Under DVAT Act. By: CA Sandeep Garg M:

|

|

|

- Mabel Wade

- 6 years ago

- Views:

Transcription

1 Under DVAT Act By: CA Sandeep Garg M: casandeepgarg@gmail.com;

2 Contents Introduction to VAT Audit Applicable Provisions Notification Calculation of Gross Turnover Form AR-I Conclusion

3 Introduction to VAT Audit The overall objective of the system is to maximize the collection of VAT Revenue by maximizing the level of voluntary compliance and by deterring evasion. The principle of checking of submitted returns by going through books of accounts has been assigned to the Professional Chartered Accountants. In India, VAT Audit is compulsory in all except 4 States, (subject to Turnover limits for the dealers) Till recently, Delhi was a part of this list. However, the Delhi Government has notified that a Dealer with a Turnover of over Rs. 10 crore has to submit a VAT Audit report. Delhi Andra Pradesh Haryan a Himacha l Pradesh Sikkim

4 Applicable Provisions Section 49 If, in respect of any particular year, the gross turnover of a dealer exceeds sixty lakh rupees or such other amount as may be prescribed, then, such dealer shall submit a report in such manner, form and period as may be notified by the Commissioner.

5 Applicable Provisions Rule 42A Date of Amendment: 31 st March, 2013 Post Amendment: For the purpose of Section 49, a dealer whose gross turnover in a year exceeds one crore rupees, shall get his accounts of such year audited by an accountant, and shall be liable to submit a report, as notified by the Commissioner, from time to time: PROVIDED that the Commissioner may, by an order, require a dealer or class or classes of dealers, to submit a simplified version of the report in lieu of report notified by him under section 49, PROVIDED FURTHER that the Commissioner may, by an order, exempt a dealer or class or classes of dealers, from furnishing a report, for the purpose of Section 49. Prior to Amendment: A dealer whose gross turnover in a year exceeds the prescribed limit as fixed for the purpose, under section 44AB of the Income Tax Act, 1961 as amended from time to time or any other law substituting the Act, he shall get his accounts of such year audited by an accountant, as per the provisions of section 49.

6 Notification Prior to the notification, Audit under DVAT was governed by Section 49 along with Rule 42A of the Act. Prior Section 49 states, if, in respect of any particular year, the gross turnover of a dealer exceeds sixty lakh rupees or such other amount as may be prescribed, then, such dealer shall submit a report in such manner, form and period as may be notified by the commissioner. Rule 42A reads as a dealer whose gross turnover in a year exceeds the prescribed limit as fixed for the purpose, under section 44ab of the income tax act, 1961 as amended from time to time or any other law substituting the act, he shall get his accounts of such year audited by an accountant, as per the provisions of section 49. (Amended on 20th march, 2013) Issue of notification no. F.7/420/Policy/Vat/2011/ dated 11 th Feb, 2013 made Audit under Delhi VAT compulsory for dealers having a turnover more than Rs. 10 crore.

7 Notification Issue of notification no. F.7/420/Policy/VAT/2011/ dated 11 th Feb, 2013 made Audit under Delhi VAT compulsory for dealers having a turnover more than Rs. 10 crore. Notification no. F.7/420/Policy/VAT/2011/ was issued by the commercial tax department of Delhi on 11th February, After According to the notification, every dealer liable to get his accounts audited as per Section 49 read with Rule 42A of the DVAT Act, shall submit the audit report to the department in the following manner: In the prescribed form: Form AR I Within seven and a half months from the end of the year. This notification is applicable only for the dealers whose Gross Turnover exceeds Rs. 10 crore in or any of the subsequent financial years. The following are exempt from the purview of the notification: Dealers exclusively dealing in commodities listed in the First schedule appended to the act. Dealers with 100% export turnover.

8 Applicability of Notification This notification is applicable on the following: A dealer whose Gross Turnover exceeds Rs. 10 crore in or any of the subsequent financial years. The definition of Turnover under Delhi VAT is the aggregate of the amounts of sale price received or receivable by the person in any tax period, reduced by any tax for which the person is liable under section 3 of this Act The following are exempted from the applicability of the notification: Dealers exclusively dealing in commodities listed in the First Schedule appended to the Delhi VAT Act. The First Schedule contains the list of 85 exempted commodities under DVAT. Dealers with 100% export turnover. First Schedule

9 Who is Liable for VAT Audit S.N. Nature of the Dealer Based upon Turnover 1. Dealers whose Gross Turnover does not exceed Rs. 1 crore 2. Dealers whose turnover exceeds Rs. 1 crore but is less than Rs. 10 crore 3. Dealers whose Gross Turnover is Rs. 10 crore or more. Form Exemption, if any. Not liable for VAT Audit Form of Audit Report and its time and manner yet to be notified by the Commissioner. 1) Dealers exclusively dealing in Commodities listed in first schedule to the ACT 2) Dealers with 100 % export Turnover. Form AR 1

of Delhi VAT Amendment Act, 2013, in case the dealer fails to comply with the provision of audit, the dealer shall be liable to pay penalty, a sum equal to 1% of his")

10 Time limit and Penalty Audit Report in Form AR 1 to be submitted within Seven and half months from the date of the Financial year in duplicate. Penalty As per section 86(18) of Delhi VAT Amendment Act, 2013, in case the dealer fails to comply with the provision of audit, the dealer shall be liable to pay penalty, a sum equal to 1% of his Turnover or sum of one lakh rupee, whichever is less. Issue :????

11 Calculation of Gross Turnover Part 4 of the form prescribes for the calculation of Gross Turnover. GTO Includes Taxable Sales (including Central Sales) Exempted Sales Goods specified in the First Schedule Penultimate Exports u/s 5(3) of the CST Act Labour & Service Charges involved in the execution of Works Contract Sale of Capital Goods (Refer section 6(3) of DVAT) Dealers specified in the Fifth Schedule Others Consignment Sales/ Stock Transfer Job Work Charges (In case of Works Contract, the full value of the contract is considered)

12 How to Calculate Gross Turnover Particulars Sale within Delhi Taxable under DVAT ACT Add: Inter State Sale Add: Sale in Course of Import and export including penultimate export Add: Stock Transfer from Delhi to Branches/agents in Other State Rs. XXX XXX XXX XXX Add: Excise Duty (Local and Central) and Custom Duty XXX Less: DVAT/CST payable by the dealer.. ( If already included) XXX Less: Cost of Freight or delivery separately charged in the Invoice; provided that the ownership of the goods is not transferred at the buyer s place XXX Less: Cost of installation separately charged in the Invoice XXX Gross Turnover XXXX

13 Points for Discussion Gross Turnover Turnover as per DVAT Return or P & L Account. Turnover of Delhi office or Entire Entity Turnover of and A criteria Exemption to Dealers exclusively dealing in Exempted Goods. Exemption to Dealers with 100 percent Export Turnover.

14 Relevant Definitions Turnove r Under Section 2(zm) of DVAT Act, "turnover" means the aggregate of the amounts of sale price received or receivable by the person in any tax period reduced by any tax for which the person is liable under section 3 of this Act; Goods (Section (2 m) "goods" means every kind of moveable property (other than newspapers, actionable claims, stocks, shares and securities) and includes livestock, all materials, commodities, grass or things attached to or forming part of the earth which are agreed to be severed before sale or under a contract of sale; and property in goods (whether as goods or in some other form) involved in the execution of a works contract, lease or hire purchase or those to be used in the fitting out, improvement or repair of movable property; Capital Goods Capital Goods Under Section 2(f) of DVAT Act, "capital goods" means plant, machinery and equipment used directly or indirectly, in the process of trade or manufacturing or for execution of works contract in Delhi;

15 Relevant Definitions (Sale Under Section 2(zc) of DVAT Act, "sale" with its grammatical variations means: any transfer of property in goods by one person to another for not including a grant or subvention payment made by one government agency or department, whether of the central government or of any state government, to another) Cash or deferred payment or valuable consideration includes a transfer of goods on hire purchase or other system of payment by instalments, but does not include a mortgage or hypothecation of or a charge or pledge on goods; supply of goods by a society (including a co operative society), club, firm, or any association to its members for cash or for deferred payment or for commission, remuneration or other valuable consideration, whether or not in the course of business; transfer of property in goods by an auctioneer referred to in sub clause (vii) of clause (j) of this section, or sale of goods in the course of any other activity in the nature of banking, insurance who in the course of their main activity also sell goods repossessed or re claimed;

16 Relevant Definitions a transfer, otherwise than in pursuance of a contract, of property in any goods for cash, deferred payment or other valuable consideration; transfer of property in goods (whether as goods or in some other form) involved in the execution of a works contract; transfer of the right to use any goods for any purpose (whether or not for a specified period) for cash, deferred payment or other valuable consideration; supply, by way of or as part of any service or in any other manner whatsoever, of goods, being food or any other article for human consumption or any drink (whether or not intoxicating), where such supply or service is for cash, deferred payment or other valuable consideration; every disposal of goods referred to in sub clause (vii) of clause (j) of this subsection and the words "sell", "buy" and "purchase" wherever appearing with all their grammatical variations and cognate expressions, shall be construed accordingly;

17 Relevant Definitions (Dealer) Under Section 2(j) of DVAT Act, "dealer" means any person who, for the purposes of or consequential to his engagement in or in connection with or incidental to or in the course of his business, buys or sells goods in Delhi directly or otherwise, whether for cash or for deferred payment or for commission, remuneration or other valuable consideration and includes, a factor, commission agent, broker, del credere agent or any other mercantile agent by whatever name called, who for the purposes of or consequential to his engagement in or in connection with or incidental to or in the course of the business, buys or sells or supplies or distributes any goods on behalf of any principal or principals whether disclosed or not ; a non resident dealer or as the case may be, an agent, residing in the State of a non resident dealer, who buys or sells goods in Delhi for the purposes of or consequential to his engagement in or in connection with or incidental to or in the course of the business; a local branch of a firm or company or association of persons, outside Delhi where such firm company, association of persons is a dealer under any other sub clause of this definition;

18 Relevant Definitions iv. a club, association, society, trust, or cooperative society, whether incorporated or unincorporated, which buys goods from or sells goods to its members for price, fee or subscription, whether or not in the course of business; v. an auctioneer, who sells or auctions goods whether acting as an agent or otherwise or, who organizes the sale of goods or conducts the auction of goods whether or not he has the authority to sell the goods belonging to any principal, whether disclosed or not and whether the offer of the intending purchaser is accepted by him or by the principal or a nominee of the principal; vi. a casual trader ; vii. any person who, for the purposes of or consequential to his engagement in or in connection with or incidental to or in the course of his business disposes of any goods as unclaimed or confiscated, or as unserviceable or scrap, surplus, old, obsolete or as discarded material or waste products by way of sale.

19 Relevant Definitions Explanation. For the purposes of this clause, each of the following persons, bodies and entities who sells any goods whether in the course of his business, or by auction or otherwise, directly or through an agent for cash or for deferred payment or for any other valuable consideration, shall, notwithstanding anything contained in clause (d) or any other provision of this Act, be deemed to be a dealer, namely: i.customs Department of Government of India administering Customs Act, 1962 (52 of 1962); ii.departments of Union Government, State Governments and Union territory Administrations; iii.local authorities, Panchayats, Municipalities, Development Authorities, Cantonment Boards; iv.public Charitable Trusts; v.railway Administration as defined under the Indian Railways Act, 1989 ( 24 of 1989) and Delhi Metro Rail Corporation Limited;

20 Relevant Definitions vi.incorporated or unincorporated societies, clubs or other associations of persons; vii.each autonomous or statutory body or corporation or company or society or any industrial, commercial, banking, insurance or trading undertaking, corporation, institution or company whether or not of the Union Government or any of the State Governments or of a local authority; viii.delhi Transport Corporation; ix.shipping and construction companies, air transport companies, airlines and advertising agencies.

21 Relevant Definitions Sale Price Under Section 2(zd) of DVAT Act, sale price" means the amount paid or payable as valuable consideration for any sale, including I.the amount of tax, if any, for which the dealer is liable under section 3 of this Act; II.in relation to the delivery of goods on hire purchase or any system of payment by instalments, the amount of valuable consideration payable to a person for such delivery including hire charges, interest and other charges incidental to such transaction; III.in relation to transfer of the right to use any goods for any purpose (whether or not for a specified period) the valuable consideration or hiring charges received or receivable for such transfer; IV.any sum charged for anything done by the dealer in respect of goods at the time of, or before, the delivery thereof; V.amount of duties levied or leviable on the goods under the Central Excise Act, 1944 (1 of 1944) or the Customs Act, 1962 (62 of 1962), or the Delhi Excise Act, 2009 (Delhi Act 10 of 2010) whether such duties are payable by the seller or any other person; and

22 Relevant Definitions vi. amount received or receivable by the seller by way of deposit (whether refundable or not) which has been received or is receivable whether by way of separate agreement or not, in connection with, or incidental to or ancillary to the sale of goods; vii. in relation to works contract means the amount of valuable consideration paid or payable to a dealer for the execution of the works contract; less any sum allowed as discount which goes to reduce the sale price according to the practice, normally, prevailing in trade; the cost of freight or delivery or the cost of installation in cases where such cost is separately charged; and the words "purchase price" with all their grammatical variations and cognate expressions, shall be construed accordingly;

23 Relevant Definitions Provided that where the dealer makes sale of goods imported into the territory of India, the sale price shall be greater of the following; a) the valuable consideration received or receivable by the dealer; b) value determined by the Custom authorities for payment of custom duty at the time of the import of such goods. Explanation.1 A dealer's sale price always includes the tax payable by it on making the sale, if any; Explanation. 2 The amount received or receivable by oil marketing companies for the sale of diesel and petrol shall be deemed to be equivalent to the price on which the retail outlets will sell these commodities to the consumer.

24 Questions for Sale Price??? 1. Amount of Delhi VAT 2. Higher purchases 3. Transfer of right to use of goods 4. Central excise duty and state excise duty 5. Pre sale expenses 6. Service tax 7. Customs duty 8. Security deposit 9. Works contract 10. Discounts 1. At the time of making sale 2. Ex post facto 11. Cost of freight/insurance and installation charges 12. Additional consideration/subsidy/ex gratia 1. By Buyer 2. By government 3. By third party

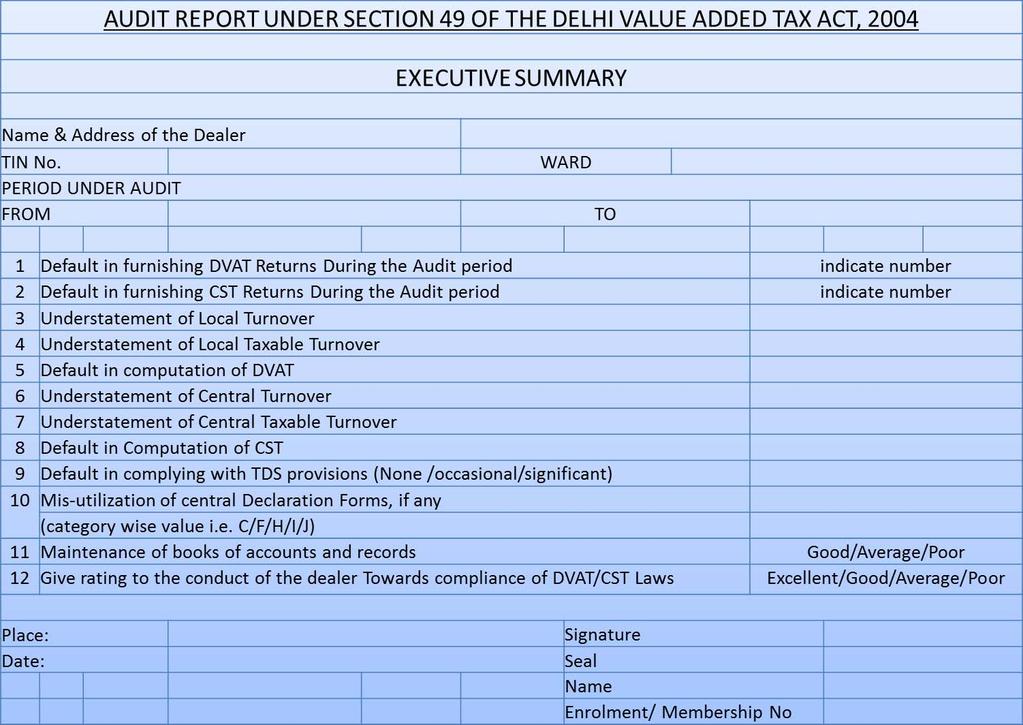

25 FORM AR I

26 Form AR-1, as prescribed by the notification, contains the following particulars: s. no. PART Particulars Relevant Annexure Incorporating observations 1 Part 1 Audit Report, verification and certification, summary of additional tax liability, adverse comments and recommendations to dealer 2 Part 2 General Information about the dealer 2 3 Part 3 Details of returns furnished und Delhi VAT Act and Central Sales Tax act 4 Part 4 Computation of Turnover under Delhi VAT Act 4 1 to Part 5 Computation of Turnover under Central Sales Tax Act to 5 5

27 Form AR-1, as prescribed by the notification, contains the following particulars: s. no. PART Particulars Relevant Annexure Incorporating observations 6 Part 6 Purchases (Local and Central) 6 1 to Part 7 Sales against declaration forms 7 8 Part 8 Tax Deduction at source 8 9 Part 9 Financial Summary and analysis of Delhi 9 10 Part 10 Questionnaire Part 11 Details of non receipt of information and records required to conduct audit 12 Part 12 Annexures forming part of Part1 to Part 10

28 The Auditor is to submit the following enclosures along with the Report: Statutory audit report with complete set of annexure including that of related party disclosure as required under accounting standard 18. Tax Audit report under the I.T Act 1961 with complete set of annexure including that of related party disclosure as required under Accounting standard 18. Audited balance sheet, P&L A/c, Income & Expenditure Account In case dealer is having multi state activities, the trial balance, trading account & P & L A/c for the business activities in the NCT of Delhi

29

30 Part 1: Audit Report & Certification Part 1 of the Form contains the following: 1. Declarations and Audit Report from the Auditor regarding the Company whose Audit has been conducted. 2. Summary of the Returns filed by the Assessee and whether they re filed on a Monthly or Quarterly basis. 3. Certifications by the Auditor regarding the verifications done by him. There are a total of 15 certifications asked to certify by the Auditor. This feature is unique to DVAT and has been seen for the first time in any VAT Audit Report. 4. Qualifications by the Auditor with regards to the above certifications, if any. 5. Summary of the additional tax liability or additional refund due to the dealer for the relevant audit period and his Tax liability for the same.

31 Clause 3 of Part 1-CERTIFICATION I/we have obtained all the information and explanations. which is to the best of my/ our knowledge and belief, were necessary for the purposes of the audit Summary of the additional tax liability or additional refund due to the dealer for the relevant audit period and his Tax liability for the same. I/we have read and followed the Instruction for conducting the audit and preparation of the audit report; The books of accounts and other Sales tax /VAT Related Record and Registers maintained by the dealer along with sales and purchase invoices as also Cash Memos and other necessary documents are sufficient for computation of tax liability under the DVAT and CST Acts;. I/We have Verified all returns (including the TDS returns) under the DVAT Act and CST Act filed by the Auditee for the period under audit The gross turnover of sales and purchases determined, includes all the transactions of sales and purchases concluded during the period under audit in accordance with the provisions of the DVAT Act and the CST Act;

32 Clause 3 of Part 1-CERTIFICATION The adjustment in turnover of sales and/or purchases is based entries made in the books of accounts during the period under audit and the same are supported by necessary documents; The deductions claimed from the gross Turnover of sales and other adjustments thereto including deduction on account or goods return, adjustment on account of discounts as also debit /credit notes issued or received on account of other reasons, are supported by necessary documents and are in conformity with the provisions of the relevant Act;

Wherever the dealer has claimed")

33 Clause 3 of Part 1-CERTIFICATION As per the information made available for the purpose of audit, the tax leviable on sales is properly computed applying rate of tax specified in the Delhi VAT Act and/or Schedules appended to that Act, advance rulings under Section 85 and Determination orders passed by the commissioner (unless overruled by the Higher Courts) Wherever the dealer has claimed sales against the declarations or certificates; except as given in para 7, duplicate copies of all such declarations and certificates are produced before me/us and the same are in conformity of the provisions related thereto: ; The records related to the receipt and dispatch of goods are correct and properly maintained ; The tax invoices in respect of sales are in conformity with the provisions of law;

34 Clause 3 of Part 1-CERTIFICATION The Auditee has maintained separate bank account for carrying its activities in the National Capital Territory of Delhi. The Bank statement have been examined by me/us and they are fully reflected in the books of accounts; The dealer is conducting his business from the place/places of business declared by him as his principal place of business/and the additional place of business; and Due professional care has been exercised while carrying the audit, and based on my observations of the business processes and practices, Stock of inventor, and books of account maintained by the dealer, 1/we fairly conclude that, i.if dealer is dealing in the commodities mentioned in the Part 3 of this report; ii.sales tax/vat related records of the dealer reflect true and fair view of the volume and size of the business for period under audit. The Auditee/Dealer, if opted for Composition Scheme under Section 16 has fulfilled all the necessary conditions of the Scheme and has complied with the requirements of the Scheme.

35 Part 2 - General Information about the Dealer: This part contains the following information: 1.General Information A. General B. Related Information under Delhi VAT Act C. Related Information under CST Act D. Related Information under Other Acts

36 Part 2 - General Information about the Dealer: 2. Business Related Information 1. Info related to Accounting 2. Business Activities in Brief 3. Commodities dealt in 4. Address of Business place 5. Accounting Software 6. Method of Accounting 7. Method of Valuation 8. Major changes during audit period 9. Nature of Business 10.Constitution of Business 11.Working Capital Employed 3. Particulars of Bank Account(s) maintained

37 Part 2 - General Information about the Dealer: Important Points: 1. Related Party disclosure 2. Information about separate books of accounts 3. Bank Account detail 3 Particulars of the Bank Account(s) maintained during the period under Audit Sr. No. Name of the Bank Branch BSR Number (Give Branch Address, if BSR code not known) Account Number(s) Whether the account is operated for other State activities

38 Part 3: Details of Returns Furnished under DVAT and CST Act PART-3 DETAILS OF RETURNS FURNISHED UNDER THE DELHI VAT ACT AND CENTRAL SALES TAX ACT Sr. No. Tax Period Due Date of e- filing Date of e-filing Due Date for filing of Hard copy Date of filing of Hard copy

39 Part 4A: Computation of Turnover under DVAT Act This part is prescribed for the calculation of Gross Turnover and computation of the VAT liability thereon with respect to Local Sales. It is calculated in the following manner: 1.Gross Turnover Of Sales (Including: Taxable Sales, Exempted Sales, Consignment / Branch Transfers, Job Work Charges.) (For works contract, gross consideration includes labor, services & land price) 2.Add: Central Sales 3.Turnover Under DVAT (1 2) 4.Computation Of Output Tax (Refer Part 4C) 5.Adjustment In Output Tax 6.Net Output Tax [4(+/ ) 5 ] 7.Input Tax Credit 8.Adjustments in ITC

40 Part 4A: Computation of Turnover under DVAT Act 9. Net ITC [ 7(+/ )8] 10. Net Tax Payable (6 9) 11. Add: Interest Payable 12. Add : Penalty Payable 13. Less T.D.S 14. Less Tax Deposited 15. Less: Amount Adjusted Against CST Liability 16. Less: Refund Availed 17. Amount Payable/( )Excess [ (13 To 16)] 18. Amount Paid During Audit (taken from Returns)

41 Part 4A: Computation of Turnover under DVAT Act Computation of Gross Turnover of Sales: 1.Taxable Sales Taxable Sales consist of the following: A. Sale of Goods Local Taxed at the rate given in the Schedules prescribed in the Act B. Sale of Goods Central Two different methods of taxability: i. Against C Form: If sold interstate to a registered dealer and C Form is procured regarding the same, then the sale will be 2% ii. Not against C Form: If C Form is not procured, then the sale will be taxable at the rate given in the Schedules prescribed in the Act. 2.Exempted Sales Exempted Sales consist of the following: A. Goods specified in the first Schedule of the Act B. Penultimate Exports u/s 5(3) of the CST Act C. Labour & Service Charges involved in the execution of Works Contract D. Sale of Capital Goods (Refer section 6(3) of DVAT) E. Dealers specified in the Fifth Schedule F. Others (Eg: E I/II (subsequent) sales made locally exempt under section 6(3) of the CST Act, Any goods exempted via some notification, Service/Admin Charges like Interest etc. )

42 Part 4A: Computation of Turnover under DVAT Act Computation of Gross Turnover of Sales: 3.Value of Consignment/Branch Transfer A Branch Transfer is where the Principle office transfers the Goods to one of its own Branches without any consideration. A branch transfer is not chargeable to VAT. However, declaration from the Branch is required as a Compliance for the same. This declaration is received in the Form F, procured from the VAT departments. Form F is issued on a monthly basis. A Consignment Sale is a Trading arrangement in which a seller sends goods to a buyer or reseller who pays the seller only as and when the goods are sold. The seller remains the owner (title holder) of the goods until they are paid for in full and, after a certain period, takes back the unsold goods. 4.Job Work Charges Job Work Charges consist of the Total Consideration received for the execution of Works Contract, for both Local and Interstate Sales. Works Contract is a contract which consists of both Sale of Goods and Provision of Service in the same contract. Under VAT, only the Goods portion is chargeable, however in calculating the Gross Turnover, the whole Contract value is considered.

43 Part 4B: Exempted Sales under DVAT Act

44 Audit Checklist for gross Turnover Check the income side of P&L A/c to ensure that job work, sale of DEPB, rent of machinery etc. Ensure reconciliation inter branch/ consignment A/c. Sale of fixed asset. Unbilled revenue in customer A/c. Income which to be taxed under service and VAT both. If income is directly credited to customer A/c. If goods are sent on delivery challan basis are bill to then as per contract. Goods in transit.

45 Computation of Taxable Turnover Gross turnover Less: Exempted goods (Sch 1) Section 6(1) Less: Turnover of Exempted dealers Section 6(2) Less: Turnover of Capital goods Section 6(3) Less: Sale in course of interstate trade or commerce Less: Sale outside Delhi Less: Sale in case of export from India and import in India Less: Works contract Value of Land and labour service and like charges Total Taxable Turnover XXX XXX XXX XXX XXX XXX XXX XXX XXX

46 Checklist for Input Tax credit 1. Credit is only against Tax invoice 2. Eligible purchase 3. Use for eligible sale means not for exempted goods 4. Reversal of input tax credit in term of section 9(6). 1. Credit Note received 2. Stock transfer/consignment transfer (2%) 5. No credit for purchases from a dealer who is paying tax u/s 16 of the DVAT Act.

47 Questions related to Input Tax Credit on Capital goods 1. Time of allowance tax credit 2. Adjustment in input tax at the time of sale of capital goods 3. Transfer of capital goods to other state before expiry of 3 years. 4. Reversal of input tax credit if capital goods sold within a 5 year at the price below the fair market value 5. Restriction on claiming depreciation on Input Tax. Detail in following format Nature of capital goods Cost of goods Amount of Tax involved Tax credit claimed during

48 Question 1. Whether ITC has been reversed on return/ rejection of goods?section 10(1). Case Alpha marketing company vs. CTT. 2. Whether ITC has been reversed on goods lost/destroyed in accordance with rule Lost or destroyed 2. Normal manufacturing lost

49 Part 4C: Computation of Output VAT 4C COMPUTATION OF OUTPUT VAT Sl. No Nature of goods / class of goods (Top 10) As per returns DVAT Turnover Output Tax Applicable Rate of Tax As per Auditor Relevant entry of schedule DVAT Turnover Output Tax Difference

50 Part 5A: Computation of Turnover under CST ACT This part is prescribed for the calculation of Gross Turnover and computation of the CST liability thereon with respect to Central Sales. It is calculated in the following manner: 1.Gross turnover of sales including Taxable & Exempted transaction like value of consignment/branch transfer & Job work charges 2.Turnover under DVAT 3.Central sales 4.Cost of freight, deliveries, insurance or installation separately charged. 5.Value of goods returned under CST. 6.CST collected, if included in the central turnover 7.Cash discounted allowed and included in Central Turnover. 8.Job work, labor & services charges for works contracts Net central turnover [ ] 9.Export outside India u/s 5(1) of the CST Act. 10.Sales in the course of import u/s 5(2) of the CST Act. 11.Penultimate sales against H forms u/s 5(3) of the CST Act. 12.Stock/branch transfer against F forms u/s 6A of the CST Act. 13.Sales against E 1 & E 11 forms u/s 6(2) of CST Act. 14.Sales to diplomatic missions & U.N etc. U/s 6(3) of CST Act. 15.Exempted sales u/s 8(5) of the CST Act. 16.Sales covered under proviso to section 9(1) read with section 8(4)(a) 17.Sales of goods outside Delhi (section 4) 18.Total of exemption /deduction [sum(10:18)] 19.Balance total taxable turnover of inter state sales (9 19)

51 Part 5A: Computation of Turnover under CST Act 21. Breakup of Turnover 22. Turnover of Declared Goods Against C Forms [Sec. 8(4) Read With Sec. 14] 23. Turnover of Declared Goods Sold Otherwise [Sec.8(2) Read With Sec.14] 24. Turnover of Other Than Declared Goods Against C forms [Sec.8(4) Read With Sec 8(1) 25. Turnover of Other Than Declared Goods Sold Otherwise [Sec.8(2)] 26. Computation of CST 27. Total CST Payable [Refer To Part 5B] 28. Add: Interest Payable 29. Add: Penalty Payable 30. Less: Amount Adjusted Against DVAT Credits. 31. Less: Tax Deposited 32. Amount Payable [ ] 33. Amount Paid During Audit (Taken from Returns)

52 Part 5B: Computation of CST 5B COMPUTATION OF CENTRAL SALES TAX Sl. No Nature of goods / class of goods As per returns CST Turnove r Tax paid Applicabl e Rate of Tax As per Auditor Relevant entry of DVAT schedule CST Turnover Tax Difference

53 Checklist for Export Sale 1. Export Invoice 2. Bill of lading/ Airway bill duly stamped by the customs authority 3. Any other documents like agreements or documents for export of goods Question: Whether the proceeds has been realized in 180 days Detail of outstanding payments

54 Branch Transfer checklist Section 6 A 1. It should not be pre determined sale. 2. Method of valuation of goods 3. Whether single form F consist stock transfer made during multiple Months 4. Whether form F duly filled and signed have been furnished to the AO. 5. Branch agent etc have been included in the central registration certificate.

55 Sale in course of import and export Section 5(2) and 5(3) Section 5(2)(1) Sale or purchase occasion such import Section 5(2)(2) By Transferring of documents of title of goods before the goods have been crossed the custom frontier of India Duty to be paid by high sea buyer Section 5(3) Last sale or purchase of any goods Proceeding the sale occasion The export of those goods out of territory of India.

56 Part 6: Purchases (Local & Central) The auditor shall furnish the following details: Purchases eligible for ITC (Capital Goods & Others) Purchases not eligible for ITC (Capital Goods & Others) Purchase made from unregistered/composition/casual dealers Interstate Purchases Stock Transfers Local Purchases Central Purchases Import from other Countries Purchases by SEZ/diplomats Local Purchases are classified into Exempted Goods, Goods from unregistered/composition/casual dealers, Goods 1%, 5%, 12.5% and 20%, Purchases against form H etc. Central Purchases are classified into Purchases against Form C, against any other form and without forms.

57 Part 7: Sale against Declaration Forms This part asks for a reconciliation between the Returns and the Declaration Forms under CST procedures already submitted. The following forms are covered: I.Form C: Declaration form to be issued by buyer to the seller incase of an Interstate Sale. II.Form E I/II: Declaration Form to be issued by subsequent buyer to buyer and then from buyer to seller in case of Subsequent Sales. III.Form F: Declaration Form to be issued in case of Branch Transfer IV.Form I: Declaration Form in the case of SEZ Sales V.Form H: Declaration Form to be issued in the case of Exports. VI.Form J: Declaration Form to be issued in the case of Sales to Notified Foreign Diplomats Authorities.

58 Checklist 1. Verify whether the Auditee has furnished declaration form within the specified period. 2. Give detail of pending forms yet to be furnished before authorities on the due date. 3. Verify whether proper extension, if necessary, has been apply along with DVAT Precaution 5. Auditor shall verify the following: a) Name and Address of both the seller and purchaser b) TIN, CST no, of the seller and purchaser c) Stamp of issuing state authority d) Date of issue of form e) Detail of invoices against which the forms have been issued f) Cutting and over writing should be properly authentic. g) Annexure attached along with the form should be properly authentic

59 Part 8: TDS u/s 36A of DVAT ACT Section 36A under the DVAT Act prescribes the liability of a Contractee to deduct WCT TDS from the payment he is to make to the Contractor in case of a Works Contract and deposit the same with the Department in the prescribed forms. It says Any person, not being an individual or a HUF who is responsible for making payment to any the contractor for discharge of any liability on account of valuable consideration payable for the transfer of property in goods in pursuance of a works contract, for value exceeding Rs. 20,000/ or such amount as may, T.D.S thereon at the rate of 2% Part 8 of the form contains a reconciliation between the TDS Return and the amount determined during the Audit of the following: Amount of Contracts awarded as a Contractor Amount of Contracts awarded as a Contractee Amount of Contracts executed by Contractor Amount of Contracts executed by Sub Contractor Tax Deducted at Source as a Contractee Tax Deducted at Source as a Contractor TDS deposited in time TDS deposited late

60 Part 9: Financial Summary & Analysis (Delhi Only) It s a detailed reflection of the Financial Books of the Company in the Audit Form. It consists of the following: A. Income: Sales, Services rendered, Misc. Income including interest. B. Expenditure Opening Stock, Purchases, Contracts, Labour & Wages, Other manufacturing expenses, Salaries, Financial Charges, Advertisement Expenses, Depreciation. C. Capital & Liabilities Capital Employed & Reserves, Long Term Loans, Short Term Loans, Creditors D.Assets Fixed Assets, Investment, Cash & Bank, Debtors, Stock, Other Current Assets, Loans & Advances E.Financial Ratios GP Ratio, NP Ratio, Stock to Sales, Creditors to Purchases, Purchases to Sales, Profit to Funds employed

61 Part 10: Questionnaire 1. Related to dealer engaged in works contract. a) Test check of contracts b) Valuation method works contract 2. Maintenance of books of Accounts. 3. Verification of RC 4. Question related to bank guarantee Fixed deposit. 5. Last but not the least 1. Whether the Auditee has violated any other provision of the DVAT Act or CST Act. 2. Are you satisfied, in general, with the compliance of VAT/CST laws by the auditee.

62 CA Sandeep Garg ( An Idea of Shared Mission)

No.VAT/AMD-1009/IB/Adm-6:-In exercise of the powers conferred by. sub-rule (2) of Rule 17A of the Maharashtra Value Added Tax Rules,

of Rule 17A of the Maharashtra Value Added Tax Rules,") COMMISSIONER OF SALES TAX, MAHARASHTRA STATE. Vikrikar Bhavan, Mazgaon, Mumbai-400 010 Dated: the 26 th August, 2009. NOTIFICATION MAHARASHTRA VALUE ADDED TAX ACT, 2002. No.VAT/AMD-1009/IB/Adm-6:-In exercise

COMMISSIONER OF SALES TAX, MAHARASHTRA STATE. Vikrikar Bhavan, Mazgaon, Mumbai-400 010 Dated: the 26 th August, 2009. NOTIFICATION MAHARASHTRA VALUE ADDED TAX ACT, 2002. No.VAT/AMD-1009/IB/Adm-6:-In exercise

INPUT INPUT TAX TAX CREDIT

INPUT TAX CREDIT PROVISIONS GOVERNING TAX CREDIT S.NO. PARTICULARS SECTION/RULE 1. Tax Credit Section 9 2. Adjustment to tax Credit Section 10 3. Apportionment of tax Credit Rule 6 4. Restrictions and

INPUT TAX CREDIT PROVISIONS GOVERNING TAX CREDIT S.NO. PARTICULARS SECTION/RULE 1. Tax Credit Section 9 2. Adjustment to tax Credit Section 10 3. Apportionment of tax Credit Rule 6 4. Restrictions and

Certification, Reporting, Accounting and Reconciliation of Turnover & Determination of Turnover of Sales and Purchases- WIRC ICAI Cuffeparade

1 Certification, Reporting, Accounting and Reconciliation of Turnover & Determination of Turnover of Sales and Purchases- WIRC ICAI Cuffeparade CA Deepali Mehta 11/16/2016 2 Matters to be covered Liability

1 Certification, Reporting, Accounting and Reconciliation of Turnover & Determination of Turnover of Sales and Purchases- WIRC ICAI Cuffeparade CA Deepali Mehta 11/16/2016 2 Matters to be covered Liability

INTERNATIONAL CHAMBER OF INDIRECT TAX PROFESSIONALS ONE DAY SEMINAR ON A PRESENTATION BY CA J.MURALI

INTERNATIONAL CHAMBER OF INDIRECT TAX PROFESSIONALS ONE DAY SEMINAR ON 01.11.2014 A PRESENTATION BY CA J.MURALI HOW IS SALES TAXED? SALES TAXED AS PER PROVISIONS OF TNVAT ACT 2006 IN TAMILNADU CA J MURALI9841028000

INTERNATIONAL CHAMBER OF INDIRECT TAX PROFESSIONALS ONE DAY SEMINAR ON 01.11.2014 A PRESENTATION BY CA J.MURALI HOW IS SALES TAXED? SALES TAXED AS PER PROVISIONS OF TNVAT ACT 2006 IN TAMILNADU CA J MURALI9841028000

CENTRAL SALES TAX ACT, 1956

725 CENTRAL SALES TAX ACT, 956 [Act No. 74 of 956] Preamble. An Act to formulate principles for determining when a sale or purchase of goods takes place in the course of inter-state trade or commerce or

725 CENTRAL SALES TAX ACT, 956 [Act No. 74 of 956] Preamble. An Act to formulate principles for determining when a sale or purchase of goods takes place in the course of inter-state trade or commerce or

Page 1 of 18. Address of the principal place of the business

FORM - XXIII Department of Commercial Taxes, Government of Uttar Pradesh (See rule 42 of the UPVAT Rules, 2008) Audit report by specified authority PART-I Certified that I/we have verified the correctness

FORM - XXIII Department of Commercial Taxes, Government of Uttar Pradesh (See rule 42 of the UPVAT Rules, 2008) Audit report by specified authority PART-I Certified that I/we have verified the correctness

SREERAM COACHING POINT, Chennai Best Oral coaching at Chennai, Bangalore and Ernakulam

VALUE ADDED TAX What is VAT? A multi point system of taxation on sale of goods where in a mechanism is provided to grant credit for tax paid on inputs. VAT vs Sales Tax VAT SALES TAX (1) VAT is multi point

VALUE ADDED TAX What is VAT? A multi point system of taxation on sale of goods where in a mechanism is provided to grant credit for tax paid on inputs. VAT vs Sales Tax VAT SALES TAX (1) VAT is multi point

TAMIL NADU GOVERNMENT GAZETTE

GOVERNMENT OF TAMIL NADU [Regd.No. TN/CCN/117/2006-08 2006 [Price: Rs. 43.20 Paise. TAMIL NADU GOVERNMENT GAZETTE EXTRAORDINARY PUBLISHED BY AUTHORITY No. 302 ] CHENNAI, SATURDAY, OCTOBER 28, 2006 Aippasi,

GOVERNMENT OF TAMIL NADU [Regd.No. TN/CCN/117/2006-08 2006 [Price: Rs. 43.20 Paise. TAMIL NADU GOVERNMENT GAZETTE EXTRAORDINARY PUBLISHED BY AUTHORITY No. 302 ] CHENNAI, SATURDAY, OCTOBER 28, 2006 Aippasi,

FORM 704 (See rule 65) Audit report under section 61 of the Maharashtra Value Added Tax Act, 2002, Location PART 1 AUDIT REPORT AND CERTIFICATION

Audit report under section 61 of the Maharashtra Value Added Tax Act, 2002, Location PART 1 AUDIT REPORT AND CERTIFICATION") FORM 74 (See rule 65) Audit report under section 6 of the Maharashtra Value Added Act, 22, Location PART AUDIT REPORT AND CERTIFICATION PERIOD UNDER AUDIT FROM TO. The audit of M/s holder of Payer Identification

FORM 74 (See rule 65) Audit report under section 6 of the Maharashtra Value Added Act, 22, Location PART AUDIT REPORT AND CERTIFICATION PERIOD UNDER AUDIT FROM TO. The audit of M/s holder of Payer Identification

AP VALUE ADDED TAX ACT CHAPTER - I 2-12 PRELIMINARY 1 Short Title and commencement 5 2 Definitions 6

AP VALUE ADDED TAX ACT 2005 INDEX Section Pg.No. CHAPTER - I 2-12 PRELIMINARY 1 Short Title and commencement 5 2 Definitions 6 CHAPTER - II 13-14 APPELLATE TRIBUNAL AND APPOINTMENT OF OFFICERS. 3 Constitution

AP VALUE ADDED TAX ACT 2005 INDEX Section Pg.No. CHAPTER - I 2-12 PRELIMINARY 1 Short Title and commencement 5 2 Definitions 6 CHAPTER - II 13-14 APPELLATE TRIBUNAL AND APPOINTMENT OF OFFICERS. 3 Constitution

Sec - 13 Credit for Input Tax 37 Sec - 14 Tax Invoices 41 Sec - 15 Power of State Government to Grant refund of Tax 41 Sec - 16 Burden of proof 42 CHA

E- BOOK ON +*[ TELANGANA ] VALUE ADDED TAX ACT 2005 * SUBS. FOR THE WORDS ANDHRA PRADESH BY G.O.MS.NO. 32 REV. ( C.T. II ) DEPT., GOVT. OF TELANGANA, DT.15-10-2014 INDEX Section CHAPTER - I PRELIMINARY

E- BOOK ON +*[ TELANGANA ] VALUE ADDED TAX ACT 2005 * SUBS. FOR THE WORDS ANDHRA PRADESH BY G.O.MS.NO. 32 REV. ( C.T. II ) DEPT., GOVT. OF TELANGANA, DT.15-10-2014 INDEX Section CHAPTER - I PRELIMINARY

Guidance on Clause 17(l) Guidance on Clause 17A in the Form No.3CD Select Issues in Accounting for State-Level VAT 29-44

Guidance on Clause 17A in the Form No.3CD Select Issues in Accounting for State-Level VAT 29-44") S. No. Particulars Page No. 1 Clause No.12(a) and (b) Para No.23 of the Guidance Note (2005 Edition) 2 Clause 17(h) of Form 3CD Pra35 of the Guidance Note 2-12 13-17 3 Guidance on Clause 17(l) 18-23 4

S. No. Particulars Page No. 1 Clause No.12(a) and (b) Para No.23 of the Guidance Note (2005 Edition) 2 Clause 17(h) of Form 3CD Pra35 of the Guidance Note 2-12 13-17 3 Guidance on Clause 17(l) 18-23 4

MEANING OF CENTRAL SALES TAX :-

MEANING OF CENTRAL SALES TAX :- Central sales tax is an indirect tax which is imposed by the central government on taxable turnover of inter state sale of goods made by a registered dealer during the prescribed

MEANING OF CENTRAL SALES TAX :- Central sales tax is an indirect tax which is imposed by the central government on taxable turnover of inter state sale of goods made by a registered dealer during the prescribed

CHAPTER III INCIDENCE, LEVY AND RATE OF TAX

CHAPTER III INCIDENCE, LEVY AND RATE OF TAX 6. Determination of taxable turnover. To determine the taxable turnover of sales, the following amounts shall, subject to the conditions specified, be deducted

CHAPTER III INCIDENCE, LEVY AND RATE OF TAX 6. Determination of taxable turnover. To determine the taxable turnover of sales, the following amounts shall, subject to the conditions specified, be deducted

Lecture Meeting Wednesday 21 st January 2009

Bombay Chartered Accountants Society Audit of Accounts Lecture Meeting Wednesday 21 st January 2009 MVAT Audit Some Important Issues - Govind G. Goyal Chartered Accountant Section 61 of MVAT Act requires

Bombay Chartered Accountants Society Audit of Accounts Lecture Meeting Wednesday 21 st January 2009 MVAT Audit Some Important Issues - Govind G. Goyal Chartered Accountant Section 61 of MVAT Act requires

Maintenance Of Records, Data Compilation & Issues In Vat Audit

Maintenance Of Records, Data Compilation & Issues In Vat Audit 26 th November 2014 DILIP PHADKE Chartered Accountant Contact: 28982388/9322231414 e-mail phadke1952@gmail.com IMP. DEFINATIONS SEC. 2 10)

Maintenance Of Records, Data Compilation & Issues In Vat Audit 26 th November 2014 DILIP PHADKE Chartered Accountant Contact: 28982388/9322231414 e-mail phadke1952@gmail.com IMP. DEFINATIONS SEC. 2 10)

CHAPTER II And CHAPTER III INCIDENCE, LEVY AND RATE OF TAX, REGISTRATION

CHAPTER II And CHAPTER III INCIDENCE, LEVY AND RATE OF TAX, REGISTRATION 3. Incidence and levy of tax (1) Subject to the provisions of this Act, every dealer under sub-section (2), shall pay tax in the

CHAPTER II And CHAPTER III INCIDENCE, LEVY AND RATE OF TAX, REGISTRATION 3. Incidence and levy of tax (1) Subject to the provisions of this Act, every dealer under sub-section (2), shall pay tax in the

5. Name / address of the dealer -

FORM - XXIV-B [See rule-45(0)(b) of the UPVAT Rules, 008] Return of Tax Period - monthly / quarterly [To be filled in block letters only]. Assessment Year - -. Tax Period Ending on - d d - m m - y y y

FORM - XXIV-B [See rule-45(0)(b) of the UPVAT Rules, 008] Return of Tax Period - monthly / quarterly [To be filled in block letters only]. Assessment Year - -. Tax Period Ending on - d d - m m - y y y

Government of Gujarat Finance Department, Sachivalaya, Gandhinagar Dated the 1 st, 2006

Government of Gujarat Finance Department, Sachivalaya, Gandhinagar Dated the 1 st, 2006 No. (GHN- ) VAR (1) / 2005 / Th: - WHEREAS the Government of Gujarat is satisfied that circumstances exist which

Government of Gujarat Finance Department, Sachivalaya, Gandhinagar Dated the 1 st, 2006 No. (GHN- ) VAR (1) / 2005 / Th: - WHEREAS the Government of Gujarat is satisfied that circumstances exist which

Answer to MTP_Intermediate_Syllabus 2012_Dec2017_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Form VAT 20. The original Form VAT-20 should be used for filing annual statement for the year

Form VAT 0 The original Form VAT-0 should be used for filing annual statement for the 005-06. (See rule 40 ) (Original) Annual Statement by a taxable person (Please read the INSTRUCTIONS carefully before

Form VAT 0 The original Form VAT-0 should be used for filing annual statement for the 005-06. (See rule 40 ) (Original) Annual Statement by a taxable person (Please read the INSTRUCTIONS carefully before

WIRC of ICAI. Understanding Annual Returns & Reconciliation Statement. Presented By CA. Kevin Shah

WIRC of ICAI Understanding Annual Returns & Reconciliation Statement Presented By CA. Kevin Shah STATUTORY PROVISIONS Section 35 (5) of the CGST Act, 2017 (5) Every registered person whose turnover during

WIRC of ICAI Understanding Annual Returns & Reconciliation Statement Presented By CA. Kevin Shah STATUTORY PROVISIONS Section 35 (5) of the CGST Act, 2017 (5) Every registered person whose turnover during

TAMIL NADU GOVERNMENT GAZETTE

GOVERNMENT OF TAMIL NADU [Regd.No. TN/CCN/117/2006-08. 2006 [price: Rs.28.80 Paise. TAMIL NADU GOVERNMENT GAZETTE EXTRA ORDINARY PUBLISHED BY AUTHORITY No.348 ] CHENNAI, FRIDAY, DECEMBER 15,2006 Karthigai

GOVERNMENT OF TAMIL NADU [Regd.No. TN/CCN/117/2006-08. 2006 [price: Rs.28.80 Paise. TAMIL NADU GOVERNMENT GAZETTE EXTRA ORDINARY PUBLISHED BY AUTHORITY No.348 ] CHENNAI, FRIDAY, DECEMBER 15,2006 Karthigai

Receipt No.. FORM 1 Date of Filing. (See Rule 3) No.: Name of the Registered Dealer.. Address :.

No.: Name of the Registered Dealer.. Address :.") Receipt No.. FORM 1 Date of Filing. (See Rule 3) No.: THE CENTRAL SALES TAX (DELHI) RULES 2005 RETURN OF SALES TAX PAYABLE FOR THE QUARTER/MONTH UNDER THE CENTRAL SALES TAX ACT, 1956 Name of the Registered

Receipt No.. FORM 1 Date of Filing. (See Rule 3) No.: THE CENTRAL SALES TAX (DELHI) RULES 2005 RETURN OF SALES TAX PAYABLE FOR THE QUARTER/MONTH UNDER THE CENTRAL SALES TAX ACT, 1956 Name of the Registered

The Institute of Chartered Accountants of India Western India Regional Council

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

The Institute of Chartered Accountants of India Western India Regional Council Seminar on E-filing of Returns and Forms under Various Acts Mumbai 11 th June 2011 E-filing of Returns and Forms under MVAT

KEY NOTES Atulya Sharma, Advocate (Noida) . :

. :") KEY NOTES Atulya Sharma, Advocate (Noida) Email. : pnsharmamail@yahoo.com The Value Added Tax (Vat Act) has been implemented in the state of U.P. Lot of section and rules are provided under the Vat Act.

KEY NOTES Atulya Sharma, Advocate (Noida) Email. : pnsharmamail@yahoo.com The Value Added Tax (Vat Act) has been implemented in the state of U.P. Lot of section and rules are provided under the Vat Act.

Transferring efficiency Advancing new options. Indirect Tax Seminar Issues and Prospects June 22, 2013 Anjlika Chopra

Transferring efficiency Advancing new options Indirect Tax Seminar Issues and Prospects June 22, 2013 Anjlika Chopra Contents Important obligations under VAT Registration Returns and payment of taxes VAT

Transferring efficiency Advancing new options Indirect Tax Seminar Issues and Prospects June 22, 2013 Anjlika Chopra Contents Important obligations under VAT Registration Returns and payment of taxes VAT

D D M M Y Y Ending on. Taxpayer's Identification Number [TIN] Entitlement Certificate No.

![D D M M Y Y Ending on. Taxpayer's Identification Number [TIN] Entitlement Certificate No.](/thumbs/77/74909038.jpg "D D M M Y Y Ending on. Taxpayer's Identification Number [TIN] Entitlement Certificate No.") FORM - XXVI [See Rule-45(7) of the UPVAT Rules, 2008 and Section 24 (7) & 26 of the UPVAT Act, 2008] Acknowledgement and self assessment of Annual Tax under Section 26 of the UPVAT Act, 2008 1- Assessment

FORM - XXVI [See Rule-45(7) of the UPVAT Rules, 2008 and Section 24 (7) & 26 of the UPVAT Act, 2008] Acknowledgement and self assessment of Annual Tax under Section 26 of the UPVAT Act, 2008 1- Assessment

Transitional Provisions

Transitional Provisions Udayan Choksi 17 May 2017 18-05-2017 1 S139 - Migration of Existing Taxpayers» Migration is for Every existing registered person Having a PAN Shall be issued a certificate of registration

Transitional Provisions Udayan Choksi 17 May 2017 18-05-2017 1 S139 - Migration of Existing Taxpayers» Migration is for Every existing registered person Having a PAN Shall be issued a certificate of registration

THE ODISHA VALUE ADDED TAX ACT, ORISSA ACT 4 OF 2005

1 ORISSA ACT 4 OF 2005 An ACT to provide for the imposition and collection of tax on the sale or purchase of goods in the State. Be it enacted by the Legislature of the State of Orissa in the Fifty-fifth

1 ORISSA ACT 4 OF 2005 An ACT to provide for the imposition and collection of tax on the sale or purchase of goods in the State. Be it enacted by the Legislature of the State of Orissa in the Fifty-fifth

ENTRY TAX ACT

Section Content Page No. Short title and commencement 2 2 Definitions 2 3 Incidence of taxation 4 4 Rate at which entry tax to be charged 7 5 Principles governing levy of entry tax on 32 [dealer or person]

Section Content Page No. Short title and commencement 2 2 Definitions 2 3 Incidence of taxation 4 4 Rate at which entry tax to be charged 7 5 Principles governing levy of entry tax on 32 [dealer or person]

IMPORTANT DATES DIRECT TAXES. TDS / TCS returns are to be filed Quarterly.

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

IMPORTANT DATES DIRECT TAXES TDS / TCS returns are to be filed Quarterly. QUARTER ENDING DUE DATE 30 TH JUNE 15 TH JULY 30 TH SEPTEMBER 15 TH OCTOBER 31 ST DECEMBER 15 TH JANUARY 31 ST MARCH 15 TH MAY

THE GUJARAT VALUE ADDED TAX (AMENDMENT) BILL, GUJARAT BILL NO. 7 OF A BILL. further to amend the Gujarat Value Added Tax Act, 2003.

BILL, GUJARAT BILL NO. 7 OF A BILL. further to amend the Gujarat Value Added Tax Act, 2003.") THE GUJARAT VALUE ADDED TAX (AMENDMENT) BILL, 2006. GUJARAT BILL NO. 7 OF 2006. A BILL further to amend the Gujarat Value Added Tax Act, 2003. It is hereby enacted in the Fifty-seventh Year of the Republic

THE GUJARAT VALUE ADDED TAX (AMENDMENT) BILL, 2006. GUJARAT BILL NO. 7 OF 2006. A BILL further to amend the Gujarat Value Added Tax Act, 2003. It is hereby enacted in the Fifty-seventh Year of the Republic

Composition Levy Under GST- A Boon or Bane

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

Composition Levy Under GST- A Boon or Bane INTRODUCTION T he appointed date for Goods and Services Tax Law (GST Law or GST) role out is 1st of July, 2017. GST Law will affect, directly and indirectly,

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

GOVERNMENT OF PUNJAB EXCISE AND TAXATION DEPARTMENT (EXCISE AND TAXATION II BRANCH) Notification

Notification") GOVERNMENT OF PUNJAB EXCISE AND TAXATION DEPARTMENT (EXCISE AND TAXATION II BRANCH) Notification The 31 st August, 2006 No. S.O. 41/P.A.8/2005/S. 2/2006. In pursuance of the provisions of item (6) of clause

GOVERNMENT OF PUNJAB EXCISE AND TAXATION DEPARTMENT (EXCISE AND TAXATION II BRANCH) Notification The 31 st August, 2006 No. S.O. 41/P.A.8/2005/S. 2/2006. In pursuance of the provisions of item (6) of clause

Form DVAT 04 Cover Page

Department of Value Added Tax Government of NCT of Delhi Form DVAT 04 Cover Page (See Rule 12 of the Delhi Value Added Tax Rules, 2005) Application for Registration under Delhi Value Added Tax Act, 2004

Department of Value Added Tax Government of NCT of Delhi Form DVAT 04 Cover Page (See Rule 12 of the Delhi Value Added Tax Rules, 2005) Application for Registration under Delhi Value Added Tax Act, 2004

MVAT AUDIT REQUIRMENT for F.Y

Prepared by :- Amit Todkari MVAT AUDIT REQUIRMENT for F.Y 2010-11 ( A ) General InformatIon 1 MVAT & CST Number* : MVAT - CST - 2 Income Tax Audit Report in Form 3CA & 3CD with all annexures of Current

Prepared by :- Amit Todkari MVAT AUDIT REQUIRMENT for F.Y 2010-11 ( A ) General InformatIon 1 MVAT & CST Number* : MVAT - CST - 2 Income Tax Audit Report in Form 3CA & 3CD with all annexures of Current

1- Assessment Year

FORM-LII-B DEPARTMENT OF COMMERCIAL TAXES,GOVERNMENT OF UTTAR PRADESH ( See sub-rule(7) of Rule 45 of U.P. VAT Rules, 2008 ) Annexures of Consolidated Details ( For the works contractors / Transfer of

FORM-LII-B DEPARTMENT OF COMMERCIAL TAXES,GOVERNMENT OF UTTAR PRADESH ( See sub-rule(7) of Rule 45 of U.P. VAT Rules, 2008 ) Annexures of Consolidated Details ( For the works contractors / Transfer of

S.O. No 219/ Date: In exercise of the powers conferred by Section 94 of the Jharkhand Value Added Tax Act, 2005 (Jharkhand Act 05, 2006),

,") S.O. No 219/ Date:- 31.03.2006 In exercise of the powers conferred by Section 94 of the Jharkhand Value Added Tax Act, 2005 (Jharkhand Act 05, 2006), the Governor of Jharkhand hereby makes the following

S.O. No 219/ Date:- 31.03.2006 In exercise of the powers conferred by Section 94 of the Jharkhand Value Added Tax Act, 2005 (Jharkhand Act 05, 2006), the Governor of Jharkhand hereby makes the following

1 GOVERNMENT OF JHARKHAND COMMERCIAL TAXES DEPARTMENT NOTIFICATION CENTRAL SALES TAX (JHARKHAND) RULES, 2006

RULES, 2006") 1 GOVERNMENT OF JHARKHAND COMMERCIAL TAXES DEPARTMENT NOTIFICATION CENTRAL SALES TAX (JHARKHAND) RULES, 2006 S.O. 143 dated 23.07.2011 In exercise of the powers conferred by sub-section (3) and (4) of

1 GOVERNMENT OF JHARKHAND COMMERCIAL TAXES DEPARTMENT NOTIFICATION CENTRAL SALES TAX (JHARKHAND) RULES, 2006 S.O. 143 dated 23.07.2011 In exercise of the powers conferred by sub-section (3) and (4) of

THE CENTRAL SALES TAX (RAJASTHAN) RULES,

RULES,") THE CENTRAL SALES TAX (RAJASTHAN) RULES, 1957 In exercise of the powers conferred by sub-section (3) and (4) of section 13 of the Central Sales Tax Act, 1956 (Central Act 74 of 1956) the State Government

THE CENTRAL SALES TAX (RAJASTHAN) RULES, 1957 In exercise of the powers conferred by sub-section (3) and (4) of section 13 of the Central Sales Tax Act, 1956 (Central Act 74 of 1956) the State Government

Get More Updates From Caultimates.com Join with us : CENTRAL SALES TAX. Categories of sales

Get More Updates From Caultimates.com Join with us : http://facebook.com/groups/caultimates Central Sales Tax 66 CENTRAL SALES TAX Categories of sales Sales may be classified as:- (i) Intra-State sales

Get More Updates From Caultimates.com Join with us : http://facebook.com/groups/caultimates Central Sales Tax 66 CENTRAL SALES TAX Categories of sales Sales may be classified as:- (i) Intra-State sales

THE UTTAR PRADESH VALUE ADDED TAX ACT, 2008 AS AMENDED

THE UTTAR PRADESH VALUE ADDED TAX ACT, 2008 AS AMENDED BY Act no. 19 of 2010 (dt. 20-08-2010) Notification No 1335 dt 10-09-2010 Notification No 421 dt 31-03-2011 Notification No 930 dt 01-09-2011 Notification

THE UTTAR PRADESH VALUE ADDED TAX ACT, 2008 AS AMENDED BY Act no. 19 of 2010 (dt. 20-08-2010) Notification No 1335 dt 10-09-2010 Notification No 421 dt 31-03-2011 Notification No 930 dt 01-09-2011 Notification

Technical Guide Goa VATT The Institute of Chartered Accountants of India New Delhi

Technical Guide to Goa VAT The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No part of this

Technical Guide to Goa VAT The Institute of Chartered Accountants of India (Set up by an Act of Parliament) New Delhi The Institute of Chartered Accountants of India All rights reserved. No part of this

7 VAT Procedures. 1. Registration. Learning objectives

7 VAT Procedures Learning objectives After reading this chapter you will be able to understand: the provisions relating to registration under VAT laws. what is tax payer identification number (TIN). the

7 VAT Procedures Learning objectives After reading this chapter you will be able to understand: the provisions relating to registration under VAT laws. what is tax payer identification number (TIN). the

GOVERNMENT OF NAGALAND. The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017)

") GOVERNMENT OF NAGALAND The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) An ACT to make a provision for levy and collection

GOVERNMENT OF NAGALAND The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) The Nagaland Goods and Services Tax Act, 2017 (Act No. 4 of 2017) An ACT to make a provision for levy and collection

ISSUES ON GST FOR PANEL DISCUSSION TO BE HELD ON 13 th AUGUST, 2017

ISSUES ON GST FOR PANEL DISCUSSION TO BE HELD ON 13 th AUGUST, 2017 1. Developer has given work contract to construct the building to a work contractor in 2016. Developer had made the payment after deducting

ISSUES ON GST FOR PANEL DISCUSSION TO BE HELD ON 13 th AUGUST, 2017 1. Developer has given work contract to construct the building to a work contractor in 2016. Developer had made the payment after deducting

Impact and Issues in GST in Textiles and Ancilliary Industries

GMAS Impact and Issues in GST in Textiles and Ancilliary Industries PRESENTATION BY CA. GAURAV V SAVE MEGA GST SERIES ON SECTORAL IMPACTS WIRC OF ICAI MUMBAI, JULY 28, 2018 Imp elements Sec 2(5) agent

GMAS Impact and Issues in GST in Textiles and Ancilliary Industries PRESENTATION BY CA. GAURAV V SAVE MEGA GST SERIES ON SECTORAL IMPACTS WIRC OF ICAI MUMBAI, JULY 28, 2018 Imp elements Sec 2(5) agent

CERTIFICATE COURSE ON INDIRECT TAXES

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

UNION TERRITORY GOODS AND SERVICES TAX ACT, 2017

UNION TERRITORY GOODS AND SERVICES TAX ACT, 2017 [14 OF 2017]* An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Union territories and

UNION TERRITORY GOODS AND SERVICES TAX ACT, 2017 [14 OF 2017]* An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Union territories and

GST Concept and Road Map... Atul Gupta

GST Concept and Road Map... Atul Gupta Goods and Service Tax What will be incidence of tax (which Activity will attract GST Definition of Supply. Schedule 1 & 2 Classification Based on HSN, A/c Code for

GST Concept and Road Map... Atul Gupta Goods and Service Tax What will be incidence of tax (which Activity will attract GST Definition of Supply. Schedule 1 & 2 Classification Based on HSN, A/c Code for

By: CA Sanjay Dhariwal

By: CA Sanjay Dhariwal sanjay@dnsconsulting.net 9972070601 Specific issues under Stock transfer: Consignment Sales, Inter unit transaction (Separate and Centralized Registration within State), E-commerce,

By: CA Sanjay Dhariwal sanjay@dnsconsulting.net 9972070601 Specific issues under Stock transfer: Consignment Sales, Inter unit transaction (Separate and Centralized Registration within State), E-commerce,

Applicability of audit under MVAT Act, 2002 To whom audit is applicable? As per Section 61(1) of the MVAT Act, 2002, audit is applicable to A dealer w

of the MVAT Act, 2002, audit is applicable to A dealer w") MVAT AUDIT 2013 Approach & Important Issues 25 TH November, 2013 By 1 Applicability of audit under MVAT Act, 2002 To whom audit is applicable? As per Section 61(1) of the MVAT Act, 2002, audit is applicable

MVAT AUDIT 2013 Approach & Important Issues 25 TH November, 2013 By 1 Applicability of audit under MVAT Act, 2002 To whom audit is applicable? As per Section 61(1) of the MVAT Act, 2002, audit is applicable

GST MSME SECTORAL SERIES CENTRAL BOARD OF EXCISE & CUSTOMS. Directorate General of Taxpayer Services. Follow

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

GST SECTORAL SERIES MSME Directorate General of Taxpayer Services CENTRAL BOARD OF EXCISE & CUSTOMS www.cbec.gov.in Question 55: Whether a registered person under the composition scheme needs to learn

UPDATE ON AMENDMENTS TO CGST ACT, 2017

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

Form VAT 15. Name of the person: Address of the person: address :

Form VAT 15 Return by a Taxable Person (See rule 36) (Please read the INSTRUCTIONS carefully before filling the form and worksheet) VRN For period (dd.mm.yy) From To Name of the person: Address of the

Form VAT 15 Return by a Taxable Person (See rule 36) (Please read the INSTRUCTIONS carefully before filling the form and worksheet) VRN For period (dd.mm.yy) From To Name of the person: Address of the

GST VALUATION H DAVE & CO. CHARTERED ACCOUNTANT FOR WIRC, MUMBAI

GST VALUATION H DAVE & CO. CHARTERED ACCOUNTANT FOR WIRC, MUMBAI Valuation under MVAT Act,2002 Incidence of TAX is on the basis of Turnover of Sales and Purchases There are no Provisions for Valuation

GST VALUATION H DAVE & CO. CHARTERED ACCOUNTANT FOR WIRC, MUMBAI Valuation under MVAT Act,2002 Incidence of TAX is on the basis of Turnover of Sales and Purchases There are no Provisions for Valuation

THE UTTAR PRADESH VALUE ADDED TAX ACT, 2008 ACT

No. 433 (2)-79-V-1-08-1(ka)-1-2008 Dated Lucknow, February 27, 2008 In pursuance of the provisions of clause (3) of Articla 348 of the Constitution of India, the Governor is pleased to order the publication

No. 433 (2)-79-V-1-08-1(ka)-1-2008 Dated Lucknow, February 27, 2008 In pursuance of the provisions of clause (3) of Articla 348 of the Constitution of India, the Governor is pleased to order the publication

PUNJAB VIDHAN SABHA BILL NO. 10-PLA-2017 THE PUNJAB GOODS AND SERVICES TAX BILL, 2017 BILL

PUNJAB VIDHAN SABHA BILL NO. 10-PLA-2017 THE PUNJAB GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the

PUNJAB VIDHAN SABHA BILL NO. 10-PLA-2017 THE PUNJAB GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR

TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR") GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

GOODS AND SERVICE TAX (GST) TRANSITIONAL PROVISIONS COMPILED AND PREPARED BY : CA SAGAR THAKKAR PRESENTATION COVERAGE TRANSITIONAL PROVISIONS UNDER CGST/SGST ACT SEC. 139 TO 142 OF CGST ACT TRANSITIONAL

Workshop on GST Audit

Workshop on GST Audit Organized Jointly by GSTPAM, AIFTP(WZ), BCAS, CTC, MCTC & WIRC OF ICAI 1 Presentation by CA Pranav Kapadia Partner APMH & Associates LLP Original GST Compliance Landscape GSTR 1 GSTR

Workshop on GST Audit Organized Jointly by GSTPAM, AIFTP(WZ), BCAS, CTC, MCTC & WIRC OF ICAI 1 Presentation by CA Pranav Kapadia Partner APMH & Associates LLP Original GST Compliance Landscape GSTR 1 GSTR

CENTRAL SALES TAX (REGISTRATION & TURNOVER) RULES, 1957 (as on 5th March 2014)

RULES, 1957 (as on 5th March 2014)") Rule 1 Central Sales Tax (Registration & Turnover) Rules, 1957 CENTRAL SALES TAX (REGISTRATION & TURNOVER) RULES, 1957 (as on 5th March 2014) 1 These Rules may be called the Central Sales Tax (Registration

Rule 1 Central Sales Tax (Registration & Turnover) Rules, 1957 CENTRAL SALES TAX (REGISTRATION & TURNOVER) RULES, 1957 (as on 5th March 2014) 1 These Rules may be called the Central Sales Tax (Registration

2- Assessment Period begins from D D M M Y Y Ending on D D M M Y Y. 4- Taxpayer's Identification Number [TIN]

![2- Assessment Period begins from D D M M Y Y Ending on D D M M Y Y. 4- Taxpayer's Identification Number [TIN]](/thumbs/77/75515048.jpg "2- Assessment Period begins from D D M M Y Y Ending on D D M M Y Y. 4- Taxpayer's Identification Number [TIN]") UPVT- XXVI-B [See Rule-45(7) of the UPVAT Rules, 2008 and Section 24 (7) & 26 of the UPVAT Act, 2008] Acknowledgement and self assessment of Annual Tax for works contractors/transfer of right to use 1-

UPVT- XXVI-B [See Rule-45(7) of the UPVAT Rules, 2008 and Section 24 (7) & 26 of the UPVAT Act, 2008] Acknowledgement and self assessment of Annual Tax for works contractors/transfer of right to use 1-

CENTRAL GOODS AND SERVICES TAX ACT, 2017

CENTRAL GOODS AND SERVICES TAX ACT, 2017 [12 OF 2017]* An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Central Government and the matters

CENTRAL GOODS AND SERVICES TAX ACT, 2017 [12 OF 2017]* An Act to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the Central Government and the matters

MTP_Intermediate_Syllabus 2016_Dec2017_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Form 221 Return form for only VAT dealer

Form 221 Return form for only VAT dealer The following instructions may please be noted before filling the return 1. Please use the correct return form. This return form is for all VAT dealers other than

Form 221 Return form for only VAT dealer The following instructions may please be noted before filling the return 1. Please use the correct return form. This return form is for all VAT dealers other than

Preliminary and Administration

Chapter I Preliminary and Administration FAQ s Definitions (Section 2) Section 2 of the Central Goods and Services Tax Act, 2017 ( the CGST Act, 2017 or the CGST Act ) Agriculturist [Section 2(7)] Q1.

Chapter I Preliminary and Administration FAQ s Definitions (Section 2) Section 2 of the Central Goods and Services Tax Act, 2017 ( the CGST Act, 2017 or the CGST Act ) Agriculturist [Section 2(7)] Q1.

The following instructions may please be noted before filling the return

The following instructions may please be noted before filling the return Form 225 1. Please use the correct return form. This return form is for all Notified Oil Companies. (Transactions by Oil Companies

The following instructions may please be noted before filling the return Form 225 1. Please use the correct return form. This return form is for all Notified Oil Companies. (Transactions by Oil Companies

Draft Tamil Nadu Value Added Tax Rules, 2006

Draft Tamil Nadu Value Added Tax Rules, 2006 In exercise of the powers conferred by subsection (1) of section 80 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 37 of 2006), the Governor of

Draft Tamil Nadu Value Added Tax Rules, 2006 In exercise of the powers conferred by subsection (1) of section 80 of the Tamil Nadu Value Added Tax Act, 2006 (Tamil Nadu Act 37 of 2006), the Governor of

THE Uttar Pradesh GOODS AND SERVICES TAX BILL, 2017 BILL

THE Uttar Pradesh GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the State of Uttar Pradesh and the matters

THE Uttar Pradesh GOODS AND SERVICES TAX BILL, 2017 A BILL to make a provision for levy and collection of tax on intra-state supply of goods or services or both by the State of Uttar Pradesh and the matters

DUAL TAX METHOD IN INTRA STATE SUPPLY

DUAL TAX METHOD IN INTRA STATE SUPPLY 1 INTRA STATE SUPPLY OF GOODS-Section 8(1) of IGST Act (1) Subject to the provisions of section 10, supply of goods where the location of the supplier and the place

DUAL TAX METHOD IN INTRA STATE SUPPLY 1 INTRA STATE SUPPLY OF GOODS-Section 8(1) of IGST Act (1) Subject to the provisions of section 10, supply of goods where the location of the supplier and the place

DEPARTMENT OF LAW, JUSTICE AND LEGISLATIVE AFFARIS NOTIFICATION

PART IV] DELHI GAZETTE : EXTRAORDINARY 113 4 of 1882. DEPARTMENT OF LAW, JUSTICE AND LEGISLATIVE AFFARIS NOTIFICATION Delhi, the 14th June, 2017 No. F.14(3)/LA-2017/ cons2law / 49-58. The following Act

PART IV] DELHI GAZETTE : EXTRAORDINARY 113 4 of 1882. DEPARTMENT OF LAW, JUSTICE AND LEGISLATIVE AFFARIS NOTIFICATION Delhi, the 14th June, 2017 No. F.14(3)/LA-2017/ cons2law / 49-58. The following Act

NOTES ON CENTRAL SALES TAX Sec.3, Sec.4, Sec.5, Sec.6A & Sec. 6(2)

") NOTES ON CENTRAL SALES TAX Sec.3, Sec.4, Sec.5, Sec.6A & Sec. 6(2) Introduction:- Sales Tax is a state subject. Entry 92A of List I and entry 54 of List II of the constitution of India demarcates the power

NOTES ON CENTRAL SALES TAX Sec.3, Sec.4, Sec.5, Sec.6A & Sec. 6(2) Introduction:- Sales Tax is a state subject. Entry 92A of List I and entry 54 of List II of the constitution of India demarcates the power

Master class on GST. Institute of Company Secretaries of India - WIRC. CA Ashit Shah. Shah & Savla LLP. Chartered Accountants

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

Master class on GST Institute of Company Secretaries of India - WIRC CA Ashit Shah Chartered Accountants Matters to be covered Job work E-Commerce Valuation of Goods and Services Accounts & Records Tax

Case Studies in Service Tax - Covering various important Issues/ Aspects. July 2014

Case Studies in Service Tax - Covering various important Issues/ Aspects July 2014 Index 1 Exemption limit of Rs. 10 lakh 2 Reverse Charge Mechanism 3 Place of Provision of Service 4 CENVAT Credit on Input

Case Studies in Service Tax - Covering various important Issues/ Aspects July 2014 Index 1 Exemption limit of Rs. 10 lakh 2 Reverse Charge Mechanism 3 Place of Provision of Service 4 CENVAT Credit on Input

The following instructions may please be noted before filling the return

Form 222 The following instructions may please be noted before filling the return 1. Please use the correct return form. This return form is for all composition dealers whose entire turnover is under composition

Form 222 The following instructions may please be noted before filling the return 1. Please use the correct return form. This return form is for all composition dealers whose entire turnover is under composition

GOODS AND SERVICE TAX FILING OF RETURN. Prepared by Dharmendra Academy of GST Awareness

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

GOODS AND SERVICE TAX FILING OF RETURN 1 Returns Chapter IX of the CGST/SGST Act, 2017 GST Return Rules, 2017 2 RETURNS: SALIENT FEATURES A return is a statement of specified particulars relating to business

TAX AUDIT POINTS TO BE CONSIDERED

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

TAX AUDIT POINTS TO BE CONSIDERED Contributed by : CA. Tejas Gangar As per section 44AB of the Income tax act, 1961 ( the Act ), certain persons are required to get their accounts audited till 30th September

CHAPTER - III INCIDENCE AND LEVY OF TAX

CHAPTER - III INCIDENCE AND LEVY OF TAX 9. Determination of total turnover:- (1) The total turnover of a dealer for the purposes of these rules shall be the aggregate of- (a) the amount for which goods

CHAPTER - III INCIDENCE AND LEVY OF TAX 9. Determination of total turnover:- (1) The total turnover of a dealer for the purposes of these rules shall be the aggregate of- (a) the amount for which goods

Treading the GST Path 50! FAQ on TDS (GST) (A Team effort of Swamy Associates)

(A Team effort of Swamy Associates)") Treading the GST Path 50! FAQ on TDS (GST) (A Team effort of Swamy Associates) Q 1. What is TDS in GST law? Section 51 of the CGST Act, 2017 (any reference to CGST Act, would refer to the corresponding

Treading the GST Path 50! FAQ on TDS (GST) (A Team effort of Swamy Associates) Q 1. What is TDS in GST law? Section 51 of the CGST Act, 2017 (any reference to CGST Act, would refer to the corresponding

FORM 217 (See sub-rule (1) of rule 44) Audit report under section-63 of Gujarat Value Added Tax Act, 2003.

of rule 44) Audit report under section-63 of Gujarat Value Added Tax Act, 2003.") FORM 217 (See sub-rule (1) of rule 44) Audit report under section-63 of Gujarat Value Added Tax Act, 2003. To, M/s.... 1. I/We have verified correctness and completeness of the annual return with reference

FORM 217 (See sub-rule (1) of rule 44) Audit report under section-63 of Gujarat Value Added Tax Act, 2003. To, M/s.... 1. I/We have verified correctness and completeness of the annual return with reference

fgekpy izns'k ljdkj 30th June, 2017 Shimla , the

jkti=] fgekpy izns'k fgekpy izns'k jkt; 'kklu }kjk izdkf'kr 'kqøokj] 30 twu] 2017@9 vk"kk

jkti=] fgekpy izns'k fgekpy izns'k jkt; 'kklu }kjk izdkf'kr 'kqøokj] 30 twu] 2017@9 vk"kk