What You Don t Know Will Hurt You

|

|

|

- James Anthony

- 6 years ago

- Views:

Transcription

1 What You Don t Know Will Hurt You Avoiding International Tax and Estate Planning Traps STEP Silicon Valley April 19, 2017 Richard S. Kinyon, Partner, Shartsis Friese, LLP E.J. Hong, Esq., Law Offices of E.J. Hong

2 Nothing contained in this presentation is intended to be used or can be used by any taxpayer for the purpose of avoiding penalties under the Internal Revenue Code or the Revenue and Taxation Code. A taxpayer should seek advice from a qualified professional with respect to any tax transaction or matters contained in this presentation. The information provided in this presentation is not legal advice. No attorney client relationship is created as a result of this presentation. The content is intended to be a general overview of the subject matter covered and is educational and informational only. E.J. Hong, Esq., Law Offices of E.J. Hong 2

3 I. What is the client s U.S. income tax status a U.S. citizen, resident alien, or non resident alien (NRA)? II. If the client is a NRA, where is the client domiciled? III. What kinds of gratuitous transfer taxes apply to this client? IV. What are the reporting requirements for U.S. persons: e.g., income, gift, and/or estate tax returns, FBAR, FATCA, receipt of gifts, bequests and distributions from foreign trusts? V. What type of planning requires the assistance of foreign counsel? VI. How are gifts or bequests to non U.S. citizen spouses taxed? VII. What tax and estate planning should be done for NRAs whether they intend to immigrate to the U.S. or not? VIII.Who are covered expatriates and what are exit taxes? IX. What is a foreign trust and how is its income taxed? E.J. Hong, Esq., Law Offices of E.J. Hong 3

4 A Story Husband s wife died in a car accident leaving a small child. Husband s parents from a foreign country decide to help raise child, so they get green cards and move to the U.S. Parents have $30M of non U.S. situs assets. No reporting done, no world wide income tax returns filed. Exit Tax if they are covered expatriates. Exit tax covered later. Have to take active steps to give up green card. Impetus for this presentation E.J. Hong, Esq., Law Offices of E.J. Hong 4

5 International Estate Planning Society is global there are many cross border issues. o o o U.S. citizens with foreign situs assets. Resident aliens (Green Card holders) with foreign situs assets or not. Non resident aliens (NRAs) with U.S. situs assets. U.S. income tax applicable to non resident aliens (NRAs). U.S. gratuitous transfer taxes (i.e., estate, gift, and generationskipping transfer ( GST ) taxes) applicable to NRAs. The term "residence" has different meanings for immigration, income tax, and gratuitous transfer tax purposes. E.J. Hong, Esq., Law Offices of E.J. Hong 5

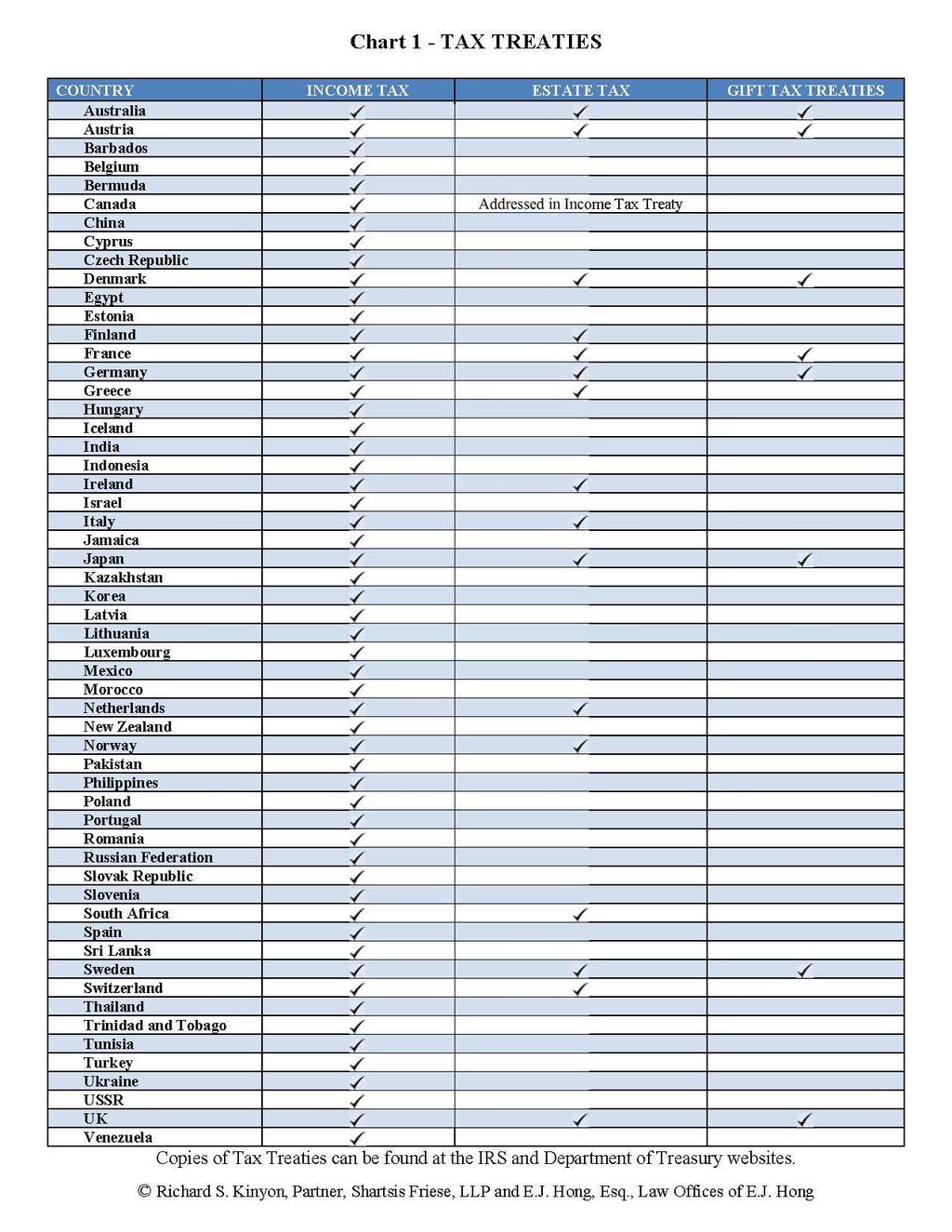

6 IRC 2100 et seq. default rules not necessarily applicable if there is a treaty. (See Chart 1 Tax Treaties) It is not necessary to know foreign laws but consider collaborating with foreign counsel or limiting scope of engagement. Reporting Requirements (applicable to trustees and executors) o FBAR has substantial criminal and civil penalties. o IRS Form 8938 (FATCA). o Other reporting requirements (listed later). Offshore Voluntary Disclosure Program (OVDP). Foreign trusts, asset protection, and fraudulent conveyances. E.J. Hong, Esq., Law Offices of E.J. Hong 6

7 7

8 An individual is a U.S. citizen if he or she is: Born in the U.S. or naturalized, or Born outside the U.S. with a U.S. parent, generally. See State Department guidance because application is very fact specific. o Even if such a child has never set foot in the U.S., upon turning 18, this child must file U.S. income tax returns and has U.S. reporting requirements, unless he or she relinquishes U.S. citizenship by age 18 ½. Dual Citizens: Even if a dual citizen has never set foot in the U.S., he or she still must file U.S. income tax returns. o Dual citizens have reporting requirements (FBAR and/or FATCA) because of their U.S. citizenship status. E.J. Hong, Esq., Law Offices of E.J. Hong 8

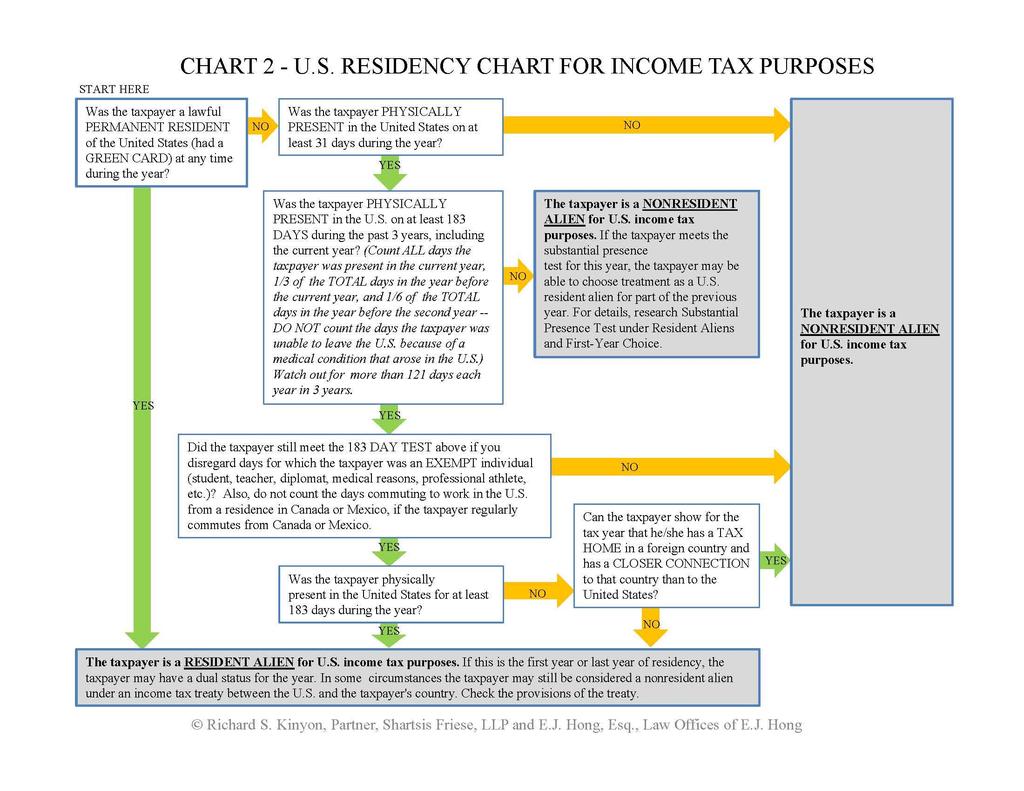

9 U.S. Resident vs. Non Resident See Chart 2 U.S. Residency Chart for Income Tax Purposes This type of analysis should always be done with a tax professional well versed in these issues. Work with an international tax lawyer or accountant. Example of substantial presence: o Physically present in the U.S. for 120 days in each of the years 2014, 2015, and o Count the full 120 days of presence in 2016, 40 days in 2015 (1/3 of 120), and 20 days in 2014 (1/6 of 120). o Total for the 3 year period is 180 days, so not considered a resident under the substantial presence test for Certain individuals are exempt from the substantial presence test (IRS Form 8843) E.J. Hong, Esq., Law Offices of E.J. Hong 9

10 10

11 A U.S. Person (U.S. citizen or resident alien) is taxed on his or her world wide income. IRC 61. o Only U.S. and Eritrea tax world wide income based on citizenship. Other countries tax world wide income based on residency. A NRA with U.S. source income must file a non resident U.S. income tax return (Form 1040NR). IRC 871. E.J. Hong, Esq., Law Offices of E.J. Hong 11

12 NRAs are subject to U.S. withholding or income tax on two types of U.S. source income: o o Fixed, Determinable, Annual or Periodic income (FDAP) flat 30% withholding tax on such income. Generally, investment (passive income) and salary. Effectively Connected Income (ECI) graduated income tax rates on income that is effectively connected with a U.S. trade or business. Reported on an annual income tax return. A NRA can elect to treat investment real property as a U.S. trade or business for purposes of getting ECI treatment rather than withholding 30%. IRC 871(d). E.J. Hong, Esq., Law Offices of E.J. Hong 12

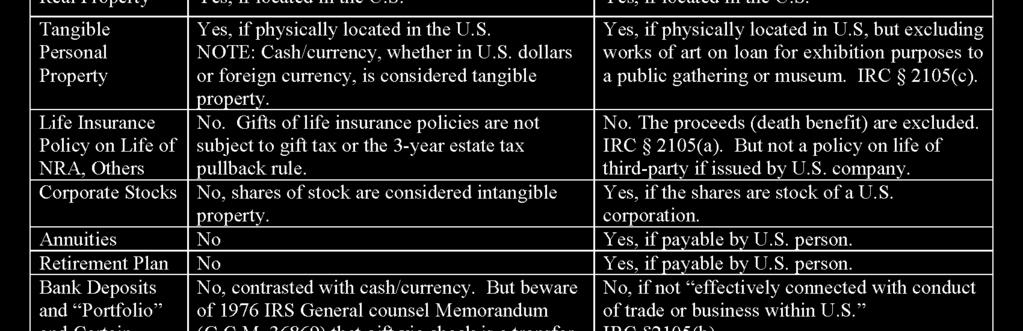

13 FDAP Exceptions to Withholding Tax However, generally, withholding and income taxes do not apply to: o o o Capital gains (stocks) Bank deposit interest Portfolio investment interest: A foreign investor can invest in qualified securities, such as corporate bonds, U.S. government securities, and municipal bonds, or receive a promissory note for a qualified loan ( portfolio debt ) and not pay income tax on the interest. See IRC 871(h), 2104(c), 2105(b)(3). See Chart 7 for example re: portfolio debt instrument. E.J. Hong, Esq., Law Offices of E.J. Hong 13

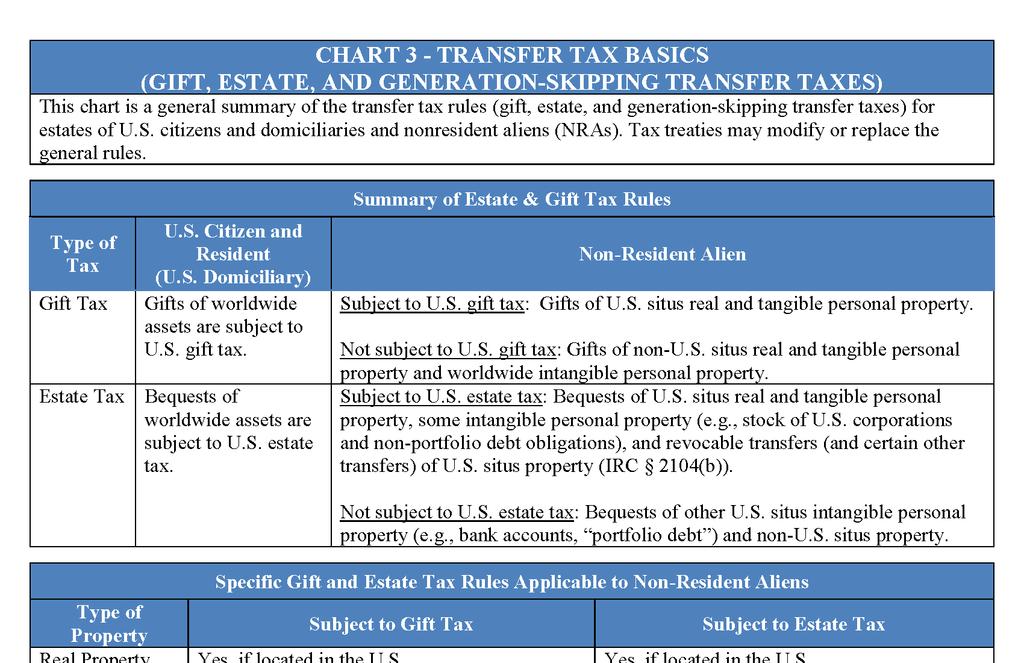

14 Residence means domicile for gratuitous transfer tax purposes. Treas. Reg. Secs (b); (b). The residency test for income tax purposes is relatively objective, but the residency test for gratuitous transfer tax purposes ( domiciliary test) is subjective. Individuals who pass the domiciliary test are U.S. residents for gratuitous transfer tax purposes and are not NRAs. IRC 2001(a) U.S. estate tax is imposed on the worldwide taxable estate of every decedent who is a U.S. citizen or resident. IRC 2501(a) U.S. gift tax is imposed on worldwide gifts by a U.S. citizen or resident. E.J. Hong, Esq., Law Offices of E.J. Hong 14

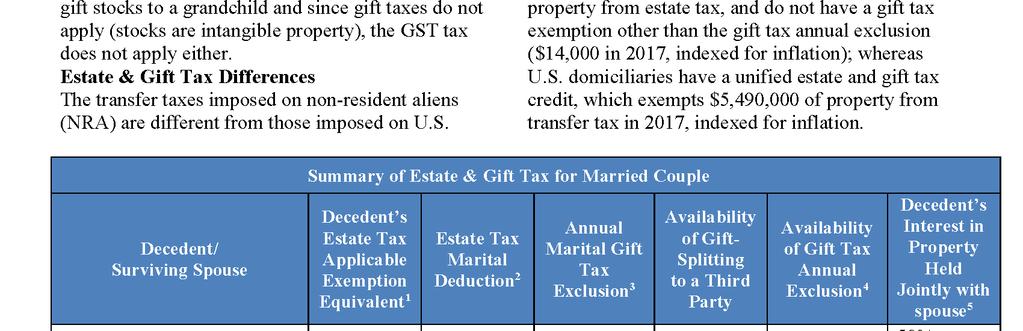

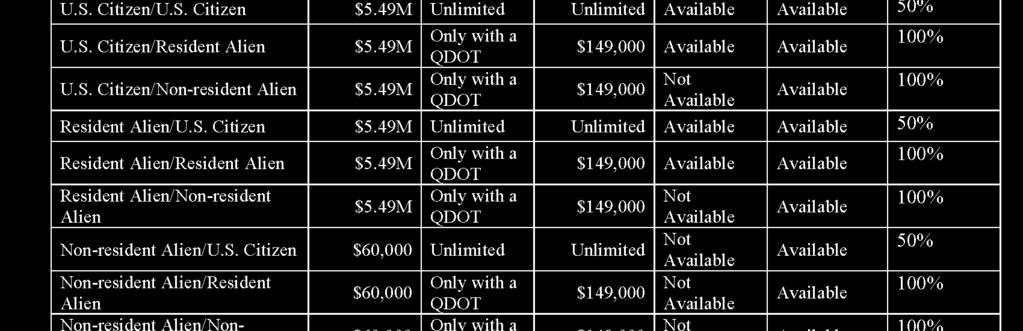

15 GST tax is imposed on direct skip taxable distributions and taxable terminations with respect to gifts and estates that are subject to U.S. estate or gift taxes. No bright line domiciliary test. Considerations include: o Intent to make the U.S. the individual s permanent home. o o o o o o o Actual presence in the U.S., at least initially. Location of his or her principal residence. Domicile of the individual s family and friends. Written or oral statements of intent are relevant. A green card creates a strong presumption of U.S. domicile. Affidavit of Domicile if intend to make U.S. permanent home. Domicile for state probate and inheritance or estate tax purposes. E.J. Hong, Esq., Law Offices of E.J. Hong 15

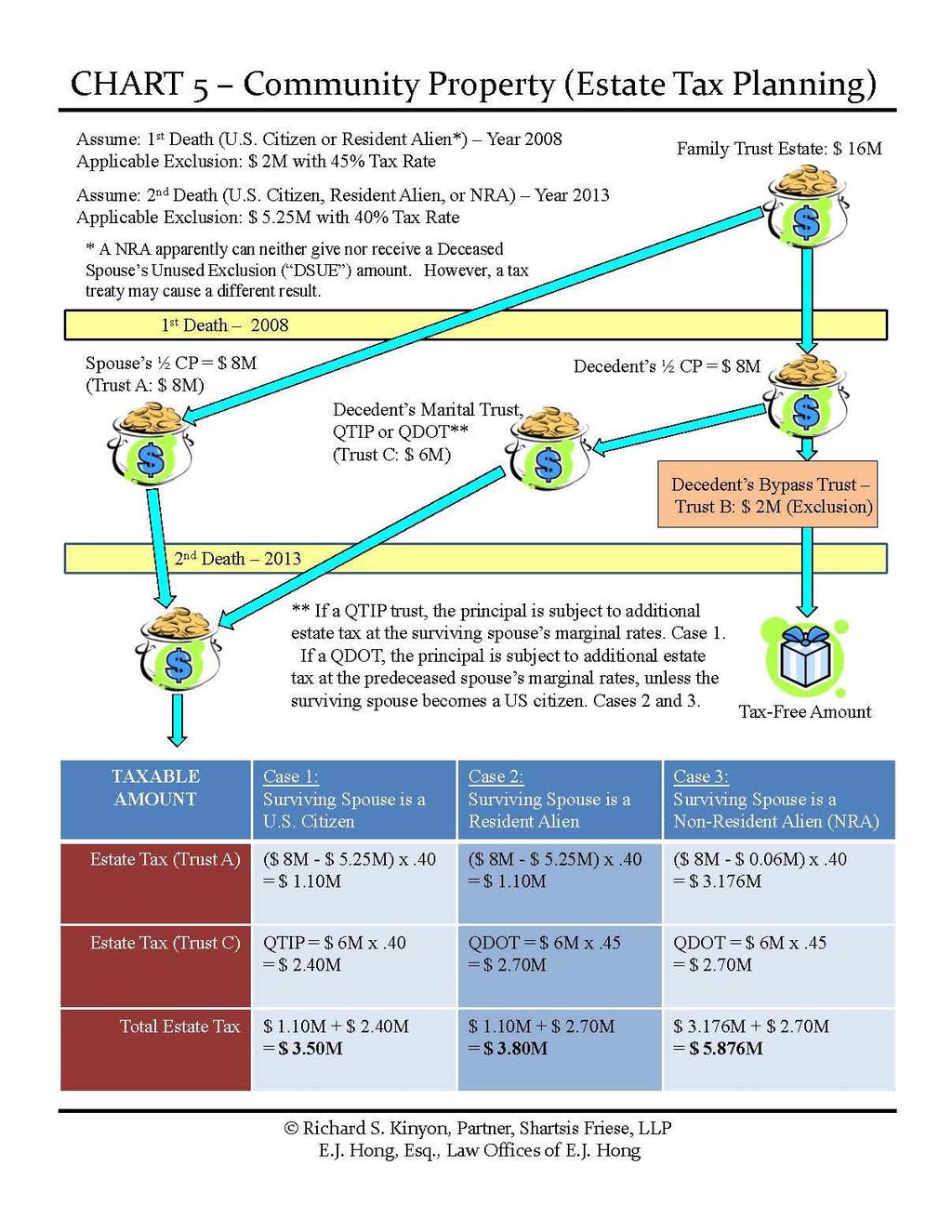

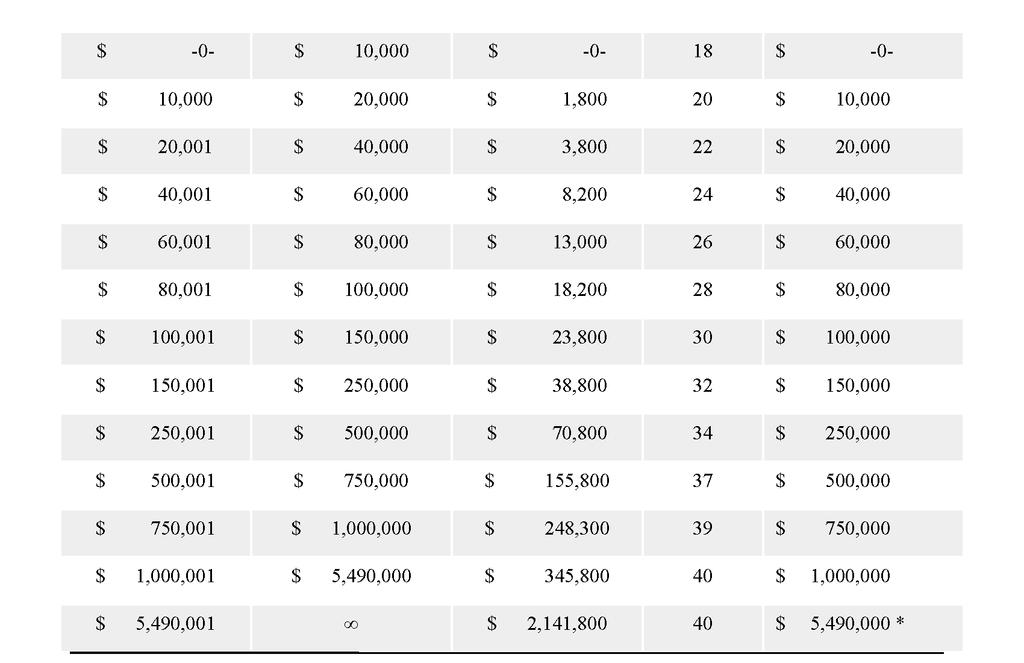

16 Transfers by U.S. Residents (Domiciliaries) Transfers of all assets (during lifetime or at death), wherever situated, are subject to gratuitous transfer taxes. Limited gift and GST tax annual exclusions ($14,000 per donee in 2017, indexed for inflation). Unlimited exclusion for direct medical/tuition payments do not count against annual exclusions and are not subject to the GST tax. Unlimited gratuitous transfer tax deductions for qualified transfers to spouses and charitable organizations. Unified gratuitous transfer tax exemptions $5,490,000 in 2017, indexed for inflation. Portability of Deceased Spousal Unused Exclusion (DSUE) (gift and estate tax, but not GST tax). E.J. Hong, Esq., Law Offices of E.J. Hong 16

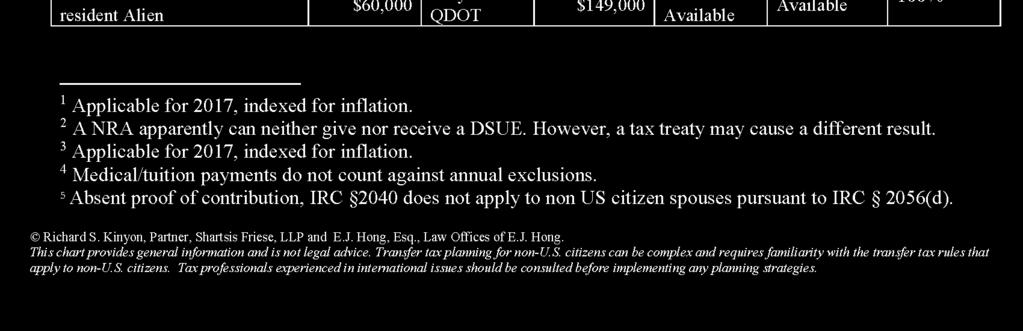

17 Transfers by NRAs Only transfers of U.S. situs assets are taxable. Limited gift and GST tax annual exclusions and unlimited exclusion for direct medical/tuition payments the same as for gifts by U.S. Citizens and Domiciliaries. Unlimited gift and estate tax deductions for qualified transfers to U.S. Citizen spouses and charitable organizations the same as for U.S. Citizens and Domiciliaries. No gift tax exemption and only a $60,000 estate tax exemption. GST exemption of 5.49M in 2017, apparently. Portability a NRA generally can neither give nor receive a Deceased Spouse s Unused Exclusion (DSUE) amount. E.J. Hong, Esq., Law Offices of E.J. Hong 17

18 18

19 19

20 A. FBAR Report of Foreign Bank and Financial Accounts FinCEN Report 114, enforcement was generally ignored until recently. See Christopher Berg and Ty Warner cases. U.S. prosecution of foreign banks (UBS/Swiss) that fail to report foreign accounts of U.S. persons. A U.S. person who has a financial interest in, or signatory authority over, a foreign account with a balance over $10,000 at any time during the year, is required to file a report. A trustee is required to file a FBAR if applicable to the trust. Penalties Civil and criminal (although most are not criminal). Three different formal IRS voluntary disclosure initiatives or programs (OVDI or OVDP) discussed later. E.J. Hong, Esq., Law Offices of E.J. Hong 20

21 B. FATCA Foreign Account Tax Compliance Act 2009 A Foreign Financial Institution (FFI) is required to provide information to the IRS for accounts held by U.S. persons. o IRS negotiating Inter Governmental Agreements with 50 countries currently to agree on information to be provided. o o Foreign trusts also may need to be FATCA compliant. If non compliant, the penalty is a 30% withholding tax on gross proceeds from the sale of U.S. securities. U.S. individuals and trusts are required to provide detailed information on Form 8938 (in addition to FBAR). o Applies to foreign accounts with a balance of $50,000 or more at any time during the year. E.J. Hong, Esq., Law Offices of E.J. Hong 21

22 C. Additional Reporting Requirements Form 3520 ( Annual Return to Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts ). Form 3520 A ( Annual Information Return of Foreign Trust With a U.S. Owner ). Form 5471 ( Information Return of U.S. Persons with Respect to Certain Foreign Corporations ). E.J. Hong, Esq., Law Offices of E.J. Hong 22

23 C. Additional Reporting Requirements Form 8865 ( Return of U.S. Persons with Respect to Certain Foreign Partnerships ). Form 8621( Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund ). Form BE 10 the U.S. Department of Commerce s Bureau of Economic Analysis requires a mandatory survey that imposes reporting requirements on U.S. persons who owned or controlled 10% or more of the voting securities of a foreign affiliate. E.J. Hong, Esq., Law Offices of E.J. Hong 23

24 D. Offshore Voluntary Disclosure Initiative (OVDI) or Program (OVDP) 27.5% penalty under this amnesty program (reduced from 50%) of highest aggregate balance in undisclosed foreign bank assets during the 8 full tax years before disclosure. Virtual assurance that the IRS will forgo criminal prosecution and will not assert other civil penalties, including FBAR penalties. If reported on tax return, but not an FBAR, may be able to just file delinquent FBARs. If the IRS commences an audit, cannot then elect OVDP. People who elect OVDP and later drop out may be able to avoid penalties, if reasonable cause for failure to comply. E.J. Hong, Esq., Law Offices of E.J. Hong 24

25 If the client holds foreign situs assets, you may need to work with local counsel in that country (e.g., forced heirship issues). The European Succession Regulation (the Regulation ), effective on August 17, 2015, was adopted by 25 countries in the European Union (but not binding on Denmark, the United Kingdom or Ireland). The Regulation provides for the application of one uniform law governing succession. The law of the jurisdiction of the decedent s habitual residence at the time of death will govern the decedent s entire estate. E.J. Hong, Esq., Law Offices of E.J. Hong 25

26 Since the U.S. is not an EU Member State, each of our states will apply its own choice of law principles to the disposition of the decedent s estate, which may conflict with those of the Member State of the decedent s last habitual residence. Choice of Law Option in some instances, the Regulation allows a person to choose the application of a different law in his or her will from the law of his or her habitual residence to govern disposition of his or her estate. The need for coordinated estate planning is critical. E.J. Hong, Esq., Law Offices of E.J. Hong 26

27 In Canada, revocable trusts are generally undesirable. Canada has no gratuitous transfer taxes, but generally, any transfer of property, even to a revocable trust, will cause a recognition of gain or loss (deemed disposition), except for transfers to a spouse or surviving spouse. Some countries, like Germany and France, generally do not recognize trusts. International Will: Uniform Law on the Form for an International Will appears in CA Probate Code Best practice, however, is to engage local counsel for tax and estate planning advice in that foreign jurisdiction and collaboration. E.J. Hong, Esq., Law Offices of E.J. Hong 27

28 No gift tax marital deduction, but $149,000 gift tax annual exclusion in 2017, indexed for inflation. Estate tax marital deduction qualified domestic trust (QDOT) see Chart 4 and Chart 5. o Net income must be payable to the surviving spouse. o Principal must not be payable to anyone other than the surviving spouse during his or her lifetime. o Incremental estate tax at the settlor s marginal rates for principal paid to the surviving spouse (subject to a hardship exemption) and upon the spouse s death. o At least one trustee must be a U.S. citizen with a tax home in the U.S. or a U.S. corporate trustee. E.J. Hong, Esq., Law Offices of E.J. Hong 28

29 If the QDOT has a value in excess of $2 million, the trustee must either be a U.S. corporate trustee, or if the trustee is a U.S. citizen, a bond must be posted with the IRS. A QDOT can be established by the surviving spouse postmortem if the deceased spouse did not establish it. However, there may be gift tax consequences if the surviving spouse transfers the property received to an irrevocable trust. To avoid making a completed gift upon a post mortem transfer to a QDOT, the surviving spouse should retain a power of revocation or appointment over the trust. E.J. Hong, Esq., Law Offices of E.J. Hong 29

30 If the QDOT is established by the surviving spouse postmortem, it will be a grantor trust for U.S. income tax purposes, and the assets also will be included in the surviving spouse s gross estate for U.S. estate tax purposes, subject to a credit for the estate tax paid with respect to the deceased spouse (IRC 2036(a)(1) and 2013). Consider the probable loss of creditor protection with respect to a QDOT established by the surviving spouse. If the surviving spouse later becomes a U.S. citizen, the QDOT principal thereafter can be distributed to the spouse free of estate tax, and the trust will be treated as a regular QTIP trust or the spouse s property. E.J. Hong, Esq., Law Offices of E.J. Hong 30

31 31

32 3732

33 Lifetime creation of a joint tenancy bank account: There is no immediate gift upon the creation of a joint tenancy bank account (or a similar type of ownership in which the contributing spouse (or any contributor for that matter) can recover the entire fund without the consent of the other joint tenant). There is a gift, however, when the non contributing joint tenant draws upon the account for his or her own benefit, to the extent of the amount withdrawn without any obligation to account for use of the amount withdrawn by the noncontributing joint tenant (although the $149,000 gift tax annual exclusion may be available). Treas. Reg (h)(4). E.J. Hong, Esq., Law Offices of E.J. Hong 33

34 Estate taxation of joint tenancy bank account at death of first joint tenant to die: The remaining balance in the account will be included in the gross estate of the contributing spouse if he or she dies first. None of the remaining balance in the account will be included in the gross estate of the non contributing U.S. citizen spouse if that spouse dies first. E.J. Hong, Esq., Law Offices of E.J. Hong 34

35 Lifetime transfer of real property into joint tenancy The lifetime transfer of real property into joint tenancy by someone with a non U.S. citizen spouse also is not subject to immediate gift tax because of Treasury Regulation (a)(2). However, a gift will occur if 1) the property is sold and the non contributing spouse receives a share of the proceeds, or 2) transfer of title is made to the non contributing spouse or into the names of the two spouses as tenants in common. Query: Would a transfer of the real property into community property with right of survivorship by someone with a non U.S. citizen spouse likewise not be subject to gift tax? E.J. Hong, Esq., Law Offices of E.J. Hong 35

36 Estate taxation of joint tenancy real property at death: If both spouses are U.S. citizens, only ½ of the value of the joint tenancy property is included in the gross estate of the first spouse to die. IRC 2040(b). If the surviving spouse is not a U.S. citizen, however, IRC 2056 (d)(1)(b) provides that Section 2040(b) does not apply, and the value of the entire property is included in the gross estate of the deceased spouse, absent proof of contribution from the surviving non U.S. citizen spouse. See page 2 of Chart 3. E.J. Hong, Esq., Law Offices of E.J. Hong 36

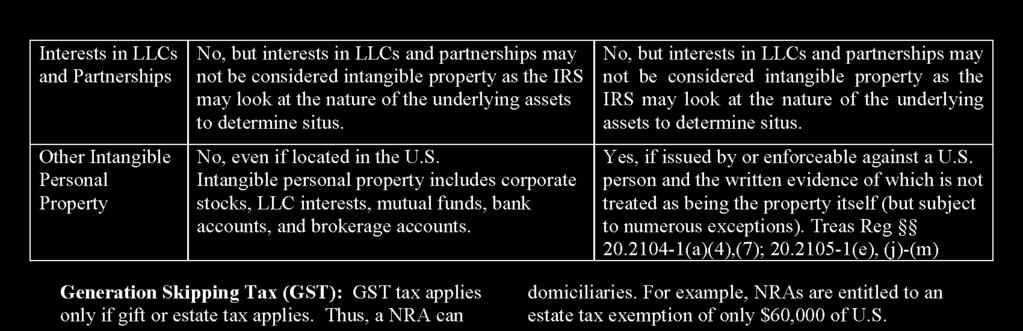

37 If a NRA owns U.S. situs real or tangible personal property through an LLC (or limited partnership) or corporation: Lifetime gifts of LLC (or limited partnership interests) or shares of corporate stock generally are not subject to U.S. gift or GST taxes because the interests or shares are intangible property. However, stock of a U.S. corporation owned by a NRA decedent is subject to U.S. estate and GST taxes without regard to the nature or situs of the assets owned by the corporation. E.J. Hong, Esq., Law Offices of E.J. Hong 37

38 Gifts or bequests of stock of a foreign corporation transferred by a NRA generally will avoid U.S. gift, estate and GST taxes even if the corporation owns U.S. situs assets. Instead of making substantial outright gifts or bequests to a U.S. citizen or resident beneficiary (e.g., a child), a NRA generally should transfer the assets to an irrevocable GST exempt dynasty trust for the benefit of the child and his or her issue. The NRA can make gifts or bequests of an unlimited amount of non U.S. situs assets to this trust, free of U.S. gift, estate, and GST taxes, and the trust assets would not be subject to future U.S. gift, estate, and GST taxes. E.J. Hong, Esq., Law Offices of E.J. Hong 38

39 However, trust income might or might not be subject to U.S. income tax, depending on whether the trust has U.S. source income, whether it is a U.S. or foreign trust, and when it was established. If the trust is a foreign trust, its undistributed net income generally will not be subject to U.S. income taxes, at least currently. But see the throwback rule (IRC ). Gifts and bequests of non U.S. situs assets received by U.S. persons (including domestic trusts) from NRA s are subject to reporting requirements but are not taxable unless the transferor is a covered expatriate. See Part VIII, below. E.J. Hong, Esq., Law Offices of E.J. Hong 39

40 A NRA planning to become a U.S. Citizen or Resident should consider giving excess non U.S. situs assets to an irrevocable GST exempt dynasty trust f/b/o his or her spouse and/or issue before becoming a U.S. citizen or resident. The beneficiaries generally should have special testamentary powers of appointment, exercisable in favor of the settlor as well as others. Note that an irrevocable foreign trust established by a NRA within 5 years before the NRA becomes a U.S. citizen or resident will be treated as a grantor trust for U.S. income tax purposes if the trust has any U.S. beneficiaries, in which case the trust s income will be taxed to the NRA after he or she becomes a U.S. person. See IRC 679(a)(4). E.J. Hong, Esq., Law Offices of E.J. Hong 40

41 Departure Planning For U.S. Citizens and Long Term Permanent Residents (HEART Act). IRC 877A, effective June 16, o Special taxes apply with respect to covered expatriates. o A covered expatriate is an individual who surrendered his or her U.S. citizenship or long term permanent resident status (a green card holder for at least 8 years during the 15 year period ending with the year of expatriation); and Had an average income tax liability above a minimum threshold ($162,000 for 2017, indexed for inflation) during each of the five previous tax years (the tax liability test ); or Has a net worth of at least $2M (the net worth test ); or Fails to certify, under penalties of perjury, compliance with all U.S. Federal tax obligations for the 5 previous tax years. E.J. Hong, Esq., Law Offices of E.J. Hong 41

42 Covered expatriates are subject to an exit tax based on a deemed sale of all of his or her assets for their fair market values as of the day before the expatriation occurred. There is an exemption for total net gain below $699,000 in 2017, indexed for inflation, and the tax is deferred with respect to eligible deferred compensation. Unless otherwise elected, the tax also is deferred on the value of the expatriate s interest in a non grantor trust, whether the trust is a domestic trust or a foreign trust. E.J. Hong, Esq., Law Offices of E.J. Hong 42

43 The trustee must withhold 30% of the gross amount of the distribution, but 877A(f)(2) appears to limit the withholding to the amount of distributable net income attributable to the distribution. See IRS Notice ( IRS 598), 7.D). The withholding requirement with regard to future distributions from a domestic trust is not limited to the amount on which the expatriate would have been taxed if the value of the expatriate s interest in the trust had been taxed at the time of expatriation. Therefore, the expatriate may want to elect to pay tax up front on the value of his or her interest in the trust, if feasible. E.J. Hong, Esq., Law Offices of E.J. Hong 43

44 There are no provisions for a foreign trust to elect to be treated the same as a U.S. trust for withholding tax purposes (in contrast with the rules on how the deferred tax on eligible deferred compensation will be paid by a non U.S. person). o Thus, there is no mechanism for the IRS to directly enforce the requirement that the expatriate must report any tax due with regard to future distributions from a foreign trust. Future U.S. taxes may be reduced if the prospective expatriate makes pre departure gifts up to his or her remaining gift tax exemption amount. Gifts of fractional and minority interests in property and closely held entities should be considered. E.J. Hong, Esq., Law Offices of E.J. Hong 44

45 Inheritance Tax: New IRC 2801(a) imposes an inheritance tax on the fair market value of gifts or bequests of property situated anywhere in the world received by a U.S. citizen or resident beneficiary from a covered expatriate. o The tax is imposed at the highest rate at which the federal estate or gift tax is imposed, presently 40%. o The amount subject to tax has no relationship to the expatriate s net worth at the time of expatriation. The new inheritance tax does not apply to property subject to U.S. gift or estate taxes shown on timely filed gift and estate tax returns, or to annual exclusion gifts that are excluded under IRC 2503(b) (and probably gifts excluded under IRC 2503(e), too). It also does not apply to qualifying transfers to a spouse or charitable organization. E.J. Hong, Esq., Law Offices of E.J. Hong 45

46 The new inheritance tax also is imposed on a gift or bequest by an expatriate to a domestic trust. A gift or bequest to a foreign trust is deferred until distribution is made from the trust to the U.S. citizen or resident beneficiary, and an income tax deduction is allowed under IRS 164 for the 2801 tax attributable to the portion of the distribution included in gross income. A foreign trust may elect to be treated as a domestic trust for this purpose. Section 2801(d) provides for a reverse foreign tax credit equal to the amount of any gift or estate tax imposed on the gift or bequest by any foreign country. However, the beneficiary cannot claim the benefit of a reduction or elimination of the tax under an estate or gift tax treaty, because no existing treaty applies to inheritance type taxes imposed on a U.S. transferee. E.J. Hong, Esq., Law Offices of E.J. Hong 46

47 Definition: A trust is a domestic (U.S.) trust if: o A U.S. court is able to exercise primary supervision over the administration of the trust (the court test ); and o One or more U.S. persons have the authority to control all substantial decisions of the trust (the control test ). A trust must meet both the court test and control test to be a U.S. domestic trust. Any other trust is a foreign trust. U.S. person includes a citizen or resident of the United States, a domestic partnership, and a domestic corporation. IRC 7701(a)(30). o Contrasted with an individual trustee of a QDOT who must be a U.S. citizen with a U.S. tax home. E.J. Hong, Esq., Law Offices of E.J. Hong 47

48 The undistributed net income (UNI) of a foreign trust is not currently subject to U.S. (or state) income taxes, but it is subject to the throwback rules of IRC 665 through 668. If little or no UNI is likely to be distributed to a U.S. beneficiary, a foreign trust may be preferable, at least from an income tax perspective. Otherwise, a domestic (U.S.) trust may be preferable. California has somewhat similar throwback rules relating to the income taxation of a foreign or domestic trust s UNI if not all of the fiduciaries are California residents and not all of the beneficiaries interests in the trust are noncontingent (vested). E.J. Hong, Esq., Law Offices of E.J. Hong 48

49 Examples of failing the control test, making a U.S. trust a foreign trust: o o o If a NRA acts as trustee of a U.S. trust. If a NRA is co trustee of a U.S. trust in which all co trustees have to act unanimously. Unless the trust provides otherwise, CA Probate Code requires co trustees to act unanimously. If a NRA trust protector has the power to remove and replace the trustee, Treas. Reg provides that this is a substantial decision (but the ability to appoint a U.S. trustee in case of vacancy is not a substantial decision ). E.J. Hong, Esq., Law Offices of E.J. Hong 49

50 Examples of failing the court test, making a U.S. trust a foreign trust: o o If both U.S. and foreign courts are able to exercise primary supervision over the administration of the trust, the court test is satisfied. If there is an automatic migration provision (trust automatically migrates if a certain condition happens), the court test fails. E.J. Hong, Esq., Law Offices of E.J. Hong 50

51 Consequences where the trust has a Canadian trustee with a U.S. beneficiary: o Gain recognition when appreciated property is contributed to a foreign trust, all gain is recognized but not loss, even if property is not sold. o Every 21 years, deemed disposition. o Withholding usually 30% unless treaty, ECI or exception. o Reporting Obligations: IRS 3520 (Report of Foreign Trust) IRS 3520A if create grantor trust Penalty is percentage of assets in the trust greater of $10,000 or 5% of trust corpus FBAR FATCA penalty is 30% withholding tax E.J. Hong, Esq., Law Offices of E.J. Hong 51

52 What to do? o o o o If revocable, amend the trust. If irrevocable, modify the trust. One year grace period if the trust fails the control test (no grace period if it fails the court test). Consider reformation of the trust retroactive to the date the trust was established. Bosch IRS does not have to respect state court order, and reformation has not been tested in this specific context, although reformations are approved by the IRS regularly. E.J. Hong, Esq., Law Offices of E.J. Hong 52

53 #1. A NRA is a Beneficiary of a U.S. Trust or Estate IRC 1441, 1442, and 1443 govern NRA withholding (See Publication 515). FDAP received by a U.S. estate or trust and distributed to a NRA beneficiary other than a qualifying foreign organization is subject to U.S. withholding tax of 30%. Definition of withholding agent a person that has control, receipt, custody, disposal, or payment of any item of income of a foreign person. Trustees and executors are included. Withholding agents are personally liable for any tax required to be withheld. To determine whether a treaty or other exception applies for withholding, work with knowledgeable tax lawyer or accountant. E.J. Hong, Esq., Law Offices of E.J. Hong 53

54 #2. A NRA parent owns real estate in CA, $1M value. Only has $60,000 estate tax exemption. No gift tax exemption. Only $14,000 gift tax annual exclusion and would have to pay gift tax if the gift is over this amount. U.S. Citizen child is the beneficiary. Parent sells the property to child. Capital gains may have to be paid (installment or all at once). Parent child exclusion from reassessment of property taxes. Child gives parent a promissory note which meets the requirement for portfolio debt (see Chart 7). Income from the note is not taxable, and the promissory note is not included in the parent s gross estate because it is portfolio debt. E.J. Hong, Esq., Law Offices of E.J. Hong 54

55 #3. Temporary Executive Executive is here on visa. He has $2M in stock shares and options, $1M home. His wife is a citizen of a foreign country and a U.S. Permanent resident. They have 2 children who will be raised here. Intends to live in U.S. indefinitely. Needs to show that he is U.S. domiciliary and completes an Affidavit of Domicile. Note that a person who has no foreign domicile may very well be a U.S. domiciliary. E.J. Hong, Esq., Law Offices of E.J. Hong 55

56 #4. A NRA has $12M in brokerage account Corporate stocks are intangible property. Can gift without U.S. gift tax consequences. If the NRA dies and the account contains U.S. corporate stock, the stock will be subject to U.S. estate tax with only a $60,000 exemption. Create an irrevocable, GST exempt trust for children and gift stock to this trust. Because the gift is not subject to U.S. gift tax, it is not subject to GST tax either. E.J. Hong, Esq., Law Offices of E.J. Hong 56

57 #5. Probate of a NRA s bank account $300,000 No will. All family members (heirs) are NRAs. Non resident of CA cannot serve as personal representative if not named in a will. PC 8465 allows non resident heirs to nominate a personal representative. $60,000 estate tax exemption but bank accounts not included in the gross estate of a NRA, if the bank account is not effectively connected to a U.S. trade or business. E.J. Hong, Esq., Law Offices of E.J. Hong 57

58 #6. Revocable trusts and BVI corp for a NRA A NRA father with foreign and U.S. situs assets has 3 U.S. citizen sons. Father creates 3 separate revocable trusts foreign grantor trusts of which the sons are trustees and primary beneficiaries. The separate revocable trust for each child owns all the shares of a BVI corporation which is used to hold any U.S. situs assets. Cash is distributed to the son s foreign bank accounts. When father dies, trusts become irrevocable dynasty type trusts. BVI corporation then becomes a foreign personal holding company (FPHC), so it should be liquidated within 30 days to avoid adverse income tax consequences. E.J. Hong, Esq., Law Offices of E.J. Hong 58

59 #7. Family Investment Company for U.S. Domiciliary Wealthy settlor has investment assets (stocks, bonds, real estate, etc.). Consolidate most, if not all, of those assets into one or more investment entities (LLC). Required annual distributions of hypothetical trust net income and trust tax liability. Substantial valuation discounts for transfers of minority interests in the LLC. Transfers of interests are subject to buy sell agreement (right of first refusal). Annual appraisals and annual accountings. Keeps family working together. E.J. Hong, Esq., Law Offices of E.J. Hong 59

60 60

61 61

62 61

63 62

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

What Every Domestic Estate Planning Attorney Should Know About International Estate Planning October 21, 2015 Todd Angkatavanich, Esq., Withers Bergman LLP (Connecticut) Richard Cassell, Esq., Withers

I. Basic Rules. Planning for the Non- Citizen Spouse: Tips and Traps 2/25/2016. Zena M. Tamler. March 11, 2016 New York, New York

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

Planning for the Non- Citizen Spouse: Tips and Traps Zena M. Tamler March 11, 2016 New York, New York Attorney Advertising Prior results do not guarantee a similar outcome. Copyright 2016 2015 Sullivan

International Trade and/or Investment Affords Opportunities

Overview of International Estate Planning Issues Affecting U.S. Persons or Non-U.S. Persons with U.S. Sitused Assets 2010 Advanced Tax Institute November 3, 2010 Baltimore, Maryland Elizabeth M. Schurig

Overview of International Estate Planning Issues Affecting U.S. Persons or Non-U.S. Persons with U.S. Sitused Assets 2010 Advanced Tax Institute November 3, 2010 Baltimore, Maryland Elizabeth M. Schurig

Estate Planning for Foreign Nationals

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Estate Planning for Foreign Nationals What Financial Professionals Need to Know www.mcnulty-law.com Tel. (212) 431-7526 What We ll Be Covering Non-Tax Estate Planning Issues US Estate Taxation of US citizens

Estate & Gift Tax Treatment for Non-Citizens

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens BECAUSE YOU ASKED It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the

Looking Beyond Our Borders:

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Looking Beyond Our Borders: U.S. Income, Estate, and Gift Tax Implications 2017 Advanced Estate Planning Conference MGM Grand Las Vegas June 13, 2017 Peggy A. Ugent, CPA 100 CONGRESS AVENUE, SUITE 1440

Estate Planning Council of Toronto: Estate Tax Update

www.pwc.com/ca Estate Planning Council of Toronto: Ian Macdonald November 5, 2013 Agenda US Estate and Gift Tax Update 1. New Rules 2. Implications for US Citizens Living in Canada 3. Implications for

www.pwc.com/ca Estate Planning Council of Toronto: Ian Macdonald November 5, 2013 Agenda US Estate and Gift Tax Update 1. New Rules 2. Implications for US Citizens Living in Canada 3. Implications for

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons Matthew R. Hillery, Director September 27, 2016 Speaker Matthew R. Hillery Director in the Private Client Department. Concentrates

Meritas Capability Webinar U.S. Tax and Estate Planning for Foreign Persons Matthew R. Hillery, Director September 27, 2016 Speaker Matthew R. Hillery Director in the Private Client Department. Concentrates

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

(b) TAX BENEFITS OF A HYBRID TRUST. The following are some US Federal Tax benefits of a Hybrid Grantor Trust.

TAX BENEFITS OF A HYBRID TRUST. The following are some US Federal Tax benefits of a Hybrid Grantor Trust.") NON RESIDENT ALIENS OF THE UNITED STATES AND HYBRID GRANTOR TRUSTS Last Updated: May 19, 2014 Article by Milagros Gomez Munoz of Milagros Gomez Munoz, P.A. I. HYBRID GRANTOR TRUSTS. (a) WHAT IS A HYBRID

NON RESIDENT ALIENS OF THE UNITED STATES AND HYBRID GRANTOR TRUSTS Last Updated: May 19, 2014 Article by Milagros Gomez Munoz of Milagros Gomez Munoz, P.A. I. HYBRID GRANTOR TRUSTS. (a) WHAT IS A HYBRID

PRESENTATION FOR VAELA

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

ESTATE PLANNING ISSUES SPECIFIC TO NON-U.S. CITIZENS PRESENTATION FOR VAELA BY YAHNE MIORINI, ESQ. Miorini Law PLLC 1816 Opalocka Drive McLean, VA 22101 www.miorinilaw.com (703) 448-6121 Yahne.miorini@miorinilaw.com

RBC Wealth Management Services

RBC Wealth Management Services The Navigator C HARLES W. C ULLEN III CFP(Canada and U.S.),CIM Associate Portfolio Manager & Wealth Advisor 902-424-1092 charles.cullen@rbc.com D AYNA P ARK Associate 902-421-0244

RBC Wealth Management Services The Navigator C HARLES W. C ULLEN III CFP(Canada and U.S.),CIM Associate Portfolio Manager & Wealth Advisor 902-424-1092 charles.cullen@rbc.com D AYNA P ARK Associate 902-421-0244

TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

`` TAX CONSEQUENCES FOR U.S. CITIZENS AND OTHER U.S. PERSONS LIVING IN CANADA Over the past few years, there has been increased media attention in Canada with respect to the U.S. income tax filing requirements

STILL THINKING OF COMING TO AMERICA? ADVISING THE FOREIGN PRIVATE CLIENT ON FUNDAMENTALS OF U.S. ESTATE, GIFT AND GST TAX PLANNING

STILL THINKING OF COMING TO AMERICA? ADVISING THE FOREIGN PRIVATE CLIENT ON FUNDAMENTALS OF U.S. ESTATE, GIFT AND GST TAX PLANNING By M. Katharine Davidson, Esq. Henderson, Caverly, Pum & Charney, LLP

STILL THINKING OF COMING TO AMERICA? ADVISING THE FOREIGN PRIVATE CLIENT ON FUNDAMENTALS OF U.S. ESTATE, GIFT AND GST TAX PLANNING By M. Katharine Davidson, Esq. Henderson, Caverly, Pum & Charney, LLP

Federal Estate, Gift and GST Taxes

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

Federal Estate, Gift and GST Taxes 2018 Estate Law Institute November 2, 2018 Bradley D. Terebelo, Esquire Peter E. Moshang, Esquire Heckscher, Teillon, Terrill & Sager, P.C. 100 Four Falls, Suite 300

"US recipients of gifts and bequests from Covered Expatriates will now incur gift and estate tax"

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Steve Leimberg's Estate Planning Email Newsletter - Archive Message #1324 Date: 23-Jul-08 From: Steve Leimberg's Estate Planning Newsletter Subject: HEART Legislation Enacts New Expatriation Rules "US

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Dean C. Berry, Partner, Cadwalader Wickersham & Taft, New York

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Presenting a live 90-minute webinar with interactive Q&A Estate Planning Involving Resident and Non-Resident Aliens Navigating Estate, Gift and GST Tax Rules; Leveraging Estate and Lifetime Gifting Opportunities

Private Company Services. U.S. Estate and Gift taxation of resident aliens and nonresident aliens

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

Private Company Services U.S. Estate and Gift taxation of resident aliens and nonresident aliens 2010 2012 Non-U.S. citizens, both resident and nonresident aliens, may be subject to U.S. estate and gift

Non-Citizen Spouse. Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs)

and Irrevocable Life Insurance Trusts (ILITs)") Guiding you through life. SALES STRATEGY NEEDS ANALYSIS Non-Citizen Spouse Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs) As large numbers of people

Guiding you through life. SALES STRATEGY NEEDS ANALYSIS Non-Citizen Spouse Estate Planning Using Qualified Domestic Trusts (QDOTs) and Irrevocable Life Insurance Trusts (ILITs) As large numbers of people

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset.

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

What is a disclaimer? A disclaimer is an irrevocable statement that the beneficiary/recipient of an asset does not wish to receive the asset. The disclaimed asset passes as if the disclaimant had predeceased

Estate Planning for the Multinational Family. Steven L. Cantor Cantor & Webb P.A., October 15, 2015

Estate Planning for the Multinational Family Steven L. Cantor Cantor & Webb P.A., October 15, 2015 Introduction U.S. Tax Issues Discussion Points Planning Issues and Strategies U.S. Reporting Requirements

Estate Planning for the Multinational Family Steven L. Cantor Cantor & Webb P.A., October 15, 2015 Introduction U.S. Tax Issues Discussion Points Planning Issues and Strategies U.S. Reporting Requirements

QDOT-ting I's and Crossing T's: Estate Tax Planning for Non-United States Citizen Spouses

QDOT-ting I's and Crossing T's: Estate Tax Planning for Non-United States Citizen Spouses Written By John R. Cella, Jr. (jrcella@wardandsmith.com) April 17, 2017 Individual and corporate citizens from

QDOT-ting I's and Crossing T's: Estate Tax Planning for Non-United States Citizen Spouses Written By John R. Cella, Jr. (jrcella@wardandsmith.com) April 17, 2017 Individual and corporate citizens from

Tax Guide For Foreign Investors In U.S. Residential Real Estate

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

A T T O R N E Y S A T L A W Tax Guide For Foreign Investors In U.S. Residential Real Estate 2018 Edition In this guide I. Introduction 2 II. The U.S. Tax System 3 A. U.S. Persons 3 1. Basic Rules 3 2.

Top 10 Tax Issues facing U.S. Citizens living in Canada

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

Top 10 Tax Issues facing U.S. Citizens living in Canada An individual may be considered a U.S. citizen if he or she: was born in the U.S.; successfully applied to become a naturalized citizen of the U.S.;

Private Wealth Services

Private Wealth Services Winter 2007 Volume 5, Issue 3 Estate Planning for the International Private Client Melinda Merk The laws governing estate plans of nonresident aliens and non-citizens of the United

Private Wealth Services Winter 2007 Volume 5, Issue 3 Estate Planning for the International Private Client Melinda Merk The laws governing estate plans of nonresident aliens and non-citizens of the United

An Introduction to the US Estate and Gift Tax Regime

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

An Introduction to the US Estate and Gift Tax Regime DAVID G. ROBERTS www.crossborder.com CTF Edmonton Young Practitioners Group September 2012 Issues Who is a US person? US transfer taxes Common estate

PREPARING GIFT TAX RETURNS

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

PREPARING GIFT TAX RETURNS I. Overview A sample 2014 gift tax return illustrating several different types of gifts is attached at Tab A. The instructions for the 2014 gift tax return can be found at Tab

Advisory. Will and estate planning considerations for Canadians with U.S. connections

Advisory Will and estate planning considerations for Canadians with U.S. connections Canadian citizens and residents may be exposed to U.S. estate, gift, and generation-skipping transfer tax (together,

Advisory Will and estate planning considerations for Canadians with U.S. connections Canadian citizens and residents may be exposed to U.S. estate, gift, and generation-skipping transfer tax (together,

A Guide to Estate Planning

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON, DC www.daypitney.com A Guide to Estate Planning THE IMPORTANCE OF ESTATE PLANNING The goal of estate planning is to direct the transfer and management

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

12. Canadians who are also U.S. citizens and considering renouncing such citizenship - Some U.S. tax implications By Simon Sturm Under U.S. tax laws an individual who is either a U.S. citizen or a U.S.

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

Generation-Skipping Transfer Tax: Planning Considerations for 2018 and Beyond The Florida Bar Real Property Probate and Trust Law Section 2018 Wills, Trusts & Estates Certification and Practice Review

9/20/2017. USA the dream destination. EB5 visa allows dream to be a reality. Tax regulations in USA affecting NRIs Resident Indians

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USA affecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA the dream destination USA has always been and will be a dream destination Getting a job Sending

ABA RPTE 2016 Spring Symposia Boston, MA

Hot Topics: Foreign versus Domestic Trusts, US Trusts for Foreign Families, Migration of Trusts, FATCA Requirements, Investment in US Real Estate, and FIRPTA ABA RPTE 2016 Spring Symposia Boston, MA Brian

Hot Topics: Foreign versus Domestic Trusts, US Trusts for Foreign Families, Migration of Trusts, FATCA Requirements, Investment in US Real Estate, and FIRPTA ABA RPTE 2016 Spring Symposia Boston, MA Brian

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015 Danielle R. Greene Loring, Wolcott & Coolidge Trust,

Estate, Gift and GST Tax Basics for the New Estate Planner Boston Bar Association Trusts & Estates Practice Fundamentals Committee November 4, 2015 Danielle R. Greene Loring, Wolcott & Coolidge Trust,

Mark A. Feigenbaum U.S. Attorney at Law Certified Public Accountant (U.S.) Chartered Accountant (Canada)

Chartered Accountant (Canada)") Mark A. Feigenbaum U.S. Attorney at Law Certified Public Accountant (U.S.) Chartered Accountant (Canada) 1137 Centre Street, Suite 201 Thornhill, ON L4J 3M6 905-695-1269 mark@feigenbaumlaw.com http://www.feigenbaumlaw.com

Mark A. Feigenbaum U.S. Attorney at Law Certified Public Accountant (U.S.) Chartered Accountant (Canada) 1137 Centre Street, Suite 201 Thornhill, ON L4J 3M6 905-695-1269 mark@feigenbaumlaw.com http://www.feigenbaumlaw.com

Filing Requirements U.S. citizens residing in Canada must file both Canadian and U.S. income tax returns every year.

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

RBC Wealth Management Services The Navigator Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

Tax Planning for U.S. Citizen Residents in Canada. Maximize your wealth by utilizing tax planning ideas and understanding the tax issues

The Navigator RBC WEALTH MANAGEMENT SERVICES Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

The Navigator RBC WEALTH MANAGEMENT SERVICES Tax Planning for U.S. Citizen Residents in Canada Maximize your wealth by utilizing tax planning ideas and understanding the tax issues The United States is

ALI-ABA Course of Study Estate Planning for the Family Business Owner. July 11-13, 2007 San Francisco, California

1041 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Probate and Trust Law and the ABA Section of Taxation July 11-13, 2007 San Francisco,

1041 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Probate and Trust Law and the ABA Section of Taxation July 11-13, 2007 San Francisco,

Introduction: recent trends... CROSS BORDER ESTATE PLANNING. Advocis Breakfast Meeting. Are you American? Is your child? Who should consider U.S. tax?

Introduction: recent trends.... CROSS BORDER ESTATE PLANNING Advocis Breakfast Meeting Will Todd Taxation / Wills, Estates & Trusts Practice Group April 4, 2013... Why pay attention now. More Canadian

Introduction: recent trends.... CROSS BORDER ESTATE PLANNING Advocis Breakfast Meeting Will Todd Taxation / Wills, Estates & Trusts Practice Group April 4, 2013... Why pay attention now. More Canadian

TAX CONSEQUENCES OF U.S. INVESTMENTS FOR NON-U.S. CITIZENS

TAX CONSEQUENCES OF U.S. INVESTMENTS FOR NON-U.S. CITIZENS WHAT A GLOBAL FAMILY NEEDS TO KNOW If you are not a United States ( U.S. ) citizen (or a U.S. resident/ domiciliary) and are considering an investment

TAX CONSEQUENCES OF U.S. INVESTMENTS FOR NON-U.S. CITIZENS WHAT A GLOBAL FAMILY NEEDS TO KNOW If you are not a United States ( U.S. ) citizen (or a U.S. resident/ domiciliary) and are considering an investment

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory. Outline. G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory Outline G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON,

U.S. Tax Planning for Non-U.S. Persons, Assets and Trusts An Introductory Outline G. Warren Whitaker Dina Kapur Sanna Day Pitney LLP, New York, NY BOSTON CONNECTICUT FLORIDA NEW JERSEY NEW YORK WASHINGTON,

ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2008 San Francisco, California

1203 ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2008 San Francisco, California Postmortem Planning Considerations for the Family Business Owner: A Review of Income, Gift,

1203 ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2008 San Francisco, California Postmortem Planning Considerations for the Family Business Owner: A Review of Income, Gift,

Arthur Winter Winter & Melbinger, LLP

Arthur Winter Winter & Melbinger, LLP Arthur ( Art ) Winter is a principal of Winter & Melbinger, LLP of Evanston, Illinois, he received his J.D. degree from the University of California, Berkeley (Boalt

Arthur Winter Winter & Melbinger, LLP Arthur ( Art ) Winter is a principal of Winter & Melbinger, LLP of Evanston, Illinois, he received his J.D. degree from the University of California, Berkeley (Boalt

Link Between Gift and Estate Taxes

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

Link Between Gift and Estate Taxes Each is necessary to enforce the other The taxes are assessed at essentially the same rates Though, the gift tax is measured exclusively while the estate tax is measured

D'Amico Family Wealth Management Group Of RBC Dominion Securities

D'Amico Family Wealth Management Group Of RBC Dominion Securities Presents David Altro from Altro Levy, Lawyers "Cross Border Tax & Estate Planning for Canadians with U.S. Real Estate" Angelo D Amico FCSI,

D'Amico Family Wealth Management Group Of RBC Dominion Securities Presents David Altro from Altro Levy, Lawyers "Cross Border Tax & Estate Planning for Canadians with U.S. Real Estate" Angelo D Amico FCSI,

ESTATE EVALUATION. John and Jane Doe

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

ESTATE EVALUATION John and Jane Doe Adam Advisor Investment Advisors 265 Anystreet Suite 123 AnyCity, AnyState, AnyZip (555) 555-5555 adam@investmentadvisors.inv Important Notes Estate Evaluation is a

ESTATE AND GIFT TAXATION

H Chapter Fourteen H ESTATE AND GIFT TAXATION INTRODUCTION AND STUDY OBJECTIVES Estate taxes are imposed on transfers of property by decedents, and gift taxes are imposed on the transfers by living individual

H Chapter Fourteen H ESTATE AND GIFT TAXATION INTRODUCTION AND STUDY OBJECTIVES Estate taxes are imposed on transfers of property by decedents, and gift taxes are imposed on the transfers by living individual

Tax & Estate Planning for Snowbirds

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

Tax & Estate Planning for Snowbirds Amin Mawani Schulich School of Business York University amawani@schulich.yorku.ca Taxes do influence behaviour Windowless Castles Narrow frontages SIN & gasoline taxes

KEVIN MATZ & ASSOCIATES PLLC. U.S. Estate and Gift Taxation of Nonresident Aliens

KEVIN MATZ & ASSOCIATES PLLC An abridged version of this article was published in the April 2012 issue of CPA Journal. U.S. Estate and Gift Taxation of Nonresident Aliens Kevin Matz, Esq., C.P.A., LL.M.

KEVIN MATZ & ASSOCIATES PLLC An abridged version of this article was published in the April 2012 issue of CPA Journal. U.S. Estate and Gift Taxation of Nonresident Aliens Kevin Matz, Esq., C.P.A., LL.M.

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

HOPKINS & CARLEY GUIDE TO BASIC ESTATE PLANNING TECHNIQUES FOR 2017 PART I: REVOCABLE TRUST vs. WILL A. Introduction In general, an estate plan can be implemented either by the use of wills or by the use

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation 5 December 2016; 1 November 2017; 1 December 2017; 18 January 2018; 19 April 2018 INTRODUCTION This side-by-side analysis

ESTATE PLANNING 101:

Introduction ESTATE PLANNING 101: THE IMPORTANCE OF DEVELOPING AN ESTATE PLAN At some point, most people will contemplate estate planning. Often, this is prior to or shortly after a significant life event,

Introduction ESTATE PLANNING 101: THE IMPORTANCE OF DEVELOPING AN ESTATE PLAN At some point, most people will contemplate estate planning. Often, this is prior to or shortly after a significant life event,

American Citizens Abroad. Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

1 November 2017; 1 December 2017; 19 January 2018 American Citizens Abroad Side-By-Side Analysis: Current Law; Residency-Based Taxation INTRODUCTION This side-by-side analysis compares Current Law (i.e.,

Identifying and Solving Problems in the Taxation of Non-Resident Aliens. Presented to New York Step Conference. March 10, New York, New York

Identifying and Solving Problems in the Taxation of Non-Resident Aliens Presented to New York Step Conference March 10, 2016 New York, New York By Leigh-Alexandra Basha, Partner/Private Client Group McDermott

Identifying and Solving Problems in the Taxation of Non-Resident Aliens Presented to New York Step Conference March 10, 2016 New York, New York By Leigh-Alexandra Basha, Partner/Private Client Group McDermott

MARITAL DEDUCTION TRUSTS

One Commerce Plaza Albany, New York 12260 P 518.487.7600 F 518.487.7777 www.woh.com QTIPS Unlimited Marital Deduction IRC 2056(a) Estate taxes are not imposed on any assets passing to a surviving spouse

One Commerce Plaza Albany, New York 12260 P 518.487.7600 F 518.487.7777 www.woh.com QTIPS Unlimited Marital Deduction IRC 2056(a) Estate taxes are not imposed on any assets passing to a surviving spouse

NRIs Resident Indians. By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR

Tax regulations in USAaffecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA thedream destination USA has always been and will be a dream destination Getting a job Sending

Tax regulations in USAaffecting NRIs Resident Indians By SANKET SHAH CO-FOUNDER AND MANAGING DIRECTOR USA thedream destination USA has always been and will be a dream destination Getting a job Sending

29th Annual Elder Law Institute

TAX LAW AND ESTATE PLANNING SERIES Tax Law and Practice Course Handbook Series Number D-489 29th Annual Elder Law Institute Co-Chairs Jeffrey G. Abrandt Douglas J. Chu To order this book, call (800) 260-4PLI

TAX LAW AND ESTATE PLANNING SERIES Tax Law and Practice Course Handbook Series Number D-489 29th Annual Elder Law Institute Co-Chairs Jeffrey G. Abrandt Douglas J. Chu To order this book, call (800) 260-4PLI

T he relatively strong U.S. economy continues to attract

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

Daily Tax Report Reproduced with permission from Daily Tax Report, 243 DTR J-1, 12/18/15. Copyright 2015 by The Bureau of National Affairs, Inc. (800-372-1033) http://www.bna.com Foreign Taxpayers Jenny

A comparison of the Form filing requirements and the Form 8938 filing requirements follows:

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

This week Mark Jennings, Assistant Vice President of Investments, at LOM Securities (Bermuda) Ltd. hosted a conference on International Taxes and Trusts for US Citizens Living in Bermuda and US Beneficiaries

SELECTED ISSUES FOR CANADIANS HOLDING AND

SELECTED ISSUES FOR CANADIANS HOLDING AND DISPOSING OF U.S VACATION PROPERTY Carol Fitzsimmons Hodgson Russ LLP Buffalo Philip Friedlan Friedlan Law Richmond Hill Adam Friedlan Friedlan Law Richmond Hill

SELECTED ISSUES FOR CANADIANS HOLDING AND DISPOSING OF U.S VACATION PROPERTY Carol Fitzsimmons Hodgson Russ LLP Buffalo Philip Friedlan Friedlan Law Richmond Hill Adam Friedlan Friedlan Law Richmond Hill

Estate Planning Techniques for Multinational Families

Presenting a live 90-minute teleconference with interactive Q&A Estate Planning Techniques for Multinational Families Navigating Interests in Foreign Business, Real Estate and Financial Accounts TUESDAY,

Presenting a live 90-minute teleconference with interactive Q&A Estate Planning Techniques for Multinational Families Navigating Interests in Foreign Business, Real Estate and Financial Accounts TUESDAY,

Section 11 Probate Glossary

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Section 11 Probate Glossary 2012 Investors Empowerment Academy, LLC 119 Abatement A proportional diminution or reduction of the pecuniary legacies, when there are not sufficient funds to pay them in full.

Estate planning for non-citizens.

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Estate Planning Estate planning for non-citizens. The federal gift and estate tax laws that apply to non-united States citizens (aliens) are different from those for citizens. Further, there are different

Expatriation from the United States

Expatriation from the United States Hal J. Webb November 15, 2012 Bahamas Discussion Points Tax Rules Applicable to Expatriations on or After June 17, 2008 Reporting Requirements Planning for Expatriation

Expatriation from the United States Hal J. Webb November 15, 2012 Bahamas Discussion Points Tax Rules Applicable to Expatriations on or After June 17, 2008 Reporting Requirements Planning for Expatriation

TECHNICAL EXPLANATION OF H.R

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

TECHNICAL EXPLANATION OF H.R. 6081, THE HEROES EARNINGS ASSISTANCE AND RELIEF TAX ACT OF 2008, AS SCHEDULED FOR CONSIDERATION BY THE HOUSE OF REPRESENTATIVES ON MAY 20, 2008 Prepared by the Staff of the

EXPAT TAX HANDBOOK. Non-Citizens and U.S. Tax Residency. Tax Year Ephraim Moss, Esq Ext 101

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

EXPAT TAX HANDBOOK Non-Citizens and U.S. Tax Residency Tax Year 2018 Ephraim Moss, Esq. 718-887-9933 Ext 101 emoss@expattaxprofessionals.com Joshua Ashman, CPA 718-887-9933 Ext 102 jashman@expattaxprofessionals.com

Memorandum. LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes. 1. Overview of Federal Transfer Tax System

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

LEBLANC & YOUNG FOUR CANAL PLAZA, PORTLAND, MAINE 04101 FAX (207)772-2822 TELEPHONE (207)772-2800 INFO@LEBLANCYOUNG.COM TO: LeBlanc & Young Clients DATE: January 2017 SUBJECT: Primer on Transfer Taxes

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

Practical Solutions to Deal with the Inconvenience of Having a Family Member Who is a U.S. Person! Shawn P. Wolf, Esq. Packman, Neuwahl & Rosenberg E-mail: spw@pnrlaw.com! 1500 San Remo Ave. Suite 125

II. Residence for Federal Estate and Gift Tax Purposes

KEVIN MATZ & ASSOCIATES PLLC U.S. Estate and Gift Taxation of Nonresident Aliens Kevin Matz, J.D., C.P.A., LL.M. (Taxation) Kevin Matz, Esq. I. Introduction The U.S. transfer tax regime requires special

KEVIN MATZ & ASSOCIATES PLLC U.S. Estate and Gift Taxation of Nonresident Aliens Kevin Matz, J.D., C.P.A., LL.M. (Taxation) Kevin Matz, Esq. I. Introduction The U.S. transfer tax regime requires special

The United States Government defines an alien as any individual who is not

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

The United States Government defines an alien as any individual who is not a U.S. citizen or U.S. national. A nonresident alien is an alien who has not passed the green card test or the substantial presence

Trusts That Affect Estate Administration

Trusts That Affect Estate Administration NBI Estate Administration Boot Camp September 22-23, 2016 Baltimore, Maryland By: Jill A. Snyder, Esq. Law Office of Jill A. Snyder, LLC 410-864- 8788 1 I. When

Trusts That Affect Estate Administration NBI Estate Administration Boot Camp September 22-23, 2016 Baltimore, Maryland By: Jill A. Snyder, Esq. Law Office of Jill A. Snyder, LLC 410-864- 8788 1 I. When

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

RECENT LEGISLATION INVOLVING FOREIGN TRUSTS AND GIFTS 1997 Robert L. Sommers I. INTRODUCTION... 1 1. Rich Immigrating Foreigners - The New Villain... 1 2. Foreign Gifts - New Reporting Requirements...

U.S. TAX UPDATE: ISSUES THAT CANADIAN ADVISORS SHOULD BE AWARE OF FOR THEIR CLIENTS

STEP LONDON & SOUTHWESTERN ONTARIO CHAPTER LAUNCH EVENT THURSDAY, October 17, 2013 @ 4:30 p.m. U.S. TAX UPDATE: ISSUES THAT CANADIAN ADVISORS SHOULD BE AWARE OF FOR THEIR CLIENTS Speaker : Edward Northwood,

STEP LONDON & SOUTHWESTERN ONTARIO CHAPTER LAUNCH EVENT THURSDAY, October 17, 2013 @ 4:30 p.m. U.S. TAX UPDATE: ISSUES THAT CANADIAN ADVISORS SHOULD BE AWARE OF FOR THEIR CLIENTS Speaker : Edward Northwood,

Annual Advanced ALI-ABA Course of Study Planning Techniques for Large Estates. November 17-21, 2003 San Francisco, California

Annual Advanced ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2003 San Francisco, California Estate Administration: A Review of Income, Gift, and Estate Tax Planning Issues

Annual Advanced ALI-ABA Course of Study Planning Techniques for Large Estates November 17-21, 2003 San Francisco, California Estate Administration: A Review of Income, Gift, and Estate Tax Planning Issues

Pensioners of the. Department of RETIREMENT OAS Staff. Human LECTURE. Resources SERIES. of Retirees Federal. of the OAS 2 2 Credit Union

Association of OAS Pensioners of the Retirement OAS Retirement and Pension and Pension Fund Fund (ASPEN) PRE- Department of RETIREMENT OAS Staff Human LECTURE Association Resources SERIES of the OAS Association

Association of OAS Pensioners of the Retirement OAS Retirement and Pension and Pension Fund Fund (ASPEN) PRE- Department of RETIREMENT OAS Staff Human LECTURE Association Resources SERIES of the OAS Association

REVISING ESTATE PLANS IN LIGHT OF THE RECENT NYS ESTATE TAX CHANGES. October 30, 2014

REVISING ESTATE PLANS IN LIGHT OF THE RECENT NYS ESTATE TAX CHANGES October 30, 2014 By: Stanley E. Bulua, Esq. ROBINSON BROG LEINWAND GREENE GENOVESE & GLUCK P.C. (212) 603-6311 (212) 956-2164 (fax) sbulua@robinsonbrog.com

REVISING ESTATE PLANS IN LIGHT OF THE RECENT NYS ESTATE TAX CHANGES October 30, 2014 By: Stanley E. Bulua, Esq. ROBINSON BROG LEINWAND GREENE GENOVESE & GLUCK P.C. (212) 603-6311 (212) 956-2164 (fax) sbulua@robinsonbrog.com

U.S. Citizens Living in Canada

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

BMO Wealth Management U.S. Citizens Living in Canada Income Tax Considerations Many U.S. citizens have lived in Canada most of their lives and often think of themselves as Canadians. This may be true in

EXPATRIATION TAX AND PLANNING

New Haven New York Geneva EXPATRIATION TAX AND PLANNING Greenwich London Speaker: Ivan A. Sacks, Esq. Chairman, Withersworldwide Partner, Withers Bergman LLP Milan May 1, 2014 Miami, Florida Hong Kong

New Haven New York Geneva EXPATRIATION TAX AND PLANNING Greenwich London Speaker: Ivan A. Sacks, Esq. Chairman, Withersworldwide Partner, Withers Bergman LLP Milan May 1, 2014 Miami, Florida Hong Kong

Income Tax Rates are Higher

MICKEY R. DAVIS MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS APRIL 19, 2017 "Permanent" Unified Transfer Tax System $5,000,000 exemption for gift, estate and GST tax Indexed for inflation $5.45

MICKEY R. DAVIS MELISSA J. WILLMS DAVIS & WILLMS, PLLC HOUSTON, TEXAS APRIL 19, 2017 "Permanent" Unified Transfer Tax System $5,000,000 exemption for gift, estate and GST tax Indexed for inflation $5.45

Bypass Trust (also called B Trust or Credit Shelter Trust)

") Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

Vertex Wealth Management, LLC Michael J. Aluotto, CRPC President Private Wealth Manager 1325 Franklin Ave., Ste. 335 Garden City, NY 11530 516-294-8200 mjaluotto@1stallied.com Bypass Trust (also called

TRUST AND ESTATE PLANNING GLOSSARY

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

TRUST AND ESTATE PLANNING GLOSSARY What is estate planning? Estate planning is the process by which one protects and disposes of his or her wealth, sometimes during life and more often at death, in accordance

CHAPTER 14: ESTATE PLANNING

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

CHAPTER 14: ESTATE PLANNING MATCHING a. marital deduction b. charitable remainder c. gift splitting d. present interest e. legal life estate f. stepped-up basis g. general power of appointment h. term

Estate Tax Conflicts Resulting from a Change in Residence

Originally published in: International Fiscal Association 56 th Congress August 25, 2002 Estate Tax Conflicts Resulting from a Change in Residence By: Sanford H. Goldberg The focus in my presentation is

Originally published in: International Fiscal Association 56 th Congress August 25, 2002 Estate Tax Conflicts Resulting from a Change in Residence By: Sanford H. Goldberg The focus in my presentation is

ESTATE PLANNING. Estate Planning

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

ESTATE PLANNING Estate Planning 2 Why do you need estate planning? Estate planning is a way for your family to create a plan in case something happens to you. It may help you take care of both the financial

A Primer on Portability

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

A Primer on Portability Presentation to: Estate Planning Council of New York City, Inc. Estate Planners Day 2013 May 8, 2013 Ivan Taback, Esq. Proskauer Rose LLP Eleven Times Square New York, New York

Tax Implications of Family Wealth Transfers

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

Tax Implications of Family Wealth Transfers Jill Choate Beier, Esq. Federal and Estate Gift Tax Overview Estate Tax Formula: Less: Plus: Equals: Decedent s Gross Estate Allowable Deductions Adjusted Taxable

Recent Developments in the Estate and Gift Tax Area. Annual Business Plan and the Proposed Regulations under Section 2642

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

DID YOU GET YOUR BADGE SCANNED? Gift & Estate Tax Recent Developments in the Estate and Gift Tax Area Annual Business Plan and the Proposed Regulations under Section 2642 #TaxLaw #FBA Username: taxlaw

Private Client Estate and Tax Planning. JANUARY 2015 No. 1

JANUARY 2015 No. 1 Private Client 2015 Estate and Tax Planning Blank Rome s annual estate planning newsletter discusses certain concepts and techniques that we hope may be of interest to our clients and

JANUARY 2015 No. 1 Private Client 2015 Estate and Tax Planning Blank Rome s annual estate planning newsletter discusses certain concepts and techniques that we hope may be of interest to our clients and

ALI-ABA Course of Study Estate Planning for the Family Business Owner

1089 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

1089 ALI-ABA Course of Study Estate Planning for the Family Business Owner Cosponsored by the ABA Section of Real Property, Trust and Estate Law - ABA Section of Taxation July 9-11, 2008 Boston, Massachusetts

AN ASSOCIATION OF ATTORNEYS EST BEVERLY HILLS, CALIFORNIA (310) (323)

(323)") Altshuler and and Spiro Spiro AN ASSOCIATION OF ATTORNEYS EST. 1959 ssor 9301 wtishrre WILSHIRE BouLEVARD, BOULEVARD, sutre SUITE s04 504 BEVERLY HILLS, CALIFORNIA 90210-5412 0-5412 (310) 275-4475 - (323)

Altshuler and and Spiro Spiro AN ASSOCIATION OF ATTORNEYS EST. 1959 ssor 9301 wtishrre WILSHIRE BouLEVARD, BOULEVARD, sutre SUITE s04 504 BEVERLY HILLS, CALIFORNIA 90210-5412 0-5412 (310) 275-4475 - (323)

State of Expatriation 2012 TTN Conference New York 2013

State of Expatriation 2012 TTN Conference New York 2013 Michael G. Pfeifer, Esq. Caplin & Drysdale, Chartered May 6, 2013 Session Overview HISTORY OF EXPATRIATION RULES ( Alternative Tax Regime to Mark-to-Market

State of Expatriation 2012 TTN Conference New York 2013 Michael G. Pfeifer, Esq. Caplin & Drysdale, Chartered May 6, 2013 Session Overview HISTORY OF EXPATRIATION RULES ( Alternative Tax Regime to Mark-to-Market

The confluence of several events

Estate Planning Gets More Complex for Non-U.S. Citizens Tax treaties, as well as the Internal Revenue Code, need to be reviewed when advising non-u.s. citizens about strategies to minimize transfer taxes.

Estate Planning Gets More Complex for Non-U.S. Citizens Tax treaties, as well as the Internal Revenue Code, need to be reviewed when advising non-u.s. citizens about strategies to minimize transfer taxes.

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning

Impact of the Tax Cuts and Jobs Act of 2017 on Estate Planning Where Were We vs. Where Are We Now 2017 2018 (Pre-Act) 2018 (Post-Act) Transfer Tax Rate 40% 40% 40% Estate/Gift Tax Exemption $5.49 million