Changes in Service Tax Overview Reverse Charge and VCES Bimal Jain FCA, ACS, LLB, B.Com (Hons)

|

|

|

- Lesley Davidson

- 6 years ago

- Views:

Transcription

1 Changes in Service Tax Overview Reverse Charge and VCES Bimal Jain FCA, ACS, LLB, B.Com (Hons) Co-Chairman of IDT of PHD Chamber of Commerce Member of IDT of FICCI/ Assocham Special Invitee of IDT of ICAI/ ICSI Member of Indirect Tax faculties of ICAI/ICSI/ICWAI

2 TAXATION OF SERVICES NEGATIVE LIST Restoration of Service Specific Accounting codes for Registration & Payment of Service Tax 2

3 Taxable Event - Service Tax S. 66 of Finance Act There shall be levied a tax on the Value of taxable services referred to in various sub clauses of (105) of S.65 and collected in such manner as may be prescribed S. 65(105) Any Service provided or to be provided ( ) Association of Leasing & Financial Service Companies vs. UOI 2010 (20) STR 417 SC Taxable Event Rendering of Service S. 65B (51) Taxable service means any service on which service tax is leviable under section 66B; S. 66B There shall be levied a tax at the rate of 12% on the value of all services, other than those services specified in the negative list, provided or agreed to be provided in the taxable territory by one person to another and collected in such manner as may be prescribed 3

4 Definition of Service S. 65B (44) Service" means Any Activity carried out by a Person for another for Consideration, and includes a Declared service, but shall not include (a) an activity which constitutes merely, (i) a transfer of title in goods or immovable property, by way of sale, gift or in any other manner; or (ii) such transfer, delivery or supply of any goods which is deemed to be sale within Article 366 (29A) of the Constitution; or (iii) a transaction in money or actionable claim; (b) a provision of service by an employee to the employer in the course of or in relation to his employment; Employer Employee / Secondment/ Jt Employment/ Director (c) fees taken in any Court or tribunal established under any law for the time being in force. 4

5 Definition of Service Explanation 1. Nothing contained in this clause shall apply to functions performed by MP, MLA, Other Govt. Officers or Govt. Bodies. Explanation 2. For the purposes of this clause, transaction in money shall not include any activity relating to the use of money or its conversion by cash or by any other mode, from one form, currency or denomination, to another form, currency or denomination for which a separate consideration is charged. Explanation 3. For the purposes of this Chapter, (a) an unincorporated association or a body of persons, as the case may be, and a member thereof shall be treated as distinct persons; (b) an establishment of a person in the taxable territory and any of his other establishment in a non taxable territory shall be treated as establishments of distinct persons. Explanation 4. A person carrying on a business through a branch or agency or representational office in any territory shall be treated as having an establishment in that territory; 5

6 Declared Services S S 66E 9 Activities declared to be Service: Renting of Immovable Property (Entry 49 List II) b. Construction of a complex, building, civil structure for which consideration received before issuance of completion certificate (Entry 49) Temporary Transfer/Permitting Use or Enjoyment of Intellectual Property Rights {IPR -10/9/2004} Development, Design, Implementation etc. of Information Technology Software {IT Software Services 16/5/2008} Agreeing to the obligation or to refrain from an act, or to tolerate an act or a situation, or to do an act; Transfer of goods by way of hiring/ leasing/ licensing without transfer of right to use such goods {16/5/2008} Activity in relation to delivery of goods on hire purchase/ any system of payment by instalments h. Service portion in the execution of a works contract {A -366 (29A)} Service portion in an activity involving supply of food/drinks/article of human 6 consumption Page 6 {A -366 (29A)}

7 TAXATION OF SERVICES NEGATIVE LIST 7

8 Obligation & POT 8

9 Budget Notifications issued under Service Tax laws Notification No. Description 2/2013 Service Tax Seeks to amend Abatement Notification No. 26/2012 Service Tax, dated the20th June, 2012, Effective from: /2013 Service Tax Seeks to amend Mega Exemption Notification No. 25/2012 Service Tax, dated the 20th June, 2012, Effective from /2013 Service Tax Seeks to notify the resident public limited company as a class of persons under sub clause (iii) of clause (b) of section 96A of the Finance Act, Effective from

10 SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME, 2013 (VCES) CHAPTER VI Launched Registered Assessee: 17 Lakhs ST Return Filed: 7 Lakhs SSI (Rs.9 10 Lakhs) / Surrender STC Eligible Person: Non Filers/ Stop Filers No Notice or an Order U/S 72 (Best Judgment) or U/S 73 (Taxes not levied/ not paid or short levied/ short paid or erroneously refunded) or U/S 73A (ST collected to be deposited with CG) has been issued or made before the

11 SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME, 2013 (VCES) CHAPTER VI Ineligible Person: Filed Truthful Return but not deposited ST Inquiry or investigation initiated by way of (i) Search of premises U/S 82 of Finance Act, 1994 (ii) Issuance of summons U/S 14 of CE Act, 1944 (iii)requiring production of accounts, documents or other evidence or Audit has been initiated, Such inquiry, investigation or audit is pending as on

12 SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME, 2013 (VCES) CHAPTER VI Period for Declaration: From October 1, 2007 to December 31, 2012 on or before Pay at least half of that dues before December 31, 2013; remaining half to be paid by: (a)june 30, 2014 without interest; or (b)by December 31, 2014 with interest from July 1, 2014 onwards; Pay Normal liability from January, 2013 as normally being paid under the present law No Refund of payment made under VCES 12

13 SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME, 2013 (VCES) CHAPTER VI Immunity from Interest/ Penalty/ Other Proceedings Consequences of not paying declared Amount: To be recovered as Arrear of land revenue by attaching movable and immovable properties Consequences of not making True declaration: Where Commissioner of Central Excise has reasons to believe that the declaration was substantially false, serve notice to show cause why he should not pay the tax dues not paid or short paid. No action shall be taken after the expiry of one year from the date of declaration. 13

14 SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME, 2013 (VCES) CHAPTER VI Form of Declaration of Tax dues in Form VCES 1 Form of Acknowledgment of Declaration by the designated authority in Form VCES 2, within a period of seven working days from the date of receipt of the declaration Form of Discharge Certificate by the designated authority in Form VCES 3 upon payment of Tax dues declared Any person, if not already registered, take registration Rule 4 of STR CENVAT Credit cannot be utilized for payment of service tax under this scheme; 14

15 SERVICE TAX VOLUNTARY COMPLIANCE ENCOURAGEMENT SCHEME, 2013 (VCES) CHAPTER VI Comments: Biased to Honest Assessee All India Federation of Tax Practitioner & Anothers Vs. UOI [1998 (2) SCC 161] No Secrecy clause as to confidentiality of information Declared tax dues subject to approval by designated authority Neutral & fair Portion of Cut off period for which declaration can be made before December 31, 2013 for the period from October 1, 2007 to December 31, 2012 is beyond period of limitation i.e. 5 Years from the relevant date of declaration. 15

16 Changes in Finance Bill, 2013 Changes in Negative List 16

17 Changes in Negative List 17

18 Changes in Negative List Process amounting to manufacture or production in S. 65B(40) expanded Process on which duties of excise are leviable under section 3 of the Central Excise Act, 1944 or the Medicinal and Toilet Preparations (Excise Duties) Act, 1955 and any process amounting to manufacture of alcoholic liquors for human consumption, opium, Indian hemp and other narcotic drugs and narcotics on which duties of excise are leviable under any State Act for the time being in force Comment: No benefit for past period 18

19 Changes in Negative List S. 66D(l) Pre School & Higher Secondary/ Certified courses recognized by Law/ Approved Vocational course S. 65B (11) (i) a course run by an industrial training institute or an industrial training centre affiliated to the National Council for Vocational Training or State Council for Vocational Training offering courses in designated trades notified under the Apprentices Act, 1961; or Comment: No benefits for past period 19

20 Advance Rulings Notification No. 4/2013 ST dated The benefit of Advance Ruling extended to Resident public limited companies U/S 96A (b)(iii) Public company as defined in S. 3(1)(iv) of Companies Act and Resident in S. 2(42) of IT Act Advance ruling means the determination, by the Authority, of a question of law or fact specified in the application regarding the liability to pay service tax in relation to a service proposed to be provided, by the applicant; 20

21 Changes in Mega Exemption Lists Effective from vide Notification No.3/2013 ST dated

22 Mega Exemption Education Institutions 22

23 Mega Exemption Cinematographic films 23

24 Mega Exemption AC Restaurants Under S. No 19 Exemption will now be available only to non air conditioned/ non centrally air heated restaurants; Earlier air conditioned and license to serve alcohol Rule 2C 24/2012 ST 40% (No Cenvat on Input) Comments: Definition of Service S.65B(44) Inclusion/ exclusion of Deemed Sale A. 366 (29A) K Damodaraswami Naidu Sales tax on 100% value Open Joint in malls e.g. Corn shop/ Ice cream Parlous/ Home delivery/ Take Away/ Self Service/ Sale of MRP based products 24

25 Mega Exemption Railways 25

26 Mega Exemption GTA Under S. No. 21 Services provided by GTA (a) agricultural produce; (b) goods, where gross amount charged for the transportation of goods on a consignment transported in a single carriage does not exceed Rs. 1500/ (c) goods, where gross amount charged for transportation of all such goods for a single consignee does not exceed Rs. 750/ (d) foodstuff including flours, tea, coffee, jaggery, sugar, milk products, salt and edible oil, excluding alcoholic beverages; (e) chemical fertilizer and oilcakes; (f) newspaper or magazines registered with the Registrar of Newspapers; (g) relief materials meant for victims of natural or man made disasters, calamities, accidents or mishap; or (h) defence or military equipments; Earlier: (a) fruits, vegetables, eggs, milk, food grains or pulses in a goods carriage; Clause (b) and (c) above 26

27 Mega Exemption Others Under S. No. 24 The exemptions for vehicle parking to general public is withdrawn. Under S. No 25 Exemption for repair or maintenance service of Govt s aircrafts are being withdrawn but for vessel, exemption will continue. Charitable activities: Benefit to charities providing services for advancement of any other object of general public utility up to Rs. 25 Lakh will not be available. However the threshold exemption will continue to be available up to Rs 10 lakh. 27

28 Changes in Abatement Services Effective from vide Notification No.2/2013 ST dated

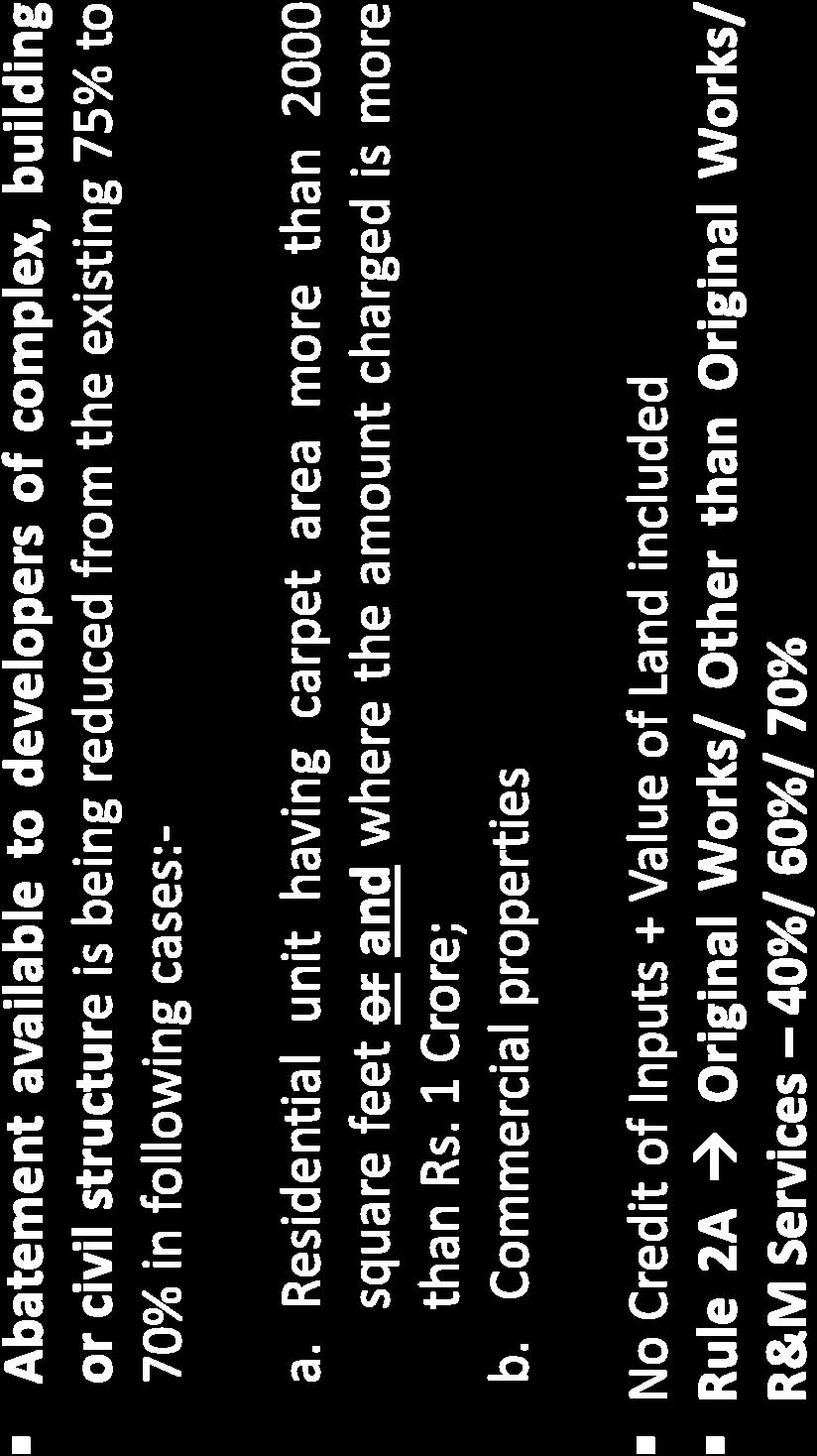

29 Abatement Constructions 29

30 Reverse Charge Service Tax Notification No. 30/2012 ST, dated (Further, amended by Notification No. 45/2012 ST dated ) Services notified U/S 68(2) for reverse charge purposes STR, 1994 amended by Notification No. 36/2012 ST, dated to specify the person liable for paying service tax in respect of such Notified services under Rule 2(1)(d) of the said Rules. 30

31 Partial Reverse Charge Sl. No Description of Service Service Recipient (Business Entity as Body Corporate) Service Provider (Individual, Firm, HUF, AOP) Renting or Hiring of Motor vehicles designed to carry passenger to any person who is not in the similar line of business 7. (a)with abatement CC not availed by SP 100% NIL (b)without abatement CC availed by SP 40% 60% 8. Supply of Manpower for any purpose or Security Services ( ) 75% 25% 9. 31Works Contract Service CS 50% Bimal Jain 50%

32 Reverse Charge -Partial Body Corporate U/S 2(7) of Companies Act, 1956 Includes a Company incorporated outside India but does not include (a) Corporation sole; (b) Registered Co operative Society; (c) Any other body corporate which CG notify in OG (Except a Company as defined in the Act) 32

33 Reverse Charge -Partial Rule 2(1)(g) of STR Supply of manpower means supply of manpower, temporarily or otherwise, to another person to work under his superintendence or control Manpower Recruitment/ Piece Rate/ Hourly Rate basis/ Cleaning Services Rule 2(1)(fa) of STR Security services means services relating to the security of any property, whether movable or immovable, or of any person, in any manner and includes the services of investigation, detection or verification, of any fact or activity 33

34 Reverse Charge Service Tax Notification No. 30/2012-ST Dated 20/06/

35 Reverse Charge 35

36 Reverse Charge 36

37 F-30/31/32, Pankaj Grand Plaza 1 st Floor, Mayur Vihar, Phase I, Delhi India Desktel: Mobile: bimaljain@hotmail.com

ARTICLE. Service Tax (Finance) Act, 1994 By. On Finance Bill (Budget) Proposals 2013 CA. SATISH AGARWAL

Act, 1994 By. On Finance Bill (Budget) Proposals 2013 CA. SATISH AGARWAL") ARTICLE On Finance Bill (Budget) Proposals 01 Service Tax (Finance) Act, 1994 By CA. SATISH AGARWAL Mobile : +919811081957 Phone : +91115769111 Office : 9/14, Ist Flo East Patel Nagar, (Near Jaypee Sidharthe

ARTICLE On Finance Bill (Budget) Proposals 01 Service Tax (Finance) Act, 1994 By CA. SATISH AGARWAL Mobile : +919811081957 Phone : +91115769111 Office : 9/14, Ist Flo East Patel Nagar, (Near Jaypee Sidharthe

Finance Bill-2013-Analysis of Service Tax by CA Atul Kumar Gupta

A. Changes applicable from the date of enactment of Finance Bill, 2013 I. Expansion in the Scope of Negative List:- 1. The agriculture sector has been supported by keeping the bulk of services relating

A. Changes applicable from the date of enactment of Finance Bill, 2013 I. Expansion in the Scope of Negative List:- 1. The agriculture sector has been supported by keeping the bulk of services relating

Budget Amendments 2013 Service Tax

Budget Amendments 2013 Service Tax By: A.Saiprasad B.Com, LLB, ACA, DISA, AMIMA Advocate Meaning of Budget The word Budget was derived from the French word, bougette, which in turn is a diminutive of bouge,

Budget Amendments 2013 Service Tax By: A.Saiprasad B.Com, LLB, ACA, DISA, AMIMA Advocate Meaning of Budget The word Budget was derived from the French word, bougette, which in turn is a diminutive of bouge,

Consignor Or Consignee who is - (a) factory, society, registered dealer of excisable goods, body corporate, partnership firm, AOP &

factory, society, registered dealer of excisable goods, body corporate, partnership firm, AOP &") READY RECKONER S (No Change) Nature of Service Service Provider Service Receiver % of Service Tax Liability Remarks Provid er Receiv er 1 Insurance Insurance Agent Insurance Company 2 Goods Transport Agency

READY RECKONER S (No Change) Nature of Service Service Provider Service Receiver % of Service Tax Liability Remarks Provid er Receiv er 1 Insurance Insurance Agent Insurance Company 2 Goods Transport Agency

Maven Legal Advocates & Consultants BRIEF OF FEW CHANGES MADE IN SERVICE TAX BY FINANCE ACT, 2012, APPLICABLE FROM 1, JULY, 2012

BRIEF OF FEW CHANGES MADE IN SERVICE TAX BY FINANCE ACT, 2012, APPLICABLE FROM 1, JULY, 2012 Budget has unhered a new system of taxation of services known as Negative List Approach. Till now services of

BRIEF OF FEW CHANGES MADE IN SERVICE TAX BY FINANCE ACT, 2012, APPLICABLE FROM 1, JULY, 2012 Budget has unhered a new system of taxation of services known as Negative List Approach. Till now services of

Case Studies in Service Tax - Covering various important Issues/ Aspects. July 2014

Case Studies in Service Tax - Covering various important Issues/ Aspects July 2014 Index 1 Exemption limit of Rs. 10 lakh 2 Reverse Charge Mechanism 3 Place of Provision of Service 4 CENVAT Credit on Input

Case Studies in Service Tax - Covering various important Issues/ Aspects July 2014 Index 1 Exemption limit of Rs. 10 lakh 2 Reverse Charge Mechanism 3 Place of Provision of Service 4 CENVAT Credit on Input

INDIRECT TAX LAWS AMENDMENTS MADE BY THE FINANCE ACT, 2013

1. Amendment to Section 11(2)(n) AMENDMENTS MADE IN CUSTOMS SECTION 11. Power to prohibit importation or exportation of goods (2) (n) the protection of patents, trademarks, copyrights, design and geographical

1. Amendment to Section 11(2)(n) AMENDMENTS MADE IN CUSTOMS SECTION 11. Power to prohibit importation or exportation of goods (2) (n) the protection of patents, trademarks, copyrights, design and geographical

Amnesty Scheme {Chapter VI of Finance Act,2013} Presented By CA Avinash Poddar

Amnesty Scheme {Chapter VI of Finance Act,2013} Presented By CA Avinash Poddar Contents Brief Introduction of Tax Structure Constitutional Validity of Amnesty Schemes Need and Purpose of Amnesty Scheme

Amnesty Scheme {Chapter VI of Finance Act,2013} Presented By CA Avinash Poddar Contents Brief Introduction of Tax Structure Constitutional Validity of Amnesty Schemes Need and Purpose of Amnesty Scheme

Payment of Service Tax under reverse charge A Comprehensive Study

CA. Rajkamal Shah, CA Bhavin Mehta & CA Chirag Bhojani Payment of Service Tax under reverse charge A Comprehensive Study Punishing Peter for the sins of Paul!!! Admittedly, the failure of the Government

CA. Rajkamal Shah, CA Bhavin Mehta & CA Chirag Bhojani Payment of Service Tax under reverse charge A Comprehensive Study Punishing Peter for the sins of Paul!!! Admittedly, the failure of the Government

Goods and Services Tax on Transportation of Goods by Road

988 Goods and Services Tax on Transportation of Goods by Road The levy of Service Tax on Road Transportation Service has always been a contentious issue. The legal position prevailing under Service Tax

988 Goods and Services Tax on Transportation of Goods by Road The levy of Service Tax on Road Transportation Service has always been a contentious issue. The legal position prevailing under Service Tax

SERVICE TAX. BUDGET ANALYSIS All right Reserved with Bizsolindia Services Pvt. Ltd.

SERVICE TAX NEW NOTIFICATION / CIRCULAR ISSUED UNDER SERVICE TAX Notification/Section Existing 3/2015 1/03/2015 Service tax exemption on services provided by commission agent located outside India under

SERVICE TAX NEW NOTIFICATION / CIRCULAR ISSUED UNDER SERVICE TAX Notification/Section Existing 3/2015 1/03/2015 Service tax exemption on services provided by commission agent located outside India under

qwertyuiopasdfghjklzxcvbnmqwertyui opasdfghjklzxcvbnmqwertyuiopasdfgh jklzxcvbnmqwertyuiopasdfghjklzxcvb nmqwertyuiopasdfghjklzxcvbnmqwer

qwertyuiopasdfghjklzxcvbnmqwertyui opasdfghjklzxcvbnmqwertyuiopasdfgh jklzxcvbnmqwertyuiopasdfghjklzxcvb nmqwertyuiopasdfghjklzxcvbnmqwer ALL ABOUT REVERSE CHARGE AND JOINT CHARGE MECHANISM tyuiopasdfghjklzxcvbnmqwertyuiopas

qwertyuiopasdfghjklzxcvbnmqwertyui opasdfghjklzxcvbnmqwertyuiopasdfgh jklzxcvbnmqwertyuiopasdfghjklzxcvb nmqwertyuiopasdfghjklzxcvbnmqwer ALL ABOUT REVERSE CHARGE AND JOINT CHARGE MECHANISM tyuiopasdfghjklzxcvbnmqwertyuiopas

The parameters for availing ITC by a registered taxpayer has been defined in Sec. 16 of CGST Act 2017:

We paid GST 5% ON GTA Freight Inward & Outward on reverse charge mechanism. Now we availed the credit on both inward & outward paid amount. Is it correct or we availed only for inward freight amount. Kindly

We paid GST 5% ON GTA Freight Inward & Outward on reverse charge mechanism. Now we availed the credit on both inward & outward paid amount. Is it correct or we availed only for inward freight amount. Kindly

Negative Blues - V. A Brief Note on Reverse Charge Mechanism. (G. Natarajan, Advocate, Swamy Associates)

") Negative Blues - V A Brief Note on Reverse Charge Mechanism (G. Natarajan, Advocate, Swamy Associates) The general principle in is that provider is liable for payment of tax. But, in certain cases, the

Negative Blues - V A Brief Note on Reverse Charge Mechanism (G. Natarajan, Advocate, Swamy Associates) The general principle in is that provider is liable for payment of tax. But, in certain cases, the

NOTES ON BUDGET 2013

NOTES ON BUDGET 2013 MAJOR AMENDMENTS PROPOSED IN FINANCE BILL 2013 & CHANGES IN SERVICE TAX PROVISIONS Prepared by BY Chartered Accountants 3 rd & 4 th Floor, Vaastu Darshan Bldg., B Wing, Azaad Road,

NOTES ON BUDGET 2013 MAJOR AMENDMENTS PROPOSED IN FINANCE BILL 2013 & CHANGES IN SERVICE TAX PROVISIONS Prepared by BY Chartered Accountants 3 rd & 4 th Floor, Vaastu Darshan Bldg., B Wing, Azaad Road,

TAX LIABILITY UNDER REVERSE CHARGE MECHANISM AND JOINT CHARGE MECHANISM

TAX LIABILITY UNDER REVERSE CHARGE MECHANISM AND JOINT CHARGE MECHANISM - BY CA MAYUR ZANWAR INTRODUCTION Service Tax is a Vital Part of Indirect Tax Structure. It can be spelled as tax on specified services

TAX LIABILITY UNDER REVERSE CHARGE MECHANISM AND JOINT CHARGE MECHANISM - BY CA MAYUR ZANWAR INTRODUCTION Service Tax is a Vital Part of Indirect Tax Structure. It can be spelled as tax on specified services

WIRC INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA. Preamble

WIRC INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Workshop on Service Tax Subject : 1. Point of Taxation Rules, 2011 - amended till date 2. Reverse Charge Mechanism [Section 68(2)] 3. Amendments in Service

WIRC INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Workshop on Service Tax Subject : 1. Point of Taxation Rules, 2011 - amended till date 2. Reverse Charge Mechanism [Section 68(2)] 3. Amendments in Service

Shah & Savla Chartered Accountants

1 Reverse Charge Mechanism & Valuation Rules J. B. Nagar CPE Study Circle CA Ashit Shah Chartered Accountants 2 Matters to be covered Notices: Reverse Charge Mechanism of Taxation [N. No. 30/2012 dated

1 Reverse Charge Mechanism & Valuation Rules J. B. Nagar CPE Study Circle CA Ashit Shah Chartered Accountants 2 Matters to be covered Notices: Reverse Charge Mechanism of Taxation [N. No. 30/2012 dated

FREQUENTLY ASKED QUESTIONS (FAQ) ON SERVICE TAX, CENVAT CREDIT ISSUES AND RELATED PROCEDURAL MATTERS IN INDIAN RAILWAYS.

ON SERVICE TAX, CENVAT CREDIT ISSUES AND RELATED PROCEDURAL MATTERS IN INDIAN RAILWAYS.") 1 FREQUENTLY ASKED QUESTIONS (FAQ) ON SERVICE TAX, CENVAT CREDIT ISSUES AND RELATED PROCEDURAL MATTERS IN INDIAN RAILWAYS Check Note These FAQ have been compiled by the Taxation Cell of Railway Board based

1 FREQUENTLY ASKED QUESTIONS (FAQ) ON SERVICE TAX, CENVAT CREDIT ISSUES AND RELATED PROCEDURAL MATTERS IN INDIAN RAILWAYS Check Note These FAQ have been compiled by the Taxation Cell of Railway Board based

Budget Indirect tax proposals

AMBALAL PATEL & CO CHARTERED ACCOUNTANTS Budget Indirect tax proposals Ambalal Patel & Co 1 St Floor, Sapphire Business Centre Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad 380013 Email: apcca@apcca.com

AMBALAL PATEL & CO CHARTERED ACCOUNTANTS Budget Indirect tax proposals Ambalal Patel & Co 1 St Floor, Sapphire Business Centre Above SBI Vadaj Branch, Usmanpura, Ashram Road, Ahmedabad 380013 Email: apcca@apcca.com

Union Budget 2015 Tax proposals February 28, 2015

Union Budget 2015 Tax proposals February 28, 2015 New Delhi Mumbai Bangalore Hyderabad 1 Union Budget 2015 Efforts on various fronts to implement Goods and Services Tax ( GST ) from next year Effective

Union Budget 2015 Tax proposals February 28, 2015 New Delhi Mumbai Bangalore Hyderabad 1 Union Budget 2015 Efforts on various fronts to implement Goods and Services Tax ( GST ) from next year Effective

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012 A. SERVICE TAX 1. Pursuant to the negative list becoming effective from July 1, 2012, various consequential

SIGNIFICANT NOTIFICATIONS / CIRCULARS ISSUED DURING THE PERIOD 16 TH JUNE, 2012 TO 15 TH JULY, 2012 A. SERVICE TAX 1. Pursuant to the negative list becoming effective from July 1, 2012, various consequential

Description of Service Liability of Recipient of Service Rate of Tax Remarks

The Central Government has expanded the scope of payment of service tax under reverse charge mechanism under the negative list based service taxation. The relevant provisions are contained in Notification

The Central Government has expanded the scope of payment of service tax under reverse charge mechanism under the negative list based service taxation. The relevant provisions are contained in Notification

CHAPTER 1 INTRODUCTION TO GST CHAPTER 2 CHARGE OF GST

1 CHAPTER 1 INTRODUCTION TO GST CHAPTER 2 CHARGE OF GST REVERSE CHARGE IN CASE OF SERVICES {Section 9(3)} {GST To Be Payable Under Reverse Charge On Renting Of Immovable Property By Central/State Government,

1 CHAPTER 1 INTRODUCTION TO GST CHAPTER 2 CHARGE OF GST REVERSE CHARGE IN CASE OF SERVICES {Section 9(3)} {GST To Be Payable Under Reverse Charge On Renting Of Immovable Property By Central/State Government,

CA Pritam Mahure. May 14

CA Pritam Mahure There shall be levied a tax (hereinafter referred to as the service tax) at the rate of twelve per cent. On the value of all services, Other than those services specified in the negative

CA Pritam Mahure There shall be levied a tax (hereinafter referred to as the service tax) at the rate of twelve per cent. On the value of all services, Other than those services specified in the negative

INDIRECT TAXES SERVICE TAX. Amendments effective from

INDIRECT TAXES SERVICE TAX Amendments effective from 02.02.2017 Amendment in Mega Exemption Notification No. 25/2012 ST dated 20.06.2012 Services provided or agreed to be provided by the Army, Naval and

INDIRECT TAXES SERVICE TAX Amendments effective from 02.02.2017 Amendment in Mega Exemption Notification No. 25/2012 ST dated 20.06.2012 Services provided or agreed to be provided by the Army, Naval and

Value of taxable service: (a) 1,000/- Add: Service 14% on (a) 140/- Add: SB 0.5% on (a) 5/- Add: 0.5% on (a) 5/- Total: 1,150/-

1,000/- Add: Service 14% on (a) 140/- Add: SB 0.5% on (a) 5/- Add: 0.5% on (a) 5/- Total: 1,150/-") Dear Professional Colleague, Krishi Kalyan Cess Applicability & Open Issues Pursuing with an objective to finance and promote initiatives to improve agriculture and farmer welfare, the Government announced

Dear Professional Colleague, Krishi Kalyan Cess Applicability & Open Issues Pursuing with an objective to finance and promote initiatives to improve agriculture and farmer welfare, the Government announced

N. K. SHETH & COMPANY

Western Region of Institute of Charted Accountants of India Seminar on Budget Demystified (Indirect ) Subject : Exemption / Abatement in service tax and Amendments in valuation Rules Day & Date : Saturday,

Western Region of Institute of Charted Accountants of India Seminar on Budget Demystified (Indirect ) Subject : Exemption / Abatement in service tax and Amendments in valuation Rules Day & Date : Saturday,

Important Service Tax Amendments through Union Budget 2016 (By CA. Vikas Khandelwal) 1. Krishi Kalyan Cess (Applicable w. e. f

1. Krishi Kalyan Cess (Applicable w. e. f") Important Service Tax Amendments through Union Budget 2016 (By CA. Vikas Khandelwal) 1. Krishi Kalyan Cess (Applicable w. e. f. 01.06.2016): Effective rate of service tax is being increased from 14.5%

Important Service Tax Amendments through Union Budget 2016 (By CA. Vikas Khandelwal) 1. Krishi Kalyan Cess (Applicable w. e. f. 01.06.2016): Effective rate of service tax is being increased from 14.5%

Virtual Certificate Course on GST Organised by: IDT Committee of ICAI

1 Virtual Certificate Course on GST Organised by: IDT Committee of ICAI Sector Specific Studies on Construction Information Technology Tourism Service Trader Manufacturer 23 of June 2017 2 HIGHLIGHTS OF

1 Virtual Certificate Course on GST Organised by: IDT Committee of ICAI Sector Specific Studies on Construction Information Technology Tourism Service Trader Manufacturer 23 of June 2017 2 HIGHLIGHTS OF

DIVISION - I. 2. Basic Concepts of Excise Duty Basic Concepts of Customs Duty Basic Concepts of VAT Basic Concepts of CST 146

Contents DIVISION - I 1. Basic Concepts of Indirect Taxes 1 2. Basic Concepts of Excise Duty 11 3. Basic Concepts of Customs Duty 63 4. Basic Concepts of VAT 101 5. Basic Concepts of CST 146 DIVISION -

Contents DIVISION - I 1. Basic Concepts of Indirect Taxes 1 2. Basic Concepts of Excise Duty 11 3. Basic Concepts of Customs Duty 63 4. Basic Concepts of VAT 101 5. Basic Concepts of CST 146 DIVISION -

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]

![[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]](/thumbs/74/70052643.jpg "[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)]") [TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE CENTRAL BOARD OF EXCISE & CUSTOMS NEW DELHI NOTIFICATION

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II, SECTION 3, SUB-SECTION (i)] GOVERNMENT OF INDIA MINISTRY OF FINANCE DEPARTMENT OF REVENUE CENTRAL BOARD OF EXCISE & CUSTOMS NEW DELHI NOTIFICATION

UNION BUDGET Service tax --- CMA R.K.DEODHAR

UNION BUDGET-2016 Service tax --- CMA R.K.DEODHAR A] CHANGES IN FINANCE ACT,1994 [ To be effective from the date of enactment of Finance Act,2016] 1] Section 65B :- Interpretations :- a)the definition

UNION BUDGET-2016 Service tax --- CMA R.K.DEODHAR A] CHANGES IN FINANCE ACT,1994 [ To be effective from the date of enactment of Finance Act,2016] 1] Section 65B :- Interpretations :- a)the definition

Union Budget CA. Ashok Batra. (The author is a member of the Institute. He can be reached at )

") 1449 Changes in the Finance Act, 1994 And Rules [Except Mega Exemption Notification, Negative List Changes And Cenvat Credit Rules, 2004 Changes] One of the striking features of the Finance Bill, 2015

1449 Changes in the Finance Act, 1994 And Rules [Except Mega Exemption Notification, Negative List Changes And Cenvat Credit Rules, 2004 Changes] One of the striking features of the Finance Bill, 2015

SERVICE TAX EXEMPTION LIMIT 2012 NOTIFICATION

23 April, 2018 SERVICE TAX EXEMPTION LIMIT 2012 NOTIFICATION Document Filetype: PDF 344.62 KB 0 SERVICE TAX EXEMPTION LIMIT 2012 NOTIFICATION Do you want to know about the small service provider exemption?..

23 April, 2018 SERVICE TAX EXEMPTION LIMIT 2012 NOTIFICATION Document Filetype: PDF 344.62 KB 0 SERVICE TAX EXEMPTION LIMIT 2012 NOTIFICATION Do you want to know about the small service provider exemption?..

Background Study Material on Service Tax

Background Study Material on Service Tax CA Bimal Jain FCA, FCS, LLB, B.Com (Hons.) F-30/31/32, Pankaj Grand Plaza, MayurVihar Phase-1,Delhi-110091 E-mail: bimaljain@hotmail.com Mobile: +91 9810604563

Background Study Material on Service Tax CA Bimal Jain FCA, FCS, LLB, B.Com (Hons.) F-30/31/32, Pankaj Grand Plaza, MayurVihar Phase-1,Delhi-110091 E-mail: bimaljain@hotmail.com Mobile: +91 9810604563

Service Tax Voluntary Compliance Encouragement Scheme, 2013

Service Tax Voluntary Compliance Encouragement Scheme, 2013 CHAPTER VI OF FINANCE ACT, 2013 Service Tax Voluntary Compliance Encouragement Scheme, 2013 104. Short title. This Scheme may be called the Service

Service Tax Voluntary Compliance Encouragement Scheme, 2013 CHAPTER VI OF FINANCE ACT, 2013 Service Tax Voluntary Compliance Encouragement Scheme, 2013 104. Short title. This Scheme may be called the Service

WESTERN INDIA REGIONAL COUNCIL THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA. Welcome members and participants

WESTERN INDIA REGIONAL COUNCIL THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Welcome members and participants Subject : Intricacies of Composite Transactions in Construction activities (Valuation, Reverse

WESTERN INDIA REGIONAL COUNCIL THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Welcome members and participants Subject : Intricacies of Composite Transactions in Construction activities (Valuation, Reverse

INDIRECT TAXES CENTRAL EXCISE

INDIRECT TAXES CENTRAL EXCISE Amendments made effective immediately The Clean Energy cess is to be renamed as Clean Environment cess. The effective rate of Clean Energy cess proposed to be increased from

INDIRECT TAXES CENTRAL EXCISE Amendments made effective immediately The Clean Energy cess is to be renamed as Clean Environment cess. The effective rate of Clean Energy cess proposed to be increased from

UPDATE ON AMENDMENTS TO CGST ACT, 2017

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

UPDATE ON AMENDMENTS TO CGST ACT, 2017 Dear Person, August 31, 2018 TEAM TRD An amendment to CGST Act, 2017 has been introduced on 29 th August, 2018 with the following objective by The Central Government:-

INTERMEDIATE EXAMINATION GROUP - II (SYLLABUS 2016)

") INTERMEDIATE EXAMINATION GROUP - II (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS DECEMBER - 2017 Paper-11 : INDIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

INTERMEDIATE EXAMINATION GROUP - II (SYLLABUS 2016) SUGGESTED ANSWERS TO QUESTIONS DECEMBER - 2017 Paper-11 : INDIRECT TAXATION Time Allowed : 3 Hours Full Marks : 100 The figures in the margin on the

APPLICABILITY OF SERVICE TAX:

SERVICE TAX It is an indirect tax. Service tax is a tax on services provided.the provisions of service tax are contained in chapter V of the Finance Act, 1994 and administered by the Central Excise Department.

SERVICE TAX It is an indirect tax. Service tax is a tax on services provided.the provisions of service tax are contained in chapter V of the Finance Act, 1994 and administered by the Central Excise Department.

INDIRECT TAX NON TARIFF. All the amendments in the said rule are applicable from 1st April 2011 except otherwise specified.

INDIRECT TAX NON TARIFF CHANGES IN CENVAT CREDIT RULES 2004 I) Changes in the definitions under Rule 2 : All the amendments in the said rule are applicable from 1st April 2011 except otherwise specified.

INDIRECT TAX NON TARIFF CHANGES IN CENVAT CREDIT RULES 2004 I) Changes in the definitions under Rule 2 : All the amendments in the said rule are applicable from 1st April 2011 except otherwise specified.

Levy & Composition, Exemption from Tax

Levy & Composition, Exemption from Tax CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI) 1 All About GST Goods & Services Tax Single Tax Payable on Taxable Supply GST Single Tax on the Supply

Levy & Composition, Exemption from Tax CA Ganesh Prabhu Balakumar B.Com, MFM, F.C.A, LL.B, DISA (ICAI) 1 All About GST Goods & Services Tax Single Tax Payable on Taxable Supply GST Single Tax on the Supply

EXEMPTIONS AND ABATEMENTS

5 EXEMPTIONS AND ABATEMENTS SIGNIFICANT NOTIFICATIONS/CIRCULARS ISSUED BETWEEN 01.05.2014 AND 30.04.2015 1. Mega Exemption Notification amended Mega Exemption Notification No. 25/2012 ST dated 20.06.2012

5 EXEMPTIONS AND ABATEMENTS SIGNIFICANT NOTIFICATIONS/CIRCULARS ISSUED BETWEEN 01.05.2014 AND 30.04.2015 1. Mega Exemption Notification amended Mega Exemption Notification No. 25/2012 ST dated 20.06.2012

CERTIFICATE COURSE ON INDIRECT TAXES

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA Indirect Taxes Committee CERTIFICATE COURSE ON INDIRECT TAXES SUGGESTED ANSWERS OF THE ASSESSMENT TEST HELD ON 25 TH AUGUST, 2012 PART A Write the correct

ROUTINE PROCEDURES

A. REGISTRATION ROUTINE PROCEDURES AS SERVICE Procedure, conditions and safeguards for registration under service tax will be as prescribed by CBE&C by order rule 4(9) of Service Tax Rules, inserted w.e.f.

A. REGISTRATION ROUTINE PROCEDURES AS SERVICE Procedure, conditions and safeguards for registration under service tax will be as prescribed by CBE&C by order rule 4(9) of Service Tax Rules, inserted w.e.f.

CA Sunil Gabhawalla S B Gabhawalla & Co Chartered Accountants

CA Sunil Gabhawalla S B Gabhawalla & Co Chartered Accountants Tax on all services provided in the taxable territory Attaches itself to the service rather than to a person Multiple Point Taxation based

CA Sunil Gabhawalla S B Gabhawalla & Co Chartered Accountants Tax on all services provided in the taxable territory Attaches itself to the service rather than to a person Multiple Point Taxation based

Key Service Tax Budget Proposals and Amendments

Key Service Tax Budget Proposals and Amendments Right advice at right time 2/22 Nityanand Nagar, Sahar Road, Andheri (East), Mumbai-400 069. 28/02/2015 Contents 1. Change in rate of Service tax... 4 2.

Key Service Tax Budget Proposals and Amendments Right advice at right time 2/22 Nityanand Nagar, Sahar Road, Andheri (East), Mumbai-400 069. 28/02/2015 Contents 1. Change in rate of Service tax... 4 2.

FINAL MAY 2018 INDIRECT TAX LAWS

FINAL MAY 2018 INDIRECT TAX LAWS Test Code F73 Branch (MULTIPLE) (Date : 25.02.2018) (50 Marks) Note: All questions are compulsory. Question 1 (5 Marks) This supply would be regarded as mixed supply, since

FINAL MAY 2018 INDIRECT TAX LAWS Test Code F73 Branch (MULTIPLE) (Date : 25.02.2018) (50 Marks) Note: All questions are compulsory. Question 1 (5 Marks) This supply would be regarded as mixed supply, since

Indirect tax issues. Workshop on Tax and Accounting Developments in Indian Real Estate Sector

Workshop on Tax and Accounting Developments in Indian Real Estate Sector Indirect tax issues Manoj Mishra Associate Director, Tax & Regulatory Services Grant Thornton India LLP. All rights reserved. Contents

Workshop on Tax and Accounting Developments in Indian Real Estate Sector Indirect tax issues Manoj Mishra Associate Director, Tax & Regulatory Services Grant Thornton India LLP. All rights reserved. Contents

GST Implications. All India Distillers Association Hotel Crowne Plaza February 23, Discussion by: CA Gaurav Gupta

GST Implications All India Distillers Association Hotel Crowne Plaza February 23, 2017 Discussion by: CA Gaurav Gupta FCA, LLB, DISA Author GST Law & Practise - Service Tax Law & Practise Agenda GST exclusion

GST Implications All India Distillers Association Hotel Crowne Plaza February 23, 2017 Discussion by: CA Gaurav Gupta FCA, LLB, DISA Author GST Law & Practise - Service Tax Law & Practise Agenda GST exclusion

TSSIA HOUSE, Plot No. P- 26, Road No16/T, Wagle Industrial Estate, Thane Phone , Fax:

5 Days (Part Time) Certificate Course In Central Excise & Service Tax Day & Dates: - Tuesday, 23 rd June, 2015 to Saturday 27th June, 2015 Time: 5pm to 8pm At TSSIA HOUSE, Plot No. P- 26, Road No16/T,

5 Days (Part Time) Certificate Course In Central Excise & Service Tax Day & Dates: - Tuesday, 23 rd June, 2015 to Saturday 27th June, 2015 Time: 5pm to 8pm At TSSIA HOUSE, Plot No. P- 26, Road No16/T,

Exemptions under GST for Services

Exemptions under GST for Services S. No. Description of Service 1 All Services provided by Government or a local authority except a. Some services of the Department of Posts b. Services in relation to

Exemptions under GST for Services S. No. Description of Service 1 All Services provided by Government or a local authority except a. Some services of the Department of Posts b. Services in relation to

Subject: Taxation of Real Estate Transactions including Works Contract Date : Saturday, 28 th December 2013 Faculty: Advocate Shailesh Sheth

WIRC of Institute of Chartered Accountants of India National Conference on Issues in Service Tax Subject: Taxation of Real Estate Transactions including Works Contract Date : Saturday, 28 th December 2013

WIRC of Institute of Chartered Accountants of India National Conference on Issues in Service Tax Subject: Taxation of Real Estate Transactions including Works Contract Date : Saturday, 28 th December 2013

EXPLANATORY NOTES - SERVICE TAX. The following changes are being proposed in the Finance Bill, [refer clause 125 of the Finance Bill, 2007]

![EXPLANATORY NOTES - SERVICE TAX. The following changes are being proposed in the Finance Bill, [refer clause 125 of the Finance Bill, 2007]](/thumbs/73/68365115.jpg "EXPLANATORY NOTES - SERVICE TAX. The following changes are being proposed in the Finance Bill, [refer clause 125 of the Finance Bill, 2007]") EXPLANATORY NOTES - SERVICE TAX The following changes are being proposed in the Finance Bill, 2007. [refer clause 125 of the Finance Bill, 2007] (I) Secondary and Higher Education Cess: A cess @ 1% is

EXPLANATORY NOTES - SERVICE TAX The following changes are being proposed in the Finance Bill, 2007. [refer clause 125 of the Finance Bill, 2007] (I) Secondary and Higher Education Cess: A cess @ 1% is

MTP_Intermediate_Syllabus 2016_Dec2017_Set 1 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the rate of service tax was reduced to 10% vide Notification

Rate of service tax restored to 12% As per section 66, rate of service tax is 12% of the value of taxable services. However, in February 2009, the rate of service tax was reduced to 10% vide Notification

Government of India Ministry of Finance (Department of Revenue) Notification No. 13/2017- Union Territory Tax (Rate) New Delhi, the 28 th June, 2017

Notification No. 13/2017- Union Territory Tax (Rate) New Delhi, the 28 th June, 2017") Disclaimer: This updated version of the notification as amended upto 25th January, 2018 has been prepared for convenience and easy reference of the trade and business and has no legal binding or force.

Disclaimer: This updated version of the notification as amended upto 25th January, 2018 has been prepared for convenience and easy reference of the trade and business and has no legal binding or force.

Service tax. Key Budget Proposals and Amendments. Union Budget

Key Budget Proposals and Amendments Union Budget 2017-2018 2/19, Nitya Priya, Nityanand Nagar, Sahar Road, Andheri (East), Mumbai-400 069. 03/02/2017 Contents 1. Retrospective Amendment in Valuation of

Key Budget Proposals and Amendments Union Budget 2017-2018 2/19, Nitya Priya, Nityanand Nagar, Sahar Road, Andheri (East), Mumbai-400 069. 03/02/2017 Contents 1. Retrospective Amendment in Valuation of

SOLVED PAPER. CA Final - Indirect Tax Laws November

APPENDIX : Solved Paper CA Final Indirect Tax Laws November 2014 SOLVED PAPER CA Final - Indirect Tax Laws November - 2014 Ap.1 APPENDIX Question 1 : From the following particulars for the financial year

APPENDIX : Solved Paper CA Final Indirect Tax Laws November 2014 SOLVED PAPER CA Final - Indirect Tax Laws November - 2014 Ap.1 APPENDIX Question 1 : From the following particulars for the financial year

Answer to MTP_Intermediate_Syllabus 2016_Jun2017_Set 2 Paper 11- Indirect Taxation

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

Paper 11- Indirect Taxation Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 11- Indirect Taxation Full Marks: 100 Time allowed:

HARYANA GOVT. GAZ. (EXTRA.), SEPT. 28, 2018 (ASVN. 6, 1940 SAKA) 267 PART - I HARYANA GOVERNMENT LAW AND LEGISLATIVE DEPARTMENT Notification The 28th

, SEPT. 28, 2018 (ASVN. 6, 1940 SAKA) 267 PART - I HARYANA GOVERNMENT LAW AND LEGISLATIVE DEPARTMENT Notification The 28th") Haryana Government Gazette EXTRAORDINARY Published by Authority Govt. of Haryana No. 166-2018/Ext. ] CHANDIGARH, FRIDAY, SEPTEMBER 28, 2018 (ASVINA 6, 1940 SAKA ) LEGISLATIVE SUPPLEMENT CONTENTS PAGES

Haryana Government Gazette EXTRAORDINARY Published by Authority Govt. of Haryana No. 166-2018/Ext. ] CHANDIGARH, FRIDAY, SEPTEMBER 28, 2018 (ASVINA 6, 1940 SAKA ) LEGISLATIVE SUPPLEMENT CONTENTS PAGES

SIPOY SATISH CA IPCC MAY-2013/ NOV-2013 F.Y F. A MARKS. VALUE ADDED TAX `100

SIPOY SATISH www.cacwacs.wordpress.com sipoysatish@gmail.com VALUE ADDED TAX 25 MARKS Including EXAMINATION QUESTIONS CA IPCC MAY-2013/ NOV-2013 F.Y. 2012-13 F. A. 2012 100 VALUE ADDED TAX INDEX 2 Q1 (V.

SIPOY SATISH www.cacwacs.wordpress.com sipoysatish@gmail.com VALUE ADDED TAX 25 MARKS Including EXAMINATION QUESTIONS CA IPCC MAY-2013/ NOV-2013 F.Y. 2012-13 F. A. 2012 100 VALUE ADDED TAX INDEX 2 Q1 (V.

A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S)

") A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S) 1 PRESENTATION PLAN: LEGAL PROVISIONS COMMON TO THE GST LAW(S) LEGAL PROVISIONS SPECIFIC TO IGST ACT & COMPENSATION CESS ACT NEERAJ

A BRIEF INTRODUCTION TO CGST, SGST/UTGST, IGST & COMPENSATION CESS ACT(S) 1 PRESENTATION PLAN: LEGAL PROVISIONS COMMON TO THE GST LAW(S) LEGAL PROVISIONS SPECIFIC TO IGST ACT & COMPENSATION CESS ACT NEERAJ

PROVISIONS RELATED TO INDIRECT TAXES NEW TAX AUDIT REPORT. Ex-Chairman, NIRC /8/

PROVISIONS RELATED TO INDIRECT TAXES IN NEW TAX AUDIT REPORT CA Vishal Garg, Ex-Chairman, NIRC +91-98141-33353 9/8/2014 1 EXTRA WORK OPPORTUNITY 2 3 1994-1995 407 1995-19961996 862 1999-2000 2072 2000-2001

PROVISIONS RELATED TO INDIRECT TAXES IN NEW TAX AUDIT REPORT CA Vishal Garg, Ex-Chairman, NIRC +91-98141-33353 9/8/2014 1 EXTRA WORK OPPORTUNITY 2 3 1994-1995 407 1995-19961996 862 1999-2000 2072 2000-2001

Levy. FAQs. S.No. Query Reply

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

Email FAQs The emails were received by the GST Policy Wing from various sources and were scrutinized and developed into a short FAQ of 100 emails. It should be noted that the emails received or the replies

GST Overview. ~CA Unmesh G. Patwardhan~ Mobile No Unmesh Patwardhan Mobile No

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

GST Overview ~CA Unmesh G. Patwardhan~ Mobile No.98224 24968 Unmesh Patwardhan Mobile No.98224 24968 1 Brief History & Concept of GST Unmesh Patwardhan Mobile No.98224 24968 2 1 st Jul 2017 The D Day Journey

CHAPTER VI SERVICE TAX

Page 1 of 16 CHAPTER VI SERVICE TAX 119. In the Finance Act, 1994, with effect from such date as the Central Government may, by notification in the Official Gazette, appoint, (1) for section 65, the following

Page 1 of 16 CHAPTER VI SERVICE TAX 119. In the Finance Act, 1994, with effect from such date as the Central Government may, by notification in the Official Gazette, appoint, (1) for section 65, the following

Summary of Notifications, Circulars from 16 th January2018 to 15 th February 2018

Summary of Notifications, Circulars from 16 th January2018 to 15 th February 2018 Collection of Revenue from Indirect Taxes Post introduction of GST, Central Revenue from Indirect Taxes has been estimated

Summary of Notifications, Circulars from 16 th January2018 to 15 th February 2018 Collection of Revenue from Indirect Taxes Post introduction of GST, Central Revenue from Indirect Taxes has been estimated

VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH]

![VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH]](/thumbs/72/67119637.jpg "VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH]") VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH] 1 BACK GROUND In his Budget Speech on 29 th February, 2016, the Finance Minister has listed 9 objectives for his tax proposals. One of the objectives relates to

VOLUNTARY DISCLOSURE SCHEME [CA P N SHAH] 1 BACK GROUND In his Budget Speech on 29 th February, 2016, the Finance Minister has listed 9 objectives for his tax proposals. One of the objectives relates to

Goods and Services Tax (GST) M.R.Narain & Co., Chartered Accountants 1

M.R.Narain & Co., Chartered Accountants 1") Goods and Services Tax (GST) 1 How GST Works Following are the Important Features of GST 1. Tax on Supply of Goods and Service (Except Alcoholic Liquor) 2. Multistage Tax 3. Tax on Value Added 4. Destination/Consumption

Goods and Services Tax (GST) 1 How GST Works Following are the Important Features of GST 1. Tax on Supply of Goods and Service (Except Alcoholic Liquor) 2. Multistage Tax 3. Tax on Value Added 4. Destination/Consumption

CLARIFICATION ON ISSUES RELATING TO CENVAT CREDIT RULES 2004

May 25, 2011 CLARIFICATION ON ISSUES RELATING TO CENVAT CREDIT RULES 2004 The Board has issued Circular No. 943/04/2011 CX, dated: April 29, 2011 and has clarified the eligibility of credit with respect

May 25, 2011 CLARIFICATION ON ISSUES RELATING TO CENVAT CREDIT RULES 2004 The Board has issued Circular No. 943/04/2011 CX, dated: April 29, 2011 and has clarified the eligibility of credit with respect

C. B. Thakar, Advocate

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

Refresher Course on GST by WIRC 26 th June,2017 Basic Concepts of GST Presentation by C. B. Thakar, Advocate B.Com., F.C.A., LLB C. B. THAKAR, Advocate 1 Journey towards GST 122 nd CAB Approved by Lok

Institute of Chartered Accountants of India

Institute of Chartered Accountants of India National Conference on Issues in Service Tax Subject : Negative List Is it really negative? Date : Friday, 27 th December 2013 Venue Faculty : ICAI Tower, Near

Institute of Chartered Accountants of India National Conference on Issues in Service Tax Subject : Negative List Is it really negative? Date : Friday, 27 th December 2013 Venue Faculty : ICAI Tower, Near

DG Education (P) Ltd [CENVAT : Service Provider] SERVICE PROVIDER:

![DG Education (P) Ltd [CENVAT : Service Provider] SERVICE PROVIDER:](/thumbs/95/125051621.jpg "DG Education (P) Ltd [CENVAT : Service Provider] SERVICE PROVIDER:") Rule 1 [Extent of applicability] SERVICE PROVIDER: 1 State whether the following can claim cenvat credit: i) Service provider providing services chargeable to tax from business premises located in Delhi

Rule 1 [Extent of applicability] SERVICE PROVIDER: 1 State whether the following can claim cenvat credit: i) Service provider providing services chargeable to tax from business premises located in Delhi

Proposed Amendments in GST Law

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

Proposed Amendments in GST Law On 09.07.2018, the Goods and Service Tax Council has issued draft proposal for the amendment in the "Goods and Services Tax" Law. The entire proposal gives brief view on

F O R E W O R D. We trust that this presentation would be useful. If you have any suggestions for improvement, please do write to us.

F O R E W O R D The objective of this note is to inform our clients and staff of the important changes proposed in Direct Taxes and Indirect Taxes (Service Tax) by the Finance Bill, 2013 which was introduced

F O R E W O R D The objective of this note is to inform our clients and staff of the important changes proposed in Direct Taxes and Indirect Taxes (Service Tax) by the Finance Bill, 2013 which was introduced

Swachh Bharat Cess ('SBC') - Is it really so Swachh?

- Is it really so Swachh?") 1 of 5 12/11/2015 6:27 PM Click to Print Click to Close Swachh Bharat Cess ('SBC') - Is it really so Swachh? NOVEMBER 12, 2015 By Naresh K Sheth, CA & Shraddha Mehta, CA Preamble and Background: SECTION

1 of 5 12/11/2015 6:27 PM Click to Print Click to Close Swachh Bharat Cess ('SBC') - Is it really so Swachh? NOVEMBER 12, 2015 By Naresh K Sheth, CA & Shraddha Mehta, CA Preamble and Background: SECTION

Respected Sir, Subject: Representation on Model GST Law

Honorable Finance Minister Government of India, Ministry of Finance, North Block, Parliament Street, New Delhi 110001. 7 th September, 2016 Respected Sir, Subject: Representation on Model GST Law The Chamber

Honorable Finance Minister Government of India, Ministry of Finance, North Block, Parliament Street, New Delhi 110001. 7 th September, 2016 Respected Sir, Subject: Representation on Model GST Law The Chamber

Applicability of CST/ VAT on E-Commerce Transactions:

Applicability of CST/ VAT on E-Commerce Transactions: The business model of e-com firms is they provide a platform for enabling sellers of goods to be able to sell without boundaries of location across

Applicability of CST/ VAT on E-Commerce Transactions: The business model of e-com firms is they provide a platform for enabling sellers of goods to be able to sell without boundaries of location across

Service Tax Procedures

6.1 Introduction 6 Service Tax Procedures We have already understood the concept of service, negative list of services, point of taxation, valuation, exemptions and abatement in respect of various taxable

6.1 Introduction 6 Service Tax Procedures We have already understood the concept of service, negative list of services, point of taxation, valuation, exemptions and abatement in respect of various taxable

Paper - 18 : Indirect Tax Laws and Practice

Paper - 18 : Indirect Tax Laws and Practice Directorate of Studies, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 18 : Indirect Tax Laws and Practice

Paper - 18 : Indirect Tax Laws and Practice Directorate of Studies, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 18 : Indirect Tax Laws and Practice

Pre-Budget proposal of construction sector for

Pre-Budget proposal of construction sector for 0-7 8 9 0 7 Direct Taxes Income Tax Introduction of Transfer Pricing provisions to domestic transaction Applicability of alternate minimum tax on persons

Pre-Budget proposal of construction sector for 0-7 8 9 0 7 Direct Taxes Income Tax Introduction of Transfer Pricing provisions to domestic transaction Applicability of alternate minimum tax on persons

FILE // SERVICE TAX EXEMPTION NOTIFICATION FOR EXPORT OF SERVICES

18 March, 2018 FILE // SERVICE TAX EXEMPTION NOTIFICATION FOR EXPORT OF SERVICES Document Filetype: PDF 325.31 KB 0 FILE // SERVICE TAX EXEMPTION NOTIFICATION FOR EXPORT OF SERVICES So export of services

18 March, 2018 FILE // SERVICE TAX EXEMPTION NOTIFICATION FOR EXPORT OF SERVICES Document Filetype: PDF 325.31 KB 0 FILE // SERVICE TAX EXEMPTION NOTIFICATION FOR EXPORT OF SERVICES So export of services

Reverse Charge Mechanism - Reverse gear of tax burden

Reverse Charge Mechanism - Reverse gear of tax burden A. Introductory provisions of reverse charge under GST Law. In terms of section 9(1) of Central Goods and Services Tax Act, 2017, Central Goods and

Reverse Charge Mechanism - Reverse gear of tax burden A. Introductory provisions of reverse charge under GST Law. In terms of section 9(1) of Central Goods and Services Tax Act, 2017, Central Goods and

BASIC CONCEPTS, SUPPLY, LEVY & COLLECTION OF GST

BASIC CONCEPTS, SUPPLY, LEVY & COLLECTION OF GST GST Basic Concepts Single Tax Payable on Taxable Supply of G&S Multi Stage & Destination based Consumption Tax GST Charged only on Value Addition No (Reduced)

BASIC CONCEPTS, SUPPLY, LEVY & COLLECTION OF GST GST Basic Concepts Single Tax Payable on Taxable Supply of G&S Multi Stage & Destination based Consumption Tax GST Charged only on Value Addition No (Reduced)

Vasai Branch of WIRC of ICAI

Vasai Branch of WIRC of ICAI Event : Two Days Mega Members Conference on GST Date & Day : 16 th October,2016 (Sunday) Subject : Job-work and E-commerce under GST Venue : Green Court Club (GCC), GCC International

Vasai Branch of WIRC of ICAI Event : Two Days Mega Members Conference on GST Date & Day : 16 th October,2016 (Sunday) Subject : Job-work and E-commerce under GST Venue : Green Court Club (GCC), GCC International

Chapter 1 - Basic Concepts

Chapter 1 - Basic Concepts 1.1 Introduction Prior to 1944 there were 16 individual Acts which levied excise duty. Each such act dealt with one or same type of commodities. All these acts were consolidated

Chapter 1 - Basic Concepts 1.1 Introduction Prior to 1944 there were 16 individual Acts which levied excise duty. Each such act dealt with one or same type of commodities. All these acts were consolidated

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST What is GST?

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST 1.1.1 What is GST? Goods and Services Tax (GST) is a value-added indirect tax at each stage of the supply of goods and services precisely on the amount

CHAPTER 1: INTRODUCTION TO GST 1.1 BASICS OF GST 1.1.1 What is GST? Goods and Services Tax (GST) is a value-added indirect tax at each stage of the supply of goods and services precisely on the amount

Goods and Service Tax in India. CA Ashutosh Thaker

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

Goods and Service Tax in India CA Ashutosh Thaker Ashutosh.thaker@verita.co.in Contents 01 Why &Salient features of Indian GST 02 Key Concept of GST 03 What should be of concern Central Govt. & State Govt.

Indirect tax issues in the Hotel and Tourism Industry. 10 December 2011

Indirect tax issues in the Hotel and Tourism Industry Parind Mehta 10 December 2011 Contents 1 2 Background Issues for consideration under Service tax laws 3 4 Issues for consideration under VAT laws Likely

Indirect tax issues in the Hotel and Tourism Industry Parind Mehta 10 December 2011 Contents 1 2 Background Issues for consideration under Service tax laws 3 4 Issues for consideration under VAT laws Likely

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS Gautam Nayak Chartered Accountant BCAS Seminar 29 th August 2009 Rates of Taxes Substantial increase

Direct Taxes Code Bill, 2009 NPOs, Unincorporated Bodies, Financial Intermediaries, Rates of Taxes & TDS Gautam Nayak Chartered Accountant BCAS Seminar 29 th August 2009 Rates of Taxes Substantial increase

BOMBAY CHARTERED ACCOUNTANTS' SOCIETY

President Rajesh S. Kothari Vice President Anil J. Sathe Hon. Secretaries Pradip K. Thanawala Mayur B. Nayak Hon. Treasurer Deepak R. Shah BOMBAY CHARTERED ACCOUNTANTS' SOCIETY 7, Jolly Bhavan No. 2, New

President Rajesh S. Kothari Vice President Anil J. Sathe Hon. Secretaries Pradip K. Thanawala Mayur B. Nayak Hon. Treasurer Deepak R. Shah BOMBAY CHARTERED ACCOUNTANTS' SOCIETY 7, Jolly Bhavan No. 2, New

An overview of. Service Tax, Presented By: Team Voice of CA

An overview of Service Tax, 2015 Presented By: Team Voice of CA Change in Rates General (Effective date to be notified) The Service Tax rate is being increased from 12% plus Education Cesses to 14%. The

An overview of Service Tax, 2015 Presented By: Team Voice of CA Change in Rates General (Effective date to be notified) The Service Tax rate is being increased from 12% plus Education Cesses to 14%. The

Updates on GST GST Hope For Betterment Released.. For ICMAI Members Here Today

Updates on GST GST Hope For Betterment Released.. For ICMAI Members Here Today WELCOME DELEGATES Humble Request : Silence Please and Urgent Calls Only CMA Dr. Pawan Jaiswal Special Invited Member on GST

Updates on GST GST Hope For Betterment Released.. For ICMAI Members Here Today WELCOME DELEGATES Humble Request : Silence Please and Urgent Calls Only CMA Dr. Pawan Jaiswal Special Invited Member on GST

All About GST and Model GST Law

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

All About GST and Model GST Law 1 Contents GST Basics Supply Meaning & Scope Supply - Time & Place Valuation Rules Input Tax Credit Administration & Procedures Transitional Provisions 2 Basics of GST 3

Chapter -2 Central Excise Law

1 Solution of Paper 10 Applied Indirect Taxes (CMA) December, 2012 Chapter -2 Central Excise Law Descriptive Question Answer (a): Particular CST Service tax Excise duty Customs duty 2012-Dec[2] (a) Taxable

1 Solution of Paper 10 Applied Indirect Taxes (CMA) December, 2012 Chapter -2 Central Excise Law Descriptive Question Answer (a): Particular CST Service tax Excise duty Customs duty 2012-Dec[2] (a) Taxable

The Black Money (Undisclosed Foreign Income and Assets) and Imposition Tax Act, 2015

and Imposition Tax Act, 2015") Introductory presentation on The Black Money (Undisclosed Foreign Income and Assets) and Imposition Tax Act, 2015 By CA. Abhishek Nagori abhishek.nagori@jlnus.com +91-94260-75397 Backdrop to the Act Long-standing

Introductory presentation on The Black Money (Undisclosed Foreign Income and Assets) and Imposition Tax Act, 2015 By CA. Abhishek Nagori abhishek.nagori@jlnus.com +91-94260-75397 Backdrop to the Act Long-standing

Indirect Tax - Deemed Supply - Present Vs GST 3

Indirect Tax - Deemed Supply - Present Vs GST 3 CA Nagendra Hegde & vetted by CA Vasant K. Bhat In the previous article, we had briefed on the term supply and its scope in GST. As discussed, the definition

Indirect Tax - Deemed Supply - Present Vs GST 3 CA Nagendra Hegde & vetted by CA Vasant K. Bhat In the previous article, we had briefed on the term supply and its scope in GST. As discussed, the definition