SBE CGT Concessions. SBE CGT & Ancillary Concessions Peter C Adams. Session 6. Small business CGT Concessions:

|

|

|

- Loraine Hawkins

- 6 years ago

- Views:

Transcription

1 SBE CGT & Ancillary Concessions Peter C Adams Session 6 SBE CGT Concessions Small business CGT Concessions: CGT 15-year asset exemption CGT 50% active asset reduction CGT retirement exemption CGT roll-over 1

2 Small business CGT concessions: methodology Then consider the 4 concessions (3 of the 4 concessions have further conditions) SBE CGT Concessions Basic conditions for eligibility to small business concessions: CGT event happens to an asset that the taxpayer owns event would otherwise have resulted in a capital gain taxpayer must either: (1) be a "small business entity"; or (2) satisfy the maximum net asset value test ($6M), and asset satisfies the active asset test If asset is a share in a company or interest in a trust, the company / trust must have CGT concession stakeholder. 2

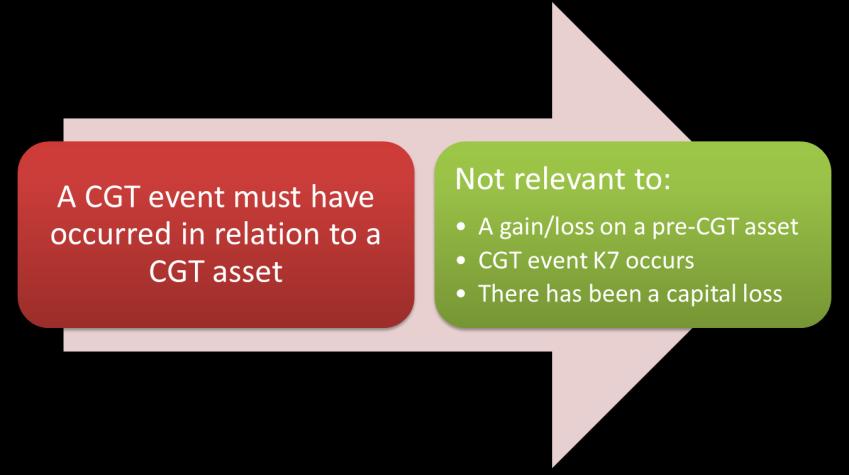

3 Basic conditions: Step 1 Step 2: CGT event 3

Requirement: SBE must carry on a")

4 Basic conditions Steps 3(a) & (b): who can access the concessions? SBE CGT Concessions SBE requirement1 Small Business Entity (SBE) Requirement: SBE must carry on a business and satisfy a $2m "aggregated turnover" test Can be based on aggregated turnover for the previous year or the current year Aggregated turnover is sum of SBE annual turnover and the annual turnovers of connected or affiliated entities 4

5 Maximum NAV Test: NAV less than $6m SBE CGT Concessions - NAV Calculation 5

>40% of income First entity >40% of")

6 Connected with CGT Small Business Concessions (continued) >40% of income First entity >40% of capital 6

7 CGT Small Business Concessions (continued Control of a discretionary trust Influence Test - Trustee acts in accordance with directions, control, etc. First entity Any of the 4 years before >40% distribution (can nominate up to 4 individuals as controllers)) Discretionary Trust: control 7

8 Affiliate Basic conditions step 4: CGT asset an active asset? 8

9 Basic conditions step 4: what is an active asset? SBE CGT Concessions SBE requirement1 Active asset requirement Used in the course of carrying on a business by taxpayer, connected entity or affiliate The following are not active assets Assets whose main use is to derive rent, royalties or FX gains recent case re holiday park Shares in widely held companies or trusts Financial instruments 9

10 SBE CGT Concessions SBE requirement1 Active asset requirement The 80% rule is a look through test to ensure interests in companies and trusts meet the active asset test Market values of active assets and financial instruments (cash) inherently connected with the business - must exceed 80% or more of the market value of all assets of the trust Basic conditions step 5: CGT asset is a share in a company or interest in a trust 10

11 CGT concession stakeholder Calculating small business participation percentage 11

12 CGT Small Business Concessions (continued) Significant individual s are a subset of the concession stakeholders CGT Concession Stakeholders Significant Individual Spouse of significant Individual Participation % must be > = 20% CGT Small Business Concessions (continued) XYZ Unit Trust Mr A 20% Mrs A 5% Mrs B 20% Mr B 5% Mr C -20% Mrs C -5% MrsD -20% Mr D -5% 8 concession stakeholders 12

13 Small business CGT concessions 15 year asset exemption 50% reduction Has priority over the other concessions Can choose not to apply Additional to the general CGT discount available to some taxpayers Retirement exemption Rollover relief Capped to $500,000 lifetime limit Can be applied before the retirement exemption Defers capital gains 15 year asset exemption: conditions 13

14 Distribution of the 15-year CGT asset exemption amount 50% reduction 14

15 Small business retirement concession Retirement exemption eligibility conditions 15

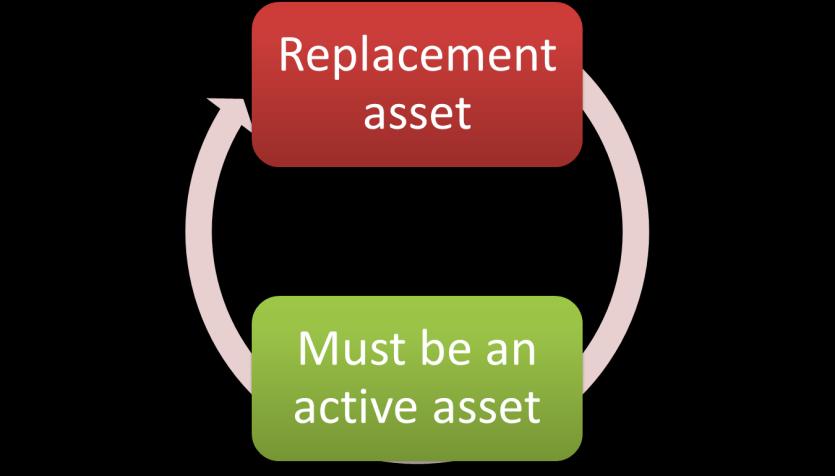

16 Small business CGT rollover relief Eligibility conditions 16

17 Consequences of rollover relief Where no replacement asset acquired CGT event J5 17

18 Where the replacement asset changes its status: CGT event J2 Proposed Measures - Small business entities There are special rules for determining the income or loss of small business entities. They qualify for various concessions that can affect the final figures. An entity will be a small business entity if it: carries on a business, and satisfies the $2m aggregated annual turnover test. In the May 2016 Budget, the Government announced that the small business entity threshold is to increase from $2m to $10m from 1 July For the year ended 30 June 2016, the tax rate for corporate small business entities is 28.5% but is also prposed to be decreased to 27.5% initially and then eventually to 25% for all companies. For the year ended 30 June 2016, a small business tax offset is available to individuals who are small business entities, individuals who are a partner in a partnership that is a small business entity, and individuals who are a beneficiary of a trust that is a small business entity. It is 5% of the tax on total small business income (except from companies) capped at $1,

19 Tax Update Federal Budget Measures Increasing the small business entity turnover threshold The Government will increase the small business entity turnover threshold from $2 million to $10 million from 1 July The current $2 million threshold will be retained for access to the small business CGT concessions. The eligibility threshold for the unincorporated small business tax discount will be raised to $5 million. Small business threshold to increase to $10m As a result of the Government s proposal, a business with an aggregated annual turnover of less than $10m will be able to access a number of small business tax concessions from 1 July

20 Small business threshold to increase to $10m These include: the reduced company tax rate for incorporated small businesses the simplified depreciation rules, including immediate tax deductibility for asset purchases costing less than $20,000 until 30 June 2017 the simplified trading stock rules immediate deductibility for various start-up costs a 12-month prepayment rule Small business threshold to increase to $10m Unfortunately, the $2 million turnover threshold will be kept for access to the small business CGT concessions. Also note the different threshold for access to the tax offset 20

21 Tax Update 2016 The timeframe for the progressive increase in the rate of the unincorporated small business tax discount: The 10-year implementation of the discount increase will coincide with the 10 years of staggered cuts in the corporate tax rate to 25%. 5% 8% 10% 13% 16% and later Tax Update Federal Budget Measures Increasing the unincorporated small business tax discount The current cap of $1,000 per individual for each income year will be retained. The retention of the $1,000 cap will place restrictions on individuals being able to fully utilise the discount as the rate incrementally increases to 16%. The discount is available to individual taxpayers with business income from an unincorporated small business entity. Currently the aggregated turnover threshold of the small business is $2 million. The Government intends to increase this threshold to $5 million. 21

22 Increase in small business tax offset In the May 2016 Budget, the Government announced that with effect from 1 July 2016, the discount would be available for individual taxpayers with business income from an unincorporated business that had an aggregated annual turnover of less than $5m ie. an increase in the threshold from $2m to $5m. The Government also announced that with effect from 1 July 2016, the discount would be increased from 5% to 8%, capped at $1,000 Small business tax offset The tax offset is available to individuals who are small business entities, individuals who are a partner in a partnership that is a small business entity, and individuals (not minors) who are a beneficiary of a trust that is a small business entity 22

23 Tax Update 2016 The initial 27.5% rate will be implemented progressively from to based on the company s annual aggregated turnover: Annual aggregated turnover threshold Income year in which the 27.5% rate will apply Less than $10 million $25 million $50 million $100 million $250 million $500 million $1 billion Tax Update Federal Budget Measures Reducing the company tax rate to 25% Government will reduce the company tax rate to 25% over 10 years. Once all companies are at a rate of 27.5%, the rate will be progressively reduced to 25% in : 23

24 Tax Update Federal Budget Measures Reducing the company tax rate to 25% Government will reduce the company tax rate to 25% over 10 years. Dividends will be frankable in line with the rate of tax paid by the company. This is a departure from last year s small business company tax rate cut, under which eligible small business companies could frank to 30% despite the rate reduction to 28.5%. Given that Australia has a dividend imputation system, any additional tax is borne by the shareholder at their personal marginal rate. Small business entities Immediate deductibility for professional expenses re start-ups With effect 1 July 2015, small business entities and individuals are able to immediately deduct certain costs incurred when starting up a business, Expenditure that would be deductible over five years under s ITAA 1997 is fully deductible in the income year in which the expenditure is incurred if the expenditure: relates to a business that is proposed to be carried on; and is either: incurred in obtaining advice or services relating to the proposed structure or the proposed operation of the business; or is a payment to an Australian government agency of a fee, tax or charge incurred in relation to setting up the business or establishing its operating structure 24

25 New Developments Immediate deduction for professional expenses Eligible expenses will include fees for: professional advice; accounting advice; and legal advice These expenses will no longer be deductible over five years under section of the ITAA Small business entities Small business restructure rollover relief With effect 1 July 2016, the Tax Laws Amendment (Small Business Restructure Roll-Over) Act 2016 provides Australian resident Small Business Entities ("SBEs") with a new roll-over for gains and losses arising from the transfer of CGT assets, trading stock, revenue assets and depreciating assets The roll-over applies if the arrangement is part of a genuine restructure of a small business where the ultimate economic ownership ("UEO") of the asset (directly or indirectly) does not change. 25

26 Small business entities Small business restructure rollover relief The legislation enables SBEs to disregard any tax gain or loss made on the transfer of their business or assets into the new structures. The exclusion does not cover GST or Stamp Duty. Where an individual operates as a sole trader, they hold the UEO. Where the entity is a company, the provisions will look at the ultimate shareholders to determine the UEO. If there is more than one individual who is an ultimate economic owner of an asset, there is an additional requirement that each of those individuals shares of that ultimate economic ownership be materially unchanged, maintaining the same proportionate ownership in the asset. Small business entities Small business restructure rollover relief The provisions specifically provide for the inclusion of discretionary trusts as an eligible entity type by utilising the existing Family Trust Election ("FTE") rules as a test of the UEO. For example, where an individual transfers his/her business to a newly established discretionary trust, the UEO will be deemed not to have changed where the trust has made a FTE and the individual is part of the same family group. Exempt entities and complying superannuation funds are excluded. This means that assets such as land and buildings cannot be transferred into SMSF even though there may be no change in UEO. The roll over relief provides for tax neutral consequences for a transfer by "switching off" the application of the existing income tax law - but only for the purpose of the transfer and not for the purposes of GST, FBT or stamp duty. 26

27 Tax Update - Legislation TLA (Small Business Restructure Roll-over) Bill 2016 In addition to rollover, certain specific consequences for CGT assets: pre-cgt assets will retain their pre-cgt status in the hands of the transferee for purpose of determining whether capital gain may be discounted, transferee is treated as having acquired the CGT asset at the time of the transfer for purpose of determining eligibility for 15 year CGT exemption for small businesses, transferee will be taken as having acquired asset when transferor acquired it. Tax Update - Legislation TLA (Small Business Restructure Roll-over) Bill 2016 Eligibility requirements: A small business entity for the income year during which the transfer occurs for CGT assets that are active assets. An affiliate of a small business entity for passively held assets that used by the small business entity in its business. A connected entity of a small business entity for passively held assets that are used by the small business entity in its business. A partner in a partnership that is a small business entity for the income year during which the transfer occurs for passively held assets that are used by the small business entity in its business. Both transferor and transferee must be residents of Australia For partnerships, at least one partner must be an Australian resident. NOTE no requirement to meet $6m NAV test also (only $2m T/O test) 27

28 Tax Update - Legislation TLA (Small Business Restructure Roll-over) Bill 2016 Ultimate economic ownership requirement: The small business restructuring transaction must not have effect of changing ultimate economic ownership of transferred assets in a material way. Ultimate economic owners of an asset are the individuals who, directly or indirectly, beneficially own an asset. Ultimate economic ownership of asset can only be held by natural persons. Where a company, partnership or trust owns an asset it will be the natural person owners of the interests in these interposed entities that will ultimately benefit economically from that asset. Tax Update - Legislation TLA (Small Business Restructure Roll-over) Bill 2016 Genuine restructure Transaction must be, or part of, a genuine restructure of an ongoing business EM sets out some factors that would indicate a genuine restructure: it is a bona fide commercial arrangement undertaken to enhance business efficiency business continues to operate following the transfer, through a different entity structure but under the same ultimate economic ownership transferred assets continue to be used in the business restructure results in a structure likely to have been adopted had the business owners obtained appropriate professional advice when setting up the business restructure is not artificial or unduly tax driven; and it is not divestment or preliminary step to facilitate economic realisation of assets 28

29 Tax Update - Legislation TLA (Small Business Restructure Roll-over) Bill 2016 Genuine restructure - safe harbour: Bill provides a safe harbour which deems a SBE to satisfy genuine restructure requirement where, for three years following roll-over: there is no change in ultimate economic ownership of assets of the business (other than trading stock) that were transferred under the transaction those significant assets continue to be active assets; and there is no significant or material use of those significant assets for private purposes. Small business entities Example Small business restructure rollover relief (SBRR) Pep and Sally, a married couple, are directors and shareholders in Vitamin Pty Ltd which has issued two shares. Vitamin Pty Ltd carries on a naturopathy business. A new discretionary trust, the P&S Trust, is settled and a family trust election is made with Pep as the primary individual. On 1 January 2017, Pep and Sally cause Vitamin Pty Ltd to transfer all of its assets (except petty cash) to the trustee of the P&S Trust (the trustee) in consideration for the trustee undertaking to discharge Vitamin Pty Ltd's liabilities. The company and the trustee choose to apply the SBRR. 29

30 Small business entities Example Small business restructure rollover relief (SBRR) As at 1 January 2017, the active assets of the company are: a small consulting room, which was acquired by Vitamin Pty Ltd for $200,000 in The market value is $230,000. a pill pressing machine, with an adjustable value of $14,000 goodwill, which is self-generated, and 50 bottles of homeopathic pills, which became Vitamin Pty Ltd's trading stock during the income year at a cost of $250. Small business entities Example Small business restructure rollover relief (SBRR) No capital gain or loss arises from the transfer of the consulting room or goodwill. The trustee is taken to have acquired the consulting room at the time of the transfer for $200,000, being Vitamin Pty Ltd's cost base for the asset immediately before the transfer takes effect. 30

31 Small business entities Example Small business restructure rollover relief (SBRR) No amount is included in Vitamin Pty Ltd's assessable income, or deduction allowed, as a result of a balancing adjustment event for the transfer of the pill pressing machine. The trustee's cost for the pill press is its adjustable value to Vitamin Pty Ltd just before the transfer ($14,000). The trustee can deduct the decline in value of the pill press using the same method and effective life (or remaining effective life, if using the prime cost method) as Vitamin Pty Ltd was using. The trustee is taken to have acquired the goodwill at the time of the transfer for $0, being Vitamin's Pty Ltd's cost base for the goodwill immediately before the transfer takes effect. Small business entities Example Small business restructure rollover relief (SBRR) As a result of the disposal of the pills to the trustee, Vitamin Pty Ltd is taken to have transferred the pills for their cost ($250) and not for their market value. Vitamin Pty Ltd includes $250 in its assessable income under section The pills are trading stock on hand in the hands of the trustee. No dividend arises as a result of the transfer of CGT assets (that are not depreciating assets) by Vitamin Pty Ltd (including any 'deemed dividend' under Division 7A of Part III of the ITAA 1936 or any other provision of the tax law). Apart from pre-cgt assets, the transferee acquires the asset at the time of the transfer. That is, the time of acquisition is not altered by Subdivision 328-G. Following the transfer of assets to the trustee of the P&S trust, a property investor makes an attractive offer to the trustee for the consulting room. On 30 September 2017, the trustee enters into an agreement for the sale of the consulting room. Trustee disposes of the room and CGT event A1 happens on 30 September

32 Small business entities Example Small business restructure rollover relief (SBRR) Trustee is treated as having acquired the CGT asset at the time of the SBRR transfer, on 1 January The trustee is not entitled to access the 50% general CGT discount on disposal, as the trustee acquired the asset less than a year before the CGT event causing this gain. However, for the purpose of determining eligibility for the 15 year CGT exemption for small businesses, the transferee will be taken as having acquired the asset when the transferor acquired it. New Developments Changes to tax treatment of employee share schemes New concession small start-up companies Most significant reform to be implemented is a tax exemption for discounts on ESS interests acquired in eligible small start-up companies. If a share, discount is exempt from tax - share is subject to CGT regime, with market value cost base. If a right, discount is not subject to upfront taxation - right and resulting share once acquired, are subject to CGT regime, with cost base equal to employee s cost of acquiring right. 32

33 New Developments Changes to tax treatment of employee share schemes New concession small start-up companies Company which ESS interest is in the employer (including its holding company) must satisfy the following conditions: No equity interests in employer can be listed on stock or securities exchange at end of year prior acquisition of ESS interest. Employer must be company incorporated less than 10 years before end of income year prior to when ESS interest acquired. Company s aggregated turnover for income year prior to income year in which ESS interest was acquired must not exceed $50m. The employing company (which may or may not be the company issuing the ESS interest) must be an Australian tax resident. Board of Taxation Report - SBEs Recommendations: Increase the small business entity turnover threshold to at least $3 million and investigate the feasibility of an increase to $5 million Allow superannuation for employees against quarterly threshold of $1,350 Superannuation guarantee charge (SG Charge) should be calculated on the basis of Ordinary Times Earnings (OTE) rather than salary and wages to align it with the way that superannuation contributions are calculated SG Charge and any employer contributions paid to a super fund that are used to offset the SG Charge payable be deductible to the employer Removing automatic requirement on employers to lodge SG Charge statement with the ATO when they become liable to the SG Charge Raise the minor and infrequent FBT threshold from $300 to $500 Aligning the FBT year to the income tax year. 33

34 34

16/11/2016 THE NEW SMALL BUSINESS RESTRUCTURE ROLLOVER. by Susan Young B.Com LLB Grad Dip Law

THE NEW SMALL BUSINESS RESTRUCTURE ROLLOVER by Susan Young B.Com LLB Grad Dip Law 1 What we are covering How the new provisions work Interaction with existing small business CGT concessions Necessary elements

THE NEW SMALL BUSINESS RESTRUCTURE ROLLOVER by Susan Young B.Com LLB Grad Dip Law 1 What we are covering How the new provisions work Interaction with existing small business CGT concessions Necessary elements

SMALL BUSINESS. by Susan Young B.Com LLB Grad Dip Law

SMALL BUSINESS by Susan Young B.Com LLB Grad Dip Law Topics we are covering The tax benefits available Immediate deductibility of start-up expenses Treatment of prepayments Small business restructure rollover

SMALL BUSINESS by Susan Young B.Com LLB Grad Dip Law Topics we are covering The tax benefits available Immediate deductibility of start-up expenses Treatment of prepayments Small business restructure rollover

Structured for Success Tax Events September-October 2016

Structured for Success Tax Events September-October 2016 Brian Richards & Trung Vu Locked Bag 2 Fortitude Valley QLD 4006 T +61 7 3223 6100 taxevents.com.au Table of Contents INTRODUCTION... 1 STATUTORY

Structured for Success Tax Events September-October 2016 Brian Richards & Trung Vu Locked Bag 2 Fortitude Valley QLD 4006 T +61 7 3223 6100 taxevents.com.au Table of Contents INTRODUCTION... 1 STATUTORY

Taxation Aspects on Existing a Business

Taxation Aspects on Existing a Business 1 Overview of key considerations 1. SALE OF SHARES / UNITS OR BUSINESS ASSETS 2. COSTS ASSOCIATED WITH SALE 3. COMPONENTS OF THE PRICE 4. LAND, STOCK AND EQUIPMENT

Taxation Aspects on Existing a Business 1 Overview of key considerations 1. SALE OF SHARES / UNITS OR BUSINESS ASSETS 2. COSTS ASSOCIATED WITH SALE 3. COMPONENTS OF THE PRICE 4. LAND, STOCK AND EQUIPMENT

The Australia Taxation reflects legislation in place at 1 November Exam questions will be based upon the tax year.

AUSTRALIA TAXATION CPA Program subject outline First edition A professional accountant is required to possess fundamental tax law knowledge and skills. Australia Taxation introduces fundamental concepts

AUSTRALIA TAXATION CPA Program subject outline First edition A professional accountant is required to possess fundamental tax law knowledge and skills. Australia Taxation introduces fundamental concepts

TAXATION CAPITAL GAINS TAX CONCESSIONS FOR SMALL BUSINESS. Paper CONTENTS

TAXATIO CAPITAL GAIS TAX COCESSIOS FOR SMALL BUSIESS COTETS Page 1. Introduction CGT Concessions... 2 2. 50% Capital Gains Tax Discount For Individuals... 2 3. Capital Losses... 3 4. Order Of Concessions...

TAXATIO CAPITAL GAIS TAX COCESSIOS FOR SMALL BUSIESS COTETS Page 1. Introduction CGT Concessions... 2 2. 50% Capital Gains Tax Discount For Individuals... 2 3. Capital Losses... 3 4. Order Of Concessions...

What s new. An explanation of key changes that may affect your business. Insight Business Partners Pty Ltd Level 1, 1109 Hay Street West Perth WA 6005

What s new An explanation of key changes that may affect your business Insight Business Partners Pty Ltd Level 1, 1109 Hay Street West Perth WA 6005 P +61 (08) 6315 2700 F +61 (08) 6315 2741 E perth.ap@rocg.com

What s new An explanation of key changes that may affect your business Insight Business Partners Pty Ltd Level 1, 1109 Hay Street West Perth WA 6005 P +61 (08) 6315 2700 F +61 (08) 6315 2741 E perth.ap@rocg.com

Year end tax planning 2016 primary producers

Tax planning for primary producers Year end tax planning 2016 primary producers Important in 2015/16 Reduction to company tax rate for small business companies from 1 July 2015 From 1 July 2015, the income

Tax planning for primary producers Year end tax planning 2016 primary producers Important in 2015/16 Reduction to company tax rate for small business companies from 1 July 2015 From 1 July 2015, the income

TAX IN PRACTICE CONVERTING FROM A TRUST TO A COMPANY

TAX IN PRACTICE CONVERTING FROM A TRUST TO A COMPANY MAY 2012 ABOUT PRACTISING TAX Practising Tax is a specialist tax information provider. Practising Tax is a team of passionate tax professionals with

TAX IN PRACTICE CONVERTING FROM A TRUST TO A COMPANY MAY 2012 ABOUT PRACTISING TAX Practising Tax is a specialist tax information provider. Practising Tax is a team of passionate tax professionals with

TAXATION DISCRETIONARY TRUSTS - TAXATION TREATMENT. Paper CONTENTS

TAXATION DISCRETIONARY TRUSTS - TAXATION TREATMENT CONTENTS Page 1. Introduction To Discretionary Trusts... 3 2. Determination Of Discretionary Trust Profit... 3 3. Discretionary Trust Taxable Income...

TAXATION DISCRETIONARY TRUSTS - TAXATION TREATMENT CONTENTS Page 1. Introduction To Discretionary Trusts... 3 2. Determination Of Discretionary Trust Profit... 3 3. Discretionary Trust Taxable Income...

2016/17 Budget. 1. Effective Budget Night 7.30pm (AEST) 3 May New lifetime cap for non-concessional superannuation contributions

3 May New lifetime cap for non-concessional superannuation contributions") 2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

2016/17 Budget Superannuation reform changes 1. Effective Budget Night 7.30pm (AEST) 3 May 2016 1.1 New lifetime cap for non-concessional superannuation contributions The government will introduce a $500,000

INTRODUCTORY TAXATION

INTRODUCTORY TAXATION SUBJECT OUTLINE A professional accountant is required to possess fundamental tax law knowledge and skills. Introductory Taxation introduces fundamental concepts of income tax law,

INTRODUCTORY TAXATION SUBJECT OUTLINE A professional accountant is required to possess fundamental tax law knowledge and skills. Introductory Taxation introduces fundamental concepts of income tax law,

WHITE PAPER. Top 30 Crucial Tax Minimisation Strategies for Businesses

WHITE PAPER Top 30 Crucial Tax Minimisation Strategies for Businesses 1 INTRODUCTION Are You Paying Too Much Tax? FACT: If you re a small business owner chances are you re paying too much tax. Imagine

WHITE PAPER Top 30 Crucial Tax Minimisation Strategies for Businesses 1 INTRODUCTION Are You Paying Too Much Tax? FACT: If you re a small business owner chances are you re paying too much tax. Imagine

` CHARTERED ACCOUNTANTS. Making Your Business Count

` CHARTERED ACCOUNTANTS Making Your Business Count 2016 Federal Budget Overview The Federal Budget for the coming year was handed down on Tuesday 3rd May 2016. With an election due to be held on 2 July

` CHARTERED ACCOUNTANTS Making Your Business Count 2016 Federal Budget Overview The Federal Budget for the coming year was handed down on Tuesday 3rd May 2016. With an election due to be held on 2 July

Changing CGT Small Business Concessions - For Better Or Worse?

Revenue Law Journal Volume 19 Issue 1 Article 5 2009 Changing CGT Small Business Concessions - For Better Or Worse? John Tretola Follow this and additional works at: http://epublications.bond.edu.au/rlj

Revenue Law Journal Volume 19 Issue 1 Article 5 2009 Changing CGT Small Business Concessions - For Better Or Worse? John Tretola Follow this and additional works at: http://epublications.bond.edu.au/rlj

YEAR END TAX STRATEGIES

THE 30 June deadline is fast approaching. It is important that business owners, large and small, take the time now to focus on their tax planning strategies. This bulletin highlights the opportunities

THE 30 June deadline is fast approaching. It is important that business owners, large and small, take the time now to focus on their tax planning strategies. This bulletin highlights the opportunities

Capital Gains Tax. Foreign and Temporary Residents - Changing Residency Status. Prepared and Presented by:

Capital Gains Tax Foreign and Temporary Residents - Changing Residency Status Prepared and Presented by: Tom Delany Tax Partner Pty Ltd 3 Inadale Court Toowoomba Queensland 4350 Mobile: 0428 357413 Email:

Capital Gains Tax Foreign and Temporary Residents - Changing Residency Status Prepared and Presented by: Tom Delany Tax Partner Pty Ltd 3 Inadale Court Toowoomba Queensland 4350 Mobile: 0428 357413 Email:

Tricks, traps and tantalising opportunities: new Subdiv 328-G explained by Matthew Burgess, CTA, Director, View Legal

Tricks, traps and tantalising opportunities: new Subdiv 328-G explained by Matthew Burgess, CTA, Director, View Legal Abstract: Following the federal government s jobs and small business package introduced

Tricks, traps and tantalising opportunities: new Subdiv 328-G explained by Matthew Burgess, CTA, Director, View Legal Abstract: Following the federal government s jobs and small business package introduced

Company Tax Return Preparation Checklist 2017

COMPANY TAX RETURN PREPARATION CHECKLIST 2017 This checklist should be completed in conjunction with the preparation of tax reconciliation return workpapers. The checklist provides a general list of major

COMPANY TAX RETURN PREPARATION CHECKLIST 2017 This checklist should be completed in conjunction with the preparation of tax reconciliation return workpapers. The checklist provides a general list of major

Tax Time Monthly MARCH ISSUE INCOME TAX... pg 3. 2 SUPERANNUATION... pg 5

Tax Time Monthly MARCH ISSUE 2018 1 INCOME TAX... pg 3 1.1 CGT small business concessions: restricted to assets used in business draft legislation released 1.2 Amendments to consolidation regime to close

Tax Time Monthly MARCH ISSUE 2018 1 INCOME TAX... pg 3 1.1 CGT small business concessions: restricted to assets used in business draft legislation released 1.2 Amendments to consolidation regime to close

Business Succession and Estate Planning Bulletin

August 2016 Business Succession and Estate Planning Bulletin In this bulletin: Can my attorney change my binding death benefit nomination? Should my attorney be able to? The "new rising" of trust cloning

August 2016 Business Succession and Estate Planning Bulletin In this bulletin: Can my attorney change my binding death benefit nomination? Should my attorney be able to? The "new rising" of trust cloning

Converting small business wealth to SMSF savings CGT small business concessions. Jordan George, Senior Manager- Technical & Policy SMSF Association

Converting small business wealth to SMSF savings CGT small business concessions Jordan George, Senior Manager- Technical & Policy SMSF Association Agenda A quick overview of the CGT small business concession

Converting small business wealth to SMSF savings CGT small business concessions Jordan George, Senior Manager- Technical & Policy SMSF Association Agenda A quick overview of the CGT small business concession

Chapter 1: Eligibility checklist 1. Chapter 2: Some general CGT issues 5

vi Contents Preface iii Abbreviations v Chapter 1: Eligibility checklist 1 1-100 Determining eligibility for CGT small business relief... 2 Pre-CGT asset... 4 Chapter 2: Some general CGT issues 5 2-100

vi Contents Preface iii Abbreviations v Chapter 1: Eligibility checklist 1 1-100 Determining eligibility for CGT small business relief... 2 Pre-CGT asset... 4 Chapter 2: Some general CGT issues 5 2-100

From business start-up to exit Key decisions and the tax implications

From business start-up to exit Key decisions and the tax implications Brian Richards March 2018 Redchip Level 8, 100 Skyring Tce Newstead QLD 4006 Locked Bag 2 Fortitude Valley QLD 4006 T +61 7 3223 6100

From business start-up to exit Key decisions and the tax implications Brian Richards March 2018 Redchip Level 8, 100 Skyring Tce Newstead QLD 4006 Locked Bag 2 Fortitude Valley QLD 4006 T +61 7 3223 6100

PRACTICE UPDATE - JUNE 2017

PRACTICE UPDATE - JUNE 2017 Reduction in FBT Rate from 1st April 2017 Planned Changes to GST on Low Value Imported Goods Company tax cuts pass the senate with amendments Costs of Travelling in relation

PRACTICE UPDATE - JUNE 2017 Reduction in FBT Rate from 1st April 2017 Planned Changes to GST on Low Value Imported Goods Company tax cuts pass the senate with amendments Costs of Travelling in relation

DECEMBER 2015 BUSINESS NEWSLETTER

DECEMBER 2015 BUSINESS NEWSLETTER Example industries include; Exploration and Mining; Manufacturing; Education; Building and Construction; Offshore Oil and Gas Support Services; Retail and Hospitality;

DECEMBER 2015 BUSINESS NEWSLETTER Example industries include; Exploration and Mining; Manufacturing; Education; Building and Construction; Offshore Oil and Gas Support Services; Retail and Hospitality;

Class Ruling Income tax: scrip for scrip roll-over Caledonia group reorganisation: Caledonia Small Caps No. 2 Trust

Page status: legally binding Page 1 of 23 Class Ruling Income tax: scrip for scrip roll-over Caledonia group reorganisation: Caledonia Small Caps No. 2 Trust Contents LEGALLY BINDING SECTION: Para What

Page status: legally binding Page 1 of 23 Class Ruling Income tax: scrip for scrip roll-over Caledonia group reorganisation: Caledonia Small Caps No. 2 Trust Contents LEGALLY BINDING SECTION: Para What

Preview for Foreign Residents and CGT:

Preview for Foreign Residents and CGT: FOREIGN RESIDENTS AND CGT: 1. Are they an Australian resident? 2. If not, there are special rules relating to capital gains/losses made by foreign residents. (Division

Preview for Foreign Residents and CGT: FOREIGN RESIDENTS AND CGT: 1. Are they an Australian resident? 2. If not, there are special rules relating to capital gains/losses made by foreign residents. (Division

2018/19 Federal Budget

1. Personal income tax changes 1.1 Personal income tax plan 2018/19 Federal Budget The Government will introduce a seven-year, three-step, Personal Income Tax Plan, as follows: Step 1: Targeted tax relief

1. Personal income tax changes 1.1 Personal income tax plan 2018/19 Federal Budget The Government will introduce a seven-year, three-step, Personal Income Tax Plan, as follows: Step 1: Targeted tax relief

Taxation is a key component of the overall skills base of today's professional accountant.

ADVANCED TAXATION CPA PROGRAM SUBJECT OUTLINE Study guide: Third edition Taxation is a key component of the overall skills base of today's professional accountant. Business leaders appreciate that there

ADVANCED TAXATION CPA PROGRAM SUBJECT OUTLINE Study guide: Third edition Taxation is a key component of the overall skills base of today's professional accountant. Business leaders appreciate that there

With the gap between the highest marginal and company tax rates to increase what can we expect for Division 7A?

With the gap between the highest marginal and company tax rates to increase what can we expect for Division 7A? Contributed by Dr Justin Dabner CTA, Associate Professor, Law School, James Cook University;

With the gap between the highest marginal and company tax rates to increase what can we expect for Division 7A? Contributed by Dr Justin Dabner CTA, Associate Professor, Law School, James Cook University;

Aspects of Financial Planning

Aspects of Financial Planning Taxation implications of overseas residency More and more of our clients are being given the opportunity to live and work overseas. Before you make the move, it is worthwhile

Aspects of Financial Planning Taxation implications of overseas residency More and more of our clients are being given the opportunity to live and work overseas. Before you make the move, it is worthwhile

Tax Rates Tables REVISED VERSION. September 2017

Tax Rates Tables 2017-18 REVISED VERSION September 2017 Individual income tax rates Residents 2016-17 Taxable income Marginal rate Tax on this income $0 $18,200 Nil Nil $18,201 $37,000 19% 19c for each

Tax Rates Tables 2017-18 REVISED VERSION September 2017 Individual income tax rates Residents 2016-17 Taxable income Marginal rate Tax on this income $0 $18,200 Nil Nil $18,201 $37,000 19% 19c for each

Introduction. How will a company s tax rate payable be determined?

Introduction On 18 October 2017, the following related items were released regarding access to the lower 27.5% corporate tax rate: the Treasury Laws Amendment (Enterprise Tax Plan Base Rate Entities) Bill

Introduction On 18 October 2017, the following related items were released regarding access to the lower 27.5% corporate tax rate: the Treasury Laws Amendment (Enterprise Tax Plan Base Rate Entities) Bill

Challenges Ahead & Maximising Tax Changes Federal Budget IPA Tony Greco May, 2016

Challenges Ahead & Maximising Tax Changes Federal Budget 2016 IPA Tony Greco May, 2016 Compliance is not dead Significant difficulty in passing on cost increases to clients and charging for compliance

Challenges Ahead & Maximising Tax Changes Federal Budget 2016 IPA Tony Greco May, 2016 Compliance is not dead Significant difficulty in passing on cost increases to clients and charging for compliance

Class Ruling Income tax: Insurance Australia Group Limited Distribution and Share Consolidation

Page status: legally binding Page 1 of 23 Class Ruling Income tax: Insurance Australia Group Limited Distribution and Share Consolidation Contents LEGALLY BINDING SECTION: Para Summary what this Ruling

Page status: legally binding Page 1 of 23 Class Ruling Income tax: Insurance Australia Group Limited Distribution and Share Consolidation Contents LEGALLY BINDING SECTION: Para Summary what this Ruling

Tax and Superannuation Laws Amendment (2014 Measures No. 6) Bill 2014 No., 2014

Bill 2014 No., 2014") 0- The Parliament of the Commonwealth of Australia HOUSE OF REPRESENTATIVES Presented and read a first time Tax and Superannuation Laws Amendment ( Measures No. ) Bill No., (Treasury) A Bill for an Act

0- The Parliament of the Commonwealth of Australia HOUSE OF REPRESENTATIVES Presented and read a first time Tax and Superannuation Laws Amendment ( Measures No. ) Bill No., (Treasury) A Bill for an Act

2016/17 Federal Budget 4 May 2016

2016/17 Federal Budget 4 May 2016 Last night s Federal Budget contains important changes for small business, superannuation, individual and company tax rates, and multinationals operating in Australia.

2016/17 Federal Budget 4 May 2016 Last night s Federal Budget contains important changes for small business, superannuation, individual and company tax rates, and multinationals operating in Australia.

Concessions for small business entities

Guide for small business operators Concessions for small business entities Information to help you work out the concessions you can use. For more information visit www.ato.gov.au NAT 71874-06.2008 OUR

Guide for small business operators Concessions for small business entities Information to help you work out the concessions you can use. For more information visit www.ato.gov.au NAT 71874-06.2008 OUR

END OF YEAR TAX PLANNING CHECKLIST

END OF YEAR TAX PLANNING CHECKLIST FOR THE YEAR ENDING 30 JUNE 2014 Cornwall Stodart Level 10 114 William Street DX 636 Melbourne VIC 3000, Australia Phone +61 3 9608 2000 Fax +61 3 9608 2222 cornwallstodart

END OF YEAR TAX PLANNING CHECKLIST FOR THE YEAR ENDING 30 JUNE 2014 Cornwall Stodart Level 10 114 William Street DX 636 Melbourne VIC 3000, Australia Phone +61 3 9608 2000 Fax +61 3 9608 2222 cornwallstodart

Succession Planning biggest killer, accounting for over 30,000 deaths in 2013.

ISSUE 20 2016 FAST TRACKING YOUR BUSINESS SUCCESS Personal Risk Management Plan Do you have one? Risk Management Plans don t only apply to businesses every person and family should also have a plan to

ISSUE 20 2016 FAST TRACKING YOUR BUSINESS SUCCESS Personal Risk Management Plan Do you have one? Risk Management Plans don t only apply to businesses every person and family should also have a plan to

FORMS OF PUBLIC PRACTICE BUSINESS STRUCTURES

FORMS OF PUBLIC PRACTICE BUSINESS STRUCTURES FOR PUBLIC PRACTITIONERS OPERATING IN AUSTRALIA INTRODUCTION Members who satisfy the requirements under CPA Australia s By-Law 9 can apply for a Public Practice

FORMS OF PUBLIC PRACTICE BUSINESS STRUCTURES FOR PUBLIC PRACTITIONERS OPERATING IN AUSTRALIA INTRODUCTION Members who satisfy the requirements under CPA Australia s By-Law 9 can apply for a Public Practice

Superannuation Fund Return Preparation Checklist 2017

SUPERANNUATION FUND RETURN PREPARATION CHECKLIST 2017 The following checklist for superannuation funds should be completed in conjunction with the preparation of tax reconciliation return workpapers. The

SUPERANNUATION FUND RETURN PREPARATION CHECKLIST 2017 The following checklist for superannuation funds should be completed in conjunction with the preparation of tax reconciliation return workpapers. The

CAPITAL GAINS TAX EXEMPTIONS

CAPITAL GAINS TAX EXEMPTIONS The following details the principal measures that provide relief from the full application of the CGT provisions of the Income Tax Assessment Act: Background: Generally, the

CAPITAL GAINS TAX EXEMPTIONS The following details the principal measures that provide relief from the full application of the CGT provisions of the Income Tax Assessment Act: Background: Generally, the

Understanding tax Version 5.1

Understanding tax Version 5.1 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to tax. This document has been published

Understanding tax Version 5.1 This document provides some additional information to help you understand the financial planning concepts discussed in the SOA in relation to tax. This document has been published

Class Ruling Income tax: Tatts Group Limited Scheme of Arrangement and payment of Special Dividend

Page status: legally binding Page 1 of 27 Class Ruling Income tax: Tatts Group Limited Scheme of Arrangement and payment of Special Dividend Contents LEGALLY BINDING SECTION: Para Summary what this ruling

Page status: legally binding Page 1 of 27 Class Ruling Income tax: Tatts Group Limited Scheme of Arrangement and payment of Special Dividend Contents LEGALLY BINDING SECTION: Para Summary what this ruling

State Tax Warning for Family Trusts

State Tax Warning for Family Trusts Recent changes to State laws may trigger a surprise tax bill for family trusts (discretionary trusts). The problem for family trusts stems from recent legislative changes

State Tax Warning for Family Trusts Recent changes to State laws may trigger a surprise tax bill for family trusts (discretionary trusts). The problem for family trusts stems from recent legislative changes

Income Tax Employee share scheme: real risk of forfeiture - minimum term of employment and good leaver provisions

ATO Interpretative Decision ATO ID 2010/61 Income Tax Employee share scheme: real risk of forfeiture - minimum term of employment and good leaver provisions FOI status: may be released CAUTION: This is

ATO Interpretative Decision ATO ID 2010/61 Income Tax Employee share scheme: real risk of forfeiture - minimum term of employment and good leaver provisions FOI status: may be released CAUTION: This is

Tax and the sharing economy

Information Newsletter - Tax & Super March 2017 Tax and the sharing economy The concept of a sharing economy has been around for long enough now to have had a very real impact on how we transact with each

Information Newsletter - Tax & Super March 2017 Tax and the sharing economy The concept of a sharing economy has been around for long enough now to have had a very real impact on how we transact with each

AUSTRALIAN BUDGET

MAY 2015 AUSTRALIAN TAX UPDATE AUSTRALIAN BUDGET 2015-2016 INTRODUCTION The Australian Government has released a measured but significant 2015-2016 Federal Budget. The three main tax changes include a

MAY 2015 AUSTRALIAN TAX UPDATE AUSTRALIAN BUDGET 2015-2016 INTRODUCTION The Australian Government has released a measured but significant 2015-2016 Federal Budget. The three main tax changes include a

SMSF Association Budget Update : The most significant changes to superannuation since 2007

SMSF Association Budget Update 2016-17: The most significant changes to superannuation since 2007 Last night, the Government delivered the 2016-17 Federal Budget, its last before a looming double dissolution

SMSF Association Budget Update 2016-17: The most significant changes to superannuation since 2007 Last night, the Government delivered the 2016-17 Federal Budget, its last before a looming double dissolution

Look before you leap: the small business CGT concessions

Client Information Newsletter - Tax & Super September 2017 Look before you leap: the small business CGT concessions The CGT relief concessions that are available to small businesses can be very generous.

Client Information Newsletter - Tax & Super September 2017 Look before you leap: the small business CGT concessions The CGT relief concessions that are available to small businesses can be very generous.

BOURKE O BRIEN KENNEDY

2017 Tax Highlights BOURKE O BRIEN KENNEDY Year End Tax Highlights Summary June 2017 Please consult us at BOK to discuss your specific circumstances before acting on the information in this document. TAX

2017 Tax Highlights BOURKE O BRIEN KENNEDY Year End Tax Highlights Summary June 2017 Please consult us at BOK to discuss your specific circumstances before acting on the information in this document. TAX

Implications of the 2016 Federal Budget

Implications of the 2016 Federal Budget This information is correct as at 16 May 2016. Information contained in this presentation is general in nature and does not constitute personal advice. It has been

Implications of the 2016 Federal Budget This information is correct as at 16 May 2016. Information contained in this presentation is general in nature and does not constitute personal advice. It has been

Income Tax Basics 2008 Day 2

Introduction...1 1. What is the aim and structure of this seminar?...1 2. The self-assessment system...1 2.1 Complexity of returns has increased...2 3. Introduction to completing the business return...2

Introduction...1 1. What is the aim and structure of this seminar?...1 2. The self-assessment system...1 2.1 Complexity of returns has increased...2 3. Introduction to completing the business return...2

Contents. Contact us.

This document is for permanent employees of BOC Limited. Retained and Spouse members should refer to their version of the Other information document. BOCSUPER Contents 3 How super works 7 Your benefits

This document is for permanent employees of BOC Limited. Retained and Spouse members should refer to their version of the Other information document. BOCSUPER Contents 3 How super works 7 Your benefits

INTRODUCTION Overview... [13 010] Nature of CGT events... [13 020] What if more than one event applies?... [13 030]

![INTRODUCTION Overview... [13 010] Nature of CGT events... [13 020] What if more than one event applies?... [13 030]](/thumbs/82/86973374.jpg "INTRODUCTION Overview... [13 010] Nature of CGT events... [13 020] What if more than one event applies?... [13 030]") SAMPLER CGT EVENTS 13 INTRODUCTION Overview... [13 010] Nature of CGT events... [13 020] What if more than one event applies?... [13 030] ASSET DISPOSAL OR TERMINATION CGT event A1 disposal of CGT asset...

SAMPLER CGT EVENTS 13 INTRODUCTION Overview... [13 010] Nature of CGT events... [13 020] What if more than one event applies?... [13 030] ASSET DISPOSAL OR TERMINATION CGT event A1 disposal of CGT asset...

BUSINESS NEWS. Welcome to the June 2018 Edition Of our PBD Business Newsletter. I trust the following items are informative and interesting.

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

BUSINESS NEWS Welcome to the June 2018 Edition Of our PBD Business Newsletter I trust the following items are informative and interesting Regards, Pio De Corso ABN 26 645 374 624 15 Gorge Road, Paradise

RECENT CHANGES AFFECTING FOREIGNERS AND POTENTIALLY AUSTRALIAN RESIDENTS

RECENT CHANGES AFFECTING FOREIGNERS AND POTENTIALLY AUSTRALIAN RESIDENTS Recently, both the Federal and Victorian Governments have announced many legislative changes affecting foreigners. Many of the legislative

RECENT CHANGES AFFECTING FOREIGNERS AND POTENTIALLY AUSTRALIAN RESIDENTS Recently, both the Federal and Victorian Governments have announced many legislative changes affecting foreigners. Many of the legislative

2010 CGT ROADSHOW WORKBOOK

i. XX Division National Division 28 July 2010 The Grace Hotel, Sydney WORKBOOK Written & presented by: Brian Richards Tax Consulting Partner BDO (QLD) Brisbane Taxation Institute of Australia 2010 Disclaimer:

i. XX Division National Division 28 July 2010 The Grace Hotel, Sydney WORKBOOK Written & presented by: Brian Richards Tax Consulting Partner BDO (QLD) Brisbane Taxation Institute of Australia 2010 Disclaimer:

Commonwealth Budget Report

PERSONAL TAX RATES The income tax thresholds and tax rates for residents (excluding the Medicare levy) are: 2014-2015 Income year (current) 2015-17 Income years Taxable income Rate Taxable income Rate

PERSONAL TAX RATES The income tax thresholds and tax rates for residents (excluding the Medicare levy) are: 2014-2015 Income year (current) 2015-17 Income years Taxable income Rate Taxable income Rate

BWR Accountants & Advisers

BWR Accountants & Advisers June 2013 Newsletter Special points of interest: A large number of tax changes apply in the 2012/13 income year. A brief summary is provided in this newsletter. There may be

BWR Accountants & Advisers June 2013 Newsletter Special points of interest: A large number of tax changes apply in the 2012/13 income year. A brief summary is provided in this newsletter. There may be

Parliament of Australia Department of Parliamentary Services

Parliament of Australia Department of Parliamentary Services Parliamentary Library Information, analysis and advice for the Parliament RESEARCH PAPER www.aph.gov.au/library 4 September 2009, no. 4, 2009

Parliament of Australia Department of Parliamentary Services Parliamentary Library Information, analysis and advice for the Parliament RESEARCH PAPER www.aph.gov.au/library 4 September 2009, no. 4, 2009

Wrap Tax Guide. Part 1. Wrap Tax Policy Guide For the year ended 30 June 2011

Wrap Tax Guide Wrap Tax Policy Guide For the year ended 30 June 2011 Part 1 General Information Part 1 of the Wrap Tax Guide outlines the tax assumptions and policies Wrap Services has used to prepare

Wrap Tax Guide Wrap Tax Policy Guide For the year ended 30 June 2011 Part 1 General Information Part 1 of the Wrap Tax Guide outlines the tax assumptions and policies Wrap Services has used to prepare

For business owners Accounting & Tax Investment Management Strategy & Planning. tax facts

For business owners Accounting & Tax Investment Management Strategy & Planning tax facts 2014... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2

For business owners Accounting & Tax Investment Management Strategy & Planning tax facts 2014... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2

GENERAL TAX ISSUES. represents. income and gains

GENERAL TAX ISSUES Income tax represents approximately 70 percent of the total tax revenue of the Australian Federal Government Income tax represents approximately 70% of the total tax revenue of the Australian

GENERAL TAX ISSUES Income tax represents approximately 70 percent of the total tax revenue of the Australian Federal Government Income tax represents approximately 70% of the total tax revenue of the Australian

... for individuals, their superannuation and their businesses.

tax facts 2017... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2 Medicare levy surcharge 1.3 Low income tax offset 1.4 Tax discount for unincorporated

tax facts 2017... ... for individuals, their superannuation and their businesses. For individuals 1.1 Income tax rates 1.2 Medicare levy surcharge 1.3 Low income tax offset 1.4 Tax discount for unincorporated

can do so and claim an immediate deduction. It is also possible to prepay and claim a deduction for your upcoming property insurance premiums.

YEAR END STRATEGIES 2017/18 TAX GUIDE FOR YOU AND YOUR BUSINESS Tax tips for investment property One of the greatest benefits of owning an investment property (besides the additional income) is your entitlement

YEAR END STRATEGIES 2017/18 TAX GUIDE FOR YOU AND YOUR BUSINESS Tax tips for investment property One of the greatest benefits of owning an investment property (besides the additional income) is your entitlement

Federal Budget 2016 & subsequent superannuation announcement

15 September 2016 Federal Budget 2016 & subsequent superannuation announcement Key superannuation proposals in this budget: Retention of the Low Income Superannuation Contribution (LISC) renamed the Low

15 September 2016 Federal Budget 2016 & subsequent superannuation announcement Key superannuation proposals in this budget: Retention of the Low Income Superannuation Contribution (LISC) renamed the Low

Go-To Guide CGT relief

Go-To Guide CGT relief SMSF Association Technical Team Table of Contents Key Advice Issues... 2 Prohibition of the use of the segregated method and member investment choice... 3 Segregated assets method...

Go-To Guide CGT relief SMSF Association Technical Team Table of Contents Key Advice Issues... 2 Prohibition of the use of the segregated method and member investment choice... 3 Segregated assets method...

Additional information about your superannuation

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

Elphinstone Group Superannuation Fund 19 March 2018 Additional information about your superannuation Contents Important information 1 How super works 2 Benefits of investing with the Elphinstone Group

Self managed superannuation funds. A Financial Planning Technical Guide

Self managed superannuation funds A Financial Planning Technical Guide 2 Self managed superannuation funds Contents What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are

Self managed superannuation funds A Financial Planning Technical Guide 2 Self managed superannuation funds Contents What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are

BT Portfolio SuperWrap Essentials

BT Portfolio SuperWrap Essentials Information Brochure Personal Super Plan Pension Plan Term Allocated Pension Plan Product Disclosure Statement ( PDS ) The distributor of BT Portfolio SuperWrap Essentials

BT Portfolio SuperWrap Essentials Information Brochure Personal Super Plan Pension Plan Term Allocated Pension Plan Product Disclosure Statement ( PDS ) The distributor of BT Portfolio SuperWrap Essentials

2007 Taxation Statement Guide

MLC MasterKey Unit Trust 2007 Taxation Statement Guide Issue Date: 10 July 2007 MLC Investments Limited ABN 30 002 641 661 AFSL 230705 Information in the Annual Taxation Statement This guide has been prepared

MLC MasterKey Unit Trust 2007 Taxation Statement Guide Issue Date: 10 July 2007 MLC Investments Limited ABN 30 002 641 661 AFSL 230705 Information in the Annual Taxation Statement This guide has been prepared

Taxation of Australian nationals working overseas

nationals working overseas 2 Contents Introduction 1 1. Will I still have to pay tax in Australia while I work overseas? 2 1.1 The Australian tax system 2 1.2 Impact of overseas assignment 2 2. Will I

nationals working overseas 2 Contents Introduction 1 1. Will I still have to pay tax in Australia while I work overseas? 2 1.1 The Australian tax system 2 1.2 Impact of overseas assignment 2 2. Will I

Important EOFY actions

Important EOFY actions Reducing your tax exposure, maximising the opportunities available to you, and reducing your risk of an audit by the regulators is in your best interests. With the end of the financial

Important EOFY actions Reducing your tax exposure, maximising the opportunities available to you, and reducing your risk of an audit by the regulators is in your best interests. With the end of the financial

2001 tax returns: companies and trusts

2001 tax returns: companies and trusts 28 November 2001 Western Australian Division Stuart Third, Winduss & Associates Presented by: Stuart Third Tax ation Institute of Australia 2001 The Tax ation Institute

2001 tax returns: companies and trusts 28 November 2001 Western Australian Division Stuart Third, Winduss & Associates Presented by: Stuart Third Tax ation Institute of Australia 2001 The Tax ation Institute

Relevant matters for Tax Practitioners

Impact of recent tax & super changes Tony Greco FIPA Who Institute should of Public you trust? Accountants Relevant matters for Tax Practitioners Work related expenses - update Enterprise tax plan Cash

Impact of recent tax & super changes Tony Greco FIPA Who Institute should of Public you trust? Accountants Relevant matters for Tax Practitioners Work related expenses - update Enterprise tax plan Cash

Tax Hot Spots II 2009 WHAT S NEW IN 2009/ Division 7A expanded problems for clients using company assets...3

Contents Topic Page No. WHAT S NEW IN 2009/10...1 Division 7A expanded problems for clients using company assets...3 1. The use of company assets by shareholders...3 2. Proposed carve-outs under the new

Contents Topic Page No. WHAT S NEW IN 2009/10...1 Division 7A expanded problems for clients using company assets...3 1. The use of company assets by shareholders...3 2. Proposed carve-outs under the new

Exit fee (if you make a withdrawal)** $154 ($157 from. Switching fee (if you change your investment choice more than once each calendar year)

** $154 ($157 from. Switching fee (if you change your investment choice more than once each calendar year)") Dow Australia Superannuation Fund Fees and Tax Sheet Super and tax The information in this document forms part of: the Product Disclosure Statement for Employee members (including Insurance Only members)

Dow Australia Superannuation Fund Fees and Tax Sheet Super and tax The information in this document forms part of: the Product Disclosure Statement for Employee members (including Insurance Only members)

Federal Budget Summary

10 May 2006 2006-07 Federal Budget Summary Snapshot of major tax proposals Economic review and key policies Personal tax proposals A super plan Welcome to the 2006-07 edition of Grant Thornton s Federal

10 May 2006 2006-07 Federal Budget Summary Snapshot of major tax proposals Economic review and key policies Personal tax proposals A super plan Welcome to the 2006-07 edition of Grant Thornton s Federal

JUNE 2017 NEWSLETTER. The 2017 financial year has seen the raft of changes, first introduced in the 2016 budget, legislated into law.

JUNE 2017 NEWSLETTER The 2017 financial year has seen the raft of changes, first introduced in the 2016 budget, legislated into law. Fortunately the 2017 budget did not announce any further large reform

JUNE 2017 NEWSLETTER The 2017 financial year has seen the raft of changes, first introduced in the 2016 budget, legislated into law. Fortunately the 2017 budget did not announce any further large reform

Active vs passive assets and the small business CGT concession

Client Information Newsletter - Tax & Super February 2017 Active vs passive assets and the small business CGT concession The small business capital gains tax concessions are extremely valuable. For small

Client Information Newsletter - Tax & Super February 2017 Active vs passive assets and the small business CGT concession The small business capital gains tax concessions are extremely valuable. For small

Income Tax Basics 2012 Day 2. Overview...1

Contents Overview...1 1. The self-assessment system...1 1.1 Periods of review...2 2. Preparing the business return...3 2.1 Accounting records vs. tax records...3 2.2 Process for completing the business

Contents Overview...1 1. The self-assessment system...1 1.1 Periods of review...2 2. Preparing the business return...3 2.1 Accounting records vs. tax records...3 2.2 Process for completing the business

How to Survive and Thrive under the new Super System

How to Survive and Thrive under the new Super System THE NEW SUPER SYSTEM. In my presentation I plan on covering What will the effect be of the 2018 budget Revisiting CGT relief for transfers back to accumulation

How to Survive and Thrive under the new Super System THE NEW SUPER SYSTEM. In my presentation I plan on covering What will the effect be of the 2018 budget Revisiting CGT relief for transfers back to accumulation

Division 7A: A complete guide: Extract DIVISION 7A: A COMPLETE GUIDE EXTRACT. CPA Australia Ltd

DIVISION 7A: A COMPLETE GUIDE EXTRACT CPA Australia Ltd 2015 1 CONTENTS Course overview 1 Learning objectives 1 Knowledge assessment 1 Symbols 1 1. Outline of Division 7A 3 1.1 What is Division 7A? 3 1.2

DIVISION 7A: A COMPLETE GUIDE EXTRACT CPA Australia Ltd 2015 1 CONTENTS Course overview 1 Learning objectives 1 Knowledge assessment 1 Symbols 1 1. Outline of Division 7A 3 1.1 What is Division 7A? 3 1.2

CR 2017/48. Class Ruling Income tax: CGT roll-over exchange of shares in Touchcorp Limited for shares in Afterpay Touch Group Limited

Page status: legally binding Page 1 of 9 Class Ruling Income tax: CGT roll-over exchange of shares in Touchcorp Limited for shares in Afterpay Touch Group Limited Contents LEGALLY BINDING SECTION: Para

Page status: legally binding Page 1 of 9 Class Ruling Income tax: CGT roll-over exchange of shares in Touchcorp Limited for shares in Afterpay Touch Group Limited Contents LEGALLY BINDING SECTION: Para

Federal Budget Summary

Federal Budget Summary 2016 / 2017 Overview Federal Treasurer Scott Morrison s first Federal Budget is an unusual election year Budget, focussing on superannuation changes rather than the usual election

Federal Budget Summary 2016 / 2017 Overview Federal Treasurer Scott Morrison s first Federal Budget is an unusual election year Budget, focussing on superannuation changes rather than the usual election

In this Issue. Financial Navigator. Budget 2018/2019. Business Names. Tax Planning

Financial Navigator Budget Edition May 2018 In this Issue Budget 2018/2019 Federal Budget 2018/2019 how it affects 1. Personal income tax 2. Business taxpayers 3. Superannuation 4. Companies 5. Trusts

Financial Navigator Budget Edition May 2018 In this Issue Budget 2018/2019 Federal Budget 2018/2019 how it affects 1. Personal income tax 2. Business taxpayers 3. Superannuation 4. Companies 5. Trusts

Property Settlement Risks new 10% withholding tax affecting transfers of real property interests will impact on family lawyers

Property Settlement Risks new 10% withholding tax affecting transfers of real property interests will impact on family lawyers 1 From 1 July 2016 it is presumed that the vendor of real property is a non-resident

Property Settlement Risks new 10% withholding tax affecting transfers of real property interests will impact on family lawyers 1 From 1 July 2016 it is presumed that the vendor of real property is a non-resident

Self managed superannuation funds. A Financial Planning Guide

Self managed superannuation funds A Financial Planning Guide 2 Self managed superannuation funds Contents What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are the risks?

Self managed superannuation funds A Financial Planning Guide 2 Self managed superannuation funds Contents What is a self managed 4 superannuation fund (SMSF)? What are the benefits? 4 What are the risks?

Budget 2006 Personal Tax and Fringe Benefits Tax Personal Income Tax

Tax Brief 9 May 2006 Budget 2006 Every year there is frenzied speculation about the likely content of the upcoming Budget. And, as is usually the case, some of the speculation proved to be close to the

Tax Brief 9 May 2006 Budget 2006 Every year there is frenzied speculation about the likely content of the upcoming Budget. And, as is usually the case, some of the speculation proved to be close to the

INTERNATIONAL ASPECTS OF AUSTRALIAN INCOME TAX

INTERNATIONAL ASPECTS OF AUSTRALIAN INCOME TAX Chartered Accountants Business Advisers and Consultants Suite 201, Level 2 65 York Street, Sydney NSW 2000 Australia Telephone: 61+2+9290 1588 Facsimile:

INTERNATIONAL ASPECTS OF AUSTRALIAN INCOME TAX Chartered Accountants Business Advisers and Consultants Suite 201, Level 2 65 York Street, Sydney NSW 2000 Australia Telephone: 61+2+9290 1588 Facsimile:

Superannuation Superannuation

Superannuation Superannuation Using superannuation as a savings vehicle is a tax-effective way to increase your savings to meet your retirement goals. Types of superannuation funds There are many types

Superannuation Superannuation Using superannuation as a savings vehicle is a tax-effective way to increase your savings to meet your retirement goals. Types of superannuation funds There are many types

For personal use only

5 July 2016 Company Announcements Australian Securities Exchange Level 40 Central Park 152-158 St Georges Terrace Perth WA 6000 Dear Sir/Madam DISTRIBUTION OF EXPLORATION DEVELOPMENT INCENTIVE (EDI) CREDITS

5 July 2016 Company Announcements Australian Securities Exchange Level 40 Central Park 152-158 St Georges Terrace Perth WA 6000 Dear Sir/Madam DISTRIBUTION OF EXPLORATION DEVELOPMENT INCENTIVE (EDI) CREDITS

2013/2014 BUDGET & ATO ITEMS

pics 21 June 2013, Volume 3, Page 1 INDIVIDUALS AND FAMILIES Taxable Income Threshold and Marginal Tax Rates The following rates for 2013/14 apply from 1 July 2013: Resident thresholds $ Marginal rates

pics 21 June 2013, Volume 3, Page 1 INDIVIDUALS AND FAMILIES Taxable Income Threshold and Marginal Tax Rates The following rates for 2013/14 apply from 1 July 2013: Resident thresholds $ Marginal rates

Exposure draft improving the small business CGT concessions

28 February 2018 Small Business Entities and Industry Concessions Unit The Treasury Langton Crescent PARKES ACT 2600 By e-mail: SBCGTintegrity@treasury.gov.au Attention: Mr Greg Derlacz Dear Greg Exposure

28 February 2018 Small Business Entities and Industry Concessions Unit The Treasury Langton Crescent PARKES ACT 2600 By e-mail: SBCGTintegrity@treasury.gov.au Attention: Mr Greg Derlacz Dear Greg Exposure

2013 Tax Planning Checklist

Phone: 02 8296 0000 Email: admin@taccountants.com.au Web: taccountants.com.au Suite 404, Level 4, 25 Lime Street, Sydney NSW 2000 GPO Box 280, Sydney NSW 2001 2013 Tax Planning Checklist Table of Contents

Phone: 02 8296 0000 Email: admin@taccountants.com.au Web: taccountants.com.au Suite 404, Level 4, 25 Lime Street, Sydney NSW 2000 GPO Box 280, Sydney NSW 2001 2013 Tax Planning Checklist Table of Contents

Self-employed? You could claim a deduction for saving for your retirement

Client Update Newsletter Tax & Super September 2018 Self-employed? You could claim a deduction for saving for your retirement Photo by RhondaK Native Florida Folk Artist on Unsplash A recent change to

Client Update Newsletter Tax & Super September 2018 Self-employed? You could claim a deduction for saving for your retirement Photo by RhondaK Native Florida Folk Artist on Unsplash A recent change to

Relevant matters for Tax Practitioners

Relevant matters for Tax Practitioners Work related expenses Enterprise tax plan Cash economy ATO system outages Superannuation Changes/ Pre 1 st July Checklist Division 7A Sharing economy Whistle-blowers

Relevant matters for Tax Practitioners Work related expenses Enterprise tax plan Cash economy ATO system outages Superannuation Changes/ Pre 1 st July Checklist Division 7A Sharing economy Whistle-blowers