PASS THROUGH BUSINESS UPDATES

|

|

|

- Candace Bradford

- 6 years ago

- Views:

Transcription

1 PASS THROUGH BUSINESS UPDATES

2

3

which does not have a valid election under section 307 in effect.")

defines a small corporation as: Small corporation means any corporation which has a valid")

4 A Pass Through Entity (PTE) includes the following: A partnership p as defined in the Pennsylvan nia Statue at 72 P.S. 7301(n.0): Partnership means a domestic or foreign general partnership, joint venture, limited partnership, limited liability company, business trust or other unincorporated entity that for federal income tax purposes is classified as a partnership. o Essentially, if the entity is considered d a partnership for federal income tax purposes, it is considered a partnership for Pennsylvania Personal Income Tax (PA PIT) purposes. A PA S corporation as defined in the Pennsylvania Statute at 72 P.S (n. 1): Pennsylvaniaa S corporation means any small corporation as defined in section 301(s.2) which does not have a valid election under section 307 in effect. A qualified Subchapter S subsidiary owned by a Pennsylvania S corporation shall be treatedd as a Pennsylvania S corporation without regard to whether an election under section 307 has been made with respect to the subsidiary. o Pennsylvania Statute 72 P. S (s.2) defines a small corporation as: Small corporation means any corporation which has a valid election in effect under Subchapter S of Chapter 1 of the Internal Revenuee Code of 1986, as amended to January 1, o Essentially, if the entity is considered an S corporation for federal income tax purposes, it is considered a PA S corporation for PA PIT purposes, unless it elects out of that status by filing form REV-976. An LLC filing as a partnership or S corporation federally.

5 REV-976 (05-16) BUREAU OF CORPORAtiON taxes PA S UNit PO BOx HARRiSBURG PA ELECTION NOT TO BE TAXED AS A PENNSYLVANIA S CORPORATION Corporation is not subject to PA corporate net income tax; election is for PA resident shareholder purposes only. Revenue id Federal Employer identification Number (FEiN) Please fill in Corporate Name, Address, City, State and ZiP Code above. Election is for this corporation and its qualified subchapter S subsidiaries as identified on the included schedule showing the names and tax year ending: Revenue ID numbers of all subsidiaries. (A) (B) Social Security (C) (D) Number or Federal Percentage Employer of identification Stock Number Owned Name and address of each shareholder, member or partner having an interest in the corporation s stock without regard to the manner in which the stock is owned. if additional space is needed, complete a separate schedule and include it with this form. You must provide your Social Security number so the department may establish your identity and cross-reference other tax systems, as is authorized under federal law, 42 U.S.C. 405 (c). Name Street City State ZiP Code Election is to be first effective for: tax year beginning: MMddYYYY Signature/date MMddYYYY We, the undersigned shareholders, consent to the election of the corporation not to be taxed as a Pennsylvania S corporation. Name Signature/date Street City State ZiP Code Name Signature/date Street City State ZiP Code Name Signature/date Street City State ZiP Code Name Signature/date Street City State ZiP Code Name Signature/date Street City State ZiP Code Name Signature/date Street City State ZiP Code Name Signature/date Street City State ZiP Code the corporate statement must be signed by an authorized officer of the corporation. the above-named corporation hereby elects not to be taxed as a Pennsylvania S corporation under Section 401 of the tax Reform Code of Under penalties of perjury, I declare that I have examined this Election Not To Be Taxed As A Pennsylvania S Corporation, and to the best of my knowledge and belief it is true, correct and complete. Total = 100% NAME OF CORPORAtE OFFiCER SiGNAtURE ANd title SOCiAL SECURitY NUMBER telephone NUMBER date

states, a qualified subchapter S subsidiary owned by a Pennsylvania S corporation shall not")

owned by an individual or wholly owned by")

.")

6 Pennsylvania statute 72 P.S (e) states, a qualified subchapter S subsidiary owned by a Pennsylvania S corporation shall not be treated as a separate corporation, and all assets, liabilitiess and items of income, deduction and credit of such qualified subchapter S subsidiary shall be treated as assets, liabilities and items of income, deduction and credit of the parent Pennsylvania S corporation. A single-member limited liability company (SMLLC) owned by an individual or wholly owned by another PTE is not a separate entity. Pennsylvania statute 72 P.S says, Unless subject to tax under Article IV, Corporate Net Income Tax an unincorporated entity thatt has a single owner shalll be disregarded as an entity separate from its owner. A partnership which ultimately has only one owner is not a PTE. In Rev. Rul , the Internal Revenue Service (IRS) concluded that: a limited partnership p of LLC owned byy a corporation and SMLCC whose sole member is the corporation, is an entity that has only one owner for federal tax purposes and therefore is not a partnership p (assuming the partnership hasn t made an election to be treated as an association taxable as a corporation). Accordingly, because it is not a partnership for federal purposes, it is not a partnership for PA purposes and, like federal, is an entity disregarded from its owner.

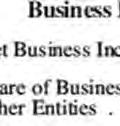

7 PTEs should file the PA-20S/PA-65 along with all applicable schedules including Schedule RK-1 Pennsylvania S Corporation/Partnership Information Return or Schedule NRK-1 for all owners. Partnerships and LLCs taxed as partnerships should file a complete copy of the federal Form 1065 U.S. Return of Partnership Income with all schedules including federal Schedule K-1 Partner s Sharee of Income, Deductions, Credits, etc. S corporations and LLCs taxed as S corporations should file a complete copy of the federal Form 1120-S U.S. Income Tax Return for an S Corporation with all scheduled including federal Schedule K-1 Shareholder s Share of Income, Deductions, Credits, etc. LLCs and S corporations will no longer file the RCT-101 for tax periods beginning 1/1/16 and after due to the elimination of the Capital Stock/Foreign Franchise tax. Also, because LLCs and S corporations will no longer file the RCT- 101, a copy of the federal return must be included with the PA-20S/PA-65 return.

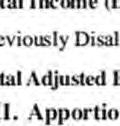

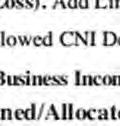

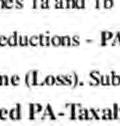

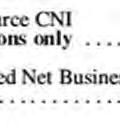

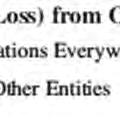

8 FEIN Business Name If a loss, fill in the oval next to the line Part I. Total Taxable Business Income (Loss) from Operations Everywhere LOSS 1a Taxable Business Income (Loss) from Operations Everywhere a 00 LOSS 1b Share of Business Income (Loss) from All Other Entities b 00 LOSS 1c Total Income (Loss). Add Lines 1a and 1b c 00 1d Previously Disallowed CNI Deductions - PA S Corporations only d 00 LOSS 1e Total Adjusted Business Income (Loss). Subtract Line 1d from Line 1c e 00 Part II. Apportioned/Allocated PA-Taxable Outside PA PA Source Business Income (Loss) 2 Net Business Income (Loss) a 00 2e 00 2 Share of Business Income (Loss) from Other Entities b 00 2f 00 2 Previously Disallowed PA Source CNI Deductions - PA S Corporations only c 00 2g 00 2 Calculate Adjusted/Apportioned Net Business C Income (Loss) d 00 2h 00 Part III. Allocated Other PA PIT Income (Loss) 3 Interest Income from PA Schedule A h 00 4 Dividend Income from PA Schedule B h 00 5 Net Gain (Loss) from PA Schedule D a 00 5b 00 6 Rent/Royalty Net Income (Loss) from PLEASE PRINT. USE BLACK INK. Filing Status: PA-20S PA-65 P-S KOZ First Line of Address - Street Address - If Address has Apartment Number, Suite, RR No. - Place on this Line. Second Line of Address - PO Box PA-20S/PA-65 PA S Corporation/Partnership Information Return PAGE 1 of 3 (05-16) (F) 2016 City or Post Office State ZIP Code Revenue ID NAICS Code Inactive SUBMIT ALL SUPPORTING SCHEDULES LOSS LOSS LOSS LOSS LOSS Outside PA PA Schedule M, Part B a 00 6b 00 7 Estates or Trusts Income from PA Schedule J a 00 7b 00 LOSS LOSS 8 Gambling and Lottery Winnings from PA Schedule T.. 8a 00 8b 00 9 Total Other PA PIT Income (Loss) b 00 Page 1 of 3 EC OFFICIAL USE ONLY FC LOSS LOSS LOSS LOSS LOSS LOSS Fill in the applicable ovals Method of Accounting Accrual Cash Other, Describe Extension Requested Initial Year Fiscal Year Short Year Beginning Ending Final Return FEIN/Name/Address Change Amended Information Return Date activity began in PA (MMDDYYYY) USE BLACK INK PA Source

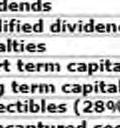

9 Schedule K-1 (Form 1065) 2016 Department of the Treasury For calendar year 2016, or tax Internal Revenue Service year beginning, 2016 ending, 20 Partner s Share of Income, Deductions, Credits, etc. See back of form and separate instructions. DRAFT AS OF August 2, 2016 DO NOT FILE Part I Information About the Partnership A Partnership s employer identification number B Partnership s name, address, city, state, and ZIP code C IRS Center where partnership filed return D Check if this is a publicly traded partnership (PTP) Part II Information About the Partner E Partner s identifying number Final K-1 Amended K-1 OMB No Part III Partner s Share of Current Year Income, Deductions, Credits, and Other Items 1 Ordinary business income (loss) 15 Credits 2 Net rental real estate income (loss) 3 Other net rental income (loss) 4 Guaranteed payments 5 Interest income 6a Ordinary dividends 6b Qualified dividends 7 Royalties 8 Net short-term capital gain (loss) 9a Net long-term capital gain (loss) 9b Collectibles (28%) gain (loss) 16 Foreign transactions 17 Alternative minimum tax (AMT) items F Partner s name, address, city, state, and ZIP code 9c Unrecaptured section 1250 gain 10 Net section 1231 gain (loss) 18 Tax-exempt income and nondeductible expenses G General partner or LLC member-manager Limited partner or other LLC member 11 Other income (loss) H Domestic partner Foreign partner I1 What type of entity is this partner? I2 If this partner is a retirement plan (IRA/SEP/Keogh/etc.), check here Section 179 deduction 19 Distributions J Partner s share of profit, loss, and capital (see instructions): Beginning Ending Profit % % Loss % % Capital % % 13 Other deductions 20 Other information K Partner s share of liabilities at year end: Nonrecourse $ 14 Self-employment earnings (loss) Qualified nonrecourse financing. $ Recourse $ L Partner s capital account analysis: *See attached statement for additional information. Beginning capital account... $ Capital contributed during the year $ Current year increase (decrease). $ For IRS Use Only Withdrawals & distributions.. $ ( ) Ending capital account.... $ Tax basis GAAP Section 704(b) book Other (explain) M Did the partner contribute property with a built-in gain or loss? Yes No If Yes, attach statement (see instructions) For Paperwork Reduction Act Notice, see Instructions for Form IRS.gov/form1065 Cat. No R Schedule K-1 (Form 1065) 2016 OMB No D Employer identification number U.S. Return of Partnership Income For calendar year 2016, or tax year beginning, 2016, ending, 20. Information about Form 1065 and its separate instructions is at Form 1065 Department of the Treasury Name of partnership Internal Revenue Service A Principal business activity E Date business started Number, street, and room or suite no. If a P.O. box, see the instructions. DRAFT AS OF June 21, 2016 DO NOT FILE City or town, state or province, country, and ZIP or foreign postal code Type or Print B Principal product or service F Total assets (see the instructions) C Business code number $ G Check applicable boxes: (1) Initial return (2) Final return (3) Name change (4) Address change (5) Amended return (6) Technical termination - also check (1) or (2) H Check accounting method: (1) Cash (2) Accrual (3) Other (specify) I Number of Schedules K-1. Attach one for each person who was a partner at any time during the tax year J Check if Schedules C and M-3 are attached Caution. Include only trade or business income and expenses on lines 1a through 22 below. See the instructions for more information. 1a Gross receipts or sales a b Returns and allowances b c Balance. Subtract line 1b from line 1a c 2 Cost of goods sold (attach Form 1125-A) Gross profit. Subtract line 2 from line 1c Ordinary income (loss) from other partnerships, estates, and trusts (attach statement) Net farm profit (loss) (attach Schedule F (Form 1040)) Net gain (loss) from Form 4797, Part II, line 17 (attach Form 4797) Other income (loss) (attach statement) Income 8 Total income (loss). Combine lines 3 through Salaries and wages (other than to partners) (less employment credits) Guaranteed payments to partners Repairs and maintenance Bad debts Rent Taxes and licenses Interest a Depreciation (if required, attach Form 4562) a b Less depreciation reported on Form 1125-A and elsewhere on return 16b 16c 17 Depletion (Do not deduct oil and gas depletion.) Retirement plans, etc Employee benefit programs Other deductions (attach statement) Total deductions. Add the amounts shown in the far right column for lines 9 through Ordinary business income (loss). Subtract line 21 from line Deductions (see the instructions for limitations) Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than general partner or limited liability company member manager) is based on all information of which preparer has any knowledge. May the IRS discuss this return with the preparer shown below (see instructions)? Yes No Signature of general partner or limited liability company member manager Date Print/Type preparer s name Preparer s signature Date PTIN Sign Here Check if self-employed Paid Preparer Use Only Firm s name Firm s EIN Firm s address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No Z Form 1065 (2016)

10 OMB No U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Information about Form 1120S and its separate instructions is at Schedule K-1 (Form 1120S) Department of the Treasury Internal Revenue Service Form 1120S 2016 Department of the Treasury Internal Revenue Service For calendar year 2016 or tax year beginning, 2016, ending, 20 A S election effective date Name D Employer identification number For calendar year 2016, or tax year beginning, 2016 ending, 20 Shareholder s Share of Income, Deductions, Credits, etc. See back of form and separate instructions. Part I DRAFT AS OF July 14, 2016 DO NOT FILE Information About the Corporation A Corporation s employer identification number B Corporation s name, address, city, state, and ZIP code C IRS Center where corporation filed return Part II Information About the Shareholder D Shareholder s identifying number Final K-1 Amended K-1 OMB No Part III Shareholder s Share of Current Year Income, Deductions, Credits, and Other Items 1 Ordinary business income (loss) 13 Credits 2 Net rental real estate income (loss) 3 Other net rental income (loss) 4 Interest income 5a Ordinary dividends 5b Qualified dividends 6 Royalties 7 Net short-term capital gain (loss) 8a Net long-term capital gain (loss) 8b Collectibles (28%) gain (loss) 8c Unrecaptured section 1250 gain 14 Foreign transactions E Shareholder s name, address, city, state, and ZIP code 9 Net section 1231 gain (loss) 10 Other income (loss) 15 Alternative minimum tax (AMT) items F Shareholder s percentage of stock ownership for tax year % 11 Section 179 deduction 16 Items affecting shareholder basis 12 Other deductions 17 Other information For IRS Use Only * See attached statement for additional information. For Paperwork Reduction Act Notice, see Instructions for Form 1120S. IRS.gov/form1120s Cat. No D Schedule K-1 (Form 1120S) 2016 B Business activity code Number, street, and room or suite no. If a P.O. box, see instructions. E Date incorporated number (see instructions) OR PRINT City or town, state or province, country, and ZIP or foreign postal code F Total assets (see instructions) C Check if Sch. M-3 attached $ G Is the corporation electing to be an S corporation beginning with this tax year? Yes No If Yes, attach Form 2553 if not already filed H Check if: (1) Final return (2) Name change (3) Address change (4) Amended return (5) S election termination or revocation TYPE DRAFT AS OF I Enter the number of shareholders who were shareholders during any part of the tax year Caution: Include only trade or business income and expenses on lines 1a through 21. See the instructions for more information. June 16, 2016 DO NOT FILE 1 a Gross receipts or sales a b Returns and allowances b c Balance. Subtract line 1b from line 1a c 2 Cost of goods sold (attach Form 1125-A) Gross profit. Subtract line 2 from line 1c Net gain (loss) from Form 4797, line 17 (attach Form 4797) Other income (loss) (see instructions attach statement) Income 6 Total income (loss). Add lines 3 through Compensation of officers (see instructions attach Form 1125-E) Salaries and wages (less employment credits) Repairs and maintenance Bad debts Rents Taxes and licenses Interest Depreciation not claimed on Form 1125-A or elsewhere on return (attach Form 4562) Depletion (Do not deduct oil and gas depletion.) Advertising Pension, profit-sharing, etc., plans Employee benefit programs Other deductions (attach statement) Total deductions. Add lines 7 through Deductions (see instructions for limitations) 21 Ordinary business income (loss). Subtract line 20 from line a Excess net passive income or LIFO recapture tax (see instructions).. 22a b Tax from Schedule D (Form 1120S) b c Add lines 22a and 22b (see instructions for additional taxes) c 23 a 2016 estimated tax payments and 2015 overpayment credited to a b Tax deposited with Form b c Credit for federal tax paid on fuels (attach Form 4136) c d Add lines 23a through 23c d 24 Estimated tax penalty (see instructions). Check if Form 2220 is attached Amount owed. If line 23d is smaller than the total of lines 22c and 24, enter amount owed Overpayment. If line 23d is larger than the total of lines 22c and 24, enter amount overpaid Enter amount from line 26 Credited to 2017 estimated tax Refunded 27 Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. Tax and Payments May the IRS discuss this return with the preparer shown below (see instructions)? Yes No PTIN Signature of officer Date Title Print/Type preparer's name Preparer's signature Date Sign Here Check if self-employed Paid Preparer Use Only Firm's name Firm's EIN Firm's address Phone no. For Paperwork Reduction Act Notice, see separate instructions. Cat. No H Form 1120S (2016)

If, during the taxable")

.")

11 There are 3 scenarios where a PTE is required to file a PA-20S/PA-65: or SMLLC owned by the 1) If, during the taxable year, the PTE (or QSSS PTE) had gross taxable income allocable or apportionable to PA ( PA-source income ). The PTE must file regardless of: a. The amount of the income; i.e. there is no de minimis rule, b. Whether expenses offset the income resulting in a net loss, or c. Whether the income was distributed or not. 2) If, during the taxable year, the PA S corporation had at least one sharehold er that was a PA resident individual, estate, trust or SMLLC. 3) If, at the end of the tax year, the partnership had at least one partner that was a PA resident individual, estate, trust or SMLLC.

.")

.")

).")

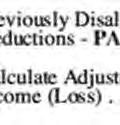

12 PTEs must follow PA PIT rules when calculating taxable income. PA PIT is not based on federal Internal Revenue Code (IRC). The first PIT passed by PA legislature mirrored the IRC, but was found to be unconstitutional (Kelley v Kalodner case 320 Pa. 180, 181 Atl. 598 (1935) - violated Uniformity Clause of the PA Constitution). The second attempt came in 1971 and it tooo was found to be unconstitutional (Amidon v Kane case 444 Pa. 38, 279 A.2d 53 (1971)). The current structure is built on eight classes of income and there are no provisions for standard or itemized deductions or personal exemptions. Lossess are limited: 1) Losses in one class may not offset income from another class, 2) Losses of one spouse may not offset income of another spouse, even if within the same classs of income, and 3) Losses may not be carried backward or forward from year to year.

453 Installment")

13 Some concepts from the IRC are followed, but some sections are specifically not permitted including: 1) 453 Installment Sales - discussed later 2) 1031 Like-Kind Exchanges - discussed later 3) 338(h)(10) Election to Treat a Stock Sale as an Asset Sale a. These transactions are treated as a sale of stock, not a sale of assets. b. The S corporation must file their PA-20S/PA-65 return including a pro forma Form 1120-S that excludes the sale of assets from the return. c. The S corporation stockholder reports the sale of stock on his individual Schedule D. 4) 754 Election for optional basis adjustment a. No allocation of additional basis to underlying partnership assets. b. No depreciation or amortization of the additional basis. Tables 16-1 and 16-3 in Chapter 16 of the PA Personal Income Tax Guide provide examples of common IRC sections and explain whether PA PIT follows the concepts of that IRC section or not.

14 TABLE 16-1 SCHEDULE OF DIFFERENCES BETWEEN FEDERAL TAX LAW AND PENNSYLVANIA PERSONAL INCOME TAX LAW FOR PARTNERSHIPS IRC Code Section Description of Federal Tax Treatment 108 Exclusion of cancellation of indebtedness (COD) income 179 Federal law extends and expands the IRC 179 enhanced expensing provisions beginning in 2002 through year It provides an increase in the expensing limit from $125,000 to $500,000 with phase-out beginning at $2,000,000 for 2010 and Pennsylvania Tax Treatment Pennsylvania does not follow federal treatment. Refer to Chapter 24: Cancellation of Debt for Pennsylvania Personal Income Tax Purposes Pennsylvania follows federal treatment. However, any changes made to IRC 179 after Jan. 1, 1997 are not applicable to Pennsylvania. The Pennsylvania 179 expense is limited to $25,000 and will be phased out for purchases in excess of $200,000. Pennsylvania allows a carryover of the excess. Refer to PA PIT Tax Bulletin Passive or portfolio income Pennsylvania does not follow federal treatment. 704(b) Special allocations with substantial economic effect 704(c) Allocations with respect to precontribution gain inherent in contributed assets 704(d) Limitation of losses to the extent of adjusted basis 705(a) Determination of basis of partner s interest (general rule) Pennsylvania follows federal treatment. Pennsylvania follows federal treatment. Pennsylvania follows federal treatment; however, there is no provision for carryover of losses. For Pennsylvania personal income tax, a partner must reduce their basis in their partnership interest by losses, but only to the extent that the losses reduce either the income subject to Pennsylvania tax or the income tax of another state or country. If losses are not used, the basis must be reduced by the partner s share of straight-line depreciation Pennsylvania follows federal treatment. 706(c) Federal closing of the books Pennsylvania follows federal treatment. 707(a) Federal disguised sale rules Pennsylvania follows federal treatment. 707(c) Guaranteed payments for the use of capital unreasonable guaranteed payments 707(c) Guaranteed payments for the use of capital or other services Pennsylvania follows federal treatment. Pennsylvania does not follow federal treatment for guaranteed payments for services. Under Pennsylvania tax law, to the extent paid for other services or for the use of capital, a guaranteed payment is: a. A withdrawal proportionately from the capital of all partners; b. A gain from the disposition of the recipient s partnership interest and a loss from the disposition of the other partners partnership interests, to the extent derived from the capital of the other partners; and c. A return of capital by the recipient to the extent derived from his/her own capital. Pennsylvania allows the deduction

15 TABLE 16-1 SCHEDULE OF DIFFERENCES BETWEEN FEDERAL TAX LAW AND PENNSYLVANIA PERSONAL INCOME TAX LAW FOR PARTNERSHIPS (CONT D) IRC Code Section Description of Federal Tax Treatment 708 Technical termination of a partnership (involves greater than 50% change in ownership) 709(a) Treatment of organization and syndication fees (general rule) 722 Basis of Contributing Partner s Interest Pennsylvania Tax Treatment Pennsylvania follows federal treatment. Pennsylvania follows federal treatment. Pennsylvania follows federal treatment Contribution of property to a partnership on a tax-free basis Pennsylvania generally follows federal treatment. Neither the partnership nor the partners, recognize gain or loss in the case of a contribution of property in exchange for an interest in the partnership. The partners recognize gain or loss in the following circumstances: The purpose of the contribution was to affect an exchange of property between two or more partners; or The contributing partner receives, in exchange for his or her contribution, an interest in the partnership plus other property or cash. Pennsylvania has not adopted the following concepts: 731(c)(3)(C)(iv) Look-Thru of Partnership Tiers, 731(c)(5) Subsection Disregarded in Determining Basis of Partner s Interest in Partnership and of Basis of Partnership Property. Pennsylvania has not adopted the following concepts: 732(d) Special Partnership Basis to Transferee, 732(f) Corresponding Adjustment to Basis of Assets of a Distributed Corporation Controlled by a Corporate Partner. 752 Increases or decreases in liabilities create deemed cash contribution or distributions to partner Pennsylvania follows federal treatment. 732(d) 734(b) 743(b) 754 Election to step-up or down basis upon certain events Pennsylvania does not follow federal treatment No gain (loss) recognized on any like-kind exchange transactions. Pennsylvania does not follow federal treatment. NA Tax benefit rule (requirement to adjust basis) For Pennsylvania personal income tax, a partner must reduce their basis in their partnership interest by losses, but only to the extent that the losses reduce either the income subject to PA tax or the income tax of another state or country. If losses are not used, the basis must be reduced, but not below zero, by the partner s share of straight-line depreciation.

16 TABLE 16-3 SCHEDULE OF DIFFERENCES BETWEEN FEDERAL TAX LAW AND PENNSYLVANIA PERSONAL INCOME TAX LAW FOR PA S CORPORATIONS Reconciliation of Federal-Taxable Income to Pennsylvania-Taxable Income The PA S corporation should use the PA-20S/PA-65 Schedule M, Reconciliation of Federal-Taxable Income to Pennsylvania-taxable Income to reconcile from federal ordinary income (loss) to Pennsylvania-taxable income (loss) from business, profession, or farm operations, and from rental or royalty income (loss). In many instances, Pennsylvania personal income tax law and regulations do not provide specific treatment similar to federal tax laws. This is especially true with regard to federal elections concerning the timing of income and expense items. Taxpayers should not use federal elections to determine Pennsylvania personal income tax income (loss). IRC Code Section Description of Federal Tax Treatment 108 Exclusion of cancellation of indebtedness (COD) income 179 Federal law extends and expands the IRC 179 enhanced expensing provisions beginning in 2002 through year It provides an increase in the expensing limit from $125,000 to $500,000 with phase-out beginning at $2,000,000 for 2010 and (h)(10) Election to treat a stock as an asset sale 351 Contribution of property to a corporation on a tax-free basis 465 Federal loss not allowed due to federal at risk limitations Federal loss for year higher than Pennsylvania loss as a result of federal at risk carryover 469 Federal loss not allowed due to federal passive loss limitations Federal loss for year higher than Pennsylvania loss as a result of federal passive loss carryover Pennsylvania Tax Treatment Pennsylvania does not follow federal treatment. See new Chapter 24: Cancellation of Debt for Pennsylvania Personal Income Tax Purposes Pennsylvania follows federal treatment. However, any changes made to IRC 179 after Jan. 1, 1997 are not applicable to Pennsylvania, including the PA 179 expense is $25,000 and will be phased out for purchases in excess of $200,000. Pennsylvania does not follow federal treatment. Pennsylvania follows federal treatment. Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result. There is no carryover of a loss for Pennsylvania personal income tax purposes. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone. Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result. There is no carryover of a loss for Pennsylvania personal income tax purposes. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone.

17 TABLE 16-3 SCHEDULE OF DIFFERENCES BETWEEN FEDERAL TAX LAW AND PENNSYLVANIA PERSONAL INCOME TAX LAW FOR PA S CORPORATIONS (CONT D) IRC Code Section Description of Federal Tax Treatment Pennsylvania Tax Treatment 1031 No gain (loss) recognized on any like-kind exchange transactions. Pennsylvania does not follow federal treatment One class of stock requirement Qualified Subchapter S Subsidiaries (QSSS) Pennsylvania follows federal treatment. Pennsylvania permits qualified subchapter S subsidiaries; however, each qualified subchapter S subsidiaries is considered a separate corporation for purposes of the capital stock / foreign franchise tax. See Act Election of S corporation Pennsylvania follows federal treatment for tax years beginning Jan. 1, (d) Passive income test Pennsylvania does not follow federal treatment Accumulated Adjustments Account (AAA) Calculation required for years when PA S status is in place. Federal subchapter S corporations that have been Pennsylvania S corporations throughout their corporate existence always should have tracked their Pennsylvania adjustments account and Pennsylvania accumulated earnings and profits, if applicable, to provide the information required for resident shareholders to correctly report distributions. Federal subchapter S corporations that have become Pennsylvania S corporations by the operation of Act 67 of 2006 similarly should track Pennsylvania accumulated adjustments account and Pennsylvania accumulated earnings and profits. However, it may be extremely difficult to obtain the necessary information to calculate the initial Pennsylvania accumulated earnings and profits. The Pennsylvania Department of Revenue will allow a transitional election by federal subchapter S corporations that have become Pennsylvania S corporations by the operation of Act 67 of The department may allow such a "new" Pennsylvania S corporation taxpayer to elect to use its federal accumulated adjustments account as the functional equivalent of its Pennsylvania accumulated earnings and profits Built-in-gains tax Pennsylvania generally follows federal treatment. Pennsylvania does not follow federal for 25 percent passive income test. If any built-in-gains tax is imposed on a PA S corporation (or any qualified subchapter S subsidiary owned by such PA S corporation), the amount of tax so imposed shall be treated as a loss sustained by such PA S corporation during such years. The character of such loss shall be determined by allocating the loss proportionately among the recognized built-in gains giving rise to such tax Election to terminate year Pennsylvania follows federal treatment. NA Tax Benefit Rule For Pennsylvania purposes, a shareholder must reduce basis in the S corporation by losses but only to the extent that the losses reduce either the income subject to Pennsylvania tax or the income tax of another state or country. If losses are not utilized, the basis must be reduced by the shareholder s share of straight-line depreciation.

18 PA law requires PTEs with PA resident ownerss to file, but they may not always comply. This schedule can be used as guidance for translating federal K-1 data to PA base numbers. This schedule should only be used if the federal K-1 is all you receive; if you get an RK-1/NRK- -1, you must use those numbers.

19

20

21 PTEs reporting income/losss from other PTEs should receive both an RK-1 and an NRK-1 from other PTE. The RK-1 and NRK-1 received reports income which is already apportioned. PTEs should report the flow through income on Line 1b and, if applicable, Lines 2b and 2f on the PA-20S/PA-65. PTEs may not re-apportion the flow through apportionment factor as calculated on its own Schedule H. income using the

22 Calculation of basis in a PTE for PA PIT purposes must be done separately from the federal basis calculation. All the differences s in how income is calculated each year for PA PIT purposes vs. federal income tax purposes play into what can be significant differences in basis. Federal basis in PTE Pennsylvania basis in PTE Pennsylva ania basiss in PTE federal basis + unused losses Each partner must separately determine his own outside basis in the partnership; this can differ from the amount shown on the partnership s books as the partner s capital or equity account as well as the outside basis of the partnerr calculated for federal income tax purposes. Each shareholderr must individually determine his/her basis in the this willl consist of stock basis and loan/debt basis. S corporation; Tables 16-2 and 16-4 in Chapter 16 of the PA Personal Income Tax Guide provide examples of common IRC sections used to calculate basiss in a PTE and explain whether PA PIT follows the concepts of that IRC section or not. Schedules REV-999 and REV-998 are worksheets that can be used to assist with basis calculations.

23 TABLE 16-2 SCHEDULE OF DIFFERENCES BETWEEN FEDERAL TAX LAW AND PENNSYLVANIA PERSONAL INCOME TAX LAW FOR PARTNER S OUTSIDE BASIS CALCULATION IRC Code Section Description of Federal Tax Treatment Pennsylvania Personal Income Tax Treatment Pennsylvania Tax Benefit Rule 465 Federal loss not allowed due to federal-at-risk limitations Federal loss for year higher than Pennsylvania loss as a result of federalat-risk carryover Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. There is no carryover of a loss for Pennsylvania personal income tax purposes. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by partner s share of straight-line depreciation. Basis is reduced by the result. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone. 469 Federal loss not allowed due to federal passive loss limitations Federal loss for year higher than Pennsylvania loss as a result of federal passive loss carryover 704 Federal loss not allowed due to federal basis limitations Federal loss for year higher than Pennsylvania loss as a result of federal loss carryover Federal loss allowed because of federal basis. For Pennsylvania personal income tax no income to offset in class Federal loss for year higher than Pennsylvania loss as a result of Pennsylvania personal income tax adjustments Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. There is no carryover of a loss for Pennsylvania personal income tax purposes. Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. The loss is only allowed if the partner is responsible for making up losses to the partnership. There is no carryover of a loss. There is no carryover of a loss for Pennsylvania personal income tax. No loss allowed for Pennsylvania personal income tax against any other class of income. There is no carryover of a loss. Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. Do not use federal loss. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by partner s share of straight-line depreciation. Basis is reduced by the result. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by partner s share of straight-line depreciation. Basis is reduced by the result. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by partner s share of straight-line depreciation. Basis is reduced by the result. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone.

24 REV-999 PT (08-12) Partner s Outside Tax Basis in a Partnership Worksheet Partnership Name: EIN: Partner s Name: Tax Year: SSN: Partner s Outside Basis 1. Partner s Outside Basis at Beginning of Year * 1 INCREASES TO PARTNER S BASIS 2. Partner s Contributions: 2a Cash 2a 2b Property (adjusted value) 2b 2c Services (fair market value if taxed) 2c 3. Increase in Partner s Assumption of Partnership Liabilities 3 4. Partner s Distributive Share of Income 4a Interest income (resident only) 4a 4b Dividend income (resident only) 4b 4c Net income from the operation of a business, profession or farm 4c 4d Net income from rents, royalties, copyrights and patents 4d 4e Net gain from sale, exchange or disposition of property 4e 4f Other classes of income (excluding gross compensation) 4f 4g Non-taxable income 4g 4h Other increases to basis (submit detailed statement) 4h 5. Total Increases to Partner s Basis (Add Lines 2a through 4h) 5 DECREASES TO PARTNER S BASIS 6. Decreases for Non-Taxable Distributions 6a Non-taxable cash distributions 6a ( ) 6b Non-taxable property distributions 6b ( ) 6c Decrease in share of partnership liabilities 6c ( ) TOTAL NON-TAXABLE DISTRIBUTIONS (Add Lines 6a through Line 6c) 6 ( ) 7. Partner s Basis after Distributions Notes: Basis cannot be less than zero due to distributions. Distributions in excess of basis are taxed as gains for PA purposes. 7a Line 1 + Line 5 + Line 6 7a 7b If Line 7a is $0 or greater, then Line 7 = Line 7a and Line 7c = $0 (go to Line 8) 7c If Line 7a is less than $0, then Line 7 = $0 and Line 7c = Line 7a 7c 7d Enter Line 7c on PA-40 Schedule D, Line 8 7 PARTNER S SHARE OF DISTRIBUTIVE LOSSES ** 8. Net Loss from the Operation of a Business, Profession or Farm 8a Net loss from the operation of a business, profession or farm from RK-1 / NRK-1 8a ( ) 8b Partner s utilized loss (amount of 8a loss used to offset PA-40 in-class income) 8b ( ) 8c Partner s share of straight-line depreciation 8c ( ) If Line 8a = Line 8b, then Line 8 = Line 8a 8 ( ) If Line 8b = $0, then Line 8 = Line 8c If neither of the above apply, then Line 8 = 8b + {[(8a 8b) / 8a] x 8c} 9. Net Loss from Rents, Royalties, Copyrights and Patents 9a Net loss from rents, royalties, copyrights, and patents from RK-1 / NRK-1 9a ( ) 9b Partner s utilized loss (amount of 9a loss used to offset PA-40 in-class income) 9b ( ) 9c Partner s share of straight-line depreciation 9c ( ) If Line 9a = Line 9b, then Line 9 = Line 9a 9 ( ) If Line 9b = $0, then Line 9 = 9c If neither of the above apply, then Line 9 = 9b + {[(9a 9b) / 9a] x 9c} 10. Net Loss from Sale, Exchange or Disposition of Property 10a Net loss from sale, exchange or disposition of property from RK-1 / NRK-1 10a ( ) 10b Partner s utilized loss (amount of 10a loss used to offset PA-40 in-class income) 10b ( ) Line 10 = Line 10b 10 ( ) 11. Total Share of Partner s Distributed Losses (Add Lines 8, 9 and 10) 11 ( ) 12. Decrease for PA Business Credits 12 ( ) 13. Total Other Decreases to Basis Including Nondeductible Expenses (Submit detailed statement) 13 ( ) 14. Partner s Ending Outside Basis (Add Lines 7, 11, 12 and 13) Cannot be less than zero 14 ( ) * Enter prior year ending basis or zero if it is the first year. ** PA law requires a partnership to depreciate property by a minimum amount it determines using the straight-line method even if the depreciation calculated under this method does not provide any tax benefit. Tax benefit means that the partner reduces the PA tax liability or the tax liability to another state. Therefore, if a partner receives a distributable share of a loss and does not receive a benefit from the loss, the partner must still reduce the basis by the share of straight-line depreciation. However, if the partner only received a partial benefit from the loss, the partner must reduce the basis by (1) the loss utilized and (2) a portion of the partner s share of straight-line depreciation. This is calculated by the unutilized loss divided by the total loss multiplied by the partner s share of straight-line depreciation. This is calculated by the unutilized loss divided by the total loss, multiplied by the partner s share of straight-line depreciation. The partner must reduce the basis by the total loss if the partner receives full benefit of the loss

25 TABLE 16-4 SCHEDULE OF DIFFERENCES BETWEEN FEDERAL TAX LAW AND PENNSYLVANIA PERSONAL INCOME TAX LAW FOR S CORPORATION S OUTSIDE BASIS CALCULATION Table 16-4 IRC Code Section Description of Federal Tax Treatment Pennsylvania Personal Income Tax Treatment Pennsylvania Tax Benefit Rule 465 Federal loss not allowed due to federal at risk limitations Federal loss for year higher than Pennsylvania loss as a result of federal at risk carryover Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. There is no carryover of a loss for Pennsylvania personal income tax purposes. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone. 469 Federal loss not allowed due to federal passive loss limitations Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result. Federal loss for year higher than Pennsylvania loss as a result of federal passive loss carryover There is no carryover of a loss for Pennsylvania personal income tax purposes. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone Federal loss not allowed due to federal basis limitations Federal loss for year higher than Pennsylvania loss as a result of federal loss carryover Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. There is no carryover of a loss for Pennsylvania personal income tax. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result. Loss was incurred in prior year. Any unused Pennsylvania personal income tax loss in prior year is forgone. Federal loss allowed because of federal basis. For Pennsylvania personal income tax no income to offset in class No loss allowed for Pennsylvania personal income tax against any other class of income. There is no carryover of a loss. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result. Federal loss for year higher than Pennsylvania loss as a result of Pennsylvania personal income tax adjustments. Pennsylvania personal income tax loss allowed to extent of Pennsylvania personal income tax basis and income in class. There is no carryover of a loss. Do not use federal loss. Basis is reduced by amount of loss offset by income. Percentage of unused loss is multiplied by shareholder s share of straight-line depreciation. Basis is reduced by the result.

26 REV-998 PT (08-12) Shareholder Tax Basis in PA S Corporation Stock Worksheet PA S Corporation EIN: Shareholder s Name: Tax Year: SSN: Stock Basis Debt Basis 1. Shareholder s Stock Basis at Beginning of Year 1 2. Shareholder s Debt Basis at Beginning of Year 2 ADJUSTMENTS TO SHAREHOLDER S BASIS 3. Adjustments to Stock Basis (shareholder s contributions to capital / stock purchases) 3 4. Adjustments to Debt Basis 4a New shareholder s loans to the corporation 4a 4b Replacement of debt principal (Enter debt principal repayments made during the year, but only if debt basis has not been reduced in previous years by pass through losses. If debt basis has been previously reduced by losses, see Line 21b.) 4b ( ) ADJUSTMENTS FOR INCOME AND GAINS (FROM PA RK-1 OR NRK-1) 5. Shareholder s Distributed Share of Income 5a Interest income (resident only) 5a 5b Dividend income (resident only) 5b 5c Net income from business, profession or farm 5c 5d Net income from rents, royalties, patents, etc. 5d 5e Net gain from the disposition of property 5e 5f Other classes of income (excluding gross compensation) 5f 5g Non-taxable income 5g Total Increases for Income and Gains (Add Lines 5a through 5g) 5 DECREASES TO SHAREHOLDER S BASIS 6. Decreases for Non-Dividend Distributions 6a Accumulated Adjustments Account (AAA) distributions 6a ( ) 6b Distributions in excess of AAA 6b ( ) Total Distributions (Add Lines 6a + 6b) 6 ( ) DISTRIBUTIVE LOSSES 7. Net Loss from the Operation of a Business, Profession, or Farm 7a Net loss from the operation of a business, profession or farm from RK-1 / NRK-1 7a ( ) 7b Shareholder s utilized loss (amount of Line 7a loss used to offset PA-40 in-class income) 7b ( ) 7c Shareholder s share of straight-line depreciation 7c ( ) If Line 7a = Line 7b, then Line 7 = Line 7a If Line 7b = $0, then Line 7 = Line 7c If neither of the above apply, then Line 7 = 7b + {[(7a 7b) / 7a] x 7c} 7 ( ) 8. Net Loss from Rents, Royalties, Copyrights and Patents 8 Net loss from rents, royalties, copyrights and patents from RK-1 / NRK-1 8a ( ) 8b Shareholder s utilized loss (amount of Line 8a loss used to offset PA-40 in-class income) 8b ( ) 8c Shareholder s share of straight-line depreciation 8c ( ) If Line 8a = Line 8b, then Line 8 = Line 8a If Line 8b = $0, then Line 8 = Line 8c If neither of the above apply, then Line 8 = 8b + {[(8a 8b) / 8a] x 8c} 8 ( ) 9. Net Loss from Sale, Exchange or Disposition of Property 9a Net loss from sale, exchange or disposition of property from RK-1 / NRK-1 9a ( ) 9b Shareholder s utilized loss (amount of Line 9a loss used to offset PA-40 in-class income) 9b ( ) Line 9 = 9b 9 ( ) 10. Decrease for PA Business Credits 10 ( ) 11. Non-Deductible Expenses 11 ( ) 12. Total Distributed Losses & Credits ( Add Lines 7, 8, 9, 10 and 11) 12 ( ) 13. Net Increase / (Decrease) (Add Lines 5, 6 and 12) 14. If Line 13 is Positive: 13 14a 14b Restore any negative debt basis caused by pass through losses from the Line 13 income. Any excess over the debt basis adjustment should be entered as stock basis on Line 14a. If not restoring debt basis, enter Line 13 on Line 14a. 15. If Line 13 is Negative: Enter the Shareholder s Distributed Share of Income from Line 5. If Line 13 is positive, enter Line 14a Subtotals Line 16a = Line 1 + Line 3 + Line 15 Line 16b = Line 2 + Line 4a + Line 4b + Line 14b 16a 16b 17. If Line 13 is Negative: Adjustment for Non-Dividend Distributions 17a ( ) Enter amount from Line 6 but no more than the amount in the stock basis column on Line 16a. However, if there is an entry on Line 14a, leave this line blank and go to Line Subtotals Line 18a = Line 16a + Line 17a Line 18b = Line 16b 18a 18b 19. If Line 13 is Negative: Adjustment for Distributed Losses & Credits 19a ( ) 19b ( ) Enter in the Stock Basis column the amount on Line 12 to the extent of the subtotal on Line 18a. Any excess is entered in the debt column to the extent of the subtotal on Line 18b. If there are entries on Lines 14a and 14b, leave this line blank and go to Line Subtotals Line 20a = Line 18a + Line 19a Line 20b = Line 18b + Line 19b 20a 20b 21. Adjustments for: 21a Sale or other disposition of stock 21a ( ) 21b Repayment of debt principal due pass-through losses. (Enter debt principal repayments made during the corporation s tax year, but only if debt basis has been reduced in previous years by pass- through losses. If debt basis has not been previously reduced by losses, see Line 4b. Repayment of reduced-basis loans triggers gain recognition. 21b ( ) 22. End of Year Balances (not less than zero) Line 22a = 20a + 21a Line 22b = 20b + 21b 22a 22b Lines 1 and 2 - Enter prior year ending stock and debt basis or initial basis in S corporation stock. Line 17a - Distributions in excess of basis are taxable to residents and should be reported on PA-40 Schedule D, Line 9 Distributive Losses - PA law requires a PA S corporation to depreciate property by a minimum amount it determines using the straight-line method, even if the depreciation calculated under this method does not provide any tax benefit. Tax benefit means that the shareholder reduces PA tax liability or tax liability to another state. Therefore, if a shareholder receives a distributable share of a loss and does not receive a benefit from the loss, the shareholder must still reduce the basis by the share of straight-line depreciation. However, if the shareholder only received a partial benefit from the loss, the shareholder must reduce the basis by (1) the loss utilized and (2) a portion of the shareholder s share of straight-line depreciation. This is calculated by the unutilized loss divided by the total loss, multiplied by the shareholder s share of straight-line depreciation. The shareholder must reduce the basis by the total loss if the shareholder receives full benefit of the loss.

27 Federal charitable contributions are deduction on the Schedule M. not permitted as an additional PA business PA PIT permits a deduction to the extent an expense: Is ordinary, Is necessary, Is reasonable, and Is directly related to and necessary for the production and marketing of the taxpayer s products, good and services. Federal charitable contributions require the taxpayer to receivee or expect to receive no financial or economic benefit in order to be deductible. As a result, if a taxpayer claims a charitable contribution on the federal tax return, it has taken the position that it did not receive, nor did it expect to receive any benefit from the payment. Taxpayers must maintain consistent positions between federal and PA tax reporting. Therefore, if a taxpayer has claimed a payment as a charitable contribution for federal purposes, such payment may nott be deducted for PA PIT tax purposes because the taxpayer has stated on the federal tax return that no benefit was received or expected. Accordingly, theree can be no business purpose for the payment and it cannot be directly related to and necessary for the production of income.

.")

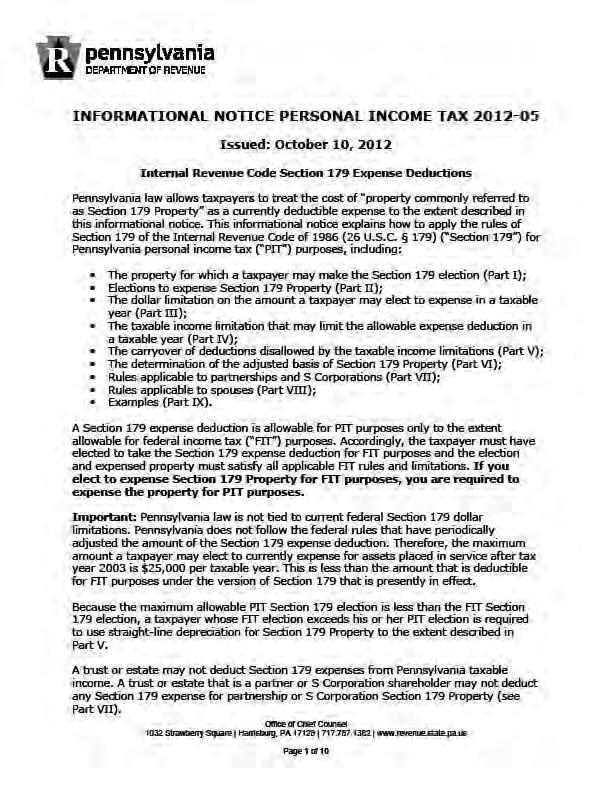

28 Depreciation expense generates a large amount of differences between Pennsylvania taxable income and federal taxable income. Pennsylvan nia recognizes the IRC 179 depreciation deduction, but with a current limitation of $25,000 (and an asset acquisition phase out of $200,000). If property is expenses under IRC 179 for federal purposes, it must be expenses for PA PIT purposes and vice versa. The $25,000 PA 179 limitation is applied first at the PTE level and again at the owner level. The $25,000 PA 179 limitation is applied on a joint basis for spouses, regardless of their filing status. A trust/estate is not eligible to deduct 179 depreciation. Informational Notice Personal Income Tax provides information regarding 179 expense for PA PIT rules including the above bullet points. In addition, IRC purposes. 168(k) bonus depreciation is nott permitted for PA PIT All these differences often lead to situations when the federal depreciable basis and PA PIT depreciable basis are different and accordingly straight-line depreciation should be used to calculate depreciation expense for PA PIT purposes.

29

30 Federal capital gain/loss is always classified ass Net Gain or Loss from the Sale, Exchange or Disposition of Property since itt results from the transfer of an asset. Federal gain/loss may be reclassed as business income/loss for PA PIT purposes only if the proceeds from the salee of tangible property used in a business are reinvested in similar property in the same business. Federal reporting of ordinary income (recapture) vs. capital gain is not a factor in determining the classification of the gain/ /loss for PA PIT purposes nor is reporting on the federal Form 4797 vs. federal Schedule D. Table 16-6 in Chapter 16 of the guidance on classifying gain/loss for PA Personal Income Tax Guide provides PA PIT purposes.

31 TABLE 16-6 REPORTING GAIN (LOSS) FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES Type of Gain Classification Gain Treatment Pennsylvania Resident Nonresident Sale of intangible personal property used in a business, profession or farm, including goodwill contractually sold with the business and allocated by the parties as to value in the sales agreement Used in determining the net income (loss) of the business, profession or farm PA-20S/PA-65, Part I or Part II Taxable Taxable Sale of intangible personal property not used in a business, profession or farm, including goodwill contractually sold with the business and allocated by the parties as to value in the sales agreement PA-20/PA-65 Schedule D Taxable Not Taxable Sale of tangible personal property used in a business, profession or farm - proceeds reinvested and used to acquire similar property used in the same kind of business, profession or farm Used in determining the net income (loss) of the business, profession or farm PA-20S/PA-65, Part I or Part II Taxable Taxable Sale of tangible personal property used in a business, profession or farm - proceeds not reinvested and used to acquire similar property used in the same kind of business, profession or farm PA-20/PA-65 Schedule D Taxable Taxable (If property is located in Pennsylvania) Sale of inventory Used in determining the net income (loss) of the business, profession or farm Taxable Taxable PA-20S/PA-65, Part I or Part II Sale of stock in trade Used in determining the net income (loss) of the business, profession or farm Taxable Taxable PA-20S/PA-65, Part I or Part II Sale of other current assets Used in determining the net income (loss) of the business, profession or farm Taxable Taxable PA-20S/PA-65, Part I or Part II Sale of tangible non-current assets and intangible non-current assets used in operating a business, profession or farm PA-20/PA-65 Schedule D Taxable Taxable Sale of tangible non-current assets and intangible non-current assets held for investment not used in operating a business, profession or farm PA-20/PA-65 Schedule D Taxable Taxable (If property is located in Pennsylvania)

32 TABLE 16-6 REPORTING GAIN (LOSS) FOR PENNSYLVANIA PERSONAL INCOME TAX PURPOSES (CONT D) Type of Gain Classification Gain Treatment Pennsylvania Resident Nonresident Sale of land and/or buildings constituting the abandonment of a business or business segment i.e. sale of a division or line of business where the seller does not continue the division or business activity PA-20/PA-65 Schedule D Taxable Taxable (If property is located in Pennsylvania) Sale of land and/or buildings used as a facility in the operation of a business, profession or farm - proceeds reinvested in a similar facility and used in the same kind of business, profession or farm Used in determining the net income (loss) of the business, profession or farm PA-20S/PA-65, Part I or Part II Taxable Taxable Sale of land and/or buildings held for investment regardless of reinvestment of proceeds Sale of stocks and bonds, other than federal or Pennsylvania obligations, and used in the operating cycle of the business, profession or farm Sale of stocks and bonds, other than federal or Pennsylvania obligations, and not used in the operating cycle of the business, profession or farm IRC exchange of insurance policy PA-20/PA-65 Schedule D Taxable Taxable Used in determining the net income (loss) of the business, profession or farm PA-20S/PA-65, Part I or Part II Taxable (If property is located in Pennsylvania) Taxable PA-20/PA-65 Schedule D Taxable Not taxable PA-20/PA-65 Schedule D With boot Without boot Taxable Not Taxable Not Taxable Not Taxable Sale of ownership interests in partnerships and business enterprises PA-20/PA-65 Schedule D Taxable Not taxable

(2) state, Cost recovery method.")

33 PA PIT rules have no provision like IRC 453. Accrual basis taxpayers may not report gain on an installment basis. Rather they must recognize the full amount of gain in the year of the transaction. The Pennsylvaniaa regulations, at 61 Pa. Code (i)(2) specifically provide the installment sales method is for cash basis taxpayers, Installment sales method. When a seller who is a cash basis taxpayer enters into an agreement for the salee of tangible personal property or real property.. Cash basis taxpayers may use the installment sale method for sales of tangible personal property or real property if: : The sale was made on or after January 1, The object of the transaction is not the lending off money or the rendition of services. The taxpayer has not elected to exclude the gains under subsection (g) which deals with the sale of principle residence Cash basis taxpayers may use the cost recovery method for sales of intangible personal property as long as the obligation is not assignable. The Pennsylvania regulations, at 61 Pa. Code (i)(2) state, Cost recovery method. When a seller who is a cash basis taxpayer enters into an agreement for the sale of intangible personal property under which agreement at least one payment is to be received in a taxable year following the year of sale,, the seller shall use the cost recovery method of accounting if the note, contractual promise or other evidence of that obligation is not assignable.

is not a deductible expense for PA PIT regardless of what the owner does with the distribution.")

34 Pennsylvania does not follow the federal interestt tracing rules. Also, Pennsylvania does not flow through separatelyy stated items to owners of PTEs like federal does. Accordingly, the deductibilityy of the interest is determined at the PTE level, not the owner level. Interest on debt incurred to make a distribution to owners (i.e. a debt financed distribution ) is not a deductible expense for PA PIT regardless of what the owner does with the distribution. The PTE incurred debt to make a distribution, which is not a deductiblee businesss expense but ratherr a transaction related to equity/ /capital, therefore the interestt associated with the debt is not a permissible deduction for PA PIT. A related topic is interest on debt incurred to purchase a partnership interest or S corporation stock. The purchase of the interest or stock by a taxpayer is a personal investment activity, not a business or rental activity. Accordingly, the interest associated with the debt is personal investment interestt and cannot reduce the flow through income (or increase the flow throughh loss) that is passed through from the PTE. Interest related to investing activities is not deductible e for PA PIT purposes.

Does the")

35 PA PIT rules have no provision like IRC 1031 and deferral of the gain is usually not allowed for PA PIT purposes. Pennsylvania PIT Bulletin addresses the tax treatment of IRC 1031 exchanges. That bulletin states, gain or losss on like-kind exchanges doess not have to be recognized at the time of the exchange if a taxpayer s method of accounting permits the deferral of gain from a like-kind exchange. For example, APB Opinion 29 provides for nonrecognition of gain or loss on certain like-kind exchanges for taxpayers who consistently use GAAP principles of accounting. A taxpayer must use the method of accounting on a consistent basis and the method of accounting must clearly reflect his income. A taxpayer may not change his method of accounting just to obtain a tax benefit for a particular transaction. Nevertheless, the deferral of gain or income associated with like-kind exchanges is the exception. There are two main issues that need to be addressed when preparing a return as a result of this bulletin: 1) Does the method of accounting the taxpayer usess to prepare their PA tax return permit the deferral of gain? 2) Is the taxpayer properly deferring the gain under their method of accounting?

36 Does the method of accounting the taxpayer uses to prepare their PA tax return permit the deferral of gain? Taxpayers must use the claimed method of accounting not only to prepare their books and records, but also use that same method to prepare their tax return. For example, if a taxpayer is deferring the gain on their books using GAAP accounting, they must then also file their PA tax return using GAAP accounting. Also, note that the federal income tax basis of accounting, while permitting the deferral of gain under 1031, is not an acceptable accounting method for PA PIT purposes. Secondly, the taxpayer must consistently use the claimed method of accounting and cannot change methods from year to year. Typically, a taxpayer cannot change their method of accounting just to obtain a tax benefit; there must be some other non-tax reason. There is an exception to this rule that allows taxpayers to change to a method of accounting that permits the deferral of gain even if that is the only reason for the change. However, the change cannot be made in the year of the transaction; the taxpayer must demonstrate they have consistently applied the method prior to the transaction. Is the taxpayer properly deferring the gain under their method of accounting? APB Opinion 29 provided the original GAAP guidance for nonmonetary exchanges (of which like-kind exchanges are a subset). APB Opinion 29 was amended by SFAS 153 and is now codified under ASC 845. When applying GAAP rules, there is a high probability that a like-kind exchange will have to be recorded at fair market values and the gain on the transaction recognized. GAAP rules require there to be no commercial substance in order to defer gain recognition. If the transaction has commercial substance, the gain on the transaction must be recognized. Determining commercial substance involves examining the risk, timing and amount of cash flows from the various properties. A significant change in any one of these factors results in the transaction having commercial substance. Most transactions will have a significant change in at least one of these factors and therefore the like-kind exchange transaction will most often have commercial substance. In addition, the FASB has issued an unofficial position that delayed exchanges (which most 1031 transactions are) do not qualify as transactions that lack commercial substance. Rather, the delayed exchange is really two monetary transactions (a sale and a purchase) and each should be recorded at fair value. This indicates FASB expects the application of SFAS 153 to delayed exchanges would result in the recognition of gain for GAAP purposes and the assets recorded at their fair values.

37 Taxpayers cannot take resident credit on more income in any class of income than was taxed by PA nor can they take credit on more income for an entity than was reported to the taxpayer by the entityy and taxed on the PA-40. This appears to be a problem when there are multiple states and/or multiple entities involved. Because the PA Schedule G-L looks att limiting the credit on a state-by-state basis, errors can be made in calculating the total overall credit. Example: John Smith receives an RK-1 from his company reporting $150,000 of business income. John also receives a Maryland K-1 reporting $75,000 of income and a New York K-1 reporting $100,000 of income. The Schedule G-L for Maryland will comparee the $75,000 of income to the $150,000 of business income on the PA-40 and allow credit on the full $75,000 of income. The Schedule G-L for New York will compare the $100, 000 of income to the $150,000 of business income on the PA-40 and allow credit on the full $100,000 of income. Overall, John has now taken credit on $175, 000 of income when he only reported and paid tax upon $150,000 to PA. This is a very simplistic example, but demonstrates the basic concepts thatt can snowball if there are a multitude of states and/ /or entities involved.

38 Pennsylvania considers a trust a separate taxpayer that has a filing requirement, unless the trust is a revocable trust. A grantor trust that is disregarded for federal purposes and does not have to file a federal return, must still file a Pennsylvania return if it is an irrevocable trust. Irrevocable trusts must file a PA-41PA Fiduciary Income Tax Return. Trusts calculate their taxable income in the same manner as an individual in that a loss in one class of income may not offset income in another class. Trusts are permitted a deduction for income that they currently distribute or are required to distribute per the trust document. However, trusts may only distribute their net income; they may not distribute any losses. The beneficiary will receive an RK-1 or NRK-1 from the trust reporting the amount of the distribution. In addition, the beneficiary must report the income in the Estate or Trust Income class of income; the distributed income does not retain the classification it had within the trust.

39 PTE Assessments What types of PTEs are involved? Partnerships or PA S corporations with eleven or more individual owners Partnerships with at least one partner that is a corporation, LLC, partnership, or trust Partnerships or PA S corporations that elect to be subject to the rules What happens? PTE return is adjusted and PTE is assessed for the tax. PTE is the only taxpayer that has standing to appeal the assessment. The final decision of the appeal process is binding on all owners Once the assessment is final, the PTE must notify each of its owners of the adjustment, each owner s portion of the adjustment and each owner s portion of the tax paid. Individual owner may file a petition for refund if the adjustment to the entity would not have changed that owner s tax liability. Failure to File Penalty Penalties will be imposed upon PTEs that have a filing requirement with PA, are notified of such requirement, and fail to file the appropriate forms. The penalty is $250 per failure; the following are considered forms and each missing item would incur the $250 penalty: PA-20S/PA-65 Information Return PA Schedule RK-1 or NRK-1 PA Schedule H-Corp

40 PA Schedule CP, Corporate Partner CNI Withholding Schedule CP identifies non-compliant corporate partners and calculates the withholding the partnership p is required to remit. When calculating the tax to be withheld, partnerships may take into consideration losses and other deductions when determining the corporate partner s income apportioned to Pennsylvania. Prior to this change, consideration of losses and other deductions had to be taken into account by the non-compliant corporate partner via that corporation filing the RCT-1011 return. PA 65-Corp, Directory of Corporate Partners The PA-65 Corp is a dual purpose form: Acts as the transmittal of corporate net income tax withholding Acts as a tax return filing if the partnership is 100% owned by C corporations partners (no separate PA-20S/PA-65 required for a PTE owned wholly by C corporations) The PA-6payments for corporate net income tax withholding should be remitted with the Corp should always be filed separately from any other return and any PA-65 Corp, not any other form.

.")

41 If no PA-40NRC return is being filed, the PTE claims all the quarterly withholding and final payments on line 14 of the PA-20S/PA-6the PA-20S/PA-65. and should submit the catch-up payment with the filing of PTEs are required to withhold personal income tax for nonresident individuals, estates and trusts. PTEs are not permitted to withhold personal income tax for resident individuals, estates or trusts. In addition, they should not withhold personal income tax on behalf of other PTEs. It is very important for nonresident withholding payments to be made properly so the monies are posted to the proper account(s). PTEs must make estimated payments throughout the year as well as possibly a final, catch-up payment at the time of filing the PTE return. How those estimated payments are claimed and how a final payment is made will depend on whether a PA-40 of nonresident individual owners. Nonresidentt individuals can elect to NRC, Nonresident Consolidated Income Tax Return is filed on behalf be included in the return if they meet certain qualifications. See the instructions for the form for specific requirements.

42 If a PA-40 NRC return is being filed, the PTE payments should be split and reported on the appropriate form. The PTE will need to separate the nonresident owners into two groups: Non-Partici pating owners (nonresident individual owners who either do not qualify to be included in the PA-40 NRC return or those who qualify, but do not elect to be included) ), and Participatin g owners (nonresident individual owners who qualify to be included in the PA-40 NRC return and elect to do so) Non-participating Owners The PTE claims any quarterly or final payments for non-participating are reported the same as if owners on the PA-20S/PA-6no PA-40NRC return is being filed) and any final payment that needs sent for as previously shown (payments the non-participating owners should be remitted with the PA-20S/PA-65. Participating Owners The PTE claims any quarterly or final payments for the participating owners on line 8 of the PA-40 NRC and any final payment that needs sent for the participating owners should be remitted with the PA-40 NRC.

With the exception of the EITC and OSTC (the education credits ), credits may not be passed through")

43 Sometimes PTE owners will receive correspondence from the department stating, The pass thru entity allocating the credit claimed on your PA Schedule OC has not submitted the proper paper work by the October filing date to allocate or assign the credit as requested. Please contact the assignor of the credit and have the necessary paperwork completed to authorize the assignment of the credit to your personal income tax account. Approval letters are not acceptable. Submit forms in duplicate to the Bureau of Corporation Taxes, Accounting Division, PO Box , Harrisburg PA Often, this is an issue of timing between when the PTE makes the request to pass through the credit and when the credit gets populated in the internal database and showing as available for use. Contact the department to resolve the notices. Other possible issues with credits: 1) Certain credits have a requirement to separately request pass through of the credit; this may not have been done. Placing the credit on the PTEs Schedule OC and/or RK-1s/NRK-1s is nott an acceptable request. 2) With the exception of the EITC and OSTC (the education credits ), credits may not be passed through more than once. Prior to October 31, 2014 no credits, including the education credits, could be passed through more than once. 3) Certain credits have a requirement to bee applied at the PTE level first and only the remaining amount is eligible to be passed through.

44

PA-20S/PA-65 PA S Corporation/Partnership Information Return PAGE 1 of 3 (05-10) (FI) 2010

(FI) 2010") Business Name C 1006010050 PLEASE PRINT. USE BLACK INK. Filing Status: PA-20S PA-65 PA-KOZ PS First Line of Address - Street Address - If Address has Apartment Number, Suite, RR No. - Place on this Line.

Business Name C 1006010050 PLEASE PRINT. USE BLACK INK. Filing Status: PA-20S PA-65 PA-KOZ PS First Line of Address - Street Address - If Address has Apartment Number, Suite, RR No. - Place on this Line.

U.S. Income Tax Return for an S Corporation

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Go to www.irs.gov/form1120s for

Form 1120S U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is attaching Form 2553 to elect to be an S corporation. Go to www.irs.gov/form1120s for

Appendix B Pali Rao, istockphoto

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

Appendix B Pali Rao, istockphoto Tax Forms (Tax forms can be obtained from the IRS website: www.irs.gov) Form 1040 U.S. Individual Income Tax Return B-2 Schedule C Profit or Loss from Business B-4 Schedule

Appendix P Partnership Tax Forms

Appendix P Partnership Tax Forms The Garvs, LLC Phoenix Beach Training for Business Professionals P - 1 Table of Contents Partnership Tax Forms... 3 Form 1065 U.S. Return of Partnership Income... 3 Schedule

Appendix P Partnership Tax Forms The Garvs, LLC Phoenix Beach Training for Business Professionals P - 1 Table of Contents Partnership Tax Forms... 3 Form 1065 U.S. Return of Partnership Income... 3 Schedule

Weighted average. Owned 0 on January 1, bought 50% from James on May Norma Shipper Owned all year 100

Case Study Corntax Inc Using 2017 Forms adapted for 2017 tax laws.., had three shareholders in 2018 Weighted average James Robertson Owned 50% on January 1, sold to John on May 26 40 John Bouchet Owned

Case Study Corntax Inc Using 2017 Forms adapted for 2017 tax laws.., had three shareholders in 2018 Weighted average James Robertson Owned 50% on January 1, sold to John on May 26 40 John Bouchet Owned

U.S. Return of Partnership Income. Construction RISE SHINE LLC Constructions 1391 S Dayton Court

Form A 1065 Department of the Treasury Internal Revenue Service U.S. Return of Partnership Income Information about Form 1065 and its separate instructions is at www.irs.gov/form1065. 2013 D Employer identification

Form A 1065 Department of the Treasury Internal Revenue Service U.S. Return of Partnership Income Information about Form 1065 and its separate instructions is at www.irs.gov/form1065. 2013 D Employer identification

U.S. Income Tax Return for an S Corporation

Form Sign Here 1120S Department of the Treasury Internal Revenue Service Paid Preparer Use Only U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is

Form Sign Here 1120S Department of the Treasury Internal Revenue Service Paid Preparer Use Only U.S. Income Tax Return for an S Corporation Do not file this form unless the corporation has filed or is

U.S. Return of Partnership Income For calendar year 2010, or tax year beginning, 2010, ending, 20. See separate instructions.

Form 1065 Department of the Treasury Internal Revenue Service A Principal business activity U.S. Return of Partnership Income For calendar year 2010, or tax year beginning, 2010, ending, 20. See separate

Form 1065 Department of the Treasury Internal Revenue Service A Principal business activity U.S. Return of Partnership Income For calendar year 2010, or tax year beginning, 2010, ending, 20. See separate

U.S. Return of Partnership Income

Form Department of the Treasury Internal Revenue Service For calendar year 013, or tax year beginning,, ending,. OMB No. 1545-0099 A Principal business activity Name of partnership D Employer identification

Form Department of the Treasury Internal Revenue Service For calendar year 013, or tax year beginning,, ending,. OMB No. 1545-0099 A Principal business activity Name of partnership D Employer identification

Form 3 Partnership Return of Income 2017 PARTNERSHIP NAME

PRINT IN BLACK INK FOR PRIVACY ACT NOTICE, SEE INSTRUCTIONS. Calendar year filers enter 01-01-2017 and 12-31-2017 below. Fiscal year filers enter appropriate dates. Tax year beginning Tax year ending Form

PRINT IN BLACK INK FOR PRIVACY ACT NOTICE, SEE INSTRUCTIONS. Calendar year filers enter 01-01-2017 and 12-31-2017 below. Fiscal year filers enter appropriate dates. Tax year beginning Tax year ending Form

U.S. Return of Partnership Income

U.S. Return of Partnership Income Form 1065 For calendar year 2017, or tax year beginning, 2017, OMB No. 1545-0123. 2017 Department of the Treasury ending, 20 Internal Revenue Service G Go to www.irs.gov/form1065

U.S. Return of Partnership Income Form 1065 For calendar year 2017, or tax year beginning, 2017, OMB No. 1545-0123. 2017 Department of the Treasury ending, 20 Internal Revenue Service G Go to www.irs.gov/form1065

1041 Department of the Treasury Internal Revenue Service

Form Income Deductions Tax and Payments 1041 Department of the Treasury Internal Revenue Service U.S. Income Tax Return for Estates and Trusts 2015 OMB No. 1545-0092 Information about Form 1041 and its

Form Income Deductions Tax and Payments 1041 Department of the Treasury Internal Revenue Service U.S. Income Tax Return for Estates and Trusts 2015 OMB No. 1545-0092 Information about Form 1041 and its

Street address (suite/room no.) City (if the corporation has a foreign address, see instructions.) State ZIP code

City (if the corporation has a foreign address, see instructions.) State ZIP code") TAXABLE YEAR 2018 California S Corporation Franchise or Income Tax Return FORM 100S For calendar year 2018 or fiscal year beginning and ending. (m m / d d / y y y y) (m m / d d / y y y y) RP Corporation

TAXABLE YEAR 2018 California S Corporation Franchise or Income Tax Return FORM 100S For calendar year 2018 or fiscal year beginning and ending. (m m / d d / y y y y) (m m / d d / y y y y) RP Corporation

U.S. Income Tax Return for an S Corporation