Transfer pricing documentation: Addressing the practical challenges The Dbriefs Transfer Pricing series

|

|

|

- Valentine Powell

- 6 years ago

- Views:

Transcription

1 Transfer pricing documentation: Addressing the practical challenges The Dbriefs Transfer Pricing series Fiona Craig / David Letos / Rahul Tomar 16 May 2017

2 Agenda Introduction Preparing for Country-by-Country (CbC) Reporting Practical tips for preparing Master File Local File Other issues Contract review Technology Questions and answers 2

3 Polling question 1 How advanced are you in your understanding of your CbC Reporting (CbCR) obligations? We have a detailed plan that sets out everything we need to do (notifications and filings), where, and by when We think we have our main countries covered off and the earliest deadlines under control, but after that it s less clear We are trying hard to keep up with all the requirements but finding it very difficult and don t have a real plan in place yet We are still wondering how this all got so hard 3

4 Preparing for Country-by-Country Reporting 4

5 Preparing for CbC Reporting The importance of planning Why is planning important? Our experience to date Tendency to underestimate level of complexity Tendency to over emphasise requirements in Parent Co s jurisdiction Tendency to over estimate quality and coverage of existing documentation Resourcing challenges First year will require significantly more resources and time to execute properly What can catch taxpayers off guard? Early adopters (especially those with Master File requirements) Notification requirements Potential exemptions (with deadlines) Nuance in local requirements E.g., countries with both Local File and separate local TP documentation requirements Proper planning helps clarify key questions up-front Where in which countries do you have reporting requirements? What what is required versus what is currently available? When by when do you need to prepare / file in each relevant country? Implications what potential penalties apply for not meeting certain requirements? 5

6 Preparing for CbC Reporting Key considerations in planning for CbC Reporting Strategic considerations What approach will you take to addressing the requirements? Big bang approach Complete and comprehensive refresh of your global documentation Addressing requirements in all countries Risk based approach Significance of operations and tax history Implications of non-compliance Likelihood of transfer pricing enquiry Centralized vs. decentralized Operational considerations How will you resource and execute the project Resourcing and responsibilities Project sponsor Central team Local teams Protocols for storing / sharing information Project management protocols Project timelines, stakeholder management Practical steps in developing the plan Develop reporting timeline, reflecting local country compliance requirements and priorities Confirm existing documentation and relevant transaction data Full review of all existing documentation and agreements Identify any gaps / inconsistencies in existing doc and the need for additional analysis Develop detailed project plan for execution (based on approach taken)

7 Polling question 2 Where have you got to in addressing your Master File / Local File obligations? Made good progress on the Master File Have a plan in place and are starting to meet Local File requirements On track to meet all Master File and Local File obligations globally Haven t commenced preparation of either report yet 7

8 Master File 8

9 Master File Recap on BEPS action 13 recommendations Master File includes Key challenges Group organizational structure Description of the business Intangibles Intercompany financial activities Need to centralize Financial and tax positions How much detail to include and how to articulate Use of product line approach First year will be critical Country adoption differences could create further complexity Information is made available to all jurisdictions. Taxpayers are required to create a high level blueprint of a multinational group s business Information is to be provided for the MNE as a whole holistic view Intended transparency on global operations and policies for Intellectual Property (IP) and financing Presentation either on overall group level or at product level Important requirements include Supply chain chart for the five largest products and service offerings plus other products or services amounting to more than 5% of a MNE s consolidated revenues Information on important IP or groups of IP plus information on legal ownership Unilateral income allocation rulings and Advance Pricing Agreements (APAs) 9

10 Master File Frequently Asked Questions what our clients are asking us? Is the Master File the same as the transfer pricing documentation we have previously prepared? Should we prepare comments to explain high profits in certain jurisdictions (particularly those with few people and assets)? Should we include more or less detail? What if the report is inconsistent with some of the comments in our annual report? 10

11 Master File Practical considerations Project launch and management Develop Master File strategy (e.g., minimum requirement vs. comprehensive) Consider level of transparency required to explain value chain and CbCR outputs (exercise judgement to avoid presenting unnecessary information) Drive timelines by the earliest approaching deadlines in the MNC s locations (not the headquarter regulations) Assess role of all stakeholders (including C-suite) early in the process Appoint project champion / team (linked to wider project planning phase) Information gathering process Gather exhaustive information across jurisdictions, especially in decentralized MNCs Leverage from Local File previously prepared and CbCR (if prepared first) Coordinate with local finance, legal, HR, and IT teams Identify TP positions taken across jurisdictions, business divisions, tax audits, and APAs Identify publicly available information on the supply chain, value drivers, intangibles, funding arrangements etc. Annual reports Devote sufficient resources to project management Evaluate technology solutions Establish protocols for updating and sharing of Master File (linked to protect planning phase) Investor presentations Websites Project launch and management Information gathering process Strategic alignment with BEPS Actions Information presentation and report structure 11 11

12 Master File Practical considerations (Cont d) Strategic alignment with BEPS Action Plan (8 10) Re-assess complex tax structures (e.g., IP holding companies, regional hubs, pass-through entities, central financing structures) Align risk / return based on the six step functional analysis approach Prepare a summary of key facts which support the transfer pricing policy (and capture these facts consistently and unambiguously in the Master File) Focus on augmenting substance in jurisdictions where CbCR will show disproportionate profits Information presentation and report structure Maintain proper check-lists to ensure that all elements are prepared (consider OECD and any specific country requirements) Identify information to be provided in main body of report versus appendix Validate global footprint disclosed within Master File with CbCR analysis Obtain sign-offs from respective stakeholders Evaluate translation requirements Define Groups of intangibles and General descriptions Project launch and management Information gathering process Strategic alignment with BEPS Actions Information presentation and report structure 12 12

13 Master File Sample reports 13

14 Master File OECD requirements tracked to the report 14

15 Polling question 3 What are the biggest challenges you are facing with the new CbCR obligations? Inconsistency of messaging in TP reports to date (i.e., historically prepared with focus on local view) Documentation does not always reflect what is actually happening in the business Intercompany agreements don t exist / are inconsistent / are not aligned with reality of business We don t have enough people to assist with the work required All of the above 15

16 Local File 16

, regional, or divisional Extent of outsourcing Build")

17 Local File Coordinated and appropriate attention to each jurisdiction Phase 1: planning Strategic documentation risk assessment and planning for TP documentation Review of existing reports and undertaking documentation risk assessment Is TP Policy change required in the post-beps world? Phase 1A Country-wise assessment of Local File requirement based on Jurisdiction Complexity of transactions Materiality of transactions Transaction value Phase 1B Identification of priority / complex / routine transactions, key jurisdictions Assign levels 1 to 4 to various country Local Files Decide on project management protocol central (HQ), regional, or divisional Extent of outsourcing Build consensus on process and policy among local tax directors / stakeholders Phase 2: report preparation Building the foundation through documentation Leveraging cutting edge tools and technology Getting TP compliant across jurisdictions in which client has operations Existing documentation Functional analysis validation DTi Existing transfer pricing policy Consolidated data Facilitate transfer pricing report preparation Country specific vs. OECD reports Economic analysis Digital DoX Review of Reports prepared by local Deloitte offices / your tax advisors in identified jurisdictions basis of the documentation risk assessment Regional vs. Local comparable / Local language reports on the basis of the documentation risk assessment Statutory accounts 17

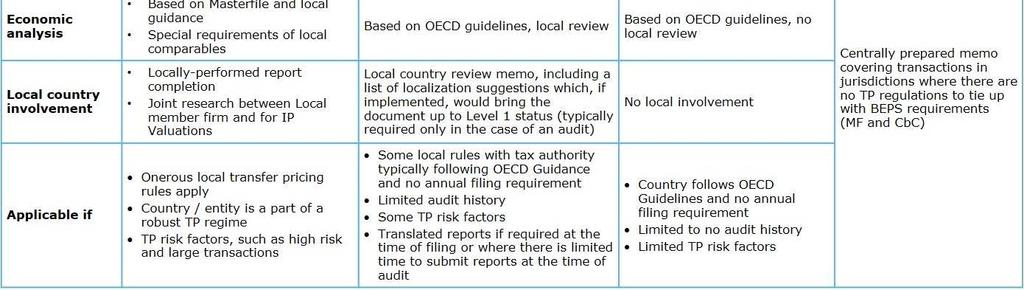

18 Local File: phase 1 Documentation risk assessment 18

19 Local File: phase 1 Documentation risk assessment (Cont d) 19

20 Local File: phase 2 Project management and report preparation Identify additional economic analyses required OR Gaps considering BEPS Economic analysis Leverage Consistency Profit split sanity check Feedback from local office / advisor Set up Project Management Tool Track timeliness and follow-up with relevant personnel Phase 1: planning Request for information Review available information and economic analysis Modular approach to minimize duplication of effort Draft Local Files for multiple countries GAP analysis vis-à-vis post- BEPS local requirements Local File elements FAR I/C agreements Industry Analysis? Review, sign-off, and finalization Set up Report Preparation Tool Old TP Reports, Master File information, I/C agreements, financials, and business reports Use Local / Master File report modules / templates Multiple people can modify / add information simultaneously Any gaps noticed OR local office suggestions Prioritize finalization based on specific country documentation deadlines Howto use an advisor and manage cost? Systematic effort (gap analysis, creation of templates and modules) in first year can significantly reduce costs in subsequent years First year, rely strongly on advisor and then employ / train internal team for subsequent years If a strong internal team and low risk structure, then use advisor for economic analysis only Discuss various aspects of technology tools upfront Data confidentiality Access rights to tool and data Future report update costs Extent and life of rights offered to the company Bundling with services Closely follow changing local laws in post-beps world to manage compliance costs and risks Establish an empowered internal team with CXO involvement 20

21 Local File Sample reports 21

22 Other issues Intercompany agreements and technology 22

23 Intercompany agreements What s changed? Inclusion of listing of intercompany agreements in Master Files and copies of intercompany agreements in Local Files Guidance on role of intercompany agreements in determining economic substance Guidance on contractual terms in context of the factors for determining comparability Increasing role of intercompany agreements for local revenue administrations Broadened definition of contractual terms 23

24 Intercompany agreements Gap analysis with respect to identifying, allocating, and addressing economically significant risks Does the actual conduct of the parties support the characterisation? Can the conduct be changed consistent with the company s business model? Can the management and control of risk be changed consistent with the company s business model? Determine changes that can be made to the contract or conduct to support intended characterisation of the entity 24

25 Intercompany agreements Some best practices Timing Consistency Consistency Clarity Pricing Flexibility 25

26 Contract analysis Sample checklist for contract review Elements that impact distributor's P&L Distributor responsible Counterparty responsible Issue not addressed Notes (e.g., elaborate if both parties are responsible) Revenue components 1. Characteristics of product (e.g., design, quality, specifications) 2. Overall business strategy 3. Product sales Cost components 1. Intercompany sale of products 2. Overall distribution process 2a. Logistics and freight (including customs costs) 2b. Inventory holding (e.g., how much to hold, how long to hold) 3. After-sales service 4. Advertising and marketing 5. Warranty 6. Product liability 6a. Other hazards (e.g., product damage, loss, recall) 6b. Regulatory 7. Routine administrative Other factors 1. Capital equipment 2. Term and termination Intangible ownership, maintenance, and protection Intellectual property ownership, maintenance, and protection 26

27 Contract analysis Sample checklist for contract review (Cont d) Elements that impact distributor's P&L Distributor responsible Counterparty responsible Issue not addressed Notes (e.g., elaborate if both parties are responsible) Cost components 4. Advertising and marketing Determine marketing and brand strategy and plans Create global marketing and advertising materials Create local marketing and advertising materials Local customization of global marketing material Execution of global marketing efforts (please specify: e.g., global sponsorship, global campaigns, operate global website) Execution of local marketing efforts (please specify: e.g., attend local tradeshows, place advertising in local outlets) Approval of locally developed marketing material Determine global marketing budget Adjust global marketing budget Determine local marketing budget Adjust local marketing budget 27

28 Technology utilization Technology for cost efficiency, collaboration, and consistency Diagnostic tools Project management tools Report preparation tools CbCdata collation and analysis of key ratios BEPS exposure heat map Profit split analysis vis-à-vis actual profits DEMPE assessor Global docs assessor Timeline management Alerts to relevant stakeholders at different milestones / deadlines Version control and file sharing Roadmap to completion Modular approach for leverage Collaboration across various MNC personnel and advisor Faster economic analysis Automation in generating consistent reports Watch out for artificial intelligence and robotics: A number of companies / advisors investing heavily 28

29 Questions and answers

30 Contact information Fiona Craig Asia Pacific Regional Leader Transfer Pricing Deloitte Sydney, Australia David Letos Tax Director Deloitte Melbourne, Australia Rahul Tomar Tax Partner Deloitte Delhi, India

31 Thanks for joining today s webcast. You may watch the archive on PC or mobile devices via itunes, RSS, YouTube. Eligible viewers may now download CPE certificates. Click the CPE icon at the bottom of your screen.

32 Join us 18 May at 2PM HKT (GMT +8) as our Global Mobility, Talent & Rewards series presents: Global immigration: A new landscape and mindset For more information, visit

33 Dbriefs Bytes This video brings you a weekly summary of the significant international tax developments. It is broadcast every Friday afternoon. Dbriefs Bytes is also available in Chinese and is broadcast every Tuesday. For more information, visit To view archives, visit

34 This presentation contains general information only and Deloitte is not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this presentation.

35 About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee ( DTTL ), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as Deloitte Global ) does not provide services to clients. Please see for a more detailed description of DTTL and its member firms.

Future of tax in a digital economy: Are you prepared? The Dbriefs International Tax series

Future of tax in a digital economy: Are you prepared? The Dbriefs International Tax series Claudio Cimetta / Li Qun Gao / William Marshall 1 June 2017 Agenda The digital economy Tax challenges of the digital

Future of tax in a digital economy: Are you prepared? The Dbriefs International Tax series Claudio Cimetta / Li Qun Gao / William Marshall 1 June 2017 Agenda The digital economy Tax challenges of the digital

China VAT: It's time to reap the savings The Dbriefs China Spotlight series

China VAT: It's time to reap the savings The Dbriefs China Spotlight series Sarah Chin / Li Qun Gao / Candy Tang 20 June 2017 Agenda Latest development of China VAT rules Saving opportunities Future development

China VAT: It's time to reap the savings The Dbriefs China Spotlight series Sarah Chin / Li Qun Gao / Candy Tang 20 June 2017 Agenda Latest development of China VAT rules Saving opportunities Future development

BEPS Country-by-Country Reporting Rules and New Documentation Requirements

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

BEPS Country-by-Country Reporting Rules and New Documentation Requirements, EY LLP, Couzin Taylor LLP 67 th Annual Tax Conference 67e Conférence fiscale annuelle 2015 Agenda 1. The BEPS project: Action

Australian government introduces bill to combat multinational tax avoidance

Australian government introduces bill to combat multinational tax avoidance The Australian Treasurer introduced a bill to combat multinational tax avoidance into parliament on 16 September 2015. The proposals

Australian government introduces bill to combat multinational tax avoidance The Australian Treasurer introduced a bill to combat multinational tax avoidance into parliament on 16 September 2015. The proposals

Global Financial Reporting.

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Randall Sogoloff / Philip Barden 18 October 2011 Agenda Updated IASB work plan Revenue recognition Exposure Draft

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Randall Sogoloff / Philip Barden 18 October 2011 Agenda Updated IASB work plan Revenue recognition Exposure Draft

China Related Party Transactions and TP Documentation Rules Highlights. 10 August 2016

China Related Party Transactions and TP Documentation Rules Highlights 10 August 2016 Related Party Transactions and TP Documentation Rules Aligned with OECD recommendations and adapted for China Bulletin

China Related Party Transactions and TP Documentation Rules Highlights 10 August 2016 Related Party Transactions and TP Documentation Rules Aligned with OECD recommendations and adapted for China Bulletin

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises Kazakhstan, 2016 Brochure / report title goes here Section title goes here Documentation requirements

New post-beps three-tiered documentation requirements Impact for Kazakhstan s multinational enterprises Kazakhstan, 2016 Brochure / report title goes here Section title goes here Documentation requirements

BEPS Impact on Manufacturing

BEPS Impact on Manufacturing Base Erosion and Profit Shifting India has emerged as the seventh largest economy. Favorable demographics, a burgeoning domestic market and an annual growth rate in excess

BEPS Impact on Manufacturing Base Erosion and Profit Shifting India has emerged as the seventh largest economy. Favorable demographics, a burgeoning domestic market and an annual growth rate in excess

MANAGING TRANSFER PRICING ISSUES IN AN EVOLVING BEPS ENVIRONMENT

MANAGING TRANSFER PRICING ISSUES IN AN EVOLVING BEPS ENVIRONMENT ANTON HUME / DAN MCGEOWN / VEENA PARRIKAR / RICHARD VAN DER POEL / JAY TANG 2 JUNE 2015 AGENDA Control Over Transfer Pricing Policies and

MANAGING TRANSFER PRICING ISSUES IN AN EVOLVING BEPS ENVIRONMENT ANTON HUME / DAN MCGEOWN / VEENA PARRIKAR / RICHARD VAN DER POEL / JAY TANG 2 JUNE 2015 AGENDA Control Over Transfer Pricing Policies and

Global Financial Reporting.

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Joel Osnoss / Randall Sogoloff / Andrew Spooner 18 January 2012 Agenda Updated IASB work plan IFRS developments Financial

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Joel Osnoss / Randall Sogoloff / Andrew Spooner 18 January 2012 Agenda Updated IASB work plan IFRS developments Financial

Legal DELOITTE TAXLAB Peter Kits & Pim Gerritsen van der Hoop

Legal DELOITTE TAXLAB 2017 Peter Kits & Pim Gerritsen van der Hoop Agenda Introduction: intragroup contracts Intragroup contract drafting Distribution and sales transaction Production settings Dealing

Legal DELOITTE TAXLAB 2017 Peter Kits & Pim Gerritsen van der Hoop Agenda Introduction: intragroup contracts Intragroup contract drafting Distribution and sales transaction Production settings Dealing

Asia Pacific Customs and Trade Conference

www.pwccustoms.com Asia Pacific Customs and Trade Conference What the BEPS?!? Frank Debets, Partner, WMS Singapore Howard Osawa, Director, WMS Japan Agenda Introduction to BEPS Potential impact of BEPS

www.pwccustoms.com Asia Pacific Customs and Trade Conference What the BEPS?!? Frank Debets, Partner, WMS Singapore Howard Osawa, Director, WMS Japan Agenda Introduction to BEPS Potential impact of BEPS

Preparing for an IPO: Build a solid plan and avoid surprises. The Dbriefs Private Companies series

Webcast title in Verdana Regular Preparing for an IPO: Build a solid plan and avoid surprises The Dbriefs Private Companies series Bernie De Jager, Partner Audit & Assurance Ryan Tolley, Senior Manager

Webcast title in Verdana Regular Preparing for an IPO: Build a solid plan and avoid surprises The Dbriefs Private Companies series Bernie De Jager, Partner Audit & Assurance Ryan Tolley, Senior Manager

A new age of talent mobility: Planning for tax reform and regulatory uncertainty The Dbriefs Global Mobility, Talent, & Rewards series Joel

A new age of talent mobility: Planning for tax reform and regulatory uncertainty The Dbriefs Global Mobility, Talent, & Rewards series Joel Eisenreich, Principal, Deloitte Tax LLP Nicole Patterson, Managing

A new age of talent mobility: Planning for tax reform and regulatory uncertainty The Dbriefs Global Mobility, Talent, & Rewards series Joel Eisenreich, Principal, Deloitte Tax LLP Nicole Patterson, Managing

Proposed new guidelines:

Proposed new guidelines: Transfer pricing documentation & Country by Country reporting (BEPS Action 13) Jeroen Geevers & Jack Favre ITS / Transfer pricing EY Rotterdam May, 2014 Changing information to

Proposed new guidelines: Transfer pricing documentation & Country by Country reporting (BEPS Action 13) Jeroen Geevers & Jack Favre ITS / Transfer pricing EY Rotterdam May, 2014 Changing information to

India releases final rules on country-by-country reporting and master file

Arm s Length Standard Global views within reach. India releases final rules on country-by-country reporting and master file India s Central Board of Direct Taxes (CBDT) on 31 October released the final

Arm s Length Standard Global views within reach. India releases final rules on country-by-country reporting and master file India s Central Board of Direct Taxes (CBDT) on 31 October released the final

BEPS Action Plan Item 13: The New Documentation Standard and Implications for the Financial Services Industry

BEPS Action Plan Item 13: The New Documentation Standard and Implications for the Financial Services Industry The Organization for Economic Cooperation and Development completed and released the Guidance

BEPS Action Plan Item 13: The New Documentation Standard and Implications for the Financial Services Industry The Organization for Economic Cooperation and Development completed and released the Guidance

COUNTRY BY COUNTRY REPORTING LOCAL FILE WEBINAR 16 November 2017 ZARA RITCHIE - BDO NATALYA MARENINA - BDO JOANNE TING THOMSON REUTERS

COUNTRY BY COUNTRY REPORTING LOCAL FILE WEBINAR 16 November 2017 ZARA RITCHIE - BDO NATALYA MARENINA - BDO JOANNE TING THOMSON REUTERS OUTLINE OF SESSION 1 Background and requirements for SGEs 2 Country

COUNTRY BY COUNTRY REPORTING LOCAL FILE WEBINAR 16 November 2017 ZARA RITCHIE - BDO NATALYA MARENINA - BDO JOANNE TING THOMSON REUTERS OUTLINE OF SESSION 1 Background and requirements for SGEs 2 Country

Global Financial Reporting.

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Joel Osnoss / Randall Sogoloff / Andrew Spooner 25 July 2012 Agenda IFRS update Project update Financial instruments

Asia Pacific Dbriefs Presents: Global Financial Reporting. IFRS: Important Developments Joel Osnoss / Randall Sogoloff / Andrew Spooner 25 July 2012 Agenda IFRS update Project update Financial instruments

Engaging title in Green Descriptive element in Blue 2 lines if needed

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

BEPS Impact on TMT Sector January 2016 Engaging title in Green Descriptive element in Blue 2 lines if needed Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure Let s be crystal clear:

The BEPS project is the beginning, but is the end in sight?

The BEPS project is the beginning, but is the end in sight? Panel Moderator Panel Michael Hewson Annet Oguttu Oliver Wehnert Ryaad Owodally Africa Transfer Pricing Leader EY Africa Professor of Tax Law

The BEPS project is the beginning, but is the end in sight? Panel Moderator Panel Michael Hewson Annet Oguttu Oliver Wehnert Ryaad Owodally Africa Transfer Pricing Leader EY Africa Professor of Tax Law

OECD/G20 Base Erosion and Profit Shifting Project

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

OECD/G20 Base Erosion and Profit Shifting Project Action 13: Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Country-by-Country Report Instructions Manual 24 June 2015 Page

transfer pricing documentation

Mai Nomura Summary Headline on Verdana CbC reporting Bold and transfer pricing documentation Mai Nomura 24 October, 2017 New transfer pricing compliance requirements in Hungary: Country-by-Country Reporting

Mai Nomura Summary Headline on Verdana CbC reporting Bold and transfer pricing documentation Mai Nomura 24 October, 2017 New transfer pricing compliance requirements in Hungary: Country-by-Country Reporting

Decoding Enhanced Transfer Pricing Documentation Requirements in India

Decoding Enhanced Transfer Pricing Documentation Requirements in India Meghnand Dungarwal Principal, Transfer Pricing Advisory Contents Indian transfer pricing documentation requirements - recent updates

Decoding Enhanced Transfer Pricing Documentation Requirements in India Meghnand Dungarwal Principal, Transfer Pricing Advisory Contents Indian transfer pricing documentation requirements - recent updates

BEPS ACTION 13 GUIDE HELPING YOUR ORGANIZATION BECOME BEPS COMPLIANT

BEPS ACTION 13 GUIDE HELPING YOUR ORGANIZATION BECOME BEPS COMPLIANT CONTENTS 1 Legal Entity Organization Charts 2 Headcount Data and Management Organization Charts 3 Country-by-Country Tables and Local

BEPS ACTION 13 GUIDE HELPING YOUR ORGANIZATION BECOME BEPS COMPLIANT CONTENTS 1 Legal Entity Organization Charts 2 Headcount Data and Management Organization Charts 3 Country-by-Country Tables and Local

Deloitte TaxMax The 43 rd series One bold step in the right direction. Theresa Goh & Subhabrata Dasgupta l 22 November 2017 By Deloitte Tax Academy

Deloitte TaxMax The 43 rd series One bold step in the right direction Theresa Goh & Subhabrata Dasgupta l 22 November 2017 By Deloitte Tax Academy What are we discussing today? 01 02 Emerging trends Key

Deloitte TaxMax The 43 rd series One bold step in the right direction Theresa Goh & Subhabrata Dasgupta l 22 November 2017 By Deloitte Tax Academy What are we discussing today? 01 02 Emerging trends Key

Enhanced disclosures: Leading practices and current trends

Enhanced disclosures: Leading practices and current trends The Dbriefs Governance, Risk & Compliance series Deb DeHaas, Vice chairman, National Managing Partner, Deloitte Consuelo Hitchcock, Management

Enhanced disclosures: Leading practices and current trends The Dbriefs Governance, Risk & Compliance series Deb DeHaas, Vice chairman, National Managing Partner, Deloitte Consuelo Hitchcock, Management

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February AM PM Conrad Hotel, Hong Kong

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

THE FUTURE OF TAX PLANNING: TRANSPARENCY AND SUBSTANCE FOR ALL? Friday, 26 February 2016 9.00AM - 12.00PM Conrad Hotel, Hong Kong THE DRIVE TOWARDS TRANSPARENCY: CHALLENGES AND OPPORTUNITIES IN INTERNATIONAL

Transfer Pricing: Theory & Practice

Transfer Pricing: Theory & Practice TEI Houston Chapter Your Auditor and Transfer Pricing Randy G. Price, Deloitte Tax LLP Rupesh R. Vadapalli, Deloitte Tax LLP March 1, 2018 Agenda Impact of International

Transfer Pricing: Theory & Practice TEI Houston Chapter Your Auditor and Transfer Pricing Randy G. Price, Deloitte Tax LLP Rupesh R. Vadapalli, Deloitte Tax LLP March 1, 2018 Agenda Impact of International

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

Headline Verdana Bold International Tax matters ICPAU Tax Seminar, Hotel Africana November, 2017 Contents Related party transactions 3 URA practice on international tax 14 OCED Action Plan on BEPS 30 2017

32nd Annual Asia Pacific Tax Conference November 2016 JW Marriott Hotel Hong Kong

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong The consequences of real transparency: Reporting,documentation and reconsidering your Asian structures in light of

32nd Annual Asia Pacific Tax Conference 10 11 November 2016 JW Marriott Hotel Hong Kong The consequences of real transparency: Reporting,documentation and reconsidering your Asian structures in light of

Day 2: Session 2 Tax governance, risk and control

Day 2: Session 2 Tax governance, risk and control The Westin, Singapore 26 February 2016 James Paul Deloitte 1 Agenda 1. The changing tax environment and business response 2. Focus on tax governance, policy

Day 2: Session 2 Tax governance, risk and control The Westin, Singapore 26 February 2016 James Paul Deloitte 1 Agenda 1. The changing tax environment and business response 2. Focus on tax governance, policy

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15. Mr. S.P. Singh, Ex-IRS 7th November, 2015

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15 Mr. S.P. Singh, Ex-IRS 7th November, 2015 Contents Action 11 - Establishing Methodologies to Collect and Analyze Data on BEPS Action 12 Requiring

Base Erosion and Profit Sharing Action Plan 11, 12, 14 & 15 Mr. S.P. Singh, Ex-IRS 7th November, 2015 Contents Action 11 - Establishing Methodologies to Collect and Analyze Data on BEPS Action 12 Requiring

SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018

CPAs & ADVISORS experience direction // SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018 William D. James Principal Transfer Pricing & David H. Whitmer Director Transfer

CPAs & ADVISORS experience direction // SUBSTANCE IS KING IN THE NEW WORLD ORDER TAX EXECUTIVES INSTITUTE, INC. MARCH 1, 2018 William D. James Principal Transfer Pricing & David H. Whitmer Director Transfer

Why Legal Entity Management matters Webcast 2014

Webcast 2014 6 March 2014 Your panel on today s webcast Samantha Keen Transaction Advisory Services Email: skeen@uk.ey.com Graham Roberts Financial Accounting Advisory Services Email: groberts1@uk.ey.com

Webcast 2014 6 March 2014 Your panel on today s webcast Samantha Keen Transaction Advisory Services Email: skeen@uk.ey.com Graham Roberts Financial Accounting Advisory Services Email: groberts1@uk.ey.com

CA T. P. OSTWAL. T. P. Ostwal & Associates LLP

CA T. P. OSTWAL BEPS strategies may not necessarily be illegal Increased globalisation enables companies to exploit gaps arising on interaction of domestic tax systems and treaty rules within the boundary

CA T. P. OSTWAL BEPS strategies may not necessarily be illegal Increased globalisation enables companies to exploit gaps arising on interaction of domestic tax systems and treaty rules within the boundary

Practical Implications of BEPS

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

www.pwc.com/il Practical Implications of BEPS Vered Kirshner, Tax Partner, PwC Israel Ben Blumenfeld, Tax and Transfer Pricing Senior Manager, PwC Israel Aim of BEPS Action plan backed by the OECD and

A Guide To Changes In Irish Tax Rules

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

A Guide To Changes In Irish Tax Rules - The Global Tax Reform Agenda 6 September 2016 THE FACTS YOU NEED TO KNOW ON IRISH TAX CHANGES 1 INTERNATIONAL TAX RULES HAVE BEEN CHANGING - IRELAND HAS BEEN PARTICIPATING

Trends in Transfer Pricing Global Research Bulletin. March 2016

Trends in Transfer Pricing Global Research Bulletin March 2016 The story in brief Businesses are looking to increase control over their Transfer Pricing positions in order to minimize risk. They are becoming

Trends in Transfer Pricing Global Research Bulletin March 2016 The story in brief Businesses are looking to increase control over their Transfer Pricing positions in order to minimize risk. They are becoming

Global Tax Alert. OECD releases report under BEPS Action 13 on Transfer Pricing Documentation and Country-by-Country Reporting.

23 September 2014 EY Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/ Services/Tax/International- Tax/Tax-alert-library#date

23 September 2014 EY Library Access both online and pdf versions of all EY Global Tax Alerts. Copy into your web browser: http://www.ey.com/gl/en/ Services/Tax/International- Tax/Tax-alert-library#date

The OECD s Discussion Draft on Transfer Pricing Documentation and Country-by-Country Reporting: A work in progress

Global Transfer Pricing Arm s Length Standard (Special Edition) In this issue: The OECD s Discussion Draft on Transfer Pricing Documentation and Country-by-Country Reporting: A work in progress... 1 The

Global Transfer Pricing Arm s Length Standard (Special Edition) In this issue: The OECD s Discussion Draft on Transfer Pricing Documentation and Country-by-Country Reporting: A work in progress... 1 The

Transfer Pricing Perspectives: The new normal: full TransParency. The post BEPS world in the automotive industry

The post BEPS world in the automotive industry 43 The automotive industry has followed a global footprint strategy since many years and it represents now the industry with the highest cross border intercompany

The post BEPS world in the automotive industry 43 The automotive industry has followed a global footprint strategy since many years and it represents now the industry with the highest cross border intercompany

China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation

Arm s Length Standard Global views within reach. China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation China s State Administration of Taxation (SAT)

Arm s Length Standard Global views within reach. China s SAT issues new rules on reporting of related-party transactions and contemporaneous documentation China s State Administration of Taxation (SAT)

Quarterly accounting roundup: An update on Q important developments The Dbriefs Financial Reporting series

Quarterly accounting roundup: An update on Q2 2017 important developments The Dbriefs Financial Reporting series Robert Uhl, Partner, Deloitte & Touche LLP Chris Chiriatti, Managing Director, Deloitte

Quarterly accounting roundup: An update on Q2 2017 important developments The Dbriefs Financial Reporting series Robert Uhl, Partner, Deloitte & Touche LLP Chris Chiriatti, Managing Director, Deloitte

Indian Tax Administration releases draft rules on Country-by-Country reporting and Master File implementation for public comment

10 October 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases draft rules on Country-by-Country reporting and Master File implementation for public comment EY Global Tax

10 October 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases draft rules on Country-by-Country reporting and Master File implementation for public comment EY Global Tax

Why Legal Entity Management Matters IV

Why Legal Entity Management Matters IV Collating and reporting legal entity information in today s environment: are you prepared? Issue 4.0 Q3 2015 Collating and reporting legal entity information in today

Why Legal Entity Management Matters IV Collating and reporting legal entity information in today s environment: are you prepared? Issue 4.0 Q3 2015 Collating and reporting legal entity information in today

Statement for the Record

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

Statement for the Record of Dorothy Coleman Vice President, Tax & Domestic Economic Policy National Association of Manufacturers For the Hearing of the Senate Finance Committee on International Tax: OECD

The discussion draft addresses BEPS Actions 8, 9, and 10, which concern the development of:

BEPS Actions 8, 9, and 10: Discussion Draft on Revisions to Chapter I of the Transfer Pricing Guidelines (Including Risk, Recharacterization, and Special Measures) The Organization for Economic Cooperation

BEPS Actions 8, 9, and 10: Discussion Draft on Revisions to Chapter I of the Transfer Pricing Guidelines (Including Risk, Recharacterization, and Special Measures) The Organization for Economic Cooperation

Functions, Assets and Risk Analysis under Transfer Pricing

Functions, Assets and Risk Analysis under Transfer Pricing September 23, 2017 Jigna P. Talati CONTENTS What is Functions, Assets and Risk ( FAR ) Analysis Why do a FAR Analysis How to do a FAR Analysis

Functions, Assets and Risk Analysis under Transfer Pricing September 23, 2017 Jigna P. Talati CONTENTS What is Functions, Assets and Risk ( FAR ) Analysis Why do a FAR Analysis How to do a FAR Analysis

LEARNING OBJECTIVES TRANSFER PRICING DOCUMENTATION. THE ROLE OF TPD Showing Compliance. Fundamentals of Transfer Pricing Documentation

UN-ATAF Workshop on Transfer Pricing Administrative Aspects and Recent Developments Ezulwini, Swaziland 4-8 December 2017 LEARNING OBJECTIVES Understanding and Reviewing Transfer Pricing Documentation

UN-ATAF Workshop on Transfer Pricing Administrative Aspects and Recent Developments Ezulwini, Swaziland 4-8 December 2017 LEARNING OBJECTIVES Understanding and Reviewing Transfer Pricing Documentation

Intercompany financing facing new challenges. EY Africa Tax Conference September 2014

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Intercompany financing facing new challenges EY Africa Tax Conference September 2014 Panel Moderator Ide Louw International Tax EY South Africa Panel Joseph Pagop Noupoue EY Jemimah Mugo EY Kenya Michael

Value Chain Management

Value Chain Management Aligning transfer pricing outcomes with value creation Annual Transfer Pricing Seminar November 23, 2016 Presenters Àgata Uceda Director +31 (0)88 90 91420 Uceda.Agata@kpmg.com Jeroen

Value Chain Management Aligning transfer pricing outcomes with value creation Annual Transfer Pricing Seminar November 23, 2016 Presenters Àgata Uceda Director +31 (0)88 90 91420 Uceda.Agata@kpmg.com Jeroen

OECD Release on Transfer Pricing Documentation: The New Global Standard

OECD Release on Transfer Pricing Documentation: The New Global Standard The OECD s final revisions to Chapter V of the transfer pricing guidelines (issued September 16) materially reduce the documentation

OECD Release on Transfer Pricing Documentation: The New Global Standard The OECD s final revisions to Chapter V of the transfer pricing guidelines (issued September 16) materially reduce the documentation

Transfer Pricing: The New Frontier Transfer Pricing Documentation in a Post-BEPS World: Evolution or Revolution? November 8, 2018

Transfer Pricing: The New Frontier Transfer Pricing Documentation in a Post-BEPS World: Evolution or Revolution? November 8, 2018 Today s Speakers Astrid Pieron Partner, Brussels apieron@mayerbrown.com

Transfer Pricing: The New Frontier Transfer Pricing Documentation in a Post-BEPS World: Evolution or Revolution? November 8, 2018 Today s Speakers Astrid Pieron Partner, Brussels apieron@mayerbrown.com

PCT WBG IMF OECD. The Platform for Collaboration on Tax (PCT) The Platform for Collaboration on Tax (PCT) Workplan: PCT 14 Actions

The Platform for Collaboration on Tax (PCT) Workplan: PCT 14 Actions") The Platform for Collaboration on Tax (PCT) The (PCT) Strengthening Tax Capacity in Developing Countries: Inter-agency ECOSOC Special Meeting on International Cooperation in Tax Matters New York, 18 May

The Platform for Collaboration on Tax (PCT) The (PCT) Strengthening Tax Capacity in Developing Countries: Inter-agency ECOSOC Special Meeting on International Cooperation in Tax Matters New York, 18 May

Transfer Pricing Update

Transfer Pricing Update Ray Brown, Principal Economist, DLA Piper - Los Angeles Mike Patton, Partner, DLA Piper - Los Angeles Eric Ryan, Partner, DLA Piper - Silicon Valley *This presentation is offered

Transfer Pricing Update Ray Brown, Principal Economist, DLA Piper - Los Angeles Mike Patton, Partner, DLA Piper - Los Angeles Eric Ryan, Partner, DLA Piper - Silicon Valley *This presentation is offered

SIFM. Annual Conference September 19, Overview of Final BEPS Report / Update on Country by Country Reporting Requirements

SIFM Annual Conference September 19, 2016 Overview of Final BEPS Report / Update on Country by Country Reporting Requirements Presenters: John Forni, Managing Director Allen Brandsdofer, Transfer Pricing

SIFM Annual Conference September 19, 2016 Overview of Final BEPS Report / Update on Country by Country Reporting Requirements Presenters: John Forni, Managing Director Allen Brandsdofer, Transfer Pricing

Indian Tax Administration releases final rules on Country-by-Country reporting and Master File implementation

6 November 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases final rules on Country-by-Country reporting and Master File implementation EY Global Tax Alert Library Access

6 November 2017 Global Tax Alert News from Transfer Pricing Indian Tax Administration releases final rules on Country-by-Country reporting and Master File implementation EY Global Tax Alert Library Access

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide Douglas Fone Global Partner, Transfer Pricing Associates 1 Content 1. Introduction

Resolving transfer pricing controversies, handling audits and queries, and best practices in TP documentation: A practical guide Douglas Fone Global Partner, Transfer Pricing Associates 1 Content 1. Introduction

BEPS Action Plan 13. Master File and Country by Country reporting: Navigating challenges with tax, accounting and IT service offerings. KPMG.

BEPS Action Plan 13 Master File and Country by Country reporting: Navigating challenges with tax, accounting and IT service offerings KPMG.com/in Introduction As one of the pioneers and major contributors

BEPS Action Plan 13 Master File and Country by Country reporting: Navigating challenges with tax, accounting and IT service offerings KPMG.com/in Introduction As one of the pioneers and major contributors

FASB's new credit impairment model: At a loss for what to do The Dbriefs Financial Executives series

FASB's new credit impairment model: At a loss for what to do The Dbriefs Financial Executives series Bob Uhl, Partner, Deloitte & Touche LLP Jon Howard, Partner, Deloitte & Touche LLP Jonathan Prejean,

FASB's new credit impairment model: At a loss for what to do The Dbriefs Financial Executives series Bob Uhl, Partner, Deloitte & Touche LLP Jon Howard, Partner, Deloitte & Touche LLP Jonathan Prejean,

Headline Verdana Bold Managing tax Balancing current challenge with future promise The EYE, Amsterdam, 30 November - 1 December 2016

Headline Verdana Bold Managing tax Balancing current challenge with future promise The EYE, Amsterdam, 30 November - 1 December 2016 Marvin de Ridder, Deloitte Netherlands Emmet Bulman, Deloitte UK Tax

Headline Verdana Bold Managing tax Balancing current challenge with future promise The EYE, Amsterdam, 30 November - 1 December 2016 Marvin de Ridder, Deloitte Netherlands Emmet Bulman, Deloitte UK Tax

Headline Verdana Bold Deloitte TaxMax The 43 rd series One bold step in the right direction Richard Mackender & Senthuran Elalingam l 22 November

Headline Verdana Bold Deloitte TaxMax The 43 rd series Richard Mackender & Senthuran Elalingam l 22 November 2017 by Deloitte Tax Academy Agenda The Digital Economy 3 Background and market research 8 Managing

Headline Verdana Bold Deloitte TaxMax The 43 rd series Richard Mackender & Senthuran Elalingam l 22 November 2017 by Deloitte Tax Academy Agenda The Digital Economy 3 Background and market research 8 Managing

China s SAT issues new rules to improve administration of special tax investigations and Mutual Agreement Procedures

1 See Deloitte Tax Analysis on Bulletin 42: https://www2.deloitte.com/content/dam/deloitte/cn/documents/tax/ta-2016/deloitte-cn-tax-tap2412016-en-160713.pdf 2 See Deloitte Tax Analysis on Bulletin 64:

1 See Deloitte Tax Analysis on Bulletin 42: https://www2.deloitte.com/content/dam/deloitte/cn/documents/tax/ta-2016/deloitte-cn-tax-tap2412016-en-160713.pdf 2 See Deloitte Tax Analysis on Bulletin 64:

Insurance Tax Insight The Global Tax Reset: BEPS & Insurance

Insurance Tax Insight The Global Tax Reset: BEPS & Insurance On 5 October 2015, the OECD published 13 papers outlining consensus actions under the base erosion and profit shifting (BEPS) project. The output

Insurance Tax Insight The Global Tax Reset: BEPS & Insurance On 5 October 2015, the OECD published 13 papers outlining consensus actions under the base erosion and profit shifting (BEPS) project. The output

Media & Entertainment Spotlight Navigating the New Revenue Standard

July 2014 Media & Entertainment Spotlight Navigating the New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Transition Considerations Thinking Ahead The

July 2014 Media & Entertainment Spotlight Navigating the New Revenue Standard In This Issue: Background Key Accounting Issues Effective Date and Transition Transition Considerations Thinking Ahead The

Global tax management Japan research report. Global Tax Management. Japan Research Report. Tax Management Consulting Deloitte Tohmatsu Tax Co.

Global tax management research report Global Tax Management Research Report Tax Management Consulting Deloitte Tohmatsu Tax Co. June 2017 Global tax management research report Evolving insights 2 Global

Global tax management research report Global Tax Management Research Report Tax Management Consulting Deloitte Tohmatsu Tax Co. June 2017 Global tax management research report Evolving insights 2 Global

Country-by-Country Reporting The FAQs. Singapore Tax and Legal

Country-by-Country Reporting The FAQs Singapore Tax and Legal The reset landscape There is a Global Tax Reset underway. The confluence of the OECD s actions relating to Base Erosion & Profit Shifting (BEPS)

Country-by-Country Reporting The FAQs Singapore Tax and Legal The reset landscape There is a Global Tax Reset underway. The confluence of the OECD s actions relating to Base Erosion & Profit Shifting (BEPS)

IBFD Course Programme Transfer Pricing: Compliance and Audit Management in Southeast Asia

IBFD Course Programme Transfer Pricing: Compliance and Audit Management in Southeast Asia Summary This course will provide you with the best practices for implementing transfer pricing documentation requirements

IBFD Course Programme Transfer Pricing: Compliance and Audit Management in Southeast Asia Summary This course will provide you with the best practices for implementing transfer pricing documentation requirements

Arm s Length Principle. Kavita Sethia Gambhir

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

Arm s Length Principle Kavita Sethia Gambhir January 2017 Introduction 2 Background Economic Globalization Multinational Structure Different Objectives Top Management/Key Personnel Shareholders Tax Authorities

G20/OECD: BEPS, Intangibles, ICE and Transfer Pricing. Brazil October 2013

G20/OECD: BEPS, Intangibles, ICE and Transfer Pricing Brazil October 2013 Disclaimer This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting,

G20/OECD: BEPS, Intangibles, ICE and Transfer Pricing Brazil October 2013 Disclaimer This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting,

Indian rules on Master File and Country-by-Country-Reporting requirements

from Transfer Pricing Indian rules on Master File and Country-by-Country-Reporting requirements December 21, 2017 In brief Reiterating India s commitment to implement the OECD s BEPS Action Plan 13, the

from Transfer Pricing Indian rules on Master File and Country-by-Country-Reporting requirements December 21, 2017 In brief Reiterating India s commitment to implement the OECD s BEPS Action Plan 13, the

Presentation by Shigeto HIKI

Presentation by Shigeto HIKI Co-chair of Forum on Harmful Tax Practices Director International Tax Policy Division, Tax Bureau Ministry of Finance, Japan The Fifth IMF-Japan High-Level Tax Conference For

Presentation by Shigeto HIKI Co-chair of Forum on Harmful Tax Practices Director International Tax Policy Division, Tax Bureau Ministry of Finance, Japan The Fifth IMF-Japan High-Level Tax Conference For

Prior to joining Microsoft, Angel worked for Arthur Andersen in their New York Office.

Steve covers Finance, CELA and Human Resource (HR). The Finance function includes: Purchasing, RE&F, Venture Integration, Corporate Finance, Finance Operations, Physical Security, Treasury, Investor Relations,

Steve covers Finance, CELA and Human Resource (HR). The Finance function includes: Purchasing, RE&F, Venture Integration, Corporate Finance, Finance Operations, Physical Security, Treasury, Investor Relations,

BEPS Impact on Private Equity

BEPS Impact on Private Equity BEPS impact on private equityspace An Indian perspective In this age of increasing focus on bottomlines, it is indeed tempting for a global tax director of a multinational

BEPS Impact on Private Equity BEPS impact on private equityspace An Indian perspective In this age of increasing focus on bottomlines, it is indeed tempting for a global tax director of a multinational

Australia issues draft guidelines on inbound distribution arrangements. Global Transfer Pricing Alert

Global Transfer Pricing 7 December 2018 Australia issues draft guidelines on inbound distribution arrangements Global Transfer Pricing Alert 2018-036 The Australian Taxation Office on 23 November released

Global Transfer Pricing 7 December 2018 Australia issues draft guidelines on inbound distribution arrangements Global Transfer Pricing Alert 2018-036 The Australian Taxation Office on 23 November released

BEPS & transfer pricing

BEPS & transfer pricing May 2015 Suchint Majmudar, Taxand India Amit Rana, GE Polly Mak, Michelin Tim Wach, Taxand Global Contents 1. Introduction: background to BEPS 2. What is BEPS? 3. Key BEPS concerns

BEPS & transfer pricing May 2015 Suchint Majmudar, Taxand India Amit Rana, GE Polly Mak, Michelin Tim Wach, Taxand Global Contents 1. Introduction: background to BEPS 2. What is BEPS? 3. Key BEPS concerns

How global megatrends could change tax in Africa

How global megatrends could change tax in Africa Panel Moderator Panel Mark Goulding George Trollope Mark Kingon Michael Lalor EY Tax market segment leader Southern region Vice President Tax Sasol South

How global megatrends could change tax in Africa Panel Moderator Panel Mark Goulding George Trollope Mark Kingon Michael Lalor EY Tax market segment leader Southern region Vice President Tax Sasol South

Paradigm shift Using Value Chain Alignment to reshape your operating model and tax strategies to the modern business landscape

Paradigm shift Using Value Chain Alignment to reshape your operating model and tax strategies to the modern business landscape June 2018 A global tax reset is underway. Is your business positioned to thrive?

Paradigm shift Using Value Chain Alignment to reshape your operating model and tax strategies to the modern business landscape June 2018 A global tax reset is underway. Is your business positioned to thrive?

Irish Revenue release details on monitoring compliance with transfer pricing rules. Global Transfer Pricing Alert

Global Transfer Pricing 7 June 2018 Irish Revenue release details on monitoring compliance with transfer pricing rules Global Transfer Pricing Alert 2018-017 The Irish Revenue on 28 May 2018 released a

Global Transfer Pricing 7 June 2018 Irish Revenue release details on monitoring compliance with transfer pricing rules Global Transfer Pricing Alert 2018-017 The Irish Revenue on 28 May 2018 released a

Korean Tax Update BEPS Implementation

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

Presentation for KGCCI Korean Tax Update BEPS Implementation May 2018 CONTENTS I. BEPS: Backgrounds What is BEPS? Backgrounds for OECD BEPS Project BEPS Action plans II. BEPS Implementation in Korea I.

OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting

17 September 2014 OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Action 13 On 16 September 2014, the Organization for Economic Co-operation and Development (

17 September 2014 OECD Publishes Guidance on Transfer Pricing Documentation and Country-by-Country Reporting Action 13 On 16 September 2014, the Organization for Economic Co-operation and Development (

Unlocking the potential of Finance for insurers

Unlocking the potential of Finance for insurers Contents 1 Executive summary 2 Increasing role of Finance 3 Setting a strategic vision 5 Developing a roadmap for change 6 Potential benefits of Finance

Unlocking the potential of Finance for insurers Contents 1 Executive summary 2 Increasing role of Finance 3 Setting a strategic vision 5 Developing a roadmap for change 6 Potential benefits of Finance

Value Chain Planning post BEPS

Value Chain Planning post BEPS Tax Executives Institute Houston Chapter TS1815 Transfer Pricing Planning after BEPS Thursday, May 10, 2018 Agenda 1 Defining a Supply Chain 3 2 Impact of Transfer Pricing

Value Chain Planning post BEPS Tax Executives Institute Houston Chapter TS1815 Transfer Pricing Planning after BEPS Thursday, May 10, 2018 Agenda 1 Defining a Supply Chain 3 2 Impact of Transfer Pricing

Deloitte Tax Max The 44 th Series #ReadyMalaysia2019: A refreshed landscape. Tuesday, 27 November 2018 l One World Hotel

Deloitte Tax Max The 44 th Series #ReadyMalaysia2019: A refreshed landscape Tuesday, 27 November 2018 l One World Hotel Navigating the transfer pricing and international tax landscape confidently Theresa

Deloitte Tax Max The 44 th Series #ReadyMalaysia2019: A refreshed landscape Tuesday, 27 November 2018 l One World Hotel Navigating the transfer pricing and international tax landscape confidently Theresa

Luxembourg transfer pricing legislation at a glance

2017 EY TAX Alert Luxembourg Luxembourg transfer pricing legislation at a glance Executive summary The law of 23 December 2016 on the budget for the year 2017 ( Budget Law ) has introduced a new article

2017 EY TAX Alert Luxembourg Luxembourg transfer pricing legislation at a glance Executive summary The law of 23 December 2016 on the budget for the year 2017 ( Budget Law ) has introduced a new article

Analysing BEPS Impact Private Equity sector

Analysing BEPS Impact Private Equity sector January 2016 Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure In this age of increasing focus on bottomlines, it is indeed tempting for

Analysing BEPS Impact Private Equity sector January 2016 Second line optional lorem ipsum B Subhead lorem ipsum, date quatueriure In this age of increasing focus on bottomlines, it is indeed tempting for

Revenue Recognition: A Comprehensive Update on the Joint Project

The Dbriefs Financial Reporting series presents: Revenue Recognition: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Mark Crowley, Deloitte & Touche LLP Bryan Anderson, Deloitte

The Dbriefs Financial Reporting series presents: Revenue Recognition: A Comprehensive Update on the Joint Project Bob Uhl, Deloitte & Touche LLP Mark Crowley, Deloitte & Touche LLP Bryan Anderson, Deloitte

OECD TP Guidelines July 2017 Brief synopsis

OECD TP Guidelines July 2017 Brief synopsis Introduction to the OECD TP Guidelines Snapshot OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations Commonly referred to as

OECD TP Guidelines July 2017 Brief synopsis Introduction to the OECD TP Guidelines Snapshot OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations Commonly referred to as

Taxing and Pricing of Intangibles. Alan Ross

SMU-TA Centre for Excellence in Taxation Inaugural Conference 2015 Taxing and Pricing of Intangibles Alan Ross 17 September 2015 2 Outline of Discussion Areas Today Address the various BEPS documents impacting

SMU-TA Centre for Excellence in Taxation Inaugural Conference 2015 Taxing and Pricing of Intangibles Alan Ross 17 September 2015 2 Outline of Discussion Areas Today Address the various BEPS documents impacting

Global FS view on BEPS latest developments for asset managers. Event Date: Thursday 22 October Event Time: 9am EDT/3pm CET

Global FS view on BEPS latest developments for asset managers Event Date: Thursday 22 October Event Time: 9am EDT/3pm CET Notice The following information is not intended to be written advice concerning

Global FS view on BEPS latest developments for asset managers Event Date: Thursday 22 October Event Time: 9am EDT/3pm CET Notice The following information is not intended to be written advice concerning

Transfer Pricing newsletter

Southeast Asia Transfer Pricing updates October 27 Transfer Pricing newsletter Southeast Asia Transfer Pricing Center Introduction The legal landscape within Southeast Asia is constantly evolving, with

Southeast Asia Transfer Pricing updates October 27 Transfer Pricing newsletter Southeast Asia Transfer Pricing Center Introduction The legal landscape within Southeast Asia is constantly evolving, with

Financing for Energy & Sustainability

Financing for Energy & Sustainability Understanding the CFO and Translating Metrics This resource was completed with support from the Department of Energy s Office of Energy Efficiency and Renewable Energy

Financing for Energy & Sustainability Understanding the CFO and Translating Metrics This resource was completed with support from the Department of Energy s Office of Energy Efficiency and Renewable Energy

Value chain perspectives and their increased importance under BEPS, tax policy and technological change

Value chain perspectives and their increased importance under BEPS, tax policy and technological change February 22, 2017 FOR DISCUSSION PURPOSES ONLY Disclaimer This material has been prepared for general

Value chain perspectives and their increased importance under BEPS, tax policy and technological change February 22, 2017 FOR DISCUSSION PURPOSES ONLY Disclaimer This material has been prepared for general

Transfer Pricing in India. Winner of India Tax Firm of the Year 2016 at the Asia Tax Awards

Transfer Pricing in India Coverage Evolving Transfer Pricing Regulations in India Legislation and Trends Critical issues in India Advance Pricing Agreements vis-à-vis Safe Harbour Provisions Secondary

Transfer Pricing in India Coverage Evolving Transfer Pricing Regulations in India Legislation and Trends Critical issues in India Advance Pricing Agreements vis-à-vis Safe Harbour Provisions Secondary

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS)

") Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

Overview of OECD Action Plan on Base Erosion and Profit Shifting (BEPS) Monia Naoum, IBFD Research Associate Emily Muyaa, IBFD Research Associate 18 June 2015 1 Introduction: Globalization and its impact

OECD White Paper on Transfer Pricing Documentation

OECD White Paper on Transfer Pricing Documentation October 1, 2013 Presented by Mark Schuette, Patrick McColgan, and Emily Sanborn Note: The opinions expressed in this submission are entirely those of

OECD White Paper on Transfer Pricing Documentation October 1, 2013 Presented by Mark Schuette, Patrick McColgan, and Emily Sanborn Note: The opinions expressed in this submission are entirely those of

OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS)

") 22 July 2013 OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS) Executive summary On 19 July 2013, the Organisation for Economic Cooperation and Development (OECD) issued its much-anticipated

22 July 2013 OECD issues Action Plan on Base Erosion and Profit Shifting (BEPS) Executive summary On 19 July 2013, the Organisation for Economic Cooperation and Development (OECD) issued its much-anticipated

Emerging trends in BEPS arena

For private circulation only October 2018 01 Emerging trends in BEPS arena Background OECD s BEPS Project was launched after one of the most severe financial and economic crisis period during 2008, with

For private circulation only October 2018 01 Emerging trends in BEPS arena Background OECD s BEPS Project was launched after one of the most severe financial and economic crisis period during 2008, with

Country-by-country reporting Adapting to a changing documentation regime

Country-by-country reporting Adapting to a changing documentation regime Setting the context The base erosion and profit shifting (BEPS) project of the Organisation for Economic Co-operation and Development

Country-by-country reporting Adapting to a changing documentation regime Setting the context The base erosion and profit shifting (BEPS) project of the Organisation for Economic Co-operation and Development