item is shipped or delivered to customer or where service is performed) 3. Billing Address (based on the address that the seller has in their records for the customer) Minnesota Statutes 297A.668 and 297A Sales and Use Tax Basics How do I determine what taxes apply to the sale? Sourcing rules for leases or rentals of TPP 1 st Payment General Sourcing Rules (where transfer of property occurs) Subsequent Payments Primary Property Location (address provided to lessor by lessee) 14 Sales and Use Tax Basics ALL charges that are a condition of sale Service charges Tips added to bill by seller Retail price of good or service Sales Price Taxes that are obligation of seller Fabrication labor Delivery charges Installation labor 15 5

Less coupon -.50 $ 2.67 Selling price $ 2.00 -.50 Tax on $2.00 +.14 (6.875%) $ 2.17 Total Due $ 2.")

17 Sales and Use Tax Basics When is labor taxed?")

6 Sales and Use Tax Basics Sales price does not include: Credit allowed for trade-in Term discounts Cash discounts Coupons, unless reimbursed by a 3 rd party Taxes legally imposed on consumer Interest charges Finance charges from extension of credit 16 Sales and Use Tax Basics Manufacturer s Coupon Light bulb Tax on $2.50 Subtotal Less coupon Total Due Retailer s Coupon 50 cents off 50 cents off $ 2.50 Light bulb $ (6.875%) Less coupon -.50 $ 2.67 Selling price $ Tax on $ (6.875%) $ 2.17 Total Due $ 2.14 Retailer s coupon seller reduces price by coupon before taxing Manufacturer s coupon apply tax before coupon is subtracted (seller is reimbursed by the manufacturer for the amount of the coupon) 17 Sales and Use Tax Basics When is labor taxed? Type of Labor Examples Is it taxable? Repair labor Construction labor Fabrication labor Installation labor Car repair Equipment repair Calibrating equipment Sharpening tools Build an office building Kitchen remodel Custom sawing Bending sheet metal Computer equipment Modular furniture No (if separately stated) No Yes Yes

7 Sales and Use Tax Basics When are repair and maintenance contracts taxed? Type of Contract Is the contract taxable? Optional maintenance contracts Yes. Tax is due when the contracted (bundled one nonitemized price) maintenance is sold. Optional maintenance contracts No. The service provider charges sales (unbundled separate itemized prices) tax to the customer on the taxable items when the repair is performed. Extended warranty contracts No. The service provider owes tax on the parts provided under the contract. 19 Sales and Use Tax Basics When are software maintenance agreements taxed? Details of agreement Taxability of agreement Required by vendor The entire charge is taxable Includes only upgrades or enhancements Optional and includes upgrades, enhancements and support services Optional and includes support services only The entire charge is taxable 20% of the charge is taxable Not taxable 20 Who Needs to Register? Part

8 Who needs to register? You must register if you: Make taxable sales in Minnesota Make purchases subject to use tax 22 Who needs to register? Sales made over the Internet 23 Who needs to register? Leasing or renting TPP Business location Performing services Delivering TPP in own vehicle NEXUS Repairing or installing TPP Performing construction work Agent, sales rep, solicitor, or affiliated company Tradeshow or convention 24 8

9 Local Taxes Part 3 25 Local Taxes Local taxes are added to the state general sales tax rate to compute the total tax rate. City tax County tax Special local tax(es) Motor vehicle $20 excise tax Note: Some cities and counties impose a $20 excise tax on sales of motor vehicles rather than a sales tax. See Fact Sheet 164, Local Sales and Use Taxes. 26 Local Taxes Where do I find local tax information? Select the Sales & Use Tax link under For Businesses on our website s home page. Then, click on the Tax Information tab. Select the Local Tax Information link. 27 9

10 Local Taxes Local Taxes The Department also has an interactive tool on our website that provides the state and local general sales and use tax rates that apply to sales made to specific locations in Minnesota. What is the name of this interactive tool? Sales Tax Rate Calculator 29 Local Taxes 30 10

11 When and How to Use Exemption Certificates Part 4 31 When and How to Use Exemption Certificates There are three ways for a sale to be exempt from sales and use taxes: 1. Product-based exemption (Do not need exemption certificate exempt by statute) 2. Entity-based exemption (Need exemption certificate unless exempt by statute) 3. Use-based exemption (Always need an exemption certificate) 32 When and How to Use Exemption Certificates Product-based exemptions Food (grocery items) for human consumption (F.S. 102A) Clothing for general use (F.S. 105) Prescription and over-the-counter drugs for humans (F.S. 117) Publications sold by subscription 33 11

12 When and How to Use Exemption Certificates Entity-based exemptions Federal government agencies Tribal governments State and local governments (exceptions apply) Exempt organizations (organized for charitable, educational, or religious purposes) Note: The sales tax exemption for entity-based organizations does not apply to prepared food, candy, soft drinks or alcoholic beverages; the purchases, lease or rental of most motor vehicles; lodging; or waste collection and disposal services unless purchased directly by the federal government. 34 When and How to Use Exemption Certificates Use-based exemptions Advertising materials shipped out of state Inventory purchased for resale Items consumed in performing a taxable service Items used or consumed in agricultural production Materials used or consumed in the manufacturing process Note: See applicable fact sheets for specific details on the exemptions. 35 When and How to Use Exemption Certificates Authorization letters and permits Businesses claiming these exemptions must complete an exemption certificate: Direct Pay Exempt Status (nonprofit exemption) Motor Carrier Direct Pay Resource Recovery Facility 36 12

Uniform Sales and Use Tax Certificate (Multistate Tax Commission form) Other state s exemption certificates (if all required elements are included) Self-prepared")

13 When and How to Use Exemption Certificates Authorized exemption certificates: Certificate of Exemption, Form ST3 (Minnesota Department of Revenue form) Certificate of Exemption, Form F0003 (Streamlined Sales Tax form) Uniform Sales and Use Tax Certificate (Multistate Tax Commission form) Other state s exemption certificates (if all required elements are included) Self-prepared exemption certificate (if all required elements are included) 37 When and How to Use Exemption Certificates Required elements for a complete exemption certificate: Purchaser's name and address Purchaser's Minnesota tax ID number Purchaser s type of business Reason for exemption Purchaser's signature 38 The red boxes identify the fields that are required for a complete exemption certificate. The purchasing agent must retain the contract as supporting documentation. The seller s information is not required but it doesn t hurt to complete these fields. Jane Smith 39 13

14 When and How to Use Exemption Certificates Purchaser s responsibilities: Know if you qualify to claim an exemption Complete an exemption certificate Give it to the seller at the time of purchase Pay any use tax, penalty, and/or interest if used incorrectly 40 When and How to Use Exemption Certificates Seller s responsibilities Review all exemption certificates Keep exemption certificates as part of your business records Do not unlawfully solicit exemption certificates 41 How Sales and Use Tax Applies to Business Activity Part

Cities, counties, and townships are not taxable (exceptions apply) 43 Government Agencies")

(3) organizations)")

15 Government Agencies Collect sales tax on taxable goods and services sold Determine taxability of purchases of taxable goods and services based on type of government: Federal government agencies are not taxable Tribal governments are not taxable State agencies are taxable (use direct pay authorization) Cities, counties, and townships are not taxable (exceptions apply) 43 Government Agencies Purchases made by government employees are taxable unless paid for directly by the government agency Purchases of prepared food, lodging, and motor vehicles are taxable (except by federal government) Other states or political subdivisions of other states may qualify for an exemption 44 Nonprofit Organizations Examples of nonprofit organizations are: Charitable (Federal 501(c)(3) organizations) Religious Educational 45 15

16 Nonprofit Organizations Collect sales tax on taxable goods and services sold, unless the fundraising exemption applies Do not pay sales or use tax on purchases used to further the nonprofit s activities Pay sales tax on the following: Lodging Motor vehicles Prepared food Purchases made by employees unless paid for directly by the nonprofit 46 Contractors A contractor is someone who: Supplies labor and materials Constructs, alters, repairs, or improves real property Is the end user of the materials and equipment 47 Contractors The following purchases are taxable: Building materials and supplies, unless an exemption applies for the job* Construction equipment and tools Business assets and office supplies * If the job is not exempt by statute, the contractor needs a valid purchasing agent agreement (see F.S. 128, Contractors) in order to buy the building materials exempt

17 Contractors For sales and use tax purposes, real property includes: Land Permanent buildings and structures Improvements and fixtures incorporated into a building or structure given its current use intended to be of a permanent benefit cannot be removed without causing substantial damage to the building or structure Exception: Real property does not include tools, implements, machinery, and equipment attached or installed into real property that qualify for exemption under section 297A.68 (for example capital equipment used in manufacturing to produce a product ultimately sold at retail.) 49 Contractors Examples of real property include: Commercial and residential buildings Drywall, flooring, and roofing materials incorporated into real property Landscaped lawns and gardens Roads, bridges, and railroad tracks 50 Retailers Retailers sell TPP to businesses and individuals. They must collect sales tax on goods they sell.* Their inventory bought for resale is not taxable.* Their purchases of business assets and office supplies are taxable. They are responsible for paying use tax on goods taken out of inventory for their own use. * The seller must charge tax unless the item is specifically exempt by law or they have a completed exemption certificate on file (if the sale is sourced to Minnesota and the seller has nexus here.) 51 17

.")

18 Contractor/Retailer Primarily a contractor - at least 50 percent of your business purchases are used for construction activities Primarily a retailer - at least 50 percent of your business purchases are sold at retail 52 Contractor/Retailer If you are primarily a contractor: Pay tax on all your purchases. Charge sales tax on the actual sales price (including your mark-up). Deduct the cost of the materials on which you already paid tax when you file your sales and use tax return. 53 Contractor s Purchase Invoice Materials Materials $ Tax Tax (6.875%) (6.875%) $ Total Total $ Customer s Sales Invoice Materials Materials $ $ Tax Tax (6.875%) (6.875%) $ Total Total $ $ Amount Reported on the Sales and Use Tax Return Gross Receipts $150 Less: Original Invoice $ 50 General Rate Sales $100 Note: The $50 purchase amount from the contractor s original invoice is not recorded on your return. This is an example only. Report total taxable sales on the return

19 Contractor/Retailer If you are primarily a retailer: Buy the items exempt for resale. Pay use tax on your cost of the materials if any of the items are later used in a construction contract. 55 Nontaxable Service Providers Examples include: Accountants Attorneys Banks Consulting firms Counselors Health care providers 56 Nontaxable Service Providers The majority of services offered by these businesses are not taxable. Sales of TPP made by a service provider are taxable. Purchases of business assets and office supplies are taxable

20 Taxable Service Providers The majority of sales are taxable (see fact sheets for exceptions). Materials used or consumed in providing the service may qualify for exemption. Short-lived detachable tools may qualify for exemption. Machinery and equipment used in providing the services are taxable. 58 Manufacturers The industrial production process includes: Design, Research and Development for production of a product Removal of raw materials from stock to begin production activities Actual production activities that affect changes to produce the product Testing and quality control of the product Placement of the product in finished goods inventory 59 Manufacturers Business assets and office supplies are taxable Returnable packaging is taxable Product packaging and other nonreturnable packaging is not taxable* Raw materials, chemicals and utilities used or consumed in production are not taxable* Separate detachable tools and special tooling are not taxable* * The purchaser must provide the seller with a completed exemption certificate for these items

21 Manufacturers Upfront exemption for capital equipment available (effective July 1, 2015) Machinery and equipment may qualify as capital equipment if: used in Minnesota and essential to the integrated production process 61 Agricultural Production Agricultural production includes: Agriculture Aquaculture Floriculture Horticulture Silviculture 62 Agricultural Production Feed, seed, fertilizers, and herbicides are not taxable. Fuels, electricity, gas, and steam used or consumed in agricultural production are not taxable. Packaging materials used to package food products are not taxable. Farm machinery is not taxable. Returnable containers used to package non-food items are taxable

22 Sales and Use Tax is a Transaction Tax 64 Transaction Tax - Seller The seller must look at each transaction. A general contractor rents equipment (without an operator) to a subcontractor. A wholesaler makes a retail sale to an employee. A farm implement dealer sells equipment to a contractor. An accounting firm sells software to a client and installs it on the client s computers. A lawn care business provides snow removal services in the winter. 65 Transaction Tax - Purchaser The purchaser must look at each transaction. A general contractor buys materials for a tax-exempt job. A retail electronics store buys taxable office supplies. A manufacturer buys utilities to heat their facility. A farmer buys tires for a tractor. A building cleaning company buys vacuum cleaners

23 Managing your Use Tax Liability Part 6 67 Managing Your Use Tax Liability Review your invoices 68 Managing Your Use Tax Liability What is the basis for use tax? Use tax is based on: your purchase price of taxable items or services. This is true whether you buy items: for your own business use without paying sales tax, take them out of inventory and use them in a taxable manner, or donate them to a charitable organization. Note: Even if you paid Minnesota sales tax, a local use tax may still apply

24 Managing Your Use Tax Liability What should I look for when reviewing invoices? Review every invoice before you pay it. Determine if items on the invoice are taxable. Watch for taxable items purchased with an exemption certificate. Watch vendor changes (e.g. new computer system). Never add use tax to a vendor payment; always self-assess the tax and remit it directly to the Department of Revenue. Record the amount of use tax accrued on the actual invoice. 70 Managing Your Use Tax Liability What is a variable rate credit? Minnesota allows a credit for the amount of sales tax paid to another state Must be legally due to the other state to receive credit 71 Managing Your Use Tax Liability 1. Calculate the applicable amount of tax due (variable rate X sales price). 2. Enter the amount(s) as variable rate use tax when you file your Minnesota sales and use tax return. Minnesota sales tax rate 6.875% Wisconsin state and local sales tax ( 5.500%) Variable rate tax due to Minnesota 1.375% 72 24

25 Managing Your Use Tax Liability Recording your use tax liability Record this information: Date of purchase Invoice number Vendor s name and description of item Taxable amount Amount of state and local use taxes paid Keep a copy of the backup documentation. 73 Maintaining your Records Part 7 74 Maintaining Your Records Recordkeeping Basics Use a recordkeeping system that: Incorporates Generally Accepted Accounting Principles Allows you to keep track of the data you need Does not require an excessive amount of time Works for you and your business 75 25

26 Maintaining Your Records Recordkeeping Basics Record each transaction the same Do not mix personal and business transactions Do not mix records if you have more than one business Choose the appropriate accounting method 76 Maintaining Your Records Accounting methods Cash Basis Record income when actually received Report sales tax when actually received Report use tax when invoice is paid vs. Accrual Basis Record income when sales are made Report sales tax when sales are made Report use tax based on the invoice date 77 Filing and Payment Instructions Part

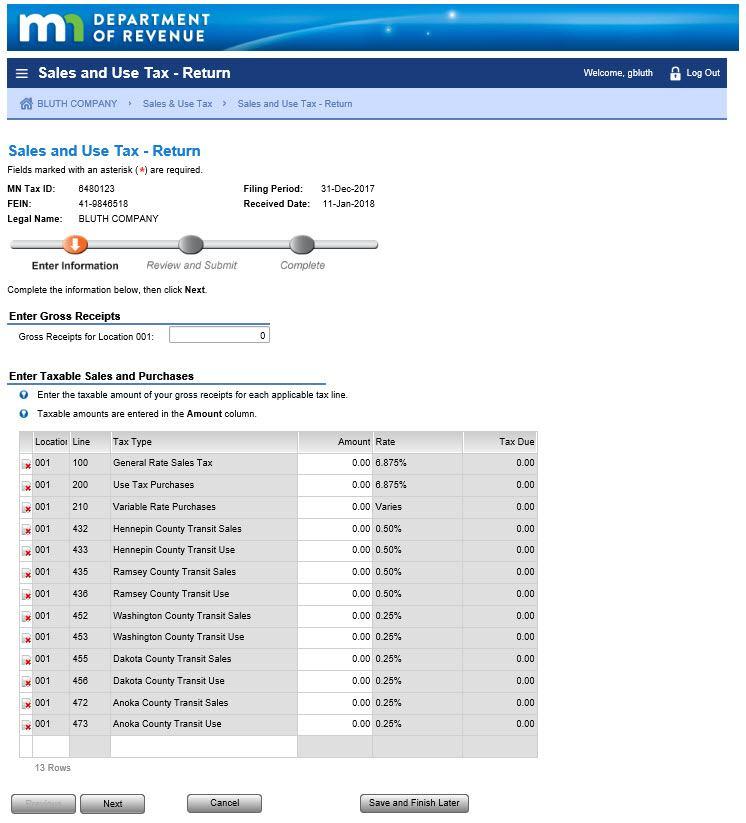

27 Filing and Payment Instructions You must do two things to avoid late filing and/or late payment penalties: 1. File your return electronically by the due date. (either online or by telephone) 2. Pay your sales and use tax liability electronically or by check on or before the due date. 79 Filing and Payment Instructions Filing Frequency Average Tax Liability Due Date Monthly filers Quarterly filers Annual filers More than $500 per month (more than $6,000 per year) Less than $500 per month (less than $6,000 per year) Less than $100 per month (less than $1,200 per year) 20th day of the following month 20th day of the month following the end of the quarter (April 20, July 20, October 20, and January 20) February 5 of the following year 80 Filing and Payment Instructions 27

28 Filing and Payment Instructions Filing and Payment Instructions Filing and Payment Instructions 28

29 Filing and Payment Instructions Common reasons you may need to file an amended return are: Reported too much or too little tax on your original return Reported the tax on the wrong tax line Charged tax incorrectly to a customer and have refunded the tax to the customer Received a completed exemption certificate from a customer (you reported the tax in a prior period and have since refunded the tax to your customer) Note: Do not file an amended return for tax paid to a vendor in error. 85 Communicating with the Department of Revenue Part 9 86 Communicating with the Department of Revenue Have a sales and use tax question? 87 29

30 Communicating with the Department of Revenue Sales and Use Tax Division Minnesota Revenue website: revenue.state.mn.us Questions relating to Sales and Use Tax Law? Questions relating to your Sales and Use Tax account activity? Prefer telephone assistance? Phone: or Communicating with the Department of Revenue for Other Divisions Business Income Taxes (Corporation Franchise Tax, Partnership Tax, S Corporation Tax, Estate Tax, Fiduciary Tax) businessincome.tax@state.mn.us Withholding Tax or withholding.tax@state.mn.us Business Registration or Business.Registration@state.mn.us 89 Minnesota Department of Revenue Website revenue.state.mn.us 90 30

31 Minnesota Department of Revenue Website revenue.state.mn.us 91 Minnesota Department of Revenue Website Sales and Use Tax Videos youtube.com/mnrevenue Available Videos: e-services Instructional Videos Education Video Series Inside Scoop: Streamlined Sales Tax Training Videos 92 Minnesota Department of Revenue Website GovDelivery Choose the updates you want - by tax type and publication type Choose the frequency of notifications Sign in directly or use your social media account Facebook, Yahoo! or Google 93 31

32 Minnesota Department of Revenue Website Social Media Keep up with the latest news from the Minnesota Department of Revenue on Twitter, Facebook, and LinkedIn. twitter.com/mnrevenue facebook.com/mnrevenue linkedin.com/company/minnesota-department-of-revenue 94 Communicating with the Department of Revenue Please notify us if you have changes to any of the following: Mailing address(es) Business location(s) Legal organization NAICS code Contact information Owners and/or officers 95 Communicating with the Department of Revenue Did you receive a letter or a bill from us? 96 32

33 Financial Consequences of Noncompliance Part Financial Consequences of Noncompliance Days Late Late Filing Penalty Late Payment Penalty 1-30 days 5 percent 5 percent days 5 percent 10 percent 60+ days 5 percent 15 percent Note: The maximum combined late file and late payment penalty is 20 percent. Additional civil and criminal penalties may apply. 98 Financial Consequences of Noncompliance Interest rates used by the Department of Revenue in recent years: % % 99 33

34 Financial Consequences of Noncompliance Collection tools available to the Department include: Levies License revocation Liens Property seizures Revenue recapture 100 Course Review During this class, we discussed The basic sales and use tax concepts for Minnesota and its local taxing jurisdictions. The difference between taxable goods and services and those that are nontaxable or exempt. The different types of users and how tax applies to different businesses. How to use and when to accept an exemption certificate. The documentation necessary for sales and use tax records and returns. Where to find information to help you answer your questions. 101 Basic Sales and Use Tax Review 1. Who is responsible for paying sales or use tax on these purchases? a. Retailer purchasing inventory for resale b. Cleaning service buying window cleaner c. Manufacturer buying raw materials d. Business leasing a photocopier e. None of the above

35 Basic Sales and Use Tax Review 2. Which of these are not considered part of the sales price? a. Installation charges b. Finance charges c. Retail price of product or service d. Service charges added to the bill by the seller e. All of the above 103 Basic Sales and Use Tax Review 3. Which of these services are not taxable in Minnesota? a. Motor vehicle washing b. Pet grooming c. Accounting services d. Detective services e. All of the above 104 Basic Sales and Use Tax Review 4. Which of the following is considered tangible personal property? a. Office supplies b. Food (e.g. fresh or frozen fruits, vegetables and meat) c. Machinery and equipment d. Utilities (e.g. gas, water, electricity, fuel, etc.) e. All of the above

36 Basic Sales and Use Tax Review 5. Which of these types of labor are taxable? a. Repair labor b. Construction labor c. Fabrication labor d. Installation labor (item remains TPP after installation) e. Both c & d 106 Basic Sales and Use Tax Review 6. An exempt organization cannot use their exempt status to purchase which of the following exempt from tax? a. Toilet paper b. Toner for their printer c. Lunch at a restaurant for a business meeting d. Cleaning service for the office e. None of the above 107 Basic Sales and Use Tax Review 7. What is the largest percent that can be charged for combined late filing/late payment penalties? a. 5% b. 10% c. 15% d. 20% e. All of the above

37 Basic Sales and Use Tax Review 8. According to contractor/retailer rules, a carpenter who builds cabinets and installs the majority of his products into real property can buy the materials used to fabricate the cabinets exempt. TRUE FALSE 109 Basic Sales and Use Tax Review 9. Taxable items taken out of inventory to be given away for a donation or as free samples are subject to use tax. TRUE FALSE 110 Basic Sales and Use Tax Review 10. Out-of-state customers who pick up their taxable merchandise in Minnesota have to pay Minnesota sales tax and all applicable local taxes. TRUE FALSE

38 Basic Sales and Use Tax Review 11. Making a phone call to a customer located in Minnesota is enough business activity to establish Nexus in Minnesota. TRUE FALSE 112 Basic Sales and Use Tax Review 12. Nonprofits who have been granted federal nonprofit status automatically qualify for sales tax exempt status. TRUE FALSE 113 Basic Sales and Use Tax Review 13. A business creates and sells custom DVDs and pays sales tax on the blank DVDs when they buy them. The business does not have to charge sales tax to their customer because tax was already paid. TRUE FALSE

for the tax paid. TRUE FALSE 116 Questions?")

39 Basic Sales and Use Tax Review 14. Since cutting hair is not a taxable service in Minnesota, a beauty salon or barber shop would not need to register for a Minnesota Tax ID#. TRUE FALSE 115 Basic Sales and Use Tax Review 15. I paid sales tax on capital equipment purchased. I can file a refund request (Form ST11) for the tax paid. TRUE FALSE 116 Questions?

40 Thank you! Permission of the Minnesota Department of Revenue must be secured before exhibiting, reproducing, distributing or making any other use of any part of this presentation. Produced by the Minnesota Department of Revenue 600 North Robert Street, St. Paul, Minnesota Copyright 2018, Minnesota Department of Revenue, All Rights Reserved Minnesota Business Tax Education 40

Course Guide. Basic Sales and Use Tax February 2018

Course Guide Basic Sales and Use Tax February 2018 This course is an introduction to sales and use taxes in Minnesota. It is designed for business owners, bookkeepers, purchasing agents, and accountants

Course Guide Basic Sales and Use Tax February 2018 This course is an introduction to sales and use taxes in Minnesota. It is designed for business owners, bookkeepers, purchasing agents, and accountants

Use Tax for Businesses 146

www.revenue.state.mn.us Use Tax for Businesses 146 Sales Tax Fact Sheet 146 What s new in 2017 We updated the layout to make this fact sheet easier to use. Minnesota Use Tax applies when you buy, lease,

www.revenue.state.mn.us Use Tax for Businesses 146 Sales Tax Fact Sheet 146 What s new in 2017 We updated the layout to make this fact sheet easier to use. Minnesota Use Tax applies when you buy, lease,

Contractors. Defining real property. What s New in 2018

www.revenue.state.mn.us Contractors Sales Tax Fact Sheet 128 128 Fact Sheet What s New in 2018 A 2017 law change added a definition of real property for purposes of sales tax. (Minnesota Statute 297A.61,

www.revenue.state.mn.us Contractors Sales Tax Fact Sheet 128 128 Fact Sheet What s New in 2018 A 2017 law change added a definition of real property for purposes of sales tax. (Minnesota Statute 297A.61,

2/5/2018. Sales and Use Tax for Manufacturers. Disclaimer. Introduction

Sales and Use Tax for Manufacturers Minnesota Business Tax Education February 2018 Disclaimer This presentation is for educational purposes only. It is meant to accompany an oral presentation and not to

Sales and Use Tax for Manufacturers Minnesota Business Tax Education February 2018 Disclaimer This presentation is for educational purposes only. It is meant to accompany an oral presentation and not to

Reference Guide. Sales and Use Tax e-services Webinar January 2018

Reference Guide Sales and Use Tax e-services Webinar January 2018 This course is a live demonstration of e-services related to Minnesota sales and use tax. The webinar is designed for e- Services users

Reference Guide Sales and Use Tax e-services Webinar January 2018 This course is a live demonstration of e-services related to Minnesota sales and use tax. The webinar is designed for e- Services users

Also, you may write the addresses below and fax or mail this letter back to us.

To Our Valued Customers: In an effort to continually improve our service to you, our valued customers, Brabazon Pump Company is preparing to initiate electronic delivery of invoices. We are presently building

To Our Valued Customers: In an effort to continually improve our service to you, our valued customers, Brabazon Pump Company is preparing to initiate electronic delivery of invoices. We are presently building

What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and Use Taxes on page 4.

www.revenue.state.mn.us Landscaping Construction Contracts Sales Tax Fact Sheet 121B 121B Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales

www.revenue.state.mn.us Landscaping Construction Contracts Sales Tax Fact Sheet 121B 121B Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales

Photography and Video Production

www.revenue.state.mn.us Photography and Video Production Sales Tax Fact Sheet 169 169 Fact Sheet What s New in 2015 Starting July 1, 2015, the capital equipment refund is an up-front sales tax exemption.

www.revenue.state.mn.us Photography and Video Production Sales Tax Fact Sheet 169 169 Fact Sheet What s New in 2015 Starting July 1, 2015, the capital equipment refund is an up-front sales tax exemption.

NEW CUSTOMER CHECKLIST

NEW CUSTOMER CHECKLIST Name of Account & Number: Salesperson: Type of Account (i.e. street etc ) Is this account affiliated with any other current accounts? Delivery Information: Name: Street Address Line

NEW CUSTOMER CHECKLIST Name of Account & Number: Salesperson: Type of Account (i.e. street etc ) Is this account affiliated with any other current accounts? Delivery Information: Name: Street Address Line

Changes in Arkansas Sales and Use Tax Law Effective January 1, 2008

STATE OF ARKANSAS Department of Finance and Administration http://www.state.ar.us/dfa SALES & USE TAX SECTION P. O. BOX 1272 LITTLE ROCK, AR 72203-1272 PHONE: (501) 682-7104 FAX: (501) 682-7904 sales.tax@rev.state.ar.us

STATE OF ARKANSAS Department of Finance and Administration http://www.state.ar.us/dfa SALES & USE TAX SECTION P. O. BOX 1272 LITTLE ROCK, AR 72203-1272 PHONE: (501) 682-7104 FAX: (501) 682-7904 sales.tax@rev.state.ar.us

Wayfair Impacts for Minnesota Sellers Webinar: October 2018

Wayfair Impacts for Minnesota Sellers Webinar: October 2018 Disclaimer: Information in this document is based on the laws in effect when it was written. It does not supersede or alter any provision of

Wayfair Impacts for Minnesota Sellers Webinar: October 2018 Disclaimer: Information in this document is based on the laws in effect when it was written. It does not supersede or alter any provision of

New Customer Questionnaire and Credit Application

Remit all payments to: CMA/Flodyne/Hydradyne, Inc., 3265 Gateway Road, Suite 300, Brookfield, WI 53045 Phone: 262-781-1815 Fax: 262-781-2521 New Customer Questionnaire and Credit Application As you are

Remit all payments to: CMA/Flodyne/Hydradyne, Inc., 3265 Gateway Road, Suite 300, Brookfield, WI 53045 Phone: 262-781-1815 Fax: 262-781-2521 New Customer Questionnaire and Credit Application As you are

Sales and Use Tax Return Filing Guide

Sales and Use Tax Return Filing Guide GENERAL QUESTIONS How often must I file? Depending on your filing schedule, your business will receive a sales and use tax form on a regular basis. Average tax due

Sales and Use Tax Return Filing Guide GENERAL QUESTIONS How often must I file? Depending on your filing schedule, your business will receive a sales and use tax form on a regular basis. Average tax due

Florida Annual Resale Certificate for Sales Tax

Florida Annual Resale Certificate for Sales Tax GT-800060 R. 12/17 What s New for 2015 Florida Annual Resale Certificates for Sales Tax Florida Annual Resale Certificates for Sales Tax are available for

Florida Annual Resale Certificate for Sales Tax GT-800060 R. 12/17 What s New for 2015 Florida Annual Resale Certificates for Sales Tax Florida Annual Resale Certificates for Sales Tax are available for

12A SALES AND USE TAX CHAPTER 12A-1 SALES AND USE TAX

12A SALES AND USE TAX CHAPTER 12A-1 SALES AND USE TAX 12A-1.001 Specific Exemptions. 12A-1.0011 Schools Offering Grades K through 12; Parent-Teacher Associations; and Parent-Teacher Organizations. 12A-1.0015

12A SALES AND USE TAX CHAPTER 12A-1 SALES AND USE TAX 12A-1.001 Specific Exemptions. 12A-1.0011 Schools Offering Grades K through 12; Parent-Teacher Associations; and Parent-Teacher Organizations. 12A-1.0015

Detective and Security Services 114

www.revenue.state.mn.us Detective and Security Services 114 Sales Tax Fact Sheet 114 Fact Sheet What s New in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and

www.revenue.state.mn.us Detective and Security Services 114 Sales Tax Fact Sheet 114 Fact Sheet What s New in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and

SALES TAX INFORMATION GUIDE. Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO (970)

") SALES TA INFORMATION GUIDE Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO 81615 www.tosv.com (970) 923-3796 Table of Contents *You will be taken directly to any section in this document by

SALES TA INFORMATION GUIDE Town of Snowmass Village P.O. Box 5010 Snowmass Village, CO 81615 www.tosv.com (970) 923-3796 Table of Contents *You will be taken directly to any section in this document by

State Tax Return. Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

June 2005 Volume 12 Number 6 State Tax Return Out With The Old And In With The New: Ohio Abandons Its Corporate Franchise Tax And Enacts A Commercial Activities Tax Maryann B. Gall Jason R. Grove Columbus

Business Tax Application

Business Tax Application Welcome to The Kansas business community! IMPORTANT: The information contained in this booklet regarding Telefile is no longer valid as the program has been discontinued. This

Business Tax Application Welcome to The Kansas business community! IMPORTANT: The information contained in this booklet regarding Telefile is no longer valid as the program has been discontinued. This

Florida Department of Revenue Tax Information Publication. TIP 03A01-20 Date Issued: Dec 17, 2003

Florida Department of Revenue Tax Information Publication TIP 03A01-20 Date Issued: Dec 17, 2003 COUPONS, DISCOUNTS, REBATES, FREE MERCHANDISE, AND OTHER PROMOTIONAL GIFTS Florida law provides that "discounts

Florida Department of Revenue Tax Information Publication TIP 03A01-20 Date Issued: Dec 17, 2003 COUPONS, DISCOUNTS, REBATES, FREE MERCHANDISE, AND OTHER PROMOTIONAL GIFTS Florida law provides that "discounts

ARIZONA TRANSACTION PRIVILEGE AND USE TAX

ARIZONA TRANSACTION PRIVILEGE AND USE TAX DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail

ARIZONA TRANSACTION PRIVILEGE AND USE TAX DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail

SALES AND USE TAX TECHNICAL BULLETINS SECTION 12 SECTION 12 - HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES

SECTION 12 - HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES 12-1 SALES TO AND BY HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES A. Purchases of Tangible Personal Property Hospitals, sanitariums,

SECTION 12 - HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES 12-1 SALES TO AND BY HOSPITALS, SANITARIUMS, NURSING HOMES, AND REST HOMES A. Purchases of Tangible Personal Property Hospitals, sanitariums,

FYI For Your Information

TAXPAYER SERVICE DIVISION FYI For Your Information How to Document Sales to Retailers, Tax-Exempt Organizations and Direct Pay Permit Holders GENERAL INFORMATION The information contained in this FYI is

TAXPAYER SERVICE DIVISION FYI For Your Information How to Document Sales to Retailers, Tax-Exempt Organizations and Direct Pay Permit Holders GENERAL INFORMATION The information contained in this FYI is

Sales & Use Tax for Government & Municipalities

Sales & Use Tax for Government & Municipalities Sales Tax 12-36- 910(A) reads: A sales tax, equal to [six] percent of the gross proceeds of sales, is imposed upon every person engaged or continuing within

Sales & Use Tax for Government & Municipalities Sales Tax 12-36- 910(A) reads: A sales tax, equal to [six] percent of the gross proceeds of sales, is imposed upon every person engaged or continuing within

ACCG Annual Conference 2013 Sales Tax Update

ACCG Annual Conference 2013 Sales Tax Update This presentation is the property of the Commissioner, Georgia Department of Revenue. All rights reserved. No part of this publication may be reproduced, stored

ACCG Annual Conference 2013 Sales Tax Update This presentation is the property of the Commissioner, Georgia Department of Revenue. All rights reserved. No part of this publication may be reproduced, stored

North Carolina Department of Revenue

DIRECTIVE Subject: Charges for Shop Supplies Tax: Sales and Use Tax Law: N.C. Gen. Stat. 105-164.3(37), 105-164.4(a)(1), and 105-164.4(a)(16) Issued By: Sales and Use Tax Division Date: May 25, 2018 Number:

DIRECTIVE Subject: Charges for Shop Supplies Tax: Sales and Use Tax Law: N.C. Gen. Stat. 105-164.3(37), 105-164.4(a)(1), and 105-164.4(a)(16) Issued By: Sales and Use Tax Division Date: May 25, 2018 Number:

Certificate of Exemption

ST3 Purchaser: Complete this certificate and give it to the seller. Seller: If this certificate is not fully completed, you must charge sales tax. Keep this certificate as part of your records. This is

ST3 Purchaser: Complete this certificate and give it to the seller. Seller: If this certificate is not fully completed, you must charge sales tax. Keep this certificate as part of your records. This is

APPLICATION FOR IN STORE CHARGE ACCOUNT

APPLICATION FOR IN STORE CHARGE ACCOUNT Business or Organization Name Contact Person Name Billing Address City/State/Zip Phone and Fax Numbers E-mail Address For Main Contact Bank Name Tax Exempt Number

APPLICATION FOR IN STORE CHARGE ACCOUNT Business or Organization Name Contact Person Name Billing Address City/State/Zip Phone and Fax Numbers E-mail Address For Main Contact Bank Name Tax Exempt Number

Lawn and Garden Maintenance, Tree and Shrub Services

www.revenue.state.mn.us Lawn and Garden Maintenance, Tree and Shrub Services Sales Tax Fact Sheet 121A 121A Fact Sheet Minnesota Sales Tax applies to lawn and garden maintenance, indoor plant care, tree

www.revenue.state.mn.us Lawn and Garden Maintenance, Tree and Shrub Services Sales Tax Fact Sheet 121A 121A Fact Sheet Minnesota Sales Tax applies to lawn and garden maintenance, indoor plant care, tree

Direct Selling Companies 168

www.revenue.state.mn.us Direct Selling Companies 168 Sales Tax Fact Sheet 168 Fact Sheet What s New in 2017 We updated the layout of this fact sheet easier to make it use. For sales tax purposes, a direct

www.revenue.state.mn.us Direct Selling Companies 168 Sales Tax Fact Sheet 168 Fact Sheet What s New in 2017 We updated the layout of this fact sheet easier to make it use. For sales tax purposes, a direct

Business Information. Application for Registered Businesses to Add a New Florida Location

Reason for Applying Identification Nos. Application Eligibility When to Use this Application Application for Registered Businesses to Add a New Florida Location Register online at floridarevenue.com/taxes/registration.

Reason for Applying Identification Nos. Application Eligibility When to Use this Application Application for Registered Businesses to Add a New Florida Location Register online at floridarevenue.com/taxes/registration.

If no tax ID number, FEIN Driver s license number/state issued ID number enter one of the following: state of issue number

ST3 give it to the seller. purchases, or until otherwise cancelled by the purchaser.. Exempt entity name Name of purchaser Business address City State Zip code Type or print Purchaser s tax ID number State

ST3 give it to the seller. purchases, or until otherwise cancelled by the purchaser.. Exempt entity name Name of purchaser Business address City State Zip code Type or print Purchaser s tax ID number State

Hotels and Lodging Facilities 141

www.revenue.state.mn.us Hotels and Lodging Facilities 141 Sales Tax Fact Sheet 141 Fact Sheet What s New in 2017 We have clarified who is responsible for collecting sales tax on residential short-term

www.revenue.state.mn.us Hotels and Lodging Facilities 141 Sales Tax Fact Sheet 141 Fact Sheet What s New in 2017 We have clarified who is responsible for collecting sales tax on residential short-term

Lawn and Garden Maintenance, Tree and Shrub Services

www.revenue.state.mn.us Lawn and Garden Maintenance, Tree and Shrub Services Sales Tax Fact Sheet 121A 121A Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes.

www.revenue.state.mn.us Lawn and Garden Maintenance, Tree and Shrub Services Sales Tax Fact Sheet 121A 121A Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes.

Certificate of Exemption

Purchaser: Complete this certificate and give it to the seller. Seller: If this certificate is not completed, you must charge sales tax. Keep this certificate as part of your records. This is a blanket

Purchaser: Complete this certificate and give it to the seller. Seller: If this certificate is not completed, you must charge sales tax. Keep this certificate as part of your records. This is a blanket

Sales and Use Taxes Real Property and Services to Real Property. Eric K. Wayne, Sales & Use Tax Director March 30, 2017

Sales and Use Taxes Real Property and Services to Real Property Eric K. Wayne, Sales & Use Tax Director March 30, 2017 Disclaimer Presentation is for general information only. Presentation content should

Sales and Use Taxes Real Property and Services to Real Property Eric K. Wayne, Sales & Use Tax Director March 30, 2017 Disclaimer Presentation is for general information only. Presentation content should

Sales and Use Tax Returns. Sales and Use Tax Return HD/PM Date: / / DR-15 R. 08/18 Florida 1. Gross Sales 2. Exempt Sales 3. Taxable Amount 4.

Instructions for DR-15 Sales and Use Tax Returns Rule 12AER18-07, F.A.C. Effective 08/18 Page 1 of 8 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos and estimated tax

Instructions for DR-15 Sales and Use Tax Returns Rule 12AER18-07, F.A.C. Effective 08/18 Page 1 of 8 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos and estimated tax

Sales and Use Tax for Manufacturers. Connecticut Business & Industry Association

www.pwc.com Sales and Use Tax for Manufacturers Connecticut Business & Industry Association Robert L. Day III Jennifer Whalley June 29, 2015 Agenda The Basics and 2015 budget Full Exemptions Manufacturing

www.pwc.com Sales and Use Tax for Manufacturers Connecticut Business & Industry Association Robert L. Day III Jennifer Whalley June 29, 2015 Agenda The Basics and 2015 budget Full Exemptions Manufacturing

Managing Sales Tax Exemptions

Managing Sales Tax Exemptions Diane Yetter May 11, 2017 Introduction Sales are taxable unless a specific exemption or exclusion Proceed with caution when determining which transactions qualify Careful

Managing Sales Tax Exemptions Diane Yetter May 11, 2017 Introduction Sales are taxable unless a specific exemption or exclusion Proceed with caution when determining which transactions qualify Careful

Building Cleaning and Maintenance

www.revenue.state.mn.us Building Cleaning and Maintenance 112 Sales Tax Fact Sheet What s New in 2016 We updated this fact sheet to clarify that maintenance contracts for mechanical systems and junk removal

www.revenue.state.mn.us Building Cleaning and Maintenance 112 Sales Tax Fact Sheet What s New in 2016 We updated this fact sheet to clarify that maintenance contracts for mechanical systems and junk removal

Isolated and Occasional Sales 132

www.revenue.state.mn.us Isolated and Occasional Sales 132 Sales Tax Fact Sheet 132 Fact Sheet What s new in 2017 We updated the layout of this fact sheet to make it easier to use. Most sales of business

www.revenue.state.mn.us Isolated and Occasional Sales 132 Sales Tax Fact Sheet 132 Fact Sheet What s new in 2017 We updated the layout of this fact sheet to make it easier to use. Most sales of business

Dear New Business Owner,

Dear New Business Owner, The City of Beckley would like to take this opportunity to welcome you! The city believes that all business is important not only to our city but to the overall economy. I would

Dear New Business Owner, The City of Beckley would like to take this opportunity to welcome you! The city believes that all business is important not only to our city but to the overall economy. I would

Minnesota State Fair Sales Tax 140

www.revenue.state.mn.us Minnesota State Fair Sales Tax 140 Sales Tax Fact Sheet 140 Fact Sheet What s new in 2018 For 2018: Taxable sales at the Minnesota State Fair are now subject to the Ramsey County

www.revenue.state.mn.us Minnesota State Fair Sales Tax 140 Sales Tax Fact Sheet 140 Fact Sheet What s new in 2018 For 2018: Taxable sales at the Minnesota State Fair are now subject to the Ramsey County

STREAMLINED SALES TAX COMPLIANCE CHECKLIST WEST VIRGINIA

STREAMLINED SALES TAX COMPLIANCE CHECKLIST WEST VIRGINIA August 1, 2006 SECTION TOPIC DESCRIPTION Is this requirement met by law, regulation or administrative practice ( or No). Enter N/A when not applicable.

STREAMLINED SALES TAX COMPLIANCE CHECKLIST WEST VIRGINIA August 1, 2006 SECTION TOPIC DESCRIPTION Is this requirement met by law, regulation or administrative practice ( or No). Enter N/A when not applicable.

3. How can I contact the Department of Taxation with questions about the CAT?

1. What is the Commercial Activity Tax ("CAT")? The CAT is an annual tax imposed on the privilege of doing business in Ohio, measured by taxable gross receipts from most business activities. Most receipts

1. What is the Commercial Activity Tax ("CAT")? The CAT is an annual tax imposed on the privilege of doing business in Ohio, measured by taxable gross receipts from most business activities. Most receipts

North Carolina Association of CPAs 2015 Not-for-Profit Conference Sales and Use Taxes. Eric K. Wayne, Sales & Use Tax Director May 19, 2015

North Carolina Association of CPAs 2015 Not-for-Profit Conference Sales and Use Taxes Eric K. Wayne, Sales & Use Tax Director May 19, 2015 Disclaimer Presentations are for general information only Presentation

North Carolina Association of CPAs 2015 Not-for-Profit Conference Sales and Use Taxes Eric K. Wayne, Sales & Use Tax Director May 19, 2015 Disclaimer Presentations are for general information only Presentation

Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers

New York State Department of Taxation and Finance Publication 774 (1/10) Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers About this publication

New York State Department of Taxation and Finance Publication 774 (1/10) Purchaser's Obligations to Pay Sales and Use Taxes Directly to the Tax Department Questions and Answers About this publication

ST-3 Form for all in state resellers

ST-3 Form for all in state resellers ST-3 (4-08, R-11) The seller must collect the tax on a sale of taxable property or services unless the purchaser gives him a properly completed New Jersey exemption

ST-3 Form for all in state resellers ST-3 (4-08, R-11) The seller must collect the tax on a sale of taxable property or services unless the purchaser gives him a properly completed New Jersey exemption

Course Guide. Sales and Use Tax for Manufacturers September 2018

Course Guide Sales and Use Tax for Manufacturers September 2018 This course is for businesses located in Minnesota that make products intended to be sold ultimately at retail. It is designed for business

Course Guide Sales and Use Tax for Manufacturers September 2018 This course is for businesses located in Minnesota that make products intended to be sold ultimately at retail. It is designed for business

DR-15EZ. Sales and Use Tax Returns

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 07/12 Rule 12A-1.097 Florida Administrative Code Are you Eligible to Use a DR-15EZ Return? Collection Allowance Our records indicate you are

Instructions for DR-15EZ Sales and Use Tax Returns DR-15EZN R. 07/12 Rule 12A-1.097 Florida Administrative Code Are you Eligible to Use a DR-15EZ Return? Collection Allowance Our records indicate you are

South Carolina Department of Revenue

SMALL BUSINESS TAX WORKSHOP South Carolina Department of Revenue Topics To Be Covered Today Checklist for New Businesses in South Carolina Purchasing the Assets of a Business The Retail License Sales &

SMALL BUSINESS TAX WORKSHOP South Carolina Department of Revenue Topics To Be Covered Today Checklist for New Businesses in South Carolina Purchasing the Assets of a Business The Retail License Sales &

ARIZONA TRANSACTION PRIVILEGE AND USE TAX

ARIZONA TRANSACTION PRIVILEGE AND USE TAX DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail

ARIZONA TRANSACTION PRIVILEGE AND USE TAX DEFINITION TRANSACTION PRIVILEGE TAX (TPT) Commonly referred to as sales tax, TPT is tax on the retail sale of tangible personal property AND services. Retail

Petroleum Products 116

www.revenue.state.mn.us Petroleum Products 116 Sales Tax Fact Sheet 116 Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and Use Taxes

www.revenue.state.mn.us Petroleum Products 116 Sales Tax Fact Sheet 116 Fact Sheet What s new in 2018 We clarified when sellers are required to collect local sales taxes. See Local Sales and Use Taxes

12A Manufacturing. (1)(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible

(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible") 12A-1.043 Manufacturing. (1)(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible personal property for his own use shall pay a tax upon the

12A-1.043 Manufacturing. (1)(a) Any person who manufactures, produces, compounds, processes, or fabricates in any manner an article of tangible personal property for his own use shall pay a tax upon the

HOUSE FINANCE COMMITTEE BRIEFING. February 7, 2017 Finance Committee Staff

HOUSE FINANCE COMMITTEE BRIEFING February 7, 2017 Finance Committee Staff Presentation Overview 2 Introduction to the Finance Committee Overview of General Fund Revenue Sources Personal Income Tax Overview

HOUSE FINANCE COMMITTEE BRIEFING February 7, 2017 Finance Committee Staff Presentation Overview 2 Introduction to the Finance Committee Overview of General Fund Revenue Sources Personal Income Tax Overview

GLOSSARY. IPT Sales and Use Tax Symposium Beginner Basics

GLOSSARY IPT Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

GLOSSARY IPT Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 20

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 20 Lease and Rental Transactions This bulletin is intended solely as advice to assist persons in determining and complying

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION INSTRUCTIONAL BULLETIN NO. 20 Lease and Rental Transactions This bulletin is intended solely as advice to assist persons in determining and complying

Connecticut. Connecticut Will Implement App and Cookie Nexus. November 2017

November 2017 Connecticut Connecticut Will Implement App and Cookie Nexus Commissioner Kevin B. Sullivan stated that the Connecticut Department of Revenue Services will issue revised guidance early in

November 2017 Connecticut Connecticut Will Implement App and Cookie Nexus Commissioner Kevin B. Sullivan stated that the Connecticut Department of Revenue Services will issue revised guidance early in

2013 Tax Law Changes Overview: Sales and Use Tax

2013 Tax Law Changes Overview: Sales and Use Tax Tax Type Statute Brief Description Effective Date 116J.3738, Subd. 1 : Provides a definition and method of certification for businesses in Greater Minnesota

2013 Tax Law Changes Overview: Sales and Use Tax Tax Type Statute Brief Description Effective Date 116J.3738, Subd. 1 : Provides a definition and method of certification for businesses in Greater Minnesota

CHAPTER Committee Substitute for Senate Bill No. 1690

CHAPTER 98-141 Committee Substitute for Senate Bill No. 1690 An act relating to taxes on sales, use, and other transactions (RAB); amending s. 212.0506, F.S.; revising guidelines for tax liability of service

CHAPTER 98-141 Committee Substitute for Senate Bill No. 1690 An act relating to taxes on sales, use, and other transactions (RAB); amending s. 212.0506, F.S.; revising guidelines for tax liability of service

CERTIFICATE OF COMPLIANCE -- STATE OF GEORGIA Revised May 2010*

CERTIFICATE OF COMPLIANCE -- STATE OF GEORGIA Revised May 2010* SECTION Section 301 Section 302 Section 303 State level administration State and local tax base Seller registration Does the state provide

CERTIFICATE OF COMPLIANCE -- STATE OF GEORGIA Revised May 2010* SECTION Section 301 Section 302 Section 303 State level administration State and local tax base Seller registration Does the state provide

Nonprofits Organizations and Fundraising 180

www.revenue.state.mn.us Nonprofits Organizations and Fundraising 180 Sales Tax Fact Sheet 180 Fact Sheet What s new in 2017 Starting July 1, 2017 Qualifying fundraising sales may be made at premises that

www.revenue.state.mn.us Nonprofits Organizations and Fundraising 180 Sales Tax Fact Sheet 180 Fact Sheet What s new in 2017 Starting July 1, 2017 Qualifying fundraising sales may be made at premises that

Are You a Vendor? Issued June 1, 2015/Revised January 23, 2017 Wyoming Department of Revenue

Are You a Vendor? Issued June 1, 2015/Revised January 23, 2017 Wyoming Department of Revenue W.S. 39-15-101(a)(xv) states a Vendor means any person engaged in the business of selling at retail or wholesale

Are You a Vendor? Issued June 1, 2015/Revised January 23, 2017 Wyoming Department of Revenue W.S. 39-15-101(a)(xv) states a Vendor means any person engaged in the business of selling at retail or wholesale

Sales and Use Tax Returns. File and pay electronically and on time to receive a collection allowance.

Instructions for DR-15 Sales and Use Tax Returns DR-15N R. 01/18 Rule 12A-1.097 Florida Administrative Code Effective 01/18 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos

Instructions for DR-15 Sales and Use Tax Returns DR-15N R. 01/18 Rule 12A-1.097 Florida Administrative Code Effective 01/18 Lawful deductions (Line 6) cannot be more than tax due (Line 5). DOR credit memos

CHAPTER 13 STATE TAXES

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

CHAPTER 13 STATE TAXES Latest Revision 1994 13.01 INTRODUCTION Ohio relies on various taxes to support its governmental activities. Some of these taxes have transfer provisions which accrue to the benefit

Greenwood Village Tax Compliance Guide

Greenwood Village Tax Compliance Guide The following information is intended to serve as a complement to the Greenwood Village Municipal Code and official tax policies as adopted by the Greenwood Village

Greenwood Village Tax Compliance Guide The following information is intended to serve as a complement to the Greenwood Village Municipal Code and official tax policies as adopted by the Greenwood Village

Certificate of Exemption

Purchaser: Complete this certificate and give it to the seller. Seller: If this certificate is not fully completed, you must charge sales tax. Keep this certificate as part of your records. This is a blanket

Purchaser: Complete this certificate and give it to the seller. Seller: If this certificate is not fully completed, you must charge sales tax. Keep this certificate as part of your records. This is a blanket

Sales Tax Guidelines for the Construction Industry Originally issued March 26, 2003/Revised August 1, 2014 Wyoming Department of Revenue

Sales Tax Guidelines for the Construction Industry Originally issued March 26, 2003/Revised August 1, 2014 Wyoming Department of Revenue This publication is intended for those in the construction industry.

Sales Tax Guidelines for the Construction Industry Originally issued March 26, 2003/Revised August 1, 2014 Wyoming Department of Revenue This publication is intended for those in the construction industry.

PST-38 Issued: February 1985 Revised: March 22, 2017 INFORMATION FOR NON-RESIDENT REAL PROPERTY AND SERVICE CONTRACTORS

Information Bulletin PST-38 Issued: February 1985 Revised: March 22, 2017 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT Click here to complete our short READER SURVEY INFORMATION FOR NON-RESIDENT

Information Bulletin PST-38 Issued: February 1985 Revised: March 22, 2017 Was this bulletin useful? THE PROVINCIAL SALES TAX ACT Click here to complete our short READER SURVEY INFORMATION FOR NON-RESIDENT

GLOSSARY. IPT 2016 Sales and Use Tax Symposium Beginner Basics

GLOSSARY IPT 2016 Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

GLOSSARY IPT 2016 Sales and Use Tax Symposium Beginner Basics GLOSSARY The following definitions have been developed to facilitate an understanding of the course material. They tend to be generic in nature,

Explanation / Uses of each account in the Chart of Accounts:

Explanation / Uses of each account in the Chart of Accounts: 1 Debtors Debtors tracks money that customers owe you for products or services, and payments customers make. QuickBooks Online Plus automatically

Explanation / Uses of each account in the Chart of Accounts: 1 Debtors Debtors tracks money that customers owe you for products or services, and payments customers make. QuickBooks Online Plus automatically

Restaurants and Bars 137

www.revenue.state.mn.us Restaurants and Bars 137 Sales Tax Fact Sheet 137 Fact Sheet What s new in 2017 Starting July 1, 2017, the only taxable food sold through vending machines is prepared food, soft

www.revenue.state.mn.us Restaurants and Bars 137 Sales Tax Fact Sheet 137 Fact Sheet What s new in 2017 Starting July 1, 2017, the only taxable food sold through vending machines is prepared food, soft

Ch. 33 COMPUTATION OF TAX CHAPTER 33. COMPUTATION OF TAX

Ch. 33 COMPUTATION OF TAX 61 33.1 CHAPTER 33. COMPUTATION OF TAX Sec. 33.1. Definitions. 33.2. Scope. 33.3. Cancellations, returns, allowances and exchanges. 33.4. Credit and lay-away sales. 33.1. Definitions.

Ch. 33 COMPUTATION OF TAX 61 33.1 CHAPTER 33. COMPUTATION OF TAX Sec. 33.1. Definitions. 33.2. Scope. 33.3. Cancellations, returns, allowances and exchanges. 33.4. Credit and lay-away sales. 33.1. Definitions.

CONTRACTORS EXCISE TAX

CONTRACTORS EXCISE TAX The information in this presentation does not cover every aspect of tax, nor does it alter or supersede any state statute or administrative regulation. The information in this presentation

CONTRACTORS EXCISE TAX The information in this presentation does not cover every aspect of tax, nor does it alter or supersede any state statute or administrative regulation. The information in this presentation

Sales Tax Guidelines for Contractor-Fabricators and Contractor- Manufacturers

-2$1:$*1216(&5(7$5< '(3$570(172)5(9(18( 32/,&

-2$1:$*1216(&5(7$5< '(3$570(172)5(9(18( 32/,&

Sales Tax 101 For The Small Business Owner

Sales Tax 101 For The Small Business Owner Presented by Brian Mackin Sales Manager Avalara About the Presenter Brian Mackin Small business owner for over 30 years Joined Avalara 5 years ago as a project

Sales Tax 101 For The Small Business Owner Presented by Brian Mackin Sales Manager Avalara About the Presenter Brian Mackin Small business owner for over 30 years Joined Avalara 5 years ago as a project

SALES & USE TAX FOR PUBLIC PROCUREMENT THE BASICS OF SALES TAX

SALES & USE TAX FOR PUBLIC PROCUREMENT SC ASSOCIATION OF GOVERNMENTAL PURCHASING OFFICIALS SEPTEMBER 14, 2017 1 THE BASICS OF SALES TAX South Carolina imposes a sales tax equal to 6%, plus applicable local

SALES & USE TAX FOR PUBLIC PROCUREMENT SC ASSOCIATION OF GOVERNMENTAL PURCHASING OFFICIALS SEPTEMBER 14, 2017 1 THE BASICS OF SALES TAX South Carolina imposes a sales tax equal to 6%, plus applicable local

INSTR. DRAFT 12/11/14

INSTR. DRAFT 12/11/14 Instructions for Form 4567 Michigan Business Tax (MBT) Annual Return Purpose To calculate the Modified Gross Receipts Tax and Business Income Tax as well as the surcharge for standard

INSTR. DRAFT 12/11/14 Instructions for Form 4567 Michigan Business Tax (MBT) Annual Return Purpose To calculate the Modified Gross Receipts Tax and Business Income Tax as well as the surcharge for standard

Local Sales and Use Taxes 164

Local es 164 Sales Tax Fact Sheet 164 Fact Sheet What s New in 2017 Starting October 1, 2017: Anoka County will have a 0.25 percent Transit Carver County will have a 0.5 percent Transit Clay County will

Local es 164 Sales Tax Fact Sheet 164 Fact Sheet What s New in 2017 Starting October 1, 2017: Anoka County will have a 0.25 percent Transit Carver County will have a 0.5 percent Transit Clay County will

Michael Silver & Company CPAs Comprehensive Automobile Dealer Sales Tax Checklist

5750 Old Orchard Road Suite 200 Skokie, IL 60077 Main: 847-982-0333 Fax: 847-982-0219 www.msco.net Michael Silver & Company CPAs Comprehensive Automobile Dealer Sales Tax Checklist Sales Taxable Trade

5750 Old Orchard Road Suite 200 Skokie, IL 60077 Main: 847-982-0333 Fax: 847-982-0219 www.msco.net Michael Silver & Company CPAs Comprehensive Automobile Dealer Sales Tax Checklist Sales Taxable Trade

SOMN.ORG SOMN.ORG. Special Olympics Minnesota Finance Guide

Special Olympics Minnesota Finance Guide 1 TABLE OF CONTENTS SOMN Finance Staff...3 SOMN Finance Overview...4 Finance Chair Responsibilities...5 Centralized Accounting Log In Procedures...6 Centralized

Special Olympics Minnesota Finance Guide 1 TABLE OF CONTENTS SOMN Finance Staff...3 SOMN Finance Overview...4 Finance Chair Responsibilities...5 Centralized Accounting Log In Procedures...6 Centralized

Prepare, print, and e-file your federal tax return for free!

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

Prepare, print, and e-file your federal tax return for free! www.freetaxusa.com SCHEDULE F (Form 1040) Department of the Treasury Internal Revenue Service (99) Name of proprietor Profit or Loss From Farming

CERTIFICATE OF COMPLIANCE -- STATE OF KENTUCKY Revised May 2010*

CERTIFICATE OF COMPLIANCE -- STATE OF KENTUCKY Revised May 2010* SECTION Section 301 TOPIC DOCUMENT COMMENTS/ REFERENCE TO CRIC INTERPRETATIONS State level administration DESCRIPTION Is this requirement

CERTIFICATE OF COMPLIANCE -- STATE OF KENTUCKY Revised May 2010* SECTION Section 301 TOPIC DOCUMENT COMMENTS/ REFERENCE TO CRIC INTERPRETATIONS State level administration DESCRIPTION Is this requirement

HOW TO DOCUMENT TAX-EXEMPT SALES

GENERAL INFORMATION HOW TO DOCUMENT TAX-EXEMPT SALES This informational document is for vendors who must determine whether a customer is eligible to purchase goods without paying sales tax. In general,

GENERAL INFORMATION HOW TO DOCUMENT TAX-EXEMPT SALES This informational document is for vendors who must determine whether a customer is eligible to purchase goods without paying sales tax. In general,

Instructions for Wisconsin Sales and Use Tax Return, Form ST-12, and County Sales and Use Tax Schedule, Schedule CT

Instructions for Wisconsin Sales and Use Tax Return, Form ST-12, and County Sales and Use Tax Schedule, Schedule CT General Instructions As part of the Wisconsin Department of Revenue s (DOR) efforts to

Instructions for Wisconsin Sales and Use Tax Return, Form ST-12, and County Sales and Use Tax Schedule, Schedule CT General Instructions As part of the Wisconsin Department of Revenue s (DOR) efforts to

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54 RESALE CERTIFICATES This Bulletin is intended solely as advice to assist persons in determining, exercising

MAINE REVENUE SERVICES SALES, FUEL & SPECIAL TAX DIVISION SALES TAX INSTRUCTIONAL BULLETIN 54 RESALE CERTIFICATES This Bulletin is intended solely as advice to assist persons in determining, exercising

SALES TAX School District of Okaloosa County

I. General Provisions A. Schools do not pay sales tax on the purchase of goods and services necessary for instructional and extra-curricular activities, unless those items are purchased for resale. (See

I. General Provisions A. Schools do not pay sales tax on the purchase of goods and services necessary for instructional and extra-curricular activities, unless those items are purchased for resale. (See

Income Tax Organizer

Income Tax Organizer 1200 W. Cherry Lane, Suite 100 Meridian, ID 83642 208-888-6501 office 866-408-1836 fax 1. Personal Information Roberts Hart and Company, CPA's Income Tax Organizer Taxpayer Last Name

Income Tax Organizer 1200 W. Cherry Lane, Suite 100 Meridian, ID 83642 208-888-6501 office 866-408-1836 fax 1. Personal Information Roberts Hart and Company, CPA's Income Tax Organizer Taxpayer Last Name

Request to Participate in the Certified Audit Program

Request to Participate in the Certified Audit Program Rule 12-25.037 Florida Administrative Code Effective 01/16 1. Taxpayer ame: 2. Telephone o.: 3. FAX o.: 4. Taxpayer Mailing Address: 5. Taxpayer Business

Request to Participate in the Certified Audit Program Rule 12-25.037 Florida Administrative Code Effective 01/16 1. Taxpayer ame: 2. Telephone o.: 3. FAX o.: 4. Taxpayer Mailing Address: 5. Taxpayer Business

Laundry and Cleaning Services 120

www.revenue.state.mn.us Laundry and Cleaning Services 120 Sales Tax Fact Sheet 120 Fact Sheet What s New in 2017 We updated the fact sheet layout to make it easier to use. Laundry, dry cleaning, linen

www.revenue.state.mn.us Laundry and Cleaning Services 120 Sales Tax Fact Sheet 120 Fact Sheet What s New in 2017 We updated the fact sheet layout to make it easier to use. Laundry, dry cleaning, linen

Tax Information. for. Motor Vehicle Dealers

GT-400400 R. 07/12 Tax Information for Motor Vehicle Dealers This publication was designed to be used as a training aid. It should not be used as a reference to cite the Department s position. If legal

GT-400400 R. 07/12 Tax Information for Motor Vehicle Dealers This publication was designed to be used as a training aid. It should not be used as a reference to cite the Department s position. If legal

OPIC. Making Mail-Order and Internet Sales

New Jersey Division of Taxation TAX OPIC Making Mail-Order and Internet Sales Making Mail-Order and Internet Sales Bulletin S&U-5 Introduction If you operate a business in New Jersey that sells products

New Jersey Division of Taxation TAX OPIC Making Mail-Order and Internet Sales Making Mail-Order and Internet Sales Bulletin S&U-5 Introduction If you operate a business in New Jersey that sells products

Florida. Sales Tax Tales:

Sales Tax Tales: Objectives Registration and Account Maintenance Sales Tax Transactions Use Tax Tax Rates How to File and Pay Fact or Fiction New businesses must register at their nearest service center.

Sales Tax Tales: Objectives Registration and Account Maintenance Sales Tax Transactions Use Tax Tax Rates How to File and Pay Fact or Fiction New businesses must register at their nearest service center.

PST-38 Issued: February 1985 Revised: June 30, 2017 INFORMATION FOR NON-RESIDENT REAL PROPERTY AND SERVICE CONTRACTORS

Information Bulletin PST-38 Issued: February 1985 Revised: June 30, 2017 THE PROVINCIAL SALES TAX ACT Was this bulletin useful? Click here to complete our short READER SURVEY INFORMATION FOR NON-RESIDENT

Information Bulletin PST-38 Issued: February 1985 Revised: June 30, 2017 THE PROVINCIAL SALES TAX ACT Was this bulletin useful? Click here to complete our short READER SURVEY INFORMATION FOR NON-RESIDENT

Business Owner s Guide for Sales and Use Tax

GT-300015 R. 02/18 Business Owner s Guide for Sales and Use Tax including general information on: Communications Services Tax Corporate Income Tax Lead-Acid Battery Fee New Tire Fee Prepaid Wireless E911

GT-300015 R. 02/18 Business Owner s Guide for Sales and Use Tax including general information on: Communications Services Tax Corporate Income Tax Lead-Acid Battery Fee New Tire Fee Prepaid Wireless E911

West Virginia State Taxability Matrix

West Virginia State Taxability Matrix version 2014.3 Effective Date: August 1, 2014 Completed by: Mark W Matkovich E-mail Address: tax.commissioner@wv.gov Phone number: 304-558-0751 Date Revised:August

West Virginia State Taxability Matrix version 2014.3 Effective Date: August 1, 2014 Completed by: Mark W Matkovich E-mail Address: tax.commissioner@wv.gov Phone number: 304-558-0751 Date Revised:August

INFORMATION FOR RENTAL BUSINESSES

Ministry of Finance Revenue Division 2350 Albert Street Regina, Saskatchewan S4P 4A6 Information Bulletin PST-72 Issued: January 2014 THE PROVINCIAL SALES TAX ACT INFORMATION FOR RENTAL BUSINESSES Was

Ministry of Finance Revenue Division 2350 Albert Street Regina, Saskatchewan S4P 4A6 Information Bulletin PST-72 Issued: January 2014 THE PROVINCIAL SALES TAX ACT INFORMATION FOR RENTAL BUSINESSES Was

2017 Conversion Instructions TaxACT to ATX Individual

Updated 08/27/2017 2017 Conversion Instructions TaxACT to ATX Individual TaxACT is a registered trademark of 2nd Story Software, Inc.2nd Story Software, Inc. does not sanction nor participate in this conversion

Updated 08/27/2017 2017 Conversion Instructions TaxACT to ATX Individual TaxACT is a registered trademark of 2nd Story Software, Inc.2nd Story Software, Inc. does not sanction nor participate in this conversion

19.5 Manufacturing, Converting, Processing, Compounding, Assembling, Preparing, and Producing

280-RICR-20-70-19 TITLE 280 DEPARTMENT OF REVENUE CHAPTER 20 DIVISION OF TAXATION SUBCHAPTER 70 SALES AND USE TAX Part 19 Manufacturing, Property and Public Utilities Service Used In 19.1 Purpose This

280-RICR-20-70-19 TITLE 280 DEPARTMENT OF REVENUE CHAPTER 20 DIVISION OF TAXATION SUBCHAPTER 70 SALES AND USE TAX Part 19 Manufacturing, Property and Public Utilities Service Used In 19.1 Purpose This

Towing Services Issued May 5, 2017 Wyoming Department of Revenue

Towing Services Issued May 5, 2017 Wyoming Department of Revenue There is often confusion with regard to towing services, a towing only service versus other work performed in conjunction with the tow service.

Towing Services Issued May 5, 2017 Wyoming Department of Revenue There is often confusion with regard to towing services, a towing only service versus other work performed in conjunction with the tow service.