Tax Reform and Deficit Reduction

|

|

|

- Anne Shepherd

- 6 years ago

- Views:

Transcription

1 Tax Reform and Deficit Reduction Professor Jon Forman University of Oklahoma Slides for a panel of the Comm. on Tax Policy and Simplification ABA Section of Taxation Washington, DC May 6, 2011 Overview The Budget Outlook Short-term Long-term Taxes The Current Tax System Recent Tax Reform Proposals 2 1

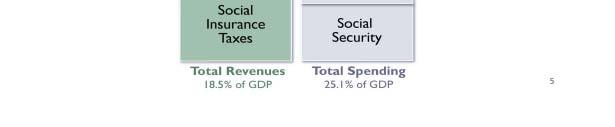

2 Short-Term: Projected Budget Totals Budget Totals, $billions Receipts $2, $39,084 Outlays $3,708 $46,055 Deficit $1,480 $ 6,971 Budget Totals, % GDP Receipts 14.8% 19.9% Outlays 24.7% 23.5% Deficit 9.8% 3.6% Public Debt, % GDP 69.4% 75.3% Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2011 to 2021 (January 2011), 3 Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2011 to 2021 (January 2011), 4 2

3 5 Congressional Budget Office, Four Observations about the Federal Budget (March 7, 2011), at

, at 7 http://www.cbo.gov/ftpdocs/120xx/doc12087/cbo_presentation_to_nabe_3-7-11.")

, http://www.cbo.gov/ftpdocs/120xx/doc12039/01-26_fy2011outlook.")

4 Congressional Budget Office, Four Observations about the Federal Budget (March 7, 2011), at Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2011 to 2021 (January 2011), 8 4

5 9 10 5

6 11 Congressional Budget Office, Four Observations about the Federal Budget (March 7, 2011), at

.")

, at 5,")

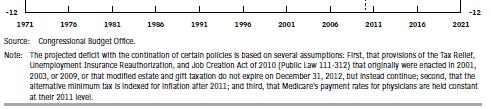

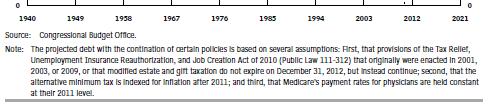

7 U.S. Department of the Treasury, Financial Management Service, A Citizen s Guide to the Financial Report of the United States Government (2009). 13 Congressional Budget Office, The Long-Term Budget Outlook (Revised August 2010), at 5,

, at 12 (Box 1-2).")

8 Factors Explaining Future Federal Spending on Medicare, Medicaid, and Social Security (percentage of GDP) Congressional Budget Office, The Long-Term Budget Outlook (June 2009), at 12 (Box 1-2). Taxes Overview of the federal tax system Recent tax reform proposals 16 8

9 Joint Committee on Taxation, Present Law and Historical Overview of the Federal Tax System (JCX-1-11), January 18, 2011, at 71, 17 Proposed Budget Receipts Receipts, $billions Individual income taxes 998 1,671 Corporation income taxes Payroll taxes 819 1,092 Excise taxes Estate and gift taxes Custom duties and other receipts Total receipts 2,228 3,442 GDP $15,034 $17,258 Receipts, % GDP 14.8% 19.9% Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2011 to 2021 (January 2011),

, Joint Committee January on 18, Taxation, 2011, www.jct.gov.")

10 Center on Budget and Policy Priorities, Top Ten Tax Charts (April 14, 2011), /top-ten-tax-charts/. 19 Joint Committee on Taxation, Present Law and Historical Overview of the Federal Tax System (JCX-1-11), Joint Committee January on 18, Taxation, 2011, Present Law and Historical Overview of the Federal Tax System (JCX-1-11), January 18, 2011, at 70,

11 U.S. Payroll Tax Rates: Selected Years employer rcent paid jointly by employee and Per Medicare Social Security Year 21 Tax-to-GDP ratio, 2008 OECD Tax Database,

, January 18, 2011, at 72,")

12 Edward D. Kleinbard, Muddling Through the Budget Crisis (January 6, 2011); OECD Tax Database, 23 Joint Committee on Taxation, Present Law and Historical Overview of the Federal Tax System (JCX-1-11), January 18, 2011, at 72,

, at")

, http://www.")

13 Congressional Budget Office, Trends in Federal Tax Revenues and Rates (December 2, 2010), at 10, 25 Center on Budget and Policy Priorities, Top Ten Tax Charts (April 14, 2011), /top-ten-tax-charts/

, January 18, 2011, at 66, www.jct.")

, http://www.offthecharts blog.org/top-ten-taxcharts/.")

14 Joint Committee on Taxation, Present Law and Historical Overview of the Federal Tax System (JCX-1-11), January 18, 2011, at 66, 27 Center on Budget and Policy Priorities, Top Ten Tax Charts (April 14, 2011), blog.org/top-ten-taxcharts/

15 Top 10 Income Tax Expenditures, 2012 (Billions) Health insurance exclusion $184 Mortgage interest deduction (k) plans 68 Step-up of basis at death 61 Exclusion of net imputed rental income 51 Deductible nonbusiness state and local taxes other 49 than on houses Employer plans 45 Charitable contrib. (other than health & education) 43 Capital gains (except agriculture, timber, iron, coal) 38 Exclusion of interest on tax-exempt bonds Federal Budget, Analytical Perspectives, Chapter 17, Tax Expenditures, Table 17-3, 29 Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2011 to 2021 (January 2011),

16 Office of Management and the Budget, A New Era of Responsibility: Renewing America s Promise (2009). 31 Productivity and Real Income 20 Facts About U.S. Inequality that Everyone Should Know,

, http://www.census.gov.")

, at 24,")

17 Rising Poverty U.S. Census Bureau, Income, Poverty, and Health Insurance Coverage in the United States: 2009, (Current Population Report No. P60-238, September 2010), 33 Congressional Budget Office, Trends in Federal Tax Revenues and Rates (December 2, 2010), at 24,

18 Rising Inequality Ratio Figure 3. Ratio of Average Household Income of the Top 5 and 20 Percent of Households to the Average Household Income of the Bottom 20 Percent of Households, Top 20%/bottom 20% Top 5%/bottom 20% Year Source: U.S. Census Bureau, table IE-3, 35 Congressional Budget Office, Trends in Federal Tax Revenues and Rates (December 2, 2010), at 15,

19 37 Shares of Total Business Returns and Net Income, S Corporations Returns 4% 8% 11% 12% Net Income 1% 8% 14% 14% Partnerships Returns 11% 8% 8% 10% Net Income 3% 3% 18% 23% Sole Proprietorships Returns 69% 74% 72% 72% Net Income 17% 26% 15% 10% C Corporations Returns 17% 11% 9% 6% Net Income 80% 62% 53% 53% Internal Revenue Service, Statistics of Income,

20 Expired Tax Provisions 2010 First-time homebuyer credit Making work pay credit Build America Bonds Estate and gift tax regime for 2010 Joint Committee on Taxation, List of Expiring Federal Tax Provisions, (JCX-2-11), January 21, 2011, 39 Expiring Tax Provisions 2011 Tax credit for research and experimentation expenses Increased AMT exemption amount Increase in expensing to $500,000/$2,000,000 Above-the-line deduction for qualified tuition and related expenses Temporary 2% payroll tax cut Joint Committee on Taxation, List of Expiring Federal Tax Provisions, (JCX-2-11), January 21, 2011,

, http://www.offthechartsblog.")

21 Expiring Tax Provisions 2012 Most 2001 and 2003 tax cuts 35% maximum rate 10% minimum rate $1,000 child tax credit 15% capital gain and dividend rates Expanded earned income tax credit American opportunity tax credit Reduced estate and gift taxes Joint Committee on Taxation, List of Expiring Federal Tax Provisions, (JCX-2-11), January 21, 2011, 41 Center on Budget and Policy Priorities, Top Ten Tax Charts (April 14, 2011), /top-ten-tax-charts/

22 Recent Tax Reform Proposals President s Economic Recovery Advisory Board, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation (August 2010). National Commission on Fiscal Responsibility and Reform, The Moment of Truth (December 2010). Bipartisan Policy Center, Restoring America s Future (November 2010). Co-Chairs: Pete Domenici & Alice Rivlin 43 Recent Tax Reform Proposals Bipartisan Tax Fairness and Simplification Act of 2011 (2011). Senators Ron Wyden and Dan Coats Rep. Paul Ryan, The Roadmap Plan (2010). National Taxpayer Advocate, 2010 Annual Report to Congress (December 31, 2010). President Obama s FY2012 Budget 44 22

23 Recent Tax Reform Proposals President Obama, Framework for Shared Prosperity and Shared Fiscal Responsibility (April 13, 2011). See also: Choosing The Nation s Fiscal Future (National Research Council & National Academy of Public Administration 2010) The Peterson-Pew Commission on Budget Reform, Red Ink Rising: A Call to Action to Stem the Mounting Federal Debt (2009). 45 Principles of Sound Tax Policy Simplicity Transparency Neutrality Stability No Retroactivity Broad Bases and Low Rates Tax Foundation, The Principles of Sound Tax Policy,

24 More Principles of Sound Tax Policy Distribution matters A just distribution of economic resources Intergenerational justice/ Deficits Behavioral consequences matter Encourage work and savings Marriage penalties and bonuses Keep effective rates as low as possible Growth and a stronger dollar 47 Tax Base Income Consumption Earnings Wealth 48 24

25 PERAB: Simplification Options Simplification for Families Consolidate Family Credits and Simplify Eligibility Rules Simplify and Consolidate Tax Incentives for Education PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation, 49 PERAB: Simplification Options Simplify Savings and Retirement Incentives Consolidate Retirement Accounts Integrate IRA and 401(k)-type Contribution Limits and Disallow Nondeductible Contributions Consolidate Non-Retirement Savings Reduce Retirement Account Leakage Simplify Taxation of Social Security PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation,

26 PERAB: Simplification Options Simplify Taxation of Capital Gains Harmonize Rules and Tax Rates for Long-Term Capital Gains Simplify Capital Gains Tax Rate Structure Limit or Repeal Section 1031 Like-Kind Exchanges Capital Gains on Principal Residences PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation, 51 PERAB: Simplification Options Simplify Tax Filing The Simple Return Data Retrieval Raise the Standard Deduction and Reduce the Benefit of Itemized Deductions Simplification for Small Business The Alternative Minimum Tax PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation,

27 PERAB: Compliance Options Dedicate More Resources to Enforcement and Enhance Enforcement Tools Increase Information Reporting and Source Withholding Clarify the Definition of a Contractor PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation, 53 PERAB: Corporate Tax Reform Reduce Marginal Corporate Rates Broaden the Corporate Tax Base Eliminate or Reduce Tax Expenditures Eliminate the Domestic Production Deduction Eliminate or Reduce Accelerated Depreciation Eliminate Other Tax Expenditures PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation,

28 PERAB: International Corporate Tax Issues Option 1: Move to a Territorial System Option 2: Move to a Worldwide System with a Lower Corporate Tax Rate Option 3: Limit or End Deferral with the Current Corporate Tax Rate Option 4: Retain the Current System but Lower the Corporate Tax Rate PERAB, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation, 55 President s Fiscal Commission Co-chairs: Alan Simpson & Erskine Bowles Designed to raise 21% of GDP Individual tax rates of 12, 22, and 28% Eliminate the AMT Eliminate the phase-out of personal exemptions & limits on itemized deductions Eliminate itemized deductions but retain standard deduction & personal exemptions Tax capital gains & dividends as ordinary income The National Commission on Fiscal Responsibility and Reform, The Moment of Truth (December 2010), Tax Policy Center,

29 President s Fiscal Commission Eliminate tax expenditures except: child credit and earned income tax credit mortgage interest deduction replace with 12% credit; $500,000 mortgage cap cap and phase out the exclusion for employer-sponsored health care charitable giving deduction replace with 12% credit for contributions over 2% AGI The National Commission on Fiscal Responsibility and Reform, The Moment of Truth (December 2010), 57 President s Fiscal Commission Eliminate tax expenditures except: exclusion of interest on state and municipal bonds tax interest only on newly-issued bonds retirement savings maintain basic preferences, but consolidate retirement accounts and cap annual tax-preferred contributions at lower of $20,000 or 20 percent of income; expand savers credit defined benefit pensions The National Commission on Fiscal Responsibility and Reform, The Moment of Truth (December 2010),

30 President s Fiscal Commission Eliminate corporate tax expenditures & reduce corporate tax rate to 28% Territorial tax system for active foreign-source income Increase Social Security taxable wage base to 90% of wages, by 2050 Increase the gasoline excise tax on gasoline by 15 per gallon The National Commission on Fiscal Responsibility and Reform, The Moment of Truth (December 2010), 59 Bipartisan Policy Center Co-Chairs: Pete Domenici & Alice Rivlin one-year payroll tax holiday in 2011 to help stimulate economic recovery individual tax rates: 15% on the 1st $50, of taxable income ($100, for married couples, 27% on excess eliminate the AMT Bipartisan Policy Center, Restoring America s Future (November 2010),

31 Bipartisan Policy Center Eliminate tax expenditures: exclusion from tax of the inside buildup of life insurance and deferred annuities credits and deductions for higher education expenses credit for child & dependent care exclusion from income of benefits under Section 125 cafeteria plans foreign earned income exclusion Bipartisan Policy Center, Restoring America s Future (November 2010), 61 Bipartisan Policy Center Exempt the first $1,000 of net longterm gains from taxation (indexed for inflation) tax any additional long-term gains and all qualified dividends as ordinary income include in income unrealized capital gains at death Cap and phase out the exclusion for employer-sponsored health care Bipartisan Policy Center, Restoring America s Future (November 2010),

32 Bipartisan Policy Center Eliminate deduction for state and local taxes Replace charitable contributions and mortgage interest deductions with 15% refundable credits Retain medical deduction Bipartisan Policy Center, Restoring America s Future (November 2010), 63 Bipartisan Policy Center Replace the standard deduction, personal exemptions, head of household filing status, the child tax credit, and the earned income tax credit with two refundable credits: $1,600 for each dependent child an earnings credit equal to 21.3 percent of the first $20,300 of earnings Bipartisan Policy Center, Restoring America s Future (November 2010),

33 Bipartisan Policy Center Tax all Social Security benefits, eliminate the elderly credit & provide 2 new credits: 7.5% of Social Security benefits 15% of the current standard deduction for individuals age 65 or older Increase Social Security taxable wage base to 90% of wages Bipartisan Policy Center, Restoring America s Future (November 2010), 65 Bipartisan Policy Center Impose a 6.5% broad-based consumption tax Impose an excise tax 1 /ounce on sugar-sweetened beverages Raise the excise tax on alcoholic beverages to 25 /ounce Estate tax: $3.5 million exemption and 45% maximum tax rate Bipartisan Policy Center, Restoring America s Future (November 2010),

34 Bipartisan Policy Center Corporate taxes reduce the corporate rate to 27% eliminate many tax expenditures: domestic production deduction research and experimentation credit accelerated depreciation for rental housing retain deferral of income for controlled foreign corporations Bipartisan Policy Center, Restoring America s Future (November 2010), 67 Wyden-Coats Tax Act Like the Tax Reform Act of 1986 Individuals top tax rate of 35% standard deduction of $15,000 ($30,000 for couples) repeal AMT 35% exclusion for capital gains and qualified dividends eliminate lots of tax breaks Senator Ron Wyden, The Bipartisan Tax Fairness and Simplification Act of 2011 (2011),

35 Wyden-Coats Tax Act Corporate & business replaces the graduated corporate rate structure with a flat rate of 24% eliminates many business tax breaks allow unlimited expensing of equipment and inventories for small businesses Senator Ron Wyden, The Bipartisan Tax Fairness and Simplification Act of 2011 (2011), 69 Rep. Ryan s Roadmap Designed to raise 19% of GDP Pay income taxes through existing law, or Through a highly simplified code with virtually no tax breaks 10% on the first $50, ($100, for couples), 25% on the rest $39,000 standard deduction & personal exemptions for a family of 4 Paul Ryan, The Roadmap Plan (2010),

36 Rep. Ryan s Roadmap eliminate the AMT eliminate taxes on interest, capital gains, and dividends Eliminate the estate tax Replace the corporate income tax with a border-adjustable business consumption tax of 8.5% See also House Committee on Budget, The Path to Prosperity (2011) Paul Ryan, The Roadmap Plan (2010), 71 National Taxpayer Advocate Repeal the AMT Consolidate the family tax provisions Improve other provisions relating to taxation of the family unit Consolidate education savings incentives Consolidate retirement savings incentives National Taxpayer Advocate, 2010 Annual Report to Congress (December 31, 2010),

37 National Taxpayer Advocate Simplify worker classification determinations Eliminate (or reduce incentives for lawmakers to enact tax sunsets Eliminate (or simplify) phase outs Streamline the penalty regime National Taxpayer Advocate, 2010 Annual Report to Congress (December 31, 2010), 73 President Obama: Reform Corporate & Individual Tax I m asking Democrats and Republicans to simplify the system. Get rid of the loopholes. l Level the playing field. And use the savings to lower the corporate tax rate for the first time in 25 years without adding to our deficit. It can be done. In fact, the best thing we could do for all Americans is to simplify the individual tax code. This will be a tough job, but members of both parties have expressed interest in doing this, and I am prepared to join them. Text of President Barack Obama s State of the Union Address,

38 President Obama s 2012 Budget Extend the Earned Income Credit Expand the Dependent Care Credit Extend American Opportunity Credit Tax Dividends and Net Long-Term Capital Gains at a 20-Percent Rate for Upper-Income Taxpayers Reduce the Value of Certain Tax Expenditures for Upper-Income U.S. Department of the Treasury, General Explanations of the Administration s Fiscal Year 2012 Revenue Proposals (February 2011), 75 President Obama s 2012 Budget Enhance and Make Permanent the Research and Experimentation (R&E) Tax Credit Reform & Extend Build America Bonds Reform Treatment of Financial Institutions and Products Reinstate Superfund Taxes Reform U.S. International Tax System U.S. Department of the Treasury, General Explanations of the Administration s Fiscal Year 2012 Revenue Proposals (February 2011),

, http://www.treasury.")

39 President Obama s 2012 Budget Eliminate Oil and Gas Preferences Eliminate Coal Preferences Expand Information Reporting Improve Compliance by Businesses Require Greater Electronic Filing Worker Classification Strengthen Tax Administration Expand Penalties U.S. Department of the Treasury, General Explanations of the Administration s Fiscal Year 2012 Revenue Proposals (February 2011), 77 President Obama s Framework for Shared Prosperity and Shared Fiscal Responsibility The White House,

40 President Obama s Framework: another 12-year estimate: $5.3T Restore high-bracket tax rates to Clinton-era levels: l $1T Cut tax-expenditure spending through the tax code: $1T Cut health care spending: $0.5T Cut other mandatory spending by: $0.4T Cut security spending: $0.4T Cut non-security discretionary spending: $0.8T Those reductions will carry with them a reduction in net interest of: $1.2T Brad DeLong, 79 President Obama s Framework: Tax Reform $3 of spending cuts and interest savings for every $1 from tax reform that contributes to deficit reduction comprehensive tax reform to produce a system which is fairer, has fewer loopholes, less complexity, and is not rigged in favor of those with lawyers and accountants to game it. The White House, Fact Sheet: The President s Framework for Shared Prosperity and Shared Fiscal Responsibility (April 13, 2011),

41 President Obama s Framework: Tax Reform Would not extend the Bush tax cuts for the wealthiest Americans Builds on the Fiscal Commission s goal of reducing tax expenditures to both lower rates and lower the deficit Corporate tax eliminate loopholes reduce distortions lower the corporate tax rate The White House, Fact Sheet: The President s Framework for Shared Prosperity and Shared Fiscal Responsibility (April 13, 2011), 81 Consumption Tax Options Progressive Personal Consumption Tax Subtraction method Value Added Tax Treasury Department proposal for Business Activity Tax (BAT) Credit-method (European) VAT National retail sales tax (RST) Charles E. McClure, Jr., Why the United States Needs a Value Added Tax (2009),

42 Earlier Tax Reform Proposals President s Advisory Panel on Tax Reform, Final Report (2005), rmpanel. U.S. Treasury Department, The President's Tax Proposals to the Congress for Fairness, Growth, and Simplicity (1985)

43 Earlier Tax Reform Proposals U.S. Treasury Department, Tax Reform for Fairness, Simplicity, and Economic Growth: The Treasury Department Report to the President (3 volumes, 1984). David Bradford and the U.S. Treasury Tax Policy Staff, Blueprints for Tax Reform (Arlington, VA: Tax Analysts. 2nd ed. 1984). 85 Conclusion President needs 60 votes in the Senate and cooperation in the House The whole tax system is in play And will be in play for years Lobbyists will be tripping over each other Change is almost always incremental 86 43

44 Sources The President s Economic Recovery Advisory Board, The Report on Tax Reform Options: Simplification, Compliance, and Corporate Taxation (August 2010), The National Commission on Fiscal Responsibility and Reform, The Moment of Truth (December 2010), The Bipartisan Policy Center Debt Reduction Task Force, Restoring America s Future: Reviving the Economy, Cutting Spending and Debt, and Creating a Simple, Pro- Growth Tax System (November 2010), 87 Sources Senators Ron Wyden & Dan Coats, Bipartisan Tax Fairness and Simplification Act of 2011 (2011), b5b603a-ed94-48a8-8ff1-c220c1052b3f. Representative Paul Ryan, The Roadmap Plan (2010), House Committee on Budget, The Path to Prosperity: Restoring America s Promise (2011), gov/uploadedfiles/pathtoprosperity FY2012.pdf. Joint Committee on Taxation, Present Law and Historical Overview of the Federal Tax System (JCX-1-11), January 18, 2011,

45 Sources National Taxpayer Advocate, 2010 Annual Report to Congress (December 31, 2010), Resources/Annual-Report-To-Congress-Full-Report. Office of Management and Budget, 2012 Federal Budget, The White House, Fact Sheet: The President s Framework for Shared Prosperity and Shared Fiscal Responsibility (April 13, 2011), whitehouse Joint Committee on Taxation, List of Expiring Federal Tax Provisions, (JCX-2-11), January 21, 2011, 89 Sources The Tax Policy Center, Deficit Reduction Proposals, org/taxtopics/deficit- Reduction-Proposals.cfm. Joshua Rosenberg, The U.S. Fiscal Trajectory: Causes and Consequences (January 21, 2011), U.S. Department of the Treasury, General Explanations of the Administration s Fiscal Year 2012 Revenue Proposals (February 2011),

.")

46 About the Author Jonathan Barry Forman ( Jon ) is the Alfred P. Murrah Professor of Law at the University of Oklahoma College of Law and the author of Making America Work (Washington, DC: Urban Institute Press, 2006). Jon was the Professor in Residence at the Internal Revenue Service Office of Chief Counsel, Washington, DC, for the academic year. Jon can be reached at jforman@ou.edu, , These slides are available at BA-TAX-forman.ppt

Law and Economic Justice

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 29, 2011 Law and Economic Justice JONATHAN B FORMAN, University of Oklahoma Available at: https://works.bepress.com/jonathan_forman/170/

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 29, 2011 Law and Economic Justice JONATHAN B FORMAN, University of Oklahoma Available at: https://works.bepress.com/jonathan_forman/170/

Should We Replace the Current Pension System with a Universal Pension System

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 27, 2010 Should We Replace the Current Pension System with a Universal Pension System JONATHAN B FORMAN, University

University of Oklahoma College of Law From the SelectedWorks of Jonathan B. Forman April 27, 2010 Should We Replace the Current Pension System with a Universal Pension System JONATHAN B FORMAN, University

xiii Executive Summary

Executive Summary President George W. Bush created the President s Advisory Panel on Federal Tax Reform in January 2005. The President instructed the Panel to recommend options that would make the tax

Executive Summary President George W. Bush created the President s Advisory Panel on Federal Tax Reform in January 2005. The President instructed the Panel to recommend options that would make the tax

2015 Homebuilder CFO Roundtables. Four Seasons Las Vegas June 2015

2015 Homebuilder CFO Roundtables Four Seasons Las Vegas 14-16 June 2015 Page 0 2015 Homebuilder CFO and Tax Director Roundtables 14-16 June 2015 Disclaimer EY refers to the global organization, and may

2015 Homebuilder CFO Roundtables Four Seasons Las Vegas 14-16 June 2015 Page 0 2015 Homebuilder CFO and Tax Director Roundtables 14-16 June 2015 Disclaimer EY refers to the global organization, and may

Tax Reform: An Overview of Proposals in the 112 th Congress

Tax Reform: An Overview of Proposals in the 112 th Congress James M. Bickley Specialist in Public Finance October 26, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Tax Reform: An Overview of Proposals in the 112 th Congress James M. Bickley Specialist in Public Finance October 26, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Using Refundable Tax Credits to Help Lowincome

Using Refundable Tax Credits to Help Lowincome Taxpayers by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma Norman, Oklahoma & ATAX Fellow, UNSW University of Melbourne Melbourne, Australia

Using Refundable Tax Credits to Help Lowincome Taxpayers by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma Norman, Oklahoma & ATAX Fellow, UNSW University of Melbourne Melbourne, Australia

Expiring Tax Provisions

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

Expiring Tax Provisions The term Bush-era tax cuts or Bush tax cuts is often used to describe the tax related reductions that were contained in legislation enacted by Congress in 2001 and 2003, the Economic

FISCAL FACT President s Deficit Commission Says Federal Government Should Be 21 Percent of GDP

December 2, 2010 No. 253 FISCAL FACT President s Deficit Commission Says Federal Government Should Be 21 Percent of GDP Proposal Would Cut Spending and Raise Taxes to Reduce Deficit; Many Principled Tax

December 2, 2010 No. 253 FISCAL FACT President s Deficit Commission Says Federal Government Should Be 21 Percent of GDP Proposal Would Cut Spending and Raise Taxes to Reduce Deficit; Many Principled Tax

Funding Investments for the Common Good with Responsible and Fair Tax Policies

Funding Investments for the Common Good with Responsible and Fair Tax Policies Joan Entmacher National Women s Law Center, 11 Dupont Circle, NW Suite 800 Washington, DC jentmacher@nwlc.org June 11, 2009

Funding Investments for the Common Good with Responsible and Fair Tax Policies Joan Entmacher National Women s Law Center, 11 Dupont Circle, NW Suite 800 Washington, DC jentmacher@nwlc.org June 11, 2009

New Tax Legislation for Low Income Taxpayers

New Tax Legislation for Low Income Taxpayers ABA Tax Section May Meeting Committee on Low Income Taxpayers May 9, 2009 by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma jforman@ou.edu

New Tax Legislation for Low Income Taxpayers ABA Tax Section May Meeting Committee on Low Income Taxpayers May 9, 2009 by Jon Forman Alfred P. Murrah Professor of Law University of Oklahoma jforman@ou.edu

With an August 2 deadline looming,

Budget Control Act of 2011 HIGHLIGHTS Tax Reform Linked To Deficit Reduction Fate Of Bush-Era Tax Cuts Unclear AMT Proposed To Be Abolished Corporate Tax Preferences Under Fire Lower Corporate Tax Rate

Budget Control Act of 2011 HIGHLIGHTS Tax Reform Linked To Deficit Reduction Fate Of Bush-Era Tax Cuts Unclear AMT Proposed To Be Abolished Corporate Tax Preferences Under Fire Lower Corporate Tax Rate

American Taxpayer Relief Act of 2012 & Prospects for Tax Reform

American Taxpayer Relief Act of 2012 & Prospects for Tax Reform Wayne M. Zell, Esq. FPA of the National Capital Area February 1, 2013 Overview A Little Bit of History and 2013 Outlook ATRA 2012 in Detail

American Taxpayer Relief Act of 2012 & Prospects for Tax Reform Wayne M. Zell, Esq. FPA of the National Capital Area February 1, 2013 Overview A Little Bit of History and 2013 Outlook ATRA 2012 in Detail

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE. Reconciliation Recommendations of the Senate Committee on Finance

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE November 26, 2017 Reconciliation Recommendations of the Senate Committee on Finance As ordered reported by the Senate Committee on Finance on November 16, 2017

CONGRESSIONAL BUDGET OFFICE COST ESTIMATE November 26, 2017 Reconciliation Recommendations of the Senate Committee on Finance As ordered reported by the Senate Committee on Finance on November 16, 2017

American Taxpayer Relief Act of 2012 and Other 2012/2013 Tax Highlights 1. Suzanne L. Shier Director of Wealth Planning and Tax Strategy

American Taxpayer Relief Act of 2012 and Other 2012/2013 Tax Highlights 1 Suzanne L. Shier Director of Wealth Planning and Tax Strategy Amanda C. Andrews Wealth Planning Associate January 31, 2013 Chicago

American Taxpayer Relief Act of 2012 and Other 2012/2013 Tax Highlights 1 Suzanne L. Shier Director of Wealth Planning and Tax Strategy Amanda C. Andrews Wealth Planning Associate January 31, 2013 Chicago

Taxes Primer September 27, 2013

Taxes Primer September 27, 2013 WHERE DOES THE MONEY COME FROM? Each year, some of the revenue the federal government collects comes from various taxes. In 2012, taxpayers paid almost $2.5 trillion, which

Taxes Primer September 27, 2013 WHERE DOES THE MONEY COME FROM? Each year, some of the revenue the federal government collects comes from various taxes. In 2012, taxpayers paid almost $2.5 trillion, which

FEDERAL TAX REFORM AND THE STATES

FEDERAL TAX REFORM AND THE STATES Harley Duncan Sally Wallace August 12, 2013 Got conformity? Corporate and individual income taxes come in all shapes and sizes conformity does as well VERY simple look

FEDERAL TAX REFORM AND THE STATES Harley Duncan Sally Wallace August 12, 2013 Got conformity? Corporate and individual income taxes come in all shapes and sizes conformity does as well VERY simple look

October 31, Policy Priorities, October 28, 2011,

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org October 31, 2011 REPUBLICAN PLAN CONTAINS MINUSCULE REVENUE INCREASE ALONGSIDE DEEP

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org October 31, 2011 REPUBLICAN PLAN CONTAINS MINUSCULE REVENUE INCREASE ALONGSIDE DEEP

Tax Reform: An Overview of Proposals in the 111 th Congress

Tax Reform: An Overview of Proposals in the 111 th Congress James M. Bickley Specialist in Public Finance March 19, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and

Tax Reform: An Overview of Proposals in the 111 th Congress James M. Bickley Specialist in Public Finance March 19, 2010 Congressional Research Service CRS Report for Congress Prepared for Members and

What the New Tax Laws Mean to You

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

What the New Tax Laws Mean to You The American Taxpayer Relief Act of 2012 and other 2013 tax provisions January 2013 White Paper AN OVERVIEW OF THE AMERICAN TAXPAYER RELIEF ACT OF 2012 AND OTHER 2013

Senator Kerry s Tax Proposals. Leonard E. Burman and Jeffrey Rohaly 1 Revised July 23, 2004

Senator Kerry s Tax Proposals Leonard E. Burman and Jeffrey Rohaly 1 Revised July 23, 2004 This note provides a very preliminary summary and distributional analysis of Senator Kerry s tax proposals. Some

Senator Kerry s Tax Proposals Leonard E. Burman and Jeffrey Rohaly 1 Revised July 23, 2004 This note provides a very preliminary summary and distributional analysis of Senator Kerry s tax proposals. Some

President Obama Releases 2014 Federal Budget Proposal

Private Wealth Management Products & Services April 2013 President Obama Releases 2014 Federal Budget Proposal 2014 proposal consistent with prior budgets, but enactment is uncertain After more than two

Private Wealth Management Products & Services April 2013 President Obama Releases 2014 Federal Budget Proposal 2014 proposal consistent with prior budgets, but enactment is uncertain After more than two

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now Rich Shavell, CPA, CVA, CCIFP Shavell & Company, P.A. info@shavell.net www.shavell.net 1 THE DISCLAIMER Information provided herein

THE NEW YEAR S DAY TAX BILL: What Contractors Need to Know Right Now Rich Shavell, CPA, CVA, CCIFP Shavell & Company, P.A. info@shavell.net www.shavell.net 1 THE DISCLAIMER Information provided herein

An Overview of Recent Tax Reform Proposals

Mark P. Keightley Specialist in Economics February 28, 2017 Congressional Research Service 7-5700 www.crs.gov R44771 Summary Many agree that the U.S. tax system is in need of reform. Congress continues

Mark P. Keightley Specialist in Economics February 28, 2017 Congressional Research Service 7-5700 www.crs.gov R44771 Summary Many agree that the U.S. tax system is in need of reform. Congress continues

SPECIAL REPORT. IMPACT. At this time, the framework is just a proposal. No legislative. IMPACT. If a tax reform package moves in Congress under the

Tax Briefing GOP s 2017 Tax Reform Framework September 29, 2017 Highlights Reduced and Consolidated Individual Tax Rates Elimination of Personal Exemptions 20% Corporate Tax Rate 25% Pass-through tax rate

Tax Briefing GOP s 2017 Tax Reform Framework September 29, 2017 Highlights Reduced and Consolidated Individual Tax Rates Elimination of Personal Exemptions 20% Corporate Tax Rate 25% Pass-through tax rate

Tax Reform in the 2016 Presidential Campaign

Tax Reform in the 2016 Presidential Campaign Presented by: Robert J. Grossman Shawn Firster Assessment of Tax Policies by the Tax Foundation Tax Foundation: Washington, D.C. based organization founded

Tax Reform in the 2016 Presidential Campaign Presented by: Robert J. Grossman Shawn Firster Assessment of Tax Policies by the Tax Foundation Tax Foundation: Washington, D.C. based organization founded

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

UNIFIED FRAMEWORK FOR FIXING OUR BROKEN TAX CODE SEPTEMBER 27, 2017 1 OVERVIEW It is now time for all members of Congress Democrat, Republican and Independent to support pro-american tax reform. It s time

TAX CUTS AND JOBS ACT. National Economic Council

TAX CUTS AND JOBS ACT National Economic Council December 18, 2017 Massive Tax Cuts and Reforms The TCJA provides $5.5 trillion of tax cuts Nearly 60% of these cuts go to families, not corporations The

TAX CUTS AND JOBS ACT National Economic Council December 18, 2017 Massive Tax Cuts and Reforms The TCJA provides $5.5 trillion of tax cuts Nearly 60% of these cuts go to families, not corporations The

Summary Table of Fiscal Plans

Major Areas of Each Plan Defense Domestic Discretionary Social Security Fiscal Commission Plan Cap 2012 spending at 2011 levels, return to 2008 levels in 2013, then limit growth to half the rate of inflation

Major Areas of Each Plan Defense Domestic Discretionary Social Security Fiscal Commission Plan Cap 2012 spending at 2011 levels, return to 2008 levels in 2013, then limit growth to half the rate of inflation

An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012

An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012 Margot L. Crandall-Hollick Analyst in Public Finance January 10, 2013 CRS Report for Congress Prepared for Members and Committees

An Overview of the Tax Provisions in the American Taxpayer Relief Act of 2012 Margot L. Crandall-Hollick Analyst in Public Finance January 10, 2013 CRS Report for Congress Prepared for Members and Committees

Tax Reform: Reducing Tax Rates and the Deficit October 15, 2012

CHAIRMEN BILL FRENZEL JIM NUSSLE TIM PENNY CHARLIE STENHOLM PRESIDENT MAYA MACGUINEAS DIRECTORS BARRY ANDERSON ERSKINE BOWLES CHARLES BOWSHER STEVE COLL DAN CRIPPEN VIC FAZIO WILLIAM GRADISON WILLIAM GRAY,

CHAIRMEN BILL FRENZEL JIM NUSSLE TIM PENNY CHARLIE STENHOLM PRESIDENT MAYA MACGUINEAS DIRECTORS BARRY ANDERSON ERSKINE BOWLES CHARLES BOWSHER STEVE COLL DAN CRIPPEN VIC FAZIO WILLIAM GRADISON WILLIAM GRAY,

working paper President Obama s First Budget By Veronique de Rugy No March 2009

No. 09-05 March 2009 working paper President Obama s First Budget By Veronique de Rugy The ideas presented in this research are the author s and do not represent official positions of the Mercatus Center

No. 09-05 March 2009 working paper President Obama s First Budget By Veronique de Rugy The ideas presented in this research are the author s and do not represent official positions of the Mercatus Center

Making the IRS Work. Jonathan B. Forman University of Oklahoma College of Law Roberta F. Mann University of Oregon School of Law

Making the IRS Work Jonathan B. Forman University of Oklahoma College of Law Roberta F. Mann University of Oregon School of Law Our Focus Our Paper considers how to redesign the federal tax system so that

Making the IRS Work Jonathan B. Forman University of Oklahoma College of Law Roberta F. Mann University of Oregon School of Law Our Focus Our Paper considers how to redesign the federal tax system so that

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the

Tax Briefing Tax Cuts and Jobs Act December 4, 2017 Highlights Changes to Individual Tax Rates Special Tax Rules for Pass-Throughs Enhanced Child Tax Credit Larger Standard Deduction Corporate Tax Rate

Tax Briefing Tax Cuts and Jobs Act December 4, 2017 Highlights Changes to Individual Tax Rates Special Tax Rules for Pass-Throughs Enhanced Child Tax Credit Larger Standard Deduction Corporate Tax Rate

Social Security and Medicare funding

Chapter 14 Looking Forward 1 Social Security and Medicare funding Medicare projected date of HI Trust Fund depletion is 2030, four years later than projected in last year s report Social Security - After

Chapter 14 Looking Forward 1 Social Security and Medicare funding Medicare projected date of HI Trust Fund depletion is 2030, four years later than projected in last year s report Social Security - After

CONGRESS JANUARY Tax Cuts and Jobs Act (H.R. 1)

") Advanced Planning Group EYE ON JANUARY 2018 Tax Cuts and Jobs Act (H.R. 1) The Tax Cuts and Jobs Act (TCJA) has been passed by Congress and signed by President Trump. TCJA contains major tax revisions

Advanced Planning Group EYE ON JANUARY 2018 Tax Cuts and Jobs Act (H.R. 1) The Tax Cuts and Jobs Act (TCJA) has been passed by Congress and signed by President Trump. TCJA contains major tax revisions

If you have any questions or would like to discuss any of the information in the following pages, please feel free to contact us at (585)

") February 2013 Jeff Bush from the Washington Update recently gave a presentation about the complex and everchanging political and tax environment. We would like to share the highlights of Jeff s presentation

February 2013 Jeff Bush from the Washington Update recently gave a presentation about the complex and everchanging political and tax environment. We would like to share the highlights of Jeff s presentation

The Effects of the Candidates Tax Plans on Households at Different Income Levels: Examples

CTJ October 29, 2008 Citizens for Tax Justice Contact: Bob McIntyre (202) 299-1066 x22 The Effects of the Candidates Tax Plans on Households at Different Income Levels: Examples Presidential candidates

CTJ October 29, 2008 Citizens for Tax Justice Contact: Bob McIntyre (202) 299-1066 x22 The Effects of the Candidates Tax Plans on Households at Different Income Levels: Examples Presidential candidates

Tax policy and tax reform in an uncertain world: What is driving the tax legislative and tax reform agenda, and how to prepare for change

Tax policy and tax reform in an uncertain world: What is driving the tax legislative and tax reform agenda, and how to prepare for change 5 December 2011 Disclaimer Any US tax advice contained herein was

Tax policy and tax reform in an uncertain world: What is driving the tax legislative and tax reform agenda, and how to prepare for change 5 December 2011 Disclaimer Any US tax advice contained herein was

Updated Tables for Using a VAT to Reform the Income Tax

Updated Tables for Using a VAT to Reform the Income Tax Eric Toder, Jim Nunns, and Joseph Rosenberg Urban-Brookings Tax Policy Center November 20, 2013 In 100 Million Unnecessary Returns, Michael Graetz,

Updated Tables for Using a VAT to Reform the Income Tax Eric Toder, Jim Nunns, and Joseph Rosenberg Urban-Brookings Tax Policy Center November 20, 2013 In 100 Million Unnecessary Returns, Michael Graetz,

TAX POLICY CENTER BRIEFING BOOK. Background. Q. What are tax expenditures and how are they structured?

What are tax expenditures and how are they structured? TAX EXPENDITURES 1/5 Q. What are tax expenditures and how are they structured? A. Tax expenditures are special provisions of the tax code such as

What are tax expenditures and how are they structured? TAX EXPENDITURES 1/5 Q. What are tax expenditures and how are they structured? A. Tax expenditures are special provisions of the tax code such as

FISCAL FACT No. 516 July, 2016 Director of Federal Projects Key Findings Embargoed

FISCAL FACT No. 516 July, 2016 Details and Analysis of the 2016 House Republican Tax Reform Plan By Kyle Pomerleau Director of Federal Projects Key Findings The House Republican tax reform plan would reform

FISCAL FACT No. 516 July, 2016 Details and Analysis of the 2016 House Republican Tax Reform Plan By Kyle Pomerleau Director of Federal Projects Key Findings The House Republican tax reform plan would reform

Disclosure 11/1/2011. From Jeff Bush

From Jeff Bush The views and opinions expressed in this presentation are those of the author and presenter and do not necessarily reflect the views and opinions of the sponsoring companies or their affiliates.

From Jeff Bush The views and opinions expressed in this presentation are those of the author and presenter and do not necessarily reflect the views and opinions of the sponsoring companies or their affiliates.

Year-End Tax Tips for Individuals

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

Year-End Tax Tips for Individuals New tax legislation has brought greater certainty to year-end planning, but also created new challenges. There is still time to set up an appointment for year-end planning.

THE TAX CUTS AND JOBS ACT OF 2017

THE TAX CUTS AND JOBS ACT OF 2017 Understanding the Impact and Opportunities for Your Clients VLP1045-0418 Integrated Retirement Integrated Retirement is an independent consulting firm that provides industry

THE TAX CUTS AND JOBS ACT OF 2017 Understanding the Impact and Opportunities for Your Clients VLP1045-0418 Integrated Retirement Integrated Retirement is an independent consulting firm that provides industry

Re: 2012 Year-End Tax Planning for Individuals

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

Re: 2012 Year-End Tax Planning for Individuals To Our Valued Clients and Friends: Year-end tax planning is always complicated by the uncertainty that the following year may bring and 2012 is no exception.

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 20, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 20, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Could US tax reform be a catalyst for disruption for Canadian businesses?

Could US tax reform be a catalyst for disruption for Canadian businesses? In the wake of the November elections that gave Republicans control of the White House and both houses of Congress, the chances

Could US tax reform be a catalyst for disruption for Canadian businesses? In the wake of the November elections that gave Republicans control of the White House and both houses of Congress, the chances

THE PRESIDENTIAL CANDIDATES TAX PLANS. Lucia N. Smeal

THE PRESIDENTIAL CANDIDATES TAX PLANS Lucia N. Smeal 2 PROPOSED CHANGES FOR INDIVIDUALS INDIVIDUAL TAX RATES CLINTON Add a 4% fair share surcharge on incomes over $5 million, to provide 43.6% top marginal

THE PRESIDENTIAL CANDIDATES TAX PLANS Lucia N. Smeal 2 PROPOSED CHANGES FOR INDIVIDUALS INDIVIDUAL TAX RATES CLINTON Add a 4% fair share surcharge on incomes over $5 million, to provide 43.6% top marginal

Government Affairs. The White Papers TAX REFORM.

Government Affairs The White Papers TAX REFORM www.independentagent.com January 3, 2018 Below is a summary of the provisions of the new tax reform law that are most likely to impact Big I members. This

Government Affairs The White Papers TAX REFORM www.independentagent.com January 3, 2018 Below is a summary of the provisions of the new tax reform law that are most likely to impact Big I members. This

New Analysis Finds GOP Tax Plan would Give Richest One Percent of CT Residents $125,380 More Per Year on Average than Obama s Approach

NEWS RELEASE FOR IMMEDIATE RELEASE Wednesday, June 20, 2012 33 Whitney Avenue New Haven, CT 06510 Voice: 203-498-4240 Fax: 203-498-4242 www.ctvoices.org Contact: Wade Gibson, Senior Policy Fellow, CT Voices

NEWS RELEASE FOR IMMEDIATE RELEASE Wednesday, June 20, 2012 33 Whitney Avenue New Haven, CT 06510 Voice: 203-498-4240 Fax: 203-498-4242 www.ctvoices.org Contact: Wade Gibson, Senior Policy Fellow, CT Voices

CONGRESS HAS CUT DISCRETIONARY FUNDING BY $1.5 TRILLION OVER TEN YEARS First Stage of Deficit Reduction Is In Law

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised November 8, 2012 CONGRESS HAS CUT DISCRETIONARY FUNDING BY $1.5 TRILLION OVER

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised November 8, 2012 CONGRESS HAS CUT DISCRETIONARY FUNDING BY $1.5 TRILLION OVER

The Climate in Washington: Partly Cloudy with a Chance of Change

: Partly Cloudy with a Chance of Change IFG Wealth Management Forum April 23, 2012 VOGEL CONSULTING 1 The stark realities Debt as a percentage of GNP is at its highest level since World War II The path

: Partly Cloudy with a Chance of Change IFG Wealth Management Forum April 23, 2012 VOGEL CONSULTING 1 The stark realities Debt as a percentage of GNP is at its highest level since World War II The path

Issue Brief for Congress

Order Code IB95060 Issue Brief for Congress Received through the CRS Web Flat Tax Proposals and Fundamental Tax Reform: An Overview Updated May 1, 2003 James M. Bickley Government and Finance Division

Order Code IB95060 Issue Brief for Congress Received through the CRS Web Flat Tax Proposals and Fundamental Tax Reform: An Overview Updated May 1, 2003 James M. Bickley Government and Finance Division

Our Tax System Revealed. Lee R. Nackman, Ph.D. October 24, 2018

Our Tax System Revealed Lee R. Nackman, Ph.D. October 24, 2018!1 Topics Tax System Desiderata Follow the Money! Social Security Payroll Taxes Sales Taxes Federal Individual Income Taxes The Big Picture:

Our Tax System Revealed Lee R. Nackman, Ph.D. October 24, 2018!1 Topics Tax System Desiderata Follow the Money! Social Security Payroll Taxes Sales Taxes Federal Individual Income Taxes The Big Picture:

Fiscal Challenges for State and Federal Governments

Fiscal Challenges for State and Federal Governments Robert C. Pozen Senior Lecturer, Harvard Business School Senior Fellow, Brookings Institution Agenda Fiscal Crisis in State and Local Governments Outlook

Fiscal Challenges for State and Federal Governments Robert C. Pozen Senior Lecturer, Harvard Business School Senior Fellow, Brookings Institution Agenda Fiscal Crisis in State and Local Governments Outlook

Testimony to the President s Tax Reform Panel

Testimony to the President s Tax Reform Panel John D. Podesta President Center for American Progress May 11, 2005 Overview The Center for American Progress Tax Reform Plan Fair and Responsible Reform The

Testimony to the President s Tax Reform Panel John D. Podesta President Center for American Progress May 11, 2005 Overview The Center for American Progress Tax Reform Plan Fair and Responsible Reform The

Tax Reform in the 114 th Congress: An Overview of Proposals

Tax Reform in the 114 th Congress: An Overview of Proposals Molly F. Sherlock Coordinator of Division Research and Specialist Mark P. Keightley Specialist in Economics March 18, 2016 Congressional Research

Tax Reform in the 114 th Congress: An Overview of Proposals Molly F. Sherlock Coordinator of Division Research and Specialist Mark P. Keightley Specialist in Economics March 18, 2016 Congressional Research

2013 NEW DEVELOPMENTS LETTER

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

2013 NEW DEVELOPMENTS LETTER INTRODUCTION We have witnessed more tax changes and developments in 2013 than in any year in recent memory, and these changes impact virtually every individual and business

The Tax Reform Agenda. Martin Feldstein

The Tax Reform Agenda Martin Feldstein The good news about our tax system is that, over the years, our tax rules have been getting better. Those who write the tax laws have been listening to the advice

The Tax Reform Agenda Martin Feldstein The good news about our tax system is that, over the years, our tax rules have been getting better. Those who write the tax laws have been listening to the advice

THE NATIONAL COMMISSION ON FISCAL RESPONSIBILITY AND REFORM. The Moment of Truth

THE NATIONAL COMMISSION ON FISCAL RESPONSIBILITY AND REFORM The Moment of Truth DECEMBER 2010 II. Tax Reform America's tax code is broken and must be reformed. In the quarter century since the last comprehensive

THE NATIONAL COMMISSION ON FISCAL RESPONSIBILITY AND REFORM The Moment of Truth DECEMBER 2010 II. Tax Reform America's tax code is broken and must be reformed. In the quarter century since the last comprehensive

H.R. 1 TAX CUT AND JOBS ACT. By: Michelle McCarthy, Esq. and Tyler Murray, Esq.

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

H.R. 1 TAX CUT AND JOBS ACT By: Michelle McCarthy, Esq. and Tyler Murray, Esq. Introduction History H.R. 1, known as the Tax Cuts and Jobs Act ( Act ), was introduced on November 2, 2017. It was passed

How the Trump Tax Proposals Might Affect Planning

How the Trump Tax Proposals Might Affect Planning On April 26, 2017, President Donald Trump presented the core principles of his proposal to significantly overhaul the Tax Code. We believe that from a

How the Trump Tax Proposals Might Affect Planning On April 26, 2017, President Donald Trump presented the core principles of his proposal to significantly overhaul the Tax Code. We believe that from a

ESTATE TAXES, DEFICITS and BUDGET IMPLICATIONS

ESTATE TAXES, DEFICITS and BUDGET IMPLICATIONS Stephen J. Entin American Family Business Foundation October 2011 INTRODUCTION The future of the Federal Estate Tax is still uncertain. Over the summer, Congress

ESTATE TAXES, DEFICITS and BUDGET IMPLICATIONS Stephen J. Entin American Family Business Foundation October 2011 INTRODUCTION The future of the Federal Estate Tax is still uncertain. Over the summer, Congress

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 16, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Top Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 16, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Top Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

SPECIAL REPORT. IMPACT. Many of the changes to the Internal Revenue Code in the INDIVIDUALS

Tax Briefing Tax Cuts and Jobs Act December 22, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Tax Briefing Tax Cuts and Jobs Act December 22, 2017 Highlights 37-Percent Top Individual Tax Rate 21-Percent Flat Corporate Tax Rate New Tax Regime for Pass-throughs Individual AMT Retained/Modified Federal

Overview of the Federal Tax System

Overview of the Federal Tax System Molly F. Sherlock Specialist in Public Finance Donald J. Marples Specialist in Public Finance May 16, 2013 CRS Report for Congress Prepared for Members and Committees

Overview of the Federal Tax System Molly F. Sherlock Specialist in Public Finance Donald J. Marples Specialist in Public Finance May 16, 2013 CRS Report for Congress Prepared for Members and Committees

The Tax Cuts and Jobs Act

Advanced Planning The Tax Cuts and Jobs Act Congress has passed the Tax Cuts and Jobs Act, the most sweeping tax reform since 1986. In today s world, pursuing your life s goals is being challenged in new

Advanced Planning The Tax Cuts and Jobs Act Congress has passed the Tax Cuts and Jobs Act, the most sweeping tax reform since 1986. In today s world, pursuing your life s goals is being challenged in new

Tax Alliance for Economic Mobility: Asset Building Tax Policy Reform Proposals Original April 2014, with updates April 2015

Tax Alliance for Economic Mobility: Asset Building Tax Policy Reform Proposals Original April 2014, with updates April 2015 PROPOSAL BACKGROUND RESOURCES Child Savings Universal savings accounts at birth

Tax Alliance for Economic Mobility: Asset Building Tax Policy Reform Proposals Original April 2014, with updates April 2015 PROPOSAL BACKGROUND RESOURCES Child Savings Universal savings accounts at birth

100 West Fifth Street, Suite 1100 Tulsa, Oklahoma Federal Tax Alert. January 4, 2018

100 West Fifth Street, Suite 1100 Tulsa, Oklahoma 74103-4217 918-595-4800 Federal Tax Alert January 4, 2018 Federal Tax Reform; H. R. 1-Tax Cuts and Jobs Act The following is a summary of some of the significant

100 West Fifth Street, Suite 1100 Tulsa, Oklahoma 74103-4217 918-595-4800 Federal Tax Alert January 4, 2018 Federal Tax Reform; H. R. 1-Tax Cuts and Jobs Act The following is a summary of some of the significant

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL34343 Tax Reform: An Overview of Proposals in the 110th Congress James M. Bickley, Government and Finance Division November

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL34343 Tax Reform: An Overview of Proposals in the 110th Congress James M. Bickley, Government and Finance Division November

line of Sight Tax Transitions Navigating the Continuing Complexities of a Changing Landscape Suzanne Shier Tax Strategist

line of Sight 2012 2013 Tax Transitions Navigating the Continuing Complexities of a Changing Landscape Suzanne Shier Tax Strategist We hope you enjoy the latest presentation from Northern Trust s Line

line of Sight 2012 2013 Tax Transitions Navigating the Continuing Complexities of a Changing Landscape Suzanne Shier Tax Strategist We hope you enjoy the latest presentation from Northern Trust s Line

Administration s 2017 Tax Reform Outline

May 2017 taxalerts.plantemoran.com Administration s 2017 Tax Reform Outline White House Calls For Big Individual And Business Tax Cuts, And More President Trump on April 26 unveiled his tax reform outline

May 2017 taxalerts.plantemoran.com Administration s 2017 Tax Reform Outline White House Calls For Big Individual And Business Tax Cuts, And More President Trump on April 26 unveiled his tax reform outline

Can America Govern Itself? Deficits, Debt, and Delay

Can America Govern Itself? Deficits, Debt, and Delay Ron Haskins Senior Fellow, The Brookings Institution Senior Consultant, The Annie E. Casey Foundation Brookings Mountain West University of Nevada,

Can America Govern Itself? Deficits, Debt, and Delay Ron Haskins Senior Fellow, The Brookings Institution Senior Consultant, The Annie E. Casey Foundation Brookings Mountain West University of Nevada,

Why Tax Revenues Must Rise

Why Tax Revenues Must Rise Edward Kleinbard USC Gould School of Law Center in Law, Economics and Organization Research Papers Series No. C13-1 Legal Studies Research Paper Series No. 13-1 February 14,

Why Tax Revenues Must Rise Edward Kleinbard USC Gould School of Law Center in Law, Economics and Organization Research Papers Series No. C13-1 Legal Studies Research Paper Series No. 13-1 February 14,

An Overview of the 2017 Tax Legislation: Impact to Individuals! Prepared by First Foundation Advisors December 2017!!!!!!!!!!

An Overview of the 2017 Tax Legislation: Impact to Individuals Prepared by First Foundation Advisors December 2017 Summary of the Bill On Friday, December 15, the House and Senate Tax Cuts and Jobs Act

An Overview of the 2017 Tax Legislation: Impact to Individuals Prepared by First Foundation Advisors December 2017 Summary of the Bill On Friday, December 15, the House and Senate Tax Cuts and Jobs Act

Tax Cuts & Jobs Act of 2017

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

Tax Cuts & Jobs Act of 2017 WHAT BUSINESSES & S NEED TO KNOW DECEMBER 19, 2017 TO RECEIVE CPE CREDIT Participate in entire webinar Answer polls when they are provided If you are viewing this webinar in

CRS Issue Brief for Congress

Order Code IB95060 CRS Issue Brief for Congress Received through the CRS Web Flat Tax Proposals and Fundamental Tax Reform: An Overview Updated September 30, 2004 James M. Bickley Government and Finance

Order Code IB95060 CRS Issue Brief for Congress Received through the CRS Web Flat Tax Proposals and Fundamental Tax Reform: An Overview Updated September 30, 2004 James M. Bickley Government and Finance

continue to average 0.2 percent of GDP from 2018 through 2028, CBO projects.

74 The Budget and Economic Outlook: 2018 to 2028 April 2018 continue to average 0.2 percent of GDP from 2018 through 2028, CBO projects. Tax Many exclusions, deductions, preferential rates, and credits

74 The Budget and Economic Outlook: 2018 to 2028 April 2018 continue to average 0.2 percent of GDP from 2018 through 2028, CBO projects. Tax Many exclusions, deductions, preferential rates, and credits

Notes Numbers in the text and tables may not add up to totals because of rounding. Unless otherwise indicated, years referred to in this report are fe

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE An Analysis of the President s 2015 Budget APRIL 2014 Notes Numbers in the text and tables may not add up to totals because of rounding. Unless

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE An Analysis of the President s 2015 Budget APRIL 2014 Notes Numbers in the text and tables may not add up to totals because of rounding. Unless

Tax Reform Proposal Signals White House Broad Tax Policy for 2017

When you have to be right White Paper October 24, 2017 Highlights Reduced individual tax rates Elimination of many itemized deductions 20 percent corporate tax rate Repeal of federal estate tax Repatriation

When you have to be right White Paper October 24, 2017 Highlights Reduced individual tax rates Elimination of many itemized deductions 20 percent corporate tax rate Repeal of federal estate tax Repatriation

The current tax landscape and planning opportunities for clients

The current tax landscape and planning opportunities for clients Christopher P. Hennessey Lawyer and CPA Member, Putnam Business Advisory Group Faculty Director, Babson College Executive Education Not

The current tax landscape and planning opportunities for clients Christopher P. Hennessey Lawyer and CPA Member, Putnam Business Advisory Group Faculty Director, Babson College Executive Education Not

Year-end Tax Moves for 2017

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

Year-end Tax Moves for 2017 Holloway Wealth Management One of our main goals as holistic financial advisors is to help our clients recognize tax reducing opportunities within their investment portfolios

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017 SUMMARY FOR 2017 NEW TAX LAW Publication Date: March 2017 Field of Studies: Level: Taxes Basic Cpe Hours: 3 Prerequisites: Advanced Preparation: None None Type

2017 NEW TAX LAW BOOKLET UPDATE MARCH 2017 SUMMARY FOR 2017 NEW TAX LAW Publication Date: March 2017 Field of Studies: Level: Taxes Basic Cpe Hours: 3 Prerequisites: Advanced Preparation: None None Type

Administration s 2017 Tax Reform Outline

April 2017 taxalerts.plantemoran.com Administration s 2017 Tax Reform Outline White House Calls For Big Individual And Business Tax Cuts, And More President Trump has unveiled a tax reform outline the

April 2017 taxalerts.plantemoran.com Administration s 2017 Tax Reform Outline White House Calls For Big Individual And Business Tax Cuts, And More President Trump has unveiled a tax reform outline the

Tax Code Connections: How Changes to Federal Policy Affect State Revenue Technical appendix

A methodology from Feb 2016 Tax Code Connections: How Changes to Federal Policy Affect State Revenue Technical appendix Overview of the tax model The tax model used in this analysis calculates both federal

A methodology from Feb 2016 Tax Code Connections: How Changes to Federal Policy Affect State Revenue Technical appendix Overview of the tax model The tax model used in this analysis calculates both federal

Five Easy Pieces Scorecard

Five Easy Pieces Scorecard John S. Irons, Ph.D. October 19, 2005 As journalists like Nicholas Confessore and Jonathan Chait have recounted, conservatives seeking to shift America away from progressive

Five Easy Pieces Scorecard John S. Irons, Ph.D. October 19, 2005 As journalists like Nicholas Confessore and Jonathan Chait have recounted, conservatives seeking to shift America away from progressive

INTRODUCTION. The Solutions Initiative

Investing in America s Economy: A Budget Blueprint for Economic Recovery and Fiscal Responsibility Economic Policy Institute John Irons, Andrew Fieldhouse, Ethan Pollack, and Rebecca Thiess INTRODUCTION

Investing in America s Economy: A Budget Blueprint for Economic Recovery and Fiscal Responsibility Economic Policy Institute John Irons, Andrew Fieldhouse, Ethan Pollack, and Rebecca Thiess INTRODUCTION

CRS Report for Congress

Order Code RL33443 CRS Report for Congress Received through the CRS Web Flat Tax Proposals and Fundamental Tax Reform: An Overview May 31, 2006 James M. Bickley Specialist in Public Finance Government

Order Code RL33443 CRS Report for Congress Received through the CRS Web Flat Tax Proposals and Fundamental Tax Reform: An Overview May 31, 2006 James M. Bickley Specialist in Public Finance Government

Key Provisions of 2017 Tax Reform

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Priority Guidance Plan

Chapter 16 Looking Forward 1 2014-2015 Priority Guidance Plan Released 8/26/14 317 projects including Employer provided meals under 119 and 132 Regs under 199 on software 1.1502-76 relating to when a member

Chapter 16 Looking Forward 1 2014-2015 Priority Guidance Plan Released 8/26/14 317 projects including Employer provided meals under 119 and 132 Regs under 199 on software 1.1502-76 relating to when a member

President Obama called for expanding

Fiscal Year (FY) 2017 Budget Proposals February 11, 2016 Special Report Highlights Modifications Within NII Tax And SECA Tax New Oil Fee For Infrastructure/Clean Energy Revisions To ACA s Cadillac Tax

Fiscal Year (FY) 2017 Budget Proposals February 11, 2016 Special Report Highlights Modifications Within NII Tax And SECA Tax New Oil Fee For Infrastructure/Clean Energy Revisions To ACA s Cadillac Tax

Donald Trump s election as the 45th

POST-ELECTION TAX POLICY UPDATE November 9, 2016 HIGHLIGHTS New Administration Takes Office In January Possible Revisions To Tax Code For Individuals Possible Revisions To Tax Code For Businesses Remaining

POST-ELECTION TAX POLICY UPDATE November 9, 2016 HIGHLIGHTS New Administration Takes Office In January Possible Revisions To Tax Code For Individuals Possible Revisions To Tax Code For Businesses Remaining

PRESIDENT TRUMP AND TAX REFORM ARE WE THERE YET? CONFUSION REIGNS: WILL SIGNIFICANT REFORM ACTUALLY HAPPEN?

PRESIDENT TRUMP AND TAX REFORM ARE WE THERE YET? CONFUSION REIGNS: WILL SIGNIFICANT REFORM ACTUALLY HAPPEN? Jane Pfeifer and Matt McKinnon AGENDA 1. Interesting Facts 2. History of Proposed Tax Reform

PRESIDENT TRUMP AND TAX REFORM ARE WE THERE YET? CONFUSION REIGNS: WILL SIGNIFICANT REFORM ACTUALLY HAPPEN? Jane Pfeifer and Matt McKinnon AGENDA 1. Interesting Facts 2. History of Proposed Tax Reform

Year-End Tax Planning Letter

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Year-End Tax Planning Letter 2014 The country s taxpayers are facing more uncertainty than usual as they approach the 2014 tax season. They may feel trapped in limbo while Congress is preoccupied with

Generational Outlook: The Federal Budget Now and in the Future THE CONCORD COALITION

Generational Outlook: The Federal Budget Now and in the Future presented by Joshua Gordon, Policy Director THE CONCORD COALITION Composition of Projected FY 2012 Federal Government Revenues and Outlays

Generational Outlook: The Federal Budget Now and in the Future presented by Joshua Gordon, Policy Director THE CONCORD COALITION Composition of Projected FY 2012 Federal Government Revenues and Outlays

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2015

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2015 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 30, 2015 JCX-70-15 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

OVERVIEW OF THE FEDERAL TAX SYSTEM AS IN EFFECT FOR 2015 Prepared by the Staff of the JOINT COMMITTEE ON TAXATION March 30, 2015 JCX-70-15 CONTENTS Page INTRODUCTION... 1 I. SUMMARY OF PRESENT-LAW FEDERAL

The White House Office of the Press Secretary EMBARGOED UNTIL DELIVERY OF THE PRESIDENT S SPEECH APRIL 13, 2011

The White House Office of the Press Secretary EMBARGOED UNTIL DELIVERY OF THE PRESIDENT S SPEECH APRIL 13, 2011 ***EMBARGOED UNTIL DELIVERY OF THE PRESIDENT S SPEECH*** FACT SHEET: THE PRESIDENT S FRAMEWORK

The White House Office of the Press Secretary EMBARGOED UNTIL DELIVERY OF THE PRESIDENT S SPEECH APRIL 13, 2011 ***EMBARGOED UNTIL DELIVERY OF THE PRESIDENT S SPEECH*** FACT SHEET: THE PRESIDENT S FRAMEWORK

EVALUATING BROAD-BASED APPROACHES FOR LIMITING TAX EXPENDITURES

National Tax Journal, December 2013, 66 (4), 807 832 EVALUATING BROAD-BASED APPROACHES FOR LIMITING TAX EXPENDITURES Eric J. Toder, Joseph Rosenberg, and Amanda Eng This paper evaluates six options to

National Tax Journal, December 2013, 66 (4), 807 832 EVALUATING BROAD-BASED APPROACHES FOR LIMITING TAX EXPENDITURES Eric J. Toder, Joseph Rosenberg, and Amanda Eng This paper evaluates six options to

Tax Reform 2017 What to Watch Out For March 22, 2017

NAR Resort and Second Home Property Specialist (RSPS) Webinar Tax Reform 2017 What to Watch Out For March 22, 2017 Presented by Evan M. Liddiard, CPA Sr. Policy Representative Federal Taxation National

NAR Resort and Second Home Property Specialist (RSPS) Webinar Tax Reform 2017 What to Watch Out For March 22, 2017 Presented by Evan M. Liddiard, CPA Sr. Policy Representative Federal Taxation National

Individual Taxation and Planning

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -

Individual Taxation and Planning Brandy Bradley, CPA May 19, 2016 Tax Bracket Comparison 2016 & 2012 2016 MARRIED FILING JOINT 10% - up to $18,550 15% - $18,551 - $75,300 25% - $75,301 - $151,900 28% -