19 th XBRL International Conference

|

|

|

- Darcy Reynolds

- 6 years ago

- Views:

Transcription

1 IASC Foundation 19 th XBRL International Conference Reducing reporting burden with XBRL: a catalyst for better reporting 24 June 2009 IASC Foundation The views expressed in this presentation are those of the presenter, not necessarily those of the IASC Foundation or the IASB 2009 IASC Foundation 30 Cannon Street London EC4M 6XH UK

2 IASC Foundation IFRSs in XBRL for receivers: The value of IFRS reporting in XBRL for regulators, supervisors and stock exchanges IASC Foundation The views expressed in this presentation are those of the presenter, not necessarily those of the IASC Foundation or the IASB 2009 IASC Foundation 30 Cannon Street London EC4M 6XH UK

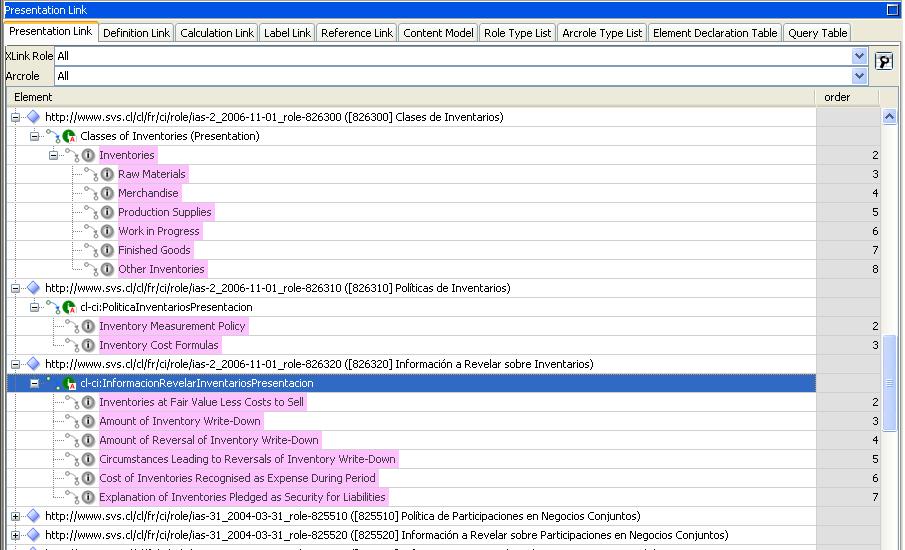

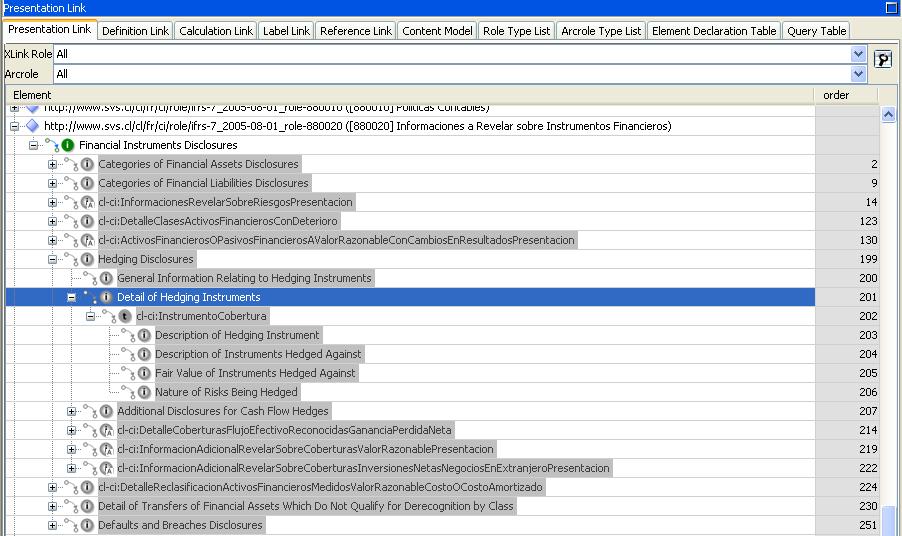

3 Track 7: XBRL and International Financial Reporting Standards SVS develop a taxonomy for listed corporations under IFRS - Chile, Ana Cristina Sepúlveda June 24, 2009

4 I. General Considerations II. Taxonomy Framework III. XBRL Technology Used IV. XBRL Implementation V. Assessment and Conclusions

5 This presentation will examine the project developed by the Superintendencia de Valores y Seguros (SVS) of Chile to present financial statements under IFRS The main task was to develop a taxonomy for listed corporations supervised by the SVS, extending it from the IFRS-GP 2006 taxonomy, which was available when this project started in January This month of June the taxonomy is being used for the first time. The Companies deadline to send their financial statements in XBRL is June 20th.

6 The SVS CL-CI XBRL Taxonomy represents the legal regulations (IFRSs and Chilean GAAP) applicable at the moment of the taxonomy release. SVS CL-CI XBRL Taxonomy is an extension of the IFRS-GP Taxonomy (version 2006). It consists of a single schema file that imports IFRS-GP elements and defines additional concepts.

7 I. General Considerations Local rules Chilean Laws Taxonomy IFRS-GP 2006 Information Model

8 Although the SVS CL-CI Taxonomy is an extension of the IFRS-GP Taxonomy (version 2006), its architecture is based on the IFRS 2008 Taxonomy. Additionally, the taxonomy has been modularized standard by standard and regulation by regulation based on the International Financial Reporting Standards and the Chilean GAAP. Each standard has been organized in components of the report (statements, notes and disclosures).

9 I. General Considerations

10 II. Taxonomy Framework At the moment of beginning the development of the SVS CL-CI XBRL Taxonomy, the IFRS-GP Taxonomy (version 2006) was the most recently available in a final version. The SVS CL-CI XBRL Taxonomy is an extension of the IFRS-GP Taxonomy (version 2006). It uses 2636 IFRS-GP concepts of which around 2490 are non-abstract items. It does not use the presentation and calculation relationship defined in the IFRS- GP. In total, the SVS CL-CI XBRL Taxonomy uses- in its relationships concepts of which around 3360 are nonabstract items

11 II. Taxonomy Framework The IFRS-GP element definition schema file (ifrs-gp xsd) is imported. This last one in turn imports the IFRS specific data type definition schema file (ifrs-gp-typ xsd). The basic IFRS-GP schema automatically incorporates the IFRS-GP English labels (ifrs-gp lab.xml) and the references to IFRS' bound volume (ifrs-gp ref.xml). Additionally, the official translation of the label linkbase to Spanish (ifrsgp lab-es.xml) is referred to and modified by adding contextual labels to a number of the IFRS-GP concepts (ifrs-gp lab-es_cl-ci_ xml) and correcting inadequate or wrong translations (ifrs-gp lab-es_patch_cl-ci_ xml). All IFRS-GP Taxonomy references has been prohibited in file ifrs-gp ref_remove_cl-ci_ xml due to application of standards based on IFRS bound volume 2008.

12 The SVS XBRL Taxonomy is built using hierarchies, intersection tables and tuples. It is important to indicate that the taxonomy does not use dimensions as a result of being an extension of IFRS-GP Taxonomy version 2006 which is also not dimensional in that sense. Hierarchical modeling applies to the majority of the taxonomy linkbases and presents tree-like structures of elements dependencies.

13 Example: Statement of financial position, current/non-current classification This is a tree-like structures of elements dependencies

14 Modeling of tabular information was conducted using intersection tables and tuples An Intersection table is a table, where reportable concepts are identified as intersections of headers of rows and headers of columns Tuples represent tables with unknown or unlimited number of rows (with known headers of columns) or columns (with known headers of rows)

15 III. XBRL Technology Used Statement of Changes in Equity

16

17 We prepared information about XBRL Project for the website and published Taxonomy. The companies can download Taxonomy from there, get documentation about XBRL and an example of financial statement prepared with the taxonomy We developed two tools to help Companies get to know and work with the Taxonomy. One is a Taxonomy Explorer: It is useful in reviewing the taxonomy Another is Module Manager: It generates a shell file containing the financial statements and notes which the company wants to submit

18 Our IT Department program online interactive form to enter the financial information and generate the XBRL file For the presentation of their financial statements, the companies can either use the interactive form developed by SVS to enter the information, or generate the XBRL file from their own systems The Companies can also submit the file for a validation process. Once validated, the final version of the file can be sent to SVS.

19 Supervised companies Our first experience with the system has yet to finish so we cannot draw definitive conclusions, however 33 out of 86 Companies have chosen to generate their own XBRL files. We acknowledge that we made a wrong decision regarding the online interactive form. We intended to offer a tool which would enable companies to enter the info and generate their XBRL files. For this, we had our IT Department program the forms. This proved to be a mistake, as we have had many problems with their performance. We should have purchased software that could read the taxonomy and automatically generate the form. Our biggest concern is that some Companies have attributed these form problems to the XBRL taxonomy, but the latter has not shown any problems to this date.

20 External Auditors and SVS Analysts We have had resistance to change inside the financial department. It has been hard for our analysts to accept this information model. They did not like the presentation for disclosures ordered by IAS or IFRS, for this was not the usual way they were presented in a real-life financial statement in Chile With the Information Model it becomes easier to prepare financial statements because it contains every disclosure required by the IFRS rules and there are clear references to where to go and what to do in case of doubt On the other side, it is more complex. We have gotten criticism in the sense that too much detail is asked for, considering that Chilean Companies many times don't have that information readily available

21 XBRL Knowledge The biggest amount of questions submitted by users have been about the context definition, understanding the concept of tuples and entering the info in the tuples. Conceptually it has been hard for the Companies to understand the function of the shell file, and the overall modularity of the taxonomy. Some thought that the instance to be sent should enclose the taxonomy itself. But each time that new software has been implemented it has been difficult. Startup is always hard. At the beginning there is lack of knowledge and resistance to change, but as people learn, they embrace the new standard. When we first started there were no experts in XBRL, but with the current demand to present financial statements many software companies have set to develop tools to make possible the generation of XBRL files from within the Companies' own systems. We have also seen auditing companies working towards technological solutions for their clients.

22 Overall Project Assessment Beyond the difficulties and the mistake made in the implementation, we are sure that XBRL is the technological solution for financial statement reporting. We were able to quickly detect inconsistencies in the submitted financial information due to the validation process implicit in the taxonomy We hope that with the companies increased familiarity to XBRL they will improve the quality of the information they prepare This learning process should also help the companies automate their systems and directly generate the XBRL files Among the companies supervised there are many matrices which have to consolidate with their subsidiaries, some who have to report to their parent abroad and others that have ADR in the United States. We hope they all perceive the benefits of XBRL in the presentation of their financial statements.

23 The management of change has not been easy but as a team we are proud to have made XBRL a reality in Chile The End

Streamlining IFRS reporting with XBRL Wednesday 28 October, Montreal

International Financial Reporting Standards Streamlining IFRS reporting with XBRL Wednesday 28 October, Montreal The views expressed in this presentation are those of the presenter, not necessarily those

International Financial Reporting Standards Streamlining IFRS reporting with XBRL Wednesday 28 October, Montreal The views expressed in this presentation are those of the presenter, not necessarily those

Proposed Interim Release Package 2 on the IFRS Taxonomy 2013

Deloitte Accountants B.V. Wilhelminakade 1 3072 AP Rotterdam P.O.Box 2031 3000 CA Rotterdam Netherlands Tel: +31 (0)88 288 2888 Fax: +31 (0)88 288 9830 www.deloitte.nl Ms Rita Ogun-Clijmans Product Manager

Deloitte Accountants B.V. Wilhelminakade 1 3072 AP Rotterdam P.O.Box 2031 3000 CA Rotterdam Netherlands Tel: +31 (0)88 288 2888 Fax: +31 (0)88 288 9830 www.deloitte.nl Ms Rita Ogun-Clijmans Product Manager

XBRL activities at IASB Jornadas Latinoamericanas de

September 2013 International Financial Reporting Standards XBRL activities at IASB Jornadas Latinoamericanas de Capacitación IFRS y XBRL 5-6 September 2013 Amaro Luiz de Oliveira Gomes - Member of the

September 2013 International Financial Reporting Standards XBRL activities at IASB Jornadas Latinoamericanas de Capacitación IFRS y XBRL 5-6 September 2013 Amaro Luiz de Oliveira Gomes - Member of the

Accounting Standards the International Setting

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

IFRS 9 Financial Instruments

November 2009 Project Summary and Feedback Statement IFRS 9 Financial Instruments Part 1: Classification and measurement Planned reform of financial instruments accounting 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2 Q3

November 2009 Project Summary and Feedback Statement IFRS 9 Financial Instruments Part 1: Classification and measurement Planned reform of financial instruments accounting 2009 2010 Q1 Q2 Q3 Q4 Q1 Q2 Q3

XBRL US Corporate Actions Taxonomy 2012 Scope

Corporate Actions Taxonomy XBRL US Corporate Actions Taxonomy 2012 Scope Version 1.1 March 31, 2012 Prepared by: Phillip Engel Chief Data Architect XBRL US, Inc. Campbell Pryde Chief Executive Officer

Corporate Actions Taxonomy XBRL US Corporate Actions Taxonomy 2012 Scope Version 1.1 March 31, 2012 Prepared by: Phillip Engel Chief Data Architect XBRL US, Inc. Campbell Pryde Chief Executive Officer

Snapshot: Financial Instruments: Amortised Cost and Impairment

November 2009 Exposure Draft Snapshot: Financial Instruments: Amortised Cost and Impairment This snapshot is a brief introduction to a proposed IFRS on amortised cost and the impairment of financial assets.

November 2009 Exposure Draft Snapshot: Financial Instruments: Amortised Cost and Impairment This snapshot is a brief introduction to a proposed IFRS on amortised cost and the impairment of financial assets.

Accounting Standards the International Setting

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards Accounting Standards the International Setting Sir David Tweedie IASB Chairman The views expressed in this presentation are those of the presenter, not necessarily

INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF PRESENTATION OF ITEMS OF OTHER COMPREHENSIVE INCOME (PROPOSED AMENDMENTS TO IAS 1)

") 2 June 2010 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF PRESENTATION OF ITEMS OF OTHER COMPREHENSIVE INCOME (PROPOSED AMENDMENTS

2 June 2010 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IASB EXPOSURE DRAFT OF PRESENTATION OF ITEMS OF OTHER COMPREHENSIVE INCOME (PROPOSED AMENDMENTS

March Basis for Conclusions Exposure Draft ED/2009/2. Income Tax. Comments to be received by 31 July 2009

March 2009 Basis for Conclusions Exposure Draft ED/2009/2 Income Tax Comments to be received by 31 July 2009 Basis for Conclusions on Exposure Draft INCOME TAX Comments to be received by 31 July 2009 ED/2009/2

March 2009 Basis for Conclusions Exposure Draft ED/2009/2 Income Tax Comments to be received by 31 July 2009 Basis for Conclusions on Exposure Draft INCOME TAX Comments to be received by 31 July 2009 ED/2009/2

XBRL at the Federal Public Services Finance, Belgium Caroline Dupae, Project lead

18 th International XBRL Conference XBRL at the Federal Public Services Finance, Belgium Caroline Dupae, Project lead Kurt Cogghe, Deloitte Consulting Location/Filename/Unit/Aut thor/assistant (Change

18 th International XBRL Conference XBRL at the Federal Public Services Finance, Belgium Caroline Dupae, Project lead Kurt Cogghe, Deloitte Consulting Location/Filename/Unit/Aut thor/assistant (Change

TransCanada In business to deliver

w - 1 6 3 0-1 0 0 * LETTER OF COMMENT NO. TransCanada In business to deliver April 14, 2009 Technical Director International Accounting Standards Board 30 Cannon Street London EC4M 6XH TransCanada Pipelines

w - 1 6 3 0-1 0 0 * LETTER OF COMMENT NO. TransCanada In business to deliver April 14, 2009 Technical Director International Accounting Standards Board 30 Cannon Street London EC4M 6XH TransCanada Pipelines

International Financial Reporting Standard. Small and Medium-sized Entities

A Staff Overview This overview of the IASB s exposure draft of a proposed International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) was prepared by Paul Pacter, IASB

A Staff Overview This overview of the IASB s exposure draft of a proposed International Financial Reporting Standard for Small and Medium-sized Entities (IFRS for SMEs) was prepared by Paul Pacter, IASB

IFRS and Taiwan The Move to Global Accounting Standards

International Financial Reporting Standards IFRS and Taiwan The Move to Global Accounting Standards Sir David Tweedie The views expressed in this presentation are those of the presenter, not necessarily

International Financial Reporting Standards IFRS and Taiwan The Move to Global Accounting Standards Sir David Tweedie The views expressed in this presentation are those of the presenter, not necessarily

COMPARING EXPERIENCES OF IFRS/XBRL IMPLEMENTATION FOR FINANCIAL SUPERVISION IN LATIN AMERICA.

COMPARING EXPERIENCES OF IFRS/XBRL IMPLEMENTATION FOR FINANCIAL SUPERVISION IN LATIN AMERICA. MILENA CASTILLO EX D I R E C T O R F O R S U P E R V I S I O N, F I D U C I A R Y I N D U S T R Y Methodology:

COMPARING EXPERIENCES OF IFRS/XBRL IMPLEMENTATION FOR FINANCIAL SUPERVISION IN LATIN AMERICA. MILENA CASTILLO EX D I R E C T O R F O R S U P E R V I S I O N, F I D U C I A R Y I N D U S T R Y Methodology:

Reporting the Financial Effects of Rate Regulation

September 2014 Discussion Paper DP/2014/2 Reporting the Financial Effects of Rate Regulation Comments to be received by 15 January 2015 Reporting the Financial Effects of Rate Regulation Comments to be

September 2014 Discussion Paper DP/2014/2 Reporting the Financial Effects of Rate Regulation Comments to be received by 15 January 2015 Reporting the Financial Effects of Rate Regulation Comments to be

Version 1.0 November 30, Campbell Pryde Chief Standards Officer XBRL US, Inc.

XBRL US Schedule of Investments Taxonomy 2008 Architecture Version 1.0 November 30, 2008 Prepared by: Phillip Engel Director Goffengel Consulting Campbell Pryde Chief Standards Officer XBRL US, Inc. i

XBRL US Schedule of Investments Taxonomy 2008 Architecture Version 1.0 November 30, 2008 Prepared by: Phillip Engel Director Goffengel Consulting Campbell Pryde Chief Standards Officer XBRL US, Inc. i

IFRIC DRAFT INTERPRETATION D8

IFRIC International Financial Reporting Interpretations Committee IFRIC DRAFT INTERPRETATION D8 Members Shares in Co-operative Entities Comments to be received by 13 September 2004 IFRIC Draft Interpretation

IFRIC International Financial Reporting Interpretations Committee IFRIC DRAFT INTERPRETATION D8 Members Shares in Co-operative Entities Comments to be received by 13 September 2004 IFRIC Draft Interpretation

Snapshot: Disclosure Initiative Principles of Disclosure

March 2017 Discussion Paper Snapshot: Disclosure Initiative Principles of Disclosure This Snapshot provides an overview of the Discussion Paper Disclosure Initiative Principles of Disclosure published

March 2017 Discussion Paper Snapshot: Disclosure Initiative Principles of Disclosure This Snapshot provides an overview of the Discussion Paper Disclosure Initiative Principles of Disclosure published

December 10, International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom

December 10, 2012 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: IFRS for SMEs Comprehensive Review - Request for Information Dear Board Members, The Group

December 10, 2012 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: IFRS for SMEs Comprehensive Review - Request for Information Dear Board Members, The Group

The IFRS Taxonomy. Today and tomorrow. International Financial Reporting Standards. Il Seminario Central de Balances y XBRL - 22 June 2011

International Financial Reporting Standards The IFRS Taxonomy Today and tomorrow Il Seminario Central de Balances y XBRL - 22 June 2011 Olivier Servais Director, XBRL Activities The views expressed in

International Financial Reporting Standards The IFRS Taxonomy Today and tomorrow Il Seminario Central de Balances y XBRL - 22 June 2011 Olivier Servais Director, XBRL Activities The views expressed in

Belgian Primary Financial Statement Commercial and Industrial Taxonomy Release Date: Release Type: Final version Taxonomy Documentation

Belgian Primary Financial Statement Commercial and Industrial Taxonomy Release Date: 2015-04-01 Release Type: Final version Taxonomy Documentation Summary Taxonomy Information: Status: Final version. Issued:

Belgian Primary Financial Statement Commercial and Industrial Taxonomy Release Date: 2015-04-01 Release Type: Final version Taxonomy Documentation Summary Taxonomy Information: Status: Final version. Issued:

SEC Proposes New Rules Mandating XBRL-Format Filings. by Joseph D. Kline, Elaine Wolff and William L. Tolbert, Jr.

Corporate SEC Client Alert May 22, 2008 SEC Proposes New Rules Mandating XBRL-Format Filings by Joseph D. Kline, Elaine Wolff and William L. Tolbert, Jr. On May 14, 2008, the Securities and Exchange Commission

Corporate SEC Client Alert May 22, 2008 SEC Proposes New Rules Mandating XBRL-Format Filings by Joseph D. Kline, Elaine Wolff and William L. Tolbert, Jr. On May 14, 2008, the Securities and Exchange Commission

XBRL US Schedule of Investments Taxonomy v2008. Campbell Pryde Chief Standards Officer XBRL US, Inc.

XBRL US Schedule of Investments Taxonomy v2008 Preparers Guide Version 1.0 November 30, 2008 Prepared by: Phillip Engel Goeffengel Consulting Campbell Pryde Chief Standards Officer XBRL US, Inc. i Notice

XBRL US Schedule of Investments Taxonomy v2008 Preparers Guide Version 1.0 November 30, 2008 Prepared by: Phillip Engel Goeffengel Consulting Campbell Pryde Chief Standards Officer XBRL US, Inc. i Notice

International Financial Reporting Standards

International Financial Reporting Standards as issued at 1 January 2009 The consolidated text of International Financial Reporting Standards (IFRSs ) including International Accounting Standards (IASs

International Financial Reporting Standards as issued at 1 January 2009 The consolidated text of International Financial Reporting Standards (IFRSs ) including International Accounting Standards (IASs

Summary of the IFRS Taxonomy Consultative Group discussions

ITCG Meeting June 2017 Summary of the IFRS Taxonomy Consultative Group discussions The IFRS Taxonomy Consultative Group (ITCG) held a face-to-face meeting on 12 June 2017. The meeting took place in the

ITCG Meeting June 2017 Summary of the IFRS Taxonomy Consultative Group discussions The IFRS Taxonomy Consultative Group (ITCG) held a face-to-face meeting on 12 June 2017. The meeting took place in the

International Financial Reporting Interpretations Committee IFRIC DRAFT INTERPRETATION D9

IFRIC International Financial Reporting Interpretations Committee IFRIC DRAFT INTERPRETATION D9 Employee Benefit Plans with a Promised Return on Contributions or Notional Contributions Comments to be received

IFRIC International Financial Reporting Interpretations Committee IFRIC DRAFT INTERPRETATION D9 Employee Benefit Plans with a Promised Return on Contributions or Notional Contributions Comments to be received

IFRS for SMEs scope and concepts

28 April 2010 International Financial Reporting Standards IFRS for SMEs scope and concepts World Bank GDLN Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this

28 April 2010 International Financial Reporting Standards IFRS for SMEs scope and concepts World Bank GDLN Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this

March Income Tax. Comments to be received by 31 July 2009

March 2009 Exposure Draft ED/2009/2 Income Tax Comments to be received by 31 July 2009 Exposure Draft INCOME TAX Comments to be received by 31 July 2009 ED/2009/2 This exposure draft Income Tax is published

March 2009 Exposure Draft ED/2009/2 Income Tax Comments to be received by 31 July 2009 Exposure Draft INCOME TAX Comments to be received by 31 July 2009 ED/2009/2 This exposure draft Income Tax is published

Business combinations (phase I)

") September 2004 The International Accounting Standards Board met in London on 21-24 September 2004, when it discussed: Business combinations Exploration for and evaluation of mineral resources Financial

September 2004 The International Accounting Standards Board met in London on 21-24 September 2004, when it discussed: Business combinations Exploration for and evaluation of mineral resources Financial

Revenue from Contracts with Customers

June 2010 Basis for Conclusions Exposure Draft ED/2010/6 Revenue from Contracts with Customers Comments to be received by 22 October 2010 Basis for Conclusions on Exposure Draft REVENUE FROM CONTRACTS

June 2010 Basis for Conclusions Exposure Draft ED/2010/6 Revenue from Contracts with Customers Comments to be received by 22 October 2010 Basis for Conclusions on Exposure Draft REVENUE FROM CONTRACTS

International Financial Reporting Standards

May 2011 International Financial Reporting Standards International Financial Reporting Standards Michael Wells, Director, Education Initiative, IFRS Foundation IFRS Foundation The views expressed in this

May 2011 International Financial Reporting Standards International Financial Reporting Standards Michael Wells, Director, Education Initiative, IFRS Foundation IFRS Foundation The views expressed in this

Anheuser-Busch InBev SA/NV

(Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F/A (Amendment No. 1) REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF

(Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 20-F/A (Amendment No. 1) REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF

November Proposed IFRS Taxonomy Update Taxonomy/2017/3. IFRS Taxonomy Annual Improvements. Comments to be received by 29 January 2018

November 2017 Proposed IFRS Taxonomy Update Taxonomy/2017/3 IFRS Taxonomy 2017 Annual Improvements Comments to be received by 29 January 2018 Proposed IFRS Taxonomy Update IFRS Taxonomy 2017 Annual improvements

November 2017 Proposed IFRS Taxonomy Update Taxonomy/2017/3 IFRS Taxonomy 2017 Annual Improvements Comments to be received by 29 January 2018 Proposed IFRS Taxonomy Update IFRS Taxonomy 2017 Annual improvements

Amendments to International Accounting Standard 39 Financial Instruments: Recognition and Measurement The Fair Value Option

Amendments to International Accounting Standard 39 Financial Instruments: Recognition and Measurement The Fair Value Option These Amendments to IAS 39 Financial Instruments: Recognition and Measurement

Amendments to International Accounting Standard 39 Financial Instruments: Recognition and Measurement The Fair Value Option These Amendments to IAS 39 Financial Instruments: Recognition and Measurement

IFRS Taxonomy January Proposed Interim Release XBRL/2014/1. IFRS 9 Financial Instruments (Hedge Accounting)

") January 2014 Proposed Interim Release XBRL/2014/1 IFRS Taxonomy 2013 IFRS 9 Financial Instruments (Hedge Accounting) Comments to be received by 14 February 2014 Proposed Interim Release IFRS Taxonomy 2013

January 2014 Proposed Interim Release XBRL/2014/1 IFRS Taxonomy 2013 IFRS 9 Financial Instruments (Hedge Accounting) Comments to be received by 14 February 2014 Proposed Interim Release IFRS Taxonomy 2013

March IFRS Taxonomy Update. IFRS Taxonomy Annual Improvements

March 2018 IFRS Taxonomy Update IFRS Taxonomy 2017 Annual Improvements IFRS Taxonomy Update IFRS Taxonomy 2017 Annual Improvements IFRS Taxonomy 2017 Annual Improvements is published by the IFRS Foundation

March 2018 IFRS Taxonomy Update IFRS Taxonomy 2017 Annual Improvements IFRS Taxonomy Update IFRS Taxonomy 2017 Annual Improvements IFRS Taxonomy 2017 Annual Improvements is published by the IFRS Foundation

Resolution of Comments

XBRL US Mutual Fund Risk/Return Summary Taxonomy v2008 Resolution of Comments Version 1.0 December 31, 2008 i of ii Table of Contents Public Comment: Future Years for Bar Chart Annual Return Tags... 1

XBRL US Mutual Fund Risk/Return Summary Taxonomy v2008 Resolution of Comments Version 1.0 December 31, 2008 i of ii Table of Contents Public Comment: Future Years for Bar Chart Annual Return Tags... 1

Discussion Paper DP/2014/2 Reporting the Financial Effects of Rate Regulation

International Accounting Standards Board 30 Cannon Street London - United Kingdom EC4M 6XH Nossa Referência: CR-00113/2015 Data: 14/01/2015 Sua Referência: - Assunto: Discussion Paper DP/2014/2 Reporting

International Accounting Standards Board 30 Cannon Street London - United Kingdom EC4M 6XH Nossa Referência: CR-00113/2015 Data: 14/01/2015 Sua Referência: - Assunto: Discussion Paper DP/2014/2 Reporting

December 10, International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom

December 10, 2012 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: IFRS for SMEs Comprehensive Review - Request for Information Dear Board Members, We are sending

December 10, 2012 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: IFRS for SMEs Comprehensive Review - Request for Information Dear Board Members, We are sending

IFRS and the Financial Crisis: The end of a chapter

IFRS and the Financial Crisis: The end of a chapter Amaro Gomes Board Member International Accounting Standards Board (IASB) The views expressed in this presentation are those of the presenter, not necessarily

IFRS and the Financial Crisis: The end of a chapter Amaro Gomes Board Member International Accounting Standards Board (IASB) The views expressed in this presentation are those of the presenter, not necessarily

New items for initial consideration IAS 12 Income Taxes Recognition of deferred taxes when acquiring a single-asset entity

STAFF PAPER IFRS Interpretations Committee Meeting September 2016 Project Paper topic New items for initial consideration IAS 12 Income Taxes Recognition of deferred taxes when acquiring a single-asset

STAFF PAPER IFRS Interpretations Committee Meeting September 2016 Project Paper topic New items for initial consideration IAS 12 Income Taxes Recognition of deferred taxes when acquiring a single-asset

Our detailed comments and responses to the questions in the Exposure Draft are set out in the Appendix. To summarise EFRAG:

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom 11 May 2015 Dear Sir/Madam, Re: Exposure Draft Disclosure Initiative (Proposed amendments to IAS 7) On behalf of

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom 11 May 2015 Dear Sir/Madam, Re: Exposure Draft Disclosure Initiative (Proposed amendments to IAS 7) On behalf of

Globalization of Accounting Standards & China s Role in It. Content

International Financial Reporting Standards Globalization of Accounting Standards & China s Role in It March 10, 2014 London School of Economics Wei-Guo Zhang, IASB Member The views expressed in this presentation

International Financial Reporting Standards Globalization of Accounting Standards & China s Role in It March 10, 2014 London School of Economics Wei-Guo Zhang, IASB Member The views expressed in this presentation

IFRS Update. International Financial Reporting Standards. OECD Accrual Accounting Symposium 7 March March 2013

4 March 2013 International Financial Reporting Standards IFRS Update OECD Accrual Accounting Symposium 7 March 2013 The views expressed in this presentation are those of the presenter, not necessarily

4 March 2013 International Financial Reporting Standards IFRS Update OECD Accrual Accounting Symposium 7 March 2013 The views expressed in this presentation are those of the presenter, not necessarily

IFRS for SMEs IFRS Foundation-World Bank

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

International Financial Reporting Standards (IFRSs)

") May 2010 International Financial Reporting Standards International Financial Reporting Standards (IFRSs) Gilbert Gélard, IASB member The views expressed in this presentation are those of the presenters,

May 2010 International Financial Reporting Standards International Financial Reporting Standards (IFRSs) Gilbert Gélard, IASB member The views expressed in this presentation are those of the presenters,

The Life Insurance Association of Japan

June 11, 2002 Sir David Tweedie Chair International Accounting Standards Board 30 Cannon Street, London EC4M 6XH, United Kingdom Dear Sir David: This letter is submitted on behalf of the American Council

June 11, 2002 Sir David Tweedie Chair International Accounting Standards Board 30 Cannon Street, London EC4M 6XH, United Kingdom Dear Sir David: This letter is submitted on behalf of the American Council

IASB Update: prospects and challenges

10 November 2008 International Financial Reporting Standards IASB Update: prospects and challenges IASB@AFRAC 2008 Philippe Danjou, IASB member The views expressed in this presentation are those of the

10 November 2008 International Financial Reporting Standards IASB Update: prospects and challenges IASB@AFRAC 2008 Philippe Danjou, IASB member The views expressed in this presentation are those of the

May Proposed IFRS Taxonomy Update Taxonomy/2017/1. IFRS Taxonomy IFRS 17 Insurance Contracts. Comments to be received by 18 September 2017

May 2017 Proposed IFRS Taxonomy Update Taxonomy/2017/1 IFRS Taxonomy 2017 IFRS 17 Insurance Contracts Comments to be received by 18 September 2017 Proposed IFRS Taxonomy Update IFRS Taxonomy 2017 IFRS

May 2017 Proposed IFRS Taxonomy Update Taxonomy/2017/1 IFRS Taxonomy 2017 IFRS 17 Insurance Contracts Comments to be received by 18 September 2017 Proposed IFRS Taxonomy Update IFRS Taxonomy 2017 IFRS

International Accounting Standards Board Press Release

International Accounting Standards Board Press Release For immediate release 31 March 2004 INTERNATIONAL ACCOUNTING STANDARDS BOARD FINALISES MACRO HEDGING AMENDMENTS TO IAS 39 The International Accounting

International Accounting Standards Board Press Release For immediate release 31 March 2004 INTERNATIONAL ACCOUNTING STANDARDS BOARD FINALISES MACRO HEDGING AMENDMENTS TO IAS 39 The International Accounting

Business Combinations II

April 2006 IASB Update is published as a convenience to the Board's constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

April 2006 IASB Update is published as a convenience to the Board's constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

Article from The Modeling Platform. November 2017 Issue 6

Article from The Modeling Platform November 2017 Issue 6 Actuarial Model Component Design By William Cember and Jeffrey Yoon As managers of risk, most actuaries are tasked with answering questions about

Article from The Modeling Platform November 2017 Issue 6 Actuarial Model Component Design By William Cember and Jeffrey Yoon As managers of risk, most actuaries are tasked with answering questions about

Request for Information: Comprehensive Review of IFRS for SMEs

30 November 2012 Level 7, 600 Bourke Street MELBOURNE VIC 3000 Postal Address PO Box 204 Collins Street West VIC 8007 Telephone: (03) 9617 7600 Facsimile: (03) 9617 7608 Mr Hans Hoogervorst Chairman International

30 November 2012 Level 7, 600 Bourke Street MELBOURNE VIC 3000 Postal Address PO Box 204 Collins Street West VIC 8007 Telephone: (03) 9617 7600 Facsimile: (03) 9617 7608 Mr Hans Hoogervorst Chairman International

Michael Ohata Managing Director - KPMG. Landon Westerlund Audit Partner - Financial Services -KPMG

Preparers Track Integrating XBRL into your reporting process Michael Ohata Managing Director - KPMG Landon Westerlund Audit Partner - Financial Services -KPMG Michael Schlanger VP, Development & Strategy

Preparers Track Integrating XBRL into your reporting process Michael Ohata Managing Director - KPMG Landon Westerlund Audit Partner - Financial Services -KPMG Michael Schlanger VP, Development & Strategy

Date issued: (15 January 2004) International Accounting Standards Committee Foundation (IASC Foundation) and XBRL International

International Accounting Standards Committee Foundation (IASC Foundation) and XBRL International") Financial Statements of all Profit Oriented Entities (GP), 2004-01-15 International Financial Reporting Standards (IFRS), General Purpose Financial Reporting of all Profit-Oriented Entities (GP), 2004-01-15,

Financial Statements of all Profit Oriented Entities (GP), 2004-01-15 International Financial Reporting Standards (IFRS), General Purpose Financial Reporting of all Profit-Oriented Entities (GP), 2004-01-15,

Business Combinations II

October 2006 IASB Update is published as a convenience for the Board's constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

October 2006 IASB Update is published as a convenience for the Board's constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

Discussion Paper: Preliminary Views on Financial Statement Presentation

1 6 3 0-1 0 O * International Accounting Standards Board 30 Cannon St London EC4M 6XH LETTER OF COMMENT NO. \ Z> O G Chapter Street, London, SW1P4NP Tel: 020 7663 5441 Fax: 020 8849 2468 www.cimaalobal.com

1 6 3 0-1 0 O * International Accounting Standards Board 30 Cannon St London EC4M 6XH LETTER OF COMMENT NO. \ Z> O G Chapter Street, London, SW1P4NP Tel: 020 7663 5441 Fax: 020 8849 2468 www.cimaalobal.com

FINANCIAL REPORT FILING REQUIREMENTS AROUND THE WORLD PROFILE: Australia

FINANCIAL REPORT FILING REQUIREMENTS AROUND THE WORLD PROFILE: Australia Disclaimer: The information in this profile is for general guidance only and may change from time to time. You should not act on

FINANCIAL REPORT FILING REQUIREMENTS AROUND THE WORLD PROFILE: Australia Disclaimer: The information in this profile is for general guidance only and may change from time to time. You should not act on

IFRS for SMEs. World Bank, Chisinau. International Financial Reporting Standards. Michael Wells, Director of IFRS Education Initiative IASC Foundation

27 May 2010 International Financial Reporting Standards IFRS for SMEs World Bank, Chisinau Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this presentation

27 May 2010 International Financial Reporting Standards IFRS for SMEs World Bank, Chisinau Michael Wells, Director of IFRS Education Initiative IASC Foundation The views expressed in this presentation

The Proposed IFRS for SMEs: Benefits for Honduras. World Bank Conference on Promoting Business Development in Honduras 12 February 2008

The Proposed IFRS for SMEs: Benefits for Honduras Paul Pacter IASB Director of Standards for Small and Medium-sized Entities World Bank Conference on Promoting Business Development in Honduras 12 February

The Proposed IFRS for SMEs: Benefits for Honduras Paul Pacter IASB Director of Standards for Small and Medium-sized Entities World Bank Conference on Promoting Business Development in Honduras 12 February

Trustees enhance public accountability through new Monitoring Board, complete first part of Constitution Review

IASC Foundation Press Release 29 January 2009 Trustees enhance public accountability through new Monitoring Board, complete first part of Constitution Review The Trustees of the IASC Foundation, the oversight

IASC Foundation Press Release 29 January 2009 Trustees enhance public accountability through new Monitoring Board, complete first part of Constitution Review The Trustees of the IASC Foundation, the oversight

ED 8 Operating Segments

January 2006 Implementation Guidance ED8 DRAFT IMPLEMENTATION GUIDANCE ED 8 Operating Segments Comments to be received by 19 May 2006 International Accounting Standards Board Draft Implementation Guidance

January 2006 Implementation Guidance ED8 DRAFT IMPLEMENTATION GUIDANCE ED 8 Operating Segments Comments to be received by 19 May 2006 International Accounting Standards Board Draft Implementation Guidance

Deutsches Rechnungslegungs Standards Committee e.v. Accounting Standards Committee of Germany

e. V. Zimmerstr. 30 10969 Berlin Mr Hans Hoogervorst Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom IFRS Technical Committee Telefon: +49 (0)30

e. V. Zimmerstr. 30 10969 Berlin Mr Hans Hoogervorst Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom IFRS Technical Committee Telefon: +49 (0)30

8 June Re: FEE Comments on IASB/FASB Phase B Discussion Paper Preliminary Views on Financial Statement Presentation

8 June 2009 Sir David Tweedie Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom E-mail: commentletters@iasb.org Ref.: ACC/HvD/LF/SR Dear Sir David, Re: FEE

8 June 2009 Sir David Tweedie Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom E-mail: commentletters@iasb.org Ref.: ACC/HvD/LF/SR Dear Sir David, Re: FEE

IFRS Foundation: Training Material for the IFRS for SMEs. Module 1 Small and Medium-sized Entities

2009 IFRS Foundation: Training Material for the IFRS for SMEs Module 1 Small and Medium-sized Entities IFRS Foundation: Training Material for the IFRS for SMEs including the full text of Section 1 Small

2009 IFRS Foundation: Training Material for the IFRS for SMEs Module 1 Small and Medium-sized Entities IFRS Foundation: Training Material for the IFRS for SMEs including the full text of Section 1 Small

New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1)

") New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1) Issued November 2007 and incorporates amendments to 31 December 2016 other than consequential

New Zealand Equivalent to International Accounting Standard 1 Presentation of Financial Statements (NZ IAS 1) Issued November 2007 and incorporates amendments to 31 December 2016 other than consequential

We commend the IASB for its efforts to address standards implementation issues.

277 Wellington Street West, Toronto, ON Canada M5V 3H2 Tel: (416) 977-3322 Fax: (416) 204-3412 www.frascanada.ca 277 rue Wellington Ouest, Toronto (ON) Canada M5V 3H2 Tél: (416) 977-3322 Téléc : (416)

277 Wellington Street West, Toronto, ON Canada M5V 3H2 Tel: (416) 977-3322 Fax: (416) 204-3412 www.frascanada.ca 277 rue Wellington Ouest, Toronto (ON) Canada M5V 3H2 Tél: (416) 977-3322 Téléc : (416)

USING XBRL FOR LOCAL GOVERNMENT BUDGET REPORTING IN SPAIN

15th International XBRL Conference USING XBRL FOR LOCAL GOVERNMENT BUDGET REPORTING IN SPAIN Juan Zapardiel Carlos Palomino Ministry of Economy and Finance. Spain Munich, Germany. June 2007 THE SPANISH

15th International XBRL Conference USING XBRL FOR LOCAL GOVERNMENT BUDGET REPORTING IN SPAIN Juan Zapardiel Carlos Palomino Ministry of Economy and Finance. Spain Munich, Germany. June 2007 THE SPANISH

ED/2013/7 Exposure Draft: Insurance Contracts

Ian Laughlin Deputy Chairman 31 October 2013 Mr. Hans Hoogervorst Chairman IFRS Foundation 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr. Hoogervorst, ED/2013/7 Exposure Draft: Insurance Contracts

Ian Laughlin Deputy Chairman 31 October 2013 Mr. Hans Hoogervorst Chairman IFRS Foundation 30 Cannon Street London EC4M 6XH United Kingdom Dear Mr. Hoogervorst, ED/2013/7 Exposure Draft: Insurance Contracts

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH. Submitted electronically to

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH Submitted electronically to www.ifrs.org 5 th November 2013 Dear Mr Hoogervorst EFFECTIVE DATE OF

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London EC4M 6XH Submitted electronically to www.ifrs.org 5 th November 2013 Dear Mr Hoogervorst EFFECTIVE DATE OF

IASC Foundation: Training Material for the IFRS for SMEs. Module 4 Statement of Financial Position

2009 IASC Foundation: Training Material for the IFRS for SMEs Module 4 Statement of Financial Position IASC Foundation: Training Material for the IFRS for SMEs including the full text of Section 4 Statement

2009 IASC Foundation: Training Material for the IFRS for SMEs Module 4 Statement of Financial Position IASC Foundation: Training Material for the IFRS for SMEs including the full text of Section 4 Statement

Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011

1 November 2010 Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011 Online filing requirement Online filing to HMRC will be mandatory for all UK companies from 1 April 2011.

1 November 2010 Online filing of Corporation Tax returns with statutory accounts in XBRL from 2011 Online filing requirement Online filing to HMRC will be mandatory for all UK companies from 1 April 2011.

Discontinued Operations

September 2008 EXPOSURE DRAFT Discontinued Operations Proposed amendments to IFRS 5 Comments to be received by 23 January 2009 Exposure Draft DISCONTINUED OPERATIONS (PROPOSED AMENDMENTS TO IFRS 5) Comments

September 2008 EXPOSURE DRAFT Discontinued Operations Proposed amendments to IFRS 5 Comments to be received by 23 January 2009 Exposure Draft DISCONTINUED OPERATIONS (PROPOSED AMENDMENTS TO IFRS 5) Comments

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR)

") Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 32nd SESSION 4-6 November 2015 Room XVIII, Palais des Nations, Geneva Wednesday, 4 November 2015

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 32nd SESSION 4-6 November 2015 Room XVIII, Palais des Nations, Geneva Wednesday, 4 November 2015

Eurofiling Data modelling and ExcelXBRLGen (Excel Add In) Webinar

Webinar") Eurofiling Data modelling and ExcelXBRLGen (Excel Add In) Webinar Agenda 1. Data Model: Purpose, Challenges, Solutions 2. FINREP/COREP/BSI MIR Information Requirements and Data Models Overview 3. Eurofiling

Eurofiling Data modelling and ExcelXBRLGen (Excel Add In) Webinar Agenda 1. Data Model: Purpose, Challenges, Solutions 2. FINREP/COREP/BSI MIR Information Requirements and Data Models Overview 3. Eurofiling

Uncertainty over Income Tax Treatments

October 2015 Draft IFRIC Interpretation DI/2015/1 Uncertainty over Income Tax Treatments Comments to be received by 19 January 2016 [Draft] IFRIC INTERPRETATION Uncertainty over Income Tax Treatments Comments

October 2015 Draft IFRIC Interpretation DI/2015/1 Uncertainty over Income Tax Treatments Comments to be received by 19 January 2016 [Draft] IFRIC INTERPRETATION Uncertainty over Income Tax Treatments Comments

RE: Exposure Draft (ED ) on Equity Method in Separate Financial Statements Proposed amendments to IAS 27

on Equity Method in Separate Financial Statements Proposed amendments to IAS 27") January, 2014 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: Exposure Draft (ED 2013 10) on Equity Method in Separate Financial Statements Proposed amendments

January, 2014 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom RE: Exposure Draft (ED 2013 10) on Equity Method in Separate Financial Statements Proposed amendments

PARIS 6 SEPTEMBER 2017

JOINT OUTREACH EVENT BETTER COMMUNICATION SUMMARY REPORT PARIS 6 SEPTEMBER 2017 This report has been prepared for the convenience of European constituents by the EFRAG Secretariat and has not been subject

JOINT OUTREACH EVENT BETTER COMMUNICATION SUMMARY REPORT PARIS 6 SEPTEMBER 2017 This report has been prepared for the convenience of European constituents by the EFRAG Secretariat and has not been subject

Re: IASB Request for information: Comprehensive review of the IFRS for SMEs

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street GB LONDON EC4M 6XH E-mail: commentletters@ifrs.org 14 December 2012 Ref.: FRP/PRJ/TSI/IDS Dear Chairman, Re: IASB

Mr Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street GB LONDON EC4M 6XH E-mail: commentletters@ifrs.org 14 December 2012 Ref.: FRP/PRJ/TSI/IDS Dear Chairman, Re: IASB

Exposure Draft ED 2015/6 Clarifications to IFRS 15

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

Hans Hoogervorst Chairman International Accounting Standards Board 30 Cannon Street London United Kingdom EC4M 6XH Deloitte Touche Tohmatsu Limited 2 New Street Square London EC4A 3BZ United Kingdom Tel:

XBRL Taxonomy Recognition Process

XBRL Taxonomy Recognition Process Approved Version of 2007-10-17 Copyright XBRL International Inc. 2003-2006, 2007 Editors Name Contact Affiliation Peter Calvert pscalvert50@hotmail.com Calvert Consulting

XBRL Taxonomy Recognition Process Approved Version of 2007-10-17 Copyright XBRL International Inc. 2003-2006, 2007 Editors Name Contact Affiliation Peter Calvert pscalvert50@hotmail.com Calvert Consulting

GAA. Project Manager International Accounting Standards Board 1 st Floor 30 Cannon Street London EC4M 6XH United Kingdom.

THE I N S T I T U T K Of Chartered Accountants I N I R E L A N D Burlington House, Burlington Road, Dublin 4 Tel. +-353 1 637 7200 Fax; +-3B3 1 6680842 Project Manager International Accounting Standards

THE I N S T I T U T K Of Chartered Accountants I N I R E L A N D Burlington House, Burlington Road, Dublin 4 Tel. +-353 1 637 7200 Fax; +-3B3 1 6680842 Project Manager International Accounting Standards

Dear Sir or Madam: Discussion Paper Preliminary Views on Financial Statement Presentation

- 1 6 3 O - 1 Q O * LETTER OF COMMENT NO. Yonsei Severance B/D 4th Fl. Chung-gu Namdaemunro 5-ga 84-11 Seoul 100-753, (South) Korea 14 April 2009 International Accounting Standards Board 30 Cannon Street,

- 1 6 3 O - 1 Q O * LETTER OF COMMENT NO. Yonsei Severance B/D 4th Fl. Chung-gu Namdaemunro 5-ga 84-11 Seoul 100-753, (South) Korea 14 April 2009 International Accounting Standards Board 30 Cannon Street,

FILING OF ANNUAL FINANCIAL STATEMENTS TO THE CIPC IN XBRL

FILING OF ANNUAL FINANCIAL STATEMENTS TO THE CIPC IN XBRL Filers Guidelines: Business Aspects Author: Hennie Viljoen XBRL Programme Manager: CIPC This document provides General Information and Guidelines

FILING OF ANNUAL FINANCIAL STATEMENTS TO THE CIPC IN XBRL Filers Guidelines: Business Aspects Author: Hennie Viljoen XBRL Programme Manager: CIPC This document provides General Information and Guidelines

IFRS APPLICATION AROUND THE WORLD JURISDICTIONAL PROFILE: Nepal

IFRS APPLICATION AROUND THE WORLD JURISDICTIONAL PROFILE: Nepal Disclaimer: The information in this Profile is for general guidance only and may change from time to time. You should not act on the information

IFRS APPLICATION AROUND THE WORLD JURISDICTIONAL PROFILE: Nepal Disclaimer: The information in this Profile is for general guidance only and may change from time to time. You should not act on the information

FORM 20-F/A. Shinhan Financial Group Co., Ltd.

As filed with the Securities and Exchange Commission on July 26, 2010 SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 20-F/A (Amendment No. 1) REGISTRATION STATEMENT PURSUANT TO SECTION 12(b)

As filed with the Securities and Exchange Commission on July 26, 2010 SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 20-F/A (Amendment No. 1) REGISTRATION STATEMENT PURSUANT TO SECTION 12(b)

Comments on the Exposure Draft Financial Instruments: Amortised Cost and Impairment

June 30, 2010 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir or Madame, Comments on the Exposure Draft Financial Instruments: Amortised Cost and Impairment

June 30, 2010 International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir or Madame, Comments on the Exposure Draft Financial Instruments: Amortised Cost and Impairment

Discussion Paper DP/2014/1 Accounting for Dynamic Risk Management: a Portfolio Revaluation Approach to Macro Hedging

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Stockholm October 13, 2014 Discussion Paper DP/2014/1 Accounting for Dynamic Risk Management: a Portfolio Revaluation

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Stockholm October 13, 2014 Discussion Paper DP/2014/1 Accounting for Dynamic Risk Management: a Portfolio Revaluation

BELGIAN ACCOUNTING STANDARDS BOARD

BELGIAN ACCOUNTING STANDARDS BOARD 1111111111111111111111111111111111111111111111111 * 163 0-100 * LEDER OF COMMENT NO. Z2.J International Accounting Standards Board 30 Cannon Street london EC4M 6XH United

BELGIAN ACCOUNTING STANDARDS BOARD 1111111111111111111111111111111111111111111111111 * 163 0-100 * LEDER OF COMMENT NO. Z2.J International Accounting Standards Board 30 Cannon Street london EC4M 6XH United

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C Amendment No. 1 to FORM 20-F

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Amendment No. 1 to FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 Amendment No. 1 to FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR

re: Comments on Exposure Draft Financial Instruments: Amortized Cost and Impairment

30 June 2010 Sir David Tweedie International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir David: re: Comments on Exposure Draft Financial Instruments: Amortized Cost

30 June 2010 Sir David Tweedie International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sir David: re: Comments on Exposure Draft Financial Instruments: Amortized Cost

January IFRS Taxonomy Update. IFRS Taxonomy IFRS 17 Insurance Contracts

January 2018 IFRS Taxonomy Update IFRS Taxonomy 2017 IFRS 17 Insurance Contracts IFRS Taxonomy Update IFRS Taxonomy 2017 IFRS 17 Insurance Contracts IFRS Taxonomy 2017 IFRS 17 Insurance Contracts is published

January 2018 IFRS Taxonomy Update IFRS Taxonomy 2017 IFRS 17 Insurance Contracts IFRS Taxonomy Update IFRS Taxonomy 2017 IFRS 17 Insurance Contracts IFRS Taxonomy 2017 IFRS 17 Insurance Contracts is published

Erste Group Bank AG comments to Consultation paper on amendments to the Guidelines on Financial Reporting (FINREP 10 March 2009)

") CEBS Secretariat Tower 42 (level 18) 25 Old Broad Street London EC2N 1HQ United Kingdom Erste Group Bank AG Graben 21 1010 Vienna Head office: Vienna Commercial Court of Vienna Commercial Register No.:

CEBS Secretariat Tower 42 (level 18) 25 Old Broad Street London EC2N 1HQ United Kingdom Erste Group Bank AG Graben 21 1010 Vienna Head office: Vienna Commercial Court of Vienna Commercial Register No.:

Do you agree with the Board s proposal to amend the IFRS as described in the exposure draft? If not, why and what alternative do you propose?

Mr Hans Hoogervorst Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Düsseldorf, 31 August 2012 540/602 Dear Mr Hoogervorst Re.: IASB Exposure Draft

Mr Hans Hoogervorst Chairman of the International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Düsseldorf, 31 August 2012 540/602 Dear Mr Hoogervorst Re.: IASB Exposure Draft

Re: Request for Information: Comprehensive Review of the IFRS for SMEs

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sirs, 29 November 2012 Re: Request for Information: Comprehensive Review of the IFRS for SMEs The Institute

International Accounting Standards Board 30 Cannon Street London EC4M 6XH United Kingdom Dear Sirs, 29 November 2012 Re: Request for Information: Comprehensive Review of the IFRS for SMEs The Institute

IASP 2. Prepared by the Subcommittee on Actuarial Standards of the Committee on Insurance Accounting. Published 16 June 2005

International Actuarial Association Association Actuarielle Internationale IASP 2 Actuarial Practice When Providing Professional Services Concerning Financial Reporting of Insurance Contracts, Financial

International Actuarial Association Association Actuarielle Internationale IASP 2 Actuarial Practice When Providing Professional Services Concerning Financial Reporting of Insurance Contracts, Financial

Exposure draft: Amendments to IFRS 1 and IAS 27, Cost of an investment in a subsidiary, jointly controlled entity or associate

PricewaterhouseCoopers LLP 1 Embankment Place London WC2N 6RH Telephone +44 (0) 20 7583 5000 Facsimile +44 (0) 20 7822 4652 pwc.com/uk Jeff Singleton International Accounting Standards Board 1st Floor

PricewaterhouseCoopers LLP 1 Embankment Place London WC2N 6RH Telephone +44 (0) 20 7583 5000 Facsimile +44 (0) 20 7822 4652 pwc.com/uk Jeff Singleton International Accounting Standards Board 1st Floor

January Global financial crisis

J January 2009 IASB Update is published as a convenience for the Board s constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

J January 2009 IASB Update is published as a convenience for the Board s constituents. All conclusions reported are tentative and may be changed or modified at future Board meetings. Decisions become final

At this meeting, the Interpretations Committee discussed the following items on its current agenda.

IFRIC Update From the IFRS Interpretations Committee January 2014 Welcome to the IFRIC Update IFRIC Update is the newsletter of the IFRS Interpretations Committee (the 'Interpretations Committee'). All

IFRIC Update From the IFRS Interpretations Committee January 2014 Welcome to the IFRIC Update IFRIC Update is the newsletter of the IFRS Interpretations Committee (the 'Interpretations Committee'). All